2. Policies and partnerships to achieve Egypt’s potential

Egypt is looking to unleash its potential amid a fast-changing global landscape. Its development agenda emphasises innovation and sustainability and places high priority on continental integration and digitalisation. This second chapter of the PTPR of Egypt provides a comparative assessment of Egypt’s strategy, policies and tools for transforming the economy. It draws on peer learning to identify key areas for future reforms.

As seen in Chapter 1 of this Production Transformation Policy Review (PTPR), Egypt is among Africa’s industrial heavyweights. Scaling up productive investments and innovation are needed to unlock opportunities for all and achieve sustained and sustainable, job-rich growth. In its reform programme and development strategy, the country has placed a strong emphasis on digitalisation and greening and accelerating industrialisation through enhanced ties with the continent. This second chapter of the PTPR draws on policy dialogue and peer learning carried out during the implementation of the review process to provide a comparative assessment of Egypt’s strategy, policies and tools for transforming the economy. It provides an overview of the key elements of Egypt’s current vision and a snapshot of the country’s achievements in embracing institutional modernisation and red-tape simplification. The chapter identifies key recommendations for better capturing the gains of Industry 4.0, better harnessing the potential of industrial parks, and modernising the policy mix for economic transformation – responding to the challenge of fostering a knowledge- and innovation-based economy through enhanced partnerships and targeted investments.

The first chapter of the PTPR of Egypt provided an overview of the country’s economic transformation focusing on production, trade, investment and innovation. Following this chapter, Chapter 3 will provide a snapshot of agro-food and engineering-related activities, while Chapter 4 will focus on the AfCFTA as an accelerator of industrial upgrading in Egypt and its partner countries.

Egypt launched the National Structural Reforms Program (NSRP) in April 2021 under the auspices of the Ministry of Planning and Economic Development (MPED) (Box 2.1). The NSRP is the second stage of the National Economic and Social Reform Programme, launched in 2016. It is aligned with Sustainable Development Strategy: Egypt Vision 2030, a national agenda launched in 2016, and the African Union Commission’s (AUC) Agenda 2063: the Africa We Want.

The NSRP (2021-24) aims at achieving balanced and sustainable growth in light of national and international developments, such as the COVID-19 pandemic and the global transformation towards digital and green technologies. It announces both structural and legislative reforms to increase resilience, promote employment and employability and increase productivity and competitiveness. The NSRP is aligned with and builds on Vision 2030, a long-term strategy launched by Egypt’s president in 2016, encompassing areas such as promoting Industry 4.0 and the green economy, maintaining water and food security and controlling population growth. Some of the key targets identified are raising the real GDP growth rate from 3.6% in 2019/20 to 6%-7% in 2023/24, and to increase the share of investment in GDP from 13.7% of GDP in 2019/20 to at least 20% in 2023/24.

The scope of the NSRP covers five identified key systems: demographic, financial, logistical, government performance, and legislative; and six pillars. Economic diversification is the main pillar of the program, aiming to scale up the contribution of manufacturing, agriculture and information and communication technologies in GDP. This pillar also aims at encouraging upgrading, local value addition, productivity and competitiveness as well as increasing exports and investments in the three sectors, among other objectives. The other five pillars are as follows:

Improving the efficiency of the labour market and technical and vocational education and training (TVET), by developing the TVET system, activating the role of private sector, matching supply to market demand, and empowering women, youth and people with special skills;

Improving the business environment and enhancing the role of the private sector, through a supportive and enabling environment for competition, removing trade barriers, upgrading logistics, easing investment procedures, and supporting the sustainable use of natural resources;

Upgrading the governance and the efficiency of public institutions, through administrative and institutional reforms, empowering local administration units, and improving the governance of state-owned enterprises (SOEs);

Promoting financial inclusion and facilitating access to finance, through accelerating financial inclusion, increasing and diversifying options available to private sector, and stimulating the money market;

Bolstering human capital development, through raising the scope and efficiency of healthcare services, activating the Egyptian family development strategy, upgrading the competence of educational system, and widening the coverage of the social protection network.

The NSRP’s pillars are supported by dedicated targets and quantifiable key performance indicators, and defines the responsibility of each ministry or entity to implement each reform under a set time frame (short-term of 18 months or medium-term of 36 months). Additionally, a Supreme Committee for Structural Reforms, headed by the prime minister, has been put in place, with a technical secretariat and specialised working groups to follow up on the implementation of the program. The Committee has members from several relevant ministries, the Egyptian Regulatory Reform and Development Activity (ERRADA) initiative and the private sector.

Source: Authors’ elaboration based on official information from the Ministry of Planning and Economic Development.

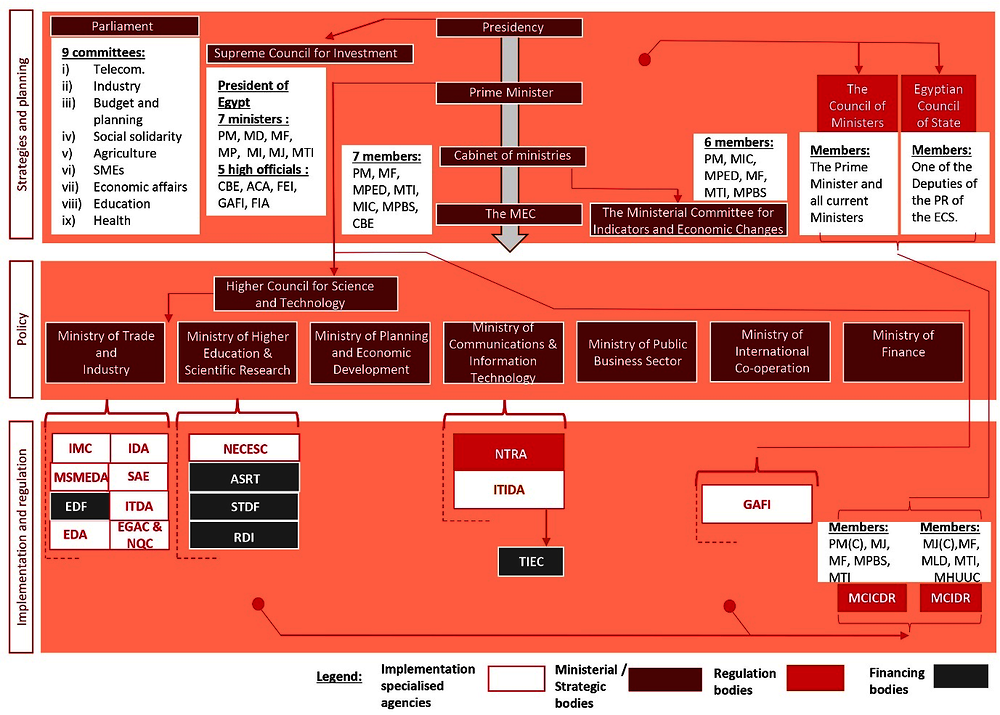

Egypt has developed an articulated institutional setting to foster economic transformation. The president and the prime minister (PM) chair several ministerial councils to ensure co-ordination at the strategic level. While leadership is key for success, the multiplicity of spaces for co-ordination creates some bottlenecks in fast-tracking the decision-making process.

Since the end of the 1990s, Egypt has undergone a process of institutional strengthening for economic transformation. Several new institutions at the implementation and regulatory level have been created, reflecting the evolving priorities of the national strategies along with new legal frameworks (Box 2.2).

Reforms started in 1997 with the creation of the General Authority for Investment and Free Zones (GAFI) in 1997 to regulate investments, and transformed into an investment promotion body under the Ministry of Investment in 2004. In 2019, GAFI became an autonomous agency under the PM’s office.

The Supreme Council for Investment, chaired by the president, was created in 2016. The Council was tasked with supervising investment policies in the country. Based on the Council’s recommendations, the Law of Investment Guarantees and Incentives (Law No. 72/2017) was enacted. The law gave the Council authority to approve policies and plans for investments (Box 2.2).

Law of Investment Guarantees and Incentives No. 72/2017

Egypt passed a long-promised new investment law in 2017 to boost investment. Under the new law, foreign investors are able to get domestic and even preferential treatment (with approval from the Council of Ministers), guarantees against nationalisation, a unified approval mechanism for companies undertaking strategic projects, and multi-tiered mechanisms for the settlement of investment disputes. In addition, GAFI will provide one-stop-shop investor services through the Investor Service Centre. The Law also announces tax incentives such as:

A 2% customs tax exemption (down from 5%) on imported equipment and machinery, and exemptions from stamp tax and registration fees.

