2. Uzbekistan’s net-zero challenge: Macroeconomic and environmental state of play

This chapter provides the necessary context to understand the scale of the challenges that Uzbekistan faces in pursuing its green transition and the gap between available financing and the estimated sums required. Uzbekistan’s economy is dynamic and growing, but also highly energy- and GHG-intensive. The Government of Uzbekistan has set ambitious targets for the country in terms of economic development and climate change mitigation, but the scale of the economic transformation required to meet these targets requires sizeable investments, particularly in infrastructure. This transition will necessitate a major shift in Uzbekistan’s existing infrastructure systems, especially its fossil fuel-reliant energy sector. By facilitating private investment, including from international sources, in projects that satisfy growing demand for infrastructure services without exacerbating existing environmental problems, Uzbekistan has an opportunity to establish itself as a regional leader in sustainable development. Such projects could, for instance, seek to harness Uzbekistan’s large renewable energy potential.

Uzbekistan’s economy is growing rapidly and has proven resilient to recent external shocks, including the COVID-19 pandemic and Russia’s invasion of Ukraine. Prudent debt management and market reforms have improved the country’s investment climate.

Uzbekistan’s economy is highly energy-intensive and, given the reliance of Uzbekistan’s energy system on fossil fuels, GHG-intensive. The economy is dominated by large state-owned enterprises, and the country is highly reliant on natural gas, its domestic reserves of which are nearing exhaustion.

Given the potential for renewable power generation, particularly solar, there is considerable scope for Uzbekistan to cut its GHG emissions in line with its commitments under the Paris Agreement (-35% reduction in GHG intensity of the economy compared to 2010 levels) by rapidly increasing the share of renewable energy sources as well as boosting energy security and improving and greening infrastructure in the energy, transport and other sectors.

Uzbekistan has set 2030 targets for inter alia reducing the GHG intensity of the economy (-35% compared to 2010 levels) and renewable energy integration (25% of TPES). It also aims to reduce the state’s share in the national economy and develop the domestic capital market. However, Uzbekistan’s strategies lack credible costing information and financing strategies.

Uzbekistan has not yet adopted a comprehensive economy-wide net-zero target and supporting long-term low-emission development strategy.

Given the magnitude of the investments needed (at least USD 6 billion annually), domestic public financing is insufficient for Uzbekistan to achieve the SDGs and its climate and development ambitions.

2.1.1. Macroeconomic overview

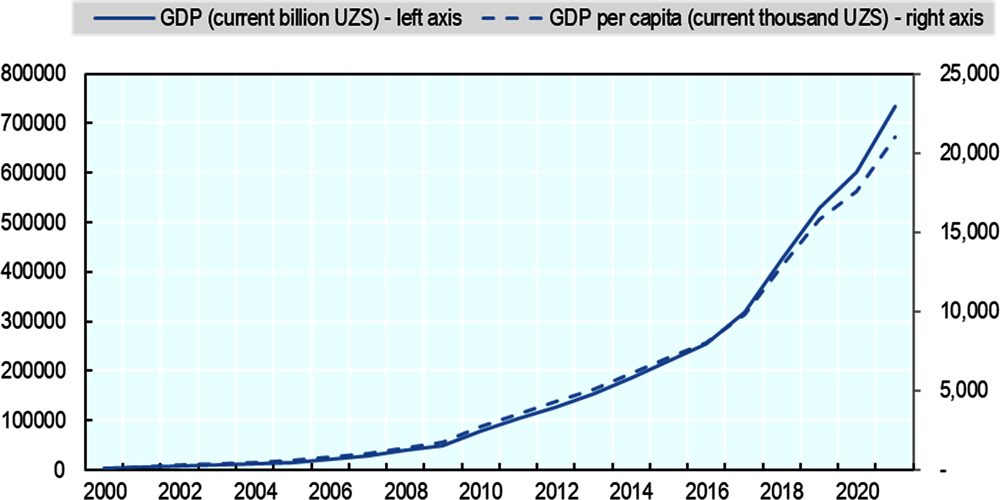

Uzbekistan’s economy has experienced rapid, sustained growth since achieving independence from the Soviet Union in 1991, with GDP and GDP per capita increasing by about 3.7 and 2.6 times respectively since 2010 (see Figure 2.1). Its economy, the second largest in Central Asia after neighbouring Kazakhstan’s, grew by over 6% on average annually between 2010 and 2019 (World Bank, 2023[1]) driven by growth in commodity exports, foreign investment, industry, services and the private sector as well as stable demographic growth of about 1.7% on average since 2000 (UNECE, 2020[2]). Rapid growth returned in 2021 (+7.4%) following brief dip due to the COVID-19 pandemic in 2020 (+1.9%). Since 2017, Uzbekistan has undertaken a raft of ambitious reforms, opening the country up to foreign trade, liberalising prices, abandoning the long-held peg on the Uzbek sum (UZS)’s value on foreign exchange markets and granting greater operation independence to the Central Bank of Uzbekistan (Al Rasasi and Cabezon, 2022[3]).

Source: World Bank (2023[1]), World Bank Indicators Database, https://data.worldbank.org/indicator

State dominance is a central characteristic of Uzbekistan’s economy. 2 800 state-owned enterprises (SOEs) are under direct central government control, and they are responsible for 18% of employment, 20% of exports and approximately 50% of GDP. The outsized role played by SOEs across most sectors of the economy, including the energy, finance, transport and agriculture sectors, stifles competition and the emergence of more innovative firms, leads to misallocations of labour and capital, slows private sector development and burdens the state budget. Uzbekistan has made progress on strengthening corporate governance with a view to privatise many of its SOEs in the coming years, notably through the introduction of governance by supervisory boards including independent board members. However, the central government still maintains the power to appoint and dismiss SOE CEOs and civil servants are overrepresented in supervisory boards (World Bank, 2021[4]).

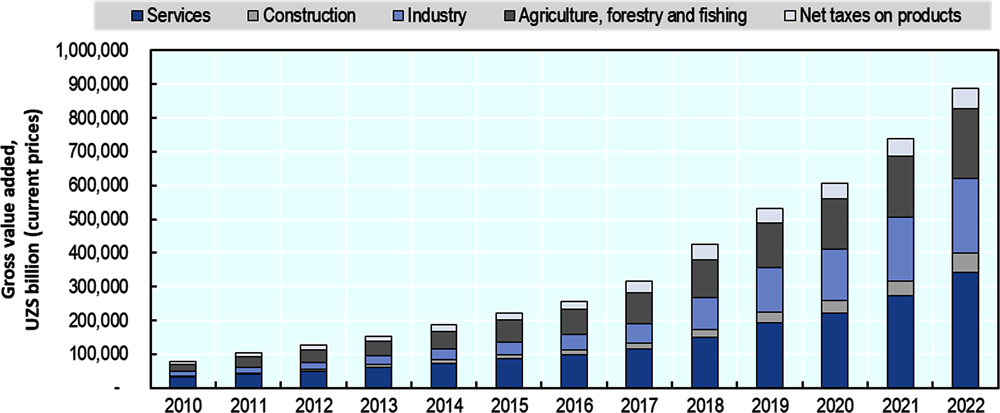

Services account for the largest share (39%) of Uzbekistan’s GDP followed by industry (25%) and agriculture (23%). The service sector’s share of GDP has remained broadly stable over the past two decades, while industry’s share has grown (from 16% in 2010) and agriculture’s has declined slightly (from 27% in 2010) (see Figure 2.2). Uzbekistan’s industrial sector includes several greenhouse gas (GHG)-intensive industries, such as natural gas production, cement production and chemicals production (including ammonia and nitric acid, primarily used in fertilisers). Agriculture employs about 27% of Uzbekistan’s population, particularly in rural areas where the figure is closer to 60%. As a whole, the agricultural sector in Uzbekistan has been progressively modernised, with increasing productivity thanks to crop diversification (notably away from cotton monocultures), land rehabilitation and increased mechanisation (Uzhydromet, 2021[5]). The informal sector plays a large role in Uzbekistan’s economy, particularly the service and agriculture sectors; it is estimated that in 2019 the informal economy was equal to 40-50% of the country’s GDP (Hamidov and Davletov, 2020[6]).

