Chapter 6. Access to finance

Introduction

An extensive literature supports the principle that barriers to accessing formal external finance prevent all firms from reaching their optimal size, and that greater access to a broad range of financial products can also aid innovation (Ayyagari et al (2017[1]; Aghion, Fally and Scarpetta, 2007[2]). Well-functioning financial markets that allow firms to access alternative sources of financing, outside informal finance and retained earnings allow competitive firms to invest further in tangible assets, to select more efficient organisational forms (Demirguc-Kunt, Love and Maksimovic, 2006[3]), and to ride out periods of stunted or volatile cash flow (Siedschlag et al., 2014[4]).

While all firms seem to benefit from well-functioning financial markets, studies show that this is particularly critical for small to medium-sized enterprises. Studies indicate that financing obstacles do indeed impede growth in small firms, often to a greater extent than in large firms (Beck et al., 2006[5]). Moreover, SMEs often find it harder to access external financing. Financial institutions are often reluctant to lend to this segment – even though it can be perceived as attractive – given the higher risk profile associated with it. This is largely due to the high failure rate among small firms combined with three challenges implicit in SME lending: information asymmetry, principal/agent problems and transaction costs.

Information asymmetry reflects the fact that the owner/operator of an SME tends to have more accurate information on firm operations than an external financier due to the difficulty of capturing all relationships, activities and funds in formal reporting documents like financial statements (OECD, 2015[6]). Principal/agent problems stem from the risk that once financing is received, an entrepreneur may not use the funds in the way they were intended, potentially increasing the risk of non-repayment. SME financing is more exposed to this risk due to the greater opacity surrounding this type of enterprise and the more limited exit options available to them. Finally, transaction costs tend to be higher in SME lending due to the need to conduct the same, or more rigorous, checks for the appraisal, monitoring and enforcement of lower-value loans as for large loans. These fixed costs reduce the lending profit margin for banks and can drive a wedge between the funding costs of such institutions and their expected return on investment (Beck and de la Torre, 2007[7]). Such costs are largely transferred to SMEs via interest rates and fees and collateral requirements, which can render the total loan costs prohibitively expensive.

These three challenges exist in all economies to some extent, but they tend to be particularly pronounced in emerging economies, where SMEs may lack professional management and financial literacy skills, where gaps may exist in the legal framework to protect creditor rights, and where financiers may have more opportunities to gain acceptable returns from other borrowers given limited market-based financing alternatives, and thus less incentive to invest in the skills and technology required to lend to SMEs. This also appears to be the case in ASEAN. Data collected by the International Finance Corporation suggest that SMEs faced a credit shortage totalling USD 184.7 billion in 2010, while a study of seven ASEAN Member States (AMS) found that SMEs tend to experience credit rationing and high risk premiums, particularly in the lower-income AMS and among SMEs that are small and new (Harvie, Narjoko and Oum, 2013[8]). Moreover, the study found limited access to finance to have a significant impact on the innovation capability and export market participation of SMEs.

This identified competitive disadvantage, coupled with the belief that taking corrective action can create positive spillovers for an economy as a whole, is a key rationale for policy intervention in the field of SME finance, particularly in emerging economies. Policy makers wishing to address these gaps can take various steps. They include providing support for the development of institutions to mitigate credit risk, such as credit information facilities and collateral registries, and adopting rules and regulations to protect creditor rights and to streamline settlement procedures in the event of insolvency. The key is to avoid many of the market distortions associated with government-sponsored SME financing programmes and policies that risk diverting funds away from the most productive and creditworthy enterprises. Policy makers should therefore carefully consider where interventions are needed and which instruments are the most suitable, and carefully monitor both their costs and their benefits.

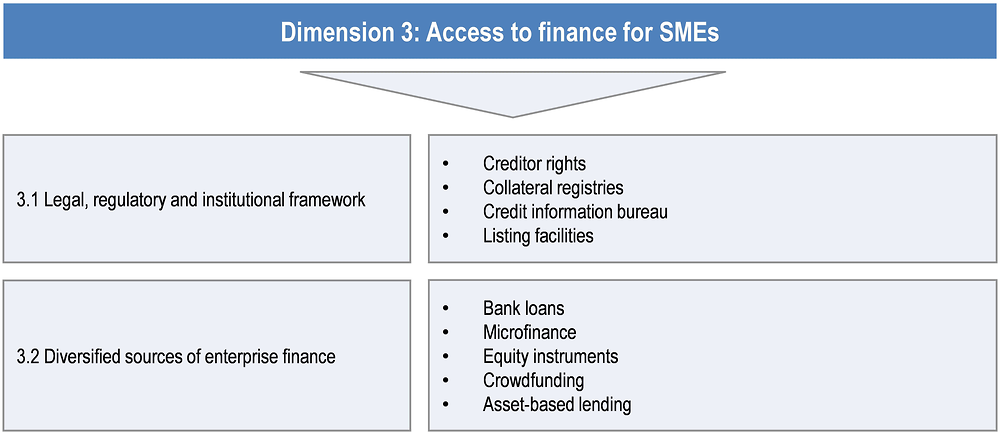

Assessment framework

The framework used to assess policy interventions for boosting SME finance in ASEAN (Dimension 3) covers two sub-dimensions. The first looks at the legal and institutional framework governing SME lending in ASEAN – namely the rules, regulations and facilities available to structure and inform lending to this segment. The second looks more closely at the capacity of financiers in each AMS and the policy instruments provided to support them more directly in lending to SMEs, with the output being the range of financial products available to SMEs in ASEAN. These sub-dimensions and key components are illustrated in Figure 6.1.

In the 2018 ASPI framework, the first sub-dimension is assigned the greatest weight. The logic underpinning this choice is based on various studies that have shown the level of institutional development to be the most significant determinant of cross-country variation in SME access to financing (Beck et al., 2006[5]). The component looks at the extent to which some of the information asymmetries and principal/agent problems implicit in SME lending are mitigated. It looks at the depth and breadth of credit reporting systems, which can reduce information asymmetries faced by lenders in assessing the credit risk of a prospective borrower. It looks at registries for recording the ownership and value of assets, both immovable and movable, which can reduce moral hazard1 and guarantee partial repayment in the event of loan default. It looks at creditor rights, which protect the ability of creditors to reclaim their money in the event of default. Finally, it measures facilities for listing firms, including SMEs.

The second component looks at the products available to SMEs across AMS. Traditional debt finance provided by commercial banks is generally the most common source of external finance for the ordinary and short-term needs of low- to medium-risk SMEs. Generating moderate returns, it is generally characterised by stable cash flow, modest growth, tested business models and access to collateral or guarantees. Policy makers looking to stimulate the flow of this type of credit to SMEs can consider providing (properly structured) guarantees and lines of credit on the supply side, or financial literacy programmes and interest rate subsidies on the demand side.

Another form of debt finance provided to SMEs by financial institutions is microfinance. Microfinance institutions (MFIs) provide relationship-based lending to very low-income borrowers or to borrowers located in remote areas. Alongside loans, most MFIs provide basic financial literacy modules prior to credit allocation, and other advisory services to support business development. Instead of asking for collateral, which many of their clients do not have, most MFIs pool borrowers together, using peer pressure as a buffer to incentivise loan repayment.

Aside from traditional debt finance and microfinance, SMEs can benefit from access to alternative financing instruments. These have been discussed at length by the OECD (2015[6]) and are illustrated in Table 6.1. This group of instruments can be characterised by different degrees of risk and return.

The 2018 ASPI framework covers asset-based finance and equity instruments, but does not score countries on the presence of hybrid instruments and includes only one alternative debt instrument (debt crowdfunding). This limitation is due to the lack of bond markets across the Asia region, including Southeast Asia.