A 50% investment tax allowance for priority areas (Sector A: e.g. lagging regions, the Suez Canal Economic Zone, Golden Triangle Economic Zone) and 30% for other specified areas (Sector B: e.g. SMEs, labour-intensive projects, electricity and renewables, tourism, national and strategic projects, projects that export more than 10%, automotive, wood/furniture/printing/ packaging/chemicals, pharmaceuticals, agro-food, engineering/metallurgical, textile and leathers).

Special incentives agreed by the Council of Ministers may include subsidised utilities, free land, cost reimbursement for staff technical training, and the establishment of special customs offices that meet certain criteria, such as projects that are exporting at least 20% of their products abroad or have 50% local content, or are applying the results of R&D carried out in Egypt.

Micro, Small and Medium Enterprise (MSME) Law No. 152/2020

The new Law on MSMEs defines the size of MSMEs according to turnover and capital for manufacturing and non-manufacturing firms, with thresholds amendable by prime ministerial decree. The Law grants a series of incentives, such as:

Non-tax financial incentives for MSMEs, such as partial or full reimbursements (and in some cases postponement of payment) for certain expenses [e.g. costs for land, participation in exhibitions, infrastructure (utilities installation), facilitations for financing against allocated property, social security, commercial registration], cost-sharing of workers’ technical training and exemption of patent registration fees. It also allows for financial incentives from the State Budget (up to 0.3% of GDP, with a minimum of EGP 1.5 billion annually), and announces conditional financial incentives for non-bank financial institutions investing in entrepreneurial enterprises.

Tax-related financial incentives, such as a tax exemption for capital gains resulting from the sale of assets and machinery if the proceeds are used to purchase new ones, a unified custom duty rate of 2% on imported machinery required for setting up a business, simplified income tax and bookkeeping rules, exemption from income tax for dividend distributions of one-person companies, and a possible partial or full exemption for property tax on buildings for micro and small enterprises for a defined period of time.

Non-financial incentives, such as the establishment of MSME Service Provision Units in MSMEDA and GAFI offices to streamline licensing; allocation of 30% of unutilised land in industrial zones to MSMEs, along with facilitation for payments of land costs and discounted prices and information provision; a goal to devote at least 20% of public entities’ contracts to MSMEs; and various incentives to formalise firms, such as facilitated allocation of property, facilitated procedures for registration and social security, putting on hold lawsuits and penalties, no retroactive application of taxes, and the application of MSME tax rates to formalised enterprises.

MCIT Decree no. 361/2020: Amendments to the executive regulations of the E-Signature Law

MCIT Decree 361/2020 amended the executive regulations of the e-signature Law No. 15/2004 to provide additional services, such as electronic seals for organisations and government entities (not only for individuals) and timestamp services that link date and time with the electronic document/file. The amendments aim to promote the adoption of e-signature among individuals, businesses, and government entities, as well to keep up with the technological developments in the public-key infrastructure and encryption technology domains. Egypt is in the process of issuing additional licenses for local companies to provide e-signature services in the country.

Source: Official documents and stakeholders interviews; (OECD, 2020[1]) for Investment Law No. 72/2017.

In 2000, Egypt set up the Industrial Modernization Centre (IMC) to foster the expansion and upgrading of the Egyptian industrial sector. IMC provides advisory services to firms and fosters business linkages.

In 2006, the Ministry for Trade and Industry (MTI) reunited the former ministries of trade and industry to strengthen industrial development and streamline production policies.

In 2017, the Medium, Small and Micro Enterprises Development Agency (MSMEDA) was established, replacing the Social Fund for Development that had been set up in 1991 to develop MSMEs and entrepreneurship in Egypt through enhancing the business environment, facilitating access to finance and raising awareness among others. A Law on MSMEs was enacted in 2020 (Law No. 152/2020), which replaced the previous Small Enterprises Law of 2004 and provided financial and non-financial incentives (Box 2.2). The Export Development Authority was established in 2017 to promote exports through the management of export grants, information dissemination, business matchmaking and capacity building.

In 2016, Law No. 83/2016 amended Law No. 7/1991 on the privately State-Owned Properties and granted the Industrial Development Authority (IDA) the authority to manage, exploit and dispose of lands allocated for Industrial development. In 2018, the role of IDA was strengthened with Law No. 95/2018, which transformed it into an economic entity and granted it more authority to allocate and manage lands for industrial use. The executive regulations of Law No. 95/2018 were issued in May 2021.

In 2019, the National Council for Artificial Intelligence was created, under the responsibility of the MCIT and with the inclusion of other relevant ministries, to steer national policies in this field.

While the creation of the new agencies and legal frameworks went hand-in-hand with the recognition that the country requires a modernised institutional setting to deal with emerging global, continental and national issues, it has also led to institutional proliferation. For example, GAFI, MSMEDA and IDA all have responsibilities in attracting manufacturing investments. There are also overlaps when it comes to sectoral support. The Information Technology Industry Development Agency (ITIDA) under the Ministry of Communication and Information Technology (MCIT) disburses funding for research projects and start-ups, including some electronics firms, whereas the Engineering Export Council and IMC also offer support across the value chain (see Chapter 3). Some common funding instruments, such as a joint fund between IMC and the Science and Technology Development Fund (STDF) for industry-academia linkages, and the position of representatives from different ministries in specialised agencies, aim to facilitate co-operation among relevant authorities.

In recent years, Egypt has also reduced administrative burdens, mostly through reforms to simplify the following:

Trade and customs. Egypt has introduced the National Single Window (NSW) (completed in 2021), which operates as an online platform to speed up customs processes. The transition to the NSW is part of Customs Law No. 207/2020, which aims to simplify customs procedures within the framework of Egypt’s national strategy to take advantage of the African Continental Free Trade Area (AfCFTA) (see Chapter 4 of this PTPR for more information on Egypt and AfCFTA). As part of the law, the Ministry of Finance issued Decree No. 38/2020 on Advance Cargo Information (ACI) to speed up and simplify cargo clearance.

Business registration. Egypt reduced the red tape associated with setting up new business through Law No. 15/2017 on the Simplification of the Procedures for Licensing Industrial Installations (Industrial Licensing Law), which reduced the paperwork and time required to open up an industrial facility. The time required to receive a license was reduced to 7 days, compared to up to 600 previously. The investment Law No. 72/2017 and MSME Law No. 152/2020 also simplified registration procedures for MSMEs and increased incentives for investments, while MSMEDA operates one-stop-shops to enable quick registration for MSMEs.

Closing down businesses. A new bankruptcy law (Law No. 11/2018) introduced a shorter timeline for procedures, added flexibilities for seeking business reorganisation and decriminalised bankruptcy, bringing the country closer in line with global standards.

Box 2.3 summarises the current institutional governance structure regarding policies for production, development and innovation.

In Egypt, the president, the prime minister, and multi-agency councils chaired by the president or prime minister, play a central role in charting strategies for economic development. Councils aim to facilitate cross-ministerial co-operation and ensure that policies designed at the ministerial level meet national strategic objectives.

Several ministries and agencies are in charge of portfolios linked to production transformation, notably:

The Ministry of Planning and Economic Development, which elaborated Egypt Vision 2030 and the National Structural Reforms Program 2021-24.

The Ministry of Trade and Industry (MTI), which launched the Industry and Trade Development Strategy (ITDS) (2016-20) and is currently elaborating the Inclusive and Sustainable Industrial Development Strategy (ISIDS) (2020-24) – with a view to fostering trade and integration in global value chains, digitalisation and Industry 4.0, increasing local value addition and sophistication, clean and sustainable production, and SMEs.

The Ministry of Communications and Information Technology (MCIT), which in 2016 launched the Egypt ICT Strategy 2030 to boost digital infrastructure, skills, ICT innovation and technology development.

The Ministry of Higher Education and Scientific Research (MHESR), which has launched the National Strategy for Science Technology and Innovation (STI) (2015-30) to boost innovation in the private and public sectors.

The Micro, Small and Enterprise Development Agency (MSMEDA) is developing the 5-year MSME and Entrepreneurship National Strategy and its operational plan to address barriers that MSMEs face in Egypt in line with Vision 2030.

Other ministries also hold relevant roles, such as the Ministry of Finance, the Ministry of Public Business Sector and the Ministry for International Co-operation. Specialised agencies attached to ministries are tasked with regulatory functions, strategy implementation, monitoring and evaluation, and funding.

Multiple business associations, chambers of commerce, and consultation bodies exist in Egypt. Among the more prominent ones are the Federation of Egyptian Industries (FEI), which dates back to 1922, and the 13 sector-specific export councils set up in 2005 by MTI (engineering, food, medical devices, agriculture, readymade garments, building materials, home textiles, printing and packaging, leather, construction, textiles, furniture and chemicals). These bodies are engaged in the policy-making process through formal consultation and through membership in multi-stakeholder bodies and participation in the boards of specialised agencies. For example, FEI participates in the Supreme Council for Investment and sits on the board of Egypt’s Internal Trade Development Authority (ITDA), while MTI regularly consults with the Export Councils, FEI and other bodies for designing and adapting policies. The Export Councils are also important for disbursing firm-level services to promote exports, often in co-operation with the Export Development Authority (EDA). The FEI president and the chairpersons of the Export Councils are appointed by the Minister of Trade and Industry.

