Assessment and recommendations

Reforms are working, but disparities persist across Mexico

Mexico is now the world’s 11th largest economy (in terms of GDP measured at purchasing power parity). The country has gone through tremendous structural changes over the past three decades. From an oil-dependent economy up to the early 1990s to a booming manufacturing centre in the aftermath of NAFTA in the mid-1990s, Mexico is now increasingly becoming an international trade hub. The proximity to the US export market continues to be a competitive advantage, but Mexico has strategically boosted free trade, signing 12 agreements with 46 countries. Mexico is now a top global exporter of cars and flat screen TVs, among other products. Yet, Mexico’s economic potential has been hindered by important challenges such as high levels of poverty, extensive informality, low female participation rates, insufficient educational achievement, financial exclusion, weak rule of law, and persistent levels of corruption and crime. To address these problems, the current government has rolled out major structural reforms since 2012 aimed at improving growth, well-being and income distribution (Table 1). The initial wave of reforms, kicked-off by the multi-partisan political commitments in the Pacto por México, has led to notable progress across a range of areas and has put Mexico at the forefront of reformers among OECD countries (OECD, 2015a). Key laws and constitutional amendments were approved, and secondary laws or regulations passed.

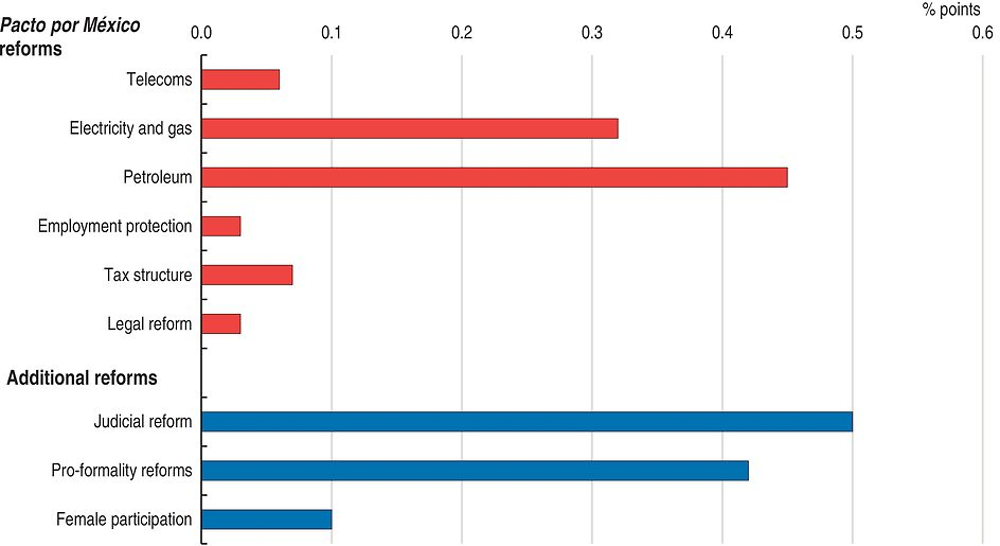

Strong progress has been made to open sectors such as energy and telecoms to more competition. Institutional designs have been improved with a new National Productivity Commission, a strengthened competition authority, and expanded sectoral regulators. Initial progress has been made with education and social benefits, although parts of these plans have run into difficulties. The OECD estimated in the last Economic Survey that a subset of the Pacto por México reforms could add one percentage point to GDP growth after five years (OECD, 2015a). These estimates made a series of assumptions for reforms where sufficient information and quantitative impact assessment models were available. An additional set of selected reforms could add another percentage point to GDP (Figure 1).

1. The reform impacts are estimated using a combination of Mexico-specific and cross-country economic models (see Annex 2 in Dougherty, 2015). Effects are envisioned to occur through accelerated total factor productivity convergence to the global technological frontier, as well as through capital deepening. These baseline estimates include only a selection of the sectors affected by the reforms.

Source: OECD Economic Survey of Mexico, 2015.

Reforms have already demonstrated short-term benefits, especially on productivity growth, which has picked up recently. However, the declining trend of labour utilisation in recent years calls for more to be done to make it more worthwhile to participate in the labour market, while ensuring satisfactory work-life balance, and equip workers with the skills necessary to be productive and receive adequate wage gains. Such reforms fit well with the long-term sustainable development goals (SDGs) to be achieved in 2030, notably to eradicate extreme poverty, reduce income inequality, improve economic opportunities, lower informality, raise female participation, and encourage more responsible business practices.

In addition, inequalities continue to grow across states and sectors, emphasising the divergence of a modern Mexico – highly productive, competing globally, mostly located at the border with the United States, in the central corridor and in tourism areas; and a traditional Mexico, less productive, with small-scale informal firms, mostly located in the South.

Against this background, this report focuses on:

-

How to ensure that resilient growth continues, reducing oil dependence, preparing for vulnerabilities and exogenous shocks, and supporting more social spending.

-

How to reduce inequalities with policies to better fight poverty, promote women’s opportunities, and foster responsible business practices.

-

How to ensure inclusive productivity growth by reforming key sectors of the economy, climbing global value chains, lowering regulatory barriers, tackling informality, and reducing corruption.

Despite external headwinds, growth is resilient

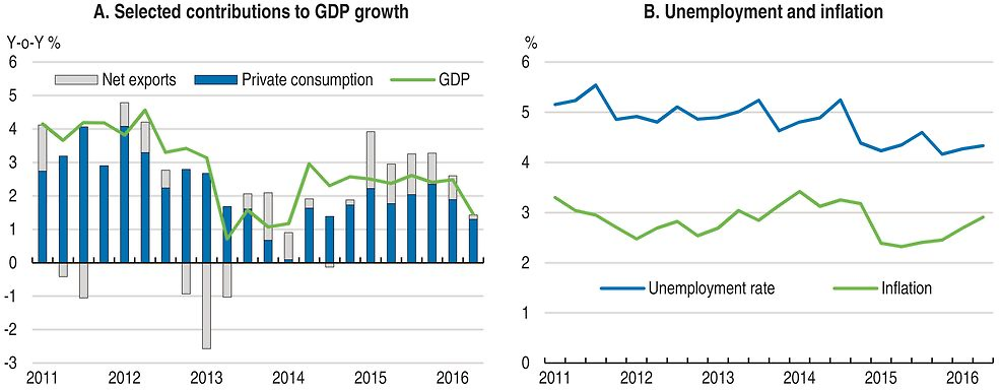

Despite being hit by several external shocks, the Mexican economy is resilient and recent indicators suggest further growth ahead (Figure 2 and Box 1). The external environment is difficult, with the global economy remaining in a low-growth environment, and weak global trade, investment, productivity and wages, in addition to uncertainty about the future evolution of economic and trade policies in the United States. Headwinds specific to Mexico include collapsing oil prices, which reduced government receipts and led to cutbacks in energy sector investments, as well as the sharply depreciating Mexican peso following market expectations of US Federal Reserve tightening and rising global policy uncertainty (Box 2). Despite these shocks, performance is good, supported by domestic demand. The structural reforms are supporting a low inflation environment and strong expansion of credit, leading to gains in real wages and employment. The large depreciation of the peso further increases the competitiveness of Mexican non-oil exports, and has not pushed up inflation. It also has a positive impact on the fiscal balances, reflecting the dollar denominated oil receipts and the low exposure to foreign currency debt. Furthermore, sufficient resources have been accumulated in the oil stabilisation fund, allowing Mexico to stay on course with its fiscal consolidation trajectory without additional measures.

Source: OECD Economic Outlook 100, Banco of Mexico, and INEGI.

Economic activity has been resilient to sharply lower oil prices, weak world trade growth and monetary policy tightening in the United States. Domestic demand remains the main driver of economic activity, supported by recent structural reforms that have cut prices to consumers, notably on electricity and telecoms services. Growth may be held back in 2017 and 2018, mostly through investment and consumer confidence, following uncertainties about future US policy, although the economy could benefit from the expected fiscal stimulus in the United States which would bring stronger import demand (Table 2).

Private investment in the oil sector will generate activity partially offsetting cutbacks in public oil-related investment, and industrial production will remain tied to activity in the United States. The substantial depreciation of the peso during 2016 will continue to support foreign trade, with limited pass-through to domestic prices, allowing inflation to converge towards Mexico’s central bank target band (3% ±1%).

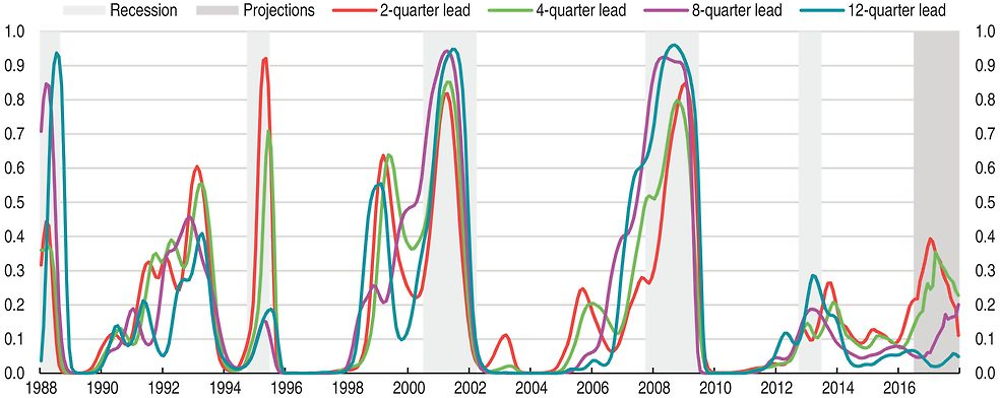

The Mexican national statistics office (INEGI) calculates coincident and leading business cycles indicators, using a methodology in line with the OECD’s (see Sistema de indicadores cíclicos, www.inegi.org.mx). They incorporate the following underlying components: a global activity indicator, the real bilateral exchange rate (Mexican peso to the US dollar), employment trends in manufacturing, an index of prices and quotations of the Mexican Stock Exchange, the Interbank Equilibrium Interest rate, the Standard & Poor’s 500 (US stock market index), imports, remittances, and the number of workers affiliated with IMSS (Social Security). Those indicators are available at the monthly frequency starting in 1988.

Since the end of 2015, INEGI reports point to a negative opening of the leading indicator’s gap relative to its long-term value (i.e. the indicator is turning negative), indicating the possibility of a deceleration of the economy. In order to provide a more systematic stance on the probability of a recession, this analysis builds on recent OECD studies (Hermansen and Röhn 2015; Röhn et al., 2015) that associate the probability of recession to indicators of potential imbalances (calculated as the deviation from historical trend, using HP-filtering methods). In order to fit more closely the case of Mexico, we use the same components as INEGI’s co-incident and leading indicators. Importantly, some indicators are common to both models, but they are also more frequent (monthly instead of quarterly) and timely (the latest data point available is October 2016). Additionally, principal component analysis is used to downplay the noise from each indicator separately and focus on their collective signalling content (OECD, 2016b). Figure 3 shows estimates of the recession probability at horizons of 2, 4, 8, and 12 quarters, using models estimated with monthly data for three components that have been identified over the entire time span from January 1988 to September 2016. These models show elevated recession probabilities around the time of most downturns but are still subject to errors, notably the 1990s. Estimates from the latest months (up to October 2016) suggest that vulnerabilities have risen in the short term, due in part to the significant depreciation of the peso. Looking forward, we project monthly indicators until December 2017 using the OECD Economic Outlook forecasts. Recessions risks remain below levels typically indicating an imminent recession, even given the large depreciation of the peso, in particular the 12-quarter lead indicator that is showing the most accurate predictions over time.

Source: OECD calculations using INEGI business cycle indicators.

