Chapter 2. Circular business models

This chapter focusses on circular business models, their key characteristics, and the main drivers for adoption. It begins by presenting a typology of the five headline circular business models that are discussed in this report: circular supply, resource recovery, product life extension, sharing, and product service system models. The key characteristics of each of these are then discussed, with a particular focus on the underlying business case. The chapter concludes with an overview of the higher level factors that could drive the adoption of circular business models in the longer term. Technological change and a range of emerging business risks are identified as being of particular importance.

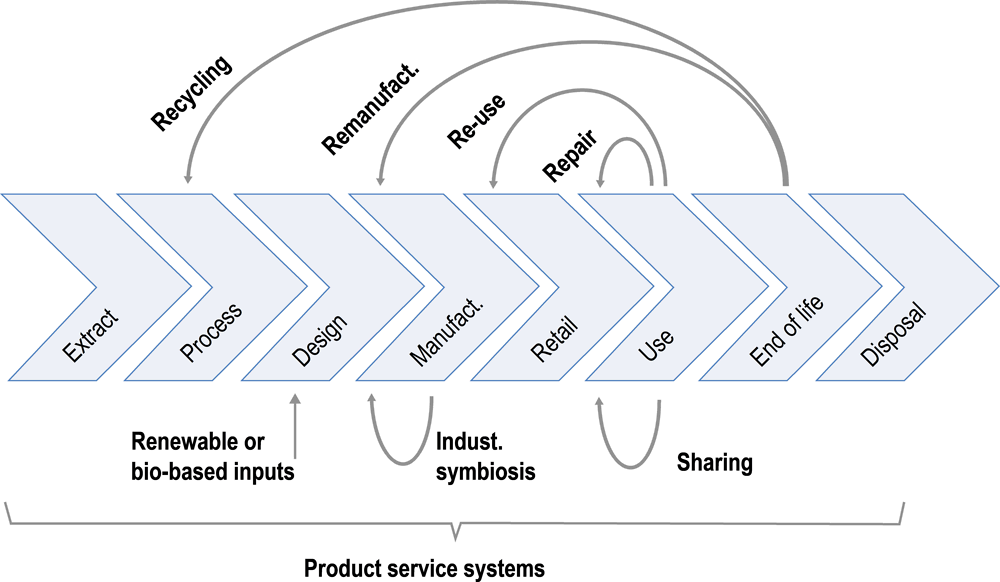

This chapter identifies five key business models that could facilitate a transition towards a more resource efficient and circular economy. In this report, the term business model is used to describe how a firm creates, captures, and delivers value. In other words, it is a firm’s competitive strategy. Osterwalder, Pigneur and Tucci (2010[1]) differentiate nine main elements of a business model. These are, the value proposition involved, who the key supply chain partners are, what resources and activities are involved in product creation, what their cost structure is, how products are delivered, which customer segments are targeted, how customer relationships are managed, and how revenues are collected. In this chapter, this framework is applied to five headline circular business models. Much of the focus is on character of the business case for an adopting firm, but attention is also given to the activities involved in production and the characteristics of revenue collection. Circular business models are often quite innovative in these respects.

Circular business models have a number of other distinguishing characteristics beyond their relatively sparing use of natural resource inputs. First, the underlying sales strategy tends to place less emphasis on maximising the sales volume of low-margin and short-lived products. Instead, the focus tends to be on selling higher quality products or, increasingly, marketing access to, rather than ownership of products. Second, the business case often leverages the value contained in already existing materials, components, and products. For example, by largely avoiding the use of new material and energy inputs, firms offering repair, refurbishment, or remanufacturing services can market products at a significantly lower cost than their traditional counterparts. Third, circular business models often involve greater levels of collaboration between different actors in the supply chain. There are often repeated interactions between suppliers and customers, and this can foster a heightened sense of customer loyalty. For example, operating within an industrial symbiosis framework requires significant inter-firm cooperation to ensure the ongoing availability of high quality of raw material inputs.

2.1. A typology of circular business models

The literature on circular business models is growing rapidly and contains a variety of different typologies. There are considerable differences in the level of granularity, as well as the classification approach that is taken. Some authors take a value chain perspective that structures business models into circular design, optimal use, and value recovery types (Achterberg, Hinfelaar and Bocken, 2016[2]). Others distinguish business models according to the material flows they address. IMSA (2015[3]) focus on short loops, long loops, cascades, and pure cycles while Lewandowski (2016[4]) focus on regeneration, sharing, optimisation, or looping. The activities implicit in all of these typologies overlap significantly, but are often given different names.

The typology that is adopted in this report draws on that developed by Accenture (Lacy and Rutqvist, 2015[5]). In contrast to the typologies discussed above, circular activities are categorised according to a business-centric perspective. This draws attention to the business proposition underlying each of the business models, which is significant given that widespread adoption will remain largely theoretical unless the private sector perceives substantial value. The five types of headline circular business models addressed in this report are: (i) circular supply models, (ii) resource recovery models, (iii) product life extension models, (iv) sharing models, and (v) product service system models (Table 2.1).

