Chapter 3. Towards green growth1

New Zealand experienced strong economic growth for most of 2000-15. The Business Growth Agenda aims to continue improving the productivity and environmental performance of the natural resource-based sectors to support the country’s growth. This chapter reviews New Zealand’s efforts to promote green growth and sustainable development at the domestic and global levels. It analyses progress in using economic and tax policies to pursue environmental objectives and in reforming potentially harmful incentives. The chapter also discusses policies to promote low carbon energy and transport infrastructure and services, and reviews the country’s eco-innovation performance.

1. New Zealand’s economy and the environment

New Zealand is a small open economy with one of the highest living standards in the OECD (Figure 1.2). The economy grew faster than the OECD as a whole in 2000-15, at an annual rate of 2.7% (Figure 1.1; Chapter 1). Key drivers of growth over the decade include a sharp increase in the international prices of dairy products, the main exports; a booming tourism sector; and housing and infrastructure construction (OECD, 2015a). Rapid population growth, partly linked to large net immigration flows, and low responsiveness of housing supply have exacerbated housing constraints, notably in Auckland, and increased pressures on transport, water and wastewater infrastructure (Indicator 5; Chapter 5).

New Zealand has built an international reputation as a “green” country, both as tourism destination and as producer of natural and safe food. Natural resources are a major contributor to growth: the products of the primary sector (including agriculture, forestry, fishery and aquaculture, as well as oil and coal) account for over half of the country’s exports. New Zealand is the world largest exporter of dairy products and sheep meat, which account for more than 40% of total exports. Overall, agriculture accounts for 7% of gross domestic product (GDP), a much larger share than in most OECD member countries. At the same time, tourism and other services have grown rapidly, representing more than a quarter of exports in 2015. The country’s pristine wilderness and spectacular landscapes attract millions of tourists every year (Chapter 1).

New Zealand’s growth model has begun to show its environmental limits, with increased greenhouse gas (GHG) emissions and waste generation, freshwater contamination (Chapter 4) and threats to biodiversity (Chapter 1). The country has benefited from the increase in international dairy prices, which has encouraged a large conversion of land from forestry and other types of farming to dairy over the last two decades (Chapter 1). This has also led to a more intensive use of agricultural inputs (such as fertilisers and feed) and higher water demand for irrigation. Such changes have generated adverse environmental impacts, including nitrogen losses to water bodies, soil compaction, biological GHG emissions and reduced variety in pastoral landscapes (Baskaran, Cullen and Colombo, 2009). Foote, Joy and Death (2015) estimate that the cost of some environmental impacts exceeded the dairy export revenue in 2012.

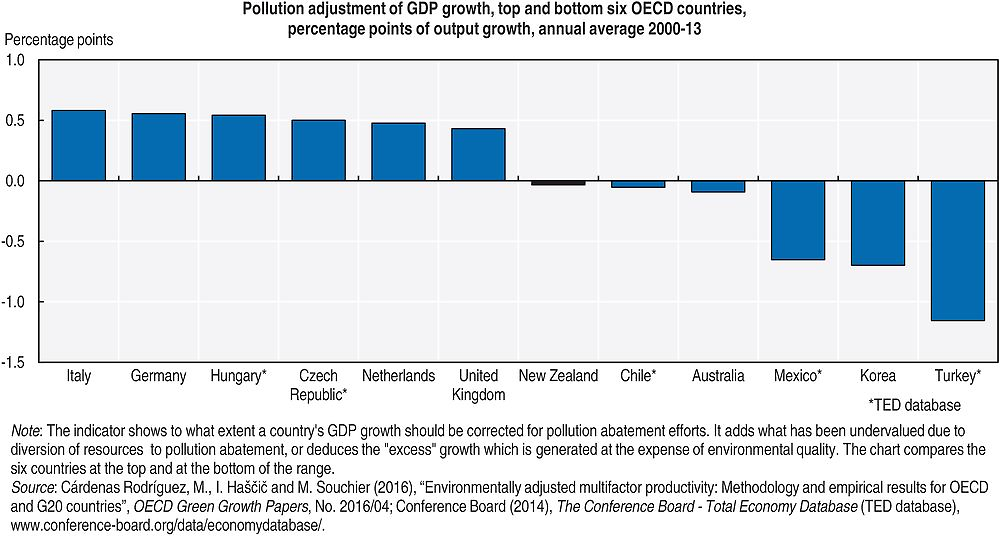

A 2016 OECD study estimate that adjusting New Zealand’s GDP growth for the cost of total pollution abatement would reduce growth over 2000-13 by 0.03 percentage points on average per year (Cárdenas Rodríguez, Haščič and Souchier, 2016; Figure 3.1).2 While this is a very low loss in GDP growth, accounting for pollution abatement leads to an increase in economic performance in three-quarters of other OECD member countries. This may indicate that New Zealand’s strong growth has come partly at the expense of environmental quality, a dynamic that puts the country’s “green” reputation at risk. This could be detrimental to the competitiveness and attractiveness of the economy in a global market as consumer and investor preferences shift towards sustainability and strong environmental performance.

2. Building a green growth strategy

New Zealand has strengthened the institutional and policy arrangements for ensuring environmental and economic policy coherence (Chapter 2). In 2009, it signed the OECD Declaration on Green Growth; in 2011, the government established the Green Growth Advisory Group to advise on green growth opportunities and support preparation of the Business Growth Agenda (the government development programme). The group recommended that “green growth enablers become part of the core platform in the government’s overall economic management”, as opposed to suggesting a stand-alone strategy for green growth.

The Business Growth Agenda (BGA), launched in 2012 and revamped in 2015, considered the group’s recommendations, but only to a limited extent. The BGA pursues the broad goal of building a more competitive and productive economy, with a strong focus on international markets and innovation. It sets the target of making exports account for 40% of GDP by 2025 (from about 30% in 2015). The improvement of the natural resource base is one of its six pillars, as natural resources are an input to key economic sectors, especially the large export-oriented livestock production sector (Box 3.1).

The Business Growth Agenda (BGA) aims to encourage a more productive and competitive economy. It foresees increasing the value added of export products and developing stronger international connections. To that end, it envisions further strengthening the education and innovation systems, removing infrastructure bottlenecks and improving the natural resource base. The BGA focuses on six key areas or inputs for successful business performance: export markets, investment, innovation, skills, natural resources and infrastructure, which are additionally considered in the context of three cross-cutting themes – Maori economic development, sectors and regions, and regulation.

The BGA natural resource chapter (“Building Natural Resources”), published in 2015, focuses on improving the productivity of, and the value added generated by, natural resource-based sectors, while reducing their environmental impact. It highlights the role of higher land productivity, improved efficiency in agricultural input use (such as water and fertilisers) and advanced technologies in enabling a lighter environmental footprint and ensuring the most productive use of resources. The chapter puts forward 74 projects that revolve around seven principal drivers of growth: maximising the productivity of agricultural and horticultural land, while reducing environmental effects; providing more flexible governance options for Maori land, and assisting Maori trusts and landowners to improve the productivity of their land; encouraging regional economic development with certain and timely processes for allocating access to resources; freeing up urban land supply and accelerating access and use of it; improving the efficiency of freshwater allocation and usage within limits and encouraging investment in water storage and irrigation; developing aquaculture, fisheries and other marine resources, while maintaining marine biodiversity and sustainability; and improving energy efficiency and use of renewable energy to raise productivity, reduce carbon emissions and promote consumer choice.

Over the past four years, 35 projects have been completed in the Natural Resources workstream. Their scope has been broad, ranging from commissioning detailed economic growth studies for selected regions to reducing nitrogen discharge into Lake Taupo (Chapter 4).

Source: Government of New Zealand (2015a, 2015b).

Nonetheless, the BGA is far from providing a long-term vision for the transition of New Zealand to a low-carbon, greener economy. Such transition is likely to entail increasing trade-offs with the current production and export targets. In particular, reducing GHG emissions and improving water quality would be difficult with a strict reliance on productivity gains and no reductions in agricultural output (Royal Society of New Zealand, 2016). At the same time, growing tourism exports can pose risks to natural and cultural resources, especially if the number of tourists increased rapidly and concentrated in a few places in national parks and conservation areas. New Zealand should consider establishing a collaborative (whole-of-government, multi-stakeholder) process to develop a long-term vision for the country’s transition towards a low-carbon, greener economy. This vision should take into account the economic opportunities arising from exporting higher value products, tapping into emerging markets and investing in environmental quality improvements. This will ultimately help the country reduce its reliance on agriculture and the use of natural resources, and withstand the risks of dairy price fluctuations.

New Zealand has many opportunities for a transition towards a low-carbon, greener economy. Vivid Economics and University of Auckland (2012) identified several green growth opportunities, including exporting green products and technology such as sustainable agricultural products and services, geothermal energy, biotechnology, second-generation biofuels and forestry products; importing new technologies and ideas to enhance domestic environmental policies, and resource and energy efficiency; improvements in building and transport energy efficiency; and electricity grid technology. As Indicator 5 discusses, the latter should be given priority, alongside raising investment in research and development (Indicator 6).

As the Green Growth Advisory Group (2011) acknowledged, New Zealand would benefit from a framework for monitoring progress towards green growth objectives. This framework should be based on sound indicators that link economic activity with environmental performance; it should include indicators on the effectiveness of the policy response in addressing environmental challenges and generating eco-innovation and green business opportunities. New Zealand could build on the OECD green growth indicators framework and on the experience of other OECD member countries that have customised it to their national circumstances (e.g. Chile, Denmark, Germany, Korea, the Netherlands) (OECD, 2014a). Systematic reporting on progress would help create a common understanding in society and build consensus and ownership about the low-carbon, green transition.

3. Greening the system of taxes, charges and prices

In line with recommendations of the 2007 OECD Environmental Performance Review, New Zealand has extended the use of economic instruments to put a price on environmental externalities and encourage efficient use of natural resources. It launched a GHG emissions trading system in 2008, discussed in Indicator 3.5, and piloted a nitrogen cap-and-trade system in the Lake Taupo catchment. This internationally unique policy experiment has proved a cost-effective way to address nitrogen pollution from diffuse sources (Box 4.7). A tradable quota system has long been in place to manage fisheries (Indicator 3.6). New Zealand also introduced some new environmentally related taxes, namely the waste disposal levy (described in Indicator 3.3) and a levy on goods containing synthetic GHGs (Indicator 3.1). Some local authorities used new pricing instruments in water and waste management, with positive results. Quantity- or volume-based waste charges have encouraged households to limit waste generation, and volumetric water charges have helped reduce per capita water consumption in some cities (Chapters 1and 5). However, current legislation limits the ability of cities to apply volumetric charges to wastewater services and make greater use of road tolls and congestion charges (NZPC, 2016).

