1. The outlook for transport: Speedy recovery, new uncertainties

This chapter summarises the main impacts of the Covid-19 pandemic on the transport sector and describes the major uncertainties currently affecting recovery from the pandemic. The chapter also covers the main drivers of transport demand and the externalities that complicate efforts to decarbonise transport. Next, it outlines the scale of the decarbonisation challenge for the transport sector and provides an update on international co-operation to achieve decarbonisation goals. Finally, it outlines the priorities national transport ministries need to consider when meeting their commitments to the aims of the Paris Agreement.

Global disruptions have hindered the transport sector’s post-pandemic recovery

The Covid-19 pandemic led governments worldwide to introduce lockdowns and restrictions on travel and movement in 2020-22. These actions profoundly affected the global transport sector, which has nevertheless bounced back quicker than expected. Policy responses have also moved on. Some measures, such as travel restrictions, have ended. Others, such as investment in active travel, have become more mainstream in several regions.

However, in 2022, just as the post-Covid recovery gained momentum, the war in Ukraine brought untold destruction and human suffering. The war has been accompanied by an energy crisis and widespread supply-chain disruptions. These disruptive events create new uncertainties for users and providers of transport worldwide, and their effects continue to unfold as this report went to press.

Global gross domestic product (GDP) trends, changing trade patterns, and the volatility of energy prices provide clues as to the potential impact of current events on transport demand. GDP influences both freight and passenger transport. International trade determines freight transport patterns and demand. Fluctuations in energy prices affect travel behaviour.

Uncomfortable truths accompany evidence of the sector’s recovery. Yes, passenger travel is booming now that restrictions on movement have ended. Yes, new trade routes have replaced those closed by the war and sanctions. But the transport sector remains overwhelmingly reliant on fossil fuels. And this continues to make it particularly vulnerable to energy price variability.

The transport sector's future sustainability depends, to a large extent, on its response to the structural crisis created by global warming. Populations and economies are due to grow in the coming years, meaning freight and passenger demand will also increase. The projections for this report demonstrate that current commitments to reduce carbon emissions are insufficient.

The scale of the decarbonisation challenge is vast. International co-operation to achieve decarbonisation goals is making progress but needs to accelerate. The question of equity in meeting climate goals becomes even more urgent in this context. For many governments, balancing national priorities against the need to meet their commitments under the Paris Agreement remains a serious challenge.

Key takeaways

The transport sector’s recovery following the pandemic has been faster than expected but significant challenges remain.

Turmoil in energy markets and cost-of-living crises complicate efforts to decarbonise transport.

Despite some progress, transport emissions will not fall fast enough in the coming years to meet international climate objectives.

Mechanisms exist to advance decarbonisation goals but they need to become more ambitious.

Governments face the challenge of balancing multiple priorities while meeting climate commitments.

The global transport sector’s recovery from the Covid-19 pandemic has exceeded expectations but there remain significant differences between and within countries, with new uncertainties exacerbating these gaps.

Population and economic growth will continue to drive demand for transport, necessitating international co-operation to meet decarbonisation goals. In this context, transport ministries worldwide will face competing priorities, and will need solutions that can address multiple challenges.

This chapter discusses the transport sector’s recovery in the aftermath of the Covid-19 pandemic. It looks closely at how the determinants of transport demand are expected to shape demand in the current economic climate, and in the face of new uncertainties.

All projections of future transport trends are subject to uncertainty. This edition of the ITF Transport Outlook is no exception: it reflects both expected and unexpected impacts of the Covid-19 pandemic and the subsequent transport disruptions. In 2022, just as the global economy was recovering from the pandemic, the war in Ukraine caused further turmoil. Despite the current volatility in global trade and supply chains, transport demand will grow significantly in the long term due to expected economic growth. Population growth, density, and urbanisation trends will move upwards and play an essential role in changing transport activity. Other factors, such as energy prices, land-use policies and behavioural shifts, will also affect transport demand and peoples’ or businesses’ travel/transport choices.

The transport sector plays a significant role in increasing accessibility and influencing individuals’ economic and social outcomes. It also contributes to sustainable development worldwide and is a crucial global actor in the 2030 Agenda for Sustainable Development (UN, 2015[1]). The United Nations defines sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs” (UN, 2022[2]). As demand for transport increases, it will be critical to meet the need for travel and, at the same time, tackle increased carbon dioxide (CO2) emissions, poor air quality and congestion, and improve access to opportunities, goods and services for all.

However, the challenge is stark. In 2018, the transport sector produced 23% of global energy-related CO2 emissions (IEA, n.d.[3]). and had the highest reliance on fossil fuels of all sectors (IEA, 2022[4]). In nearly half of all countries, transport is the highest-emitting sector of the economy (UN, 2021[5]). Yet transport is relatively difficult to decarbonise, due to its high dependence on oil and the complexity that arises from individuals’ own transport choices. At the same time, people and goods will continue to move. With increasing transport demand, even in uncertain times, policy makers must address and mitigate emissions from the transport sector in line with the goals of the Paris Agreement. Transport demand will have to be met in a socially and environmentally just manner, reducing emissions while enabling the movement of people and goods.

Changes in the economy, population and energy markets primarily impact the demand for transport. A rise in economic activity and disposable household incomes increases passenger and freight transport demand. Similarly, a rising population leads to a rise in demand for transport. Accompanying demographic changes, such as increasing urbanisation and changes in national age profiles, also impact the demand for transport and how policy makers tackle it. Furthermore, price fluctuations in energy markets influence travel patterns and investments in alternative fuels. In addition, technological advances and long-term behavioural changes impact the demand for transport. All of these factors, taken together, affect travel demand. This demand, in turn, shapes transport planning and investment decisions.

The Covid-19 pandemic has led to widespread social, economic and environmental changes. Like most parts of the economy, the transport sector has felt the shock of the pandemic across all modes. National and local lockdowns and other travel restrictions have resulted in unprecedented restraints on the movement of people and goods. The pandemic has affected all national and international transport modes, from private vehicles and public transport in urban areas to buses, trains and flights.

Social-distancing requirements and lockdown policies have also affected public transport ridership and shared mobility services. There has been a significant disruption in global supply chains, and passenger travel by aviation fell by 60% in 2020 (ICAO, 2023[6]). Employment levels have taken a severe hit across all sectors, especially in the retail and tourism industries. Workers in large informal sectors in emerging and developing countries suffered, in particular, experiencing more limited access to social safety nets than workers in formal sectors (World Bank, 2020[7]).

In the first months of the pandemic in 2020, essential service workers experienced restrictions and limited public transport options. As an immediate response, governments adopted protocols allowing these workers to make exceptional use of available transport services. Policy makers initially focused on ensuring equitable and continued access to basic services and the movement of essential goods (ITF, 2023[8]).

The transport sector adapted to these changing circumstances. Rail and other public transport providers, bikesharing programmes, taxis and ride-hailing services offered free or discounted rides to health workers. Many bus and train services continued with reduced capacity. A number of measures were taken a few months into the pandemic to create street space for walking and cycling in cities (ITF, 2023[8]).

With the pandemic, many changed the way they travelled. Initially, not just individuals but entire cities and countries came to a halt and supply chains came under heavy strain. As the subsequent waves of the pandemic materialised, countries shifted their focus towards maintaining and restoring the operations of transport services and minimising supply-chain strains. Governments developed financing mechanisms and restructuring packages for transport operators to relieve their financial distress and support their functions in a post-pandemic world.

Post-pandemic recovery has been faster than expected but challenges remain

The ITF Transport Outlook 2021 assumed a set of potential challenges and opportunities for decarbonising transport arising from the Covid-19 pandemic. It presented three scenarios that assessed the impacts of different policy pathways on transport demand, greenhouse gas emissions, local pollutant emissions, accessibility, connectivity and resilience. All three scenarios accounted for the impacts of the pandemic by including assumptions on the economic implications, the expected behavioural shifts and the degree to which the pandemic would affect transport supply and travel patterns in the short and long term.

But economic recovery from the pandemic has been faster than previously estimated. The ITF Transport Outlook 2021 assumed a global drop in gross domestic product (GDP) projections and trade in 2020. It then assumed that, in subsequent years, countries would return to the kinds of growth rates predicted prior to the pandemic. The modelling approximated this trend by assuming a five-year delay in GDP and trade projections returning to pre-Covid-19 levels (ITF, 2021[9]). As the pandemic progressed, however, solutions were found that allowed trade flows to continue.

By 2021, GDP in several countries had already returned to pre-pandemic levels. Among the Group of Seven (G7) countries, by the fourth quarter of 2021, Canada had exceeded its pre-Covid-19 GDP level by 0.2%, compared to the fourth quarter of 2019. The United States and France had already reached their pre-pandemic GDP levels in the second and third quarters of 2021, respectively (OECD, 2022[10]). For the Group of Twenty (G20), while there were significant differences between countries, the GDP for the group returned to pre-pandemic levels in the first quarter of 2021. India, the People’s Republic of China and Türkiye were the first countries in the G20 to do so by the end of 2020. Australia, Brazil and Korea also returned to pre-Covid-19 levels in the first quarter of 2021 (OECD, 2021[11]).

The economic recovery across the world continued strongly in 2021. Still, it slowed down towards the end of the year due partly to the Delta variant of the coronavirus and to continued pandemic-related supply disruptions (IMF, 2021[12]). The International Monetary Fund (IMF) made a downward revision in the growth prospects for 2021 for advanced economies due to inventory drawdowns and softening consumption in the third quarter of the year. At the same time, the IMF made an upwards revision for emerging economies, driven by stronger than anticipated domestic demand. This revision differed from the underlying assumptions for the ITF Transport Outlook 2021, which expected a slower economic recovery.