While the distinction between each type of business model is clear in theory, it may be less so in practice. In some cases, firms adopt combinations of business models rather than one in isolation. For example, the adoption of product service system model – and the retention of product ownership that goes with it – may well serve to incentivise the parallel adoption of the product life extension model (Thompson et al., 2010[6]). In other cases, the decision to adopt a particular circular business model by a firm or group of firms can facilitate the adoption of a related business model by others. The adoption of the circular supply model, where strategic sourcing and design decisions are made early in a product’s life, can improve the business case for component and material recovery further downstream.

Not all of the business models discussed included in this typology are necessarily new or novel. The resource recovery business model, where secondary raw materials are produced from waste, has operated in the metals sector for millennia. Similarly, ensuring that products attain their intended service life through reuse and repair has probably been widespread since the emergence of manufacturing. Other business models often appear to be novel, but have instead evolved from well-established traditional activities. One example involves peer to peer sharing of existing, but under-utilised, consumer assets. Sharing has always taken place; the distinction today is that it often takes place between individuals who did not previously know each other. In this case, it is the emergence and diffusion of digital networks, portable devices, and smart software systems that has enabled business model evolution.

Some circular business models do not have obvious historic equivalents. One example concerns circular supply models, where traditional material inputs are replaced by bio-based, renewable, or recoverable materials. These are probably emerging partly in response to greener consumer preferences in certain segments of the population. Firms are leveraging an increased willingness to pay for green products by ensuring that the environmental footprint of their supply chains is relatively small. Another example concerns product service system models in the context of dematerialised consumer products like e-books, streamed music and films, and digital newspaper subscriptions. Digitalisation has meant that the suppliers of these products can avoid the material input costs associated with producing physical products, and thereby produce additional output with virtually no additional cost.

2.2. Individual circular business model characteristics

2.2.1. Circular supply models

Circular supply business models involve the replacement of traditional production inputs with bio-based, renewable, or recovered materials. By making strategic sourcing decisions at the outset of product development, adopting firms can reduce the environmental pressures emanating from their supply chains, while ensuring that the materials embedded in their products do not eventually become waste. In this sense, the circular supply model can be viewed as a form of resource recovery model, albeit one where material recovery is considered at a much earlier stage of the product lifecycle. Essentially, waste is designed away.

The philosophy underlying the circular supply model is often referred to as “cradle to cradle” product design.1 This is intended to create a distinction with cradle to grave material flows, where the materials embedded in products end their lives in incineration or landfill facilities. Instead, these materials become inputs in the manufacture of new products. In this context, a parallel is often drawn with natural systems, where the death of an organism results in the cycling of nutrients to other organisms. Cradle-to-cradle is now also an official certification system, with around 500 certified products. One example of a firm selling C2C certified products is Tarkett, a global manufacturer of floor coverings (see Annex 1). Other examples include Advance Nonwoven, a Danish manufacturer of insulation material, and Green Packaging, an American manufacturer of food packaging.

The business case underlying the adoption of circular supply business models is twofold. First, replacing traditional inputs with bio-based, renewable, or recovered equivalents allows firms to market their products as “green”. By differentiating their products in this way, adopting firms can target environmentally conscious consumers who are perhaps prepared to pay a premium for the knowledge that their consumption decisions have a smaller environmental footprint. Second, switching towards alternative material inputs is a way of managing regulatory and supply chain risk. With respect to the former, the introduction of more stringent environmental regulation is a possibility in many countries, and represents an important business risk for firms using polluting inputs in their production process. With respect to the latter, the natural resources from which key production inputs are derived are often geographically concentrated in a small number of countries, sometimes in politically unstable parts of the world. Manufacturers can at least partially mitigate the associated sourcing risk by integrating locally derived secondary materials into their supply chains.

Implementing the circular supply business model has implications for various aspects of a firm’s operations. It influences the conceptualisation of the product design and the manufacturing process, and also concerns product branding and eventual distribution channels. Successful implementation requires that certain conditions are met. First, there must be sufficient market demand, and willingness to pay, for green products. This condition is likely to differ across jurisdictions; consumers in developing countries may have a limited ability to pay for products that are relatively expensive. Second, the bio-based, renewable, or recovered material inputs that are adopted must be good substitutes for the traditional materials that they replace. They also need to be sufficiently available and affordable; firms are unlikely to adopt the circular supply business model where it significantly increases their cost of doing business or risk profile.

2.2.2. Resource recovery models

Resource recovery business models involve the production of secondary raw materials from waste streams. There are three main activities involved, each of which is typically undertaken by different market actors (Gaillochet and Chalmin, 2009[7]). As its name suggests, collection involves the collection of the waste materials generated by households, businesses, and industry; it is generally organised by local governments. Sorting involves separation of a particular waste stream into its constituent materials; in some cases it is undertaken in public facilities and in others by the private sector. Secondary production involves the transformation of sorted waste material back into finished raw materials; it is generally undertaken by firms operating in the private sector. The resulting secondary raw materials – metals, plastics, paper, etc – are then sold to various manufacturing firms.