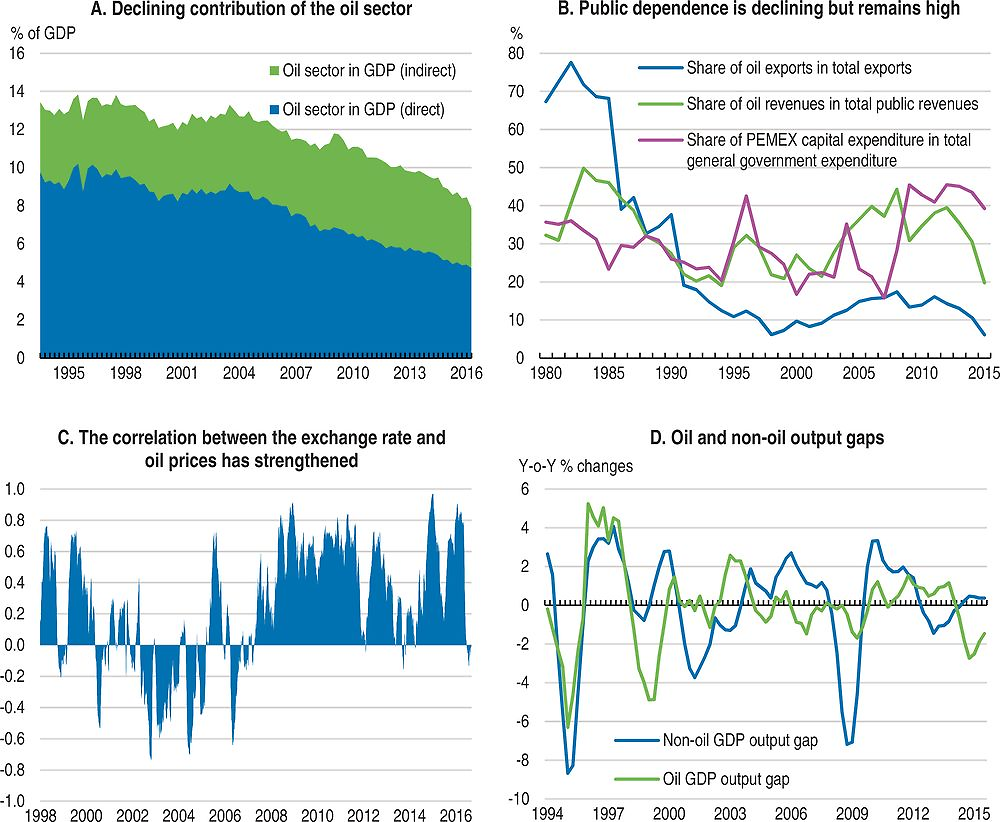

Mexico has a long legacy of oil dependence. Until the mid-2000s, oil-related activities (including petrochemicals and oil-derivative products) accounted for about 13% of GDP (Figure 4, Panel A). Over the last decade however, declining oil extraction from the national oil company (PEMEX: Pétroleos Méxicanos) has had an important effect on the oil-GDP contribution, which has fallen to about 8% in 2016. Oil-related revenues and exports were also a major source of government revenues and foreign exchange receipts but they also declined significantly in recent years due the collapse of oil prices and increase in tax revenues following the tax reform (Figure 4, Panel B). Yet, PEMEX capital spending remains high, at about 1/3 of public capital spending (Figure 4, Panel B), and the MXN/USD exchange rate has been highly correlated with oil prices (Figure 4, Panel C).

Oil dependence caused several difficulties when global energy prices collapsed (Figure 4, Panel D). Reforms implemented in 2014 to improve PEMEX’s governance, to gradually open the oil sector to private and foreign participation, and to decrease the budget reliance on oil revenues have therefore been timely. Additionally, the Government has an oil hedge strategy to insure against oil price volatility (see Table 5). Nonetheless, the government needed to support PEMEX in 2016 (up to MXN 73.5 billion in capital and a bond exchange to absorb some pension liabilities) and exposed the urgent need to downsize and corporatise the company. As a complementary measure, the tax regime of PEMEX was modified to increase the cap for capital cost deductions. More broadly, the Mexican economy will benefit from opening the energy sector more widely.

Note: Panel A: The direct oil sector share represents the Oil and Gas Extraction sector in the National Accounts. The indirect represents services related to the extraction of oil, National Accounts #211 213 237 324 3251 and 3 259. Panel C: The chart shows the average of 1 to 12 months correlation coefficients between the MXN/USD and Mezcla Mexicana (i.e. the average price of crude oil produced in Mexico). Panel D: The same definition as in Panel A is used to define non-oil GDP and a HP filter is applied to disentangle the trend from the cycle components.

Source: OECD calculations using data from INEGI, SHCP and Banxico.

Vulnerabilities persist

Mexico faces a weak and uncertain external environment, as the global economy remains in a low-growth mode and many emerging market economies lack momentum. Low commodity prices and accommodative monetary policies offer some support, albeit punctuated by periods of financial instability, which heighten aversion to risk and discourage productive investment and employment gains. This challenging environment affects Mexico through various channels:

-

Weak exports to trading partners, notably the United States and South American countries;

-

Uncertainties related to US monetary policy normalisation or possible adverse developments in EMEs could increase global financial volatility with significant spillover effects;

-

Further downward pressures on oil prices and difficulties in implementing PEMEX’s reform could delay reaching the budget deficit target and erode market confidence;

-

Second-round effects could raise the pass-through of past depreciations, in particular if they feed into wage growth, and increase inflation above the target.

More extreme vulnerabilities could also materialise (Box 3).

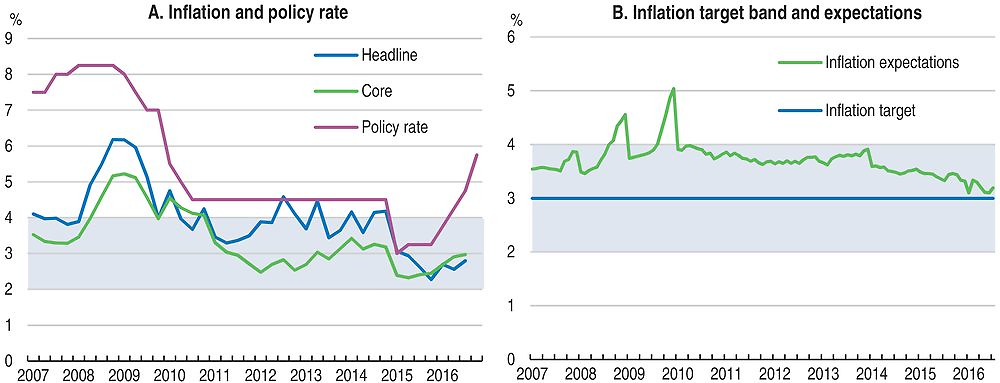

Monetary policy has been successful at containing inflation

Banco de Mexico (Banxico) has contained inflation within its target band despite significant depreciation of the peso (Figure 5, Panel A). The policy interest rate was raised 275 basis points since December 2015 to 5.75% in December 2016, to stem inflationary pressures resulting from the significant depreciation of the peso, and considering the relative monetary stance vis-à-vis the US Federal Reserve, and the output gap (Banxico 2016a, 2016b). Foreign exchange interventions requested by the Exchange Commission to provide liquidity to the peso market and preserve its orderly functioning stopped in February 2016. Mexico renewed and increased its access under the IMF Flexible Credit Line (FCL) in May 2016. Those policy actions allowed the central bank to keep inflation expectations anchored (Figure 5, Panel B).

Note: The blue shaded area represents Banxico’s inflation target band of 3% ±1%.

Source: Banco de México.

The economic environment has been complex. The country has been facing significant external headwinds with the collapse of oil prices in 2014/15, the significant depreciation of the peso, the tightening stance of the US Federal Reserve, increased volatility in financial markets, and the slowdown of the US economy. Banxico has therefore enhanced its communication, focusing on the possible pass-through from the depreciation of the peso. To continue building its credibility, the bank should carry on acting timely and flexibly in order to ensure the efficient convergence of inflation to its target.

Financial stability risks appear to be generally well contained (Table 3). Hedging strategies have contained much of the risk, and regulatory reforms to comply with Basel III, as well as supervision helped to protect the banking sector. Expanded lending by development banks, following the financial reform, has reduced the cost of credit for small and medium enterprises, but could pose a risk of non-performing loans in the event of an adverse downturn scenario.

Given recent episodes of heightened volatility, Mexico could consider expanding its macro-prudential tools to support financial stability. While Mexico has developed a wide range of macro-prudential tools following the Tequila crisis in the mid-1990s, recent studies indicate that Mexico has scope to increase its existing macro and micro-prudential toolbox (Cerutti et al., 2015). Mexico has some appropriate regulations in place regarding foreign exchange (FX) exposure, such as limits to FX net open position of banks. However, given the recent significant depreciation of the peso, and despite the common use of derivative hedges, currency mismatches and balance sheet risk should continue to be monitored closely.

Fiscal performance is improving but the credibility of the fiscal rule could be enhanced

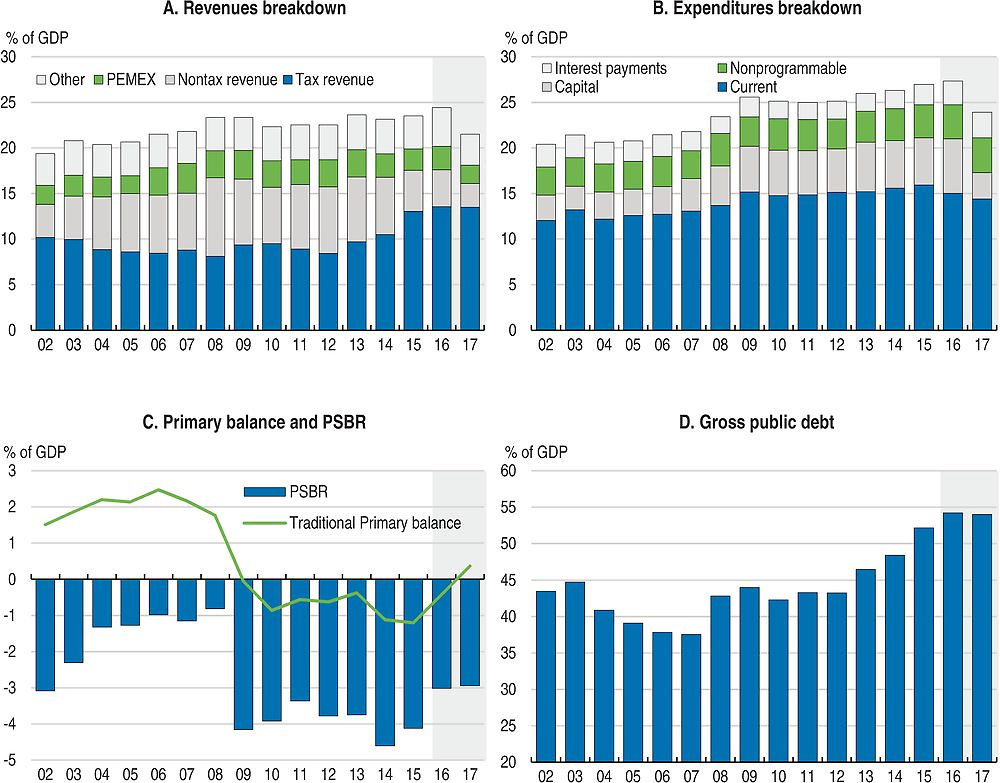

The timely tax reform introduced by the government in 2014 has raised non-oil tax revenue collection in 2015 and 2016 by about 3 percentage points of GDP (Figure 6, Panel A) and compensated for the fall in oil-related revenues over the period. Overall public spending grew in 2016 (Figure 6, Panel B) due to the government financial support to PEMEX, growing debt service payments, and pension costs. With total revenue rising faster than expenditure, the public sector borrowing requirement (PSBR) has declined by 1.1 percentage points of GDP to 3% of GDP in 2016, and is expected to reach 2.9% in 2017 and 2.5% by 2018 (Figure 6, Panel C).

The 2017 budget set the path to the return to primary surplus. Additional spending cuts of about 1.0% of GDP compared to 2016 were approved (Figure 6, Panel C). Those cuts will fall mostly on current expenditures in communications, transportation, and tourism; education; as well as agriculture.

How to read this chart: Figures for 2017 are from the approved budget. Budgeted revenues and expenditures are typically lower than actual revenues and expenditures, hence the significant drop between 2016 expected actual figures and 2017 budget proposals. Panel C: the traditional balance is a measure used by the government that does not fully take into account the position of the overall public sector.

Source: SHCP and OECD Calculations using data from SHCP.

Important changes to the Fiscal Responsibility Law (FRL) were made in 2014 and 2015 (Table 5). The fiscal responsibility law initially introduced a zero-balance target on the traditional measure of the deficit back in 2006. However, the traditional balance was too narrow as it did not include state-owned enterprises capital spending and led to a pro-cyclicality bias. In 2014, amendments to the fiscal responsibility law added a broader definition of the deficit, the public sector borrowing requirement (PSBR), as a target and introduced a cap on the real growth of current spending to limit pro-cyclicality. Starting in 2015, a new sovereign wealth fund, the Mexican Oil Fund was created to manage all hydrocarbon-related wealth to better insulate public spending from transitory fluctuations in oil revenues. The previous budgetary revenue stabilization fund (FEIP) and the states’ revenue stabilization fund (FEIEF) continue to operate and be the first line of defence in case of temporary and unexpected drop in revenues. Yet, those stabilisation funds had few assets over the last decade, except in 2008 and 2009 when oil prices were high, and have been drawn down invoking the exceptional circumstances clause, leaving Mexico with limited capacity to face future shocks. In 2015, the FRL was amended regarding the use of Banco de Mexico’s operating surplus to ensure that the full amount of a surplus is used to reduce the budget deficit or net government debt.

