Chapter 2. Environmental cost-benefit analysis: Foundations, stages and evolving issues

The rationale for and foundations of environmental CBA are well known but nevertheless provide a logical starting point. In summary, these are that: benefits are defined as increases in human well-being (or “utility”) and costs are defined as reductions in that well-being; for a project or policy to qualify on cost-benefit grounds, its social benefits must exceed its social costs. The geographical boundary for considering these costs and benefits is usually the nation but this can readily be extended to wider limits. Aggregating benefits across different social groups or nations can involve summing willingness to pay or to accept (WTP, WTA) regardless of the circumstances of the beneficiaries or losers (or it can involve giving higher weights to disadvantaged or low-income groups). Aggregating over time involves discounting where discounted future benefits and costs are known as present values. Much of the rest of this volume can be understood as developments to this standard practice with the emphasis on environmental CBA.

2.1. Introduction: Why use CBA?

The primary aim in this volume is to describe recent developments in CBA, with an emphasis on those developments relevant to the environment as well as illustrate their applications. Those developments, of course, need to be placed within a context of what the foundations of CBA are (i.e. to establish more exactly what it is that these developments add). It is also instructive to rehearse why it is that economists tend to favour CBA (not unanimously, however).

The aim and structure of this chapter is, as a result, threefold with its structure in reverse order to the points made above. That is: why use CBA? (the remainder of this introduction); what is CBA? (Section 2.2); and, what emerges in this volume about developments in CBA pertaining to environmental applications (Section 2.3).

Starting with the question of “why use?”, arguments for and against CBA have been well rehearsed elsewhere (for critiques see, for example, Sagoff, 1988 and 2004; Heinzerling and Ackerman, 2004. See also Pearce, 2001 for some of the sources of controversy). Often lost in those critical discussions are the reasons why economists broadly agree on favouring CBA.

The first reason for using CBA is that it provides a model of rationality. Independently of its use of money measures of gain and loss, of which this volume has plenty to say later, CBA forces the decision-maker to look at who the beneficiaries and losers are in both the spatial and temporal dimensions. It avoids what might be called “lexical” thinking, whereby decisions are made on the basis of the impacts on a single goal or single group of people. For example, policies might be decided on the basis of human health alone, rather than on the basis of health and ecosystem effects together. CBA’s insistence on all gains and losses of “utility” or “well-being” being counted means that it forces the wider view on decision-makers.1 In this respect, CBA belongs to a group of approaches to policy analysis which do the same thing. Related to this, while it is often ignored in practice, properly executed CBA should show the costs and benefits accruing to different social groups of beneficiaries and losers. But the point remains, these groups should refer to all, not just a single subset of people.

Second, CBA is clear in its requirement that any policy or project should be seen as one of a series of options. Hence, setting out the alternatives for achieving the chosen goal is a fundamental prerequisite of CBA. Again, this feature is shared by some other policy analysis procedures, but not all. A more distinctive element of CBA, however, is that it has the capacity to determine the optimal scale of the policy, following an appraisal of these options. This would be where net benefits are maximised. The ability to do this rests on expressing benefits and costs in the same units (which for convenience is typically money values). In the same vein, CBA offers a rule for deciding if anything at all should be chosen, unlike other approaches which can decide only between alternatives to do something.

Third, CBA is explicit that time needs to be accounted for in a rigorous way. This is done through the process of discounting. This rightly remains controversial, but it is impossible not to discount – or to (in one way or another) decide how impacts in the future, including the very distant future, should be regarded compared to present impacts. Note that the treatment of time in other decision-making guidance is far from clear. But failing to discount means using a discount rate of 0% which means that USD 1 of gain 100 years from now is treated as being of equal value to USD 1 of gain now. Zero is a real number. But it is true that what the “correct” real number is, continues to be debated and that debate is reflected amply in this volume.

Fourth, CBA is explicit that it is individuals’ preferences that count. To this extent, CBA is “democratic”, but some see this as a weakness rather than a strength since it implies that preferences should count, however badly informed the holders of those preferences might be. They also argue that there are two kinds of preference, those made out of an individual’s self-interest and those made when the individual expresses a preference as a citizen. There are clearly pros and cons to the underlying value judgement in CBA, namely that preferences count.

Finally, CBA seeks explicit preferences rather than implicit ones. To this extent, CBA looks directly for what people want, although it does so in a variety of ways as environmental applications make clear. All decisions, however they are made, imply preferences and all decisions imply money values. If a decision to choose Policy X over Policy Y is made, and X costs USD 150 million and Y costs USD 100 million, then it follows that the expected benefits of X must exceed the benefits of Y by at least USD 50 million. The unavoidability of money values was pointed out some time ago by Thomas (1963). It may be that leaving decisions to reveal implicit values is better than seeking those values explicitly. But CBA is clear in favouring the latter.

2.2. Basic stages of a CBA

In this section, the basic stages of a CBA are reviewed. This might be viewed as a CBA of any investment project or policy, although where relevant, issues relating to environmental applications are briefly mentioned too. It is also important to bear in mind that CBA has a long-established (albeit much debated) theory from economics as the foundations of such practical steps. This theory is briefly reviewed in Box 1 below and in Annex 2.A1. Subsequent chapters, however, will explore theory a little further in relation to developments in environmental CBA.

2.2.1. Opening questions

While it may seem obvious, the first and fundamentally most important issue to be addressed in practical CBA is what question is being asked. Typically an analysis begins by considering the set of options that are available and so the first question is: what are the options under consideration? Hopefully there is some reasonably defined goal, although there are likely to be different ways of reaching any given target. Options can be sifted into feasible and non-feasible ones, and other issues, such as the political factors driving the policy, will also tend to limit the options. An option that is often ignored is when to commence the policy (or project). This option should be considered whatever the policy or project in question, but also this can be important in the presence of particular characteristics surrounding the policy decision.

The next question that is likely to arise is: should action X be undertaken at all? An action here might refer to policies or to projects (investments) and usually this question will be asked ex ante. That is, determining whether something that has not yet been done should be done. But it could also be asked ex post. That is, finding out whether something that has been done (or perhaps is in the process of being done) should have been done. The reason for asking the question ex ante is to find out whether what are often significant sums of money should be spent in the public interest. The rationale for asking the same question ex post is that, while it cannot reverse expenditure already made, it can (a) cast light on the accuracy of the ex ante answer, or (b) cast light on whatever decision rule was used to justify the policy or project. In both cases, the answer ex post is designed to assist the process of learning about what does and what does not contribute to overall social well-being.

