1. Environmental, social and governance (ESG) investing

ESG investing is attracting growing attention from investors and policy makers over its promise of utilising a range of non-financial information to better align finance with long-term value and societal values. ESG practices, however, remain at an early stage of development, with challenges around consistency, comparability, and financial materiality. This chapter assesses current market developments, as well as the financial ecosystem and the key stakeholders shaping ESG practices related to disclosure, consistency of metrics, comparability of rating methodologies, and alignment with financial materiality. It scrutinises the performance of ESG approaches by exploring different ESG investment strategies of portfolios and investment funds, and their returns relative to traditional market benchmarks. The chapter concludes with a set of global recommendations to improve market confidence and integrity, so that sustainable finance can more effectively support resilient and inclusive economic growth.

In the past decade, forms of sustainable finance have grown substantially due to an increasing demand by institutional and retail investors to better reflect sustainability issues in their investment choices. In particular, the use of environmental, social and governance (ESG) investment approaches has been driven by increased investor demand to make better use of non-financial information to guide asset allocation decisions to improve long-term value, while also better aligning portfolios with societal values. In this respect, growing concerns over the impact of climate change and the consequences of pandemics have drawn greater attention to environmental and social risks, combined with policy signals that the financial sector should be a driving force in advancing global sustainability.

In recent years, investors and financial intermediaries have been increasingly factoring ESG assessments into investment decisions. As of 2018, the number of signatories of the UN Principles of Responsible Investment (UN PRI) – an instrument that calls for the integration of ESG factors - had grown to over 2,300, managing over USD 80 trillion in assets.1 Surveys of professional investors suggest that they consider ESG-related information increasingly important to determine whether a company is adequately managing risk and aligning its strategy to achieve long-term returns. However, even within the investments made by actors integrating ESG factors, insufficient distinction has been made between ESG assessments and related approaches such as socially responsible investing, suggesting that even a basic characterisation and measurement of the ESG market is a challenge.

Despite the mainstreaming of forms of sustainable finance, the terminology and practices vary considerably. One reason is that while ESG investing stems from investment philosophies such as Socially Responsible Investing (SRI), it has since evolved into a distinct form of investing. While earlier approaches used exclusionary screening and value judgments to improve their investment decisions, ESG Investing now looks to find long-term value in companies, beyond supporting a set of values.2

ESG disclosures and ratings represent an increasingly important tool for integrating sustainability considerations into the investment process, in several ways. First, ESG practices help financial investors who seek to evaluate the financial materiality of non-financial reporting about conditions, practices and strategies related to environmental, social and governance issues over the medium term. For example, they could relate to risk management practices to reduce the impact of climate change on corporate performance, or renewables strategies for new growth opportunities. Second, ESG ratings and metrics are also being used by social investors to monitor and assess the impact from their investments, such as to reduce carbon emissions or to better adhere to human rights standards. Moreover, certain investors may use these metrics to incorporate a blend of both factors, depending on the investment strategy and objectives. For each of these purposes, ESG criteria provide a useful framework for investors to assess how these prominent non-financial factors in the short-term could affect firm performance and impact its external environment over the long term. Thus, in concept, the ESG disclosures, metrics, and rates should serve to support investors to make more informed decisions and value judgments.

Despite substantial efforts to improve ESG disclosure in recent years, concerns arise over the current lack of standardised reporting practices and transparency at the international level. In particular, the absence of a universally accepted global set of principles and guidelines for consistent and meaningful reporting, creates a barrier to the effective comparability and integration of sustainable factors into the investment decision process.

In addition, consistency and comparability of ESG ratings could be hindered by the vast amounts of ESG related data that are disclosed using divergent core metrics and methodologies. This could be further compounded given the relatively early stage of development of ESG practices and the differences in methodologies adopted by ESG rating providers, including the incorporation and transformation of determined aspects, such as materiality. At the current stage, outputs across providers show a low degree of correlation as to what constitutes a high or low-scoring ESG rating, due to differences in subcategories, number of metrics, weighting and scope.

While market research of loosely defined sustainable metrics seem to show superior returns, a more in depth analysis suggests that financial performance based on ESG ratings is mixed and there is little evidence of consistent over-performance in recent years. Challenges in assessing ESG performance arise, in part due to the wide variance in ESG practices, such as negative and positive screening, proprietary ESG scoring, and rebalancing portfolios toward entities with higher ESG scores. Also, ESG practices are combined with other investment strategies that may include thematic focus, or an investment style, such that it is difficult to determine the extent to which particular ESG approaches are gaining success in generating long-term value.

Importantly, these identified challenges do not negate the benefits, in principle, of considering ESG criteria in the investment process. The additional information provided by ESG criteria offers further valuable insights on how companies are managed and operated to support long-term investing. Nonetheless, current approaches to ESG assessments and ratings appear highly inconsistent and incomparable, and risk undermining their potential value. While ESG ratings are constructive in concept and potentially useful in driving the disclosure of valuable information, a number of current challenges need to be addressed before investors can trust the integrity of such instruments in financial markets.

This means that, notwithstanding the potential for ESG investing to unlock value and align with societal values, the extent to which current ESG practices sufficiently unlock material information to deliver on value and values remains uncertain. What is clear, however, is that strengthening ESG practices at a global level would be needed to help ensure that disclosure and rating are transparent, consistent and comparable, which would improve outcomes both financial and social investors.

In light of these growing questions surrounding ESG investing, this chapter explores a number of key issues that are shaping ESG practices; the materiality of ESG disclosures; the current usefulness of ESG ratings; and, performance of ESG indices and funds. In addition, challenges that relate to transparency, consistency, materiality, and the ability of financial consumers to understand both the loose taxonomy and how it relates to portfolio composition, returns and risks are also reviewed. This is particularly relevant where investors have an expectation that they can use ESG factors to improve financial returns while aligning with societal values related to ESG practices.

The first section provides an overview of the size and composition of the ESG market, in terms of issuers and assets under management, while offering working definitions of ESG investing within the investment spectrum. In addition, it maps the ESG financial ecosystem, in terms of various market participants and other stakeholders involved in providing ESG information, ratings, indices, and investment products. Findings suggest that many organisations are now involved in coordinating the reporting of more consistent forward-looking information into issuer disclosures, setting principles and standards aligned with societal values, or establishing good practices on ESG reporting and analysis.

The second section reviews the challenges associated with ESG rating outputs and methodologies. The section observes that there remains fundamental distinctions between different approaches, including the wide range of categorisation and weighing of publicly available information, in part compounded by the subjective judgments of rating providers. While some key criteria are the same across providers, important aspects of the methodologies can differ, undermining the usefulness of the results.

The third section offers an assessment of ESG scoring, as well as benchmark and fund performance based on several prominent industry databases. The assessment builds on several strands of portfolio theory, including Markowitz modern portfolio theory, Fama-French factor models and an analysis of ESG funds. The aim of the assessment is to understand how the integration of ESG factors in the investment process affects performance and volatility when compared to traditional investments.

The fourth section introduces the main policy implications of the chapter, highlighting that greater transparency and consistency of core metrics and methodologies in the rating process is needed to improve the reliability of ESG ratings and investment approaches.

1.2.1. Dimensions of ESG investing

The sustainable market size has grown considerably in the past decade and was estimated to exceed USD 30 trillion in total assets in the five major markets3 at end-2019, an increase of more than 30% compared to 2016. Globally, almost USD 1 trillion of assets were held in sustainable funds at end-2019. Of these, around 75% were held by institutional investors and the remaining 25% by retail investors. The majority of sustainable investments are allocated in public equities (51%) and fixed income (36%) assets, with the remaining share divided among real estate, private equities and other types of assets (Global Sustainable Investment Alliance, 2018[1]). In this regard, it is important to understand the difficulties related to the differentiation between ESG investing and impact investing. ESG investing generally applies ESG ratings to the investment process (even though some of the strategies, such as exclusionary screening, may rely on product or norms-based information), while impact investing is focused on solving social or environmental issues through targeted investments. For the latter and according to the Global Impact Investing Network, the estimated current size of the global impact investing market is USD 715 billion.

