Chapter 2. Social protection coverage in Kyrgyzstan

This chapter charts the evolution of social protection in Kyrgyzstan. It outlines the economic, political and legislative context for social protection, which is still undergoing transition from a Soviet-era system predicated on full employment, to a system more appropriate for a market-based economy with chronic unemployment and long-term poverty. It inventories existing social protection schemes, analyses their key design features and scale of operation, and discusses how well they meet the present and future needs identified in Chapter 1.

Social protection is perceived as a basic right of all citizens in Kyrgyzstan – a vestige of cradle-to-grave social protection provision under the Soviet Union. Transition to a market economy and the economic upheavals of the past three decades have undermined the feasibility of the old model, prompting a succession of major reforms to the social protection system.

The Government of Kyrgyzstan (GoK) spends more on social protection than on any other area. A broad range of programmes exits across the main pillars (social assistance, social insurance and labour market policies), along with the health care system. However, these pillars are not equally well developed and have evolved at different times in response to different demands, leading to fragmentation. Social insurance programmes achieve much greater coverage than social assistance and active labour market policies, which were established only after the collapse of the Soviet Union.

Moreover, the challenges identified in Chapter 1 are undermining existing social protection provision. Informality and declining labour force participation threaten the sustainability of the social insurance system, while fiscal and structural constraints limit the impact of social assistance on poverty and the effectiveness of labour market policies.

Kyrgyzstan’s social protection system has shrunk since the Soviet era but remains large

In 1990, approximately half the population of Kyrgyzstan received either pensions or family allowances. In the same year, expenditure on social protection was 29% of gross domestic product (GDP), a level of spending only sustainable due to transfers from the Soviet Union (World Bank, 1993[1]). When these transfers disappeared in 1992, the existing system of social protection became unviable.

A second shock occurred when the country embarked on a programme of rapid liberalisation, which fundamentally changed the structure of the economy and led to increases in poverty, inequality, unemployment and inflation. Closure of state-owned enterprises not only destroyed large quantities of jobs but also removed an important provider of social protection.

The first phase of social protection in Kyrgyzstan thus consisted of keeping the Soviet-era system from collapsing as well as protecting large portions of the population from destitution. Contributions to social insurance arrangements shrunk and demand for social assistance increased, especially instruments aimed at protecting children from poverty, reflecting the fact that approximately half the population was under the age of 20. The GoK was also required to support the incomes of unemployed workers and assist them in finding new work and acquiring new skills (World Bank, 1993[1]).

At the same time, the GoK was bound by severe fiscal constraints. Revenues declined dramatically due to the contraction of the economy, the decline in labour force participation and the abrupt end to transfers from the USSR. Government spending shrunk significantly as a result: expenditure on education and health was cut repeatedly in the early- to mid-1990s and social protection spending was also reduced, principally via reductions to family allowances.

Expenditure on the seven different types of family allowances fell from 6.7% of GDP in 1991 to 2.6% of GDP in 1992 (World Bank, 1993[1]). Pension spending nearly halved over the same period, falling from 7.0% of GDP to 3.6% of GDP, even though a large number of workers took early retirement. Importantly, GDP fell significantly in real terms over this period, compounding the decline in spending. Subsidies – food subsidies in particular – also decreased, despite high levels of food poverty (World Bank, 2000[2]).

When the macroeconomic performance improved and fiscal conditions stabilised from 1995 onwards, the GoK embarked on a second phase of longer-term structural reforms to social protection. It implemented major reforms to public health care and the pension system in the latter half of the 1990s, and introduced the first poverty-targeted social assistance programme: the Unified Monthly Benefit (UMB).

Social assistance was established in law, in recognition that social insurance coverage in the new market economy would not be universal, i.e. that benefits previously provided on a contributory basis would need to be replaced by non-contributory programmes. A large-scale “residual” social protection instrument for people excluded from the economy was needed.

Unlike the Monthly Social Benefit (MSB), which was established to provide the same categorical coverage as the social insurance system to people outside the formal labour market, the UMB was a departure from the family allowances. Family allowances were eliminated, and the UMB paid benefits at much lower levels, with much less coverage and at much lower cost to the GoK (World Bank, 2000[2]). The concept of a guaranteed monthly income – initially called the guaranteed minimum consumption level – was introduced as a benchmark for benefit levels and as a threshold for eligibility for social assistance payments.

However, these reforms only partially resolved the central dilemma facing the GoK for the past 25 years: how to respond to a fundamental shift in the demand for social protection brought about by the economic transition, in a context of limited resources and high levels of informality, without reneging on entitlements generated by the previous system? Initial reforms did not go far enough to adapt to the new socio-economic conditions, and parametric reforms implemented subsequently have not changed the structure of social protection provision.

Moreover, reforms to the social insurance arrangements and the introduction of new social assistance and labour market programmes were not carried out in a systemic fashion. As a result, there was a significant fragmentation of social protection provision and policy making that has obtained to this day.

Many post-Soviet countries have faced the challenges of transitioning from a social protection system predicated on full employment. Kyrgyzstan is unique for the extent to which it has sought to maintain entitlements established by the Soviet system despite the costs, both in overall expenditure on pensions and the crowding-out of other social protection spending.

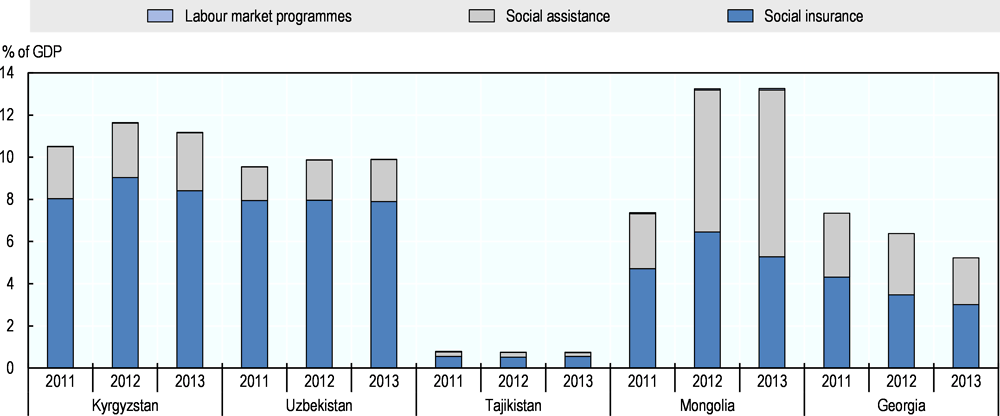

Kyrgyzstan spends more on social protection than the other benchmark countries (Georgia, Mongolia, Russian Federation, Tajikistan and Uzbekistan) for which data exist, with the exception of Mongolia, whose GDP per capita has tripled since 1992 (Figure 2.1). In contrast to Mongolia and Georgia, social insurance accounts for the vast majority of Kyrgyzstan’s social protection spending. Spending on labour market policies is extremely low across the benchmark countries.

Note: No information available for the Russian Federation or Kazakhstan.

Source: ADB (2013[3]), Social Protection Index (database), http://hdl.handle.net/11540/79, accessed December 2017.

Social protection is enshrined in the Constitution

The current system of social protection is enshrined in the 2010 Constitution, which was promulgated following the change of government in that year. Article 9 stipulates state obligations to:

-

Establish decent conditions of life and free personal development as well as assistance to employment.

-

Ensure support to socially vulnerable categories of citizens, guaranteed minimal level of labour remuneration, protection of labour and health.

-

Develop a system of social services and medical services and establish state pensions and benefits as well as other social security safeguards.

Article 53 expands on what social protection entails:

-

Social security in old age, in case of disease and in the event of disability or loss of the breadwinner shall be guaranteed to the citizens;

-

Pensions and social assistance in accordance with the economic resources of the state shall ensure a standard of living not lower than the minimum subsistence level established by the law.

