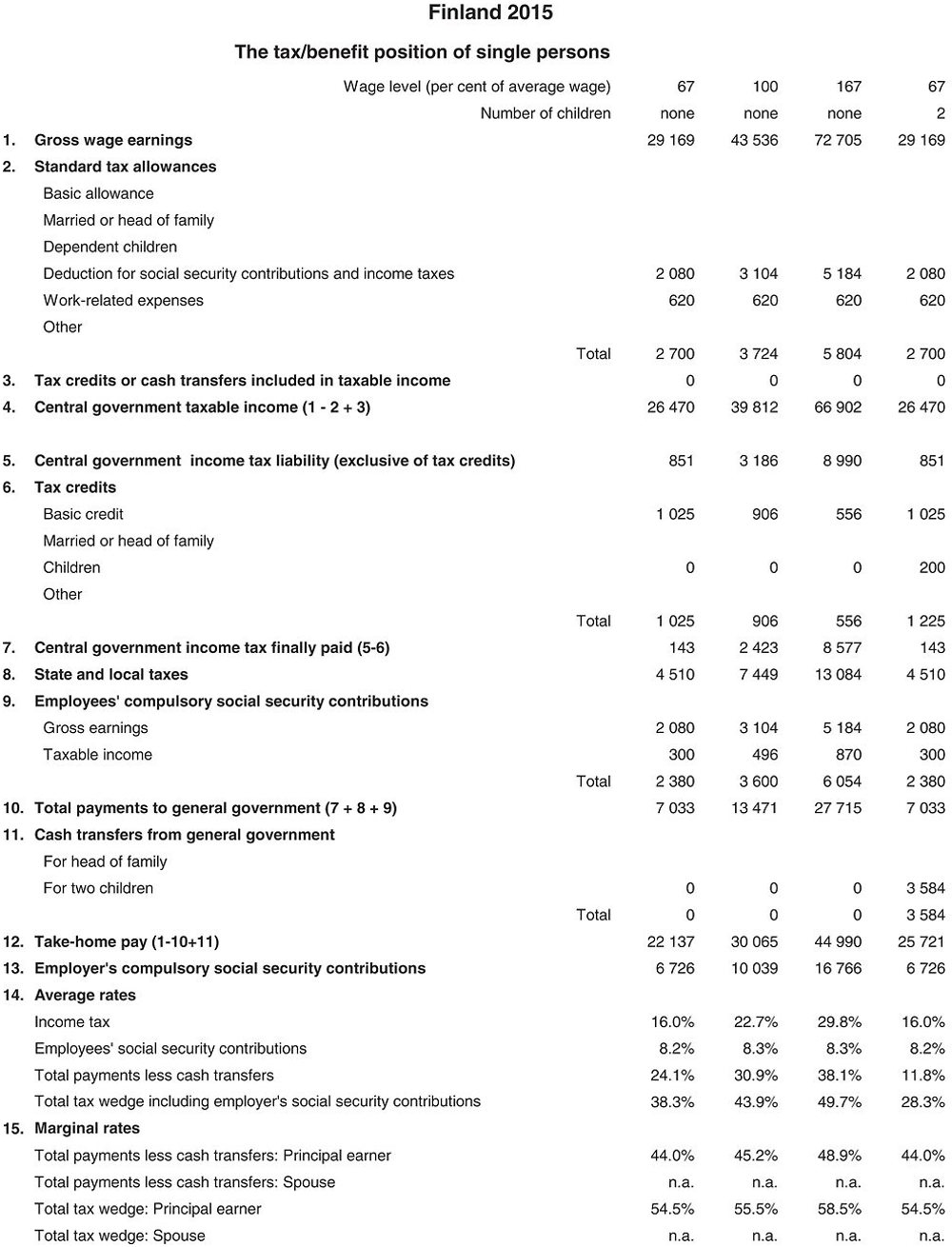

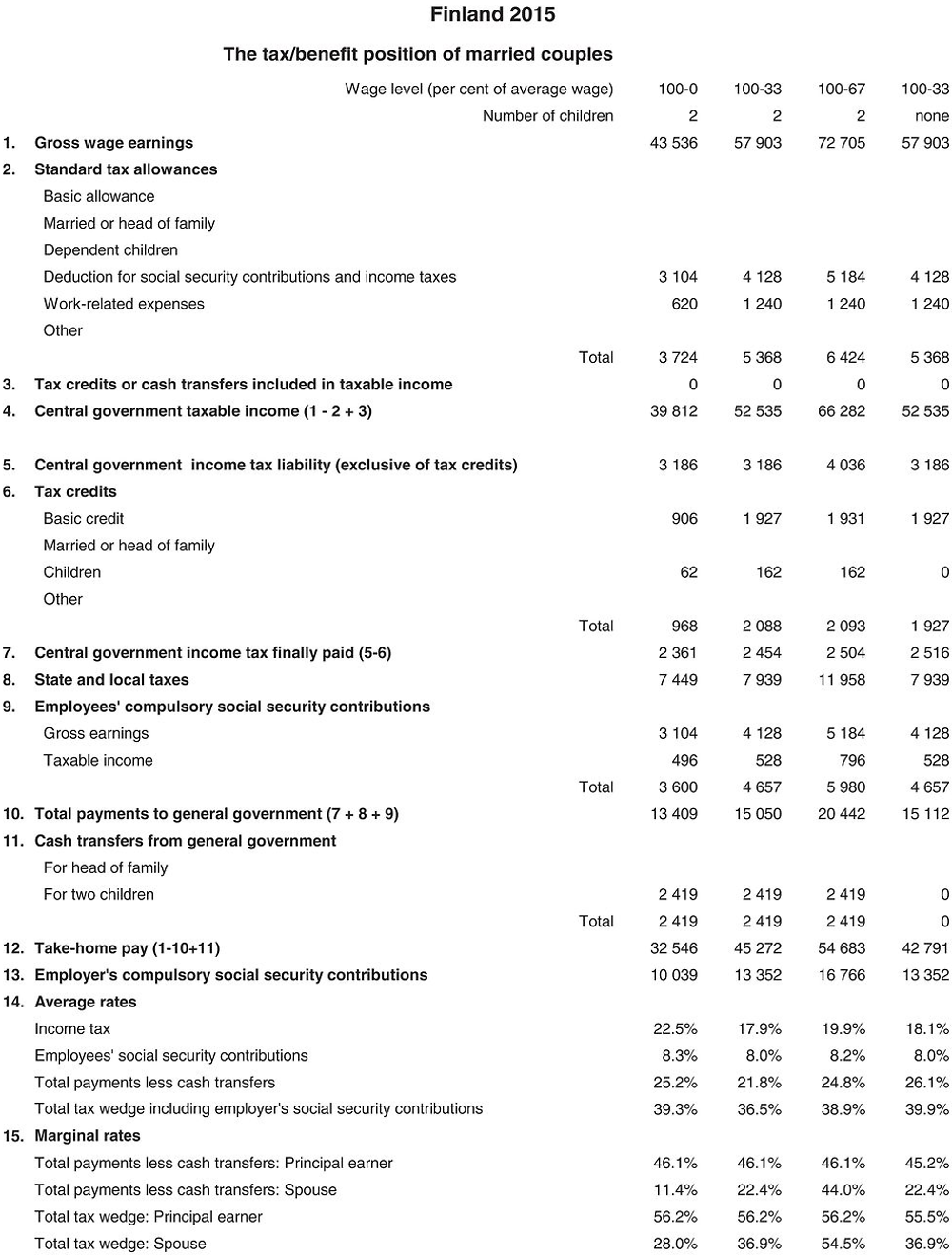

Chapter. Finland

This chapter includes data on the income taxes paid by workers, their social security contributions, the family benefits they receive in the form of cash transfers as well as the social security contributions and payroll taxes paid by their employers. Results reported include the marginal and average tax burden for eight different family types.

Methodological information is available for personal income tax systems, compulsory social security contributions to schemes operated within the government sector, universal cash transfers as well as recent changes in the tax/benefit system. The methodology also includes the parameter values and tax equations underlying the data.

The national currency is the Euro (EUR). In 2015, EUR 0.90 was equal to USD 1. In that year, the average worker earned EUR 43 536 (Secretariat estimate).

1. Personal income tax system

1.1. Central government income taxes

1.1.1. Tax unit

Spouses are taxed separately for earned income.

1.1.2. Standard tax allowances and tax credits

1.1.2.1. Standard reliefs

-

Work-related expenses: A standard deduction for work-related expenses equal to the amount of wage or salary, with a maximum amount of EUR 620 is granted.

-

Tax credit: An earned income tax credit is granted against the central government income tax. If the credit exceeds the amount of central government income tax, the excess credit is deductible from the municipal income tax and the health insurance contribution for medical care. The credit is calculated on the