The 2014 tax reform will help to rebuild savings once oil revenues are sufficient again, but the authorities should be more parsimonious about the triggering of the FRL’s exceptional circumstances clause, limiting it to cases of large output or oil price shocks, so as to strengthen the credibility of the fiscal rule. In the long term, fiscal credibility will pay off in terms of market access and financial cost. When the clause is invoked, the fiscal framework requires the establishment of a path to return to the medium-term deficit target. As in other commodity producers and to increase transparency (OECD, 2015; IMF, 2015), budgetary documents should show more explicitly the non-oil balances.

Fiscal transparency has improved with the 2014 energy and tax reforms, and with the recent initiative of the Ministry of Finance (SHCP) to provide a wide array of fiscal indicators and to use 5-year horizon budgeting with risk analyses. To support further transparency, PEMEX’s accounts should be fully separated from the budget and the taxation of state enterprises should be normalised by shifting their taxation fully to the standard tax regime applied to their private peers (Daubanes and Andrade de Sá, 2014). As it stands, it is difficult to separate PEMEX and other SOEs’ operations from the budget as defined by international standards. The government should ultimately corporatise PEMEX. Doing so would also require changing the way the government supports PEMEX, as this is now done through the budget. Instead, the government should consider explicitly guaranteeing PEMEX’s debt temporarily and, to maintain a level playing field, charge a fee to PEMEX at a level sufficient to remunerate the risk. Additionally, the Mexican System of National Accounts should be modified to display consolidated fiscal accounts of all levels of governments (OECD, 2013).

Fiscal policy needs to be more supportive of inclusive growth

Mexico has implemented major initiatives to tackle poverty. Progresa, introduced in 1997; Oportunidades, introduced in 2002; and Prospera, the cash transfer programme launched in 2014 aiming to cover multi-dimensional needs such as health, education, and nutrition, but also extending to financial services and access to jobs. These initiatives have proved successful to increase school attendance, fight malnutrition and extend health coverage to poor families. Additional measures include the extension of the coverage of the national seniors’ pension programme to ensure that all Mexicans over 65 years old (70 years before) be eligible for a minimum pension from the federal government (OECD, 2013a). Direct outreach by social workers is underway and the Social Development Ministry is currently building a computing platform containing information of current and potential beneficiaries of social programmes. The Integrated Social Information System (SISI) will consolidate information to harmonise social programmes and build a national social protection system.

Mexico affirmed its commitment to global responsibility and took up the challenge of achieving the Sustainable Development Goals (SDGs). It has acted in several areas. First, a Specialized Technical Committee involving 25 federal agencies was established to develop open and transparent statistical information to monitor and enforce accountability. Second, a platform to offer citizens updated and georeferenced data on the degree of compliance for each of the SDGs has been developed. Third, forums and alliances with companies have been instituted to encourage society to embrace SDGs (HLPF, 2016). Going forward, the federal government intends to establish a high-level commission for the implementation of the SDGs with the participation of the federal and local government, civil society, academics and the private sector. The federal government would transversally incorporate compliance with the SDGs into the budget planning, boost diffusion and adoption of SDGs by local authorities, and form an Alliance for Sustainability with the private sector (HLPF, 2016). A clear knowledge of the starting position of Mexico in relation to the SDGs would help the government to determine national priorities for implementing the SDG agenda and decide how targets should be incorporated into national planning, policies, and strategies, as well as how to track process in their implementation plans.

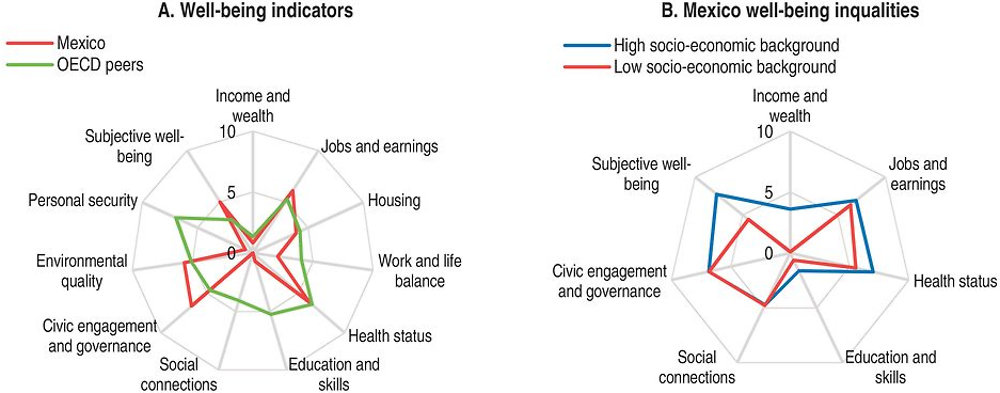

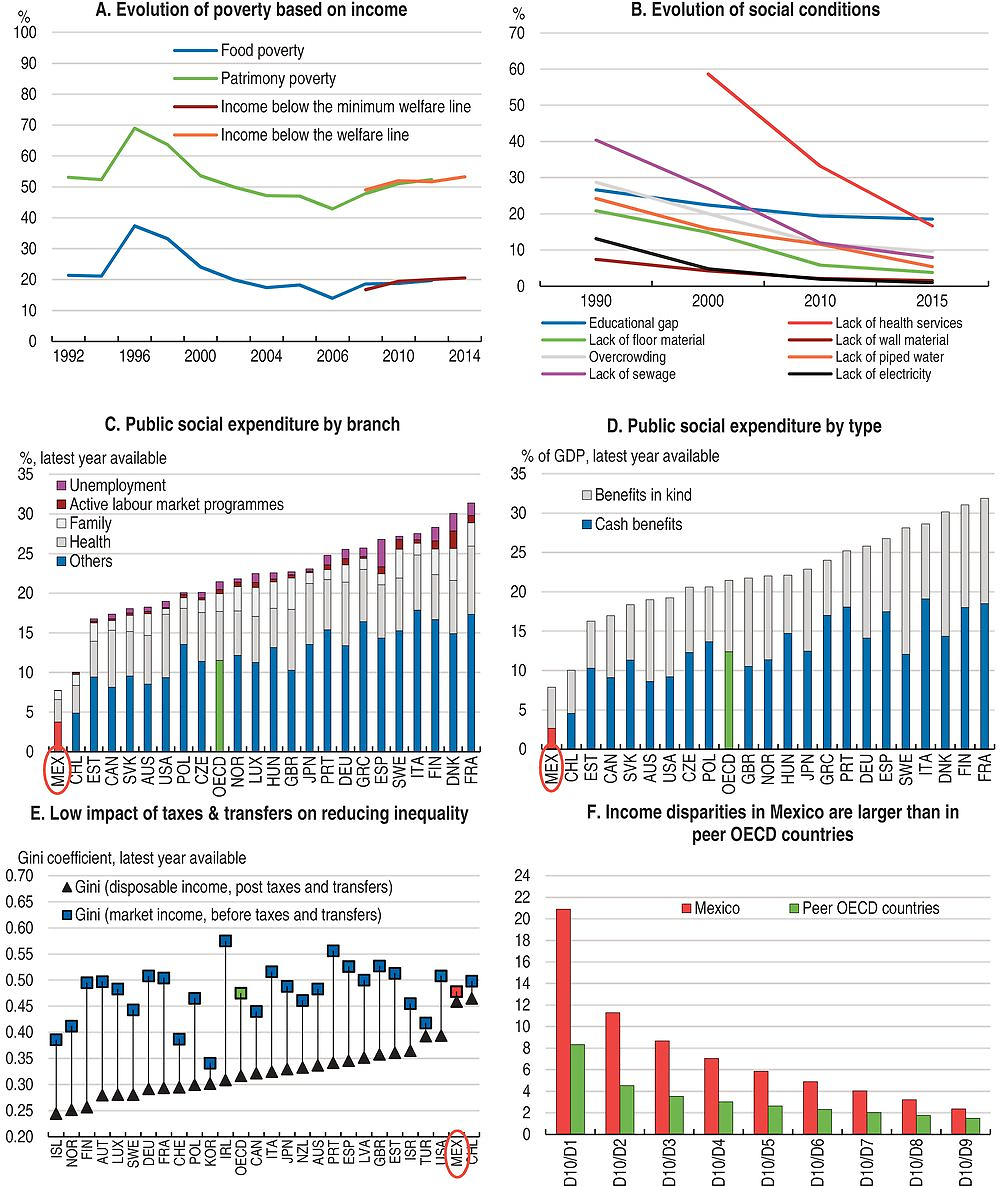

Nevertheless, the average Mexican household suffers in terms of income, wealth, social connections, education and skills, safety and work-life balance (Figure 7). Mexico is one of the few countries that have instrumented a multidimensional approach to measure poverty based on income (adjusting poverty lines as prices evolved) and access to social rights. Poverty as measured by income has increased in recent years mainly due to food inflation (Figure 8, Panel A) but significant progress has been achieved in social conditions such as access to education, housing, and healthcare (Figure 8, Panel B). Overall, the multidimensional poverty rate has remained somewhat stable (46.1% in 2010 relative to 46.2 in 2014). Challenges remain in terms of measuring income through household surveys, as the gap between this measure and that of the national accounts is the largest among OECD countries (OECD, 2013d).

How to read this chart: Outcomes are shown as normalised scores on a scale from 0 (worst condition) to 10 (best condition) computed over OECD countries. Panel A: Shows well-being outcomes in various dimensions for Mexican people compared to OECD peers: Chile, Czech Republic, Estonia, Greece, Hungary, Poland, Portugal, Slovak Republic, Slovenia and Turkey. Panel B: Shows well-being outcomes in various dimensions for people in Mexico with different socio-economic background. For further details on the indicators included, please refer to www.oecd.org/statistics/OECD-Better-Life-Index-2016-definitions.pdf

Source: OECD Better Life Initiative 2016.

Income inequality remains high relative to other OECD countries. The gap between rich and poor in Mexico is the highest among the OECD countries (after taxes and transfers). The richest 10% of the population in Mexico earn 20 times more than the poorest 10%, whereas it is about 8 times on average in peer OECD countries (Figure 8, Panel F). Inequality as measured by the Gini coefficient is high and has not declined, which suggests that transfer policies could have been more effective (Figure 8, Panel E). While social spending is not low by international comparison as a share of total public expenditure, showing the priority given to the reduction of poverty in the budget, it remains at the low end among OECD countries as a share of GDP (Figure 8, Panel D), despite having increased from less than 2% of GDP in 1985 to almost 8% in 2012. Cash transfers account only for less than 3% in GDP with the lowest spending on active labour market programmes and unemployment insurance, among others (Figure 8, Panel C).

Note: Panel A: Food poverty: insufficient income to purchase the basic food basket, even if all the household disposable income is used exclusively for the acquisition of these goods. Patrimony poverty: insufficient disposable income to acquire the food basket and make the necessary expenditures on health, education, clothing, housing and transportation, even if all the household disposable income is used exclusively for the acquisition of these goods and services. Population with income below the minimum welfare line: people who cannot acquire the value of the food basket with their current income. Population with income below the well-being line: people who cannot acquire the value of the sum of a food basket plus a basket of goods and services with their current income. Panel C: Peer countries: Chile, Czech Republic, Estonia, Greece, Hungary, Poland, Portugal, Slovak Republic, Slovenia and Turkey.

Source: OECD Income Distribution Database, OECD Social Expenditure Database, CONEVAL, INEGI.

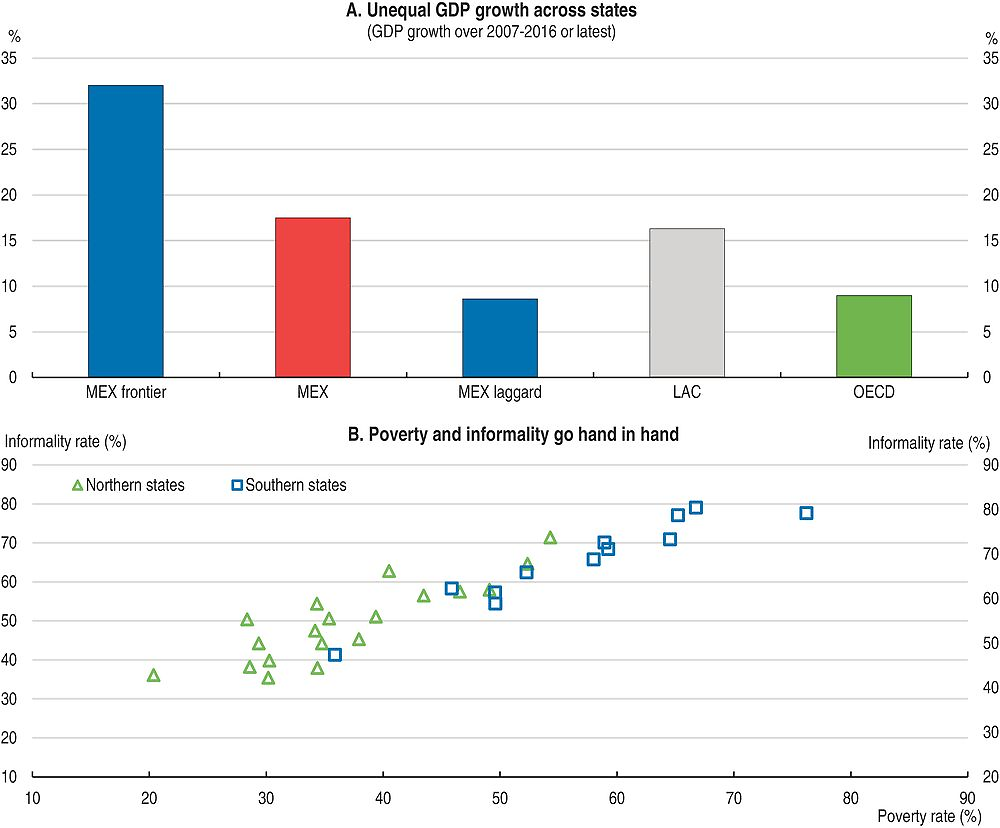

Inequalities are also growing across states and sectors (Figure 9, Panel A). Those divergences in income and informality have negative externalities on poverty and therefore inclusiveness (Figure 9, Panel B and C).