Note: The figure does not include all institutions in Egypt; it includes only the principal ones linked to policies for production, development and innovation. ACA: Administrative Control Authority; ASRT: The Academy of Scientific Research & Technology; CBE: Central Bank of Egypt; ECS: Egyptian Council of State; EDA: Export Development Authority; EGAC: Egyptian Accreditation Council; FEI: Federation of Egyptian Industries; FIA: Federation of investors associations; GAFI: The General Authority for Investment and Free Zones; IDA: Industrial Development Authority; IMC: Industrial Modernization Centre; ITDA: Egyptian Internal Trade Development Authority; ITIDA: Information Technology Industry Development Agency; MCICDR: Ministerial Committee on Investment Contracts Dispute Resolution; MCIDR: Ministerial Committee on Investment Dispute Resolution; MD: Ministry of Defence; MEC: The Ministerial Economic Commission; MF: Ministry of finance; MHUUC: Ministry of Housing, Utilities and Urban Communities; MI: Ministry of Interior; MIC: Ministry of International Cooperation; MJ: Ministry of Justice; MLD: Ministry of Local Development; MP: Ministry of Military Production; MPBS: Ministry of Public Business Sector; MPED: Ministry of Planning and Economic Development; MSMEDA: Micro, Small and Medium Enterprise Development Agency; MTI: Ministry of Trade and Industry; NECESC: The Egyptian National Commission for Education, Science and Culture; NTRA: The National Telecom Regulatory Authority; NQC: National Quality Council; PM: Prime minister; RDI: Research, Development and Innovation Programme; SAE: Export Council & development bank; STDF: Science and Technology Development Fund; TIEC: The Technology Innovation and Entrepreneurship Center.

Source: Authors’ elaboration based on official information.

Egypt is fostering the adoption and development of Industry 4.0 around five main areas under the umbrella of the Digital Egypt ICT 2030 strategy and the national AI strategy:

Upgrading digital connectivity. This area includes achieving fast and affordable Internet, expanded Internet coverage and improved electricity reliability. Among the actions in this area, it is worth noting the investments in 4G/5G networks and fibre optic networks by public and private operators, and the launch of the Tiba-1 satellite for increased call and Internet coverage. Egypt has increased investment in digital infrastructure, dedicating USD 1.6 billion since the mid-2018s to modernise it, including efforts to replace copper cables with fibre optic ones and investing in 5G infrastructure.

Modernising regulations. In this area, Egypt has issued new regulations for the digital economy, enabling digital payment options through the E-Payments Law No. 18/2019 and the Personal Data Protection Law (No. 151/2020). The MCIT Decree No. 361/2020 amended the executive regulations of the E-Signature Law to further facilitate the use of e-signature in Egypt and foster digital government, and was followed by the issuing of more additional licenses for local companies to provide e-signature services in Egypt. In 2019 it also set up pilot projects for digital delivery of 155 government services in Port Said (an activity led by MCIT in partnership with relevant ministries). The government has also upgraded its quality infrastructure by setting up the National Center for Telecommunication Services Quality Monitoring in 2020, led by the National Telecom Regulatory Authority (NTRA) under MCIT. In addition, NTRA has auctioned additional spectrum for mobile telephony and mobile broadband, through a process that concluded in December 2020.

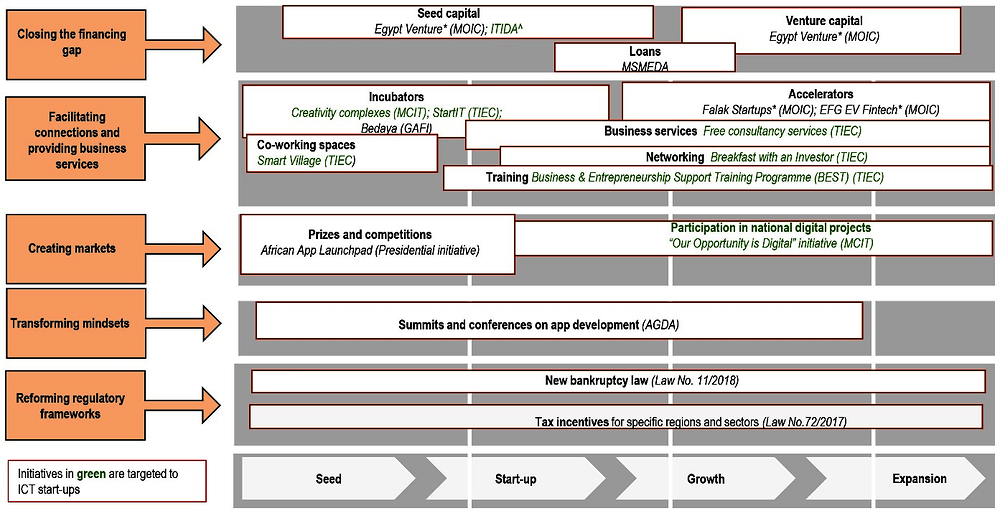

Fostering digitalisation in firms. The country has been introducing new incentives to fast-track digitalisation in firms and to support R&D, prototyping and testing in this area. Among them, it is worth noting the focus on providing start-ups and other businesses with guidance and resources to develop technologies relevant to Industry 4.0. For example, the Information Technology Industry Development Agency (ITIDA) and MCIT are establishing innovation hubs (three Electronics Innovation Complexes and seven innovation hubs at Universities) across Egypt to foster start-ups through the provision of development tools, testing facilities, co-working spaces and prototyping/digital fabrication facilities. MCIT with MTI and the private sector are also setting up a dedicated Industry 4.0 Innovation Centre (IIC) in Knowledge City, a part of the New Administrative Capital, with the aim of conducting assessments, engaging in capacity building and demonstrating best-use cases, based on the example of Germany’s Industry 4.0. The country has also issued, through the NTRA, challenges for robotics and autonomous vehicle research and has a Fintech Innovation Fund of about USD 64 million managed by the CBE to invest in fintech firms and investment funds. Egypt has also introduced fiscal incentives of up to 10-20% of exported value-added for digital services, up to approximately USD 150 000 (managed by ITIDA). A digital platform was established by MSMEDA in 2018 to facilitate information-sharing on the various services (e.g. financing and training) provided to MSMEs to support firms to start their business and develop them, along with a marketplace to help SMEs find new markets.

Fostering start-up creation. Egypt has strengthened the promotion of start-ups since 2016 (GEM and AUC, 2019[2]). Following the establishment of MSMEDA in 2017, a number of initiatives have strengthened Egypt’s policy mix for start-ups. Ministries and agencies have increased programmes and outreach to start-ups, particularly those in ICT (Figure 2.2). Efforts have been made to fill in the funding gap. The Ministry of International Cooperation (MOIC) has partnered with the private sector to create Egypt Venture, which funds start-ups, accelerators and other funds, and also to set up two accelerators, Falak start-ups and EPG EV Fintech. MSMEDA has also created a venture capital unit to support start-ups through direct investments in venture capital companies, incubators and accelerators, as well as loans to venture capital firms and early stage start-ups that partner with a strategic investor. The Ministry of Communication and Information Technologies (MCIT), together with its agencies ITIDA and the Technology Innovation & Entrepreneurship Center (TIEC), also provide a full chain of support for ICT-related firms, from seed capital to incubation services, business consultancies and networking opportunities. Some of this is directed specifically at boosting Industry 4.0 technologies. ITIDA has partnered with Innoventure and AUC Venture Labs to provide incubation, acceleration services and venture capital for start-ups engaged in electronics design, Industry 4.0 manufacturing and Internet of Things (IoT) systems. ITIDA’s funding ranges between EGP 0.5 and 2 million (approx. USD 31-125 thousand) in return for 2-4% equity for between half a year and two years. Through the “Our Opportunity is Digital” Initiative, MCIT is also setting aside at least 10% of public digital transformation projects for SMEs and start-ups, boosting demand.

