12. Gender differences in financial literacy and resilience

This chapter provides an analysis of gender differences in financial literacy and resilience, mainly using results from the OECD/INFE 2020 International Survey of Adult Financial Literacy. It then focuses on financial education interventions as a key tool to address such gaps. The chapter provides examples of such interventions, from programmes addressing women at large to interventions targeting specific groups, such as financially vulnerable, younger, older or working women. After an overview of policy examples, the chapter concludes with some policy considerations.

Gender differences in financial knowledge and financial resilience persist. Women were already at greater risk of financial vulnerability than men and recent crises – the COVID-19 pandemic and the cost-of-living crisis spurred by rapidly rising energy and food prices – threaten to further challenge their financial well-being.

Financial education is one of the relevant approaches to close gender gaps in financial literacy and resilience. In recent years, many governments and other stakeholders have targeted their financial education policies at women or have offered financial education initiatives addressing women’s needs. Some programmes address women at large, but most programmes address the financial literacy needs of specific subgroups of women, such as financially vulnerable, younger, older, or working women. Evidence on their effectiveness is still limited.

Despite progress in these financial education initiatives, challenges remain, including difficulties to reach women; women’s lower self-confidence in their financial skills than men; persisting gender stereotypes and social norms; and women’s limited time availability given their family responsibilities.

The OECD defines financial literacy as a combination of financial awareness, knowledge, skills, attitudes and behaviours necessary to make sound financial decisions and ultimately achieve individual financial well-being (OECD, 2020[1]).

Results from the OECD/INFE 2020 International Survey of Adult Financial Literacy, whose data were collected in 2019-20 before the COVID-19 pandemic, provide the latest evidence on gender differences in financial literacy at the international level, covering 26 countries and economies and including 12 OECD members (OECD, 2020[2]). The results of a new OECD/INFE financial literacy survey are expected at the end of 2023.

OECD analyses of such results shows that gender differences in financial knowledge remain in most participating countries and economies. In 16 countries and economies, men have higher financial knowledge scores than women, and in no country do women score higher than men in financial knowledge. On average, men score higher than women by 4 points out of 100 in financial knowledge, but in some countries such difference is larger than 10 points (Figure 12.1).

Financial knowledge is measured by looking at familiarity with financial concepts such as inflation, interest compounding or diversification. Financial behaviour scores look at financially savvy behaviours, such as long-term planning, making considered purchases, and keeping track of cash flows. Financial attitude scores are meant to capture respondent’s attitude towards money and planning for the future. A lack of knowledge of basic financial concepts is likely to reduce women’s ability to access and use appropriate financial products and opportunities, set up a small business; build up emergency savings; save for retirement; and choose the best financial products for their needs (OECD, 2013[3]).

These patterns have not changed with respect to previous studies, which already showed consistent gender differences in financial knowledge (OECD, 2016[4]). Gender differences in financial knowledge among adults are also found in several national studies (CFFC, 2020[5]; Greimel-Fuhrmann and Silgoner, 2018[6]; Alessio et al., 2020[7]; Hospido, Izquierdo and Machelett, 2021[8]; FCAC, 2021[9]).

There are several possible reasons for the differences in financial knowledge between men and women. Observable socio-economic characteristics appear to explain only partially gender differences in financial knowledge (Bucher-Koenen et al., 2017[10]; Cupák et al., 2018[11]; Hospido, Izquierdo and Machelett, 2021[8]). The results of the OECD/INFE 2020 International Survey of Adult Financial Literacy confirm that gender differences in financial knowledge are reduced but not eliminated once various socio-economic factors are considered (OECD, 2020[2]). Women are often found to be less confident than men in their financial skills and decisions (Bucher-Koenen et al., 2017[10]; OECD, 2013[3]), which may contribute to explaining gender differences in financial knowledge and is ultimately associated with financial behaviour (Bucher-Koenen et al., 2021[12]). Another potential reason relates to the measurement of financial literacy. Since finance is considered a male field (Boggio et al., 2014[13]), women might answer financial literacy questions by saying they do not know or skip those questions, even if they have some financial knowledge. Moreover, differences in financial knowledge may stem from a gendered division of household work in couples where men manage household finances (Hsu, 2016[14]). Other studies highlight the role of financial socialisation from an early age, gendered stereotypes, culture and social norms in contributing to differences in financial knowledge in adulthood (Aristei and Gallo, 2021[15]; Bottazzi and Lusardi, 2020[16]; Driva, Lührmann and Winter, 2016[17]; Rink, Walle and Klasen, 2021[18]; Hospido, Izquierdo and Machelett, 2021[8]).

