Executive summary

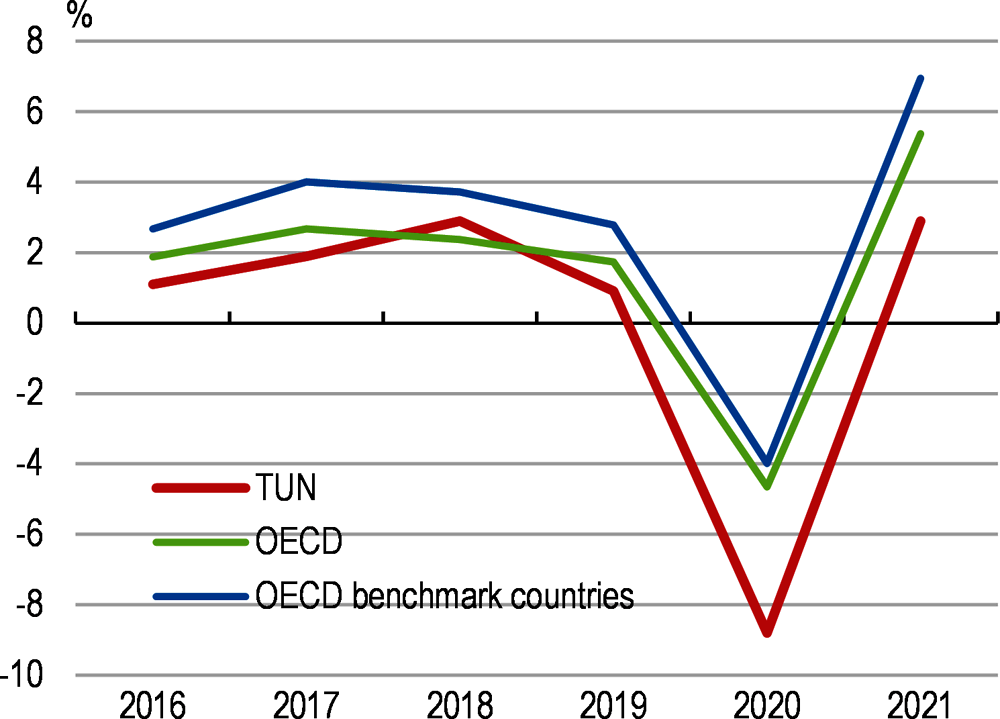

The pandemic hit an economy that was already suffering from low growth (Figure 1). In 2020, activity experienced a severe contraction, despite swift policy interventions, and poverty has increased. The recovery will be sluggish as global growth slows down, domestic demand remains subdued and uncertainty concerning the functioning of political institutions persists. High public debt requires reducing current government spending and complicates monetary policy.

The recession was unprecedented. Most sectors contracted, especially tourism and other labour-intensive services, which were particularly affected by containment measures. Investment plummeted and private consumption shrunk due to income losses. Strong foreign demand for ICT and medical goods and olive oil and rising construction activity only partially compensated. Although tourism receipts plummeted, the current account deficit narrowed thanks to weak import demand and rising remittances from Tunisians living abroad.

The healthcare system is under duress. The COVID-19 outbreak was intense, but vaccination is progressing and the health situation is slowly improving. Migration of health professionals increased and is a cause of concern.

The social fallout is severe. Unemployment has risen from already high levels, with youth disproportionally hit. In the informal sector, workers suffered a severe income shock. School closure and rudimentary distance learning penalised children from low-income households. The number of migrants started growing again.

The recovery will be slow (Table 1), with considerable downside risks. Mobility restrictions hold back the tourism revival and weigh on labour-intensive services. High unemployment dampens private consumption, political uncertainty weighs on the implementation of reforms and investment and weakening external demand holds off the recovery in manufacturing. On the other hand, the commissioning of new fields gives a short-term boost to energy production. Inflation resumed in 2021 and could rise further due to the spike in global commodity prices caused by the Ukraine war. It is crucial to minimise the risk of a price/wage spiral. High commodity prices weigh on the current account and the fiscal deficit, as Tunisia is a net importer of hydrocarbons and cereals and energy subsidies are still high.