In sum, the 2018 ASPI assessment broadly covers products that could be grouped under three headings: cash flow-based financing, asset-based financing and viability-based financing. The first covers credit lines and loans provided by banks, microfinance institutions and government entities; the second covers products such as leasing, factoring, purchase order finance and warehouse receipts, normally provided by banks; and the third covers equity provided by business angels and specialised equity funds and platforms, including venture capital (VC) funds. These are defined and discussed in greater detail under sub-dimension 3.2.

Analysis

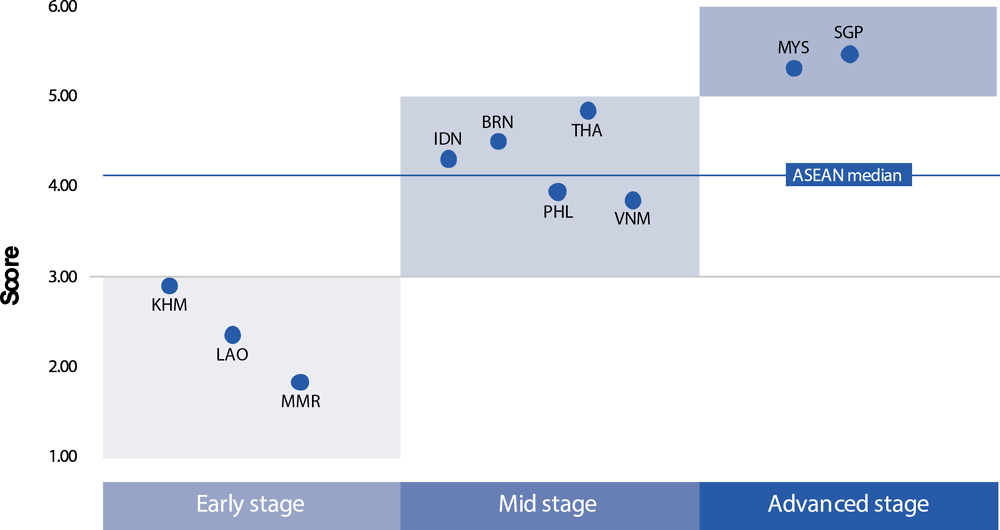

The overall assessment results for Dimension 3 (Access to finance) are presented in Figure 6.2. Countries are scored for each sub-dimension on a scale of 1 to 6, with 6 being the highest. Detailed analysis by sub-dimension follows.

Sub-dimension 3.1: Legal, regulatory and institutional framework

The legal, regulatory and institutional framework is of key importance in mitigating information asymmetries and principal/agent problems in the process of allocating credit to SMEs.

On the debt side, cash flow-based finance, which remains the most common source of SME external financing in OECD countries, depends on the ability of lenders to assess the creditworthiness of SMEs and ascertain future earnings. This process relies on having a credit reporting system in place where lenders can retrieve the credit histories of prospective borrowers. In formulating contracts that protect against credit risk, lenders are greatly assisted by a comprehensive secured transaction framework, reliable and deep asset registries, and strong creditor rights. Asset-based debt financing instruments depend particularly on the environment for secured transactions.

On the equity side, facilities that allow SMEs with high growth potential to access risk capital to finance their growth provide them with an alternative financing source that may be more suited to their needs. Many OECD countries have developed junior boards for their stock exchanges, allowing SMEs at this stage of development to access public equity with lower listing requirements. This facility is most relevant for SMEs that exhibit strong growth prospects and are sufficiently structured to meet a base level of reporting and corporate governance requirements.

The 2018 ASPI framework incorporates these elements, assigning the greatest weight to the legal framework for commercial lending (70%). Credit reporting systems and facilities for SME listing are assigned 20% and 10% respectively.

The median score across ASEAN is high in terms of institutions for credit information reporting, but rather low in terms of the creditor rights/secured transactions framework and facilities for SME listing. There is rather high variation across all groupings, however, with Singapore scoring high across all areas, Brunei Darussalam scoring high for the first and second blocks, and Malaysia and Thailand scoring high for the first and third blocks.

Credit information bureaus: Limited credit information may penalise SMEs

The two main lending technologies used by financial institutions to extend credit to SMEs are relationship lending and transaction-based lending (Berger and Udell, 2002[9]). Transaction-based lending technologies like credit scoring are becoming increasingly preferred in most mature financial markets for lending to SMEs (Berger and Black, 2011[10]), since such methods can lower transaction costs and decrease agency problems. Unlike relationship lending, which relies on “soft” information gathered over time by a loan officer, transaction-based lending often relies on “hard” quantitative data for ascertaining the creditworthiness of a prospective borrower (Berger and Udell, 2002[9]).

Credit reporting systems play an important role in the facilitation of transaction-based lending. All but one AMS have a credit reporting system in place. In most countries this service is provided by private credit bureaus or a mix of private credit bureaux and public credit registries. The exceptions are Brunei Darussalam and Lao PDR, which use a public credit registry. Since public credit registries are generally created for the purpose of monitoring system-wide banking risk, they tend to collect only data on loans above a certain threshold, meaning that private credit bureaus can be more effective at increasing the coverage of smaller firms (Hengel, 2010[11]). Brunei Darussalam’s credit registry, however, is a full credit bureau that collects both positive and negative credit information on all types of loan regardless of the amount. The country that does not yet have a credit reporting system in place, Myanmar, has made important progress since the 2014 ASPI assessment by enacting a regulation in March 2017 to allow for the establishment of credit bureaus. The Myanmar Banks Association and NSP Holdings of Singapore had signed a memorandum of understanding (MoU) in 2016 to set up a credit bureau in the country.

Three AMS – Indonesia, Malaysia and Viet Nam – use a dual credit-reporting system. In these countries, a regulation was passed allowing for the creation of private credit bureaus. These credit bureaus work alongside the registry, building on its data to provide credit scoring services. Other AMS appear to be considering the adoption of similar models to increase the depth and breadth of credit information coverage. In Lao PDR, for instance, where systems currently cover only 11.2% of the adult population, the central bank is in talks with international financial institutions on how to reform its credit reporting system to allow for the creation of private credit bureaus in the country.

Where credit information is available, it is generally accessible and comprehensive. In all remaining AMS except Cambodia, financial institutions can access a borrower’s credit information online. In terms of the depth of information, positive and negative credit data are collected in all remaining AMS except one (Cambodia), and in seven countries at least two years of historical data are distributed (all except Cambodia and the Philippines). However, coverage provided by credit reporting systems is highly varied – ranging from 73.4% of the adult population in Brunei Darussalam to 8% of the adult population in the Philippines. In four AMS, these systems became operational over the past six years. The Philippines is currently working on reforming its credit reporting system to increase coverage. In 2008, it passed the Credit Information System Act and created a public corporation, entitled the CIC, which is responsible for collecting, collating and disseminating information provided by private credit bureaus. One of its key achievements has been the issuance of a memorandum by the Securities and Exchange Commission requiring all financial institutions to submit their five-year historical and current credit data by a stipulated date.2

The Strategic Action Plan for SME Development (SAP SMED) 2016-25 lists the harmonisation of credit reporting, and potentially the creation of an ASEAN-level credit information system, as a strategic long-term goal. The findings of the 2018 ASPI suggest that important progress has taken place over the last ten years in building up credit information systems across ASEAN. However, there remain significant disparities in the breadth and depth of coverage across AMS that must be addressed as a first step. Promising signs can already be observed in cross-border co-operation, for instance with the passage of an MoU between the Myanmar Banks Association and NSP Holdings of Singapore. Once these disparities have been decreased, ASEAN policy makers could look at finding ways to foster mutual recognition and common disclosure requirements among national credit information bureaus and registries, and at harmonising the regulation and standards that currently govern credit information reporting.

Legal and regulatory framework: Some gaps remains in secured transaction laws

The legal and regulatory environment for commercial lending also affects the ability of banks to utilise contracting elements that enable them to overcome information opacity and principal/agent problems (Berger and Udell, 2006[12]; OECD, 2015[6]) and thereby reduce their credit risk. One of the most common of these elements in SME financing is securitisation. However, the efficacy of securitisation as a credit-risk mitigation technology depends on a country’s legal framework for secured transactions, its creditor rights and its systems for registering assets. These conditions also influence the viability of asset-based lending.

