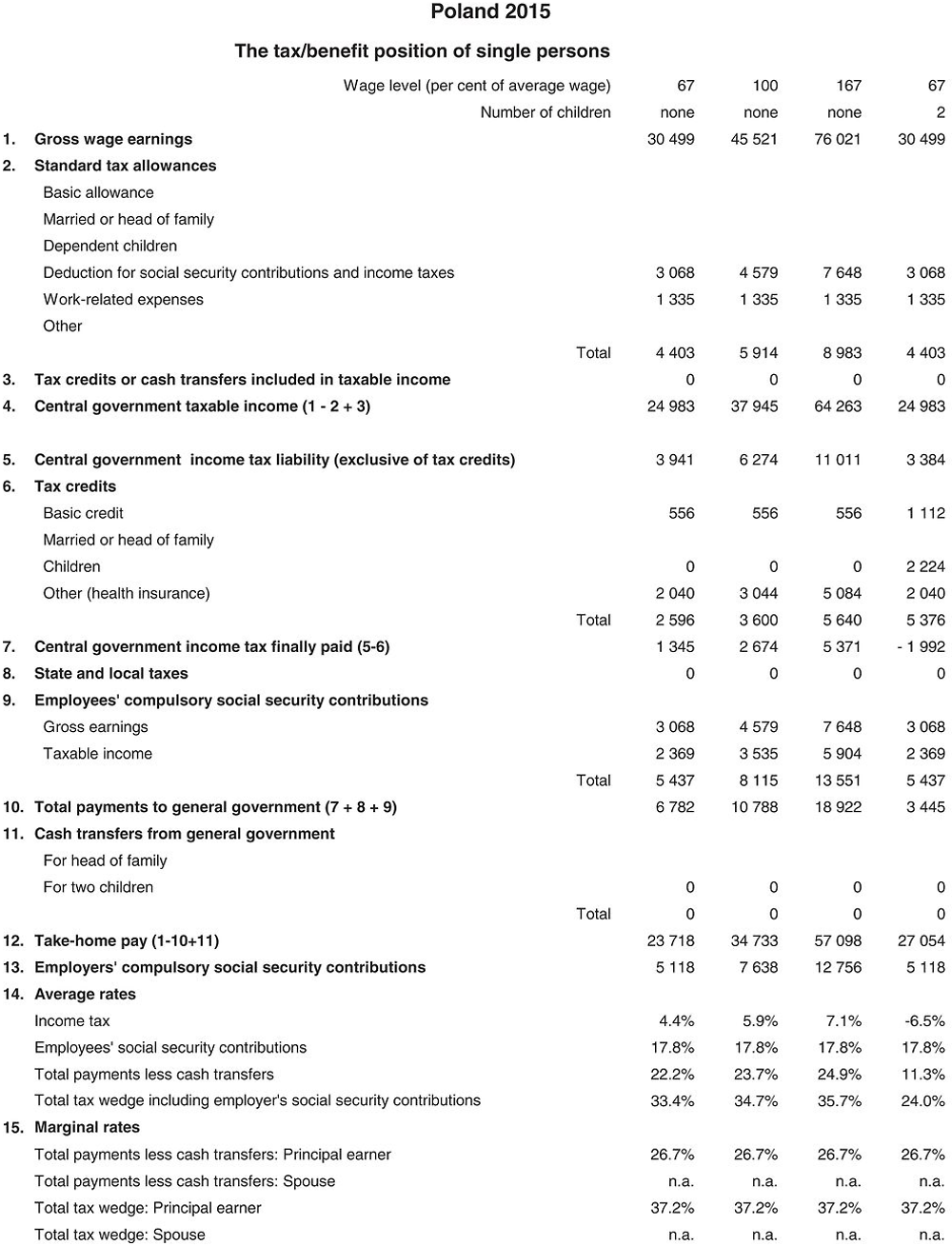

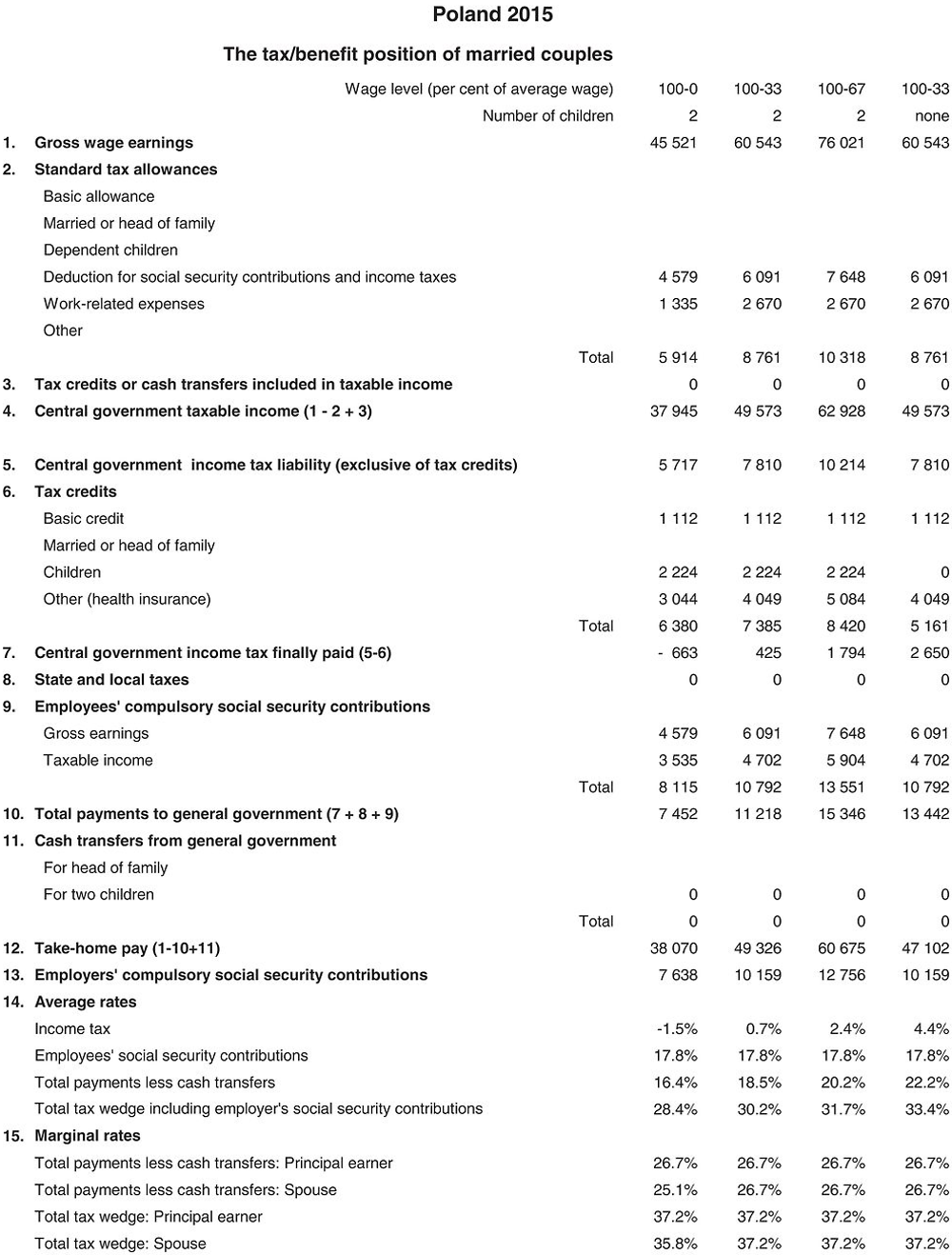

Poland

This chapter includes data on the income tax paid by workers, their social security contributions, the family benefits they receive in the form of cash transfers as well as the social security contributions and payroll taxes paid by their employers. Results reported include the marginal and average tax burden for eight different family types.

Methodological information is available for personal income tax systems, compulsory social security contributions to schemes operated within the government sector, universal cash transfers as well as recent changes in the tax/benefit system. The methodology also includes the parameter values and tax equations underlying the data.

The national currency is the Zloty (PLN). In 2015, PLN 3.77 was equal to USD 1. In that year, the average worker earned PLN 45 521 (Secretariat Estimate).

1. Personal income tax system

An individual being a tax resident in Poland is liable to tax on the basis of world-wide income, irrespective of the source and origin of that income. (The term ”residency” is understood similarly to Article 4 paragraph 2 point a) of the OECD Model Tax Convention on Income and Capital).

