2. Pathways to decarbonise transport by 2050

This chapter presents three policy scenarios for the development of transport demand and associated emissions over the next 30 years. Results are aggregated across passenger and freight transport and provide an overall view of the entire transport sector. It also discusses global approaches to transport decarbonisation that will ensure fair burden-sharing among social groups and countries.

Better transport for tomorrow requires action now

Transport is at a pivotal moment. Will its share of global emissions continue to grow? Or can it meet the decarbonisation targets of the Paris Agreement by 2050? This chapter presents the Recover, Reshape and Reshape+ scenarios: three different decarbonisation routes that transport could take over the next 30 years. They diverge in their approach and ambition, and show how the choices made now would play out as the world strives to keep global warming to below 1.5˚C.

The Recover scenario is based on the world’s current trajectory of implemented and announced policies. It assumes that the international community adheres to its current climate initiatives, but will base economic recovery from the Covid-19 pandemic largely on the economic practices of past decades. The return to such a “normal” will take us down the wrong road: In the Recover scenario, the international community falls well short of its agreed climate goals. Transport CO2 emissions would not decrease; they would surge to more than triple the amount targeted for 2050 as the maximum that would limit global warming.

The Reshape and Reshape+ scenarios present more optimistic visions of the future. Under Reshape, governments adopt transformational decarbonisation policies that pivot transport onto a sustainable path and put the climate goals of the Paris Agreement within reach. In the Reshape+ scenario, policies for pandemic recovery are accelerated and reinforced in a way that puts transport on a fast track to achieving the climate goals. In a Reshape and Reshape+ world, the historic link between economic growth and rising transport emissions is broken. Transport demand still grows, but emissions fall.

The core assumption of the Reshape and Reshape+ is an ambitious decarbonisation agenda. Their policies succeed in avoiding unnecessary travel, shifting mobility to more sustainable transport options, improving transport technologies in ways that make them less emitting They also enhance the resilience of transport networks.

Such ambitious policies can and must be executed in a way that ensures fair burden-sharing and avoids adding to existing inequalities. Implementation of climate policies, especially those that involve pricing mechanisms, should account for the specific impacts on different groups of society. They also should leverage global capital to enable all world regions to pursue effective transport decarbonisation.

The ITF Transport Outlook 2021 presents projections for transport demand and related emissions under three different policy scenarios for the coming three decades. Recover, representing the world’s current trajectory, includes existing commitments for decarbonisation and assumes governments prioritise economic recovery by reinforcing established economic activities. It shows that current ambitions are not enough to achieve climate change mitigation targets, exceeding the carbon budget for the transport sector defined by the experts of the International Panel on Climate Change (IPCC, 2018[1]) that would still be consistent with limiting global warming to below 1.5˚C. The Reshape scenario assumes an ambitious set of decarbonisation policies, characterised by pro-active policies which respond to environmental challenges in the transport sector and support the United Nations’ Sustainable Development Goals (SDGs). As a result, staying within transport’s carbon budget becomes a possibility. The Reshape+ scenario reinforces the policies of Reshape and exploits opportunities for decarbonisation created by the Covid-19 pandemic, such as encouraging certain changes in travel behaviour. Under Reshape+ scenarios, the international community could reach its goals for climate change mitigation faster and with more certainty.

The Recover, Reshape and Reshape+ scenarios assess the impacts of different policy pathways on global transport demand, greenhouse gas emissions (reported as CO2 equivalents), local pollutant emissions, accessibility, connectivity and resilience (depending on the sector) up to 2050. The emissions are based on transport activity and do not include emissions from vehicle production or construction and operation of transport infrastructure.

The three scenarios represent increasingly ambitious efforts by policy makers to decarbonise the transport sector while also meeting the UN Sustainable Development Goals (SDGs). All scenarios account for the Covid-19 pandemic by including the same baseline economic assumptions for the pandemic’s impacts. Uncertainty surrounds its economic fallout, the behavioural shifts it may trigger, and the extent to which it will affect transport supply and travel patterns both in the long and short term. The ITF models use middle-of-the-road assumptions that lie somewhere between the most optimistic and most pessimistic forecasts available at the time of modelling.

For GDP and trade in 2020, the ITF models assume a drop in all world regions, based on the International Monetary Fund’s World Economic Outlook June update (IMF, 2020[2]) and the World Trade Organization’s Trade Statistics and Outlook (WTO, 2020[3]) applied to baseline GDP and trade values from the OECD ENV-Linkages model (OECD, 2020[4]). Following years assume the previous country-specific growth rates after 2020. This is approximated by a five-year delay in GDP and trade projections compared to pre-Covid-19 levels from 2020. Assumptions of economic activity and trade are held constant between all scenarios to better compare the true transport policy impact on activity, CO2 emissions and other outcomes. Air connectivity growth is also adjusted to account for the severity of the pandemic’s impact on aviation. For 2020, ITF models assume a drop in flight frequencies and pre-Covid-19 growth rates to meet the projections for 2025 by the International Air Transport Association (IATA, 2020[5]).

In Recover, governments prioritise economic recovery by reinforcing established economic activities. They continue to pursue existing (or imminent) commitments to decarbonise the transport sector, predating the pandemic. Alongside these, governments take action with policies that ensure some of the transport trends that hinder decarbonisation observed during Covid-19 revert back to previous patterns by 2030, as a bare minimum. These include reversing trends in greater private car use and reducing public transport ridership, for example. Changes in behaviour such as reduced business travel or significant shifts to active mobility, which have lowered CO2 emissions, also revert to pre-pandemic norms by 2030. These short-term trends are listed in Chapter 1 (Table 1.1.). Due to limited policy action on technology innovation, cost reduction in clean energy and transport technologies does not take place to the extent it could. The Recover scenario is an updated version of the Current Ambition scenario in the ITF Transport Outlook 2019, accounting for Covid-19 related changes and policies announced since.

The Reshape scenario represents a paradigm shift for transport. Governments adopt transformational transport decarbonisation policies in the post-pandemic era. These encourage changes in the behaviour of transport users, uptake of cleaner energy and vehicle technologies, digitalisation to improve transport efficiency, and infrastructure investment to help meet environmental and social development goals. As in Recover, the Reshape scenario also assumes that transport trends and patterns observed during the pandemic revert to previous patterns by 2030.

In Reshape+, governments seize decarbonisation opportunities created by the pandemic, which reinforce the policy efforts in Reshape. Measures reinforce changes in travel behaviour observed during the pandemic, such as reducing business travel or encouraging walking and cycling. Some of these policies are fast-tracked or implemented more forcefully than in Reshape. The scenario assumptions also include pandemic impacts on non-transport sectors that may nevertheless influence transport, for instance, a regionalisation of trade due to near-sourcing to improve resilience. Under Reshape+, CO2 emission targets for the transport sector can be achieved sooner and with more certainty and with less reliance on CO2 mitigation technologies whose efficacy is still uncertain.

The Reshape and Reshape+ scenarios show what is possible with technologies and policies available today, but with increased investments and more political ambition. The policies act additively, meaning that while there are adjustments made for regions, most policies are applied to most regions with some adjustment for regional contexts. Results are not prescriptive in assigning certain combinations of measures to specific regions. The results show what is technically feasible under full implementation. Still, it is recognised that there may be political and financial constraints that require prioritisation of measures depending on local contexts. The policy scenarios show what may happen at a global and regional level under a set of policies to manage transport demand, shift to more sustainable modes, and improve the energy efficiency of vehicles and fuels.