Upgrading skills. Since 2016, MCIT has introduced several initiatives to increase the availability of, and financing for, training for basic digital skills among youth, and also of more advanced courses on information technologies. Dedicated centres are also being set up to build capabilities in innovating in emerging technologies, and international partnerships play a key role in this area. Egypt now has a variety of platforms/initiatives for training in digital skills, such as Future Work is Digital (training for web, data, and digital marketing for young people), Next Tech Leaders (45 advanced digital technologies for students, university staff, and professionals), Mahara-Tech [an initiative of MCIT, ITIDA and the Information Technology Institute (ITI) offering training in IT fields for young people and occasional private sector partners], and the Internet of Things Academy for training in IoT through the Mahara-Tech platform (ITI/ASRT). Advanced training is also offered through the Applied Innovation Center, which fosters R&D and skills development through international partnerships in artificial intelligence, an initiative to train trainers for digital technology (managed by the National Telecommunication Institute and Huawei) and the Advanced Training Centre for automation, IoT and other Industry 4.0 technologies, which offers vocational training (Siemens and MTI).

Egypt’s increasing efforts to mobilise public and private investments and international partnerships to enable its firms and talents to operate in an Industry 4.0 landscape are in line with global trends. Several countries are defining public policies to benefit from Industry 4.0. Germany, Italy and Malaysia are among countries that have elaborated plans to expand the adoption of Industry 4.0 in their industrial ecosystems (Table 2.1).

For Egypt to advance in enabling a transition towards Industry 4.0, five issues are of particular importance, based on international experience:

Bringing partners together for a common vision. Egypt has a complex governance structure which calls for co-ordination at the top level for strategy definition. While strategies for Industry 4.0 differ from country to country in terms of vision, ambition and focus, they tend to share one characteristic regarding their governance: they are cross-ministerial and multi-stakeholder, bringing the private sector in as a key partner in policy development and implementation. Public sector co-operation often brings together ministries and agencies that work on industrial development and innovation with those that are responsible for ICT. This is also complemented by spaces where the private sector, academia and government can define a vision for the future, priorities, respective responsibilities and financing (Box 2.4). Egypt would benefit from creating institutional spaces or mechanisms that can bring together all the relevant partners to develop a common vision for Industry 4.0 and co-ordinate its implementation.

Mobilising resources that match ambition. Enabling the shift from traditional manufacturing to Industry 4.0 will be no easy feat and will require investment commitments by both private and public sectors. Countries are investing large resources to shape the future, create the hard and soft infrastructure necessary for Industry 4.0, build skills and reduce risks for firms experimenting with new technologies.

Modernising institutions for metrology and standards. Standardisation is of central importance to the implementation of Industry 4.0. The transition to Industry 4.0 relies on an unprecedented integration of technologies and systems across different domains. As a result, quality infrastructure also needs to respond to a large number of technologies, scientific areas and stakeholders. Not only is close co-operation between research, industry, national metrology institutes and standardisation bodies necessary for realising quality infrastructure for Industry 4.0 at the national level, but it is also needed to have a strong global presence and voice. Egypt has a long-established and relatively dense quality infrastructure. The Egyptian Organisation for Standardization and Quality (EOS) (under the purview of MTI) was established in 1957, followed in 1963 by the National Institute of Standards (NIS), the National Metrology Institute (NMI) of Egypt (under MHESR), and the Egyptian Council for Accreditation (EGAC) (also under MTI). The Ministry of Electricity and Renewable Energy and MCIT also play a big role in technological standards. Egypt is also an active member of several important international quality infrastructure (QI) institutions, such as ISO, IEC, ITU and ARSO. In the context of Industry 4.0, collaborations have been emerging among institutions. For example, NTRA has been working with EOS to prepare joint positions on technology standards. NTRA has also established a roadmap for investing in R&D programmes for techno-regulatory and standardisation work in Industry 4.0 that aims to finance joint R&D initiatives and partnerships (NTRA, 2021[3]). However, there is still untapped potential in developing synergies and joint work between the different institutions and building mechanisms for working together with the private sector and academia to advance the Industry 4.0 agenda. There are different approaches to making this co-operation happen. In Germany, for example, quality infrastructure is preparing for digitalisation by building on multi-stakeholder co-operation among several different platforms (Box 2.5).

Putting in place targeted tools to enable all firms to benefit from Industry 4.0. Egypt’s approach to Industry 4.0 is similar with those of other countries, notably in setting up targeted incentives for firms to create and adopt Industry 4.0 technologies. Even though each country has a different policy mix, they all have in place specific incentives addressed to existing firms. Italy and Malaysia employ a more varied policy mix than Egypt, however, with Italy making extensive use of tax credits for R&D, training and application of Industry 4.0 and Malaysia committing up to USD 55 million for matching grants to firms to cover expenditures such as R&D, training, modernisation, licensing of new technologies and obtaining standards. In contrast, Egypt’s policy mix is more focused on start-up development, particularly in ICT areas. Extending support to other types of firms would contribute to a wider adoption of Industry 4.0 among Egypt’s industrial players.

In addition, beyond start-ups, countries are implementing dedicated actions to support SMEs’ efforts to adopt or develop Industry 4.0 technologies. The approach differs across countries, with some opting for crafting incentives and services specifically targeted to SMEs and others putting emphasis on setting up institutions for technology diffusion. Egypt, too, promotes Industry 4.0 in SMEs by stimulating demand through the “Our Digital Opportunity” initiative that engages SMEs in national digital transformation projects and supports start-ups through dedicated infrastructure and venture capital investments. The country is also in the process of setting up a dedicated Industry 4.0 Innovation Centre that will raise awareness and capacities. The function of such a centre could be boosted by enabling partnerships with other sources of knowledge and expertise in the local ecosystem (e.g. universities, federations of industry). In Italy, for example, competence centres are part of a wide net of partnerships that involves academia and the private sector to ensure MSMEs have access to multi-level support, from simple awareness raising to testing and technology development (Box 2.6).

Boosting partnerships between private sector and universities. The country’s universities could also provide an invaluable partner in implementing Industry 4.0. Already universities in Egypt are hosting incubators for start-ups, and could do more to work with the private sector to develop targeted solutions, infusing the local ecosystem with talent and expertise where possible. However, this would require pursuing outreach across the aisles to stimulate and map interest and opportunities to collaborate with different stakeholders. In addition, building partnerships would also require scaling up resources for joint research, and setting up mechanisms for long-term collaboration matched with appropriate conditionalities.

In Malaysia, Industry4WRD, the country’s strategy to promote Industry 4.0, was launched by the Ministry of International Trade and Industry (MITI) in 2018. The country dedicated at least USD 107 million in 2019 across several support actions, and has made available up to USD 1.2 billion in low-interest loans and guarantees to operationalise the strategy through a combination of different tools, such as a matching grants for investment in automation equipment, the conduct of R&D and other innovation activities, together with soft loans and tax allowances. In line with Industry4WRD’s key pillar on inclusive involvement of SMEs, Malaysia has also adopted policy tools specific to SMEs, such as the Readiness Assessment (RA) programme. Using a combination of online questionnaires and on-site visits, an RA is carried out for SMEs that identifies potential gaps; based on its outcomes, SMEs can also apply to reimburse up to 70% of eligible expenditures (up to approximately USD 120 000).

Industry4WRD was developed in co-operation with several different ministries and in extensive consultation with the private sector. The strategy also features multi-ministerial and multi-stakeholder mechanisms in its implementation. MITI oversees and chairs an Industry4WRD council that has stakeholders across government and industry and meets twice a year. High-level task forces under the Council have also been set up, as well as specialised technical working groups led by different ministries and co-chaired by the private sector. These span Funding (Ministry of Finance), Infrastructure (Ministry of Communication and Multimedia), Regulations (MITI), Skills and Talent (Ministry of Human Resources, Ministry of Education) and Technology (Ministry of Science, Technology and Innovation). The high-level task force and working groups meet quarterly.

Source: Rob Cayzer (2020), “Industry 4.0: The experience of Malaysia”, MARA Corporation, Malaysia, presentation at the PTPR Peer Learning Group (PLG) of Egypt “Accelerating the transition to industry 4.0 in a post-Covid-19 landscape”, 10 September 2020.

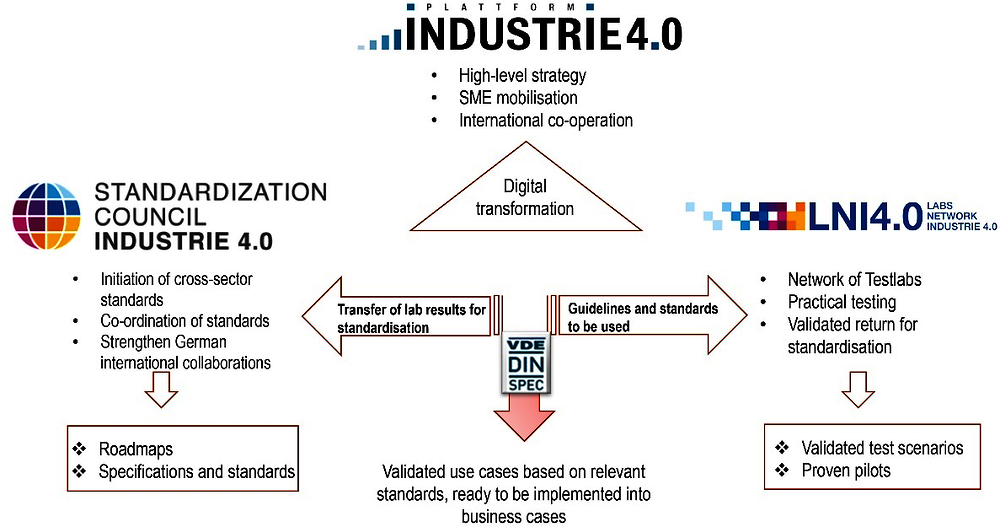

In Germany, standards for Industry 4.0 are created through co-operation among three linked institutions set up to facilitate interactions between the private sector, government, research and civil society (Figure 2.3):

Platform Industrie 4.0: A multi-stakeholder group responsible for elaborating and implementing the country’s strategies regarding Industry 4.0.

