4. Measuring and Reporting Personal Income Tax Expenditures

This chapter presents the approach that Colombia currently follows to measure and report Personal Income Tax (PIT) Expenditures, and identifies areas for improvement. It presents the equations that can be applied to measure revenue forgone from different PIT TEs on an item-by-item basis and discusses strategies to obtain more granular data. The chapter also includes the item-by-item revenue forgone estimates calculated by DIAN following the OECD’s proposed methodology and presents a distributional analysis of a number of PIT TEs.

This chapter presents the approach that DIAN currently follows to measure and report Personal Income Tax Expenditures, and identifies areas for improvement.

General assessment of the DIAN TE methodology

Following the guidance provided by the Tax Incentives Commission (OECD, DIAN and Minhacienda, 2021[1]), the two most recent editions of the Marco Fiscal de Mediano Plazo (MFMP) have introduced a number of improvements to the measurement of PIT TEs. For instance, the 2022 edition of the MFMP has started to include information on an item-by-item basis – although in terms of the amounts that are declared rather than the corresponding revenue forgone – for a selected number of PIT TEs, including the pension income exemption, the exemption of voluntary pension contributions and the mortgage interest deduction.

The aggregate estimates available in the MFMP draw on information from individual tax returns. Similar to the CIT TEs, data from specific cells in the tax return combines information on tax provisions that are viewed as a TE as well as provisions that are part of the benchmark (and are therefore not a TE).

To calculate revenue forgone, DIAN applies the average marginal tax rate based on the information available at the time of the publication of the MFMP report. This approach yields biased estimates for a number of reasons and can be improved.

Less than 2% of the taxpayers that submit a tax return are required to submit supplementary tax forms that provide more detailed information on the tax provisions they claim. Individual taxpayers are required to submit these so-called “exogenous information forms” if their gross income exceeds COP 500 million (approximately USD 132 000) and if, in addition, the sum of their gross capital and non-labour income exceeds COP 100 million. These limitations severely limit the usefulness of exogenous information for the measurement of PIT TEs.

Recommendations to improve the measurement and reporting of PIT revenue forgone

A first priority would be to ensure that provisions that are viewed as TEs are not reported together with provisions that are considered part of the benchmark in the PIT tax return. DIAN should also start collecting more disaggregated information within the tax returns that taxpayers need to file. This will allow DIAN to estimate more PIT TEs on an item-by-item basis, increase the accuracy of the PIT revenue foregone estimates and increase transparency. Furthermore, more taxpayers should be required to provide additional exogenous information.

Going forward, the methodology that is applied to estimate revenue foregone could be further refined, with the goal of using the available PIT micro data more efficiently. DIAN could also improve the way it reports PIT TEs. This analysis, and the corresponding recommendations, are developed in detail in the following sections.

Section 4.2 presents the tax equations that can be applied to measure revenue forgone from different PIT TEs on an item-by-item basis. The analysis also recommends DIAN to switch from applying an average marginal PIT rate to applying the actual PIT rate schedule to the taxable income (with and without the TE) of each taxpayer and then take the difference to estimate revenue forgone. Applying an average marginal PIT rate is only recommended when only aggregate TE data is available.

Section 4.3 includes the revenue forgone estimates calculated by DIAN following the OECD’s recommendations based on PIT returns data from all taxpayers. This Section also makes recommendations with respect to the types of tables with information on PIT revenue forgone that could be included in the TE report. Finally, the Section refers to Annex D, which provides a comprehensive list of all 124 PIT TEs that have been identified in collaboration with DIAN and the Ministry of Finance. Section 4.4 provides examples on how to use tax returns to perform distributional TE analysis by analysing the distribution of claimants and revenue forgone on an item-by-item basis for a number of TEs.

Section 4.5 discusses strategies DIAN could pursue to obtain more granular data. Recommendations include (i) redesigning the PIT return, (ii) increasing the number of taxpayers that are required to submit exogenous information, (iii) using additional data that allows for breaking down information in cells in the tax return that record both TEs and non TEs, or multiple TEs and (iv) exploring additional sources of information. Section 4.6 discusses additional analysis DIAN could conduct using tax returns such as bunching analysis to assess taxpayers’ behaviour. Section 4.7 discusses SIMPLE and whether some TEs within this preferential regime could be reported.

The Marco Fiscal de Mediano Plazo (MFMP) includes very limited information on the revenue foregone of TEs within the PIT (Minhacienda, 2022[2]). Up to 2021, the tables in the MFMP only included an aggregate estimate of all exempt income items and tax credits. The MFMP report published in 2022 includes more information; it reports the revenue foregone of all deductions although this includes not only non-standard deductions but also deductions that are part of the benchmark (and that are therefore not a TE). The revenue foregone of non-taxable income does not feature in the report. DIAN presents PIT revenue forgone estimates in summary tables that include also the revenue forgone from CIT TEs. The report then reports total exempt income and total deductions rather than the corresponding forgone tax revenue. The 2022 edition of the MFMP also includes item-by-item estimates (in terms of aggregate take-up rather than revenue forgone) for a selected number of TEs, including the pension income exemption, the exemption of voluntary pension contributions and the mortgage interest deduction.