International trade and freight transport are intrinsically linked

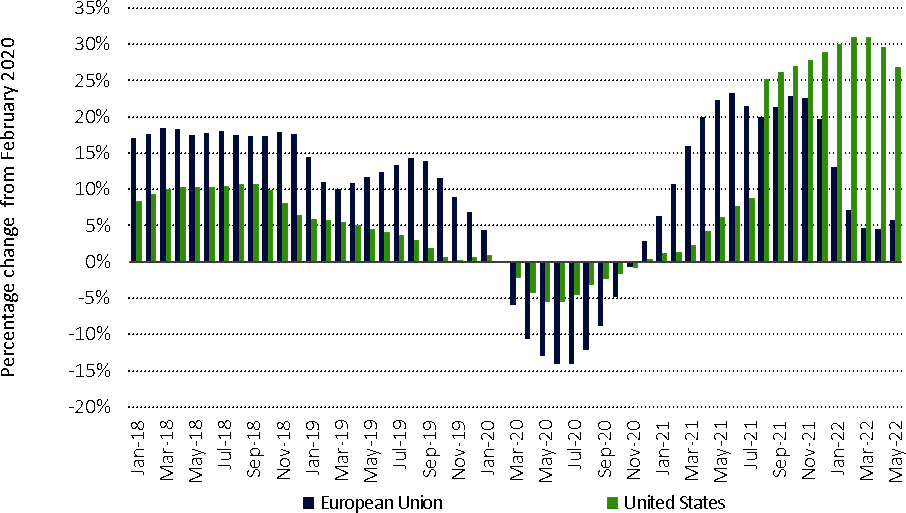

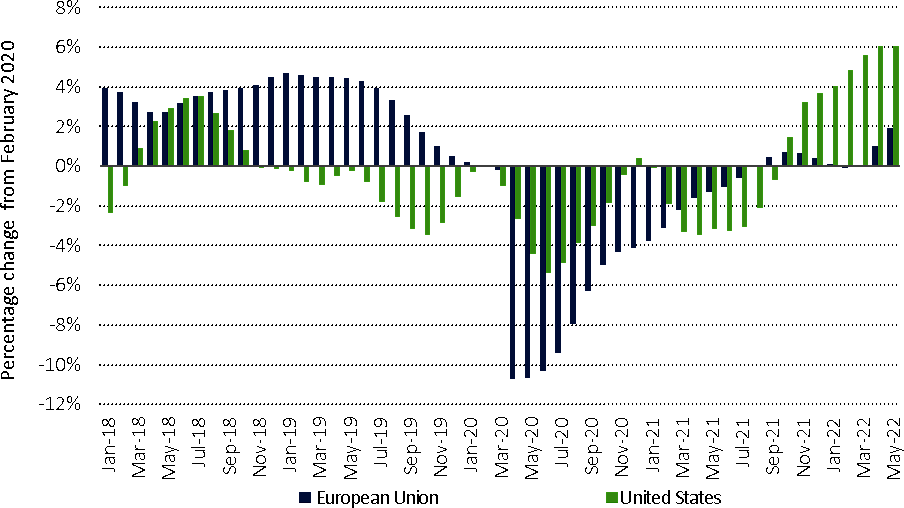

International trade had been recovering strongly from the lows of the Covid-19 pandemic when the war in Ukraine in 2022 caused it to nose-dive again. The pandemic resulted in some of the most considerable reductions in trade volumes since the Second World War (OECD, 2022[13]). The decline in international trade in the post-pandemic period was similar to the 2008 global financial crisis. Air freight volumes in April 2020 fell by 53% in European Union countries and 3% in the United States, compared to the pre-financial crisis peak of June 2008 (ITF, 2020[14]).

With lockdown measures and restrictions on movement, travel was one of the worst-hit sectors of the economy. While the initial decline in trade was comparable to that due to the 2008 global financial crisis, it was able to make a V-shaped recovery by 2021. ITF data (ITF, 2022[15]) shows that sea- and air-freight volumes had fully recovered by the third quarter of 2021. Figure 1.1 and Figure 1.2 capture the recovery in air and sea trade volumes for the EU and the United States by 2021.

Source: ITF (2022[15]).

Source: ITF (2022[15]).

However, trade gaps for different commodities closed unevenly throughout 2021. Global value chains rely immensely on international container shipping, which continued its recovery in 2021. The pandemic has also had an uneven impact on trade across countries. While exports fell at a similar rate in 2020 across most countries, the recovery was much more varied. Exports from more developed economies recovered much faster than those from less-developed economies (ITF, 2022[15]).

Increased Covid-19 cases due to the Omicron variant in late 2021 and the war in Ukraine in early 2022 brought this recovery to a halt. Trade flows from Europe to Brazil, Russia, India, China and South Africa (the BRICS countries), and Asian countries, fell significantly at the beginning of the war in February 2022. For the EU, exports by sea were 5% lower and imports were 7% higher in May 2022 than in February 2020. Global air trade also began to stagnate by the last quarter of 2021 (ITF, 2022[15]).

By May 2022, imports by the EU were just 2% above February 2020 levels, reflecting a poor performance compared to 2021 (ITF, 2022[15]). In May 2022, the EU’s exports by sea to BRICS and Asian countries were 19% and 16% lower, respectively, while imports did not change drastically. As expected, the EU’s air-trade flows with the BRICS and Asian countries contracted significantly.

Covid-19 has changed trade and transport policy

Authorities and businesses implemented measures to soften Covid-19’s impact, some of which have since become standard policies. For example, higher levels of trade regionalisation have occurred since the Covid-19 pandemic. This trend has brought out the relative advantage of shorter, more resilient supply chains. According to the World Economic Forum (WEF), in the five years before the pandemic, the average trade-weighted distance had been falling and was at its lowest in 2019 since the 2008 global financial crisis (Legge and Lukaszuk, 2021[16]).

In conjunction with this increasing regionalisation, the pandemic exposed the fragility of the global supply chains and showed their susceptibility to disruptions. As soon as borders closed, global and multi-country supply chains broke down. In response, policy makers began to emphasise implementing policies that increase resilience to future emergencies.

The pandemic also highlighted the importance of multilateralism and international co-operation. Regionalisation has again gained traction in the post-pandemic world as a way to safeguard supply chains against future crises. Long-term considerations around investment drivers and determinants are becoming a standard part of ensuring resilience in supply chains (UNCTAD, 2022[17]). Based on these observations, the ITF Transport Outlook 2023 assumes a higher degree of trade regionalisation than the previous edition.

The Covid-19 lockdowns brought about a revival of walking and cycling in cities, facilitated by supporting measures by city authorities. Measures to promote active mobility in cities during the pandemic have also become part of long-term strategic plans. Examples of such actions include removing parking lanes to make way for walking and cycling paths; enlarging footpaths; allowing cyclists to use bus lanes; and speed-limit reductions for shared lanes (UITP, 2020[18]).

A total of 1 800 cities worldwide have taken action to promote non-motorised transport since the start of the pandemic (Goetsch and Peralta Quiros, 2020[19]). Several cities have since also introduced car-free days, in addition to restricting vehicles in certain zones to reduce motorisation (Shah, Jaya and Piludaria, 2022[20]). The Shifting Streets COVID-19 Mobility Dataset catalogues government responses from over 500 cities that have directly influenced walking, cycling and other non-motorised transport modes (Combs and Pardo, 2021[21]).

Several long-term changes in mobility patterns present opportunities for decarbonisation that policy makers must channel towards the transport sector's green transition. During the pandemic, virtual mobility increased due to the increase in online activities such as teleconferencing, online learning, teleworking and online shopping (de Palma, Vosough and Liao, 2022[22]). Out of these, teleworking is another trend that has continued significantly in several regions even after the lifting of Covid-19-related restrictions (ITF, 2023[8]).

The pandemic also reinforced the pre-existing surge in e-commerce sales. According to the UN Conference on Trade and Development (2022[23]), the rise in e-commerce activity prompted by the Covid-19 pandemic continued in 2021, even though many countries had already started easing restrictions. The highest increases in e-commerce sales have occurred in developing countries. In the United Arab Emirates, the percentage of Internet users who shopped online rose from 27% in 2019 to 63% in 2020. The share also tripled in countries such as Bahrain and Uzbekistan. Greece saw the highest increase (18%) among the developed countries, followed by Hungary, Ireland and Romania, each of which saw a rise of 15% (UNCTAD, 2022[23]).

The ITF Transport Outlook 2023 assumes that e-commerce activity will continue to grow moderately and reach one-quarter of global retail sales in 2025. More e-commerce activities lead to a rise in freight transport demand, which is linked to increased emissions and congestion in the absence of measures to decarbonise freight activity.

As with the Covid-19 pandemic, the ongoing war in Ukraine has prompted changes in policy responses and disrupted the global economy. The impacts of the war can be seen in the form of economic and human repercussions, including the displacement of millions of people. The war has unleashed a humanitarian crisis in Ukraine, adding to the already record-high global refugee levels (World Bank, 2022[24]) and putting immense pressure on global geopolitical relations.

