11. Other products

This chapter provides a market overview and a description of the current market situation for roots and tubers (i.e. cassava, potato, yams, sweet potato, taro), pulses (i.e. field peas, broad beans, chickpeas, lentils), and banana and major tropical fruits (i.e. mango, mangosteen and guava, pineapple, avocado, and papaya) markets. It then highlights the medium term (2023-32) projections for production, consumption and trade for these products and describes the main drivers of these projections.

11.1.1. Market overview

Roots and tubers are plants that yield starch derived from either their roots (e.g. cassava, sweet potato and yams) or stems (e.g. potatoes and taro). They are destined mainly for human consumption (as such or in processed form) and, like most other staple crops, can also be used for animal feed or industrial processing, notably in the manufacturing of starch, alcohol, and fermented beverages. Unless they are processed, they are highly perishable once harvested, which limits the opportunities for trade and storage.

Within the roots and tubers family, potato dominates in worldwide production, with cassava a distant second. With respect to global dietary importance, potato ranks fourth after maize, wheat and rice. This crop provides more calories, grows more quickly, uses less land, and can be cultivated in a broad range of climates. However, potato production, which forms the bulk of the root and tuber sectors in developed countries, has been declining over several decades, with growth in production falling well below that of population.

Output of cassava is growing at well over 3% p.a., almost three times the rate of population growth. Cultivated mainly in the tropical belt and in some of the world’s poorest regions, cassava production has doubled over two decades. Once considered a subsistence crop, it is now seen as a commodity and key for value-addition, rural development and poverty alleviation, food security, energy security; and for bringing important macroeconomic benefits. These factors are driving rapid commercialisation of this crop and large-scale investments in upscaling the processing of cassava, both which have contributed significantly to its global expansion.

11.1.2. Current market situation

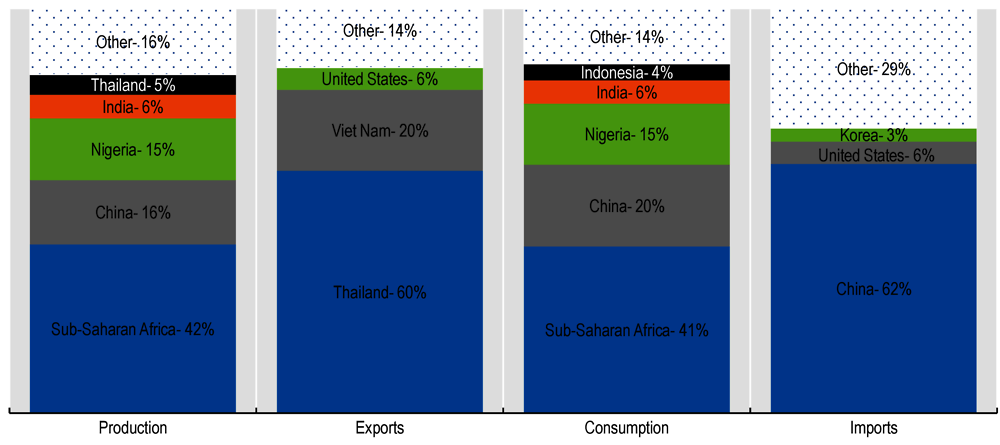

The largest producing regions of roots and tubers in the base period are Asia (102 Mt) and Africa (100 Mt). In Sub Saharan Africa, roots play a significant role as a staple crop. Globally, about 130 Mt are used as food, 57 Mt as feed, and 33 Mt for other uses, mostly biofuel and starch. As the perishable nature of these crops prohibits significant international trade in fresh produce, countries tend to be self-sufficient. About 15 Mt are currently traded internationally, mostly in processed or dried form. Thailand and Viet Nam are the leading exporters and the People’s Republic of China (hereafter “China”) is the main destination.

Global production of roots and tubers reached 251 Mt (dry matter) in the base period (2020-22); about 5 Mt has been added annually in the past years and consumed mainly as food. The prices of roots and tubers (measured by the Cassava (flour) wholesale price in Bangkok) increased again significantly in 2022 as demand was strong, in particular in China. Global quantities traded increased by 0.5 Mt.

