Chapter 4. Tax and skills statistics: Effective tax rates and returns to costs ratios1

This chapter presents the main results for the indicators surrounding the financial incentives to invest in skills discussed in this tax policy study. The key indicators are the Breakeven Earnings Increment (BEI), the Marginal Effective Tax Rate on Skills (METR), the Average Effective Tax Rate on Skills (AETR), the Marginal Returns to Costs Ratio for Governments (MRCR), and the Average Returns to Costs Ratio for Governments (ARCR). The chapter presents results for four stylised education, scenarios: a 17-year-old student undertaking a four-year degree, a 27 year-old undertaking a one-year degree, a 32-year old undertaking a short course of job-related training, and a 50-year old undertaking a one-year degree. The chapter also examines the impact of the form of financing of education on indicator outcomes, as well as the way the results vary by gender.

4.1. Introduction

This chapter presents the main results for the indicators surrounding the financial incentives to invest in skills discussed in this tax policy study. The key indicators are the Breakeven Earnings Increment (BEI), the Marginal Effective Tax Rate on Skills (METR), the Average Effective Tax Rate on Skills (AETR), the Marginal Returns to Costs Ratio for Governments (MRCR), and the Average Returns to Costs Ratio for Governments (ARCR). The methodology outlined in Chapter 3 is flexible; it allows for these indicators to be developed using a wide variety of assumptions about the length, nature, and cost of a given skills investment. It also allows for considerable variation with respect to the student; the income, family status, age, lost earnings, and future earnings potential of a student can all be varied. Finally, the model allows for flexibility with respect to the extent of education subsidies available; the government can pay for more or less of the direct costs of education, and it can subsidise the student with scholarship income, by writing down loan principals, by allowing students to borrow at reduced interest rates, and by using skills tax expenditures (STEs) to offset educational costs.

In this chapter results are presented for four stylised “types” of person engaged in upskilling, though the chapter also shows how these results vary by income, age, and taxes considered. The stylised cases are:

-

Tertiary Education: A 17-year-old student, single and childless, who could earn 70% of the average wage in the labour market, but instead undertakes a four-year basic undergraduate degree. During this time, the student earns 25% of the Average Wage in part-time work. This is discussed in Sections 4.2 and 4.3.

-

Graduate Education: A 27-year-old worker, single and childless, who could earn the Average Wage in the labour market, but instead undertakes a one-year graduate degree. During education the student earns 25% of their previous wage in part-time work. This is discussed in Section 4.4.

-

Job-Related In-Work Training: A 32-year-old worker, single and childless, who earns 100% of the Average Wage, and undertakes a short course of job-related training. During education the worker’s earnings fall to 95% of their previous wage, though they earn their previous wage for the rest of the year. This is discussed in Section 4.5.

-

Life-long Learning: A 50-year-old worker, single and childless, who could earn 100% of the Average Wage, but instead undertakes a one-year retraining program unrelated to their current job. During education the worker earns 25% of their previous wage in part-time work. This is discussed in Section 4.6.

For university students, the manner in which education is financed is allowed to vary. In some countries, tertiary is financed primarily by governments, while in some countries the student finances most of their tertiary education. A student can finance their education with retained earnings, debt, or a combination of the two. This is discussed in Section 4.3.

In addition, Section 4.7 examines the way in which differing expected wages for men and women in the labour market in OECD countries can affect incentives to invest in skills for individual men and women. The discussion will also examine how the gender wage gap affects expected returns for governments.

The results in this study incorporate personal income taxes (PIT) only, not social security contributions (SSCs). This means that in countries where SSCs form a large part of the labour tax wedge, the results presented in this study may differ from those that would result from incorporating both PIT and SSCs. SSCs may raise the tax rate on foregone earnings, increasing the extent to which the tax system subsidises skills investment and reducing the tax burden on skills, while at the same time raising the tax rate on earnings increments, thus raising the tax burden on skills. Thus adding SSCs to the analysis may raise or reduce the overall burden on skills investments.

The results in some countries may be particularly sensitive to the inclusion of SSCs due to the fact that in some instances there are ceilings above which an extra dollar of income may not be liable for future SSCs. This may mean that SSCs may be a component of the tax rate on foregone earnings, but not of the tax rate on the earnings increment. In these cases, accounting for SSCs may reduce the tax burden on skills substantially.

In other cases however, the SSC burden may rise with income; SSC schedules may be progressive. In these cases, accounting for SSCs will raise the tax rate on the earnings increment by more than the tax rate on foregone earnings is reduced. In these cases, the overall tax rate on skills may be higher where SSCs are taken into account.

It is also important to account for the ways in which the SSC system interacts with the PIT system. In many countries, SSCs are deductible from the PIT base. In this study the results presented factor in the impact of these deductions from the PIT system. Thus while SSCs are not taken into account in the results presented here, the study does account for their impact on the PIT system. This approach follows that taken in Taxing Wages (OECD, 2016).

Finally, it is important to account for certain skills tax expenditures that may be provided through the SSC system. For example, in certain cases student income may be subject to a reduced SSC burden relative to other forms of income. These kinds of skills tax expenditures through the SSC system are discussed further in Chapter 5.

4.2. Tertiary education

The tertiary education case examines a 17-year old person undertaking a four-year course of study. Tertiary education students receive an average level of government scholarship income and pay an average amount of direct costs.2 Their earnings during education are set at 25% of the Average Wage in any given country: that is, students are assumed to earn some part-time employment income, but at a comparatively low level.

Importantly, it is assumed that the student receives no financial support from parents towards their education costs, nor do the parents receive subsidies through the tax system for supporting their child through university. This strong assumption is made on tractability grounds. Aside from government support, the student is assumed to be independent from their parents when it comes to financing the course of study.

As discussed in Chapter 3, a variety of assumptions about how the students finance their education are examined. In this section it is assumed that students finance their education with savings. In Section 4.3, it is assumed that the student finances their education with a student loan. The amounts borrowed by the student as well as the interest rate at which they can borrow are both varied in the analysis.

Government support in OECD countries for tertiary education is usually significant; per-annum scholarship spending per student is on average USD 1 606 among the countries examined in this study.3 In many OECD countries the student’s scholarship or grant income is tax-free, which is a subsidy for tertiary education through the tax system. Direct costs of tertiary education are usually not tax deductible. In addition in some countries (notably Belgium and the Slovak Republic) students’ wage income is taxed at a lower rate than standard wage income.

It is important to note that the model is unrepresentative of tertiary education in many ways. Many students receive significant support from their parents; this support is often subsidised through the tax system many countries also allow tax deductibility of the costs of supporting a child; the model does not capture these provisions. This means that it is likely that the METRs in the model are higher than their true value.