As to whether the answer to this question is “yes” depends on whether the present value of expected (ex ante) benefits exceeds expected costs, and “no” if expected costs exceed benefits. Note that all this assumes that CBA is either the relevant decision-guiding criterion or is one of the relevant criteria. In what follows, it will be assumed that CBA is always relevant. In making this assumption, the relevance of other factors – political, ethical and so on – is also pertinent given that in reality, of course, these factors will often influence decisions. But CBA is there as a check on those decisions, so it is always sensible to carry out a CBA wherever practicable.

2.2.2. Who counts?

The issue of “who counts” in a CBA is known as the issue of “standing”. Benefits and costs are summed across individuals in accordance with the aggregation rule which defines “society” as the sum of all individuals. There are no hard and fast rules for defining the boundaries of the sum of individuals. Typically, CBA studies work with national boundaries so that “society” is equated with the sum of all individuals in (i.e. residents of) a nation state. But there will be cases where the boundaries need to be set more widely.

Examples that illustrate this are especially relevant to environmental applications of CBA. Benefits and costs to non-nationals should be included if a) the proposal relates to an international context in which there are legal obligations, such as a formal treaty of some kind (acid rain, climate change and so on), or b) there is some accepted ethical reason for counting benefits and costs to non-nationals. Generally speaking, while there are no hard and fast rules, if the well-being of people in country B matters as much to country A as the well-being of A’s own residents, then these should be considered in the CBA regardless of to whom they accrue.

In such cases, a CBA of some proposed action might appear in a two-part form. The first part would show the net benefits to that country alone of that action. The second part would show, for example, the same costs but the benefits would be shown as those accruing both to the country in question and all other countries that benefit from the action being evaluated.

2.2.3. Valuing costs and benefits

The basic decision-rule for accepting (or recommending) a project or policy is that its benefits outweigh its costs. This deceptively simple rule presupposes a number of critical steps: not least having a numerical basis for comparing benefits and costs. This is a distinctive feature of CBA (and related economic tools) and involves assigning money values to impacts of a project or policy. In what follows, the main details of this procedure are sketched out. Annex 2.A2 makes this more precise in spelling out the details of these valuation concepts.

A benefit or gain in an individual’s well-being (utility or welfare) can be measured by the maximum amount of goods or services – or money income (or wealth) – that he or she would be willing to give up or forego in order to obtain the change. Specifically, this could be written as WTPG as the willingness-to-pay of “gainers” from some proposal (G refers to gainers).

Alternatively, if the change reduces well-being, it could be measured by WTPL. This means that costs are measured by the willingness to pay to avoid the cost (L refers to losers). This is not the only way of measuring these costs. If the “losers” from the project or policy have legitimate property rights to what they lose, then WTP should be replaced by willingness-to-accept (i.e. WTAL).

The difference, then, is that losses are measured by WTA and not by WTP. It is observed later that WTA can differ significantly from WTP. Until a few decades ago, the assumption (based on what it is expected in theory) would have been that the difference between these two measures of change in well-being would be very small and so of no practical policy relevance. But empirical estimation of these magnitudes has tended to show that they do vary, sometimes significantly, and with WTA > WTP. If so, the choice of WTA or WTP could matter substantially for CBA (see Chapter 4).

The more familiar form of WTPG and WTPL (or WTA) simply speaks of benefits and costs. Clearly, benefits refer to the value of the categories of goods and service that a proposal produces. And these policy (or project) costs, in turn, will consist of a number of components. This might include “compliance costs” – falling on the business sector and on households – and “regulatory costs”, where relevant, accruing to government in implementing the policy. These are opportunity costs of committing resources to some current action rather than an alternative. This action may impose damage costs on losers too: for example, this could be the case if there was a negative impact on the provision of some environmental good or service.

Inflation: The values of benefits and costs are (or need to be) in real money terms. What this means is that any effects of inflation (a rise in the general level of prices) are netted out and so values are comparable from year to year. This means that a base year issue arises with the usual procedure being to value all costs and benefits at the prices ruling in the year of the appraisal. But it is perfectly possible to change the year prices to confirm with some other rule, e.g. in order to compare the results of one study with another study.

Relative price changes: A relative price change is different again. What this says is that some benefits and costs attract a higher valuation over time relative to the general level of prices. This might be because the benefit or cost in question is simply valued more at higher incomes. To use the terminology, it has a positive income elasticity of willingness-to-pay, such that when incomes (e.g. per capita) increase WTP also increases, with the magnitude of that latter change depending on the boost to income and estimated size of the elasticity. Annex 2.A1 shows in more detail how this is accounted for. This is not the only reason for rising (or falling) relative valuation in a CBA. For example, if a good is becoming scarcer, then its marginal value (relative to other goods) might be relatively higher as its availability dwindles. Typically, for this to happen other characteristics of the good will be important. This could include limitations for substituting it for other goods. However, these characteristics might be particularly important to consider in environmental applications.

2.2.4. Discounting costs and benefits

Costs and benefits will accrue over time and the general rule will be that future costs and benefits are weighted so that a unit of benefit or cost in the future has a lower weight than the same unit of benefit or cost now. This temporal weight is known as the discount factor and this is written:

[2.1]

[2.1]

where DFt means the discount factor, or weight in period t, and σ is the discount rate. As long as projects and policies are being evaluated from society’s point of view, s is a social discount rate. The rationales for discounting are given in Chapter 8.

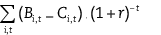

In terms of discounting the flow of benefits and costs, this can be written as:

[2.2]

[2.2]

The issue arises of how far into the future these impacts should be estimated. Yet again, there are no hard and fast rules. In its formative years, when CBA was confined to assessing the worth of investment projects, the rule was that the time horizon – the point beyond which costs and benefits are not estimated – was set by the physical or economic life of the investment. For infrastructure such as roads, ports, water supply and treatment, etc., this was usually set at a minimum of 30 years and a maximum of 50 years. Such rules applied even to longer-lived assets, e.g. housing developments which might last over 100 years. The transition to the CBA of policies has made this rule less compelling because it is unclear how long the effects of policies last. This becomes even more crucial an issue as CBA intrudes upon policy questions which have explicitly long-term goals

2.2.5. Risk and uncertainty

Benefits and costs will not be known with certainty. While conventions vary, it seems fair to distinguish “risk” from “uncertainty” in clarifying what this means and its implications for CBA. A risk context is one where benefits or costs (or both) are not known with certainty, but a probability distribution is known. Sometimes these probability distributions can be very crude. On some occasions they can be sophisticated. A context of uncertainty is different. There is no known probability distribution. End points might be known, i.e. it is known or expected that the value cannot be less than a number, and that it cannot be more than another number. But, in other cases, there may be pure uncertainty in the sense that “anything may happen”.

