3. State of play: Subnational green budgeting practices in OECD and EU countries

In recent years, as an ever-growing number of regions and cities have set ambitious climate and environmental targets, the interest in subnational green budgeting has also grown steadily as has the number of subnational governments implementing green budgeting practices. A stocktake of existing subnational green budgeting practices in OECD and EU countries found that green budgeting encompasses a variety of practices including carbon budgets, ecoBudgets, climate budgets, environmental and climate impact analyses, and more. Among the countries identified in the stocktake as having subnational green budgeting exercises, France stands out for having a large number of green budgeting exercises at all three levels of subnational government. Other interesting exercises were identified in Austria, Italy, Norway, Spain and the United Kingdom.

This chapter presents the first ever stocktake of subnational green budgeting practices in OECD and European Union (EU) countries. It was conducted based on desk research and used the Paris Collaborative on Green Budgeting’s definition of green budgeting.

Without being exhaustive, it shows that in recent years as an ever-growing number of regions and cities have set ambitious climate and environmental targets, the interest in subnational green budgeting has also grown steadily. Likewise, the number of subnational governments implementing green budgeting practices has also increased.

Post-COVID-19 recovery plans, strongly centred on environmental and climate issues, certainly contribute to this trend, especially in the European Union. For some countries, new green budgeting practices are also an extension of other priority budgeting methods such as gender budgeting or pro-poor budgeting that are completing traditional incremental budgeting practices.

The stocktake shows that there is no one-size-fits-all approach to green budgeting, particularly at the subnational level. There is a need for different approaches to reflect the differences in the scale and type of climate and environmental challenges faced by different subnational governments depending on their location (e.g. urban vs rural, coastal vs mountainous areas, etc.) and characteristics (e.g. demographic and geographic size). Subnational government responsibilities also vary across countries and across levels of government (e.g. regions vs municipalities). The socio-economic role of subnational governments, and therefore their impact on the environment and climate, differs considerably according to the level of decentralisation and the assignment of responsibilities and revenues. In federal and decentralised countries, spending and revenues decisions are likely to have a higher impact on the green transition than in more centralised countries, where local governments play a more minor financial role. However, green budgeting is not limited to the largest subnational governments, and there are some small municipalities that are experimenting green budgeting, for example in France. In fact, while environmental and climate issues may differ depending on the size of territories and the scope of responsibilities, the fact remains that implementing green budgeting in small subnational governments is equally of interest, and can in some cases be easier given the more modest size of their budgets.

Finally, this heterogeneity can also be attributed to the fact that subnational budgeting and accounting systems differ substantially from one country to another, and even within countries across levels of subnational government. This heterogeneity in terms of accounting and budgetary systems is quite normal given the extreme diversity of multi-level governance systems among OECD and EU countries, as described above.

The stocktake revealed that there is considerable diversity in terms of methodology, scope, and reporting among existing subnational green budgeting practices.

Subnational green budgeting encompasses a variety of practices including carbon budgets, ecoBudgets, climate budgets, environmental and climate impact analyses, and more. In some cases, these existing subnational practices were inspired by national green budgeting exercises and methodologies, and in other cases they are stand-alone. These practices also vary in terms of coverage, some only assess capital expenditures while others include current expenditures. In terms of green objectives, some practices focus only on climate change adaptation and mitigation while others include broader environmental objectives such as biodiversity or water and air pollution. Moreover, some practices combine green budgeting with other priority budgeting approaches such as United Nations Sustainable Development Goals (SDG) budgeting, social objectives and gender budgeting. The underlying objective for carrying out a green budgeting exercise also varies between practices. Some practices use green budgeting as a tool for issuing green bonds or accessing green loans, while others use it primarily as a transparency and accountability tool.

All of the subnational green budgeting exercises identified in the stocktake, which focused on the OECD and EU, are in European countries. France stands out for having green budgeting exercises at all three levels of subnational government: regional, departmental, and municipal. Other interesting exercises were identified in Italy, Norway, Spain and the United Kingdom. At the regional level, there are a variety of green budgeting methodologies being used. In contrast, at the municipal level, most municipalities, regardless of country, were found to have based their green budgeting practice on one of two methods – the Climate Budgetary Assessment or the Climate Budget Approach – that they then adapted to their specific context and policy aims. Although outside the scope of the stock-take, subnational green budgeting practices were also identified in non-OECD and EU countries, particularly in Asia.

At the regional level, the stocktake identified green budgeting practices in France, Italy, Spain and the United Kingdom. France is a leader in terms of subnational green budgeting, with multiple regional green budgeting practices using a common methodology inspired by the green budgeting methodology used at the national level.

France: Regional green budget tagging

In France, green budgeting practices have emerged at all subnational levels: regional, departmental,1 and municipal. At the regional level, the regions of Brittany, Grand-Est, and Occitanie have launched a green budgeting practice. The three regions use a common green budget tagging methodology to assess the climate adaptation and mitigation impact of their budgets. The methodology was developed by the Institute for Climate Economics (I4CE)2 and was inspired by the green budget tagging methodology used at the national level in France (I4CE, 2020[1]).

I4CE’s methodology was co-constructed with five French municipalities and metropolises and originally intended to be used by municipalities not regions. As a result, the regions have adapted the methodology according to their competences, their respective local climate and environmental contexts, and their green objectives. There are two specific limitations associated with applying the I4CE methodology to regional budgets. First, French regions and municipalities have different spending responsibilities and there are some regional spending areas, such as agriculture and professional training, which are climate-related but were not included in the original methodology as they are not municipal competences. To address this limitation, I4CE, the association of French regions (Régions de France), and the aforementioned three regions formed a working group in 2021 to jointly extend the methodology to cover these spending areas (Box 3.1). The second limitation of the methodology is that it is best suited for operational expenditures rather than subsidies, which make up a significant part of the regional budget. Analysing the climate impact of subsidies requires additional information about the objective and nature of the subsidy, which can increase the administrative burden of the exercise.

The purpose of the methodology is to assess the climate adaptation and mitigation impact of all regional expenditure and to incorporate this information into future budgetary decisions. Ideally, the methodology should be applied to the entire budget, however, when starting out it is suggested that as a minimum the analysis should assess current and capital expenditure in the main budget, special budgets, and any delegated public service provision contracts. Revenues are not currently covered by the methodology as subnational governments in France have limited revenue autonomy; however, I4CE notes that they could be incorporated in the future. The methodology can be applied to both draft budgets and closed administrative accounts, in other words it can be applied ex ante and ex post.

Brittany launched their green budgeting practice by assessing the climate adaptation and mitigation impact of expenditure in their closed 2020 administrative accounts in order to test out the I4CE methodology and adapt it to their local context. They subsequently applied the adapted methodology to the 2022 draft budget. Their green budget excluded EU funds and funds linked to the COVID-19 pandemic response.

Grand Est applied the methodology to their 2022 draft budget. This initial analysis only assessed the climate mitigation impact of the budget; however, they have indicated plans to expand the analysis to include social and biodiversity impacts in the future. Their green budget excluded EU funds and funds linked to the COVID-19 pandemic response.

Occitanie was the first French region to launch a green budgeting practice, initially applying the I4CE methodology to assess the climate mitigation impact of their 2021 draft budget. Their second green budget was voted on as part of the 2022 draft budget and they now intend to apply the analysis ex post to the 2021 closed accounts to follow-up on their initial analysis of the 2021 draft budget. Their 2022 green budget excluded EU funds, funds linked to the COVID-19 pandemic response, and debt repayment expenditure.