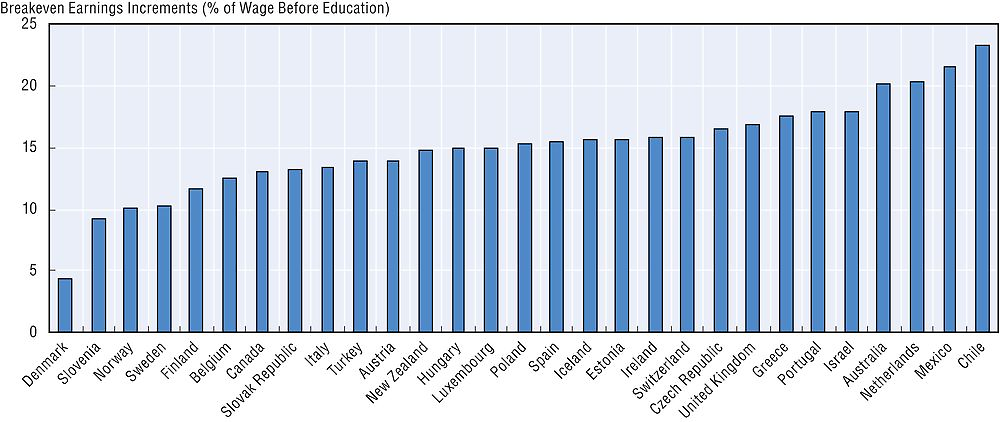

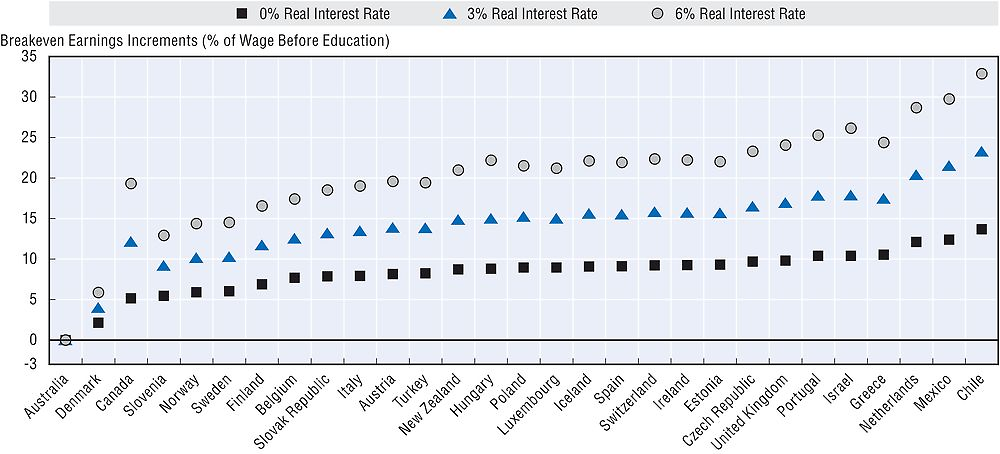

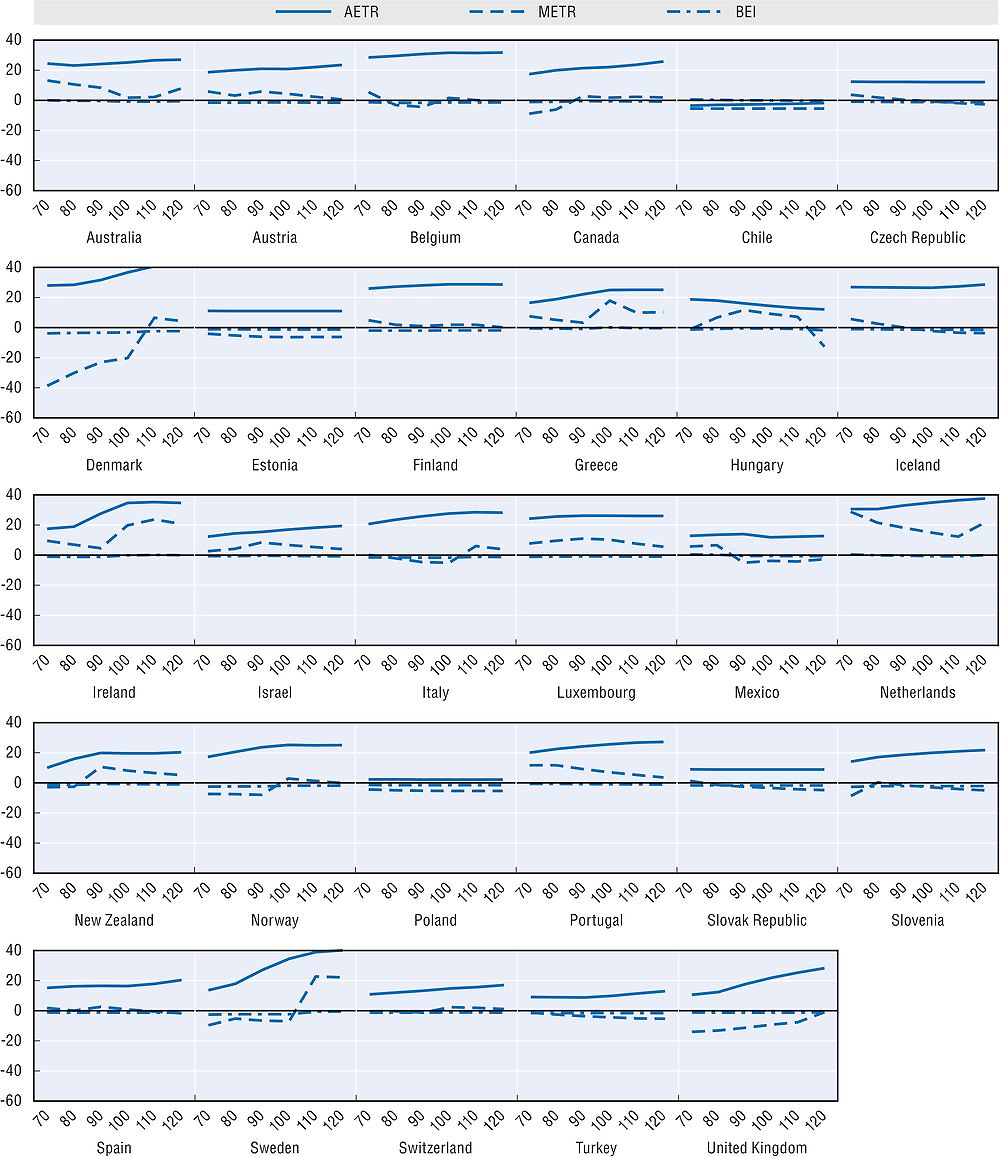

The BEI is highest for a 17-year-old completing a four-year degree than it is for any other case examined in detail in this study. This is largely due to the long duration of tertiary education for students. Foregone earnings are larger in the case of a four-year degree than in other shorter cases examined. Figure 4.1 shows that the BEI expressed as a percentage of the previous wage in this case ranges from 4.5% (Denmark) to 23.3% (Chile), with an un-weighted average among the countries in the sample of 15%.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate skills tax expenditures that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

In spite of these comparatively high costs; tertiary education pays for itself in the model. Though the BEI in the model is highest for tertiary education compared to other forms of education; the extra earnings needed to break even on a typical tertiary education are below the levels of earnings available for university students in the labour market. These values range from 20% (Denmark) to 137% (Chile); with an un-weighted average among the countries in the sample of 45%. Figure 4.2 shows the size of the gaps between the BEI (at the bottom) and the labour market premium for tertiary education (at the top).

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate skills tax expenditures that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment. Labour market data are based on the tertiary education premium earned by 15-64-year-olds.

For some countries such as Slovenia and Chile, there are significant rewards to tertiary education in the labour market; the gap between what is necessary to break even on a skills investment and what is available on average is very large. This points to the possibility of skills shortages in these countries. It also raises questions about the performance of education markets in these countries; if skills investments are so lucrative and (as indicated by lower BEIs compared to available returns) so affordable, why are more students not undertaking them?

By contrast, many other countries – some that are known to have very high levels of third-level education in their labour forces – have relatively small gaps between available earnings and breakeven earnings. This suggests that these educational investments may not be profitable for some students given the current mixture of education costs, scholarship and grant levels, and tax rates.

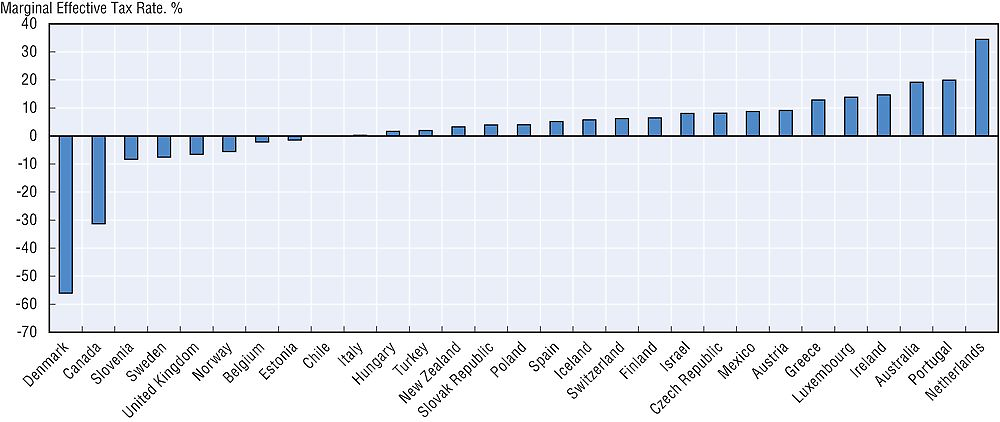

Overall, skills investments for marginal tertiary education students are taxed comparatively lightly. Figure 4.3 shows that for 17-year old tertiary education students whose outside employment opportunities are at 70% of the Average Wage, METRs range from -56% (Denmark) to 34.5% (Netherlands), with an average value in the sample of 2.9%. This means that, in the Danish case for example, that the tax system reduces the BEI by 56%, compared to what it would be in a world without taxes. These negative METRs mean that the tax system is increasing individuals’ incentives to invest in skills, compared to what these incentives would be if no taxes were levied.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

There are several reasons for these low METRs. First, the model assumes that the unskilled worker would earn a low wage, which lowers the cost of studying and, as it results in a relatively low BEI, means their extra earnings are modestly affected by the tax system. In some countries – notably Denmark – the amount of scholarship income is such that the student’s foregone earnings are almost entirely nullified by extra scholarship income received. Moreover, BEIs are also reduced by STEs that reduce taxation of scholarship income and student wage income.

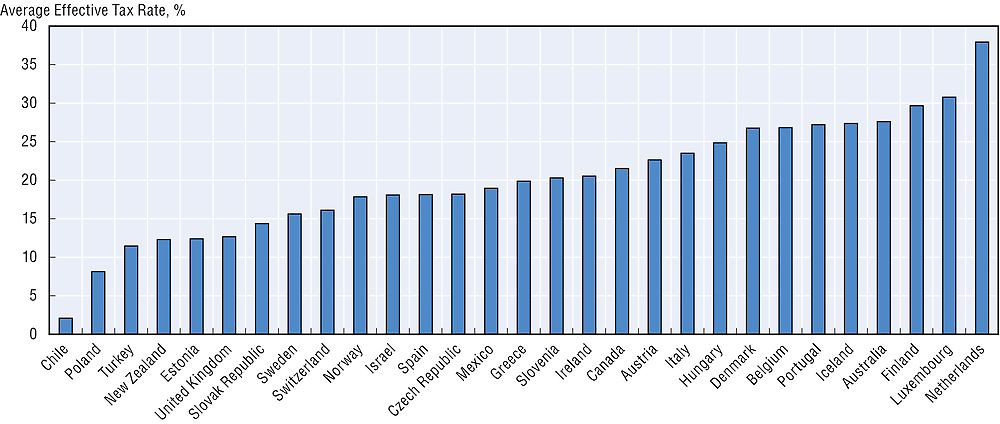

AETRs are higher than METRs as can be seen in Figure 4.4. Higher-than-breakeven earnings after education push taxpayers into higher brackets, decreasing their incentives to invest in skills. The AETRs are based on the assumption that students’ earnings after university increase by the average lifetime tertiary labour market premium. Under this assumption, these AETRs range from 2.1% (Chile) to 37.9% (Netherlands) with an un-weighted average of the countries in the sample of 19.8%. Note that AETRs tend to rise towards the statutory top PIT rates in a given country as the returns to skills investments rise. This is partly why the Netherlands has the highest AETR on tertiary education in the model; it has comparatively high PIT rates commencing at relatively low levels of income, and so has relatively high PIT progressivity. This is in contrast to Chile which has one of the lowest statutory PIT rates in the sample of countries, and so has one of the lowest AETRs.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

These tax rates yield significant returns to the government in the form of tax revenue. Figure 4.5 shows the ARCR of government investment in education. Recall from Section 3.7 that ARCRs measure the ratio of government returns to education (extra tax revenue) to the costs of education (lost tax revenue, direct costs, and scholarship or grant income given to a student and value of skills tax expenditures). It should be noted that only the returns to education in the form of extra income taxes are considered; the model does not incorporate estimates of the broader returns to education such as higher employment, faster growth, or increased productivity. The estimates of the returns to education are almost certainly lower in the model than the true estimates, as only income taxes are considered.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment. Due to data limitations, results for Mexico are omitted. Labour market data are based on the tertiary education premium earned by 15-64-year-olds.

