Chapter 7. Are survivor pensions still needed?

This chapter describes survivor pension schemes in OECD countries. It first documents expenditures on survivor pensions the number of recipients and the average level of benefits. It then provides details about eligibility rules and benefit determination across countries. The chapter includes a discussion of how survivor pensions have developed in the recent decades and whether these trends are related to the more general evolution of pension systems and the deep changes in socio-economic environments. Simulations based on the OECD pension model estimate the impact of the survivor pensions on the financial situation of survivors, including how pension splitting can affect survivor pensions in OECD countries. Main results and key policy insights follow.

As with old-age pensions, survivor schemes first started by covering selected groups of the population. A few countries, among which Ireland, Sweden, the United Kingdom and the United States, introduced survivor pensions in the 19th or first half of the 20th century, in particular for civil servants (Flora, 1986[1]). The expansion of the Welfare State in many OECD countries after 1945 included the coverage of survivor risks by placing greater emphasis on social assistance (Hannikainen and Vauhkonen, 2012[2]). Yet, potential beneficiaries were less numerous than today because more people worked in jobs, in agriculture in particular, that did not provide pension coverage (Gillion et al., 2000[3]).

The introduction of survivor pensions improved the economic situation of widows at a time when the family representation was dominated by the male-breadwinner model.1 In such a family, the husband worked and earned pension entitlements while his wife provided care and unpaid work that gave her limited pension rights. Moreover, the marriage was both widespread and a life-long contract that ended by death, most often of men, rather than by divorce.

Following the death of a partner, survivor pensions have pursued two main objectives. First, they have protected widows or widowers from poverty risks to offset sharp drops in disposable income to low absolute levels. Second, they have contributed to insuring against the decrease in disposable income relative to the situation prevailing before the death of the partner, in the same way as old-age pensions help avoid a sharp drop in income when moving out of paid work upon retirement: this is the so-called consumption-smoothing objective aiming at preserving standards of living.

Nowadays, all OECD countries provide instruments directly targeted at poverty alleviation, i.e. basic and minimum pensions as well as social assistance benefits including housing allowances.2 In many countries, the level of these benefits is low, but there is no obvious justification why widowed persons should be granted higher safety-net benefits than other individuals in a similarly poor income situation. Some countries where poverty relief was the main objective have indeed eliminated survivor pensions. Moreover, scaling down survivor benefits has also been connected to a gender-equality motive, as in Sweden for example (Section 7.4). Yet, survivor pensions still effectively reduce the gender pension gap in most countries. The consumption-smoothing rationale is today the main justification for the existence of survivor pensions.

While both parents work in more than half of couples with children on average in the OECD, the single-breadwinner family model is still frequent in many countries, at least in households with dependent children (Section 7.2). Moreover, the need of a policy instrument to avoid the drop in disposable income following the death of a spouse applies beyond the male-breadwinner model, even if both partners achieve similar pension entitlements. This is because living in a couple benefits from economies of scale in the cost of running the household. It is generally estimated that the cost of living for a single household exceeds 50% of the cost of living for a couple (Section 7.1). According to the equivalence scale used by the OECD, a drop of total household income larger than roughly 30% after the death of a partner leads to a fall in the living standards of the survivor. Hence, the absence of survivor pensions typically implies that the death of one partner causes a drop in living standards of the survivor, even in couples where both partners earned the same own (50% of the couple’s) pension income.

One way to cover the survivor’s income risk is to purchase targeted financial products like joint-and-survivor annuity contracts which pay an agreed pension until the second partner dies. However, standard problems in insurance markets commonly referred to as market failure, such as adverse selection due to asymmetric information about health problems (Akerlof, 1970[4]), may lead to the lack of supply of adequate products. On top of that, the demand for a voluntary contract might also be limited by myopic behaviour – driven for example by the underestimation of the probability of a premature death of the partner or its financial consequences. Consequently, couples may not be well prepared financially to cope with the death of the partner through voluntary private insurance markets, and mandatory survivor pension schemes overcome market failures by enlarging the pool of insured people sharing the related risks.3

Most existing survivor pensions in pay-as-you-go (PAYGO) schemes are financed through contributions and taxes. As individuals within couples typically do not pay higher contributions or receive lower old-age pension benefits before death, these schemes imply redistribution from singles to individuals eligible for survivor pensions. Means-testing of survivor pensions limits the level of benefits, and therefore also limits this type of redistribution, but it favours single-breadwinner over dual-breadwinners couples (Section 7.5).

Moreover, survivor pensions might hamper the employment of women as the benefits could reduce incentives to work, potentially leading to labour market exit or reduced working hours. For this reason, survivor pensions typically set an age threshold or are, at younger ages, granted for a limited period to facilitate the adaptation to the new situation. When means-tested, survivor pensions reduce incentives to work even more as the benefit amount declines with own earnings. Disincentives to work at younger ages could even be at play before the age of eligibility to survivor pensions due to anticipation effects, especially when large differences in age or health status between partners make acquiring own old-age pension rights less important.

The socio-economic basis for the design of survivor and old-age pension systems has evolved substantially in various dimensions over the last decades. Ultimately they might question the raison d’être of survivor pensions. Survivor pension reforms over the past decades have indeed mainly focused on tightening or eliminating these schemes. This Chapter provides a description of survivor schemes in OECD countries and analyses whether they are well-designed and adapted to the ongoing profound socio-economic changes. It seeks to contribute to answering three main interrelated questions:

-

What is the role pension systems should play to protect survivors given existing old-age safety nets?

-

Are current survivor schemes well-designed given the deep developments societies are going through?

-

Beyond country-specific historical contexts, are survivor pensions still needed and if so how would they look like if they were now built from scratch?

The rest of the chapter is organised as follows. The first section gives an overview of the current survivor benefits (total expenditures, recipients and benefit levels) and the second one examines how the socio-economic environment that has been central in the design of survivor pensions, including female employment, gender gap in pensions and family structure, has changed over time. Section 3 focuses on the current rules while Section 4 discusses the reforms to survivor pensions and how systemic reforms of old-age pensions have affected survivor schemes over the last decades. Based on the OECD pension model, the chapter then explores the impact of survivor pensions on the financial situation of survivors and how pension splitting can affect survivor pensions. Section 6 presents a general discussion of what survivor pensions should look like in the current socio-economic context while the final section summarises the main results and concludes.

7.1. Survivor benefits today: Expenditures, recipients and benefit levels

There is a great variety in the type and scope of survivor pension schemes across OECD countries. This materialises in substantial differences in the number and characteristics of total expenditures for survivor benefits, nowadays recipients and average benefit levels. Survivor benefits is indeed a broad category that includes permanent and temporary payments targeted at widows and widowers and other surviving dependent family members.

Expenditures

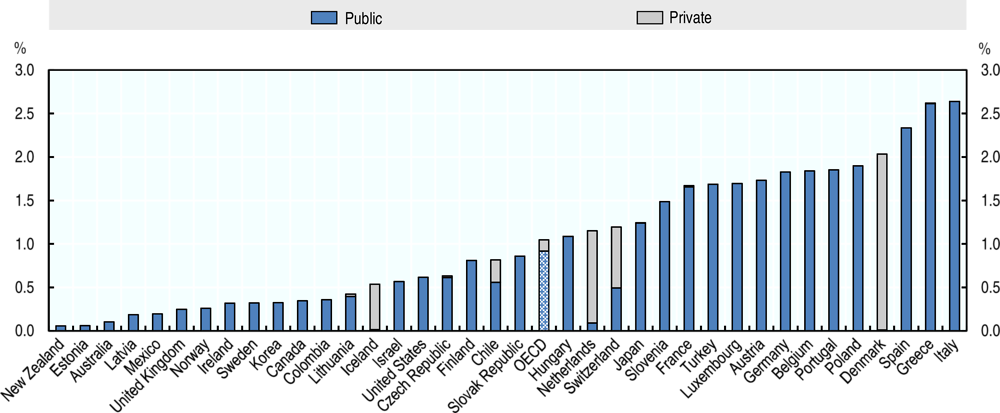

OECD countries spend on average about 1% of GDP on survivor benefits in mandatory schemes (Figure 7.1. ). Greece, Italy and Spain are the OECD countries which report the highest spending on survivor benefits, more than 2.3% of GDP. By contrast, twelve OECD countries (Australia, Canada, Estonia, Ireland, Korea, Latvia, Lithuania, Mexico, New Zealand, Norway, Sweden and the United Kingdom) spend less than 0.5% of GDP.

Note: The data on the United Kingdom are based on data provided by Department for Work and Pensions.4 Data on (mandatory and voluntary) survivor pensions in mandatory private schemes in Denmark (ATP), Estonia, Israel, Mexico, Norway, the Slovak Republic and Sweden are not available. Data for Chile, Israel, Korea, New Zealand and the United States are 2017. Australia and Mexico are 2016. Poland is 2014. The other countries are 2015.

Source: OECD preliminary social expenditure database and information provided by countries.

In most countries, spending on survivor benefits is mostly public while mandatory private schemes dominate in Denmark, Iceland, the Netherlands and Switzerland only. In Chile, the mandatory private pension scheme, introduced in 1981, is still maturing and makes up for less than one-third of all expenditures on survivor benefits. Beyond survivor benefits, safety-net benefits and basic pensions, especially those which are residency-based as e.g. in Australia, the Netherlands and New Zealand, provide income unrelated to work experience and cover poverty risks for everyone including surviving spouses.