11.1.3. Main drivers for projections

Producing cassava requires few inputs and affords farmers greater flexibility in terms of timing the harvest as the crop can be left on the ground well after reaching maturation. Cassava’s tolerance to erratic weather conditions, including drought, makes it an important part of climate change adaptation strategies. Compared to other staples, cassava competes favourably in terms of price and diversity of uses. In the form of High Quality Cassava Flour (HQCF), cassava is increasingly targeted by governments in Africa as a strategic food crop which does not exhibit the same levels of price volatility as other imported cereals. Mandatory blending with wheat flour helps reduce the volume of wheat imports, thereby lowering import bills and conserving precious foreign exchange. The drive towards energy security in Asia, combined with mandatory blending requirements with gasoline, has led to the establishment of ethanol distilleries that use cassava as a feedstock. With regard to trade, processed cassava manages to compete successfully in the global arena, e.g. with maize-based starch and cereals for animal feeding applications.

Potatoes are generally confined to food use and are a substantial component of diets in developed regions, particularly in Europe and North America. As overall food intake of potato in these regions is very high and may have reached saturation, the scope for consumption increases to outpace population growth remains limited. Developing regions, however, provide some growth momentum to potato production at the world level.

Global sweet potato cultivation has declined in recent years, mostly due to a sharp decline in acreage (which shows no sign of abating) in China, the world’s foremost producer. Food demand largely defines the growth potential of sweet potato and other less prominent roots and tuber crops given the limited commercial viability for diversified usage. Consequently, consumer preferences along with prices play important roles in shaping consumption.

11.1.4. Projection highlights

World production and utilisation of roots and tubers is projected to increase by about 18% over the next decade. Production growth in low-income regions could reach 2.6% p.a. while supply in high-income countries should grow at only 0.3% annually. Global land use is projected to increase by 6 Mha to 71 Mha, but there will be some regional shifts. African countries are expected to increase their cultivation area, while reductions are projected for Europe and America. Moreover, many farmers in Thailand shifted from Cassava to rice which had better production incentives. Production growth is mainly attributed to investments in yield improvements in Africa and Asia, as well as an intensification of land use in these regions.

Note: Presented numbers refer to shares in world totals of the respective variable

Source: OECD/FAO (2023), ''OECD-FAO Agricultural Outlook'', OECD Agriculture statistics (database), https://doi.org/10.1787/agr-outl-data-en.

By 2032, an additional 1.4 kg/capita per year of root crops will enter diets at the global level, driven mostly by consumers in Africa where per capita intake of roots and tubers could surpass 41 kg per year. Biofuel use, albeit from a low basis (3% of use), is expected to grow by 37% over the next ten years driven by the Chinese biofuel industry. Feed and other industrial use will remain significant, albeit with slower growth of about 10% and 15% respectively, over the outlook period.

International trade in roots and tubers comprises about 6% of the global market production. Over the medium term, this share is expected to remain constant. Exports from Thailand and Viet Nam are growing and are expected to reach a combined total of 15 Mt, mainly to supply the growing biofuel and starch industries in China.

After a moderate decrease expected in 2023 due to high pressure on cassava markets in Thailand and the shortfall of potato production in Ukraine, prices of roots and tubers are projected to follow a similar path to cereal prices in the medium term given the substitutability between roots and tubers and cereals on food and feed markets; namely, an increase in nominal prices but a decline in real terms.

11.2.1. Market overview

Pulses are the edible seeds of plants in the legume family. Commonly, eleven types are recognised.1 They provide high level of protein, dietary fibre, vitamins, minerals, phytochemicals, and complex carbohydrates. Apart from the nutritional benefits, pulses help to improve digestion, reduce blood glucose, minimise inflammation, lower blood cholesterol, and prevent chronic health issues such as diabetes, heart disease, and obesity. However, their consumption levels differ from region to region depending on the dietary patterns, availability and prevailing conditions.

Cultivation of pulses has a long tradition in almost all regions of the world. For centuries, legumes have played a fundamental role in the functioning of traditional agricultural systems. Prior to 2000, global production of pulses stagnated due to the widespread disappearance of small farms in developing countries which led to a decline of traditional farming systems that included pulses in their crop rotation. Production was further hampered because of their weak resilience to diseases due to a lack of genetic diversity, limited access to high-yield varieties, and the lack of policy support to pulses growers. The sector began to recover in the early 2000s and has since seen an average annual increase of about 3% globally, led by Asia and Africa. These two regions combined accounted for more than half of the 12 Mt production increase in the past decade.

Global per capita consumption of pulses started to decline in the 1960s (Figure 11.2) due to slow growth in yields and resulting increases in price. Income growth and urbanisation shifted preferences away from pulses as human diets became richer in animal proteins, sugar, and fats. Nonetheless, pulses have remained an important source of protein in developing countries, and average global per capita food consumption has increased to about 7 kg/year to date. This growth has been driven mainly by income gains in countries where pulses are an important source of protein; this particularly true of India where vegetarians account for about 30% of the population.