There are many modelling approaches to assess necessary actions for decarbonisation. The ITF models are demand-based and favour a bottom-up approach which starts with potential policy scenarios and evaluates resulting activity and CO2 emissions. Other useful modelling exercises such as backcasting from a specific goal offers a different set of advantages and drawbacks. Backcasting starts with a goal and works backwards to see where demand and technologies must be to meet such a goal. The ITF favours the current method over backcasting because it allows for creating the most realistic, and therefore relevant scenarios. The current lack of data available to determine regional and sectoral goals across the globe means that selecting a realistic scenario that reflects the unique constraints of every region is not possible.

This chapter provides aggregate long-term results from the sector chapters and presents an overall summary of possible future trends under the policy scenarios. Aggregate CO2 emissions are compared against the carbon targets for transport as determined by the (IPCC, 2018[1]). Chapters 3 to 5 discuss how the transport challenges created by Covid-19 can be addressed and how decarbonisation and sustainable mobility policies can be implemented equitably to achieve environmental and societal goals.

Measures to decarbonise transport: Avoid, shift, improve

Transport decarbonisation measures aim to avoid unnecessary travel, shift necessary travel to sustainable modes and improve vehicle and energy technologies. In recent years, the latter has also encompassed the improvement of transport system efficiency. These measures have positive impacts on CO2 emissions but vary in their impact on society. Concentrating on any one of these in isolation will not solve the social and environmental challenges transport faces. Instead, policy makers will need to adopt a holistic approach to prioritising policies based on a balance of what is most appropriate in terms of impact, sector, and region.

Avoid measures reduce transport activity without limiting access to goods and services. For instance, integrated urban planning with mixed neighbourhoods can reduce trip lengths. Teleconferencing can replace some air travel. Avoid measures aim to offer the same economic and social benefits with fewer passenger-kilometres (or tonne-kilometres) travelled. Avoid measures can help reduce demand, but their effectiveness and pace of adoption are limited by the constraints posed by structural issues including the distribution of jobs, existing land-use patterns and the presence of pre-existing infrastructure. For example, sprawled neighbourhoods require densification to enable this sort of demand reduction.

Shift measures transfer trips from energy-intensive transport modes to energy-efficient ones. A shift from motorised to active modes is most desirable, where possible. It also provides benefits by reducing costs for users, congestion and air pollution. For longer urban trips, using urban rail instead of private cars delivers a 91% lower final energy use per passenger-kilometre (IEA, 2020[6]). Similar reductions hold for shifts from aviation to high-speed rail (93% lower energy use per passenger-kilometre) and from trucks to freight rail (72% lower energy use per tonne-kilometre) (IEA, 2020[6]). Other lifecycle aspects need to be accounted for, however, including emissions associated with infrastructure (IEA, 2019[7]). Policy makers can promote a shift to more efficient transport modes by facilitating safe active travel and supporting the roll-out of public transport infrastructure. Additional support for the promotion and support of energy, resource and space-efficient transport modes can be provided by resources raised from taxation on land-use requirements, congestion, and energy use of private cars, and through financial incentives for energy-efficient transport modes.

A complete shift away from high-emission modes is not feasible. For many long-distance and international movements, aviation is the most feasible choice. Mode shift is difficult to achieve at scale because rail services can only replace air travel on high-demand routes and over a limited distance (IEA, 2019[7]). In the freight sector, a sizable component would still be moved by truck even if the maximum possible amount of road freight were shifted to rail and inland waterways. Freight rail services are best suited for major axes of freight transport flows, but road transport offers greater flexibility for the timely delivery of goods. In passenger transport, a shift away from private vehicles is only possible if alternatives are available. Shifting to active travel modes and public transport in compact urban areas is easier due to the density of infrastructure and services and relatively short trip distances. However, such shifts are more limited in rural and peri-urban areas where low-density developments and longer trip distances make public transport and active travel more challenging. Policy measures also have different impacts depending on socio-demographic characteristics and attitudes of individuals. The ITF urban passenger model partially accounts for these by differentiating the impact of policies by age and gender cohorts.

Improve measures enhance the energy efficiency of vehicles, lower the carbon intensity of fuels or increase operational efficiency. Optimised routing can reduce emissions from congestion, asset sharing in logistics can increase load factors, and seamless transfers between transport modes can make multimodal solutions more attractive. Fuel economy standards can accelerate the adoption of new vehicle technologies and thereby reduce fuel use. Carbon taxes, low-carbon fuel standards or biofuel blending mandates lower the emission-intensity of transport fuels. Promoting a shift to electric vehicles can both improve the energy efficiency of vehicles and facilitate the use of electricity, which can be a low-emission source of energy. These policies can also stimulate major investments in material extraction and recycling, battery manufacturing, the refurbishment or construction of vehicle manufacturing facilities, the deployment of reinforced and smart electricity grids and charging infrastructure, with a positive impact on economic development.

