4. Ensuring integrity and accountability in public procurement in the State of Mexico

This chapter analyses the system for ensuring the integrity and accountability of public procurement processes in the State of Mexico, the existing integrity policies and the legal framework to establish how effective they are at mitigating the risk of corruption and managing conflicts of interest during the public procurement cycle. The chapter also discusses the risk management strategies and tools available in the State of Mexico to identify and address corruption and fraud risks and adapt control activities effectively in order to ensure the proper function of the public procurement system. Finally, it assesses the measures implemented to actively engage the private sector and civil society in promoting integrity in public procurement and the courses of action that suppliers can take to challenge procurement decisions during tender procedures and contract execution.

Public procurement is one of the government activities most vulnerable to corruption. In addition to the volume of transactions and the financial interests at stake, corruption risks are exacerbated by the complexity of the process, the close interaction between public servants and businesses, and the multitude of stakeholders.

Various types of corrupt acts may exploit these vulnerabilities, such as embezzlement, undue influence in the needs assessment, bribery of public officials involved in the award process, or fraud in bid evaluations, invoices or contract obligations. In many OECD countries, significant corruption risks arise from conflicts of interest in decision-making, which may distort the allocation of resources through public procurement. Moreover, bid rigging and cartelism may further undermine the procurement process (OECD, 2016[1]).

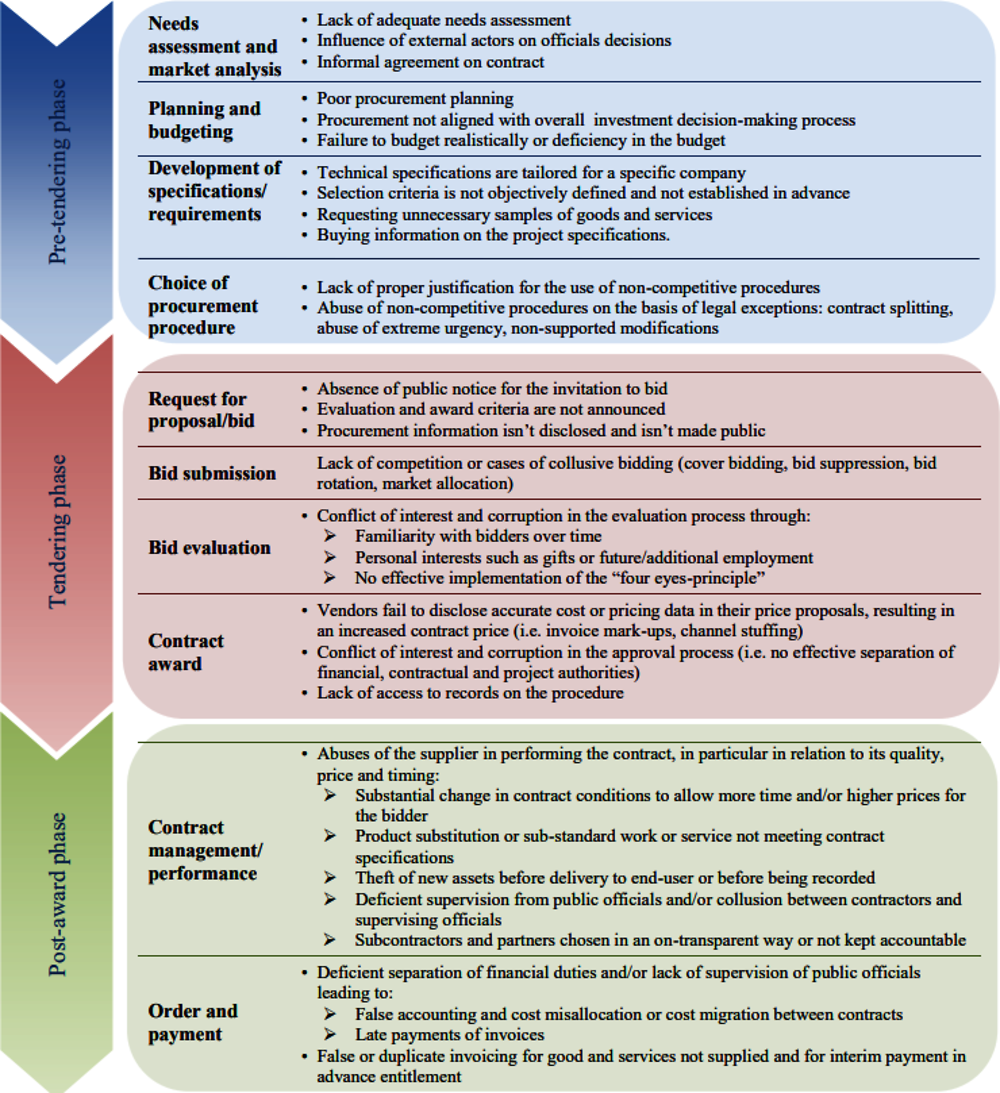

Integrity risks affect all stages of the procurement cycle, as they exert different kinds of pressure at every step – from needs assessment to execution, contract management and evaluation (see Figure 4.1).

Source: (OECD, 2016[1]).

Corruption in public procurement can both occur at the national and subnational levels. On the one hand, decentralisation may narrow the scope for corruption, in line with the assumption that politicians and public servants at local levels are more accountable to the citizens they serve. Voters may be better able to discern the quality of their leadership and the results they deliver. Likewise, local politicians and civil servants can be more in touch with specific needs and contexts of their constituencies. However, greater opportunities and fewer obstacles to corruption may be at play at the subnational level, due to weaker governance capacity (through for example less developed auditing functions, limited legal expertise or low IT capacity) or closer community contacts between public officials and business representatives (OECD, 2016[1]).

In fact, previous OECD public procurement reviews in Mexico’s federal states (i.e., Nuevo León and Sonora) found many opportunities to further integrity and internal control in public procurement. For example, while integrity policies and frameworks have been adopted by many federal states, very few guidelines and tools have been specifically developed for procurement officials. State governments are often unaware of the integrity risks present in public procurement and hence lack the tools to map such risks and apply mitigation measures. Issues such as conflicts of interest have been further regulated but the implementation of such rules is work in progress and still has to demonstrate effectiveness in preventing misbehaviour.

This chapter analyses the State of Mexico integrity policies and the legal framework it applies to public procurement operations. The chapter highlights recent developments and emphasises areas where further efforts are needed. Specifically, it discusses ethics frameworks, corruption risk mapping, disclosures and management of conflicts of interest, as well as integrity training and awareness programmes. It also addresses the key role of the private sector in these issues and the importance of making extensive the integrity standards to all stakeholders in the procurement cycle. Finally, the chapter assesses these issues against the key principles of the OECD Recommendation on Public Procurement (OECD, 2015[2]) and the initiatives taken in the context of establishing the anti-corruption system of the State of Mexico (Sistema Anticorrupción del Estado de México y Municipios, SAEMM).

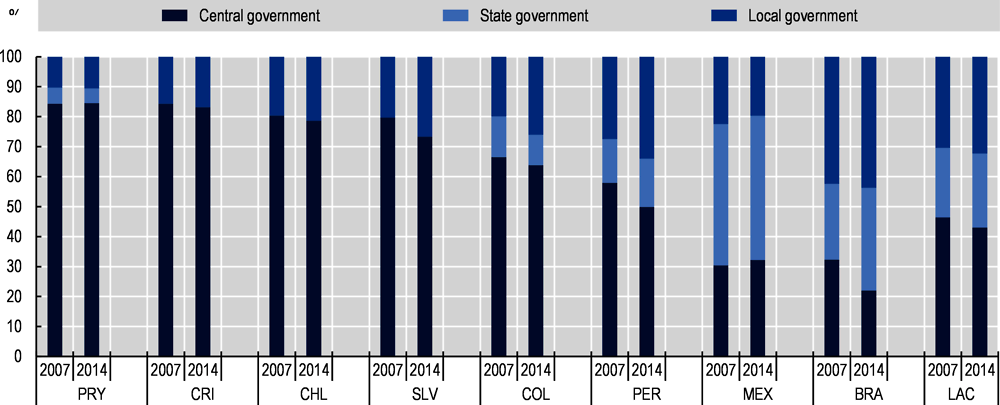

In Mexico, public procurement represents 5.2% of GDP and 70% of this activity is carried out at the sub-national level, as described in Figure 4.2. Public procurement activities in the State of Mexico accounted for nearly MXN 71 968 million in 2019, which represents 24.7% of the expenditures budget of the state. Spending on public procurement in the State of Mexico is concentrated in the areas of health, public safety, social development, and education, as illustrated in Table 4.1.