Labs Network Industrie 4.0 (LNI4.0). This institution fosters knowledge transfer and develops certifications and benchmarks measurements related to new, disruptive technologies. Validated results from test projects enter the standardisation process through the LNI4.0. The guidelines and standards to be used by the LNI4.0 derive from the Standardization Council Industrie 4.0.

Standardization Council Industrie 4.0 (SCI 4.0). The SCI 4.0 was founded by the German private sector with the aim of proposing standards for digital production and co-ordinating them nationally and internationally. It is an initiative originating from Bitkom (an association for digital economy companies), DIN (the German Institute for Standardization), DKE/VDE (the German Commission for Electrical, Electronic & Information Technologies), VDMA (the Mechanical Engineering Industry Association) and ZVEI (the German Electrical and Electronic Manufacturers' Association). The SCI 4.0 has also taken over the co-ordination between industry players and various European and global standardisation bodies, such as the ITU.

Note: The links to the three platforms are as follows: https://www.plattform-i40.de/PI40/Navigation/EN/Home/home.html; https://www.sci40.com/english/; https://lni40.de/

Accurate measurements for Industry 4.0 are an important part of quality infrastructure. In Germany, the PTB (the National Metrology Institute of Germany) launched a Digitalisation Strategy in 2017 aiming both to digitalise metrological services and to advance the metrology of new technologies. The PTB aims to implement a digital calibration certificate (DCC) that can accelerate the automatisation of the calibration process. The PTB is also working through EURAMET (the European Association of National Metrology Institutes) on a “Metrology Cloud” (i.e. a digital quality infrastructure).

Source: Karl-Christian Göthner, German National Metrology Institute (PTB), background information provided for the PTPR Peer Learning Group (PLG) of Egypt, held virtually, 10 September 2020.

Italy is committed to fostering the transition towards Industry 4.0. With its Piano Transizione 4.0 2020-22 (Transition Plan 4.0), Italy is building on the country’s previous experience to further strengthen the adoption of Industry 4.0 technologies, particularly among smaller firms. The Piano Transizione 4.0 allocated a further EUR 9 billion for 2020-22, combining innovative investments with broad fiscal measures to stimulate Industry 4.0 across Italian firms. It updated, via the National Budget Law 2020 (Law No. 160 of 2019), several existing measures and introduced new ones. The reforms expanded the number of firms eligible for R&D tax credits, brought in new beneficiaries (e.g. higher institutions for training incentives), and broadened the scope of activities for Industry 4.0 to include the circular economy, environmental sustainability and the support of the Made in Italy brand.

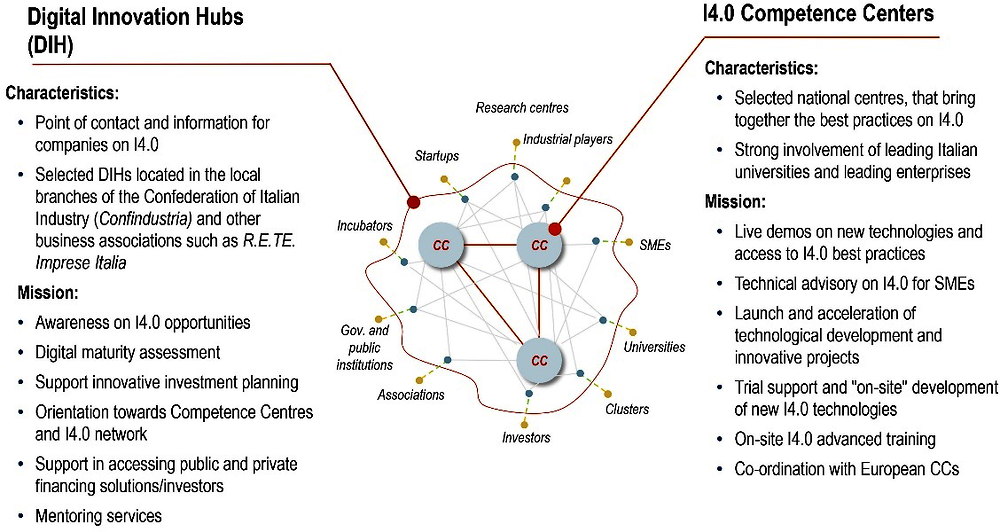

In addition, Italy seeks to strengthen the role of SMEs in Industry 4.0 through the Digital Innovation Hubs (DIHs) and Industry 4.0 (“I4.0”) Competence Centres (Figure 2.4). Overall, the aim of these institutions is to guide companies, particularly SMEs, towards a transition to Industry 4.0 technologies by increasing awareness, providing training and measurement services to entrepreneurs for innovation and research projects, and facilitating access to best-use cases. The core of both hubs and centres is the strong partnerships that build on the long-standing experiences of industrial and business associations and leading national universities.

The DIHs are established within and run by the regional branches of the Italian Confederation of Industry (Confidustria) and other business associations such as R.E TE. (Italian Enterprise Network). They represent the boundaries of the ecosystem through which firms and entrepreneurs are guided and receive mentoring support. The Competence Centres are the nodes of the network and carry out training activities for companies as well as support the implementation of innovation projects, industrial research and experimental development in the area of I4.0. They also provide training, live demonstrations, presentation of best practices, and technical advisory services for SMEs. A public tender process run by the Ministry of Economic Development in 2020 led to the selection of 8 centres hosted by universities and research institutes including the Polytechnics of Turin and Milan; the Universities of Bologna, Padua, Naples (Federico II) and Rome (La Sapienza); the Sant'Anna School of Advanced Studies (Pisa); and the Italian Research Council (CNR). The selected centres receive direct financial support as follows:

Establishing the centre: 50% contribution of expenses incurred, up to EUR 7.5 million.

Launching innovation, industrial research and experimental development projects in co-operation with companies: up to 50% of expenses incurred, up to EUR 200 000 per project.

Source: Paolo Carnazza (2020), “Industry 4.0: The experience of Italy”, Directorate-General for Industrial policy, Innovation and SMEs (DGPICPMI), Ministry of Economic Development, Italy, presentation at the PTPR Peer Learning Group (PLG) of Egypt “Accelerating the transition to industry 4.0 in a post-covid-19 landscape”, 10 September 2020.

Egypt has heavily relied on industrial parks to foster its industrialisation and upgrading. The first industrial parks in Egypt were established following the opening-up reforms started in 1973. Since then, the country has continued to rely on industrial parks within the country’s various zones as tools for fostering local industrial development and attracting foreign direct investment (FDI). More recently, the country has been working to develop the investment attraction and export-oriented growth potential of the Suez Canal through the Suez Canal Economic Zone (SCZone) (Box 2.7). Industrial parks in Egypt follow traditional models. They consist of dedicated land and infrastructure spaces in which firms can access a wide range of services while setting up operations that benefit from the special conditions and incentive packages.

Prior to the pandemic outbreak, Egypt prioritised, as outlined in Egypt’s Vision 2030 national agenda, the building of new industrial parks and increasing investments in old ones as a tool to foster industrial upgrading, boost local development, decrease informality, increase employment, and stimulate trade with Africa and Europe. As part of the national vision, the Industry and Trade Development Strategy 2016-20, launched by the Ministry of Trade and Industry (MTI) in 2016, announced the creation of 22 industrial parks, 13 of which have already been constructed in 12 governorates in industrial zones. A total of EGP 5.4 billion (approx. USD 340 million) has been allocated from the state budget for the creation of the 13 parks. In line with the government priority of fostering local development, most of these have been built in Upper Egypt (9) and the rest are located in the governorates of Alexandria, Al Buhayarah, El Gharbeya and Red Sea governorates. The government estimates that the completed parks will be able to house up to 4 500 companies. The public parks aim to complement efforts by the private sector, which since the mid-2000s has started to build and manage parks within industrial zones in the Cairo region.