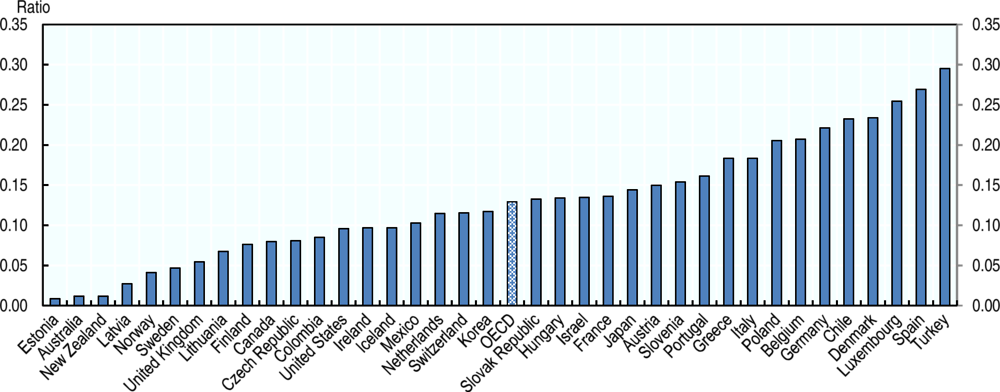

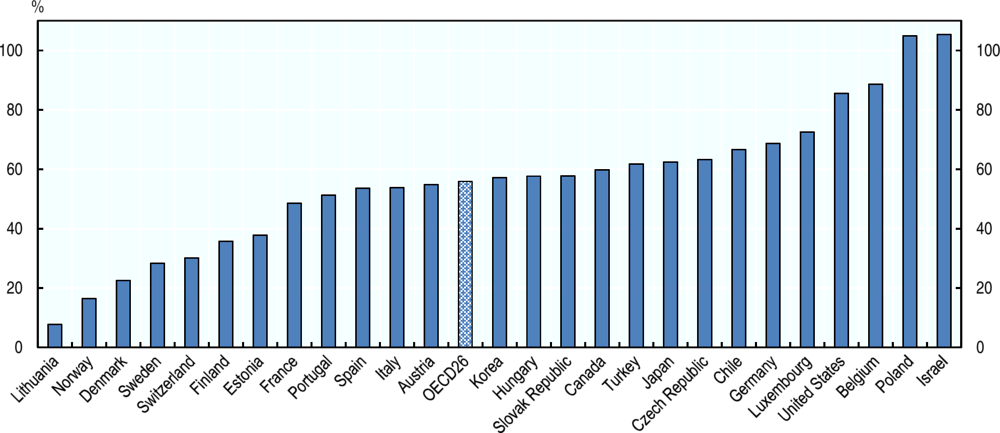

Relative to mandatory old-age benefit spending, expenditures on survivor benefits differ substantially across countries. On average, about one dollar is spent on survivor benefits for each eight dollars spent on old-age benefits, or a ratio of 13% (Figure 7.2. ). Belgium, Chile, Denmark, Germany, Luxembourg, Poland, Spain and Turkey spend more than 20% while Australia, Estonia, Latvia, New Zealand and Norway spend less than 5%. However, in some countries including Australia, the spending data do not account for the fact that the remaining account balance in the private-sector schemes is typically transferred to the surviving spouse.

Note: See preceding figure.

Source: OECD preliminary social expenditure database and information provided by countries.

Survivor expenditures consist mainly of survivor pensions, but they may also include funeral expenses and other benefits in cash or kind. In all countries except Latvia and Lithuania the share of pensions in survivor expenditures exceeds 85%. In Latvia, survivor pensions are granted only to orphans. In Lithuania, assistance for families of deceased persons in the public scheme and special benefits for survivors in the private scheme provide comparatively large benefits in addition to the pension.

Recipients

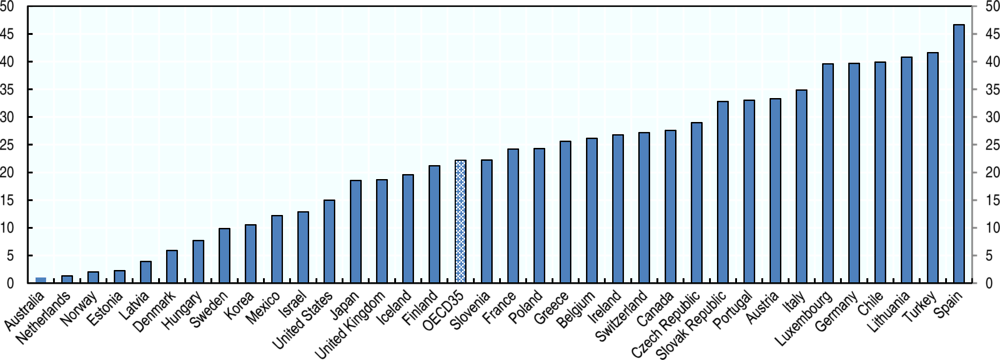

There are 22 survivor benefit recipients for each 100 beneficiaries of old-age pensions within public schemes on average in the OECD (Figure 7.3). Comparatively many survivor benefits are paid in Germany, Lithuania, Luxembourg, Spain and Turkey; close to or more than 40 per each 100 old-age pension payments. By contrast, only few recipients of survivor benefits within public scheme – less than 5 for every 100 recipients of old-age pensions - are recorded in Australia, Estonia, Latvia, the Netherlands and Norway.5 In Australia, the Netherlands and Norway, survivors’ income risks after retirement age are basically not covered by survivor schemes but indirectly by residency-based basic pensions.

Note: Data refer to public schemes, except for Chile where it includes the mandatory private scheme. See the StatLink for more details.

Source: OECD social benefits recipients’ database and information provided by countries. See the StatLink for more details.

Detailed information on recipients of survivor pensions reveal the following features.6 First, in Canada, Ireland and Korea survivor pensions cover only widows and widowers; social benefits for orphans in these countries are not related to the accumulated old-age pension entitlements of their parents. Also, over 90% of survivor pension recipients in the Czech Republic, Finland, Germany and Sweden are widows or widowers. Conversely, orphans make up for a large share of survivor pension recipients in Hungary and the United States, amounting to 43% and 28%, respectively, and in Latvia where only orphans can be granted survivor pensions since 1996. Second, most of recipients of survivor pensions also receive own old-age pensions if such accumulation is allowed. In 2016, in the Czech Republic and the United Kingdom, for example, it was the case for 95% and 72% of recipients of survivor pensions, respectively.

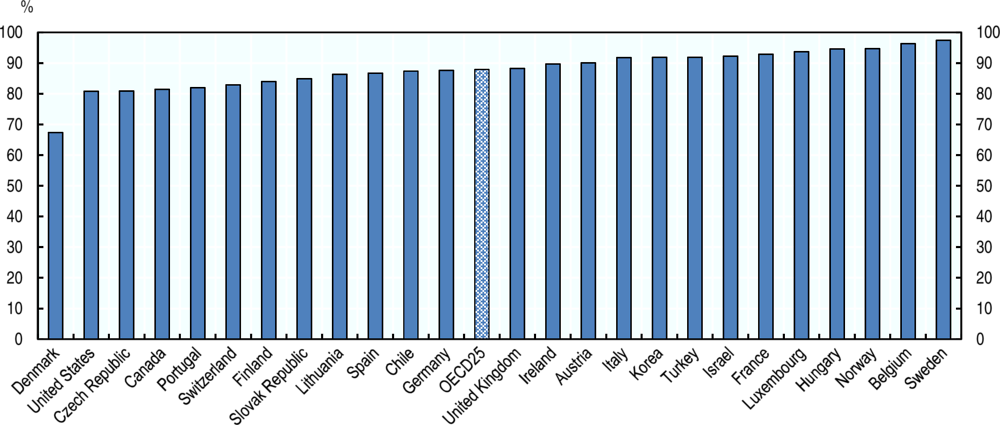

Third, women represent more than 85% of survivor-pension recipients for widowed persons on average across 25 OECD countries (Figure 7.4). This is because they tend to live longer, be the younger partner within a couple and accumulate lower individual pension entitlements. The share of women is lower than 80% only in Denmark at 67% where gender differences in both old-age pensions and life expectancy are comparatively small.

On average across OECD countries, less than two-thirds of widowed people older than 65 receive some survivor benefits. That share varies greatly across countries. For example, countries with a very high share of widowed persons such as Hungary, Korea and Mexico have very few recipients.

Average benefit levels

Based on data reported by 26 OECD countries, the mean survivor pension to widows and widowers is equal to 56% of the mean old-age pension on average (Figure 7.5). It is 8% in Lithuania, which grants a low flat benefit, and lower than 20% in Norway where survivor pensions are subject to strict means-testing (and will be phased out for survivors reaching the retirement age and born in 1963 or later).7

Note: Data refer to the main mandatory schemes.

Source: Data provided by countries for 2016 or 2017 and, for Ireland, OECD social benefit recipients database 2014.

Note: Data for both, old-age and survivor pensions, refer to the main mandatory scheme paying survivor pensions in year 2016 or 2017.

Source: Information provided by countries. For Germany data stem from Deutsche Rentenversicherung (2017[5]) and for Poland from ZUS (2018[6]).

Conversely, it is higher than 80% in Belgium, Israel, Poland and the United States. In Israel, 50% of the basic pension is paid to survivors on top of their own entitlement to a full basic pension and even 100% if the survivor has no own entitlements.8 High levels of the average survivor pension relative to the average old-age pension in Belgium and the United States are consistent with the high survivor replacement rate from the public scheme (Section 7.3). This also applies to Poland, where in addition old-age benefit levels of current pensioners from the old pension scheme are comparatively high. Comparable data across countries about the share of individual income provided by survivor pensions are missing. In France, as an example, among people receiving their own pension benefits, survivor pensions represented 23% of pension income for women and only 1% for men in 2015 (Lavigne, 2018[7]).

7.2. A changing socio-economic environment

The socio-economic environment matters to assess whether survivor pensions are necessary and well-designed. Female employment levels, the structure of family formation and survival rates have changed substantially from the time when survivor pensions were introduced in most OECD countries. Hence, the number of survivor-pension recipients as well as total expenditure are affected, in particular due to means-testing, which often applies to survivor pensions (Section 7.3).

Women work more often and gender employment gaps are narrowing

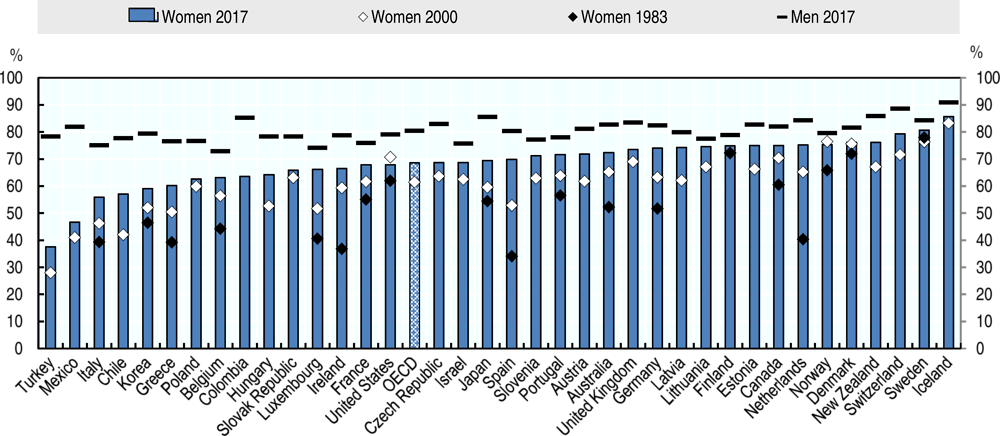

Although large gender gaps remain in some countries, more often than in the past women of young generations participate in the labour market, earn money and acquire pension rights. Female labour force participation rates increased substantially from 61% in 2000 to 69% in 2017 on average in the OECD (Figure 7.6). The increase exceeded 10 percentage points (p.p.) in Austria, Chile, Germany, Hungary, Latvia, Luxembourg, the Netherlands and Spain. This added to a longer trend in many countries, with the strongest increases of over 15 p.p. between 1983 and 2000 in Ireland, Luxembourg and Spain.9 Higher education levels and lower fertility rates have contributed to these developments.

