Japan

This chapter includes data on the income taxes paid by workers, their social security contributions, the family benefits they receive in the form of cash transfers as well as the social security contributions and payroll taxes paid by their employers. Results reported include the marginal and average tax burden for eight different family types.

Methodological information is available for Personal income tax systems, Compulsory social security contributions to schemes operated within the government sector, Universal cash transfers as well as recent changes in the tax/benefit system. The methodology also includes the parameter values and tax equations underlying the data.

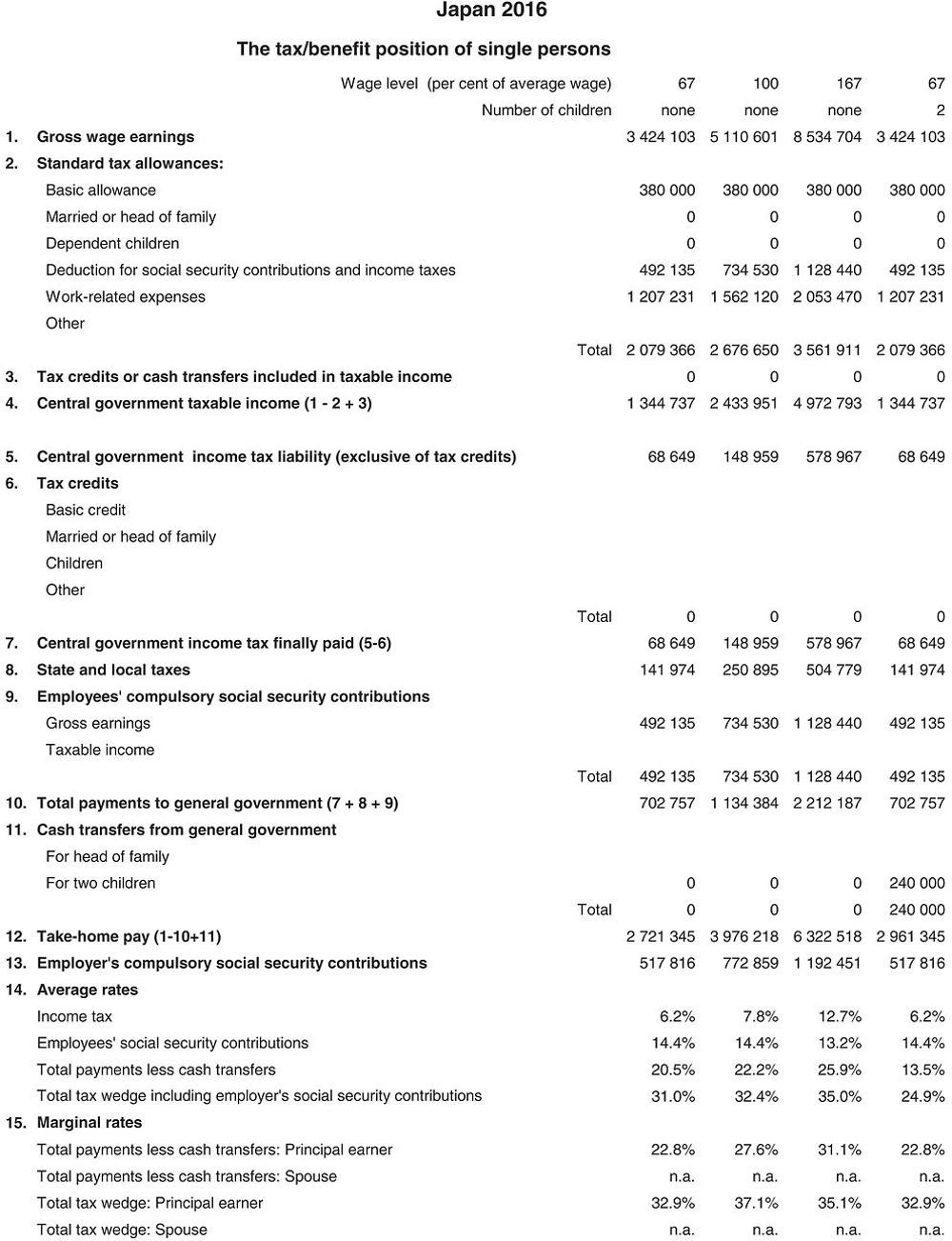

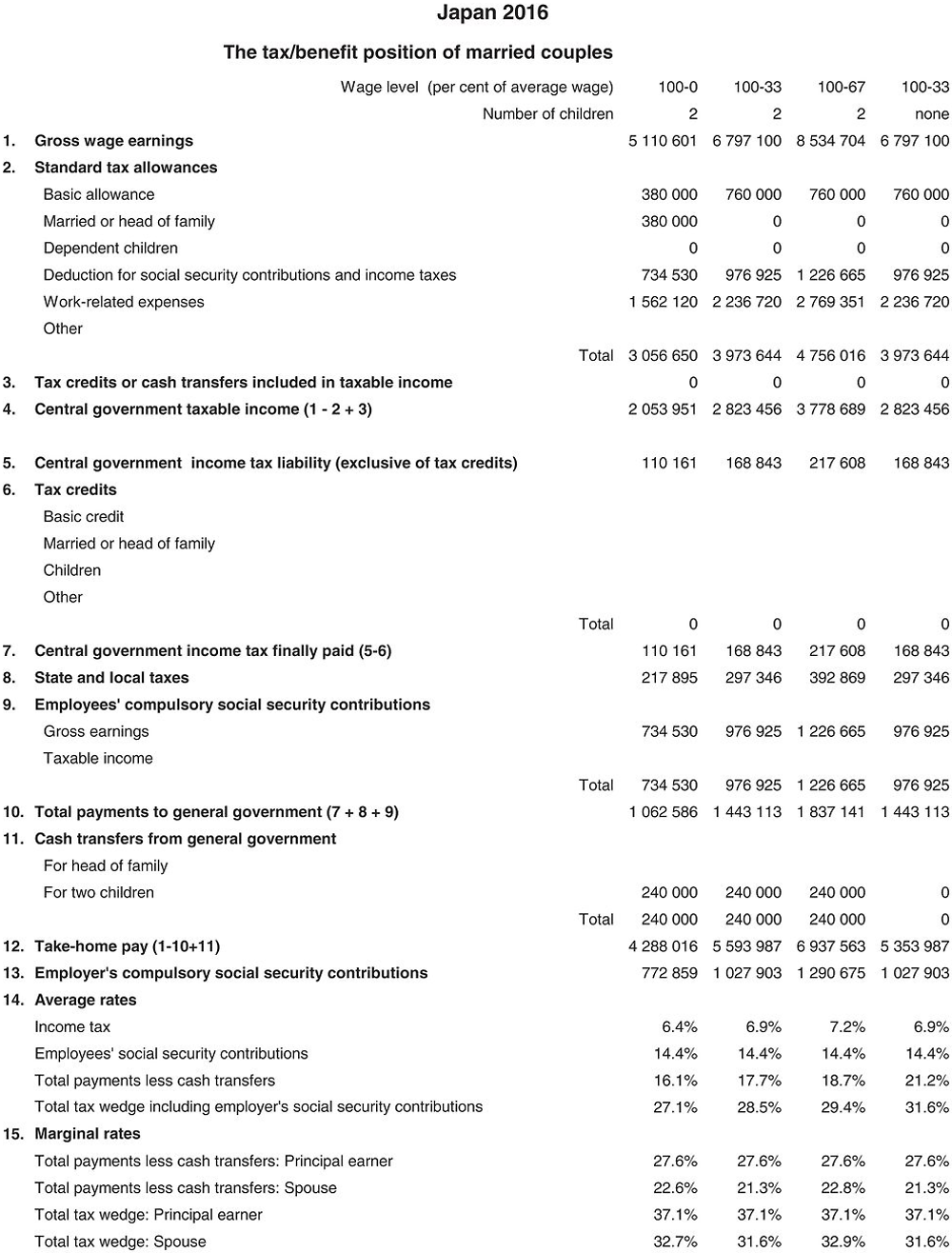

The national currency is the Yen (JPY). In 2016 JPY 108.80 was equal to USD 1. In that year, the average worker is assumed to earn JPY 5 110 601 (Secretariat estimate). In Japan, the central government income tax year is a calendar year and the local government income tax year is from April to March. The calculations in this report are based on the tax rules and rates, which are applicable the 1 April.