Source: (OECD, 2017[3]), "Share of general government procurement by level of government, 2007 and 2014", in Public procurement, OECD Publishing, Paris, https://doi.org/10.1787/9789264265554-graph110-en.

The OECD Recommendation on Public Procurement highlights the importance of safeguarding integrity in the public procurement system.

The Council:

III. RECOMMENDS that Adherents preserve the integrity of the public procurement system through general standards and procurement-specific safeguards.

To this end, Adherents should:

i. Require high standards of integrity for all stakeholders in the procurement cycle. Standards embodied in integrity frameworks or codes of conduct applicable to public sector employees (such as on managing conflict of interest, disclosure of information or other standards of professional behaviour) could be expanded (e.g. through integrity pacts).

ii. Implement general public sector integrity tools and tailor them to the specific risks of the procurement cycle as necessary (e.g. the heightened risks involved in public-private interaction and fiduciary responsibility in public procurement)

iii. Develop integrity training programmes for the procurement workforce, both public and private, to raise awareness about integrity risks, such as corruption, fraud, collusion and discrimination, develop knowledge on ways to counter these risks and foster a culture of integrity to prevent corruption.

iv. Develop requirements for internal controls, compliance measures and anticorruption programmes for suppliers, including appropriate monitoring. Public procurement contracts should contain “no corruption” warranties and measures should be implemented to verify the truthfulness of suppliers’ warranties that they have not and will not engage in corruption in connection with the contract. Such programmes should also require appropriate supply-chain transparency to fight corruption in subcontracts, and integrity training requirements for supplier personnel.

Source: (OECD, 2015[2]).

Maintaining the integrity of the procurement system requires, amongst others, the following features:

Procurement procedures are transparent, and promote fair and equal treatment of bidders;

public resources linked to public procurement are used in accordance with intended purposes;

procurement officials’ behaviour is in line with the public purpose of their organisations; and

systems are in place to challenge procurement decisions, ensure accountability and promote public scrutiny (OECD, 2018[4]).

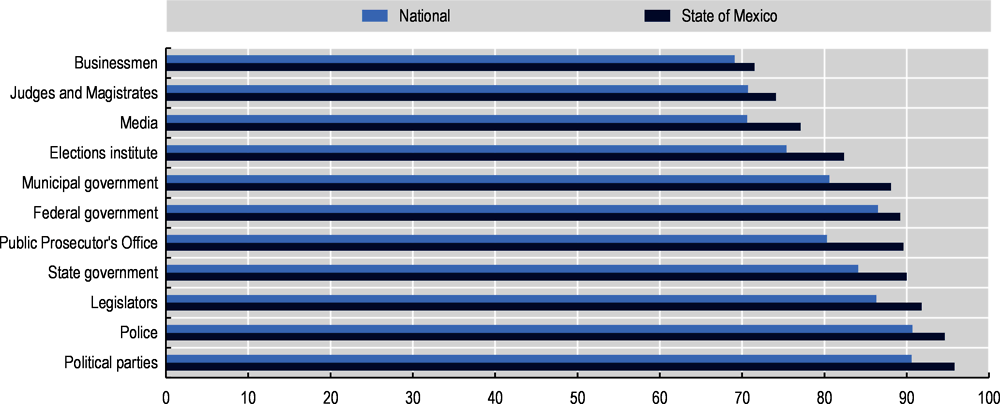

Safeguarding integrity has been a major concern for the public in the State of Mexico for some time. According to a survey published by the National Statistics and Geography Institute (Instituto Nacional de Estadística y Geografía, INEGI) in 2017, corruption was identified by 57.5% of the state population as the second major problem, just behind public safety and crime (78.6%). A high percentage of citizens perceive that corruption is taking place in the state. In fact, the percentage of citizens who report government corruption is frequent or very frequent in the State of Mexico surpassed the percentage of citizens who perceived corruption as frequent or very frequent at the national level in Mexico (93.4% vs 91.1%), as shown in Figure 4.3.

Source: (INEGI, 2017[5]).

The results of a survey on government quality by INEGI in 2017 show that corruption of political parties, police, legislators, and the state government are the main integrity problems perceived by citizens (see Figure 4.4).

Source: (INEGI, 2017[5]).

In this context and in compliance of the Constitution, the General Law on the National Anticorruption System and the General Law of Administrative Responsibilities, the State of Mexico was one of the first federal entities to set up a local anticorruption system, aligned with the one established at the national level in May 2015.

The State Development Plan 2017-2023 establishes four pillars (social, economic, territorial, and public safety) and three horizontal axis (gender equality, capable and responsible government, and connectivity and technology for good government). The axis on capable and responsible government identifies five elements to develop: i) Greater transparency and permanent accountability; ii) preventing and fighting corruption through the effective operation of the SAEMM; iii) good governance based on dialogue and social peace; iv) balanced public finances; and v) public management by results and permanent evaluation.

Objective 5.5 of the axis on capable and responsible government consists of promoting transparent and accountable government institutions. Strategy 5.5.5 refers specifically to public procurement: Ensuring that state government institutions comply with transparency regulations relative to procurement and contracts.

Objective 5.6 mandates the implementation of the SAEMM, which mirrors the reforms establishing the National Anti-corruption System (Sistema Nacional Anticorrupción, NACS). The NACS was approved at the federal level in May 2015 through the publication of a decree modifying several articles of the Mexican Constitution, the enactment of the General Law of the National Anti-Corruption System and seven secondary laws. On 30 May 2017, the State of Mexico government published in its Official Gazette (Periódico Oficial “Gaceta del Gobierno”) the Law of the SAEMM. The SAEMM sets out the principles, general basis, public policies, and procedures to co-ordinate state and municipal authorities in preventing, detecting and punishing administrative offences and acts of corruption, as well as auditing, controlling public resources, transparency and accountability, in line with the NACS.

4.1.1. The State of Mexico, through collaboration of the relevant institutions, could balance the rules-based approach of some provisions by recognising the limits of excessive controls and prompting ethical reasoning by procurement officials

Under the policy framework described above, the State of Mexico developed rules and tools to advance ethics in the public service. Firstly, the Law of Administrative Responsibilities for the State of Mexico and its Municipalities was aligned with the national framework to regulate administrative responsibilities of public servants, namely with the General Law for Administrative Responsibilities (Ley General de Responsabilidades Administrativas, LGRA). Subsequently, on 2 April 2019, the Code of ethics for public officials of the executive power and auxiliary bodies was published. Previously, on 23 September 2015, in compliance with the Law of Administrative Responsibilities for the State of Mexico and its Municipalities, the State Executive issued the Protocol for public servants intervening in public procurement or granting licenses, permits, authorisations or concessions (hereafter, “the Protocol”).

The Code of Ethics establishes fifteen principles to be followed by all public servants: legality, honesty, loyalty, impartiality, efficiency, economy, discipline, professionalism, objectivity, transparency, accountability, merit-based competition, effectiveness, integrity, and equality. Likewise, it dictates the values to be observed by public servants of the state administration: public interest, respect, consideration of human rights, non-discrimination, gender equality, cultural and environmental preservation, co-operation, and leadership. In Chapter IV, Rules of Integrity, Article 8 establishes that state ministries and auxiliary bodies should incorporate rules of integrity, within their attributions on public conduct, public information, procurement, licences, permits, authorisations, concessions, government programmes, services, human resources, real estate management, evaluation, internal control, administrative procedure, permanent performance with integrity, co-operation with integrity and adequate behaviour.

While these principles, values and rules are applicable for all public servants, Integrity Rules in codes of conduct refer specifically to public officials managing procurement, licenses, permits or concessions. It mandates that public servants performing such activities should behave transparently, legally and impartially, guiding their decisions by the interests of society and ensuring the best conditions to fulfil the state responsibilities. It provides examples of how this mandate is broken:

Failing to declare potential conflicts of interest and business transactions with businesses or individuals listed in the Registry of suppliers and service providers of the Government of the State of Mexico.

Failing to apply the principle of equity and fair competition that should prevail in procurement procedures.

Asking for prerequisites different from those strictly necessary to provide public services, leading to excessive and unnecessary costs.

Establishing conditions in the calls for tender leading to an advantage or differentiated treatment for bidders.

Favouring bidders by accepting their compliance with tendering requirements when there is really lack of compliance, simulating compliance or allowing compliance out of time.

Favouring suppliers relative to their compliance with the requisites for requests for quotes.