Note: Statistically significant gender differences are marked with an asterisk. Only countries with comparable data are reported.

Source: OECD (2020[2]), OECD/INFE 2020 International Survey of Adult Financial Literacy, https://www.oecd.org/financial/education/oecd-infe-2020-international-survey-of-adult-financial-literacy.pdf.

Financial resilience is the ability of individuals or households to resist, cope and recover from negative financial shocks. Such negative financial shocks can result from various unexpected events, including those related to employment, health, changes in family composition, damage to household possessions, or other large unexpected expenses (OECD, 2021[19]). At the individual level, financial resilience depends on having appropriate resources to cover cost of living expenses while also covering long term needs and/or unexpected shocks or emergencies. Access to instruments to build such resources requires adequate levels of financial inclusion and financial literacy in order for individuals to manage their finances, develop budget strategies, avoid crippling debt, and plan for the future.

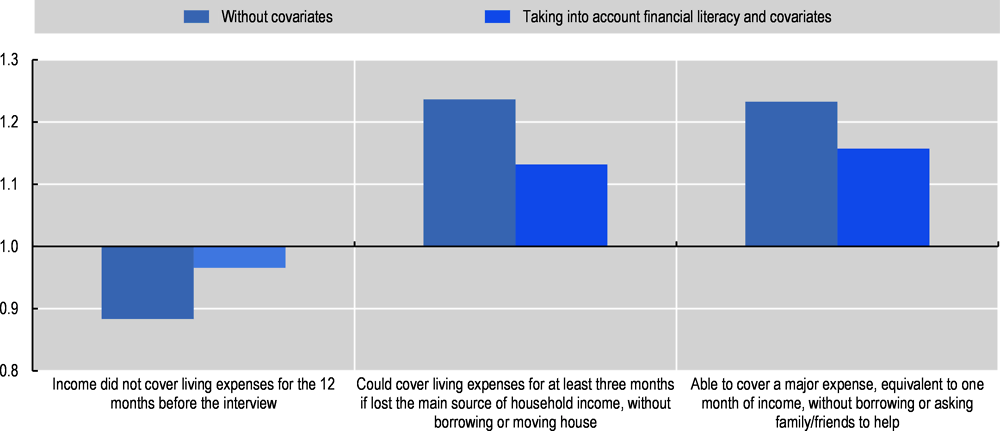

Data from the OECD/INFE 2020 International Survey of Adult Financial Literacy (collected before the COVID-19 pandemic) show that women tended to have lower levels of financial resilience than men in some countries (OECD, 2020[2]). Figure 12.2 shows that, on average across countries and economies, women were 22 percentage points more likely than men to report that their income did not cover living expenses for the 12 months before the interview. Moreover, on average across countries and economies, men were 24 percentage points more likely than women to report that they could cover their living expenses for at least three months if they lost their main source of household income without borrowing or moving house, and 23 percentage points more likely to be able to cover a major expense, equivalent to one month of income, without borrowing or asking family/friends to help. Gender differences in financial resources and financial resilience are also found in other national and international research (Austen, Jefferson and Ong, 2014[20]; Sierminska, Frick and Grabka, 2010[21]; Schneebaum et al., 2018[22]; FCAC, 2021[9]).