The fact that uncertainty characterises CBA will be nothing new to cost-benefit practitioners. Indeed, various procedures for dealing with risk and uncertainty are long-standing. These vary in terms of justification in theory and analytical practicalities. For risk, this includes expected value or expected utility approaches with corresponding assumptions (respectively) about whether the decision-maker are risk-neutral or risk-adverse.2,3 If the context is one of uncertainty, i.e. the distribution of benefits (costs) is not known, then, at the very least, CBA requires that a sensitivity analysis is performed. Sensitivity analysis requires that the CBA is computed using different values of the parameters about which there is uncertainty. Such procedures require some assumption about likely minima and maxima, but do not necessarily make assumptions about the distribution of values between these limits. For example, if a discount rate of 4% is chosen as the central case, then, say, 2 and 6% could also be chosen for a sensitivity analysis. One possible outcome is that the sign of the net benefits will be unaffected by these alternatives, in which case the analysis is said to be “robust” with respect to these assumptions. In other cases, changing assumptions may alter the CBA result. If so, then some judgement has to be made about the reasonableness of the chosen values.

2.2.6. Decision rules

In [2.2] benefits and costs are discounted so that when summed over time the resulting magnitude is known as a present value (PV). A present value is simply the sum of all the discounted future values. [2.2] might therefore be written very conveniently as:

[2.3]

[2.3]

The correct criterion for reducing benefits and costs to a unique value is the present value criterion. The correct rule is to adopt any project with positive NPVs and to rank projects by their NPVs. When budget constraints exist, however, the criteria become more complex. Single-period constraints – such as capital shortages – can be dealt with by a benefit-cost ratio (BCR) ranking procedure. That is, rank projects according to their BCR and recommend projects in that queue until the capital constraint binds. In other respects, the benefit-cost ratio has less generally to commend it as a decision rule for choosing projects.

There is broad agreement among economists that the internal rate of return (IRR) should not be used to rank and select mutually exclusive projects. Where a project is the only alternative proposal to the status quo, the issue is whether knowing the IRR provides worthwhile additional information. Views differ in this respect. Some argue that there is little merit in calculating a statistic that is either misleading or subservient to the NPV. Others see a role for the IRR in providing a clear signal as regards the sensitivity of a project’s net benefits to the discount rate. Yet, whichever perspective is taken, this does not alter the broad conclusion about the general primacy of the NPV rule.

Ultimately, CBA is a practical tool which can be used to assist in actual policy formulation. But it would be remiss not to stress that it has theoretical foundations, which support the aforementioned practical stages. These can be briefly summarised as:

-

The preferences of individuals are to be taken as the source of value. To say that an individuals’ well-being, welfare or utility is higher in state A than in state B is to say that he/she prefers A to B;

-

Preferences are measured by a willingness-to-pay (WTP) for a benefit and a willingness-to-accept compensation (WTA compensation) for a cost.1

-

It is assumed that individuals’ preferences can be aggregated so that social benefit is simply the sum of all individuals’ benefits and social cost is the sum of all individuals’ costs. Effectively, some degree of cardinalisation of utility is assumed;

-

If beneficiaries from a change can hypothetically compensate the losers from a change, and have some net gains left over, then the basic test that benefits exceed costs is met.

This latter foundation is the Kaldor-Hicks compensation test. This loosened the highly restrictive condition known as the “Pareto condition”, whereby a policy is “good” if at least some people actually gain and no-one actually loses.2 Virtually all real-life contexts involve gainers and losers and the Kaldor-Hicks “compensation principle” established the idea of hypothetical compensation as a practical rule for deciding on policies and projects in these real-life contexts. All that is required is that gainers can compensate losers to achieve a “potential” Pareto improvement. The compensation principle establishes the prima facie rule that benefits (gains in human well-being) should exceed costs (losses in human well-being) for policies and projects to be sanctioned. Hence, the decision rule in equation [2.3].

Underlying all this theory, culminating in the Kaldor-Hicks test, is welfare economics or, more strictly, neoclassical welfare economics. This has always been the subject of significant debate originating from both “inside” and “outside” of the economics profession.3 The “inside” debate, for example, has focused on a number of anomalies that reliance on the “welfarist” underpinning might give rise to. These incongruities mean that perspectives on the cost-benefit case for policy or project options might be held with less confidence, although the practical import of these complications in the theory remains the subject of debate.4 One starting point for “outside” debate (although it may reflect views held by many economists too) is the proposition that the “welfarist” perspective is too narrow a way to judge the “value” to individuals and society of policy actions or projects. Section 2.3.4 discusses the implications of this and the way it might circumscribe the use of (rather than remove the need for) CBA.

← 1. The notions of WTP and WTA can be extended to include WTP to avoid a cost and WTA compensation to forego a benefit.

← 2. Pigou regarded actual payment as being necessary and the task of the economist was to work out how such payments could be made. As noted, however, CBA has proceeded on the basis of saying that if the polluter could compensate the losers and still have a net profit, then the polluting activity passes a cost-benefit test.

← 3. All of this, of course, precedes contemporary CBA. The body of modern-day welfare economics which underlies CBA was established by Hicks (1939, 1943), Kaldor (1939) and others in the 1930s and 1940s with the contribution of Pareto (1848-1923) being presented much earlier in his Cours d’Economie Politique in 1896

← 4. For example, one major strand of criticism relates to what happensto income distribution as a policy or project is implemented. In theory, it could change in such a way that the policy originally sanctioned by the potential compensation principle could also be negated by the same principle – i.e. benefits exceed costs for the policy, but the move back to the original pre-policy state could also be sanctioned by CBA. This is the “Scitovsky paradox” (Scitovsky, 1941). Another problem arising from the fact that policies may change income distributions (and hence relative prices) is the “Boadway paradox” (Boadway, 1974). A possibility is that the policy showing the highest net benefits may not in fact, be the best one to undertake. This led to a search for “escapes” from this type of problem starting with Bergson (1938) and focusing on assuming a “social welfare function” – a rule that declared how aggregate welfare would vary with the set of all individuals’ welfare. This, in turn, led to further conundrums (see, for example, Arrow, 1951). One of these is the problem of finding a social welfare function that might be regarded as a socially “consensus” function – there are many possible functions and no practical prospect of deciding which one to use.