The estimates available in the MFMP draw on information from individual tax returns. Similar to the concerns that were raised with respect to the CIT TEs, the aggregated data that is filed within the PIT returns combines tax provisions that are TEs as well as provisions that are part of the benchmark. As a result, DIAN’s current revenue foregone estimate of exempt income is biased upwards by income that is not taxed under the TE benchmark, such as income that is exempt as a result of double taxation treaties.1 Similarly, by treating all deductions as TEs, the MFMP overestimates the PIT TEs as many of these deductions are included in the benchmark tax system, and they are therefore not a TE.2

Because tax returns data is only available with a time lag, DIAN produces estimates for two consecutive years based on the same data source. For example, the revenue forgone estimates for 2021 and 2020 that are published in the 2022 edition of the MFMP both draw upon tax returns from 2020.

To calculate revenue forgone, DIAN applies an average marginal tax rate based on the information available at the time of the publication of the MFMP report. For example, the MFMP 2022 estimated an average marginal tax rate of 7.4% on the basis of tax returns data from 2020. Section 4.2 discusses the use of the average marginal tax rate and makes recommendations for an alternative approach that would yield more accurate estimates of the TEs’ revenue foregone.

Similarly to the CIT, supplementary “exogenous information” is available to calculate the revenue foregone of PIT TEs. However, less than 2% of the taxpayers that submit a tax return are obliged to submit these supplementary tax forms. Individual taxpayers are required to submit exogenous information forms if their gross income exceeds COP 500 million (approximately USD 132 000) and if, in addition, the sum of their gross capital and non-labour income exceeds COP 100 million. Taxpayers who receive capital or non-labour income are also required to submit exogenous information if they are unincorporated businesses that employ workers and therefore withhold income tax on behalf of their employees and/ or are VAT registered. In light of the limited scope of the exogenous information, Section 4.2 includes recommendations on how to optimise the use of the tax returns data for the measurement of the revenue foregone of PIT TEs. Section 4.3 presents recommendations on how to improve the reporting on PIT TEs and Section 4.4 discusses how more data could be collected, either from tax returns or from additional information sources, in order to improve the accuracy of the TE estimates.

Exempt income, non-taxable income and non-standard deductions

Unlike CIT TEs, and as a result of the progressive PIT rate schedule, the removal of a PIT TE that would increase taxable income could push a taxpayer into a higher tax bracket, which implies that the increase in taxable income would be taxed at a higher marginal PIT rate than the statutory PIT rate that applied when the TE was in place.

As micro data for each taxpayer is available, DIAN can estimate tax revenue forgone by applying the actual PIT rate schedule (Table 4.1) to the actual taxable income of each individual in each fiscal year. Instead, DIAN currently applies an average marginal tax rate, which is the average effective marginal rate across all taxpayers. This method, however, results in biased estimates as it disregards that a reduction in exempt income, non-taxable income and non-standard deductions (as a result of the withdrawal of a TE) can have an impact on the taxpayer’s marginal PIT rate. Furthermore, the average marginal tax rate that DIAN applies may be different from the average marginal rate that applies to taxpayers who benefit from a particular TE. As a result, DIAN currently underestimates the tax revenue forgone from regressive TEs, which are claimed by taxpayers with high taxable income and who therefore face a higher marginal PIT rate.

To implement the suggested approach, DIAN should first calculate, for each taxpayer, the PIT liability when the exempt income, non-taxable income or non-standard deduction is added to taxable income. Then, it should take the difference between the re-calculated tax liability and the current tax liability that the taxpayer faces when applying the PIT schedule to the actual taxable income that has been declared. Finally, the revenue forgone would be aggregated across individuals.

For a provision that grants and the defined by the general PIT schedule (see Table 4.1), revenue forgone generated by taxpayers would be estimated as follows:3

Dividend income and occasional gains

As discussed in Chapter 1, the proposed benchmark rate for dividend income and occasional gains is the proportional rate currently in place (10%). As a consequence, TEs that narrow the tax base linked to dividend income and occasional gains should be measured by taking into account the 10% benchmark rate. Tax revenue forgone from the exemption for dividend income up to 300 UVT (art 35, Law 2010 of 2019) would be measured as follows:

Let represent exempt dividend income from individual up to 300 UVT, then revenue forgone from this item is calculated as follows:

TEs that require a specific estimation methodology

The estimation of revenue foregone of a number of TEs would require a different estimation methodology than the method that has been introduced above:

Pension income exempt up to 12 000 UVT (art 96, Law 223 of 1995). Under the proposed income benchmark, the zero-rate bracket of the general PIT rate schedule (1 090 UVT) is included within the benchmark. However, pension income benefits from an additional exemption (12 000 UVT). The excess allowance claimed above the standard allowance is a TE. To compute revenue forgone, this excess allowance should be added to the pensioner’s taxable income and the general PIT rate schedule should then be applied. Finally, the difference between this amount and the current tax liability of the pensioner, summed over all pensioners, then yields revenue foregone from this TE.