1. Personal income tax systems

1.1. Central government income tax

1.1.1. Tax unit

Each individual is taxed separately.

1.1.2. Allowances and tax credits

1.1.2.1. Standard reliefs

-

Basic allowance: a taxpayer may deduct JPY 380 000 as a basic allowance from his or her income.

-

Allowance for spouse: allowance equal to JPY 380 000 is given to a resident taxpayer who lives with a spouse whose income does not exceed JPY 380 000.

-

Special allowance for spouse: the allowance included in the following table is given to a resident taxpayer who lives with a spouse:

-

Allowance for dependents: if a resident taxpayer has children and other relatives over 15 years old whose income does not exceed JPY 380 000 and who live with the resident, an allowance of JPY 380 000 is given for each dependent.

-

Special allowance for dependents: if a resident taxpayer has dependents between 19 and 22 years old whose income does not exceed JPY 380 000 and who live with the resident, an allowance of JPY 630 000 is given for each dependent instead of the allowances for dependents mentioned above.

-

Deduction for social insurance premiums: the whole amount of social insurance premiums for a resident taxpayer or his/her dependents shall be deducted from his/her income.

-

Employment income deduction: the following amounts may be deducted from employment income in calculating salary income:

-

If gross employment income does not exceed JPY 1 800 000, the deduction is 40% of salaries (etc.), but the minimum amount deductible is JPY 650 000.

-

If gross employment income exceeds JPY 1 800 000, but not JPY 3 600 000, the deduction is JPY 180 000 plus 30% of salaries.

-

If gross employment income exceeds JPY 3 600 000, but not JPY 6 600 000, the deduction is JPY 540 000 plus 20% of salaries.

-

If gross employment income exceeds JPY 6 600 000, but not JPY 10 000 000, the deduction is JPY 1 200 000 plus 10% of salaries.

-

If gross employment income exceeds JPY 10 000 000, but not JPY 12 000 000, the deduction is JPY 1 700 000 plus 5% of salaries.

-

If gross employment income exceeds JPY 12 000 000, the deduction will be fixed at JPY 2 300 000.

-

1.1.2.2. Main non-standard tax reliefs applicable to an AW

-

Credit for housing loans: A resident taxpayer who constructs, purchases, enlarges or rebuilds a house and finances the cost by means of a housing loan and uses the property as his or her own dwelling is entitled to an income tax credit up to the amount described below for 10 years [or 15 years] after the first use of the house, provided that the floor space is not less than 50m2 and that at least half of the floor space is used as the owner-occupied dwelling. The base of the tax credit equals the balance of the housing loan debt amount, calculated at the end of each year, consisting of the loan obtained not only from private financial institutions but also from public institutions. This tax credit cannot be claimed by those whose total income is more than JPY 30 million.

The rates of the tax credits correspond to the year in which residence in the house commenced. The rates are as follows:

-

Deduction for life insurance premiums: If a resident taxpayer pays insurance premiums on life insurance contracts and the recipient of the insurance proceeds is the taxpayer, his/her spouse or other relatives living with him/her, the portion of these insurance premiums which does not exceed the maximum prescribed below, is deductible from ordinary income, retirement income or timber income.

-

In addition, if a resident taxpayer pays insurance premiums for a “qualified personal pension plan (insurance type)”, and the recipient of the pension payment is the taxpayer or his/her spouse under a specific condition, the portion of such premiums which does not exceed the maximum prescribed below, is deductible from ordinary income, retirement income, or timber income.