Notes: COVID-19 response funds were considered exceptional expenditure and excluded to allow for comparability with the results of future analyses. Information for Brittany comes from the regional case study presented in Chapter 5 of this report.

Source: Région Grand Est (2021[2]), Grand Est Budget 2022, https://www.grandest.fr/wp-content/uploads/2022/01/grand-est22-budget-2022-papok.pdf (accessed on 8 April 2022); La Région Occitanie (2021[3]), Budget Primitif 2022.

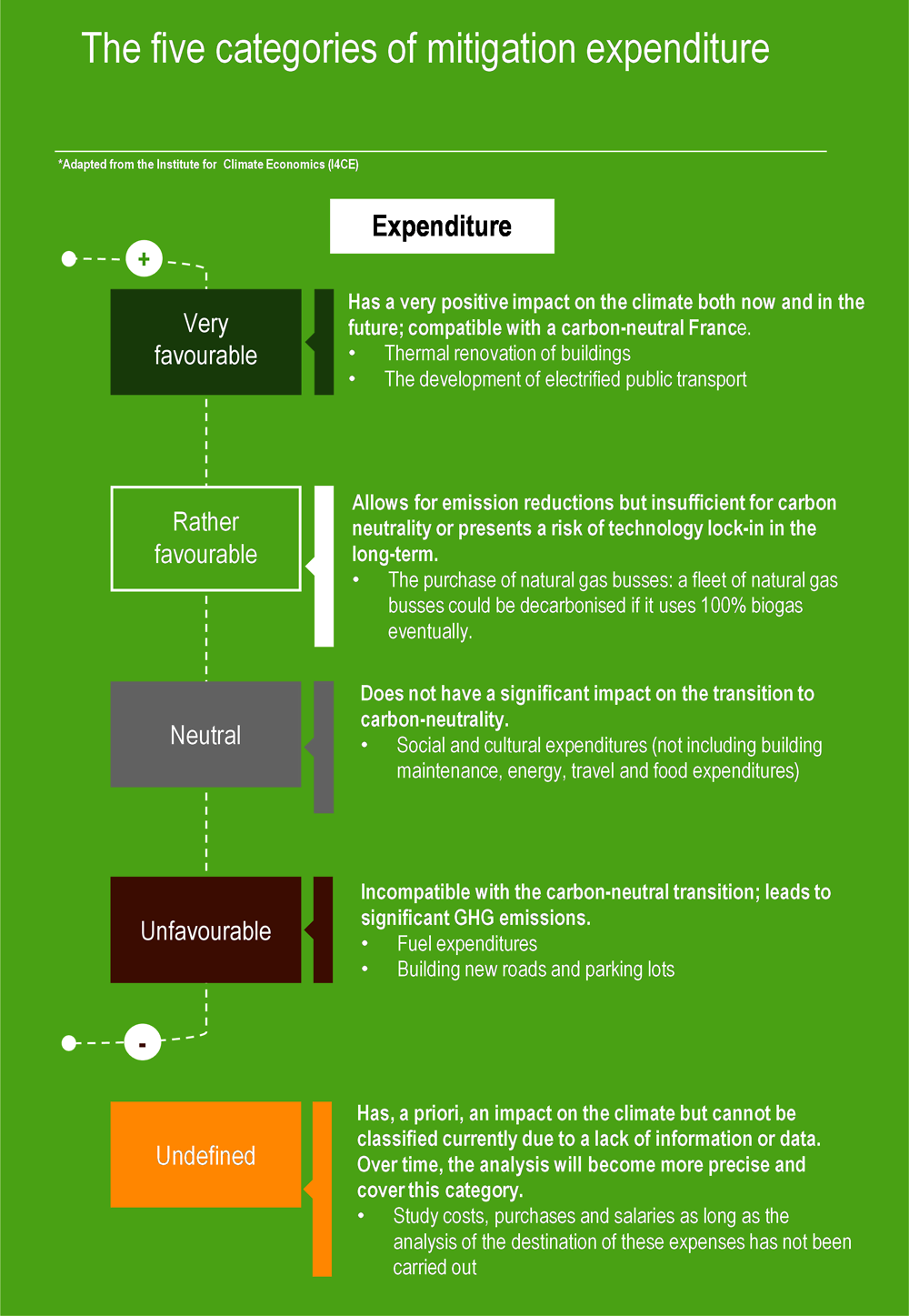

An analysis of the climate impact of expenditure using the I4CE methodology takes place in two steps:

The first step is a high-level analysis of all the expenditure items to classify them into three categories: those with a neutral climate impact, those lacking sufficient information to be classified (labelled “undefined” in the I4CE methodology), and those to be further analysed for their climate impact (labelled “to analyse”).

The second step is applied only to those expenditures classified as “to analyse” by the first step. This subset of expenditures is further analysed according to their climate impact using “structuring hypotheses” and a colour-coded grade scale ranging from favourable to unfavourable (Figure 3.1).

The structuring hypotheses for climate mitigation are based on France’s net-zero carbon emissions by 2050 objective corresponding to the French National Low-Carbon Strategy (SNBC). I4CE defined nine sectoral structuring hypotheses (for construction, transport infrastructure, vehicle purchase and maintenance, highways, food, waste, energy purchases, energy network and infrastructure, software and new technologies, and green spaces) and six transversal hypotheses (for personnel expenditure, business travel expenses, climate taxes, subsidies, public procurement and sustainable purchasing, carbon compensation). Regional expenditure is therefore analysed based on these sectoral or transversal hypotheses to determine whether an expense reduces emissions, increases emissions, or has no impact. To assess the impact of expenditure on climate adaptation, the I4CE methodology requires the region or municipality to link the structuring hypotheses to their local adaptation plans and objectives, given the highly localised nature of climate change adaptation actions and impacts. The adaptation expenditure tagging methodology, therefore, differs from the mitigation tagging methodology, most notably in the fact that it does not use the colour-coded grading system. Instead, expenditure items are first analysed to determine if they are neutral or “potentially structuring”, meaning if they have a climate adaptation “lever” and could contribute to local climate adaptation objectives. Next all potentially structuring expenditures are analysed to see if an adaptation policy for the policy area of the expenditure in question exists. If it does, and the policy is being correctly implemented, then the expenditure is flagged as having a “suitable” climate adaptation impact. If not, it is considered to be “unsuitable”. Thus far, Brittany is the only French region to have begun evaluating the climate adaptation impact of its budget; more information is available in Chapter 5 of this report.

Note: This grading scale is used in both region and municipal level green budgeting exercises in France. This is a similar scale to what is used in France’s national-level green budgeting exercise.

Source: Adapted and translated by the author from I4CE (2020[1]), Évaluation climat des budgets des collectivités territoriales: guide méthodologique, https://www.i4ce.org/download/evaluation-climat-des-budgets-des-collectivites-territoriales-guide-methodologique.