The business case underlying resource recovery models centres on the valorisation of the materials contained in waste streams. Raw waste is available at little or no cost; indeed the households and firms that generate it are often willing to pay to have it taken away. At the same time, finished secondary raw materials fetch significant prices on commodity markets. The challenge for firms adopting the resource recovery model is in ensuring that the unit cost of undertaking this valorisation process is sufficiently small relative to the market price of finished materials.

Adoption of the resource recovery business model is only likely under certain conditions. First, there needs to be a market for secondary raw materials. Concerns about the quality or composition of these materials mean that this is not always the case. Some technologically advanced sectors (aerospace for example) tend to avoid recovered materials because of uncertainty about their performance characteristics in extreme conditions. Similarly, food packaging providers in some countries are unable to use recovered plastics and paper due to hazardous chemicals regulation. Second, adoption of the business model requires that a sufficient volume of waste material being generated. This is not always the case, especially in regions characterised by low population densities or low levels of consumption. Although the transport of waste to central processing facilities is technically possible, it is not always economically feasible given the bulky and low value character of many waste streams.

The resource recovery business model, or recycling as it is better known, has several variants, each of which is described below:

Downcycling

Like recycling, downcycling involves the transformation of waste into secondary raw materials. The key difference is that the recovered materials are of an inferior quality, and can only be used as an input in a limited subset of applications. For example, in the context of paper and cardboard recycling, each additional loop results in a reduction of the length of cellulose fibres. As a result, recovered paper cannot always be used for the same applications that virgin paper can.

Upcycling

Upcycling is the opposite of downcycling. It involves the transformation of waste into secondary raw materials, and their subsequent use in relatively high value applications. An illustrative example is undertaken by Freitag, a German apparel manufacturer, that produces bags made from truck tarps, car seat belts, and bicycle inner tubes (see Annex 1).

Industrial symbiosis

Industrial symbiosis, or closed loop recycling as it is sometimes called, involves the use of production by-products from one firm as production inputs by another (Achterberg, Hinfelaar and Bocken, 2016[2]). Relative to classical recycling, there is more of an emphasis on commercial and industrial waste streams and, at the same time, fewer intermediate actors involved in material transformation. Industrial symbiosis is most common in industries that produce very pure and homogeneous material flows, such as the chemical industry. Some of these tight relationships develop organically. Most often, however, they are the result of carefully planned industrial parks that connect one firm with another via pipelines or short-distance truck deliveries (Taranic, Behrens and Topi, 2016[8]).

2.2.3. Product life extension models

As their name suggests, product life extension models involve extending the life of products. This is desirable from a circular economy perspective because products, and the materials embedded in them, remain in the economy for longer, and thereby potentially reduce the extraction of new resources. There are three mechanisms involved. First, manufacturers can extend the service life of their products by designing them in a way that increases durability. This is referred to as the classic long life model in the remainder of this report. Second, reuse and repair activities, and their associated business models, ensure that products actually attain their intended service life (rather than being prematurely discarded). Third, remanufacturing extends the life of products by “resetting the clock” – remanufactured products attain an entirely new service life. Each of these business model sub-types is summarised in Table 2.2 and discussed briefly below.

With the exception of the classic long life model, it is not necessarily the case that product life extension models are undertaken by the original equipment manufacturer (OEM). In many cases, it is actually third party operators that facilitate the reuse of second-hand goods, or carry out repair, refurbishment, or remanufacturing activities. The business case varies accordingly. For third party adopters, offering repair, refurbishment, or remanufacturing services is about leveraging the cost savings associated with using already existing materials and products as inputs. These activities produce products of a similar quality to new equivalents, but at a considerably lower cost. For original equipment manufacturers, the decision to adopt life extension activities probably rests upon two additional considerations. First, adoption is a strategic way of addressing the threat from third party firms and may foster greater customer loyalty (Long et al., 2017[9]). Second, in the case of remanufacturing, adoption can partially mitigate procurement risks associated with key material inputs.

Classic long life

As discussed above, the classic long life model involves designing products with longer service lives. The business case for adoption is similar to that for circular supply models; firms that produce higher quality products have an ability to charge customers higher prices. Essentially, low sales volumes are offset by a premium pricing strategy.

Direct reuse

In many cases, products are not disposed of because they have reached the end of their (functional) life, but because consumers decide to replace them with updated versions. For example, Cooper (2004[10]) finds that around one third of appliances in the UK are still in working order when thrown away. The direct reuse business model takes advantage of this by facilitating the redistribution of used products to new owners. In this way, products that would have otherwise been disposed of continue to remain in circulation.