Still, the average male labour force participation rate is at a much higher level, equalling 80% in 2017. The gender gap exceeds 20 p.p. in Chile, Colombia, Korea, Mexico and Turkey while it is below 5 p.p. in Finland, Lithuania, Norway and Sweden. Moreover, the share of part-time and temporary workers among women is still higher than for men.

Female employment is strongly influenced by the persisting imbalances in sharing various tasks within partnerships. The pure single-breadwinner family model, where one partner works full time while the other does not work at all, represents 31% of households with children (OECD Family Database, Chart LMF1.1C). The single-breadwinner family model is frequent in Turkey (65%) and in Greece and the Slovak Republic (more than 40%). However, among couples with children younger than 15 years-old, both parents work in 59% of households on average across 24 OECD countries in 2014, with (both working full time in 41% of them. The share of couples with two full-time earners exceeds 60% of couples with children in Denmark, Portugal, Slovenia, Sweden and the United States.

Gender gap in pensions and old-age poverty

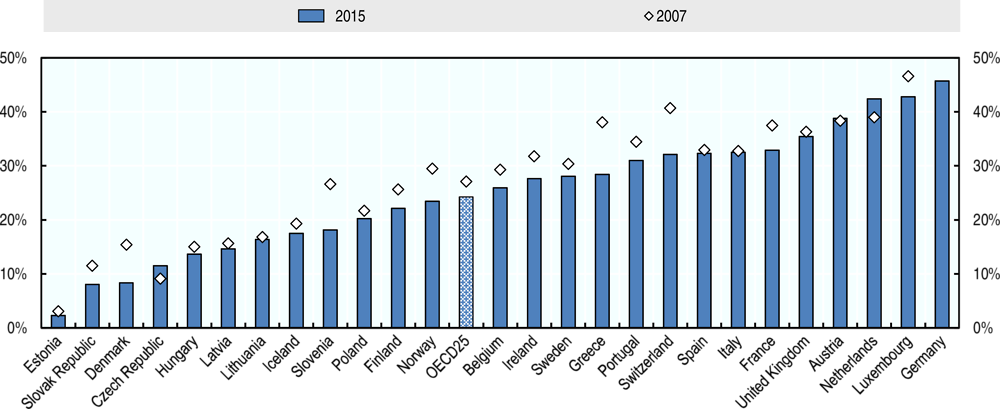

Weaker labour market attachment for women than for men and lower wages result in lower pensions and lower coverage by contributory pension schemes. On average across the 25 OECD countries for which data are available since 2007, women had pensions 24% lower than men in 2015, slightly less than the 2007 average of 27% (Figure 7.7). In 2015, that gap was below 10% in Denmark, Estonia and the Slovak Republic only and larger than 40% in Germany, Luxembourg and the Netherlands. In this context, survivor pensions, which are predominantly paid to women lower the gender pension gap. In France, for example, survivor pensions diminish the gender pension gap by about one-third (DREES, 2018[8]).

Note: OECD average calculated for all countries for which data were available.

Source: OECD Labour Force Survey indicators.

Lower pension entitlements and higher longevity result in higher poverty rates among older women. On average in the OECD, 17% of women older than 75 years fall below the relative poverty line defined at 50% of median equivalised income, against 10% for men at the same age and 12% for women aged 66-75. Many pensions are indexed to prices which tend to grow less than wages, implying that the relative value of pension in payments tends to fall, especially for people who survive long enough during retirement. Beyond potentially lower pensions due to indexation rules, very old people face higher poverty risk as they live more often in single-person households, hence not benefiting from the economies of scale that larger households provide (Box 7.1).

Living expenses usually rise less than proportionally with the size of a household. Collective goods such as fixed living costs (like base rates of utilities or rental costs for common spaces such as kitchens and bathrooms) can be shared. These economies of scale in living costs reduce the per-person cost, especially accommodation cost, and mean that one dollar of a couple’s income leads to higher individual living standards than for a single person with 50 cents of income.

Income equivalence scales are commonly used to compare the income of individuals living in households of different size and composition. These scales are based on defining the number of consumption units which are equivalent full-cost family members for each household.

Exactly how this adjustment for household size and composition should be made is debated in the literature, and several alternative scales exist (James, 2009[9]). One common equivalence scale, the standard scale, weights the first adult in the household as 1, each additional adult as 0.5 and each child as 0.3. Recent OECD publications divide the total income of a couple by the square root of the size of the household, i.e. the square root of 2 (≈1.4) when comparing with single-person households - cf., e.g. OECD (2017[10]). The ratio of total household income divided by the equivalence scale is the “equivalised income” at the individual level. This publication follows the recent OECD approach. It implies that if each individual has an income of 100, then the equivalised income of a couple at the individual level is equal to 2*100 / √2 ≈ 141 and a single person would have a standard of living which is only 100 / 141 = 71% of the individuals living in a couple. With the standard scale, it is slightly lower at 67%.

These orders of magnitude might not capture well the situation of widowhood. In particular they assume that widowed persons downsize their house after the death of the partner, which is typically not the case. Bonnet and Hourriez (2008[11]) estimate that when widows or widowers do not change accommodation, their living cost is 8% larger than what the above scales assume. That is, 71% becomes 77%, and in that case if the total income falls by more than 23% after the partner’s death then the standards of living of the survivor decline.

Note: The gender gap in pensions is calculated as the difference of average pensions between men and women divided by the average pension of men. The average for OECD25 does not include Germany as the value for 2007 was not available. The “2015” values for Germany and Iceland are from 2014. The “2007” value for France is an average of 2006 and 2008.

Source: EU-SILC, 2016.

Note: OECD average calculated for all countries for which data are available for all three time periods. Observations from different sources (censuses, surveys) averaged for each 7-years span.

Source: OECD calculation based on the UNSD Demographic Statistic database (http://data.un.org). For Chile, data are from CASEN and period is 2009-2015 instead of 2010-16. For the United States in Panel B and C, the age group is 65-74 instead of 65-69.

Changes in families

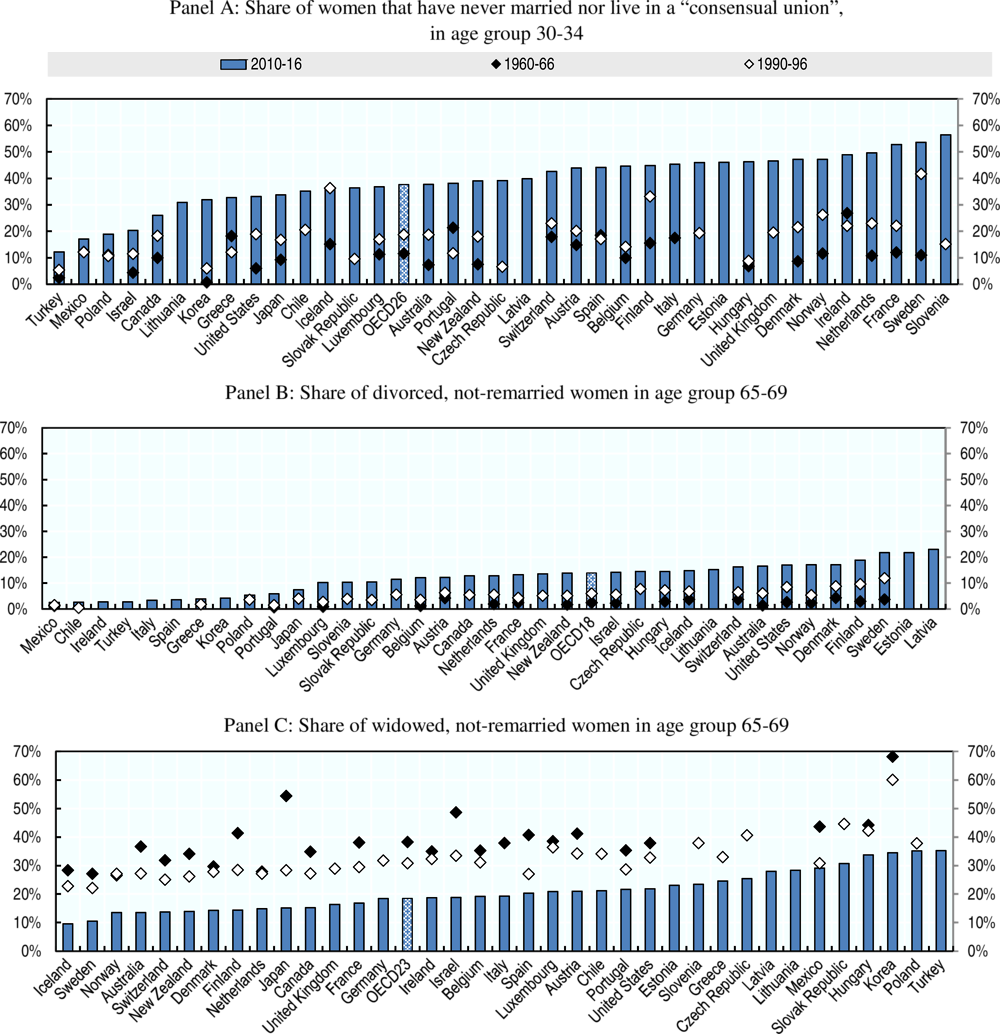

Couples and marriages are being formed later and are less stable than in the past. In the 2010-2016 period, 38% of women aged 30-34 have never been married nor were living in a “consensual union”10 compared to 19% in 1990-1996 and 12% in 1960-1966 on average across 26 OECD countries (Figure 7.8, Panel A). In France, the Netherlands, Slovenia and Sweden, more than half of women aged 30-34 in 2010-2016 have never been married nor were living in a “consensual union”. The increase between 1990-1996 and 2010-2016 was spectacular, larger than 10 percentage points in all countries but Canada, Iceland, Israel, Mexico, Poland and Turkey. The increasing role of less formal partnerships only offsets part of this trend, such that the share of singles has risen. 11

Moreover, between 1960-1966 and 2010-2016 the share of divorced, not remarried women aged 65-69 increased from 2% to 14% on average in the 18 countries for which data are available (Panel B). The highest levels in 2010-2016 of more than 20% were recorded in Estonia, Latvia and Sweden.