3.1. Environmentally related taxes: An overview

New Zealand has a competitive and efficient tax system. Tax-to-GDP ratio stood at 32% in 2014, lower than the OECD average of 34%; the government is committed to keep it low. Over 55% of tax revenues are collected through income and profits – the third highest share after Denmark and Australia. The central government collects nearly 90% of general government revenues (only Ireland and the United Kingdom have comparable shares), which indicates local governments have relatively limited fiscal autonomy (Chapter 5).

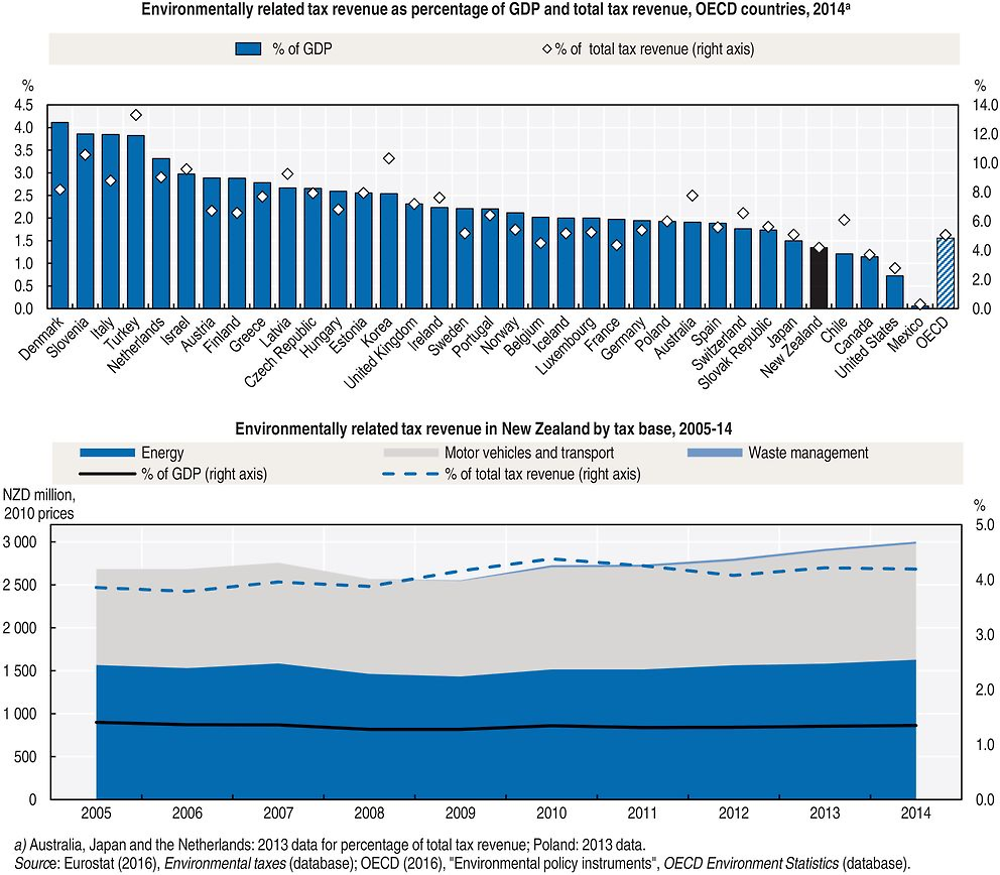

Revenue from environmentally related taxes is low in international comparison. It accounts for 4.2% of total tax revenue and 1.3% of GDP (data 2014), among the lowest shares in the OECD (Figure 3.2). Environmentally related taxes are defined as any compulsory, unrequited payment to general government levied on tax bases deemed to be of particular environmental relevance. As in all other OECD member countries, most environmentally related tax revenue is collected through taxes on consumption of energy products (54%) and vehicle ownership and use (45%).

Since the mid-2000s, environmentally related tax revenue (in real terms) has increased by almost 15%, with a dip in 2008-09 linked to the economic recession. Revenue from energy taxes has grown since 2012, owing to tax rate hikes. It had declined between 2005 and 2011 following less use of petrol and the shift to diesel, which is exempt from the excise duty and is indirectly taxed via a distance-based tax on diesel vehicles (see next section).3 The expanding vehicle fleet, especially of those running on diesel (Chapter 1),4 has resulted in increased revenue from vehicle taxes. This combination of factors meant that environmentally related tax revenue grew at a slower rate than GDP: indeed, its ratio on GDP has declined by nearly 4% since 2005 (Figure 3.2).

Taxes on pollution and resource use are virtually limited to the waste disposal levy, which accounts for a negligible share of revenue (Indicator 3.4). In 2013, New Zealand introduced the Synthetic Greenhouse Gas (Goods) Levy on imported products containing hydrofluorocarbons (HCFCs) and perfluorocarbons (PFCs) such as fridges, freezers, heat pumps, air-conditioners and refrigerated trailers. Rates are linked to the price of carbon in the NZ Emissions Trading Scheme (ETS) (Indicator 3.5) and vary across products to reflect the amount, type and global warming potential of the gas they contain. Rates have been low – e.g. around NZD 1 or less per household air conditioning system – and revenue is negligible.

While a low tax burden is conducive to growth, New Zealand could boost environmentally related taxes and charges by reforming fuel taxes, raising their rates and introducing new instruments such as taxes on industrial emissions and water pollution, as well as congestion charges. This could provide the government with some flexibility to lower other taxes that may be detrimental to growth; taxes on corporate income, for example, account for nearly 14% of total tax revenue, the second highest in the OECD.

Furthermore, expanding the use of environmentally related taxes and charges could help the government in its fiscal consolidation efforts. While New Zealand enjoys a solid fiscal position, with a near-balanced budget and low government debt in international comparison, the government is planning fiscal consolidation measures to reduce the Crown’s net debt from 25% to 20% of GDP over 2015-20 (OECD, 2015a).5 Much of the consolidation is expected to be achieved through spending cuts. However, New Zealand needs to ensure that reduced spending does not delay needed investment in infrastructure (Indicator 5; Chapter 5) or impede efforts to improve the well-being of the most vulnerable groups (OECD, 2015a). Additional revenue may, therefore, be necessary.

3.2. Energy and vehicle taxes and charges

Energy taxes account for a lower share of environmentally related tax revenue than on average in the OECD (54% compared to 70%). New Zealand is almost unique in the OECD in taxing only transport energy. It is also the only OECD member country that does not apply a fuel excise duty on diesel; a distance-based charge applies instead (see below). The fuel excise duty applies to all other transport fuels, i.e. mainly to petrol, but ethanol is exempt. Other levies – the Petroleum or Engine Fuel Monitoring Levy and the Local Authorities Fuel Tax – apply to nearly all fuels. The government raised the excise rate in 2012-15, seeking to increase infrastructure funding. However, the petrol price and tax rate remain low by international standards, and even more so those of diesel. New Zealand presents the largest tax gap between petrol and diesel when tax rates are converted per unit of energy (Figure 3.3).

All road vehicles are subject to a one-off registration fee and a periodic licensing fee, which vary according to the weight of the vehicle and the fuel it runs on, but not on environmental performance parameters.6 All vehicles that run on a fuel not subject to fuel excise duty, which comprise mostly diesel vehicles, must have a road user charge (RUC) licence. RUCs, which are distance based, can be purchased in multiples of 1 000 km. The cost of a licence varies, depending on the type of vehicle and its weight:7 heavy vehicles (over 3.5 tonnes) face a higher RUC, on the premise they cause more damage to roads and require pavement and roads to be built to a higher standard. All light vehicles (weighing less than 3.5 tonnes), including passenger cars, face the same rate, on the assumption they cause little road damage. This provides no incentive to move towards smaller, low-emission and more fuel-efficient vehicles. However, electric vehicles (EVs) have been exempt from the charge since 2009. The exemption, initially granted up to 2013, was recently extended until EVs reach 2% of the vehicle fleet (Indicator 5.2).

In theory, the rates of the petrol excise duty and the RUC rates are set so that, on average, petrol and diesel vehicle users pay the same tax amount (either in fuel tax or in RUC). However, the different charging systems favour diesel vehicles due to their lower fuel consumption per kilometre driven.8 This is not justified from an environmental perspective, as diesel has a higher carbon content per litre and diesel cars are generally considered to have worse local air pollution effects than petrol (diesel vehicles emit more particulate matter and nitrogen oxides per litre) (Harding, 2014a). This tax differential is even less justified in New Zealand, which has no mandatory vehicle fuel efficiency or emission standards. The vehicle fleet is relatively old, with a large share of second-hand, emission-intensive cars.9 While petrol light vehicles account for the vast majority of New Zealand’s fleet, the share of diesel light vehicles increased to 17% in the mid-2010s (Chapter 1). New Zealand has the highest, or among the highest, road-transport emissions per capita of nitrogen oxides, non-methane volatile organic compounds and CO2 in the OECD (Figure 1.7).

Revenue from fuel excise duty and road user charges is allocated to the National Land Transport Fund (NLTF). It is used to finance investment in land transport infrastructure and services, mostly in the road network (Indicator 5.2). The rates of the fuel excise duty and the RUC are set using a cost allocation model: the expected infrastructure costs are allocated to different vehicles depending on each vehicle’s estimated impact on those costs (heavy vehicles have a larger impact). In so doing, those who benefit from transport infrastructure and services contribute to a large part of the related investment. However, the cost allocation model and the associated tax and charge rates do not consider environmental externalities of road transport. In addition, the earmarking mechanism reduces flexibility of fiscal decisions.

New Zealand’s system of fuel taxes and vehicle charges is unique and partly linked to the large share of off-road use of diesel. About 33% of diesel is not used for road transport (compared to 30% in the OECD as a whole); it is used mainly in farms, industrial facilities and fishing vessels. The government considers that taxing off-road use of diesel would impose an unfair burden on these sectors, as the fuel excise duty and the RUC are levied to finance investment in land transport infrastructure that do not benefit off-road users. Operating a refund system would be administratively costly and potentially non transparent or vulnerable to abuse (e.g. fraudulent refund claims). However, in practice, the differential tax treatment of diesel and petrol vehicles implicitly encourages off-road use of diesel. This is partly common to other countries, where fuel use in the agriculture and fishing sectors benefits from tax exemption or partial refunds, but industrial use of fuels is generally taxed.