Direct reuse is not usually facilitated by the original manufacturer, but by a third-party who distributes goods that already exist in the economy. In this context, internet reselling platforms such as eBay and Craigslist have gradually tapped into the market and are competing with more traditional second-hand shops and bulletin boards (Lacy and Rutqvist, 2015[5]). Because profit is usually made via a small margin of the reselling price, the residual value of the product should be high enough for reselling. It is, therefore, important that the product is not severely damaged and generally in good condition. A challenging aspect of this model is to reach a critical mass of sellers/donors and buyers to make the platform attractive.

Maintenance and repair

By fixing or replacing defective components, product maintenance and repair ensures that products reach their full expected service life. In this way, degraded products that would otherwise have been discarded of and replaced continue to remain in circulation. This is no small issue; research undertaken by WRAP (2011[11]) finds that 23% of the electronic equipment discarded in the UK could be reused or resold with minor or moderate repair. Fairphone, a smartphone manufacturer, is one example of a firm attempting to address this issue. By incorporating greater modularity into the design of their smartphones, Fairphone facilitates the repair of existing products and reduces demand for new equivalents.

Maintenance and repair is carried out by both original equipment manufacturers (such as Fairphone) and by third party firms (such as iMend or Mister Minit). For original manufacturers, a major benefit of integrating service components to the value proposition of a physical product is the high-quality branding and customer trust that it affords. Selling the same product at a price premium is also conceivable from a marketing point of view. Through potential multiple points of contact between the seller and buyer after the initial sale, there is furthermore a chance to build up higher brand loyalty, especially when customer experience has been positive (Bocken et al., 2016[12]).

Refurbishment and remanufacturing

Refurbishment and remanufacturing involve the restoration of degraded products, either for a fee, or for subsequent resale to original or new owners. In refurbishment, the emphasis is largely on aesthetic improvements, with limited restoration of product functionality (Spelman and Sheerman, 2014[13]). Remanufacturing, by contrast, is a broader concept that involves the restoration of used products to their original level of functionality (Box 2.1). As such, despite the usually lower sales price, remanufactured products are usually labelled “as good as new” (Parker et al., 2015[14]). Remanufacturing is usually carried out by the original equipment manufacturer (OEM), which has the both the technical expertise and the appropriate components to allow product performance to be fully restored.

According to the European Remanufacturing Network (Parker et al., 2015[14]), the only definition for remanufacturing that is recognised as a national standard is that produced by the British Standards Institution. BS 8887-2 states that remanufacturing involves “returning a product to at least its original performance with a warranty that is equivalent or better than that of new, newly manufactured product”. Supplementary notes to this definition state that remanufacturing involves the dismantling of products, restoring and replacing components, and testing individual parts and the whole product to ensure it fits within the original design specifications. It is this process that ensures that remanufactured products have at least the same performance level as the original new product.

Remanufacturing can be a profitable business model; it has been adopted by an increasing number of multinationals worldwide. Its earning model is based upon generating additional revenue by reselling the same or similar products multiple times. Moreover, cost savings can be achieved by reducing the amount of virgin material and components being sourced. Often, a remanufactured product is 40% less expensive than a newly manufactured one (Le Moigne and Georgeault, 2016[15]). In times of highly volatile natural resource prices, this may lead to a reduced sourcing risk. The successful and profitable integration of an in-house remanufacturing capacity requires several factors to be in place, such as dedicated factory facilities, a specialized workforce, and a sophisticated reverse logistics system. Although remanufactured goods are usually cheaper than newly manufactured ones, they often come with a comparable quality standard and warranty which makes them an interesting alternative for customers. Products suited for the remanufacturing model are mostly capital intensive and durable. They should have long product life cycles and a modular design for easy disassembly and repair in order to be economically viable. Annex 1 provides a case example for heavy machinery manufacturer Caterpillar.

2.2.4. Sharing models

Sharing models, or sharing economy or sharing platform models as they are sometimes called, involve using under-utilised consumer assets more intensively, either through lending or pooling (Box 2.2). There are a variety of products that sit unused for much of their effective life; housing, vehicles, clothing, and tools are some examples. Research by the Ellen McArthur Foundation finds that the average European vehicle is parked 92% of the time and that, even when it is in use, only 1.5 of the available 5 seats are typically used (Ellen McArthur Foundation, 2015[16]). Sharing of these products has always taken place, but has become more widespread in recent years as the phenomenon of “sharing between strangers” has emerged. This has largely resulted from the emergence of various technologies – the internet, mobile phone technology, and the development of referral and reputational systems – that have reduced the transaction costs and risks associated with sharing assets.

Most of today’s sharing practices are facilitated by online platforms, some of which – Airbnb for example – have become powerful market actors. Sharing models have two sub-types: co-ownership and co-access. The underlying business case for both is clear. Online platforms facilitate transactions between the owners of under-utilised assets and individuals seeking to use them; platform owners can generate a small margin on each related transaction. Significantly, because the capital cost of the underlying goods has already been paid (by owners), the up-front investment cost required to launch an online platform is significantly smaller than that required to become a traditional provider. Platforms usually also have very small operational costs and significant potential for scale up.