Voluntary contributions to private pension funds and AFC housing savings (art 15-16, Law 1819 of 2016). In the 2020 tax return, voluntary contributions to private pension funds and AFC housing savings are reported separately from other exempt income, as part of DIAN’s strategy to increase transparency. However, as these contributions can be reported in four different boxes (one for each type of income), there is a risk that taxpayers declare the same amount several times. However, DIAN’s analysis shows that this type of over-reporting is not very common and that more than 96% of taxpayers only record a contribution in one of the four cells. Furthermore, it is not clear whether taxpayers who report values in multiple boxes mistakenly included contributions multiple times or whether they attempted to split their actual contribution among several boxes. In the future, DIAN could estimate revenue forgone based on the sum of all four cells, while making sure it does not exceed the maximum 3 800 UVT and noting in the report that revenue forgone may be somewhat overestimated. In the future, DIAN is encouraged to revise the tax return and only include one (instead of four) cell in the tax return (see recommendation in Section 4.5) so that the contribution can be declared independently of the type of income the taxpayer earns. The same methodology and suggestion applies to the deduction of mortgage interest (art 89, Law 2010 of 2019) which is also reported in four cells (i.e. one cell per type of income).

It is currently only possible to estimate jointly revenue forgone from the exemption of both voluntary contributions to private pension funds and AFC housing savings. Despite of being incomplete, the available “exogenous information” from the supplementary tax form (1022) could be used to obtain an indication of the respective size of these TEs. The exogenous information suggests that between half and two thirds of the revenue forgone is due to voluntary pension contributions. However, it should be noted that the aggregate revenue forgone calculated from the supplementary data form does not match with the aggregate calculated from individual tax returns because fewer taxpayers need to submit the additional form.

Additional measurement tools to deal with low data availability in PIT returns

Unfortunately, the structure of the tax returns with several provisions being grouped into one box implies that the approach described above cannot be implemented for many items in the short term. In many cases, the information that is grouped within a single entry point within the tax return combines deductions (exempt or non-taxable income) that are considered TEs with deductions that are not viewed as a TE (e.g. mandatory contributions to RAIS, exempt income from CAN treaties). In some of these instances, the revenue foregone could be estimated indirectly, as is the case for the following PIT provisions:

Voluntary contributions to the individual savings schemes (Law 1819 of 2016) and inflationary component (art 27, Law 75 of 1986). Under the proposed benchmark, the non-taxation of mandatory contributions to pension schemes is not viewed as a TE. However, the PIT tax return includes non-taxable income cells in which taxpayers record both the mandatory social security contributions, which are not a TE, together with other non-taxable income that is considered a TE including voluntary pension contributions and the inflationary component. DIAN could simulate the amount of compulsory pension contributions that taxpayers were required to make and deduct this amount of the total amount that has been declared. The difference would then equal non-taxable income that is viewed as a TE. Once this amount is determined, the revenue foregone can be calculated using the formula that was presented above.

25% of labour income (art 104, Law 1607 of 2012). The 25% labour income deduction is considered a TE because it applies in addition to the zero-rate bracket. Even though the value of this exemption is not recorded separately in the tax return, it can be simulated based on other information on labour income that is declared in the tax return. DIAN may wish to include a separate cell for this tax provision in the tax return in order to estimate the corresponding TE in an accurate manner, in particular as the revenue forgone associated to it is high as Table 4.3 shows.4

Suggested methodology to integrate sources that cannot be merged with tax returns

DIAN could use aggregate data from other sources (beyond the information from tax returns) in order to increase the number of TEs for which the revenue foregone can be estimated even though aggregate information is expected to yield less accurate estimates. In some instances, data on the aggregate usage of a TE may be available from a data source that cannot be merged with the data from the tax returns. In this case, DIAN could possibly revert back to using an average marginal tax rate approach. This approach is used in the Chilean TE report for the exemption of returns from voluntary pension savings (SII, 2021[3]). However, rather than using the approach as described above, DIAN could refine its use by targeting it more closely to groups of taxpayers, depending on whether they use or not a particular TE. For example, DIAN could first estimate the average marginal tax rate that applies to taxpayers who make voluntary pension contributions to then, estimate the corresponding TE if no other data sources are available. Table 4.2 demonstrates that calculating the average based on a subpopulation that is more aligned with the target group of a TE can yield significantly different average marginal rate estimates.