Source: UzStat (2023[7]), “Volume of gross domestic product by types of economic activities”, https://www.stat.uz/en/official-statistics/national-accounts.

Since Uzbekistan began opening its economy more to foreign trade, the country’s trade balance has been negative and declining, reaching USD 11.4 billion in 2022. Uzbekistan’s primary trade partners are China and Russia, each of which accounts for approximately 15% of exports and 20% of imports. Other important trading partners are Kazakhstan, Turkey, Korea and Kyrgyzstan. Gold is Uzbekistan’s single largest export product, accounting for 21% of exports. The largest category of exports, however, is industrial goods – including cotton yarn for textiles – (23%), followed by services (21%), food products (8%) and fuels and lubricating products, including natural gas (6%). While most of Uzbekistan’s export products are raw materials or basic manufactures, many of which are emissions-intensive, Uzbekistan has a growing car and bus manufacturing industry, including for electric vehicles. Manufactures and finished products account for the majority of Uzbekistan’s imports, primarily machinery and transport equipment (31%), industrial goods (19%) and chemicals (19%) (UzStat, 2022[8]).

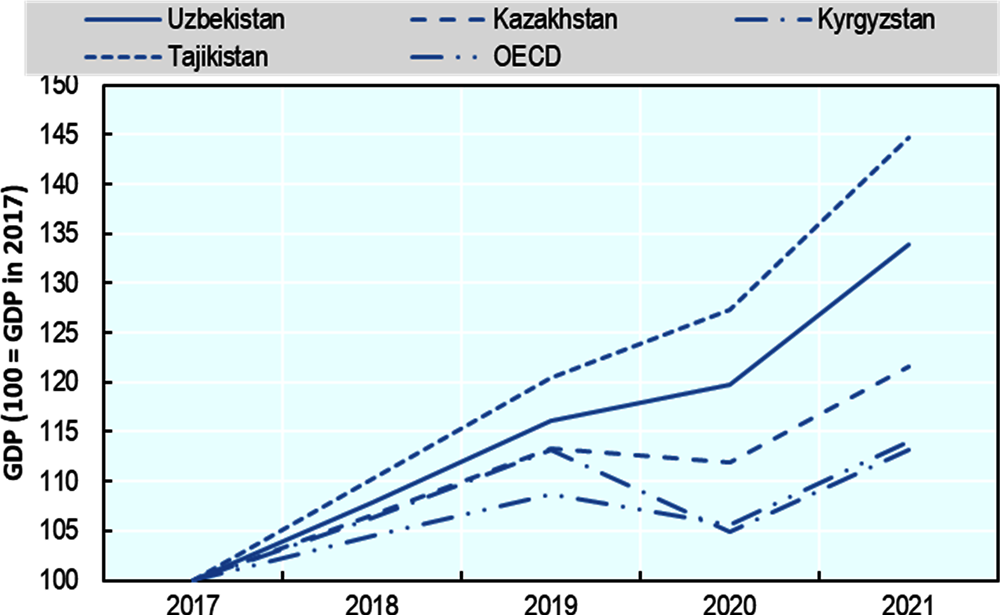

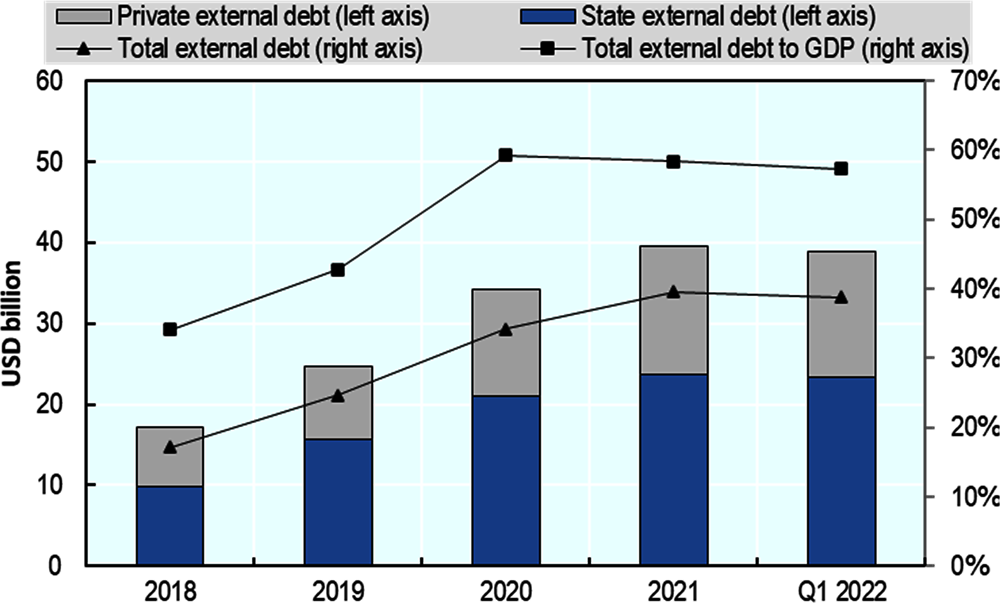

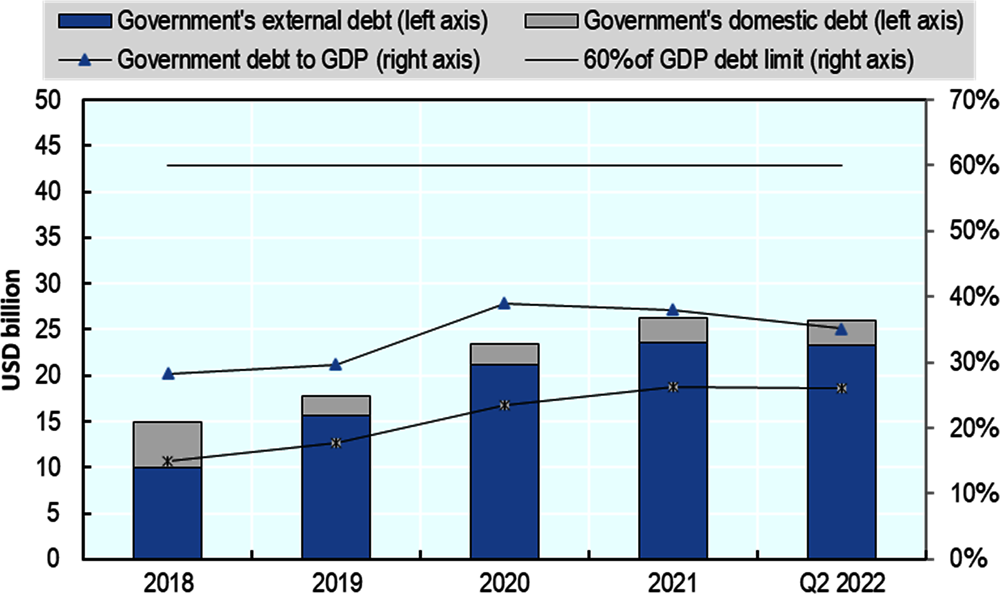

According to the IMF, Uzbekistan’s economy is expected to continue growing at rates of about 4.5-5% until at least 2027 (IMF, 2022[9]). The economy has proved resilient to recent external shocks, notably the COVID-19 pandemic and the effects of Russia’s invasion of Ukraine (see Figure 2.3), in part thanks to its low levels of government and external debt (see Figure 2.4 and Figure 2.5), a low and declining budget deficit (about 4.8% in 2022), sizeable international reserves (USD 33.5 billion for 2023-24), sizeable domestic energy resources and its somewhat limited integration in international financial markets. The government has also continued to bolster resilience to economic shocks through fiscal consolidation (including through formalisation of the country’s large informal economy and improvements to tax efficiency) and strict controls on public debt (e.g. the Law on Public Debt, which introduces a public debt ceiling of 60% of GDP, annual borrowing limits and required corrective measures if debt rises above 