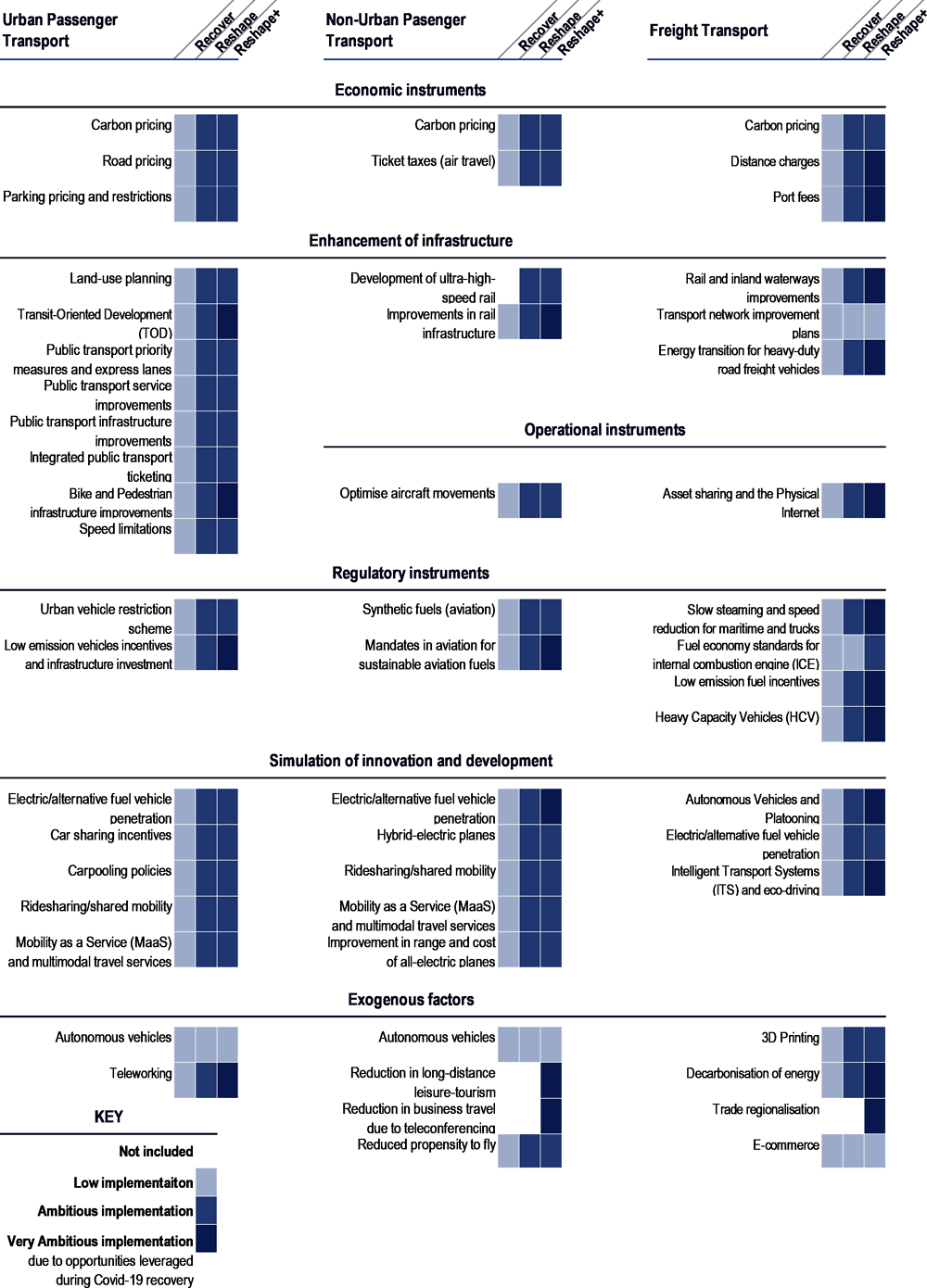

The policy measures included in Recover, Reshape, and Reshape+ scenarios are illustrated in Figure 2.1 for all sectors. More detailed assumptions for each measure are available in the sector-specific discussions in Chapters 3-5. More than 60 decarbonisation measures for all modes and transport sectors are available in the Transport Climate Action Directory, a database provided by ITF for use by governments and industry (see Box 2.1).

Climate change cannot be stopped without addressing the transport sector. In 2016, after the signing of the Paris Agreement, the International Transport Forum (ITF) launched the Decarbonising Transport initiative to help governments and industry transform their climate ambitions into actions through carbon-neutral mobility.

The Decarbonising Transport initiative (www.itf-oecd.org/decarbonising-transport) is a partnership of more than 70 governments, organisations, institutions, foundations, and companies under the auspices of the ITF. In July 2020, the Transport Climate Action Directory, a key output of the Decarbonising Transport initiative, was launched.

The Transport Climate Action Directory (TCAD) (http://www.itf-oecd.org/tcad) is an online database of policy measures to reduce transport CO2 emissions across all modes including maritime and aviation, and for both passenger and freight activity. It currently contains more than 60 different mitigation measures along with an evidence base to help assess their effectiveness. It is a living directory, and additional measures will be reviewed and added over time.

The web tool offers the user filters to short-list measures for targeted decarbonisation results. The categories include measure type, transport mode and geographic scope. For ease of use, the Transport Climate Action Directory also categorises decarbonisation measures under five different policy outcomes:

The outline for each measure is concise and includes links to external sources. Each outline contains a description of the measure and potential impact on CO2 emissions. A costs section describes potential sources of cost and potential co-benefits, to help with evaluating business cases and further understanding of how a measure could contribute to wider objectives. Equally, some considerations that may need to be taken into account in implementation planning are outlined. There is also a function allowing users to suggest additional information for the measures or to propose new measures for inclusion in the directory. This further allows the sharing of knowledge from one user to others.

Both passenger and freight sectors are projected to continue growing in the long term. Total passenger-kilometres and freight demand (measured in tonne-kilometres) will more than double by 2050 under current policies, even if their growth rates diminish as a result of the global pandemic. When compared to the Current Ambition scenario of the ITF Transport Outlook 2019, the growth of total passenger and freight activity is now lower than projected due to updates to reflect new policy commitments and less optimistic economic growth figures, even before the effects of the Covid-19 pandemic were felt.

As economies and populations grow, demand for goods grows, as does the number of people with the desire and means to travel. Yet economic growth that comes in tandem with increased transport activity is unsustainable because of the huge negative impacts its emissions create. Only decoupling transport activity and emissions from economic activity will enable us to maintain a strong economy while saving the climate and, ultimately, improving human well-being,

The modelling results for all sectors indicate a decoupling of transport activity from GDP growth by 2050 if government policies follow the Reshape or Reshape+ scenario. Under Recover policies, only passenger transport in OECD countries, which are primarily developed economies, no longer correlates strongly with changes in GDP. Figure 2.2 compares the sensitivity of transport demand to GDP. The comparison is based on the elasticity of transport demand concerning GDP. For example, a demand elasticity of 0.5 means that for every 1% increase in GDP (in 2011 USD), transport activity (in passenger or tonne-kilometres) will increase by 0.5%. An elasticity of less than 1 indicates decoupling (Tapio, 2005[8]) because the increase in GDP is stronger than the increase in demand. Lower elasticity values indicate greater decoupling between demand and GDP.

Urban transport activity can decouple from GDP growth to a significant degree. GDP and population growth are already expected to be comparatively lower in OECD countries than the rest of the world, but urban passenger transport growth is expected to be even less. The urban demand elasticity is very responsive to higher ambition policies, reducing elasticity from 0.65 to 0.22 between Recover and Reshape. Differences between passenger transport behaviour in OECD and non-OECD countries are partially due to higher rates of teleworking in the Reshape and Reshape+ scenario, which is expected to be more prevalent in wealthier economies (Dingel and Neiman, 2020[9]). In addition, in some emerging non-OECD economies, the existing trip rates are quite low. As incomes and quality of life increases in these regions, it may unlock latent demand and increase per-capita trip rates. Supposing current policies continue, as under a Recover scenario, cities in non-OECD countries would likely grow in sprawling patterns that increase average trip distances. In such a scenario, transport demand would grow more in line with the economy causing a significant surge in demand. However, the scenarios show that urban transport activity in non-OECD countries responds to an accessibility-focussed approach, decoupling from economic growth under Reshape and Reshape+ due to more sustainable land-use policies and other measures.

Growth of non-urban passenger transport and GDP remains linked, even under higher-ambition decarbonisation policies. Unlike urban passenger transport and to a certain extent regional non-urban transport, which can be influenced by land-use changes to enable individuals to access opportunities closer to home, intercity non-urban passenger transport has limited potential to shorten trips since it entails longer distances and limited alternative destinations. While some long-distance tourism may be substituted by destinations closer to home, the primary way to reduce non-urban transport activity is to reduce the number of trips. This happens to a certain extent through teleconferencing (especially after Covid-19), although the impact is not as strong as teleworking in urban travel. The demand elasticity of OECD countries shows the least responsiveness to the policy scenarios, while non-OECD countries show greater sensitivity. Economic growth and non-urban passenger activity in OECD countries are more decoupled in absolute terms. As incomes increase and latent travel demand is realised, the responsiveness of transport demand to GDP in non-OECD countries could decrease.

Domestic freight is less sensitive to GDP growth than international freight transport. Under Recover policies, international freight remains coupled with GDP growth. Both international and domestic freight decouples under Reshape policies. However, changes in trade patterns, including a reduction in demand for fossil fuels and potential trade regionalisation, play a part in reducing international freight activity even more significantly under the policies of a Reshape+ scenario. Domestic freight is not as affected since international trade shifts to more regional goods transport in Reshape+.

Note: Elasticity is calculated as the change in demand (passenger-kilometres or tonne-kilometres) from 2015 to 2050 divided by change in GDP (in 2011 USD) from 2015 to 2050. Elasticities less than one indicate decoupling (i.e. GDP grows more than demand); lower values indicate greater decoupling.

Source: GDP data is from ITF estimates used in the models. Based on the OECD (2020[4]) OECD ENV-Linkages model, http://www.oecd.org/environment/indicators-modelling-outlooks/modelling.htm and the IMF (2020[2]), World Economic Outlook Update, June 2020, https://www.imf.org/en/Publications/WEO/Issues/2020/06/24/WEOUpdateJune2020.