Sardinia, Italy: Regional green budget analysis

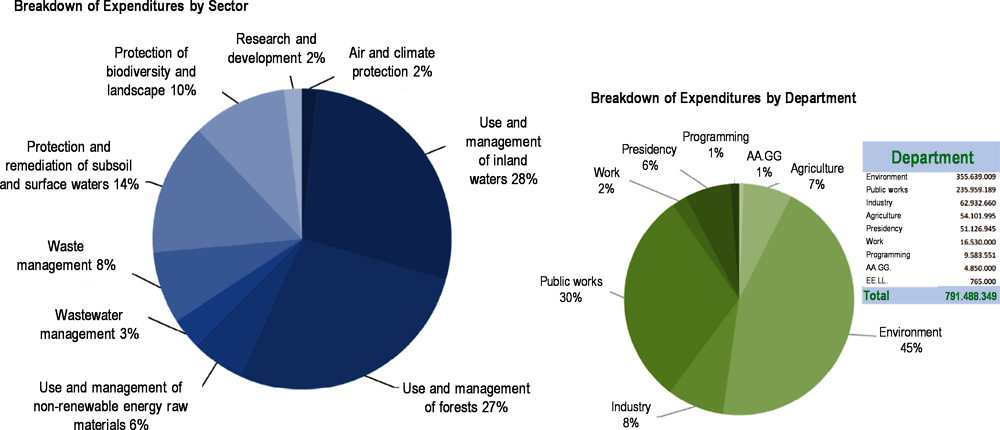

The region of Sardinia’s (Italy) approach to green budgeting is centred on an annual analysis of its environmental protection and natural resource use and management expenditure (Direzione Generale dei Servizi Finanziari, 2021[4]). Sardinia was inspired by the national-level green budgeting practice conducted annually by the Italian government, which also tracks environmental protection and natural resource use expenditure.

Implemented for the first time in 2019, the exercise tracks both current and capital expenditures at the level of each individual budget chapter, reconciling the expenditure by missions, programmes, and COFOG codes with CEPA3 and CRUMA4 codes for environmental protection expenditure and natural resource use and management expenditure, respectively. Tracking is carried out on the draft budget and therefore the results show the forecasted expenditure in these two areas for a given year.

Climate-favourable expenditures are tagged for a list of 13 sectors that include forest management and use, inland water sources management and use, protection and rehabilitation of soil, subsoil and surface water; wastewater management, research and development, and waste management to name a few.5

The data collected from this exercise is used to produce a report with graphs showing the breakdown of forecasted expenditure by sector, by type of expenditure (capital or current), and by government department (Figure 3.2). In 2021, the region’s environmental protection and natural resource use and management expenditure totalled nearly EUR 790 million across nine sectors (Direzione Generale dei Servizi Finanziari, 2021[4]).

Source: Direzione Generale dei Servizi Finanziari (2021[4]), Ecobilancio 2021 della Regione Sardegna, https://www.regione.sardegna.it/j/v/2592?&s=1&v=9&c=10803&n=10&nodesc=1 (accessed on 6 April 2022).

Andalusia, Spain: A multifaceted approach to green budgeting

The autonomous region of Andalusia, Spain was the first Spanish region to adopt green budgeting, in 2018, and the only subnational green budgeting practice identified in this stocktake to have made green budgeting mandatory by regional law.6 Andalusia’s green budgeting practice is predicated on a regional strategy to integrate a green perspective into all aspects of regional strategic planning, which itself serves as guidance for the region’s budgetary decision-making (Autonomous Community of Andalusia, 2020[5]). Moreover, in developing its green budgeting practice Andalusia is building on its well-established gender budgeting practice, dating back to 2004, and which the region intends to link with their green budgeting approach given that the impacts of climate change affect men and women differently and require public action that takes this into account in order to ensure a just transition (Autonomous Community of Andalusia, 2020[5]).

Andalusia’s green budgeting practice is multifaceted and includes climate impact assessments, green budget tagging, and environmental tax reform, among other aspects. The 2018 Andalusian climate change law set outs two key aspects of the region’s green budgeting approach: budgetary climate indicators and climate impact assessments for regional and local planning and strategy documents (Boletín Oficial del Estado, 2018[6]). The law stipulates that the region is to develop climate change budgetary indicators to measure and track the impact of budget programmes on climate change adaptation and mitigation, and that the Budget Department is to prepare an annual report tracking the evolution of these indicators. In the 2021 budget, more than 60 climate change indicators were presented to identify the climate impact of budget measures (Autonomous Community of Andalusia, 2021[7]). The second key aspect is a multi-step climate impact assessment for regional and local plans and programmes thought to have an impact on climate change and the clean energy transition. Plans and programmes identified as having a climate change impact must include five elements as part of their proposal:

A climate change vulnerability analysis from an environmental, economic, and social perspective.

Steps to promote medium- and long-term climate change mitigation.

Justification of how the plan or programme aligns with the Andalusian Plan of Action for the Climate.

Indicators to evaluate the climate impact of the plan or programme.

An analysis of the potential direct and indirect impact of the plan or programme on energy consumption and greenhouse gas emissions.

An additional aspect of the region’s green budgeting practice is the EUR 1 million Green Budget Fund set up to fund projects that integrate a green perspective into the region’s budget (Junta de Andalucía, 2020[8]). Among all levels of government practising green budgeting in the OECD and EU, Andalusia is the only one to have established such a fund. Proposed projects must focus on at least one of several green objectives including environmental protection, the fight against climate change, environmental sustainability, and/or mitigating the socio-economic impacts associated with climate change mitigation and adaptation. Additionally, proposals are also required to address one of three budget-programming objectives which include promoting climate impact assessments; fostering the development and monitoring of budget objectives, actions, and indicators; and promoting capacity building and climate change awareness among public officials, particularly regarding the relationship between climate change and the budgetary process. Among the projects selected under the Fund’s first call for proposals was a project entitled “Study of the theoretical foundations and main indicators, to integrate the gender approach in the Green Budget in the framework of the competences of the Andalusian Regional Government”. This project carried out an initial analysis on how to consolidate the region’s well-established gender budgeting approach with its newly-established green budgeting approach (Autonomous Community of Andalusia, 2020[9]). This work led to the development of a set of guidelines for regional officials to use to assess the gender and green impact of proposed budget measures and to assign relevant impact indicators.

Beyond these existing green budgeting tools, Andalusia is also currently collaborating with DG REFORM of the European Commission to develop two additional aspects of their green budgeting practice. Firstly, the Region has developed a Sustainable Finance Framework to serve as the basis for issuing sustainable bonds to fund green and social projects. Part of developing this framework included implementing green budget tagging within the regional budget in order to identify projects to be funded using the proceeds of sustainable (green and social) bond issuances.

The final aspect of Andalusia’s green budgeting practice is environmental tax reform. As part of a second ongoing DG REFORM project, the region is collaborating with the OECD to design, develop, and implement tax reforms in four green domains: climate change and air pollution; electricity usage; water pollution; and circular economy. The project aims to provide recommendations to Andalusia so that it can plan potential adjustments to its environmental and climate relevant tax legal framework, with a view to improving regional green outcomes and strengthening contributions to national and global performance.