50% of GDP). Uzbekistan’s competent debt management strategy has contributed to the country’s rise to a BB- sovereign credit rating (as of 2023, according to Standard and Poor’s and Fitch Ratings, both with stable outlooks). Although a BB- rating classifies Uzbekistan’s credit worthiness as non-investment grade speculative, it places Uzbekistan in the same category as Brazil, Georgia and Greece (Investment Promotion Agency, 2023[10]).

Source: World Bank (2023[1]), World Bank Indicators Database, https://data.worldbank.org/indicator.

Source: Ministry of Finance of Uzbekistan (2022[11]), The State Debt of the Republic of Uzbekistan for the 1st Quarter of 2022, https://api.mf.uz/media/post_attachments/1kv_2022_eng.pdf.

Source: Ministry of Finance of Uzbekistan (2022[11]), The State Debt of the Republic of Uzbekistan for the 1st Quarter of 2022, https://api.mf.uz/media/post_attachments/1kv_2022_eng.pdf.

2.1.2. Environmental challenges

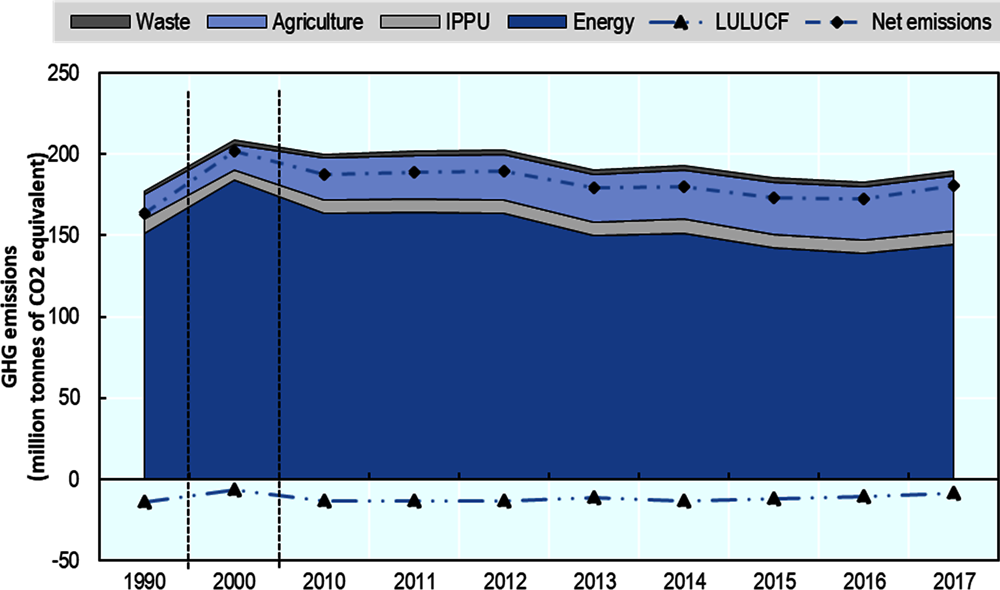

Uzbekistan's economic successes have come at great environmental cost. Uzbekistan’s total greenhouse gas (GHG) emissions are the second largest in the region after Kazakhstan, and its emissions per unit of GDP are the fifth largest in the world (World Bank, 2022[12]). Uzbekistan’s economy is also highly energy-intensive (8.36 MJ per 2017 USD PPP according to 2019 IEA data, the second highest in the region after Turkmenistan) (IEA, 2022[13]). Consequently, energy accounts for the vast majority of Uzbekistan’s GHG emissions, led by electricity generation from Uzbekistan’s primarily gas-fired thermal power plants (see Figure 2.6). Natural gas accounts for 82.7% of the country’s total energy supply (TES), followed by oil (9.5%) and coal (6.4%). Hydroelectric power plants make up only 0.9%, and although Uzbekistan has accelerated the development of renewable energy projects harnessing solar and wind, their share of TES remains negligible (IEA, 2022[14]). This is further aggravated by generous fossil-fuel subsidies provided to oil, gas and electricity consumers. In 2021, total fossil-fuel subsidies amounted to 19.3% of GDP, the highest among all countries in the IEA dataset (IEA, 2023[15]).

Source: Centre of Hydrometeorological Services of Uzbekistan (Uzhydromet) (2021[5]), First Biennial Update Report to the United Framework Convention on Climate Change, https://unfccc.int/documents/283216.