Tax credits

Similar to the CIT, the revenue forgone from PIT tax credits is equal to the total amount claimed by the individual that either (i) reduces the final tax liability or (ii) is refunded. Not all tax credits are viewed as a TE – for example, the tax credit for taxes paid abroad by national taxpayers who receive income from foreign sources would be part of the proposed benchmark. DIAN is therefore advised to break down revenue forgone from tax credits on an item-by-item basis in addition to providing an estimate of total revenue forgone.

Revenue forgone estimates

This Section presents item-by-item revenue forgone estimates for 2020. The OECD calculated preliminary estimates based on a representative sample of PIT tax returns that was merged with exogenous information on mandatory contributions reported by employers. The coding was shared with DIAN so that the proposed methodology could be applied to the taxpayer population. This Review includes the results of these calculations made by DIAN based on the OECD’s suggestions and following the methodology described in the previous section.

Table 4.3 reports revenue forgone from PIT TEs for the limited number of items for which this analysis was feasible given the high degree of aggregation of the information that needs to be filed within the tax returns. It cannot be compared to the estimates included in the MFMP 2022 as Table 4.3 disregards boxes in which TEs and non-TEs are reported together unless a credible approach to disentangle the two components has been identified.

Reporting recommendations

This Section also provides recommendations on how to report revenue forgone from Personal Income Tax expenditures in the TE report:

Whenever possible, DIAN should report revenue forgone rather than the size of the tax exemptions, non-taxable income, deductions or tax credits that are claimed. Under the PIT with its progressive rate schedule and zero-rate bracket, revenue forgone cannot be easily inferred from the value of the TE.

The main revenue forgone table (Table 4.3) would present revenue forgone from all PIT TEs that can be measured; the table follows a similar structure as the CIT table.

For each type of TE, the table also contains a row that records the revenue forgone that cannot be measured on an item-by-item basis (“Other”). Currently, no estimate can be provided in these rows because the aggregate boxes in the tax return (for example, total exempt income) include both TE and non-TE components. As a large fraction of TEs cannot be measured on an item-by-item basis, the revenue forgone linked to the “other” category is likely large. If Colombia were to follow the recommendations made in 4.5, the design of future tax returns would ensure that the aggregated information does not mix TEs and tax provisions that are part of the TE benchmark.

In the TE report, values would be expressed both in thousand million pesos and as a percentage of GDP.

Over time, DIAN could add more information in the table by adding the revenue forgone in previous years. This will indicate how the revenue foregone has changed over time. If the calculations for two or more consecutive years are based on the same underlying data source (as is currently the case in the MFMP), this information should be highlighted and the change in revenue forgone between years that are based upon the same underlying data should not be discussed in the text.

The table could include the sum of all PIT TEs. This total should, however, be interpreted with caution given the limitations of summing different TEs. If the total is provided, the report should explicitly mention that some TEs are not included in the total because of a lack of data (see chapter 5 for further discussion).

The most recent edition of the MFMP includes revenue foregone from total exempt income across economic sectors and income schedules. Including tables with breakdowns by sector or types of taxpayers constitutes good practice insofar as it is possible to distinguish between tax provisions that are TEs and those that are included in the benchmark. A similar analysis could be included with respect to non-taxable income and special deductions in order to further increase transparency with respect to the types of taxpayers that benefit the most from PIT TEs.

Item-by-item discussion

In addition to the tables that provide an overview of revenue forgone from individual PIT TEs, and in line with the reporting recommendations for the CIT (see Chapter 3), the TE report could include item-specific tables for each TE measured on an item-by-item basis. These tables would include information about the reliability of the revenue forgone estimate. For example, the table would indicate if the estimate is based upon a simulated full take-up of the tax benefit, as it is done for the 25% labour income deduction. Table 4.4 provides an illustrative example.

More specifically, the item-by-item table could include the following elements:5

(i) TE identifier; (ii) Name of the TE; (iii) Revenue forgone in the current year and in the five preceding years; (iv) Tax type; (v) TE type; (vi) Year of implementation; (vii) Year of expiration; (viii) Legal reference; (ix) Reliability of the estimate; (x) Data source used to estimate revenue forgone; (xi) Estimation method; (xii) Paragraph that states why the provision deviates from the benchmark and provides more detail about the TE.

Appendix tables

Finally, a comprehensive list of TEs could be included in the annex of the TE report. This list could provide information about the legal reference of the tax provision and explain why the provision is considered a TE. This list would include all TEs, and not just those that are measured on an item-by-item basis. The list could be compiled by building upon the detailed list of PIT TEs included in Annex D of this report, and which is the result of several rounds of input and discussions with DIAN and the Ministry of Finance.