Gender differences in financial resilience could result from a variety of factors, including differences in labour market participation as well as in career continuity and progression, and gender wage gaps. The relatively limited financial knowledge of women with respect to men may be another factor contributing to greater risk of financial vulnerability among women. Data from the OECD/INFE 2020 International Survey of Adult Financial Literacy confirm that gender differences in financial resilience are reduced when considering demographic and socio-economic factors such as age, level of education, employment status, location (rural/urban), and household composition. As shown in Figure 12.2, gender differences in financial resilience are further reduced when also taking into account levels of financial literacy. This suggests that improving the financial literacy of men and women could help them acquire relevant skills and set up successful strategies to cope with future negative financial shocks.

Note: in the series “without covariates”, all values are statistically significant. In the series “Taking into account financial literacy and covariates”, statistically significant odds ratios are marked in a darker colour.

Source: OECD (2020[2]), OECD/INFE 2020 International Survey of Adult Financial Literacy, https://www.oecd.org/financial/education/oecd-infe-2020-international-survey-of-adult-financial-literacy.pdf.

A vast majority of individuals and households saw their finances impacted by the COVID-19 pandemic. A survey conducted in 2020 in OECD countries reported that around one-third of respondents experienced at least one of the following financial difficulties during the pandemic: failed to pay a usual expense, took money out of savings or sold assets to pay for a regular expense, took on additional debt or used credit to pay for a usual expense, went hungry because they could not afford to pay for food, lost their home because they could not afford the mortgage or rent, or declared bankruptcy or asked a credit provider for assistance. In every country surveyed, women were more concerned with their households’ financial security than men (OECD, 2021[23]).

As women were already, on average, at greater risk of financial vulnerability than men, the unique challenges posed by the COVID-19 pandemic disproportionally affected their financial well-being (OECD, 2020[24]; MAPS, 2020[25]). Other recent crises, such as the cost-of-living crisis spurred by rapidly rising energy and food prices, threaten to further challenge their financial well-being.

The 2020 OECD Recommendation on Financial literacy recognises the importance of developing financial education policies and programmes that address the needs of women and girls, and encourages adherents to incorporate financial literacy in policies designed to address gender gaps in financial outcomes.

While many approaches are relevant to close gender gaps in financial literacy and reliance, this chapter focuses on the role of financial education (OECD, 2021[19]). Many governments and other stakeholders have been targeting their financial education policies at women, or offering financial education initiatives addressing women’s needs. While some programmes target women specifically, others are attended mostly by a female audience because they address groups mostly made of women. Information on these policies and programmes is based on desk research and on the replies to a stocktaking survey circulated among members of the OECD International Network on Financial Education (OECD/INFE) in June-July 2021. The questionnaire received responses from 46 institutions in 35 countries and economies, including 20 OECD members (Angola; Australia; Austria; Bangladesh; Brazil; Canada; Chile; Colombia; Croatia; the Czech Republic; Dominican Republic; Germany; Honduras; Hong Kong, China; Hungary; India; Indonesia; Ireland; Italy; Japan; Kosovo1; Mexico; Mongolia; Namibia; New Zealand; Nigeria; Paraguay; Peru; Poland; Portugal; the Slovak Republic; South Korea; Spain; Sweden and the United Kingdom).

Several countries have taken a co-ordinated approach at women’s financial education needs, by including women and/or girls as a specific target group of their national strategy for financial literacy/education. This is the case in Australia, Austria, Bangladesh, Brazil, Canada, Chile, Colombia, the Dominican Republic, India, Indonesia, Italy, Mexico, New Zealand, Nigeria, Peru, Spain and the United Kingdom. This is usually motivated by evidence of gender differences at national level in financial literacy, in financial behaviour (such as different engagement with private pensions) or in financial outcomes (such as different financial inclusion levels or specific financial vulnerabilities). Box 12.1 provides an example of how financial education needs and interests may diverge between men and women.