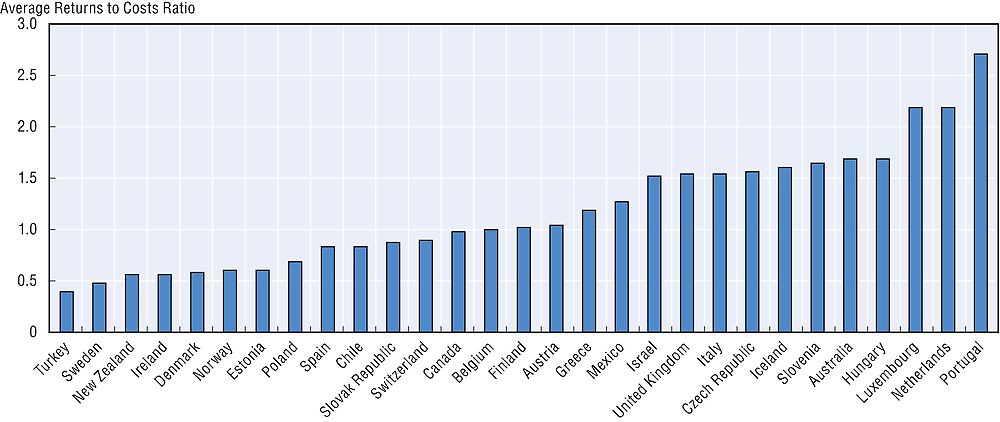

Based on the existing labour market, tax and expenditure data, the ARCR is on average larger than 1 in the OECD. This could suggest that extra investment in education would yield positive returns for governments in the OECD in terms of income tax revenue. The average value of the ARCR in the sample is 1.2, where an ARCR of 1 would be the level at which the present value of the stream of returns was equal to that of the costs.

For some countries, such as the Netherlands and Portugal, the returns to education are more than double the costs. This is driven by comparatively low spending, both on scholarships and directly to universities in these countries, coupled with a comparatively high labour market premium for tertiary education. The results also suggest that for some countries the share of the costs borne by the government in education is comparatively high. For countries such as Ireland and New Zealand, a larger fraction of the costs of education are borne by governments than is recouped in costs.

In contrast to the results for ARCRs, MRCRs are significantly lower for most OECD countries. This is due to the gap between the BEI and the tertiary education premium available in the labour market, as shown in Figure 4.2. In the ARCR case, the student earns the premium in the labour market. For the MRCR, the student is assumed to earn just the break-even earnings level, which is substantially lower than the average wage earned by a tertiary graduate in most countries. These values can be considered to be the government’s returns to educating a student who just breaks even on a skills investment. As is the case with the ARCR, the returns are probably underestimated, as the analysis in this study only incorporates returns in the form of higher income taxes, and so does not include a broader set of financial or social returns.

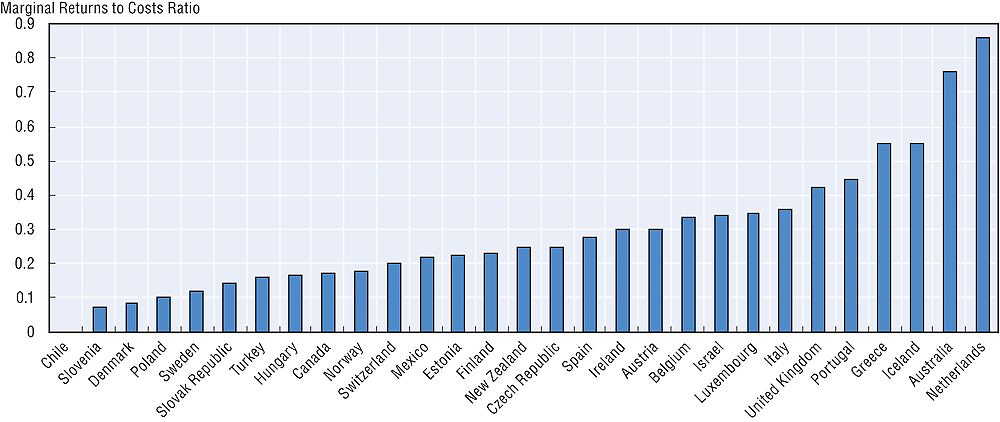

As is shown in Figure 4.6, MRCRs are usually below one in OECD countries. The highest value is in the Netherlands at 0.85, while the lowest is Chile with a MRCR of 0. This reflects the high PIT thresholds in Chile; taxpayers who are just breaking even on a skills investment will not pass the threshold to begin to pay PIT in Chile, so the government’s returns on a skills investment will be zero. The mean value across the countries modelled is 0.198. This low value suggests that while skills investments more than make up their costs from the government’s perspective on average, for marginal students income tax revenues do not cover the governments costs in income tax revenue; these costs may however be recouped in terms of lower social spending, higher revenues from other tax categories, and lower unemployment. However the results nonetheless suggest the government’s share of income taxes received from marginal students are lower than its share of the costs of skills investments.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