With respect to sustainable investments, the European Union leads in total assets committed, with the total estimated amount higher than USD 14 trillion (Global Sustainable Investment Alliance, 2018[1]). The United States follows with more than USD 12 trillion of assets under management (AUM). The majority of this is held by asset managers and investment institutions. The data for the United States also suggests that USD 2.6 trillion (around 20% of total AUM) is managed through mutual funds, exchange traded funds and closed-end funds. Japan is the third largest centre for sustainable investing, showing strong growth potential, despite a more modest AUM of around USD 2 trillion.

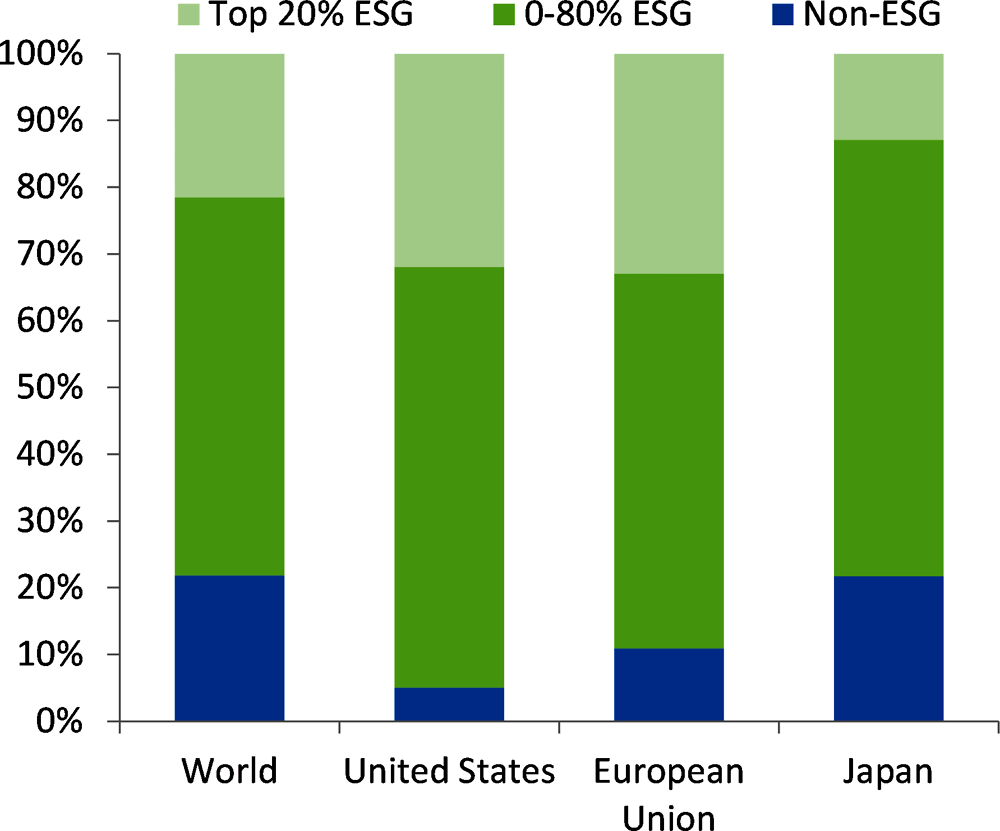

Note: Calculated as the number of public companies with an ESG score over the total number of public companies, in each year for the different areas.

Source: Refinitiv, OECD calculations

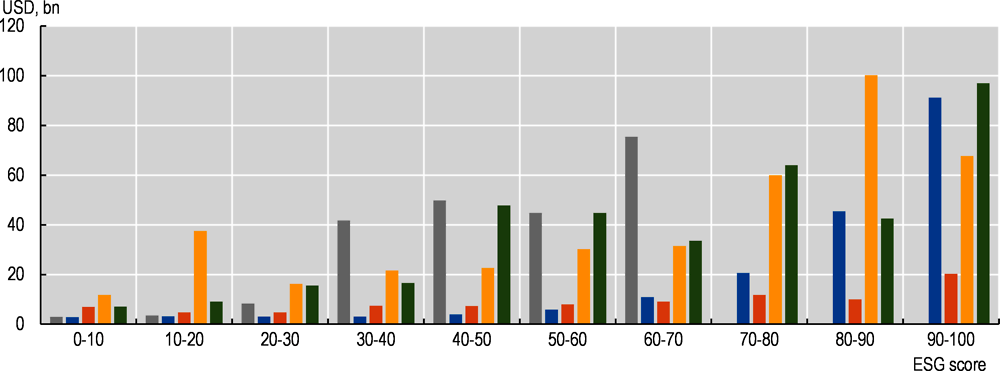

OECD analysis using Refinitiv ESG data yields similar findings when focused exclusively on ESG ratings. Findings illustrate disparate ESG market coverage across economic regions when analysing the following markets: World, United States, European Union, and Japan. Notably, market coverage is low in markets outside the United States, despite significantly increasing in recent years (see Figure 1.1). In the United States, market coverage has reached an all-time-high of almost 25% of public companies while in Europe and worldwide it remains just over 10%. Japan lags behind with just over 5%.

When analysing market capitalisation, however, a different pattern emerges: The market capitalisation of total ESG scoring companies (companies for which Refinitiv has calculated an ESG score based on the information reported by the company) represents 78% of the total global market capitalisation, representing around 95% in the US, 89% in the EU, and 78% in Japan (see Figure 1.2).

Source: Refinitiv, OECD calculations

Of total assets under management in sustainable funds, the majority are currently held by institutional investors, even though retail investors are increasing at a higher rate. Evidently, investor interest in ESG products is growing, yet concerns remain that, if ESG products are not clearly labelled with transparent methodologies, this could contribute to misaligned expectations when compared to actual outcomes.

ESG investing can fall within a broader spectrum of investing based on financial and social impact. At one end of the spectrum, pure social investing, such as philanthropy for example, seeks only social return. At the other end, pure financial investment pursues the objective of maximising financial returns based on a given investment strategy, risk parameters or constraints. Additionally, impact investing4 seeks a social return, in addition to financial returns – but the balance of social and financial returns depends greatly on the chosen investment objective and strategy. As such, the delineation between what constitutes these different approaches and their anticipated impact on long-term value is not obvious.

In contrast, ESG investing incorporates different meanings depending on the motivation of the investor that uses it. When used by impact investors who want to better align capital allocation with environmental and social causes, what matters the most is how the sustainable practices of the company are reflected in the ESG rating. Yet, investors who have pledged ESG integration broadly see it as a necessity for long-term value creation, which will reward long-term investments, such as those that reduce exposure to reputational risks. Anecdotal evidence from surveys of institutional and retail investors suggest that investors are increasingly seeking both enhanced financial returns over time, and the societal alignment of their investments, to maximise financial and social returns. While such alignment may be possible in concept as environmental and social factors become more material,5 in practice the returns of ESG have yet to show such evidence.

In this regard, ESG investment approaches may include some or all of five distinct forms. On one side, the least amount of complexity is through excluding certain firms categorically (e.g. based on moral or risk-related considerations), and on the other side is full ESG integration such that it becomes an integrate part of the investment processes, governance and decisions.

To this end, three broad investment approaches can be identified. The first form is “exclusion” or “avoidance” which signifies the exclusion of corporates and governments whose behaviours do not align with societal values. This is the largest sustainable investment strategy globally, with almost USD 20 trillion of AUM. Causes for exclusion commonly include:

manufacturing controversial weapons;

violation of global compact principles;6

countries systematically violating compact principles; and,

companies with more than a certain percentage of revenues from coal extraction, tobacco production or similarly activities with a negative impact on society.

This category can also include “norms-based” or “inclusionary screening” which pursues the inclusion or higher representation of issuers that are compliant with international norms, such as those by the OECD and UN.7 This can include “best in class” investing whereby firms achieving above a pre-defined ESG score thresholds are included. This form of investment approach is applied to roughly USD 5 trillion in assets.

The second form, which in many cases is a step following exclusion, is the realignment of the remaining assets by ESG scores, with greater tilting toward higher ESG and away from lower ESG scores. Funds can chose to align with an ESG type of index for passive investing, or engage in active investment through a selected approach relative to an index. One derivation of this approach is a reweighting by which index providers or investors rebalance initial ESG ratings of “best in class” companies in each sector to ensure that there are high ESG scores per industry.