Passenger transport demand

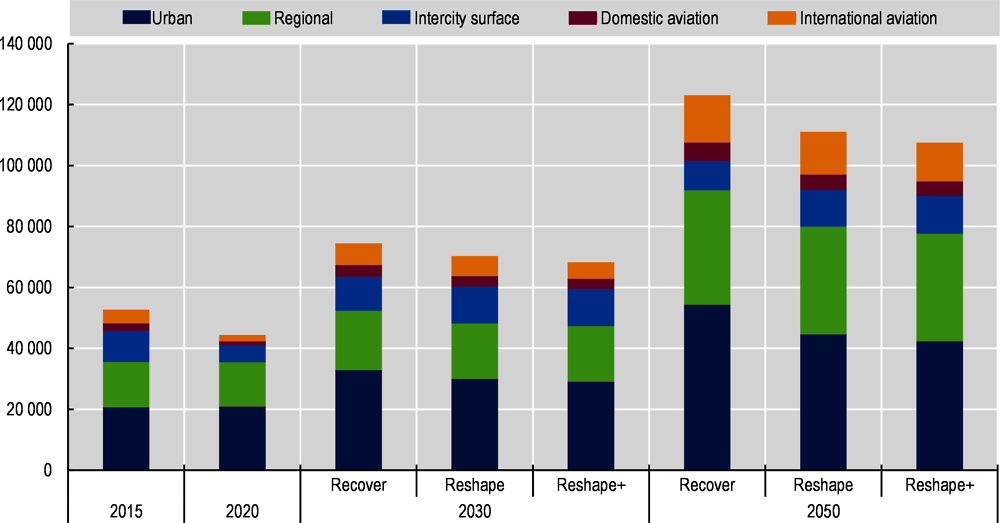

After a temporary reduction in 2020, passenger transport demand doubles between 2015 and 2050 under the Recover scenario (Figure 2.3). Reshape policies could reduce this expected activity by 10% in 2050, and Reshape+ policies could achieve a reduction of 13%.

Daily travel will contribute to nearly three-quarters of total passenger demand by 2050 under a Recover policy environment. Most urban and regional activity (in rural and peri-urban areas) is comprised of daily trips. Together these trips make up two-thirds of demand in 2015, and by 2050 could make up three-quarters (under Recover policies). Accessibility-focussed policies to change land-use patterns and increased adoption of teleworking in the Reshape+ scenario could successfully reduce 22% of 2050 urban demand compared to Recover. Regional demand has less potential for reduction due to limited alternatives; Reshape+ policies could cut passenger-kilometres by 6% in 2050.

Aviation sees the largest relative growth by 2050, increasing by a factor of 3.5 compared to 2015 under the Recover scenario. Demand for air travel is expected to make a strong recovery after the Covid-19 pandemic, particularly for international flights. ITF estimates see aviation should reach 2019 levels by around 2023. Stringent policy measures such as carbon pricing and ticket taxes have only a modest impact as it remains the primary mode of intercity travel in all scenarios due to limited alternatives. As personal lives and business become increasingly globalised, demand for international travel also rises. Stronger policy action under a Reshape scenario reduces domestic aviation demand by 17% compared to Recover in 2050, while international aviation is reduced by 10%. Under Reshape+, these reductions are 19% and 18%, respectively, for domestic and international aviation. The more pronounced change for international travel in Reshape+ shows what may be possible if some post-pandemic behaviours persist, including teleconferencing to replace some business travel and the shift away from long-distance tourism.

Intercity surface travel declines in absolute terms as aviation gains market share in the Recover scenario. However, under Reshape and Reshape+ policies, surface modes become relatively more attractive, and some of aviation’s share is redistributed to them. With the increasing availability of rail infrastructure and the development of low-emission road vehicles, which are less affected by carbon-pricing schemes, intercity surface modes become more attractive.

Note: Figure depicts ITF modelled estimates. Recover, Reshape and Reshape+ refer to the three scenarios modelled, which represent increasingly ambitious post-pandemic policies to decarbonise transport. Regional refers to daily local transport activity that happens outside of urban areas (peri-urban, rural); intercity surface refers to transport movements by private road vehicles (two- and three-wheelers, cars), buses, and rail between urban areas

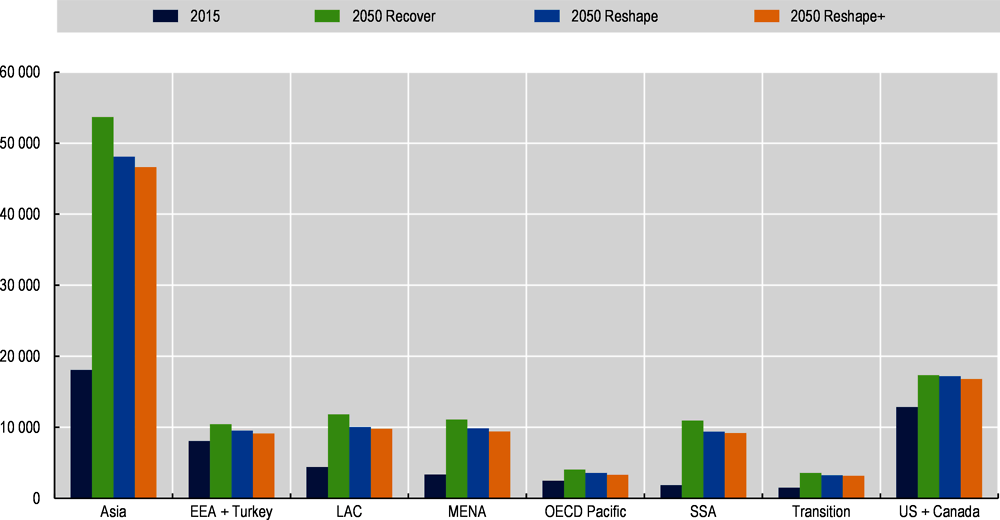

Transport demand increases in all regions regardless of policy scenario. Demand for passenger transport grows most significantly in regions where population and economic growth are expected to be the highest. In absolute terms, Figure 2.4 demonstrates that Asia grows the most, firmly establishing the region as the largest generator of transport demand by a significant margin. A more progressive policy agenda in the region, as envisioned in Reshape+ achieves a reduction of 7 trillion passenger-kilometres in 2050, compared to Recover. Relative to Recover results in 2050, OECD Pacific shows the largest relative response to decarbonisation policies, reducing 2050 passenger-kilometres by 18% under a Reshape+ scenario.

Note: Figure depicts ITF modelled estimates. Recover, Reshape and Reshape+ refer to the three scenarios modelled, which represent increasingly ambitious post-pandemic policies to decarbonise transport. International aviation demand is attributed to the origin country. EEA: European Economic Area. LAC: Latin America and the Caribbean. MENA: Middle East and North Africa. OECD Pacific: Australia, Japan, New Zealand, South Korea. SSA: Sub-Saharan Africa. Transition economies: Former Soviet Union and non-EU South-Eastern Europe.

Freight transport demand

Freight demand continues to grow, but at a slower pace due to economic impacts from the Covid-19 crisis (Figure 2.5.) In Reshape and Reshape+, the global drop in fossil fuel consumption reduces the demand for transport of these resources. The impact of 3D printing in these scenarios is smaller but nevertheless causes some drop in demand. The materials required for 3D printing are primarily raw materials that can be transported at higher load factors compared to finished products (Wieczorek, 2017[10]; Chen, 2016[11]). The exogenous factors of trade regionalisation assumed in Reshape+ slow freight growth even further.

Sea-based transport continues to dominate freight activity with more than 70% of tonne-kilometres, regardless of scenario (Figure 2.5). In Reshape+, the mode share of maritime trade drops slightly due to the drop in import/export transport activity, and particularly in longer distance inter-regional trade. Air and rail activity increases in all scenarios. The share of airfreight remains very small, however, with less than 1% of total tonne-kilometres. Lighter but higher-value goods tend to be transported by air. Urban freight activity growth follows the same overall pattern: it grows in all scenarios compared to 2015 values, but its growth slows in Reshape and even more in Reshape+. Parcel deliveries, such as those in urban freight, can seem small when measured in tonne-kilometres but can account for a large number of trips and vehicle-kilometres given their low weight-to-volume ratio. Parcels are expected to grow more than other commodities in the urban freight commodity mix.