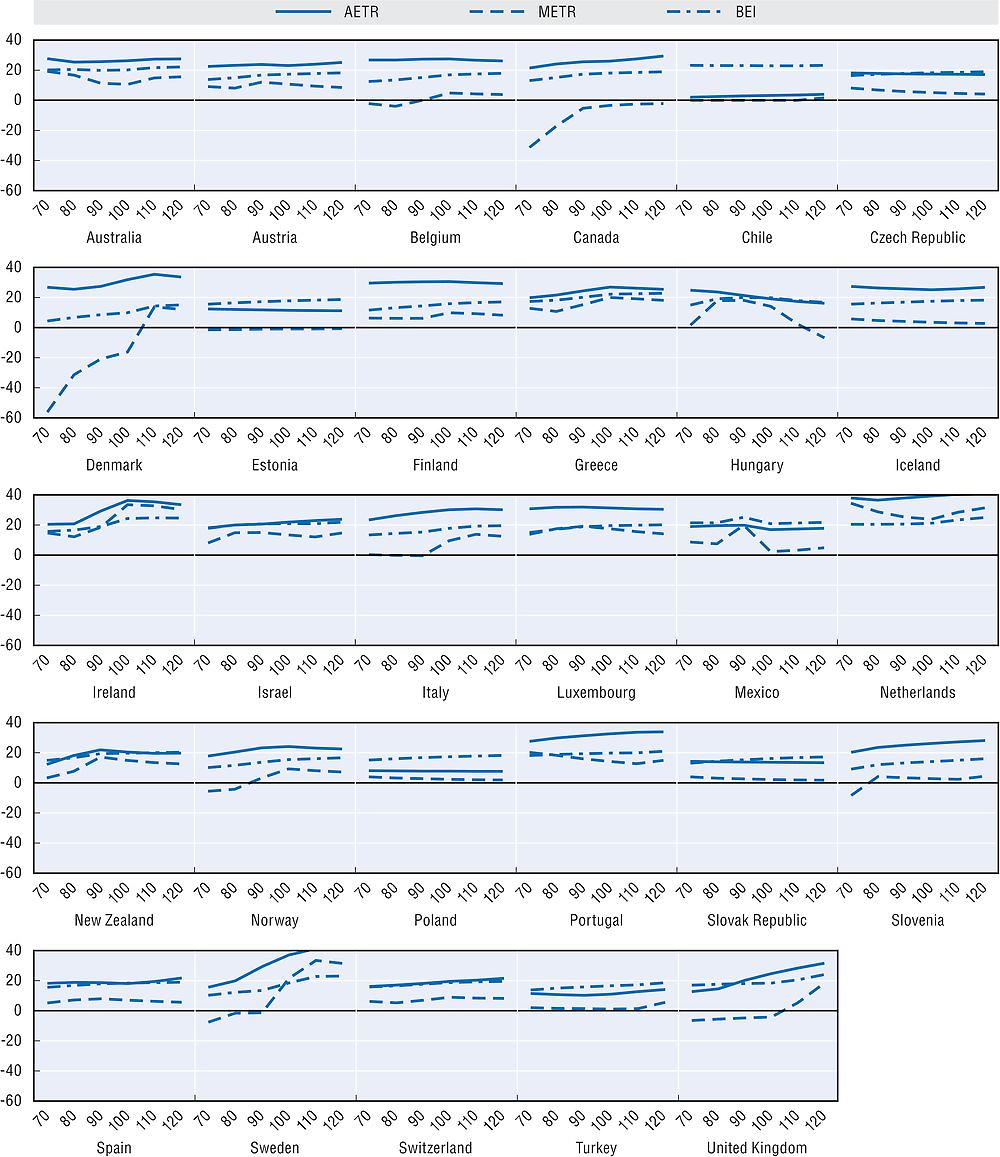

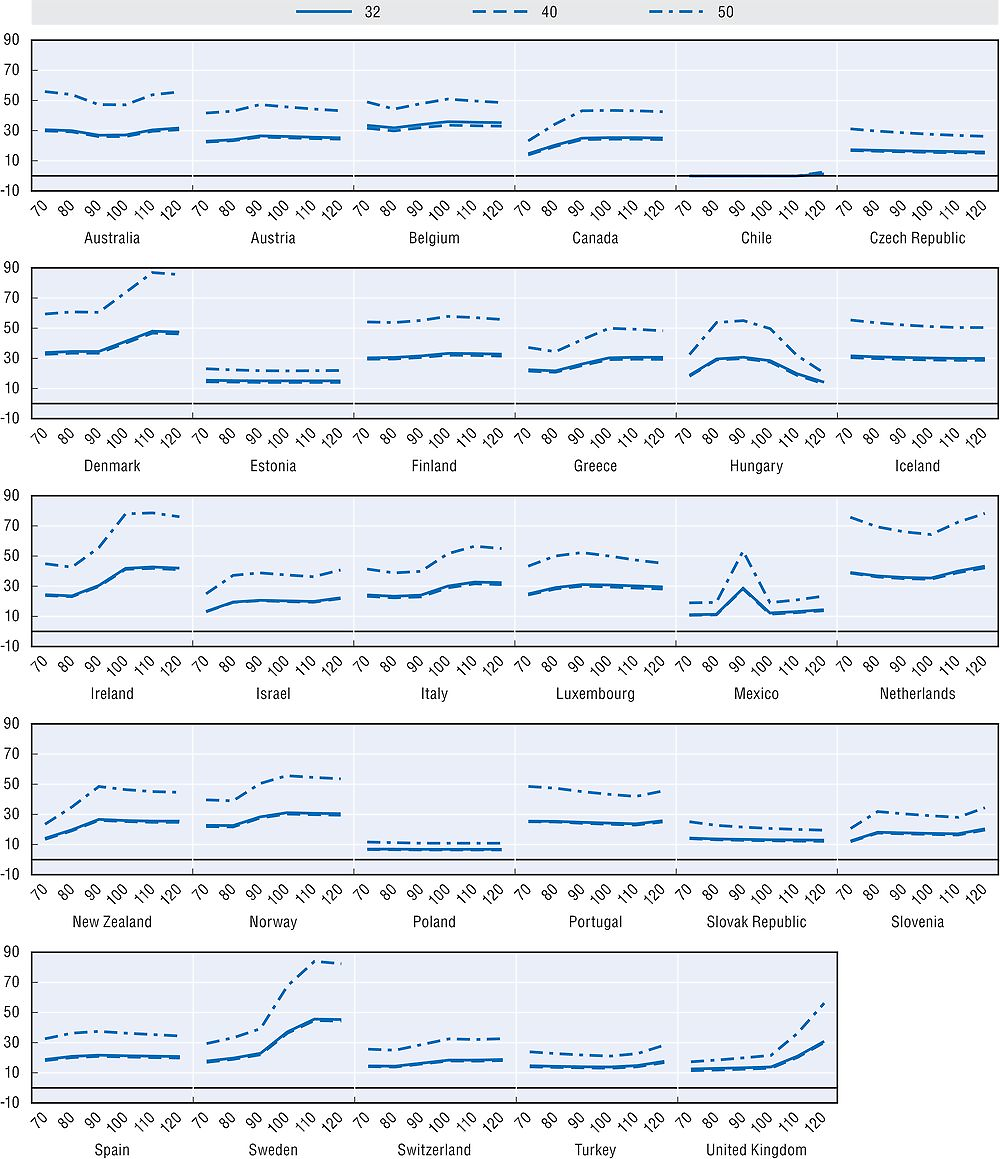

Figure 4.7 shows results when the assumption that students earn 70% of the average wage in the absence of upskilling is relaxed. In this figure, the income the student forgoes is allowed to vary, allowing the calculation of METRs and AETRs at various income levels. These results for tertiary education are either flat or increasing in income before education, though this is not the case for all countries, most notably Hungary. The results from Section 3.6 hold; AETRs are larger than METRs because returns are higher. Moreover, countries with progressive PIT schedules especially at lower levels of income tend to have more progressive AETRs. This is because of the rate at which the returns to skills investments are taxed away.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

Denmark and Sweden have sharply negative METRs at very low income levels; this is due to the provision of comparatively large amounts of tax-free scholarship and grant income in these countries. In these examples, not only is a significant amount of income provided to the student by the state; but this income is also tax-free. This means that an extra subsidy is being provided to the student through the tax system in addition to the benefit being provided to the student directly. Secondly, in some of these countries, the large amount of grant income can mean that the amount of foregone earnings can be low or even negative; the amount of scholarship and grant income the government provides is as much or even exceeds what a low-income student could earn in the labour market. In such cases the incentives to invest in skills become high indeed. This may lead to problems regarding tertiary completion in these countries as it becomes profitable for a student to stay in university.

4.3. Financing tertiary education

The previous section assumes that a student finances skills investments using savings. However, in reality most university students have little or no savings to call upon. Most students finance their education through their parents or through student debt. This section examines how the costs of this financing can affect students’ and workers’ financial incentives to invest in skills.

As discussed in Chapter 3, the model used in this tax policy study can account for a student financing all or part of their education using debt. Several aspects of this debt, including the amount, interest rate, repayment duration, and tax treatment of debt can be modelled. Due to data limitations, the results presented here do not take advantage of the full flexibility available in the model. Data on average rates of interest on student loans are not available, nor are data on average loan amounts. Hypothetical interest rates and loan amounts are used instead. These still offer suggestive results as to the importance of financing for the overall cost of investing in skills.

The base case is as outlined in Section 4.2: a 17-year old single childless student engaging in a four-year period of upskilling. The student has some direct costs, as does the government. These costs are set at average levels for each country. Students are also in receipt of scholarship income at the average level for the country concerned. Various debt-based provisions are incorporated concerning the treatment of student debt in OECD countries, such as the deductibility of interest payments and income contingent repayments of debt.

Throughout this section, borrowing levels and interest rates are varied uniformly across countries. More detailed data on the level of borrowing per student and the average interest rate pertaining to student loans are not available. A second reason as to why borrowing levels are varied uniformly is to increase comparability across countries. In spite of this, it should be noted that the results presented here, though they incorporate statutory provisions in individual countries concerning the tax treatment of student debt and the structure of repayments, are not representative of any particular country in terms of average debt levels or interest rates.

Figure 4.8 shows how these financing costs impact the overall costs of skills investments. In this figure it is assumed that the student can borrow at a nominal interest rate of 6%, which in the model corresponds to a real rate of 4%. Having to borrow to finance the cost of education raises the BEI substantially; the student must earn more to pay interest on student debt in addition to whatever other costs they must earn to break even on their skills investment.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. This figure does not incorporate interest deductibility of student loans in Finland.

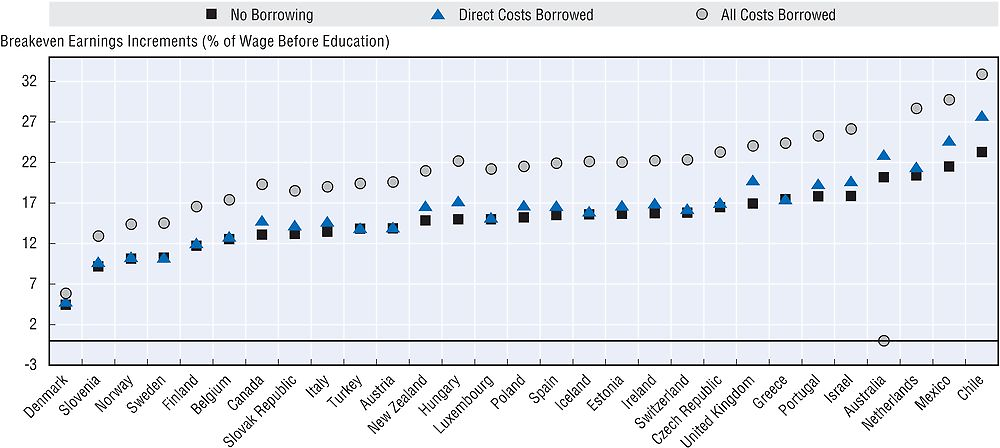

The black squares show the BEIs with no borrowing; these are the same BEIs as outlined in Figures 4.1 and 4.2. The blue triangles show BEIs when the student borrows just the direct costs of a skills investment. These costs are taken from Education at Glance (OECD, 2014): details are given in Box 3.1 in Chapter 3. These costs are roughly analogous to the student borrowing tuition fees to finance their education. BEIs rise most in these circumstances where private direct costs are high for students. This means that countries such as Chile have large gaps between black squares (BEIs with no borrowing) and blue triangles (BEIs where direct costs are borrowed). By contrast, in countries where direct costs for the individual student are modest, the amount of borrowing is modest too. In these cases the BEI does not rise much as the amount of debt incurred is low.