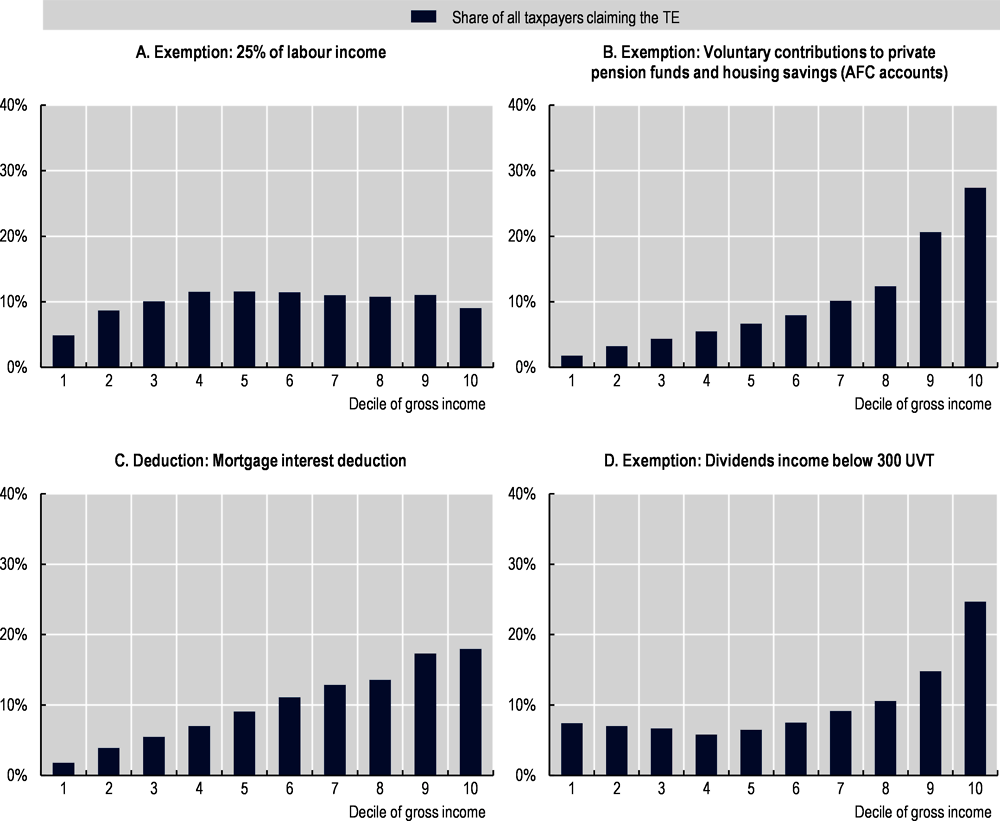

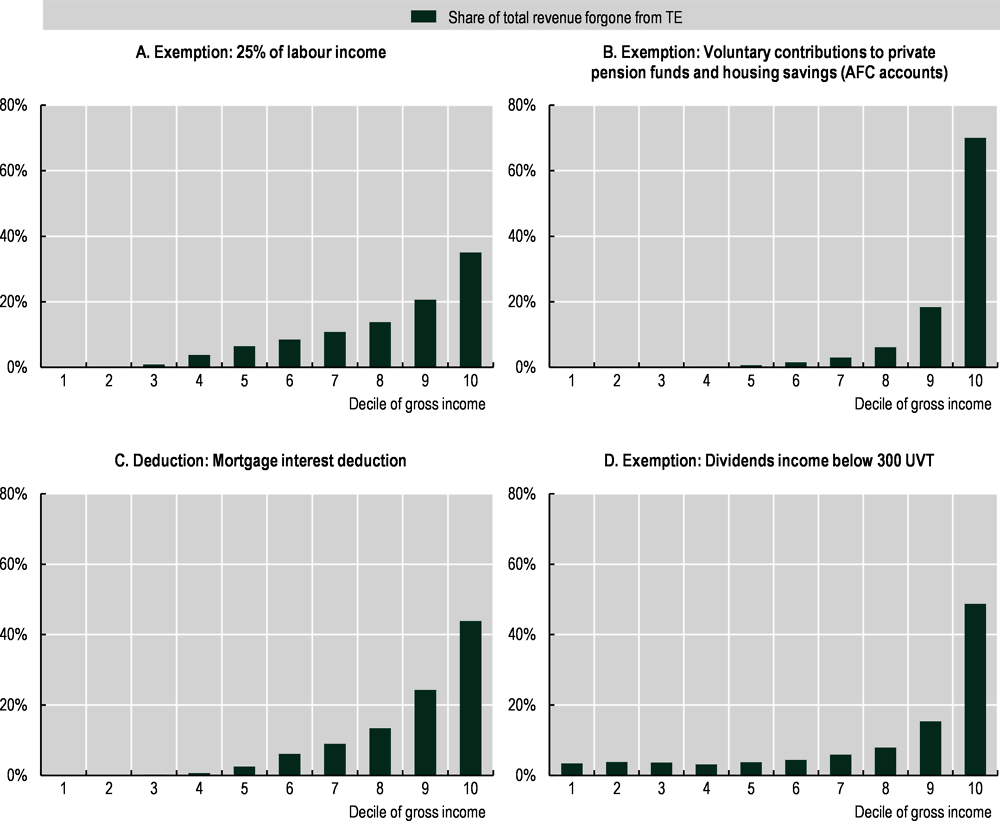

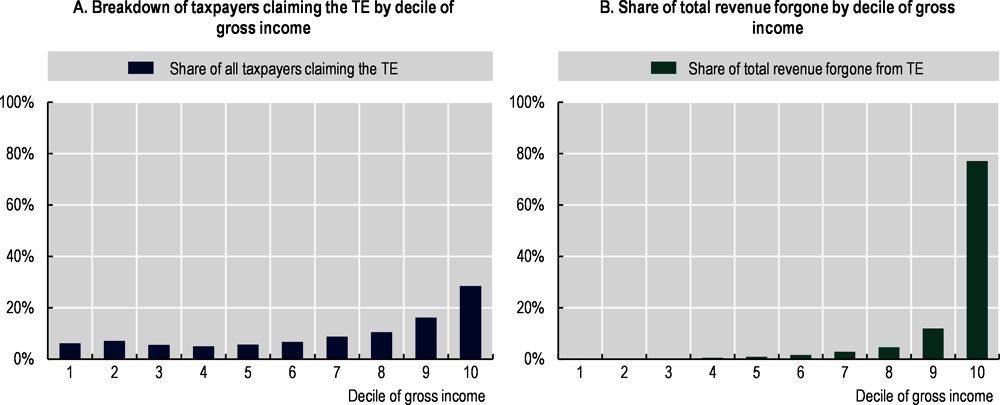

The tax return data allows DIAN to move beyond total revenue forgone estimates for each category and present a distributional analysis of PIT TEs. Figure 4.1 and Figure 4.2 provide an example for four TEs that can currently be measured on an item-by-item basis estimated by DIAN based on OECD recommendations. Figure 4.1 shows the breakdown of taxpayers who claim the TE across gross income deciles and Figure 4.2 plots the share of revenue forgone by gross income decile. Figure 4.3 replicates the analysis for voluntary contributions to the mandatory individual savings scheme (capital income) and the inflationary component (both items are non-taxable income TEs). Deciles are calculated among taxpayers who submit a tax return and the fraction of the population who does not submit any return is excluded.

Note: Based on personal income tax returns of the full taxpayer population in 2020. The OECD had access to a representative sample of 110 695 personal income tax returns and calculated preliminary estimates. The OECD provided DIAN with an initial coding proposal but was not involved in the final calculations. Gross income is defined as the sum of gross income from: labour income, income from professional services, capital income, non-labour income, pension income, dividend income and occasional gains.

Source: DIAN.

Note: Based on personal income tax returns of the full taxpayer population in 2020. The OECD had access to a representative sample of 110 695 personal income tax returns and calculated preliminary estimates. The OECD provided DIAN with an initial coding proposal but was not involved in the final calculations. Gross income is defined as the sum of gross income from: labour income, income from professional services, capital income, non-labour income, pension income, dividend income and occasional gains.

Source: DIAN.