The war has contributed to a worsening global economy, mainly through further disruption to supply chains, commodity markets and energy prices (World Bank, 2022[25]). Its repercussions point towards a global growth slowdown, rising inflation and increased poverty levels (World Bank, 2022[24]). While the immediate impact, outside of Ukraine, is felt in Europe, the war’s effects extend worldwide. The UN Global Crisis Response Group estimates that 1.6 billion people in 94 countries face the combined threat of a cost-of-living crisis, food shortages, energy poverty, and social unrest (UN, 2022[26]). This could create considerable challenges for implementing environmental goals. The ITF Transport Outlook 2023 considers the current and expected impacts of the war to the extent possible.

Turmoil in energy markets could impact decarbonisation

The war in Ukraine has exacerbated weaknesses in international energy supply chains that had not yet fully recovered from the shocks of the pandemic. The International Energy Agency (IEA) has described the current context as “full-blown energy turmoil”, primarily due to Russia’s position before the war in Ukraine as the world’s largest exporter of fossil fuels. The reduction of supply to Europe and the imposition of sanctions in the region “are severing one of the main arteries of global energy trade” (IEA, 2022[27]).

The ongoing war also influences climate policy worldwide, as energy security has become a top priority for many countries. The impacts of the war on the global energy market have prompted some countries to revise their energy policies – for example, by delaying previous ambitions to phase out fossil fuels (Ember, 2022[28]). Continued dependence on fossil fuels could result in postponed climate action.

Many countries dependent on Russian fossil-based energy do not have formal plans to accelerate clean energy investment or identify alternative energy sources. However, some countries and regional blocs have taken action to simultaneously mitigate the risks of the energy crisis and push for their climate targets (Beyer and Molnar, 2022[29]).

For example, in May 2022 the European Commission published its REPowerEU plan, which aims to phase out Russian fossil fuels by 2027 and boost renewable energy production and energy efficiency measures in the EU (EC, 2022[30]). In July 2022, the EU also agreed on its Winter Plan, a political agreement on a voluntary 15% reduction in natural gas demand during the northern winter of 2022-23, compared to average consumption in the last five years (Council of the European Union, 2022[31]).

Rising energy prices will also significantly impact emerging economies, which could shift their focus towards achieving a stable energy supply at the cost of a green energy transition (Zhang, 2022[32]). It will therefore be necessary to combine reductions in fossil-fuel dependency with energy security planning in order to continue advancing the decarbonisation of transport. Reducing dependence on fossil energy will require focused and sustained policy measures across sectors, combined with international dialogue and co-operation on energy security.

Economic uncertainties resulting from the war also impact the transport sector

Ukraine’s economy is currently experiencing severe distress. It is estimated that by mid-2022 the damage to the country’s infrastructure, housing and non-residential buildings was over USD 100 billion, with widespread destruction of houses, roads and railways, agricultural land and other productive capacities (Kyiv School of Economics, 2022[33]). The EU will likely feel the most significant impacts outside of Ukraine. This is due to its close economic ties with both Russia and Ukraine. The World Bank (2022[24]) forecasts a contraction of 0.2% in the output in the Europe and Central Asia region in 2022.

The war in Ukraine is a significant contributor to the slowing of global economic growth. This is due primarily to the impacts of rising energy prices and reduced energy supply on a global economy that has not yet fully recovered from the repercussions of the pandemic (IEA, 2022[27]; World Bank, 2022[25]; IMF, 2022[34]; UN, 2022[35]). Indeed, while the OECD (2022[36]) projects a brief improvement in economic activity in the aftermath of the pandemic, global output growth will remain muted in 2022 and slow down further to 2.2% in 2023. Inflation has also surged worldwide, backed by rising commodity prices and continued supply-chain disruptions.

The Covid-19 pandemic had a dramatic impact on transport. Travel restrictions forced many airlines to leave their aircraft idled. Road transport relies heavily on human resources at various stages and has therefore been hampered due to the pandemic. With the gradual easing of sanitary measures and travel restrictions, air-passenger traffic levels started to return to normal. However, disruptions to global supply chains before the war in Ukraine continued to impact the global transport sector.

In 2021, international air passenger traffic between Russia and the rest of the world accounted for 5.2% of global international traffic. In the same year, 5.7% of all European air traffic travelled to or from Russia, while a further 3.3% travelled to or from Ukraine (IATA, 2022[37]). By March 2022, 36 countries had closed their airspace to Russian airlines. Russia, in turn, banned airlines in most of those countries from entering or flying over its airspace. Several airlines belonging to countries not impacted by sanctions (e.g. countries in Asia) have also temporarily reduced flights to and from Russia. The war in Ukraine halted 2.4% of total international air passenger traffic compared to 2021 data.

The war in Ukraine has also seriously disrupted the transport of essential products, particularly food and energy. Russia and Ukraine are significant agricultural economies and providers of basic agro-commodities, including wheat, maize and sunflower oil (FAO, 2022[38]). Ukraine also exports raw materials, chemical products and machinery. The EU is Ukraine's leading trading partner, accounting for over 40% of Ukraine’s trade in 2019 (EC, 2022[39]). Ukraine ships its highest freight volumes by sea but carries out its freight activities via all modes.

The war in Ukraine is expected to have a lasting impact on global trade. The imposition of sanctions due to the war has led to trade and supply chain disruptions. These disruptions are expected to hamper the global value chains that rely on commodity inputs from Russia. They will primarily affect regional economies that are big importers of these inputs (World Bank, 2022[24]). Countries in Central Asia are highly exposed to risks from supply chain disruptions, with transit on main freight corridors in the region being restricted (ITF, 2022[40]).

The war in Ukraine dampened the global trade recovery of the preceding year. The combined effect of border closures, trade restrictions and increased fuel costs has caused trade patterns and volumes to change significantly. The World Trade Organization (WTO) made a downward revision to expected growth in merchandise trade volumes, from 4.7% to 3% in 2022 and 3.4% in 2023 (WTO, 2022[41]). Some regions will be more acutely affected by the war than others.

Russia and Ukraine are significant actors in the agri-food sectors, accounting for 53% of global trade in sunflower oil and seeds and 27% in wheat (UNCTAD, 2022[42]). The disruption in trade will likely impact Africa and the Middle East the most since they import more than 50% of their cereals from the two countries (WTO, 2022[43]). The price increase is expected to strain low-income net food-importing countries in particular.

High energy prices will further exacerbate the increase in food prices and will also raise the cost of transport. Table 1.1 provides an overview of the WTO’s annual merchandise trade volumes since 2018 and projections for 2022 and 2023. In 2021, all regions saw a sharp recovery from a slump in trade due to the pandemic. They will have muted growth in 2022 and 2023.

The OECD’s (2022[36]) projections suggest that inflation in most countries will have peaked in the third quarter of 2022 and will start declining by the end of the year into 2023. All major commodity markets have experienced the inflationary shock, pointing towards broad-based inflation. This has prompted central banks to respond with tighter monetary policy to bring it back under the target levels. Inflation has become widespread across the world’s regions but to varying extents.

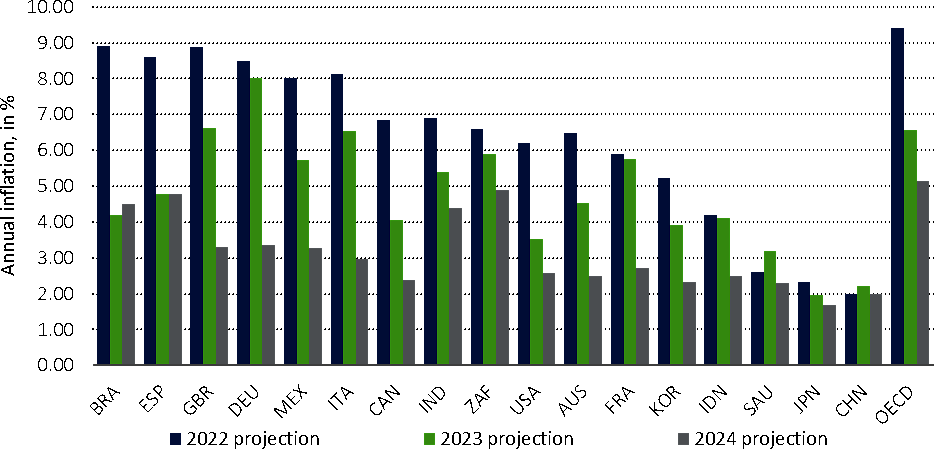

According to OECD estimates, annual inflation in the OECD countries is projected at 6.6% in 2023, falling from 9.4% in 2022 (OECD, 2022[44]). This rate is expected to fall further to 5.1% in 2024. The United Kingdom experienced annual inflation of 8.9% in 2022, up from 2.6% in 2021, one of the steepest hikes in Europe (OECD, 2022[36]). Türkiye’s annual inflation rate was 73.2% in 2022, the highest in the last two decades (World Bank, 2022[45]). China's inflation will remain low and stable, while India is expected to continue experiencing its usual rate of 5-6% in 2023.

The hike in food prices will likely exacerbate income inequality as inflation impacts lower-income households the hardest due to their high share of expenditure on food and fuel (Laborde Debucquet, Lakatos and Martin, 2019[46]). Driven by tight monetary policy and a slowdown in global demand, inflation will likely fall in 2023 but remain above the target levels in many countries. Figure 1.3 shows the projections for annual inflation in 2022, 2023 and 2024. China and Saudi Arabia are the only countries where inflation is expected to be higher in 2023 than in 2022.