Note: Panel A: The fastest-growing states are: Ciudad Mexico, Queretaro, Nuevo Leon, Tabasco, and Aguascalientes. The slowest-growing states are: Baja California, Baja California Sur, Chiapas, Nayarit, and Tlaxcala. States mostly dependent on the oil sector (Campeche and Tamaulipas) are excluded since they suffered from both a deep recession since the collapse of oil prices and from the trend decline of oil production. GDP growth in Mexican states is for the period 2007-14.

Source: INEGI and CONEVAL.

Mexico’s health system has progressed and some health performance indicators have improved. Some of recent measures include a national agreement towards health service universalization with the goal to gradually ensure portability across providers and the strengthening of institutional collaboration to ensure competitive and transparent bidding and procurement procedures. IMSS has continued to expand its PREVENIMSS programme which includes preventive health actions, monitoring of nutritional status and screenings. Nevertheless, for many Mexican families, the health system fails to translate into better health. Health indicators remain worrying such as obesity, diabetes, and survival after heart attack. In addition, high out-of-pocket payments and administrative costs suggest ongoing inefficiencies and unequal access (OECD, 2016h). Comprehensive health reforms remain an urgent need (see Table 8).

Fiscal policy has a key role to ensure a fair and inclusive society through redistribution and the tackling of market failures. The needs of the Mexican society in infrastructure, poverty-reduction, education, health care and parental support are large. Across OECD countries, social spending is currently at historical highs, having increased significantly in response to the 2009 recession, while it was marginally raised in Mexico (OECD, 2014c). Those needs call for higher and better-targeted social spending, adopting a spending rule could support such policy:

-

Most of the lower social spending relative to OECD countries is explained by pensions and, to a lesser extent, by health spending. In addition, Mexico is the only OECD country without a national system of unemployment insurance (Figure 8, Panel C). An ambitious unemployment insurance and universal pension reform was initially planned as part of the 2012 Pacto and partially approved with passage in the lower chamber, but it has been delayed in the Senate since April 2014. However, administrative steps should be taken to allow key elements of the reform to improve supervision and returns for the pension funds.

-

The cash transfer programme, Prospera, would benefit from being less complex and being simplified in its design and needed institutional co-ordination. Recent research shows that conditionality, although useful in some circumstances, might not be needed in others and that it could result in adverse effects on participation in the programmes for the poorest individuals (OECD, 2013a). Further supporting efforts to use social workers in order to reach out to marginalised families is essential to tackle extreme poverty, in particular to remote areas and in the South.

-

Work by the OECD suggests that improving the efficiency of public services can yield significant savings (OECD, 2009). For example, adopting best practices in health care spending could save on average 0.7% of GDP in Mexico, while achieving the same health outcomes (OECD, 2012). Mexico has adopted some of those practices regarding procurement, which have saved MXN 11 billion to date. High out-of-pocket payments and administrative costs suggest ongoing inefficiencies and unequal access (OECD, 2016h). With the general government wage bill accounting for roughly one quarter of public spending, bringing public pay closer to private counterparts, such as recent reforms in Hungary and Ireland aimed to do (OECD, 2012), is another area to explore (INEGI, 2015).

To catch up with OECD average and to ensure a more inclusive society, reprioritising government spending should be envisaged in the short term, but further reforms will be needed in the medium term to tackle poverty and raise living standards. While the Government has made significant efforts in tax efficiency with the 2014 tax reform, it is crucial to further raise revenue, by further raising taxes, tackling more aggressively tax evasion and limiting tax expenditures:

-

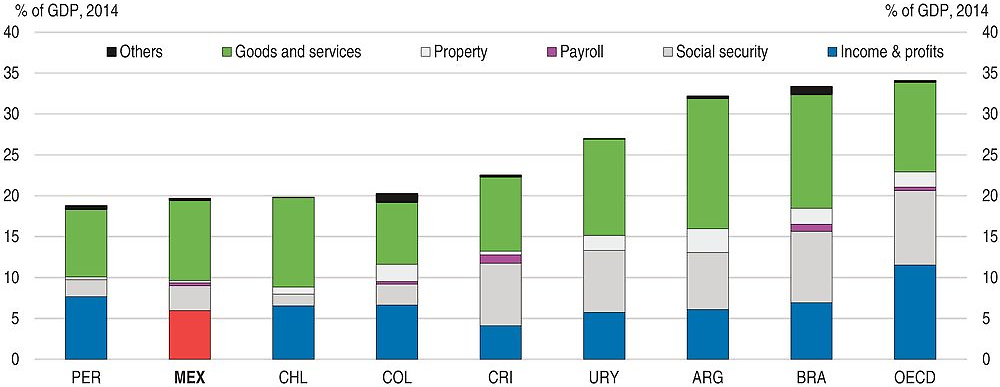

Mexico has made significant progress with the 2014 tax reform and raised the tax-to-GDP ratio by some 3% of GDP since then. There is room to increase property tax as it stands at some 0.3% of GDP compared to about 1.5% in Latin America and 1.9% of GDP for OECD countries (Figure 10) (OECD, 2012c).

Note: For Mexico, revenues from PEMEX are included in Goods and services taxes. They represented 7.1% of GDP in 2014 according to SHCP.

Source: OECD, Revenue Statistics in Latin America and the Caribbean 2016.

-

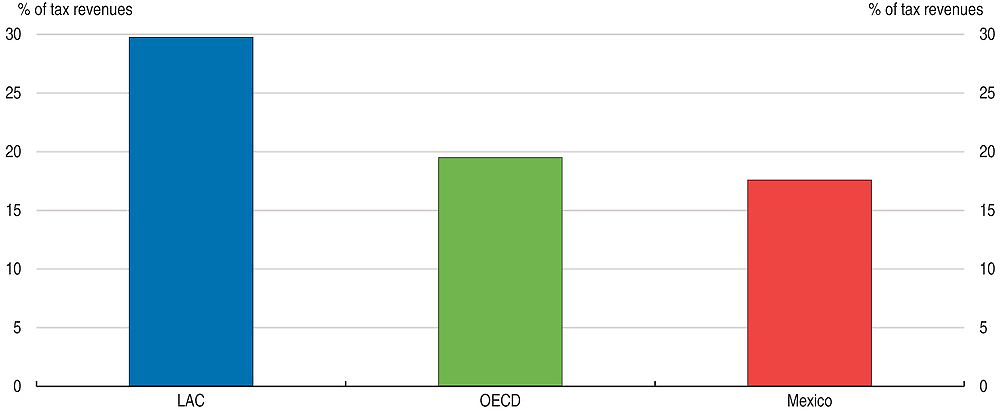

Tax expenditures have been significantly reduced over time. According to the tax administration, they declined from about 6% of GDP in 2005 to about 3% in 2015 (Table 9). The reduction in corporate tax expenditures was particularly significant. However, Mexico has some margin to further raise the VAT, when compared to peer countries in Latin America (Figure 11). Reduced rates on VAT on products should be phased out while paying attention to equity concerns. Further efforts need to be done to limit exemptions on personal income which account for about 0.8% of GDP in 2015.

Source: OECD Revenue Statistics in Latin America and the Caribbean 2016.

-

Tax evasion is relatively high in Mexico (Table 10). Mexico has started introducing reforms in line with the OECD/G20 Base Erosion and Profit Shifting (BEPS) project in the 2014 and 2015 fiscal reforms. Continuing to strengthen international tax rules in line with the OECD/G20 BEPS Actions is needed to ensure a significant reduction in corporate tax avoidance by multinational enterprises. The integration of income and social security administrations could reduce evasion as firms tend to understate labour cost to the social security system (IMSS) and overstate it to the tax administration. For example, merging administration would ensure a single tax ID number, therefore limiting auditing needs across institutions and bring the efficiencies of using a single digital system (HM Treasury, 2011, provides rationale for such integration).

-

Additional measures could be taken to reform the housing programme, INFONAVIT. Under this programme, workers contribute on their wages for housing purposes. The system could be more flexible and allow workers to use such contributions for other purposes, such as unemployment or retirement benefits. Requiring the self-employed to contribute to the social security system (IMSS) could also yield significant contributions and contribute to tackling informality, as the self-employed represent an important share of the labour force.

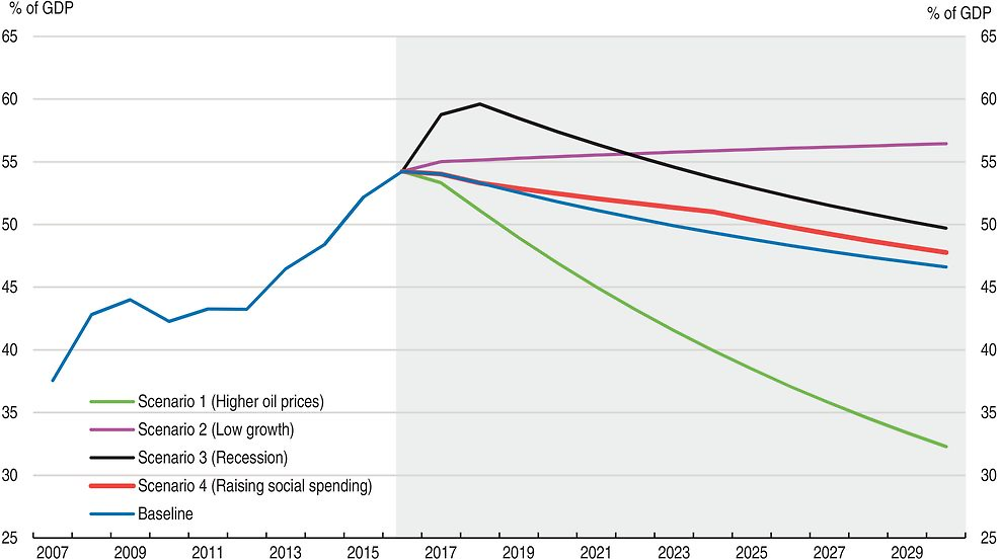

Mexico’s debt-to-GDP ratio is among the lowest among OECD countries. Although it has risen by almost 10% of GDP over the past 3 years and is estimated to have reached about 54% in 2016 (Figure 12), Mexico has scope to increase social spending. Risk scenarios show how vulnerable the baseline is to shocks though. A low growth scenario in which real GDP would grow at its 2016 rate of 2.3% per year, instead of 3% in the baseline would put the debt-to-GDP ratio on an upward trend. A recession in 2017 would significantly increase the public debt, and without additional consolidation measures would raise the debt-to-GDP ratio to almost 60% of GDP in 2018. But if oil revenues rose to pre-2014 levels and were used to amortise the public debt, debt would fall below 35% of GDP before 2030. Finally, an active policy scenario in which the government increases the tax-to-GDP ratio progressively by 0.5% of GDP yearly from 2019 to 2023 and raises social spending by the same amount over the period, would leave the debt-to-GDP ratio only slightly above the baseline in 2030. The drag on growth from the increase in tax is estimated to be about 0.5 percentage points yearly but the growth gains from increasing spending are deliberately left to 0 in order to focus on the downside component of the scenario. More social and education spending will certainly have a positive effect on growth.

Note: The baseline projection assumes: nominal GDP growth of 6.5% year-over-year, constant exchange rates – at about 19 Mexican pesos to one US dollar, and oil prices at USD 45 a barrel, consistent with EO100).

Source: OECD calculations with data from Economic Outlook 100, INEGI and Banxico.