basis of taxpayers’ income from work. The credit amounts to 8.6% of income exceeding EUR 2 500, until it reaches its maximum of EUR 1 025. The amount of the credit is reduced by 1.2% of the earned income minus work related expenses exceeding EUR 33 000. The credit is fully phased out when taxpayers’ income is about EUR 119 000.

-

Child tax credit: The credit is granted to taxpayers who have children in their care and custody according to the Population Register System records. It is given for four children at most. All parents and custodians get it regardless of which one of them has the child(ren) living with them. The size of the child tax credit depends on the number of children and whether the taxpayer has joint custody or single custody: for joint custody the credit is EUR 50 per year and child, and for single custody it is EUR 100 per year and child. If net taxable income exceeds EUR 36 000 per year (earned income and capital income combined), the credit is reduced. For the part of the income exceeding the threshold, the amount to be credited is phased out by a one percentage point rate. The child tax credit is will be in force from 2015 through 2017.

1.1.2.2. Main non-standard tax reliefs applicable to an AW

-

Interest: Interest on loans associated with the earning of taxable income, 65% of the interest on loans for the purchase of owner-occupied dwellings, and student loans guaranteed by the state can be deducted against capital income. Of the excess of interest over capital income, 30% (32% for first-time homebuyers) can be credited against income tax up to a maximum of EUR 1 400.