All AMS have a cadastre in place for registering immovable property, though in some countries, like Cambodia, these systems are still being piloted and are therefore not yet fully functional. Nine AMS have a movable assets register in place (all except Myanmar), but in the Philippines this remains a document-based system covered by the Registry of Deeds. Five AMS3 – Brunei Darussalam, Cambodia, Indonesia, Lao PDR and Viet Nam – have a centralised registry for listing movable assets4, and in six AMS – Brunei Darussalam, Cambodia, Indonesia, Lao PDR, Malaysia and Singapore – third parties can conduct registrations, amendments, cancellations and searches online. In only three AMS – Cambodia, Lao PDR and Brunei Darussalam – are these registries notice-based, whereby potential creditors can easily assess their ranking priority in potential claims over specific collateralised assets.

Credit risk can be decreased not only by having access to a reliable and comprehensive asset registry, but also by having clearly crafted rules over perfection and priority in case of competing claims on or interests in the same assets (World Bank, 2015[13]). According to World Bank (2017a[14]) data, only Malaysia and Singapore currently have clear rules over perfection and priority in place, while Brunei Darussalam and Cambodia have completed most of the reforms required. In Brunei Darussalam, the Secured Transactions Order (2016) includes provisions on the perfection of security interests (Part IV) as well as the order of priority between security interests (Part VI). Non-possessory security rights such as liens and hypothecation are only recognised without a specific description of the collateral in Brunei Darussalam, Cambodia, Malaysia, Singapore and Viet Nam.

Few AMS have a sufficient legal framework overall for conducting secured transactions, according to the World Bank Doing Business methodology. In the World Bank’s 2018 assessment, only the three civil law countries (Cambodia, Lao PDR and Viet Nam) are scored as having a complete legal framework in place. Outside ASEAN, many common-law jurisdictions are currently reviewing their secured transaction frameworks to ascertain whether and how reform is needed. Canada, New Zealand, Australia and Jersey have recently enacted Personal Property Securities Registration Act regimes based on Article 9 of the US Uniform Commercial Code, which is generally held as a model for secured transaction reform in common-law countries (see Box 6.1). Brunei Darussalam, which operates under common law in commercial affairs, has recently overhauled its secured transaction framework, removing many of the ambiguities over perfection, priority and notification of collaterals.5 Thailand has also enhanced its secured transaction laws through the introduction in 2016 of its Business Collateral Act, which increases the range of eligible securities and the enforcement rights of secured creditors.

Many common law countries currently lack a unified statute for secured transactions, meaning that such transactions tend to be governed by a number of different laws. This can increase complexity in the legal framework governing secured transactions, with treatment varying based on type of legal entity. Without clear rules governing secured transactions, particularly on the perfection and priority of collaterised assets, financial institutions may be reluctant to make use of hedging instruments such as securitisation to extend loans. This can particularly penalise SMEs, which may have fewer assets to collatarise and not be covered under existing secured transaction laws.1

With this in mind a number of common laws have started to amend domestic legislation governing the possession and transference of security interests. Many have adopted a Personal Property Security Act (PPSA) regime, which establishes a single national regime governing security interests in personal property, covering most tangible and intangible assets, including intellectual property.

New Zealand introduced its PPSA regime in 1999. Some good practice features of the regime and its implementation include:

Design features:

-

1. Uniform rules: a wide range of security devices (including fixed and floating charges) were replaced with a single concept, that of the security interest. All are now subject to the same rules of registration, priority and, generally, enforcement.

-

2. Perfection flexibility: a security interest can be perfected by registration, possession or (in the case of financial collateral) control. Registration can also be done in advance of the security being created (“notice filing”).

-

3. Clearer ownership: a national, centralised, electronic registry was established.

-

4. Priority coherence: a clear set of rules were introduced to govern competing claims on security interests. Priority is typically determined based on the date of perfection.

Implementation features:

-

1. Involvement of stakeholders early on in reform process.

-

2. Justification of departure from status quo.

-

3. Continued to educate stakeholders on nature of reforms post-implementation.

Changes to the legal framework governing secured transactions can be politically contentious, particularly among legal professionals. However surveys indicate a high approval rating for the regime among practitioners in New Zealand (Gedye, 2012).2

← 1. In many common law countries secured transactions are principally governed under the country’s Company Act, meaning that only incorporated entities tend to be covered and a highly restrictive regime is applied to unincorporated entities (such as sole proprietorships and partnerships).

← 2. Gedye (2012) cites an approval rating of 95%.

Source: SSM (2017), https://www.ssm.com.my/sites/default/files/acts/konsultasi_awam_ppsr.pdf; STR (2017) https://securedtransactionslawreformproject.org/.

In terms of enforcement rules, secured creditors are paid first in the event of either business liquidation or a debtor defaulting outside an insolvency procedure in only four countries: Brunei Darussalam, Malaysia, Singapore and Thailand. In three countries – Indonesia, Lao PDR and Myanmar – they are paid first in neither case. In four countries – Brunei Darussalam, Cambodia, Indonesia and the Philippines – the debtor can file a stay on enforcement of a security interest. In Brunei Darussalam, under the Secured Transaction Order, this stay is automatic when the debtor is insolvent. However, in eight AMS, a range of out-of-court debt resolution procedures are possible. The only countries that face some obstacles in this area are Indonesia and the Philippines, according to World Bank data. In Indonesia, auction houses generally insist that banks can only liquidate collateral with a court order, meaning that out-of-court debt resolution is complicated in practice if not by law. In addition, creditor rights are negatively affected by loopholes in Indonesia’s Bankruptcy Law, last amended in 2008, whereby creditors can be prevented from enforcing their security interest for up to 270 days if the debtor obtains a debt moratorium, or 90 days of s/he is declared bankrupt. Strong creditor rights are particularly important in countries that demonstrate lower judicial efficiency – for instance in Cambodia, Lao PDR, Myanmar and Viet Nam, where procedures to resolve insolvency can take five years or more (World Bank, 2017a[14]).

Stock market operations: Most AMS have launched a junior board for SME listing

All AMS have a stock exchange except Brunei Darussalam, which is due to establish one in the next few years. These stock exchanges vary in depth and liquidity – capitalisation ranges from around 228% of GDP in Singapore to 40% in Viet Nam, and turnover from 68% in Thailand to 13% in the Philippines.6 Lao PDR and Cambodia have had a stock exchange in place since 2012, and Myanmar since 2016, but currently all three exchanges have fewer than ten firms registered, with most firms being state-owned enterprises. In these three countries, therefore, relatively few enterprises of any size have access to public equity financing, and this constraint is particularly acute for SMEs. In the six countries with the deepest stock markets, the number of listed companies per 10 000 people is only particularly substantial in Singapore and Malaysia, which have listed 8 542.5 and 2 863.4 companies per 10 000 people respectively.7 In Indonesia, the Philippines, Thailand and Viet Nam, the figure ranges from 205.7 (Indonesia) to 952.6 (Thailand), skewed towards the lower end (World Bank, 2018[15]).

Note: Dataset does not include recent data for Brunei Darussalam, Cambodia, Lao PDR and Myanmar.

Source: World Bank (2018), http://www.worldbank.org/en/publication/gfdr/data/financial-structure-database.

Six AMS – Cambodia, Indonesia, Malaysia, the Philippines, Thailand and Singapore – have also established a junior board on which SMEs can list. Malaysia, Singapore and Thailand have had such facilities in place for ten years or more and have more than 100 listed firms. Indonesia launched its junior board, the IDX Incubator, this year, with the goal of listing 1 000 “unicorn” start-ups with a total market capitalisation of USD 1 billion by 2020. In 2015, Cambodia launched its junior board, called the Growth Board, for the CSX, and an Excellence Programme for building SME capacity to meet listing requirements, although the board remains relatively shallow and illiquid. In Viet Nam a similar proposal is being considered, though various Vietnamese start-ups have criticised the measure, contending that few start-ups in the country have the valuation size and structure for the facility to reach any sustainable level of depth and liquidity. The most advanced junior board in the region is the Singapore’s Catalist. As of December 2017, it had 201 listed companies (200 primary listings and 1 IPO) with a combined market capitalisation of SGD 12.8 billion (Singapore dollars) (SGX, 2017[16]).