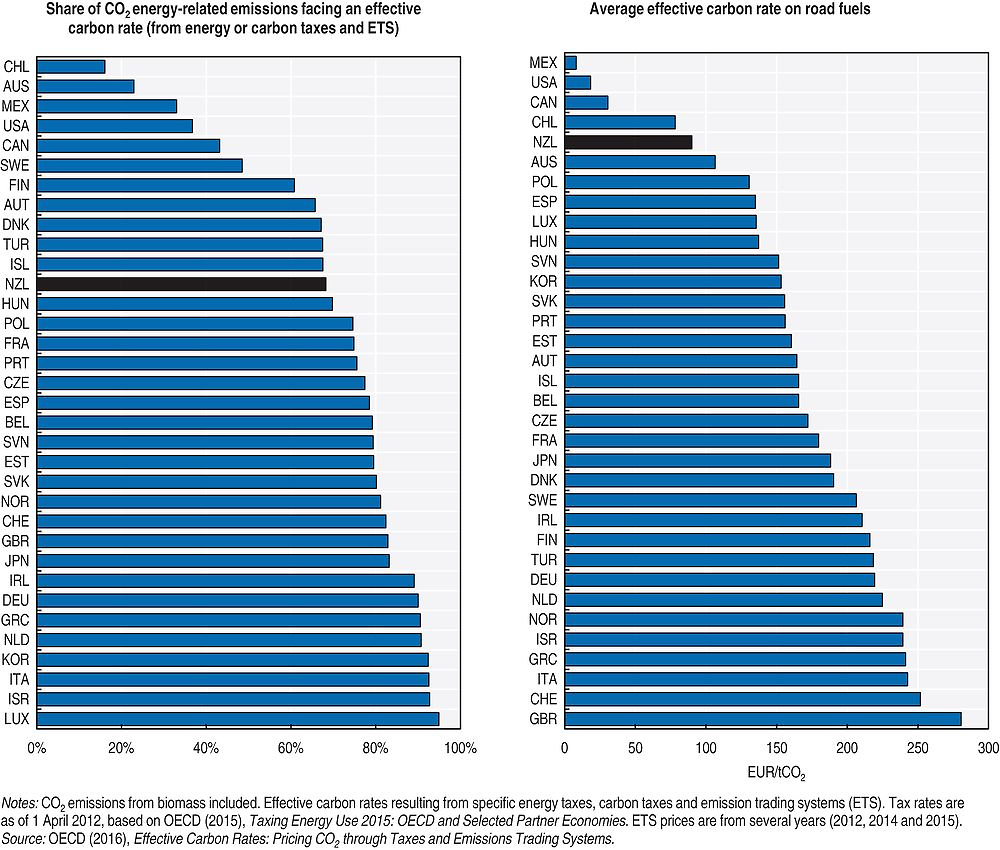

In addition to the absence of an excise duty on diesel, use of fossil fuels for heating, industrial processes and electricity generation is not taxed or else benefits from refund schemes. As a result, New Zealand taxes only slightly more than 40% of CO2 emissions from energy use, below the share in all OECD-Europe countries, and above the share in all non-European OECD countries but Japan (OECD, 2016a). This does not take into account the carbon price emerging from the NZ ETS, discussed in Indicator 3.5. OECD (2016a) estimates that, when accounting for both energy taxes and emission allowance price, a higher share (68%) of CO2 emissions from energy use face a carbon price signal in New Zealand. However, this share is still below that of CO2 energy-related emissions priced in many other OECD member countries (Figure 3.4).

The carbon price offers limited incentives for more efficient use of fossil fuels, especially in the transport sector. Only 56% of emissions from fuels used in road transport face a form of carbon price (either tax or ETS) above EUR 30 tCO2, which is a conservative estimate of the climate cost of emissions (OECD, 2016a). This is the third lowest share in the OECD (before Mexico and the United States). New Zealand was one of the few OECD member countries with average effective carbon rates faced by road transport below EUR 100 tCO2 in 2012. Despite rising emission allowance prices since mid-2015, the carbon price component of petrol and diesel prices remains at around NZD 0.01 per litre, too low to influence behaviour (Royal Society of New Zealand, 2016).

Even if carbon prices in the NZ ETS increase further, there is scope to raise taxes on fuels used for transport, heating and industrial processes, to the extent that the NZ ETS will continue to operate without an actual cap on domestic GHG emissions (Indicator 3.5). If such a domestic cap is ultimately introduced, the interactions between the NZ ETS and fuel taxes should be carefully assessed to ensure fuel taxes address environmental effects other than CO2 emissions. In particular, New Zealand should consider the introduction of an excise duty on diesel or otherwise remove the tax treatment disparity between petrol and diesel use.

In addition to the social costs of CO2 emissions, fuel taxes can help account for local air pollution and other social costs directly or indirectly linked to energy use (e.g. congestion, accident and noise costs in transport). Other instruments, however, may theoretically be more appropriate. Congestion, noise and accident costs are a function of the amount, location and timing of vehicle traffic; they are only indirectly linked to fuel use, as greater fuel use generally reflects increased distance driven. The impact of local air pollution also partly depends on the location of vehicle use or emitting facility: higher pollution in remote or rural regions may have lower health effects than in more populated or urban regions, but a higher impact on natural resources and vegetation (Harding, 2014a). Local air pollution from stationary sources could be better addressed through a tax on emissions with rates depending on the size of the affected population and on the social costs of different pollutants, similar to the tax Chile plans to introduce in 2017 (OECD, 2016b). A country-wide, time- and location-specific road pricing would generally be a more cost-effective tool to address congestion, accidents and noise. Still, the experience of the Netherlands indicates that political economy reasons are a serious barrier to implementation (OECD, 2015b). With its experience in distance-based road charging, New Zealand is well placed to move in this direction (Road User Charges Review Group, 2009). In the meantime, in the absence of a domestic GHG emission cap, comprehensive road pricing system and air emission taxes, New Zealand should consider broadening the fuel tax base and ensure that the excise duties and the RUC rates are set to take adequate account of environmental externalities. Higher fuel tax rates would provide an incentive for driversto reduce fuel consumption; to the extent this happens through reductions in distance travelled, other social costs may decrease. Any adverse impact on vulnerable population groups could be addressed with targeted benefit schemes.

3.3. Tax treatment of company cars and commuting expenses

Like many other OECD member countries, New Zealand favourably taxes benefits deriving from the personal use of company cars. According to an OECD study, the New Zealand tax system captures slightly more than 40% of a benchmark for neutral tax treatment of company car benefits relative to cash wage income (Harding, 2014b). This is a relatively low share compared to the other 25 OECD member countries covered in the study (Figure 3.5). This is because company cars used for private purpose increase an employee’s annual taxable income by only 20% of the vehicle’s acquisition value. In addition, the fuel costs paid by employers do not increase the employee’s taxable income. As a result, there is no incentive for employees to limit the use of company cars or choose more fuel-efficient vehicles. This tax treatment results in an annual subsidy of more than USD 2 500 per year, the third highest among the OECD member countries surveyed. Therefore, it is attractive for employees to be paid part of their salary in the form of company cars. Assuming about 30% of newly registered vehicles were company cars in 2012, this favourable tax treatment led to approximately USD 205 million in revenue forgone, or about 20% of the tax revenue from vehicle-related taxes, in the same year.

Employees cannot deduct expenses related to commuting between home and work from their taxable income, and public transport expenses paid by employers are considered fully as taxable income to employees. This leaves the employee neutral in choosing between commuting options: it encourages neither long driving distances that can trigger additional peak-hour traffic, nor use of public transport (as would be the case if only expenses for public transport use were deductible). However, free or subsidised parking spaces provided on the employer’s premises are not considered to be taxable income for employees. Given the increasing financial cost of parking, this can be a benefit of substantial value; it decreases the cost of driving to work relative to other forms of transport and thereby distorts decisions about the form of commuting (Harding, 2014b).

In addition to be a cost for the public budget, the favourable tax treatment of company cars and parking lots tend to encourage private car use, long-distance commuting and urban sprawl. It can result in increasing fuel consumption, emissions of GHGs and local air pollutants, noise, congestion and risk of accidents (Roy, 2014). As Chapter 5 notes, major New Zealand cities are expanding at their fringes, rather than in inner-city areas, to host a growing population. Despite more use of public transport, driving remains the main urban transport mode; for example, in Auckland, nine out of ten dwellers drive to work. New Zealand should, therefore, reconsider the taxation system of company cars and parking spaces, which runs against its climate mitigation goals and the sustainable urban development objectives of major cities.

3.4. Waste disposal levy and waste charges

The 2008 Waste Minimisation Act introduced a disposal levy (NSD 10 per tonne on waste sent to landfill). The levy aims to increase the cost of waste disposal, thereby changing the price signals associated with waste disposal and potentially promoting waste minimisation, recycling and alternative forms of treatment. However, the levy rate was not set on the basis of the social costs of landfilling; it was primarily designed to generate funding to finance waste minimisation projects at local and national levels (Bibbee, 2011).

The levy generates about NZD 25 million each year. Half of the levy revenue is redistributed to territorial authorities and the other half feeds the Waste Minimisation Fund (WMF). Most funding available for waste minimisation projects in the WMF is allocated through an annual competition. A 2014 review of the waste landfill levy found that its revenue has supported a broad range of initiatives to minimise waste, although outcomes need to be measured and monitored effectively.

The levy has increased the cost of waste disposal to disposal facilities. However, as it effectively covers only 30% of total landfilled waste, the cost of disposal has not increased for the majority of waste; many waste generators have perceived no incentive from the levy (MfE, 2014a). Extending the levy obligation to a larger number of waste disposal facilities would help improve its effectiveness.

Expanding the use of a pricing system for waste collection services would also help increase the levy’s effectiveness, encourage waste minimisation and recycling, and finance advanced waste management services (Chapter 5). Some territorial authorities apply quantity- or volume-based waste charges (weight-based, pay-per-bin or pay-per-bag), which provide incentives to households to reduce waste. Evidence from the Auckland region indicates that districts applying volume-based charges send nearly half of the waste volume to landfills than do districts financing waste management through flat charges included in property taxes. This is consistent with experience from other countries (e.g. Germany and Korea).