The specific inclusion of social assistance in the 2010 Constitution was a departure from the 1993 Constitution. Articles 27 and 28 of the 1993 Constitution committed the state to provide income support in the event of a worker’s retirement, disability or illness and to provide a standard of living not below the minimum wage established by the law, subject to the resources it has at its disposal. This constitution also acknowledged the state’s responsibility to provide protection against unemployment. The Constitutions of 1993 and 2010 identify a clear role for local government in supporting the implementation of social protection programmes.

Social protection featured prominently in the GoK’s National Poverty Reduction Strategy (NPRS) in 2002, which was part of the Comprehensive Development Framework of the Kyrgyz Republic to 2010 – the county’s first national development plan. The NPRS placed an emphasis on targeted social assistance and on strengthening the link between individuals’ contributions to the pension system and their retirement benefits to ensure the system’s sustainability.

There were two major structural reforms to social protection towards the end of the first decade of the 2000s: the inclusion of a fully funded component in the pension system and the monetisation of in-kind benefits for certain “privileged” groups. The GoK also introduced new subsidies and increased the benefit levels of existing social protection programmes to compensate for substantial increases in electricity prices in 2009/10.

These latter measures did not quell popular anger about the tariff increases or numerous other public services- and governance-related issues. Revolution ensued in April 2010 (Wooden, 2014[4]). The resultant change in government was a pivotal moment for the country’s democratic development, and social protection was at the forefront of the new government’s priorities. One of its first actions was to roll back the tariff increases, leaving in place measures to compensate the population for their impact. The combined impact of monetising the privileges, the electricity subsidy and the increased benefit levels caused a step-change in social protection spending.

The present analysis of social protection provision principally concerns the period since 2010. The GoK has published its first two social protection strategies, covering 2012-14 and 2015-17, respectively. These strategies were based around the identification of vulnerable groups. The first strategy identified four such groups: families and children in a difficult life situation; people with disabilities; elderly citizens; and homeless people. The second strategy specified three vulnerable groups; these were the same as in the previous strategy with the exception of homeless people.

Between these two strategies, the GoK launched the National Sustainable Development Strategy for the Kyrgyz Republic for the Period of 2013-2017, a development plan whose recommendations for social protection closely follow the first social protection strategy.

At the time of writing, a third social protection strategy and a new development plan are under development. The new social protection strategy focuses on programmes rather than vulnerable groups. It will feed into the national development strategy called 40 Steps to a New Era, which covers the period 2018-2022. Social protection is included under Step 28: “Equal opportunities - base for development of the society”.

This chapter begins by examining the most important programmes within the three main pillars of the social protection system in order of their size: social insurance, social assistance and active labour market policies. It examines the coverage of different programmes and recent policy developments with reference to the needs identified in Chapter 1.

Social insurance coverage is almost universal among the elderly

Social insurance dominates the social protection system both in terms of coverage and expenditure, a legacy of the Soviet economic system whereby full employment entailed universal coverage by social insurance. The contributory system in place at the end of the Soviet Union consisted of a Pensions Fund, a Social Insurance Fund and an Employment Fund that provided a full range of social protection instruments except for poverty-related income support (which in theory would not be necessary in a context where employment was guaranteed).

During the Soviet era, social insurance provision was divided between a complex system of government agencies and state enterprises. Nowadays, the state pension system provides a more limited range of benefits and is overseen by the Social Fund, a Ministry-level institution established in 1993 to co-ordinate the different social insurance arrangements established prior to the collapse of the Soviet Union. The Social Fund initially reported to the Ministry of Labour and Social Protection (MLSP) but in 1998 it was granted full autonomy and in 2000 was made responsible to the President alone (Andrews et al., 2006[5]).

The Social Fund’s responsibilities, as codified in 2004, are to design social insurance policy, provide pension payments to the insured population and ensure the financial sustainability of the social insurance system (GoK, 2004[6]). Not all the benefits that are paid by the Social Fund are contributory: it also pays pensions or top-ups to certain groups on a non-contributory basis based on categorical status rather than contributions:

-

pensions for military personnel

-

pensions for Heroine mothers and mothers of children with disabilities

-

top-ups for individuals working in highland conditions or remote areas

-

increments for persons with disabilities

-

increments for outstanding military and civil service

-

a compensatory increment for the increase in electricity tariffs

Full, formal employment in the Soviet era not only ensured high social insurance coverage but also the financial sustainability of the system through a large contribution base. Until 2000, social security contributions worth 39% of wages were required (33% employer/6% employee), a rate that proved a major impediment to formal job creation following the transition to a market economy and which could therefore not be sustained. Thereafter, the contribution rate was reduced progressively. As of 2018, the rate for formal workers is 27.25% of salaries, of which 25.00% is for pensions, 2.00% for health insurance and 0.25% for an occupational injury arrangement.

Pension coverage of the elderly is almost universal: the World Bank (2014[7]) calculated that pension coverage as a proportion of the population over age 65 was 142% in 2011, reflecting coverage rates among that age group in excess of 90% and significant early retirement from the system. According to Social Fund data, there were 661 000 beneficiaries (including retirement, disability and survivor pensioners) in 2016, up from 466 000 in 2011 – a 42% increase (Social Fund of the Kyrgyz Republic, 2018[8]).

Recent data for the number of contributors are not available, but this figure appears to be growing far more slowly: the number of contributors increased by 15% between 2010 and 2013, from 1.16 million to 1.33 million. This disparity in growth rates means that the number of contributors per beneficiary – a key variable for the sustainability of a pay-as-you-go pension system – is already below two beneficiaries per worker and is expected to decline further.

Moreover, the proportion of contributors in the formal sector declined from 63.1% of contributors in 2011 to 59.1% in 2014. This implies that the number making full contributions is declining. The majority of self-employed workers contribute at a rate equivalent to 10% of the economy-wide average wage (9% to pensions and 1% to health), although there are special categories of the self-employed with contribution rates of 12%, 6% or 3% of the average wage. Farmers’ contributions vary by the amount of land they own, with many contributing 1% of their income or less. In 2011, farmers accounted for 34% of contributors and salaried workers accounted for 60%, with the self-employed comprising the balance.

Because of these high coverage levels, pensions are the principal means of poverty alleviation not only among the elderly but also among younger generations, as shown by the Latent Class Analysis in Chapter 1. However, high coverage is not synonymous with generosity and pension receipt is no guarantee against poverty (discussed in Chapter 3).

Successive administrations have been unable to arrest the decline in pensioners’ purchasing power. In part, this is a function of challenges identified in Chapter 1: a decline in per capita incomes, contraction of the formal labour force and growth in the elderly population since the collapse of the USSR. A reduction in the contribution rate has also contributed to the fall in pension values. However, the design of the pension system is also responsible for the decline, as will be discussed below.

A high contribution rate is an endogenous challenge to pension coverage. Unfunded pension arrangements need a certain level of contributions to meet their commitment to older workers, but if the contribution rate is so high as to deter workers from contributing then the adverse impact is felt for current and former workers alike: payments to current beneficiaries cannot be made and current workers will not be eligible for pensions when they retire.

Old-age pensions

The pension system in place at the collapse of the Soviet Union has undergone major reforms since 1992. These measures have sought to improve the sustainability of the pension system without affecting the entitlements accrued prior to reforms or significantly altering the structure of the system. As a result, the pension system confronts major structural challenges to its sustainability and is increasingly reliant on support from the Republican Budget (discussed in Chapter 4).

The largest reforms took place in 1997. In response to recurrent deficits in the Social Fund, which reached 1.7% of GDP in 1996, the Government committed to increasing the retirement age by three years for men and women over a nine-year period (to age 63 and 58, respectively) and a new pillar was introduced to the pension system (IMF, 2000). The Soviet-era defined benefit arrangement, which has become known as the SP1 component, was closed to new members and to further contributions from existing members, but the entitlements it generated for workers who had contributed up to that point remained valid. This part of the system will remain operational until around 2035-40 (Schwarz et al., 2014[9]).