Unduly disclosing information about bidders participating in a procurement process.

Being partial in the selection, award, withdrawal or cancellation of a contract stemming from a procurement procedure.

Influencing the decisions by public servants to favour a particular bidder in procurement procedures.

Failing to apply fines to bidders, suppliers and contractors that infringe regulations.

Sending e-mails to bidders, suppliers or contractors from personal accounts instead of institutional ones.

Meeting bidders, suppliers or contractors outside of institutional premises, except for onsite inspections.

Failing to comply with the Protocol when interacting with the private sector.

Receiving, directly or through relatives up to the fourth grade, government contracts from the entity in which one works.

Hiring advisory or professional services with individuals or organisations in which one has a personal interest or participation, or with relatives up to the fourth grade.

The Protocol aims to establish general guidelines that should be observed by procurement officials in their interactions with private individuals and companies to prevent corruption and ensure that public decision-making is not taken captive by private interests. It is applicable to all procurement officials registered in the Information System of Public Servants of the State of Mexico (Sistema Informático de Registro de Servidores Públicos del Estado de México, SIRESPEM), managed by the Ministry of Control (Secretaría de la Contraloría, SECOGEM). Indeed, SECOGEM, through its internal control bodies (Órganos Internos de Control, OIC) deployed in ministries and auxiliary bodies of the state public administration, is responsible of monitoring compliance, while both the Ministry of Finance and SECOGEM are responsible for its implementation. The protocol follows a similar instrument implemented at the federal level and published in the Official Gazette on 20 August 2015. Such a federal instrument was assessed by OECD in a previous review (OECD, 2017[6]) and, indeed, the State of Mexico protocol replicates many of its shortcomings.

Some of the main rules established in the protocol are the following:

Contact with private individuals and companies by public institutions should take place only through public officials. During procurement procedures, there will be no personal interactions, except for those necessary to carry out the process, as established by law.

If public procurement officials become aware of wrongdoing by other public servants or private individuals or companies, they should report it to the OIC.

During procurement procedures, bidders will submit a statement (manifiesto) disclosing their business, personal, or family relationships, as well as potential conflicts of interest, with senior public servants (Governor, ministers, legal counsellor, attorney general, deputy ministers, heads of unit, etc.) and those intervening in procurement procedures, including their wives, partners, and relatives up to the second degree.

Contact with private individuals and companies should only take place in official premises and through official means, preferably, in written form (paper-based or electronically). In case of phone calls or meetings, the conversations will be taped or videotaped, so the public official will inform beforehand that the conversation will be recorded.

In the case of meetings, they should be agreed previously and the public official should inform his boss. At least two procurement officials should be present in the meeting and the OIC should appoint one of its officials to participate as well. At the end of the meeting, the minutes will describe the contents of the discussions and it will be signed by the participants.

Procurement officials will abstain from sharing information regarding deliberative processes, analyses and assessments, until a resolution is formally issued.

In addition to the elements mentioned above, the Ministry of Finance, which serves as a centralised purchasing body, issued its own Code of Conduct, published on 30 August 2019. This code dictates the principles and values to be observed by the ministry’s officials and builds on the mandate of the Agreement of the executive to issue the Ethics Code for Public Officials of the State of Mexico, and the Guide to develop codes of conduct and integrity rules in the ministries and auxiliary bodies of the State of Mexico. It includes specific provisions on the responsibility and expected behaviours of procurement officials.

While the Protocol addresses some of the main risks of interactions between procurement officials and the private sector, it has weaknesses that may hamper its potential to achieve the intended effect (i.e., positively influencing the behaviour of public servants) and may even be counterproductive. In fact, the Protocol would benefit from a more balanced approach between rules and values, as there is a limit to what can be achieved from traditional controls and sanctions. The Protocol is rules-based, minimising a more values-based approach which could lead to negative consequences for motivation and commitment of public servants under the belief that they are intrinsically considered as corrupt.

Public integrity refers to the consistent alignment of, and adherence to, shared values, principles and norms for upholding and prioritising the public interest in the public sector. Fostering integrity therefore relates to encouraging desired behaviour over undesired behaviour, including – but not limited to – corrupt practices. Several approaches can be taken to promote these desired behaviours, including a compliance/rules-based approach and a values-based approach. A compliance-based approach includes attention to prevention through establishing enforceable standards, often in laws, regulations, and codes of conduct, as well as providing education, training, and counselling on these standards. This approach ultimately provides for a range of enforcement mechanisms based on the severity of the misconduct. A values-based approach aims to inspire integrity through raising awareness of ethics, public-sector values, and the public interest, and adherence to codes of ethics or guiding principles.

International experiences show that integrity policies are most successful when these two approaches are combined and well balanced, with the exact relative importance, as well as the actual shape of both approaches, depending on the social, political and administrative context and on the history of the organisation concerned. After interviewing government stakeholders, this review finds that a better balance must be struck in the State of Mexico to create a “culture of integrity”, shifting away from an overwhelming rules-based approach.

Source: (OECD, 2017[6]).

The protocol also states the rules which are easy to evade or hard to enforce. For example, recording conversations between public servants and private individuals or companies could be avoided by having them in person and off site, which in itself is also forbidden. Even the requirement to favour written communications can be averted through informal communications. Likewise, the requirement to have two procurement officials and an OIC representative in meetings does not fully impede the possibility of colluding to benefit a particular bidder in response to a bribe. In other words, rules in themselves are not enough to hinder corrupt behaviour. However, they should be complemented by raising awareness of public servants and private representatives about the importance of integrity in public decision-making and service delivery and by the interiorisation of public service values.

Mexico as a country, including its federal entities, suffers the consequences of previous integrity failures in the form of excessive formal controls, which hinder flexibility and innovation in the public service. As documented in previous OECD reviews (see, for example, (OECD, 2018[7]), this leads to procurement officials worrying more about compliance with regulations than generating value for money. The tone and content of the Protocol reinforces the idea that public servants are inherently corrupt and should be distrusted. Too many controls may damage intrinsic motivations to behave ethically, such as commitment to the public interest or to the institution. Such motivations are necessary as no rule is infallible and, as discussed above, the rules dictated by the protocol may not be so difficult to evade. This does not mean controls should be eliminated, but they should certainly be balanced with values, principles, and other intrinsic motivations public servants may have.

Another potentially controversial practice is the application of reliability tests (evaluaciones de confianza) upon those whose main functions include supervising public works. The Administrative Code of the State of Mexico (12th Book, Chapter IX) establishes that public servants supervising public works will be subjected to reliability tests performed by SECOGEM’s Unit for Reliability Testing (Unidad Estatal de Certificación de Confianza) upon recruitment, reincorporation, promotion and permanence.

Furthermore, an approach leaning excessively towards control may hinder market engagement activities of procurement officials. Public institutions need to have a sound understanding of the nature, size and composition of the supply markets from which they purchase goods and services. Procurement officials need to keep up to date with new ideas and developments, as well as emerging technologies, to be better placed to create value-for-money. They can do so through several activities throughout the procurement cycle, all of them requiring interactions with market agents, such as trade shows, “meet the buyer” events, meeting with industry chambers and debriefing suppliers (New Zealand Government Procurement Branch, 2015[8]). While such interactions should indeed be regulated and subject to control items, they should also be subjected to behaviour principles and values, allowing procurement officials the flexibility to reach out to markets with clear objectives and protocols.

An alternative approach to balance controls is by facilitating ethical reasoning of procurement officials. SECOGEM, in collaboration with the Co-ordination Committee of the SAEMM and other relevant institutions, could develop case studies, checklists, and practical manuals illustrating typical ethical dilemmas of procurement officials and prompting them to solve such situations applying not only the rules, they cannot foresee every possible scenario, but also the values contained in the Code of Ethics and the codes of conduct. The Ethics, probity and accountability in procurement manual, developed by the Government of Queensland, Australia, provides a good reference for illustrating ethical dilemmas (see Box 4.3).

The following excerpt from the Ethics, probity and accountability in procurement manual describes how procurement officials in Queensland should act in situations where they risk committing unethical behaviour. The example below details what officials should do when they receive an invitation to a seminar from a supplier:

“Attendance by a procurement officer at a public seminar offered by a potential supplier is unlikely to create a conflict of interest. However, the officer must not discuss confidential matters relating to the tender process, and must not use the tender process to obtain a discount on any registration fee. Officers directly involved in the tender process should inform the tender management team as well as their own manager, and gain approval for their attendance at the seminar, which should be fully documented.”

Source: (The State of Queensland, 2019[9]).