Catalonia, Spain: Climate budget tagging using the OECD DAC Rio Markers for Climate

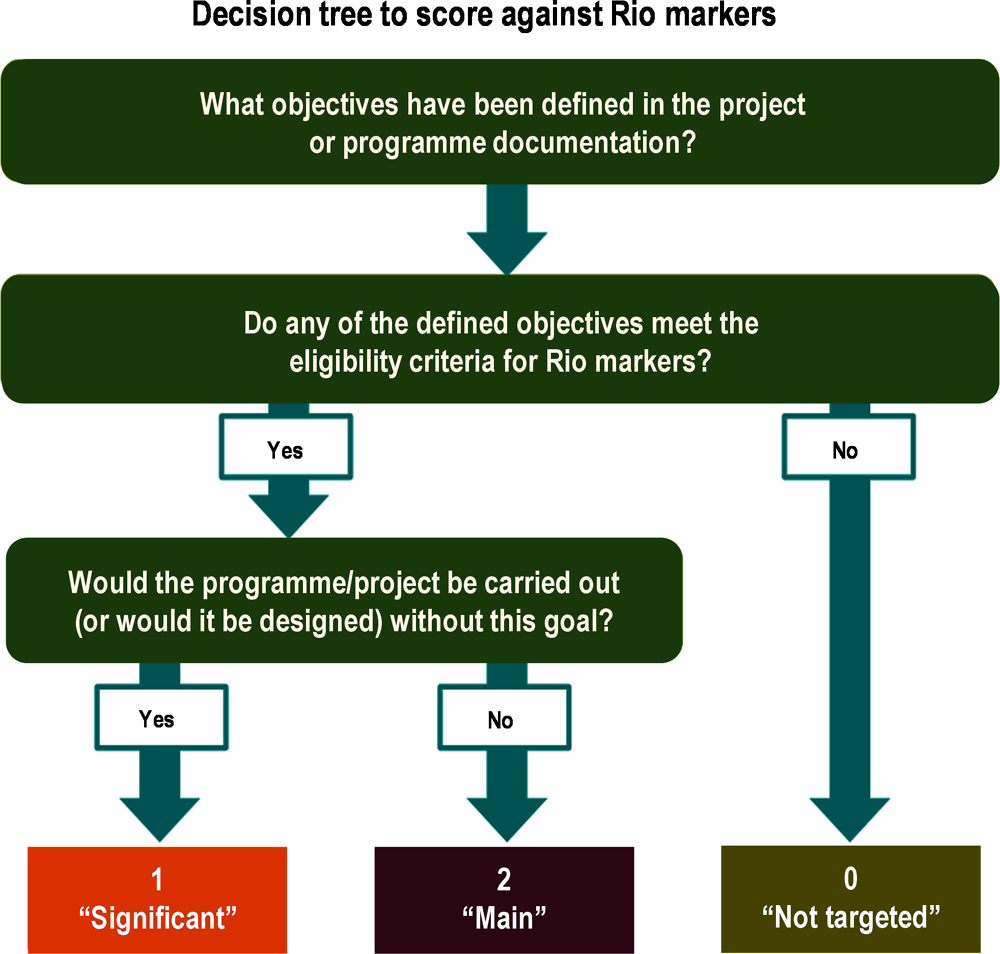

The Catalonian government recently released the results of its first climate budget tagging practice in March 2022 (Generalitat de Catalunya, 2022[10])The regional government chose to base their methodology on the European Commission’s climate tagging methodology, which uses the OECD DAC Rio Markers and a set of climate coefficients (OECD, 1998[11])

Catalonia’s methodology analyses the climate adaptation and mitigation impact of budget programmes, based on their stated objective. The methodology consists of three steps. The first step analyses whether each programme’s strategy is in line with Rio Markers’ eligibility criteria. Expenditures that do not meet these criteria are labelled as “not targeted”, with a score of 0 points. Expenditures that meet Rio’s eligibility criteria are further classified based on whether they contribute to mitigation or adaptation objectives. Then, the second step consists in determining the degree of contribution of the expenditure to the corresponding marker. Expenditure programmes that are essentially oriented towards the objective set by the Rio Marker are allocated 2 points (“Main”). Expenditure whose objectives are only partially aligned with Rio Markers are allocated 1 point (“Significant”) (Figure 3.3).

Source: Generalitat de Catalunya (2022[10]), Green Budgets: Report on the Climate Perspective in the Budget of the Government of Catalonia, https://aplicacions.economia.gencat.cat/wpres/AppPHP/2022/pdf/VOL_P_CLI.pdf (accessed on 3 May 2022).

Finally, the third step consists in translating the results into a percentage of analysed expenditure that can be considered significant in terms of fighting against climate change. While there is no detailed methodology to derive coefficients from the Rio Markers, Catalonia followed the convention set up by the European Commission, which stipulates that 100% of expenditure with a score of 2 should be counted, 40% for expenditure with a score of 1, and 0% for expenditure lines with a score of 0. Based on this methodology, it was estimated that 19.8% of Catalonia’s 2022 Budget Programme contributes to the fight against climate change (corresponding to 21 budget programmes, 12 focused on mitigation and 9 focused on adaptation) (Generalitat de Catalunya, 2022[10]).

Scotland, United Kingdom: Carbon impact assessments

Scotland’s green budgeting practice uses a form of environmental impact assessment to analyse the carbon footprint of all goods and services purchased by the Scottish government’s annual budget. Based on Section 94 of the 2009 Climate Change (Scotland) Act, a “Carbon Assessment” is included alongside the draft budget, detailing the emissions impact of expenditure proposals within the budget (Scottish Government, 2020[12]). By including this statement within the draft budget, Scotland is also using the green budget statement tool (Box 3.2).

The Carbon Assessment covers direct emissions (e.g. emissions from the generation of electricity consumed by the government) and imported emissions that are generated outside of Scotland in producing the direct and indirect goods and services that the government purchases. The Assessment, however, does not account for “second-round” emissions. For example, the emissions generated from constructing a road paid for by the government would be assessed but the emissions generated from the cars using the road would not be accounted for. Within the annual report, the emissions estimates are broken down by spending portfolio (e.g. justice, health and sport, education and skills, etc.) and by industry (energy, water, and waste; manufacturing; agriculture, forestry, and finishing; etc.) to provide information on which area of spending generates the most emissions. Additionally, data is provided on the total emissions per type of expenditure (current versus capital).

The 2021 Carbon Assessment estimated that the total emissions linked to GBP 5.8 billion in capital expenditure in the 2021-22 Budget amounted to 1.3 million tonnes of carbon dioxide equivalent (MtCO2e), while emissions associated with current expenditure amounted to 8.9 MtCO2e. The expenditure portfolio “Communities and Local Government” had the highest total amount of CO2 emissions, followed by the Health and Sport portfolio and the Transport, Infrastructure, and Connectivity portfolio.

Source: Scottish Government (2021[13]) (2021), Carbon Assessment of the Scottish Budget 2021-22, https://www.gov.scot/publications/carbon-assessment-scottish-budget-2021-22/documents/ (accessed on 8 April 2022).

This stocktake identified ongoing municipal green budgeting practices in Austria, France, and Norway. Interestingly, each of the municipal practices identified uses one of two methods: the “climate budget approach” developed by the city of Oslo or the “climate budgetary assessment” methodology developed by I4CE (Table 3.1). The climate budget approach is a climate governance system that directly links the municipality’s annual carbon budget to its financial budget through the integration of ex-ante analysis of the emissions reduction potential of proposed budget measures into budget and policy decision-making processes. In comparison, the climate assessment of budget is a technical methodology to tag budget expenditure according to its climate impact (favourable, neutral, or harmful) and to provide a snapshot of the climate impact of a region or municipality’s budget, but not in terms of quantified emissions reductions

A third method, City and Local Environmental Accounting and Reporting (CLEAR), was also identified by the stocktake, however, very few of the 18 municipalities that participated in developing the methodology in the early 2000s continue to use it. As such, it is not included in Table 3.1 which only covers existing green budgeting practices. Also, a new approach to budgeting, “participatory budgeting” is excluded from this inventory as it cannot be considered as a green budgeting exercise per se, although many participatory budgeting exercises have increasingly begun to focus on funding green projects, with climate change adaptation or mitigation benefits (Box 3.3. Green Participatory Budgeting). Each of the methods is outlined in detail below with additional information on how municipalities have adapted them to their specific contexts.