Mexico still needs to deliver on skills and education gaps

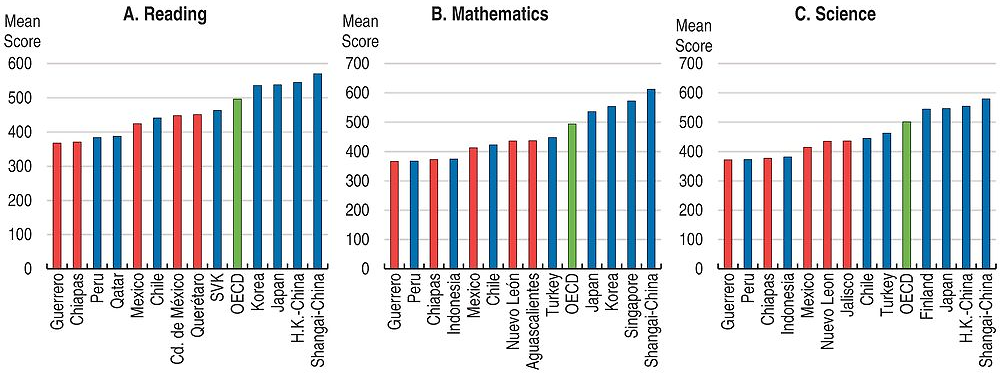

Changes to the education sector were among the first in the series of ambitious reforms introduced by the government’s Pacto. Most recent PISA figures show improvement in mathematics and reading since the mid-2000s, although regional differences in educational outcomes are large (Figure 13) and educational challenges remain high: 56.6% of students are unable to demonstrate attainment of the baseline Level 2 of proficiency in PISA mathematics exams while the OECD average is 22.9%. This level of skills is assumed to represent the skills necessary for participating fully in modern economies (OECD, 2016j). Reaching universal basic skills by 2030 would have a large positive impact on inclusive growth (OECD, 2015c).

Note: Graphs show those countries from OECD and non-OECD countries with the highest and lowest scores, as well as the two Mexican states with the highest and lowest scores. The PISA scores for 2012 are shown since regions were oversampled in that round. Note that the OECD-wide PISA average for 2015 is 1 point lower than the 2012 average in all three categories.

Source: (OECD, 2014b), PISA 2012 Results: What Students Know and Can Do (Volume I, Revised edition, February 2014): Student Performance in Mathematics, Reading and Science.

Educational outcomes also vary significantly across states, with some states failing to achieve national standards for primary and secondary teacher performance. Over half of teachers evaluated in 2015 obtained insufficient or sufficient results (as opposed to good or outstanding), meaning there is still ample room for improvement (SEP, 2016). In this context, it is very important for the government to continue with the full implementation of the reform, emphasising and rewarding the merit of teachers who do well in their job, and by providing courses and training for those requiring support, in order to guarantee the quality of education. In 2016, changes to the teachers’ evaluation design were announced making the evaluation mandatory for those who previously obtained insufficient results or those who want to be certified as evaluators. Teachers willing to access economic promotions may attend voluntarily. Those not taking the evaluation will not be penalised but the gradual evaluation of all teachers would be mandatory starting in 2017. In addition, teachers from indigenous and multi-grade schools will be evaluated by 2018-19 (INEE, 2016). Finally, although in Mexico the overall public and private expenditure on educational institutions is similar to the OECD average, it is very low when looking at the level of expenditure per student. Boosting investment in education remains a significant challenge (OECD, 2016f).

A successful education system is not only one which has high levels of academic achievement, but one that provides all students, regardless of their social origin, the opportunity to obtain a performance of excellence. Between PISA 2003 and PISA 2015 equity levels improved in Mexico. While in 2003 there was a difference of 30 points in mathematics between more socio-economically advantaged students and less-advantaged students, in 2015 this gap narrowed to 18 points. This is the lowest gap across OECD countries. Yet, this positive trait is diminished considering that the performance of both groups is low in comparison with other OECD countries. Since the aim is to provide all students the opportunity to have an excellent academic performance, it is important to continue with the implementation of the reform process aimed at improving and strengthening the support systems for teachers’ capacity building (OECD, 2012a).

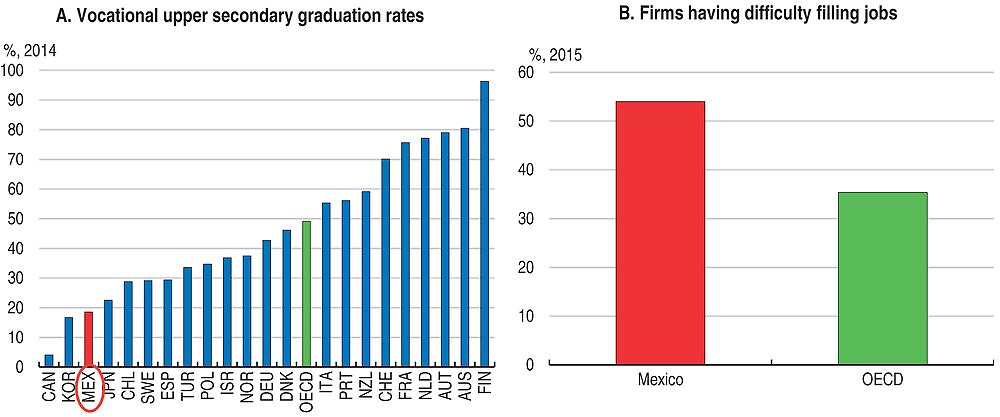

The knowledge and skills of the population have a strong influence on the economic potential for growth and prosperity. And Mexico has a strong demographic advantage, being one of the youngest populations among OECD countries. A higher share of high-skilled adults seems to be related with higher levels of economic output, while a higher share of low-skilled adults relates positively to greater social inequality (Damme, 2014). Fully unleashing the country’s potential requires a comprehensive programme to improve the skills of all Mexicans, both at school and in the labour market, in order to better equip students with the skills demanded by employers. Mexico has a high share of firms reporting having difficulties in finding the skills they require (Manpower Group, 2015) (Figure 14). One way to tackle skill shortages is through investment in vocational education and training (VET), work-based programmes and further promoting the training of students in subjects related to science, technology and mathematics. A Skills Strategy for Mexico is currently ongoing, with the support of the OECD.

Note: Panel A: Data for Canada is 2013. Panel B: OECD refers to the average of 27 member countries with available data.

Source: OECD Education at a Glance 2016 (OECD, 2016c) and Manpower Group (2015).

With the recent education reform, the government has taken steps to expand the supply of technical education by promoting training and vocational programmes (e.g. CONALEP, Bécate, Modelo de Emprendedores de Educacón Media Superior). The National Productivity Committee has led efforts to facilitate the immersion of students in the labour market and the development of skills required by productive sectors and major clusters such as the aerospace and automotive industry, among others, through technological and polytechnic institutes that provide vocational training. However, the VET sector remains among the smallest among OECD countries. Only few students are enrolled in vocational programmes in upper secondary education relative to the total students enrolled in all programmes (38% compared to 44% for OECD countries) and the graduation rate is just 19% of students (OECD average of 49%) (OECD, 2016f).

Moreover, annual expenditure per student in upper secondary vocational programmes in Mexico was USD 3 300 in 2013, lower than the USD 4 700 spent in general programmes. In contrast, across OECD countries, expenditure per student is higher for vocational programmes than for general programmes, over three times as high as Mexico’s expenditure (OECDc, 2016). The government should continue its efforts to support a consultation framework between employers, unions, and the VET system for effective co-ordination, through the implementation of the Occupational Competency Standardization and Certification Council (CONOCER), by adopting apprenticeships to expand workplace training and provide pedagogical training to VET teachers (OECD, 2015b). OECD work in this area has offered insights into how education providers can work more effectively with local businesses, employment agencies, and non-governmental organisations to better match skills supply with demand.

Realising Mexican women’s aspirations

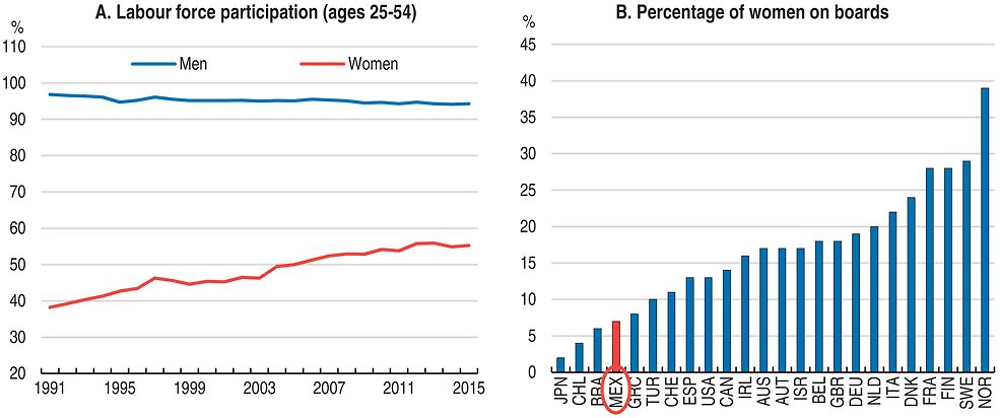

Gender inequalities are large in Mexico (Table 12). While Mexico has made progress in increasing prime-age (25- to 54-year old) women’s participation in the labour force since early 1990s, it remains lower than the OECD average for women and significantly lower than Mexican men’s participation rate. Likewise, Mexican women still earn on average 16.7% less than men, which is partly the result of women’s career breaks, occupational and sector segregation in low-paid and informal jobs, glass ceiling effects, preferences, constraints, differences for paid and unpaid work hours, as well as discrimination in hiring and promotions (OECD, 2016f). Transparency of salary is crucial to facilitate salary negotiations which can narrow the gender pay gap (IPP, 2015).

Recent actions have been taken seeking to empower women and discourage gender discrimination. Among others, maternity leave was made more flexible; a protocol for prevention, care, and sanction of sexual harassment was published; and the requirement of marital status or pregnancy tests as criteria for hiring or dismissing workers is now forbidden. However, employers are still required to pay 100% of wages if they hire a worker who is in the early stages of pregnancy and has not contributed to social security, raising a serious risk of hiring discrimination. Therefore, the government should strengthen laws, enforcement, and implement further strategies for effectively combating all forms of discrimination in pay, recruitment, training and promotion (OECD, 2016d). In addition, measures to help retain talented women at all management levels, particularly at senior positions are needed. In Mexico, less than 10% seats on boards are held by women, a low level compared to other OECD countries (Figure 15). The negative bias in how female leaders’ effectiveness is perceived provides support for the imposition of gender quotas, at least temporarily (Beaman, Chattopadhyay, Duflo, Pande, & Topalova, 2009). Gender quotas to narrow the gender gap in corporate boards have been enforced in several countries (e.g. Norway, Belgium, France, Quebec, etc.) ranging mostly from 30% to 50%, varying for public and private companies. In the case of Mexico, such quotas could be set voluntarily in the first place, and implemented in the public sector to begin with. If progress in the private sector is insufficient, a mandate with fines in case of non-compliance could be introduced.

Source: OECD Labour Force Statistics Database and MSCI ESG Research 2014 Survey of Women on Boards (MSCI, 2014).

Many barriers prevent Mexican women from engaging in the labour force and one of the main challenges that women face is to combine paid and unpaid work: Mexican women spend about four hours more than men on unpaid work per day, the highest gap among OECD countries. The participation of mothers is particularly low, in part owing to the lack of quality and affordable early childhood education, especially for children less than 3 years of age. Early education and child care contribute to raising women’s participation in the labour force. Efforts to expand coverage and enforce mandatory preschool in Mexico have been made by the government and evidence suggests a significant and positive effect in maternal employment (De la Cruz Toledo, forthcoming). However, limited capacity, lack of geographic coverage, incompatibility of service schedules and affordability are some of the factors hindering women’s participation in the labour force. Further expansion of public early childcare and preschool coverage and opening hours is needed to facilitate the entry of mothers into the labour market.

In Mexico, the maternity leave available to mothers is fully paid but short (12 weeks) relative to the OECD average. Likewise, recently legislated paid paternity leave is only one week long compared to the OECD average of seven weeks (paternity and parental leave reserved for fathers). The recent change to make maternity leave more flexible and the recent legal recognition of teleworking are advances in the right direction. However, more gender-equitable use of parental leave entitlements by extending the length of father-specific leave could also level the playing field, reduce the traditional role of women as caregivers, and increase women’s working hours (Akgunduz and Plantenga, 2011; Dearing, 2015; Kotsadam and Finseraas, 2011; OECD, 2012b; OECD, ILO, IMF, and WB, 2014).

Mexico’s self-employment rates (25% for women and 27% for men) are higher than the OECD averages (10% for women and 18% for men). Both men and women face challenges to growing their businesses in Mexico, including inadequate access to credit. However, self-employed men are more likely to be employers and to be formally registered in the tax and social security system. Self-employed women tend to be own-account workers (22%) more than employers (3%), more likely to work informally, have lower earnings than men, start businesses at a smaller scale and in a limited range of sectors (OECD, ILO, IMF, & WB, 2014). The fact that women are coming across complications in transitioning into the formal sector and growing their enterprises represents a source of untapped potential.