Notes: BRA: Brazil. ESP: Spain. GBR: United Kingdom. DEU: Germany. MEX: Mexico. ITA: Italy. CAN: Canada. IND: India. ZAF: South Africa. USA: United States. AUS: Australia. FRA: France. KOR: Korea. IDN: Indonesia. SAU: Saudi Arabia. JPN: Japan. CHN: China. OECD: OECD member countries.

Source: OECD Economic Outlook database (2022[47]).

Oil prices had been rising before the war. These rises were fuelled by a combination of the bounce back in global demand and supply uncertainties regarding production by the Organization of the Petroleum Exporting Countries plus closely affiliated non-members (OPEC+) falling short of expectations (IEA, 2022[48]). The war in Ukraine prompted several countries to announce a ban on Russian oil. The EU also embargoed Russian crude oil, starting in December 2022. Prices have since eased slightly with co-ordinated stock releases by the United States and IEA member countries (IEA, 2022[49]). The energy price volatility will likely continue into 2023 (World Bank, 2022[50]).

Energy prices have significant impacts on the transport sector. Fluctuations in oil prices affect the cost of transport, usage levels and behaviours and investment in renewable energy. Higher crude oil prices translate into a higher retail price of transport fuel relatively quickly. This increases the overall cost of transport activity, especially freight activity, due to higher container freight rates. The higher prices across markets can also strain the automotive sector due to shortages and high prices for the raw materials of most vehicle batteries, such as lithium and cobalt (Coface, 2022[51]).

The steep rise in energy prices could also directly affect the rail freight market in the EU. The European Rail Freight Association anticipates that rail freight operators not purchasing enough energy for 2022 and 2023 will face significantly higher prices in future purchases. The cost could be passed on to consumers, or the operators could even be forced to leave the market, posing a threat to the progress made in the freight modal shift (ERFA, 2022[52]).

High and volatile energy prices also temporarily increase the risk of shifting investments towards extractive industries and fossil energy. Several countries have already made plans to expand fossil gas production and infrastructure. It is essential for policy makers to mitigate this risk by deploying more renewables. This would help accelerate the clean energy transition and improve the energy security of countries dependent on Russia’s fossil energy. Several countries have recognised this risk and implemented measures to combat it. As noted in the World Energy Outlook 2020 (IEA, 2020[53]), policy responses to the energy crisis are pushing renewable energy investments faster than before, accelerating the green transition.

The EU and the United Kingdom have announced plans to boost the deployment of renewable energy (Climate Action Tracker, 2022[54]). The EC's REPowerEU plan proposes to update the renewable energy target from 40% to 45% in the overall energy mix by 2030 (EC, 2022[30]). The plan also includes measures to ramp up the production of green hydrogen in the EU. Meanwhile, Germany, New Zealand, Ireland, Italy and some states in the United States have temporarily reduced public transport fares to discourage private vehicle usage and temper fuel demand (Archie, 2022[55]; Euronews.green, 2022[56]; NZ Herald, 2022[57]).

Population growth and worldwide economic growth will put greater pressure on transport policy makers to meet subsequent rises in transport demand. Changes in these drivers are bound to influence transport planning and investment decisions in the coming years. Governments must address the twin challenge of catering to increases in demand and meeting the transport sector's emission-reduction goals.

A growing population means growth in transport demand

The UN Department of Economic and Social Affairs (UN DESA) projects (2022[58]) that the world population will reach 9.7 billion by 2050 and 10.4 billion by 2100, up from 8 billion in 2022. This increase will be driven by falling mortality rates, the relatively youthful structure of the current population and sustained global fertility rates. A rapidly rising population implies the need for increased travel. Governments will have to ensure that this rise in travel demand is met in an equitable and environmentally friendly manner.

A growing majority of the population lives in urban areas globally. By 2050, an additional 2.5 billion people will live in urban areas, with Africa and Asia accounting for about 90% of this increase (UNDESA, 2019[59]). Urbanisation can also lead to urban sprawl, which has implications for increased land use and car dependency (ITF, 2022[60]). As urbanisation increases, the number of more populous cities also increases. In 2018, there were 33 cities with over 10 million inhabitants (so-called megacities) worldwide. By 2030, there will be 43 megacities, primarily in developing regions (UNDESA, 2019[59]). This will put pressure on policy makers to ensure the integration of transport and land-use policies that enhance access to sustainable transport in and around cities.

Over the next three decades, the population distribution of the world’s regions will change significantly, and this will further impact the type and distribution of transport demand. UN DESA (2022[58]) projects that more than half of the projected rise in global population up to 2050 will be from eight countries: the Democratic Republic of the Congo, Egypt, Ethiopia, India, Nigeria, Pakistan, the Philippines and the United Republic of Tanzania. During the same period, 61 countries are likely to experience a population decline of 1% or more during the same period. Bulgaria, Latvia, Lithuania, Serbia and Ukraine are expected to experience some of the most prominent relative falls in population by 2050, each with a decline of 20% or more, compared to 2022. An absolute population decline is also expected in China in 2023.

The age distribution of a population also impacts transport policy decisions. Countries with increasingly ageing populations must adapt their transport systems to address their needs. At the same time, countries with an increasing working-age population will have to cater to growing travel demand. In 2050, the global population aged 65 years or above will rise to 16%, up from 10% in 2022. Using UN DESA’s regional classifications (2022[58]), by 2050, the regions with the highest percentage of the population aged 65 years or over will be Europe and North America (27%) and East and South-eastern Asia (26%). This will also pressure countries with a higher proportion of aged populations to adopt policies that enhance the sustainability of social security and pension schemes.

Growth in demand for transport goes hand in hand with economic growth

In most parts of the world, there is a close relationship between GDP and demand for freight and passenger transport. Despite the prevailing uncertainty in the current economic climate, economic growth is projected to persist in the long term. Therefore, long-term transport demand is expected to rise simultaneously with economic growth in the coming years.

Before the war in Ukraine, the OECD estimated that economic recovery from Covid-19 would continue in 2022 and 2023 (OECD, 2022[10]). Continued global vaccination efforts, supportive macroeconomic measures in major economies, and favourable financial conditions would aid this recovery. However, the war hindered global growth and aggravated inflationary pressures. This generated a new negative supply shock for the global economy, just as the supply-chain challenges due to the pandemic appeared to be fading.

Due to its dependence on Russian oil and natural gas, the EU appears to be highly exposed to the economic impacts of the war in Ukraine. There is no likely short- to medium-term substitute for Russia’s natural gas supply to Europe, and current price levels will adversely affect inflation. While some countries are more reliant than others on natural gas from Russia, the trade interdependence of Eurozone countries points to a general slowdown (Coface, 2022[51]).

According to the OECD (2022[36]), growth remained muted in the second half of 2022 before dropping further in 2023 to a growth rate of 2.2% annually. Compared to OECD forecasts from December 2021, global GDP will fall by USD 2.8 trillion in 2023. The OECD projects slow GDP growth in most G20 economies in 2022 and 2023. In Europe, there is likely to be marginal growth (0.3%) in 2023.

Within the EU, Germany and Italy are expected to have negative growth in 2023. The United States is expected to grow but at only 0.5% in 2023. Similarly, Argentina and Brazil will grow by 0.4% and 0.85, respectively. China, India, Indonesia and Saudi Arabia are relatively less affected, with growth rates of between 4.7% and 6% in 2023. Table 1.2 gives an overview of the GDP growth projections assumed in the ITF’s models for the world’s regions up to 2025.

Globally, the transport sector is not on track to reach its decarbonisation goals. In 2015, parties to the United Nations Framework Convention on Climate Change (UNFCCC) concluded the Paris Agreement, a legally binding treaty to combat greenhouse gas (GHG) emissions. By 2022, 193 countries plus the European Union had ratified it (UN, 2015[61]). Under the agreement, countries have agreed to a goal to limit the increase in global average temperature to well below 2 degrees Celsius (°C) compared to pre-industrial levels, and pursue efforts to limit the temperature increase to 1.5°C.

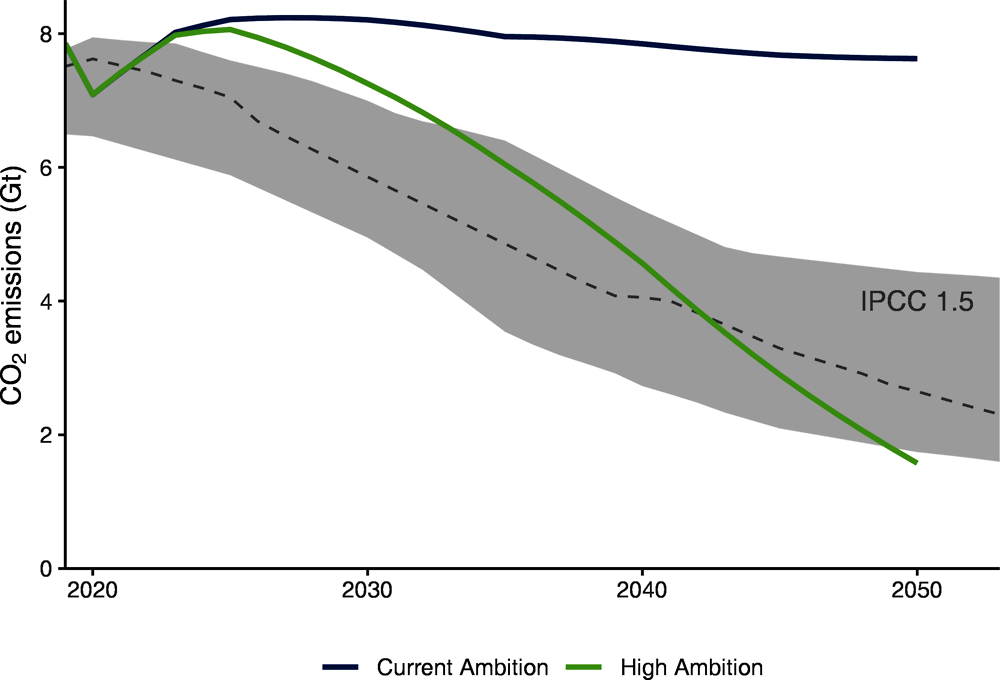

Note: Current Ambition (CA) and High Ambition (HA) refer to the two main policy scenarios modelled, which represent two levels of ambition for decarbonising transport. IPCC 1.5˚C represents the emission levels needed to limit warming to 1.5˚C as introduced by the Intergovernmental Panel on Climate Change. The levels were calculated based on data sourced from the International Assessment Modelling Consortium.