Ownership and management of the newly constructed public industrial parks sits with the Industrial Development Authority (IDA), an agency affiliated with MTI. IDA is responsible for selling and renting units in constructed parks; issuing all relevant licenses, approvals and permits; and releasing land, providing infrastructure, and granting licenses to private park developers for the establishment and management of private industrial zones. The parks benefit from the incentives stipulated in Egypt’s Investment Law No. 72/2017 as well as additional incentives by IDA, such as facilitating land payments in instalments and partial exemptions from licensing fees for micro and small projects. Following a Memorandum of Understanding (MoU) between IDA and MSMEDA to co-operate on industrial parks in 12 governorates, MSMEDA is responsible to provide financing for the implementation of small industrial projects and a package of non-financial services, such as market and training services.

Compared to previous efforts, Egypt’s current policy for industrial parks is more targeted and specialised, and now prioritises continental value chain development. Whereas previously industrial parks mostly attracted firms with no specific industrial or sectoral focus, the current policy seeks to attract firms operating in the same value chain with a view to leveraging the co-location in the park to develop specialised industrial clusters and foster co-ordination between firms. These efforts complement other initiatives as the Leather special zone in the Robeky area located in the Eastern side of Greater Cairo and one for furniture in New Damietta.

Industrial parks are costly projects that require multi-year financing. Development banks are thus key partners in implementing effective industrial park project development. The Africa Import-Export Bank (Afreximbank), a pan-African multilateral trade finance institution created in 1993 under the auspices of the African Development Bank, actively supports industrial parks on the continent. Afreximbank’s vision is to stimulate Africa’s trade diversification and increase the continent’s share of global trade. The bank holds approximately USD 15 billion in assets and has 51 participating member states. Supporting the development of industrial parks and special economic zones forms a core part of Afreximbank’s strategy to foster structural transformation in Africa. In fact, the Bank aims to create 3 000 hectares of industrial parks and SEZs across sub-regions by 2021 (Box 2.8).

Egypt has been actively promoting investments in mega projects as part of Egypt’s Vision 2030 to create jobs and achieve sustainable growth, but also to better integrate itself in the global economy. One of the projects that stands out as a priority is the development of the Suez Canal Economic Zone (SCZone). Established on 461 km² of land, which encompasses six maritime ports, it is strategically located along the international waterway of the Suez Canal. It aims at reinforcing the position of the Suez Canal as a global maritime trade route, and exploiting its potential for investment attraction and export-oriented growth. With annual traffic of over 17 000 vessels of around 10% of global trade, the Suez Canal represents a major trade route between Europe and Asia as well as Europe and all of Africa.

The SCZone has recently developed a Strategy for 2020-25 to become an international investment hub and an export platform with a distinctive access to African markets. To support the implementation of the Strategy, the SCZone relies on several value propositions, namely the set-up and ecosystem readiness, regulatory framework, financial incentives, provision of services, and the cost advantage. The SCZone has four industrial zones (Sokhna, East Ismailia, Port Said, and Qantara West industrial zones), targeting various types of manufacturing investments within a wide range of industrial clusters. While it has a focus on maritime-related services, it is also striving to provide an attractive investment environment for medium, light and heavy manufacturing industries as well as higher value-added services such as renewable energies and information and communication technology. Other sectors that are targeted include pharmaceuticals, agribusiness, textiles and consumer electronics.

The Covid-19 health and economic crisis may have important implications for the SCZone’s future investments. While the future remains uncertain, it may affect multinational enterprises (MNEs) decisions to reorganise the geographical and sectoral spread of their production activities, providing possible opportunities for the SCZone. MNEs could shorten their supply chains and reduce the distance between suppliers and clients, or choose to move manufacturing activities back to their home country. Some companies may diversify their supply networks in order to increase resilience to shocks, which will involve divestments from some locations but expansion in others, providing opportunities for Egypt in sectors such as electronics and electrical equipment (see Chapter 3). For the SCZone, such changes will also require a rethinking of investment strategies and business climate reforms to manage investor expectations, new sectoral prioritisation and better targeting, as well as improved investment facilitation through digitalisation.

Source: OECD (2020[4]; 2020[5]), N Gage Consulting (2016[6]) and SCzone (2021[7]).

To foster the creation of industrial parks in Africa, Afreximbank offers five instruments:

Project finance for Industrial Parks and Special Economic Zones (SEZs): These programmes seek to provide debt financing for developing industrial parks and SEZs, covering infrastructure development both within and outside of “the fence”. One example is the USD 1 billion China Africa industrialization Programme (CAIP) jointly developed by Afreximbank and China Eximbank in 2016 to provide debt financing for the design and construction of parks and SEZs, the establishment of manufacturing facilities within them, and the development of logistics and trade-facilitating infrastructure.

Afreximbank’s Project Preparation Facility (APPF): APPF supports public and private sector entities in preparing projects that will attract equity and debt finance. Structured as a self-sustainable revolving fund operated on commercial terms, APPF finances activities such as advisory services, technical studies and assistance.

Trade finance facilities: These facilities can support export trading companies (ETCs) within industrial parks with letters of credit, pre-export finance, payment guarantees, factoring solutions, stocking and inventory financing, export credit insurance and packing credit.

Fund for Export Development in Africa (FEDA): Through FEDA, Afreximbank intervenes in the form of equity or quasi-equity to support, among others, companies in industrial parks and ETCs.

Advisory services: This instrument provides advice to promoters of projects related to capital market and debt solutions, as well as to trade information, investment promotion and market access.

While the Bank’s initiative to promote industrial parks in the continent is recent, some projects are already bearing fruit. In Gabon, Afreximbank has provided financing for the Gabon Special Economic Zone (GSEZ). The GSEZ, a joint venture between Olam International, the Republic of Gabon, and Africa Finance Corporation, was established in 2010 and is focused on timber processing and furniture, with approximately 1.2 million cubic meters exported annually. In 2018 Afreximbank provided a USD 35 million revolving trade financing facility to CDC Gabon, which manages GSEZ, to provide tenants with the capital needed to process timber for exports. Additionally, Afreximbank provided a bond-backed medium-term loan for the extension of a railway line from the GSEZ to the Owendo International Port and the GSEZ mineral port in Gabon. The increased transport connectivity for GSEZ is expected to reduce the cost of production and exports. Afreximbank is in advanced talks to finance the development of more parks in Côte d’Ivoire, Nigeria, Burkina Faso and Benin, and is exploring opportunities in Togo, Ghana, Rwanda and Kenya.

Source: Tania Katanga (2020), “Relevance of Industrial Parks and Special Economic Zones in a Post COVID 19 World”, Afreximbank, presentation at presentation at the Peer Learning Group Meeting of the PTPR of Egypt, held virtually on 21 April 2020.

Putting industrial parks to the task of combatting COVID-19 has been a key dimension of the response to the pandemic of big manufacturing hubs, such as the People’s Republic of China (hereafter “China”) and India. Both countries have faced the twin challenge of meeting steep domestic demand in PPE and ventilators, while ensuring that production takes place in a safe way, and industrial parks have contributed on both counts. Egypt has also been facing the challenge of making the parks work during the pandemic.

While there is no blueprint for effectively mobilising industrial parks during a pandemic outbreak, some lessons can be learned, from Egypt and other countries:

Safeguard workers’ health. While prioritising the reopening of industrial facilities in many countries exiting the lockdown, ensuring workers are not at risk and contagion is minimised is essential. The availability of protective equipment, disinfectants and spaces for quarantining workers (if needed) is critical, as is the observance of social distancing rules. Industrial parks should also closely monitor the state of the epidemic within their premises so that they can adapt quickly.

Make use of available policy space to ensure speedy response. In these exceptional circumstances, governments are stepping in to quickly deploy adequate resources and fight the pandemic. Countries have put in place a wide range of fiscal and financial measures to promote the manufacture of COVID-19 related products, such as guaranteeing procurement, tax discounts, fast-track customs clearance and mobilisation of public sector firms (Box 2.9). Egypt, too, has put in place various measures to support firms and workers during the pandemic, including facilitating licensing for factories that provide medical supplies (MPED, 2021[8]).

Bring stakeholders together to foster collective action. Responding to COVID-19 requires not only speed, but also the co-ordinated efforts of many different stakeholders. Industrial parks could exploit their institutional and physical structure to foster dialogue and co-operation between scientists, government and manufacturers. Multi-stakeholder special task forces, and crisis committees within industrial parks or between industrial parks and other actors, could help in this respect.

Have realistic expectations. Scale-ups and industrial reconversions are not easy. It takes time to learn to manufacture a new product, even in good times, let alone in the middle of a pandemic that has caused disruptions in supply chains and the movement of personnel. Facilitating learning among firms, particularly those from countries that have already successfully engaged in reconversions, could help make this process faster and more effective. It is also important to continue minimising the risk to human life from newly produced equipment by maintaining vigilant regulatory oversight.