Note: Figure depicts ITF modelled estimates. Recover, Reshape and Reshape+ refer to the three scenarios modelled, which represent increasingly ambitious post-pandemic policies to decarbonise transport. Surface includes freight transport by road and rail, as well as inland waterways, excluding urban freight. Air transport accounts for less than 1% of total demand.

The share of fossil fuels movements among all international transport activity drops from 29% in 2015 to as little as 8% by 2050. Under the conditions of the Recover scenario, its share in 2050 is 17%. Under Reshape, that share is halved to 8%. Under Reshape+, it falls even more compared to 2015 levels but keeps the same 8% share because other commodities also grow at a slower pace. Lower fossil fuel use will have significant impacts on imports and exports in different regions. In 2015, fossil fuels made up nearly half of import-related transport in the European Economic Area (EEA) and Turkey. In Reshape, fossil fuel imports drop 51% by 2050 and 53% in Reshape+. Worldwide, total imports grow 129% in Reshape, and 108% in Reshape+. Transition countries (made up of the Former Soviet Union and non-EU south-eastern European countries) and MENA, which rely heavily on fossil fuel exports, have their export-elated transport activity drop by 21% and 27%, respectively, in a Reshape scenario from 2015 to 2050. In Reshape+ the drop is 26% and 32% respectively.

Figure 2.6 shows the distribution of surface freight demand by region. While tonne-kilometres generated by surface transport (less than 30% of total demand in all scenarios) are attributed to regions, tonne-kilometres completed by sea or air are particularly challenging to attribute to specific countries. In international waters, freight activity is under the jurisdiction of the International Maritime Organisation (IMO). The International Civil Aviation Organization (ICAO) governs international airfreight. Airfreight is responsible for less than 1% of total tonne-kilometres. Figure 2.7 shows the sea regions where maritime activity occurs.

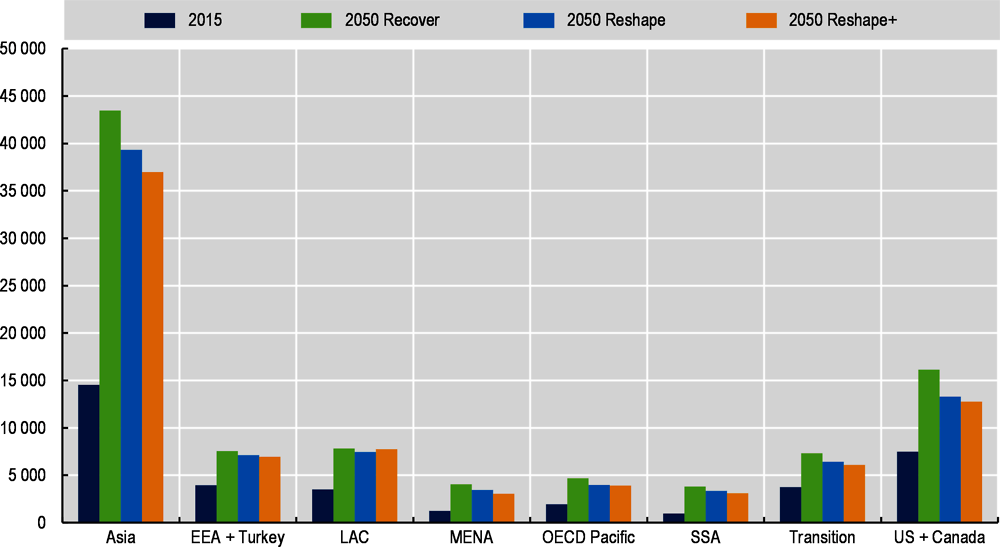

Asia has the greatest demand for surface freight, which could triple under current policies reflected in the Recover scenario. The largest relative increase in freight transport by road, rail, and inland waterways is expected in Sub-Saharan Africa (SSA), where freight demand could quadruple. However, in absolute figures, the region generates the least demand. Reshape+ policies achieve a 15% to 24% decrease in most world regions compared to Recover by 2050, except for Latin America and the Caribbean (LAC) and EEA and Turkey. EEA and Turkey could limit demand by 8% in 2050. LAC experiences a slight increase in surface freight in Reshape+ for Reshape. The assumptions on trade regionalisation in Reshape+ favour trade within the region, leading to an increase in surface tonne-kilometres. However, the total impact when sea-based import and export activity is considered is a reduction in freight activity.

Note: Figure depicts ITF modelled estimates. Recover, Reshape and Reshape+ refer to the three scenarios modelled, which represent increasingly ambitious post-pandemic policies to decarbonise transport. Surface freight includes road, rail and inland waterways. It does not include international maritime and airfreight. EEA: European Economic Area. LAC: Latin America and the Caribbean. MENA: Middle East and North Africa. OECD Pacific: Australia, Japan, New Zealand, South Korea. SSA: Sub-Saharan Africa. Transition economies: Former Soviet Union and non-EU South-Eastern Europe.

The North Pacific and Indian Ocean have the highest levels of freight activity which is expected to more than double in all scenarios, as shown in Figure 2.7. The North Atlantic had similarly high levels of freight activity in 2015 but will not grow to the same extent. The IMO is responsible for setting measures and targets concerning decarbonising freight activity in maritime regions. However, the international nature of shipping requires greater co-ordination and collaboration amongst operators, owners, flag states and port states. Individual countries are often reluctant to act alone in case more ambitious restrictions impact their competitiveness.

Note: Figure depicts ITF modelled estimates. Recover, Reshape and Reshape+ refer to the three scenarios modelled, which represent increasingly ambitious post-pandemic policies to decarbonise transport.