The circles in Figure 4.8 show the BEIs when students borrow not just these direct costs of their education, but rather the entirety of the costs: they borrow their after-tax foregone earnings as well. This can be thought of as analogous to a situation in which a student borrows not just to pay tuition fees but also to maintain their standard of living at a level that they would have had if they had worked instead of entering the workforce. The circles are substantially higher than the black squares in Figure 4.8, sometimes double in size. These BEIs can rise to up to 33% (Chile).

An exception to this pattern is the circle for Australia, which illustrates the effect of the Australian income contingent loan scheme.4 In the Australian case, students do not repay any part of their loan unless their earnings pass a certain threshold. In this modelling, a marginal student who earns 70% of the average wage in Australia will not pass the threshold to begin repaying their loans, and will so not need to pay back their loans. This is because an amount that is 70% of the average wage plus the BEI does not add up to enough to pass the threshold for repayment. This means that the costs of a skills investment is essentially zero, though these costs will rise if they move up the income distribution. It is important to note that in the case where Australian students borrow a lower fraction of the total cost of their education, they may still benefit as their loan principal will be written down, but as their borrowing will be low, they will not benefit as much they would if they had borrowed all of their costs. It should be noted that this modelling pertains to 2011; average wages, thresholds and other features of the policy may have changed in Australia.

These results illustrate several points. First, student debt, when the interest rate is sufficiently high, can act as a significant barrier to upskilling, in some cases nearly doubling the required earnings level at which a student can breakeven. Without knowing details on interest rates that students face in OECD countries it is not possible to determine the exact size of this barrier, however it is worth noting that the BEIs in this model are very sensitive to the amount borrowed.

A second point worth noting is that the impact of borrowing on the BEI is much larger when lost earnings are borrowed than when just direct costs are borrowed. This highlights the importance of the mix of education costs in determining the financial barriers to investing in skills. Some students receive support in kind for day-to-day living expenses from parents. This means that they do not have to borrow to finance their living expenses during periods of upskilling. In such cases the barriers to educational investment in terms of the returns that must be earned post-education are reduced substantially. The results highlight that the implications of these in-kind benefits should not be underestimated.

Figure 4.9 shows the impact of differing levels of borrowing on BEIs for university students. The difference in this figure compared to Figure 4.8 is the real interest rate faced by students. Many countries, such as Australia and the United Kingdom offer students low-interest rate loans. This example examines these kinds of provisions. In the results shown in Figure 4.9 the student can borrow at a 0% real interest rate. The results are instructive; where a student can borrow cheaply the BEIs falls by a significant margin. Again the difference is apparent with varying borrowing levels. Where direct costs for students are large, reduced interest rates even on direct costs alone reduce BEIs substantially. However, for most countries, having students borrow just the direct costs of their education at a reduced rate does not affect their costs of education to a large extent. It nonetheless does lower the BEI below the level of the BEI for a skills investment financed with savings.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. This figure does not incorporate interest deductibility of student loans in Finland.

Where the full costs of education are borrowed, Figure 4.9 shows that BEIs can fall dramatically. It is important to realise the impact of reduced borrowing rates on BEIs in the model. In the model developed in this study, a key component of the BEI is the opportunity cost of the funds directed towards a skills investment.5 Students who choose to spend savings on a skills investment must not only recoup back those savings, but they must also recoup whatever those savings would have earned had they been invested in some other non-skills investment. In the model used in this study, it is assumed that had the funds used for a skills investment been invested elsewhere, they would yield a 3% real return per year. This 3% is used to calculate the opportunity cost component of the BEI in these results.

The ability to borrow the costs of a skills investment changes these incentives substantially. Where a student can borrow at a real rate of interest that is below the real rate of return that they might earn an alternative investment, the BEI is reduced substantially. Due to the fact that the student can borrow at a rate lower than the rate of return on a risk-free bond, the availability of education finance acts as an extra subsidy for the student. Even where a student has sufficient savings to finance a skills investment, the student may have an incentive to borrow to finance the investment, and invest their savings to earn the opportunity return. The financial gain made will reduce the cost of the investment substantially. In these scenarios, indeed, a large gap between the after-tax opportunity return at the interest rate on student debt means that higher levels of borrowing reduce the BEI steadily: if an investment yields returns at a higher rate than the interest rate through which they are financed, more borrowing is preferable. These results emphasise the impacts of financing costs on the overall financial incentives to invest in skills. Figure 4.10 highlights these effects showing that as borrowing costs rise, the BEIs rise commensurately.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. This figure does not incorporate interest deductibility of student loans in Finland.

4.4. Graduate education

The graduate education model examines a 27-year old person undertaking a one-year course of study. As with the case of a university student, they are in receipt of an average level of government scholarship income and pay an average amount of direct costs.6

The calculations assume that a graduate student earns 25% of the wage they earned before commencing a one-year course of study. This is instead of earning 25% of the average wage, which was assumed in the case of the tertiary education results. This is a proxy for the idea that while a university student’s skills in the labour market will be lower, a graduate student may have developed some skills so that their earnings throughout their period of additional studies are likely to be a function of their earnings before they began their graduate education. In these examples, as in Section 4.2, it is assumed that education is financed with savings, not with debt.

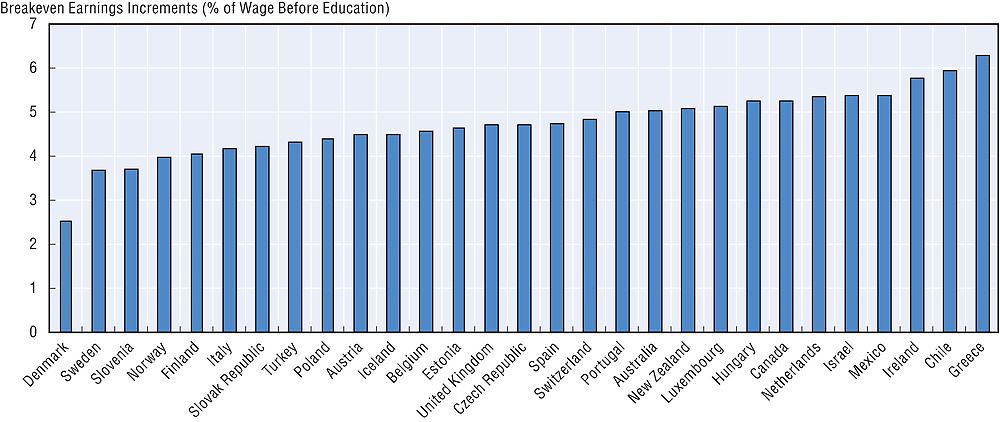

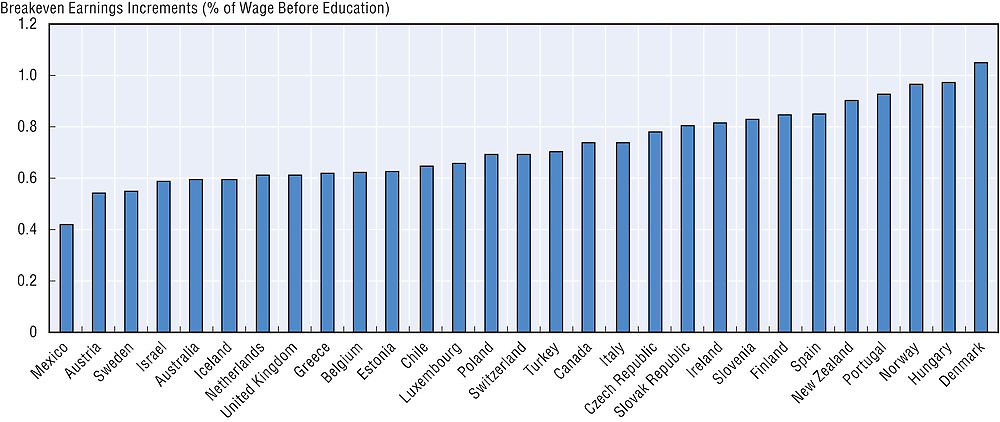

BEIs are lower in the model for graduate education than for tertiary education. This is largely because graduate education is shorter and so less costly for students. Direct costs are assumed to be the same on a per-year basis for graduate and undergraduate education. Undergraduate education is, however, assumed to be four years long while graduate education is only one year long, so the costs are commensurately higher. Figure 4.11 shows that BEIs range from 2.5% (Denmark) to 6.3% (Greece) with an un-weighted average in the sample of 4.7% (see Figure 4.11). Variation in these figures is driven in part by the amount of education spending in a given country and in part by the reduced taxation that comes with reduced earnings.