The third form is the pursuit of a thematic ESG focus within at least one of the ESG areas. These types of funds may or may not exclude or rebalance, in line with the approaches set out above. The thematic focus could include low-carbon funds, or good governance funds, which explicitly search for better-rated issuers in these areas in at least one of the environmental, social or governance areas, using particular expertise to assess the submetrics that drive the pillar score (see Chapter 2). The amount managed under thematic focuses is around USD 1 trillion.

Funds can also employ an impact focus, which in this case would suggest investing in lower ESG companies that show some propensity to transition to higher ESG, and/or where the fund engages in some form of shareholder activism through share voting or bilateral communications to change company behaviour and practices. This approach can be generalised across ESG, or can be thematic in focus, where fund managers may have expertise in one area of ESG, such as green finance or good governance.

Lastly, ESG integration, which refers to systematic and explicit inclusion of ESG risks and opportunities in investment analysis. Unlike the best-in-class method, ESG integration does not necessarily require peer group benchmarking or overweighting (underweighting) the leaders (laggards). Similarly, ESG integration does not require any ex ante criteria for inclusion or exclusion. The integration of ESG risks and opportunities into investment analysis is relevant for most, if not all, investors. Signs of ESG integration often include dedicated governance to oversee ESG integration; substantial resources given to the assessment of ESG considerations; explicit exclusion policies to avoid certain companies with very low scores and engagement policies to improve impact for those with relatively low scores but opportunities for improvement; and quantitative research and tools to assess performance. It is the second largest strategy, with more than USD 17 trillion of assets under management.

Within these rebalancing and thematic approaches, ESG can be used to pursue certain strategies that can be superimposed on the ESG investing approach. These strategies can include momentum, shorting, alpha investing, factor investing, carbon transition strategies, exploiting ESG rating inefficiencies in emerging markets, and alignment with Sustainable Development Goals (SDGs). Certain strategies seek to overweight high-ESG issuers, and others seek to overweight low-scoring ESG issuers with the intention that they will improve over time, either due to market pressures or direct investor engagement with company management. While these represent only some of the strategies adopted, their use illustrates that the resulting portfolio composition of an ESG fund can vary widely, and the wide range of approaches may mean that there can be little difference between the ESG portfolio choice to traditional funds.

1.2.2. The financial ecosystem

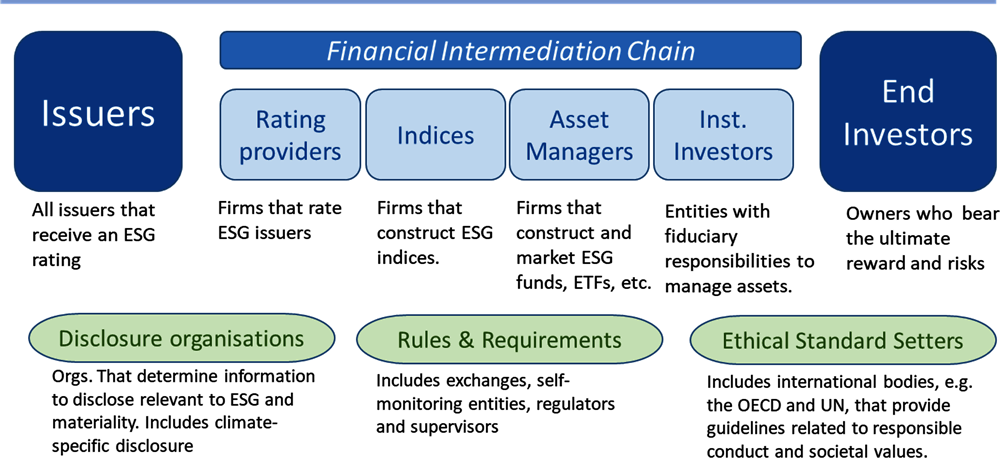

In light of the various assessment and portfolio construction practices, it is important to understand the financial intermediation chain that converts sustainable finance concepts into ESG practices, identifying subsequent implications for the end investor. This ecosystem is illustrated in the diagram below, and includes issuers and investors who disclose and use information related to environmental, social and governance issues. Many players are now involved in the ESG ecosystem, which is becoming increasingly complex, as the methodologies are different with a continual growth in the number and type of investment products. This in turn, puts pressure on regulators and framework providers to be more and more involved, trying to determine how data should be reported and used as well as how best to provide greater transparency for retail investors and asset managers.

Financial Issuers. In short, financial issuers are any issuers that supply equity or debt to the financial market, through either public or private channels. ESG information is also being provided by sovereign bond issuers, as well as by SME equity issuers, and other types of issuers. In concept, all issuers belong in some part of the ESG ecosystem, as ESG assessment is being demanded by a growing number of investors, who are seeking to analyse information that comes from issuers directly, and other sources including financial and social media.

ESG ratings and index providers. ESG ratings and index providers include firms that (i) provide assessments of equity and debt issuers based on their disclosures that explicitly or implicitly offer metrics and information that help determine ESG scores, and (ii) index providers that convert ratings into market indices by reweighting market portfolios in accordance with some or all of the approaches described above. Some of these ratings are highly quantitative, by using and weighing numerous subcategory metrics based on identified quantitative data, either offered by corporate issuers or pulled from other sources such as financial media.8 A number of rating providers are also index providers. The use of such indices is growing rapidly as a means to benchmark relative performance. These providers offer a range of stylised benchmarks that in turn allow for fund products to be developed for passive or active investment, and also for portfolio managers to utilise as a benchmark to compare their ability to generate risk-adjusted returns. By virtue of their growing use as benchmarks for ESG investing, the way in which indices are created, including exclusion, extent of tilting toward higher ESG scores, and other forms such as thematic indices (e.g. high “S” issuers), is highly influential in guiding overall ESG portfolio management.

ESG users: asset managers, institutional investors, and public authorities including central banks. The users of ESG ratings and information include, at the very least, types of investors across private and public entities. Asset managers that create investment products such as investment funds and ETFs use ESG ratings to either inform portfolio composition decisions, or to contribute to the portfolio managers’ own ESG ratings. Institutional investors (e.g. insurance and pension plans) may incorporate ESG ratings for portfolio management, and to align with their fiduciary duty to incorporate forward-looking material information in their investment process (see Chapter 4).9 Public sector institutions, including central banks and public debt issuers, have begun to consider the importance and need for ESG integration. A key reason is that central bank reserve managers increasingly seek long-term financial sustainability of their portfolios, and are striving to assess climate transition risks and the market impact of investors’ shift toward lower carbon-intense industries.

ESG framing, guidance and oversight. ESG framing, guidance and oversight includes an array of actors that help define forward-looking, non-financial reporting to help ensure long-term sustainability as well as alignment with societal values. Many are disclosure bodies that assess and determine appropriate issuer information at national and international levels, including exchanges, self-regulating bodies, and related industry associations. In addition, a host of other bodies set rules and requirements, or influence them. These include oversight authorities such as markets regulators and bank and pensions supervisors. Lastly, standard setters for responsible conduct include international organisations that set standards and guidelines regarding responsible investing and sustainability goals. Given the number of regional and global organisations that seek to coordinate the reporting of forward-looking information in issuer disclosures, the integration of consistent and material reporting of ESG information remains work in progress.10

Different framework providers attempt to map and measure key criteria to help issuers provide consistent, meaningful ESG ratings to investors. A host of organisations have contributed to this wave of increased ESG transparency, ranging from the Sustainability Accounting Standards Board (SASB) and Global Reporting Initiative (GRI) to the Task Force on Climate-related Financial Disclosures (TCFD), including stock exchanges such as NASDAQ and the World Exchange Council. In addition, regulators from around the world are getting more involved in the supervision and understanding of how ESG metrics are created and measured, in order to create a clear framework for investors.

Regulators are taking action to provide more clarity around sustainable finance ESG practices

Specific bodies such as the FASB, TCFD and GRI have already taken steps on sustainable finance and ESG, in order to develop common standards on how basic data are gathered, how metrics should be created and the way in which materiality should be incorporated.

In light of the rapid growth of assets under management by asset managers utilising forms of ESG practices, national financial regulators have begun to assess a range of practices associated with forms of sustainable finance, with an increasing focus on ESG taxonomies, approaches, and marketing to investors.