Along with improvements in men’s life expectancy, fewer marriages and more frequent divorces contributed to more than halving the share of widows in the age group 65-69, from 38% in 1960-66 to 18% in 2010-16 for the OECD23 average (Panel C). In 2010-16, the highest shares of widows of more than 30% are found in Hungary, Korea, Poland, the Slovak Republic and Turkey, in part related to large gender gaps in life expectancy.

Life expectancy gaps between women and men

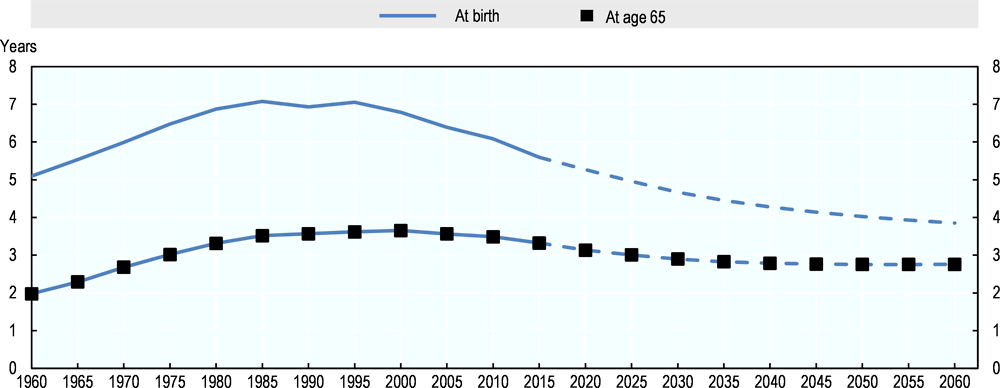

Life expectancy gains have been impressive. On average, female life expectancy at birth increased from 69 to 82 years between 1960 and 2015. It is expected to increase further, although at a slower pace, reaching 88 years in half a century. For men, life expectancy has been increasing faster since the 1990s across OECD countries, narrowing the gender gap from a peak of 7.1 years in 1985 to 5.6 years in 2015 on average (Figure 7.9).

Central and Eastern European Countries made a large contribution to this reduction, which is likely to be linked to the decline in heavy industry jobs, the increase in female alcohol and tobacco consumption and perhaps the reduction in gender paid-work gaps. Some health-care improvements such as better treatment of heart-related diseases may have also benefitted men more than women (Barthold et al., 2014[9]). Lower gender differences in life expectancy imply that the duration of widowhood should also diminish. The narrowing of the gender gap is less clear when focusing on remaining life expectancy at age 65, for which the peak was reached in 2000, with only a small decline since. Yet, the downward trend is expected to continue with the average gender gap in life expectancy at birth reaching 4.0 years and 2.8 years at age 65 in the middle of the century based on UN projections.

Note: Life expectancy is calculated for 5-year intervals; the upper bound of which is displayed at the horizontal axis.

Source: United Nations, Department of Economic and Social Affairs, Population Division (2017). World Population Prospects: The 2017 Revision, DVD Edition.

7.3. Eligibility criteria and benefit determination

Almost all OECD countries cover survivor risk through survivor pensions for at least some parts of the population. The following discussion focuses on future derived pension entitlements of widowed persons – who neither are disabled nor have dependent children - from the main mandatory scheme covering private-sector workers.12 It is thus a narrower category than the survivor benefits discussed in Section 7.1. Neither survivor pension programmes in Australia, Latvia, New Zealand, Norway13, Sweden and the United Kingdom, which were abolished over the past decades but still exist during the phase-out period, nor survivor schemes providing only temporary benefits or lump-sum payments are covered here. Detailed rules are shown in the Annex 7.A. Only policy changes enacted by the end of August 2018 are accounted for.

Eligibility criteria

Eligibility criteria to survivor pensions for widows and widowers vary significantly across countries as they depend on gender and age of both the survivor and the deceased as well as on the forms of partnerships. As for the eligibility of the deceased, most countries require having contributed for a minimum period to the disability or old-age pension scheme (see Annex 7.A).

Gender differences in eligibility have been eliminated over the last decades in many countries (Section 7.4) but a few exceptions remain. In Switzerland, for example, unlike women, men are only eligible for survivor pensions as long as they have a dependent child. Also in Israel and Japan the access for men is more restricted than for women.

Age-related criteria for widowed people are commonly applied for survivor pension eligibility to limit their negative impact on labour market participation. No minimum age requirements apply in Austria, Canada (from 2019), Chile, Ireland, Italy, Korea, Luxembourg, Mexico, Norway, Spain and Turkey while only widowed persons above a certain age can receive permanent survivor pensions in 17 OECD countries (Table 7.1). Widowed persons who are not able to work - with disabilities or caring for children - are usually exempted from these age tests.

Among the countries which set a minimum age for permanent benefits within survivor pension programmes, the lowest minimum age is 35 years in Portugal. Many countries set a minimum eligibility age below the statutory retirement age to reflect that, after a short work experience, the earnings capacity from e.g. age 50 is reduced. Estonia, Hungary, Lithuania and the Slovak Republic do not grant access to permanent survivor pensions before the recipient reaches the retirement age. The strictness of the eligibility age condition varies across countries. Indeed, a survivor who is younger than the age threshold when the spouse deceases never acquires the right to a permanent survivor pension in some countries including Finland, Israel and Japan; by contrast, in Belgium, France, Germany and Greece it is only delayed until the survivor reaches the required age.

Before the eligibility age to a permanent survivor pension is reached, many countries grant survivor benefits for a limited time period to help the survivor adjust to the new situation without limiting work incentives in the longer term. For example, in Greece, survivor pensions are paid for only 3 years if the survivor has not reached 55 years of age. In Portugal, the pension is paid to the spouse under 35 years-old for only 5 years, and in Hungary for only one year before age 63. In France, widowhood allowance is payable for 2 years if the widowed is younger than 50 years-old or until age 55 otherwise, which serves as a bridge to the survivor pension starting from age 55.

In Norway, permanent survivor pensions cease at the statutory retirement age when residents start to receive a basic pension. Survivor pensions are therefore a bridge benefit that provides income between partner’s death and access to their own pension. The same applies to the basic component of survivor pensions in Finland while access to the earnings-related component continues after the retirement age.

While marriage used to be required to access survivor pensions, an increasing number of countries have expanded survivor benefits to civil unions and even registered cohabitations (Table 7.1). Sixteen countries provide survivor benefits to civil unions, while Canada, Hungary, Japan, Korea, Mexico, Norway, Portugal, Slovenia and Spain grant survivor pensions to cohabitants, upon meeting additional conditions. In Spain for example, five years of cohabitation are needed. Fourteen countries require a minimum length of marriage to grant survivor benefits varying from 6 months to 5 years.14

In many countries survivor pensions are indirectly linked to family policies. Having or caring for a dependent child can increase the survivor benefits or waive some eligibility conditions such as age or length of marriage requirements. For example, in the Czech Republic, Germany, Hungary, Israel, Portugal, the Slovak Republic, Switzerland and the United States, the age requirement is waived if the survivor is caring for a dependent child. Also, the length of marriage condition is waived in Finland, Greece, Israel, Lithuania, Luxembourg, Norway, Portugal and Switzerland if there is a child from this marriage.15

After divorce or separation, the death of the former partner does not cause any drop in income to the survivor (unless alimony was granted) because there were no shared income any longer. Still, nineteen countries grant survivor pensions after divorce treating this entitlement as a right acquired during marriage (Table 7.1) as long as the spouse meets additional conditions. For example, a minimum marriage period of 5-10 years is required in Greece, Switzerland and the United States. In Estonia, the divorced spouse can receive the benefit when reaching the statutory retirement age within 3 years after divorce and if the marriage has lasted for at least 25 years.

Also remarriage affects the entitlements to survivor pensions in some countries. If the widowed spouse is remarried, the survivor pension ceases in most OECD countries, while in some they are still paid for a certain time period or as a lump sum. In Estonia, for example, the survivor pension is paid for 12 months after remarriage. In the Czech Republic and Mexico, the survivor receives a lump sum equal to one or three years of the survivor benefits, respectively (see Annex 7.A for further details).

Benefit determination

The level of the survivor pension depends mostly on the pension entitlements of the deceased spouse and the replacement rate that the survivor pension guarantees. If the deceased did not reach the retirement age, some countries (for example Belgium, Finland, Luxembourg and Norway) assume for the calculation of the survivor pension that the deceased would have continued her career until the retirement age. In addition, means-tests against the survivor’s own income (or of other household members) apply in many countries (details of benefit rules are shown in the Annex 7.A).

Survivor pensions are not limited to earnings-related schemes. In the Czech Republic, Ireland, Israel and Luxembourg contribution-based basic pensions are paid to survivors who never contributed.16 Moreover, in Canada, Denmark, Finland, New Zealand and the Netherlands, residence-based basic pensions – which are not part of contributory pensions - help smooth consumption after the death of a partner as the benefit level for individuals exceeds 50% of the couple’s rate.