Pulses can be processed into different forms such as whole pulses, split pulses, pulse flours, and pulse fractions like protein, starch and fibre. The flour and fractions have diverse applications in industries related to meat and snack food, bakery and beverages, and batter and breading.

11.2.2. Current market conditions

India is by far the largest producer of pulses, accounting for about 25% of global production in the past decade. Canada (9%), China (6%) and the European Union (5%) are the next largest producing countries. The Asian market accounts for 52% of all consumption, but only about 43% of production, making it the most significant import destination. About 21% of global production is traded internationally with Canada (35% of global trade) by far the largest exporter and India the largest importer (19% of global trade). Africa has further expanded its production and consumption in the past decade and has remained largely self-sufficient.

In 2022, the global pulses market reached a volume of 93 Mt, after an average annual growth of 1.7% p.a. during the previous decade; this growth was led by Asia and Africa. World trade volumes were registered at 19.5 Mt, 0.5 Mt higher than in 2021.International prices for pulses, approximated by the Canadian field pea price, have started to fall from their peak value of 2021 to USD 359/Mt in 2022, following the production recovery in Canada.

11.2.3. Main drivers for projections

As pulses are associated with various health benefits and represent an important meat substitute due to their high protein content, health and environmentally conscious consumers are increasingly integrating these in their daily diets, which in turn is propelling the growth of the global pulses market. Rapid urbanisation, changing lifestyles, and hectic work schedules are also making healthy snack foods popular amongst the working population, and pulses are increasingly used in the processing of ready-to-eat (RTE) food products.

Health and environmental benefits are reasons why governments of pulses-producing countries are providing assistance to farmers, and thus supporting growth of this market. Support to the production of pulses production plays an important role in the Protein Strategy of the European Union and are a major ingredient in products such as meat substitutes. Depending on the future dynamics of demand for such products, this could significantly change the future importance of pulses in the agricultural production mix.

11.2.4. Projection highlights

Pulses are expected to regain importance in the diets in many regions of the world. This Outlook foresees the global trend in this area to continue and projects global average annual per capita food use to increase to 8.6 kg by 2032. Per capita food consumption is projected to increase in all regions over the coming decade, with the largest increase expected in Europe (+4% p.a.) (Figure 11.2).

Global supply is projected to increase by 29 Mt. Almost half of this increase is expected to come from Asia, particularly India, the world’s largest producer. Sustained yield improvements are projected to raise India’s domestic production by an additional 11 Mt by 2032. India has introduced high-yielding hybrid seeds, supported mechanisation, and implemented a minimum support price aimed at stabilising farmer’s income. In addition, the central government and some state governments have included pulses in their procurement programmes, although not with the same geographical coverage as in the case of wheat and rice.

This expected production expansion is driven by the assumption of continued intensification of the pulses production systems due to improved yields and intensified land use. About 60% of production growth can be attributed to land use intensification during the projection period, and the remaining 40% to yield improvements.. Particularly in Africa, a combination of area expansion and yield growth is estimated to add about 0.6 Mt annually to the regional production.

This Outlook assumes that growth will be sustained by increased intercropping of pulses with cereals, in particular in Asia and Africa where smallholder farmers represent a large share of producers. The projected yield improvements of pulses will continue to lag cereals and oilseeds because in most countries pulses are not included in the development of high-yielding varieties, improved irrigation systems, and agricultural support policies.

World trade of pulses grew from 15 Mt to 19 Mt over the past decade and is projected to reach 23 Mt by 2032. Canada remains the main exporter of pulses, with volumes expected to grow from 6.8 Mt at present to 9.9 Mt by 2032, followed by Russia and Australia with 2 Mt and 1.9 Mt of exports by 2032, respectively.

International prices in nominal terms are expected to decrease further until 2025 then increase slightly over the coming decade, while real prices will decline.

Bananas and the four major fresh tropical fruits – mango, pineapple, avocado and papaya – play a vital role in world agricultural production, and especially in securing the nutrition and livelihoods of smallholders in producing countries. In recent decades, rising incomes and changing consumer preferences in both emerging and high-income markets, alongside improvements in transport and supply chain management, have facilitated fast growth in international trade in these commodities. Based on provisional 2022 figures, the global banana and major tropical fruit export industries respectively generate around USD 10 billion and USD 11 billion per year. Although only approximately 16% of global banana production and 7% of global major tropical fruit production are traded in international markets (provisional 2022 figures), in exporting countries, which are mostly low- or middle-income economies, revenue from production and trade can weigh substantially in agricultural GDP. For instance, bananas represented about 50% of agricultural export revenue in Ecuador in 2021, while combined exports of pineapples and bananas accounted for some 40% of agricultural export revenue in Costa Rica. As such, trade in bananas and major tropical fruits has the potential to generate significant export earnings in producing countries. For all these underlying reasons, it is important to assess the potential future market development of these agricultural commodities.