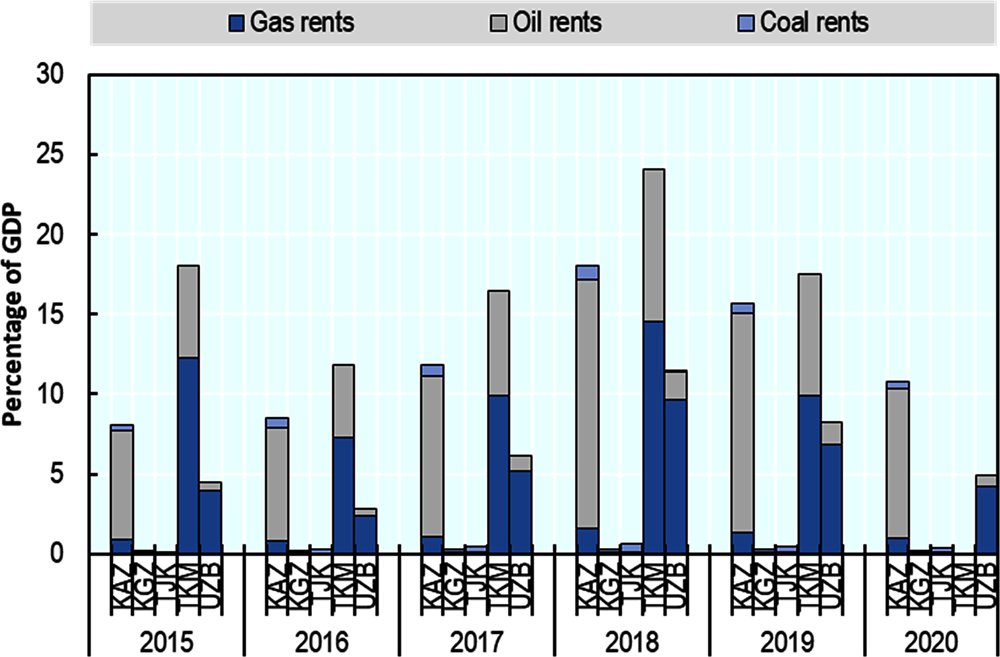

Uzbekistan is the 13th largest producer of natural gas worldwide and is home to the 24th largest reserves (IEA, 2022[14]). While fossil fuel rents, especially from natural gas, account for a significant portion of the country’s GDP, Uzbekistan is less reliant on fossil-fuel revenue than neighbouring Kazakhstan and Turkmenistan (see Figure 2.7). On average between 2010 and 2019, Uzbekistan exported approximately 21% of its gas production, amounting to 10 billion cubic metres, to China, Kazakhstan and Russia (IEA, 2022[14]). However, with rising domestic demand for gas products and a shift in government strategy towards domestic production of petrochemicals using natural gas, the share of exports has declined (6% in 2020), and the government plans to stop all exports of gas by 2025. At current rates of production (approximately 55-57 billion cubic metres per year), Uzbekistan’s reserves are at risk of significant depletion by 2030. (IEA, 2022[14]). In early 2023, a spike in demand during the harsh winter exceeded domestic supply, leading to widespread gas shortages for electricity and heating (Lillis, 2023[16]). This episode and the wider context of Russia’s invasion of Ukraine have brought energy security to the top of the policy agenda for Uzbekistan’s government. Given the country’s more modest oil reserves, Uzbekistan has already become a net importer as a result of dwindling production and rising domestic demand (Uzhydromet, 2021[5]).

Note: No Turkmenistan data available for 2020.

Source: World Bank (2023[1]), World Bank Indicators Database, https://data.worldbank.org/indicator.

Uzbekistan is already feeling the effects of climate change. Average air temperatures are rising faster in Uzbekistan than the global average. Between 1950 and 2013, temperatures rose by 0.27°C per decade on average with significant regional variation (World Bank Group and ADB, 2021[17]). Although these impacts are dependent on global emissions, of which Uzbekistan is only responsible for a relatively small share, Uzbekistan has considerable scope to contribute to global efforts and reduce its domestic emissions in line with its nationally determined contribution (NDC). Uzbekistan, a Party to the United Nations Convention on Climate Change and signatory of the Paris Agreement, has adopted emissions-reduction objectives through national strategies and international commitments.

Water scarcity, which has long been a challenge for the arid country, could worsen due to climate change as glaciers in Uzbekistan and Central Asia more broadly continue to shrink (UNECE, 2020[2]). This could have direct impacts on human quality of life through decreased water availability and quality from increased salinisation of water sources. Water scarcity, erosion and salinisation are expected to negatively impact soil quality and, as a result, crop yields in the agricultural sector (UNECE, 2020[2]). The Aral Sea, which straddles the border between Kazakhstan and Uzbekistan, is the most striking example of human impact on the environment in the region. Since 1960, water volumes have reduced by over 90%, due to diverted water from the Amu Darya and Syr Darya rivers for mass irrigation of crops in Central Asia, primarily for water-intensive cotton production in Uzbekistan. An increasing area of land formerly covered by water or river deltas has transformed into desert, and storms carrying 43 million tonnes of dust annually pass through the dry seabed, leading to further pollution of surface water and health impacts as far as 200 km from the sea itself. Since the Aral Sea is an endorheic body of water (i.e. with no outflowing rivers), its salt and agricultural pollutant concentrations continue to rise. As a result, local populations suffer from myriad health impacts, including lower fertility, poor organ function and potentially higher rates of cancer (Wæhler and Dietrichs, 2017[18]).

2.1.3. Infrastructure challenges and opportunities

Infrastructure lies at the heart of Uzbekistan’s green transition challenge. In its current state, Uzbekistan’s infrastructure constrains the growth of the economy due to ageing infrastructure stock, unreliable service delivery, higher transport and logistics costs for exporters and disruptions to production. Regular service interruptions to electricity, gas and water supplies, leading to output losses of approximately 24% among large firms and 38% among smaller firms (World Bank, 2022[19]). Uzbekistan stands to benefit economically from investment in projects to replace its ageing infrastructure assets, and it can seize the opportunity to transition towards lower-carbon alternatives.

Energy sector

Uzbekistan would garner the largest benefits in terms of emissions reduction from transforming its energy infrastructure. Uzbekistan’s thermal power plants and co-generation plants have been in operation for 42 and 63 years on average respectively, and the country’s hydroelectric power plants were commissioned on average 46 years ago (IEA, 2022[14]). The infrastructure stock is therefore inefficient, largely obsolete and due for decommissioning. To cope with increasing demand for electricity, which amounted to 63 terawatt-hours in 2018 and is projected to grow by 4% annually to 2030, Uzbekistan needs not only to replace existing power plants but build new generation capacity (World Bank, 2022[19]). Given these pressures, timely action to renew and expand generation capacity is necessary to ensure the economy continues to function.

There is an urgent need for Uzbekistan to diversify its energy mix, and doing so through renewables integration would allow Uzbekistan to address its GHG emissions and energy security concerns simultaneously. As Uzbekistan’s existing power plants are decommissioned and replaced, the country has an opportunity to reduce its reliance on natural gas and bolster energy security. Natural gas fuels 88% of domestic electricity generation, 50% of transportation (in the form of compressed natural gas) and the majority of district heating (IEA, 2022[14]). Current domestic production rates would exhaust Uzbekistan’s natural gas reserves by 2030, and imports are increasingly required to supplement domestically produced natural gas, increasing vulnerability to external supply shocks.

Solar power, even from a purely economic perspective, offers a promising alternative to gas-fired electricity in Uzbekistan, given the growing affordability of solar panels and Uzbekistan’s favourable conditions. Uzbekistan’s median global horizontal irradiance (GHI), a measure of solar potential, is estimated at 4.52 kWh per square metre per day, higher than the levels in Spain (4.46 kWh/m2/day) and Italy (4.07 kWh/m2/day) (IEA, 2022[14]). In addition to solar, Uzbekistan has untapped potential for wind power and other renewable energy sources. In fact, the potential for electricity generation from renewable energy sources is three times larger than current fossil fuel consumption (179 million tonnes of oil equivalent using modern technology) (Uzhydromet, 2021[5]).

However, Uzbekistan’s outdated electricity transmission and distribution system represents a significant barrier to increased renewables integration. Over half of the network was built 30 years ago or more, and it leads to significant losses (14-16% of generation according to 2019 data) (Regional Electrical Networks, 2019[20]). Although Uzbekistan’s grid is linked to neighbouring Central Asian countries’ networks and, via Kazakhstan, to Russia and Afghanistan’s networks, the electricity markets of Central Asian countries are less integrated than they were during the Soviet Union. In 1990, cross-border electricity trade amounted to 25 billion kilowatt-hours (kWh) between Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan, but by 2016 trade had decreased by over 90% to 2 billion kWh (ADB, 2019[21]). Although the current low levels of variable renewable power integration do not pose a threat to network performance, there is a pressing need for the modernisation of the domestic transmission and distribution system and improved integration with neighbouring countries to prepare for higher levels of supply variability in the future.