At the same time, a new pillar – the SP2 component – was introduced for contributions made from 1997 onwards and is commonly assumed to cover individuals born after 1980. This arrangement is run on a notional defined contribution (NDC) basis, meaning contributors are no longer guaranteed a certain level of benefits in retirement but generate an accumulation throughout their working careers that will be converted into an annuity at retirement. In both systems, contributions by today’s workers are used to finance the benefits of current retirees. This move to an NDC system was consistent with the approaches taken in various other countries in the region around the same time (World Bank, 2012[10]), most notably Latvia (Müller, 2005[11]).

The 1997 reform sought to retain a strong link between a pensioner’s benefits in retirement and their income during their career at a time when replacement rates (the proportion of the former to the latter) were low and declining. This principle was reinforced by the introduction of a defined contribution pillar in 2010, which is currently financed by contributions worth 2% of a worker’s salary. This arrangement works on a funded basis, meaning workers contributions are invested and the capital plus interest will be paid to a worker upon retirement. The Social Fund initially proposed funded individual accounts in 2002 but this was opposed by the World Bank on the grounds that Kyrgyzstan’s financial markets were not sufficiently well developed to accommodate such arrangements (World Bank, 2014[7]), a concern that remained more than a decade later (Andrews et al., 2006[5]).

These arrangements are built on a basic pension component, which is set at a maximum rate of 12% of the economy-wide average wage. The basic pension is quasi contributory insofar as it is payable to individuals according to the duration of their contributions but not the value of their contributions nor the rate at which they contributed. For individuals with shorter contribution histories than the statutory minimum, the basic pension payout is pro-rated.

The design of the basic pension component means that it is highly redistributive between workers at different income levels. This is an important means of incentivising individuals to contribute but it allows people to game the system by opting for one of the lower contribution rates.

As well as a basic pension, a social pension exists for elderly individuals who did not contribute to the social insurance system while they worked, although the eligibility age is higher than the statutory retirement age governing receipt of the pension. This social pension is contained within the MSB (discussed below).

Table 2.1 shows the structure of the pension system. As of 2018, an individual’s pension in retirement comprised the basic pension plus their entitlement to SP1 and SP2. For the SP1, the benefit is calculated as the length of service multiplied by the average monthly wage over the five years in which their earnings were highest and by an accrual rate of 1%. For the SP2 component, the benefit is calculated as the (notional) accumulated contributions multiplied by an actuarial factor that reflects an individual’s age of retirement and life expectancy across the population.

The decline in average pension levels reflects the design of the insurance components (SP1 and SP2) rather than the value of the basic pension, which is indexed to average earnings. For the SP1 contributions, the 1% accrual rate is not very generous; it implies that workers who contributed for 40 years receive a pension from this component worth 40% of their highest earnings, which is not particularly high given the level of contributions. However, the SP1 is more generous than the SP2 component, the pensions from which are constrained by the way past earnings are indexed: the Social Fund adjusts the value of pension contributions over the most recent year to reflect the impact of price rises but not the value of the entire (notional) accumulation, meaning the value of previous contributions reduces significantly over time in real terms.

By allowing inflation to erode the value of pension accumulations, the SP2 has protected the solvency of the Social Fund but has also contributed to the decline in pension values. According to World Bank calculations, the average pension will decrease from 43% of the average wage in 2011 to 25% of the average wage over the subsequent three decades unless the indexation method is changed. The pension for groups whose contributions are set at a lower rate, such as the self-employed and farmers, will be below this level.

In part, the GoK is able to address low pension levels by adjusting their value post retirement. At present, such adjustments are made in an ad hoc manner and typically link pension increases to wage growth in the economy, a strategy that is costlier than indexing to prices and thus reinforces the need to restrict the value of pension accumulations.

Moreover, the Social Fund is increasingly reliant on the Republican Budget to subsidise pension expenditure (discussed in Chapter 4). This reflects not only a policy decision that the basic pension should be fully financed by transfers from the Republican Budget but also the growing burden of military pensions.

There are two principal concerns with military pensions beyond the fact they are non-contributory. The first relates to the very low retirement ages, whereby individuals are able to retire upon attaining 20 years of service or reaching age 50 (for men) and 45 (for women) – whichever happens first. The second relates to the fact it is not only members of the military who are covered; employees from a wide range of government agencies with a security component are also eligible (GoK, 1993[13]).

Disability and survivor pensions

In addition to old-age pensions, the Social Fund provides benefits to contributing workers in the event of disability and pays survivor benefits to a worker’s household in the event of death before retirement. In 2011, the proportion of beneficiaries for each of the three components was 71% for old age, 19% for disability and 10% for survivorship (World Bank, 2014[12]).

Disability pensions follow the same structure as old age pension system and are payable until vocational rehabilitation or for life. Contributors to the Social Fund are entitled to a disability pension provided they have contributed for the following periods at the age of onset:

-

aged 23 years or younger: 1 year

-

aged 23-26 years: 2 years

-

aged 26-31 years: 3 years

-

aged 31 years and older: 5 years.

The level of disability payment depends on the degree of disability: Group I (total disability and requiring constant attendance), Group II (total disability with an 80% loss of mobility) or Group III (partial disability with some loss in working capacity). The GoK assigns disability pensions equal in value to the basic and insured (SP1 and SP2) old-age pensions for those with disabilities in groups I and II and 50% of the old-age pension for people with disabilities in Group III.

A contributor’s dependants are eligible for pension payments should a contributor die before retirement age. The following categories are eligible for survivor pensions:

-

children up to age 16 (over age 16 if they have disabilities)

-

siblings or grandchildren up to 16 years of age

-

parents or spouse, if they have reached the pensionable age or have disabilities by the time of the contributor’s death.

The survivor pension benefit is a sum of the basic and insured (SP1 and SP2) pension components for disability Group II, assigned at the following rates:

-

one dependent: 50%

-

two dependents: 90%

-

three dependents: 120%

-

four or more dependents: 150%.

Social assistance is small in scale and caught between categorical benefits and poverty-targeting

Social assistance is implemented on a much lower scale than social insurance, reflecting the legacy of the Soviet social protection system. As the World Bank (1993[1]) noted in its report on social protection in Kyrgyzstan: “At present there is no system of social assistance in Kyrgyzstan…To date, [it] has been largely synonymous with charity, caring for orphans, the elderly, the infirm, the disabled, and so forth.”

Social assistance is managed by the Ministry of Labour and Social Development (MoLSD), which also has responsibility for labour-market programmes. As of 2015, the two largest programmes were the poverty-targeted Monthly Benefit for Poor Families with children (MBPF, previously called the UMB) and the MSB, a categorical benefit for people with disabilities and other vulnerable groups. Combined expenditure on these programmes was 1.2% of GDP in 2015, versus 7.4% of GDP spent on pensions in the same year.

Monthly Benefit for Poor Families

As of 2017, the MBPF provided a monthly cash transfer to households with contain children under age 16 (or under age 18 if they are still in education) whose per capita income does not exceed the value of the guaranteed minimum income (GMI). According to official data, the programme covered 304 000 children in 2015, or around 5% of the total population.

Applying for the MBPF is a complex process involving a range of institutions and documentation. Households apply for the benefit to the MoLSD branches at rayon (district) level or, if they reside in rural areas, to the aiyl okmotu (community government). When applying for the benefit, households must supply information regarding their income, household and assets, including the amount of land they own. This information forms the basis of an official document known as the social passport for poor families (SPPF), which is filled in either by MoLSD staff or social protection specialists employed by the aiyl okmotu. A commission from the aiyl okmotu then visits the household to verify the information it provided (CASE/MoLSD/UNICEF, 2008[14]).