11.3.1. Market Situation: Overview

According to preliminary data and information, global trade in bananas and major tropical fruits continued to be negatively affected by several factors on the supply side in 2022, which induced rising producer costs and consequent supply shortages, against relatively stable demand in key import markets. Industry sources reported that the high prices for fertilisers and their reduced availability in 2021 and throughout the first half of 2022 resulted in a reduced application by farmers, hampering the productivity and quality of banana and major tropical fruit cultivation in key producing areas. Adverse weather conditions, including abnormally cold weather related to the La Niña phenomenon as well as the passing of yet another severe tropical storm through the Caribbean further impacted the quantities available for export. Shortages in refrigerated containers stemming from the prolonged lockdowns implemented in some Asian countries during 2022, alongside high global transportation costs in the first half of the year, posed additional obstacles to export growth.

The difficult operating environment in 2022 was further complicated by the depreciation of many currencies against the United States dollar, which affected operations all along the value chain since transactions in the banana and tropical fruits industries, including the purchasing of inputs, are habitually conducted in United States dollars. This exerted additional upward pressure on costs to producers, exporters and importers. Although prices along the respective value chains for bananas and major tropical fruits displayed a tendency to increase in response to firm demand in major import markets in 2022, in most cases this was not sufficient to compensate for the substantially higher costs. While producer costs reportedly ranged some 40-50% above their pre-pandemic levels, prices at export, import, wholesale and retail level rose by only some 10 to 20% on average, leaving concerns about heavily reduced profit margins a key topic for the industry in 2022.

11.3.2. Bananas

Market situation

Preliminary estimates indicate that global exports of bananas, excluding plantain, experienced a decline of 4% in 2022, marking another year of disruption to the fast-paced growth experienced in pre-pandemic years. Total export quantities were thereby estimated to have fallen from 20.5 Mt in 2021 to approximately 19.6 Mt in 2022. The persistently high costs of fertilisers, which had already led to a reduction in use in 2021, were quoted as the key obstacle affecting producers’ ability to supply bananas in adequate quantities and to the quality standards expected in export markets in all regions. Adverse weather conditions affecting production and yields additionally continued to be of concern during the first nine months of 2022, while high costs for land transport and long-distance shipping impeded exporters’ capacity to supply international markets. Severe concerns about the spread of plant diseases, importantly the devastating spread of the Banana Fusarium Wilt Tropical Race 4 (TR4) disease in the Philippines and its alarming presence in Peru and Colombia, further continued to cause substantial strain on the industry through the additional costs associated with disease prevention and production losses. Moreover, in view of the ongoing pandemic, the persisting necessity to apply elevated sanitary measures and physical distancing to protect workers from COVID-19 continued to cause additional costs to producers and operators along the supply chain, especially during the first half of 2022.

Global net import quantities of bananas, meanwhile, declined by an estimated 2.5% in 2022, a reduction of nearly 0.5 Mt from the previous year, to just below 19 Mt. While demand in most import markets reportedly remained constant, growth over the first seven months of the year was hindered by a reduced availability of export supplies as well as continuing bottlenecks in global shipping, which posed obstacles to supplies reaching their destination. These factors particularly affected the level of import quantities received over this period by the European Union, the United States, Japan, the United Kingdom and Canada, which jointly account for some 60% of global imports. On the other hand, imports by China, the third largest importer of bananas globally, continued to expand at a fast rate over the first seven months of 2022, facilitated by strong domestic demand and ample availability of export supplies from emerging producers in Southeast Asia.

Projection highlights

As per capita demand for bananas is becoming increasingly saturated in most regions, growth in global production and consumption is expected to be primarily driven by population dynamics. In line with slowing world population growth, the current baseline projections therefore expect world production and consumption of bananas to expand at a moderate 1.5% p.a. over the outlook period. Assuming normal weather conditions and no further spread of banana plant diseases, global banana production will reach 141 Mt by 2032. At the same time, in some rapidly emerging economies – principally in India and China – fast income growth is anticipated to stimulate changing health and nutrition perceptions and support demand for bananas beyond population growth. Accordingly, Asia which is already the leading producing region is anticipated to remain so at a quantity share of 50%, with India projected to reach an output of 35 Mt by 2032.