The NZ ETS (Indicator 3.5), which covers the waste management sector, obliges landfill operators to surrender emission allowances with the aim of encouraging them to invest in any landfill gas-collection system and to separate organic from non-organic waste to reduce methane emissions. However, the low NZ ETS carbon price has provided little incentive to do so to date. The interactions between the NZ ETS and the waste landfill levy should be examined.

3.5. GHG emissions trading scheme

The New Zealand Emissions Trading Scheme (NZ ETS), launched in 2008, represents the cornerstone of the country’s climate change mitigation policy and the main instrument to achieve its emission reduction targets. Several unique features differentiate the NZ ETS from other emissions trading systems worldwide. These reflect New Zealand’s distinct emissions profile (namely, a high proportion of agriculture-related biological emissions and a large amount of forest carbon sinks; see Chapter 1), as well as carbon leakage concerns and the aim of linking the NZ ETS to other markets.

The NZ ETS was designed to be a comprehensive scheme that included all gases covered by the Kyoto Protocol and all emitting sectors.10 It was the first carbon market in the world to include emissions and removals from forestry and agriculture. Forestry entered the NZ ETS at its inception for fear that an announced later entry would encourage deforestation.11 However, subsequent amendments indefinitely postponed the inclusion of biological emissions from agriculture (methane and nitrous oxide) until technologies are available to reduce these emissions in a cost-effective way and international competitors take sufficient action on their emissions.12 Stationary energy supply, liquid fossil fuel supply, industrial processes and waste management have all gradually joined the system. As a result, the NZ ETS covers 52% of national emissions (i.e. excluding biological emissions from agriculture). This compares to 45% of the European GHG emissions in the EU ETS and 85% of the GHG emissions in the California and Quebec cap-and-trade systems (ICAP, 2016).

The NZ ETS obliges participants to report on their GHG emissions and surrender emission units that correspond to their obligations. There is no domestic cap on emissions. This differs from other ETSs in the world, which set annual absolute emission caps (ICAP, 2016). The NZ ETS was originally designed to operate within the international Kyoto Protocol emission cap and credits market. It allowed participants to surrender either New Zealand Units (NZUs, each corresponding to 1 tonne of carbon dioxide equivalent, or tCO2-eq) or international Kyoto-compliant units (certified emission reduction units, or CERs, emission reduction units, or ERUs, and removal units, or RMUs).13 Until June 2015, when the NZ ETS stopped accepting international credits (see below), there had been no limit on the purchase of international carbon credits, contrary to all other ETSs in the world. As a result, the carbon price in the NZ ETS was determined by the international carbon markets, rather than by the domestic supply of NZUs. In 2011-14, most of the units surrendered by NZ ETS participants came from international sources. A relatively small share of the supply and units surrendered came from free allocations to some activities (see below) and NZUs issued against eligible emission removals from forest management (Leining and Kerr, 2016). The NZ ETS allows the government to auction allowances, but this option has not been used yet.

The NZ ETS design was intended to expose participating companies to the international carbon price. It lets them make economically efficient decisions on whether to reduce their own emissions or invest in mitigation elsewhere in the world, thereby minimising GHG abatement costs. This would allow domestic production and associated emissions to expand efficiently and New Zealand to still contribute to global mitigation efforts through the carbon market, thereby avoiding carbon leakage.14 The system was also intended to shift the purchasing of emission units for Kyoto compliance from the government to market participants, thereby ensuring least-cost compliance with international obligations (Leining and Kerr, 2016).

The NZ ETS has been reviewed and amended several times, which has created uncertainty for participants. Some of the amendments aimed to moderate the impact of the carbon price on participants. Twenty-six emission-intensive trade-exposed activities receive free allocations based upon their historical emission intensity.15 These free allocations were to be gradually phased out by 2030, but successive amendments have indefinitely postponed their removal out of competitiveness and carbon leakage concerns. However, evidence from carbon pricing systems implemented in other countries indicates the impact on competitiveness is generally limited and does not substantially differ between the firms that benefit from preferential treatment (such as free allocations) and those that do not (Arlinghaus, 2015). The free allocations are effectively a transfer to receiving companies and should be removed on the basis of a predetermined schedule; if allowances were auctioned instead, the government could raise NZD 50 million in revenue (at the 2016 emission allowance prices) (PCE, 2016). In addition, all participating companies have the option to pay the government a NZD 25 fixed price per unit, rather than surrender eligible units, which effectively sets a price ceiling. Prices have never exceeded the ceiling since the NZ ETS introduction, but are likely to rise in the future. New Zealand should consider removing the price ceiling or, at the very least, increasing it over time. In a welcome move, in mid-2016 the government decided to gradually phase out the so-called one-for-two arrangement, which had allowed non-forestry sector participants to surrender 1 NZU for every 2 tonnes of CO2 emission, thereby halving the number of permits needed.16

The NZ ETS has made little contribution to domestic GHG emission mitigation. The one-for-two obligation (until mid-2016), the free allocations to some sectors and the lack of quantity limits on the use of Kyoto units (until mid-2015) have blunted the carbon price signal and undermined the effectiveness of the system. The NZ ETS moderately encouraged afforestation in the first few years of implementation, when the emission unit price was higher (around NZD 20/tCO2-eq). Businesses have rarely considered the carbon price in their decisions and have not invested in reducing their emissions (MfE, 2016a). Companies have mostly purchased and surrendered to the government cheap ERUs and CERs, while banking massive amounts of the allocated NZUs (both those allocated for free and against emission removals from forestry) to meet future liabilities (Leining and Kerr, 2016).17 This contributed to depress the NZU price in line with the price of international units until it reached nearly zero.

At the same time, thanks to the accumulated surplus of Kyoto units, the NZ ETS has helped New Zealand over-achieve its Kyoto target of bringing its average annual GHG emissions over 2008-12 back to 1990 levels (Figure 1.9). However, the overflow of Kyoto units has undermined the integrity of the NZ ETS, as many ERUs were of questionable environmental integrity (i.e. they did not represent real emission reductions beyond business-as-usual). New Zealand was the top buyer of Kyoto credits, mostly ERUs, in proportion to domestic emissions (Simmons and Young, 2016). The government has carried over this surplus of units from the first commitment period for meeting the 2020 target to reduce emissions by 5% below 1990 levels. As the Parliamentary Commissioner for the Environment recommended, the government should not carry any international units over beyond 2020. This would restore the integrity of the system and ensure that New Zealand’s contribution to the goals of the Paris Agreement is real (PCE, 2016).

Since mid-2015, the NZ ETS has functioned as a purely domestic emissions trading system, de-linked from the Kyoto market. As New Zealand did not make a commitment for 2013-20 under the Kyoto Protocol, international credits are no longer eligible for compliance within the system. While prices have been increasing since, the stock of banked NZUs from the previous commitment period is sufficient to cover more than four years of emissions from participating sectors (MfE, 2015a). In this context, the price is driven by market expectations about future policy stringency rather than by the costs of mitigating domestic emissions. It thus has limited value as a long-term price signal (Leining and Kerr, 2016). The unclear relationship between the number of units available in the NZ ETS and the national emission reduction targets makes determining the supply of units, and the GHG emission mitigation outcome, highly uncertain. OECD (2013a) recommended New Zealand set a domestic cap on emissions. At the very least, New Zealand should align the supply of units in the NZ ETS with its climate mitigation targets. The government should also introduce auctioning of domestic allocations as soon as possible once the stock of banked NZUs is depleted. Further, it should consider introducing a price floor, increasing over time, on auctioned allowances. This would prevent the carbon price from plummeting to near-zero levels, as was the case in the past, and would help stabilise the price signal.

Current projections indicate that existing measures will not be sufficient to reduce emissions consistently with the nationally determined contribution (NDC) target to cut GHG emissions by 30% below 2005 levels by 2030 (MfE, 2016b, 2015b; Figure 1.9). New Zealand will need to find new ways of offsetting its domestic emissions by funding mitigation efforts in other countries, with a view to minimise abatement costs. It is likely that international emission offsets will be made newly eligible in the NZ ETS (MfE, 2015a). As the Parliamentary Commissioner for the Environment recommended, there should be a clear limit to the quantity of international credits that can be used to offset domestic emissions. This would help preserve the domestic mitigation efforts and avoid the perverse outcomes of the first commitment period.

The NZ ETS can contribute effectively to achieve New Zealand’s climate mitigation objectives, provided that some changes are made. Despite some complexities, it is a well-functioning, well-managed and transparent carbon market, which does not entail excessive costs for participating companies. The government regularly provides information about market transactions (MfE, 2016a). In 2015-16, the Ministry for the Environment conducted the third review of the NZ ETS, which addressed issues such as protective measures, auctioning and restricting access to international credits. The review, still ongoing at the time of writing, led to the phase out of the one-for-two arrangement (see above). It did not consider the possibility of bringing agriculture back within the system, however.

New Zealand needs to reconsider the decision of indefinitely postponing the entry of biological emissions from farming in emission trading. If such a decision is confirmed, alternative pricing or regulatory measures should be taken to make agriculture contribute to achieving New Zealand’s climate mitigation objectives. Setting a clear date for the inclusion of agriculture in the NZ ETS or for the introduction of alternative measures would provide much-needed policy certainty, help the sector prepare for the policy change, encourage investment and accelerate innovation. It would also enhance New Zealand’s environmental credentials on the international scene. Continuing to exempt nearly half of domestic emissions from the NZ ETS or other emission mitigation obligations would make achieving the New Zealand NDC target harder; it could place a disproportionate burden on other sectors of the economy and slow the pace of adjustment in the agriculture sector (Bibbee, 2011). At the same time, putting a price on biological emissions from agriculture can help address nitrogen water contamination (Box 3.2).

Efforts to reduce agricultural GHG emissions and measures to reduce nitrogen pollution in water can provide environmental co-benefits. For example, a price on carbon advanced the achievement of nitrogen reductions as part of the Lake Taupo Nitrogen Market (Box 4.7) by promoting land-use change from pasture to forestry. Lankoski et al. (2015) show that allowing stacking of carbon and water quality credits can encourage farmers to adopt environmental practices that reduce both GHG emissions and nutrient pollution. Agricultural climate mitigation practices that increase nutrient and water retention and prevent soil degradation (such as soil carbon sequestration) can also increase resilience to droughts and flooding.