Transportation

Uzbekistan lies at the confluence of several regional cross-border transport projects, including transport corridors under China’s Belt and Road Initiative and two of the six corridors under the Central Asia Regional Economic Cooperation (CAREC) programme, and stands to benefit from better integration into the emerging Middle Corridor (or Trans-Caspian International Transport Route) running from China via Kazakhstan and the Caucasus to Europe. Uzbekistan’s existing transport network, consisting of the highest density of roads in Central Asia (41km per 100km2) and a reasonably developed public railway network (4 642 km of rail, including 1 646 km of operational electrified segments and 719 km of high-speed rail (Uzhydromet, 2021[5]), does not have sufficient capacity to handle projected increases in volume while maintaining current levels of network performance. The International Transport Forum (ITF) estimates that Uzbekistan road infrastructure capacity would need to increase by 486% by 2030 and 1365% by 2050, while rail capacity would need to increase by 459% by 2050 (ITF, 2019[22]).

The greening of Uzbekistan’s transport sector is closely linked to the energy challenges listed above. Currently, most passenger and freight transport in Uzbekistan occurs via road, and over half of the vehicle fleet is fuelled by compressed natural gas. Given these interlinkages, the modernisation and expansion of Uzbekistan’s transport infrastructure needs to be carried out in tandem with the transformation of the energy sector.

Uzbekistan’s government recognises the scale of the green transition challenge. The government of Uzbekistan has already laid out its vision for the first phase of the transition, up to 2030, summarised in Table 2.1, which focuses on reducing the GHG emissions intensity of GDP via renewables integration and electrification and shrinking the state’s role in the financial system as well as the economy as a whole. A component of the vision aims at reducing the state’s role in the economy, develop the domestic capital market and improve investment conditions to attract private capital domestically and from abroad. Uzbekistan has identified green bonds as a priority instrument for attracting private capital and has tasked the Ministry of Economy and Finance with improving the relevant regulatory framework.

The credibility of the targets, many of which are ambitious, is weakened by patchy information on costs and how the required actions would be financed. Available information on the progress towards the targets suggests that Uzbekistan is not on track to achieve them by 2026 (in the case of the New Uzbekistan Strategy) and 2030 (in the case of the Strategy for the Transition to a Green Economy and the revised Nationally Determined Contribution).

Uzbekistan still lacks a credible strategy to guide the transition in the long term (i.e. to 2050 and beyond). Ideally, such a strategy would chart the holistic transformation of Uzbekistan’s economy, taking into account the interplay between sectors as well as environmental and social impacts, and the reduction of GHG emissions towards a net-zero goal. Among Central Asian countries, Kazakhstan was the first country to adopt a Strategy for Achieving Carbon-Neutrality by 2060 (Government of Kazakhstan, 2023[27]) in early 2023, and it is now embarking on a process of translating its broad objectives into actionable reforms.

The government of Uzbekistan has made the Sustainable Development Goals (SDGs) a central part of its development planning. To increase the effectiveness of ongoing reforms and create conditions for ensuring sustainable development, the government of Uzbekistan defined a national SDG Roadmap and framework for the use of its economic resources in accordance with sustainability criteria. In 2018, the government developed its own sustainability model which adopts 16 National SDGs and their 125 corresponding targets that align with goals included in the United Nations’ 2030 Agenda for Sustainable Development. Simultaneously, an inter-agency Coordination Council for implementing the national SDG Roadmap was established, along with the creation of a bicameral Parliamentary Commission on SDGs.

2.2.1. Sectoral reforms and strategies

As part of this wider reform effort, several incentives for green investment projects are planned or have been introduced, including many sector-specific incentives.

Energy sector

Uzbekistan announced in February 2021 its aim to achieve carbon neutrality in its power generation sector by 2050, although this objective has not been enshrined in a policy document or binding legislation. Uzbekistan has strengthened its collaboration with the European Bank for Reconstruction and Development (EBRD), which supported the Ministry of Energy’s development of a low-carbon energy strategy and produced guidance on achieving net-zero emissions in Uzbekistan’s electricity sector. The strategy envisions early retirement of older, inefficient generation capacity and replacement with higher-efficiency gas-fired power plants in the short term, and a rapid scale-up of renewable energy in the medium to long term. Multilateral development banks have supported or are supporting the elaboration of a raft of medium-term strategies focusing on different aspects of the power generation sector such as the Transmission Network Development Plan to 2030 (developed with support from the World Bank) and the Distribution Network Development Plan (under development with support from the Asian Development Bank).

The government of Uzbekistan has implemented sweeping reforms of the energy sector in recent years. In 2019, the government of Uzbekistan split Uzbekenergo, a state-owned vertically integrated energy company, into four distinct joint stock companies (JSC) responsible for the development and operation of thermal power plant generation (JSC Thermal Power Plants); the development and operation of hydroelectric generation capacity (JSC Uzbekhydroenergo); the transmission, interstate transit, import and export of electricity (JSC National Electric Grid) and local electricity distribution and the management of 14 territorial JSCs in charge of sales to end-use consumers (JSC Regional Power Grids) (Government of Uzbekistan, 2019[28]). The creation of an independent gas and electricity regulator is expected in the near future (Turkstra, 2021[29]).

A project office headed by the Deputy Minister of Energy in charge of the electricity sector was created under the Ministry of Energy. It serves as the working body of the Commission on the Reform of the Electric Energy Sector (Government of Uzbekistan, 2019[28]). The project office has mapped out a three-step plan to transform Uzbekistan’s electricity market into a competitive wholesale market by 2025. The first phase focuses on liberalising the energy market and granting licences to more private firms wishing to sell electricity. The second phase foresees the creation of a system operator for power distribution and a transfer to energy suppliers of the right to sell to consumers on the basis of licences. Consumers will be able to select suppliers through an online trading platform, encouraging competition and innovation. The third phase envisions the establishment of intraday and hourly sales on the wholesale market (Kun.Uz, 2021[30]).

In 2020, Uzbekistan’s Ministry of Energy adopted a Concept Note for Ensuring Electricity Supply in Uzbekistan in 2020-2030, which aims to reduce the existing electricity deficit while simultaneously promoting balanced development and paying due attention to sustainability and the green economy. The Concept Note also stipulates the need to reconstruct and modernise existing power generation, distribution and transmission infrastructure to increase energy efficiency, to improve the power metering systems, and to diversify fuel sources and further promote and develop the use of renewable energy. The note sets out both medium-term and long-term targets for the power sector. Specifically, it sets out the following objectives:

the satisfaction of the country’s electrical power demand in full through domestic generation, avoiding dependence on energy imports and ensuring energy security;

the improvement of the energy efficiency of the economy and a reduction in its energy intensity, including through the creation of economic mechanisms to stimulate rational use of electrical power by consumers;

an increase in the energy efficiency of the generation, transmission and distribution of electrical power to satisfy the growing demand;

a reduction of power equipment wear-and-tear through constant renewal and an increased reserve of generation and transmission assets;

the development and expansion of the use of renewables and their integration into the unified power system;

the development of an efficient basic electricity market model.