Note: Data are for a 27-year-old single taxpayer with no children, who undertakes a one-year course of non-job-related education, earning 25% of their wage before education during education. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system and the social security contribution system are incorporated. The results do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

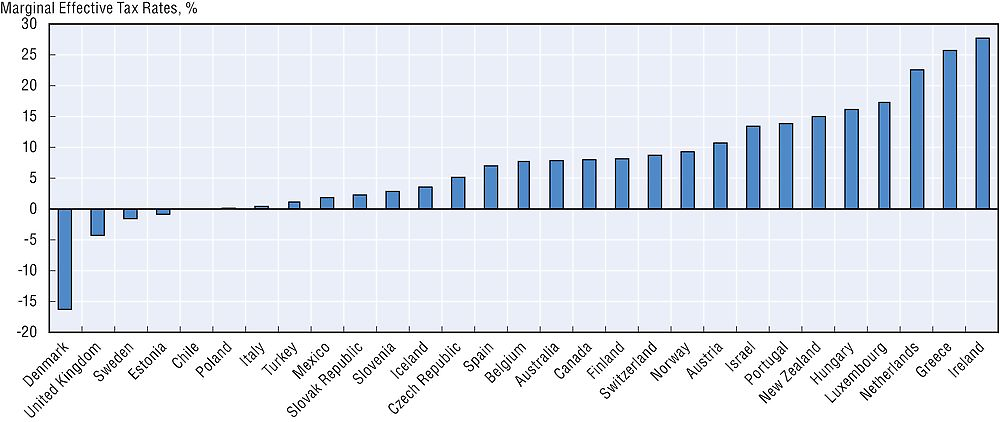

Despite these lower BEIs, METRs are often – though not always – higher in the model for graduate education than they are for tertiary education. They range from -16.2% (Denmark) to 27.7% (Ireland), with an un-weighted average of 7.6% (see Figure 4.12). These higher METRs result in large part from the impact of the tax rate on foregone earnings. The typical graduate student is assumed to earn the Average Wage if they do not enter education, whereas the typical university student is assumed to earn only 70% of the Average Wage. Tax progressivity means that the returns to skills investments are taxed away at a higher rate for the graduate student than they are for the typical university student, at least initially. Many of these METRs depend on the marginal tax rates on earned income over the middle of the income distribution; where these marginal rates are steepest, METRs are higher.

Note: Data are for a 27-year-old single taxpayer with no children, who undertakes a one-year course of non-job-related education, earning 25% of their wage before education during education. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system and the social security contribution system are incorporated. The results do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

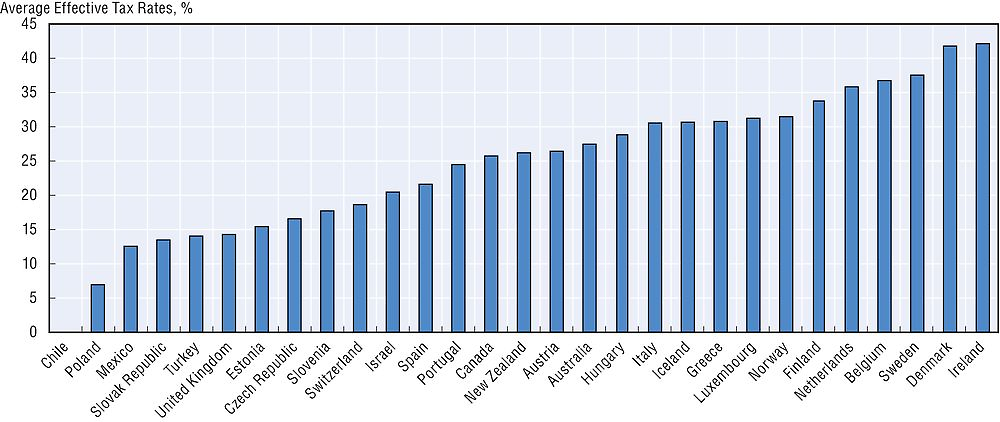

To calculate the AETR, a 5% increase in earnings from graduate education is assumed compared with those without graduate education.7 As is the case throughout, AETRs are usually higher than the METRs, as the assumed returns to skills investments are higher than the breakeven level. This means that they are taxed away at a higher rate by a progressive tax system. Figure 4.13 shows that the AETRs range from 0.0% (Chile) to 42.2% (Ireland) with an average in the sample of countries of 24.6%. As is discussed in Chapter 3 of this study, the higher returns to average skills investments over marginal skills investments means that AETRs are often closer to the tax rate on the extra earnings that come after education. Thus, those countries that have high and progressive taxes are more likely to have a higher average tax burden on skills.

Note: Data are for a 27-year-old single taxpayer with no children, who undertakes a one-year course of non-job-related education, earning 25% of their wage before education during education. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system and the social security contribution system are incorporated. The results do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

Figure 4.14 shows how the BEI, METR, and AETR vary with income. AETRs are usually rising in income before education. This is due to tax progressivity; being at a higher income level before education means that any extra earnings are taxed away at a higher rate. This is particularly true where the returns are high. For breakeven returns, which are usually lower, the relationship between the tax rate and income before education varies significantly. As outlined in Section 3.6 these METRs are a product of the interaction of the tax rate on foregone earnings with the tax rate on the earnings increment (this can be seen in Figure 3.6 in particular). Sharp rises in the tax rate on foregone earnings - because taxes fall suddenly during education - will sharply decrease the METR, as the tax system reduces the costs of skills investments. Similarly, sharp increases in the tax rate on the earnings increment will cause sharp rises in the METR, as extra earnings cause taxpayers to shift to higher brackets. These interactions cause the non-linear METR schedules over income before education that can be seen in Figure 4.14.

Note: Data are for a 27-year-old single taxpayer with no children, who undertakes a one-year course of non-job-related education, earning 25% of their wage before education during education. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system and the social security contribution system are incorporated. The results do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

This figure suggests that for taxpayers on the margin between making a skills investment or not, the METR can vary a lot depending on their current position in the labour market. The tax system does not treat skills investments similarly at various income levels. This is an argument for ensuring that fewer steep rises exist in tax schedules, as these can exacerbate the METR on skills at certain points in the tax schedule. A shift to fewer brackets and away from large tax increases over narrow bands could be broadly friendly to investments in skills.

4.5. Job-related training

The model of workplace training examines a 32-year old person undertaking a short (approximately two-week) course of study. In contrast to the graduate and tertiary education cases, it is assumed that they are not in receipt of any scholarship income, but still pay an average amount of direct costs (usually tuition fees).8 As with the graduate education case, it is assumed that earnings during education are a function of earnings before education. It is assumed that due to reduced labour effort during a skills investment, earnings in the year where a skills investment is undertaken are 95 % of what they would be in the absence of the skills investment.

A key assumption in the case of workplace training is that the training undertaken, while privately funded, is “necessary or related for the workers’ job”. Many OECD countries have STEs in their tax systems that offer tax deductions or credits for training where this training is job-related.9 These STEs are often not available for education in general – they are not, for example, available for tertiary education or for normal graduate studies. The precise stringency of the availability varies from country to country. Some countries allow the costs of training to be deducted from taxable income where the training is “related” to a current job, while other countries require the training to be ‘necessary for the maintenance’ of a current job. There are clearly kinds of training that would be eligible for a deduction in the former case that would not be in the latter case. The model does not consider these nuances in detail; rather it simply makes a distinction between two broad categories: “job-related” training, which is modelled as eligible for all of these deductions and credits, and non-job-related training, which is modelled as ineligible.

As with tertiary and graduate education, a variety of simplifying assumptions are made. Just as tertiary education is significantly subsidised by parents in the OECD, so job-related training is likely to be heavily, if not wholly, subsidised by firms. The model does not, however, cover the effective tax rate on human capital investment by firms, as this would require a broader discussion of the effective tax rate on corporate income, which is beyond the scope of this study. This means that despite being job-related, the model assumes that the training is financed by the individual. As before, it is assumed that training is financed with savings, not with debt.

METRs on job-related training are usually, though not always, lower than those on graduate education, and often roughly similar in size to those on tertiary education. There are several drivers of this. First, the length of the education period considered here is the shortest of any of the kinds of education considered in this study. This means that the costs are the lowest of those modelled, directly and in terms of lost earnings. A result of this is that BEIs are similarly low. In this case, BEIs range from 1.16% (Iceland) to 1.7% (Chile), with an un-weighted average of 1.3%. These results are shown in Figure 4.15. This means that the amount that earnings need to rise tends to be comparatively small; reducing the impact of tax progressivity on the METRs.

Note: Data are for a 32-year-old single taxpayer with no children, who undertakes a short course of job-related education, earning 95% of the average wage over the year while they study. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

A second reason why METRs are low in this case is the impact of the tax deductions and exemptions discussed above. These offset many of the direct costs of education, and are usually not available in the two cases – graduate education and tertiary education – that have been discussed previously. While some STEs did exist in those cases – some countries do offer tax credits for the costs of tertiary education, and scholarship income is usually tax exempt – job-related training is usually in receipt of the largest amount of STEs. This means that METRs are comparatively modest, ranging from -15.1% (Mexico) to 10.6% (Norway), with an average in the sample of 1.8%. For most countries, however, the METR is between -1% and 5%. These results are shown in Figure 4.16. The efficiency of these tax expenditures is discussed further in Chapter 5.

Note: Data are for a 32-year-old single taxpayer with no children, who undertakes a short course of job-related education, earning 95% of the average wage over the year while they study. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

4.6. Lifelong learning

The model of a worker reskilling in later life examines a 50-year old person undertaking a one-year course of study. It is assumed that the worker can earn 25% of previous earnings, and that they are in receipt of some scholarship income. In contrast to the case of workplace training, it is assumed that the course is not “job-related” and so is not eligible for most tax deductions for skills expenditures. In doing so, the results highlight the fact that it can potentially be more costly to finance training that may involve changing careers than training that facilitates advances within careers. In this way, the tax system may place a hidden burden on labour market mobility and flexibility, though this will vary from country to country.