To facilitate the listing of small firms and increase market capitalisation, some AMS provide support programmes for SMEs. The Securities and Exchange Commission in Thailand ran two programmes from 2012-16, namely the Scheme of The New Stock, Pride of the Province, and the Scheme of Creative Innovation Stock, Pride of Thai. Thailand’s Department of Industrial Promotion is currently running a programme preparing entrepreneurs to list on the Market for Alternative Investment (MAI) within three years of programme inception. In Singapore, such programmes are also provided, but they are delegated to the private sector, specifically the country’s stock exchange (SGX). In carrying out these programmes, the SGX is known to partner with the public sector. For instance, it announced in 2017 that it would be partnering with Exploit Technologies Pte Ltd, the commercialisation arm of the Agency for Science, Technology and Research (A*Star), to select high-potential tech start-ups and SMEs and support them in raising growth capital on private or public capital markets in Singapore. The advantage of such a scheme is that it enables founders to tap into A*Star’s research and development (R&D) and product development capabilities alongside SGX’s knowledge of listing requirements and marketing.

Viet Nam does not yet have a junior board, but a secondary market, UPCoM, was created for the Hanoi Exchange (HNX) in 2009. At the time of writing, UPCoM counted 710 listed companies with a total market capitalisation USD 27.4 billion, making it more than double the size of the HNX main board.8 The market enables enterprises of different sizes to access equity financing with no listing fees. Since 2017, HNX has begun to categorise UPCoM listed firms by size in order to better monitor and supervise the market. Currently, 40 UPCoM Large, 291 UPCoM Medium and 379 UPCoM Small companies are listed. HNX is also looking to establish a market for start-up firms. In Malaysia, the LEAP Market (Leading Entrepreneur Accelerator Platform) was launched on 25 July 2017, with the aim of providing SMEs with an alternative platform to raise equity funds in an efficient, fast and transparent manner. Aside from fundraising, the platform provides SMEs with an opportunity to raise their visibility, by being a listed entity, and to enhance their corporate governance and operational standards. Listing on the LEAP Market could also enable small firms to take a first step towards listing on the country’s ACE9 or Main Market platforms in the future. Due to the risks associated with investing in companies that are at developmental stage, only sophisticated investors (those individuals and corporations that fulfil certain income or net asset-value thresholds) can invest in companies listed on the LEAP Market. The creation of the LEAP Market is part of an accelerated push by the government to stimulate alternative financing in the country.

Stock exchange consolidation has taken place within various AMS over recent years. In the Philippines, the Manila Stock Exchange and the Makati Stock Exchange were merged in 1992 to form the Philippines Stock Exchange (PSE). In Indonesia, the Surabaya Stock Exchange and the Jakarta Stock Exchange were merged in 2007 to form the Indonesia Stock Exchange (IDX). In Viet Nam, two stock exchanges still exist, the Hanoi Stock Exchange, formed in 2005, and the Ho Chi Minh Stock Exchange, formed in 2000. Steps are currently underway to merge these two markets, which it is hoped will increase transparency and foreign investment. The authorities expect this process to be completed in 2018. Such processes can increase the scale and solidity of listing facilities, allowing them more room to develop specialised SME-platforms.

Sub-dimension 3.2: Diversified sources of enterprise financing

SMEs require access to a range of financial products suitable to their stage of development, particularly if they are to bridge the “growth capital gap” (OECD, 2015[6]). Three types of financial products can be discerned in the literature: cash flow-based financing, asset-based financing and viability-based financing.

The first covers traditional debt, usually provided by commercial banks. This type of financing is contingent on future cash flow as the principal source of repayment, and a pre-decided share of the principal and interest must be repaid at regular intervals regardless of the performance of the investment or the financial situation of the borrower (OECD, 2015[6]). It is the most common form of SME financing found in most markets, since it tends to be less risky for the lender and therefore cheaper than other forms of financing. It is generally well suited to serve the day-to-day and short-term financing needs of SMEs that are able to demonstrate stable cash flow, modest growth, tested business models and access to collateral or sureties (OECD, 2015[6]). The credit allocation decision for these products is based on an appraisal of estimated future income along with collateral support.

The second type of product covers lending that is based on the liquidation value of a particular asset owned by or due to the firm. Common assets include accounts receivable (factoring), letters of credit (trade finance), agricultural commodities (warehouse receipts), purchase orders (purchase order finance), and vehicles, machinery and equipment (leasing). This type of financing often allows for increased repayment flexibility and quicker access to credit or goods, which can be a useful facility for a growing firm that faces temporary and immediate cash flow shortages, for instance in fulfilling a particular order. Such instruments are often provided with a revolving facility, which allows for more flexibility than instalment credit by allowing firms to access additional funds once advances on an initial asset are paid off (OECD, 2015[6]). This can be a helpful facility for bridging recurring or cyclical cash flow shortages.

The third product type covers all instruments targeted at high-potential SMEs, where investors take on a high level of investment risk in return for a share of future profits. This type of financing is based on the perceived viability of a firm’s business model and the profits to be gained from it. It covers all forms of public equity (stocks and shares) and private equity (venture capital and private equity), as well as certain classes of mezzanine finance. The financing allocation decision for these products is either based on direct contact with the firm (business angels and venture capital or other forms of private equity), often supported by fund managers in the case of non-VC private equity, or indirect communication via company accounts and activity reports regulated by a designated government authority (public equity).

The 2018 ASPI covers all three product types, grouping asset-based and equity financing together as alternative sources of enterprise finance. Cash-flow based debt is also split into two categories: i) conventional credit lines and loans provided by banks; and ii) microfinance. Policies that support access to bank credit are assigned the greatest weight, accounting for 70% of the overall score. Policies to support microfinance are assigned the second highest weight, or 20%, given the need to increase financial inclusion in many AMS. Policies to stimulate alternative sources of enterprise finance are assigned a weight of 10%.

The median score across AMS is generally the same in all three product groups, though with quite high cross-country variation in terms of the level of policies to facilitate access to bank credit, reflecting disparities in income levels across ASEAN. Of the three, fewer policy interventions seem to be taking place in the area of stimulating SME access to alternative financing instruments, a pattern that can also be observed in OECD countries.

Bank credit: Many interventions for SMEs flow through state-owned institutions

The 2018 ASPI indicator covering policies to stimulate bank credit scores countries on two main instruments. The first, a credit guarantee scheme (CGS), is generally regarded as a more “market-friendly” and scalable instrument for increasing general credit to SMEs. It provides banks with an additional surety in the event of loan default, thereby decreasing the credit risks faced by banks and thus often increasing the extension and improving the contracting terms of debt products. The second, an export financing scheme, is an SME financing tool that supports one of the main priorities of the ASEAN community. It provides exporters with a concessional short-term financing facility, with the objective of increasing a country’s overall exports.

Five ASEAN countries have a public or public/private credit guarantee scheme in place,10 and six AMS have government-sponsored export financing schemes. Brunei Darussalam, Cambodia, Lao PDR and Myanmar currently have neither facility, though the necessity of the former is limited in Brunei Darussalam given its small size and well capitalised banking sector. Singapore has no credit guarantee scheme, but Enterprise Singapore (SPRING at the time of information gathering and validation) continues to offer a range of risk-sharing products with eligible banks – including a SGD 2 billion SME Working Capital Loan Programme and a SGD 500 million Venture Debt Programme. In both schemes, SPRING covered 50% of loan default risks.