-

Membership fees: Membership fees paid to employees’ organisations or trade unions.

-

Travelling expenses: Travelling expenses from the place of residence to the place of employment using the cheapest means in excess of EUR 750 up to a maximum deduction of EUR 7 000.

-

Double housing expenses: If the place of employment is located too far from home in order to commute (distance > 100 km), the taxpayer can deduct the costs of hiring a second dwelling located near the place of work up to EUR 250 per month. This deduction can be claimed only by one person per household.

-

Other work-related outlays: Outlays for tools, professional literature, research equipment and scientific literature, and expenses incurred in scientific or artistic work (unless compensated by scholarships).

Travelling expenses and other work-related outlays are deductible only to the extent that their total amount exceeds the amount of the standard deduction for work-related expenses.

1.1.3. Rate schedule

Central government income tax:

1.2. Local income tax

1.2.1. Tax base and tax rates

The tax base of the local income tax is taxable income as established for the income tax levied by central government.

Municipal tax is levied at flat rates. In 2015 the tax rate varies between 16.50 and 22.50%, the average rate being approximately 19.84%.

Municipal tax is not deductible against central government taxes. Work-related expenses and other non-standard deductions are deductible, as for purposes of the central government income tax.

1.2.2. Tax allowances in municipal income taxation

-

An earned income tax allowance is calculated on the basis of taxpayer’s income from work. The allowance amounts to 51% of income between EUR 2 500 and EUR 7 230 and 28% of the income exceeding EUR 7 230, until it reaches its maximum of EUR 3 570. The amount of the allowance is reduced by 4.5% on earned income minus work related expenses exceeding EUR 14 000.

-

A basic tax allowance is granted on the basis of taxable income remaining after the other allowances have been subtracted. The maximum amount, EUR 2 970, is reduced by 18% on income exceeding the aforementioned amount.

2. Compulsory social security contributions to schemes operated within the government sector

2.1. Employee contributions

2.1.1. Rate and ceiling

In 2015, the rate of the health insurance contribution for medical care paid by an employee is 1.32%. The tax base for this contribution is net taxable income for municipal income tax purposes.

In addition there is an employees’ pension insurance contribution which amounts to 5.70% of gross salary, an employees’ unemployment insurance contribution equal to 0.65% of gross salary and a health insurance contribution for daily allowance equal to 0.78% of gross salary. For employees aged 53 and older, the pension insurance contribution amounts to 7.30% of gross salary. These contributions are deductible for income tax purposes.

2.1.2. Distinction by marital status or sex

The rates do not differ.

2.2. Employers’ contributions

The average rate of the employers’ social security contribution in 2015 is 23.06% of gross wage.

3. Universal cash transfers

3.1. Amount for marriage

None.

3.2. Amount for children

The central government pays in 2015 the following allowances (EUR):

The child subsidy for a single parent is increased by an annual amount of EUR 582.6 for each child.

4. Main changes in the tax/benefit system since 2014

As a means to compensate low to middle income earners for a 8% cut in child benefits a temporary (2015-17) child tax credit was introduced. The credit is granted to taxpayers who have children in their care and custody. It is given for four children at most. For joint custody parents the credit is 50 EUR per year and child, and for single custody parents it is 100 EUR per year and child.

Adjustments for inflation and rise of earnings levels were, with exception of the two top brackets, made to the central government tax scale in 2015.

In 2014 the public broadcasting tax is 0.68% on taxable earned income, taxes of min. EUR 51 and max. EUR 143 will be collected.

The maximum amount of the earned income tax credit in state taxation was raised from EUR 1 010 to EUR 1 025.

The maximum amount of the basic allowance in municipal taxation was raised from EUR 2 930 to EUR 2 970.

Home-loan interest counts at 65%, down from 75%, as deductible/creditable interest.

5. Memorandum items

5.1. Calculation of average gross annual wage

The Finnish figures are generally calculated as follows:

-

Gross annual earnings are calculated at an individual level on the basis of the hour’s usually worked, average hourly pay for the fourth quarter, and the share of annual periodic bonuses.

-

The earnings exclude sickness and unemployment compensations, but include all normal overtime compensations, bonuses, holiday remunerations and remunerations for public holidays.

5.2. Employer contributions to private pension and health schemes

No information is available.

2015 tax equations

The equations for the Finnish system are mostly on an individual basis except for the child benefit which is calculated only once. This is shown by the Range indicator in the table below.

The functions which are used in the equations (Taper, MIN, Tax etc) are described in the technical note about tax equations.

Variable names are defined in the table of parameters above, within the equations table, or are the standard variables ”married” and ”children”. A reference to a variable with the affix ”_total” indicates the sum of the relevant variable values for the principal and spouse. And the affixes ”_princ” and ”_spouse” indicate the value for the principal and spouse, respectively. Equations for a single person are as shown for the principal, with ”_spouse” values taken as 0.