-

Furthermore, if a resident taxpayer pays insurance premiums on nursing and medical insurance contacts and the taxpayer receipts the nursing and medical proceeds caused by payments for medical expenses, the portion of such premiums which does not exceed the maximum prescribed below, is deductible from ordinary income, retirement income, or timber income.

-

For the insurance contracts made on or after 1 January 2012 the maximum deduction is JPY 120 000. A resident taxpayer can claim the deduction up to JPY 40 000 for life insurance premiums, personal pension plan premiums and nursing and medical insurance premiums respectively.

-

For the insurance contracts made on or before 31 December 2011, a resident taxpayer can claim the deduction up to JPY 50 000 for life insurance premiums, personal pension plan premiums respectively. Thus, a resident tax payer can claim the deduction up to JPY 100 000 in total.

-

Deduction for medical expenses: If a resident taxpayer pays bills for medical or dental care for himself/herself or for his/her spouse or other relatives living with him/her and the amount of such expenses (excluding those recovered by insurance) exceeds the lesser of JPY 100 000 or 5% of the total of his/her ordinary income, retirement income and timber income, the excess amount is deductible from his/her ordinary income, retirement income or timber income. The maximum deduction is JPY 2 million.

-

Deduction for earthquake insurance premiums: Earthquake insurance premiums up to JPY 50 000 can be deducted from income. Although the income deduction for casualty insurance premiums was basically abolished, the deduction for long-term casualty insurance premiums remains available if contracted before 31 December, 2006. The maximum deduction for long-term casualty insurance premiums is JPY 15 000. If an individual applies for both a deduction for earthquake insurance premiums and a deduction for long-term casualty premiums, the maximum deductible amount is JPY 50 000 in total.

1.1.3. Tax schedule

Tax liability is obtained by multiplying the taxable income by tax rate (A) and deducting the amount (B). For example, income tax due on taxable income of JPY 7 million is:

7 000 000 × 0.23 (A) - 636 000 (B) = JPY 974 000.

In addition, a taxpayer is required to file tax returns and make tax payments for additional 2.1% of the base income taxes from 2013 through 2037 (special income tax for reconstruction) annually together with the regular income tax of respective years.

1.2. Local taxes (personal inhabitant’s taxes)

1.2.1. General description of the system

Local taxes in Japan (personal inhabitant’s taxes) consist of prefectural inhabitant’s tax levied by prefectures and municipal inhabitant’s tax levied by cities, towns and villages. The prefectural inhabitant’s tax is collected together with the municipal inhabitant’s tax by cities, towns and villages.

1.2.2. Tax base

Basically, personal inhabitant’s taxes (prefectural and municipal inhabitant’s taxes) consist of two parts; one is proportional taxable income and the other is a fixed per capita amount. The taxable income of personal inhabitant’s taxes is computed on the basis of the previous year’s income. The main difference from state tax (income tax) is the amount of income reliefs. For example, the amount of Basic Allowance, Allowance for Spouse, Allowance for Dependants is JPY 330 000, and the amount of specified Allowance for dependants is JPY 450 000, etc. Allowance for Dependents is available for dependent relatives 16 years or older excluding the specified dependents. Specified Allowance for dependents is available for the specified dependent relatives (between 19 and 22 years old).

1.2.3. Tax rate

-

The standard fixed (annual) per-capita amount of Prefectural inhabitant’s tax is JPY 1 500;

-

The standard fixed (annual) per-capita amount of Municipal inhabitant’s tax is JPY 3 500;

-

The standard rate of the local taxes equals a proportional rate of 10% (Prefectural inhabitant’s tax: 4%, Municipal inhabitant’s tax: 6%).1

1.2.4. Tax rate selected for this study

State tax (income tax) rates as described above. The local tax (personal inhabitant’s taxes) rates chosen for the purpose of this Report represent the standard rate.

2. Compulsory social security contribution to schemes operated within the government sector

2.1. Employees’ contributions

2.1.1. Pension

8.914% (9.091% as from September 2016) of total remuneration (standard remuneration and bonuses). The insurable ceiling of the monthly amount of pensionable remuneration is JPY 620 000 and the insurable ceiling of the standard amount of bonus is JPY 1 500 000.