The Concept Note calls for the development of 62 energy projects by 2030, including the construction of 35 hydroelectric power plants (1 537 MW) and the modernisation of 27 existing hydroelectric power plants. It also envisions the addition of 3 GW of wind power and 5 GW of solar power capacity by 2030. In addition to these large-scale projects, several small-scale solar power plants, which are not connected to the central grid, are to be constructed in remote areas. The plan also calls for the construction of medium-scale solar power facilities to cover the power needs of individual producers and industrial hubs. Residential renewable energy installations supplying individual houses and residential complexes are expected to be constructed in the form of independent power units. In order to achieve these targets, solar plants will be equipped with large storage systems. Aware that attracting foreign direct investment (FDI) will be instrumental in reaching the targets, the government is working on promoting FDI in the renewable energy sector through the introduction of competitive bidding processes. The government is dedicated to working with the IFIs during the initial stages of the implementation process in order to identify potential investors under the Build-Own-Operate framework and to sign long-term Power Purchase Agreements (PPAs) for the supply of renewable energy.

The pace of renewable energy development in Uzbekistan has begun to accelerate markedly, although is currently at extremely low levels. Since 2019, the government of Uzbekistan, with support from the Asian Development Bank (ADB), the European Bank for Reconstruction and Development (EBRD) and the World Bank Group, have been launching competitive bidding processes for the construction and operation of large-scale solar photovoltaic generation projects. Contracts amounting to 1 300 MW of new generation capacity have been awarded to international companies, and projects representing a further 750 MW of capacity are open to tender (IEA, 2022[31]). The government and the International Finance Corporation (IFC) have signed an agreement on advisory services for the preparation of 500 MW of wind farm projects for tender through public-private partnerships (Djunisic, 2022[32]).

However, compared to the installed capacity of thermal power stations and combined heat power plants (14 520 MW in 2020) and hydroelectric power stations (2 023 MW in 2020) (UzStat, 2023[33]), the planned renewable capacity is modest in size. The development of solar power, where Uzbekistan’s relatively high global horizontal irradiance (GHI) gives the country a distinct advantage, faces several barriers. In addition to capacity constraints (e.g. lack of qualified workforce and local knowledge, poor quality and availability of data), prospective developers of solar energy face market barriers (e.g. elevated fossil fuel subsidies, non-cost-reflective energy pricing, inadequate accounting of social and environmental externalities), complex policies lacking transparency, “stop-and-go” policy approaches that undermine investor confidence, restrictive local content requirements paired with insufficient available local technologies and an electricity market design unsuitable for large-scale integration of variable renewable energy sources (IEA, 2022[31]). To address some of the non-economic barriers related to in-country capacity for the development of renewable energy projects, the government established the National Renewable Energy Research Institute under the Ministry of Energy in 2022 (Government of Uzbekistan, 2022[34]). It is charged with designing training programmes for renewable and hydrogen energy. New master’s programmes are set for introduction into six leading Uzbek universities (Government of Uzbekistan, 2021[35]).

Energy efficiency and industry

Recent legislation has introduced several incentives for investment in energy efficiency-related projects, including deductions of up to 50% of import tariffs for energy-efficient equipment, preferential credit under government guarantee for state-owned firms financing state, sectoral and regional energy efficiency programmes and lower tariffs on energy resources for firms producing products with lower energy consumption than the established standards. An energy saving fund was created in August 2020, sourced from annual payments of 5% of net revenue from the oil, gas and energy sectors, income from higher energy tariffs on excess energy consumption, and fines for infractions related to energy use. The fund aims to support firms and individuals undertaking energy audits, capacity building, the introduction of energy saving technologies and the development of renewable energy and financing energy saving and renewable energy projects (Energy Charter, 2022[36]).

Several policies were also introduced to incentivise the adoption of more energy-efficient industrial processes, including energy tariff reductions for industrial firms using energy efficient technology. Since 2020, firms have been obliged to set energy saving targets to 2023, although the targets are only indicative and no mechanism is in place to encourage their achievement. Industrial firms are also eligible to apply for financial support (from the state budget and loans from international financial institutions) to carry out mandatory energy audits. State-owned enterprises must comply with more stringent regulations on energy efficiency than private firms (Energy Charter, 2022[36]).

Transport sector

The Ministry of Transport submitted a draft Strategy for the Development of Uzbekistan’s Transport System to 2035 for public consultation in 2019, but the Strategy has not yet been adopted by the government. The Strategy calls for the construction of new rail lines (525.2 km by 2035 compared to 129.2 km in 2018; increasing density to 16.5 km / 1000 km2), roads (756 km by 2035 compared to 130 km in 2018), urban transport services (including metro lines and bus routes) and airport runways. It also sets objectives for alternative fuels in automobiles (80%), electric and hybrid vehicles in the national motor vehicle fleet (20%) and GHG reductions per unit of transported cargo (Government of Uzbekistan, 2019[37]).

The government has also adopted incentives for the domestic production of hybrid and electric vehicles, including exemption from recycling fees as well as customs duties on imported parts, and their purchase by individuals in the form of partial credit reimbursement for loans (Government of Uzbekistan, 2022[38]). Uzbekistan aims to increase the domestic production of electric vehicles to 15-25 thousand units per year (Kapital.Kz, 2022[39]), which is roughly equivalent to average monthly purchases of domestically produced vehicles (approx. 19 thousand) (Centre for Economic Research and Reforms, 2023[40]).

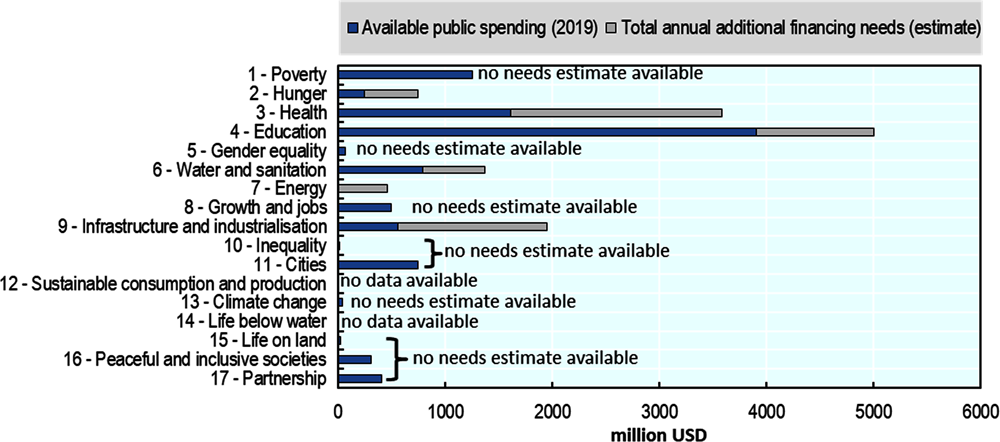

Despite Uzbekistan’s progress on socioeconomic development, the investment requirements for Uzbekistan to achieve its development and climate goals are vast. Uzbekistan needs to tap into all possible sources of finance, particularly by attracting more capital from the private sector. While some development objectives and SDGs are inherently more reliant on public funding, such as education, health and some environmental goals, others offer opportunities to attract private capital, notably in the electricity sector, which is Uzbekistan’s largest contributor to GHG emissions.

There is no assessment of the investments required for Uzbekistan to achieve the targets in its development strategies. The investment needs estimates that do exist vary widely in their scope and projected spending requirements, but each provides a partial picture of the scale of financing required.

One such estimate relates to the investments required for Uzbekistan to achieve some of the SDGs. Given that the UNDP has judged Uzbekistan’s domestic development objectives outlined in its strategies and development programmes to be in full alignment with the SDGs in a number of areas, including the SDGs related to poverty reduction (SDG 1), the elimination of hunger (SDG 2), education (SDG 4), water (SDG 6), energy (SDG 7), reducing inequalities (SDG 10) and cities (SDG 11), they can act as a relatively good partial proxy for Uzbekistan’s overall development and climate goals. However, other government objectives, notably on climate change, are not yet fully compatible with the SDGs (UNDP, 2021[41]).