However, climate policies may also send the wrong signal to farmers. For example, the NZ ETS required owners of forests that existed prior to 1990 to pay for carbon credits upon any land conversion to other uses such as pasture. In the upper Waikato River catchment,this triggered some landowners to clear their forests before the NZ ETS started in 2008. The amendment to the NZ ETS that delayed surrender obligations for agriculture de facto indefinitely postponed the price restraint on land-use conversion from forestry (carbon sinks) to pastoral farming. This ultimately led to additional clearing of forested land in the Waikato River catchment and increased nutrients leaching to the river (Dickie, 2016).

Source: Dickie (2016); Lankoski et al. (2015).

Some mitigation technologies are available or will be commercially viable in the near future as a result of the considerable investment in research (Emissions Trading Scheme Review Panel, 2011; Indicator 6); a carbon price is needed to make them cost-competitive with current practices and encourage farmers to adopt them. Free allocations and other measures could be used to allow farmers to gradually adjust to the carbon market and protect vulnerable small, family-run farms, provided they are strictly time-bound and phased out on the basis of a clear timeline. If agriculture is to be included in the ETS, the point of obligation should be shifted from the processor level, as in the current design, to the farm level in order to ensure farmers directly perceive the price incentive. Concerns about the high costs of measuring on-farm GHG emissions could be addressed by further investing in monitoring and reporting tools such as OVERSEER®, which provides on-farm information about nutrient use and leaching (Royal Society of New Zealand, 2016; Chapter 4).18

The NZ ETS is likely to be insufficient on its own to drive New Zealand towards a low-emissions economy and its long-term goal of reducing emissions by 50% below 1990 levels by 2050. There are already viable emission mitigation options in all sectors of the economy (Royal Society of New Zealand, 2016), and a sufficiently high and stable carbon price is essential to unlock them. However, despite their increase, prices remain too low to influence behaviour. In mid-2016, the NZU price was NZD 17.8 or USD 12.5;19 this compares with the estimated social cost of carbon of USD 32 tCO2eq that is commonly used in cost-benefit analyses in New Zealand (Smith and Braathen, 2015). Even if prices increase further, other market failures and non-price barriers (such as split incentives between those making the investment and those benefiting from it, transaction and information costs, difficult access to capital, risk aversion) may prevent investment in emission abatement (Hood, 2013). Hence, the NZ ETS needs to remain the main climate mitigation policy instrument for reducing domestic emissions as part of a wider and coherent package. Managing the interactions between the emission trading and other GHG mitigation measures (such as in the electricity supply and transport sectors) will be essential to the effectiveness of the package.

3.6. Tradable fishing quotas

New Zealand has had an effective system of tradable fish quotas since 1986 to manage commercial and customary fisheries, a model replicated in many countries (Bibbee, 2011). Each year, the government determines a total allowable commercial catch (TACC) for each species and region based on the maximum sustainable yield, net of an allowance for recreational fishing and customary Maori uses (Chapter 1).20 Individual fishing quotas are distributed among commercial fishers; the quotas entitle them to a given percentage of the TACC, determined on an annual basis, and can be subsequently traded within given regions and species (OECD, 2015c).

Allocating individual catch entitlements reduces the incentives to maximise catch at the opening of the fishing season (OECD, 2007). The quota system has helped reduce overfishing and maintain the fish stock at sustainable levels (Chapter 1); temporary reductions in the quotas have allowed some species populations to recover within or above their target range (OECD, 2015c). Between its inception and 2016, quota system coverage has increased from 26 to 100 species, including more than 630 fish stocks; it has become one of the largest such schemes in the world.

The government provides financial transfers for general fisheries management and conservation services. In 2013, the amount of these transfers was 12% above their 2005-10 average (OECD, 2015c). The costs of these transfers are recovered through levies charged to commercial fishing companies.21 In the framework of the World Trade Organization (WTO) negotiation, New Zealand has supported elimination of certain forms of subsidies that contribute to overcapacity and overfishing (OECD, 2015c).

4. Greening financial support to the energy and agriculture sectors

4.1. Fossil fuel subsidy reform

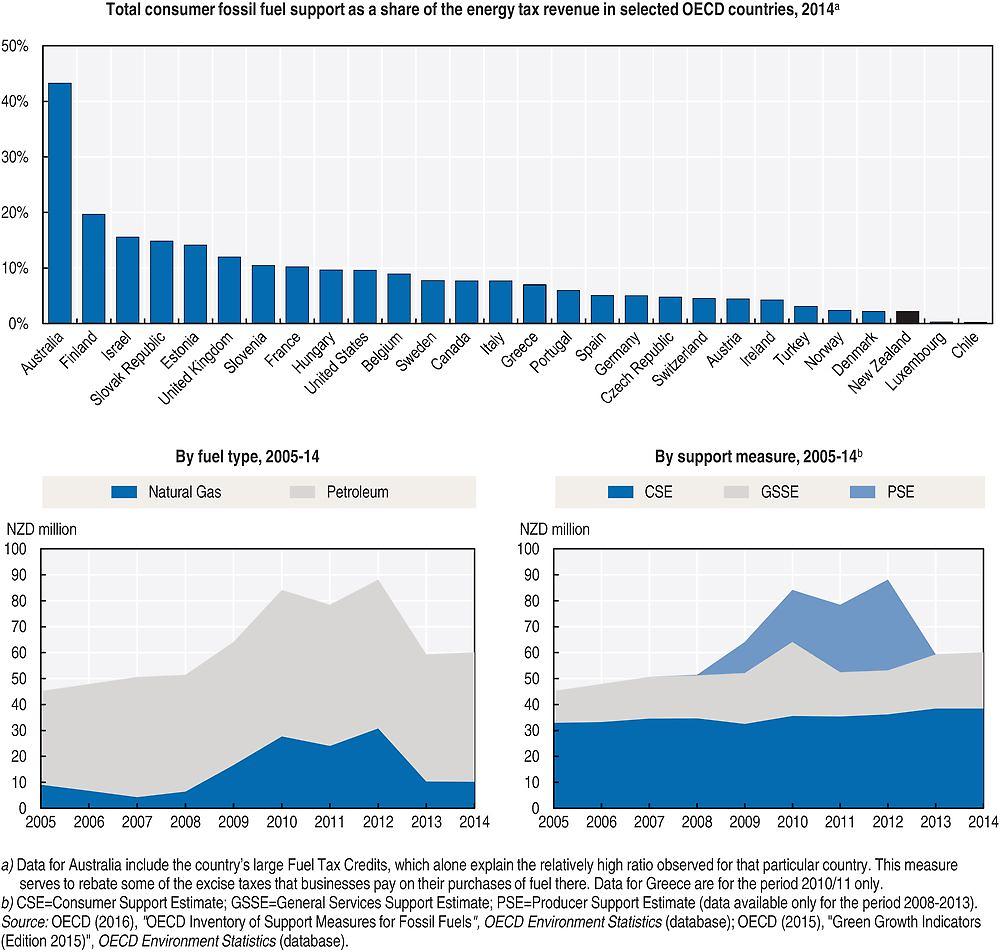

New Zealand is a founding member of the Friends of Fossil Fuel Subsidy Reform, an informal group of non-G20 countries established in 2010 working to build political consensus on the importance of fossil-fuel subsidy reform.22 To lead by example, in 2015, New Zealand voluntarily underwent a fossil-fuel subsidies peer review in the context of Asia-Pacific Economic Co-operation (APEC).23 The APEC panel reviewed eight measures that could be considered to support fossil fuels: motor spirit excise duty refund; funding of international treaty obligation to hold oil stocks; non-resident drilling rig and seismic ship tax exemption; indemnity for mining land remediation; research and development funding for the oil industry; tax deductions for petroleum-mining expenditures; financial restructure of solid energy; petroleum tax and royalty regime. Some of these measures cost the New Zealand government about NZD 60 million in tax breaks and budgetary transfers in 2014 (Figure 3.6; OECD, 2016c). The peer review concluded that none of these measures were “inefficient subsidies that encourage wasteful consumption” of fossil fuels. This was partly because the subsidies do not lower domestic fuel prices as New Zealand is a price taker on world oil market (i.e. it pays market prices for its petroleum products) (APEC, 2015).

New Zealand provides some of the lowest amounts of support to fossil fuel consumption in both absolute and relative terms. This can be seen in Figure 3.6, which expresses total consumer support for fossil fuels as a share of the revenue from energy-related taxes. In particular, off-road users of fuels (petrol, liquid and compressed natural gas) can obtain refunds for excise duty payments. Total refunds (and revenue forgone) have been relatively modest in the last decade, amounting to about NZD 30-40 million annually or about 3-4% of the revenue collected through the excise duty (Figure 3.6; OECD, 2016d).

A competitive tax and royalty regime is in place to attract investment in oil and gas exploration (IEA, forthcoming). For example, investors can deduct some exploration and development expenditures for tax and royalty purposes in the year they are incurred, rather than over the lifetime of the well; since 2005, non-resident companies exploring and developing offshore have benefited from income tax exemptions (this tax concession was extended until 2019). As OECD (2013a) notes, these incentives can distort investment decisions in favour of fossil fuel production over more sustainable sources of energy; they counteract New Zealand’s efforts to address global climate change and should thus be discontinued.

4.2. Financial support to agriculture

Total support to agriculture represented 0.3% of GDP in 2013-15, the vast majority of which was channelled to general services such as agricultural innovation, inspection and control, and infrastructure maintenance. This includes the Sustainable Farming Fund, which supports projects aimed at improving the environmental performance of agriculture (Box 3.3). Since the reforms of agricultural policies in the mid-1980s, production and trade distorting policies supporting agriculture in New Zealand have virtually disappeared. For more than 25 years, the level of support to farmers has been the lowest among OECD member countries. Agricultural support in the form of transfers to farmers, as measured by the producer support estimate (PSE), was less than 1% of gross farm receipts in 2013-1524 – the lowest in the OECD. However, the majority of such low support to producers is based on output and variable input use without input constraints: in 2013-15, this support represented 80% of the PSE, up from about 50% in the mid-1990s (OECD, 2016e; Figure 3.7). This form of support reduces the cost of capital and other purchased inputs; it indirectly encourages agricultural production and increases risk of overuse or misuse of inputs such as pesticides and fertilisers, with potentially negative environmental impacts.