Once the information is verified, the rayon-level branch of the MoLSD calculates whether a household’s per capita income falls below the means test threshold. This calculation takes into account cash income as well as imputed or in-kind income from land and possession of durable goods and livestock. The MoLSD aims to visit 30% of new recipients to double-check they meet eligibility requirements. Should a household be deemed eligible, it receives the MBPF for one year, after which it must reapply. Payments are made via the post office; beneficiaries typically collect these payments themselves but in some cases they will receive them by post.

Since 2015, the value of the benefit has been set equal to the value of the GMI. Previously, it was calculated as the difference between a household’s aggregate per capita income and the value of the GMI. This link between the value of the GMI and the MBPF is not legislated: the value of the latter can vary (either up or down), according to government resources.

Benefits values are multiplied by an altitude coefficient which is applied to all public payments (including social protection benefits and public-sector wages) according to the altitude at which each rayon is situated. This represents a belief that individuals living at high altitudes are in greater need of support from the state. The altitude coefficient ranges from 1 to 1.95, meaning that the value of MBPF is almost twice as high for individuals living in extremely mountainous areas than the standard value of the benefit.

The MBPF’s predecessor, the UMB, was established to eliminate extreme poverty. The connection between the MBPF and extreme poverty remains codified in the design of the programme even though extreme poverty has almost been eliminated. The income eligibility threshold is set at the same level as the GMI, which was introduced at a level around 50% of the extreme poverty line (EPL) for affordability reasons, with the intention of equalising the two benchmarks. This increase never transpired; in fact, the GMI dropped as low as 21% of the EPL before returning to its original level in 2015. This highly restrictive targeting means that the MBPF has in fact been aimed at only the poorest of the extreme poor.

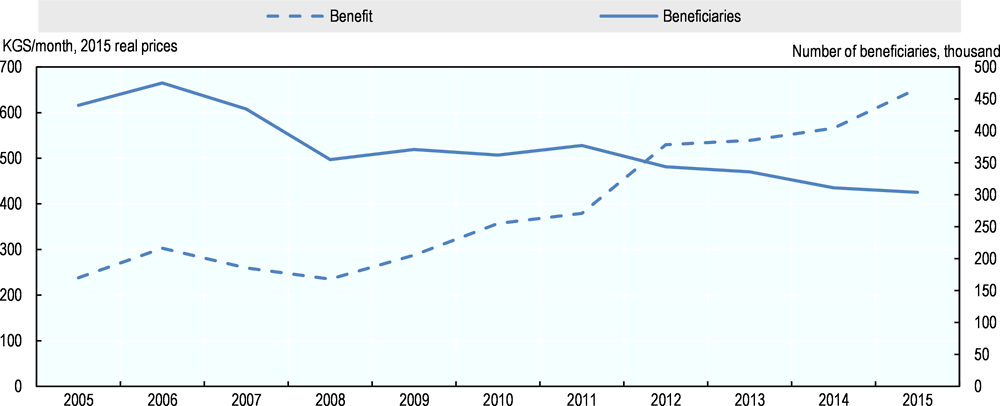

The restrictive targeting criteria and the near-elimination of extreme poverty have driven a decline in the number of beneficiaries. Between 2005 and 2015, the number of beneficiaries fell from 440 000 to 304 000 (Figure 2.2). This represents a reduction in coverage of just over 30% in absolute terms and an even larger decline in relative terms, since the number of children grew over this period.

Source: Authors’ calculations based on NSC (2015[15]), Kyrgyz Integrated Household Survey (database).

The sharpest decline in coverage occurred between 2005 and 2008, when the poverty rate also declined by 10 percentage points. Changes to the design of the MBPF might also have contributed to the decline: targeting criteria were tightened by including durable goods and livestock in the proxy means test and updating valuations of revenue from land.

The decline in coverage has been accompanied by increases in benefit levels. Between 2005 and 2015, the average benefit level more than doubled in real terms (in 2015 prices). The overall effect has been to increase spending on the MBPF, which overtook the MSB as the largest social assistance programme in expenditure terms in 2015. The increase in benefit levels magnifies the cost of targeting errors.

The MBPF’s impact in reducing poverty is diminished by both errors of inclusion (ineligible households receiving the MBPF) and exclusion (eligible households not receiving it). In the strictest terms, inclusion error is built into the programme, given it is targeted at extremely poor households with children, the number of which has fallen declined to very low levels. Yet, even by this strict definition, exclusion errors occur.

As in many other countries, identifying and enrolling the very poorest households is a major challenge. It is a particular challenge in the case of the MBPF given the complexity of the income assessments, the low capacity of the local-level of social workers employed to implement these assessments and the remoteness of the locations where many poor individuals reside.

How agricultural incomes are imputed is a major weakness of the programme. As Kyrgyz agriculture is semi-subsistence, and virtually all produce sales are cash-based, direct accounting for household income from agricultural activities is challenging. The means test uses imputed agricultural income norms that are usually very low and rarely adjusted for inflation, leading to an underestimation of the imputed income from land that allows the GMI (the means test threshold) to be kept very low. This effectively excludes urban households from the programme, such that more than 90% of MBPF beneficiaries reside in rural areas.

Targeting errors might also be driven by the fact that livestock provisions do not take household size into account. A household with two residents is granted the same livestock allowance under the income assessment as one with eight. The means test’s failure to account for income from remittances might exacerbate inclusion errors, while its failure to take into account household labour potential might do the same for exclusion errors; a household’s landholdings might exclude it from the MBPF even if no resident can use the land.

Potential MBPF beneficiaries face high application costs. Registering often requires multiple documents and travel to rayon (district) centres to collect them – a more significant impediment for those with the lowest incomes. The absence of an electronic document circulation system among government agencies increases application costs for beneficiaries. The complexity of the application process and the number of role players involved also creates room for corruption.

Monthly Social Benefit

The MSB is a descendent of invalidity pensions (also known as social pensions) paid out during Soviet times, which has since expanded to include seven groups considered vulnerable or living in difficult conditions:

-

children under age 18 with disabilities

-

children of mothers living with HIV/AIDS, until 18 months

-

persons with lifelong disabilities (Groups I, II and III), if not eligible for a pension

-

persons with systemic disabilities (Groups I, II and III), if not eligible for a pension

-

senior citizens who are not eligible for a pension

-

mothers of seven or more children who are not eligible for a pension (known as Heroine mothers)

-

orphaned children, if not eligible for a survivor pension.

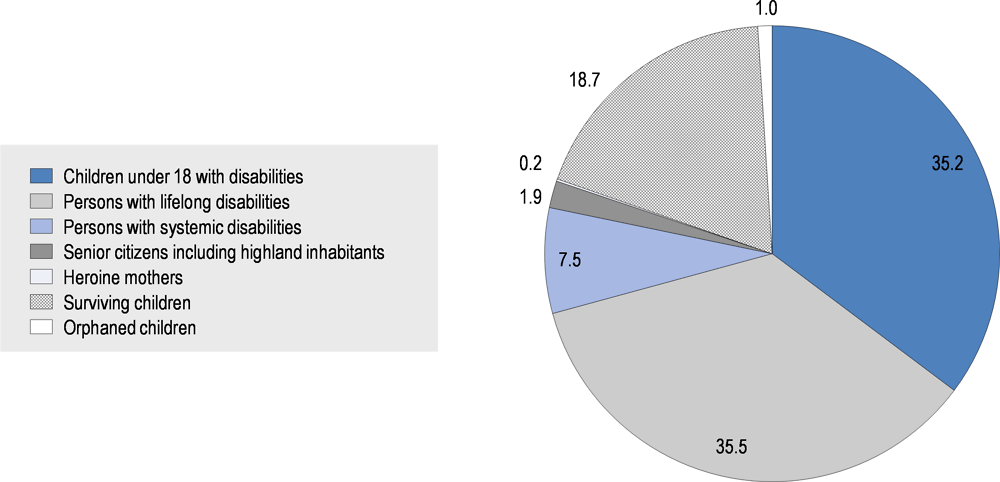

In 2015, 78.5% of MSB beneficiaries were people with disabilities; among this group, 45% were children (Figure 2.3). Each of the disability categories is sub-divided. For adults, lifelong and systemic disability are divided into Groups I, II and III. For individuals under age 18, there are different categories, including general disabilities, cerebral palsy and those with HIV/AIDS.