Sources: (IAMC, 2019[62]); IPCC (2018[63]).

To achieve this long-term goal, countries aim to reach global peaking of emissions as soon as possible to achieve a climate-neutral world by mid-century. The agreement also recognises that not all regions can decarbonise at the same rate, citing “equity and common but differentiated responsibilities and respective capabilities, in the light of different national circumstances” as guiding principles (UN, 2015[61]).

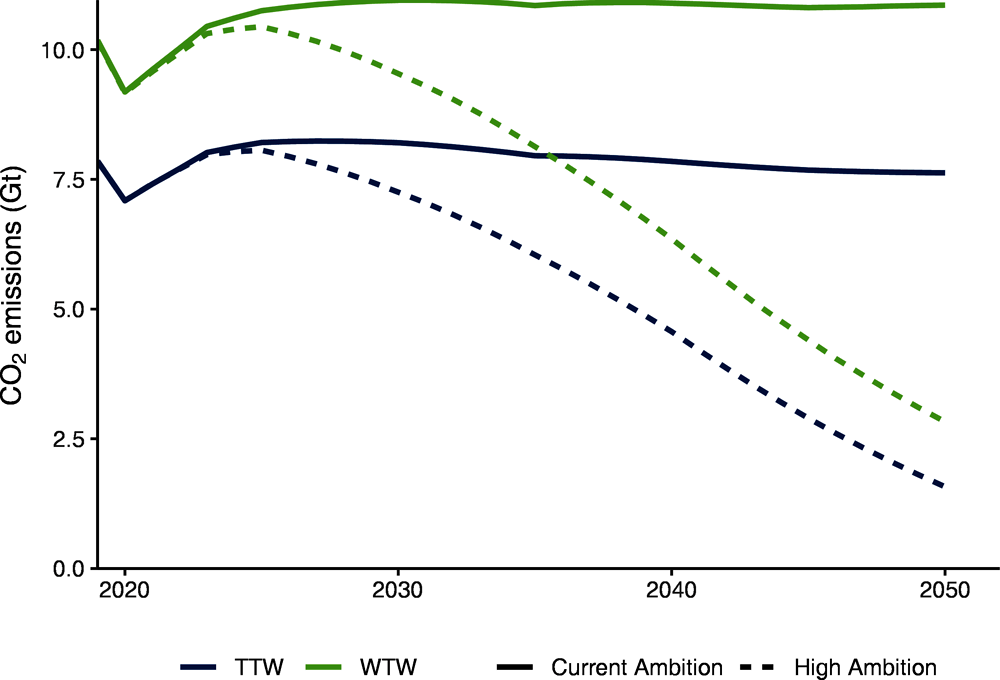

However, as shown in Figure 1.4, based solely on commitments made to date, global transport emissions will not fall fast enough to meet the Paris Agreement goals. In fact, although several regions have taken concrete actions to deliver on their ambitions, continuing along the path will result in a continued rise in the transport sector’s tank-to-wheel (TTW) CO2 emissions during the 2020s, culminating in a slight fall (of 3%) by 2050 (see Box 1.1).

The modelling in this report refers to tank-to-wheel (TTW) emissions, defined as any emissions due solely to the energy used during a trip. However, there are also upstream emissions associated with transport activity. The emissions inherent in the production of the energy or fuel source used in the vehicle fleets are referred to as well-to-tank (WTT) emissions. Well-to-wheel (WTW) emissions include both TTW and WTT emissions and represent the total emissions associated with a vehicle’s activity.

Note: Figure depicts ITF modelled estimates. Current Ambition (CA) and High Ambition (HA) refer to the two main policy scenarios modelled, representing two levels of ambition for decarbonising transport. Tank-to-wheel (TTW) emissions (or tailpipe emissions) are generated from the use of transport vehicles. This excludes well-to-tank emissions, which make up part of the total well-to-wheel (WTW) emission pathway.

As shown in Figure 1.5, global WTW emissions were 30% higher than TTW emissions in 2019. As vehicle fleets become more efficient, WTT emissions will make up a larger share of total transport emissions than TTW emissions. The ITF Transport Outlook focuses on TTW emissions to identify specific policies that will speed up decarbonisation in the transport sector. However, greater collaboration with the energy sector to decarbonise fuel and energy production and distribution remains critical to achieving global climate goals.

Source: ITF (2021[9]).

Intergovernmental Panel on Climate Change (IPCC) estimates provide a sobering benchmark. Restricting the global average temperature increase to 1.5°C will require reducing total transport emissions to just 2-3 gigatonnes by 2050 (IPCC Working Group III, 2022[64]; IPCC Working Group II, 2022[65]). Additionally, the IPCC analysis suggests that transport needs to decarbonise faster than any other sector – a reduction of 70-80% below 2015 amounts – to achieve the necessary levels for the Paris Agreement.

The IEA states that decarbonisation needs to begin immediately, with transport CO2 emissions already needing to fall by 3% per year through to 2030 to achieve Net Zero by 2050 (IEA, 2021[66]). The High Ambition scenario modelled for this edition of the Outlook suggests that the world could reduce its transport emissions by 80% by 2050. Achieving this reduction will require more ambitious policies and faster actions that combine a mixture of mode shift, demand management and vehicle and fuel improvement measures.

International co-operation will be needed to meet ambitious goals

The Paris Agreement includes a mechanism for countries to put forward plans for decarbonising their economies, and how they will play their part in delivering the goals of the agreement, known as Nationally Determined Contributions (NDCs; see Box 1.2). Under the agreement, parties to the UNFCCC were to renew their NDCs in five-year cycles, thereby showing increasing ambition and updated targets over time.

The Conference of the Parties to the UNFCCC held in Glasgow, Scotland, in 2021 (COP26) marked the end of the first five-year cycle of NDCs. ITF analyses of the NDCs submitted at COP26 (ITF, 2018[67]; ITF, 2021[68]) show that a number of countries increased their commitments to transport decarbonisation in time for the conference. Notably, by COP26, the number of countries mentioning transport had “risen by 19 percentage points, those who list measures by 22 percentage points and those setting targets by eight percentage points” compared to countries’ initial NDC submissions (ITF, 2021[68]).

However, at COP26, updates on overall GHG reduction targets were deemed to be insufficient. As a result, the COP26 agreement now requires countries to update their NDCs on an annual basis. In the year following COP26, only 32 parties to the UNFCCC (or 16%) provided updates to their NDCs in time for COP27. Some of these parties had failed to provide updates in time for the previous cycle. The UN notes that countries’ efforts to bend the emissions curve downward are not yet enough to limit the global temperature rise to 1.5°C by the end of the century (IPCC Working Group III, 2022[64]).

The ITF launched its Decarbonising Transport initiative in 2016, shortly after the signing of the Paris Agreement. Since then, the ITF has tracked countries’ submissions to the United Nations Framework Convention on Climate Change (UNFCCC). These submissions, known as Nationally Determined Contributions (NDCs), define countries’ pledges to reduce greenhouse gas emissions. The ITF’s Transport NDC Tracker, available online, provides information on the NDCs’ transport content.

ITF Transport NDC Tracker: https://www.itf-oecd.org/ndc-tracker/en.

The ITF’s Transport Climate Action Directory, launched in 2020, provides policy makers with a tool to identify transport CO2-reduction measures that can translate their decarbonisation ambitions into actions and achieve their climate objectives. The UNFCCC has endorsed the directory as a tool that can help decision makers define measures when revising their NDCs or defining national transport decarbonisation plans.

ITF Transport Climate Action Directory: https://www.itf-oecd.org/tcad.

While transport has been acknowledged in 82% of NDCs, only 18% include a specific emission-reduction target for transport (ITF, 2023[70]). At an international level, governments, businesses and non-governmental organisations have been working to set up processes to support international collaboration to overcome shared challenges and maximise the shared benefits of decarbonising the transport sector.

The UN Climate Change High-Level Champions and the Marrakech Partnership have developed a series of high-level roadmaps (or “Breakthroughs”) for over 30 sectors of the economy and transition goals to be achieved by 2030 to stay on track with the Paris Agreement goals (UNFCCC, 2021[69]).

The 2030 Breakthroughs set ambitious targets for the transport sector, focusing on energy transitions for road transport, aviation and shipping with the aim of creating economies of scale due to the alignment between countries’ domestic policies. These goals focus specifically on technology shifts, rather than efforts to change demand or modal shift. Table 1.3 outlines the 2030 Breakthrough Goals and policy recommendations to move forward in the transportation policy landscape.