The room for fiscal support and much-needed infrastructure investment is constrained by high fiscal deficit and public debt, partly reflecting a large and expanding public wage bill. The deficit-to-GDP ratio has receded slightly from 10.2% in 2020 to 8.2% in 2021. Protecting the most vulnerable and investing in social and physical infrastructures will depend on rebalancing budget outlays and increasing public spending efficiency. Priorities include reining in staffing and pay levels in the public administration, gradually replacing regressive and inefficient energy subsidies with targeted income support for the poor, widening the tax base by eliminating exemptions and special regimes, and improving tax enforcement.

Monetary policy should be on watch to maintain inflation moderate. The central bank cut its policy rate by 150 basis points in 2020 while also injecting liquidity into the money market. It was requested to intervene in support of deficit financing but, going forward, it is important to respect clear boundaries between fiscal and monetary policy.

Public and external debt are high and exacerbate vulnerabilities. Financial stability is put at risk by high public debt in foreign currency. Risk spreads signal a deterioration of creditworthiness. Investor sentiment remains fickle and any sudden deterioration may rapidly trigger a vicious currency depreciation and inflation cycle.

Poverty is rising again. Prior to the COVID crisis, poverty was declining and a sizeable middle class had emerged. Some of these advances have been reverted, as jobs were lost and living conditions deteriorated. Social policies have contained the damage and should be further improved and better targeted, including through the use of digital tools and linking administrative data sources.

Substantial gains can be expected from structural reforms. Model-based simulations show that in a reform scenario – which includes lowering regulatory barriers, raising the quality of institutions and reducing corruption, improving education outcomes and reducing the tax burden on labour – income per capita after 15 years would be 15% higher than in a no-reform scenario. A structural reform plan should be adopted rapidly and be accompanied by an implementation monitoring mechanism.

There are numerous obstacles to competition, due to market reserves for public enterprises, authorisation regimes and tariff and non-tariff barriers that hurt imports, including of capital goods.

SOE reform should be a top priority. The state’s dominant role in many sectors is meant to favour productive transformation, but inefficiencies and high costs mar these efforts. SOEs enjoy market power and favourable financing, but their performance is poor, requiring capital injections and government guarantees on their rising debt that represent a fiscal risk. The creation of a government shareholding agency would bring benefits, provided clear guidelines are established on the scope of state intervention in the economy. Corporate governance should be improved and competitive competence-based procedures be adopted for board and management appointments.

Some progress has been made in removing obstacles to domestic competition, but extra efforts are needed. Authorisation regimes for market entry and a complex tax system discourage entrepreneurship and investment. In the banking sector, low competition and the rising share of loans to the public sector reduce access to finance for private businesses, in particular smaller firms. Competition enforcement should be reinforced. Sectoral regulation is still incomplete and more ambitious anti-graft policies are needed to enhance business integrity.

There is considerable unexploited trade potential. Tunisia has a special regime for export-processing firms. This offshore sector is well-integrated into global value chains and operates in promising sectors, but has few linkages with the domestic economy. Other (onshore) firms are less efficient. Lowering tariffs and non-tariff barriers, especially on inputs and capital goods, would reduce their production costs, facilitate technology adoption and raise productivity and exports.

Comprehensive trade agreements can open new opportunities. Preferential market access is a potential boon for exporters that must be complemented by progress in customs procedures and product quality. More competition from imports can reduce the market power of incumbent firms, lower prices and benefit consumers, particularly poorer ones.

Infrastructures have deteriorated due to insufficient investment, hampering domestic and international market integration. Firms see ports as poor and sea transport as unreliable. Digital infrastructure is relatively weak, in particular in interior regions. Filling infrastructure gaps requires significant financial resources that could be sought from private investors. Air transport is crucial to the development of tourism and existing limitations on the operations of low-cost carriers should be removed.

Abating greenhouse gas emissions and improving waste management are pressing issues. Greenhouse gas emissions increased in the past decade. Renewables still account for a marginal share of electricity generation. Air pollution is a major concern. In view of the importance of tourism and the country's rich natural assets, bolder actions are needed to protect the environment and promote investment in clean energy.