A distributional analysis of TEs would allow DIAN to examine to which extent tax provisions are progressive, proportional or regressive across the income distribution. For example, the Tax Incentives Commission noted that the 25% labour income exemption is expected to be highly regressive as the amount of the exempt income is increasing with earnings, and the value of the TE is increasing in the taxpayer’s marginal PIT rate (OECD, DIAN and Minhacienda, 2021[1]). This observation is confirmed in Figure 4.2.The fact that there are fewer taxpayers in the first three deciles of the gross income distribution who report labour income is consistent with a finding of the Tax Incentives Commission (OECD, DIAN and Minhacienda, 2021[1]). The distributional analysis calls for a more in-depth analysis that would allow making concrete tax policy recommendations. This could include an analysis of the overall statutory and effective tax burden across the income distribution and an evaluation of the possible behavioural responses to particular tax policy reforms.

Note: Based on personal income tax returns of the full taxpayer population in 2020. The OECD had access to a representative sample of 110 695 personal income tax returns and calculated preliminary estimates. The OECD provided DIAN with an initial coding proposal but was not involved in the final calculations. Voluntary contributions to mandatory pension funds and the inflationary component are determined by simulating mandatory contributions to pension funds or by subtracting mandatory contributions based on information provided by third parties. In the case of capital income, the methodology may overestimate the mandatory contributions effectively made and thereby lead to an underestimation of revenue forgone from voluntary contributions to mandatory pension schemes and the inflationary component. Gross income is defined as the sum of gross income from: labour income, income from professional services, capital income, non-labour income, pension income, dividend income and occasional gains.