Governments have increasingly put in place programmes to address such needs, including workshops, classes, training seminars, and online/print resources. Some programmes are quite broad and address women at large. For instance, in 2018, the Australian Securities and Investments Commission ran a comprehensive campaign, Women Talk Money, featuring high-profile Australian women explaining their experiences with money to help motivate and inspire other women to take action with their own finances. In Poland, the Bank Guarantee Fund targeted women as part of its educational campaign in 2020/21, aimed at raising awareness of deposit guarantee scheme in Poland. This included texts published in women’s magazines and short videos by female celebrities.

In most other cases, however, programmes address the financial literacy needs of specific subgroups of women, as described below.

Financially vulnerable women

Not surprisingly, many public authorities have developed initiatives aimed at addressing women in a financially vulnerable situation (such as the unemployed, informal sector workers, financially excluded, etc.), including those facing financial difficulties during the COVID-19 crisis.

For example, the Bank of Italy has implemented training courses for low-incomes and/or low-education women to respond to the challenges of the pandemic. Modules relate to topics of relevance during the crisis, such as digital payments, the risk of fraud and scams, and financial planning, with the aim of increasing consumers’ financial resilience. Moreover, the Bank of Italy has been working with an international women’s association to train their trainers to deliver financial education among women living in anti-violence centres, unemployed women, fragile single mothers and other vulnerable groups of women.

Other programmes target low-income women and female informal workers in developing countries. The Capital Markets Commission of Angola carries out a yearly financial education programme for women who work in informal sectors and have a limited use of formal financial products. In Indonesia, financial literacy training is provided, as a complement to other interventions, to women beneficiaries of the conditional money transfer “Family Hope Program”. In Peru, the National Financial Inclusion Policy includes various initiatives targeting vulnerable women, including training programmes for rural and indigenous women.

Younger and older women

Public authorities in some countries have developed initiatives for young women to help them build a sound financial future. In 2020, the Australian Securities and Investments Commission assisted the social enterprise “Wake by Reach” with the launch of their Glassbreaker educations series, helping young women build financial skills and resilience. The central bank of Austria developed the My Money Guide in co-operation with the Vienna University of Economics and Business, aimed specifically at young women but also at anyone else who is interested. The guide provides tips on how to get started in personal finance, including how to control income and expenses, make decisions based on reliable information, and seek advice from competent sources. The Financial Consumer Agency of Canada (FCAC) is designing a series of interventions aimed at increasing the confidence among women and girls. The first intervention targets students in middle and high school and is delivered using a gamified online platform. Students participate in virtual seek-and-find activities where they can build their knowledge and confidence around money management, budgeting, and other areas of financial literacy.

At the other end of the age spectrum, some programmes aim at supporting women in planning for their old age. In 2021, the Social Security Secretariat of Brazil launched the Complementary Social Security Guide for Women, addressed at women who want to take care of their future. The educational material addresses the importance of financial planning for retirement, provides information on public pensions for women, and describes the main features of private pension plans. In Sweden, the financial supervisory authority (Finansinspektionen) developed a programme for senior citizens to enhance their knowledge about their pensions and personal finance.

Women are also indirectly targeted by programmes that are aimed at families and parents. For instance, the Investor and Financial Education Council in Hong Kong, China delivers financial education seminars at the Family Planning Association, which primarily serves women. In the United Kingdom, the Money and Pensions Service implements the Talk Learn Do programme for parents to encourage them to talk to their children about money. While this is open to all parents, most participants are women.

Working women

Targeting women in certain occupational categories can be another way of reaching out to women facing similar challenges (such as female entrepreneurs) or simply reaching large numbers of women (such as through workplace programmes for employees).