According to the SDG assessment, the gap between current annual public spending and the financing required each year to achieve the goals by 2030 are considerable. In a pre-COVID-19 IMF assessment, it was estimated that Uzbekistan would need to mobilise capital equivalent to USD 6 billion in additional annual spending to achieve the SDGs in social and infrastructure sectors alone (SDGs 2, 3, 4, 6, 7 and 9) (see Figure 2.8). Compared to 2019 levels of public spending, this would amount to a 57.6% increase. This only represents a partial picture of Uzbekistan’s SDG financing needs, since no estimates were available for the remaining SDGs, including those related to cities (11) and climate change (13). Moreover, additional spending needs, estimated at USD 4 billion, emerged as a result of the COVID-19 pandemic (UNDP, 2021[41]). Global estimates confirm the widening gap in developing countries due to increased financing needs and reduced available financing flows brought on by the pandemic. The OECD estimates that the annual SDG financing gap increased by 56%, from USD 2.5 trillion to USD 3.9 trillion, across developing economies (OECD, 2022[42]).

Note: No needs estimates available for SDGs 1, 5, 8, 10-17.

Source: UNDP (2021[41]), Development Finance Assessment of the Republic of Uzbekistan, https://www.undp.org/uzbekistan/publications/development-finance-assessment-republic-uzbekistan.

Another partial needs estimate focuses more squarely on the issues of climate change mitigation and resilience, although it limits its scope to the power sector. Looking beyond 2030, the European Bank of Reconstruction and Development (EBRD) estimates that Uzbekistan could achieve carbon neutrality in its power sector by mobilising less than 2% of annual GDP between 2030 and 2050 (EBRD, 2021[43]). Regional analysis covering emerging Eastern European and Central Asian countries by the World Bank estimates that 8.8% of regional GDP could be sufficient to achieve low-emission, climate-resilient infrastructure systems by 2030, but no country-level needs assessment for Uzbekistan is available. This estimate includes projected costs of renewable energy and energy efficiency investments, a mobility shift towards rail, public transport and electric vehicles, the provision of safe water supply and sanitation and flood protection (World Bank, 2019[44]).

References

[21] ADB (2019), Regional Cooperation on Increasing Cross-Border Energy Trading within the Central Asian Power System: Subproject 2: Provision of Solutions to Bottlenecks to the Regional Power Trade, Asian Development Bank (ADB), https://www.adb.org/sites/default/files/project-documents/52112/52112-003-tasp-en.pdf (accessed on 23 June 2023).

[3] Al Rasasi, M. and E. Cabezon (2022), “Uzbekistan’s Transition to Inflation Targeting”, IMF Working Papers 2022, No. 2022/229, International Monetary Fund (IMF), Washington, D.C., https://www.imf.org/en/Publications/WP/Issues/2022/11/18/Uzbekistan-s-Transition-to-Inflation-Targeting-525745 (accessed on 15 June 2023).

[40] Centre for Economic Research and Reforms (2023), What is happening with the car market in Uzbekistan: CERR assessed the level of activity, https://www.cer.uz/en/post/publication/what-is-happening-with-the-car-market-in-uzbekistan-cerr-assessed-the-level-of-activity.

[32] Djunisic, S. (2022), “IFC backs Uzbekistan’s plan for up to 500 MW of new wind power”, Renewables Now, https://renewablesnow.com/news/ifc-backs-uzbekistans-plan-for-up-to-500-mw-of-new-wind-power-782230/ (accessed on 23 June 2023).

[43] EBRD (2021), A Carbon Neutral Electricity Sector in Uzbekistan: Summary for Policy Makers, European Bank for Reconstruction and Development (EBRD), https://minenergy.uz/uploads/57c6df8d-6ec0-8362-504a-fb3162895df6_media_.pdf (accessed on 23 June 2023).

[36] Energy Charter (2022), In-Depth Review of the Energy Efficiency Policy of the Republic of Uzbekistan, Energy Charter, https://www.energycharter.org/fileadmin/DocumentsMedia/IDEER/IDEER-Uzbekistan_2022__en.pdf (accessed on 23 June 2023).

[27] Government of Kazakhstan (2023), Об утверждении Стратегии достижения углеродной нейтральности Республики Казахстан до 2060 года [On the adoption of the Strategy for achieving carbon neutrality of the Republic of Kazakhstan to 2060], https://adilet.zan.kz/rus/docs/U2300000121.

[38] Government of Uzbekistan (2022), О мерах по государственной поддержке организации производства элетромобилей [On government support measures to organise the production of electric vehicles], https://lex.uz/ru/docs/6316585 (accessed on 23 June 2023).

[34] Government of Uzbekistan (2022), О мерах по организации деятельности Национального научно-исследовательского института возобновляемых источников энергии при Министерстве энергетики [On measures to organise the activities of the National Scientific Research Institute for Renewable Energy Sources under the Ministry of Energy], https://lex.uz/ru/docs/5925093 (accessed on 23 June 2023).

[24] Government of Uzbekistan (2022), О мерах по повышению эффективности реформ, направленных на переход Республики Узбекистан на «зеленую» экономику до 2023 года [On measures to improve the efficacy of reforms aimed at transitioning the Republic of Uzbekistan to a green economy by 2030], https://lex.uz/ru/docs/6303233 (accessed on 21 June 2023).

[23] Government of Uzbekistan (2022), О Стратегии развития Нового Узбекистана на 2022-2026 годы [On the New Uzbekistan Development Strategy 2022-2026], https://lex.uz/ru/docs/5841077 (accessed on 15 June 2023).

[35] Government of Uzbekistan (2021), О мерах по развитию возобновляемой и водородной энергетики в Республике Узбекистан [On measures to develop renewable and hydrogen energy in the Republic of Uzbekistan], https://lex.uz/ru/docs/5362035 (accessed on 23 June 2023).

[28] Government of Uzbekistan (2019), О Стратегии дальнейшего развития и реформирования электроэнергетической отрасли Республики Узбекистан [On the Strategy for the Further Development and Reform of the Electricity Sector of the Republic of Uzbekistan], https://lex.uz/ru/docs/4257085 (accessed on 23 June 2023).

[37] Government of Uzbekistan (2019), Об утверждении Стратегии развития транспортной системы Республики Узбекистан до 2035 года [On the approval of the Strategy for the Development of the Transport System of the Republic of Uzbekistan until 2035], https://regulation.gov.uz/oz/d/3867 (accessed on 23 June 2023).

[6] Hamidov, B. and F. Davletov (2020), “Вызовы теневой экономики [Challenges of the shadow economy]”, Review.Uz, https://review.uz/post/vzov-tenevoy-ekonomiki (accessed on 16 June 2023).

[15] IEA (2023), Energy subsidies: Tracking the impact of fossil-fuel subsidies, https://www.iea.org/topics/energy-subsidies (accessed on 15 June 2023).

[13] IEA (2022), SDG7: Data and Projections: Energy intensity, https://www.iea.org/reports/sdg7-data-and-projections/energy-intensity (accessed on 19 June 2023).