This follows actions by the EU, as part of its commitment to achieve the United Nation's 2030 Agenda and Sustainable Development Goals and to comply with various international agreements, such as the Paris Climate Agreement, to move ahead on ESG disclosures and benchmarks trough the EU Action Plan on Sustainable Finance, with the aim of providing a regulatory framework to support and promote sustainable investment in the EU. The European Commission’s Technical Expert Group on Sustainable Finance has published its final Taxonomy report for screening environmentally sustainable activities. The taxonomy is expected to facilitate a pan-European ecolabel for financial products The Commission will conduct a consultation of the first draft of the screening criteria for the taxonomy shortly. Moreover, mid-2020, three European supervisory bodies – ESMA, EIOPA and EBA - issued a Consultation Paper seeking input on proposed environmental, social and governance (ESG) disclosure standards for financial market participants, advisers and products. These standards were developed under the EU Regulation on sustainability-related disclosures in the financial services sector (SFDR), with the aim of strengthening protection for end-investors; improving the disclosures to investors from a broad range of financial market participants and financial advisers; and improving the disclosures to investors regarding financial products.

The US SEC has launched an initiative to scrutinise ESG investing strategies of regulated investment products. The review will consider the potential risks associated with inconsistent ESG disclosure, including with respect to investor protection and breach of fiduciary duties. One objective is to provide investors with the “material, comparable, consistent information they need to make investment and voting decisions” by developing a framework to disclose material in order to reduce reliance on third-party ESG data providers or disclosures. [”Recommendation from the Investor-as-Owner Subcommittee of the SEC Investor Advisory Committee Relating to ESG Disclosure, 14 May 2020, https://corpgov.law.harvard.edu/2020/05/28/recommendation-from-the-investor-as-owner-subcommittee-of-the-sec-investor-advisory-committee-relating-to-esg-disclosure/]

In Japan, the Financial Services Agency revised its code of conduct for institutional investors in March 2020 to encourage institutional investors to focus on ESG when making investments. The revisions call on institutional investors to engage in dialogue with investee companies and clearly state how they will incorporate ESG into their investment strategies. [ “Finalization of Japan’s Stewardship Code”, FSA, 24 March 2020, www.fsa.go.jp/en/refer/councils/stewardship/20200324.html]

On this matter, a number of additional jurisdictions are taking steps to address perceived concerns about the clarity of ESG among asset managers, retail investors and other market participants, to help strengthen market resilience and integrity.

The sustainable finance transition is currently under way and as such ESG ratings are an evolving instrument being shaped by industry and expectations. In this regard, the analysis of ESG ratings and related outputs underlines the difficulties faced by investors and how fundamentally different these ratings can be depending on the provider. This is mainly due to methodological differences in structuring the ratings and also on how materiality is incorporated. This section explores potential possibilities to overcome bias and increase transparency to improve the usefulness of and trust in ESG ratings.

1.3.1. ESG rating outputs

Scoring approaches begin with the consideration and identification of relevant criteria within each of the E, S, and G factors. Environmental factors can include natural resource use, carbon emissions, energy efficiency, pollution and sustainability initiatives. Social factors can include workforce related issues (health, diversity, training), and broader societal issues such as human rights, data privacy, and community engagement. Governance factors can include corporate governance and corporate behaviour, ranging from shareholders’ rights to executive compensations.

Different providers use different metrics and submetrics, aggregated and translated in different ways to create the overall ESG scores. Every provider ranks different aspects of the sustainability of the companies it assesses. These metrics and aspects are then aggregated to create a key pillar score, which usually defines one of the elements supporting the pillars (E, S and G).

Both MSCI and Sustainalytics state that their services are designed to help investors identify and understand financially material ESG risks and opportunities, in order to integrate these factors into their portfolio construction and management process. Thomson Reuters and Bloomberg provide an ESG reporting score, which focuses on how and what type of information is reported by companies.

Even though the users of ESG information largely retrieve information directly from issuer disclosures, with third party analysis and scores largely developed using the same base of information, ESG scores can still vary widely from one ESG provider to another.11 ESG scoring can be criticised because the adoption of different methodologies by rating providers can lead to wide variance in results. This implies that if investors are using and relying on different service providers, the inputs of the scores that shape securities selection and weighting could be driven by the choice of rating provider.

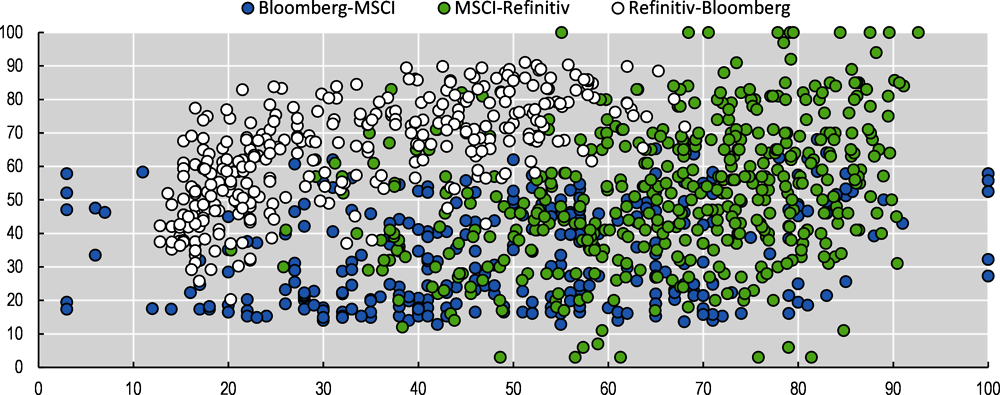

The metrics used by companies and data providers are affected by the lack of consistency and varying levels of transparency between stakeholders in the ESG ecosystem. Among the major market data providers such as Bloomberg, Thomson Reuters, FTSE, MSCI and Sustainalytics, the methodologies vary significantly. While variation in analytical practices and judgment can bring additional insights to investors, the correlation is low between the scores they assign to the same companies (see Figure 1.4).

OECD analysis assesses different rating providers, namely Bloomberg, MSCI and Refinitiv in order to understand how their ratings vary when analysing specific indices, such as the S&P500. The results illustrate wide differences in the ESG ratings assigned, with an average correlation of 0.4.

This highlights how some companies ranked top by one provider get much lower scores from others. This depends on what is measured, and how the measurement is affected by company disclosure.12 Research by (Berg, Kölbel and Rigobon, 2019[2]) investigates the differences in ESG ratings of five providers. It decomposes the differences in ratings into three sources and finds that different scores among providers are mostly driven by the scope and the measurement of categories, explaining more than 50% of results, while the weight assigned has a limited impact. This assessment substantiates concerns over the meaning of current ESG scores and their value to investors.

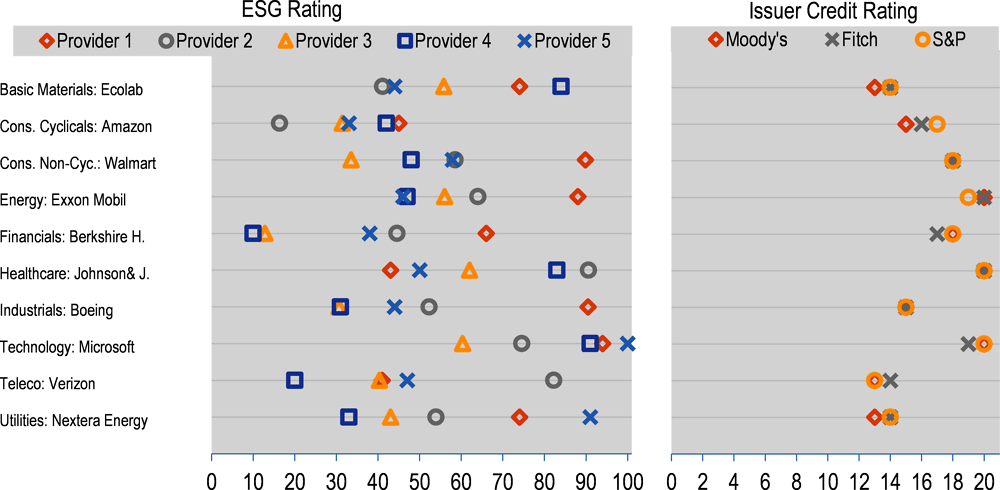

OECD analysis then compared ESG ratings with the issuer credit rating by major providers and found that credit scores for selected issuers vary much less, in part because they are based on a clear set of financial metrics that drive ratings results, while qualitative judgments tend to influence decisions that most affect notches (see Figure 1.5). These differences raise important questions on the reliance of ESG ratings to make investment decisions, including for structuring investment portfolios that are considered to have a tilt toward higher ESG scores. In short, if high ESG scores are simply a judgment that varies significantly across firms, the extent to which investors can be assured that this approach either provides enhanced returns or aligns with particular societal values merits further scrutiny by policy makers and the investment community.