In Chile, both the Commission for Financial Markets (CMF) and the National consumer service (SERNAC) implement financial educational programmes for female micro and small entrepreneurs. Banco del Bienestar (a public development bank) in Mexico conducts various financial empowerment workshops for women in working age and female business owners. In Peru, the Multisectoral Strategic Plan of the National Financial Inclusion Policy includes financial literacy trainings for micro and small female entrepreneurs.

In New Zealand, the Te Ara Ahunga Ora Retirement Commission designed a programme dedicated to women as part of its workplace courses, Sorted Women. This is designed and delivered by women for women, and it aims at providing a safe and non-judgemental space to learn money skills.

Indirectly, most train-the-trainer programmes targeting school teachers or social workers have a majority of female participants. They can be useful in improving the personal financial literacy of the trainers, beyond providing skills to teach financial literacy to students or other audiences.

The public website https://moneysmart.gov.au/ is a central element of the Moneysmart programme developed by the Australian Securities and Investments Commission. The Commission has examined content engagement from visitors through a gendered lens.

Overall access to the Moneysmart website is roughly balanced across genders. During the pandemic, while most COVID-19 content was accessed evenly across men and women, 2 out of 3 people visiting the “Living on a reduced income” page were women.

It is interesting to see which specific pages and topics are visited by men and women. Most topics are of equal interest to men and women, however there are several areas and pages which tend to skew to a particular gender. While men seem to mostly focus on information about financial investments or loans, women appear to be mainly searching for information about budgeting, saving, coping with financial difficulties (financial scams, financial abuse, paying off multiple credit cards, financial counselling) and for teaching resources to be used in school (as most teachers are women).

Many governments and other stakeholders are developing financial education initiatives to support women in a financially difficult position or to help close gender gaps in a variety of financial outcomes. Yet, challenges remain.

Women may be a difficult target to reach than men. In many countries women have lower financial knowledge and lower self-confidence in their financial skills than men. The limited scope of observable socio-economic characteristics in explaining gender differences in financial literacy suggests that social norms are likely to play a role. As a result, women may tend to avoid complex financial topics, may try to avoid financial and economic subjects altogether, and may be more likely than men to feel anxious when they have to deal with personal or household financial issues (Hasler, Lusardi and Valdes, 2021[26]). In addition, as workers and caregivers, they have many daily responsibilities, and they may rarely have time to devote to themselves and their education. Delegating important household financial decisions to their partners may be the outcome of women’s lack of confidence and lack of time, and may in turn reinforce their lack of familiarity and knowledge about financial issues.

Countries are making efforts to ensure that financial education contributes to closing gender gaps in financial outcomes and helps women in a financially vulnerable situation. Countries have also developed various strategies for facilitating women’s participation in financial education, such providing gender sensitive content, setting up gender-friendly environments, using role models, and providing tailored advice specifically to women on financial topics women are less familiar with, such as debt or investments (OECD, 2013[3]). Providing financial education in the workplace may facilitate attendance by women with caring responsibilities, but competes with professional priorities during working hours (OECD, 2022[27]). Digital financial education may be another way of offering opportunities to enhance financial knowledge and skills in a flexible and tailored way, provided that women have access to the internet and/or smartphones (OECD, 2020[28]). More generally, it is important to adapt both the content and delivery of programmes to specific needs of different groups of women, as well as to the regional and local contexts. Most of the financial education programmes described in this chapter have yet to be formally evaluated (as is the case for many financial education programmes more widely), and refined evaluation evidence would be needed to understand any differential impact and outcomes of financial education for men and women.

Broad approaches may also be needed to avoid gender stereotypes and reduce different outcomes by gender, ensuring that a gender lens is applied in financial education programmes. This includes collaborating with financial education providers to review and update the content and delivery of financial education, as well as updating the financial education teacher training curriculum to address any gender bias in the learning environment.

Ultimately, is it also important to recognise that financial education is an important element is aspect in strengthening the financial resilience and well-being of men and women, but other factors need to be dealt with to improve the financial well-being of women, including facing structural and systemic issues (e.g. gender pay gap), addressing social norms and providing support to women in different life stages.