For the owners of under-utilised assets and products, the emergence of online platforms provides an opportunity to earn additional income. Unused apartments, rooms, vehicles, vehicle seats, clothing, or tools can be leveraged, rather than sitting idle. Potential buyers also benefit to the extent that shared products are cheaper than their traditional equivalents. For example, one reason why accommodation sharing has performed so strongly in recent years is because it is often available at a price discount to traditional hotel rooms. Several recent assessments find that the average price of an Airbnb listing was between 15% and 20% lower than a traditional hotel equivalent (STR, 2017[17]; Statista, 2017[18]).

There are widely diverging views about what activities sharing models encompass. This is partially a consequence of the use of the key enabling technology – online platforms – in a number of other closely related business models. The definition of sharing models used in this report follows that developed by Frenken and Schor (2017[19]), who describe the activities involved as “consumers granting each other temporary access to under-utilized physical assets, possibly for money”. In this view, sharing models have three key aspects:

-

They involve peer to peer or, alternatively, consumer to consumer (C2C) transactions. Transactions that involve renting or leasing products from firms are separate since, in many cases, they would considered as product service system business models (consider urban car sharing schemes such as Autolib or the leasing of idle industrial capacity for example).

-

They involve the temporary, rather than permanent transfer of product ownership. Online platforms that facilitate the sale and purchase of second hand goods would be considered to fall under product life extension business models (consider EBay for example).

-

They involve the more efficient use of under-utilised physical assets, rather than services provided by private individuals. Online platforms that facilitate the service transactions between individuals are examples of on-demand business models (consider Uber or Task Rabbit).

Focusing on the business activities facilitated by online platforms, rather than the platforms themselves, has two main advantages. First, not all of the business activities that utilise online platforms necessarily have the potential to improve material efficiency or stimulate a transition to a more circular economy. Consider the migration of traditional retail sales to online platforms such as Amazon or the emergence of on-demand services platforms such as Uber for example. Second, the regulatory issues relating to online platforms differ considerably according to the specific business activities involved. Consider the distinction between B2C and C2C transactions and questions about who is, and is not, considered to be a producer for tax (and other) purposes.

Co-ownership

The co-ownership variant of sharing models involves the lending of physical goods. The sharing of household tools and appliances on platforms like Peerby is one such example. Products that are especially suited for the co-ownership model are capital intensive, infrequently used, and have a low ownership rate (IDDRI, 2014[20]). Moreover, they must be easy to transport and should be durable, in order to allow for the increased usage during their effective lifespan. Urban areas are particularly suited to co-ownership models; high population densities reduce the transaction costs associated with a temporary change in product ownership (IDDRI, 2014[20]). Annex 1 provides examples of several sharing models.

Co-access

The co-access variant of sharing models involves allowing others to take part in an activity that would have taken place anyway. Thus, carpooling allows seats that would otherwise have remained empty to be occupied during a particular journey. Blablacar is a prominent example of this business model. Though its online platform, it links drivers intending to undertake long journeys with passengers that are willing to pay for a spare seat.

2.2.5. Product service systems models

Product service system (PSS) models combine a physical product with a service component. There are several variations, some of which place more emphasis on the physical product, and others that focus more on the service aspect. The typology used in this report follows that developed by Tukker (2004[21]). It separates product service system models into three main variants: product-oriented, user-oriented, and result-oriented PSS models. Each of these is briefly discussed below.

Product-oriented product service system models

Product-oriented PSS systems are focused mostly on the product end of the PSS spectrum. Manufacturing firms that adopt this business model continue to produce and sell products in a conventional way, but include additional after-sales service in the value proposition. Services may, for instance, take the form of maintenance contracts and repair offerings through extended product warranties or take back agreements (COWI, 2008[22]). For example, the high-end outdoor clothing company Patagonia guarantees to repair broken apparel and operates a platform for customers to sell their products as second-hand products.

User-oriented product service system models

User-oriented (or access-oriented as they are sometimes called) PSS models put products and services on a more balanced footing. Customers pay for temporary access to a particular product, typically through a short- or long-term lease agreement, while the service provider retains full ownership of the product. Urban car sharing schemes, office equipment leases, and garment rental services are widely cited examples of user-oriented PSS models. Another rapidly emerging example concerns the digitalisation of various forms of traditional media.2 Online platforms like Amazon, Netflix, Spotify, and Coursera allow literature, film, music, and education to be consumed without ownership of the underlying books, CDs, DVDs etc.

User-oriented PSS models provide access to the services associated with a particular good without ownership of the good itself. That means that consumers only pay for a product when they actually need it; the upfront and ongoing costs of ownership are largely avoided.3 In the case of urban car sharing schemes, customers can temporarily use a vehicle without having to bear the associated running, maintenance, and parking costs. In addition, user-oriented PSS models can also provide consumers with access to high quality or technologically advanced products that they could not otherwise afford. One example concerns clothing; it is common for individuals to lease, rather than own, some types of expensive garments.