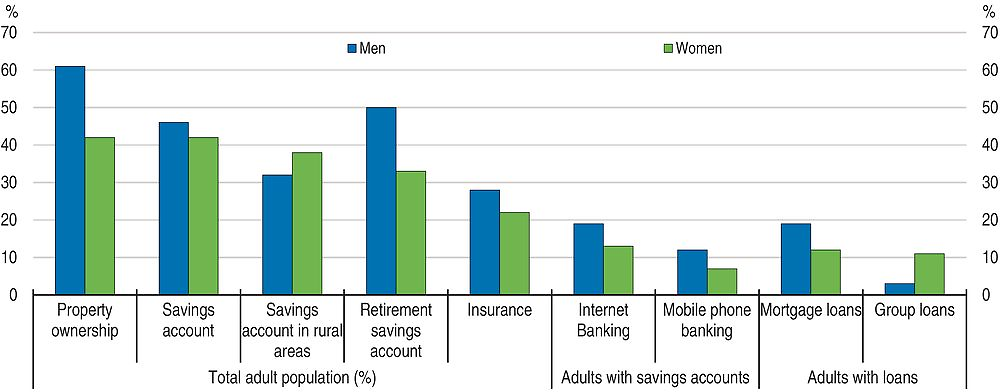

Financial inclusion can have a positive impact on self-employment, women’s empowerment and well-being (Bauchet, Marshall, Starita, Thomas, & Yalouris, 2011; Pasali, 2013; Cull, Ehrbeck, and Holle, 2014). Recent research (Fareed, Gabriel, Lenain and Reynaud, 2017) shows that access to financial services in Mexico can open up economic opportunities for women, particularly as entrepreneurs. Mexico has shown a clear focus on financial inclusion by developing a national financial inclusion body and introducing crucial financial reforms. The recently launched Programa Integral de Inclusión Financiera is a clear effort in this direction. (Gobierno de la República, 2014). Still, big gender gaps exist in terms of savings account, possession of assets, savings for retirement, insurance and credit for housing (Figure 16).

Source: Encuesta Nacional de Inclusión Financiera (ENIF) 2015, (CNBV, 2015).

Many of the issues faced by women entrepreneurs are similar to those faced by men and are largely related to access to finance and market. However, many characteristics of women entrepreneurs and of their enterprises differ from those of men, and therefore require specific policy interventions. Programmes such as Mujeres PYME, which seeks the development of micro-, small-, and medium-sized enterprises (SME) led by women by providing access to preferential financing and business development tools, is a step in the right direction. The government should continue its efforts to enhance financial infrastructure, increase the diffusion, scale and reach of current public programmes that facilitate access to low-interest credit for female-owned SMEs, provide financial capability trainings, and increase the capacity of financing institutions to respond to female entrepreneurs’ needs. The National Entrepreneur Fund also represents an effort by the Mexican government to streamline SME policy regulations and increase transparency in funding allocation; promoting the development and management of funds to provide financial support exclusively for women entrepreneurs could also be considered (OECD, 2014a).

Reforms are boosting productivity in certain industries

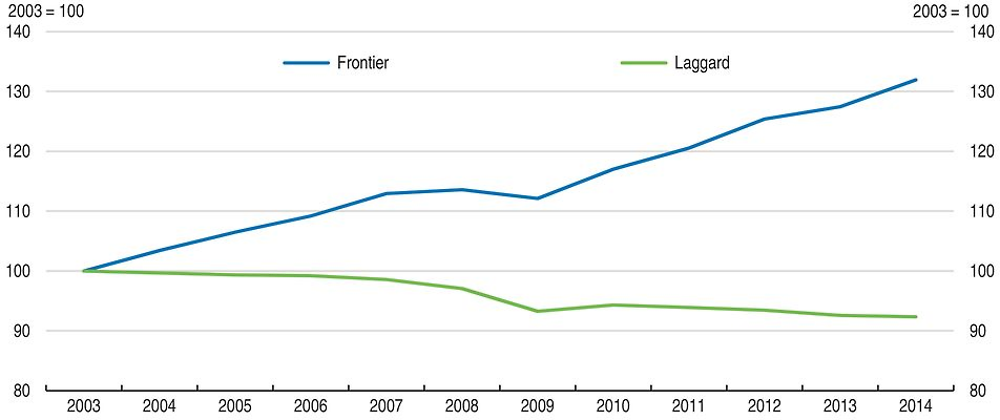

Structural reforms have paid off and should be pushed further. The government has continued to roll out its package of reforms to introduce further competition in the energy sector (electricity, oil and gas) and telecommunications, while empowering the competition authorities to deter collusion, monopolies, and other anti-competitive practices. This has reduced prices – by more than 25% in the case of telecommunications – to the advantage of consumers and businesses. Some benefits have emerged more quickly than expected, in particular for productivity growth, which has picked up recently, with multifactor productivity growth turning from negative to positive since 2014. Nonetheless, large differences prevail across sectors, states, and firms – a situation not unlike that in many OECD countries. Mexico’s most productive firms are performing well, such as in the sector of transportation equipment manufacturing, but the majority of firms are still struggling to perform better with limited success, leading to a growing dispersion in productivity, with a few leading sectors pulling ahead (Figure 17).

Note: Frontier sectors are the 10 NAICS (North-American Industry Classification System) three-digit sectors (out of 65) with the highest TFP growth over the period. They include the auto sector, telecommunications, quarrying, warehousing services and services associated with agriculture, among others. The laggard sectors represent the average of all non-frontier industries, meaning the 55 industries with the lowest TFP growth.

Source: INEGI KLEMS Productivity database.

A reallocation of resources from low-productivity to high-productivity industries would boost Mexico’s economic prospects. Within manufacturing, a more efficient allocation of productive factors across the bottom three-quarters of firms could increase production by 2.4 percentage points of GDP; a more efficient allocation across all firms could yield a boost of 5.9 percentage points of GDP (Dougherty and Escobar, 2016b). In successful emerging market economies, re-allocation from low to high productivity sectors has contributed substantially to income convergence. However, in Mexico, the contribution of labour reallocation across sectors is low, contributing only about 15% to productivity growth. On the positive side, reallocation in transportation equipment and services has been more frequent – with wholesale trade in particular a major success story – and considerable within-industry productivity growth, such as in retail trade and banking. The establishment of Special Economic Zones will also channel efforts and resources into a cohesive strategy that targets areas with a higher concentration of unproductive firms and sectors.

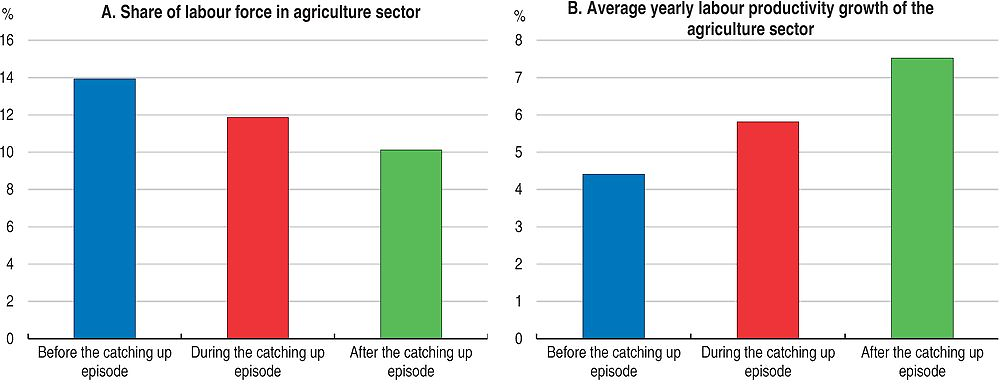

Given its sheer size in terms of labour share and typical low productivity levels, agriculture is a sector for which the transition has not happened yet in Mexico. In past episodes of rapid diminution of the income gap with first tier OECD countries, yearly averages of labour productivity growth in the sector were three percentage points higher after the episode and the employment share of agriculture decreased on average by four percentage points in selected OECD countries (Figure 18). Since the agriculture sector is also typically characterised by high informality and poverty rates, modernization has the benefit of increasing productivity and income which typically raises those more productive workers from informality and poverty.

Note: Catching-up periods have been identified as period of sharp decrease in the GDP per capita gap with the highest tier of OECD members. The selected countries/periods are as follows: CHL (2007-13), GRC (2001-09), HUN (2000-06), KOR (2007-15), POL (2006-12), SVK (2000-08), SVN (2000-08), and TUR (2001-11).

Source: OECD calculation using Economic Outlook 100 and World Bank data.

Mexico has a high share of jobs in agriculture (13%) among OECD countries. This has remained almost unchanged since the early-2000s. Structural reforms should boost the modernization of agriculture, such as reforms of the legal framework of eijidos and tierras communales (areas of communal lands used for agriculture). The PROAGRO programme introduced in 2013 reformed agricultural subsidies, the new payments are linked to specific actions to improve land productivity (OECD, 2014), as farmers must give proof that the payment has been used for technical, productive, organisational or investment improvements, that is, technical assistance, machinery, certified seeds, fertilisers, restructuring, insurance or price hedging.

Mexico’s high rate of informality, excluding agriculture, has declined by two percentage points since 2012, from 54.7% to 52.5% (INEGI-ENOE 2016) – or three percentage points with agriculture included (from 60% to 57%). The absolute number of workers with an informal employment relationship (“informal employment”) is still high and women are more likely than men to work informally. About half of Mexico’s informal workers are employed in extremely small, informal firms, which suffer from low productivity. The productivity of microenterprises (under 10 workers) could be boosted dramatically if these firms were pushed to either grow or exit. Simulations suggest that aggregate growth could be boosted by up to one percentage point if informality were reduced by 10 percentage points (OECD, 2015a; Dougherty and Escobar, 2016a). States and industries with high productivity suffer disproportionately more because their resources tied up in informal activities are not used in more productive activities.

The government should therefore further enforce compliance with social security contributions for all workers in formal companies. While there has been strong take-up in the fiscal regime for incorporation (Régimen de Incorporación Fiscal, RIF), which has induced 1.5 million informal firms to join the tax system since 2014, there is too little awareness of a related programme from 2014, the social security regime for incorporation (Régimen de Incorporación a la Seguridad Social, RISS), which offers reduced contribution rates for workers joining IMSS, the national social security system. This programme has design features that borrow from the successful experiences of countries such as Brazil that have made important inroads in fighting informality (Box 4). Stepped-up enforcement measures have been employed focusing on firms with 50 or more employees. Focusing also on smaller firms, which should include state-level informality reduction targets, and a range of complementary policies to boost skills and reduce regulatory barriers, is warranted.

The business sector can also contribute to higher formalisation by making sure that all business partners across each firm’s value chains follow key labour rules, for instance by having a corporate policy or code of conduct that addresses labour standards – mandating formality among suppliers and distributors. Certification measures are particularly helpful in this regard, and have been successful in the automotive sector, where informality rates are among the lowest.

Several Latin American countries have been relatively successful at reducing informality during the last decade. Among these, Brazil stands out as one of the most successful cases and could, therefore, be of interest for Mexico to learn what policies have been successful in countries with a similar level of development (Tornarolli et al., 2014). Brazil experienced a significant reduction in its informality rate – from over 60% in 2000 to under 50% in recent years (Filho and Veloso, 2016). As in other Latin America countries (e.g. Argentina, Peru and Ecuador), this significant reduction in the informality rate was driven, on a large extent, by economic growth. Hence, it is likely that continued emphasis on creating the right conditions for economic growth will lead to further gains in formal employment. However, evidence suggests that, in the case of Brazil, specific policy interventions also contributed to reduce the informality rate. For instance, a number of studies of the Brazilian case suggest that the reduction of employment costs helped to reduce informality. In particular, the introduction of an integrated tax and contribution payment system for micro and small enterprises (the 1996 SIMPLES Law), had a significant effect on the informality rate. This law facilitated registration and lowered the rate of taxation for small and microenterprises. Evidence suggests that this law contributed to the formalisation of nearly 500 000 microenterprises between over five years in the early 2000s, accounting for around two million jobs. A more recent law aimed at microenterprises with one employee (Lei Complementar 128/2008) also significantly reduced the cost of formalisation and contributions to social security. Recent evidence suggests that this law also had an impact on the formalisation of the self-employed, although there appears to be some perverse effect also on firms substituting regular employees for self-employed service providers.

Stricter enforcement mechanisms have also contributed to a higher proportion of formal employment. Evidence suggests that stricter enforcement leads to a higher proportion of formal employment. Although Brazil did not increase the number of labour inspectors to the level recommended by the ILO, it introduced a couple of initiatives that have enhanced monitoring and enforcement. In particular, Brazil changed the incentives under which inspectors work, including a bonus system linking salaries to performance targets, which have greatly increased the effectiveness of enforcement and led to an increase in formal worker registration.

Source: OECD (2013e, 2015a, 2016).