Production from the leading exporting region of Latin America and the Caribbean is projected to reach 37 Mt by 2032, encouraged by rising demand from key importing markets, most importantly the European Union and the United States. With inflationary pressures expected to continue in 2023 and potentially beyond, demand for bananas in these markets is likely to be supported by the fruit’s relative affordability. Rising import demand from China, where domestic production is likely to continue to decline, is assumed to be an additional factor driving production growth in Latin America and the Caribbean. The largest exporters from the region – critically Ecuador, Guatemala, Colombia, and Costa Rica – all continue to be well positioned to benefit from this growth, assuming that it can be shielded from the adverse effects of erratic weather events and disease outbreaks. Rising import demand from the European Union and the United Kingdom is further expected to benefit some Caribbean exporters, most notably the Dominican Republic and Belize, as well as exports from Africa, which are projected to expand at 1.8% p.a. over the outlook period – led by Ivory Coast – to reach a total quantity of approximately 0.85 Mt in 2032. Against this background, world exports of bananas are projected to reach some 23.7 Mt by 2032.

11.3.3. Mango, mangosteen and guava

Market situation

Preliminary data indicate that global exports of mango, mangosteen and guava declined to approximately 2.1 Mt in 2022, a decrease of 5%, or some 0.12 Mt, from the previous year. The main reasons behind this were a substantial drop in exports of mangosteen from Thailand, as well as lower exports of mangoes from Brazil and Peru, which could not be offset by higher exports from Mexico, the leading exporter of this commodity group. In terms of export quantities by type at the global level, mango accounted for around 83% of global shipments and mangosteen for around 16%. As previously, guava continued to display a low availability in import markets, in particular due to its lower suitability for transport.

Total global import quantities of fresh mangoes, mangosteens, and guavas fell by an estimated 1% in 2022, to some 2 Mt, as suggested by available monthly trade data up to August 2022. The United States and the European Union remained the two leading global importers, with approximate import shares of 26% and 18%, respectively. In both markets industry sources reported higher consumer demand for mangoes, despite prices and inflationary pressures being high, in line with a generally higher nutritional awareness of the assumed health benefits of these fruits. However, import growth in the United States over the first eight months of the year were somewhat constrained by the difficult supply situation in Peru and Brazil, the second and third leading origins for mangoes in the United States, which seemingly could not be fully offset by higher imports from Mexico. Overall, imports into the United States thereby remained largely at their previous year’s level of approximately 0.56 Mt in 2022. Imports into the European Union, meanwhile, declined by an estimated 5% in 2022, to some 0.39 Mt, similarly on the back of supply shortages in Brazil and Peru, the two primary origins of mangoes imported to the European Union.

Projection highlights

Global production of mangoes, mangosteens and guavas is projected to increase at 3.3% p.a. over the next decade, to reach 84 Mt by 2032. As with most other tropical fruits, growth in mango production will mainly respond to income-driven demand growth in producing countries, additionally supported by population dynamics. Asia, the native region of mangoes and mangosteens, will continue to account for some 70% of global production in 2032. This will be primarily due to strong growth in domestic demand in India, the leading producer and consumer of mangoes globally, where rising incomes and associated shifts in dietary preferences will be the main drivers of production expansion. Mango production in India is accordingly projected to account for nearly 38 Mt in 2032, or 45% of global production, destined largely for local informal markets. As such, India is projected to experience increases in per capita consumption of 2.4% p.a. over the outlook period, reaching 24.8 kg in 2032, compared to 18.3 kg in the base period. By contrast, in Mexico and Thailand, the leading exporters of this commodity cluster to world markets, production growth will primarily be driven by expanding global import demand. Exports are accordingly anticipated to reach a 31% share of production in Mexico by 2032, and 26% in Thailand. However, at projected production quantities of 3.2 and 1.8 Mt in 2032, respectively, Mexico and Thailand will account only for comparatively small shares in global production.

Global exports of mangoes, mangosteens and guavas are projected to reach 2.8 Mt in 2032, compared to 2.2 Mt in the base period, on account of higher procurements from the United States, China, and the European Union. Mexico, the leading supplier of mangoes, is expected to benefit from further growth in import demand from its major market, the United States, and reach a 35% share of world exports in 2032. Shipments from Thailand, almost exclusively mangosteens, will cater mainly to rising import demand from China, while supplies from Peru and Brazil, two emerging exporters, will be mostly mangoes destined for the European Union. Both Thailand and Peru are projected to reach a share in global exports of 15% each by 2032, followed by Brazil at some 11%. China, whose per capita mango, mangosteen and guava consumption of 2.6 kg in the base period is relatively low compared to other Asian countries, is expected to experience a rise in imports of 3% p.a., to some 0.36 Mt in 2032. This will be mainly due to a strong income-driven increase in Chinese import demand for mangosteen, as domestic production of this fruit remains low in China.