1.1. Central government income tax

1.1.1. Tax unit

Individuals are taxed on their own income, but couples married during the whole calendar year1 can opt to be taxed on their joint income. In the latter case, the ”splitting” system applies: the tax bill for a couple is twice the income tax due on half of joint income, provided the joint income does not include capital income taxed at the flat 19 per cent rate. Single individuals with dependent children are also entitled to use the splitting system (their family quotient is two). For the purpose of this report, it is assumed that married couples are taxed on joint income.

1.1.1.1. Tax base

For taxation purposes, taxable gross employment income in Poland includes both cash income and the value of benefits in kind. More specifically, gross employment income includes base salary, overtime payments, bonuses, awards, compensation for unused holidays, and costs that are paid in full or in part by the employer on behalf of the employee.

1.1.2. Tax allowances and tax credits

1.1.2.1. Standard reliefs

-

Basic relief: A non-refundable tax credit of PLN 556.02 per person.

-

Marital status relief: None.

-

Relief for children: Yes.2

A taxpayer can deduct from the due tax decreased by the amount of health contributions specified in the PIT Act, the amount, which is equal for each month of raising a child:

-

PLN -92.67 (annually PLN 1 112.04) for the first child, if the income received by parents (married or single parent, who meets special requirements) doesn’t exceed in the tax year the amount of PLN 112 000. For other parent the threshold of income is PLN 56 000;

-

PLN -92.67 (annually PLN 1 112.04) for the second child;

-

PLN -166.67 (annually PLN 2 000.04) for the third child;

-

PLN -225.00 (annually PLN 2 700.00) for the fourth and every next child.

-

Since 1st of January 2015 taxpayers whose due tax is lower than the amount of relief for children, may claim for cash refund for amount of relief which has not been utilized. However, such cash refund cannot exceed the amount of deductible social security and health insurance contributions paid by taxpayer (with some exceptions).

-

Relief for health insurance contributions: A tax credit is almost equal to health insurance contribution paid to the National Health Fund. The contribution is 9 per cent of the calculation basis whereas the tax credit is 7.75 per cent of this basis.

-

Relief for other social security contributions: An allowance is provided for all social insurance contributions paid by the taxpayer.

-

Relief for selected work-related expenses: Standard deductions depend on the number of workplaces and on whether place of residence and workplace are within the same town/city or not. The annual amounts in PLN (deductible from income) are:

1.1.2.2. Main non-standard tax reliefs applicable to an average worker

Allowances:

-

Expenses for the purpose of rehabilitation incurred by a taxpayer who is a disabled person, or a taxpayer, who supports the disabled;

-

Equivalent of blood donations, donations made for the purposes of public benefit activity and of religious practice – in the amount of donation, no more than 6 per cent of income;

-

Donations made for charity church care – in the amount of the donation;

-

Expenses incurred for the use of the Internet – a taxpayer is entitled to deduct the Internet tax allowance within the next two years, providing that during the phase preceded this period he did not deduct Internet for the use of the Internet (up to PLN 760);

-

Abolished allowance (since 2007 continued on the acquired right basis) for interests payments on mortgage loans raised no later than in 2006 on acquisition of housing property on the primary market – up to the amount of interests related to the part of loan not exceeding PLN 325 990 for investments finished in 2015.

Tax credits:

-

Donation made to public benefit organizations – up to 1 per cent of due tax.3

-

Abolished tax credits (continued on the acquired rights basis), i.e. expenses for saving with the aim of buying a house or flat, the amount of social contributions paid on income of an unemployed person hired by a taxpayer in order to take care of their children and/or house.

1.1.3. Tax schedule

The tax schedule is as follows:

A tax-free threshold of PLN 3 091 is applied in the income tax calculations.

1.2. State and local income tax

There are no regional or local income taxes.

1.3. Wealth tax

There is no wealth tax.

2. Social security contributions

2.1. Employees’ contributions

Employees pay 13.71 per cent of the gross wage. This contribution includes:

-

Pension insurance contribution – 9.76 per cent of the gross wage.4 3.65 percentage points of the pension contribution are treated as non-tax compulsory payments because these payments are either made to the OPF (1.46 per cent) and to personal sub-account in ZUS (2.19 per cent) or only to sub-account in ZUS (3.65 per cent).Disability insurance contribution – 1.5 per cent of the gross wage,

-

Sickness/maternity insurance contribution – 2.45 per cent of the gross wage,

-

In case of pension and disability insurance, contributions are not paid on the part of the wage that exceeds PLN 118 770.5

2.2. Employers’ contributions

In respect of income paid under an employment contract with a Polish entity, employers have an obligation to pay social security contributions equal to 20.43 per cent of gross wage. This value consists of:

-

9.76 percentage points are aimed for pension insurance.6 3.65 percentage points of the pension contribution are treated as non-tax compulsory payments because these payments are either made to the OPF (1.46 per cent) and to personal sub-account in ZUS (2.19 per cent) or only to sub-account in ZUS (3.65 per cent).-.