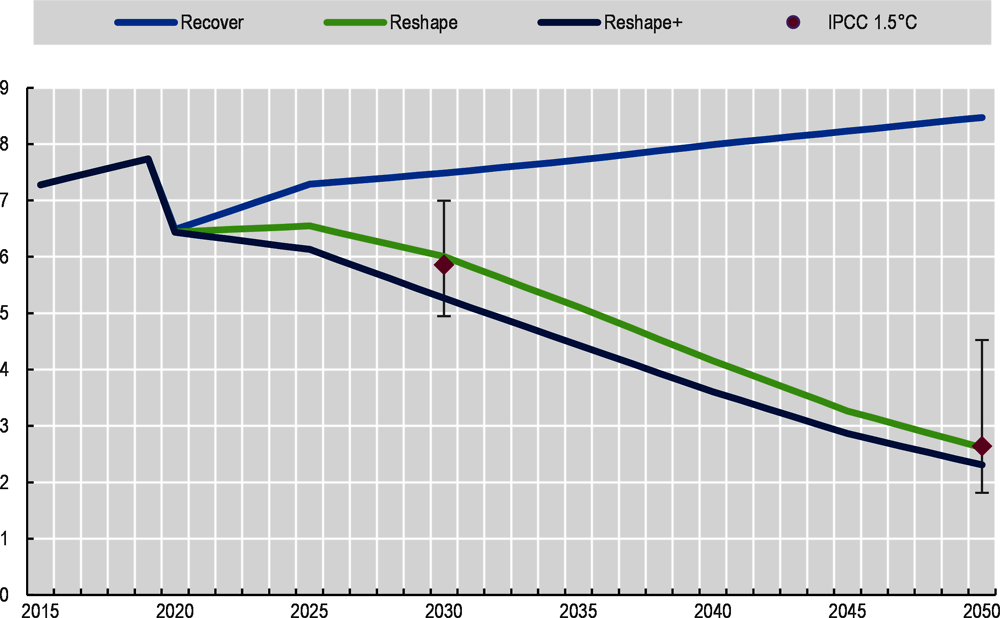

Limiting global temperature increases to “well below 2°C” and pursuing efforts to limit the increase to 1.5°C in line with the Paris Agreement (UN, 2015[12]), means restraining cumulative greenhouse gas (GHG) emissions to below a limited ‘carbon budget’. Since GHG emissions accumulate in the atmosphere, the earlier measures are put in place, the higher the chances of limiting climate change. As part of the latest IPCC special report on 1.5°C, some academic institutions modelled high ambition, decarbonisation scenarios across all sectors of the global economy. The results of these ‘whole system’ models suggest that annual emissions from the transport sector must drop to approximately 5.9 gigatonnes CO2 by 2030 and 2.6 gigatonnes CO2 by 2050 to limit temperature increases to 1.5°C and avoid overshooting carbon budgets (IPCC, 2018[13]). While there continues to be a large degree of uncertainty about the magnitude of remaining carbon budgets, these median estimates can serve to gauge the levels of ambition required to meet climate targets.

CO2 emissions under a Recover policy agenda will not meet climate targets. Annual transport CO2 emissions in the three ITF Transport Outlook 2021 scenarios are presented in Figure 2.8. In the Recover scenario, transport emissions continue to grow, driven by increasing travel demand, a limited shift to more energy-efficient modes, and limited adoption of low carbon vehicle technologies without further stimulus from policy makers. Annual emissions produced in the years 2030 and 2050 would be 7.5 GtCO2 and 8.5 GtCO2 respectively, meaning the Recover scenario would be insufficient to meet Paris climate goals.

A policy agenda based on Reshape+ gives the world greater certainty of meeting its climate targets. Both the Reshape and Reshape+ scenarios offer the possibility of meeting the targets of the Paris Agreement. The decisive policy action that underpins the Reshape scenario succeeds in shifting transport activity to more sustainable modes, improving energy efficiency, and rapidly upscaling the use of electric vehicles and low-carbon fuels. Reshape+ policies further limit emissions by harnessing the momentum created by post-pandemic economic stimulus packages for accelerating the impact of emission-reductions technologies and measures.

Note: Figure depicts ITF modelled estimates. Recover, Reshape and Reshape+ refer to the three scenarios modelled, which represent increasingly ambitious post-pandemic policies to decarbonise transport. ITF models used in this Outlook are typically run by five-year increments, therefore the 2020 to 2025 recovery trend may not necessarily be linear despite being shown as such in the figure. The shape of this “recovery curve” will depend on policy implementation and economic trajectories. IPCC 1.5˚C represents the emissions levels needed to limit warming to 1.5˚C as introduced by the IPCC (2018[13]) IPCC, 2018: Summary for Policymakers. In: Global Warming of 1.5°C, https://www.ipcc.ch/sr15/. The levels were calculated based on data sourced from https://data.ene.iiasa.ac.at/iamc-1.5c-explorer similarly to ICCT (2020[14]), https://theicct.org/sites/default/files/publications/ICCT_Vision2050_sept2020.pdf Transport sector emissions pathways with low or no overshoot were selected before estimating the median emissions in each year, error bars represent the 25th and 75th percentiles of scenarios. Emissions of black carbon are excluded as these are not estimated in the ITF or IEA MoMo models.

Urban passenger transport has the greatest potential to decarbonise. Annual GHG emissions for each transport sector in the Recover and Reshape+ scenario are presented in Figure 2.9. In the Recover scenario, emissions from freight and non-urban passenger travel continue to grow while urban emissions remain relatively constant. In contrast, emissions in the Reshape+ scenario reduce in all transport sectors over time. The fastest reductions could occur in the urban passenger sector if highly ambitious policies are implemented; annual emissions in 2050 could be approximately 79% lower than 2015 levels.

Many ways exist to decarbonise urban mobility and make rapid emissions reductions possible. The greening of city transport is driven by measures that shift travel away from private cars to other modes, stimulate the adoption of low-emission vehicles and tilt fuel demand towards low-carbon sources of energy such as electricity from renewable sources. Densification of cities through land-use policies and increased teleworking also reduce demand.

Improving energy efficiency is essential to reduce emissions from freight and longer-distance passenger travel

Longer-distance passenger travel and freight face great obstacles to reduce their emissions. Both offer fewer opportunities to shift demand on these modes to more sustainable alternatives, and low-carbon alternative fuels are still not available at scale. Electrifying aviation and maritime shipping remain limited by the relatively lower energy density of batteries compared to fossil fuels. Other alternative fuels such as hydrogen, ammonia and synthetic fuels are still at early levels of technological maturity (ITF, 2020[15]). Therefore improving energy efficiency is essential to reduce emissions from freight and longer-distance passenger travel. Under ambitious Reshape+ policies, efficiency improvements would help bring emissions from non-urban passenger transport down 57% by 2050 and freight emissions by 72% from 2015 levels. Without a strong steer from policy action, emissions in both sectors will continue to increase over the coming decades, rapidly consuming the remaining carbon budget.

Note: Figure depicts ITF modelled estimates. Recover and Reshape+ represent the most conservative and the most ambitious scenarios modelled. Graph depicts tank-to-wheel emissions for urban and non-urban passenger and freight transport in the Recover (left) and Reshape+ (right) scenarios. IPCC 1.5˚C represents the emissions levels needed to limit warming to 1.5˚C as introduced by the IPCC (2018[13]) IPCC, 2018: Summary for Policymakers. In: Global Warming of 1.5°C, https://www.ipcc.ch/sr15/. The levels were calculated based on data sourced from https://data.ene.iiasa.ac.at/iamc-1.5c-explorer similarly to ICCT (2020[14]) https://theicct.org/sites/default/files/publications/ICCT_Vision2050_sept2020.pdf. Transport sector emissions pathways with low or no overshoot were selected before estimating the median emissions in each year, error bars represent the 25th and 75th percentiles of scenarios. Emissions of black carbon are excluded as these are not estimated in the ITF or IEA MoMo models.

Policy measures play a key role in the adoption of low-carbon technologies in more ambitious scenarios. Vehicle technologies are adopted most rapidly in developed economies represented by OECD countries in the model and other fast-growing economies such as the People’s Republic of China. They proceed at a slower pace in developing economies. Countries that pursue net-zero emissions as their official policy or that have made other ambitious national mitigation pledges achieve decarbonisation objectives more rapidly than others. The uptake of electric vehicles, for example, is stimulated by firm commitments to phase out internal combustion engines. Conversely, vehicle fleets in countries without fuel economy standards or similar regulations are likely to pocket fewer efficiency gains.

The United States and Canada plus the EEA and Turkey produced more transport emissions than the rest of the world combined in 2015 despite accounting for just 13% of the world’s population. Future trends suggest that developing economies will account for a larger share of emissions in the coming decades. Under Recover policies, only regions with relatively high income – EEA and Turkey, OECD Pacific and the United States and Canada – are expected to see reductions in annual emissions between 2015 and 2050 due to the relatively constant demand for transport and slight improvements in vehicle technologies. Conversely, emissions in non-OECD countries are likely to increase rapidly under a Recover policy agenda due to growing levels of income and population. In higher ambition scenarios, emissions levels could drop significantly in all regions. Figure 2.10 presents annual CO2 emissions for the years 2015 and 2050 in each scenario by region.