Source: Authors’ calculations based on NSC (2015[15]), Kyrgyz Integrated Household Survey (database).

The number of people covered by the MSB has grown steadily, from 53 900 in 2005 to 80 500 in 2015 (Figure 2.4), the 2015 figure representing about 1.3% of the population or about one-quarter of the number of MBPF beneficiaries. Despite the disparity in coverage between the two programmes, the MSB was the largest social assistance programme in expenditure terms until 2015, reflecting the fact that MSB benefits have historically been higher than those of the MBPF.

Source: Authors’ calculations based on NSC (2015[15]), Kyrgyz Integrated Household Survey (database).

There is overlap between the categorical benefits covered by the MSB and the compensations for privileges for special population groups (Box 2.1). Although these transfers, which are a legacy of the Soviet era, are financed through the budget of the MoLSD, they are treated separately from state benefits. This reflects their history: until 2010 the privileges were in-kind payments to groups on the basis of merit rather than need. As a result, not all privileges can be considered as social protection instruments; reprioritising funding towards state benefits would be a political choice that has so far been resisted.

One of the most contentious features of the Kyrgyz social protection system are the state privileges to compensate certain groups for vulnerabilities or contributions to the previous regime. Before 2010, this system was governed by ten laws (ADB/IMF/World Bank, 2010[16]), providing 40 types of privileges to 39 categories of beneficiaries (World Bank, 2014[7]). Privileges were usually price discounts for utilities, housing, health services and sanatoriums, and various other municipal services.

A 2010 reform reduced the number of privileged groups to 25 and replaced price discounts with monetary benefits, known as compensations for privileges. Under the new system, the value of cash benefits varies between categories1, from a minimum of KGS 1 000 to a maximum of KGS 7 000 per month. Recipients remain eligible for early retirement or pension top-ups that existed under the previous system and are financed by the Republican Budget, paid through the Social Fund.

As of 2017, beneficiaries of the compensations for privileges include veterans of the Second World War, survivors of concentration camps, heroes of the Soviet Union or the Kyrgyz Republic and individuals involved in clean-up operations following the Chernobyl nuclear disaster. However, less venerated groups, such as people living in mountainous areas and people with disabilities, account for the majority of recipients.

The monetisation of privileges led to a spike in the cost of the programme, in part because many beneficiaries were unable to access services that they would have received at a subsidised cost. In 2010, spending on compensations was approximately 75% of combined spending on the MSB and the MBPF, leading to intense pressure to reprioritise from privileges to state benefits.

The burden of the compensations has diminished considerably since then (discussed in Chapter 4). The value of benefits was frozen at their 2010 level, leading to a significant decline in their real value. Moreover, the death of elderly beneficiaries is likely to further reduce spending into the future.

Supplementary Monthly Social Benefit

The Supplementary Monthly Social Benefit (SMSB) is a categorical benefit awarded to the families of those killed and injured in the violence that occurred in 2010, regardless of income or access to other social benefits.

Maternity benefit

In the Soviet and early post-Soviet era, maternity benefits were paid from the Social Insurance Fund. The link between contributions and eligibility was weak: all women who gave birth to a live child were eligible for a one-time, flat-rate payment set at two months of the minimum wage. Maternity leave was also paid to all employees for a period of 126 days (140 days in certain circumstances) at 100% of salary, regardless of length of service. The expense was considered a deterrent in hiring women (World Bank, 1993[1]).

Today’s maternity dispensation is much less generous. As of 2017, there was no once-off benefit for the birth of a child, although a reform of state benefits in 2018 might reintroduce it. Entitlement to paid maternity leave is also restricted to women who pay tax or are registered as unemployed, thus excluding the informal sector.

According to a 2011 government decree, the duration of paid maternity leave is 126-180 days, depending on the difficulty of delivery, the number of births and the region. Only employed women living in mountainous areas are entitled to a benefit worth 100% of salary throughout their maternity leave. Otherwise, women in formal wage employment are eligible for 100% of their salary for just ten days, whereupon the benefit drops to ten times the so-called imputed rate2, paid by the Republican Budget. Women who are (formally) self-employed, who work in farm enterprises or who are registered as unemployed are entitled to a benefit equivalent to ten times the imputed rate for the duration of their maternity leave.

In 2015, the average maternity benefit was KGS 7 660). The benefit payable to women who are either self-employed, members of farm enterprises or registered as unemployed was KGS 3 500. The benefit payable to women residing and working in mountainous and remote areas exceeded KGS 30 700.

Funeral benefit

Kyrgyzstan citizens are entitled to a funeral benefit, the level of which varies according to a range of factors stipulated in the 2011 decree that also governs maternity payments. For different categories of deceased individual, the benefit is calculated with reference either to the average wage, the imputed rate or the basic pension. Annex 2.AB details the different benefit levels. The benefit is not paid for Kyrgyzstan workers who die abroad.

School meals

The Ministry of Education and Science is integrating social protection into its plans as a means of making education more pro-poor. The sectoral budget for 2012-2020 allocates resources for catering services in primary schools with a view to increasing enrolment of low-income students. The World Food Programme is supporting the school feeding initiative for children in grades 1-4 by funding the purchase of kitchen equipment to provide hot meals using the KGS 7-10 per child provisioned by the Republican Budget in 275 schools.

Natural disasters

The MoLSD provides assistance for those affected by natural disasters in the form of grants and loans. However, the Ministry has no specific capacity for emergency assistance and does not have a mandate to support affected individuals or communities recover from livelihood losses caused by natural disasters.

Social services still consist mostly of residential care

The state has an obligation to provide social services to poor and vulnerable groups, such as children, the elderly and people with disabilities, as codified in Article 5 of the 2010 Constitution. In practice, only a very small proportion of vulnerable individuals or households have access to social services, due to a lack of resources, low capacity at local level and the absence of a clear statutory framework for social services. As a result, residential institutions remain the foremost social services intervention in Kyrgyzstan, despite the GoK’s commitment to making the enrolment of vulnerable individuals in such institutions a last resort (Box 2.2).

The extremely low provision of social services represents a major gap in the social protection system and severely constrains the impact of other social protection interventions. For instance, it will not be possible to enhance the impact of state benefits without enhancing the capacity of social workers at local government level, since they are responsible for identifying poor households.

Improving social services nationally is complicated by the fact that social services are a core function of the aiyl okmotu, the administrations of the aiyl aimak. Aiyl okmotu are responsible for implementing economic development and social protection programmes and for ensuring the welfare of poor and vulnerable residents. They are also responsible for verifying and updating the information contained in SPPFs and thus play a critical role in the payment of state benefits. In reality, however, social protection is one of the functions of local government that is not executed due to a lack of resources Mukanova (2007[17]).

Aiyl okmotu must employ one social protection worker for every 5 000 inhabitants (GoK, 2011[18]). However, training opportunities are limited and a very low proportion of social protection experts at a local level are qualified: according to GiZ (2012[19]), only 6% of social workers have a basic education in social work. An important part of enhancing capacity is standardising the status and responsibilities of these social workers, which in turn relies on an overarching legal and regulatory framework for the sector. There is not even uniformity regarding key terms used in the design and implementation of social services.

In recent years, the MoLSD at rayon level has sought to play a greater role in the provision of social services. The Ministry must employ one member for each of the 459 aiyl aimaks to implement sector policies, such as the identification of poor households, maintain the SPPF and develop capacity among local social workers. However, the budget allocated to their activities is extremely small.

It is critical that a state guaranteed minimum level of social services provision be established in law. From this starting point it will be easier to allocate roles and responsibilities for the provision of social services between the MoLSD and local government and thence to allocate budgetary resources and manpower accordingly.