4.2.1. The State of Mexico should develop its framework to manage conflicts of interest with a shared definition, practical illustrations, and systematic training for procurement officials

The current institutional framework in the State of Mexico involves a network of actors in charge of preventing, investigating and sanctioning corruption acts – as well as solving conflicts of interest and ethical dilemmas. SECOGEM and its different administrative units are responsible for promoting best practices and internal monitoring. They are also responsible for investigating acts, omissions or behaviours by public servants to determine administrative responsibilities SECOGEM has jurisdiction per the Organic Law of the Public Administration of the State of Mexico (Ley Orgánica de la Administración Pública del Estado de México, LOAPEM) and the Internal Bylaws of SECOGEM (Reglamento Interior de la Secretaría de la Contraloría), amongst other secondary regulations. However, such jurisdiction only extends to ministries and entities of the state public administration – not to municipalities. Nonetheless, SECOGEM has attributions to intervene at the municipal level, when authorised by law, regarding state transfers.

The Internal Bylaws of SECOGEM currently in force were approved and published in November 2018. Among the reforms, two new units were created: the Unit on Public Procurement Policies and the Unit on Corruption Prevention. On the one hand, the Unit on Public Procurement Policies has the following attributions:

Providing preventive advice to ministries, auxiliary bodies and municipalities relative to public procurement processes financed with state resources.

Verifying, directly or through the OICs, that the registry of procurement officials contains all the information established by law.

Receiving the reports by social witnesses, as well as their suggestions and proposals to strengthen the transparency and impartiality of public procurement.

On the other hand, the Unit on Corruption Prevention has the following responsibilities, among others:

Analysing and suggesting measures to support ministries and auxiliary bodies in preventing, detecting and hindering administrative faults and corruption.

Requesting information and documents to ministries, auxiliary bodies and OICs to produce analyses on anticorruption in the state public administration.

Developing and proposing policies, guidelines, criteria, indicators, strategies and other general tools relative to ethics, integrity rules, prevention and hindering administrative faults and corruption and prevention of conflicts of interest for public servants of the ministries and auxiliary bodies of the State of Mexico.

Proposing the Ethics Code for the public servants of the State of Mexico, communicating its content and verifying compliance with it.

Issuing an opinion upon request about the realisation of conflicts of interest by public servants of the state public administration.

Requesting information and documents to ministries and auxiliary bodies in order to issue an opinion about the realisation of a conflict of interest.

Issuing general statements and recommendations to prevent corruption and conflicts of interest in the public service.

Collecting, analysing, and assessing information to produce analyses relative to ethics, integrity and prevention of corruption and conflicts of interest in the ministries and auxiliary bodies of the government of the State of Mexico.

Coordinating, keeping a record, and following up the recommendations issued by the Ethics Committees.

Designing and promoting communication, training and raising awareness programmes relative to ethics, integrity and prevention of corruption and conflicts of interest.

The integrity framework of the State of Mexico mandates the creation and maintenance of an Ethics Committee in each ministry and auxiliary body of the state administration to analyse and advise on public servants’ compliance with integrity rules, per the Ethics Code for Public Officials of the State of Mexico and the Codes of Conduct. Since then, the Ethics Committees has borne the responsibility of providing support to the integrity system by ensuring that public servants and citizens are informed of the state government’s ethics rules. Its nine members occupy an honorary position with voting rights, eight of them elected by peers, representing different levels of the hierarchy and one serving as the president of the committee (the minister or head of agency), who is a permanent member, and whose role is merely advisory. While its decisions are non-binding, the opinions and suggestions given should enhance integrity in the State of Mexico public sector. This is an example of another initiative where the State of Mexico followed the policy established at the federal level.

According to the Agreement mentioned above, the Ethics Committees have the following attributions:

Drafting and approving its annual working plan during the first trimester of each year. The working plan should include specific objectives, goals and activities.

Monitoring implementation and compliance with the Code of Ethics and the Integrity Rules.

Participating in the drafting, review and update of the corresponding code of conduct and oversee its implementation and compliance.

The Ethics Committees can receive reports of violations of the Code of Ethics, the Integrity Rules, and the corresponding Code of Conduct. If confirmed, the Ethics Committees should refer the case to the corresponding OIC.

The framework for the management of conflicts of interest is elaborated in the table on the following page.

A basic and shared definition of conflict of interest is critical, as it helps public servants determine objectively whether they can execute their duties and functions in situations where there appears to be a conflict of interest, but this is not or may not be the case. The definition adopted by the State of Mexico should label the situation above as an “apparent conflict of interest” – which could be as serious as having an actual conflict. Since potential or apparent conflicts of interest are not listed in the State of Mexico regulations, detection and enforcement may be difficult. Whichever approach the State of Mexico adopts in its framework for the management of conflicts of interest however, it is important to ensure that it clearly defines the concept in its legislative framework as related to public procurement.

The OECD report Managing Conflict of Interest in the Public Service: OECD guidelines and country experiences makes a distinction between actual, apparent and potential conflict of interest in various situations. The OECD defines a conflict of interest as a clash between the public duty and private interests of a public official, in which the public official has private-capacity interests that could improperly influence the performance of his or her official duties and responsibilities. An actual conflict of interest is a direct conflict between a public official’s current functions and his private interests. An apparent conflict of interest occurs when a public official’s private interests could improperly influence the performance of his duties, but this is not, in fact, the case. A potential conflict of interest encompasses, on the other hand, a situation in which a public official has private interests which could create a conflict of interest if the official becomes involved in the future (OECD, 2004[10]). The framework to manage conflicts of interest in the State of Mexico does not distinguish between these three types of conflict of interest. OECD data shows that 85% of member countries have a specific definition of conflicts of interest for public procurement officials in their regulatory frameworks (OECD, 2019[11]). The definitions used by other OECD countries, such as Canada or New Zealand, could be a good reference for the State of Mexico.

Canada

Canada’s Conflict of Interest Act (S.C. 2006, co., sq.) states that “a public office holder is in a conflict of interest when he exercises an official power, duty or function that provides an opportunity to further his private interests or those of his relatives or friends or to improperly further another person’s private interests” (Article 4). In addition, Article 5 specifies the general duty expected of public servants. “Every public office holder shall arrange his private affairs in a manner that will prevent the public office holder from being in a conflict of interest.” While the Conflict of Interest Act is primarily aimed at elected and other senior officials, the Treasury Board Code of Values and Ethics applies this definition and similar responsibilities to every public servant in government.

New Zealand

The definition of conflict of interest is tailored to targeted groups, such as public servants, ministers or board members of crown companies. Nevertheless, these definitions contain common features. For example, they all cover actual and perceived conflicts of interest, as well as direct and indirect conflicts. In addition to the general definitions developed for these targeted groups, other documents list possible types of situations where conflicts of interest arise, together with concrete practical examples.

Public servants: “Conflicts of interest are defined as any financial or other interest or undertaking that could directly or indirectly compromise the performance of their duties, or the standing of their department in its relationships with the public, clients, or ministers. This would include any situation where actions taken in an official capacity could be seen to influence or be influenced by an individual’s private interests (e.g. company directorships, shareholdings, offers of outside employment).

Ministers: “Conflicts of interest can arise because of the influence and power they wield – both in the individual performance of their portfolio responsibilities and as members of Cabinet. Ministers must conduct themselves at all times in the knowledge that their role is a public one; appearances and propriety can be as important as actual conflict of interest in establishing what is acceptable behaviour. A conflict of interest may be pecuniary (that is, arising from the Minister’s direct financial interests) or nonpecuniary (concerning, for example, a member of the Minister’s family) that may be either direct or indirect” (Cabinet Manual).

Members of the Board of Crown Companies: Conflict of interest is defined as a situation in which a board member is “party to, or will or may derive a material financial benefit from” a transaction involving his or her company (The Companies Act 1993, Part VIII, Sections 138 and 139).

Source: (OECD, 2004[10]).

Implementing appropriate measures to prevent apparent and potential conflicts of interest is as important as implementing measures to manage actual conflicts of interest. For example, State of Mexico authorities should be particularly vigilant of cases in which potential bidders are former public servants or when newly hired public servants have experience in the private sector (for instance, in the construction industry). This practice, of working with actors who are closely linked to the sector in which procurement will occur, is known as a “revolving door”, and is not fully anticipated by the state law. “Revolving door” practices increase the risk of integrity breaches and opportunities for conflicts of interest.