Note: Providers’ names in the legend correspond to the Y axis when at the left and to the X axis when at the right.

Source: Bloomberg, MSCI, Refinitiv, OECD Staff calculations

Note: Sample of public companies selected by largest market capitalisation to represent different industries in the United States. The issuer credit ratings are transformed using a projection to the scale from 0 to 20, where 0 represents the lowest rating (C/D) and 20 the highest rating (Aaa/AAA).

Source: Refinitiv, Bloomberg, MSCI, Yahoo finance, Moody’s, Fitch, S&P; OECD calculations.

1.3.2. Methodological challenges

ESG rating methodologies are still evolving following demand from investors and regulators. Therefore, the methodologies of different providers have been analysed to understand how the underlying data is transformed. As discussed earlier, ESG scoring methodologies include both quantitative and qualitative elements, which include different weight factors for each industry and a highly subjective judgment of each company based on disclosures and a host of other public information used to arrive at scoring results.

Nonetheless, concerns arise over methodology and metrics issues in ESG ratings. In particular, industry participants have noted that a lack of consistent corporate disclosure regimes at the international level hinders information available to investors. There is a poor understanding of ESG rating agency approaches, in part due to the opacity of detailed rating methodologies and specific metrics, highlighting difficulties in assessing the rating results and the wide differences across key providers. Many organisations report difficulties in obtaining specific guidance on the ESG information reviewed by each ESG rating agency and how they analyse data and qualitative information. Disparate rating outputs by different agencies can create confusion in the market, both for investors and issuers. Moreover, the mixed ratings results and mixed evidence on financial performance raise the need for more thorough assessment of how financial materiality and values alignment are captured. In particular, the assessment of each industry to determine the relative importance of each factor and sub-factor depending on the external environment and business model is extremely important to have a clear view of what ESG ratings reflect.

The mixed results regarding the final ESG score of different providers raise the need for more thorough assessment of how financial materiality is captured in ESG data and ratings. Currently, the various ESG reporting and ratings approaches generally do not sufficiently clarify either financial materiality or non-financial materiality (e.g. social impact), so investors are not currently able to get a clear picture of whether the measurements suggest a net positive or negative effect on financial performance. An example of a financial material framework for ESG reporting is the materiality map developed by SASB, which emphasises the importance of materiality and embeds its importance at the industry level. SASB notes that it prioritises and maps issues that are reasonably likely to directly impact the financial condition or operating performance of a company and therefore are most important to investors. Financial materiality may be influenced by societal values related to environment, governance and social issues and these factors can change over time, creating the need to constantly improve and adapt materiality.

Note: Comparison of five different providers of ESG scores (shown in different colours) in terms of average market capitalisation.

Source: Bloomberg, MSCI, Refinitiv, OECD calculations

Methodological concerns also arise when looking at the final ESG product. External research and OECD analysis indicates an implicit ESG scoring bias in favour of large-cap companies and against SMEs. This is reflected in the OECD analysis of ESG ratings compared to market capitalisation and may be due to the fact that SMEs do not have the resources to invest in non-financial disclosure, as the costs may outweigh the investment gains in the near term. However, this bias, and the hurdle of unlocking useful ESG information from smaller companies, creates a market inefficiency that affects both the relative cost of capital and corporate reputation.

There is some evidence that this bias also exists with respect to ESG scores among Emerging Market issuers. As there is lower ESG disclosure practice in parts of EMEs, some companies with sound practices with respect to environmental, social and governance issues could be penalised because they do not yet disclose their assessment of ESG risks and opportunities in a manner consistent with emerging good practices.

1.3.3. Transparency of ESG products alignment with investors’ sustainable finance objectives related to financial and social returns

Where expectation gaps exist between investor objectives, between impact and regular financial investing, such gaps need to be addressed to ensure market integrity and trust in financial markets. OECD analysis shows that methodological issues, differences between providers, and biases raise concerns with respect to investors’ expectations. Recalling the investment spectrum between social and financial investing, investors should be able to ascertain sufficient information from investment funds or institutional investors as to how, and the extent to which, they would be expected to sacrifice financial returns for social returns. Put differently, if a fund excludes certain companies due to values (e.g. tobacco), or rebalances portfolios due to the incorporation of socially relevant information then there are potential impacts to absolute and risk adjusted returns relative to a similar traditional index (same constituents, but without an ESG scoring tilt). At least, such historical attribution analysis is entirely feasible, but communicating such variations in returns and risk does not appear to be the norm.

On a related matter, the trends in using ESG scoring illustrate that a substantial portion of those who pursue ESG investing are doing so, at least partly, for ethical reasons and may have expectations of what their investments will and will not support. Yet, much of ESG scoping and fund offerings illustrate that rebalancing based on ”best in class” shifts investments within industries. In this manner, some investors may not realise that their ESG funds are even more heavily weighted toward very large carbon-intensive oil companies or BigTechs that face data privacy scrutiny, or behave in a manner that is not aligned with societal values.

More transparency is therefore needed to ensure that funds disclose the full spectrum of performance criteria in terms of past returns and risks, and the extent to which this is due to portfolio decisions that could compromise absolute or risk-adjusted returns relative to a suitable traditional index, based at least on past performance.

Given the current market size dimensions of ESG investing and the methodological challenges faced by investors, an analysis of the financial performance of portfolios integrating ESG strategies is conducted, in order to provide a broader view of what ESG really means. Different methodologies have been applied, ranging from classical portfolios theory to funds analysis, to different rating providers.

The review of academic and industry literature reveals a wide range of approaches and results, which are largely inconsistent with one another. The research highlights the difficulty of identifying the real impact of ESG on investment performance. While some show a positive impact, improving the overall performance of investments, others do not show any meaningful effect. The inconclusiveness of research may be caused by problems with different providers, methodologies, investment strategies, geographical selection, sample selection and timeframes.

A considerable amount of research has been conducted over the past decade on socially responsible and sustainable investing, including the impact of corporate social responsibility and good governance on market-based and financial statement measures of financial performance. These studies analyse Corporate Social Responsibility comprehensively but do not directly relate to ESG ratings and their impact on shareholders returns.

The financial industry has in recent years turned its attention to the extent to which ESG investing can achieve superior returns, or at least avoid inferior returns, relative to traditional investing that does not incorporate sustainability considerations beyond immediate financial performance and corporate strategy to further enhance future performance. It has pursued several forms of analysis: (i) academic studies of performance using ESG or other related sustainability metrics; (ii) financial industry studies using established ESG ratings; (iii) megastudies that assess various forms of prior studies of corporate social responsibility and good governance, and impact on performance.

This chapter seeks to answer some important questions that have arisen from the review of practices. They include:

Composition and bias. To what extent have ESG scores penetrated firm coverage by count and market capitalisation? Are there biases in ESG scores that favour or penalise certain types of firms? This question has been already been addressed to some extent in the previous section, focusing on the methodology and the biases underlying the ratings.

Portfolio performance. How do ESG portfolios and funds perform; do they show clear signs of superior performance over the past decade? To answer this question different classical financial analysis methodologies have been used to enable a broad view on the subject.

Concentration. Does tilting of portfolios lead to higher concentration and volatility for a given return? Classical financial theory indicates that an increase in returns depends on the level of risk that investors are willing to take. Therefore, analysis is conducted to assess the extent to which the volatility of ESG portfolios and indices change with respect to traditional indices.

OECD analysis of ESG scores and performance using different providers aims to answer these questions. The analytical approach focuses on portfolio optimisation and efficient frontier portfolios, using Markowitz’s portfolio theory and the Fama and French factor model, which are widely used in financial analysis. Markowitz’s methodology is used to create the best portfolio based on different assumptions and based on expected risk and return. The Fama and French model instead aims to understand the return of a portfolio after taking into account the variables underlying the risks of the market and of the portfolio itself. Tail risks and maximum drawdowns are analysed in order to have a comprehensive view on the subject.