Adopting a user-oriented PSS models can create various opportunities for firms. By retaining ownership of products, and the components and materials embedded in them, manufacturers can potentially mitigate a range of supply chain risks (access to, and price volatility of, material inputs for example). This is likely to be an important driver of business model adoption in certain situations (such as where the security of supply of key manufacturing inputs is uncertain), but not in others (such as where the business model is adopted by third party, non-manufacturing firms). In the latter case, the adoption of user-oriented PSS is probably motivated by a different set of opportunities. For example, for expensive goods such as vehicles and high-end clothing, there may be value in targeting consumers who are unable or unwilling to purchase new products, but who may be interested in paying for temporary access to them. Similarly, providing goods like literature and music digitally can reduce unit production costs while also increasing revenues (through the ability to sell advertising on the associated online platform).

Result-oriented product service system models

Result-oriented PSS models are situated at the service end of the PSS spectrum. Instead of marketing manufactured assets or goods in a traditional way, adopting firms market the services or outcomes provided by these goods. For example, an adopting firm might sell a heating outcome (maintaining a certain temperature level within a building), rather than the underlying heating equipment or energy inputs. Alternatively, an adopting firm may undertake the manufacturing of a particular brand’s products rather than selling the capital equipment itself.4 Essentially, contracts between suppliers and customers therefore describe a specific outcome, without necessarily specifying the means through which it is achieved (COWI, 2008[22]). This creates strong incentives for the efficient use of variable (and potentially polluting) inputs such as energy or chemicals. Result-oriented PSS models have been adopted in a range of sectors; US EPA (2017[23])gives the following three examples:

Energy service companies (ESCOs) offer energy efficiency and related services to their customers by assuming full performance risk for the project and products used. The level of compensation is tied closely to the energy efficiency savings they are able to accomplish. An example is the Dutch lighting company Philips which introduced ‘Circular Lighting’ or ‘pay-per-lux’ back in 2009. A client may agree with Philips on a specific level of brightness for a facility measured in lux. The task of Philips then is to provide the level of brightness with the most cost-effective lighting equipment possible (see additional details on this in annex 1).

Chemical management services (CMS) or chemical leasing aims at supplying and managing the customer’s chemicals. The business model emerged first in the late 1980s in the US and has resulted in many long-term contract relationships (OECD, 2017[24]). Similar to the case of ESCO’s, the compensation of the provider is linked to the quantity and quality of the service and not, as in traditional models, to the volume of the chemicals used. By taking full responsibility of the chemicals used, the providing firm will also be responsible for their handling at the end-of-life and have incentives to optimise these costs.

Integrated pest management (IPM) and performance based pest management (PPMS) is a special form of chemical leasing in the agricultural sector. The chemicals used for pest control are owned and handled by the providing company which possesses expertise about their optimal application. The compensation is not based on the chemical volumes sold, but on the level of crop loss prevented.

2.3. Drivers of circular business model adoption more generally

The business case for the adoption of circular business models is not static, but varies according to a broad set of societal level factors. Changes in consumer behaviour, the threat of new regulation, or concerns about the stability of key supply chains represent considerable business risks for firms operating traditional business models, and can stimulate switching towards greener, more circular modes of production. In a similar way, the appearance of new technologies can reduce the cost structure of relatively circular production, thereby creating opportunities for potential adopters. The following section presents a brief snapshot of the factors that are facilitating the adoption of circular business models.

2.3.1. Traditional “linear” modes of production: emerging business risks

Regulatory risk is becoming a significant concern for firms that operate traditional business models. One example concerns the emerging prospect of more widespread and stringent carbon pricing. This probably partly explains the broader adoption of internal shadow carbon pricing within the private sector (CDP, 2016[25]), and the diversification of some fossil fuel producers into renewable electricity technologies (Climate Home, 2016[26]). Another example concerns the potential introduction of more stringent product design and material recovery standards in various countries. The recent adoption of bans of certain products made from plastic (e.g. such as single carrier plastic bag bans) in a number of countries, as well as the recent European Union strategy on plastics are such examples (European Commission, 2018[27]), and probably represents a significant risk for firms whose products rely heavily on virgin plastic inputs.

Many emerging renewable energy and information communication technologies are heavily reliant on materials that are geographically concentrated in a handful of countries. More than 80% of the global production of rare earth elements – a key input in several renewable energy technologies – takes place in China (USGS, 2016[28]). Similarly, about half of global cobalt production – a key input in smartphone, laptop, and automotive batteries – takes place in the Democratic Republic of Congo. For the firms that manufacture these products, geo-politically related supply chain disruptions are an important operational risk, but one that can be partially mitigated by the adoption of the circular supply, resource recovery, or product service system models.