In this regard, the regulatory framework in the State of Mexico needs to be more specific. For example, the Law of Administrative Responsibilities for the State of Mexico and its Municipalities, in its Article 76 states that private agents are forbidden to hire individuals who served in the public sector during the previous year and who possess information that will benefit their market position or provide an advantage vis-à-vis its competitors. This practice is defined in the law as “unduly hiring a former public official” (contratación indebida de ex servidores públicos) and also stipulates a sanction for the public official. However, sharing information is not the only potential integrity risk for a former procurement official now working in the private sector. For example, he may also want to take advantage of his insider relationships to influence an award decision or the selection of a direct award over a public tender.

Elaborating and further developing the conflict of interest rules also applies for gifts. While the Law of Administrative Responsibilities for the State of Mexico and its Municipalities forbids public servants to receive any kind of gift, there might be situations, for example a protocolary gift, in which it might be hard for procurement officials to refuse receiving the gift. The main point, even beyond the actual cost of the gift, is the extent to which receiving the gift might jeopardise the impartiality and objective judgement of a procurement official or the extent to which it may create the will to reciprocate. A very strict approach completely forbidding gifts may lead to cynical behaviour in which the public official not only fails to comply with the regulation, but also is unaware of the impact on his judgement. The OECD toolkit Managing Conflict of Interest in the Public Sector proposes a checklist for public servants to reflect on the potential implications of a gift. This prescriptive checklist reduces the potential for confusion to four simple tests, arranged under a mnemonic – GIFT (genuine, independent, free and transparent) – to make the tests easier to remember. Each element of the GIFT mnemonic recalls one of the principles of public ethics, rather than a set of complex administrative definitions and criteria or processes (see Box 4.5).

Genuine

Is this gift genuine, in appreciation for something I have done in my role as a public official, and not requested or encouraged by me?

Independent

If I accept this gift, would a reasonable person have any doubt that I could be independent in doing my job in the future, especially if the person responsible for this gift is involved or affected by a decision I might make?

4.3.1. SECOGEM could give better visibility to the registry of blacklisted companies and expand its functionalities

According to the Organic Law of the Public Administration of the State of Mexico, Article 38 Bis, XI, SECOGEM has the responsibility of monitoring compliance of duties by suppliers and contractors, requiring them the information relative to their activities. Indeed, the Law on Public Procurement of the State of Mexico and its Municipalities also establishes in Article 74 that SECOGEM will manage a registry of the individuals or businesses in the following situations:

Suppliers or service providers who incurred in delays in the delivery of goods or services, as a result of their own fault;

Those who had a contract rescinded, as a result of their own fault;

Those who provided false information or behaved in bad faith in any stage of the process to award a contract, its formalisation, execution or during the process of filing a complaint (inconformidad);

Those who have established contracts violating the statements of this Law, as demonstrated with information held by OICs.

SECOGEM, specifically the General Directorate of Administrative Responsibilities, gathers the information from ministries and auxiliary bodies to put together this registry and shares it with them. Ministries and auxiliary bodies should inform SECOGEM, within the first five working days of each month, about the individuals and businesses subject to an “administrative sanctioning process” (procedimiento administrativo sancionador) as a result of one of the situations listed above. The officials in charge of procurement of goods, services, leasing, public works and related services as well as the heads of OICs of ministries and auxiliary bodies of the executive, the Office of the Attorney General of the State of Mexico, administrative tribunals, auxiliary bodies and state public funds (fideicomisos públicos estatales) are all responsible for informing SECOGEM.

The information is kept in the Registry of barred and sanctioned companies, suppliers and contractors (Registro de empresas, proveedores y contratistas objetados y sancionados). It also includes information on companies and individuals barred from procurement procedures or sanctioned by the Federal Ministry of Public Administration (SFP) or by other federal states.

The information is public and available at www.secogem.gob.mx/EmprObje/BoletinPublico.asp. The user can search for a company by sanction (barred from participating in procurement procedures, fines, objected, and compensating administrative process or procedimiento administrativo resarcitorio1), by company name, or by activity (industry, commerce, services and others). The information provided by the system for each company includes its full denomination, number of deed, tax number, notification date, the irregular situation and the authority that reported it. In some cases, more information is available, including the exclusion date and the follow up to the case (challenges, court rulings, etc.).

The registry is not easy to find on the Internet. SECOGEM could give it more visibility by creating links from the entry point of its own webpage (www.secogem.gob.mx), the e-procurement platform COMPRAMEX or the website of the Government of the State of Mexico (www.edomex.gob.mx). Such “bad publicity” for blacklisted companies would in itself create incentives for good behaviour from suppliers.

Likewise, SECOGEM could expand the functionalities of the registry to make it more useful for procurement officials. For example, it could provide the option to download documents containing resolutions sanctioning companies so that procurement officials could have complete information on the irregular situation leading to sanctions and the implications for future procurement procedures. Debarment policies have been developed in many countries although rules differ across jurisdictions and international organisations (see Box 4.6). Furthermore, the registry could go beyond being a blacklist to become a source of information on supplier performance. It could incorporate information on contract performance so that procuring authorities could identify risks when awarding a contract to a specific company. Additionally, SECOGEM could migrate the registry to an open data format to improve accessibility and the possibility to use the data to identify trends and patterns useful for decision-making.

Integrity violations of companies may lead to permanent or temporary exclusion from public procurement. In line with European Union legislation, there are mandatory debarment rules in place in EU Member States, according to which, bidders against whom final court convictions for corruption have been handed down are excluded from future tenders. In EU Member States, laws contain debarment provisions and contracting authorities have cross access to their internal debarment databases. Multilateral Development Banks have developed an Agreement for Mutual Enforcement of Debarment Decisions and made public the list of companies and individuals ineligible to participate in their tendering processes.

The 2009 OECD Anti-Bribery Recommendation calls on Parties to the OECD Convention on Bribery of Foreign Public Officials in International Business Transactions to: “suspend, to an appropriate degree, from competition for public contracts or other public advantages, including public procurement contracts and contracts funded by official development assistance, enterprises determined to have bribed foreign public officials and, to the extent a Party applies procurement sanctions to enterprises that are determined to have bribed domestic public officials, ensure that such sanctions should be applied equally in case of bribery of foreign public officials”.

While debarment has gained significant terrain in the last decade, particularly as a device in the fight against corruption and a tool to restore trust in government procurement, there is a lack of solid theoretical underpinning for these rules, and its efficiency continuous to be discussed, in terms of access, competition and value-for money principles, amongst others.

Source: (OECD, 2016[1]), and (Hjelmeng, 2014[13]), “Debarment in Public Procurement: Rationales and Realization”, in

G.M. Racca and C. Yukins, Integrity and Efficiency in Sustainable Public Contracts, www.researchgate.net/publication/265550163_Debarment_in_Public_Procurement_Rationales_and_Realization, consulted on 5 November 2019.

Article 87 of the Law on Public Procurement of the State of Mexico and its Municipalities dictates that any individual or company, national or foreign, is liable when participating in procurement procedures in the following cases:

Commits, offers or delivers money or any other benefit to a public official so that he carries out or abstains from an action related with his duties in order to obtain a benefit or an advantage;

Carries out actions in order to obtain an undue benefit or advantage in the public procurement process;

Carries out actions or omissions in order to participate in procurement procedures even though it is barred by an administrative resolution or a legal instrument;

Carries out actions or omissions in order to evade requisites or rules in public procurement or pretends to comply with them;

Intervenes on its behalf, but for the benefit of third parties barred from procurement procedures, so that such third parties get, partially or in full, the benefits of the procurement;

Obliges a public official to subscribe, provide, destroy or deliver a document or a good in order to obtain a benefit or advantage;

Promotes or uses its influences, economic or political power, real or fictitious, on a public official in order to obtain a benefit or advantage; and

Files false or altered information or documents in order to obtain a benefit or advantage.

The individuals and companies which participate in the situations described above can be fined with the equivalent of 300 to 300 000 times the daily value of the Measurement and Update Unit (Unidad de Medida y Actualización, UMA)2 in force at the time.

In addition, the Law of Administrative Responsibilities for the State of Mexico and its Municipalities, Article 68, defines the actions by private individuals or companies related to serious administrative offenses, namely bribery, illicit participation in administrative procedures, trying to influence or capture an authority, using false information, obstructing investigations, collusion, irregular use of public resources and unduly hiring a former public official. Applicable sanctions for individuals include economic fines equivalent to one or two times the benefits obtained or, when no benefit is obtained, from 100 to 150 000 times the daily value of the UMA; a temporary bar from participating in procurement of goods, leasing, services and public works for no less than three months and no more than eight years; and compensation of damages to the public finances of the state, municipality or public entity.