Developing evidence-based financial education policies and programmes is fundamental to design well-informed tailored policies and programmes: this requires collecting gender disaggregated data on financial literacy levels, and devoting more efforts to collecting gender disaggregated data about the impact of financial education programmes.

Taking into account gender differences in financial literacy requires supporting women’s financial knowledge and confidence in financial decision making, and providing tailored guidance and advice on complex topics (such as debt and investments).

Considering financial education as part of broader approaches can improve women’s financial resilience and well-being. Efforts should aim at incorporating financial education into broader efforts to support women’s financial resilience and financial well-being (such as training on business skills, use of digital financial services, conditional financial transfers, etc.), and at closing gender gaps in areas that result in different financial outcomes by gender (such as financial inclusion, digitalisation, labour markets, social norms, etc.).

References

[7] Alessio, G. et al. (2020), “Financial literacy in Italy: the results of the Bank of Italy’s 2020 survey”, Questioni di Economia e Finanza, https://www.bancaditalia.it/pubblicazioni/qef/2020-0588/QEF_588_20_EN.pdf?language_id=1.

[15] Aristei, D. and M. Gallo (2021), “Assessing gender gaps in financial knowledge and self-confidence: Evidence from international data”, Finance Research Letters, p. 102200, https://doi.org/10.1016/J.FRL.2021.102200.

[20] Austen, S., T. Jefferson and R. Ong (2014), “The Gender Gap in Financial Security: What We Know and Don’t Know about Australian Households”, Feminist Economics, Vol. 20/3, pp. 25-52, https://doi.org/10.1080/13545701.2014.911413.

[13] Boggio, C. et al. (2014), “Seven Ways to Knit Your Portfolio Is Investor Communication Neutral?”, CeRP Working Paper Series, No. 140/14, https://www.netspar.nl/assets/uploads/030_Prast-1.pdf.

[16] Bottazzi, L. and A. Lusardi (2020), “Stereotypes in Financial Literacy: Evidence from PISA”, NBER Working Papers, No. 28065, https://doi.org/10.3386/W28065.

[12] Bucher-Koenen, T. et al. (2021), “Fearless Woman: Financial Literacy and Stock Market Participation”, NBER Working Papers, No. 28723, https://doi.org/10.3386/W28723.

[10] Bucher-Koenen, T. et al. (2017), “How Financially Literate Are Women? An Overview and New Insights”, Journal of Consumer Affairs, Vol. 51/2, pp. 255-283, https://doi.org/10.1111/JOCA.12121.

[5] CFFC (2020), Financial knowledge of New Zealanders, Commission for Financial Capability, https://assets.retirement.govt.nz/public/Uploads/Research/CFFC-Barometer-Financial-Literacy-2020.pdf.

[11] Cupák, A. et al. (2018), “Decomposing gender gaps in financial literacy: New international evidence”, Economics Letters, Vol. 168, pp. 102-106, https://doi.org/10.1016/J.ECONLET.2018.04.004.

[17] Driva, A., M. Lührmann and J. Winter (2016), “Gender differences and stereotypes in financial literacy: Off to an early start”, Economics Letters, Vol. 146, pp. 143-146, https://doi.org/10.1016/J.ECONLET.2016.07.029.

[9] FCAC (2021), Summary of findings COVID-19 surveys: Financial impact of the pandemic on Canadians, https://www.canada.ca/en/financial-consumer-agency/corporate/covid-19/summary-covid-19-surveys.html.

[6] Greimel-Fuhrmann, B. and M. Silgoner (2018), “Analyzing the Gender Gap in Financial Literacy”, International Journal for Infonomics, Vol. 11/3, pp. 1779-1787, https://doi.org/10.20533/iji.1742.4712.2018.0180.