Heightened consumer awareness is creating new sources of reputational risk for established firms. Concerns about human rights abuses, dangerous working conditions, financing conflict have existed in the jewellery and clothing sectors for many years, and have led to a proliferation of labelling schemes intended to differentiate ethically produced products from otherwise. In the environmental sphere, similar concerns – about global warming, plastics pollution and biodiversity loss among others – may be creating new impetus for the adoption of greener or more circular modes of production. The recent pledges made by eleven leading consumer goods firms (including Coca Cola, Unilever, and L’Oréal) to use 100% reusable, recyclable, or compostable packaging by 2025 (Ellen McArthur Foundation, 2018[29]) may partially reflect this issue.5

2.3.2. Emerging technologies as a driver for the adoption of more circular modes of production

The appearance and diffusion of new technologies has also been an important factor in the evolution and growth of circular business models. The emergence of the internet and the widespread uptake of digital devices have been particularly important. First, increased connectivity has reduced the transaction costs and risk associated with sharing goods, and increased the convenience of leasing rather than owning goods. Second, connectivity has allowed, in combination with smart sensor technology, real time monitoring of product performance, which is probably facilitating certain types of product service system. Third, connectivity has allowed, in combination with digitalisation, a variety of consumer products to be significantly dematerialised. In addition to the content related goods described above, digitalisation has also affected education (though the growth of so-called massive open online courses) and work travel (through the emergence of teleconferencing).

Improvements in more traditional production technologies have also improved the business case for some circular business models. In the case of the circular supply model, the rapid improvements in solar and wind generation technologies are well documented, and have allowed renewable facilities to become increasingly competitive with their fossil fuel based equivalents. In the case of the resource recovery business model, the emergence of mechanised material sorting facilities (MRFs) has significantly improved the separation of different waste streams, thereby reducing the cost of secondary material production. In the case of the repair and remanufacturing business models, improvements in sensor technology have allowed faults to be diagnosed relatively quickly, again improving the underlying business case.

Technological change is also creating a variety of risks in the context of resource use and environmental pressure. The emergence and diffusion of a variety of labour saving technologies – ranging from robotics in production to snow movers and leaf blowers in consumption – may have actually increased the environmental footprint of some activities. In addition, rebound effects, which are discussed further in Section 4.4, have probably offset at least some of the reductions in resource extraction that have been realised by efficiency improvements. Finally, the continued growth of green technologies may be shifting the environmental burden associated with resource extraction and use away from the atmosphere (in the form greenhouse gas and sulphur and nitrogen oxide emissions for example) towards water and land. The extraction and processing of the aluminium, copper, lithium, and rare earth elements used widely in the automotive, energy, and ICT sectors has a variety of often toxic by-products such as mine waste, process tailings, and smelter residues.

References

[2] Achterberg, E., J. Hinfelaar and N. Bocken (2016), The Value Hill Business Model Tool: identifying gaps and opportunities in a circular network, http://www.scienceandtheenergychallenge.nl/sites/default/files/multimedia/organization/sec/2016-06-16_NWO_Sc4CE/NWO%20Sc4CE%20-%20Workshop%20Business%20Models%20-%20Paper%20on%20Circular%20Business%20Models.pdf (accessed on 13 September 2018).

[12] Bocken, N. et al. (2016), “Product design and business model strategies for a circular economy”, Journal of Industrial and Production Engineering, Vol. 33/5, pp. 308-320, https://doi.org/10.1080/21681015.2016.1172124.

[25] CDP (2016), Embedding a carbon price into business strategy, https://b8f65cb373b1b7b15feb-c70d8ead6ced550b4d987d7c03fcdd1d.ssl.cf3.rackcdn.com/cms/reports/documents/000/001/132/original/CDP_Carbon_Price_report_2016.pdf?1474899276 (accessed on 13 September 2018).

[26] Climate Home (2016), Exxon, Shell, Total, Statoil renew clean energy drive, http://www.climatechangenews.com/2016/05/23/exxon-shell-total-and-statoil-make-clean-energy-plays/ (accessed on 13 September 2018).

[10] Cooper, T. (2004), “Inadequate Life?Evidence of Consumer Attitudes to Product Obsolescence”, Journal of Consumer Policy, Vol. 27/4, pp. 421-449, https://doi.org/10.1007/s10603-004-2284-6.

[22] COWI (2008), Promoting Innovative Business Models with Environmental Benefits, http://www.cowi.com (accessed on 13 September 2018).

[29] Ellen McArthur Foundation (2018), Eleven companies take major step towards a New Plastics Economy, https://www.ellenmacarthurfoundation.org/news/11-companies-take-major-step-towards-a-new-plastics-economy (accessed on 13 September 2018).

[16] Ellen McArthur Foundation (2015), GROWTH WITHIN: A CIRCULAR ECONOMY VISION FOR A COMPETITIVE EUROPE, https://www.ellenmacarthurfoundation.org/assets/downloads/publications/EllenMacArthurFoundation_Growth-Within_July15.pdf (accessed on 13 September 2018).

[27] European Commission (2018), Plastic Waste: a European strategy to protect the planet, defend our citizens and empower our industries, http://europa.eu/rapid/press-release_IP-18-5_en.htm (accessed on 18 January 2018).

[19] Frenken, K. and J. Schor (2017), “Putting the sharing economy into perspective”, Environmental Innovation and Societal Transitions, Vol. 23, pp. 3-10, https://doi.org/10.1016/J.EIST.2017.01.003.