2.3. Recent developments in environmental CBA: Major themes of this volume

While the basic principles of CBA are long-standing, the challenges entailed in applying these principles are constantly evolving. As Chapter 1 emphasised, it is these developments that are the primary focus of this volume. Subsequent chapters set out then a number of important areas of development in more detail. In this section, some of the major themes which emerge from those chapters are identified. In doing so, signposts are provided as to where in the rest of the volume further details and discussion can be found.

2.3.1. Finding money values

At its heart, CBA involves comparing costs and benefits of a given “change” in a common unit, which conventionally are money values, reflecting how much those affected by a project or policy value these changes. It is fair to say that environmental CBA would have very little to say if it were not for several decades of major advances in the various methods which seek to value environmental impacts. As such Chapters 3 to 7 devote a good deal of attention to this progress.

In terms of precepts, this frequently starts with stating that the net sum of all the relevant WTPs and WTAs for a project outcome or policy change defines the total economic value (TEV) of any change in well-being due to a project or policy. TEV can be characterised differently according to the type of economic value arising. It is usual to divide TEV into use and non-use (or passive use) values. Use values relate to actual use of the good in question (e.g. a visit to a national park), planned use (a visit planned in the future) or possible use. Actual and planned uses are fairly obvious concepts, but possible use could also be important since people may be willing to pay to maintain a good in existence in order to preserve the option of using it in the future. Option value thus becomes a form of use value. Non-use value refers to willingness-to-pay to maintain some good in existence even though there is no actual, planned or possible use.

The types of non-use value could be various, but a convenient classification is in terms of a) existence value, b) altruistic value, and c) bequest value. Existence value refers to the WTP to keep a good in existence in a context where the individual expressing the value has no actual or planned use for his/herself or for anyone else. Motivations here could vary and might include having a feeling of concern for the asset itself (e.g. a threatened species) or a “stewardship” motive whereby the “valuer” feels some responsibility for the asset. Altruistic value might arise when the individual is concerned that the good in question should be available to others in the current generation. A bequest value is similar but the concern is that the next and future generations should have the option to make use of the good.

The notion of total economic value (TEV) provides an all-encompassing measure of the economic value of any environmental asset. It decomposes into use and non-use (or passive use) values, and further sub-classifications can be provided if needed. TEV does not encompass other kinds of values, such as intrinsic values which are usually defined as values residing “in” the asset and unrelated to human preferences or even human observation. However, apart from the problems of making the notion of intrinsic value operational, it can be argued that some people’s willingness-to-pay for the conservation of an asset, independently of any use they make of it, is influenced by their own judgements about intrinsic value. This may show up especially in notions of “rights to existence” but also as a form of altruism.

As a practical matter then, techniques of environmental valuation can be seen as measuring (changes in) TEV either in totality or its component parts. There are other (related) ways in which to trace these practical techniques from the economic concepts. For example, one of the contributions of the attention on ecosystem services over the past two decades is the tracing of the implications on how ecosystem services that are supplied by an underlying ecosystem asset (e.g. forest, wetland, agricultural land) – ultimately provide benefits to people and businesses. This is what Freeman et al. (2013) term: “The economic channel through which wellbeing is affected” (p. 13). These channels are manifold (e.g. Brown et al., 2007; Freeman et al., 2013) but broadly speaking can be summarised in three ways.

First, there are ecosystem services which are used as inputs to economic production. Examples include nutrient cycling and pollination resulting in the accumulation of biomass that is an input to agricultural production. Water regulation and water purification services are inputs to those economic (producing) units which need a supply of clean water as an input, perhaps alongside e.g. other factors of production.

Second, ecosystem services can act as joint inputs to household final consumption. That is, there is use of ecosystem services in combination with (or as a substitute for) expenditure on produced goods and services in providing a “product” for consumption. In such cases, an ecosystem service and the market goods or services are complementary (or substitute) inputs, and because of this expenditure on the latter can provide a guide to the value of the former. Examples include nature services which in combination with travel expenditures are used to produce recreation benefits. An example where an ecosystem service is a substitute for market expenditure is air purification services which can substitute for purchase of a produced good which filters air.

Third, ecosystem services can be inputs which directly contribute to household well-being. That is, there is no existing economic production or household consumption where these services are inputs. These services are consumed directly in generating benefits: that is, directly from nature without any other (produced) inputs. Examples here are by their nature rather abstract, but include those services that are valued for reasons of what is usually termed “non-use” or “’passive-use”.

An important use of this way of thinking about ecosystems and benefits is that it maps naturally onto appropriate techniques to value unpriced ecosystem services (Day and Maddison, 2015). Some possibilities are summarised in Table 2.1 for example.

Another important feature of recent ecosystem valuation is the extent to which it has become an interdisciplinary effort. Valuation, of course, often needs to be preceded by quantifying physical impacts. As such a good understanding of the natural science characterising the (change in) provision of an ecosystem is an asset. This need for interdisciplinarity is not restricted to ecosystem assessment, although it has been prominent there (see, for example, MEA, 2006; TEEB, 2010; UK NEA, 2011). Health valuation is just one of many other examples. In this case, what is required is a physical assessment of the response of human health to, say, changes in exposure to air pollutants such as particulate matter (PM), sulphur oxides (SOX) and nitrogen oxides (NOX). These health “end states” – changes in premature mortality, reduced respiratory hospital admissions, reduced “restricted activity days” (days when activity is less than would be the case for normal health), and so on – can be valued using a variety of techniques.

One issue in such applications of CBA – the “correspondence problem”, and a major reason why it can be limited in practical use, is that scientific information on ecosystem change does not correspond to indicators that individuals recognise. The correspondence problem is less important in the context of health so long as health end states can be defined in recognisable units, such as days away from work, or extra days with eye irritation, etc. Nevertheless, the key point is that this interdisciplinarity is not a one-way street. Just as the science is often needed for subsequent robust valuation so too must there be dialogue, for example, to ensure that the former is measuring things which are meaningful for the latter.