Although decarbonisation of the transport sector is an international priority, in many countries, it is only one among many priorities for governments looking to improve their economies and the quality of life of their citizens. For many developing countries, reducing transport emissions must be considered in the context of other strategic priorities. Examples include enhanced connectivity, better road safety (see Box 1.3), improved road networks, digitalisation and provision of public transport and basic transport infrastructure.

Low-carbon transport measures have many potential co-benefits. Crucially, they can help achieve other economic and social objectives – including include enhanced equity and accessibility, improved health and safety, reduced air and noise pollution and reduced congestion – while accelerating the sector’s green transition. Policy makers must aim to maximise opportunities that meet the overall goals of the transport sector while moving to a low-carbon future.

The ITF is also involved in the cross-sectoral Energy Demand changes Induced by Technological and Social innovations (EDITS) project. This project looks at a low energy demand scenario for the future, which incorporates “major lifestyle, behaviour, infrastructure, and business model transformations” to reduce global energy use by 2050, but also improve equity and the outcomes of the Sustainable Development Goals (Grubler et al., 2018[71]).

The United Nations Sustainable Development Goals acknowledge road safety as a prerequisite for sustainable development (UNECE, 2020[72]). Governments have different ways of tackling this challenge. It could entail adapting road infrastructure to technical standards, establishing and applying harmonised standards to vehicle design, designing legislation that addresses road user behaviours, or developing comprehensive support systems for post-crash response (WHO, 2021[73]).

Low- and middle-income countries currently account for most road traffic deaths (WHO, 2021[73]). Consequently, taking action to improve road safety is high on the agenda of these countries. Interventions such as safe interchange designs, limiting central urban road traffic, expanding public transport and paying particular attention to vulnerable groups can deliver road safety goals while improving sustainability outcomes (ARUP, 2020[74]).

Australia, the European Union and New Zealand all have a long-term goal to achieve, to the extent possible, “Vision Zero”, which aims to eliminate all traffic fatalities and severe injuries, while increasing safe, healthy and equitable mobility for all (Action Vision Zero, n.d.[75]; CINEA, 2022[76]).

Increased regional connectivity enhances resilience and well-functioning markets

Increased regional connectivity helps advance economic development and boost supply chain resiliency (ESCAP, 2020[77]). Increasing connectivity through enhanced road and railways network is one of the most common priorities across different regions. New investments in expressways projects and rail corridors have continued after the pandemic.

A number of Latin American countries, including Argentina, Brazil, Colombia and Mexico, have earmarked funds for the rehabilitation of rail networks and the construction of new roads and highways (Ministry of Transport of Argentina, 2020[78]; Woof, 2020[79]; Government of Mexico, 2018[80]; Oxford Business Group, 2017[81]).

Several countries in Asia, including Bangladesh, Cambodia, India, Malaysia, Nepal, the Philippines and Viet Nam, currently have major connectivity projects in the works (ITF, 2022[82]; ITF, 2022[83]). In Asia, these projects often aim to improve connectivity to regions and remote areas within the countries and boost regional connectivity.

Improved connectivity is one of the top priorities for North and Central Asia countries. Almost all countries in the region are workings towards enhancing their road and rail network. These developments are prompted by the need to facilitate the movement of people and increase trade flows (ITF, 2022[84]). If such Infrastructure investments are green, it mitigates the risk of locking in emissions through carbon-intensive infrastructure. It will be necessary for policy makers to ensure that these priorities are met in a way that is aligned with the environmental goals of the sector globally.

The EU also stresses enhancing the interoperability of the national rail systems to strengthen connectivity (Council of the European Union, 2021[85]). Its Trans-European Transport Network (TENT-T) aims to establish a comprehensive, reliable and seamless network that provides sustainable connectivity throughout the region (EC, 2021[86]). The United States has also made significant investments. Its Inflation Reduction Act has led to substantial investment in freight and passenger rail connectivity and the road network (CleanEnergy.gov, 2022[87]; US Federal Railroad Administration, 2022[88]).

Trade corridors feature relatively highly in the list of priorities for many countries. The importance of seamless regional trade facilitation for economic development drives this prioritisation. Many countries in Africa, Asia, Europe and Latin America are investing significantly in trade and economic corridor projects to improve freight flows and reduce trade costs (ADB, 2019[89]; ITF, 2022[83]; ITF, 2022[82]; EC, 2013[90]; Oxford Business Group, 2022[91]). These projects aim to overcome infrastructure bottlenecks through high-capacity transport systems, especially in the aftermath of the Covid-19 pandemic. Given the environmental goals of the transport sector, any development of these corridors must have sustainability at its core.

Electrification and rail modernisation as a decarbonisation strategy has remained a priority in several regions. Several countries have also earmarked funding for it and the extension of networks (IEA, 2022[92]). This includes establishing high-speed rail links, modernising tracks, and upgrading and digitalising passenger and freight rail network signalling systems. All of these measures improve efficiency and reduce CO2 emissions from the sector.

China, the EU, India and the United States have targeted funding towards the electrification of existing networks (IEA, 2022[92]; The White House, 2021[93]). A significant share of high-speed rail tracks for passenger travel also exists in China, Japan, Korea and the EU (IEA, 2019[94]). Some significant high-speed rail development projects are underway in Australia, China and India.

Seamless multimodal connectivity helps improve operational efficiency and reduces emissions. Improved logistics and upgrading multimodal hubs are other trends common to many countries. Several developing and emerging economies face high logistical costs due to inefficient transport and inventory management. Investment in integration and optimisation of operations throughout the logistics chain through improved warehousing and storage and digitalisation of processes is a priority for many emerging economies.

Countries in Africa and Asia perceive multimodal connectivity as a crucial element for supply chain efficiency and reduced costs (Okyere et al., 2019[95]; ITF, 2022[82]; ITF, 2022[83]). Strengthening inter-modal and multimodal transport also improves accessibility and connectivity, and is a prerequisite to shifting the transport demand towards cleaner modes.

Improved public, shared and active transport services will accelerate decarbonisation

With rapid urbanisation and the continued increase in demand for both passenger and freight transport, governments also have the pressure of increasing investment in urban transport infrastructure to meet this growing demand. Expanding urban areas, especially in developing and emerging economies, necessitate the construction of urban road networks, transit systems and transport terminals.

Cities worldwide are seeking to adapt to the increase in demand for transport sustainably. Examples include efforts to create bus rapid transit (BRT) corridors, light rail transit, and expansion and electrification of public transport fleets. Integrated land-use planning and planning for transit-oriented development also help ensure that the increased demand is met while improving access and sustainability of urban mobility.

An integrated, connected and inclusive active-transport system contributes significantly to a clean mobility vision. Besides improved public transport alternatives, enhancing the infrastructure for active mobility is a priority for many European countries and some countries in Asia and Latin America (European Parliament, 2020[96]; UITP, 2020[18]). The focus in these countries has been the improvement of active mobility options through enhanced cycling and walking infrastructure and the reallocation of urban space.

Finally, low-carbon solutions remain on transport ministries’ global agendas. Examples of these solutions include electrification and encouraging the switch to cleaner fuels to reduce the sector’s climate impact. Since the transport sector is a driver of economic growth and social inclusion, for several countries, the priority remains towards ensuring that it contributes to these outcomes. However, being a high-emitting sector, it will be essential to ensure that it plays its role in climate change mitigation and adaptation.

Developing and emerging economies face the dual challenge of providing equitable access to affordable mobility and improved freight flows while minimising their carbon footprints. Achieving the sustainability goals of the transport sector necessitates bearing in mind the entire scope of outcomes throughout the different stages of planning, designing and delivering projects and programmes. Investments in solutions such as cleaner technologies and fuels, high-quality public transport fleets, well-planned and connected cities, and widely available active mobility options can help achieve transport ministries’ development goals and simultaneously fulfil their climate targets.

The transport sector’s recovery following the pandemic has been faster than expected but significant challenges remain.

Turmoil in energy markets and cost-of-living crises complicate efforts to decarbonise transport.

Despite some progress, transport emissions will not fall fast enough in the coming years to meet international climate objectives.

Mechanisms exist to advance decarbonisation goals but they need to become more ambitious.

Governments face the challenge of balancing multiple priorities while meeting climate commitments.

References

[75] Action Vision Zero (n.d.), Vision Zero - A history, https://actionvisionzero.org/resources/vision-zero-a-brief-history/ (accessed on 30 November 2022).

[89] ADB (2019), Cross-Border Road Corridors: The quest to integrate Africa, African Development Bank, Abidjan, https://www.afdb.org/en/documents/document/cross-border-road-corridors-109949.

[55] Archie, A. (2022), “California’s governor is proposing $11 billion of relief from record gas prices”, NPR, https://text.npr.org/1088711551.

[74] ARUP (2020), The sustainable route to improving road safety, https://www.arup.com/perspectives/the-sustainable-route-to-improving-road-safety (accessed on 6 November 2022).

[29] Beyer, S. and G. Molnar (2022), “Accelerating energy diversification in Central and Eastern Europe”, IEA Commentary, https://www.iea.org/commentaries/accelerating-energy-diversification-in-central-and-eastern-europe.

[76] CINEA (2022), EU Road Safety: Towards “Vision Zero”, European Climate, Infrastructure and Environment Executive Agency, https://doi.org/10.2840/701809.