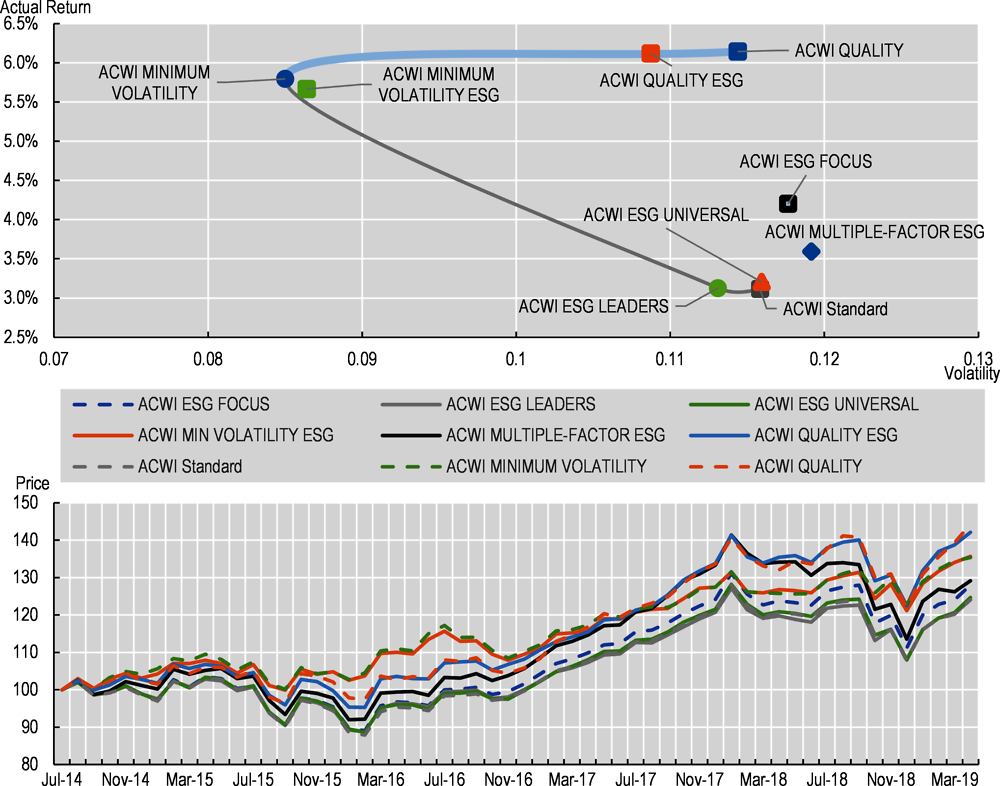

In testing for the Markowitz efficient frontier, it can be observed that, depending on the ESG index analysed, risk adjusted performances vary. In particular, risk analysis shows a varying volatility, but a lower maximum drawdown for ESG indices.

The findings are based on the analysis of ESG indices and ratings, which do not necessarily represent firms with current strong environmental and social performance, given the integration of multiple forward looking factors. The findings are meant to provide clarity over the performance of ESG ratings and not a broader sustainable framework. To compute the Markowitz efficient frontier, both ESG indices and non-ESG indices are included from a selection of indices from MSCI, to assess whether ESG criteria influences risk-adjusted performance. A framework in which every index is treated as if it was a single asset has been adopted, to understand the difference in risk adjusted returns and drawdown risk.

The drawdown risk is widely used as an indicator of tail risk over a specified time period, which helps to understand downside risk in the event of extreme conditions. It is calculated by comparing the value of a cumulative return with a previous peak that is the maximum cumulative return, in a pre-specified period of time. One example of extreme drawdown refers to the S&P500, which dropped by 48% in 2008 during the financial crisis.

Within this context, a total of nine MSCI indices are analysed, in which 6 are ESG indices, to assess returns and risk-adjusted returns (see Figure 1.7). These indices are considered using the same approach, even though they are built using different methodologies and with different objectives in mind in terms of sustainability and risk management.

The Minimum Variance Portfolio is computed and the efficient frontier of risky assets selected. The results show that different ESG indices have varying risk and performances depending on how they are built. For example, the ACWI minimum volatility performs slightly better than its ESG counterpart, even though the latter has a lower drawdown risk (-7.83% against -8.56%), with that being true for most ESG indices. For instance, the ACWI Quality ESG reduces the volatility of the benchmark while maintaining the same return. This could show that investors are willing to renounce a part of returns in order to achieve higher security, namely through a lower drawdown risk. When looking at the other indices, they are treated as inefficient according to the efficient frontier. This might be due to the different nature of the indices analysed and the fact that they are treated as single assets when in reality they are not.

Source: MSCI, OECD calculations

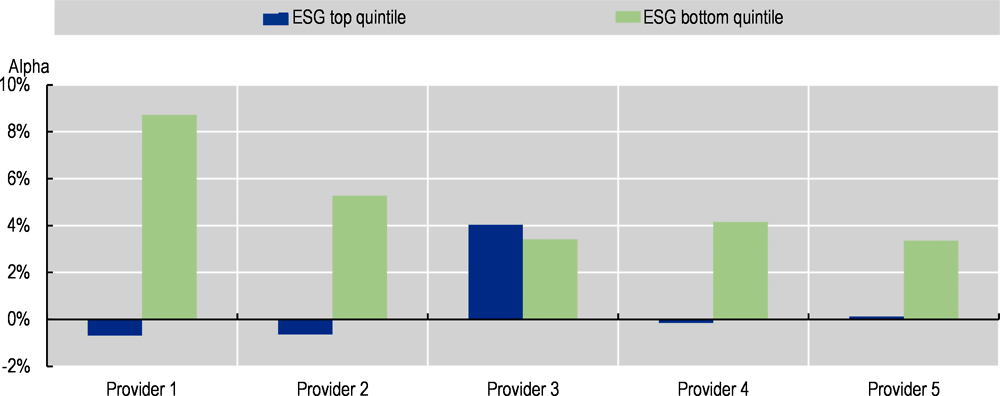

Using Fama and French portfolio analysis, it can be observed that the excess return generated depends on the provider chosen to build the portfolio, even though low scoring portfolios generally perform better than the market.

Using this hypothesis, OECD analysis examines how ESG scores perform in comparison to the market, and in particular to assess whether high ESG scoring stocks outperform low ESG scoring stocks using the Fama and French 5 factor model. A similar pattern for each provider is observed, except for one, which shows positive alpha on the best scoring ESG portfolio.

The results of the analysis are adjusted for different risk factors, excluding systemic risks, which cannot be captured by the Fama and French 5 factors model methodology.

The model aims to price assets taking into account risk factors such as systematic market risk,13 size of companies and book-to-market ratio. The risk-adjusted alpha extracted from the model measures the excess return of an investment relative to the return of a benchmark index. In this case the benchmark index is provided by Fama and French and is a proxy for the market.14 This result was obtained by running a regression between a portfolio of securities and the 5 factors provided by Fama and French.

Source: Bloomberg, Fama and French, MSCI, Refinitiv, OECD calculations

Moreover, the assessment of ESG funds considers how they perform when compared to traditional funds based on several prominent industry databases. The assessment builds on several strands.

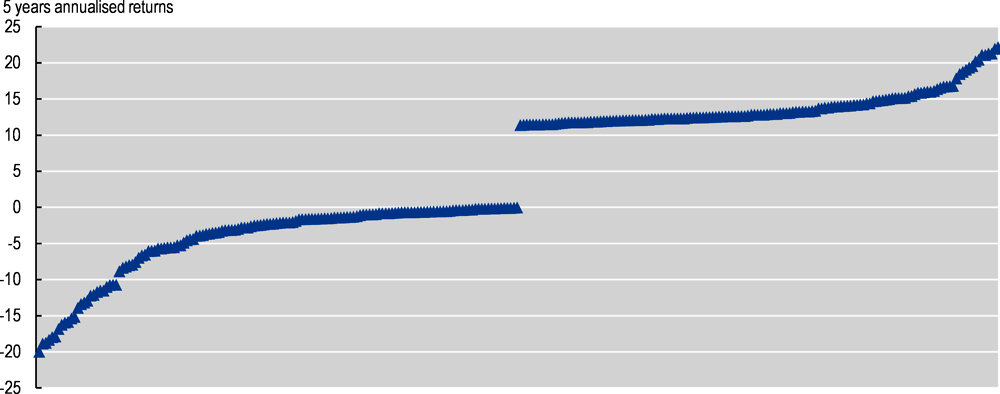

Distinct from indices and portfolios, the analysis assesses the extent to which actual investment funds holding high-ESG issuers outperformed funds which benefit from investment management strategies and decisions on ESG investments.15 To do this, a sample of funds from Morningstar is analysed to understand how ESG ratings affect fund performance.