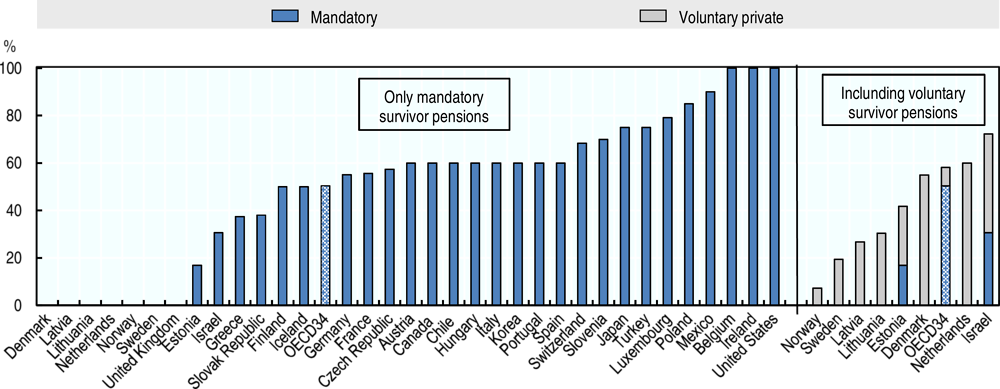

One half of OECD countries will have a survivor replacement rate at least equal to 60% based on legislated measures. However, on average in the OECD, future survivor pensions will automatically replace 50% of the deceased’s mandatory contributory pension at the retirement age, when no other income is taken into account for any household member including the survivor (Figure 7.10). When in addition the voluntary survivor option is taken into account where available, survivor pensions will replace 58% in total on average. In Denmark, Latvia, Lithuania, the Netherlands, Norway and Sweden, the replacement of the deceased’s contributory pension comes only from the voluntary option. Even if the option is chosen, the survivor pension replacement rate remains very low in Latvia, Lithuania, Norway and Sweden. At the upper end of the range, survivor pensions will grant at least 80% of the deceased’s mandatory contributory pension in Belgium, Ireland, Mexico, Poland and the United States.17

Note: Private-sector rules apply to surviving spouses of the cohort aged 20 in 2016 with no dependent child, no disability and no work history. If voluntary survivor options in mandatory private pension schemes are not specified by law, it is assumed that the joint-and-survivor annuity reduces the payments to 60% upon the death of the primary holder (Box 7.2). Calculations are made at male’s normal retirement ages assuming same-age couples. Australia is not included in the chart because joint annuities are not modelled given that most mandatory earnings-related pensions (superannuation) are paid out as lump sums. New Zealand is excluded as there is no mandatory contributory pension schemes. When countries have several components in the mandatory pension, the average value is shown using the shares of each component in the total contributory pension of a full-career average earner as weights.

Source: SSA (2018[10]), MISSOC (2018[11]) and information provided by countries.

Joint-and-survivor annuities are financial instruments that transform assets into a stream of payments which continue as long as one annuitant is alive: they thus protect against longevity and survivor risks. Joint life expectancy is not a very intuitive concept, although it is based on a simple fact: even when both partners have the same individual life expectancy, the expected remaining time until the first partner dies (it is initially unknown who this is) is shorter than this same individual remaining live expectancy while the expected remaining time until the second partner diesis longer.

Joint-and-survivor annuities which pay the same amount to the survivor (100-percent joint-and-survivor annuity) provide lower initial payments compared to the sum of two single-life (unisex) annuities because the full benefits are paid for a longer period. The following calculations assume: independent mortality rates between partners; same-age couple retiring together at 65; and indexation of annuities to price inflation.

Based on future mortality tables (using average unisex rates across OECD countries), an annuity that provides a constant payment until the survivor dies should pay a benefit that is approximately 14% lower than the sum of two single annuities.18 As alternative to the 100-percent joint-and-survivor annuity, the annuity can pay more upfront if the survivor receives a reduced benefit. As discussed above (Box 7.1), an about 70-percent joint-and-survivor annuity is sufficient to maintain standards of living upon the death of a partner. This 70-percent annuity implies an initial adjustment of about 6%. In the case of 50-percent joint-and-survivor annuity, no adjustment is needed, because the expected pay-outs are the same as for two single-life annuities: 100% until the first person dies and 50% thereafter.

Existing joint-and-survivor annuities are often designed in a similar way as survivor pensions within PAYGO schemes, but a distinction should be made between joint annuities with or without a primary annuity holder. Similar to PAYGO schemes, the annuity with a primary holder will pay a fixed amount until the death of the primary holder no matter whether his/her partner is alive. The payment is reduced only when the primary holder dies first. Conversely, the annuity without a primary holder reduces the payment upon the death of either partner. The annuity without a primary holder corresponds to the cases discussed in the previous paragraph.

The annuity with a primary holder provides higher payments than the annuity without a primary holder when the primary holder’s partner dies first. Thus, the latter annuity requires a lower adjustment to initial payments. For example, if a partner without own pension is entitled to receive a survivor pension (or a joint-and-survivor annuity with a primary holder who is the partner) equal to 50% of the deceased’s pension, the initial pension will be 8% lower instead of 0% in the case without primary holder discussed above. The 70% survivor replacement rates option requires adjustment of 11% instead of 6%.

The simulations in the chapter assume that voluntary survivor options in mandatory pension schemes takes the form of the joint-and-survivor annuity with a primary holder that provides the survivor with 60% of the deceased’s pension, if not regulated differently. This gives an adjustment of 9%. This common to all countries assumption makes the voluntary survivor options comparable to the mandatory survivor options. Indeed, on average across 26 OECD countries that provide mandatory survivor pensions, the survivor receives 62% of the deceased’s pension before means testing (Figure 7.10).

Individual earnings, individual pensions or even total household income reduce survivor pensions in 24 OECD countries (Table 7.2). Means-testing is absent in Chile, Israel (women), Lithuania, Mexico, Portugal and Spain only (and France for the mandatory occupational scheme).19 In Finland, for example, an own old-age pension beyond about 20% of average earnings reduces the survivor pension proportionally. In the Czech Republic, Ireland and Poland the higher of the two benefits, own old-age and survivor pensions, is paid. In addition in the Czech Republic, 50% of (the earnings-related component of) the lower of the two benefits is also added. Section 7.5 provides some further analysis of the impact of basic pensions and means-testing on the level of survivor pensions.

Own labour income reduces or suspends survivor pensions in 14 countries. This is aimed to better target the survivor benefits at people in need, but it coincidently encourages partial or full withdrawal from the labour market. In Belgium, labour earnings above about half of average earnings cannot be combined with receiving survivor pensions. Poland reduces or suspends survivor pensions when labour income exceeds 70% or 130% of average earnings, respectively. France (main public scheme), Israel (only men) and Turkey apply regular means-testing against all household income.20

Survivor risks in private schemes

As with public pension schemes, not all private schemes – either mandatory or voluntary - pay survivor pensions. Old-age pension pay-outs can take different forms in funded private schemes (OECD, 2016[12]). For survivor pensions, private defined benefit (DB) schemes mostly pay, as in Iceland, the Netherlands or Switzerland, a fraction of the deceased’s pension, similar to many public schemes.

In mandatory funded DC plans, survivor schemes are often voluntary and relate to the remaining capital in the individual account at the time of death, but some plans exclude payments to survivors explicitly. Chile and Mexico stand out, granting a fraction of the deceased’s annuity to the survivor on a permanent basis.21 Moreover, in Chile as well as in Norway, the pay-out of the old-age pension in the form of programmed withdrawals includes survivor benefits until the balance of the account is drawn down. In Australia lump-sum payments at the age of retirement are widespread and, outside survivor pensions, the capital from accumulated pension assets that is not consumed at death is inherited by the spouse. In other countries, at least some schemes pay survivor pensions only temporarily or make them optional. Funded DC schemes in Iceland pay survivor benefits on a temporary basis, at an about 50% rate of the deceased’s pension for 3-5 years. Similarly, temporary payments are granted for 2 years in the Slovak Republic. In occupational plans in Denmark, survivor pensions are the default option.22

Voluntary pensions are typically even less regulated in the pay-out phase than mandatory schemes and cover the survivor risks mainly through the inheritance of unspent pension capital. In the Czech Republic, only the remaining pension capital minus state subsidies can be inherited. In the United States, the market share of DC plans in voluntary pension schemes has been increasing. Traditionally, DB plans have required annuitisation and included survivor options; moreover, opting out from the default survivor pension requires spousal consent in some schemes. By contrast, DC plans have more freedom, allowing for lump sums at the age of retirement and programmed withdrawals. These options are becoming more and more popular (Orlova, Rutledge and Wu, 2015[13]). Even if annuities are chosen, annuities without survivor option prevail. As a result, the increasing prevalence of DC plans has been associated with less coverage of longevity risks for surviving spouses.

Even in the case of a lifelong marriage, it is critical to distinguish whether survivor schemes are primarily about transferring pension assets to the surviving spouse or about ensuring a predictable flow of benefits to the survivor until he or she dies. Lump-sum payments and inheritance of remaining capital in programmed withdrawals ensure the transmission of accumulated pension assets to the survivor.

Lump-sum payments and programmed withdrawals do not insure against longevity risks. But this is the case for all households within those schemes, singles and couples. If policy makers assess that longevity risks should not be covered – which might be questionable normatively - and for example opt for lump sums, then survivor pensions within those schemes cannot be expected to address longevity risks. Yet, survivors are more vulnerable to longevity risk than other pensioners as they by definition live longer. In short, lump sums deal with the transmission of pension assets, but raise risks of survivors being exposed to insufficient income in old age.

7.4. Reforms to survivor pensions

Over the last thirty years, various reforms of the survivor pension were enacted in OECD countries. The most common trend was the extension of pension eligibility to men based on the same conditions as for women. This took place in Belgium, Canada, Chile, the Czech Republic, Finland, Germany, Hungary, Ireland, Israel, Japan, Korea, the Netherlands, Sweden, the Slovak Republic, Spain and the United Kingdom. In EU countries, this change occurred mainly in the 1990s in line with the 1984 EC Directive requiring the progressive implementation of equal treatment between men and women in social security matters. Some countries extended the coverage of the beneficiaries to same-sex partners or civil partners (Table 7.1).

Survivor pension reforms within evolving pension systems

In some countries systemic reforms of old-age pensions led to the elimination of survivor protection while in others it had no impact. First, in the 1990s, Italy, Latvia, Poland and Sweden reformed their public pay-as-you-go (PAYGO) pension schemes from DB into notional (non-financial) defined contribution schemes (NDC). Norway did so in 2011. The core of the NDC design mimics funded DC schemes with strong links between individual lifetime contributions and benefits. Redistribution features such as survivor pensions can be added within NDC schemes on top of this core principle.

Sweden eliminated survivor pensions in the public scheme in 1990, almost a decade before the introduction of NDC pensions. Disincentives for women to build their own entitlements, induced to some extent by survivor pensions, and the view that derived pension rights do not fully recognise the autonomy of women and change the balance of power against women within families was the main factor that drove this change. In line with this argument, recent simulations for the United States indicate that abandoning both survivor pensions and spousal pension supplements would increase women’s employment (Nishiyama, 2018[14]; Sánchez-Marcos and Bethencourt, 2018[15]).

In Latvia, as part of the move towards more individualised pension entitlements, survivor pensions for spouses were eliminated when the NDC scheme was introduced in 1996. In Norway, benefit levels were tightened in 2002 for survivors younger than 55 who do not work. With the introduction of the NDC scheme in 2011, survivor pensions received after the retirement age from the public scheme were gradually eliminated, with full effects for the generations born in 1963 and later. There is an ongoing debate in the country about whether survivor pensions after retirement age should be part of the NDC system and about transforming the survivor pensions paid until the retirement age into a temporary benefit, for a few years only, so as to improve incentives to participate in the labour market at working age.