Source: DIAN.

In order to improve the measurement of PIT TEs, DIAN needs to collect more granular data. As Table 4.6 shows, less than 10% of the PIT TEs can be quantified based on the information that taxpayers are required to provide within the income tax return in 2020. This is a result of both the design of the cells within the PIT return and the low share (less than 2%) of taxpayers that are required to submit exogenous information. In order to increase the number of TEs that can be measured on an item-by-item basis, DIAN could undertake the following steps (in decreasing order of priority):

1. Redesign the PIT return. A first priority would be to redesign the income tax return that individuals need to file, possibly including the following:

Cells in the income tax return should not combine tax provisions that are TEs and provisions that are considered part of the PIT benchmark. Table 4.6 shows all the boxes that according to the proposed benchmark, include both income from TEs and non- TEs in the 2020 tax return. Once the PIT benchmark is defined, the tax return should distinguish between cells where TEs are filed and cells that ask for information that are part of the benchmark. This would allow DIAN to calculate total revenue forgone from aggregate PIT TE categories (e.g. exempt income, non-taxable income, special deductions and tax credits that are viewed as TEs).

The tax return should include one single cell for exempt voluntary contributions and one cell for the deduction of mortgage interest. Recently, cells for these items were included in the tax return but they were added for each type of income from the general schedule (labour, professional services, capital and non-labour), which might lead taxpayers to declare these deductions multiple times within the same tax return. More generally, the number of cells in the tax return could be increased, ideally by including a separate Section where taxpayers earning income subject to the general schedule would declare their deductions with respect to the four categories. This would minimize the number of additional boxes and would avoid confusion and multiple reporting of the same item. More detailed tax returns would also enhance DIAN’s monitoring and tax auditing possibilities.

2. Increase the number of taxpayers that are required to submit exogenous information. If adding cells to the PIT return would not be feasible in the short run, DIAN could increase the number of taxpayers that provide exogenous information by reducing the gross income thresholds that define who needs to file the exogenous information forms.

3. Use additional data that allows for breaking down information in cells in the tax return that record both TEs and non TEs, or multiple TEs. For some TEs, DIAN can already split the information reported within a particular cell in the tax return in its TE and non-TE component. This is for instance the case for mandatory pension contributions that can be distinguished from the voluntary contributions to the mandatory individual savings scheme (Law 1819 of 2016) and the inflationary component. Until it redesigns the tax return, DIAN should evaluate whether it can proxy for more items the share of TEs in the total amount that is declared within a particular cell in the tax return (Table 4.5), as this would allow DIAN to quantify additional TEs on an item-by-item basis. The same strategy could be applied if several TEs remain grouped together in one cell after redesigning the tax return.

4. Explore additional sources of information. DIAN should make use of additional information reported by third parties. This can include aggregated information (e.g. returns from voluntary contributions to private insurance), which would allow DIAN to refine the average marginal tax rate approach that it applies to estimate revenue forgone. DIAN can also make use of microdata that can be merged with the tax return data (e.g. the information that employers report on the compulsory contributions they make to pension funds on behalf of their employees or the data collected by the Ministry of Labour on the usage of the 120% first-job for employees who are under twenty-eight years of age).

Data from individual tax returns can be used by DIAN beyond estimating revenue forgone, by examining taxpayers’ behaviour. This type of analysis does not necessarily have to be included in the TE report but it could provide useful additional insights that would enrich the tax policy debate. It could also shed a light on the extent to which taxpayers use TEs strategically in order to reach certain income thresholds in the tax schedule.

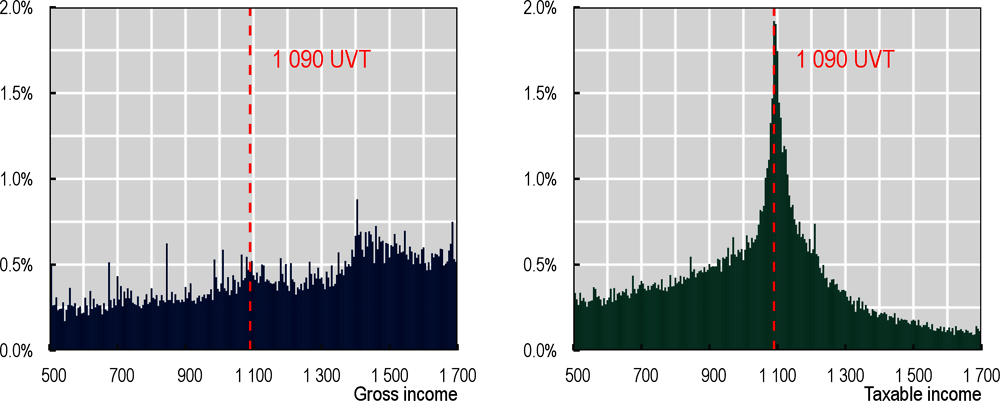

The graphs that are included below provide an example of the type of analysis that could be conducted by zooming in on the PIT exempt bracket threshold (Figure 4.4). The aim of the analysis is to assess the extent of bunching behaviour and potential tax planning around the threshold. Figure 4.4 shows that while the distribution of gross income is not particularly concentrated around the exempt bracket threshold, taxable income is significantly concentrated around this threshold both below the threshold but also slightly above it. Bunching analysis could also be carried out for the 40% deduction ceiling or 5 040 UVT, for instance.6