Openness to trade and investment is paying off in some sectors

Mexico is very open to foreign trade and investment: 12 free trade agreements have been signed with 46 countries and foreign direct investments is significant. With its strategic location, low unit labour costs and increasingly adept labour force, Mexico is gradually evolving into a global manufacturing hub. Experience suggests that participating in global value chains (GVC) and climbing up the value chain contribute to faster productivity growth (OECD, 2016).

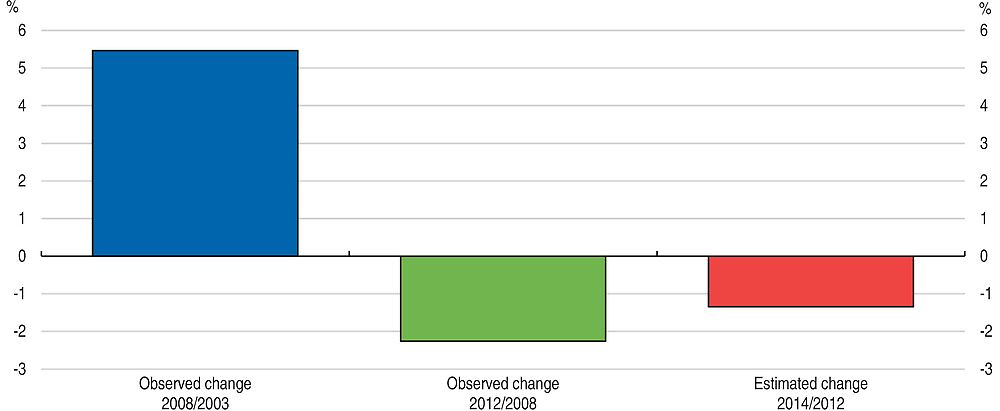

Following NAFTA, Mexico benefited from its integration in GVCs mostly as assembler of manufactured inputs. In recent years, domestic content has increased and imported content declined (Figure 19). This means that more domestic value added is present in Mexico’s exports. To draw more value-added from its global engagement, Mexico needs to further improve its capabilities in knowledge and skill-intensive activities within GVCs (such as new product development, manufacturing of core components, or brand development) and further reduce barriers to foreign investment and services trade in productive sectors not yet well integrated into GVCs but with high comparative advantages.

How to read this chart: Import content of exports is defined as the share of imported inputs in the overall exports of a country, and reflects the extent to which a country is a user of foreign inputs. The measure is also often referred to as the ‘foreign value-added share of gross exports’ and is defined as the foreign value-added in gross exports divided by total gross exports, in percentage. It is considered as a reliable measure of international “backward linkages” in analyses of global value chains. The observed changes for 2008/2003 and 2012/2008 are the unweighted averages of ICEs for each manufacture industry. The estimated change 2014/2012 is projected using regression analysis on a panel of ICEs per industries over the periods 2008/2003, 2012/2008 and 2014/2012. The estimated equation is: d.ICEit = α + d. FDIit + d.Mit + fei + εit, where d.ICEit represents the change over the periods for each industry i, d. FDIit represents the cumulated change of Foreign Direct Investment in the industry, d.Mit the cumulated change in imports in the industry, and fe fixed industries effects.

Source: OECD calculations using INEGI 2003-08-2012 Input Output tables.

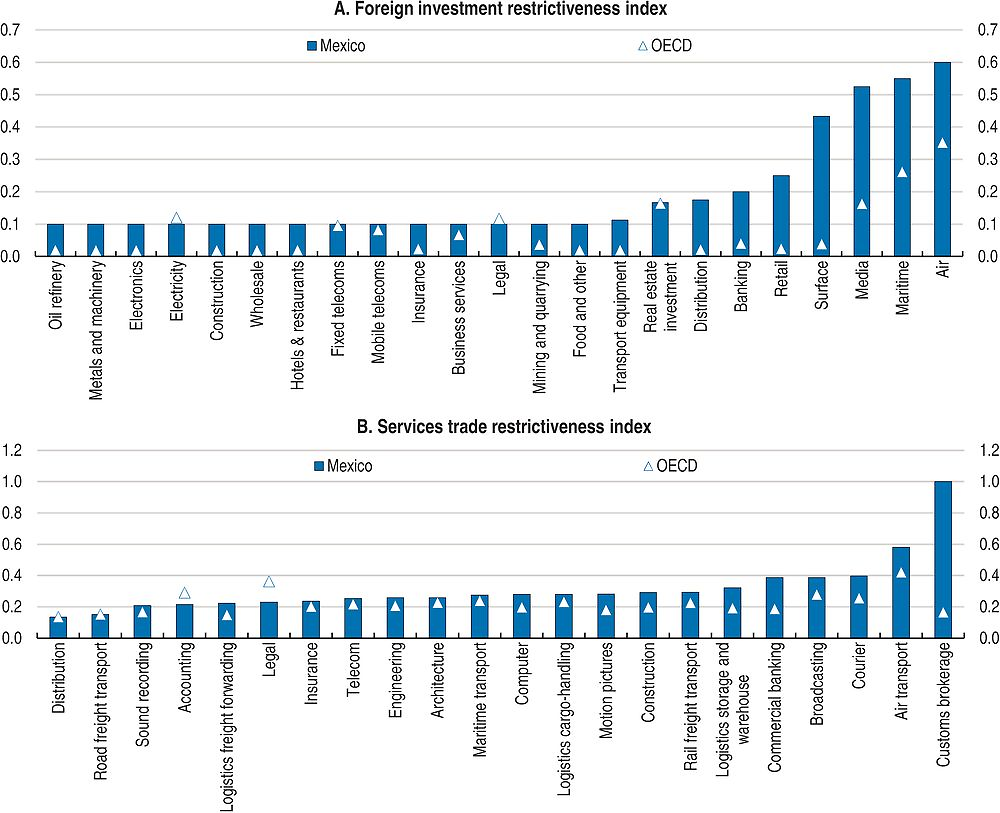

Much progress has been achieved to reduce trade barriers, make it easier to do business, and improve regulation. Barriers to foreign investment and services trade have been reduced in key sectors – notably media and telecoms – but a substantial gap remains to OECD best practice in nearly all sectors (Figure 20), such as transportation, while they could be reduced further in nearly all sectors, through systemic reforms. Greater harmonisation of rules with trading partners could yield a further boost to trade flows (Nordås, 2016).

Note: Indexes are measured on a scale from 0 to 1, 1 being highly restrictive.

Source: OECD FDI and Services trade Restrictiveness databases.

Growing disparities among states and sectors in Mexico motivated a new plan to introduce special economic zones (SEZs) by the government. These zones are intended to support development in less developed states, and have the potential to attract investment, improve infrastructure and reduce regulatory barriers in these regions. The first three such zones will begin operation in the second half of 2017. In each of these initial zones, private sector investors have already been identified. Tax incentives are being provided, using criteria based on the degree of local sourcing and related contributions, which reflects the evolving good practice for such zones. These incentives and implementation will need to be monitored in the context of a cost-benefit analysis, to ensure sufficient positive spillovers, and to ensure that the private sector maintains a leading role (OECD, 2015a; World Bank, 2011). In addition, these zones could be linked with Mexico’s emerging technology clusters and their high value added products, such as aeronautics, to help spur positive spillovers across different sectors and domestic suppliers. A mapping of such opportunities (State Innovation Agendas) is currently being undertaken by Mexico’s national research and science council (CONACYT).

Innovative firms are more likely to participate in international markets than non-innovative firms (OECD, 2008, 2015). In the case of Mexico, evidence supports the relation between innovation and spending in R&D at the industry level and GVCs integration and productivity levels. However, private sector R&D expenditure in Mexico is well below that of nearly all OECD and BRICS countries. Change in R&D policies in 2008 boosted public sector spending, which is now catching up with OECD average, standing above 0.4% of GDP in 2014 (against 0.61% for the OECD average). The relatively low level of private R&D is partly a result of Mexico’s industrial structure, as over one-third of manufacturing R&D is carried out in low and medium-technology sectors. However, obstacles to boosting the country’s innovative potential include a weak domestic research and skills base, an underdeveloped knowledge-based start-up environment and institutional challenges.

Further raising R&D intensity is one of the priorities of the current administration which intends to double R&D spending from 0.54% of GDP to 1%. A tax credit on R&D was approved by Congress in the context of the 2017 Budget. Firms will be able to offset 30% of their qualifying R&D expenditures against income tax. In order to further support the private sector to integrate and climb up GVCs, the government and states need to foster cooperation between public and private research centres. In particular, the government should aim at further improving the early stage financing framework that facilitates co-operation of public research institutes and innovative private businesses (OECD, 2013c). Further supporting joint private and public R&D could be done in the same vain as the tertiary education measures for specific productive and well integrated sectors, such as aeronautics in Querétaro.

Further reforms are needed to improve governance and legal institutions

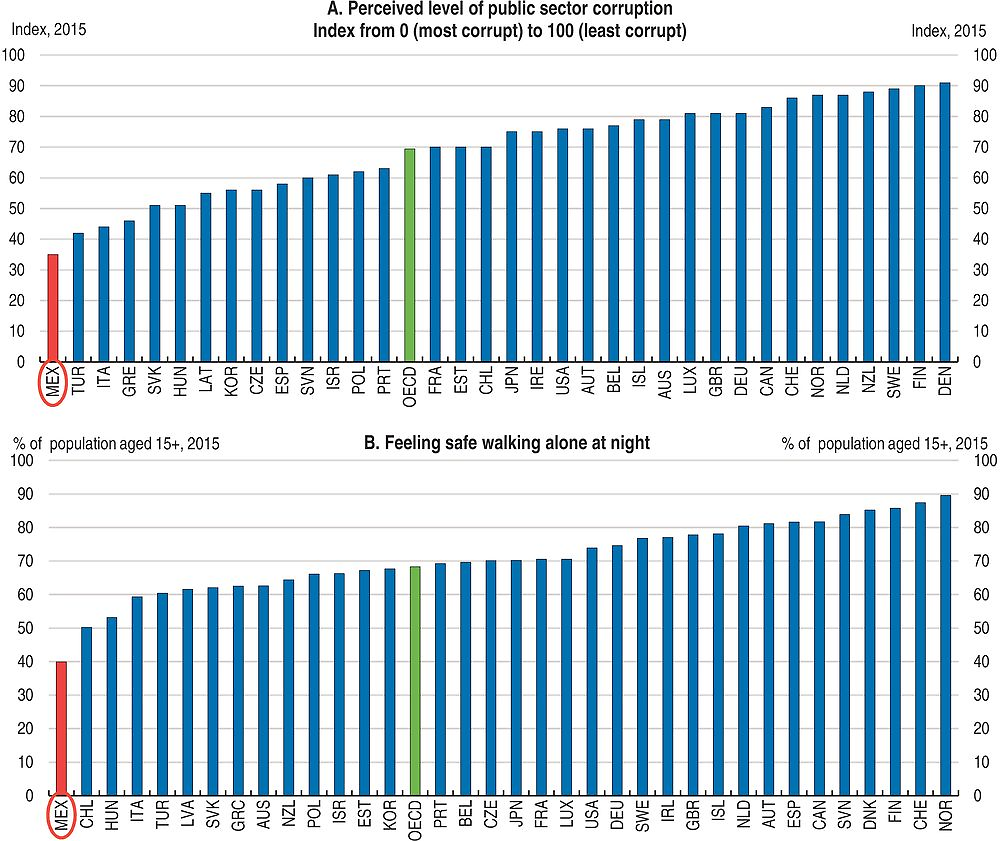

Mexico is perceived as a county that faces significant corruption problems (Figure 21, Panel A). The long delayed anti-corruption system was approved by Congress last year. The new system involves six government entities with the strong involvement of citizen committees, making the system quite complex, although less vulnerable to capture (OECD, 2017). Concerns remain about how the plan will be implemented at the local level, since states must now pass their own legislation and establish institutions that function effectively and without interference. Given the limited administrative capacity of many state and local governments, strong support and monitoring from the national level may be needed. This could involve providing a mechanism to delegate some roles to the federal anti-corruption system.

Given high crime rates in many states – notably homicide, kidnapping and extortion – which directly reduce well-being and perception of safety, an important priority of the government has been to improve security (Figure 21, Panel B). Areas of the country that have faced the most violence were often those that had the most productive firms and their average firm size and productivity has been depressed. More effective law enforcement strategies have been an important objective. Further professionalisation of police forces at all levels has been needed for quite some time, along with better co-ordination with local authorities. The federal government has facilitated this move by signing state-by-state agreements (with 17 states agreed by early 2016) that allow for integrated state-wide police forces. These shifts have boosted training and are expected to also reduce corruption.

Note: Panel B: Percentage of people aged 15 and over. The reference year is 2015 with the exception of 2013 for Iceland. The indicator is based on the question: “Do you feel safe walking alone at night in the city or area where you live?” and it shows people declaring they feel safe.

Source: OECD Better Life Index – Edition 2016 Database, Transparency International.