11.3.4. Pineapple

Market situation

Based on preliminary trade data, global exports of pineapples fell by an estimated 1.5% in 2022, to just below 3.2 Mt, determined largely by reduced supplies from Costa Rica, the world’s largest exporter at a market share of almost 70%. According to industry information, cold weather conditions, high energy costs and container problems negatively affected production and export supplies from Costa Rica in 2022. Shipments from the country were accordingly expected to fall by some 2% in 2022, equivalent to a drop of some 0.05 Mt, to just below 2.2 Mt, in strong contrast with the 11% expansion experienced in 2021. In terms of leading destinations, pineapple shipments from Costa Rica continued to be almost exclusively destined to the United States and the European Union.

Preliminary trade data point to a decline of global imports of pineapples to 2.9 Mt in 2022, a fall of an estimated 1% compared to 2021, on account of supply shortages from the main global supplier, Costa Rica. As demand in the United States and the European Union continued to be solid over the first nine months of the year, indicative average import unit values in both key destinations displayed a tendency to increase. Aided by a strong dollar and an upswing of sales in the hospitality sector, imports by the United States increased by an estimated 4% in 2022, to 1.1 Mt. Conversely, imports by the European Union, the second largest importer, fell by an estimated 8% as supply shortages and shipping issues reduced the quantities that could be received throughout at least the first nine months of the year. Weaker economic conditions and a lower value of the euro against the US dollar posed further difficulties. Over the full year, imports by the European Union were anticipated to drop to approximately 0.76 Mt, some 17% below their previous five-year average. Estimates thereby suggest that the United States procured about 39% of global export supplies over the full year 2022, and the European Union some 26%.

Projection highlights

Over the next decade, global production of pineapple is projected to grow at 2% p.a., to reach 32 Mt in 2032, on account of a 1.7% expansion in harvested area. Asia is expected to remain the largest producing region and account for some 44% of quantities produced globally, with pineapple production being sizeable in the Philippines, Thailand, India, Indonesia and China. Cultivation in Asia will continue to largely cater to domestic demand and is projected to grow solidly in response to changing demographics and income growth, especially in India, Indonesia and China. Similarly, pineapple production in Latin America and the Caribbean, the second largest producing region at a projected 34% of world production in 2032, will be primarily driven by the evolving consumption needs of the region’s growing and increasingly affluent population. Only Costa Rica and the Philippines, two important global producers and leading exporters to world markets, are anticipated to see additional stimulation from rising import demand, with exports expected to account for approximately 68% of fresh pineapple production in Costa Rica and 18% in the Philippines in 2032.

Global exports of fresh pineapple are set to grow at 1.3% p.a., to 3.5 Mt in 2032, predominantly driven by import demand from the United States and the European Union. With projected imports of 1.1 Mt in 2032 – equivalent to a 34% global share – the United States are expected to remain the largest importer, ahead of the European Union, which is expected to account for some 26% of global imports. In both key import markets, demand for fresh pineapples is assumed to benefit from the fruit’s continuously low unit prices and to some degree also from the introduction of more premium novelty varieties. Rising import demand from China, where consumption growth has been outpacing production expansion in recent years, is expected to additionally drive expansion in global exports. By 2032, China is projected to reach import quantities of some 0.39 Mt per year, with supplies likely to be primarily sourced in the Philippines.

11.3.5. Avocado

Market situation

Global exports of avocado declined by an estimated 6% in 2022, to below 2.4 Mt, on account of severe weather-induced supply shortages in Mexico, the world’s leading exporter. Although preliminary data and information indicate that exports from most alternative origins continued to grow at comparatively fast rates, these increases seemingly did not fully offset the unprecedented shortfall in supplies from Mexico. Available monthly data for exports from Mexico for the period January to August 2022 indicate a year-on-year fall in shipments of 32%, pointing to a full-year estimate of 1 Mt, some 0.38 Mt below the previous year’s level.