[87] CleanEnergy.gov (2022), “Building a Clean Energy Economy: A guidebook to the Inflation Reduction Act’s investments in clean energy and climate action”, The White House, Washington, DC, https://www.whitehouse.gov/cleanenergy/inflation-reduction-act-guidebook.

[54] Climate Action Tracker (2022), “Global reaction to energy crisis risks zero carbon transition”, https://climateactiontracker.org/publications/global-reaction-to-energy-crisis-risks-zero-carbon-transition/.

[51] Coface (2022), “Economic consequences of the Russia-Ukraine conflict: Stagflation ahead”, https://www.coface.com/News-Publications/News/Economic-consequences-of-the-Russia-Ukraine-conflict-Stagflation-ahead.

[21] Combs, T. and C. Pardo (2021), “Shifting streets COVID-19 mobility data: Findings from a global dataset and a research agenda for transport planning and policy”, Transportation Research Interdisciplinary Perspectives, Vol. 9, https://doi.org/10.1016/j.trip.2021.100322.

[31] Council of the European Union (2022), “Member states commit to reducing gas demand by 15% next winter”, https://www.consilium.europa.eu/en/press/press-releases/2022/07/26/member-states-commit-to-reducing-gas-demand-by-15-next-winter/.

[85] Council of the European Union (2021), Council conclusions on “Putting Rail at the Forefront of Smart and Sustainable Mobility”, Council of the European Union, Brussels, https://data.consilium.europa.eu/doc/document/ST-8790-2021-INIT/en/pdf.

[22] de Palma, A., S. Vosough and F. Liao (2022), “An overview of effects of COVID-19 on mobility and lifestyle: 18 months since the outbreak”, Transportation Research Part A: Policy and Practice, Vol. 159, pp. 372-397, https://doi.org/10.1016/j.tra.2022.03.024.

[39] EC (2022), “EU trade relations with Ukraine: Facts, figures and latest developments”, https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/ukraine_en.

[30] EC (2022), “REPowerEU: A plan to rapidly reduce dependence on Russian fossil fuels and fast forward the green transition”, https://ec.europa.eu/commission/presscorner/detail/en/IP_22_3131.

[86] EC (2021), “Questions and Answers: The revision of the TEN-T Regulation”, https://ec.europa.eu/commission/presscorner/detail/en/qanda_21_6725 (accessed on 30 November 2021).

[90] EC (2013), “Union guidelines for the development of the Trans-European transport network”, Journal of the European Union, Vol. L 348/1, https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32013R1315&from=EN (accessed on 6 November 2022).

[28] Ember (2022), “Coal is not making a comeback: Europe plans limited increase”, https://ember-climate.org/insights/research/coal-is-not-making-a-comeback/.

[52] ERFA (2022), “High energy prices could reverse intermodal shift, says ERFA”, https://erfarail.eu/news/press-release-development-of-energy-prices-threaten-competitive-rail-freight-market.

[77] ESCAP (2020), Connecting transport infrastructure networks in Asia and Europe in support of interregional sustainable transport connectivity: Progress in enhancing transport connectivity between Asia and Europe, UN Economic and Social Commission for Asia and the Pacific, Bangkok, https://hdl.handle.net/20.500.12870/276.

[56] Euronews.green (2022), “Cost of living crisis: Italy, Germany and Ireland are the first to cut public transport prices”, https://www.euronews.com/green/2022/05/11/cost-of-living-crisis-italy-germany-and-ireland-are-the-first-to-cut-public-transport-pric.

[96] European Parliament (2020), COVID-19 and urban mobility: impacts and perspectives, https://www.europarl.europa.eu/RegData/etudes/IDAN/2020/652213/IPOL_IDA(2020)652213_EN.pdf.

[38] FAO (2022), “Information Note: The importance of Ukraine and the Russian Federation for global agricultural markets and the risks associated with the current conflict”, https://www.fao.org/fileadmin/user_upload/faoweb/2022/Info-Note-Ukraine-Russian-Federation.pdf%0A.

[19] Goetsch, H. and T. Peralta Quiros (2020), “COVID-19 creates new momentum for cycling and walking. We can’t let it go to waste!”, World Bank: Transport For Development Blog, https://blogs.worldbank.org/transport/covid-19-creates-new-momentum-cycling-and-walking-we-cant-let-it-go-waste.

[80] Government of Mexico (2018), Programa Nacional de Infraestructura Carretera 2018-2024 [National Road Infrastructure Programme 2018-2024], https://www.gob.mx/sct/articulos/programa-nacional-de-infraestructura-carretera-2018-2024-185945?idiom=es (accessed on 3 November 2022).

[71] Grubler, A. et al. (2018), “A low energy demand scenario for meeting the 1.5 °C target and sustainable development goals without negative emission technologies”, Nature Energy, Vol. 3, pp. 515-527, https://doi.org/10.1038/s41560-018-0172-6.

[62] IAMC (2019), IAMC 1.5°C Scenario Explorer hosted by IIASA, https://data.ene.iiasa.ac.at/iamc-1.5c-explorer/.

[37] IATA (2022), “IATA Factsheet: The impact of the war in Ukraine on the aviation industry”, https://www.iata.org/en/iata-repository/publications/economic-reports/the-impact-of-the-conflict-between-russia-and-ukraine-on-aviation/.

[6] ICAO (2023), Effects of Novel Coronavirus (COVID-19) on Civil Aviation: Economic Impact Analysis, https://www.icao.int/sustainability/Documents/COVID-19/ICAO_Coronavirus_Econ_Impact.pdf (accessed on February 2023).

[49] IEA (2022), Oil Market Report: April 2022, International Energy Agency, Paris, https://www.iea.org/reports/oil-market-report-april-2022.

[48] IEA (2022), Oil Market Report: March 2022, International Energy Agency, Paris, https://www.iea.org/reports/oil-market-report-march-2022.

[92] IEA (2022), “Rail”, https://www.iea.org/reports/rail.

[4] IEA (2022), “Transport”, https://www.iea.org/topics/transport.

[27] IEA (2022), World Energy Outlook 2022, International Energy Agency, Paris, https://www.iea.org/reports/world-energy-outlook-2022.

[66] IEA (2021), Net Zero by 2050: A roadmap for the global energy sector, International Energy Agency, Paris, https://www.iea.org/reports/net-zero-by-2050.

[53] IEA (2020), World Energy Outlook 2020, International Energy Agency, Paris, https://www.iea.org/reports/world-energy-outlook-2020 (accessed on 9 November 2020).

[94] IEA (2019), The Future of Rail: Opportunities for energy and the environment, International Energy Agency, Paris, https://www.iea.org/reports/the-future-of-rail.

[3] IEA (n.d.), Global energy-related CO2 emissions by sector, https://www.iea.org/data-and-statistics/charts/global-energy-related-co2-emissions-by-sector (accessed on 19 April 2023).

[34] IMF (2022), World Economic Outlook: Countering the Cost-of-Living Crisis, https://www.imf.org/en/Publications/WEO/Issues/2022/10/11/world-economic-outlook-october-2022.

[12] IMF (2021), World Economic Outlook: Recovery During a Pandemic, International Monetary Fund, Washington, DC, https://www.imf.org/en/Publications/WEO/Issues/2021/10/12/world-economic-outlook-october-2021.

[63] IPCC (2018), Special report: Global Warming of 1.5 ºC, Intergovernmental Panel on Climate Change, Geneva, https://www.ipcc.ch/sr15/.

[65] IPCC Working Group II (2022), Sixth Assessment Report: Climate Change 2022: Impacts, Adaptation and Vulnerability, Intergovernmental Panel on Climate Change, Geneva, https://www.ipcc.ch/report/ar6/wg2/.

[64] IPCC Working Group III (2022), Climate Change 2022: Mitigation of Climate Change, Intergovernmental Panel on Climate Change, Geneva, https://www.ipcc.ch/report/ar6/wg3/.

[70] ITF (2023), How serious are countries about decarbonising transport?, https://www.itf-oecd.org/ndc-tracker/en (accessed on 1 February 2023).

[8] ITF (2023), Shaping Post-Covid Mobility in Cities: Summary and Conclusions, OECD Publishing, Paris, https://doi.org/10.1787/a8bf0bdb-en.

[84] ITF (2022), ITF North and Central Asia Transport Outlook, OECD Publishing, Paris, https://doi.org/10.1787/f3f64365-en.

[82] ITF (2022), ITF South and Southwest Asia Transport Outlook, OECD Publishing, Paris, https://doi.org/10.1787/ccd79e6d-en.

[83] ITF (2022), ITF Southeast Asia Transport Outlook, OECD Publishing, Paris, https://doi.org/10.1787/cce75f15-en.

[15] ITF (2022), “Trade recovery in 2021 impeded by Omicron virus and Ukraine war”, ITF Statistics Brief, https://www.itf-oecd.org/trade-recovery-omicron-ukraine-war.

[40] ITF (2022), “Transport Connectivity in Central Asia: Strengthening Alternative Trade Corridors between Europe and Asia”, ITF Transport Policy Responses to the War in Ukraine, https://www.itf-oecd.org/transport-connectivity-central-asia.

[60] ITF (2022), Urban Planning and Travel Behaviour: Summary and Conclusions, OECD Publishing, Paris, https://doi.org/10.1787/af8fba1c-en.

[9] ITF (2021), ITF Transport Outlook 2021, OECD Publishing, Paris, https://doi.org/10.1787/16826a30-en.