The SFF, set up in 2000, supports community- and industry-driven projects aimed at improving the productive and environmental performance of agriculture, forestry and aquaculture. The maximum total grant available for individual projects is NZD 600 000 over three years. At least 20% of project costs must be met by non-government sources, although most successful projects are able to leverage a high proportion of other funding or in-kind support to complement an SFF grant. The SFF funds a wide variety of projects, including projects focusing on sustainable land management, organic farming, improved water management, climate change mitigation and adaptation and Maori agribusiness. The expected contribution to sustainability or climate change objectives is one of the criteria used to assess applications. The fund has invested up to NZD 9 million per year and backed 948 projects over 15 years.

Source: Ministry for Primary Industries (2016); OECD (2016e, 2013b).

The Irrigation Acceleration Fund (IAF), in place since the 2011/12 financial year, and Crown Irrigation Investments Limited (CIIL), established in 2013, provide grant funding and concessional financing to community and regional irrigation-related and water storage projects. To be eligible for funding, the projects need to promote efficient use of water, environmental management and demonstrate a commitment to good industry practice (OECD, 2016e). In addition, to help address the vulnerability of agricultural production to variable rainfall patterns, investment in irrigation can help enhance efficiency in water use and augment surface and groundwater flows. However, as Chapter 4 discusses, financial support to irrigation projects indirectly encourages intensification of agriculture, which is likely to further increase pressures on freshwater resources. Environmental gains may be limited if more efficient irrigation techniques do not result in lower net water use, but simply lead to an increase in irrigated volume or area. New Zealand would benefit from systematically assessing the effectiveness of transfers to farmers and financial support for irrigation against their socio-economic objectives and potential environmental impact.

5. Investment in the environment to promote green growth

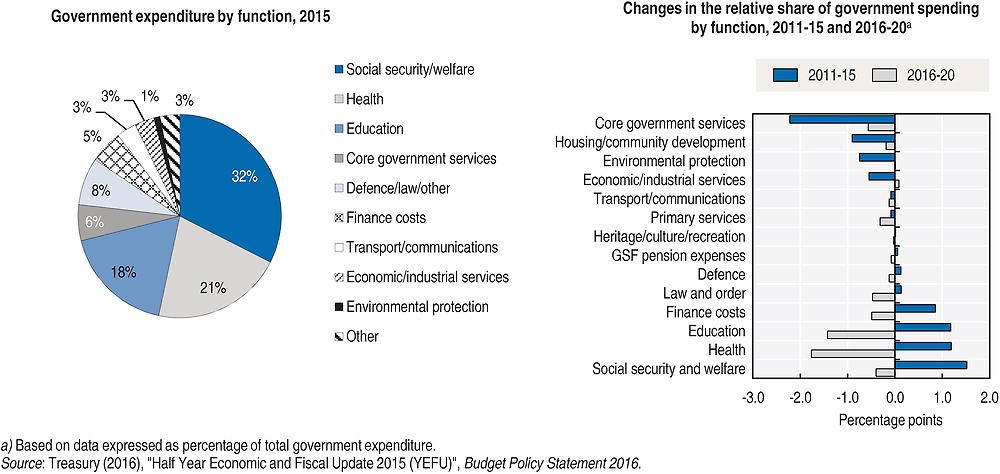

The New Zealand central government generally plays a dominant role in public finance, but its budget for environmental protection is modest compared to other expenditure categories. It carried out nearly 90% of total public spending in 2013, without substantial variations since 2007. This is second only to Ireland and twice the OECD average. In the same year, central government investment accounted for nearly 19% of total investment, among the highest shares in the OECD. In 2015, the budget for environmental protection activities represented about 1% of central government expenditure. In the framework of its fiscal consolidation efforts (Indicator 3.1), the government has cut back on several expenditure items, including environmental protection (Figure 3.8).

As in many other OECD member countries, local governments have major responsibilities in providing environment-related infrastructure and services, which account for a large share of their expenditure. In 2015, local governments spent 14% of their budgets on water supply and sanitation, 13% on public transport and 4% each on waste management and general environmental protection (Figure 5.10). At the same time, local governments have limited fiscal autonomy; revenue sources are largely limited to property taxes (Figure 5.8). Many local authorities identify lack of funding as a significant barrier to expand and upgrade infrastructure, including as it relates to the environment (NZPC, 2016).

Capital spending on infrastructure has increased considerably since 2000 (OECD, 2015a). Yet the quality of infrastructure is perceived to be low relative to local expectations. Firms surveyed continue to report an inadequate supply of infrastructure as the most important barrier to doing business (World Economic Forum, 2015). Large investment is still needed in transport infrastructure to meet the growing demand of good and passenger transport (Indicator 5.2). Growing urban populations have exerted increasing pressures on water supply and wastewater treatment infrastructure (Chapter 5).

Given the central government’s fiscal consolidation objective and the limited resources of local authorities, meeting these infrastructure needs will require diversifying funding sources (OECD, 2015a). Local and national roads could make greater use of tolls, and public-private partnerships could make more efficient use of resources (Indicator 5.2). As Chapter 5 discusses, there is scope to expand the use of water supply and wastewater charges to better cover the costs of these services and provide incentives to use water more efficiently. Legislation, however, limits the ability of local authorities to introduce volumetric wastewater charges (based on volume of water used or discharged).

5.1. Investing in renewable energy and energy efficiency

Investment in renewables has increased in recent years, without the need for any direct subsidies or public support; geothermal, hydro and wind are cost-competitive. IEA (forthcoming) considers this performance a world-class success story. New Zealand has already one of the highest shares of renewables in its energy mix among OECD member countries. Renewable sources (mainly hydro) supply 80% of its electricity (Chapter 1), and the government aims to bring this share to 90% by 2025. Taking into account projected growth in power demand, current renewable generation levels would need to increase by about 20%. Renewable energy potential is largely sufficient to achieve the target, if the current hydropower generation is maintained. However, hydro resources are vulnerable to droughts, and their long-term availability is uncertain due to climate change and water quality concerns. At the same time, as IEA (forthcoming) notes, growing shares of variable renewable resources (i.e. wind and solar power) may affect the operational security of the power system and require adjustments in the electricity market rules.

There is scope to improve energy efficiency, as the energy intensity of the economy has remained broadly stable since 2000 at levels well above the OECD average (Chapter 1). New Zealand’s approach to energy efficiency has changed from direct financial support to a greater focus on information and partnerships. The NZ ETS has not provided sufficient incentives for investing in renewables and energy efficiency. It is also not clear how much further market forces can improve efficiency. A comprehensive package of policy measures is needed to complement the NZ ETS carbon pricing and address non-pricing barriers to investing in low-carbon energy sources and adopting energy efficient technology in industry, transport and buildings. This will have multiple environmental, energy security and health benefits.

Energy efficiency in buildings

New Zealand has taken action to address the relatively poor energy performance of the building stock through public funding, local tax incentives, awareness-raising and voluntary labelling (Box 3.4). In 2009-16, the flagship Warm Up New Zealand programmes (“Heat Smart” and “Healthy Homes”) provided subsidies to households for improving house insulation and heating systems (with an overall budget of about NZD 420 million). In 2016, “Healthy Homes” was extended for two years to support insulation of rental properties occupied by low-income tenants with priority health needs related to cold and damp housing; it targets about 20 000 homes for insulation. As of 2016, the Warm Up programmes had contributed to retrofit nearly 300 000 homes (or nearly 20% of the housing stock), about half of which were occupied by low-income households. However, these programmes have not leveraged private sector funding or encouraged households to refurbish beyond simple ceiling insulation and heating retrofits. About 2 500 homes were retrofitted at their owners’ expense using voluntary targeted rates (VTR), i.e. adding the energy efficiency refurbishment costs to their rates bill (property taxes) and paying it off over a certain period of time (often ten years).

Despite progress, an estimated 30% of the housing stock remains uninsulated. The 2016 Residential Tenancies Amendment Act introduced stricter floor and roof insulation requirements for rented homes and social housing. Additional measures may be needed to encourage insulation in the untreated homes not covered by the legislation; the Building Code is below the standards required in many other OECD member countries (IEA, forthcoming) and local regulation cannot go beyond the code requirements (NZPC, 2015). The authorities should consider strengthening the standards for newly built homes under the Building Code, while minimising the risk of delaying needed growth in the housing stock (Chapter 5). They could also introduce stricter emission and efficiency requirements and more systematic control procedures for wood heating appliances, as part of the ongoing review of the National Environmental Standard on Air Quality; wood burning provides over 10% of residential heat, but is a major source of air pollution (Chapter 1; IEA, forthcoming). Additional measures (e.g. grants, subsidies and tax credits) may also be needed to provide landlords with incentives to take up more efficient heating systems, draught proofing, ventilation and moisture prevention, particularly for rentals to low-income households.

New Zealand operates three voluntary rating tools for sustainable buildings (Box 3.4). To improve the environmental performance of buildings, energy performance ratings could be made mandatory for large public buildings, and be further rolled out across the commercial and industrial sectors over time. This approach, adopted in many other OECD member countries, would encourage the housing market to factor energy efficiency into property prices (IEA, forthcoming). Ratings could be extended (or complemented) to include other sustainability dimensions such as water efficiency, waste or indoor environmental quality, building on existing voluntary rating initiatives.

-

NABERSNZ is an energy efficiency rating tool for office buildings, which New Zealand adapted from the National Australian Built Environment Rating System (NABERS) model. While the tool is mandatory throughout Australia, it is voluntary in New Zealand. It is licensed to New Zealand’s Energy Efficiency and Conservation Authority (EECA) and is administered by the non-governmental New Zealand Green Building Council (NZGBC). Trained assessors carry out ratings.

-

Home Star is an independent, voluntary rating tool for the sustainability performance of residential buildings. It awards points across seven categories: energy, health and comfort; water; waste; materials; site; home management; and an optional innovation category. So far, agreements are in place for 700 certifications across New Zealand and 16 000 completed self-assessments online. Homes that are designed and built to meet the Building Code standard typically rate 3 or 4 on the Home Star rating scale (out of 10 for best-performing buildings).