Many of the programmes designed to increase bank credit for SMEs appear to flow through state-owned entities. For instance, of the six AMS that have government-funded export financing schemes in place, five are run through EXIM banks, as is the case in Indonesia, Malaysia, the Philippines, Thailand and Viet Nam. This is a popular model in emerging and developing markets, where operational risks are generally higher, and thus the backing of a sovereign entity can facilitate financiers to take on a higher level of credit risk. In the remaining country with export financing schemes, Singapore, such instruments are provided by Enterprise Singapore (IE Singapore at the time of information gathering and validation) as dedicated export credit lines to commercial banks. Two main products are available: the Internationalisation Finance Scheme and the Trade Credit Insurance Scheme. The second mitigates the risk faced by would-be and current SME exporters, while the first enables SMEs to access up to SGD 30 million in credit facilities to support overseas expansion. In Brunei Darussalam, DARe has partnered with a local state-owned bank to provide a Microcredit Financing Scheme, which provides up to BND 15 000 to eligible firms with no collateral requirement.

Of the five countries with a public or public/private credit guarantee scheme, Malaysia and the Philippines have multiple schemes running alongside each other, while Indonesia and the Philippines have funded a network of schemes that are run at the provincial level. These approaches are generally intended to increase outreach, but may lack co-ordination and thus risk duplication of effort. In some countries, a network approach may mean that schemes become operational more often in regions that already have higher capacity, and thus perhaps lower need, as appears to be the case in Viet Nam. Most schemes provide portfolio guarantees as the dominant type of support, though some also offer individual guarantees. Some AMS have also developed credit enhancement programmes for their CGS in order to increase financial inclusion. In Malaysia, the Credit Guarantee Corporation introduced a Credit Enhancer Scheme in 2006 that allows for risk-adjusted pricing to be applied to SMEs. In the Philippines, the Credit Surety Fund was created in 2008 to facilitate the financing of riskier SMEs by pooling monetary contributions from a wide range of stakeholders, including co-operatives, non-governmental organisations (NGOs) and local government units, thereby reducing default risks by lowering information opacity faced by commercial banks.

Credit guarantee schemes are an instrument under which a guarantor contracts with a creditor to repay a proportion of a loan or loan portfolio disbursed to a third party in the event of default. This arrangement can help to stimulate bank lending to SMEs by providing banks with a security to lend to firms that are otherwise creditworthy but do not have sufficient collateral to obtain a loan. In principal, it should have the effect of reducing both credit rationing and collateral requirements, though such a scheme should be carefully designed to ensure it achieves its additionality and sustainability objectives.1

A few design considerations

Four initial elements should be formulated in the design of a CGS:

-

The mission statement. This is the basis on which the scheme’s operational objectives will be set, and outlines its purpose and objectives to future stakeholders (for instance, partner banks).

-

The delivery mechanism. Guarantees can be disbursed to cover an individual loan or a portfolio of loans. The advantage of the latter is that it entails lower operational costs and more rapid disbursement. The advantage of the former is that it allows the scheme’s owners to have a greater say in the type of firms that are guaranteed, and to have greater oversight for monitoring purposes. In either case, credit appraisal should always be performed by the partner bank.

-

Ownership of the scheme. The scheme’s owners are those who provide funds and perform executive governance of the entity. They can be public, private, public/private or international bodies. In many OECD countries, a public/private model is favoured, but the model selected will depend on available funding, oversight requirements and the institutional setting of each country.

-

The target group. This defines the scope of the scheme. It will determine whether the scheme targets specific sectors and/or regions, and how firm size is measured. Almost all CGS in OECD countries target SMEs across a range of sectors. Where schemes are mono-sectoral, they often target agricultural or rural SMEs,2 though these often also come with a much higher level of implicit lending risk.

Good practices in designing an additional and sustainable CGS

CGS must be carefully designed. A number of features could be considered to increase the scheme’s additionality and sustainability:

-

A partial coverage rate. In most OECD countries, guarantees cover only a share of the loan’s principal. This is designed to mitigate moral hazard by ensuring that the creditor remains partially liable in the event of default and thus does not extend loans to non-creditworthy SMEs. Generally a rate of not higher than 70%-80% is advised.3

-

A competitive bank selection process. Creating a competitive environment around the disbursement of guarantees, particularly when the scheme is first implemented, will encourage banks to strive harder to meet its additionality aims. Chile’s FOGAPE scheme auctions its guarantees to commercial banks, which must then bid for guarantees. The successful bidder is the one that is prepared to offer the highest leverage and the lowest interest rates.

-

Risk-adjusted fees. In principal, risk-adjusted fees enable the scheme to offset higher credit risk (and thus greater likelihood of default) through higher pricing. Japan’s Credit Guarantee Corporations charge annual fees indexed to the borrower’s credit risk, ranging from 0.5-2.2%, and these are determined by the scheme’s credit-risk database (OECD, 2013).

-

A diversified portfolio. Portfolio diversification reduces a scheme’s exposure to co-variant risks. Diversification can be achieved by guaranteeing firms from a range of sectors or regions, or by guaranteeing loans with a range of maturities or loan purposes. Lithuania’s ACGF is an example of a sectoral-focused scheme that has achieved diversification by extending guarantees to activities that are ancillary to agriculture, and by blending the type of agricultural activities it supports, to cover activities that have both short-term and long-term business cycles (crop production and livestock breeding, respectively).

← 1. The additionality of a CGS is defined in two parts, one being the scheme’s financial additionality and the other its economic additionality. Financial additionality refers to the increase in the volume of credit flowing towards viable SMEs as a result of the scheme. Specifically, it refers to guaranteed credit that would not have been provided without the guarantee, or more favourable credit conditions that emerge as a result of the guarantee – for instance, longer maturities or lower interest rates. Economic additionality describes the effect of increased access to finance on overall economic welfare. This is generally measured in terms of increased sales, employment, investment or innovation by the supported SME or, at the macro level, by increased competitiveness and growth. Sustainability refers to the CGS’s ability to cover its own costs while increasing leverage towards its target group. A sustainable scheme will also encourage more reliable partner banks to trust the value of the scheme’s guarantees, thus increasing the volume of credit extended to target firms. A scheme’s sustainability will depend on its ability to encourage lender participation so as to achieve a sufficient volume of credit.

← 2. Beck et al. (2009[30]) report a median coverage ratio of 80% across 76 schemes worldwide, but a lower rate is usually advised for schemes that are more risk-averse (such as those that cannot count on public subsidies) or that are exposed to higher risk (such as those that target only one sector).

← 3. Beck et al. (2009) noted that, in a survey of 76 partial guarantee schemes around the world, 29 were mono-sectoral schemes and 12 of these were targeted at agricultural or rural enterprises.

Source: OECD (2013); Beck et al. (2009), https://doi.org/10.1016/j.jfs.2008.12.003.

In terms of performance, the CGS in Malaysia and the Philippines seem to demonstrate a low net loss rate, but in Indonesia, Thailand and Viet Nam the net loss rate is higher than commonly advised. Few of the credit guarantee funds in Viet Nam are fully operational, and banks have reported limited trust in the programme (Le, 2016[17]).

Policy makers can tap into a range of other instruments to stimulate bank credit to SMEs, though many of these risk introducing market distortions and therefore are not scored in the ASPI framework. The most common instrument used across ASEAN as a whole tends to be the provision of a credit line to banks for SME lending, which is currently provided in eight countries (all except Brunei Darussalam and Myanmar). In Cambodia, Indonesia, the Philippines and Malaysia, interest rate subsidies are provided. In two AMS – Indonesia and the Philippines – mandatory lending programmes have been implemented. The first dates back to 2012, when Bank Indonesia issued a regulation stipulating that banks should allocate 20% of their total loan portfolios to SMEs by 2018. The second is covered by the Philippines’ Magna Carta for MSMEs, which states that until 2018 (ten years post the act coming into effect) all lending institutions registered with the central bank should direct at least 8% of their total loan portfolio to MSMEs. Both of these programmes are due to expire in 2018. Anecdotal evidence suggests that the impact of these mandatory lending programmes is limited. In the Philippines, for instance, banks tend to prefer to pay the fine for non-compliance or to channel funds to firms that deliberately understate their assets in order to qualify as an SME (Aldaba, 2011[18]).