2.3.2. Who gains, who loses

The whole history of neoclassical welfare economics has focused on the extent to which the notion of economic efficiency underlying the Kaldor-Hicks compensation test can or should be separated out from the issue of who gains and loses – the distributional incidence of costs and benefits. Of course, equity and efficiency issues are hard to separate and various “schools of thought” have emerged as to what that implies for CBA. Some argue that distributional incidence has nothing to do with CBA: CBA should be confined to “maximising the cake” so there is more to share round according to some morally or politically determined rule of distributional allocation. Others argue that notions of equity and fairness are more engrained in the human psyche than notions of efficiency, so that distribution should be considered as a prior moral principle, with efficiency taking second place. Others might agree with the second school but would argue that precisely because efficiency is “downgraded” in social discourse that is all the more reason to elevate it to a higher level of importance in CBA. Put another way, one can always rely on the political process raising the equity issue, but not the efficiency issue.

Approaches to considering equity in CBA can be seen as following all these different pathways and this is discussed in Chapter 11. The initial perspective, for example, takes the view that the cost-benefit practitioner should leave well alone such issues and so standard CBA is enough to make recommendations. The second view suggests a more proactive approach. One version of this takes account of income or wealth differences. For example, if the inhabitants of B are poor and the inhabitants of A are rich, allowance might be made for the likelihood that USD 1 of gain or loss to a poor person will have higher well-being (utility) than USD 1 of gain or loss to a rich person. This gives rise to one fairly popular form of “equity weighting”.

The final perspective is arguably more ambivalent about what to do. It might stop short of the equity weighting above. One reason for this might be that it is not altogether clear how to weight the money values of benefits and costs by measures of “social deservingness” in this way. If this muddies the waters of a CBA too much then a key strength of this approach arguably is lost. Other ways could be sought to reflect an important consideration. For example, a tabulation of costs and benefits must not only show the aggregate benefits and costs, following the rules outlined above, but should also show who gains and who loses. The “who” here may be different income groups, ethnic groups, geographically located groups and so on. Other forms of distributional incidence concern how benefits and costs might be allocated to business and consumers.

There is a growing interest in why people hold the preferences they do – their motivation – and perhaps in judging some motivations to be acceptable while others are not. Moral notions may also determine human behaviour and if so then arguably such motivations could be encompassed in the CBA framework. Despite the widespread perception of some critics of CBA, there is nothing in the notion of an individual preference that dictates it must always be based on “self-interest” and “greed”.

The consideration of distributional issues is important both for CBA generally but it is especially important for the environment. And it should be noted that such concerns (and moral judgements more broadly) arise in many areas of the environmental CBA. Chapter 14 on climate economics and the role this sub-field has played in advancing understanding in this important area of environmental policy makes clear how ethical issues and judgements are pervasive. This theme is also picked up on in the discussion of discount rates in Chapter 8. Chapter 12 on sustainability and CBA is premised on similar concerns about intergenerational equity, albeit looked at from a somewhat different perspective.

2.3.3. Selecting a discount rate

Discounting is a pervasive issue in economics, and arguably nowhere is this more so than in CBA. Indeed, the choice of the discount rate is one of the most debated issues in CBA. Technically speaking, this is “simply” a case of determining (the rate of change of) the shadow price of a unit of consumption in the future: that is, quantifying how much lower that future consumption is compared with a unit of consumption today. The practice of establishing the price that government should use for social CBA, however, is far from simple and gives rise to long-standing debates. As a practical matter, however, this had led to rather large differences in actual discount rates used across national jurisdictions (as well as organisations including international development agencies), cf. Chapter 16.

Prominent too has been concern about the “tyranny of discounting”: that is, large costs and benefits accruing in the distant future are insignificant in PV terms because the (shadow) price associated with them becomes vanishing small. Contributions within the ambit of environmental CBA – particularly, more broadly, in climate economics – have broken new ground on this enduring concern about tyrannical outcomes. As Chapter 8 makes clear, this had helped shake the conceptual foundations of discounting, in part through novel technical insights but also (and importantly) through renewed debates about ethical underpinnings.

A substantial part of this contemporary discussion has coalesced around the notion of declining discount rates: a contrast, therefore, with the constant rates familiar in CBA and which was the basis for the initial introduction to cost-benefit analysis above, a constant discount rate – i.e. r was the same regardless of which year in the project or policy life cycle is looked at. This has been reflected in much investigation on the rationale for declining discount rates. The unifying themes here have been that uncertainty about the future combined with prudence (caution by societal decision-makers in the face of these risks) generates a schedule of discount rates which decline with time. This uncertainty, for example, might be about economic growth (both its rate and variance) or future interest rates.

As economic ideas go, there appears to have been relatively rapid solidifying of support in the academic literature for declining discount rates as well as adoption by a number of national governments (see, for example, Groom and Hepburn, 2017). Nonetheless, as Chapter 8 discusses, there are other ways of conceptualising the discount rate debate in ways that are highly relevant for environmental CBA. This includes re‐emerging interest in “dual discounting”. What this means is that different discount rates could apply to different classes of commodities. For example, one of these classes might be “environmental” goods. Importantly, if those goods are relatively scarce compared with (other) “consumption” goods and, moreover, if environmental goods have limited substitutability, then they should command a different discount rate. A challenge is to make this operational, and one possible avenue for this (Weikard and Zhu, 2005) is to focus on estimating shadow values for environmental goods which reflect those parameters (growing scarcity and limited substitutability).

2.3.4. Circumscribing CBA: What are the limits?

To what extent does using CBA as a policy formulation tool require that the practitioner or user in effect, subscribes to the “welfarist” theory that typically is evoked to support its application? This is an important question, as for many this underpinning theory is a hard line to swallow. Randall (2014) sets out a number of reasons for discomfort with the theory, which essentially stem from its equating the goodness of an individual life narrowly with the level of preference satisfaction that the individual attains and, in turn, judging what is good for society in terms of the level of preference satisfaction enjoyed by its members.

The point made by Randall is that, as a moral theory to guide decisions, this is incomplete. But his assessment comes with an important corollary in that knowing about changes in welfare is far from irrelevant to making judgements about the merits of policy or project decisions. What this means is that concern about welfare changes becomes one principle – for determining the goodness of actions – and that it exists alongside other moral considerations. These other considerations – which might include (but not be restricted to) intrinsic values as well as the rights and duties of people – act then as potential constraints on welfarist considerations and thus CBA.

On the face of it, it seems hard to disagree with this “plurality” of moral perspectives. Few advocates of CBA argue that this is an exclusive and comprehensive rule, i.e. it is not the only value judgement that is relevant. But once this is admitted, it opens up a debate on when it should be admissible and when it should not. For example, in terms of circumscribing CBA, some might see these constraints “everywhere” and perhaps especially in relation to policy decisions about the environment. Others might see these constraints as at best a special case such that welfarism and CBA “almost always” has primacy. Such divergent standpoints notwithstanding, the “value pluralism” set out in Randall (2014) is at least a basis for subsequent debate about the role of CBA, and for understanding disagreement where it exists. In many ways, this volume can be seen as a contribution to that discussion. On the one hand, it sets out recent developments that are important to consider when CBA can be argued to be relevant to environmental decisions. On the other hand, this volume also reflects on circumstances where constraints seem relevant and as such it considers the practical consequences for how CBA is done.

One prominent example where constraints might bind is in reflecting concern about sustainability (defined in terms of intergenerational equity) in CBA as discussed in Chapter 12. While this might involve how to measure shadow values for (changes in) natural capital, this is very much at the frontier of CBA procedures. Routine valuation may not be possible anytime soon; or perhaps even ever. This might be because analysts believe that individuals are poorly informed about the environment and its importance as a life-support asset. In that case guiding policy with measures of human preference could risk other social goals, even human survival itself.

One reaction to this problem could be to specify sustainability constraints in physical terms. That is, if levels of natural capital needing to be conserved can be established, then this might operate as a constraint on project or policy proposals. CBA then would be required to operate within these constraints. In outcome, this is similar to what would be recommended by those who believe other species have “intrinsic value” which are not amenable to analysis using human preferences (unless humans can be judged to take those rights into account when expressing their own preferences). While some CBA practitioners may be uncomfortable at their hands being tied in this way (Pearce, 1998), arguably this is simply a consequence of the applying the “value plurality” that, for example, is proposed by Randall (2014). That said, there still seems a role for assessing the (opportunity) costs of sustainability constraints, as part of understanding what is sacrificed in observing these limits.

2.3.5. How is CBA actually done (and how to do better)?

While the emphasis of CBA is mostly on its role as a normative tool, a growing number of studies have provided a positive analysis of “when” and “why” CBA is relied upon to formulate actual policy decisions (and when it is not). Some of this literature emanates from economists looking at how their tools are actually used (e.g. Hahn and Tetlock, 2008; Groom and Hepburn, 2017). Equally interesting evidence can be found in studies by non-economists (notably political scientists and policy analysts), although typically this looks at impact assessment more generally rather than CBA per se (see, for a review, OECD, 2015 and Adelle et al., 2012). There is also evidence increasingly being gathered on use and quality of CBA by novel regulatory bodies such as the EU Regulatory Scrutiny Board (see Chapter 17).

This work has sought also to understand at what stage in the policy process this assessment actually takes place (e.g. at the beginning, when establishing potential policy options or is it well after the political decision to do something has been made). Reading the evidence to date provides a sobering moment of reflection for those who believe that CBA is always used, is always done well and is always influential in policy formulation.

This suggests the importance of ultimately placing developments in policy appraisal, including CBA, within a realistic understanding of how the policy formulation process actually works. For example, if CBA was “simply” required as a rationalistic tool to enhance evidence-based policy-making then apparent lack of quality (poorly measured impacts and so on) are straightforwardly shortcomings of those actual applications. Chapter 17 highlights the view that usage of CBA draws on a range of other motivations too. This includes communicative usages, political usage as well as more symbolic roles. The significance is that these different usages can be an effective way of understanding why the quality of actual CBA may fall short (from the perspective of using it purely as a rationalistic tool as most CBA textbooks “assume”).

From the standpoint of what makes good CBA, none of this excuses the shortcomings that have been documented. The point is that a better understanding of what is happening in actual policy formulation allows a more realistic perspective to be crafted about what to do about this. That is, it is not just a case of making further progress at the CBA knowledge frontier, refining established tools (by improving valuation methods) and improving official CBA guidelines. All of that remains important. After all, to the extent that practical CBA is perceived as lacking a robust basis it is presumably less likely to be used and more likely to be dismissed. Nevertheless, this needs to be complemented by thinking about what changes in policy processes such as further institutional infrastructure are needed (of which guidelines are only part).

There are signs of evolving practice within certain jurisdictions, which may move in this direction. Evaluation of CBA used in EU regional policy, and specifically to guide the disbursement of regional funds to infrastructure projects, has combined strengthening of guidelines along with a focus on understanding the incentives that project beneficiaries have in presenting cost-benefit cases and the limited ability of existing institutional processes for scrutinising evidence to align these incentives to what is socially desirable. Such developments reflect a broader trend toward better understanding of the incentives faced by, and the bounded rationality of, policy actors in the CBA process.

Formal organisations are being established too to provide this examination. Examples here are the European Commission’s Regulatory Scrutiny Board and the UK’s Regulatory Policy Committee. Often however these developments seem to be driven by different policy agendas, which are beyond the core mission of the CBA textbook: particularly the deregulation or public management agendas. Nevertheless, such institutional developments, in an expanded role, could also be used to reinforce and strengthen uptake and use of (environmental) CBA in the future.

One final comment seems worth making. There is a possible irony at work here between developments at the CBA frontier and what is needed for policy use. A number of recent developments, while diverse, reflect relatively technical and, increasingly, specialised debates. This specialisation has clearly been crucial to proper and sustained progress on unavoidably complex issues. But it arguably risks less chance of actual uptake unless, for example, these lessons can be easily translated in practical terms (and moreover economic capacity-building is present in decision-making venues). Translating these novel developments into practical approaches is crucial: the example for declining discount rates is apt here.

2.4. Conclusions

The foundations of CBA can be summarised as follows:

-

Benefits are defined as increases in human well-being (utility).

-

Costs are defined as reductions in human well-being.

-

For a project or policy to qualify on cost-benefit grounds, its social benefits must exceed its social costs.

-

The geographical boundary for considering these costs and benefits is usually the nation but this can readily be extended to wider limits.

-

Aggregating benefits across different social groups or nations can involve summing willingness-to-pay or to accept (WTP, WTA) regardless of the circumstances of the beneficiaries or losers, or it can involve giving higher weights to disadvantaged or low-income groups. One rationale for this is that marginal utilities of income will vary, being higher for the low-income groups.

-

Aggregating over time involves discounting. The rationale for discounting is given later. Discounted future benefits and costs are known as present values.