There is significant scope for local and international non-governmental organisations to support the GoK in the provision of social services; however, the modalities for them to do so are largely absent. More of the NGOs in Kyrgyzstan are active in the provision of social protection than in any other activity (ADB, 2011[20]). However, the institutional and financial arrangements required to harness these activities in support of an overarching vision for social services are extremely limited, not least by the absence of such a vision.

The MoLSD is responsible for accrediting NGOs and monitoring their activities. It can also outsource the provision of social services by contracting with NGOs. However, the Ministry is only able to finance these services on budget rather than by creating a results-based spending modality that would have the potential to increase financing for the sector in line with improved performance.

Residential care for orphaned or abandoned children and people with disabilities accounts for the majority of social services provided in Kyrgyzstan. Although such institutions play a less central role in social protection than in Soviet times, the number of children enrolled remains high. While there have been substantial improvements in the quality of these institutions in recent years, they are still associated with a range of adverse developmental impacts (Ismayilova and Huseynli, 2014[21]).

The state’s responsibility to raise children who are orphaned or deprived of parental care is enshrined in Article 36 of the Constitution. The number of children in institutional care increased by 69% between 1991 and 1994 (Tobis, 2000[22]). As of 2012, 10 908 children were in residential care across 117 different institutions (Ismayilova and Huseynli, 2014[21]). The number of children in residential care increased between 2005 and 2010, a period of rapid declines in poverty and in MBPF coverage.

Chronic poverty is a strong underlying factor for enrolment in the majority of cases. According to a 2005 study, children from single-parent families, large families or families vulnerable for other reasons are most likely to be enrolled; only 6% had lost both their parents. Children tend to stay for as long as they are age-eligible rather than leave as soon as conditions at home improve.

Although residential homes provide a full range of child services, budget constraints and overcrowding severely limit the level of care. As a consequence, children who attend these institutions often experience major challenges integrating into society.

This challenge is especially serious for children with disabilities, who accounted for 29% of all children in residential care in 2014 (UNICEF, 2014[23]). In the Soviet Union, almost all children with disabilities were put in residential care and faced higher levels of social exclusion as a result of their care tenure; conditions in institutions for disabled children were grim relative to other residential institutions. While the situation has improved since the collapse of the Soviet Union, progress has been hampered by resource constraints, lack of capacity among social workers and stigmatisation.

State provision of residential institutions is highly fragmented. Boarding schools, run at the local level, account for 27% of these institutions and 40% of children in residential care. The MoES runs 20% of these institutions, with 34% of children in residential care, while the Ministry of Health (MoH) runs three institutions for 200 infants. The MoLSD and the Ministry of Internal Affairs are also responsible for residential institutions. Privately-run institutions, which operate outside government control and without accreditation, run 33 residential institutions of different types, providing care for 13% of all children in residential care.

Since the introduction of the Child Code in 2012, the number of children enrolled in public institutions has declined due to the introduction of gatekeeping measures to ensure care in public residential institutions is a last resort and sanctioned by a court. The Code also gives local government greater responsibility for protecting children. However, private institutions are still able to take children on demand.

At the time of writing, a major policy push to reform residential institutions is drawing to a close. The Government Decree “On the Optimization of the Management and Financing of Residential Child Care Institutions of the Kyrgyz Republic 2013-2018”, signed in 2012, has two objectives: to reduce the number of residential institutions for children and to promote community-based and kinship care services whereby at-risk children are placed with extended family members or cared for in the community rather than in institutions.

While this approach is to be encouraged, it is unlikely to address many of the factors that drive demand for residential institutions. As discussed in Chapter 5, a systemic approach to vulnerable children (and their wider households) involving state benefits, social services and access to education and health care is needed to reduce reliance on public institutions to provide care.

Residential care for the elderly is much less prevalent than the institutionalisation of children, in large part for cultural reasons. Some 6 000 elderly receive social care at home compared with 400 in institutions. As the population ages, the number of elderly living with chronic medical conditions increases and pension levels continue to deteriorate, demand for social services is likely to increase significantly.

Labour market policies are underdeveloped, especially for women

Kyrgyzstan’s labour system was transformed by the collapse of the Soviet Union and the transition to a market-based economy. With the end of the command economy, the GoK was no longer responsible for the provision or allocation of labour. At the same time, the economic contraction that followed the end of the Soviet Union and the demise of many large-scale enterprises sparked massive unemployment.

As with its social assistance programmes, Kyrgyzstan’s labour market policies were introduced in response to high demand but in a context of severe fiscal constraints that have limited their growth. While labour market conditions have eased in the subsequent two decades, there remains a clear need for such programmes: unemployment remains relatively high, labour market participation among women has declined and productivity levels across the economy are low. Labour market conditions are a key driver of migration, both internal and external.

Despite this need, labour market policies are a very small component of social protection provision in terms of both coverage and expenditure. They are also poorly aligned with other social protection programmes, despite oversight by the same ministry. This is partly a function of the fact that the current labour market strategy – the Programme for Promoting Employment and Regulating Internal and External labour Migration until 2020 – was drawn up when the labour portfolio was under the Ministry of Labour, Migration and Youth (MoLMY), (GoK, 2014[24]).

Public Employment Services

Public Employment Services (PES) are the gateway for labour market policies. PES date back to Soviet times, when they allocated labour across the economy. From 1991, their mandate changed to matching labour supply and demand, and helping unemployed workers – often the victims of mass lay-offs by a state enterprise – find work. PES functions include registering unemployed workers, matching employers to jobseekers, and referring unemployed workers to active labour market policy instruments, such as training, micro-credit agencies or public works programmes.

The vacancy registration service attempts to simplify the process of vacancy notifications, provide recruitment assistance, systematise communications between PES and employers, and facilitate job searches. However, there is a mismatch between the supply of vacancies registered at PES – mostly low-paid jobs in the public sector – and the employment demanded by jobseekers. Registered vacancies are mostly in urban areas, leaving rural areas (where informal employment is the norm) underserved by PES (Schwegler-Rohmeis, Mummert and Jarck, 2013[25]). Only 15% of all jobseekers found work through PES in 2010; personal referrals by friends and relatives are a much more common means (Schwegler-Rohmeis, Mummert and Jarck, 2013[25]).

PES provide free training for registered unemployed individuals across all regions, but training mostly takes place in urban areas. It is also apparent that the MoLSD lacks adequate information regarding national labour market trends (GoK, 2014[24]). Participants receive a stipend of 1.2 times (120%) the unemployment benefits. Training is implemented through public providers or in partnership with private institutions. Between 2009 and 2011, 8 000 to 8 600 participants per year received training. In 2014, participants comprised 24% (8 352 participants) of the 34 800 beneficiaries of the active labour market policies.

PES also directs the registered unemployed towards the ministerial micro-credit agencies. Ala-Too Finance, an agency overseen by the MoLSD, assesses eligibility and processes the application (Schwegler-Rohmeis, Mummert and Jarck, 2013[25]). In 2014, 4% of all active labour market policy beneficiaries participated in the micro-credit programme, nearly half of whom were women (Schwegler-Rohmeis, Mummert and Jarck, 2013[25]).

In 2016-17, the World Food Programme (WFP) implemented large-scale pilots in two parts of Kyrgyzstan (Kochkor and Bazar-Korgon) to identify options for expanding active labour market policies. The pilots were undertaken for more than 8 000 households in collaboration with MoLSD, the Ministry of Agriculture, Ministry of Finance, Ministry of Emergency Situations, State Agency on Environmental protection and Forestry, State Agency on Local Self-Government, State Material Reserve and WFP.

One aspect of the pilots seeks to extend the state system of short-term agricultural training to residents of rural areas who would ordinarily not be able to attend vocation training courses that are currently on offer. Some 70 training courses (designed in collaboration with the MoES, the Agency on Vocational Education and Kyrgyz National Agrarian University) will be available, chosen according to local demand. The focus of these courses, which will be overseen by the Ministry of Agriculture, is on improving yields and reducing crop losses.