One of the most substantial SME financing schemes in the region is the Kredit Usaha Rakyat (KUR) in Indonesia. This scheme started as a financial access programme, providing partial credit guarantees for loans to micro and small-to-medium-sized enterprises. The original programme ran from 2009 to 2014, with outstanding loans supported by the KUR totalling IDR 49.5 trillion (Indonesian rupiah) by 2014, or 14% of all outstanding loans to MSMEs (World Bank, 2017b[19]). Similar to other schemes mentioned previously, the majority of the KUR is channelled through state-owned banks: 85% of total KUR-backed guarantees were disbursed by the BRI, Mandiri and BNI banks. Between 2009 and 2014, BRI alone disbursed 65% of the entire KUR programme (World Bank, 2017b[19]). In 2015, it was decided to continue the scheme, but to transmute it into more of a subsidised credit programme, with an interest rate subsidy component added to lower the cost of financing for MSMEs. The programme represents a sizeable investment by the government of Indonesia, sending a clear message of its commitment to financial inclusion. However, in an assessment of the KUR, the World Bank expressed concern over two new additions to the scheme, namely the interest rate subsidy component and the fact that it no longer limits KUR-backed loans to first-time borrowers. Both are likely to substantially increase the fiscal cost of the scheme for the government of Indonesia and to reduce its additionality over the long term (World Bank, 2017b[19])

Finally, seven AMS have established a development bank to address the missing market for SME finance. These are the Rural Development Bank in Cambodia, the Lao Development Bank, the Bank Perusahaan Kecil dan Sederhana Malaysia Berhad (SME Bank) in Malaysia, the Small and Medium Industrial Development Bank in Myanmar, the Development Bank of the Philippines and the Small and Medium Enterprise Development Bank of Thailand. An important development is the establishment in Brunei Darussalam of an SME Bank in late 2017 (after this ASPI assessment was completed). This bank, called Bank Usahawan, started its operations in 2018, and operates in accordance with Islamic Sharia principles. In Indonesia, the government is a majority shareholder of BRI, a commercial bank that specialises in providing banking services to MSMEs.

Microfinance: AMS are increasing regulatory oversight of MFIs

Eight countries in ASEAN11 have an active network of non-bank microfinance providers. In Thailand and Viet Nam, credit unions and financial co-operatives appear to dominate, with each country hosting 1 986 and 1 167 institutions respectively in 2016, according to IMF data. According to the same data, there were no MFI institutions in Thailand that year, and just four MFIs in Viet Nam, which were of the deposit-taking variety. Lao PDR and the Philippines have a mix of credit unions/financial co-operatives and microfinance institutions, with the latter being more dominant in Lao PDR (it had 76 MFIs in 2016, mostly of the non-deposit taking variety, relative to 28 credit unions/financial co-operatives). Myanmar has no credit unions/financial co-operatives, but 167 microfinance institutions, mostly deposit-taking (108). In Malaysia co-operatives and two large MFIs (non-deposit taking) are the main sources of non-bank microfinancing, but the country’s microfinancing needs are principally served through banks. No data is available for Cambodia, though there are eight deposit-taking MFIs, 56 non-deposit taking MFIs and 18 rural credit operators registered with the Cambodian Microfinance Association. The majority of these entities provide loans to households rather than firms.

In Cambodia, Lao PDR, the Philippines, Myanmar and Viet Nam, microfinance activities have principally been catalysed by NGOs, both international and domestic. In the remaining three countries – Indonesia, Malaysia and Thailand – microfinance activities have been driven by the government. The largest microfinance programme in Thailand is the government-sponsored Village and Urban Revolving Fund – a scheme with a network of 80 000 village banks and 8.5 million borrowers in 2011, and one of the largest in the world (The Economist, 2013[20]). In Lao PDR the “village bank” model of microfinance also predominates, but these were set up by NGOs and donor agencies after the country began to open up in the 1990s. Accurate data on these village banks is scarce, though it has been estimated that members numbered around 430 000 (6% of the Laotian population) in 2011 and held an aggregated loan portfolio of around USD 37 million (GIZ, 2012[21]). In Indonesia, the People’s Credit Banks (BPRs) are the most prevalent form of microfinance facility, and the government is a majority shareholder. In Malaysia, microfinance is principally provided through state-owned banks and three large MFIs: Amanah Ikhtiar Malaysia (AIM), the Economic Fund for National Entrepreneurs (TEKUN) and Yayasan Usaha Maju (YUM). AIM is an NGO, while YUM and TEKUN are run by the government (YUM falls under the Ministry of Finance and TEKUN under the Ministry of Agriculture and Agro-based Industry). In total, ten financial institutions provide microfinance in addition to non-bank entities, and 33% of the total SME financing they provide (as of 2017) takes the form of microfinance, up from 22% in 2010. In addition, the country has one co-operative bank, Bank Rakyat, which was established in 1954.12

Since the last assessment in 2014, some AMS have stepped up measures to bring MFIs and rural credit operators into the formal financial system. In 2015, the Philippines enacted the Microfinance NGOs Act, which required all MFI NGOs to file regular reports with the country’s Microfinance NGO Regulatory Council, and for this institution in turn to submit an annual report to the president of the Philippines and relevant committees (EIU, 2016[22]). Financial reporting rules were also updated for co-operatives via the Co-operative Development Authority. In the same year, Indonesia enacted its new Microfinance Law, an initiative to increase oversight of smaller microfinance providers, coupled with an institution mapping exercise, led by the Financial Services Authority (OJK). In Thailand, the government made the formalisation and consolidation of existing MFI providers a lynchpin of its Master Plan for Financial Inclusion, which was adopted in 2015. Similar steps had already been taken in Malaysia, with the approval of an institutional framework for microfinance by the National SME Development Council in 2006. In Lao PDR, Cambodia and Myanmar, there remain many unregistered entities engaging in microfinance activities, and there do not currently appear to be sufficient programmes in place to formalise them (EIU, 2016[22]). This is largely due to capacity constraints. Legal directives have been attempted previously, for instance via the Regulation on the Establishment and Implementation of Microfinance Institutions in Lao PDR (No.10/BoL) in 2005 or the Prakas on Registration and Licensing of Microfinance Institutions in 2000 (Cambodia). In some cases, regulatory gaps can also be attributable to the rapid growth of the sector: in Cambodia, the size of microfinance loans grew at four times the income growth of the average borrower between 2004 and 2014 (Hutt, 2017[23]).

Many countries have started to implement proactive financial inclusion strategies over recent years, with supply-side microfinance policies and programmes playing a key role. Following the development of an institutional framework for microfinance in 2006, Bank Negara Malaysia developed a range of microfinance products for disbursal by three state-owned banks. Thailand’s Master Plan for Financial Inclusion, which runs until 2018, likewise aims to increase the microfinancing products provided by specialised financial institutions. In the Philippines, the government launched a National Strategy for Financial Inclusion in 2015, alongside a range of programmes to pursue it. Finally, to complement regulatory measures taken by OJK, Bank Indonesia developed Branchless Banking rules in 2015 and piloted the scheme as part of a push to increase the number of banked citizens in the country. Financial inclusion programmes are particularly imperative in Cambodia, Indonesia, Lao PDR, Myanmar, the Philippines and Viet Nam, where the proportion of the 15+ population with a bank account ranges from 12.6% in Cambodia to 35.9% in Indonesia.