Despite progress in educational attainment, graduates lack the skills demanded by firms and labour market policies complicate the matching process in the labour market.

Unemployment rates have been persistently high, particularly for youth. Rising access to education has increased the supply of high-skilled labour, but the private sector has mainly created jobs in low-skill intensive and low-productivity activities. Unemployment rates are high among tertiary graduates, particularly for women.

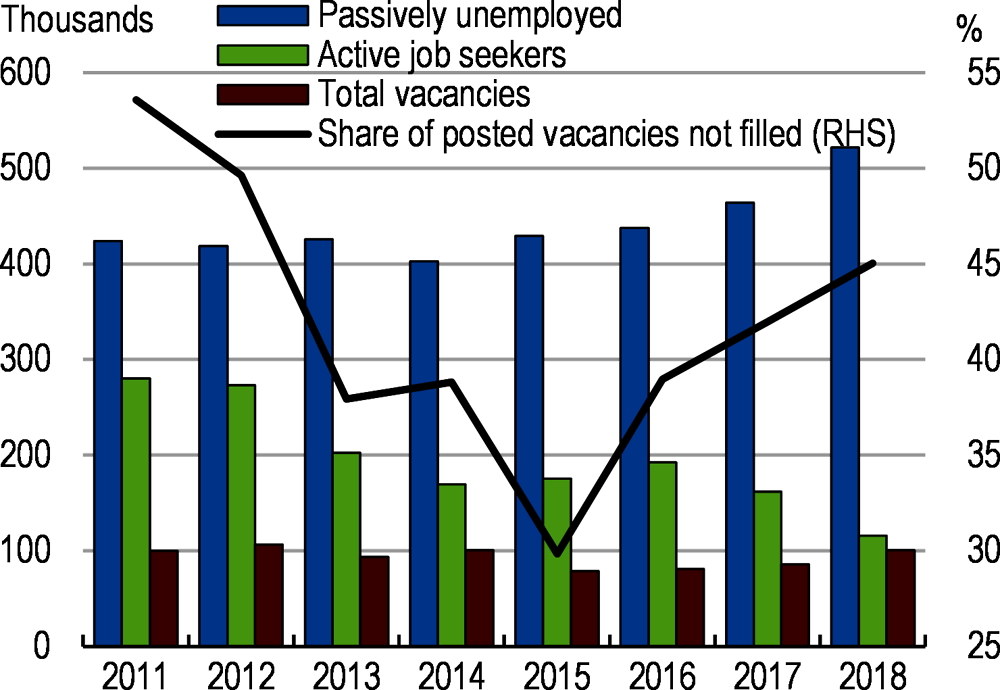

Many firms do not find workers with the skills they need (Figure 2). This is due to the low quality of education and training systems and their weak responsiveness to the skills needs of the private sector. Other factors relate to regional concentration of economic activities combined with low interregional labour mobility, as well as high reservation wages of tertiary graduates who prefer to remain unemployed and wait for better-paid public sector jobs.

Barriers to firm entry and growth discourage the creation of more and better jobs. Raising productivity and formal job creation requires lowering entry barriers and reducing the administrative burden related to authorisation regimes and complex tax incentive and subsidy regimes. Reducing the income tax rate for the lowest-income bracket and allowing for more flexibility in wage setting for smaller firms would raise formalisation.

Although education spending is high, outcomes are relatively poor. Improving teaching quality requires enhancing teacher selection, evaluation and training, providing high-quality language teaching from an early age, and focusing on soft skills. The rising wage bill has reduced resources for investments in education infrastructures. Expanding access to early-childhood education, particularly for low-income and single-parent families, would reduce inequality in opportunities.

Governance of active labour market policies (ALMPs) is highly fragmented, targeting is weak and labour mobility is low. Training subsidies go to firms and only reach formal workers. Wage subsidies reach mainly tertiary graduates. It is key to centralise governance, conduct impact evaluations and extend the coverage of ALMPs to all unemployed and disadvantaged workers. To increase labour mobility and allow for better labour market matching, it is crucial to improve public employment services by allocating more resources to personal counselling services, training counsellors, combining counselling with targeted training support, and allowing for more competition from private providers.