-

6.5 percentage points are aimed for disability insurance,

-

4.17 percentage points are aimed for other insurances i.e. 1.62 percentage points (on average) accident insurance, 2.45 percentage points for Labour Found and 0.1 percentage points for the Guaranteed Employee Benefit Fund.

-

In case of pension and disability insurance, contributions are not paid on the part of the wage that exceeds PLN 118 770.

3. Universal cash transfers

3.1. Transfers related to marital status

None.

3.2. Transfers for dependent children

From 1st of November 2012 families where the average monthly income per household member for the previous period is no greater than PLN 539 or PLN 623 when there are one or more disabled children in the household) are entitled to family allowances. From 1st of November 2014 the income criteria will be as high as PLN 574 and PLN 664. Families receive PLN 77 monthly for a child no older than 5 years, PLN 106 monthly for a child of 5 up to 18 years old, and PLN 115 monthly for a child of 18 up to 24 years old. The calculations in this Report are based on the assumption that the children are aged between 5 and 18 years.

Single parents are entitled to a supplement of PLN 170 for each child up to a maximum of PLN 340 for all children (and PLN 250 for a disabled child up to a maximum of PLN 500 for all children).

There are several supplements to family allowances:

-

for large families – PLN 80 monthly for the 3rd and next children in the family;

-

for education of disabled children – PLN 60 monthly for children not older than 5 years and PLN 80 for children older than 5 years.

4. Main changes in tax/benefit systems since 2012

There were no changes in taxation of wages. Tax schedule, work-related expenses, tax allowances, relieves are the same as in previous years.

There were only changes in Social Security Contribution. Since February 2014, 14.96% of the old-age insurance contribution (2.92 percentage points) are transferred by ZUS to a privately-managed fund (OPF) but since July 2014 this part of contribution will be transferred only if insured persons decides to – otherwise all 7.3 percentage points of the contributions will be passed to subaccount in ZUS.

5. Memorandum items

5.1. Identification of AW and valuation of earnings

The Polish Central Statistical Office calculates average monthly wages and salaries for employees on the basis of reports of enterprises. The figures include overtime and bonus payments and also include information for part-time employees converted to full-time equivalents. Male and female workers are included. The information, which includes estimates for different sectors, is published in the monthly Statistical Bulletin.

5.2. Employers’ contributions to private pension, health and related schemes

No information provided.

2015 tax equations

The equations for the Polish system are mostly calculated on a family basis.

The standard functions which are used in the equations (Taper, MIN, Tax etc) are described in the technical note about tax equations. Two additional functions (Tax93 and ftax) have been incorporated to carry out an iterative calculation for central government tax. These allow for the fact that the church tax is calculated as 9 per cent of Central Government tax and is also allowed as a deduction when calculating taxable income. Variable names are defined in the table of parameters above, within the equations table, or are the standard variables ”married” and ”children”. A reference to a variable with the affix ”_total” indicates the sum of the relevant variable values for the principal and spouse. And the affixes ”_princ” and ”_spouse” indicate the value for the principal and spouse, respectively. Equations for a single person are as shown for the principal, with ”_spouse” values taken as 0.

Notes

← 1. However, a widowed spouse is entitled to apply the join income taxation.

← 2. It concerns a child of 18 years old or younger or a child up to 25 years old provided they are students or a disabled child irrespective of their age. The actual description in indicateur 4.

← 3. This relief is distinct from an allowance for donations deducted from income.

← 4. Since July 2014 out of total 19.52% of social contributions 7.3% goes to subaccount in ZUS either – if voluntarily stated by insured person – 2.92% goes to account in open ended funds and 4.38% to subaccount in ZUS.

← 5. The contribution ceiling of pension and disability insurance funds for a given calendar year may not exceed thirty times the amount of the projected average monthly remuneration in the national economy for that year, as set forth in the Budgetary Act.

← 6. Since July 2014 out of total 19.52% of social contributions 7.3% goes to subaccount in ZUS either – if voluntarily stated by insured person – 2.92% goes to account in open ended funds and 4.38% to subaccount in ZUS.