In Poland, survivor pensions were almost unaffected by the introduction of NDC: survivor pensions were not incorporated into the NDC scheme and still pay a fraction of the deceased’s old-age pension without adjustment for the remaining life expectancy of the survivor. By contrast, Italy incorporated survivor pensions into the NDC design. To ensure financial balances of the NDC scheme including survivor pensions, the NDC cohort-specific annuity factor used to compute NDC old-age pensions is adjusted to account for the expected expenditure on survivor benefits. Second, the introduction of point systems - in the 1990s in Germany and Estonia, in the 2000s in the Slovak Republic and in 2018 in Lithuania - which also have tight links between earnings and benefits, did not affect benefit rules for survivor pensions in these countries.

Third, in the United Kingdom, after many substantial reforms since the 1960s, the 2016 reform linked old-age benefits only with the length of the contribution period and not with past earnings. At the same time survivor pensions for spouses were generally eliminated.23 Similarly, survivor pensions had been eliminated from the public schemes in Australia in 1997 and in New Zealand in 2013. The Netherlands which has a residence-based basic pension decided to eliminate the flat-rate survivor pension from their public schemes after the retirement age as indeed it was providing a higher flat-rate old-age safety net to widows and widowers than to singles.

Fourth, the role of private provisions within pension systems has increased in a number of OECD countries including Australia, Chile, Estonia, Lithuania, Latvia, Mexico, Norway, the Slovak Republic, Slovenia and Sweden. However, there have been some reversals in Lithuania, Hungary, Poland and the Slovak Republic more recently, with no major reforms in the direction of privatisation since 2007 (Bielawska, Chłoń-Domińczak and Stańko, 2015[16]; Kay, 2014[17]). All these changes have been accompanied by shifts from DB to DC schemes within occupational plans. For example, Mexico moved in 1997 from a PAYGO DB to a mandatory funded DC scheme. In the new system, survivor pensions are financed by additional contributions (Social Security Administration, 2018[10]). Already in 1981, Chile substituted its PAYGO DB scheme with the mandatory funded DC scheme, with survivor benefits remaining a strong component. Beyond these two countries, the move from DB to DC was often accompanied by a drop in the coverage of survivor risks.

In short, pension reforms in OECD countries have tended towards more individualisation through closer links between old-age benefits and lifetime contributions, and less redistribution within schemes. This might create some tension for the continuity of mandatory survivor pensions.

Trends in expenditures

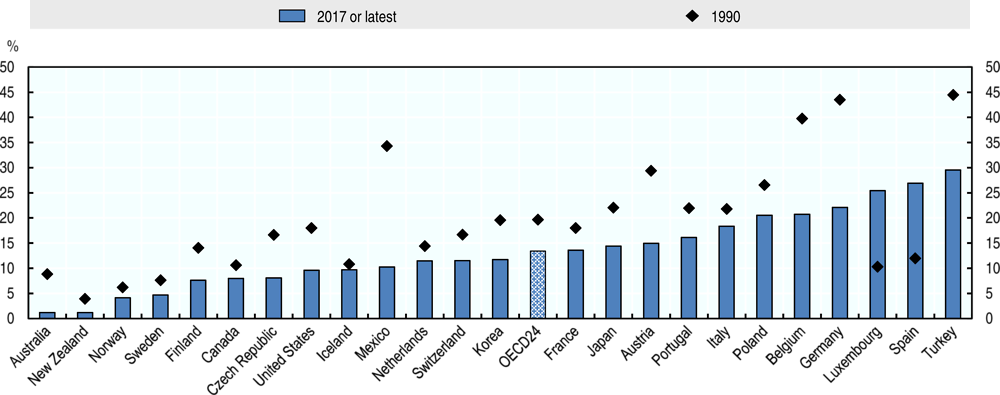

Survivor benefit expenditures have been influenced by both pension reforms and population ageing. Expenditures on survivor benefits have been stable compared to 1990 at around 1% of GDP on average across 24 OECD countries for which data are available. Austria, Belgium and Germany exhibit the strongest decline of more than 0.7 percentage points of GDP while the rise was most pronounced in Luxembourg, Portugal, Spain and Turkey (about 1 p.p. or more).

On average in the 24 OECD countries, survivor benefit expenditures have not kept pace with old-age pension spending which substantially increased from 5.5% of GDP in 1990 to 8.0% in 2017 (or latest). Indeed, survivor benefit expenditures from mandatory pensions represented 13% of old-age spending in 2017 (or latest), down from 20% about twenty-five years earlier on average (Figure 7.11). Higher women’s own contributory pensions driven by their increasing employment, a lower gender gap in life expectancy and changes in couple formation may have contributed to this fall (Section 7.2). Additionally, stricter means-testing and a tightening of benefits and eligibility conditions partly explain this trend.

Note: See Figure 7.1. Data for Chile, Denmark, Greece and Ireland were not included due to break in series. Data for the other missing OECD countries are not available for 1990.

Source: OECD preliminary social expenditure database.

The strongest declines in survivor benefit spending relative to old-age pension expenditures between 1990 and 2017 are recorded in Belgium, Germany and Mexico. Germany broadened the means-tests to nearly all kinds of income in 2001, limited the duration of some survivor benefits to two years, introduced a one-year requirement on the minimum length of marriage and cut benefit levels from 60% to 55% of old-age pensions. For Mexico, the fall is less meaningful as old-age pension spending was very low in 1990. Other countries have also tightened access to survivor pensions, such as France and Norway.24 New Zealand went further by abolishing the survivor benefit altogether in 2013.

Only in Luxembourg and Spain have expenditures on survivor benefits risen more strongly than on old-age pensions. Both countries increased the survivor benefits and expanded the coverage: Luxembourg for the same-sex couples and Spain for the registered cohabitations.

7.5. Future survivor pensions

Despite the recent trend towards more individualisation of old-age pensions and the abolishment or tightening of survivor pensions in several countries, the great majority of OECD countries still has mandatory survivor schemes for future pensioners. For people entering the labour market now, the current legislation does not include any automatic transfer of pension entitlements to the surviving spouse after the retirement age in only seven countries: Australia, Latvia, the Netherlands, New Zealand, Norway, Sweden and the United Kingdom. There, pension adequacy risks for survivors are covered through safety nets or are left to individuals who can either opt for survivor pensions within private schemes or buy an annuity with a survivor option from private insurers (Box 7.2).

This section is structured as follows. First, it discusses how own pensions affect the level of survivor pensions. Second, it shows how survivor pensions contribute on top of existing safety nets to protecting retirement income and preserving standards of living after the death of a spouse. Finally, this section presents the impact of introducing pension-rights splitting on top of or in place of existing mandatory survivor pensions.

This section is based on modelling the old-age and survivor pension entitlements from mandatory pension schemes for individuals entering the labour market in 2016. For simplicity, it focuses on same-age couples and assumes that the wife outlives her husband who dies shortly after retiring at the normal retirement age.25 For most countries, the results also apply to husbands outliving their wife and to same-sex couples.26

How much is the pension of the deceased replaced by survivor schemes alone

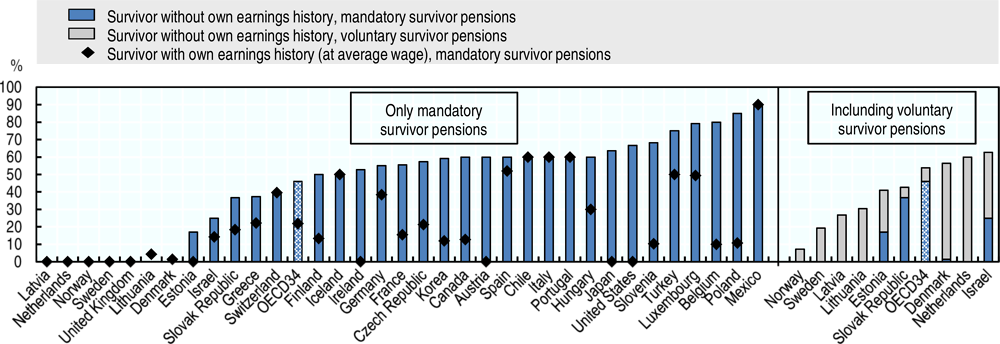

Taking into account all sources of contributory pensions - and ignoring residency-based basic pensions - a never-working survivor would, on average across OECD countries, receive a survivor pension equal to 46% of the pension of the deceased spouse who had a full career at the average wage. Figure 7.12 shows zero or minimal numbers for countries without mandatory survivor pensions, plus Denmark and Lithuania.27 Apart from these, the replacement from survivor pensions is 25% or lower in only Estonia and Israel. It is 75% or larger in Belgium, Luxembourg, Mexico, Poland and Turkey.

The average survivor pension of 46% of the deceased’s pension remains below the replacement level of 50% shown in Figure 7.10. The main reason is that several countries grant spousal pension supplements to pensioners if their spouses have no or low own pensions, but not to survivors thereby lowering the effective survivor replacement rate compared to Figure 7.10. Such supplements play a large role in Ireland where the basic pension increases by 90% in case of having a spouse without own contributions as well as in Israel and the United States, where it can equal 50% of own public pensions, and in Belgium (25%). Except for low earners, supplements are less important, in Japan and Korea which pay flat-rate benefits. Also, Switzerland has mandatory pension splitting during marriage, which increases the old-age pension of a spouse without work history but reduces the survivor pension.

Note: For voluntary survivor options in private mandatory schemes the simulation assumes that a couple buys a joint-and-survivor annuity that lowers the payment to 60% upon the death of the primary holder (Box 7.2). The only exception is the Slovak Republic where the survivor receives the same pension as the deceased but only for two years. Australia and New Zealand are not included (see note of Figure 7.10).

Source: OECD pension model.

An own pension reduces survivor benefits in many countries. On average in the OECD, the survivor replacement rate in mandatory schemes decreases from 46% for a single-earner couple to only 22% when both individuals had the same baseline career (Figure 7.12). The impact of having an own pension varies a lot across countries. In Austria, Estonia, Ireland, Japan, and the United States, own pensions fully eliminate entitlements to survivor benefits in the case of spouses having the same earnings history at the average wage. By contrast, in Chile, Iceland, Italy, Mexico, Portugal and Switzerland mandatory survivor benefits remain unaffected.