Many microfinance schemes across ASEAN target women entrepreneurs as opposed to offering universal access. In some countries this choice reflects the fact that microfinance services have principally been provided by NGOs, which have adopted a Grameen approach.13 This is the case in the Philippines, which has an active and long-established microfinance sector (MCP, 2016[24]). In Malaysia, the country’s largest MFI, Amanah Ikhtiar Malaysia (AIM), also adopts a Grameen approach and provides microfinancing predominantly to women in order to promote income-generating activities (VMWG, 2014[25]). The same is true for YUM. Conversely in Viet Nam, this approach has been influenced by the way that microfinance developed in the country – since the beginning, the Women’s Union of Viet Nam has been a major partner in implementing many of the country’s microfinance policies and programmes (VMWG, 2014[25]). This approach is consistent in AMS where women have much higher rates of financial exclusion than men, as is the case in Cambodia, Thailand and Malaysia. However, the validity of this approach could be explored in financial inclusion strategies in the Philippines, Viet Nam and Indonesia, where women are more likely to be banked than men (World Bank, 2014[26]). In these countries in particular, microfinance facilities may be directed more towards achieving social goals, such as poverty alleviation, than increasing competitiveness through more equal competition among enterprises.

Alternative sources of finance: Such instruments remain scarce in many AMS

Asset-based financing instruments are well developed in some AMS, but remain underdeveloped in others. Countries such as Malaysia, Thailand and Singapore have legal frameworks that support the use of asset-based financing instruments, and the use of such instruments is rather common. In Thailand, this was accelerated by the passage of the Business Collateral Act in 2016. Other countries, such as Cambodia and Lao PDR, have developed legal frameworks for leasing and factoring, but the use of such products is rather limited, mainly due to difficult court procedures that render it difficult to liquidate assets. In some AMS, such as Viet Nam, regulation of factoring and leasing is rather fragmented, with at least five different entities holding different responsibilities. Leasing and factoring products are not currently available in Brunei Darussalam or Myanmar.

In terms of access to equity instruments, there is a high level of variation across the region. The bulk of PE/VC deals take place in Singapore, with Malaysia and Indonesia vying for the region’s second place. In the top five destinations for PE/VC funds, which include Viet Nam and Thailand, these funds ranged from USD 3.7 billion in Singapore to USD 72 million in Thailand in 2015, with funds in Viet Nam and Thailand climbing in 2016 while dropping in Singapore, Malaysia and Indonesia (AVCJ, 2017[27]). The majority of these deals are in the technology, media and telecommunications sector (Preqin, 2017[28]; Bhalla et al., 2012[29]). A trade sale is the most common form of exit, followed by an initial public offering (AVCJ, 2017[27]), as is the case in many OECD markets. As indicated in sub-dimension 3.1, an IPO is not a common exit option offered in Brunei Darussalam, Cambodia, Lao PDR or Myanmar, given the lack or limited depth of stock exchanges in these countries.

Policy makers have attempted to stimulate this area of SME financing to varying degrees. Over recent years, Malaysia has been working on the development of its private equity/venture capital (PE/VC) industry, chiefly by directing institutional investor funds such as Khazanah (Malaysia’s sovereign wealth fund) and Kumpulan Wang Persaraan (one of the country’s largest pension funds) towards venture-backed start-ups. In addition, it has introduced the SME Investment Partner (SIP) Programme as its third High Impact Programme under the SME Masterplan (2012-2020), which aims to increase SME access to non-bank financing.14 In Singapore, various schemes are in place to catalyse the supply of venture capital. These schemes include a tax exemption for VC funds; StartupSG Equity, whereby the government will co-invest with a qualified third-party investor in a start-up; and the Early Stage Venture Fund, whereby the government seeds funds to selected VC firms that wish to invest in Singapore-based early-stage tech start-ups.

In sum, however, there are relatively few government-sponsored programmes to stimulate alternative finance in ASEAN. Many of the policies implemented in this area are concerned with secured transaction reform, a necessary condition to facilitating the use of asset-based financing instruments, or involve the creation of a junior board for SME listing. In some AMS there is not yet a critical mass of SMEs demanding such products, and therefore it is not a priority area for policy makers. However, some countries are exploring innovative ways to boost alternative financing, both as a means to provide a wider range of financial products for SMEs and to increase financial resilience and investment opportunities. In Malaysia, the government is piloting a new initiative to develop open application interfaces that can be used by third-parties to access the databases of financial institutions in order to design more innovative financial products. In many AMS, the SME agency or business support centres are also working to increase demand by providing SMEs with advisory services or awareness-raising programmes on the types of instrument available to them. This is the case in Brunei Darussalam, Malaysia, the Philippines, Singapore and Thailand.

The way forward

As in many other policy dimensions, the financing landscape for SMEs is highly heterogeneous across ASEAN. However, a number of trends can be observed.

Note: The graph demonstrates the level of policy development in each AMS as indicated by the 2018 ASPI scores. Countries fall into one of three categories and are ordered in this category alphabetically.

The majority of countries that fall within the “early stage” and lower “mid stage” bracket have undergone a wave of institution building over the past five years – in some cases, almost from scratch. This has principally been in the shape of secured transaction reform. Many have also completed (Cambodia and Brunei Darussalam) or recently begun (Lao PDR, Myanmar and the Philippines) work to increase credit information coverage. In these countries, SME finance is principally provided through microfinance facilities. The bulk of public subsidy programmes in this area are targeted at increasing SME access to bank loans, and tend to be in the form of an SME-specialised development bank, as well as a refinancing scheme for selected commercial banks.

The countries that fall within the “mid stage” category have focused on boosting some of the institutions developed previously – for instance their country’s secured transaction framework, its movable assets registry, and developing facilities for SME listing. These countries have tended to concentrate efforts across all three product categories covered in sub-dimension 3.2. In microfinance, they have stepped up efforts to bring MFIs and rural credit operators into the formal financial system and have made them a pivotal part of financial inclusion strategies. To stimulate bank financing, they provide a mix of programmes, most notably refinancing, credit guarantee and export financing schemes. In the case of Indonesia and the Philippines, interest rate subsidies are also provided, and a mandatory lending programme is in place. Efforts to boost alternative financing instruments pivot around secured transaction reform, the creation of SME listing platforms and financial literacy programmes for start-ups.

The countries within the “advanced stage” category have already developed mature financial markets, with the institutions required to provide sophisticated financial products. These countries have concentrated on boosting the level and efficiency of financial intermediation in order to increase the availability of long-term local currency funding and the menu of financial products available for innovative firms. In turn, it is hoped that an increase in PE/VC financing will foster the development of deeper and more vibrant financial markets. In Malaysia, the government is also looking to boost financial inclusion.

Across the region as a whole, and in line with the ASEAN Economic Community’s pursuit of innovation-led growth, there appears to be particular interest in developing alternative financing instruments – a trend that may be somewhat premature in some AMS.

In order to increase access to finance for SMEs in the region, governments could prioritise the following steps going forward:

References

[2] Aghion, P., T. Fally and S. Scarpetta (2007), “Credit constraints as a barrier to the entry and post-entry growth of firms”, Economic Policy, Vol. 22/52, pp. 732–779, https://doi.org/10.1111/j.1468-0327.2007.00190.x.

[18] Aldaba, R. (2011), “SMEs' Access to Finance: the Philippines”, in Harvie, C., S. Oum and D. Narjoko (eds.), Small and Medium Enterprises (SMEs) Access to Finance in Selected East Asia Economies, Economic Research Institute for ASEAN and East Asia (ERIA), Jakarta, http://www.eria.org/uploads/media/Research-Project-Report/RPR_FY2010_14_Chapter_10.pdf.

[27] AVCJ (2017), Private Equity and Venture Capital Report: Southeast Asia.

[1] Ayyagari, M., A. Demirguc-Kunt and V. Maksimovic (2017), SME finance, World Bank Group, Washington D.C., https://doi.org/10.1596/1813-9450-8241.

[7] Beck, T. and A. de la Torre (2007), “The basic analytics of access to financial services”, Financial Markets, Institutions and Instruments, Vol. 16/2, pp. 79-117, https://dx.doi.org/10.1111/j.1468-0416.2007.00120.x.