Note: Figure depicts ITF modelled estimates. Recover, Reshape and Reshape+ refer to the three scenarios modelled, which represent increasingly ambitious post-pandemic policies to decarbonise transport. Excludes emissions from international sea and airfreight. International aviation demand is attributed to the origin country. EEA: European Economic Area. LAC: Latin America and the Caribbean. MENA: Middle East and North Africa. OECD Pacific: Australia, Japan, New Zealand, South Korea. SSA: Sub-Saharan Africa. Transition economies: Former Soviet Union and non-EU South-Eastern Europe.

The impact of an economic lag on CO2 emissions

To account for the economic impact of the Covid-19 pandemic, GDP and trade projections in this Transport Outlook are adjusted from pre-pandemic forecasts by including a five-year time lag for years after 2020. For example, GDP estimates in the year 2030 are assumed to be at pre-pandemic levels of the year 2025. There are various projections for what economic recovery will look like, ranging from the more optimistic bounce-back scenarios to dampened recovery expectations. The true demand and CO2 emissions observed in the years to come will depend on the actual economic recovery pathway.

To better understand the magnitude of the impact of the five-year lag in GDP growth and trade, the Reshape+ scenario was assessed assuming pre-Covid-19 economic projections. The impact of this five-year GDP time lag assumption on 2050 CO2 emissions under a Reshape+ scenario is shown in Figure 2.11. The pre-pandemic economic growth trends lead to 6% higher CO2 emissions from non-urban passenger transport and 7% higher CO2 emissions from freight. The lag in economic growth has a limited impact on urban passenger emissions: they are 2% lower than without the lag. The impact of GDP is more pronounced in the freight and non-urban passenger sectors, which are more sensitive to income, as demonstrated by the elasticities in Figure 2.2. Although urban passenger transport in non-OECD countries is more coupled with GDP when looking at the growth between 2015 and 2050 (as is done in Figure 2.2), its effect is not linear. By 2050 the difference in the elasticity of demand to GDP between non-OECD and OECD countries is much less. As countries become wealthier and latent demand is realised, the sensitivity to GDP decreases. Therefore, by 2050, under highly ambitious decarbonisation policies (as described by a Reshape+ scenario), urban passenger transport, globally, is less affected by GDP assumptions.

Note: Figure depicts ITF modelled estimates. The ITF Transport Outlook 2021 assumes a five-year lag in economic activity from 2020 onwards to simulate the economic impacts of the pandemic. To demonstrate the impact of economic assumptions on transport emissions, this figure shows the CO2 emissions under the most ambitious of the three scenarios modelled for this Transport Outlook in terms of decarbonisation measures, the Reshape+ scenario, juxtaposing results for the assumed five-year lag and also assuming the pre-Covid-19 economic trend.

The uncertainty of whether technologies under development will be able to contribute on a large scale to reverse the rise of CO2 emissions creates an imperative for impactful near-term mitigation. The simulations presented in this Transport Outlook demonstrate that the right policies can deliver progress in transport decarbonisation and also towards sustainable development in a broader sense. The modelling results demonstrate that decarbonisation policies can narrow regional differences in per capita CO2 emissions due to action in all regions. However, the responsibility to pay or fund these initiatives is not equally borne. Inequalities between and within countries for emission contributions, climate change consequences, and economic opportunities mean that the responsibility to act and fund change is also not evenly divided.

Given transport’s strong contribution to individual well-being, all decarbonisation efforts must not apply CO2 mitigation measures at the expense of access to opportunities. This is especially true for vulnerable groups whose access has not been a priority for most transport systems in the past.

Ambitious decarbonisation policies will narrow emissions imbalances between regions. Per-capita CO2 emissions for the United States and Canada region are at least four times, and up to 36 times, higher than for inhabitants of any other world region. Yet under a Reshape+ scenario, this multiplier could be lowered to between 2.3 and 9.4 times. With the most ambitious policy agenda, the United States and Canada could by 2050 emit approximately the same amount of CO2 per capita as the Latin America and the Caribbean (LAC) region in 2015. As the region with the highest GDP per inhabitant, the United States and Canada have the means to fund a low-carbon transition that could achieve the largest relative reduction in per capita emissions of all regions: a cut in transport CO2 by 86% to 2050. Figure 2.12 juxtaposes transport CO2 contributions in 2015 per capita, and the evolution of these emissions in regions under the different policy scenarios, alongside estimates for GDP per capita for 2015 and 2050.

Sub-Saharan Africa remains the region with the lowest per capita emissions from 2015 to 2050 despite its population growth. It also generates the lowest GDP per inhabitant. The region comprising the EEA and Turkey could reduce per capita emissions to 20% of its 2015 level by 2050 under Reshape+ policies, while LAC and OECD Pacific could reduce it to 25%. The LAC region could reduce their 2050 emissions to approximately 20% of those in 2015. The MENA region and the Transition countries reduce their per capita emissions less significantly but could still reach 40% of their 2015 level by 2050. Without additional policy interventions, Asia, LAC, MENA, SSA and the Transition countries are all expected to increase per capita emissions over the next 30 years.

Responsibility for the global costs of decarbonisation is linked to cumulative emissions. The regions that have long-standing fossil-fuel-based industries have emitted the most cumulative emissions and gained the greatest economic benefits during the age of oil and coal. The latter now gives them privileged access to capital and technologies and thus the means to invest in decarbonisation. They can support climate action in regions that contribute less to global CO2 emissions. Capital investment and technology transfer could enable these regions to leapfrog transport systems that historically led to excessive emissions in developed regions (Kosolapova, 2020[16]). The United Nations conclude there are sufficient global assets to finance sustainable development. However, the available capital is currently not channelled towards these goals at the scale and within the timeframe necessary to meet the Paris Agreement targets and SDGs (United Nations, 2019[17]). Mobilising capital to fund cleaner transport and support regions where it is most needed and most crucial for global climate action is an opportunity to bridge economic and social inequalities and set the world on a cleaner, more equitable path.

Note: Figure depicts ITF modelled estimates. Recover, Reshape and Reshape+ refer to the three scenarios modelled, which represent increasingly ambitious post-pandemic policies to decarbonise transport. Graph depicts tank-to-wheel emissions. Emissions from international maritime or airfreight emissions are not attributed to countries and are therefore excluded. Emissions from international passenger movements are attributed to origin countries. EEA: European Economic Area. LAC: Latin America and the Caribbean. MENA: Middle East and North Africa. OECD Pacific: Australia, Japan, New Zealand, South Korea. SSA: Sub-Saharan Africa. Transition economies: Former Soviet Union and non-EU South-Eastern Europe.

Greater decarbonisation ambition can mean more equitable and resilient urban transport – if implemented well. There is considerable room to align environmental sustainability and well-being goals in urban transport. A passenger transport system that allows users to access their needs affordably, reliably, conveniently and safely without owning a car is not only more sustainable but more equitable than what is commonplace today. While cars will have an important role, transport systems should not plan for them as the default option for all. It also addresses important negative externalities of congestion, air pollution and road safety while at the same time reducing the amount of space currently required to accommodate privately-owned vehicles.

Chapter 3 discusses in greater detail how higher ambition decarbonisation policies such as those underpinning the Reshape and Reshape+ scenarios can improve the accessibility and resilience of urban transport systems. It also details the equity considerations policy makers will need to address to ensure policies are implemented fairly. In urban contexts, measures to reallocate road space and pricing schemes, as well as investments in affordable and safe public transport, shared mobility, active and micromobility may facilitate a shift away from private car use and support development patterns that can reduce urban sprawl. Such initiatives better serve the needs of lower-income populations, women, older and younger people who all tend to be more reliant on modes other than the private car. The travel patterns of women in particular will benefit considerably from better accommodating active travel (Miralles-Guasch, Melo and Marquet, 2015[18]).