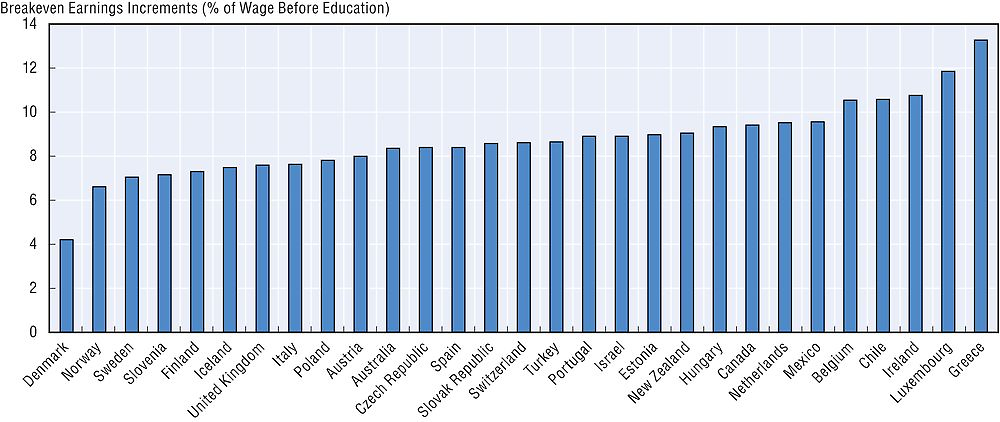

BEIs are among the highest in this example of any of the stylised cases considered, ranging from 4.2% in Denmark to 13.3% in Greece, with an average in the sample of 8.7% (see Figure 4.17). These values are higher than the value for a similar one-year course of education for 27 year-old, as examined in Section 3.2. This is because older workers have fewer years in which to recoup the cost of education. This means that the per-year amount by which earnings must increase is much higher. This is intuitive; workers who plan to retire soon may not benefit from leaving the labour market for a year to raise their earnings; after all, they may only be working for a few more years. This draws attention to the fact that it may be very difficult, and financially very costly, for the government to provide sufficient financial incentives for older workers to invest in skills, even when those workers face deterioration or obsolescence of their existing skills. It can become costly on a per-year basis for them to make such investments.

Note: Data are for a 50-year-old single taxpayer with no children, who undertakes a one-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

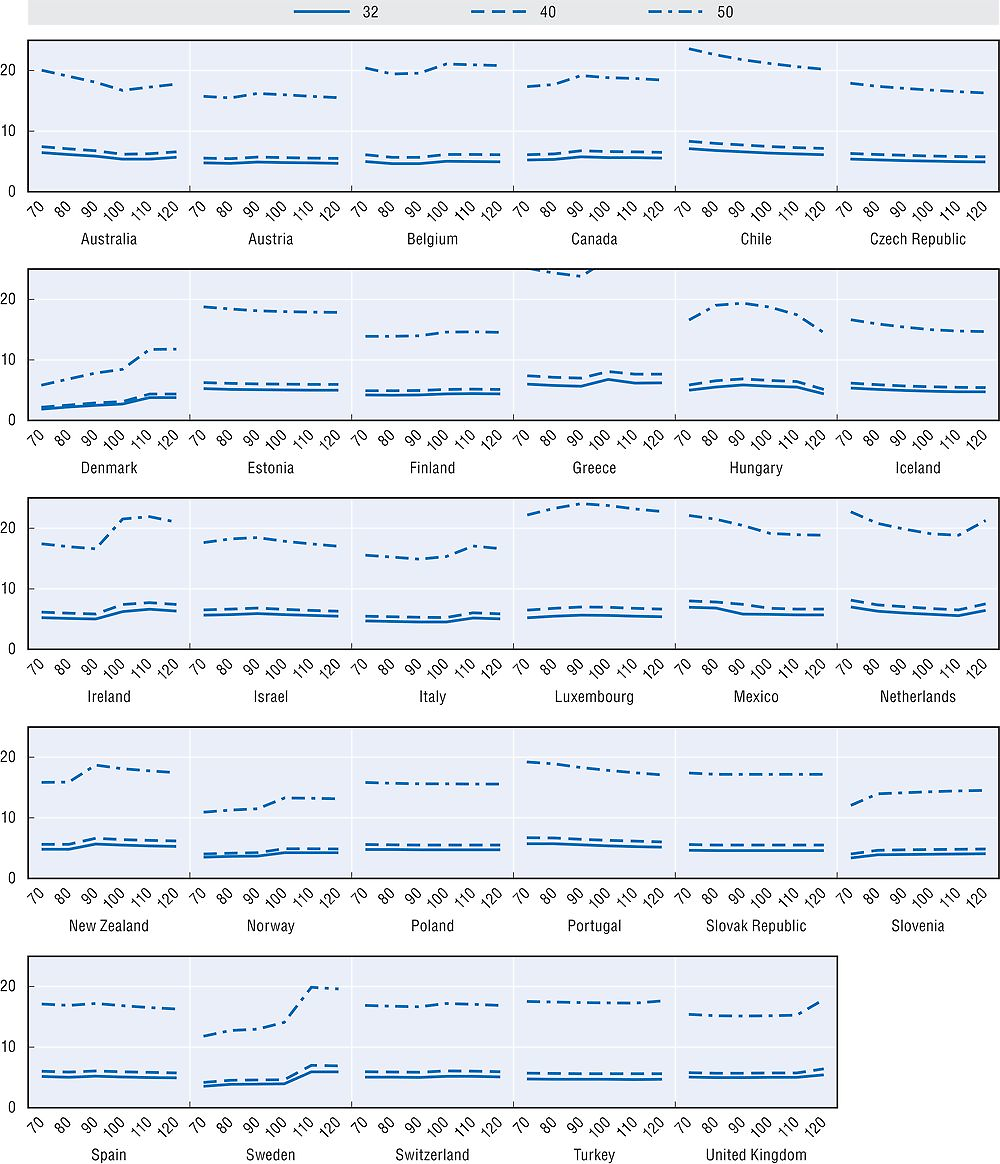

Figure 4.18 shows this pattern in further detail. It shows the BEI by income for three different ages of worker under similar circumstances: one year of non-job related education earning 25% of the previous wage. Ages are varied from 32 to 40 to 50 years old. The figure shows that the BEI rises steadily with age. This highlights the financial barriers that older workers have in pursuing educational opportunities.

Note: Data are for a single taxpayer with no children, who undertakes a one-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

There are of course key implications arising from these results in relation to the activation of older workers. Workers who have better skills and commensurately higher capacity to earn are more likely to remain in the labour market. Increasing the skills of older workers may provide a several-fold return to government; higher tax revenue while a worker continues to work, but also an expansion of the expected time that the worker remains a productive member of the labour force. This may provide a financial rationale for increased incentives to upskill workers early enough during their careers when returns will allow the investments to break even.

However, this logic works both ways; in this model, the more years that are left in the labour market, the more years a skills investment has to break even. This means that BEIs fall with the number of years left to retirement. A clear way to increase the incentives that workers have to upskill is to increase the number of years they expect to stay in the labour force by raising the retirement age.

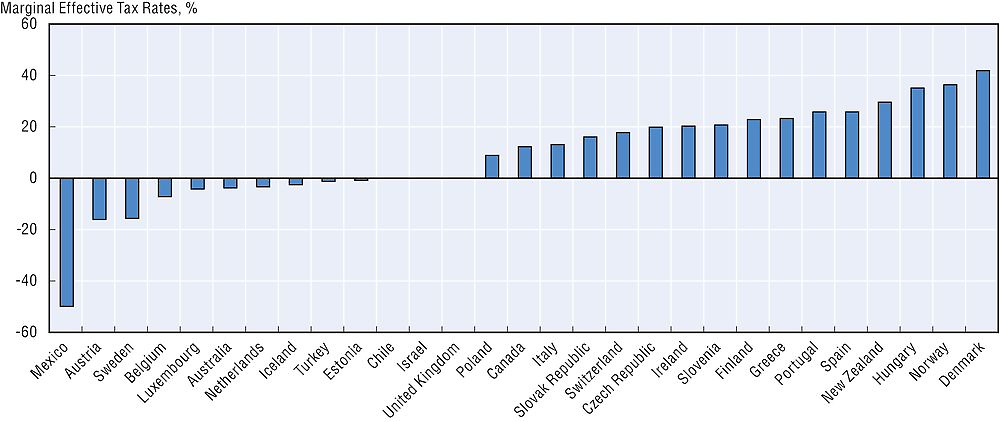

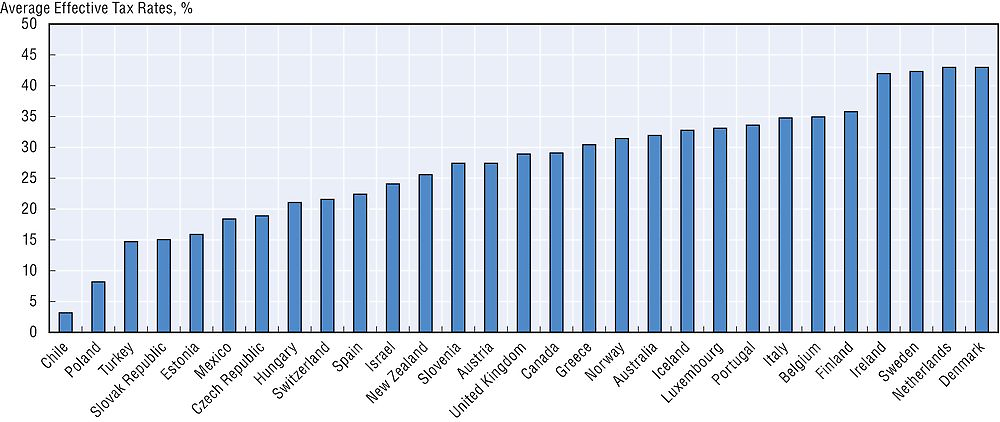

Overall, the tax burden on skills investment of older workers is lower than that for similar younger workers. Figure 4.19 shows that average rates range from 0% (Chile) to 39% (Ireland) with an average value in the sample of 21%. Figure 4.20 shows that these rates are slightly lower for older workers than for younger workers.