This Chapter has also identified some major themes in the recent development of environmental CBA. Subsequent chapters in this volume explore all of these in much more detail.

References

Adelle, C., A. Jordan and J. Turnpenny (2012), “Proceeding in Parallel or Drifting Apart? A Systematic Review of Policy Appraisal Research Practices”, Environment and Planning C: Government and Policy, Vol. 30, pp. 401-415, https://doi.org/10.1068/c11104.

Arrow, K. (1951), (2nd edition 1963), Social Choice and Individual Values, Wiley, New York.

Boadway, R. (1974), “The welfare foundations of cost-benefit analysis”, Economic Journal, Vol. 84, pp. 926-939.

Brown, T.C., J.C. Bergstrom and J.B. Loomis (2007), “Defining, valuing and providing ecosystem goods and services”, Natural Resources Journal, Vol. 47, pp. 329-376, www.fs.fed.us/rm/value/docs/defining_ valuing_providing_ecosystem_services.pdf.

Brown, G. and D.A. Hagen (2010), “Behavioral economics and the environment”, Environmental and Resource Economics, Vol. 46, pp. 139-146, https://doi.org/10.1007/s10640-010-9357-6.

Camerer, C.F., G. Loewenstein and M. Rabin (2011), Advances in Behavioral Economics, Princeton University Press, USA.

Day, B. and D. Maddison (2015), Improving Cost Benefit Analysis Guidance, Natural Capital Committee, London.

Dunlop, C.A. et al. (2012), “The Many Uses of Regulatory Impact Assessment: A Meta-Analysis of EU and UK Cases”, Regulation and Governance, Vol. 6, pp. 23-45, https://doi.org/10.1111/j.1748-5991.2011.01123.x.

Freeman, A.M. III et al. (2013), The Measurement of Environmental and Resource Values, 3rd edition, Resources for the Future, Washington, DC.

Groom, B. and C. Hepburn (2017), “Looking back at social discount rates: The influence of papers, presentations, political preconditions and personalities on policy”, Review of Environmental Economics and Policy, Vol. 11/2, pp. 336-356, London School of Economics, https://doi.org/10.1093/reep/rex015.

Heinzerling, L. and F. Ackerman (2004) Priceless: On Knowing the Price of Everything and the Value of Nothing, The New York Press, New York.

Hicks, J.R. (1939), “Foundations of welfare economics”, Economic Journal, Vol. 49, pp. 696-712.

Hicks, J.R. (1943), “The four consumer’s surpluses”, Review of Economic Studies, Vol. 11, pp. 31-41.

HM Treasury (2018), The Green Book: Central Government Guidance on Appraisal and Evaluation, HM Treasury, London, www.gov.uk/government/uploads/system/uploads/attachment_data/file/220541/green_book_complete.pdf.

Horowitz, J.K., K.E. McConnell and J.J. Murphy (2008), “Behavioral foundations of environmental economics and valuation”, in List, J. and M. Price (eds.), Handbook on Experimental Economics and the Environment, Edward Elgar, Northampton, MA.

Kaldor, N. (1939), “Welfare propositions of economics and interpersonal comparisons of utility”, Economic Journal, Vol. 49, pp. 549-552.

OECD (2015), Regulatory Policy Outlook, 2015, OECD Publishing, Paris, https://doi.org/10.1787/9789264238770-en.

Pearce, D.W. (2001), “Controversies in economic valuation”, in P. McMahon and D. Moran (eds.), Economic Valuation of Water Resources: Policy and Practice, Terence Dalton, London.

Pigou, A. (1920), The Economics of Welfare, Macmillan, London.

Sagoff, M. (1988), The Economy of the Earth, Cambridge University Press, Cambridge.

Sagoff, M. (2004), Price, Principle and the Environment, Cambridge University Press, Cambridge.

Scitovsky, T. (1941), “A note on welfare propositions in economics”, Review of Economic Studies, Vol. 9, pp. 77-88.

Shafir, E. (ed.) (2013), The Behavioral Foundations of Public Policy, Princeton University Press, New York.

Shogren, J. and L. Taylor, (2008), “On behavioral-environmental economics”, Review of Environmental Economics and Policy, Vol. 2, pp. 26-44, https://doi.org/10.1093/reep/rem027.

TEEB (2010), The Economics of Ecosystems and Biodiversity, Mainstreaming the Economics of Nature, A Synthesis of the Approach, Conclusions and Recommendations of TEEB, Routledge, Oxford, www.teebweb.org/publication/mainstreaming-the-economics-of-nature-a-synthesis-of-the-approach-conclusions-and-recommendations-of-teeb/.

UK National Ecosystem Assessment (2011), The UK National Ecosystem Assessment: Synthesis of the Key Findings, UNEP-WCMC, Cambridge.

Weikard, H.P. and X. Zhu (2005), “Discounting and environmental quality: When should dual rates be used?”, Economic Modelling, Vol. 22, pp. 868-878, https://doi.org/10.1016/j.econmod.2005.06.004.

The table below provides a simple numerical example of the calculation of discounted net benefits. It indicates that what is to be aggregated or summed is the discounted value of benefits and costs, not the absolute values: i.e. the bottom line of Table 2.A1.1.

The minus signs in the table indicate a cost. These costs as well as benefits are measured in current year prices. So to illustrate the procedure for netting out inflation, the table includes a price index which assumes an inflation rate of 3% per year and regards Year 0 (the year the appraisal is being undertaken in) as the base year. Dividing net benefits in current prices by this index computes benefits and costs at constant prices.

The distinction between inflation and discounting should then be clear: the first step is always to ensure that benefits and costs are expressed in constant prices, and it is these magnitudes that are then discounted. The discount factor is computed from equation [2.2], with an assumed discount rate of 5%. The final row shows the discounted net benefits. When these are summed, it will be found that there are positive net benefits of 105.5 which can be compared with the costs of 95.2, i.e. there is a positive net present value (NPV). The example also illustrates the notion of a “base year”, i.e. the year to which future costs and benefits are discounted. In this case there is a year 0 so that costs in year 1 are discounted back to year 0 to obtain the present value of year 1 costs (the first column of numbers). A more usual practice is to set the base year as the one in which the initial costs – usually a capital outlay – occurs. Again, there are no hard and fast rules. Any base year can be chosen, so long as the resulting procedures are consistent.