Global imports of avocados similarly fell by an estimated 6% in 2022, to approximately 2.3 Mt. Despite continuously strong demand in the two major import markets, the United States and the European Union, which were estimated to respectively account for 45% and 25% of global imports in 2022, overall growth in global imports was curtailed by the supply shortages experienced in Mexico. As such, imports by the United States declined by an estimated 11% in 2022, to approximately 1 Mt. The United States are particularly susceptible to changes in the supply situation in Mexico since they typically import some 90% of avocados from this origin. Meanwhile, imports into the European Union seemingly remained relatively stable at some 0.58 Mt, displaying only a very slight tendency to contract. Like the situation in the United States, consumption across the European Union continued to gain in popularity among an increasingly health-conscious population, with avocados widely perceived as a highly nutritious fruit.

Projection highlights

Avocado has the lowest production level among the major tropical fruits but has experienced the fastest expansion in output in recent decades and is expected to remain the most rapidly growing commodity of the major tropical fruits over the outlook period. Ample global demand, high returns per hectare and lucrative export unit prices continue to be the main drivers of this growth, stimulating investments in area expansion in both major and emerging production zones. By 2032, production is thereby projected to reach 12 Mt p.a. – more than three times its level in 2010. While new growing areas have been emerging rapidly in recent years, avocado production is likely to remain largely concentrated in a small number of regions and countries. The top four producing countries – Mexico, Colombia, Peru and the Dominican Republic – are projected to expand their production substantially over the coming decade, together accounting for over 50% of global production in 2032, with output in Colombia and Peru set to increase by some 60-70% from base period levels. As such, about 66% of avocado production is expected to remain in Latin America and the Caribbean, given the favourable growing conditions in this region.

In response to rapidly growing global demand, and facilitated by fast output expansion, avocado is on track to become the most traded major tropical fruit by 2032, reaching 3.8 Mt of exports and overtaking both pineapples and mangoes in quantity terms. Given the high average unit prices of avocado, the total value of global avocado exports would thus reach an estimated USD 8.7 billion in constant 2014-16 value terms, thereby placing avocado as one of the most valuable fruit commodities. Despite increasing competition from emerging exporters, Mexico is expected to retain its leading position in global exports at a 40% share in 2032. This will be supported by output growth of 3.6% p.a. over the coming decade and continued growth in demand in the United States, the key importer of avocados from Mexico. Exports from Peru, the second leading exporter, will reach some 24% of global shipments, with supplies mainly catering to rising demand from the European Union.

The United States and the European Union, where consumer interest in avocados is fuelled by the fruit’s claimed health benefits, are expected to remain the main importers, with 44% and 27% of global imports in 2032, respectively. However, imports are also set to rise rapidly in many other countries such as in China and some countries in the Middle East, on account of rising incomes and changing consumer preferences in these markets. Similarly, in many producing countries, per capita consumption of avocados is expected to rise with income growth, notably in Colombia, the Dominican Republic and Indonesia. It is important to note, however, that in both domestic and import markets, demand for avocados may be susceptible to changes in the macroeconomic outlook. Given the typically high unit values of avocados, as well as their relatively high income and price elasticities of demand, changes in consumer incomes – or prices – may quickly affect demand. That said, import demand for avocados has exhibited relative resilience to changes in income in both major import markets, the United States and the European Union, where demand also appears determined by changes in consumer preferences, as demonstrated by the fruit’s uninterrupted robust growth over the past decade.

11.3.6. Papaya

Market situation

Preliminary trade data indicate a rise in global exports of papayas by an estimated 1% in 2022, to some 0.37 Mt. Exports from Mexico, the largest global exporter of papayas, seemingly grew by some 4% over the full year, on account of further production expansion. Virtually all Mexican papaya exports are destined for the United States, which globally ranks as the largest importer of papayas, accounting for over half of global imports in 2022. The bulk of Mexican papaya production, however, is destined for domestic consumption, meaning that trade outcomes depend critically on developments in both domestic and foreign markets.

Global imports, meanwhile, remained largely stable at some 0.34 Mt in 2022, albeit displaying a slight tendency to contract by an estimated 0.3%. Available data indicate that imports by the United States grew by an approximate 1% in 2022, to some 0.19 Mt, facilitated by the ample supply situation in Mexico, the leading supplier of papayas to the United States. Although the estimated pace of growth was noticeably slower than in 2021, when imports by the United States grew by 5% year-on-year, industry sources stated that demand for papayas in the United States remained solid over the first nine months of 2022. The second leading importer globally continued to be the European Union, albeit with a much lower share in world imports of only 10%. Consumer awareness of papaya in the European Union remains low, mostly due to the fruit’s fragility in transport, which renders a significant expansion in this market difficult to attain.