In China, the public sector has undertaken a three-pronged response encompassing (a) worker safety, through the use of digital applications and availability of disinfectants and PPE; (b) co-ordination along the value chain, by undertaking frequent on-site visits and making standards freely available online; and (c) targeted policy support to encourage producers to scale up production of key equipment and supplies (Table 2.2). In Tamil Nadu, India’s top state by number of factories, in addition to incentives for producers, the state’s response has also focused on managing the phased resumption of manufacturing activities, through a dedicated task force headed by the chief secretary and with the participation of several government departments. The task force is responsible for providing clearances for industrial establishment, facilitating investments and co-ordinating procurement of supplies.

Industrial parks play an important role in Egypt’s industrial and innovation ecosystem. Based on the comparison with the experience of other countries, the following are some areas for policy reforms that Egypt should consider going forward:

Building and managing industrial parks is a tool, not an objective per se. Using industrial parks for local development works when these are managed as part of the overall production transformation strategy. Industrial parks can be a useful tool for harnessing the space-based nature of industrial and technological activities to foster knowledge creation and diffusion and help firms capture economies of scale. However, to succeed, the aims of industrial parks need to be aligned with other important agendas, such as those of trade, innovation, sustainability and regional development. Viewed in isolation, industrial parks risk becoming expensive projects that fail to attract investments or reach their expected objectives. Alignment helps to target scarce resources towards achieving a common vision for industrial parks, from the provision of hard and soft infrastructure to the right policy package that could enable diversification and upgrading. In Korea and Malaysia, industrial parks have been used to meet the countries’ changing needs, from deepening integration with GVCs to upgrading and boosting innovation (Box 2.10). Egypt, too, could look to combine existing measures (such as allocating industrial land and reimbursing infrastructural work) with policies and tools to encourage firms to invest in modernising their technologies; in innovation, including digital technologies; and in adopting environmentally-friendly technologies – all part of the country’s vision of production transformation for the future.

Fostering learning in local firms. Industrial parks often focus overwhelmingly on only attracting investments. While this can yield successful results in the short term, sustaining competitiveness in the long term requires complementary efforts to spur learning and innovation. Policies to foster linkages between firms inside and outside the parks, expand investments along the value chain, encourage technological upgrading and build a skilled workforce are crucial for ensuring that parks can survive beyond initial advantages that can quickly become eroded, such as low-cost labour. In Egypt, park management can be critical in this respect, by focusing not only on infrastructure but also on facilitating firms’ access to much-needed resources to innovate, such as specialised services, financing and networking. Moreover, dynamism can be encouraged by designing parks in a way that avoids turning them into monocultures. Parks in Egypt could aim instead to foster diversified environments that can bring together more than just one type of firm, including SMEs and large firms, both foreign and local. Setting up dedicated incubators for start-ups could also help foster innovation and linkages among firms. Long-term sustainability also requires withstanding crises, such as the current pandemic. Parks can contribute to dealing with future crises by designing supply-chain risk-management measures together with park tenants.

Building specialised industrial parks can help the economy find its brand. Specialisation can also help build a country’s image and reputation, important drivers of investments in a country’s industrial parks. Generating a positive image of parks by firms operating there and other stakeholders involved in management and promotion (e.g. park managers and administrators, ministries, local governments, promotion agencies and others) is essential for continuing to attract high-quality investments and becoming a desirable destination for skilled labour. However, as parks have proliferated across industrialising countries in an effort to attract investments, it is becoming harder to market them – that is, to project a value proposition that will win over investors. Park-specific branding in Egypt can enable signalling the key attractiveness factors of each park. For example, in Tamil Nadu, in India, the government is relying on the expertise of the private sector, combined with government support, to create a park that will be India’s first high-tech one-stop shop for medical equipment manufacturing (Box 2.11). In addition, India’s Department for Promotion of Industries and Internal Trade (DPIIT) has piloted an Industrial Park Rating System (IRPS) that can signal to investors which parks follow best practices and promote competition among the many developers (Mitra et al., 2020[10]). Country branding can serve as an umbrella to position Egypt’s parks as destinations for industrial investments in Middle East and Africa.

Korea and Malaysia share similarities when it comes to the role of industrial parks in development. Malaysia followed a development model inspired by that of Korea and other successful Asian economies, aiming to harness foreign direct investment (FDI) and exports to fuel a process of local industrial capability building. In both cases, the ambition of industrial parks increased over time to reflect the countries’ changing priorities as incomes increased and new development frontiers matured. Moreover, new public institutions were pioneered to enable the alignment of parks to the goals of national transformation policies.

Korea: Fom light to heavy industries and innovation

Korea has experienced one of the world’s most successful and rapid economic development transitions, going from a largely agriculture-based economy in the 1960s to a leading industrial power today. The country’s GDP per capita rose from USD 944 in 1960 to USD 26 762 in 2018 (2010 constant prices). Korea’s transformation was sustained by industrialisation, the shift from light to heavy industries, integration into world markets, and investments in developing innovative capabilities.

Industrial parks have been a component of Korea’s development. The first parks were built in Ulsan in the early 1960s for chemicals and fertilisers. These were followed by parks in the Capital Region and the south and southwestern regions in the mid-1960s, aimed at facilitating investments in export-oriented industries, particularly textiles and later also electronics, machinery and metals. As the policy focus shifted to heavy industries in the 1970s, the development of iron and steel and petrochemical industrial parks became established. At the same time, electronics also developed at a rapid pace, particularly of upstream components such as semiconductors. In the 1980s and 1990s, industrial parks continued to be built in western coastal areas to promote balanced regional development. Since the mid-1990s integrated “techno parks” have been being promoted to stimulate regional innovation systems. In each phase, legal provisions and targeted incentives were employed to ensure investments matched the goals of the parks.

This phased approach enabled Korea to make its big conglomerates globally competitive. This is mirrored by the trajectory of Korea’s share of foreign value added (FVA) in exports. In the 1970s it was high, reaching some 35%, reflecting that most inputs were imported and the country lacked the necessary skills to produce domestically core components. As the country was able to increasingly localise production of intermediates, the share of FVA in exports fell to a low of 28% in 1993. Since the mid-1990s this process has reversed, with FVA increasing again to reflect the internationalisation process of Korea’s leading firms as they shifted production of simple parts and assembly overseas.

Malaysia: From concentration in Penang to country-wide development

Malaysia has sustained a successful process of structural transformation since independence in 1957. The country’s GDP per capita doubled from USD 5 200 in 1970 to USD 10 858 in 2018 (constant 2010 prices). Within 30 years, Malaysia not only developed extensive palm oil and petrochemical industries, but also progressed from labour-intensive assembly to developing a nucleus of local firms that are globally oriented. Industrial parks have been instrumental in achieving Malaysia’s production transformation, serving as hubs for developing leading capabilities in manufacturing electronic components as well as developing services, such as Islamic banking. The country now has 500 industrial estates or parks and 18 free industrial zones.

The role of industrial parks has changed over time, reflecting Malaysia’s changing development priorities. In the 1970s, parks in Malaysia, mainly in Penang, focused on attracting FDI in the export-oriented assembly of electronic components. Over time, activities promoting information technologies (IT) and innovation were encouraged. The regional focus also shifted, from concentrating infrastructure in Penang to expanding to other states and then to larger “corridors” that span different states. Thus, the development of parks followed the “economic veins” of the country, expanding gradually as economic poles expanded into less developed regions. The different development phases are highlighted in the following table:

Institutional development has been crucial in providing a link between strategy and parks in Malaysia. The country’s federal government works closely with implementation agencies and state-level governments and bodies to ensure that parks are aligned with the country’s development agenda and meet evolving investors’ needs, notably though the following institutions:

The Ministry of Trade and Industry (MITI) is responsible for developing the country’s industrial, trade and investment policies, in line with the country’s national development plans.

The Malaysian Investment Development Authority (MIDA) was established in 1967 to promote foreign and later also domestic investments in manufacturing and services. MIDA acts as a one-stop shop for investors in all of Malaysia’s parks and zones and provides investment incentives in line with MITI’s policies.

State Economic Development Councils (SEDCs) were established by state governments in the 1960s to promote regional development. SEDCs are public enterprises and follow different models, with some focusing on acquiring corporate equity and others on developing industrial parks and other infrastructure to promote private business.

Source: Rob Cayzer (2020), “Industrial Parks: The experience of Malaysia”, MARA Corporation, and Kuen Lee (2020) “Industrial Parks and COVID-19: Commentaries”, Seoul National University, Korea, presentations at the Peer Learning Group Meeting of the PTPR of Egypt, held virtually on 21 April 2020; and OECD (2012[11]), Industrial Policy and Territorial Development: Lessons from Korea, Development Centre Studies, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264173897-en.