Likewise, for businesses sanctions include economic fines equivalent to one or two times the benefits obtained or, when no benefit is obtained, from 1 000 to 1 500 000 times the daily value of the UMA; a temporary bar from participating in procurement of goods, leasing, services and public works for no less than three months and no more than ten years; suspension of economic activities for no less than three months and no more than three years; dissolution of the society; and compensation of damages to the public finances of the state, municipality or public entity.

Public procurement can benefit from partnerships between government institutions and the private sector to advance integrity. Integrity is required to allow governments, on the one side, and businesses and citizens, on the other, to engage in a mutually responsive way thus rendering the public procurement system more accountable and ensuring value-for-money. In this sense, low levels of integrity and accountability in public procurement can jeopardise the effective use of public funds.

Preventing integrity breaches requires the active engagement and efforts from the government, the private sector and civil society, due to their complexity. Civil society and businesses can play an oversight and monitoring role in public procurement. By serving as a mechanism for direct social control on government activities, civil society and the business community can further integrity in government activities and restore public trust.

4.4.1. The Government of the State of Mexico should partner with the business community to develop and advance an agenda for business integrity in procurement activities

Currently, the State of Mexico does not have an agenda or programme to promote business integrity. This is an area of opportunity, particularly as there are already some programmes established by the Federal Government (SFP, see Box 4.7) and business chambers, such as the Business Co-ordination Council (Consejo Coordinador Empresarial, CCE) and the Mexican Chamber of the Construction Industry (Cámara Mexicana de la Industria de la Construcción, CMIC). Furthermore, advancing integrity in public procurement is an important preventive action given the fact that the LGRA and the Law of Administrative Responsibilities for the State of Mexico and its Municipalities establish sanctions for businesses that participate in acts of corruption and consider that businesses with an integrity programme could benefit from milder sanctions.

The registry consists on a distinction for those businesses that actively commit to comply with ethical standards by engaging their employees and suppliers. The objective is to provide positive incentives to promote business integrity and advance preventive measures and standards. The first stage for the implementation of the registry includes the development of an IT platform and legal reforms. The second stage consists on the implementation of the distinction for business that participate in procurement procedures.

Business integrity as described in the LGRA

Article 25 of the LGRA establishes that a programme of business integrity should include, at least, the following elements:

A clear and complete organisation and procedures manual, establishing the functions and responsibilities of each area, the chain of command and leadership in all the organisation;

A published and socialised code of conduct, including systems and mechanisms for implementation;

Adequate and effective systems for control, audit and surveillance to constantly and periodically assess compliance with the integrity standards by all the organisation;

Adequate systems to report wrong-doing, both internally and to the corresponding authorities, as well as disciplinary procedures and concrete consequences for those who behave violating internal rules or Mexico’s legislation;

Adequate systems and processes to train staff on the integrity measures;

Human resources policies preventing hiring individuals that may create an integrity risk for the company; and

Mechanisms that ensure transparency and disclosure of interests.

In order to facilitate business take up, SFP launched in June 2017 the Model Business Integrity Programme (Modelo de Programa de Integridad Empresarial), which was developed together with business associations. The model is a good example of translating legal provisions into concrete and practical guidance for the private sector by providing concrete examples on what each element of the Business Integrity Programme entails and including good practices from the private sector.

Source: SFP (2017), Modelo de Programa de Integridad Empresarial, https://www.gob.mx/cms/uploads/attachment/file/272749/Modelo_de_Programa_de_Integridad_Empresarial.pdf and https://www.gob.mx/sfp/articulos/funcion-publica-lanza-padron-de-integridad-empresarial, consulted on 5 November 2019.

While a business integrity programme, such as the one established at the federal level, would definitely be a step in the right direction for the State of Mexico, it is also important to reflect on how the verification process would work. It would be advisable that the government of the State of Mexico does not conduct any verification. Instead, SECOGEM could set guidelines on what to consider for an effective verification. International practices illustrate that policy guidance can direct companies to obtain independent third-party assurance. For example, in the UK Adequate Procedures Guidance, the Ministry of Justice suggests that organisations consider obtaining external verification or assurance of their anti-bribery system. Similarly, under the Government of Canada’s Integrity Regime, in order to be reconsidered eligible for bidding following debarment, companies are required to provide certification from an independent third party that integrity measures have been implemented. However, in Mexico there is still not a well-developed market for this kind of certification. Consequentially, SECOGEM could invite business chambers and universities to support the effort to devise a basic verification system while the market develops.

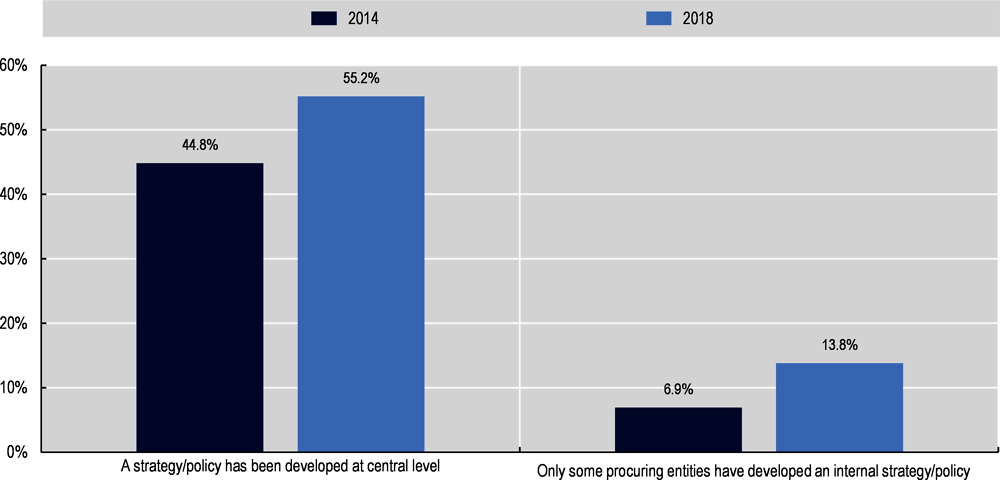

Businesses that apply an integrity programme could also be rewarded in procurement procedures. For example, the State of Mexico could advance reforms of procurement regulations to establish that, in a situation where two bids get the same score, the bid from the company with a business integrity programme gets the contract. Alternatively, during assessments based on points and percentages, companies that implemented a business integrity programme could get extra points towards the final score. In this way, the State of Mexico could leverage public procurement strategically to advance business integrity, just like 69% of OECD countries use it to promote, for example, responsible business conduct (see Figure 4.5).

Source: (OECD, 2019[11]).

In any case, developing an agenda for business integrity should necessarily be a joint effort between the state government and the business community, with other stakeholders also considered to provide feedback (i.e., academia).

4.4.2. The Government of the State of Mexico could advance other measures to promote business integrity, such as integrity pacts, anticorruption clauses and supply-chain transparency

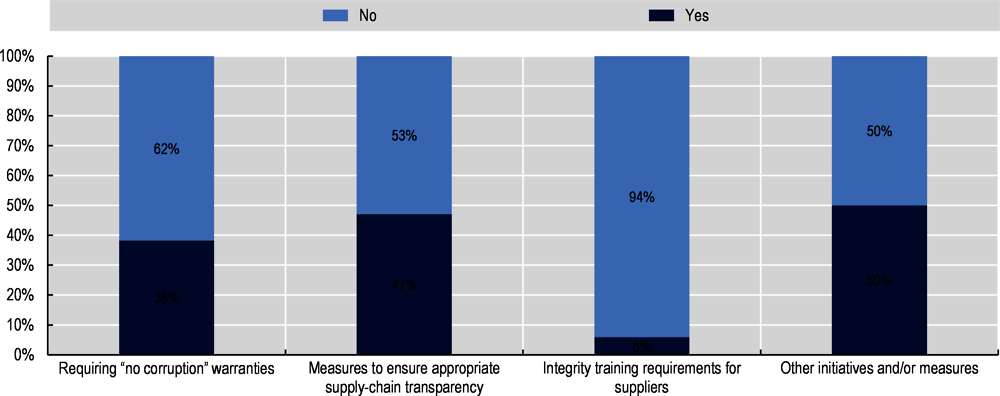

The OECD Recommendation on Public Procurement underlines the need to develop requirements for internal controls, compliance measures and anti-corruption programmes for suppliers, including appropriate monitoring. It stresses the need for procurement contracts to contain "no corruption" warranties and measures to verify the truthfulness of suppliers’ commitments that they have not and will not engage in corruption in connection with the contract. According to the OECD Recommendation, such programmes should also require appropriate supply-chain transparency to fight corruption in subcontracts, and integrity training for supplier personnel.