-

Green Star is a sustainability rating tool for non-residential buildings, including offices, industrial and education buildings, hospitals and libraries. It awards points across nine categories: energy, water, materials, indoor environment quality, transport, land use and ecology, management, emissions and innovation. So far, about 100 certifications have been delivered across New Zealand.

Source: NZGBC (2015, 2014).

5.2. Investing in low-carbon transport modes

The transport sector is the largest final energy user and the second largest source of GHG emissions (Figure 1.8). Motor vehicles are the primary transport mode for both goods and passengers, reflecting New Zealand’s dispersed population, a history of low-density urban development and insufficient development of alternative transport modes (Chapter 1). While the use of public transport has increased, it remains limited: households made less than 5% of their trips in public transport over 2012-14 (Figure 5.4). Road freight has continued to increase; it is projected to increase by around 48% over the next 30 years (in tonne-kilometres), in particular around the Auckland region (Ministry of Transport, 2014). This will likely put considerable pressure on the existing road network and on the environment.

Investment in land transport infrastructure is significant, but heavily tilted towards roads. It amounted to around 1.3% of GDP in 2012-15; the authorities plan to spend around 1.5% of GDP annually on land transport infrastructure over the next decade. However, public transport would receive only about 11%. This is a moderately higher share than in 2012-15, when 9% of the National Land Transport Fund (NLTF) was invested in public transport systems and 1% in cycling and walking infrastructure; 78% went to highways and local roads (Government of New Zealand, 2015c; NZTA, 2015). Additional investments in road infrastructure will be needed to meet increasing demand. However, further developing the rail urban public transport system, improving service quality and supply of bus services, and accelerating the roll-out of electric vehicles (see below) could provide other options for commuters, reduce road congestion and help lower GHG emissions. New Zealand should ensure investment priorities for land transport infrastructure, and the related financing model, are consistent with long-term climate and environmental objectives.

While local governments are responsible for providing part of transport infrastructure and services in their regions, funding of transport investment is highly centralised. Resources come from the NLTF, which is mostly fed by the revenue of road fuel and vehicle taxes (Indicator 3.2). The funding mechanism favours state highways and can discourage municipalities to invest in local roads or public transport. This is because the NLTF fully finances state highways – which are therefore virtually free for local governments – but only funds about half the cost of urban, suburban and rural roads and of public transport. As the Parliamentary Commissioner for the Environment noted, asking councils to co-finance even a small share of state highways could encourage councils to better consider alternative options, including public transport (PCE, 2016).

Giving a more prominent role to local governments in infrastructure investment and maintenance would require increasing their accountability and resources, as local fiscal autonomy remains limited (Indicator 3.1). Further use of joint public procurement procedures and additional private investor participation, e.g. through public-private partnerships (PPPs) in local infrastructure provision could lead to higher investment efficiency (NZPC, 2016; OECD, 2015d). Many local governments lack in-house capacity to conduct large complex projects; setting-up standardised procurement specifications would ease local collaborations and allow local authorities to share the costs, as well as best practices (Hodges, Proctor and King, 2013). PPPs should be carefully designed to avoid cost overruns, limit renegotiation risks and contain future fiscal liabilities; they should be systematically subject to ex post assessment (OECD, 2015d). Funding of national and local infrastructure should aim to recover the full costs of the investment, maintenance, use and associated environmental and social impacts to ensure competitive neutrality between transport modes. Road pricing could help place a cost on travel during peak periods and encourage more carpooling and use of public transport (Indicator 3.2; Chapter 5). In areas poorly serviced by public transport, or where concerns over equity arise, transfers could provide a partial offset of the charges. However, legislation restricts the application of road pricing to new roads where an alternative toll-free route is available.

Electric vehicles

With its large share of renewable electricity, New Zealand can use EVs to mitigate transport-related GHG emissions and reduce reliance on imported oil. Most car owners in New Zealand have access to off-street parking and park their vehicles overnight at private homes. This allows good charging possibilities, even in the absence of an extensive public charging infrastructure system. Commuters also travel relatively short distances, suitable for EVs with limited driving range (IEA, forthcoming). Nonetheless, so far the uptake of EVs in New Zealand has been very limited (around 2 000 vehicles in 2016) and growing slowly; the main barriers have been the high capital costs of the vehicles, limited availability of EV models, insufficient awareness and consumer confidence in the EV technology, and a lack of widespread public charging infrastructure (Ministry of Transport, 2016).

In mid-2016, the government launched the Electric Vehicle Programme to address these barriers. The programme aims at doubling the EV fleet every year until 2021. It foresees exempting EVs from the road user charge until they make up 2% of the light vehicle fleet. Further, the programme plans information campaigns, access to bus lanes and high-occupancy vehicle lanes on the highways and local roads, and investment in research and development (R&D) for low-emission vehicles. These measures will provide users with some incentive to switch to EVs, but their widespread adoption in the short term is unlikely without some additional policy measures. Experience from other countries suggests that fuel efficiency and emission standards are effective in encouraging the uptake of cleaner vehicles (IEA, forthcoming), but New Zealand is one of few OECD member countries without such standards. The central and local governments should lead by example and commit to purchase EVs for a proportion of their own fleets, which would provide a strong signal to the transport industry and public. More advanced options such as full electric car sharing service could be piloted. New Zealand will also need to adapt its electricity distribution system and develop the necessary charging infrastructure for accelerating the mass rollout of EVs (IEA, forthcoming).

6. Promoting eco-innovation

New Zealand has a well-developed innovation system and a sound skills base. In line with an increased emphasis on innovation as a driver of economic growth, public investment in science and innovation has increased by 60% since 2007-08. However, gross domestic expenditure on R&D has remained low at about 1.2% of GDP, about half the OECD average. Public institutions, largely universities and Crown research institutes, conduct most of the R&D. This is linked to New Zealand’s economic structure, with a large base of small and medium-sized enterprises and its remote geographic location. Distance from world markets presents an ongoing challenge to scaling-up innovative businesses and it also affects integration into global science and innovation networks. Despite close co-operation between industry and public research, the number of patents is relatively small and commercialisation of public research results could be improved (OECD, 2014b).