Projection highlights

Global papaya production is projected to rise by 1.9% p.a., to 18 Mt in 2032. As the share of exports in production is particularly low for papayas, at some 2.5% in the base period, production of this fruit is mostly driven by domestic demand due to population and income growth. Against this background, the strongest production expansion is expected to be experienced in Asia, the leading producing region globally, where both drivers are expected to have significant impact. Accordingly, Asia’s share of world production is set to rise to 60% by 2032, from 58% in the base period. The world’s largest producer, India, is projected to increase its papaya production at a rate of 1.6% p.a., thereby expanding its share of global output to 37% by 2032. Income and population growth will be the main factors behind this rise, with Indian per capita consumption of papayas expected to reach 4.4 kg in 2032, up from 4.1 kg in the base period. In Indonesia, meanwhile, production is projected to grow by 2.8% p.a. over the outlook period, primarily on account of increasing domestic demand as per-capita incomes are expected to expand at over 4% p.a.

Global exports will predominantly be shaped by production expansion in Mexico, the largest global exporter of papayas, and higher demand from the key importers, the United States and the European Union. At an expected average annual rate of 1.9%, global exports of papayas are projected to reach just over 0.46 Mt by 2032. However, a major obstacle to a significant expansion in international trade remains the fruit’s high perishability and sensitivity in transport, which makes produce problematic to supply to far afield destinations. Innovations in cold chain, packaging and transport technologies promise to facilitate a broader distribution of papaya, particularly in view of rising consumer demand for tropical fruits in import markets.

11.3.7. Uncertainties

With regard to the outlook, several significant threats to global production, trade and consumption of bananas and major fresh tropical fruits are present. On the demand side, prevailing high inflation rates, high interest expenses and exchange rate fluctuations threaten to hinder the demand for bananas and tropical fruits, especially for consumers in poorer economic strata who need to spend a higher proportion of their income on food. Some analysts have also been predicting a global recession, and while recently released forecasts now seem to rule out this scenario, at least for 2023, should it nevertheless materialize, this may further restrain demand growth. The uncertainties surrounding Russia’s war against Ukraine with regard to its impact on global supply chains, fertiliser markets, transport routes and access to export markets add further risks for the outlook.

On the supply side, the effects of global warming are resulting in a higher occurrence of droughts, floods, hurricanes and other natural disasters, which render the production of bananas and major tropical fruits increasingly difficult and costly. Given the perishable nature of tropical fruits in production, trade and distribution, environmental challenges and insufficient infrastructure continue to jeopardise production and supply to international markets. This is a particularly acute difficulty since the vast majority of tropical fruits are produced in remote, informal settings, where cultivation is highly dependent on rainfall, prone to the adverse effects of increasingly erratic weather events and disconnected from major transport routes.

In the face of rising temperatures, more rapid and more severe spreads of plant pests and diseases are additionally being observed, as for example is the case with the fungus Banana Fusarium Wilt. The currently expanding strain of the disease, described as Tropical Race 4 (TR4), poses particularly high risks to global banana supplies as it can affect a much broader range of banana and plantain cultivars than other strains of Fusarium wilt. Furthermore, despite some recent breakthroughs in the engineering of resistant varieties, no effective fungicide or other eradication method is currently available. According to official information, TR4 is currently confirmed in 21 countries, predominantly in South and Southeast Asia, but also in the Middle East, Africa, Oceania and Latin America, with Colombia reporting the first infection in August 2019, Peru in April 2021, and Venezuela in January 2023. An indicative assessment of the potential economic impact of the TR4 disease on global banana production and trade showed that a further spread of TR4 would, inter alia, entail considerable loss of income and employment in the banana sector in the affected countries, as well as significantly higher consumer costs in importing countries, at varying degrees contingent on the actual spread of the disease.

Given the popularity particularly of bananas, pineapples and avocados in import markets, their global value chains have been characterised by intense competition among market actors all the way to the retail level. For bananas and pineapples, this has exerted downward pressure on prices at each stage, which has resulted in producer prices remaining at low levels, with little fluctuation. Combined with rising production costs, low prices and tight profit margins greatly hinder the adequate remuneration of workers and smallholder farmers in these industries and act as a major obstacle for producers in coping with emerging challenges and supply chain disruptions. The prospects for production are therefore further threatened by an elevated risk of industry contraction, with producers discouraged to continue their operations by low or even negative producer margins, reducing supplies to world markets and consequently causing higher food prices. Data on developments in world export and import markets over the course of 2022 already point to this direction, with all key regions being affected.

Note

← 1. Pulses types: dry beans, dry broad beans, dry peas, chickpeas, cow peas, pigeon peas, lentils, Bambara beans, vetches, lupines and minor pulses (not elsewhere specified)