In order to preserve integrity in public procurement, it is critical to work with external actors, in particular the private sector. The results of the 2018 OECD Survey on Public Procurement show that, consistent with the overarching guidance provided in the key principles, there are initiatives being pursued to promote integrity among suppliers (see Figure 4.6). In Australia, for example, the Commonwealth Procurement Rules allow entities to exclude tenderers on the grounds of bankruptcy, insolvency, false declaration or significant deficiencies in the performance of any substantive requirement or obligation under prior contract. In Latvia, the contracting authority can exclude a candidate or tenderer (or their subcontractor where a value threshold of 10% of the total value of the contract is met) from participation in a procurement procedure in certain circumstances including tax debts, as outlined in the legislation.

Source: (OECD, 2019[11]).

As mentioned in the introduction to this chapter, the public procurement cycle involves multiple actors, and therefore integrity is a requirement for all of them. Both the public and private sectors are responsible for taking measures to preserve integrity. Private companies often have their own integrity system in place, and many countries engage with private sector actors to instil integrity in public procurement. For example, standards applicable to public sector employees may be expanded to private sector stakeholders through integrity pacts.

Integrity pacts are one way of preserving the integrity of public procurement systems. They consist of agreements between the government entity offering a contract and the companies bidding for it, that they will abstain from bribery, collusion and other corrupt practices for the extent of the contract. Following OECD recommendations (OECD 2012), the State of Mexico made it mandatory for participants in tenders to sign a Certificate of Independent Bid Determination (CIBD). These signed documents are important deterrents of anticompetitive practices and bind legal representatives of firms to penalties and sanctions included in the anti-trust frameworks to increase the likelihood of competitive tenders. This instrument is a good practice and is recommended by the OECD Guidelines on Fighting Bid Rigging, as it makes firms’ legal representatives aware of, and directly accountable for, unlawful behaviour. In order to reinforce this tool, the signed declarations of bidders could be published in COMPRAMEX or any other website aimed at promoting integrity.

As discussed before, integrity risks are present at every stage of the procurement cycle. To minimise these, the State of Mexico could consider extending the scope of CIBDs so that the bidder states that it has not engaged in anti-competitive conducts with other bidders (i.e., by exchanging bid information related to their offers or by discussing the bid strategy) and it will not engage in other forms of corrupt behaviour (i.e., bribery, providing false documents and information), turning them into far-reaching integrity pacts addressing all the stages of the procurement cycle, from bid preparation to contract execution.

4.4.3. SECOGEM should advance the process of reform of the social witness programme applied in the State of Mexico

Civil society oversight is a commonly used tool to further integrity in public procurement. It can not only play a role of scrutiny and monitoring, but also in increasing the transparency of government activities, and, as such, help restore public trust in government. The regulatory framework in the State of Mexico could be used to establish the obligation or opportunity for the government to consult with the public during the procurement planning process (e.g. prior to large-scale or environmentally or socially sensitive procurements). In some countries, citizens are –under clearly specified conditions and subject to signing a statement of confidentiality –permitted or encouraged to act as observers in procurement proceedings. Hence, the State of Mexico could consider empowering citizens to be officially involved in the monitoring of procurement performance and contract completion.

The Administrative Code of the State of Mexico (First Book, Title X) establishes the “social witness”, which is a mechanism to engage civil society in procurement procedures that imply serious risks of corruption or opacity due to their complexity, impact or the amount of resources involved. The social witness has the right to provide comments and opinions in procurement procedures and drafts a report at the end of his intervention with suggestions to improve transparency, efficiency, effectiveness and impartiality. Such a report must be made public on the webpage of the contracting authority. If the social witness identifies any irregular situation, he has the duty to promptly notify SECOGEM. In fact, SECOGEM keeps the record of the results of the interventions by social witnesses.

In order to engage a social witness, the procurement must entail actions or works with high social impact, a significant amount of resources, have significant influence on economic or social development, a growth strategy at the municipal, regional or state level, or a strong imperative to increase transparency. The contracting authority, when requesting the participation of a social witness, must explain which of the previous categories they are related to.

An individual or organisation interested in serving as a social witness must register with the Committee for the Registration of Social Witnesses (Comité de Registro de Testigos Sociales del Estado de México, CRTSEM), composed by the Autonomous University of the State of Mexico (Universidad Autónoma del Estado de México, UAEM) and the Institute for Transparency and Access to Public Information of the State of Mexico and its Municipalities (Instituto de Transparencia y Acceso a la Información Pública del Estado de México y Municipios, INFOEM), which keeps a registry of social witnesses and makes it public on their websites (http://www.testigossociales.org.mx/TestigosSociales/#tesSocRegis). The registration is valid for one year and can be extended year upon year for up to four years, depending on the performance of the social witness.

The application to become a social witness should include a written request, CV, document attesting that the interested person or individual has not been sentenced for a crime, a statement indicating the following: that the interested individual is not a public official and was not so during the last year, that he has not been barred from public service and that he will abstain from participating in procurement procedures in which he may have a conflict of interest, and an attestation of participation in the training determined by the CRTSEM.

The CRTSEM has five members, who are public servants from UAEM or INFOEM:

The contracting authority requesting the participation of a social witness must establish a contract indicating the scope of his work and the corresponding compensation, in line with the quotas established by the CRTSEM (see Table 4.4 for the quotas established for 2019).

Among other tasks, the social witness can participate in the drafting and review of the call for tender, clarification meetings, inspections of the sites for installation or construction, the events to receive and open bids, assessment of technical and economic proposals, award meetings and contract formalisation. Therefore, their work concentrates mainly on the tendering phase, with some participation in the pre-tendering phase, but no involvement in the post-tendering stage. This was identified as a risk in a study to take stock of the experience of social witnesses at the federal level (SFP and USAID, 2018[15]). There is indeed an opportunity to widen the scope of the involvement of social witnesses to include the pre-tendering (i.e., reviewing market analyses, award criteria, technical specifications) and the post-tendering stage (i.e., contract management, social audits, delivery of goods, services or works, closure of the contract and payment).

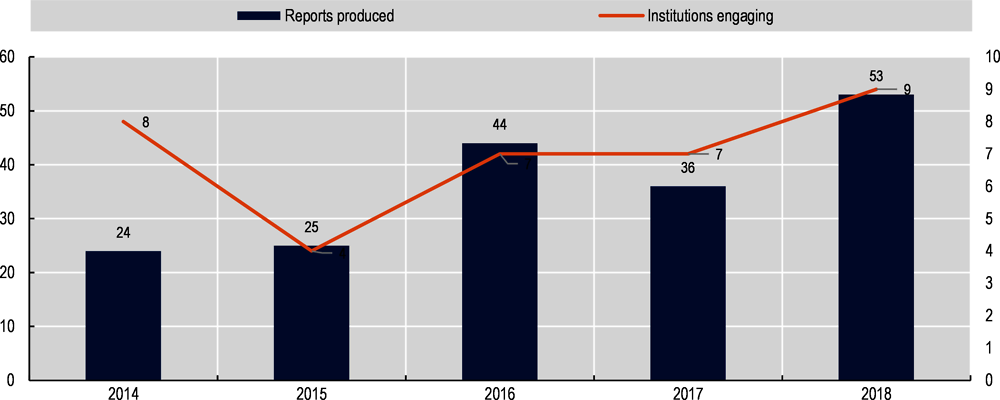

As of 6 November 2019, there were 21 individuals and one organisation (a bureau of accountants) in the registry of social witnesses. The registry includes contact information and the field of procurement expertise (goods, services or public works), as well as degrees in the case of individuals, where accountants, lawyers and public administrators prevail. During 2018, social witnesses produced 53 reports out of their engagement in procurement procedures. Interestingly, the institutions whose procurement operations were most observed by social witnesses were the Elections Institute and the State Legislature, while the entity consolidating common purchases of the central public administration, the Ministry of Finance, only used them six times (see Table 4.5).

In perspective, the use of social witnesses increased during the period 2014-2018 in terms of reports produced, except in 2017, and also in terms of the number of institutions engaging them, except in 2015 and 2017 (see Figure 4.7).

Source: INFOEM website, http://www.testigossociales.org.mx/TestigosSociales/#comite, consulted on 6 November 2019.

Social witnesses are also used at the federal level, in a programme managed by SFP. Even though there is evidence of significant benefits from it, there are also opportunities highlighted by the OECD and other institutions.