In many private mandatory pension schemes, survivor pensions are voluntary and survivor benefits are financed by an upfront reduction of earnings-related pensions. When voluntary survivor pensions (in mandatory pension schemes) are accounted for, the survivor replacement rate for a non-working partner increases from 46% to 54% on average. It is less than 25% only in the United Kingdom, which have no mandatory earnings-related schemes and no survivor scheme for basic pensions (unlike Ireland), as well as in Norway and Sweden, where the contributions to the private DC scheme are relatively low compared to the public scheme. By contrast, when accounting also for the voluntary option, the survivor replacement rate in Denmark, Israel and the Netherlands exceeds the OECD34 average from mandatory survivor pensions.

Contribution of survivor pensions to survivors’ total pension income

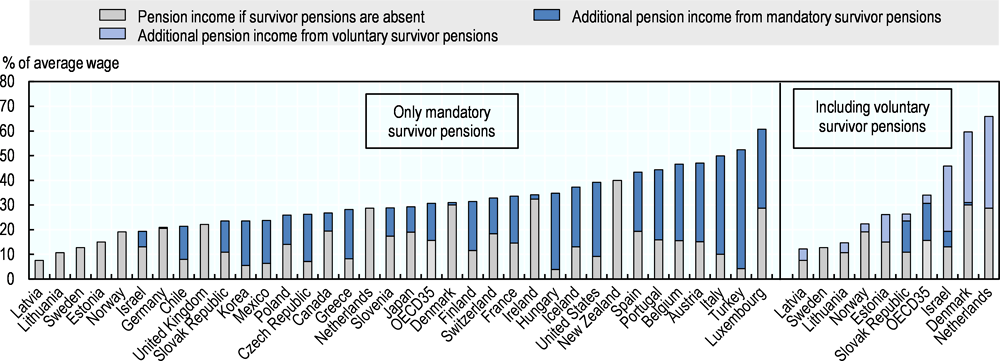

Survivor pensions can provide substantial additional income to widowed persons. On average across 35 OECD countries, basic pensions and safety nets currently provide an income of 20% of the gross average wage for those who have never worked. Based on economic assumptions used in the OECD pension model, current indexation rules imply that when those who entered the labour market in 2016 will reach the retirement age this average will fall from 20% to 16%. A spouse who has never worked and survived a full-career average-earning partner would additionally receive 15% of the average wage from mandatory survivor options, thereby 31% in total, almost doubling retirement income (Figure 7.13). Voluntary survivor pensions add a further 3 percentage points, or 34% in total.

Note: The “pension income if survivor pensions are absent” series calculates total pension income that would be paid if survivor pensions were ignored, taking into account additional benefits from first-tier pensions that would become available. Additional pension income from survivor pensions then displays the effective additional income stemming from survivor pensions. Australia is excluded due to comparability reasons.

Source: OECD pension model.

Based on mandatory survivor pensions alone, the total pension income of a widowed spouse who never worked and was partnered to a full-career average-wage worker exceeds 40% of the gross average wage in Austria, Belgium, Italy, Luxembourg, Portugal, Spain and Turkey. On the other side of the spectrum, no additional total income stems from mandatory survivor pensions in Estonia, Latvia, Lithuania, Norway, Sweden and the United Kingdom where the surviving spouse would receive less than 25% of the gross average wage. Also in Germany, where the old-age safety net is withdrawn, additional income from survivor pensions is close to zero in that case.

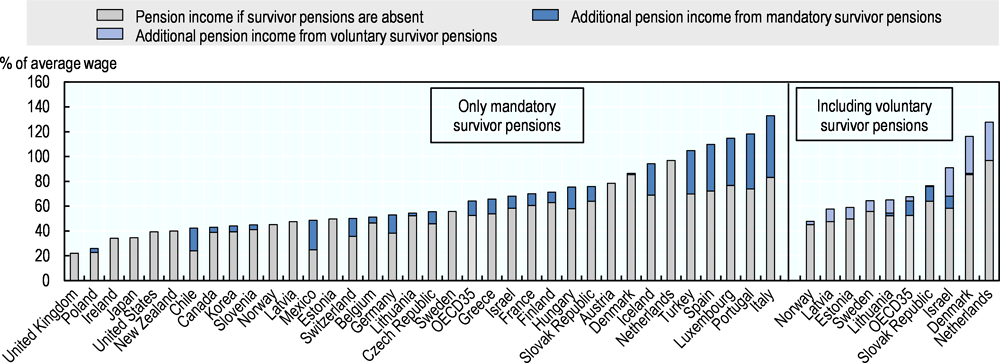

The own pensions of a survivor diminish survivor pension levels to some extent: on average in the OECD, a surviving spouse of a two-average-earners couple can expect the own gross pension of 53% of average wage to be topped up by a mandatory survivor pension of 11 percentage points – instead of 15 p.p. when the surviving spouse never worked - to 64% (Figure 7.14). Still, in that case survivor pensions substantially improve the situation of the survivor compared to a single person with a similar work experience in Austria, Belgium, Chile, Iceland, Luxembourg, Mexico and Southern European countries.

Note: The “pension income if survivor pensions are absent” series calculates total pension income that would be paid if survivor pensions were ignored, taking into account additional benefits from first-tier pensions that would become available. Additional pension income from survivor pensions then displays the effective additional income stemming from survivor pensions. Australia is excluded due to comparability reasons.

Source: OECD pension model.

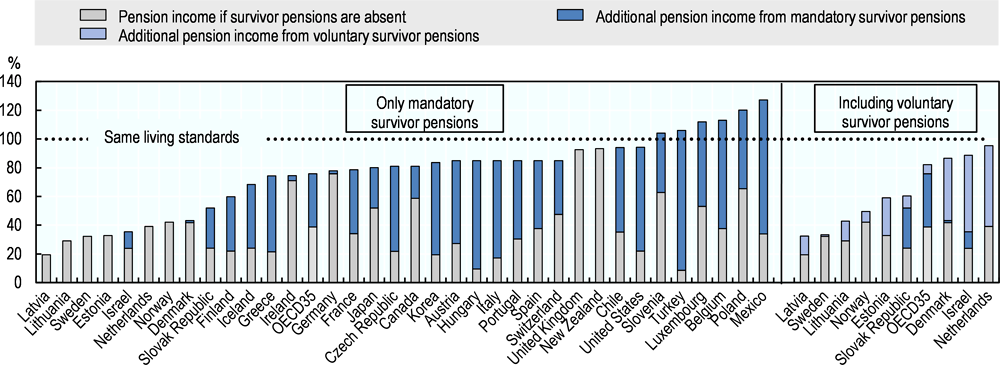

Preserving living standards after partner’s death

Economies of scale that benefit couples can be significant, but stop playing for survivors (Box 7.1). In particular, living costs do not drop by half upon the partner’s death, even when downsizing the accommodation. Based on the OECD equivalence scale, a drop of more than 30% in the total income of the couple household reduces the standards of living of the survivor upon the partner’s death.

After the death of their spouse, survivors without work history would have, on average across 35 OECD countries, an equivalised disposable income equal to 76% of its pre-death level (Figure 7.15). This means that they would lose on average 24% in standards of living (18% if voluntary survivor options are taken). Mandatory survivor pensions offset three-fifths of the financial impact induced by the loss of the breadwinner’s entitlements, as without survivor pensions the loss would reach 61%.

Countries which record the largest losses in standards of living following the death of a partner, more than 25%, are those that combine low first-tier benefits with low replacement from survivor pensions: Estonia, Finland, Greece, Iceland, Ireland, Latvia, Lithuania, Norway, the Slovak Republic and Sweden. By contrast, the equivalised disposable income increases for survivors in Belgium, Luxembourg, Mexico, Poland, Slovenia and Turkey. Single-breadwinners outliving their spouses who never contributed to pensions also experience rising living standards in most countries. On average in the OECD, their equivalised disposable income increases by about 25%.

Note: The “pension income if survivor pensions are absent” series calculates total pension income that would be paid if survivor pensions were ignored, taking into account additional benefits from first-tier pensions that would become available. Additional pension income from survivor pensions then displays the effective additional income stemming from survivor pensions. Australia is excluded due to comparability reasons.

Source: OECD pension model.

Pension splitting and survivor pensions – policy scenarios

The splitting of pension rights is often discussed as an alternative to survivor pensions, even though both can be combined. Splitting of pension rights means that old-age pension entitlements of partners are first totalled and then divided between partners, half-half or in any other proportion. The splitting can take place when contributing, separating or retiring. Hence, splitting increases the old-age pension of the surviving partner who has accumulated fewer own entitlements than the deceased partner. At the same time, it reduces the old-age pension of the surviving partner who has higher own entitlements. Moreover, pension splitting may reduce the survivor pensions that are subject to a means-test against other pension income.

Switzerland is the only country that has made pension splitting mandatory, in its public scheme since 1997. Germany introduced in 2002 the choice, at least for some restricted cases, to trade the entitlement to a survivor pension against a fifty-fifty splitting of pension claims between partners upon the retirement of the younger spouse. Take-up rates in Germany are very low though as only couples who were either married after 2001 or born after 1961 are eligible; but this may be also due to the financial disadvantage of pension splitting compared to survivor pensions. The next section provides a discussion about what splitting brings while highlighting that it is not a substitute to survivor pensions.

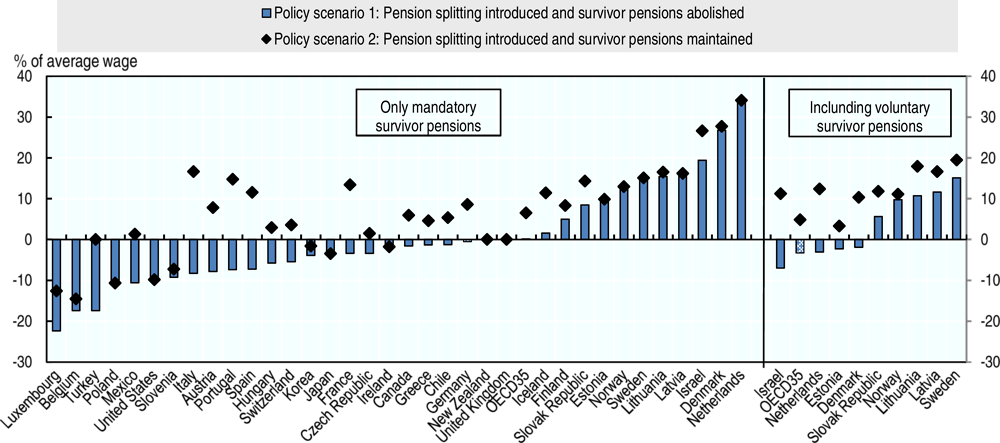

The following simulations assume that fifty-fifty splitting of total pensions is introduced in all countries, first to replace mandatory survivor pensions. Such a shift from the current mandatory survivor schemes to splitting would generate significant changes in many countries, but on average across 35 OECD countries the total pension of the survivor who never worked and was married to an average earner will be similar (Figure 7.16).