[7] Gaillochet, C. and P. Chalmin (2009), From waste to ressources : world waste survey 2009, https://www.researchgate.net/publication/41222409_From_waste_to_ressources_world_waste_survey_2009 (accessed on 13 September 2018).

[20] IDDRI (2014), The sharing economy: make it sustainable, http://www.iddri.org (accessed on 13 September 2018).

[3] IMSA (2015), Circular business models: an introduction to IMSA's circular business model scan, https://groenomstilling.erhvervsstyrelsen.dk/sites/default/files/media/imsa_circular_business_models_-_april_2015_-_part_1.pdf (accessed on 13 September 2018).

[5] Lacy, P. and J. Rutqvist (2015), Waste to wealth : the circular economy advantage.

[15] Le Moigne, R. and L. Georgeault (2016), “Remanufacturing: Une Formidable Opportunité Pour La France Industrielle de Demain”, https://www.wmaker.net/eco-circulaire/attachment/656994/ (accessed on 13 September 2018).

[4] Lewandowski, M. (2016), “Designing the Business Models for Circular Economy—Towards the Conceptual Framework”, Sustainability, Vol. 8/1, p. 43, https://doi.org/10.3390/su8010043.

[9] Long, X. et al. (2017), “Strategy Analysis of Recycling and Remanufacturing by Remanufacturers in Closed-Loop Supply Chain”, Sustainability, Vol. 9/10, pp. 1-29, https://ideas.repec.org/a/gam/jsusta/v9y2017i10p1818-d114402.html (accessed on 13 September 2018).

[24] OECD (2017), Economic Features of Chemical Leasing, https://one.oecd.org/document/ENV/JM/MONO(2017)10/en/pdf (accessed on 13 September 2018).

[1] Osterwalder, A., Y. Pigneur and C. Tucci (2010), Clarifying Business Models: Origins, Present, and Future of the Concept, https://www.researchgate.net/publication/37426694_Clarifying_Business_Models_Origins_Present_and_Future_of_the_Concept (accessed on 13 September 2018).

[14] Parker, D. et al. (2015), Remanufacturing Market Study, http://www.remanufacturing.eu/assets/pdfs/remanufacturing-market-study.pdf (accessed on 13 September 2018).

[13] Spelman, C. and B. Sheerman (2014), Triple Win: The Social, Economic, and Environmental Case for Remanufacturing, http://www.policyconnect.org.uk/apmg (accessed on 13 September 2018).

[18] Statista (2017), Airbnb - Statistics & Facts, https://www.statista.com/topics/2273/airbnb/ (accessed on 13 September 2018).

[17] STR (2017), Airbnb & Hotel Performance, http://www.str.com/Media/Default/Research/STR_AirbnbHotelPerformance.pdf (accessed on 13 September 2018).

[8] Taranic, I., A. Behrens and C. Topi (2016), Understanding the Circular Economy in Europe, from Resource Efficiency to Sharing Platforms: The CEPS Framework, http://www.ceps.eu (accessed on 13 September 2018).

[6] Thompson, A. et al. (2010), Benefits of a Product Service System Approach for Long-life Products: The Case of Light Tubes, http://www.ep.liu.se/ecp/077/011/ecp10077011.pdf (accessed on 13 September 2018).

[21] Tukker, A. (2004), “Eight types of product–service system: eight ways to sustainability? Experiences from SusProNet”, Business Strategy and the Environment, Vol. 13/4, pp. 246-260, https://doi.org/10.1002/bse.414.

[23] US EPA (2017), “U.S. EPA Sustainable Materials Management Program Strategic Plan”, https://www.epa.gov/sites/production/files/2016-03/documents/smm_strategic_plan_october_2015.pdf (accessed on 23 April 2018).

[28] USGS (2016), USGS Minerals Information: Commodity Statistics and Information, https://minerals.usgs.gov/minerals/pubs/commodity/ (accessed on 18 May 2018).

[11] WRAP (2011), Realising the Reuse Value of Household WEEE, http://www.wrap.org.uk (accessed on 13 September 2018).

Notes

← 1. Circular supply models are also often said to facilitate an economy that is “regenerative by design”.

← 2. This is perhaps an example of a hybrid circular business model. In many cases, it involves short-term access to, rather than ownership of, goods and services; a key characteristic of result-based PSS models (e.g. Spotify or Netflix). In other cases, it is no more than a traditional sales model, but with transactions of digital rather than physical products (e.g., e-books or digital newspaper subscriptions).

← 3. That said, ownership of electronic devices is normally required for consumers to participate in these product offerings (Netflix and Spotify for example).

← 4. MakeTime, a United States based online platform, facilitates the procurement of precision manufactured parts by connecting product assembers (the client) with upstream production facilities (the supplier).

← 5. Coca Cola has also pledged to, (i) collect and recycle the same volume of packaging that it produces, and (ii) incorporate 50% recycled content into new packaging (both by 2030) (Coca Cola, 2018[144]).