2.1.2. Sickness

As from April 2012 about 5.00%, (about 4.75% before March 2012), of total remuneration, (standard remuneration and bonuses). The insurable ceiling of the monthly amount of standard remuneration is JPY 1 390 000 and the insurable ceiling of the yearly amount of standard bonus is JPY 5 730 000.

2.1.3. Unemployment

0.4% of total remuneration for Commerce and industry in general except for Business of agriculture, forestry and fisheries, and the rice wine brewing business, and Construction business. It is 0.5% for those exceptions.

2.1.4-2.1.5. Work injury and family allowance

None.

2.2. Employers’ contributions

2.2.1. Pensions

8.914% (9.091% as from September 2016) of total remuneration (standard remuneration and bonuses). The insurable ceiling of the monthly amount of pensionable remuneration is JPY 620 000 and the insurable ceiling of the standard amount of bonus is JPY 1 500 000.

2.2.2. Sickness

As from April 2012, about 5.00% (about 4.75% before March 2012) of total remuneration. The insurable ceiling of the monthly amount of standard remuneration is JPY 1 390 000 and the insurable ceiling of the yearly amount of standard bonus is JPY 5 730 000.

2.2.3. Unemployment

0.7% of total remuneration for Commerce and industry in general except for Business of agriculture, forestry and fisheries, and the rice wine brewing business, and Construction business. It is 0.8% for Business of agriculture, forestry and fisheries, and the rice wine brewing business, and 0.9% for Construction business

2.2.4. Work injury

0.25% to 8.8% of total remuneration, the contribution rate depending on each industry’s accident rate over the last three years and other factors. There are twenty-nine rates for fifty-four industrial categories at present.

2.2.5. Family allowance

0.20% of total remuneration.

3. Universal cash transfers

3.1. Transfers related to marital status

Not available.

3.2. Transfers for dependent children

From April 2012 (Income caps are applied beginning from June 2012 payments):

-

For persons earning incomes below the income cap

JPY 15 000 (per month) is paid to parents/guardians for each child who is under 3 years old or for the third or subsequent child from 3 years old until he/she graduates from elementary school.

JPY 10 000 (per month) is paid to parents/guardians for each child who is for the first or second child from 3 years old until he/she graduates from elementary school or who is a junior high school student.

-

For persons earning incomes no less than the income cap

JPY 50 00 (per month) is paid to parents/guardians for each child until he/she graduates from junior high school as the Special Interim Allowances.

The income cap is set at JPY 6 220 000 (the principal’s gross earnings net of certain deductions, plus JPY 380 000 per dependent).

4. Main changes in the tax/benefit systems since 1998

As part of the Fiscal Year 1999 tax reform, the highest marginal rate of the personal income tax imposed by the central government was reduced from 50% to 37%. The top rate of the local inhabitant’s tax was reduced from 15% to 13%. A proportional tax reduction was granted with respect to the national income tax and the local inhabitant’s tax. The amount is equal to the lesser of 20% (local inhabitant’s tax: 15%) of the amount of tax before reduction or JPY 250 000 (local inhabitant’s tax: JPY 40 000).

As part of the FY 2005 tax reform, the rate of the reduction was reduced from 20% to 10% (local inhabitant’s tax: from 15% to 7.5%) and the ceiling was reduced from JPY 250 000 to JPY 125 000 (local inhabitant’s tax from JPY 40 000 to JPY 20 000) as from 2006 (local inhabitant’s tax: FY 2006). And as part of the FY 2006 tax reform, the reduction was abolished as from 2007 (local inhabitant’s tax: FY 2007).

As part of the FY 2006 tax reform, the progressive rate structure of national income tax was reformed into a 6 brackets structure with tax rates ranging from 5% to 40%, and the rate of local inhabitant’s tax became proportional at a rate of 10%.

As part of the FY 2012 tax reform, the upper limit on employment income deduction (JPY 2 450 000) was set for those who earn employment income more than JPY 15 000 000 as from 2013 (personal inhabitant’s tax: FY 2014).