[26] Hasler, A., A. Lusardi and O. Valdes (2021), Financial Anxiety and Stress among U.S. Households: New Evidence from the National Financial Capability Study and Focus Groups, GFLEC and FINRA Foundation, https://gflec.org/wp-content/uploads/2021/04/Anxiety-and-Stress-Report-GFLEC-FINRA-FINAL.pdf?x85507.

[8] Hospido, L., S. Izquierdo and M. Machelett (2021), “The gender gap in financial competences”, Economic Bulletin, No. 2021/1, Banco de España, https://www.bde.es/bde/en/secciones/informes/analisis-economico-e-investigacion/boletin-economico/.

[14] Hsu, J. (2016), “Aging and Strategic Learning: The Impact of Spousal Incentives on Financial Literacy”, Journal of Human Resources, Vol. 51/4, pp. 1036-1067, https://doi.org/10.3368/JHR.51.4.1014-6712R.

[25] MAPS (2020), Impacts of COVID-19 on financial wellbeing, Money and Pensions Service , London, https://www.financialcapability.gov.au/files/impacts-of-covid-19-on-financial-wellbeing.pdf.

[27] OECD (2022), “Policy handbook on financial education in the workplace”, OECD Business and Finance Policy Papers, No. 07, OECD Publishing, Paris, https://doi.org/10.1787/b211112e-en.

[19] OECD (2021), G20/OECD-INFE Report on Supporting Financial Resilience and Transformation through Digital Financial Literacy, OECD, Paris, https://www.oecd.org/finance/financial-education/supporting-financial-resilience-and-transformation-through-digital-financial-literacy.htm.

[23] OECD (2021), “Risks that matter 2020: The long reach of COVID-19”, OECD Policy Responses to Coronavirus (COVID-19), OECD Publishing, Paris, https://doi.org/10.1787/44932654-en.

[28] OECD (2020), Digital Delivery of Financial Education: Design and Practice, OECD, Paris, https://www.oecd.org/financial/education/Digital-delivery-of-financial-education-design-and-practice.pdf.

[2] OECD (2020), OECD/INFE 2020 International Survey of Adult Financial Literacy, https://www.oecd.org/financial/education/oecd-infe-2020-international-survey-of-adult-financial-literacy.pdf.

[1] OECD (2020), Recommendation of the Council on Financial Literacy, OECD/LEGAL/0461, https://legalinstruments.oecd.org/en/instruments/OECD-LEGAL-0461.

[24] OECD (2020), “Women at the core of the fight against COVID-19 crisis”, OECD Policy Responses to Coronavirus (COVID-19), OCD Publishing, Paris, https://doi.org/10.1787/553a8269-en.

[4] OECD (2016), OECD/INFE International Survey of Adult Financial Literacy Competencies, OECD, Paris, https://www.oecd.org/finance/OECD-INFE-International-Survey-of-Adult-Financial-Literacy-Competencies.pdf.

[3] OECD (2013), Women and Financial Education: Evidence, Policy Responses and Guidance, OECD Publishing, Paris, https://doi.org/10.1787/9789264202733-en.

[18] Rink, U., Y. Walle and S. Klasen (2021), “The financial literacy gender gap and the role of culture”, The Quarterly Review of Economics and Finance, Vol. 80, pp. 117-134, https://doi.org/10.1016/J.QREF.2021.02.006.

[22] Schneebaum, A. et al. (2018), “The Gender Wealth Gap Across European Countries”, Review of Income and Wealth, Vol. 64/2, pp. 295-331, https://doi.org/10.1111/ROIW.12281.

[21] Sierminska, E., J. Frick and M. Grabka (2010), “Examining the gender wealth gap”, Oxford Economic Papers, Vol. 62/4, pp. 669-690, https://doi.org/10.1093/OEP/GPQ007.

Note

← 1. This designation is without prejudice to positions on status, and is in line with United Nations Security Council Resolution 1244/99 and the Advisory Opinion of the International Court of Justice on Kosovo’s declaration of independence