[68] ITF (2021), Transport CO2 and the Paris Climate Agreement: Where are we six years later?, International Transport Forum, Paris, https://www.itf-oecd.org/sites/default/files/docs/transport-co2-paris-agreement-six-years-later.pdf.

[14] ITF (2020), “Unprecedented Impact of Covid-19 on Freight Volumes in Second Quarter”, ITF Statistics Briefs, https://www.itf-oecd.org/unprecedented-impact-covid-19-freight-volumes-second-quarter.

[67] ITF (2018), Transport CO2 and the Paris Climate Agreement, OECD Publishing, Paris, https://doi.org/10.1787/23513b77-en.

[33] Kyiv School of Economics (2022), “Direct damage caused to Ukraine’s infrastructure during the war has reached over $105.5 billion”, https://kse.ua/about-the-school/news/direct-damage-caused-to-ukraine-s-infrastructure-during-the-war-has-reached-over-105-5-billion/.

[46] Laborde Debucquet, D., C. Lakatos and W. Martin (2019), “Poverty impacts of food price shocks and policies”, in Inflation in Emerging and Developing Economies: Evolution, Drivers and Policies, World Bank, Washington, DC, https://openknowledge.worldbank.org/handle/10986/30657.

[16] Legge, S. and P. Lukaszuk (2021), “Regionalization vs globalization: what is the future direction of trade?”, World Economic Forum: Agenda, https://www.weforum.org/agenda/2021/07/regionalization-globalization-future-direction-trade/.

[78] Ministry of Transport of Argentina (2020), National Transportation Plan: Status and impact on Argentina’s development, Ministerio de Transporte de la República de Argentina, https://ejapo.cancilleria.gob.ar/userfiles/v7/23.National Transport Plan - v7.compressed.pdf.

[57] NZ Herald (2022), “Soaring petrol prices, cost-of-living crisis: Jacinda Ardern’s Govt slashes fuel taxes from midnight; half-price public transport”, https://www.nzherald.co.nz/nz/soaring-petrol-prices-cost-of-living-crisis-jacinda-arderns-govt-slashes-fuel-taxes-from-midnight-half-price-public-transport/K6UFHTBFO55VHOQEDBB3WGDTJE/.

[10] OECD (2022), “GDP Growth: Fourth quarter of 2021, OECD”, https://www.oecd.org/newsroom/gdp-growth-fourth-quarter-2021-oecd.htm.

[13] OECD (2022), “International trade during the COVID-19 pandemic: Big shifts and uncertainty”, OECD Policy Responses to Coronavirus, https://www.oecd.org/coronavirus/policy-responses/international-trade-during-the-covid-19-pandemic-big-shifts-and-uncertainty-d1131663/.

[36] OECD (2022), OECD Economic Outlook, Interim Report September 2022, OECD Publishing, Paris, https://doi.org/10.1787/ae8c39ec-en.

[44] OECD (2022), OECD Economic Outlook, Volume 2022, Issue 2, OECD Publishing, Paris, https://doi.org/10.1787/f6da2159-en.

[47] OECD (2022), OECD Economic Outlook: Statistics and Projections, https://doi.org/10.1787/eo-data-en.

[11] OECD (2021), “News Release: G20 GDP growth, Quarterly National Accounts”, https://www.oecd.org/sdd/na/g20-gdp-growth-Q1-2021.pdf.

[95] Okyere, S. et al. (2019), “Review of sustainable multimodal freight transportation system in African developing countries: Evidence from Ghana”, International Journal of Engineering Research in Africa, Vol. 41, pp. 155-174, https://doi.org/10.4028/www.scientific.net/JERA.41.155.

[91] Oxford Business Group (2022), “Will Latin America’s transport mega-projects revolutionise trade?”, https://oxfordbusinessgroup.com/news/will-latin-america-transport-mega-projects-revolutionise-trade (accessed on 5 November 2022).

[81] Oxford Business Group (2017), “Developing infrastructure and reducing transport costs top priorities for Colombia”, The Report: Colombia 2017, https://oxfordbusinessgroup.com/overview/paving-way-developing-infrastructure-and-reducing-transport-costs-are-top-investment-priorities.

[20] Shah, S., V. Jaya and N. Piludaria (2022), “Key levers to reform non-motorized transport: Lessons from the COVID-19 pandemic”, Transportation Research Record: Journal of the Transportation Research Board, https://doi.org/10.1177/03611981221117538.

[93] The White House (2021), Fact Sheet: The American Jobs Plan, https://www.whitehouse.gov/briefing-room/statements-releases/2021/03/31/fact-sheet-the-american-jobs-plan/ (accessed on 26 October 2022).

[18] UITP (2020), “Mobility post-pandemic: a strategy for healthier cities”, International Association of Public Transport Knowledge Briefs, https://www.uitp.org/publications/mobility-post-pandemic-a-strategy-for-healthier-cities/.

[35] UN (2022), “Global impact of the war in Ukraine: Billions of people face the greatest cost-of-living crisis in a generation”, Global Crisis Response Group Briefs 2, https://unctad.org/publication/global-impact-war-ukraine-billions-people-face-greatest-cost-living-crisis-generation.

[26] UN (2022), “Global Impact of war in Ukraine on food, energy and finance systems”, UN Global Crisis Response Group Briefs 1, https://unctad.org/publication/global-impact-war-ukraine-food-energy-and-finance-systems.

[2] UN (2022), The Sustainable Development Agenda, https://www.un.org/sustainabledevelopment/development-agenda/.

[5] UN (2021), UN Sustainable Transport Conference Fact Sheet: Climate Change, https://www.un.org/sites/un2.un.org/files/media_gstc/FACT_SHEET_Climate_Change.pdf.

[1] UN (2015), Sustainable Development Goals Knowledge Platform: Sustainable Transport, https://sustainabledevelopment.un.org/topics/sustainabletransport.

[61] UN (2015), The Paris Agreement, https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement (accessed on 16 November 2022).

[23] UNCTAD (2022), “COVID-19 boost to e-commerce sustained into 2021, new UNCTAD figures show”, https://unctad.org/news/covid-19-boost-e-commerce-sustained-2021-new-unctad-figures-show.

[17] UNCTAD (2022), Impact of the COVID-19 Pandemic on Trade and Development: Lessons Learned, United Nations Conference on Trade and Development, Geneva, https://unctad.org/publication/impact-covid-19-pandemic-trade-and-development-lessons-learned.

[42] UNCTAD (2022), “Ukraine war’s impact on trade and development”, https://unctad.org/news/ukraine-wars-impact-trade-and-development.

[58] UNDESA (2022), “2022 Revision of World Population Prospects”, https://population.un.org/wpp/.

[59] UNDESA (2019), World Urbanization Prospects 2018: Highlights, United Nations Department of Economic and Social Affairs, Population Division, New York, https://digitallibrary.un.org/record/3828520?ln=en.

[72] UNECE (2020), Road Safety for All, United Nations Economic Commission for Europe, Geneva, https://unece.org/transport/publications/road-safety-all-0.

[69] UNFCCC (2021), Upgrading Our Systems Together: A global challenge to accelerate sector breakthroughs for COP26 - and beyond, https://racetozero.unfccc.int/wp-content/uploads/2021/09/2030-breakthroughs-upgrading-our-systems-together.pdf.

[88] US Federal Railroad Administration (2022), Biden Administration Announces Over $368 Million in Grants to Improve Rail Infrastructure, Enhance and Strengthen Supply Chains, https://railroads.dot.gov/newsroom/press-releases/biden-administration-announces-over-368-million-grants-improve-rail-0 (accessed on 5 May 2023).

[73] WHO (2021), Global Plan for the Decade of Action for Road Safety 2021-2030, World Health Organization, Geneva, https://www.who.int/publications/m/item/global-plan-for-the-decade-of-action-for-road-safety-2021-2030.

[79] Woof, M. (2020), “Brazilian transport infrastructure development plans”, World Highways, https://www.worldhighways.com/wh10/news/brazilian-transport-infrastructure-development-plans (accessed on 3 November 2022).

[50] World Bank (2022), Energy Crisis: Protecting Economies and Enhancing Energy Security in Europe and Central Asia, World Bank, Washington, DC, http://hdl.handle.net/10986/38101.

[25] World Bank (2022), Global Economic Prospects, June 2022, World Bank, Washington, DC, https://doi.org/10.1596/978-1-4648-1843-1.

[45] World Bank (2022), “Sailing Against the Tide”, Turkey Economic Monitor 6, https://www.worldbank.org/en/country/turkey/publication/economic-monitor.

[24] World Bank (2022), “Weak Growth, High Inflation, and a Cost-of-Living Crisis”, Europe and Central Asia Economic Update, https://www.worldbank.org/en/region/eca/publication/europe-and-central-asia-economic-update.

[7] World Bank (2020), Global Economic Prospects, June 2020, World Bank, Washington, DC, http://hdl.handle.net/10986/33748.

[41] WTO (2022), “Russia-Ukraine conflict puts fragile global trade recovery at risk”, https://www.wto.org/english/news_e/pres22_e/pr902_e.htm.

[43] WTO (2022), “The Crisis in Ukraine: Implications of the war for global trade and development”, https://www.wto.org/english/res_e/publications_e/crisis_ukraine_e.htm.

[32] Zhang, N. (2022), “How the war in Ukraine affects the fight against climate change”, Katoikos World, https://katoikos.world/analysis/how-the-war-in-ukraine-affects-the-fight-against-climate-change.html.