Public works programmes

PES also serve as an entry point for public works programmes, which are by far the largest active labour market policy in terms of coverage and expenditure. However, provision is carried out at the local level, without an overarching national policy framework. Participants in public works programmes are not linked to other social protection instruments once they exit a programme.

Participation in public works programmes is open to all registered unemployed. However, priority is given to those registered with the authorised government agencies for more than six months, who have more than three dependents under age 16 and/or are not receiving unemployment benefits. Jobseekers cannot be compelled to participate. The majority of enrolled individuals are men.

Public works programmes provide temporary employment for approximately 23 000 to 26 000 participants per year. Average monthly wages in 2011 were KGS 750. In 2014, some 24 000 individuals were enrolled in public works programmes, representing 26% of those registered with the employment service or 12% of the total unemployed population. Such programmes accounted for 72% of all beneficiaries of the three main active labour market policies.

Public works programmes are managed by local state administrations, in collaboration with local enterprises and authorised government agencies. Temporary, low-skill employment on social infrastructure improvement projects in the region is provided on an ad hoc and contractual basis. Enrolment takes into account workers’ health, age, professional and other individual characteristics. Individuals may terminate the fixed-term employment contract before it expires if they obtain other work.

Remuneration must exceed 50% of the unemployment benefits but cannot exceed four times that amount. Remuneration includes a base wage from the employer and co-payment from the authorised government agencies’ funds, according to a procedure established by the GoK. Participants are covered by standard labour and social insurance laws and regulations.

Despite receiving the largest share of funding among active labour market policies, the annual per beneficiary spending in 2011 was much less (USD 39) than that for the micro-credit and training schemes (USD 102 and USD 88, respectively).

Unemployment benefits

A very small proportion of the unemployed population receives unemployment benefits. In the first instance, unemployed workers must have contributed to the Social Fund for at least 12 months during the last three years to be eligible. Moreover, they can only access unemployment benefits once they have passed through other labour-market programmes. As a result, Kyrgyzstan ranks 24th out of 27 Eastern European and Central Asian countries in the proportion of unemployed individuals receiving unemployment benefits (Kuddo, 2011[26]).

The basic unemployment benefit is KGS 250 (USD 3.90) per month to a maximum of KGS 500 or 10% of the subsistence minimum. Individuals can receive the benefit for a maximum of six calendar months in a year but for no more than 12 months over a period of three years. The low level of benefits and the eligibility requirements combine to constrain both demand for and access to unemployment benefits. There were just 463 beneficiaries in 2015.

Health care reforms have improved coverage and efficiency but quality and access lag behind

The health sector has undergone three major reforms since the collapse of the USSR, and the system now bears little resemblance to the system in place prior to 1992. These reforms included the Manas (1996-2005), the Manas Taalimi (2006-10) and the Den Sooluk (2012-16) programmes, whose main goal is to curb unofficial, private payments through official co-transfers in order to reduce the financial burden on patients and improve the system’s efficiency and responsiveness (MoH, 2012[27]).

Specific measures within these broader processes included the introduction of a Mandatory Health Insurance (MHI) contribution and the Mandatory Health Insurance Fund (MHIF) in 1997, as a first step in moving from subsidising the supply of health care to subsidising strategic purchasing of health services (Falkingham, Akkazieva and Baschieri, 2010[28]).3 In 2001, a single-payer system was introduced, pooling transfers from the government budgets and MHI contributions under the MHIF. This move consolidated financing for the health services and pharmaceuticals delivered by health care institutions.

Also in 2001, a State Guaranteed Benefits Package (SGBP) clarifying entitlements and co-payments for health services was introduced. The co-payments currently apply for in-patient services and for certain laboratory and diagnostic tests. With the introduction of the SGBP and co-payments, an exemption mechanism was also established. This exemption mechanism has gradually been expanded to cover 16 categories related to medical conditions (such as HIV, TB or maternal care) and 30 socially vulnerable groups. The latter includes children under the age of five or individuals older than 70, households in possession of a social passport, recipients of state benefits and beneficiaries of compensations for privileges.

Health protection in Kyrgyzstan thus includes three kinds of insurance:

-

The SGBP, which entitles all patients to primary health care services free at the point of service regardless of their insurance status and also defines the exemptions from co-payments.

-

The MHI programme, maintained under the MHIF, which covers certain co-payments for contributing members.

-

Voluntary health insurance.

The Mandatory Health Insurance Fund (MHIF)

The MHIF manages two programmes with revenues transferred from MHI premiums and government budgets: the SGBP and the Additional Drug Package (ADP) for the insured population.

The MHIF has several tasks:

-

Ensure the financial sustainability of the Basic State Health Insurance and MHI system, as well as create conditions for levelling the volume and quality of care to achieve fair and equitable access to preventive, medical and pharmaceutical services.

-

Accumulate funds to ensure financial sustainability of the single-payer and health insurance systems.

-

Supervise the rational and targeted use of single-payer system funds.

-

Create equal conditions of payment for medical services to health care organisations, public or private, under the SGBP from single-payer system funds.

-

Improve the quality of preventive, medical and pharmaceutical services delivered by providers in the health sector.

State Guaranteed Benefits Package

The SGBP has two components:

-

A universal package of services provided to the entire population (Basic Mandatory Health Insurance)

-

An additional package of services for individuals covered by the social health insurance system (Additional Mandatory Health Insurance) that includes co-payments for selected health services.

The SGBP provides the following types of health services:

-

primary health care

-

outpatient emergency care

-

emergency consultation services (air ambulance)

-

specialised outpatient health care

-

inpatient health care

-

health services financed by the high-tech medical care fund

-

dental care

-

medicines and vaccines

-

immunisation

Primary health care facilities that include family group practices (FGPs)4 or Feldsher-Obstetrical Ambulatory Points (FAPs)5 provide free health services to all individuals assigned to them. Patients needing specialised care are referred to specialists in family medicine centres (FMCs), operating as outpatient diagnostic departments of hospitals.6 The provision of laboratory testing and medical advice is free under the SGBP.

Additional Drug Package

The ADP provides subsidised drugs through its network of pharmacies, meeting two notable targets:

-

provision of medicines for individuals insured under the Additional Mandatory Health Insurance programme, implemented since 2000;

-

provision of medicines for the privileged category of patients under the SGBP programme, implemented since 2006: patients with bronchial asthma, epilepsy, paranoid schizophrenia, affective disorders and oncologic patients (GoK, 2012).

The ADP guarantees discounts on the purchase of medicines for a certain list of active ingredients. The ADP list of medicine is largely based on the Essential Medicine List. This list of medicine covered under ADP is updated regularly and new medicines have been added to the list over time. For example, medicines for mental conditions were recently added after successful campaigning by some non-governmental organisations.

Young people, migrants and the urban poor fall between the gaps in social protection coverage

Kyrgyzstan’s social protection system covers a wide range of risks and receives a significant proportion of government spending (discussed in Chapter 4). However, it has evolved in an uncoordinated manner, and the allocation of resources between these different risks is very uneven. As a result, the impact and coherence of the system is limited (discussed in Chapters 3 and 5, respectively).

Two groups are at greatest risk of exclusion from the social protection system: young people and migrants working abroad. Young people’s best chance for employment lies in the informal sector, but this diminishes the likelihood of coverage by the social insurance system. Moreover, the youth unemployment rate is higher than that of the overall economy but labour market policies are not implemented at sufficient scale to help large numbers of youth into formal employment.

Labour migrants are unable to contribute to the Kyrgyz social protection system and are at great risk of poverty should they lose their jobs abroad, where they are unlikely to be protected by public social protection policies. Moreover, they will not be able to fall back on informal social protection networks without returning to households in Kyrgyzstan for which they might have been the main breadwinner.