As part of the FY 2013 tax reform, the tax rate of 45% was set for the income beyond JPY 40 000 000 from 2015. By this, the progressive rate structure of income tax was reformed into a 7 brackets structure

As part of the FY 2014 tax reform, the upper limit on employment income deduction was determined to be gradually reduced. In 2016 (as for personal inhabitant’s taxes, in 2017), the limit became JPY 2 300 000 in case salary income is more than JPY 12 000 000. And in 2017 (as for personal inhabitant’s taxes, in 2017), the limit will become JPY 2 200 000 in case salary income is more than JPY 10 000 000.

Eligible age for transfers for dependent children was raised from three to six as from 1 June 2001, from six to nine as from 1 April 2004 and from nine to twelve as from 1 April 2006. It has been doubled to JPY 10 000 for the first and second child under the age of three as from 1 April, 2007.

As from 2010, JPY 13 000 per month is paid to parents/guardians regardless of their income for each child until he/she graduates from junior high school.

As from April 2012 (Income caps are applied beginning from June 2012 payments):

-

For persons earning incomes below the income cap

JPY 15 000 (per month) is paid to parents/guardians for each child who is under 3 years old or for the third or subsequent child from 3 years old until he/she graduates from elementary school.

JPY 10 000 (per month) is paid to parents/guardians for each child who is for the first or second child from 3 years old until he/she graduates from elementary school or who is a junior high school student.

-

For persons earning incomes no less than the income cap

JPY 5 000 (per month) is paid to parents/guardians for each child until he/she graduates from junior high school as the Special Interim Allowances.

5. Memorandum item

5.1. Average gross annual wage earnings calculation

The source of calculation is the Basic Survey on Wage Structure, published by the Ministry of Health, Labour and Welfare. This survey covers establishments with ten or more regular employees over the whole country, and contains statistical figures for monthly contractual cash earnings in June and annual special cash earnings (such as bonuses) received by various categories of workers. Male and female workers of the manufacturing, mining and quarrying, construction, wholesale and retail trade, accommodation and food service activities, financial and insurance activities, real estate activities sector are the point of departure. Their gross annual earnings have been calculated by multiplying monthly contractual cash earnings by 12 and adding any annual special cash earnings. In the Basic Survey, sickness and unemployment compensations are excluded from cash earnings, but average overtime and bonuses are included.

As far as the Basic Survey is concerned, it covers the whole country, and no special assumption is made regarding the place of residence of the average worker.

5.2. Employer contributions to private pension and health schemes

DB: JPY 3 528 billion (2013)

Employees’ Pension Funds (EPFs): JPY 1 035 billion (2014)

DC: JPY 673 billion (2014)

Data of DB and EPFs are the total amount of employers’ contribution and employees’ one and there is no data of those which indicates only employers’ contribution. As from January 2012, matching contribution which enables employee to pay additional contribution to employer’s one became available. The amount of DC does not include the amount of matching contribution. It is regulated by law that employers’ contribution must be higher than employees’ one.

2016 tax equations

The equations for the Japanese system are mostly on an individual basis. But the tax allowances for the spouse and for children are relevant only to the calculation for the principal earner. This is shown by the Range indicator in the table below.

The functions which are used in the equations (Taper, MIN, Tax etc) are described in the technical note about tax equations. Variable names are defined in the table of parameters above, within the equations table, or are the standard variables “married” and “children”. A reference to a variable with the affix “_total” indicates the sum of the relevant variable values for the principal and spouse. And the affixes “_princ” and “_spouse” indicate the value for the principal and spouse, respectively. Equations for a single person are as shown for the principal, with “_spouse” values taken as 0.

← 1. The personal inhabitant’s taxes rate and the income tax rate were changed in the FY 2006 tax reform. Adjusted credit (tax credit regime )was introduced in order to alleviate the tax burden increase arising from the changes in the tax rates and from the difference between the personal reliefs (Basic Allowance, Allowance for Spouse, Allowance for Dependents, Special Allowance for dependents, etc.) for national income tax purposes and for inhabitant tax purposes.