[5] Beck, T. et al. (2006), “The determinants of financing obstacles”, Journal of International Money and Finance, Vol. 25/6, pp. 932-952, https://dx.doi.org/10.1016/j.jimonfin.2006.07.005.

[30] Beck, T., L. Klapper and J. Mendoza (2009), “The typology of partial credit guarantee funds around the world”, Journal of Financial Stability, Vol. 6/1, pp. 10-25, https://doi.org/10.1016/j.jfs.2008.12.003.

[10] Berger, A. and L. Black (2011), “Bank size, lending technologies, and small business finance”, Journal of Banking and Finance, Vol. 35/3, pp. 724-735, https://doi.org/10.1016/j.jbankfin.2010.09.004.

[12] Berger, A. and G. Udell (2006), “A more complete conceptual framework for SME finance”, Journal of Banking & Finance, Vol. 301/11, pp. 2945-2966, https://doi.org/10.1016/j.jbankfin.2006.05.008.

[9] Berger, A. and G. Udell (2002), “Small business credit availability and relationship lending: The importance of bank organisational structure”, The Economic Journal, Vol. 112/477, pp. F32-F53, https://doi.org/10.1111/1468-0297.00682.

[29] Bhalla, V. et al. (2012), Private Equity in Southeast Asia: Increasing Success, Rising Competition, Boston Consulting Group, Boston, https://www.bcg.com/publications/2012/private-equity-mergers-acquisitions-private-equity-southeast-asia.aspx.

[3] Demirguc-Kunt, A., I. Love and V. Maksimovic (2006), “Business environment and the incorporation decision”, Journal of Banking and Finance, Vol. 30/11, pp. 2967-2993, https://doi.org/10.1016/j.jbankfin.2006.05.007.

[22] EIU (2016), Global Microscope 2016: The Enabling Environment for Financial Inclusion, http://graphics.eiu.com//assets/images/public/Global-Microscope-2016/EIU_Microscope_2016_English_web.pdf.

[33] Gedye, M. (2012), “Practitioner attitudes to the PPSA”, New Zealand Law Journal, pp. 118-119.

[21] GIZ (2012), Microfinance in the Lao PDR, https://www.giz.de/de/downloads/giz2012-en-microfinace-lao-pdr.pdf.

[8] Harvie, C., D. Narjoko and S. Oum (2013), “Small and medium enterprises’ access to finance: Evidence from selected Asian economies”, ERIA Discussion Paper Series 2013-23, http://www.eria.org/ERIA-DP-2013-23.pdf.

[11] Hengel, E. (2010), “Discussion Paper on Credit Information Sharing”, Facilitating Access to Finance Discussion Paper Series.

[23] Hutt, D. (2017), “Cambodia's microfinance industry: Why bigger may not be better”, The Diplomat, https://thediplomat.com/2017/08/cambodias-microfinance-industry-why-bigger-may-not-be-better/.

[17] Le, H. (2016), “The credit guarantee funds are sitting”, The Saigon Times, http://www.thesaigontimes.vn/143408/Cac-quy-bao-lanh-tin-dung-doanh-nghiep-dang-phai-ngoi-choi.html.

[24] MCP (2016), Social Performance Country Report, http://www.microfinancecouncil.org/wp-content/uploads/2017/04/2016-Philippines-Social-Performance-Country-Report.pdf.

[6] OECD (2015), New Approaches to SME and Entrepreneurship Financing: Broadening the Range of Instruments, OECD Publishing, Paris, https://doi.org/10.1787/9789264240957-en.

[31] OECD (2013), SME and entrepreneurship financing: The role of credit guarantee schemes and mutual guarantee societies in supporting finance for small and medium-sized enterprises, https://one.oecd.org/document/CFE/SME(2012)1/FINAL/en/pdf.

[28] Preqin (2017), Preqin Special Report: Asian Private Equity and Venture Capital, http://docs.preqin.com/reports/Preqin-Special-Report-Asian-Private-Equity-&-Venture-Capital-September-2016.pdf..

[16] SGX (2017), Market Statistics Report: December 2017, http://www.sgx.com/wps/portal/sgxweb/home/marketinfo/market_statistics.

[4] Siedschlag, I. et al. (2014), “Access to external financing and firm growth”, Background Study for the European Competitiveness Report 2014, http://www.esri.ie/pubs/BKMNEXT287.pdf.

[34] SSM (2017), Introduction of Personal Property Securities Registration Law in Malaysia: Consultative Document, https://www.ssm.com.my/sites/default/files/acts/konsultasi_awam_ppsr.pdf.

[32] STR (2017), “The case for reform”, Secured Transactions Law Reform Project, https://securedtransactionslawreformproject.org/the-case-for-reform/.

[20] The Economist (2013), Microfinance in Thailand: the Biggest Microlender of Them All, https://www.economist.com/schumpeter/2013/01/01/the-biggest-microlender-of-them-all.

[25] VMWG (2014), Microfinance in Vietnam: the Real Situation and Policy Recommendations, Vietnam Microfinance Working Group, Hanoi, http://www.microfinance.vn/wp-content/uploads/2015/05/bao-cao-TA_lan-1-17.11.pdf.

[15] World Bank (2018), Financial Development and Structure Dataset, http://www.worldbank.org/en/publication/gfdr/data/financial-structure-database.

[13] World Bank (2015), Principles for Effective Insolvency and Creditor/Debtor Regimes, World Bank Group, Washington D.C., https://doi.org/10.1596/23356.

[26] World Bank (2014), Global Findex database 2014, https://globalfindex.worldbank.org/.

[14] World Bank (2017a), Doing Business 2018: Reforming to Create Jobs, World Bank Group, Washington D.C., http://hdl.handle.net/10986/28608.

[19] World Bank (2017b), Indonesia Economic Quarterly: Staying the Course (March 2017), http://pubdocs.worldbank.org/en/278631490090358078/IEQ-MAR-2017-ENG.pdf.

Notes

← 1. By ensuring that a borrower has some “skin in the game” in the event of default.

← 2. Memorandum Circular No. 3/2016.

← 3. Namely, Brunei Darussalam (2014), Cambodia (2013), Lao PDR (2012), Viet Nam (2014).

← 4. The Secured Transactions Filing Office in Cambodia, the Fidusia Registry Office in Indonesia, the Registry Office for Security Interests in Movable Property in Lao PDR, and the National Registration Agency for Secured Transactions in Viet Nam.

← 5. Specifically, in 2016 with the enactment of its Secured Transactions Order and creation of a collateral registry within the AMBD.

← 6. World Bank Financial Structure database, data from 2017. No data for Cambodia, Lao PDR or Myanmar.

← 7. World Bank Financial Structure database, data from 2016 (last available data).

← 8. Which has 384 companies listed and a total market capitalisation of USD 10.1 billion.

← 9. ACE is Bursa Malaysia’s existing junior board.

← 10. Namely, Indonesia, Malaysia, the Philippines, Thailand and Viet Nam. Singapore and Brunei Darussalam are not scored in this area, given their limited need for this type of instrument.

← 11. All excluding Brunei Darussalam and Singapore, which are not scored on these indicators given their small and mostly urban population.

← 12. Bank Rakyat is an Islamic co-operative bank that was established in 1954 under the Co-operative Ordinance of 1948.

← 13. An approach which theorises that repayment rates are higher among female borrowers than male.

← 14. The SIP is a co-funding initiative between the government of Malaysia and private investors. It aims to provide financing to SMEs, mainly those in the start-up phase. Under this programme, three investment entities, or SME Partners, have been appointed to raise funds for SMEs from private investors, which will be matched by an initial capital investment from the government. Once sufficient capital is raised, these SME Partners are required to provide financing to viable SMEs from all sectors.

← 15. For instance in Cambodia where the majority of land titles are soft titles (those which are only established and recognised at the local government level) and the cadastre is only in a pilot phase.