The social witness programmes managed at the federal and state level have some similarities, but also important differences. First, while the federal programme is managed by the control authority (SFP), including the registration, training, and assessment of the work by social witnesses, at the state level the responsibilities are shared between UAEM, INFOEM and SECOGEM. It is said that charging UAEM and INFOEM with the registration of social witnesses is to keep them at arm’s length from the institutions of the executive branch of government. However, the control institutions (SFP and SECOGEM), as a result of the nature of their work, might be better placed to assess and develop the expertise of social witnesses in terms of integrity risks. Secondly, the federal regime establishes clear thresholds over which a procurement process must necessarily engage a social witness.3 The State of Mexico regulations are rather vague in this sense, as they do not establish a clear threshold. Third, the compensations paid to social witnesses vary significantly. At the federal level, the compensation is based on the work hours required from the social witness and a payment per hour determined after a market study carried out by SFP. As their payments are fixed in UMAs, some entities consider they can be quite onerous (SFP and USAID, 2018[15]). While a high compensation might provide an incentive for more individuals and organisations to become a social witness, it may also move public entities to avoid their participation, particularly given the lack of a clear threshold.

The differences described above give an insight into some of the reforms needed for the social witness scheme of the State of Mexico. Furthermore, the independence of social witnesses, might be jeopardised by the fact that the contracting authority, whose procurement procedure the social witness is observing, hires and pays him. The social witness might feel intimidated or uncomfortable criticising the job of an entity that is hiring and paying him. The entity might even apply some direct or indirect pressures to hinder the witness’ job, for example, delaying their payments. The budgetary pressure that the social witness programme may exert may also lead contracting authorities to avoid them in an attempt to cut costs. In order to prevent these situations and strengthen the independence of social witnesses, reforms could be advanced so that social witnesses are hired by SECOGEM or INFOEM, rather than by the contracting authority.

In addition to setting clear thresholds for the engagement of social witnesses, there could be random appointments for specific procurement procedures. These could include not only public tenders, but also restricted invitations and direct awards, where social witnesses could review, for example, the justification to carry out a non-competitive process or to modify contracts during the execution of works and services.

In the past, the OECD has noted that social witnesses at the federal level may be quite knowledgeable about the engineering of public works or specific markets, but not about integrity risks (OECD, 2018[4]). The State of Mexico should be aware of this risk and provide permanent and systematic training for social witnesses. SECOGEM, with its expertise on control activities and public ethics, could lead the work to prepare tailored training programmes for social witnesses to be able to identify and recommend actions to mitigate integrity risks. Another weakness observed at the federal level is that the same social witness may participate in several processes involving the same procuring institution, creating the risk of familiarity with procurement officials and business agents. SECOGEM, INFOEM and UAEM should strive to address this risk, which is exacerbated at the state level by the limited number of social witnesses, by rotating social witnesses so as to avoid this familiarity, which may lead to conflicts of interest.

The Annual Report 2018 by CRTSEM concludes that even though there are a growing number of applications to become social witness, there are also a significant number of social witnesses who quit or did not request the extension of their registrations (INFOEM and UAEM, 2018). The report does not provide an explanation for these trends and, therefore, INFOEM, UAEM and SECOGEM could work together to analyse and explain this behaviour. One potential explanation might be that social witnesses do not perceive that their work is appreciated or at all useful. In this case, the three institutions could launch a campaign to widely communicate the programme and the benefits it has delivered for the State of Mexico. As part of this campaign, there could be an annual report or a website to follow up on feedback from social witnesses and the improvements stemming from their suggestions.

The State of Mexico, through SECOGEM, is preparing a reform on the functioning of social witnesses, which was drafted after consultation with UAEM and INFOEM. The reform proposal is under analysis at the Ministry of Justice and Human Rights (Secretaría de Justicia y Derechos Humanos), which has to review and clear it before sending it to the State Legislature.

The reform proposes the creation of two committees, one for the registration of social witnesses, which would incorporate SECOGEM alongside UAEM and INFOEM, and another to appoint social witnesses, which would be led by SECOGEM and incorporate the participation of either business chambers or the Citizen Participation Committee of the SAEMM. The registration committee would call a public process to recruit social witnesses annually or depending on need.

The reform also aims to strengthen the profiles of social witnesses by requiring a minimum experience of five years dealing with procurement matters. This need was identified by SECOGEM as it observed that the reports by social witnesses often do not make any relevant recommendations and quite frequently are “copy-paste” versions of previous reports. However, SECOGEM has no authority to sanction social witnesses in such cases.

Likewise, the reform would require social witnesses to prepare interim reports in each stage of the procurement process, in addition to the final report.

In summary, the reform would align the State of Mexico practice for social witnesses with the federal programme.

Source: Information provided by SECOGEM.

4.4.4. The State of Mexico could explore alternative mechanisms for civil society engagement in procurement procedures and public works, such as integrity monitors, social contracts and social participation frameworks

As opposed to social witnesses, who concentrate on one phase of the cycle, the integrity monitor is particularly relevant for public works and follows the entire process, including tendering, contract management, fiscal oversight, records compliance and onsite construction monitoring. Corruption and mismanagement can stem from lack of information and internal communication. An integrity monitor following the entire process thus reduces such risks. The State of Mexico could explore the possibility of nominating an integrity monitor who can follow the entire procurement cycle for the next major work of infrastructure, as used during the Tappan Zee Bridge Project in the United States (see Box 4.9).

In order to counter the corruption risks associated with the Design-Build model of the Tappan Zee Bridge, it was decided to retain an independent procurement integrity monitor for the project. The Governor’s office and the New York State Thruway Authority (NYSTA) determined to address the tension between the need, on the one hand, for confidentiality in the evaluation of the proposals and negotiations with the proposers versus, on the other hand, the need for transparency in the decisions surrounding the expenditure of public funds, by having an independent firm, outside of the procurement process itself, monitor compliance with the controls governing that process.

The objectives of the integrity monitor included process evaluation, process enhancements and compliance monitoring. In order to achieve these ends, it was entitled to: i) obtain and review selected documentation relating to integrity and security of the procurement process; ii) make recommendations for enhancements of the process to appropriate personnel; iii) perform monitoring through: unannounced attendance at meetings selected on a random basis; review of documents produced by the procurement process; interview with those involved in process; physical observation of compliance with all critical security/integrity-related controls; communication with appropriate personnel as to any issues found so as to facilitate immediate remediation; and iv) prepare a final report.

Source: Thacher Associates, “Tappan Zee Hudson River Crossing Project: Report of the Independent Procurement Integrity Monitor”, www.newnybridge.com/documents/int-monitor-report.pdf (consulted on 6 November 2019).

There are additional mechanisms for more profound engagements that the State of Mexico could explore, such as community monitors, social contracts, and social participation frameworks (OECD, 2015[14]).

Community monitors observe progress and the quality of public works. They can be useful for creating trust among stakeholders, but need to be properly trained.

Social contracts are designed to clarify and capture stakeholder commitments. These are co-signed by the leading agency and representatives of users, contractors, local governments, and congressmen during the implementation phase of public works. The contracts reflect the agreed roles that emerge from dialogue processes. They illustrate not only the adherence of the leading agency to social participation principles, but also the contributions of each stakeholder towards public works, as well as roles and behaviours of each party that contribute implicitly to fighting corruption and to enhancing the governance environment. Social contracts can also be complemented with bilateral agreements between the leading agency and the parties.

A social participation framework (SPF), when applied, is set up from the outset of a public works project. The SPF is used during project preparation and continued throughout its cycle. The SPF contemplates three components: participation, communication, and transparency and accountability. The overall main objectives of the SPF are: i) guaranteeing a broad participation of the different stakeholders aiming at, amongst other objectives, establishing their roles and responsibilities in realistic and fair terms; ii) creating awareness of the importance of expenditures and mechanisms for maintenance to preserve the project’s condition; iii) disseminating the project’s objectives and achievements; and iv) increasing the public works transparency and accountability throughout their cycle.

Currently, the State of Mexico applies social control techniques (contraloría social) through a Control and Surveillance Citizen Committee (Comité Ciudadano de Control y Vigilancia) where citizens volunteer to monitor and prevent corruption in public works.

4.5.1. The State of Mexico could make challenge processes more accessible for bidders by allowing electronic filing and providing the necessary information in tender documents

An accountable public procurement system provides bidders with the opportunity to claim for the review of procurement processes and challenge award decisions, as established in the OECD Recommendation on Public Procurement (OECD 2015b).