Note: Illustrative example based on a sample of 110 695 income tax records (2020) provided by DIAN. 1 UVT = COP 35 607 (2020). Gross income and taxable income in this case refers to all income taxed under the general PIT general schedule (i.e. labour income, income from professional services, capital income, non-labour income and pension income).

Source: DIAN and own calculations.

The SIMPLE is a presumptive tax regime that is targeted at unincorporated businesses with gross income below 80 000 UVT per year (about USD 729 000). The SIMPLE is levied on business turnover at rates ranging between 1.8% and 14.5%, varying with turnover and the sector the business operates in. The SIMPLE replaces the income tax and the Municipal Business Turnover tax (ICA), in accordance with the rates determined by the municipal and district councils. Furthermore, taxpayers declare VAT and consumption tax (levied on sales of restaurants and bars) within the tax return of SIMPLE. Employer pension contributions can be credited against the tax liability under SIMPLE. While business costs are not deductible from the turnover-based tax base, income items that are considered “non-taxable” are deductible from the presumptive tax base.

The proposed benchmark considers the SIMPLE regime as a TE even though it is a presumptive regime that aims at strengthening tax compliance by means of tax simplification. However, as the regime is not only targeted at small businesses but reaches also medium-sized businesses, and preferential tax regimes targeted at SMEs are typically viewed as a TE, the same approach is followed regarding SIMPLE.

The estimation of revenue foregone for businesses that pay SIMPLE rather than the income tax is currently not possible as businesses only declare turnover and not their costs, which implies that DIAN cannot determine taxable income. Nevertheless, DIAN could report components of SIMPLE that are viewed as a TE such as the tax credit on mandatory employer pension contributions (art 903 of the Tax Code). The deduction of non-taxable income is also a TE insofar it corresponds to provisions that are not part of the benchmark, such as voluntary contributions to pension funds; once more disaggregated data is available, this provision could also be reported separately as a TE. However, it would be important to signal in the TE report that these individual TEs do not cover the overall TE that corresponds to SIMPLE regime as a whole. Finally, SIMPLE should ideally be included in a separate Section and not be included in either the CIT or PIT sections of the TE report.

References

[4] Australian Government the Treasury (2021), Tax Benchmarks and Variations Statement 2020.

[2] Minhacienda (2022), Marco Fiscal de Mediano Plazo 2022.

[1] OECD, DIAN and Minhacienda (2021), Tax Expenditures Report by the Tax Experts Commission.

[3] SII (2021), Chile: Informe de Gasto Tributario 2019 a 2021.

Notes

← 1. In line with the proposed benchmark, DIAN has already excluded the tax credit granted for tax payments in foreign jurisdiction from the total tax credit estimate that it provides in the latest MFMP (Minhacienda, 2022[2]).

← 2. However, the fact that exempt income is now reported separately from deductions in the 2020 tax return is viewed as an improvement.

← 3. The same formula applies to non-standard deductions or special deductions and non-taxable income.

← 4. Note that the current report estimated the revenue forgone from this TE both for labour income and for income from professional services if the taxpayer choses to deduct 25%. Taxpayers that provide professional services with a maximum of two employees can choose to either deduct 25% of income or effective costs.

← 5. The structure and content of these tables are modelled upon the reporting practices in the Australian TE report (Australian Government the Treasury, 2021[4]).

← 6. Whether the 40% of net income ceiling on exempt income and deductions (up to a maximum of 5 040 UVT) is binding or not for a particular taxpayer can currently only be determined for taxpayers who file their tax return online and create a username. Under this modality, the system includes additional questions that allow DIAN to calculate the amount of income that is not subject to the ceiling and, as a result, automatically calculate the amount of deductions that are subject to the ceiling. However, taxpayers who do not create a username are requested to complete the boxes for “limited exempt income and deductions” (Rentas Exentas y deducciones limitadas) by themselves and the information is not derived indirectly based on a formula. These boxes combine both the limited exempt income and deductions as well as the exempt income that is not subject to the ceiling. In future tax returns, DIAN may want to ensure that these two items are split and filed separately. Ideally, taxpayers should always have to provide detailed information on income that is not subject to the ceiling.