Note: The simulation assumes the deceased of the same age couple had a full career from age 20 in 2016 at the average wage and died just after having retired. Latvia, the Netherlands, New Zealand, Norway, Sweden and the United Kingdom do not provide mandatory survivor pensions in that case. The introduction of pension splitting splits total pension income with the exception of Switzerland where it only applies to the mandatory occupational scheme as splitting already exists in the public scheme. Australia is excluded due to comparability reasons.

Source: OECD pension model.

Pension splitting would increase the pension income of survivors by more than 15% of the average wage in Denmark, Israel, Latvia, Lithuania, the Netherlands and Sweden due to the lack of a mandatory survivor pension in the earnings-related schemes. By contrast, in the majority of OECD countries (22 exactly) the existing survivor pensions are more beneficial than splitting for survivors who were married to average earners and without own earnings-related pension. In Belgium, Luxembourg and Turkey the total pensions of survivors would decrease by more than 15% of average wage if survivor pensions were replaced by pension splitting due to high survivor replacement rates, markedly above 50%.

Moreover, a worker outliving his never-earning spouse would never benefit from the introduction of pension splitting as he/she would give up own old-age pension entitlements without receiving survivor pensions in the first place.

Including voluntary survivor pensions turns the average impact of splitting negative, equalling -3% of average wage across OECD countries (right part of Figure 7.16). Survivors covered by the voluntary survivor options would be worse off if splitting replaced survivor pensions in Denmark, Estonia, Israel and the Netherlands while they would be still better off in Latvia, Lithuania, Norway, the Slovak Republic and Sweden.

The second policy scenario looks at the introduction of pension splitting while preserving the existing mandatory survivor pension rules. In this simulation survivor pension rules apply to the old-age pension of the deceased after splitting. Such a change would raise the pension income level of survivors who have never worked by 7% of average wage on average in the OECD. In France, Italy, Portugal and Spain total pension income of a survivor would increase by more than 10% of average wage upon introducing pension splitting while maintaining current survivor pension rules, compared to a decline in the scenario that survivor pensions are simply replaced by splitting. By contrast, in Belgium, Luxembourg and Poland pension splitting would lead to a reduction of survivor’s total pension income by more than 10% of average wage whether survivor rules are maintained or abolished. There, strict means testing against other pension income reduces survivor pension payments drastically upon the introduction of pension splitting in mandatory schemes.

7.6. General discussion

Survivor pensions is a complex topic and is often integrated within social policies. It mixes various elements of old-age pensions, family policies and inheritance rights. Historically, survivor pensions were designed to smooth standards of livings after the death of a spouse and help widows fight poverty. Nowadays, poverty relief is a policy objective that is targeted by specific instruments which do not differentiate between singles and widows or widowers. Hence, consumption smoothing is currently the key objective pursued by survivor pensions, which in many cases de facto helps reduce the pension gap between men and women.

Inheritance of pension entitlements

Are pension entitlements part of inheritable assets? Whether pension entitlements are viewed as a more or less explicit part of own accumulated assets influences whether they should be treated as part of inheritance rights. In practice, the principles governing survivor pensions still mix the wealth and redistribution rationale.

In general, PAYGO entitlements until being withdrawn are promises and cannot be transmitted unless survivor schemes come into play. Then in the absence of survivor schemes, the contributions made for example by people who die before the retirement age are lost to the heirs, which tends to increase the pensions of people who survive until that age. Most funded defined benefit schemes also fall in this category. In all these schemes, the pension entitlements of a single person are not part of her estate.

Individual funded defined contribution accounts are closer to the idea of personal assets that can be inherited, even though recent measures have questioned the strength of pension property rights in some countries. 28 This is typically the case during the accumulation phase if the contributor dies before retiring. If the contributor survives and starts to withdraw, the choice might need to be made between lump sums (which then fall within private assets), programmed withdrawals or individual annuities which might obey some specific rules for survivor pensions, or joint-life annuities which directly address survivor risks.

Survivor pensions and redistribution

The original design of survivor pensions refers to a timeworn family model. The man was working, the woman was taking care of children and house, and everyone was assumed to be part of a unique, lifelong heterosexual marriage. The foundations of this model have been questioned, female formal employment has progressively expanded, and family formations have been less stable and more diverse (Section 7.2). In the meantime, pension entitlements have become more individualised, potentially creating some tension with redistribution mechanisms such as those inherent in survivor pensions. Over the last decades, most of survivor pension reforms, especially in Nordic and Anglo-Saxon countries, have tended to limit access to derived rights (Section 7.4).

These societal changes have been occurring in a challenging period for pension systems. Demographic changes driven by increased longevity and low fertility put pressure on old-age support ratios, weakening the finances of defined benefit schemes and the rates of return of defined contribution pensions. One policy implication has been to emphasise that pension policies should promote labour force participation for everyone.

Making a surviving partner eligible to a permanent survivor pension at an age lower than the normal retirement age is therefore inconsistent with these general principles.29 Instead, being eligible to a permanent survivor pension should be consistent with retirement age rules. For survivors of younger ages, in order to offset the financial burden created by the death of a partner, a temporary allocation – e.g. during a couple of years or until dependent children reach adulthood – should be granted to help adapt to the new situation. When the survivor reaches the retirement age, the full survivor pensions could kick in. An alternative is to set a given age threshold (lower than the retirement age) at the time of a partner’s death, from which the surviving partner is entitled to part of the survivor pension when reaching the retirement age, with that part increasing steadily with the age at partner’s death and reaching 100% for death occurring if the survivor reached the retirement age.

Survivor pensions could take the form of a redistribution within a given household through time, i.e. from before to after the death of a partner. Their current designs, however, typically involve redistribution across households which might have unintended consequences.30 If survivor pensions are combined with the same contribution rates and benefit levels for individuals being single or living in a couple, they imply some redistribution, which is difficult to justify, from singles to couples and from dual-career couples to single-earner couples, especially to those with large age differences (James, 2009[18]). For example in that case, singles get no benefit from survivor schemes and yet they contribute to financing the extension of entitlements to survivors. This arises because the individual pension amount does not account for the cost of joint-life insurance.31 The financing of survivor pensions by singles is also questionable because survivor pensions help compensate for lost economies of scale that singles never benefited from.

Internalising the cost of survivor pensions

There are two ways to avoid these undesirable forms of redistribution. First, as in Chile and Sweden for the funded schemes for example, partners while benefiting from economies of scale in their cost of living receive (or can choose to in Sweden) lower individual pension benefits when both partners are alive to finance the survivor benefit upon death. Financing a survivor benefit equal to 60% of the deceased’s pension reduces initial pensions - when both partners are alive - by about 9% compared to singles with the same contribution history (Box 7.2). Because this reduction is meant to finance survivor pensions which are currently financed by lowering the own pensions of everyone, a budget-neutral reform which implements such a mechanism would lead to an increase of pensions for singles, and therefore a much lower total reduction than 9% for couples. This internalises the expected cost of survivor pensions within a given household or at least, more generally, among couples.32 The second way of internalising is by splitting pension entitlements within couples, as discussed further below.

Less common lifelong marriage and increased female employment surely diminish the role survivor pensions have to play. Yet, beyond remaining gender gaps, consumption smoothing upon the death of a partner is still a worthwhile objective to be pursued by social policies, and in particular through survivor pensions. While fewer and fewer pensioners will rely on survivor pensions, those who have to will still be particularly vulnerable after the death of their partner. Even in the case where both partners had the same career, the standards of living of the survivor would decline by about 30% due to economies of scale of living in a couple.

Both myopic behaviour and incomplete information lead to insufficient insurance of survivor risks at a fair price through private insurance and efficient annuity markets (Barr and Diamond, 2008[19]; Blake, 2012[20]; Findley and Caliendo, 2008[21]), which justifies the need for mandatory survivor pensions.33 In particular, short-slightness, compulsory behaviour, low financial knowledge and information procession costs mean that people do not insure themselves well against especially distant, future events. These limitations may be stronger for survivor pensions than for old-age pensions because they require planning beyond the horizon of own life.

Taking stock of the recent trends in couple formation, survivor pensions should in principle be extended beyond marriages to civil unions and formal partnerships. One open question though might be whether survivor pensions should be limited to partnerships which have some legal or financial obligations in terms of solidarity within couples. If there is no formal obligation, a partner might not be protected to start with by his or her partner when both partners are alive; it might therefore be questionable whether consumption-smoothing when the partner dies is a valid objective for public policy. There is also some concern that such an extension of eligible partnerships could reinforce unions of convenience as partners approach retirement ages. However, as for marriages, if the cost of survivor pensions is internalised within couples as suggested above, these concerns will be limited. If it is not internalised then at least, in order to justify the cost to the public purse more fairly, survivor pensions should be based on the prorated length of the current union as a share of the total contributed period.

Splitting pension rights

The situation is very different for divorced and separated partners, to whom survivor pensions should not be eligible. Indeed, the consumption-smoothing motive does not apply to old partnerships because there is no current consumption to smooth. The main question, however, refers to past pension entitlements. During the partnership, resources were typically shared and some decisions such as those related to the allocated time for formal employment - that generates pension rights - and informal activities such as home-based work – that does not – have typically been taken jointly. Some OECD countries, including Estonia, France, Germany and Luxembourg, endorse this resource sharing by taxing spouses or partners jointly or allowing them to fill a joint tax statement. Therefore, pension entitlements accumulated during the partnerships can be considered at least partly to be common to the partners.

In that sense, there is a strong case to split, at least partially, the pension entitlements of both partners (Box 7.3). For example, in the case of a full split, each partner gets half of the total entitlements accumulated by both partners during the union.34 Splitting also facilitates separation arrangements; court judgements upon divorce typically split some (private) pension rights acquired during marriage similarly to splitting assets and granting alimony. With splitting, pension entitlements are automatically prorated for the duration of partnerships.

One advantage of splitting is that this mechanism focuses on entitlements earned during the partnership and minimises the impact of the ex-partners’ career after a separation. However, while splitting is fairly easy to implement in defined contribution and point systems or in defined benefit systems that are based on straightforward accrual rates, it is more complicated to introduce splitting in complex and fragmented pension systems as well as in schemes with loose links between contributions and pension entitlements.35