Rising relative valuations could also be built into this estimation. For the example where relative value is increasing because of rising per capita incomes, this would entail calculating the following in any particular year: (1 + [e × g])t, where e = the income elasticity of willingness-to-pay, i.e. the percentage change in willingness-to-pay arising from a given percentage change in real per capita income and g = the rate of growth in per capita (real) incomes. Evidence would need to be obtained for the likely size of e. But for sake of illustration, assume that the estimated range for the benefit being provided by this simplified example project is around 0.3 to 0.7. For any year t, then, and taking a mid‐estimate of 0.5 for e and a rate of growth of real incomes of, say, 2%, a given benefit in that year needs to be multiplied by: (1 + [0.5 × 0.02])t. If the year is 3 then this means year 4 benefits would be multiplied by 1.04. If the year is 40, then benefits would be multiplied by 1.49. Including relative price changes can therefore make a potentially significant change to the outcome of a CBA.

Consider an individual in an initial state of well-being U0 that he achieves with a money income Y0 and an environmental quality level of E0:

U0 (Y0, E0) [A2.1]

Suppose that there is a proposal to improve environmental quality from E0 to E1. This improvement would increase the individual’s well-being to U1:

U1 (Y0, E1) [A2.2]

One needs to know by how much the well-being of this individual is increased by this improvement in environmental quality, i.e. U1 – U0. Since utility cannot be directly measured, one can seek an indirect measure, namely the maximum amount of income the individual would be willing to pay (WTP) for the change. The individual is hypothesised to be considering two combinations of income and environmental quality that both yield the same level of well-being (U0): one in which his income is reduced and environmental quality is increased, and a second in which his income is not reduced and environmental quality is not increased, i.e.:

U0 (Y0 – WTP, E1) = U0 (Y0, E0) [A2.3]

The WTP of an individual is the point at which these two combinations of income and environmental quality yield equal well-being. At that point WTP is defined as the monetary value of the change in well-being, U1 – U0, resulting from the increase in environmental quality from E0 to E1. This WTP is termed the individual’s compensating variation, and it is measured relative to the initial level of well-being, U0.

An alternative is to ask how much an individual would be willing to accept (WTA) in terms of additional income to forego the improvement in environmental quality and still have the same level of well-being as if environmental quality had been increased. The individual is then considering the combinations of income and environmental quality that yield an equal level of well-being (U1):

U1 (Y0 + WTA, E0) = U1 (Y0, E1) [A2.4]

where WTA is a monetary measure of the value to the individual of the change in well-being (U1 – U0) resulting from the improvement in environmental quality. This is termed the equivalent variation. It is measured relative to the level of well-being after the change, W1. Here the monetary measure of the value of the change in well-being could be infinite if no amount of money could compensate the individual for not experiencing the environmental improvement.

Analogous measures for policy changes that result in losses in well-being can be derived. In this case, the compensating variation is measured by WTA, and the equivalent variation is measured by WTP. Suppose the move from E0 to E1 results in a reduction in the individual’s well-being. Then, the compensating variation is the amount of money the individual would be willing to accept as compensation to let the change occur and still leave him or her as well off as before the change:

U0 (Y0 + WTA, E1) = U0 (Y0, E0) [A2.5]

The required compensation could again, in principle, be infinite if there was no way that money could fully substitute for the loss in environmental quality.

The equivalent variation is the amount of money the individual would be willing to pay to avoid the change:

U1 (Y0 – WTP, E0) = U1 (Y0, E1)... [A2.6]

In this case the equivalent variation measure of the value to the individual of the change in well-being resulting from a deterioration in environmental quality from E0 to E1 is finite and limited by the individual’s income.

Table 2.A2.1 summarises the various measures of welfare gains and losses.

Until a few decades ago, most economists assumed that the difference between compensating and equivalent variation measures of change in well-being would be very small and of no practical policy relevance. That is, for CBA purposes, it mattered little if WTP or WTA was used in either of the relevant contexts (a gain, and a loss). There are theoretical reasons for supposing that WTP and WTA should be very similar. But empirical estimation of these magnitudes has tended to show that they do vary, sometimes significantly, and with WTA > WTP. Depending on one’s view of the evidence that WTA and WTP differ in practice, the choice of WTA or WTP could matter substantially for CBA. Accordingly, this issue is deferred for a fuller discussion in Chapter 4. From the perspective of the current discussion, on CBA, this matters. If losers have a legitimate right to what they lose, then WTA for that impact is the appropriate measure of value.

Notes

← 1. For example, cost-effectiveness analysis (CEA) and multi-criteria analysis (MCA) impose a discipline in terms of defining goals (working out what it is that the policy should achieve) and differentiating costs from indicators of achievement of the goals (see Chapter 18).

← 2. Risk-neutrality means that the decision-maker is indifferent between any two probability distributions each with the same

mean. Yet two distributions could have very different measures of dispersion and still have the same mean. Risk-neutrality

implies that the decision-maker does not care about what may be probabilities that very small returns, or even negative returns,

might be made from the policy or project. Reasons for supposing risk-neutrality is not an unreasonable assumption relate to

the fact that CBA tends to be confined to government decisions. Governments can “pool” the risks of decisions in a number

of ways. If then the context is one where probabilities are known and the decision-maker is risk-neutral, then the appropriate rule is to take the expected value of benefits and costs. Thus if benefit of B1 is thought to occur with probability p1, benefit of B2 occurs with probability of p2, and so on, the expected value of benefits is simply  .

.

← 3. Where the context is one of risk (probabilities known) but the decision-maker is risk-averse, i.e. he or she attachesa higher weight to, say, negative benefits rather than positive benefits, the expected value rule

gives way to an expected utility rule. The same process as before takes place but this time the relevant calculation is:  . The expression shows expected utility and this is most easily thought of as reflecting a set of weights that the decision-maker

attaches to the outcomes. More formally, these weights are embedded in a benefit utility function. Provided some specific form can be given to this function, it is possible to compute what is called the certainty equivalent level of benefit that corresponds to the probabilistic level of benefits. It is this certainty equivalent level that would

be entered into the CBA formula.

. The expression shows expected utility and this is most easily thought of as reflecting a set of weights that the decision-maker

attaches to the outcomes. More formally, these weights are embedded in a benefit utility function. Provided some specific form can be given to this function, it is possible to compute what is called the certainty equivalent level of benefit that corresponds to the probabilistic level of benefits. It is this certainty equivalent level that would

be entered into the CBA formula.