Improved vehicle and fuel technology decarbonises transport and drives economic growth through innovation. Measures to incentivise the development of cleaner technologies in shared and public transport fleets are particularly important to support a transition away from private car dependency (Buckle et al., 2021[19]). These fleets are more intensely used than private vehicles, and therefore cleaner technologies have a bigger impact. They also have higher rates of turnover, which makes them ideal candidates to adopt new technologies, which can be accelerated with the right policy incentives. Incorporating digital technology into vehicle operations, e.g. for optimal routing or real-time user feedback can boost energy efficiency, reduce congestion, increase safety and all the while foster economic growth.

Citizens with lower incomes should not pay high prices for decarbonising. Carbon and road pricing mechanisms to reduce the use of more polluting modes, such as private vehicles, can be implemented in a manner that does not unfairly burden lower-income populations. Pricing plays a significant role in managing non-urban passenger transport demand, and Chapters 3 and 4 offer a detailed discussion of this aspect. In some areas of the world, households are forced to own cars or motorcycles due to the lack of alternative transport options. Those who cannot afford newer vehicles may face higher costs than those who can buy cleaner vehicles that are exempt from charges or for which reduced rates apply. Pricing mechanisms also have a strong effect in aviation. Since a tiny and affluent share of the world population is responsible for most air travel, pricing flights to better reflect their carbon footprint shifts costs to those responsible (Gössling and Humpe, 2020[20]).

Policies that would impose new financial burdens on citizens warrant an analysis of distributional impacts first. Who is affected by additional costs and by how much will differ. Factors that play a role are the spatial distribution of origins and destinations, the transport options available, the cost and reliability of these alternatives, and constraints on households. Complementary measures to reduce the overall financial burden on these groups can be a help. For example, Sweden simultaneously lowered the income tax rate as it increased the levy on energy products (Speck, 1999[21]). Concerning world regions, pricing policies could have a more pronounced impact on developing economies than developed ones. The difference in per capita travel demand is greater between regions in the Reshape+ scenarios than the Recover scenario. However, even with the implementation of pricing policies, the difference in non-urban activity between regions narrows (improves) between 2015 and 2050. Ultimately, economic measures will not successfully reduce CO2 emissions while simultaneously maintaining or improving accessibility levels unless more sustainable, reliable, and affordable alternatives are provided. The focus should be on providing viable alternatives and designing land use in a way that supports these alternatives.

Delaying decarbonisation will increase freight costs. Under Reshape and Reshape+ policies, supply chains shorten and carbon pricing increases freight transport costs where higher-emitting modes are used. Regions located at a distance from the main global consumption centres or that have not decarbonised their freight sector enough see the average transport costs of their exports rise under Reshape+. This is the case notably for the MENA and SSA regions. Global freight transport will risk being perceived as unfair if the decarbonisation in these regions is not accelerated or their negative cost impacts for the concerned countries mitigated. Technology transfer and investment in regions with lesser means must be prioritised to avoid imposing prohibitive costs and ensure that the regions with the most capacity to decarbonise are not the sole winners who gain all the cost benefits of such measures.

Transport export costs drop most in the EEA and Turkey by 2050 in the Reshape scenario. Some of the most ambitious policies are deployed in the European region, reducing emissions but also bringing greater efficiency and lower costs. A stronger modal shift towards rail than in other regions also contributes to this.

Transport demand will grow under all three scenarios, but far less under ambitious decarbonisation policies. The greater the decarbonisation ambition, the more transport demand decouples from GDP growth.

Implementing more ambitious decarbonisation policies in the wake of the pandemic would bring the Paris climate goals into reach. Continuing with pre-pandemic policies will miss them.

Developed countries have the highest CO2 emissions but also the best access to capital to fund the decarbonisation of their transport systems. To avoid imbalances, they should ensure developing countries with lower per capita emissions can also transition to clean transport.

Decarbonisation policies must be implemented with care. They must consider potential distributional impacts and ensure measures are consistent with equity and well-being objectives.

References

[19] Buckle, S. et al. (2021), Draft discussion paper: Addressing the COVID and climate crises: potential economic recovery pathways and their implications for climate change mitigation, NDCs and broader socio-economic goals, OECD Publishing.

[11] Chen, Z. (2016), “Research on the Impact of 3D Printing on the International Supply Chain”, Advances in Materials Science and Engineering, Vol. 2016, https://doi.org/10.1155/2016/4173873.

[9] Dingel, J. and B. Neiman (2020), How Many Jobs Can be Done at Home?, Becker Friedman Institute, Chicago, https://github.com/jdingel/DingelNeiman-workathome. (accessed on 9 October 2020).

[20] Gössling, S. and A. Humpe (2020), “The global scale, distribution and growth of aviation: Implications for climate change”, Global Environmental Change, Vol. 65/May, https://doi.org/10.1016/j.gloenvcha.2020.102194.

[5] IATA (2020), Outlook for air travel in the next 5 years, IATA.

[14] ICCT (2020), Vision 2050.

[6] IEA (2020), IEA Mobility Model, https://www.iea.org/areas-of-work/programmes-and-partnerships/the-iea-mobility-model.

[7] IEA (2019), The Future of Rail, https://www.iea.org/reports/the-future-of-rail.

[2] IMF (2020), World Economic Outlook Update, June 2020: A Crisis Like No Other, An Uncertain Recovery, IMF, https://www.imf.org/en/Publications/WEO/Issues/2020/06/24/WEOUpdateJune2020 (accessed on 22 October 2020).

[13] IPCC (2018), IPCC, 2018: Summary for Policymakers. In: Global Warming of 1.5°C. An IPCC Special Report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty, https://www.ipcc.ch/sr15/ (accessed on 10 July 2020).

[1] IPCC (2018), Mitigation Pathways Compatible with 1.5°C in the Context of Sustainable Development. In: Global Warming of 1.5°C. An IPCC Special Report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathw.

[15] ITF (2020), Navigating towards cleaner maritime shipping: Lessons from the Nordic region.

[16] Kosolapova, E. (2020), Harnessing the Power of Finance and Technology to Deliver Sustainable Development, Eearth Negotiations Bulletin.

[18] Miralles-Guasch, C., M. Melo and O. Marquet (2015), “A gender analysis of everyday mobility in urban and rural territories: from challenges to sustainability”, Gender, Place & Culture, Vol. 23/3, pp. 398-417, https://doi.org/10.1080/0966369x.2015.1013448.

[4] OECD (2020), Environment-economy modelling tools - OECD, http://www.oecd.org/environment/indicators-modelling-outlooks/modelling.htm (accessed on 9 December 2020).

[21] Speck, S. (1999), “Energy and carbon taxes and their distributional implications”, Energy Policy, Vol. 27/11, pp. 659-667, https://doi.org/10.1016/s0301-4215(99)00059-2.

[8] Tapio, P. (2005), “Towards a theory of decoupling: Degrees of decoupling in the EU and the case of road traffic in Finland between 1970 and 2001”, Transport Policy, Vol. 12/2, pp. 137-151, https://doi.org/10.1016/j.tranpol.2005.01.001.

[12] UN (2015), The Paris Agreement, https://unfccc.int/sites/default/files/english_paris_agreement.pdf (accessed on 25 January 2019).

[17] United Nations (2019), Roadmap for Financing the 2030 Agenda for Sustainable Development 2019-2021, United Nationals.

[10] Wieczorek, A. (2017), “Impact of 3D printing on logistics”, Research in Logistics and Production, Vol. 7/5, pp. 443-450, https://doi.org/10.21008/j.2083-4950.2017.7.5.5.

[3] WTO (2020), Trade Statistics and Outlook : Trade set to plunge as COVID-19 pandemic upends global economy, WTO.