Lithuania

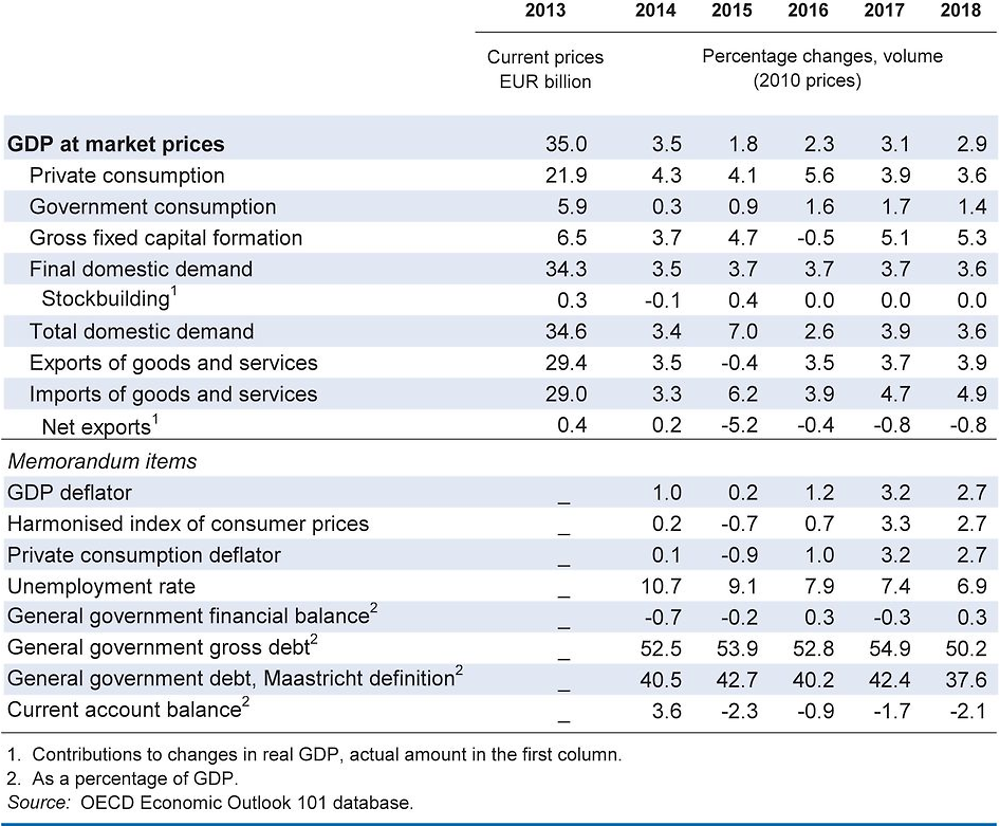

Economic growth is projected to strengthen as investment related to EU funds and external demand gather steam. Employment growth is limited due to a shrinking labour force and skill shortages. A temporary spike in energy prices and rising nominal wages will push up inflation.

The fiscal stance is projected to be broadly neutral over the period 2017-18. The structural measures in the budget are welcome. Further reforms are needed to reduce high inequality and poverty, as well as to deal with rapid population ageing. In particular, these include efforts to make activation programmes more effective, enhance outcomes and equity in education, and strengthen incentives to work.

Growth potential would be enhanced by deeper integration in global value chains with reforms in the business environment, including cutting red tape and upgrading infrastructure, and making R&D business support more effective. Promoting lifelong learning is essential to reap the benefits of globalisation and help workers who have been displaced find new, good jobs.

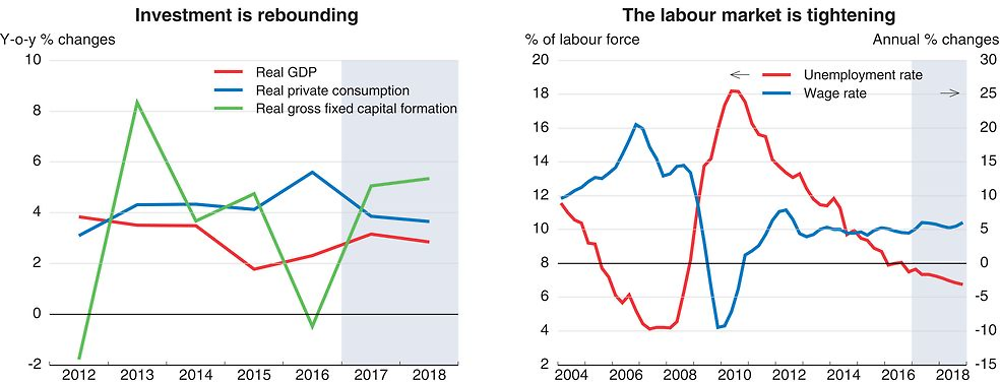

Growth is picking up

Economic activity has gained momentum as investment has strengthened with the rebound of disbursements of structural funds under the new EU programming period. Buoyant transportation activity has provided a boost to service exports. Falling unemployment has pushed up wages, and lower income taxes, that have increased disposable income, have supported private consumption. Higher energy and food prices and increases in some excise duties (including on tobacco and alcoholic beverages) have temporarily reinforced price increases.

Boosting productivity and inclusiveness requires further reforms

Euro-area monetary policy remains very accommodative, and lending to the private sector is recovering. The 2017 budget entails some discretionary fiscal measures, notably an increase in the non-taxable income threshold in the personal income tax. Structural reforms related to the budget include making labour relations more flexible, unemployment and social insurance benefits more generous, and active labour market policies broader in scope. Although the general government budget is set to move to a deficit in 2017, mostly due to the costs of structural reforms, the fiscal stance is projected to remain broadly neutral over the period 2017-18.

Source: OECD Economic Outlook 101 database.

Fostering inclusive growth requires additional reforms to raise pre-primary education participation rates and teaching quality. Poverty reduction requires increasing financial incentives to work by reducing high effective marginal tax rates and improving the monitoring and evaluation of active labour market programmes to ensure that they increase the employability of most vulnerable groups. Their financing can be accommodated by improving tax compliance and increasing spending efficiency, especially in education.

Deeper integration into global value chains would boost growth. Success hinges on improvements in the business environment, including through simplified bankruptcy procedures and further cuts in red tape to buttress investment. There is also significant scope to improve public infrastructure, including through upgrades to the railway and road network. Enhancing innovation by making R&D business support more effective and encouraging research collaboration would help foster internationally competitive firms. Upskilling the workforce through the promotion of lifelong learning and strengthening job-search support for the displaced workers would facilitate a reallocation of labour, helping to respond to globalisation challenges.

The economy will expand robustly

Real GDP is projected to grow by around 3% in 2017-18, driven by a further increase in exports as activity in major markets strengthens and by solid investment growth supported by favourable financial conditions and an increase in EU funding disbursements. Private consumption will be underpinned by rising wages. Nevertheless, a shrinking labour force will constrain consumption growth. The impact of higher commodity prices will dissipate over the projection period, but labour market tightening will continue putting pressure on inflation.

Lithuanian growth will depend on the strength of the euro area. An escalation of geopolitical tensions could hurt exports and investment. On the domestic side, labour supply constraints could limit employment growth more than projected. However, a stronger euro area recovery could push output growth beyond the projected rate. Implementation of structural reforms, notably the introduction of the new labour code and measures to boost investment, could lead to faster productivity growth.