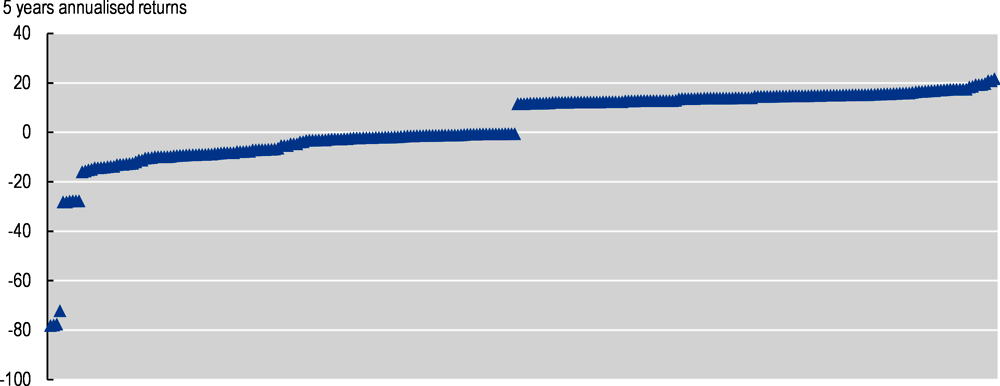

The results of the analysis, focusing on the best and worst rated funds, provide a framework which shows that the distribution of the returns has similar ranges for both categories, except for some outliers in the lower rated funds. In particular, while the distribution of the funds look similar, when focusing on the low scoring funds there is a higher likelihood that these funds will suffer from downside risk, with some funds performing well below -20%. This reflects the findings of Markowitz’s Minimum Variance portfolio, showing that ESG assets imply a lower systemic risk, for example during unexpected events. This was evident during the COVID-19 pandemic, where some ESG indices appeared to provide a better choice than standard indices, with lower underperformance (see Box 1.2).

Note: Analysis of the 150 best and worst funds with a 5 star sustainability rating by Morningstar. The returns are 5 years annualised.

Source: Morningstar, OECD calculations

Note: Analysis of the 150 best and worst funds with 1 and 2 stars sustainability rating by Morningstar. The returns are 5 years annualised.

Source: Morningstar, OECD calculations

Following the spread of the COVID-19 pandemic in Q1 2020 which put downward pressure on financial markets, sustainable finance market participants observed that ESG funds and indices outperformed traditional investments. This box provides a brief analysis of the main ESG indices to help understand the magnitude of this outperformance and whether ESG considerations can actually improve portfolios’ resilience against tail risks. Different market actors such as Bloomberg, Morningstar and MSCI showed a relative outperformance of ESG funds and indices over standard ones, with these instruments losing less value than traditional indices during the downturn. The findings are consistent with OECD analysis showing a lower drawdown risk for some ESG indices.

To understand the extent of this outperform (illustrated by lower underperformance), different indices from MSCI have been analysed to see how they compare. Figure 1.11 represents the MSCI ACWI Standard Index with value 100. This is done in order to compare MSCI ESG indices with the MSCI standard index.

The results show that almost all MSCI ESG indices had lower underperformance than the ACWI standard index during this period. The only standard index that performed better than its ESG counterpart is the MSCI Minimum Volatility Index, which performed better than the ESG counterpart until end-April as it served as a hedge against the high uncertainty regarding the extent of the economic consequences of the pandemic.

Given the rapidity with which markets change and the unpredictability of how measures to address COVID-19 will evolve, further analysis will be needed to assess the genuine differences between the returns and volatility of ESG and non-ESG indices and funds, and the factors that contribute to these differences.

Note: This figure compares selected MSCI ESG indices with the MSCI standard index

Source: MSCI, OECD calculations

The results of the analysis show a wide range of financial performance of ESG investments between indices, portfolios, and investment funds. OECD analysis generally finds little outperformance, and some underperformance of ESG-tilted indices and portfolios relative to traditional (ESG neutral) market portfolios. Where there is some evidence of superior absolute return performance, this is often accompanied by higher levels of risk, such as volatility, that dampens risk-adjusted returns, but also with a lower tail risk, namely a lower maximum drawdown. While OECD analysis is based on commercially available ESG ratings from major providers, there are a plethora of ESG portfolios and proprietary ratings that could exhibit superior risk-adjusted returns, just as a portion of active managers are able to achieve such returns against traditional market indices.

These results, however, do not call into question the fundamental purpose and potential benefits of ESG investing. In principle, and supported by some evidence, ESG investing can improve returns where knowledge of policies and certain strategies, such as momentum investing, can capture benefits of companies that are improving practices with respect to environmental, social and governance policies. In turn, new forms of disclosure to help investors and other stakeholders make decisions about financial and social returns can empower them to have a longer-term view of sustainable investing through the cycle, rather than from one reporting period to another.

More work is needed to understand the drivers of the individual Environmental, Social and Governance pillars. In this regard, the second chapter of the BFO analyses more closely the E pillar, to understand the link between environmental practices and scoring. The social pillar remains to be further analysed to acknowledge which social aspects are rating agencies taking into account, having received less attention than environmental and governance factors.

There are clearly benefits of reporting additional information that can be useful to investors willing to act upon some drawbacks in the ratings, allowing them to incorporate new data on sustainability to understand if a company is implementing more sustainable investments. As ESG investing matures, it has the potential to effectively capture forward-looking information about environmental, social, and governance issues that enhance investors’ decision-making about long-term risks and sustainability of financial performance. However, more work is needed to ensure that the ESG disclosure, rating, investment, and investment communications processes are consistent, transparent, and effective, in the following areas:

Overcoming the disclosure bias to improve fairness of issuer ESG assessments. External and OECD research indicates that there is an ESG scoring bias in favour of large-cap companies at the expense of SMEs. This phenomenon may unfairly penalise SME issuers with higher cost of capital, and could also distort the performance results of ESG vs traditional portfolios, by underrepresenting the growth dynamics of many smaller firms. As this may be due to the fact that the current costs of appropriate ESG disclosure may be perceived to be excessive by at least a portion of smaller issuers, more clarity and international standardisation of disclosures could help reduce reporting costs and incentivise adequate ESG disclosure.

Ensuring relevance and clarity in reporting frameworks for ESG disclosure. Notwithstanding progress to date, the reporting of ESG factors still suffers from considerable shortcomings with respect to consistency, comparability and quality that undermine its usefulness to investors. There is still more to be done to ensure that issuers can rely on core criteria and metrics for E, S and G disclosures that are relevant to a wide body of equity and debt investors, and are supported by stock exchanges and disclosure organisations. A universally accepted global set of principles and guidelines for consistent and meaningful reporting across ESG will help build scalable expertise for issuers, and improve consistency, comparability and reliability for investors and analysts. Moreover, it will then help all users assess the meaningfulness of such disclosures over time so that they can be further refined.

Improve transparency and standardisation of core elements of ESG ratings methodologies to ensure that metrics and methodologies of ratings outcomes are widely available to investors. Widely different outputs across major ESG rating providers – in contrast to that of credit ratings -- can create confusion in the market among institutional investors, fund managers, and retail investors as to what constitutes a high ESG-rated company. If left unaddressed, this persistent opacity could undermine investor confidence in the ESG scores, major ESG indices, and portfolios built upon these products. There is need for clarity on how E, S and G subcategory factors and metrics, their weighting, and subjective assessment contribute to final ESG scores. This would allow users and issuers to understand and compare methodologies and results. Such transparency is particularly warranted if the scores among ratings providers continue to differ widely. Also, where ESG ratings are combined with other traditional financial approaches, from credit ratings to investment strategies, the impact or output of the ESG element of the approach should be communicated distinct from the traditional approaches. Otherwise, investors will not be able to judge the effect and value of the ESG approach on portfolio construction and financial results.