[31] IEA (2022), Solar Energy Policy in Uzbekistan: A Roadmap, International Energy Agency (IEA), Paris, https://www.iea.org/reports/solar-energy-policy-in-uzbekistan-a-roadmap (accessed on 23 June 2023).

[14] IEA (2022), Uzbekistan 2022 Energy Policy Review, International Energy Agency (IEA), Paris, https://doi.org/10.1787/be7a357c-en (accessed on 19 June 2023).

[9] IMF (2022), World Economic Outlook Database 2022, World Economic Outlook database: October 2022, https://www.imf.org/en/Publications/WEO/weo-database/2022/October/weo-report (accessed on 15 June 2023).

[10] Investment Promotion Agency (2023), Узбекистан в международных рейтингах [Uzbekistan in international ratings], https://invest.gov.uz/ru/investor/uzbekistan-v-mezhdunarodnyh-rejtingah/ (accessed on 15 June 2023).

[22] ITF (2019), Enhancing Connectivity and Freight in Central Asia, International Transport Forum (ITF), Paris, https://www.itf-oecd.org/sites/default/files/docs/connectivity-freight-central-asia_2.pdf (accessed on 23 June 2023).

[39] Kapital.Kz (2022), “В Узбекистане планируют производить до 25 тысяч электромобилей в год [Uzbekistan plans to produce up to 25 thousand electric vehicles annually]”, Kapital.Kz, https://kapital.kz/world/110771/v-uzbekistane-planiruyut-proizvodit-do-25-tysyach-elektromobiley-v-god.html (accessed on 23 June 2023).

[30] Kun.Uz (2021), “В Узбекистане создается оптовый рынок электроэнергии [A wholesale electricity market is being established in Uzbekistan]”, Kun.Uz, https://kun.uz/ru/news/2021/06/16/v-uzbekistane-sozdayetsya-optovyy-rynok-elektroenergii (accessed on 23 June 2023).

[16] Lillis, J. (2023), “Fueling energy woes, Uzbekistan sees drop in gas output”, Eurasianet, https://eurasianet.org/fueling-energy-woes-uzbekistan-sees-drop-in-gas-output (accessed on 19 June 2023).

[11] Ministry of Finance (2022), “The State of Debt of the Republic of Uzbekistan for the 1st Quarter of 2022”, https://api.mf.uz/media/post_attachments/1kv_2022_eng.pdf (accessed on 15 June 2023).

[42] OECD (2022), Global Outlook on Financing for Sustainable Development 2023: No Sustainability without Equity, OECD, Paris, https://doi.org/10.1787/fcbe6ce9-en (accessed on 23 June 2023).

[20] Regional Electrical Networks (2019), Стратегия развития распределительных электрических сетей в Республике Узбекистан до 2025 года [Strategy for the Development of Electricity Distribution Networks in the Republic of Uzbekistan to 2025], "Regional Electrical Networks" Joint-Stock Company, Tashkent, https://het.uz/uploads/e2dff98e-6eb9-2c89-3ff6-2bc23943bbe7_media_.pdf (accessed on 22 June 2023).

[25] Toshkent Republican Stock Exchange (2023), “2022 Exchange Review”, https://uzse.uz/system/analytics/pdfs/000/000/154/original/Exchange_review_for_full_year_2022.pdf?1676883361 (accessed on 21 June 2023).

[29] Turkstra, A. (2021), “The Last Frontier: Energy investments in Uzbekistan reach new heights”, Euractiv, https://www.euractiv.com/section/central-asia/opinion/the-last-frontier-energy-investments-in-uzbekistan-reach-new-heights/ (accessed on 23 June 2023).

[41] UNDP (2021), Development Finance Assessment for the Republic of Uzbekistan, United Nations Development Programme (UNDP), https://www.undp.org/uzbekistan/publications/development-finance-assessment-republic-uzbekistan (accessed on 23 June 2023).

[2] UNECE (2020), Third Environmental Performance Review of Uzbekistan, United Nations Economic Commission for Europe, Geneva, https://unece.org/environment-policy/publications/3rd-environmental-performance-review-uzbekistan (accessed on 12 June 2023).

[5] Uzhydromet (2021), First Biennial Update Report (BUR) of the Republic of Uzbekistan, Centre of Hydrometeorological Service of the Republic of Uzbekistan (Uzhydromet), Tashkent, https://unfccc.int/sites/default/files/resource/FBURUZeng.pdf (accessed on 12 June 2023).

[7] UzStat (2023), National Accounts: Volume of gross domestic product by types of economic activities, https://stat.uz/en/official-statistics/national-accounts (accessed on 12 June 2023).

[33] UzStat (2023), Промышленность: Установленная мощность электростанций [Industry: Installed power station capacity], https://stat.uz/ru/ofitsialnaya-statistika/industry (accessed on 23 June 2023).

[8] UzStat (2022), Foreign economic activity 2022, Statistics Agency under the President of the Republic of Uzbekistan (UzStat), Tashkent, https://stat.uz/en/quarterly-reports/21530-2022-eng#january-december (accessed on 16 June 2023).

[18] Wæhler, T. and E. Dietrichs (2017), “The vanishing Aral Sea: health consequences of an environmental disaster”, Tidskriftet for den Norske Legeforening [Journal of the Norwegian Medical Association], Vol. 137/18, https://tidsskriftet.no/en/2017/10/global-helse/vanishing-aral-sea-health-consequences-environmental-disaster (accessed on 16 June 2023).

[1] World Bank (2023), World Development Indicators (database), World Bank Open Data, https://data.worldbank.org/ (accessed on 26 October 2018).

[19] World Bank (2022), Towards a Prosperous and Inclusive Future: The Second Systematic Country Diagnostic of Uzbekistan, World Bank, Washington, D.C., https://documents1.worldbank.org/curated/en/933471650320792872/pdf/Toward-a-Prosperous-and-Inclusive-Future-The-Second-Systematic-Country-Diagnostic-for-Uzbekistan.pdf (accessed on 22 June 2023).

[12] World Bank (2022), Политические диалоги — «Зеленый» рост и изменение климата в Республике Узбекистан: Сборник информационных материалов [Political dialogues - Green growth and climate change in the Republic of Uzbekistan: Collection of informational materials], World Bank, Washington, D.C., https://documents1.worldbank.org/curated/en/099905106302277935/pdf/P170870007081a02e0a17c025c451ef6594.pdf (accessed on 15 June 2023).

[4] World Bank (2021), Assessing Uzbekistan’s Transition: Country Economic Memorandum, World Bank, Washington, D.C., https://documents1.worldbank.org/curated/en/862261637233938240/pdf/Full-Report.pdf (accessed on 22 June 2023).

[44] World Bank (2019), Beyond the Gap – How Countries Can Afford the Infrastructure They Need while Protecting the Planet, World Bank, Washington, D.C., https://www.worldbank.org/en/topic/publicprivatepartnerships/publication/beyond-the-gap---how-countries-can-afford-the-infrastructure-they-need-while-protecting-the-planet (accessed on 23 June 2023).

[17] World Bank Group and ADB (2021), Climate Risk Country Profile: Uzbekistan, World Bank Group and the Asian Development Bank (ADB), Washington, D.C. and Manila, https://www.adb.org/sites/default/files/publication/736686/climate-risk-country-profile-uzbekistan.pdf (accessed on 15 June 2023).

[26] World Resources Institute (2023), Climate Watch Historical GHG Emissions (1990-2020), https://www.climatewatchdata.org/ghg-emissions (accessed on 21 June 2023).