Participatory Budgeting is a democratic process in which community members decide on how to spend part of a public budget. This approach builds upon two distinct needs: improving public performance and enhancing the quality of democracy. Participatory budgeting varies from city to city, however, at its core it consists of a city, region, or even country setting aside a portion of its public budget, citizens then submit project proposals, and finally citizens vote on which projects to fund using the allocated budget. The first participatory budget was in Porto Alegre, Brazil in 1989 and has since been adopted by 2 700 governments worldwide. The types of projects funded can be subject to conditionality including thematic restrictions (i.e. green or climate-related, health, education, basic services, etc.), placed-based restrictions (i.e. a specific neighbourhood, district, or city), and actor-based restrictions (i.e. focused on vulnerable communities, marginalised communities, youth, etc.). Participatory budgeting has been implemented across all levels of government, and can even be implemented at the school board or community housing board level.

With the increased urgency to transition to a carbon-neutral economy, many participatory budgeting exercises have increasingly begun to focus on funding green projects, with climate change adaptation or mitigation benefits. The city of Lisbon (Portugal) is a leader in participatory budgeting and green participatory budgeting. Beginning in 2019, the entirety of the allocated participatory budget funds has been directed towards green projects, which for the 2021 cycle totals EUR 2.5 million. Examples of projects funded include the creation of greenspaces on unused wasteland, secure bicycle parking infrastructure, and urban gardens. Another example is the city of Vienna (Austria), which launched a participatory budget for climate action in early 2022. To reach its objectives, the municipality created four new staff positions dedicated to enabling citizens’ participation and civil servant capacity building. In its pilot phase, in 2021, the participatory budget focused on three municipal districts and allocated EUR 6 million in expenditure. This initiative will unfold in parallel with several complementary green measures taken at the municipal level, including the introduction of a climate budget. Among OECD countries, other examples of green participatory budgeting initiatives include Grenoble (France), Brussels (Belgium), and San Pedro Garza Garcia (Mexico).

Source: Cabannes, Y. (2020[14]), Contributions of Participatory Budgeting to Climate Change Adaptation and Mitigation, https://issuu.com/uclgcglu/docs/2020_9_pb_contributions_to_climatechange_adaptatio (accessed on 7 May 2021); Lvovna Gelman, V. and D. Votto (2018[15]), “What if citizens set city budgets? An experiment that captivated the world - Participatory budgeting - Might be abandoned in its birthplace”, https://www.wri.org/insights/what-if-citizens-set-city-budgets-experiment-captivated-world-participatory-budgeting (accessed on 7 May 2021); City of Lisbon (2021[16]), Lisbon Participates (Lisboa participa), https://op.lisboaparticipa.pt/ (accessed on 7 May 2021); İpek, E. (2018[17]), “New approaches in public budgeting”, https://doi.org/10.5772/intechopen.82371; City of Vienna (2022[18]), The Vienna Climate Team (Ab jetzt Ideen beim Wiener Klimateam einreichen), https://www.wien.gv.at/umwelt-klimaschutz/klimateam.html.

Climate budgetary assessments: Examining the climate impact of municipal budgets

The climate budgetary assessment methodology was developed by I4CE in collaboration with five French cities and metropolises7 as well as the national environmental agency (ADEME), the Association of French Mayors (AMF), EIT Climate KIC, and the French Association of Large Cities (France Urbaine) (I4CE, 2020[1]). The methodology was inspired by the green budget tagging methodology used by the French national government. Several regions and departments in France have also adopted the I4CE climate budgetary assessment methodology and adapted it to their respective budgetary contexts (Box 3.4).

The aim of I4CE’s climate budgetary assessment is to examine the climate adaptation and mitigation of a municipality’s budget. Carrying out such an assessment enables elected officials to:

Identify and understand which expenditures have a positive impact on climate adaptation and mitigation and which ones have a negative impact.

Analyse opportunities for redirecting expenditure to improve its alignment with climate objectives.

Monitor developments in the climate impact of the budget year on year.

The methodology is designed to analyse all expenditure in a municipality’s main budget, budget annexes, direct concession budgets, and the budgets from any inter-municipal co-operation bodies that the municipality participates in. Any direct concession or inter-municipal co-operation budgets included in the assessment are prorated based on the level of participation of the municipality. Revenues are not currently covered by the methodology as municipalities in France have limited revenue autonomy; however, I4CE notes that they could be incorporated in the future. The methodology can be applied to both draft budgets and closed administrative accounts, in other words it can be applied ex ante and ex post.

An analysis of the climate impact of expenditure using the I4CE methodology takes place in two steps:

The first step is a high-level analysis of all the expenditure items to classify them into three categories: those with a neutral climate impact, those lacking sufficient information to be classified (labelled “undefined” in the I4CE methodology), and those to be further analysed for their climate impact (labelled “to analyse”).

The second step is applied only to those expenditures classified as “to analyse” by the first step. This subset of expenditures is further analysed according to their climate impact using “structuring hypotheses” and a colour-coded grade scale ranging from favourable to unfavourable.

The structuring hypotheses for climate mitigation are based on France’s net-zero carbon emissions by 2050 objective corresponding to the French National Low-Carbon Strategy (SNBC). I4CE defined nine sectoral structuring hypotheses (for construction, transport infrastructure, vehicle purchase and maintenance, highways, food, waste, energy purchases, energy network and infrastructure, software and new technologies, and green spaces) and six transversal hypotheses (for personnel expenditure, business travel expenses, climate taxes, subsidies, public procurement and sustainable purchasing, carbon compensation). Municipal expenditure is therefore analysed based on these sectoral or transversal hypotheses to determine whether an expense reduces emissions, increases emissions, or has no impact. To assess the impact of expenditure on climate adaptation, the methodology requires a municipality to link the structuring hypotheses to their local adaptation plans and objectives, given the highly localised nature of climate change adaptation actions and impacts. In this way, mitigation expenditure is tagged according to its impact, not its objective.

Source: I4CE (2020[1]), Évaluation climat des budgets des collectivités territoriales: guide méthodologique, https://www.i4ce.org/download/evaluation-climat-des-budgets-des-collectivites-territoriales-guide-methodologique.

Municipalities across France have adapted the climate budgetary assessment methodology to their specific contexts:

The city of Lille and the metropolis of Lille were both members of the I4CE working group that developed the climate budgetary assessment methodology and both chose to adapt the methodology in similar ways. This includes analysing the impact of their budgets on air quality in addition to climate change adaptation and mitigation, as these are the three pillars of the Lille Climate Plan and the Metropolitan Territorial Climate, Air and Energy Plan8 (PCAET) (Métropole Européenne de Lille, 2021[19]). They both chose to pilot the methodology on their 2019 closed administrative accounts before subsequently expanding the exercise to their draft budgets in 2021, establishing both an ex-ante and ex-post assessment. The two local authorities also have the same internal organisation for conducting the climate budgetary assessment, with the Department of Ecological Transition leading the project in collaboration with the Finance Department and other related departments. For the metropolis of Lille, the climate budgetary assessment is part of a broader systematic approach to integrating climate considerations across all of the metropolis’ actions, which also includes a green public procurement strategy and the development of carbon budgets for the metropolitan region (Lommere and Beretta-Delmarre, 2022[20]).

The city of Paris assesses the climate mitigation impact of their budgets. They started in 2020 by applying the methodology to the 2019 closed administrative accounts before subsequently expanding the assessment to their multiannual investment plan (Plan pluriannuel d’investissement - PPI) in 2021 (City of Paris, 2021[21]). Similar to the city and metropolis of Lille, the city of Paris now carries out an ex-ante assessment of their draft budgets and an ex-post assessment of their closed administrative accounts to provide a holistic picture of the climate impact of their current and capital expenditures each year.

The Eurométropole of Strasbourg analyses its draft budgets through three prisms: the Sustainable Development Goals, the climate budgetary assessment, and their PCAET. Their climate budgetary assessment examines the climate mitigation impact of current and capital expenditures in relation to the emissions reduction targets set out in the European metropole’s climate plan adopted in December 2019.

The municipality of Clermont-Ferrand constructed its 2021-2030 multiannual investment program using a socio-climate evaluation tool that integrated the I4CE methodology alongside social impact measurements (Ville de Clermont-Ferrand, 2021[22]). The climate evaluation tool uses a decision tree inspired by I4CE’s methodological approach. The social tool estimates the project contribution to the reduction of social inequalities, social inclusion and social mix, territorial balance, and user and citizen involvement. The results of these two ratings are consolidated and used during budget debates to help elected officials to make informed decisions. Adoption of this approach helped elected officials to be more aware of the cross-cutting nature of climate and social issues and to make better-informed and reasoned public investment decisions.

I4CE’s climate budgetary assessment methodology has received interest from a wide array of stakeholders. For example, ADEME9 incorporated the climate budgetary assessment into their 2021 Cit’ergie10 label criteria, thereby encouraging more municipalities to adopt green budgeting in order to receive the label (ADEME, 2021[23]). Additionally, France Urbaine (a co-creator of the methodology) convened a working group to further disseminate the tool to interested French municipalities and to assist them in implementing it (France Urbaine, 2020[24]). An internal survey, carried out by France Urbaine in April 2022, identified that at least nine members had already carried out a climate budgetary assessment and a further 14 were considering it. The survey also showed the strong interest in extending the budgetary assessment to other environmental and/or social axes including biodiversity, gender equality, and the SDGs (France Urbaine, 2022[25]).

The Climate Budget Approach: Linking carbon budgets to financial budgets

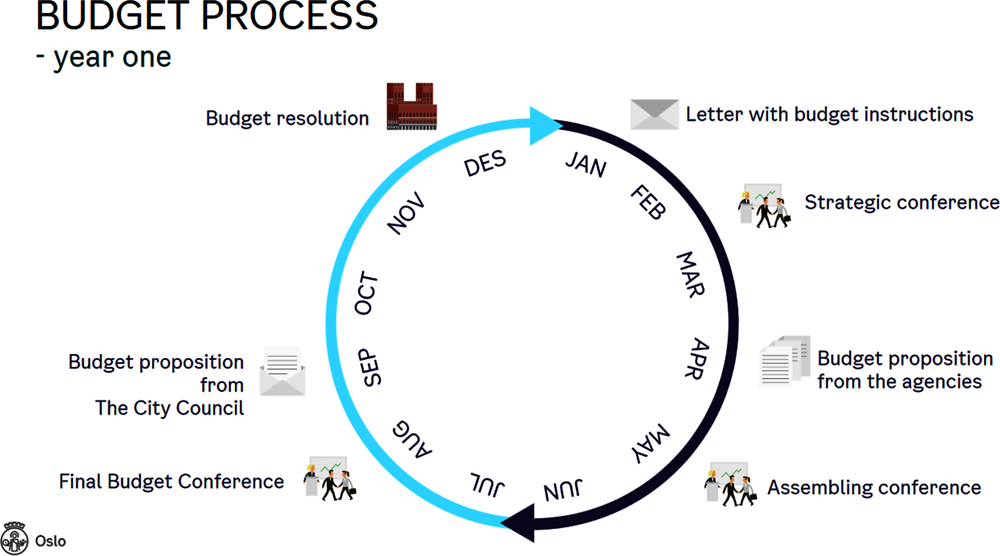

Developed by the city of Oslo (Norway) in 2017, the climate budget is a pioneering approach for budgeting municipal carbon dioxide equivalent (CO2e)11 emissions alongside municipal finances. A municipality’s climate budget transparently outlines what actions the city will take to lower their emissions, who is going to carry out those actions, how the impact of the actions will be reported and how much it will cost.

Oslo developed the climate budget approach to unify its climate governance system and mainstream climate action across the entire administration. Preparing the climate budget is the responsibility of the municipality’s Deputy Mayor of Finance, who collaborates closely with the Department of Environment, the Department of Transport, and the Oslo Climate Agency, a municipal body. The Oslo Climate Agency assists with evaluating the emissions impact of proposed measures (both individually and as a group of measures) and proposes additional measures.

Each year a short-term emissions cap is calculated, taking into account Oslo’s long-term climate goals to reduce greenhouse gas emissions by 95% from 2009 levels by 2030. This cap encompasses scope one emissions only. After the annual emissions cap is set, municipal departments are encouraged to submit project proposals detailing how they will reduce their emissions to meet these targets, the timeline for these reductions, the unit responsible for implementing these actions, and their cost. Not all of the measures proposed have an emissions reduction impact; some are “soft” measures that focus on communication and climate change education. In the 2022 Climate Budget, 15 of 44 measures had quantifiable CO2e emissions reduction impacts. The climate budget covers the geographic area of the city, not just the municipal administration’s emissions, and includes all sectors of the economy. Thus, the budget includes all actions taken by the city government, as well as county and national levels of government, businesses and civil society.

To monitor progress on the mitigation measures, all responsible departments report on the status of implementation and execution of their actions. A barometer with 17 monitoring indicators is published 3 times a year on the city’s website to transparently track the municipality’s progress.

This entire process happens as an integral part of the annual fiscal budgetary cycle and the proposed emission reduction measures are included in the draft budget submitted to City Council (Figure 3.4). In this way, the city can only approve spending plans that have a realistic change of delivering the required greenhouse gas emission reductions and are consistent with the municipality’s climate strategy.

Source: Energy Cities (2020[26]), Climate Budget: A Dialogue with Oslo.

Oslo’s climate budget approach has been widely disseminated and has inspired several other municipalities including Bergen, Hamar, and Trondheim in Norway, Vienna (Austria), and Issy-les-Moulineaux (France) (Box 3.5). Currently, Oslo is working with the organisation C40 Cities on a climate budget pilot programme to disseminate its approach to twelve other cities globally (Box 3.5).

Issy-les-Moulineaux is the first French municipality to have adopted a climate budget inspired by Oslo’s approach. The municipality highlights two reasons in particular as to why they chose this green budgeting approach. First, because this method breaks down a long-term goal (net-zero by 2050) into shorter term goals which motivates action today and not tomorrow; and second because it fosters collaboration amongst all local actors (both public and private) to reduce emissions which is key for the municipality where over one-third of emissions come from businesses.

For their first climate budget, adopted in February 2021, the municipality set an annual cap of 125 000 tonnes of CO2 equivalent, a 3.5% reduction from 2020, which was broken down by sector (residential, industry, services, etc.). The climate budget identifies measures and instruments at all levels of government that will contribute to reducing the municipality’s emissions and the municipality actively co-operates with Grand Paris Seine Ouest and Metropole du Grand Paris to develop and co-ordinate measures in the budget.

To report on its progress, the municipality developed an online, interactive dashboard with indicators that are frequently updated.

Source: Ville d’Issy-les-Moulineaux (2022[27]), Un budget climat pour agir, https://www.issy.com/decouvrir-issy/agir-pour-le-climat/lutte-contre-le-changement-climatique/un-budget-climat-pour-agir#:~:text=S'inspirant%20de%20la%20capitale,%2C%20in%C3%A9dite%2C%20exemplaire%20et%20collective (accessed on 18 April 2022).

The C40 Cities Climate Leadership Group launched a new Climate Budget Pilot in September 2021. The first phase is planned for 2021-22. Thirteen C40 cities (Barcelona, Berlin, London, Los Angeles, Milan, Montreal, Mumbai, New York, Oslo, Paris, Rio de Janeiro, Stockholm and Tshwane) are directly involved in the project and will share work on how to mainstream climate consideration in every municipal decision through new budgeting practices. The project is led by the city of Oslo which has been working on carbon and climate budgets for a few years. The involved cities will work with Oslo on investigating, developing, implementing and further improving the use of climate budgets as a key governance tool to reach the GHG emissions reduction targets.

The first step of the work will be to develop a common understanding of climate budgets and analyse the best way to implement it in a city. Throughout 2022, the project will focus on the definition of strategic priorities, the monitoring and the evaluation of a regular climate budgeting practice, and analysing how climate budgets can be adapted and implemented in different cities, according to their situational context. To disseminate information and learnings from the work sessions, C40 has launched both a newsletter and a specific page on their Knowledge Hub dedicated to climate budgeting. C40 is experiencing great interest from cities on this initiative, and the organisation is aiming to launch a programme on climate budgeting after the pilot concludes.

Source: C40 (2021[28]), Climate Budgets: Why Your City Needs One, https://www.c40knowledgehub.org/s/article/Climate-budgets-why-your-city-needs-one?language=en_US.

City and Local Environmental Accounting and Reporting: The CLEAR method

The City and Local Environmental Accounting and Reporting (CLEAR) method was developed as the first European environmental accounting methodology applicable to subnational governments (Comune di Ferrara, 2003[29]). It was also the first green budgeting methodology to be developed explicitly for subnational governments. A group of 18 Italian municipalities and provinces, as well as the international association of mayors for sustainable development, Les Eco Maires, participated in the project which took place between October 2001 and October 2003 and was 50% co-funded under the European Commission's LIFE-Environment programme.

The objective of the project was to develop a transferable environmental accounting tool to improve environmental decision-making at the subnational level. The tool was also intended to enhance multi-stakeholder engagement processes and existing environmental management systems by providing greater legitimacy to environmental accounting and reporting, which was still an underexplored area of work at the time. Its value added was to bridge the fiscal and environmental domains and serve as a tool to visualise and measure all local commitments and policies with an environmental impact using both physical and financial indicators. Since its experimentation in 2001-03, several Italian municipalities have continued to release ecobilancio developed based on the CLEAR method. The most recent ones include the municipalities of Bergeggi (2022), Varese Ligure (2019), and Reggio Emillia (2018).

The CLEAR methodology is comprised of three steps (Comune di Ferrara, 2003[29]):

The first step involves identifying the commitments and objectives of the administration that have an environmental impact. Once the relevant environmental commitments have been identified, it is possible to flag specific policy programmes and projects being undertaken to fulfil them. These policies and programs are then further classified based on a list of key "macro-competences" of Italian municipalities and provinces linked to the environment (e.g. waste, water treatment, urban development). The final output of this step is a list, for each macro-competence, of the municipality's or province's policies linked to achieving their commitments related to the environment. Using this list, it is possible to then track and calculate the amount of financial resources spent on each macro-competence by a municipality or province and to produce a "financial report".

The second step is to build a parametric system that allows for the measurement of the effects, and verification of the outcomes, of policies implemented to meet the commitments and objectives identified in Step 1. The methodology outlines several possible sources of indicators but stops short of providing a standardized set for all municipalities or provinces to use, noting the importance of accounting for individual local contexts. The chosen set of indicators is then mapped to the list of macro-competence policies obtained in Step 1, such that each policy is linked to an indicator. With this information, it is possible for each municipality or province to produce an “environmental report” showing the evolution in the indicators from year to year.

The third step involves incorporating the results from the second step into the local budgetary decision-making process. By combining the financing and environmental reports, local governments are then able to see how much money they are spending towards achieving their environmental commitments and what the impact of that expenditure is on achieving those targets. This information can then be used to reorient budget expenditure or to reassess policies that weren’t having the desired impact.

References

[23] ADEME (2021), Cit’ergie - Catalogue des 61 mesures du label, https://territoireengagetransitionecologique.ademe.fr/wp-content/uploads/2021/09/Citergie_catalogue-2021.pdf (accessed on 8 April 2022).

[33] ADEME (2021), Programme Territoire Engagé Transition Écologique, https://territoireengagetransitionecologique.ademe.fr/referentiel/organisation-interne/.

[32] Ardi, C. and F. Falcitelli (2007), The Classification of Resource Use and Management Activities and Expenditure - CRUMA, Italian National Institute of Statistics (ISTAT), Rome, https://unstats.un.org/unsd/envaccounting/LondonGroup/meeting12/CRUMA.pdf (accessed on 8 February 2021).

[7] Autonomous Community of Andalusia (2021), Incidence Report of the Climate Change Budgetary Indicators, https://www.juntadeandalucia.es/export/presupuestos2021/clima/clima.pdf (accessed on 6 June 2022).

[9] Autonomous Community of Andalusia (2020), Estudio para integrar la perspectiva de género en el Presupuesto Verde de la Junta de Andalucía.

[5] Autonomous Community of Andalusia (2020), Guía de integración de la perspectiva medioambiental en el presupuesto de la Junta de Andalucía.

[6] Boletín Oficial del Estado (2018), “Ley 8/2018, de 8 de octubre, de medidas frente al cambio climático y para la transición hacia un nuevo modelo energético en Andalucía”, Boletín Oficial del Estado 269, https://www.boe.es/buscar/pdf/2018/BOE-A-2018-15238-consolidado.pdf (accessed on 18 January 2021).

[28] C40 (2021), Climate Budgets: Why Your City Needs One, https://www.c40knowledgehub.org/s/article/Climate-budgets-why-your-city-needs-one?language=en_US.

[14] Cabannes, Y. (2020), Contributions of Participatory Budgeting to Climate Change Adaptation and Mitigation, United Cities and Local Governments, https://issuu.com/uclgcglu/docs/2020_9_pb_contributions_to_climatechange_adaptatio (accessed on 7 May 2021).

[34] CEREMA (2022), The Territorial Climate-Air-Energy Plan (PCAET), http://outil2amenagement.cerema.fr/le-plan-climat-air-energie-territorial-pcaet-r438.html.

[16] City of Lisbon (2021), Lisbon Participates (Lisboa participa), https://op.lisboaparticipa.pt/ (accessed on 7 May 2021).

[21] City of Paris (2021), 2022 Draft Budget, https://cdn.paris.fr/paris/2022/02/10/a49b1b083d7821ada12971fa5940b701.pdf (accessed on 15 April 2022).

[18] City of Vienna (2022), The Vienna Climate Team (Ab jetzt Ideen beim Wiener Klimateam einreichen), https://www.wien.gv.at/umwelt-klimaschutz/klimateam.html.

[29] Comune di Ferrara (2003), Metodo CLEAR City and Local Environmental Accounting and Reporting, http://www.agenda21.ra.it/clear-life/05risultati/metodoclear.pdf (accessed on 18 April 2022).

[30] Département de la Mayenne (2021), Budget vert 2ème édition, https://lamayenne.fr/sites/lamayenne.fr/files/telechargements/Budget_vert_web.pdf (accessed on 8 April 2022).

[31] Département des Alpes-Maritimes (2021), Budget 2022 - Département des Alpes-Maritimes, https://www.departement06.fr/budget/budget-2022-43376.html (accessed on 8 April 2022).

[4] Direzione Generale dei Servizi Finanziari (2021), Ecobilancio 2021 della Regione Sardegna, https://www.regione.sardegna.it/j/v/2592?&s=1&v=9&c=10803&n=10&nodesc=1 (accessed on 6 April 2022).

[26] Energy Cities (2020), Climate Budget: A Dialogue with Oslo.

[35] Eurostat (2020), Glossary: Classification of Environmental Protection Activities (CEPA), Eurostat Statistics Explained, https://ec.europa.eu/eurostat/statistics-explained/index.php/Glossary:Classification_of_environmental_protection_activities_(CEPA) (accessed on 8 February 2021).

[25] France Urbaine (2022), Internal Survey.

[24] France Urbaine (2020), “Les villes peuvent maintenant évaluer l’impact climat de leur budget”, https://franceurbaine.org/actualites/les-villes-peuvent-maintenant-evaluer-limpact-climat-de-leur-budget (accessed on 11 June 2021).

[10] Generalitat de Catalunya (2022), Green Budgets: Report on the Climate Perspective in the Budget of the Government of Catalonia, https://aplicacions.economia.gencat.cat/wpres/AppPHP/2022/pdf/VOL_P_CLI.pdf (accessed on 3 May 2022).

[1] I4CE (2020), Évaluation climat des budgets des collectivités territoriales: guide méthodologique, Institute for Climate Economics, Paris, https://www.i4ce.org/download/evaluation-climat-des-budgets-des-collectivites-territoriales-guide-methodologique.

[17] İpek, E. (2018), “New approaches in public budgeting”, in Açıkgöz, B. (ed.), Public Economics and Finance, IntechOpen, London, https://doi.org/10.5772/intechopen.82371.

[8] Junta de Andalucía (2020), “Número 111, Jueves, 11 de junio de 2020”, Boletín Oficial de la Junta de Andalucía 111, pp. 6-15, https://www.juntadeandalucia.es/boja/2020/111/BOJA20-111-00010-5828-01_00173223.pdf (accessed on 18 January 2021).

[3] La Région Occitanie (2021), Budget Primitif 2022.

[20] Lommere, P. and A. Beretta-Delmarre (2022), “Un budget climatique pour les collectivités ? Retour d’expérience de la Métropole Européenne de Lille et la Ville de Lille”, Construction21.

[15] Lvovna Gelman, V. and D. Votto (2018), “What if citizens set city budgets? An experiment that captivated the world - Participatory budgeting - Might be abandoned in its birthplace”, World Resources Institute, https://www.wri.org/insights/what-if-citizens-set-city-budgets-experiment-captivated-world-participatory-budgeting (accessed on 7 May 2021).

[19] Métropole Européenne de Lille (2021), “Budget climatique à la MEL”, https://www.lillemetropole.fr/sites/default/files/2021-02/20210219_analyse_budget_climatique_BP2021.pdf (accessed on 5 May 2021).

[11] OECD (1998), OECD DAC Rio Markers for Climate - Handbook, OECD, Paris, https://www.oecd.org/dac/environment-development/Revised%20climate%20marker%20handbook_FINAL.pdf.

[2] Région Grand Est (2021), Grand Est Budget 2022, https://www.grandest.fr/wp-content/uploads/2022/01/grand-est22-budget-2022-papok.pdf (accessed on 8 April 2022).

[13] Scottish Government (2021), Carbon Assessment of the Scottish Budget 2021-22, https://www.gov.scot/publications/carbon-assessment-scottish-budget-2021-22/documents/ (accessed on 8 April 2022).

[12] Scottish Government (2020), Carbon Assessment of the 2020-21 Budget, Scottish Government, https://www.gov.scot/publications/carbon-assessment-budget-2020-21/ (accessed on 19 January 2021).

[22] Ville de Clermont-Ferrand (2021), “Evaluation socio-environnementale d’une programmation pluriannuelle d’investissement Retour d’expérience de la Ville de Clermont-Ferrand”, https://www.adcf.org/files/AdCF-Direct/2021.10-Clermont-Ferrand_Evaluation-socio-environnementale-PPI.pdf (accessed on 15 April 2022).

[27] Ville d’Issy-les-Moulineaux (2022), Un budget climat pour agir, https://www.issy.com/decouvrir-issy/agir-pour-le-climat/lutte-contre-le-changement-climatique/un-budget-climat-pour-agir#:~:text=S'inspirant%20de%20la%20capitale,%2C%20in%C3%A9dite%2C%20exemplaire%20et%20collective (accessed on 18 April 2022).

Notes

← 1. The departments of Alpes-Maritimes and Mayenne have both carried out a green budgeting exercise based on the I4CE methodology (Département des Alpes-Maritimes, 2021[31]; Département de la Mayenne, 2021[30]).

← 2. I4CE is a Paris-based think tank, founded by the French National Promotional Bank Caisse des Dépôts and the French Development Agency, with expertise in economics and finance with the mission to support action against climate change.

← 3. CEPA refers to the Classification of Environmental Protection Activities classification system. It is used to classify activities, products, expenditure and other transactions whose primary purpose is environmental protection (Eurostat, 2020[35]).

← 4. CRUMA refers to Classification of Resource Use and Management Activities and Expenditure. Developed by ISTAT (Italian National Institute of Statistics) it classifies activities and expenditures related to natural resource use and management (Ardi and Falcitelli, 2007[32]).

← 5. The ecobilancio for 2021 covered 12 sectors: inland water use and management; forest use and management; protection and rehabilitation of soil, groundwater and surface water; protection of biodiversity and landscape; waste management; use and management of non-renewable energy raw materials; wastewater management; research and development; air and climate protection; wildlife use and management; radiation protection; noise and vibration abatement.

← 6. Officially entitled “Law 8/2018, of October 8, on measures against climate change and for the transition to a new energy model in Andalusia”.

← 7. The city of Paris, the city of Lille, the metropolis of Lille, the Eurométropole of Strasbourg and the metropolis of Lyon.

← 8. The PCAET is a strategic and operational planning tool which allows local governments to holistically address air, energy and climate issues within their territory (CEREMA, 2022[34]).

← 9. ADEME refers to the French Agency for Ecological Transition, which is active in the implementation of energy, environment, and sustainable development policy (ADEME, 2021[33]).

← 10. Cit’ergie refers to an ADEME management and certification program that rewards communities for the implementation of an ambitious climate-air-energy policy (ADEME, 2021[23])

← 11. CO2e refers to carbon dioxide equivalent and encompasses carbon dioxide (CO2) emissions, nitrous oxide (N2O) emissions, and methane (CH4) emissions.