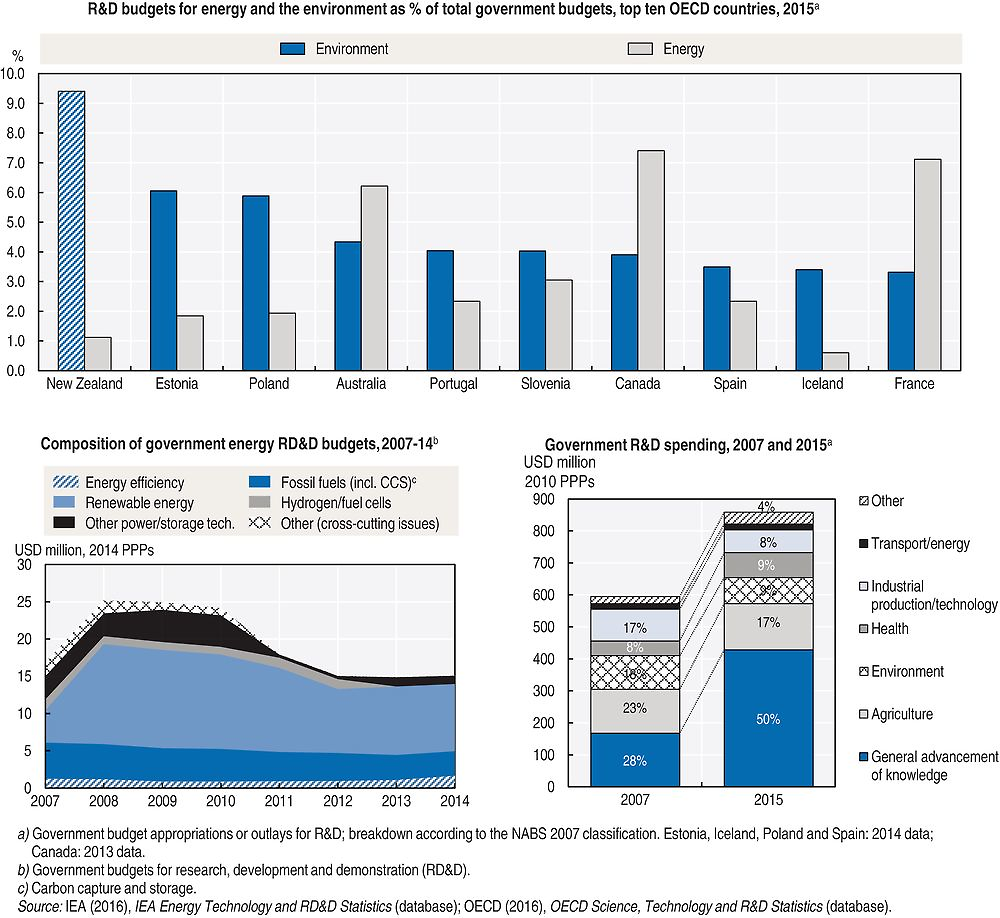

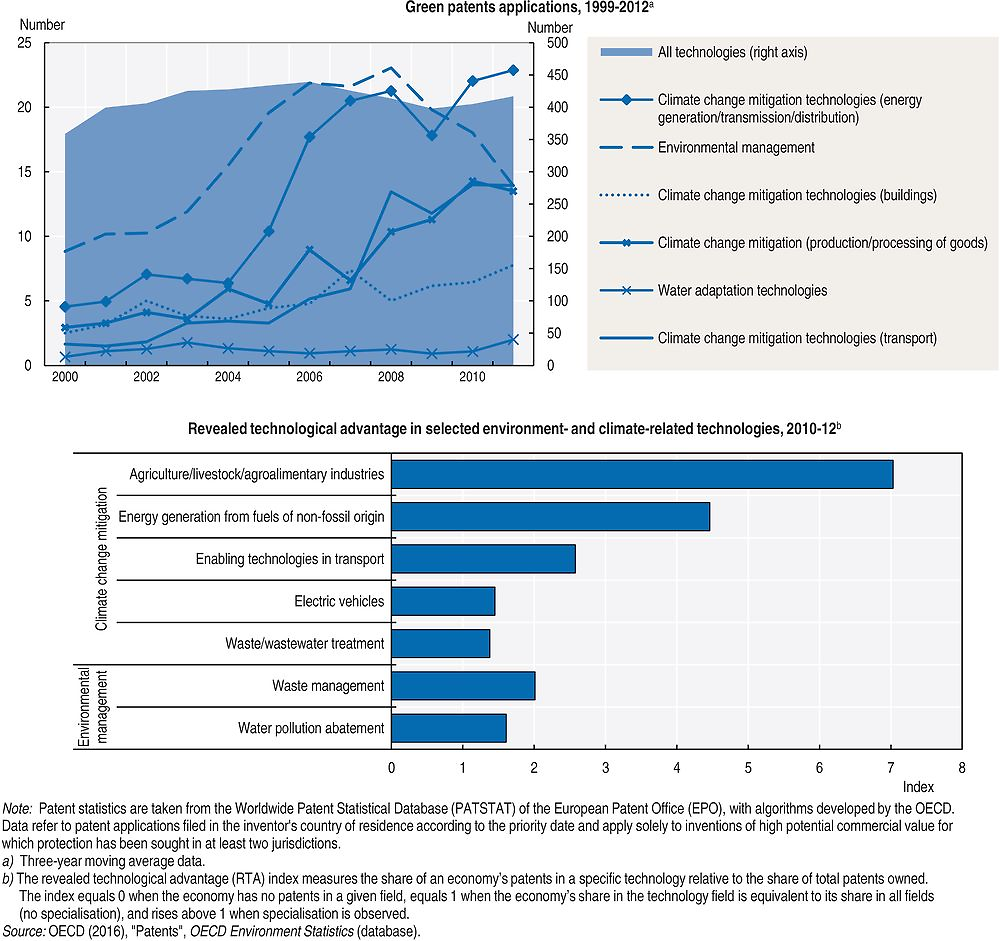

The government is the main source of funding for environmental research. Environment-related R&D accounts for nearly 10% of government R&D outlays. This is the highest share in the OECD, but it has declined from about 18% in 2007 (Figure 3.9). The share of the total energy research, development and demonstration (RD&D) budget dedicated to renewables and energy efficiency has progressively increased; it exceeded 70% in 2014, though funding for energy R&D remains overall limited to around 1% of public R&D spending (Figure 3.9). Increased R&D funding has contributed to a steady rise in patent applications related to environmental management and climate-change mitigation technologies (Figure 3.10). The latter is a trend observed in many other countries and driven by global climate mitigation commitments. Overall, environment- and climate-related technologies made up for nearly 12% of all patent applications in 2010-12, in line with the OECD average and more than three times the level in 2000.

New Zealand has developed a specialisation and competitive advantage in some technology (OECD, 2014b),25 including water pollution abatement, wastewater and waste treatment, and renewable energy generation (Figure 3.10). It is a world leader in research related to reducing the environmental impact from agriculture, primarily on GHG emissions and water quality. New Zealand led the establishment of the Global Research Alliance on Agricultural Greenhouse Gases, which groups 46 countries and fosters international co‐operation and investment in research into mitigating GHG emissions from food production. The government, in co-operation with the business sector, has launched several initiatives to support agriculture-related R&D and commercialisation of research results (Box 3.5). Partly as a result of these policy and investment efforts, New Zealand has consolidated its technology specialisation and competitive advantage in climate change mitigation technology in the agriculture and food industry (Figure 3.10), as well as in biotechnologies,26 which is second only to Denmark (OECD, 2015e).

The Pastoral Greenhouse Gas Research Consortium (PGGRC) is a partnership, formed in 2003, between the government, the dairy and fertiliser industries, and research organisations. It has invested about NZD 5 million per year in research on mitigation solutions for GHGs from pastoral agriculture (e.g. microbiology, genomics, animal nutrition, genetics and farm systems), with the ultimate goal of decreasing on-farm GHG emissions by 1.5% per year over business-as-usual. A significant area of investment for the PGGRC has been a three-year trial of nitrification inhibitors. The PGGRC works closely with the New Zealand Agricultural GHG Research Centre.

The Primary Growth Partnership (PGP) programme, launched in 2009, is a government-industry partnership that invests in research and innovation programmes to boost agricultural productivity and sustainability. Investments cover the whole of the value chain, from R&D to product commercialisation and technology transfer. PGP programmes are up to seven years in length and industry contributions must be at least equal to Crown funding. As of end-2015, the total PGP funding commitment from government and industry in these programmes was around NZD 724 million (USD 505 million).

The New Zealand Agricultural GHG Research Centre (NZAGRC), established in 2010, is a partnership between the PGGRC and leading New Zealand organisations engaged in research on agricultural GHG emissions. The centre is fully funded through the PGP, which has invested about NZD 48.5 million in the centre over ten years. The NZAGRC is a “virtual” centre: researchers carry out the work from within their own organisations.

Pastoral Genomics is an industry-led research partnership between the dairy, meat and animal feed industries and research organisations. It aims to provide pastoral farmers with better forage cultivars with improved nutritional content and higher resilience to drought and disease, while increasing productivity, profitability and environmental sustainability of New Zealand’s pastoral farming systems. The partnership intends to use non-regulated biotechnologies. Available funding includes NZD 7.3 million (USD 5.1 million) of government funding over five years; industry will match this funding. Investment in the partnership is expected to ultimately increase the value of exports of pastoral farms and contribute to the Business Growth Agenda goal of increasing the ratio of exports to GDP.

Source: OECD (2016e, 2013b).

The innovation policy increasingly focuses on environment-related research and innovation as a way to improve the natural resource base of the economy. The Conservation and Environment Science Roadmap, under development in 2016, aims to set future research priorities in these domains. The environment is among the key research sectors of the National Statement of Science Investment (NSSI), which identifies priorities for the government’s investment in research and innovation in 2015-25. The NSSI has partially shifted research funding from budget allocations for research institutions to contestable funding open to all institutions and science fields. In this way, it aims to improve efficiency of R&D spending and support impact-driven science. In particular, 5 of the 11 “science challenges” included in the National Science Challenges initiative, launched in 2013, relate to the environment and natural resources. The initiative pledges to invest over NZD 350 million in ten years to support public research on emerging and complex issues for New Zealand’s future development, drawing scientists and stakeholders together across different institutions and science fields.

Implementation of this innovation and research strategy remains challenging, in particular for energy and environmental R&D. The research funding system is fragmented across institutions and support programmes, and entails relatively high administration and transaction costs. For example, the funding of the Crown research institutes is partly uncertain. Its dependence on competitions for funding can negatively affect researchers’ career development, acquisition of specific skills and retention of human resources for science and technology. Moreover, the bidding process is time consuming and tends to increase the upfront costs of research projects. There are concerns that this may penalise environmental research, which has generally fewer market applications and has, therefore, less tangible impact. In addition, the economic efficiency of the environment-related innovation policy and its contribution on ultimately improving environmental performance, resource productivity and energy efficiency are not systematically evaluated.

7. Contributing to the global sustainable development agenda

7.1. Progress towards the Sustainable Development Goals

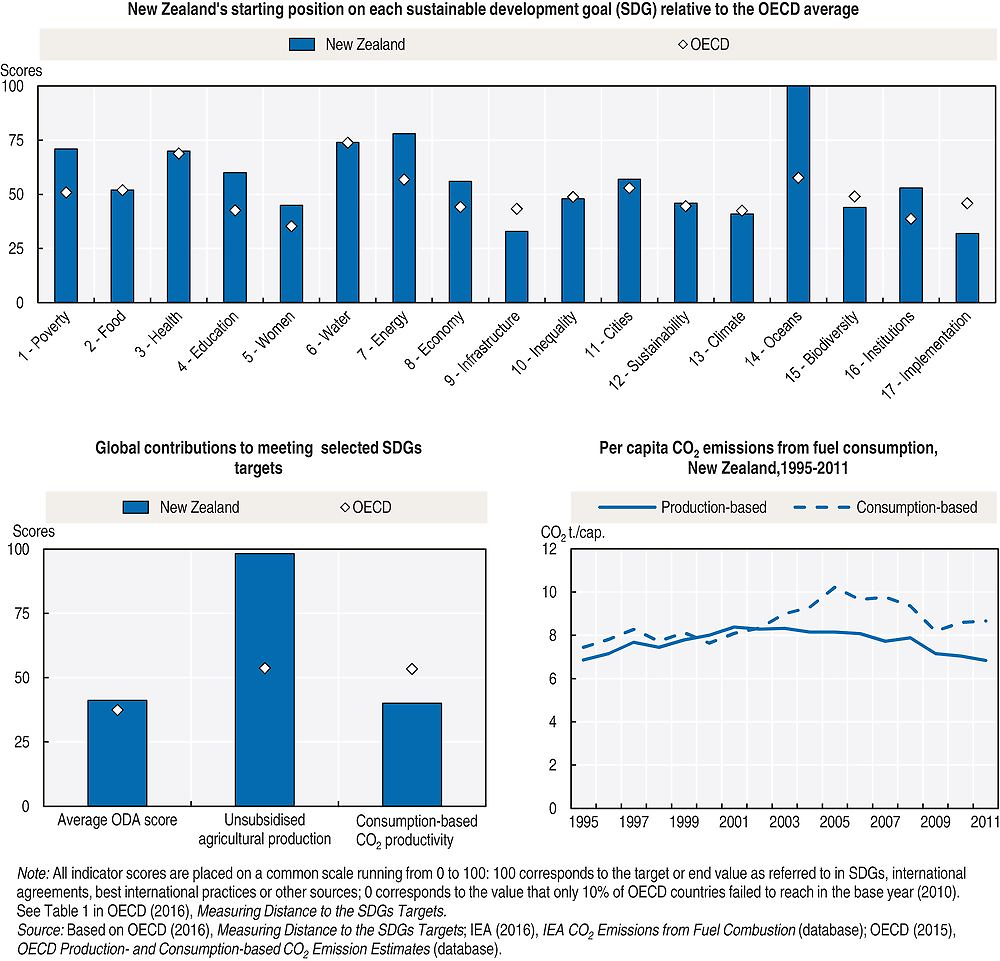

New Zealand is committed to contributing to sustainable development on a global level. In 2015, it participated in the adoption of the 2030 Agenda for Sustainable Development and of its 17 Sustainable Development Goals (SDGs) by the United Nations.27 According to the Augmented SDG Index for OECD countries developed by Sachs et al. (2016), New Zealand ranks 16th among OECD member countries for its performance towards these internationally agreed objectives in the economic, environmental and social sphere.