In addition to the gaps between programmes, there are also major gaps within them. The urban poor, for example, are largely excluded from the MBPF by the targeting criteria, even though the disparities between rural and income poverty have reduced considerably in recent years. The MBPF also has a relatively narrow focus on income poverty rather than multidimensional deprivation; the two do not always coincide.

Labour-market policies cover only a small proportion of the unemployed population and are thus ineffective in addressing the mismatch between the supply of labour and demand, particularly from the formal sector. This is further undermining the sustainability of the social insurance system and will adversely affect the retirement outcomes of today’s workers. While pension coverage is high for existing elderly populations, today’s labour force is less likely than older generations to contribute to the Social Fund, and those who do might not be contributing the full amount. As a consequence, the current generation of workers is likely to receive much lower pensions than today’s pensioners – a likelihood reinforced by the failure of the pension system to protect the value of workers’ contributions.

Labour market policies for women need to be significantly improved. Chapter 1 showed that young women are the most likely not to be in education, employment or training, teenage pregnancy is one the rise, and overall labour force participation rates for women are low. Elevated school enrolment rates for girls are not translating into good labour market outcomes, and what little assistance exists to get women into the labour force operates on a very low scale. Public works programmes are the main labour market policy but are overwhelmingly accessed by men and do not have a clear social protection rationale.

References

[3] ADB (2013), Social Protection Index, Asian Development Bank, Manila, http://hdl.handle.net/11540/79.

[20] ADB (2011), Civil Society Briefs: The Kyrgyz Republic, Kyrgyz Republic Resident Mission, Asian Development Bank.

[16] ADB/IMF/World Bank (2010), The Kyrgyz Republic Joint Economic Assessment: Reconciliation, Recovery and Reconstruction, Asian Development Bank, International Monetary Fund, World Bank, http://imf.org/external/np/pp/eng/2010/072110.pdf.

[5] Andrews, E. et al. (2006), Pension reform and the development of pension systems : an evaluation of World Bank assistance, World Bank, Washington DC, http://documents.worldbank.org/curated/en/629861468166150111/Pension-reform-and-the-development-of-pension-systems-an-evaluation-of-World-Bank-assistance.

[14] CASE/MoLSD/UNICEF (2008), Effectiveness of Benefits to Families and Children in the Kyrgyz Republic, Center for Social and Economic Research (CASE), Ministry of Labor and Social Development of the Kyrgyz Republic (MoLSD), United Nations Children's Fund (UNICEF), https://www.unicef.org/kyrgyzstan/sites/unicef.org.kyrgyzstan/files/2018-02/Effectiveness_Benefits_Families_Children_Eng.pdf.

[28] Falkingham, J., B. Akkazieva and A. Baschieri (2010), “Trends in out-of-pocket payments for health care in Kyrgyzstan, 2001–2007”, Health Policy Plan, Vol. 25/5, pp. 427-436.

[19] GIZ (2012), Исследование для изучения возможностей системы государственного управления, образования для создания системы повышения квалификации, переподготовки специалистов социальной защиты [Study to study the possibilities of the system of public administration, education to create a system of professional development, retraining of specialists in social protection], Healthcare in Central Asia regional program, German Development Organisation - Deutsche Gesellschaft für Internationale Zusammenarbeit (GiZ).

[24] GoK (2014), Programme for Promoting Employment and Regulating Internal and External labour Migration until 2020, Government of Kyrgyzstan, Bishkek, http://cbd.minjust.gov.kg/act/view/ru-ru/94692?cl=ru-ru.

[18] GoK (2011), Government Resolution No. 451 of August 5, 2011 On approval of model structure and staffing level of the executive body of local self-government of the Kyrgyz Republic.

[6] GoK (2004), Law of the Kyrgyz Republic of 02 August, 2004 No. 103 About Social fund of the Kyrgyz Republic.

[13] GoK (1993), Law of the Kyrgyz Republic of 07 May, 1993, No. 1194-XII On provision of pensions for military personnel.

[21] Ismayilova, L. and A. Huseynli (2014), “Reforming child institutional care in the Post-Soviet bloc: The potential role of family-based empowerment strategies”, Children and Youth Services Review, Vol. 47, pp. 136-148, https://doi.org/10.1016/J.CHILDYOUTH.2014.09.007.

[26] Kuddo, A. (2011), Unemployment Registration and Benefits in ECA Countries, World Bank, Washington DC.

[27] MoH (2012), Den Sooluk National Health Reform Program in the Kyrgyz Republic for 2012-2016, Ministry of Health, Government of Kyrgyzstan.

[17] Mukanova, K. (2007), Local self government in Kyrgyzstan—myth or reality?, http://nispa.org/conf_paper_detail.php?cid=16&p=1154&pid=7003.

[11] Müller, K. (2005), “Post-Socialist Pension Reform: Contributory and Non-Contributory Approaches”, Public Finance & Management , Vol. 5/2, pp. 290-309.

[29] NSC (2017), National Statistics Committee of the Kyrgyz Republic.

[15] NSC (2015), Kyrgyz Integrated Household Survey, National Statistics Committee of the Kyrgyz Republic, Bishkek.

[9] Schwarz, A. et al. (2014), The Inverting Pyramid: Pension Systems Facing Demographic Challenges in Europe and Central Asia, World Bank Group, Washington DC, http://documents.worldbank.org/curated/en/514831468029365694/Main-report.

[25] Schwegler-Rohmeis, W., A. Mummert and K. Jarck (2013), Labour Market and Employment Policy in the Kyrgyz Republic: Identifying constraints and options for employment development, Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH, Eschborn/Bishkek.

[8] Social Fund of the Kyrgyz Republic (2018), Social Fund of the Kyrgyz Republic, http://socfond.kg/ (accessed on 01 May 2017).

[22] Tobis, D. (2000), “Moving from residential institutions to community-based social services in Central and Eastern Europe and the former Soviet Union”, A World Free of Poverty series, World Bank, Washington DC.

[23] UNICEF (2014), TransMonEE: Transformative Monitoring for Enhanced Equity, http://transmonee.org/wp-content/uploads/2016/07/TM_2014_brochure_v1.pdf (accessed on 09 May 2017).

[4] Wooden, A. (2014), “Kyrgyzstan's dark ages: framing and the 2010 hydroelectric revolution”, Central Asian Survey , Vol. 33/4, pp. 463-481, https://doi.org/10.1080/02634937.2014.989755.

[12] World Bank (2014), “Kyrgyz Republic Public Expenditure Review Policy Notes: Pensions”, in Public Expenditure Review Report No. 89007, World Bank, Washington DC.

[7] World Bank (2014), “Kyrgyz Republic Public Expenditure Review Policy Notes: Social Assistance”, in Public Expenditure Review Report No. 89022, World Bank, Washington DC.

[10] World Bank (2012), The First Wave of NDC Reforms: The Experiences of Italy, Latvia, Poland, and Sweden Nonfinancial Defined Contribution Pension Schemes in a Changing Pension World, World Bank, Washington DC.

[2] World Bank (2000), Kyrgyz Republic - Fiscal sustainability study, World Bank, Washington DC.

[1] World Bank (1993), Kyrgyzstan - Social protection in a reforming economy, World Bank, Washington DC.

Notes

← 1. Benefits for merit groups are outlined in Annex 2.A.

← 2. The imputed rate is a value used to calculate different benefits, fees, fines, etc., which are usually set as multiples of this rate. Originally, this was a minimum monthly wage but subsequently became a separate value. In 2015, the imputed rate was KGS 100.

← 3. The MHIF, located in Bishkek, is responsible for the collection of contributions for the Additional Mandatory Health Insurance programme (through the Social Fund) and is the sole purchasing agency for health services within the Kyrgyz health care system.

← 4. FGPs are the main providers of primary health services.

← 5. FAPs provide the most basic services, such as prenatal and postnatal care, immunisations and health education.

← 6. FMCs are the largest outpatient health care providers in the country.