Strengthening the link between ESG ratings and financial materiality over the medium to long-term. There is mixed evidence thus far about the prospect of ESG investing meeting or exceeding the performance of traditional investment indices, which suggests the benefits of ESG disclosures to unlock forward-looking information that is financially material is still at an early stage of development. As such, it raises the need for more thorough assessment of how financial materiality is and should be captured in ESG ratings, benchmarks and portfolios. The industry and policy makers need to address two issues: first, to better define financial materiality over the medium- to long-term, to overcome short-termism that might otherwise underrepresent slower moving environmental and social risks. Second, to isolate the effects of financial materiality from alignment with social investing, which may strive for societal impact even if not aligned with financial materiality. As both are relevant to sets of market participants, more research and communication is needed in this area to make ESG investment meaningful for long-term value and values investing.

Ensure the appropriate labelling and disclosure of ESG products to assure their exposures, risks, and other traits are sufficiently material, comparable, and consistent to allow investors to make investment and voting decisions in line with their investing objectives and risk tolerance. While this chapter focuses on materiality and financial value derived from ESG investing, it also acknowledges that the motivation for end-investors – from retail investors to central banks -- is also to align their investment portfolios with societal values related to environment, social and governance issues. Therefore, the clarity with which ESG products across ratings, benchmarks, and funds explicitly delineates the financial and social investing aspects of ESG investing is of high importance. In particular, where product features are meant to align with social investing rather than financial returns, such choices should be made abundantly clear to investors. Likewise, when funds portray a positive alignment with environmental concerns, exposures to carbon-intense industries and the rationale for this exposure should be made explicitly clear. In sum, there is a greater need for consistent taxonomy of sustainable finance investing that is meaningful and reliable across global markets.

Strengthening the regulatory environment is an important step to support consistency and resilience in major markets and within jurisdictions, but more is needed to strengthen good practices across global markets. An underlying theme throughout the report is that greater engagement between the financial industry and the public sector is needed to strengthen practices as they relate to investor protection and market integrity related to disclosures, data, ratings, indices, and investment vehicles. Certainly, regulators of large jurisdictions with developed financial markets are already engaging on these very topics, and making good progress. However, capital markets and sustainable finance are global in reach, as are the societal issues they seek to assess. Therefore, global principles may be needed to help establish good practices that acknowledge regional and national differences, while ensuring a constructive level of consistency, transparency, and trust. In sum, to unlock the potential benefits of ESG investing for long-term sustainable finance, greater attention and efforts are needed to improve transparency, international consistency, alignment with materiality, and clarity in fund strategies as they relate to sustainable finance. Doing so will help strengthen transparency, confidence, and integrity of sustainable finance through global financial markets, so as to contribute to resilient and inclusive economic growth.

References

[16] Bannier, C., Y. Bofinger and B. Rock (2019), Doing safe by doing good : ESG investing and corporate social responsibility in the U.S. and Europe, https://ssrn.com/abstract=3387073.

[2] Berg, F., J. Kölbel and R. Rigobon (2019), “Aggregate Confusion: The Divergence of ESG Ratings”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.3438533.

[9] BNP (2018), Investing for tomorrow: applying ESG principles to emerging market debt..

[13] Cerulli and UN PRI (2019), Survey: Responsible Investment in Hedge Funds -The Growing Importance of Impact and Legacy..

[5] Climate Disclosure Standards Board (2012), Climate Change Reporting Framework Advancing and aligning disclosure of climate change- related information in mainstream reports..

[3] Dolvin, S., J. Fulkerson and A. Krukover (2017), “Do ’Good Guys’ Finish Last? The Relationship between Morningstar Sustainability Ratings and Mutual Fund Performance”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.3019403.

[7] European Commission (2018), Feedback Statement: Feedback Statement Public Consultation on Institutional Investors’ and Asset Managers’ Duties regarding Sustainability..

[17] Fama, E. and K. French (2013), “A Four-Factor Model for the Size, Value, and Profitability Patterns in Stock Returns”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.2287202.

[1] Global Sustainable Investment Alliance (2018), Global Sustainable Investment Review, Global Sustainable Investment Alliance.

[14] GRI (2018), The Materiality Principle: The Deep Dive..

[6] J.P. Morgan (2016), ESG, Environmental, Social and Governance Investing..

[18] Markowitz, H. (1952), “PORTFOLIO SELECTION*”, The Journal of Finance, Vol. 7/1, pp. 77-91, https://doi.org/10.1111/j.1540-6261.1952.tb01525.x.

[20] OECD (2019), Social Impact Investment 2019: The Impact Imperative for Sustainable Development..

[19] OECD (2017), Investment governance and the integration of environmental, social and governance factors., https://www.oecd.org/.../Investment-Governance-Integration-ESG-Factors. pdf.

[10] Task Force on Climate-related Financial Disclosures (2017), Final Report: Recommendations by the Task Force on Climate-related Financial Disclosures..

[11] Taskforce on Climate-related Financial Disclosures (2017), Recommendations of the TCFD.

[4] UN PRI and ICGN (2018), A Discussion Paper By Global Investor Organisations On Corporate ESG Reporting..

[15] UN Principles for Responsible Investment, (2019), What is Responsible Investment.

[12] World Economic Forum (2019), Seeking Return on ESG.

[8] World Economic Forum, I. (2019), Seeking Return on ESG: Advancing the Reporting Ecosystem to Unlock Impact for Business and Society..

Notes

← 1. While the overall AUM of the signatories is USD 80 trillion, the portion of assets overseen is materially lower than this amount, as explained in the following paragraphs.

← 2. CFA Institute: https://www.cfainstitute.org/en/research/esg-investing

← 3. Australia and New Zealand, Canada, Europe, Japan and the United States.

← 4. The (OECD, 2019[20]) explores more in detail Social Impact Investments, providing guidance and recommendations to stakeholders.

← 5. Should society’s demand for socially-aligned consumption progress, consumers would in theory align with companies that adhere to high ESG standards, providing such companies higher revenues from consumption and brand loyalty, which can translate over time into higher capital returns.

← 6. United Nations Global Compact: “The Global Compact asks companies to embrace, support and enact, within their sphere of influence, a set of core values in the areas of human rights, labour and environmental standards, and the fight against corruption.

← 7. (J.P. Morgan, 2016[6]), “ESG, Environmental, Social and Governance Investing.”; makes a particular distinction between exclusion and norms-based investing.

← 8. Large ESG providers include MSCI, Sustainalytics, Bloomberg, Thomson Reuters, and RobecoSAM. In addition, traditional ratings agencies such as Moody’s and S&P now also provide forms of ESG ratings. Index providers include, for example, MSCI, FTSE Russell, Bloomberg, Thomson Reuters, and Vigeo Eiris.

← 9. The OECD has conducted work on ESG investing and fiduciary duties, particularly with respect to pension plans, and includes guidance by the International Organisation of Pensions Supervisors (IOPS). See IOPS (2019), “Supervisory guidelines on the integration of ESG factors in the investment and risk management of pension funds.” Fiduciary duty is discussed in other parts of this publication.

← 10. Given the difficulty in reporting metrics related to sustainability, different stakeholders have called for more standardised reporting guidelines. Eighty exchanges have published their own ESG reporting guidelines and many more are willing to do so. NASDAQ, for example, issued a report to help companies to report on ESG criteria using 30 metrics, 10 for each pillar.

← 11. See https://morphicasset.com/esg-ratings-no-quick-fixes/, referring to Investment bank CLSA and Japan’s Government Pension Investment Fund (GPIF).

← 12. See https://www.wsj.com/articles/is-tesla-or-exxon-more-sustainable-it-depends-whom-you-ask-1537199931.

← 13. Systemic risk describes an event that can spark a major collapse in a specific industry or the broader economy. Systematic risk is the overall, day-to-day, ongoing risk that can be caused by a combination of factors, including interest rates, geopolitical issues, and corporate health, among others.

← 14. Fama and French provide five different factors, including the market factor. This factor represents a proxy of the market. When adding the others factors, the result is a risk-weighted performance measure.

← 15. Previous research by (Dolvin, Fulkerson and Krukover, 2017[3]) focused on the efficiency of sustainable funds and how they perform using Morningstar sustainable metrics. The analysis found no difference in risk adjusted returns of ESG against non ESG funds returns. However, it did find a relevant difference in risk profile, with high sustainability scores largely confined to large cap funds.