There has been rapid progress to reform certain parts of the judicial system, notably in the criminal domain, where the legal system was not effective. However, further reform would be beneficial. Although most states have begun to implement the new criminal trials, not all of them are equipped to implement them effectively. The full functioning of the system, with training of all of the police, lawyers, judges, and associated infrastructure, will take longer. Encouragingly, there has been a dramatic reduction in criminal case resolution time from 170 days to 27 days now, relying heavily on mediation.

A second wave of legal reform to civil and commercial justice still remains to be fully acted upon, although a start has been made for larger cases. The OECD has estimated that such reforms could add half a percentage point to GDP growth in the medium term (OECD, 2015a). Large efficiency gains from transitioning from written to oral trials can help to improve the outcomes of economic disputes such as those related to contract enforcement. The new procedures are now only applied to the largest cases, and not in all jurisdictions. This is in part due to resource constraints in state judicial systems. The concerted efforts that have been made to adopt the new procedural reforms for criminal cases need to also be fully extended to apply for all civil and commercial cases, following the 2011 framework.

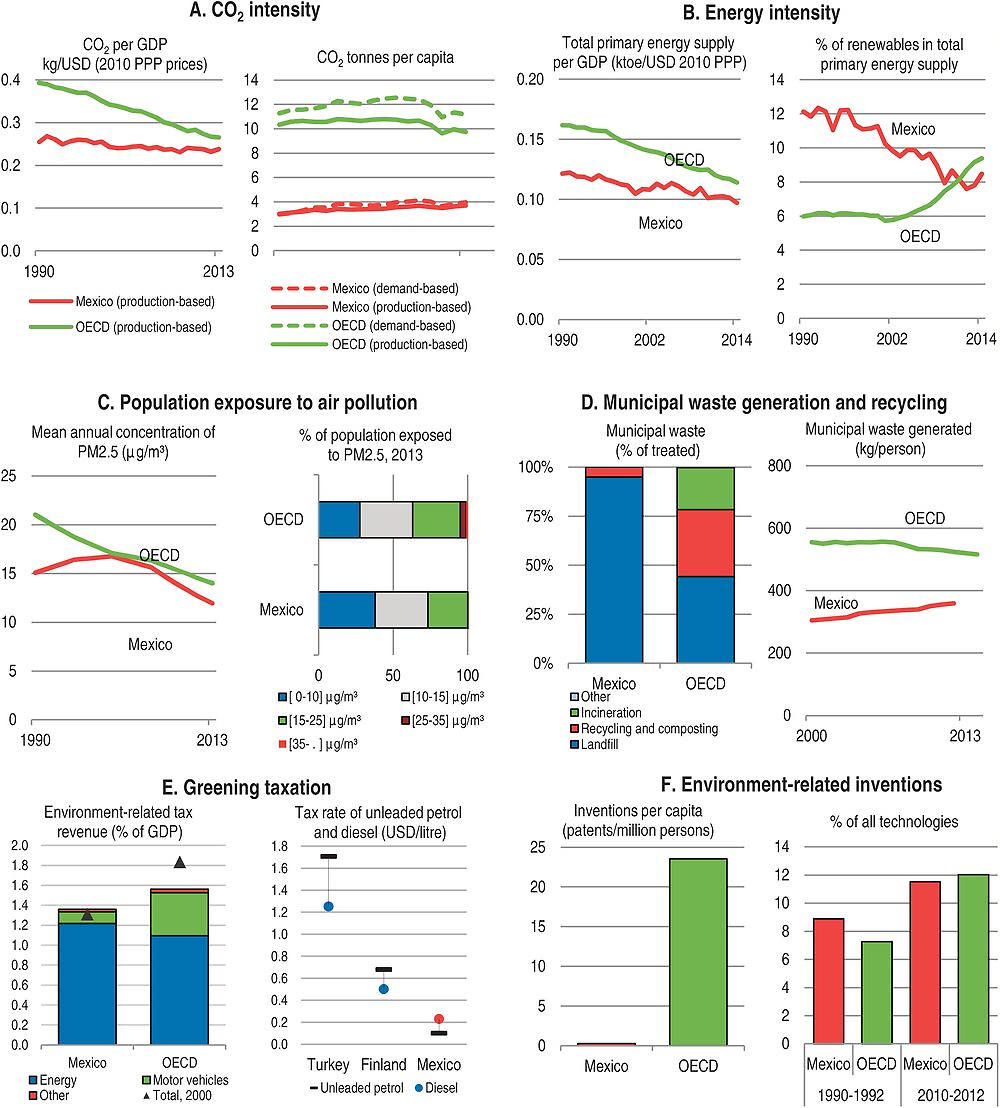

The carbon emissions tax rate remains insufficient

Mexico has made an unconditional commitment to reduce greenhouse gas (GHG) emissions by 22% by 2030 under the UNFCCC framework. The gradual deregulation of gasoline and diesel prices, which began in 2017 and should be completed by 2018, and the significant increase in rates of the “Special Tax on Production and Services” (IEPS) have improved the extent to which taxes reflect the external cost of emissions (Box 5). The increase in the effective tax rates on gasoline and diesel is remarkably large, and the 2016 rates are comparable to those of many lower-tax OECD countries. However, since those fuels are used mainly for road use, the tax burden is levied mainly on the transport sector, which accounts for roughly a third of energy use and carbon emissions in Mexico (OECD, 2016e).

Mexico’s per capita emissions of greenhouse gases – excluding most of those due to forest clearance – are well below the OECD average, but have been rising. Emissions per unit of GDP have declined very little over the past 25 years and are now not much below the OECD average. Emissions from forest clearance add approximately 10% to total emissions, but have decreased substantially as net forest clearance has fallen by over half since the 1990s.

During the 1990s, a major effort took place in order to shift electric generation from fuel to natural gas. Investments were substantial and contributed to a significant change in Mexico’s carbon emissions. Air pollution has improved very much over the past 20 years, overall somewhat cleaner than in average OECD countries. But some large cities, especially Mexico City, still have frequent episodes of bad air pollution, which seem to have increased in frequency recently.

GDP growth since 1990 has been accompanied by a decline in energy intensity (total primary energy supply per unit of GDP). In recent years the decline has faltered, however. And while the share of renewables has been relatively high in the past, it has declined significantly even as it rose in most OECD countries. More than half of renewables is from biofuels and waste; wind and solar power are insignificant. In order to facilitate green growth, the government has made several efforts. For instance, income tax provides a 100% of immediate deduction for investments in machinery and equipment used to generate energy from renewable resources or from efficient electricity cogeneration systems. Moreover, the Congress approved the 2017 Budget which included fiscal incentives for investments in the development of charging stations for electric vehicles. In March and September 2016, Mexico’s National Centre for Energy Control (CENACE), held 2 public biddings for nearly 80% of the electricity demand of the Federal Electricity Commission, for which half is dedicated to clean energy sources, specifically at wind and solar.

Water quality in rivers and lakes is acceptable or good in most of the country but very poor in the area around Mexico City, where a large share of wastewater is untreated. Following a near tripling of investment in water infrastructure between 2000 and 2010, access to piped drinking water is now over 90%, although much lower than this in some rural areas.

Precipitation varies a lot geographically and through time, so groundwater plays an important storage role; an increasing number of areas are in overdraft, with declining levels in aquifers; most aquifers in the country are affected, and salination is now an additional problem in some, such as around the regions of Baja California and Mexico City (Conagua, 2010).

Municipal waste generation per capita is lower than the OECD average but has been increasing in Mexico while it has been declining in other countries. Few municipalities charge households for waste collection, and none use quantity-based charges. Almost all such waste is sent to landfill.

Revenue from environmental taxes has increased in recent years and is now comparable to the OECD average.

Measured by patenting activity, Mexico devotes a similar, increasing, share of its R&D effort to environmentally-oriented activities as the average OECD country, but within a very low overall per capita total.

Carbon emissions outside the road sector (residential heating, industrial processes and electricity generation) are partially taxed under the newly introduced carbon tax at very low rates, or are entirely unpriced. Natural gas, which accounts for a third of carbon emission from energy use, is exempt from the carbon tax and overall only 40% of carbon emissions from non-transport sectors energy use is subject to the carbon tax. On a weighted-average basis, the carbon tax rate lies around MXN 22.79 per tCO2 (EUR 1.16 per tCO2). The Mexican carbon tax rates are far below the lower-end estimate of the climate cost of EUR 30 per tCO2 (OECD, 2015e). Therefore, for the carbon tax to send a strong price signal on the external costs of carbon emissions, its tax rates should be increased and reflect fuels’ carbon content more uniformly. Increases in the carbon tax are needed particularly in the non-road sectors (OECD, 2016e).

Increasing and fixing the tax rates of the IEPS has already benefited tax revenues. While income from the fluctuating component of the IEPS was negative in 2013 and 2014, tax receipts turned positive in 2015. The carbon tax has not accounted for more than 0.5% of total tax revenues since its introduction. If the tax rate is increased and the tax base expanded (e.g. to include natural gas), the carbon tax has the potential to account for a significantly larger share of tax revenues (OECD, 2016e).

Note: Panel E shows preliminary 2015 figures for Mexico, to better reflect the implementation of the reform IEPS on fuel and gas, and 2014 figures for other OECD countries.

Source: OECD (2016i), OECD Green Growth Indicators Database. For further details please refer to the metadata.

References

Akgunduz, Y., & Plantenga, J. (2011), “Labour Market Effects of Parental Leave. A European Perspective”, Utrecht School of Economics, Tjalling C. Koopmans Research Institute, Discussion Paper Series, No. 11-09.

Banxico (2016a), “Anuncio de Política Monetaria”, Banco de Mexico, Comunicado de Prensa, 29 September.

Banxico (2016b), “Anuncio de Política Monetaria”, Banco de Mexico, Comunicado de Prensa, 30 June.

Bauchet, J., Marshall, C., Starita, L., Thomas, J., & Yalouris, A. (2011), “Latest Findings from Randomized Evaluations of Microfinance”, Financial Access Initiative, Innovations for Poverty Action, and Abdul Latif Jameel Poverty Action Lab. Forum 2. CGAP.

Beaman, L., Chattopadhyay, R., Duflo, E., Pande, R., & Topalova, T. (2009), “Powerful Women. Does Exposure Reduce Bias?”, The Quarterly Journal of Economics (2009) 124 (4), 1497-1540.

Carstens, A. (2015), “Challenges for Emerging Economies In The Face Of Unconventional Monetary Policies In Advanced Economies”, Stavros Niarchos Foundation Lecture, Peterson Institute for International Economics, April 20, 2015, Banco de México.

Cerutti, E., Claessens, S., and Laeven, L. (2015), “The Use and Effectiveness of Macroprudential Policies: New Evidence”, IMF Working Papers, No. 15/61.

CNBV (2015), “Encuesta Nacional de Inclusión Financiera”, México, Inclusión financiera, Principales hallazgos.

CONAPRED (2012), “Reporte sobre la discriminación en México 2012”, Crédito. D.F., Consejo Nacional para Prevenir la Discriminación.

Cull, R., Ehrbeck, T., & Holle, N. (2014), “Financial inclusion and development: recent impact evidence”, Washington, DC. World Bank Group, CGAP focus note; No. 92.

Damme, D. (2014), “How Closely is the Distribution of Skills Related to Countries’ Overall Level of Social Inequality and Economic Prosperity?”, OECD Education Working Papers, No. 105.

Daubanes, J. and S. Andrade de Sá (2014), “Taxing the Rent of Non-Renewable Resource Sectors: A Theoretical Note”, OECD Economics Department Working Papers, No. 1149.

De la Cruz Toledo, E. (forthcoming), “Preschool Enrolment and Mothers’ Employment in Mexico”, extended abstract.

Dearing, H. (2015), “Does parental leave influence the gender division of labour?”, Recent empirical findings from Europe, Vienna University of Economics and Business, Institute for Social Policy, Working Paper No. 1/2015.

Dearing, H. (forthcoming), “Designing gender-equalizing parental leave schemes – what can we learn from recent empirical evidence from Europe?”, Journal of Family Research.

Dougherty, S. and O. Escobar (2016a), “Could Mexico become the new ‘China’? Policy drivers of firm-level competitiveness”, OECD Productivity Working Papers, No. 4.

Dougherty, S. and O. Escobar (2016b), “Misallocation and competition in Mexico”, OECD Economics Department and Paris School of Economics, Manuscript.

Dougherty, S., R. Herd and T. Chalaux (2009), “India’s growth pattern and obstacles to higher growth. What is Holding Back Productivity Growth in India? Recent Microevidence”, OECD Economic Studies, Vol. 45 (1).

Fareed, F., Gabriel, M., Lenain, P. and Reynaud, J. (forthcoming), “Financial inclusion and women entrepreneurs”, OECD Economics Department Working Papers, OECD Publishing, Paris.

Filho, F. and F. Veloso (2016), “Causas e Consequências da Informalidade no Brasil [Causes and Consequences of Informality in Brazil]”, Elsevier, FGV-IBRE, Rio de Janeiro.