Tamil Nadu, a state in southern India that is one of India’s industrial powerhouses, has the largest number of factories in the country. The State Industries Promotion Corporation of Tamil Nadu (SIPCOT), a government-owned institution established in 1971 to promote industrial development in the state, has been instrumental in this respect by developing industrial land and acting as a nodal unit for disbursing state-level assistance to large industrial units. To date, SIPCOT has developed 21 industrial parks and 7 special economic zones (SEZs), spanning 130 square kilometres. Apart from SIPCOT-developed infrastructure, Tamil Nadu also features:

Industrial estates targeted at micro, small and medium enterprises (MSMEs), developed by the Small Industries Development Corporation Limited (SIDCO);

Industrial parks developed by the Tamil Nadu Industrial Development Corporation (TIDCO);

Unorganised industrial infrastructure where landlords lease lands for industrial use.

To increase industrial development in lagging areas of the state, SIPCOT is now partnering with the private sector in developing industrial parks through the creation of joint ventures. The private sector offers land (at least 100 acres) and develops all internal infrastructure (such as internal roads) and the government provides utilities and trunk infrastructure, in addition to policy incentives (50% exemption on stamp duty and permission to use open-space reservation areas and roads for non-industrial purposes).

It is intended that Tamil Nadu’s industrial parks deepen the state’s industrial specialisation in specific value chains and help realise the aims of the nationwide “Make in India” campaign. One of the parks is HHL Medipark (HML), currently under construction, which will be one of the country’s first parks dedicated specifically to medical equipment. Support for the creation of the park comes from the Department of Pharmaceuticals under the Ministry of Chemicals and Fertilisers through a scheme for the development of the pharmaceutical industry. Under the scheme, the central government will cover up to 70% of the project cost (up to USD 335 000). Medipark will be developed by a joint venture created by HLL Lifecare Limited and TIDCO, with HLL developing the internal infrastructure and undertaking the leasing of plots. Tamil Nadu plans to make Medipark into a one-stop-shop high-tech manufacturing cluster that integrates industrial, commercial and business facilities.

Source: Sri Ramya Y, (2020), “Creating Resilient Industrial Ecosystems”, Guidance Tamil Nadu, Government of Tamil Nadu, presentation at the Peer Learning Group Meeting of the PTPR of Egypt, held virtually on 21 April 2020.

Egypt’s production system faces multiple challenges today that have been compounded by the disruptive effects of COVID-19 on manufacturing, commercial services and trade. On the one hand, Egypt needs to create more and better jobs (see Chapter 1). On the other hand, the prevalence of informality leave a sizeable share of Egypt’s population vulnerable to the impact of the pandemic as they have lower access to welfare and health services. Currently, the rate of informality is estimated at 63.4% of the employment. Although that is the fourth-lowest in Africa, it is still high compared to advanced economies, where the incidence is more than three times lower (around 18%) (ILO, 2021[12]). In addition, the pandemic is placing stress on Egypt’s production system through two main channels of transmission:

Lower tourist receipts: Tourism has been one of the worst-affected activities globally during the current pandemic, falling by 72% during January-October 2020 (World Tourism Organization, 2020[13]). During the pandemic, the Egyptian tourism industry, like in other countries, suffered large losses. Egypt welcomed 13 million tourists in 2019, but arrivals declined by 69% during the first half of the year. Tourism has recovered somewhat since the country opened up for international travellers on 1 July 2020, but revenues remain lower than pre-pandemic levels (CBE, 2021[14]). However, the future of the tourism industry remains highly uncertain and will depend on the success of vaccination campaigns globally, the severity of successive waves of the pandemic as well as on changing consumer preferences.

Disruptions in production and trade: Production and trade were severely disrupted globally owing to a combination of government measures to restrict social contacts (to stem the epidemic) and low consumer demand as economies came to a halt. The fall in world trade volumes also affected Egypt through lower receipts from Suez Canal, which declined by 2.88% in 2020. Canal revenues accounted for as much as 1.6% of GDP during fiscal year 2019/20 (CBE, 2021[14]; Ministry of Planning and Economic Development, 2021[15]).

To achieve Vision 2030 and the National Structural Reforms Program (NSRP) and maintain its path towards prosperity, Egypt will need to mobilise investments that address these challenges. Egypt reacted quickly to mitigate the economic effects of the pandemic and showed resilience. The country has mobilised large resources – the COVID-19 stimulus and recovery package in Egypt accounts for 1.9% of the country’s GDP (IMF, 2021[16]) – and has put in place a wide range of policy measures to protect the population from the virus, especially vulnerable groups, and stem its spread; maintain macroeconomic stability and preserve growth; and increase the capacity of the economy to react to future shocks (MPED, 2021[8]). In total, 541 policies have been implemented by more than 80 institutions. Supporting the Egyptian economy and the affected sectors represents 36% of actions taken, while 31.6% have been targeted to individual support, 26.8% to containing the virus, and 5.7% to international co-operation (ibid.).

Beyond the fiscal stimulus, the country also employed a range of tax breaks and deterred tax collection measures, as well as monetary ones, such as lower interest rates, loan repayment deferrals and credit support to several sectors that were heavily affected, such as tourism, industry, agriculture and construction (see Table 2.3 for selected measures to support businesses). In addition, the government expanded the conditional cash transfer programmes (e.g. Takaful and Karama) and introduced programmes to support irregular workers. Several government ministries and agencies also reacted quickly to offer services on line and facilitate social distancing, increasing the scope for digital services in the economy in the process. For example, MSMEDA’s SME platform allows firms to access online entrepreneurship training and marketing services, while MCIT co-operated with other government agencies to provide healthcare and educational services on line and with internet service providers to increase the quota of home Internet subscribers by 20% to tackle increased browsing needs. The country maintained positive growth during 2020 compared to a contraction globally, in Africa and MENA (see Chapter 1). Unemployment, too, which climbed to 9.6% in the second quarter of 2020, compared to an annual rate of 7.9% 2019, fell back down to 7.3%-7.2% during the rest of the year (CAPMAS, 2021[17]).

This large mobilisation of resources could be used to ensure not only that firms stay in business, but also that long-standing challenges are addressed and new opportunities from the shifting global landscape captured. Other countries have answered this call by putting in place novel instruments since the crisis. For example, Malaysia is looking to capture the benefits of increasing relocations in investments worldwide by attracting a growing share of investments, through a special incentive for relocations. It offers a 0% tax rate for 10-15 years for investments over RM 300 million (approx. USD 74 million), providing a manufacturing operation is relocated from another country to Malaysia. Egypt could similarly combine measures for supporting businesses with conditions and incentives for further fostering production transformation.

In addition to mobilising resources to cushion the impact of the pandemic, Egypt, like all countries, needs to use this support as a means of shifting the economy towards more sustainable and inclusive production and consumption modes. A major global reorganisation of production and trade is taking place, and Egypt needs to take every opportunity to benefit from it and emerge stronger.

Egypt fosters the development of domestic industrial capabilities mainly through the following incentives, among others:

Fiscal incentives. Egypt’s Investment Law No. 72/2017 offers fiscal incentives in the form of various customs tax and duty exemptions and reductions for all new investment projects, and added investment tax allowances (ITA) (between 30% to 50%) for investing in specific regions and sectors, including in export-oriented projects. The sectoral prioritisation under the law is broad, including almost all manufacturing sectors. Prior to the law’s adoption in 2017, Egypt offered almost no fiscal incentives for manufacturing projects that were not export-oriented (such as those based in special zones, discussed later in this section). Additionally, the law has clarified regional priorities to promote the development of lagging areas. Finally, according to MSME Law No. 152/2020, MSMEs are eligible for (a) tax exemptions for capital gains resulting from the sale of assets and machinery (if the proceeds are used to purchase new assets) and (b) free, discounted or reimbursed expenses such as for land and infrastructure costs (utilities installation). MSMEDA also provides discounted financing for industrial projects.

Local content requirements. Local-content rules have been used in Egypt to foster domestic capabilities in various industries. Currently, Decree No. 571/2019 by MTI has put the local content manufacturing ratio at 45% for licensing domestic automotive assembly operations. Additionally, Law No. 72/2017 specifies that projects with more than 50% local content may be eligible for additional investment incentives.

Provision of specialised infrastructure. Industrial parks and zones have been developed in Egypt with the purpose of promoting local industry, particularly SMEs. They are managed by the Industrial Development Authority (IDA) and are subject to Law No. 72/2017. Companies may also benefit from incentives granted by the MSME Law and business facilitation by IDA.

Egypt fosters exports mainly through the following incentives: