Chapter 2. Labour market, social policy and tax policy related challenges in Slovenia

High employee SSCs, employer SSCs and progressive PIT rates result in very high tax burdens on labour income in Slovenia. This lowers incentives for employers to hire workers and net-take home pay for workers, thereby reducing incentives to participate in the labour market and increase work efforts. High unemployment and inactivity traps exist. Young individuals enter the labour market late and older workers leave early. To compensate for the high tax burden on labour income, Slovenia has put in place many tax exemptions, especially aimed at low-income taxpayers, families and pensioners. High taxes on labour exacerbate existing labour market weaknesses, and result in low labour market participation rates of younger and older workers. The pension and health funds, which rely predominantly on SSCs, face budgetary difficulties. In light of the ageing population, increasing the labour market participation of older workers is a priority.

2.1. The labour tax burden is high but the personal income tax base is narrow

2.1.1. The combined personal income tax (PIT) and social security contributions (SSCs) burden is high in Slovenia

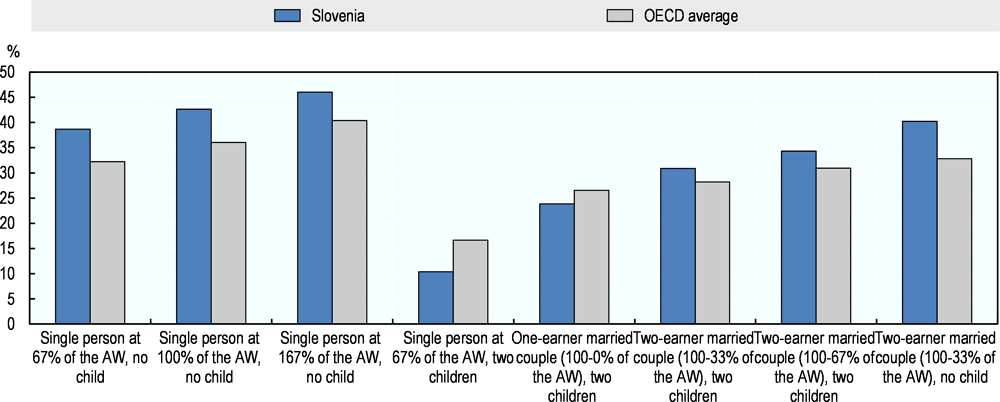

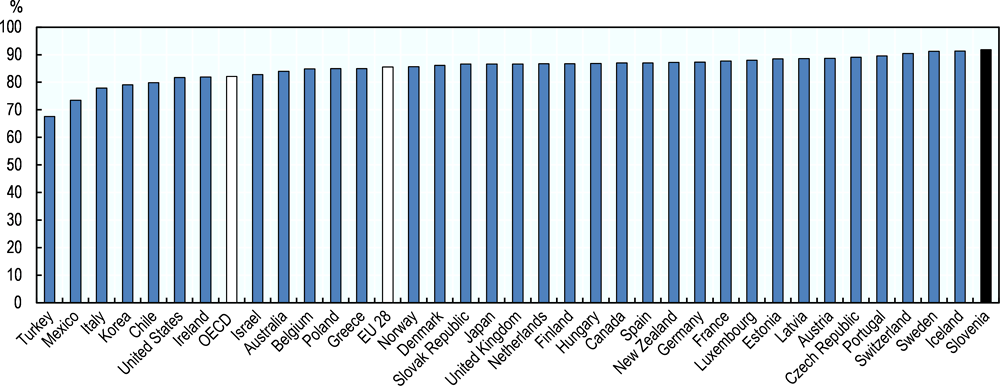

The tax burden on labour income in Slovenia is high because of the combined effect of high employee and employer SSCs and a progressive PIT rate schedule. Employee SSCs are levied at a rate of 22.1% which is the highest of all OECD countries; on average across the OECD, employee SSC rates are 9.8%1. Employer SSCs are levied at a rate of 16.1% in Slovenia compared to a rate of 17.5% on average in the OECD2. In addition, the top statutory PIT rate of 50% is high. Slovenia is among the 10 OECD countries where workers earning an average wage (AW) – i.e. the gross wage that a worker can earn yearly on average in the private sector – are taxed the most. The average tax wedge3 for single workers without children earning an AW was 43% in 2017 compared to 36% on average in the OECD (Figure 2.1). For married couples, the average tax wedge is lower than for single taxpayers but it is still above the OECD average. The tax wedge in Slovenia is below the average tax burden in the OECD only for single taxpayers and one-earner married couples who have two children.

Source: OECD (2018[1]).

High taxes on labour income increase labour costs for firms (Figure 2.2). Total labour costs are higher in Slovenia than in the Czech Republic, Hungary, or the Slovak Republic because of higher wage levels and employer SSCs. However, total labour costs in Slovenia remain below the levels in Austria and Italy.

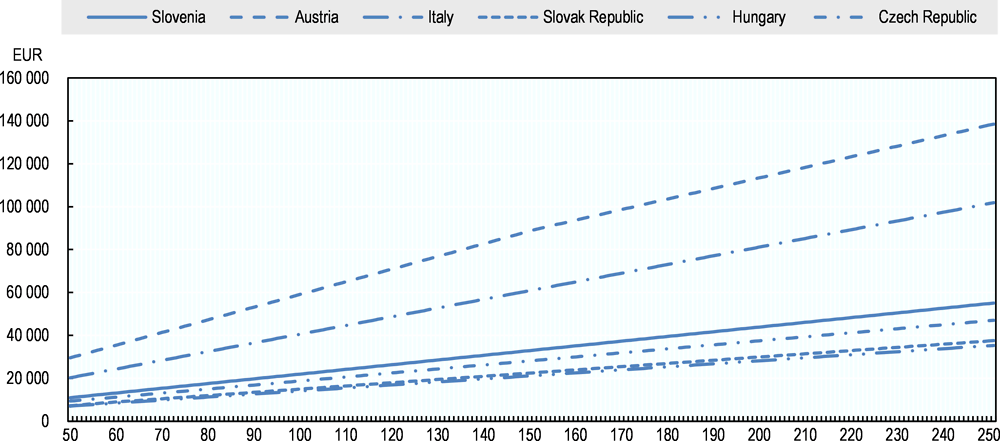

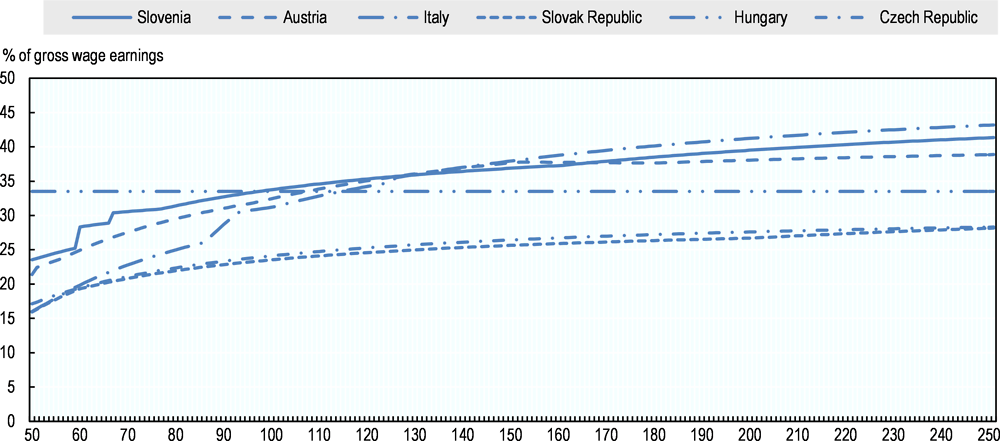

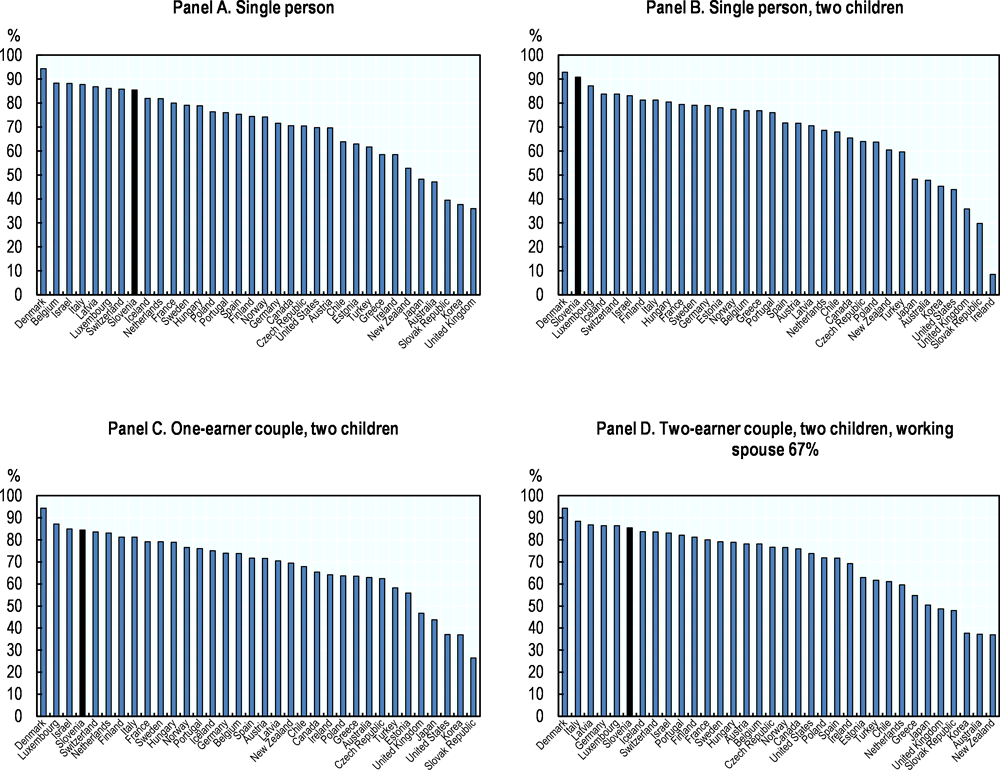

A combination of high employee SSCs and PITs reduce worker take-home pay. The net personal average tax rate4, which measures the effective employee SSC and PIT burden as a percentage of gross wage earnings, is particularly high for single workers without children. For this category of workers, Slovenia is in the top five of OECD countries with the highest personal average tax rate (33.7%), after Belgium, Germany, and Denmark. The tax burden is higher in Slovenia than selected East European countries (the Czech Republic, the Slovak Republic) at all income levels (Figure 2.3). Despite this higher tax burden, Slovenian workers have higher take-home pay because of a higher AW (Figure 2.4). However the net-take home pay in Slovenia is significantly lower than in Austria reflecting higher wages and a less burdensome tax system.

Source: OECD (2018[1]).

Source: OECD (2018[1]).

Source: OECD (2018[1]).

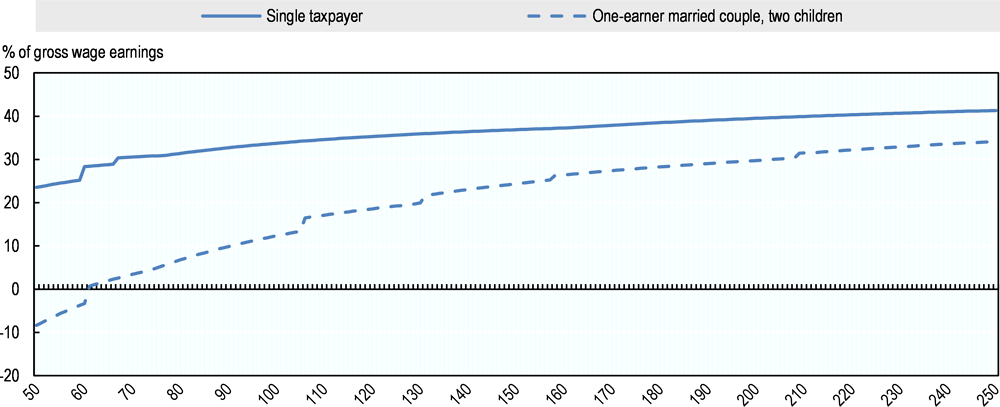

The combined effect of employee SSCs and PITs in Slovenia remains progressive. Despite of the large share of employee SSCs which are levied at flat rates, the overall average effective tax rate (AETR) (which is the joint employee SSCs and the PIT) for single taxpayers is significantly increasing with income; i.e. statutory PIT and SSC progressivity remains relatively high5. Over the 50-250% of the AW income range, the AETR increases by 0.085 percentage point for each percentage point increase in the income level. This is above Austria (0.079 pp), the OECD average (0.074 pp), the Slovak Republic (0.047 pp), the Czech Republic (0.045 pp) and Hungary (0 pp), but lower than in Italy (1.04 pp). However, the progressivity of the tax system in Slovenia is below the progressivity on average in the OECD and comparative countries for families with children despite of the generous child tax provisions.

2.1.2. Generous tax provisions narrow the PIT base considerably

Tax allowances significantly narrow the PIT base and come at a high cost in tax revenues foregone. Slovenia implements a wide range of tax allowances, including a general allowance, personal allowances, allowances for dependent family members, and other income-specific allowances. Pensioners benefit from a PIT credit. Overall, the PIT allowances and credits come at a cost in tax revenues foregone of 4.75% of GDP in 2016 (Table 2.1).

Generous tax allowances offset the impact of the high statutory labour income tax burden in Slovenia. Slovenia is among the OECD countries where labour income tax rates are high but tax bases are narrow. While generous tax allowances could be justified to prevent the distortive effects of high tax rates, their impact is selective in that they target certain taxpayers who benefit over others.

For instance, families with children benefit from very generous tax allowances which reduce their tax burden significantly. In 2017, the average tax wedge in Slovenia for one-earner married couples with two children at the average wage is 24.5%, significantly lower than the corresponding tax burden for single taxpayers (Figure 2.5). This results in large differences in disposable income across family types. Among OECD countries, Slovenia has the third highest difference between disposable income for families with or without children.

Until 2018, the allowance system had no taper rate but thresholds. Figure 2.6 shows the number of taxpayers at gross income levels going up in thousands alongside the general allowance thresholds for taxpayers with low incomes for both 2015 and 2016. Incomes below EUR 10 866 are entitled to a tax allowance of EUR 6 520. As a taxpayer’s income increases from EUR 10 866 to EUR 12 571 the allowance is reduced by 32% to EUR 4 419. For incomes beyond this point, the allowance is reduced by a further 25% to EUR 3 303. This allowance structure may produce an economic incentive for taxpayers, and potentially employers, to report incomes below these thresholds before the allowance is reduced. According to an analysis using the tax record data, in both 2015 and 2016, the highest number of taxpayers in any thousand euro band is EUR 10 000 and EUR 11 000, which is just before the most significant loss in the tax allowance. The number of taxpayers continues to fall as the allowance is further reduced in steps. The introduction in 2018 of a linearly determined general tax relief for incomes between EUR 11 166.67 and EUR 13 316.83 might reduce the taxpayers bunching below allowance thresholds in Figure 2.6. The analysis provides suggestive evidence that Slovenian employees and employers may be responding to the allowances schedule. Further multivariate analysis of the microdata is needed to uncover a causal interpretation of such behaviour.

Source: OECD (2018[1]).

Note: Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

2.2. Too few young and older people are active in the labour market

2.2.1. Labour market participation of both men and women in the prime age category of 25-54 is very high

Slovenia’s labour market participation rate6 among workers in the prime age category of 25-54 is 91.9% in 2017, which makes Slovenia the top performer in the OECD (Figure 2.7). The employment rate7 is also among the highest (86.1% in 2017), above the OECD (77.8%) and the European Union (EU) (79.7%) averages. No major differences are observed between the participation of both men and women, which suggests that Slovenia does not face a significant gender gap in the labour market. In addition, part-time work is not widespread. In 2015, only 3% of employed men were in part-time employment (5.3% on average in the OECD). The share is higher for women (8.2%) but still significantly lower than on average in the OECD (22.3%).

Source: OECD Labour market statistics.

2.2.2. Labour market participation of young workers is low

Labour market participation for younger workers (aged 15-24) drops to 33.7%, far below the participation rate in other OECD countries (47.2% on average) and the EU (42.3%). The weak participation on the labour market is worsened by emigration flows of young skilled workers (see section 2.3). The employment rate shows a similar trend (34.8% for Slovenia, against 41.3% in the OECD on average).

Young workers enter the labour market later. The duration of study for Slovenian students is relatively long (OECD, 2016[2]) which may partly be explained by the fact that students work instead of finalising their degrees. Options are available to students to work (mainly under temporary work contracts which reduce their future benefit entitlements) and study at the same while benefiting from generous conditions (state-funded tuition fee waivers, subsidies for living expenses such as meals, accommodation, transportation and cultural activities, state scholarships) (OECD, 2016[2]).

As a result, current younger cohorts have relatively shorter insurance periods than their counterparts in the past. For example, in 2002, workers aged 30-34 had been insured already for 11 years on average, while in 2015 workers in this age group had been insured for only 8 years on average (OECD, 2016[2]). Shorter insurance periods will result in lower benefit entitlements for workers in the future (e.g. lower pensions) and reduces revenues for government to finance the welfare spending of the current generation.

2.2.3. Labour market participation of older workers is very low

The labour market participation of older workers is very low. Only 41.2% of the workers in the age category 54-65 are still active in the labour market. In only two other OECD countries (Luxembourg and Turkey) older workers participate as little as in Slovenia. Similar trends can be observed with the employment rate of older workers. In 2017, only 42.8% of older workers are employed, whereas it is 57% on average in the EU and 60.4% in the OECD. Among older workers, low skilled (in particular below upper secondary schooling) leave the labour market earlier than skilled workers.

Older workers retire early. According to the tax record data, the gap between the official and the effective retirement age is more than 4 years on average. Slovenia has recently increased the official retirement age to 65 for both men and women by 2020 (from 63 for men and 61 for women)8. However if the 4-year gap persists, the effective retirement age would still be significantly below the official retirement age (around 61), which is extremely low compared to other countries.

Several factors explain the early retirement of older workers. First, the unemployment insurance system allows older workers to retire earlier (OECD, 2016[2]). 30% of pensioners used the unemployment system as a bridge to retirement, where unemployment benefits are often higher than the pension the worker will receive (Ministry of Labour, Family, 2016[3]). Seniority bonuses for older workers can make the hiring of an older worker 15% more expensive than a younger worker (OECD, 2017[4]), which could induce employers to end existing contracts of their older workers. Sickness leave is also used by older workers as a vehicle to retire early. In addition, before the 2013 pension reform, older workers faced no financial incentives to continue working as an additional year of working was associated with a 4% decrease in net pension wealth (OECD, 2016[2]).

The 2013 pension reform introduced measures to increase the labour market participation of older workers. First, the reform ensured that workers will increase their pension entitlements if they work longer. Moreover, workers eligible for retirement can choose to continue working under several different arrangements, including: i) working part-time and receiving a proportional pension which is increased by 5% if they are less than 65 years of age; ii) continuing to work full-time and receiving 20% of their pension while they work; iii) receiving a full pension and working via a so-called temporary and occasional work contract, which is subject to social security contributions and an additional 25% duty payable by the employer. Slovenia should evaluate whether the 2013 pension reform is effective in closing the gap between the statutory and effective retirement age, and whether future reforms are needed.

In addition, Slovenia should consider increasing the legal retirement age from 65 to 67, as recommended in the OECD Economics Surveys: Slovenia 2017. Such a measure could form part of a longer term proposal to lift the retirement age on a prospective basis. Following the direction taken by the 2013 pension reform, Slovenia could consider additional (tax and non-tax) reforms which help smooth the transition from work to retirement, such as part-time work and part-time retirement.

2.2.4. Significant unemployment and inactivity traps exist

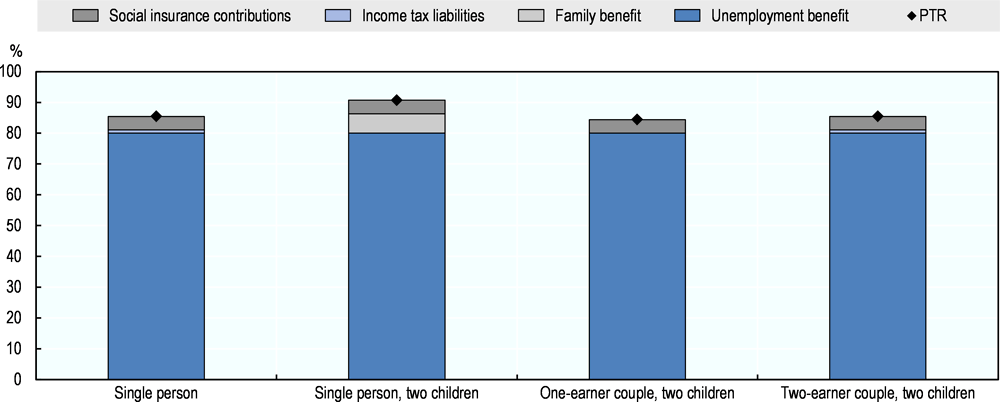

Participation tax rates (PTRs) are high in Slovenia. PTRs9 measure how much of the increase in gross earnings is taxed away when individuals enter the labour market from short-term unemployment into full-time work (Figure 2.8). Therefore high participation tax rates reflect that the tax and benefit system does not encourage unemployed workers to join the labour market.

Source: OECD Tax-Benefit Model.

High PTRs are explained by the loss in unemployment benefits when workers enter the labour market and because of the high SSC burden levied on their wage earnings (Figure 2.9). The latter does not appear in the chart as unemployment benefits are also taxed with employee SSCs. PTRs from long-term unemployment into full-time work (inactivity trap) are also high, especially for lone parents and one-earner married couples with children. The loss of social assistance and the payment of SSCs are the main drivers of inactivity traps.

Reducing both unemployment and inactivity traps is particularly important given the ageing of the population in Slovenia. Higher degrees of labour market participation will prevent people from falling into poverty and will increase the revenues from social security contributions, which can help address rising age-related public expenditure. Different options are available to encourage unemployed or inactive workers to re-enter the labour market, including a reduction in employee SSCs and the use of targeted into-work benefits. For instance, individuals who re-enter the labour market after a period of inactivity could receive, for a pre-set period of time, an additional into-work benefit equal to a fixed percentage of their previous unemployment or social assistance benefit. However, an in-depth discussion of the design of these into-work benefits goes beyond the scope of this report.

Note: For a first earner at 50% of the AW. The second earner is at 67% of the AW.

Source: OECD Tax-Benefit Model.

2.3. Low levels of skills have a negative impact on productivity

Adults skills levels are low (OECD, 2017[4]). Almost one-third of the working-age population (around 400 000 adults) in Slovenia, and in particular older workers, have low levels of literacy and/or numeracy proficiency. Slovenia has achieved a great improvement in skills across age cohorts: around 94% of 25-34 year-olds have completed at least upper secondary education, a figure which is higher than almost all other OECD countries. The percentage of young adults in Slovenia with tertiary education rose from 25% in 2005 to 41% in 2015, exceeding the EU 2020 target of 40%. However, average literacy scores for 25-34 year-olds (including tertiary graduates) are lower than for their counterparts in other countries in the Survey of Adult Skills (PIAAC).

Slovenia’s lack of skills is exacerbated by the increasing share of highly skilled people that emigrate, although evidence suggests that Slovenia is not experiencing a so-called ‘brain drain’ (OECD, 2017[4]). Of the 15 500 adults who emigrated from Slovenia in 2016, 22% were adults with tertiary education. However, this figure has almost doubled between 2011 and 2016, possibly reflecting the impact of the economic crisis. In addition, the share of young (aged 20-29) highly skilled emigrants has increased (from 18% in 2011 to 35% in 2015) perhaps driven, among other things, by better socio-economic opportunities including higher wages and lower taxes abroad. This reduces the availability of highly skilled workers for the Slovene labour market and reduces the return on public investment in education for the country (OECD, 2017[4]). The skills challenge is reinforced by the daily work-home commute to neighbouring countries (Italy, Austria) and the low attraction of foreign highly-skilled workers (16% of immigrants in 2016).

The low skill level lowers productivity and growth. Skills are central to a country’s economic prosperity (OECD, 2017[4]). Making more effective use of people’s skills in workplaces can boost labour productivity: after accounting for differences in skills proficiency, the use of reading skills explains a considerable share (26%) of the variation in labour productivity across countries (OECD, 2016[5]).

2.4. Wages are relatively low and the income distribution is narrow

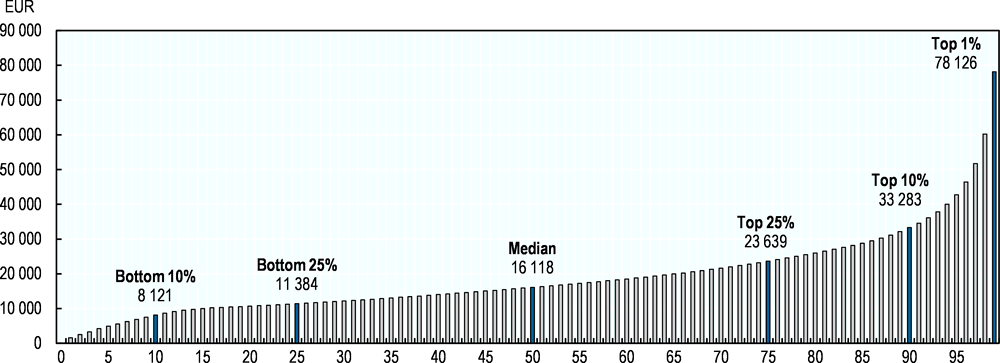

Wage levels are relatively low. In 2016, tax record data show that mean and median incomes are EUR 19 725 and EUR 16 118 respectively (Figure 2.10). The top 10% and 1% income thresholds are EUR 33 284 and EUR 78 126. Low wages have implications for the amount of PIT and SSCs that can be raised. The gap is significant when compared to neighbouring countries such as Italy (EUR 30 642), Germany (EUR 47 809) or Austria (EUR 44 409). However, compared to Central and East European members of the OECD, Slovenia has become a relatively high-wage economy (OECD, 2017[6]). In 2016 the average annual wage was EUR 18 292 which is higher than in Hungary, Poland, the Czech Republic or the Slovak Republic.

Note: Employees are defined as taxpayers with salary income plus some small self-employment income. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

Slovenia has a compressed wage structure at the low end of the wage distribution (OECD, 2017[6]). Mean and median wages are similar across income deciles distribution. In Slovenia in 2016, the top employee decile earns 26.9% of all gross income and 24.5% of all disposable income, while the lower employee decile earns 2.4% and 2.8% respectively (Table 1.1). Almost half (45%) of taxpayers earn the minimum wage and 65% of people in paid employment earn below average gross earnings (Statistical Office).

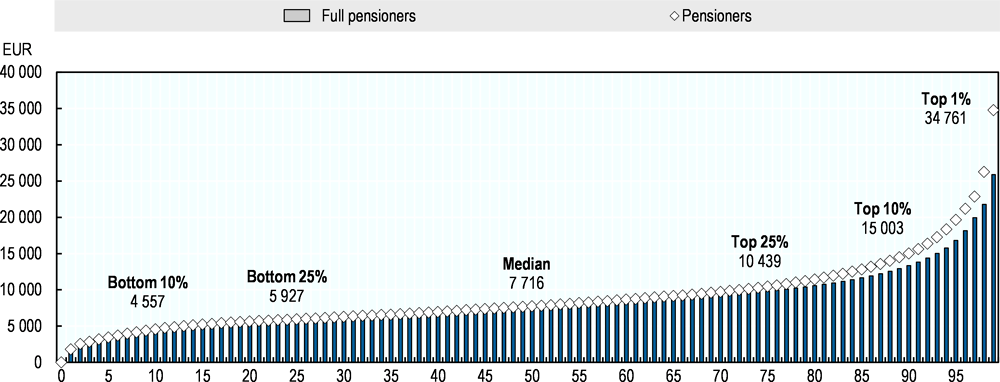

Pensions are very low in Slovenia. Figure 2.11 presents the distribution of income for pensioners – defined as taxpayers who receive pension income and, possibly, other types of income – and “full” pensioners, which are defined as pensioners who, besides their pension income, do not have any other source of wage or business income. For most of the distribution, the two groups have similar earnings: the median income for pensioners and full pensioners equals EUR 7 716 and EUR 7 479, respectively. Pensioners who have another source of income (7% of pensioners) increase their earnings. This applies in particular to the higher end of the income distribution; after the 75th percentile pensioners start to become significantly better-off due to their additional income sources from employment and self-employment. For the top 10%, full pensioners earn EUR 13 351 which is well below the gross earnings of EUR 15 003 for all pensioners together (so including pensioners who have another source of income). For the top 1%, full pensioners earn EUR 25 905 compared to EUR 34 761 for all pensioners.

Note: Pensioners are taxpayers with any pension income. Full pensioners are those with only pension income. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

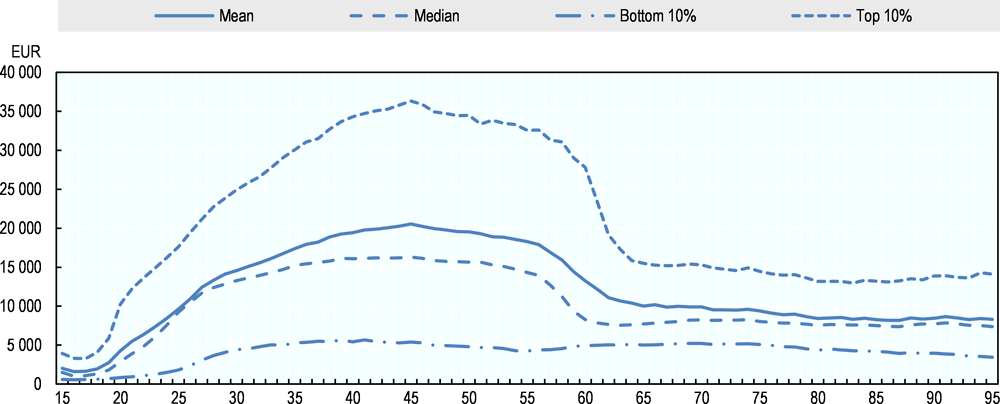

Older workers have low, stable and equal incomes. Figure 2.12 shows the gross income distribution of taxpayers aged 15 to 95 in 2016:

-

For young workers, incomes rise sharply between 20 and 30 years of age in part driven by students, a group more likely to undertake part-time work, moving from study to employment. For example, at 23 years of age, median incomes are EUR 6 106 and by 30 they have more than doubled to EUR 13 292. Thereafter, median income increases are more gradual reaching EUR 15 220 by age 35. The similarity of mean and median incomes across all ages reflects Slovenia’s condensed income distribution.

-

For middle-aged workers, approximately between 35 and 55, median incomes are stable, varying on average (median) between EUR 15 000 and EUR 16 000. The highest incomes are for those aged between 40 and 50. Mean incomes also rise faster than median incomes between these ages indicating a greater level of income inequality, which may partly by attributable to differences in worker productivity.

-

For older workers, incomes are significantly smaller and income inequality becomes significantly lower, reflected in the closing of the gap between mean and median income after 65 years of age. An extraordinary feature for high earners is the exceptionally steep income cliff as they transition to old age. For example, at age 58, the top 10% of earners have gross incomes of EUR 31 063 but by 64, only a 6 year difference, income among the top 10% have declined dramatically by almost halved. This feature is also unusual internationally compared to Ireland and the US (Kennedy, 2018[7]) (Auten, Gee and Turner, 2013[8]).

Note: Age data truncated between 15 and 95 for reasons of sample size. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

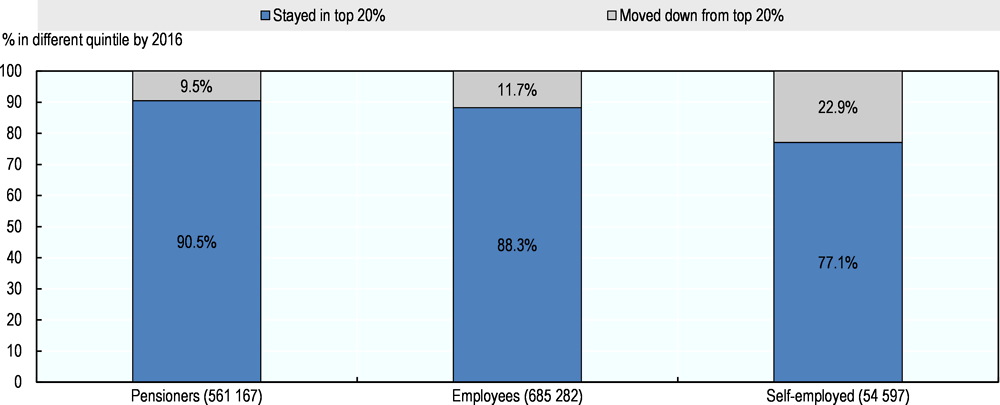

Pensioners in Slovenia have low levels of income mobility. Figure 2.13 examines income mobility in Slovenia by measuring the positional change of different taxpayer groups between 2015 and 2016. The methodology is as follows. A group of taxpayers is identified (for example, employees) and only those observed in both comparison years are retained. In each year, the employee has an origin and destination position in the income distribution. Next, two distinct gross income quintile are calculated in each year. Finally, a transition matrix is calculated across the two years. Figure 2.13 shows the transition probabilities for employees, pensioners and self-employed taxpayers remaining in the top quintile between 2015 and 2016. According to the analysis, of those employees in the top quintile (the top 20%) in 2015, almost 9 in 10 (88%) stayed in that quintile a year later. Of self-employed taxpayers in the top quintile in 2015, 77% stayed in that quintile a year later and 23% moved downwards. Among pensioners, over 90% stayed in the top quintile. Consequently, the highest downward mobility is observed among the self-employed followed by employees and then pensioners. While this analysis is suggestive of mobility trends more conclusive analysis would require producing these transitions over a longer time horizon.

Note: There are important caveats to consider when interpreting transition matrices. For example, they show relative and not absolute changes in income. They do not capture those who leave the workforce (for example, due to emigration, unemployment or death). In addition, the time horizon is important – this one year transition while illustrative is much more limited and will show less mobility than a transition over a longer time period. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

Because wages are low, many taxpayers cumulate jobs. Taxpayers who have different sources of income are considerably better off.

-

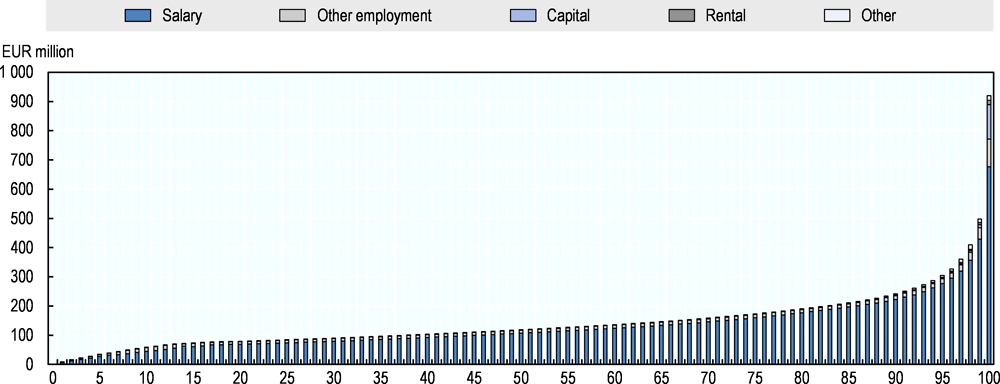

For employees, with the exception of the very bottom and top of the income distribution, the analysis shows that salary income comprises the vast majority of gross income (around 90% at most income percentiles). In the bottom decile, salary incomes approximately represent a lower 80% of gross income and this is due to relatively high levels of other employment income, which includes income from holiday bonuses, contractual relationships and student incomes (Figure 2.14). At the top end, and in particular in the top 1% of employee earners, salary represents only 70%. This is due to a high concentration of capital, other employment and rental incomes which comprise 12%, 10% and 2% respectively of total gross income in this top percentile.

-

For pensioners, for the first two-thirds of the gross income distribution, pensions comprise the vast majority of all income (above 95%) (Figure 2.15). As pensioners become better-off between the 65th and 85th percentiles, they begin to supplement their income to a greater extent with salary income, other employment income and a small proportion of rental property income, causing the pension proportion of all income to fall to about 80%. Among the top decile of pensioners, salary income increases from a proportion of 15% at the 90th percentile to 39% for the top 1%. Capital income rises more slowly – it comprises 2% at the 98th percentile, 3% at the 99th percentile but 15% in the top 1%. Indeed, the top percentile comprises only 18% of gross income from pensions, the majority comes from salary income while capital, other employment and property comprise 15%, 14% and 9% respectively.

-

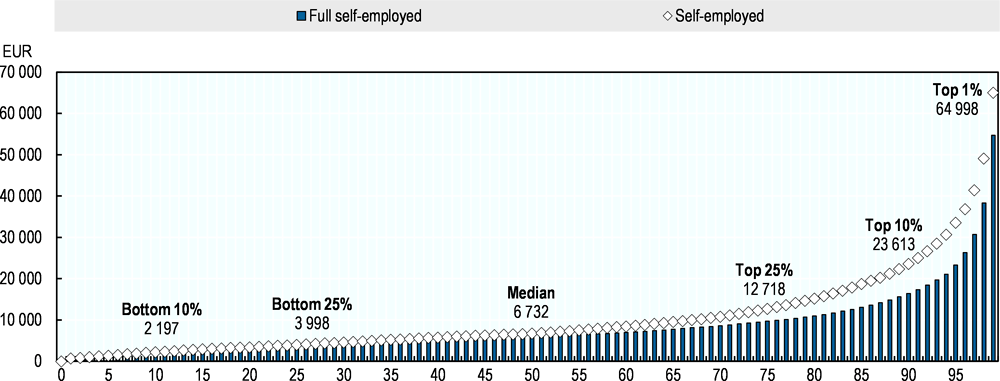

Figure 2.16 shows the self-employed and the full self-employed10 (taxpayer that derive 100% of their income from self-employment) income distribution thresholds by percentile for 2016. In the lower half of the income distribution, the more broadly defined self-employed earn approximately 10 – 15% more on average than the full self-employed. At the median, the self-employed and full self-employed earn EUR 6 732 and EUR 6 732 respectively. After this point however, incomes are significantly higher for the self-employed due to their additional employment income. For example, among the top 10% and 1%, the self-employed earn EUR 23 613 and EUR 64 998 compared to the full self-employed who earn EUR 16 377 and EUR 54 703.

-

While self-employment incomes are far lower than employment incomes on average, both income sources follow a broadly similar distributional pattern by age – most income is earned by those aged 35 to 60 (Figure 2.17). Unlike salary income however, self-employment income does not decline as sharply after age 60, suggesting that older taxpayers are more likely to supplement their income with self-employment or the self-employed remain active in the labour market after reaching the age of 60.

Note: Employees are defined as taxpayers with salary income plus some small self-employment income. For the purpose of this analysis, other includes all business, agricultural and other miscellaneous income. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

Note: Pensioners are defined as taxpayers with other income sources. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

Note: A full self-employed is a taxpayer that derives 100% of its income from self-employment. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

Note: Mean averages calculated based on all salary, pension and self-employment income including incomes reported as nil. An analysis done on a median basis shows a broadly similar distribution for salaries and pensions. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

The self-employed are the most mobile population cohort in Slovenia. At the bottom of the distribution, there is greater upward mobility among self-employed, employees and then pensioners (Figure 2.18). For example, 43% of the self-employed moved upwards out of the bottom quintile compared to only 8% for pensioners. Higher mobility among the self-employed is expected and partly reflects the greater risk and returns to business and entrepreneurship. Similarly, pensioners are much more likely to have stable incomes with little income shocks over time compared to employees and the self-employed.

Note: There are important caveats to consider when interpreting transition matrices. For example, they show relative and not absolute changes in income. They do not capture those who leave the workforce (for example, due to emigration, unemployment or death). In addition, the time horizon is important – this one year transition while illustrative is much more limited and will show less mobility than a transition over a longer time period. Methodological information on the microdata is available in the annex.

Source: Authors’ calculations based on Ministry of Finance of Slovenia tax records microdata.

2.5. The welfare system faces financing challenges

2.5.1. The costs of the pension system are rising

Pension contributions are not covering pension fund expenditures. The pension system in Slovenia is a pay-as-you-go system. In 2016 SSCs amounted to 72% of its total revenues (Ministry of Finance, 2018[9]). The budget balance was achieved with transfers from the general government (27% from the State budget, social security funds and extra budgetary funds) and non-tax revenues.

Several factors are adding pressure on the financing of the pension fund. Old-age pension transfers to individuals represented 51% of the total pension fund expenditures in 2000 (other expenditures included disability pension, family pension, other types of pensions, current expenditure, salary compensation, transfers to non-profit organisation, etc.) (Ministry of Finance, 2018[9]). This share has increased to 65% in 2016 reflecting the ageing of the population. Public expenditures on pension are projected to reach 15.6% of GDP in 2050 (11.8% of GDP over the period 2013-15) (OECD, 2017[10]). Pressure is exacerbated by the relatively low labour market participation on the one hand, and by the low development of the private pension system on the other hand. In its “White book”, government explored different options to secure the financing of adequate pensions in the future.

Despite having a minimum pension, pensions in Slovenia remain relatively low increasing the risks that pensioners might fall into poverty (Figure 2.11). In Slovenia low-income pensioners (20th percentile of the income distribution) are below the poverty threshold (OECD, 2017[11]). In addition to the general basic allowance, pensioners with low income can benefit from an additional tax credit equal to 13.5% of the pension received. The cost of this tax credit amounts to EUR 221 million in 2016 (OECD analysis of administrative tax records).

2.5.2. The reform of the public health system is even more urgent

In 2016, health expenditures reached 8.6% of GDP in Slovenia compared to 9.9% of GDP on average in the EU and 9% in the OECD countries. The health care system is primarily financed by the Health Insurance Institute of Slovenia (HIIS). This is complemented by co-payments spending and voluntary health insurance from three private insurance companies. In 2016, 72% of the health financing was from public sources, and 28% from voluntary schemes and households out-of-pocket payments.

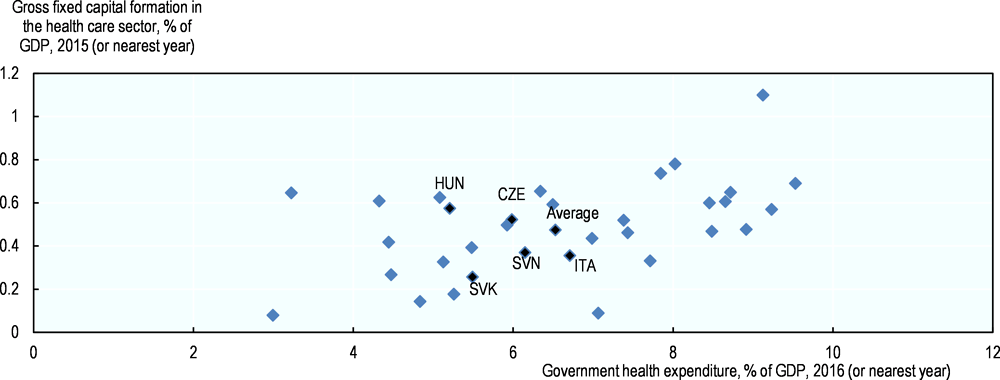

Investment in physical capital in the health sector (0.37% of GDP) is low as a share of total government health expenditure, and is below the OECD average (Figure 2.19). For example, the Czech Republic has a similar amount of government health expenditure but higher investment in physical capital in the health sector (0.52% of GDP). However, these figures should be interpreted with care and much depends on the types of physical investment that is carried out. For instance, changing demographics and disease patterns imply that there will be less need for “bricks and mortar” investment (especially hospitals) and more need for investment in information infrastructure and human capital. The latter type of investment will strengthen the transfer of information among actors, decentralisation and well-coordinated care (including home care) and prevention and self-care. An in-depth evaluation of these issues goes beyond the scope of this report and could be included in an in-depth evaluation of the functioning of the health care system in Slovenia.

Note: Only government health expenditure has been considered in the figure and voluntary/out-of-pocket health expenditure has been excluded.

Source: OECD (2017[12]).

The financing of the health care system relies heavily on social security contributions. In 2016 the HIIS revenues were EUR 2.5 billion with 80% coming from SSCs. However, because of the low labour market participation of old and young workers and because of the ageing of the population, the funding of health care in Slovenia is under increasing pressure.

The proposal for health reform aims at addressing some of the challenges. The proposal aims at increasing revenues for the HIIS through a wide variety of measures, including making the voluntary insurance co-payments compulsory while introducing lower and upper caps. While this reform would increase the financing of the health fund, it would result in even higher SSCs. A new institution would be created to advise the Ministry of Health, and a list of indicators would be compiled on a regular basis to guide health related policy decisions.

References

[8] Auten, G., G. Gee and N. Turner (2013), “Income Inequality, Mobility, and Turnover at the Top in the US, 1987–2010”, American Economic Review, Vol. 103/3, pp. 168-172, https://doi.org/10.1257/aer.103.3.168.

[7] Kennedy, H. (2018), “Income Dynamics & Mobility in Ireland: Evidence from Tax Records Microdata”, http://igees.gov.ie/wp-content/uploads/2018/04/Income-Dynamics-Mobility-in-Ireland-Evidence-from-Tax-Records-Microdata.pdf (accessed on 14 May 2018).

[9] Ministry of Finance (2018), Bulletin of Government Finance, http://www.mf.gov.si/fileadmin/mf.gov.si/pageuploads/tekgib/Bilten_javnih_financ/January_2018.pdf.

[3] Ministry of Labour, Family, S. (2016), Making work pay in Slovenia, http://www.mddsz.gov.si (accessed on 01 March 2018).

[2] OECD (2016), Connecting People with Jobs: The Labour Market, Activation Policies and Disadvantaged Workers in Slovenia, OECD Publishing, Paris, https://doi.org/10.1787/9789264265349-en.

[5] OECD (2016), Skills Matter: Further Results from the Survey of Adult Skills, OECD Skills Studies, OECD Publishing, Paris, https://doi.org/10.1787/9789264258051-en.

[12] OECD (2017), Health at a Glance 2017: OECD Indicators, OECD Publishing, Paris, https://doi.org/10.1787/health_glance-2017-en.

[6] OECD (2017), OECD Economic Surveys: Slovenia 2017, OECD Publishing, Paris, https://doi.org/10.1787/eco_surveys-svn-2017-en.

[4] OECD (2017), OECD Skills Strategy Diagnostic Report: Slovenia 2017, OECD Publishing, Paris, https://doi.org/10.1787/9789264287709-en.

[10] OECD (2017), Pensions at a Glance 2017: OECD and G20 Indicators, OECD Publishing, Paris, https://doi.org/10.1787/pension_glance-2017-en.

[11] OECD (2017), Preventing Ageing Unequally, OECD Publishing, Paris, https://doi.org/10.1787/9789264279087-en.

[1] OECD (2018), Taxing Wages 2018, OECD Publishing, Paris, https://doi.org/10.1787/tax_wages-2018-en.

Notes

← 1. This figure is the average employee SSC rate for a single person, at the average wage, without children.

← 2. See previous note.

← 3. The tax wedge is the difference between labour costs to the employer and the corresponding net take-home pay of the employee as a percentage of total labour costs. It takes into account personal income taxes, employee and employer SSCs, payroll taxes (if any) net of cash benefits. Total labour costs are the sum of gross wage earnings, employer SSCs and payroll taxes (if any).

← 4. The net personal average tax rate is defined as the sum of personal income taxes and employee social security contributions net of cash benefits expressed as a percentage of gross wage earnings.

← 5. Similar results are observed when taking into account the PIT only.

← 6. Labour market participation rate is defined as labour force divided by the total working-age population, with labour force defined as all persons who fulfil the requirements for inclusion among the employed or the unemployed.

← 7. Employment rate is defined as employed population divided by the total working-age population, with employed population defined as those aged 15 or over who report that they have worked in gainful employment for at least one hour in the previous week or who had a job but were absent from work during the reference week.

← 8. However, early retirement will still be possible for those with more than 40 years of pension contributions.

← 9. PTRs are used to investigate the financial disincentive to move into work. They show how much of the gross income earned from moving into work from either unemployment or inactivity is “taxed” away in the form of lost out-of-work benefits, reduced income-tested benefits, and taxation of in-work income.

← 10. This distributional analysis includes taxpayers in both the flat-rate and actual cost regimes. An analysis examining these regimes separately is presented in Chapter 3.