Note: Data are for a 50-year-old single taxpayer with no children, who undertakes a one-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

This seems counterintuitive: Figure 4.18 has shown that BEIs are higher where workers are older; however AETRs fall as workers age. The reason for this is in the discussion of the equation behind the AETR in Section 3.5. The AETR is the difference between the value of a skills investment with and without taxes, expressed as a fraction of the discounted value of the EI. The definition is restated below:

The returns to skills investments fall with age; this is because a worker has fewer years left in the labour market to earn any higher wages. This means the total difference in the returns with and without taxes also falls, even though it may not fall on a per-year basis. This means that the overall AETR falls with age.

Note: Data are for single taxpayer with no children, who undertakes a one-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment.

4.7. Gender differentials

The returns to education differ widely for men and women. An important question in designing skills policies is whether the financial incentives to upskill are as strong for women as they are for men. Moreover, differing returns in the labour market to skills investments raises the question as to whether skills policies are properly calibrated.

The returns to skills investments may vary for women and men for various reasons. Female labour market participation is usually lower in OECD countries than that of men. Women may foresee that, in the period after a skills investment, they may be less likely to stay in the labour market over the remainder of their working-age life. This reduces their returns to skills investments, and may make some skills investments less worthwhile from a financial perspective. Some investments may make sense if an individual were to assume full labour market participation until retirement, but not if an individual foresees extended periods of labour market absence, or lack of labour market activity at all. In such cases, skills investments may not make financial sense.

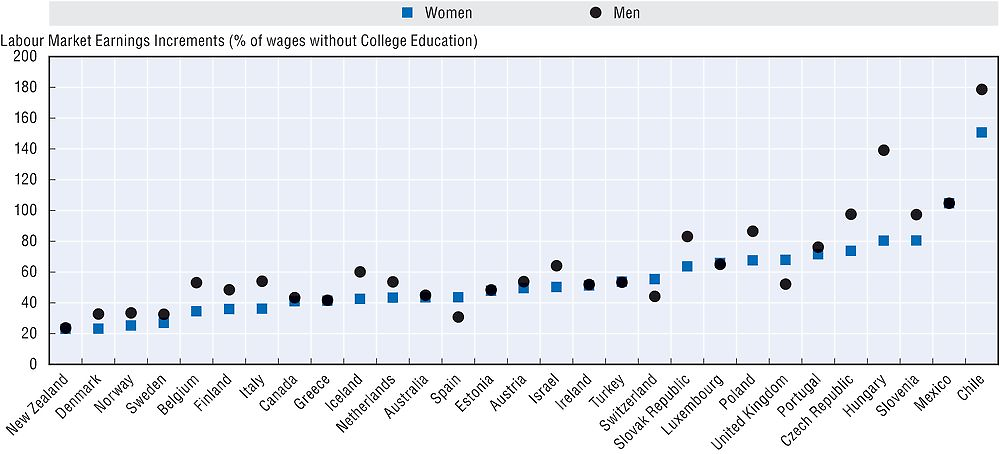

These issues may be compounded where gaps exist in the returns to skills investments across genders. Figure 4.21 shows the size of the tertiary education earnings premium disaggregated by gender for the countries examined in this study. In most countries, going to university is more financially rewarding for men than it is for women. This is not the case for all countries: for Spain, Switzerland, and the United Kingdom the pattern is reversed as evidenced below.

Note: Data are for 2011 where available.

Source: Data based on OECD Education at a Glance (2014), and author’s calculations.

Reduced earnings for women may mean that a tertiary skills investment decision may not be optimal from the perspective of the student. Financial returns to skills investments may not exist for a given student; the breakeven earnings level may not be available for women when they invest in skills. Though these data are of course presented for average cases – as are the hypothetical BEIs in previous sections – they do point to a potential issue: the gaps in wages and in labour market participation lead to different incentives to invest in human capital across gender.

There is evidence to suggest that even though the returns to skills investments may differ across gender, these differences may not be affecting enrolment rates too much. Recent OECD research (OECD, 2014) has demonstrated that enrolment rates at third level are usually higher among women than among men in OECD countries. This may be because the generation of women currently in third-level education may expect to see their wage rates and participation rates rise to parity with those of men over their working lives.

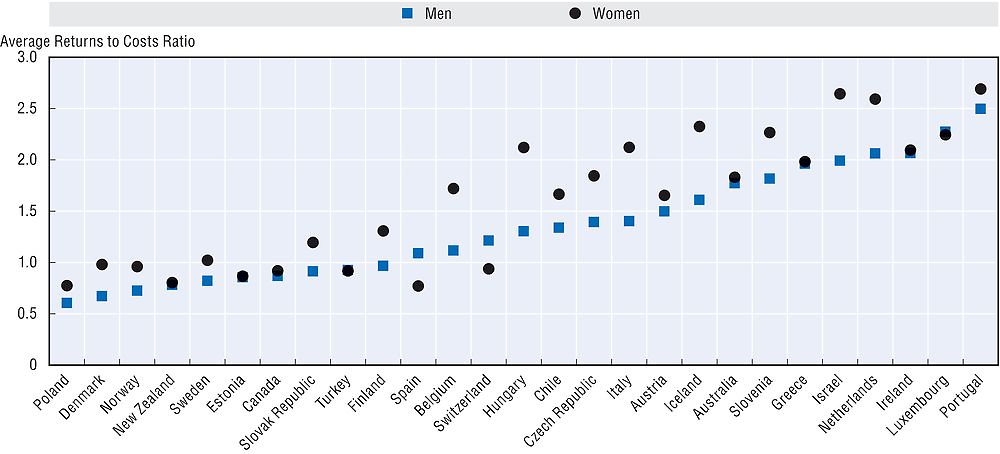

From the government’s perspective, Figure 4.22 shows ARCRs for men and women. The calculations of the returns to government are based on the earnings data in Figure 4.21. In general, the government’s returns from educating men are higher than its returns from educating women. This is due to higher expected wages for men than for women which means expected higher tax returns for the government, raising the ARCR. In the model, both genders cost the same amount to upskill. This means that those countries with the highest gaps in the ARCR are those countries that combine high or very progressive tax rates (so the government captures a substantial amount of the returns to skills investments) with comparatively high gaps in the tertiary education premium across gender (so that the returns to skills investments vary widely by gender). These gaps in the ARCR are highest for Hungary, Italy, Israel, and the Netherlands. By contrast, where the tertiary education premium is higher for women than for men, the gap in the ARCR by gender runs in the opposite direction; the returns to educating women are higher on average from the government’s perspective. This is the case for Spain, Switzerland, and the United Kingdom.

Note: Data are for a 17-year-old single taxpayer with no children, who undertakes a four-year course of non-job-related education, earning 25% of the average wage during schooling. This figure shows results that incorporate tax deductions and tax credits for direct costs, tax exemptions for scholarship income, and reduced taxes on student wage income. Tax incentives in the personal income tax system are incorporated, but not the social security contribution system. They do not incorporate STEs that subsidise parental spending on education or that subsidise firm spending on education. It is assumed that the skills investment is financed wholly with savings: students do not incur any debt to make a skills investment. Labour market data are based on the tertiary education premium earned by 15-64-year-olds.

These results present important challenges and opportunities for governments. The analysis suggests that for some governments the returns to education for women may be low due to the wage gap. Though this analysis does not account for gaps in labour market participation, accounting for these differences would likely increase the gap between the genders with respect to the returns to skills investments from the government’s perspective. This means that reducing the wage gap by raising female labour market participation and raising female wage rates could see the government recoup a greater degree of its spending on skills investments for women.

References

OECD (2014), Education at a Glance 2014: OECD Indicators, OECD Publishing, Paris, https://doi.org/10.1787/eag-2013-en.

OECD (2016), Taxing Wages 2016, OECD Publishing, Paris, https://doi.org/10.1787/tax_wages-2016-en.

Notes

← 1. The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law.

← 2. These costs are discussed in Chapter 3.

← 3. Throughout, the results refer to 2011 USD.

← 4. This would also be the case in selected other countries with income contingent loan schemes that have not been modelled in this study. For example, this would also be the case in Canada for students with Canada Student Loans through the Repayment Assistance Plan, and other provincial/territorial government loans through their respective repayment assistance plans.

← 5. This is discussed further in Section 3.3.

← 6. Note that the estimations of the costs of graduate education are the same as those for tertiary education. This is due to data limitations. These costs are discussed more in Chapter 3.

← 7. This is due to data limitations. There are good data on the premium earned in the labour market by tertiary-educated workers over non-tertiary-educated workers, but the data on the premium earned by graduate-educated workers over tertiary-educated workers is less comprehensive. A broad assumption of a 5% per annum return on the skills investment is made, while recognising that this misses a lot of between-country variation.

← 8. Note that the estimations of the direct costs of in-work training are the same as those for tertiary education. As with graduate education, this is due to data limitations.

← 9. See Chapters 2 and 5, and Annex B, for more details on STEs.