4. Monopoly’s neglected twin? The effect of labour market concentration on wages and inequality

High labour market concentration (i.e. the concentration of employment or hiring in a small number of firms) may allow employers to suppress wages. This chapter uses linked employer-employee data from seven OECD countries to analyse the extent of labour market concentration across countries, industries, geographical areas and groups of workers, as well as its effects on wages. The main findings are: (1) a significant share of workers (around 20%) are employed in highly-concentrated labour markets, especially in manufacturing and rural areas; (2) high labour market concentration reduces wages; (3) negative wage effects tend to be particularly pronounced for low-qualified workers; and (4) over the past two decades, negative wage effects have become stronger at any given level of concentration, but concentration itself has remained broadly flat. These results imply that labour market concentration is a relevant issue from the perspective of public policies aiming to address inequality but cannot explain broader economic trends related to wage stagnation and the decline in the labour income share experienced by a number of countries over the past two decades.1

This chapter analyses the links between labour market concentration (i.e. the extent to which employment or hiring is concentrated in a small number of firms), wage growth and inequality across seven OECD countries. The main findings are as follows:

On average across the seven countries covered in this chapter, around 20% of workers are exposed to high levels of local labour market concentration (defined at the disaggregated industry-by-region level).

The Hirschman-Herfindahl Index is above 2500 (a commonly used threshold for high concentration) in 55% of local labour markets, employing around 20% of workers.

The share of workers exposed to high concentration is twice as high in rural areas (around 30%) than in urban ones (around 15%).

A significantly higher share of workers faces high concentration in manufacturing (around 40%) than in services (15%). This pattern holds both within rural and urban areas.

Low-qualified workers face higher concentration than medium and high-qualified workers.

On average across countries, local labour market concentration has tended to slightly decline over the period 2003-2017, contrasting with the increase in product market concentration over the same period.

The decline has been more pronounced in services than manufacturing, where local labour market concentration has remained broadly flat.

Trends in local and national labour market concentration have been similar, but national employment concentration has decoupled from national sales concentration, especially in services.

Local labour market concentration has a significant negative impact on wages.

All else equal, a worker in a highly-concentrated local labour market (90th percentile of the employment-weighted distribution) faces a wage penalty of 7% relative to a similar worker in a market with low concentration (10th percentile).

The impact of a given level of labour market concentration tends to be significantly more negative for low-qualified workers than for high-qualified ones. Given that low-skilled workers are also exposed to higher levels of concentration, they face a wage penalty of around 6% relative to high-skilled workers.

The impact of labour market concentration has tended to become more negative over time, potentially indicating a weakening in workers’ bargaining position.

Overall, the results in this chapter suggest that labour market concentration has not been a major determinant of aggregate wage growth and the share of labour income in national income over the past 20 years. However, labour market concentration is a significant issue for around 20% of the workforce, especially low-qualified workers and workers in manufacturing and rural areas, thereby contributing to aggregate wage inequality. Public policies in the following areas could play a useful role to mitigate employers’ wage-setting power:

Labour market policies and institutions: Reducing the costs of job search and mobility for workers would reduce effective labour market concentration at any given level of concentration by expanding workers’ outside job options. In principle, wage-setting institutions in the form of minimum wages and collectively-negotiated wage floors could help to contain the wage-setting power of firms in labour markets with limited job mobility.

Product market policies: Excessive concentration in some segments of the labour market could be addressed by explicitly integrating labour market power considerations into competition policy, including into merger reviews. Competition authorities may also step up enforcement efforts against anti-competitive agreements in labour markets, including wage-fixing, no-poaching agreements and non-compete covenants, especially for low-qualified workers. Promoting market entry of firms through well-designed entrepreneurship policies may not only raise output and employment but also boost wages and reduce inequality.

Large companies with monopoly power can boost their profits by imposing high prices on consumers. But large companies may also be able to suppress wages if workers have few alternative employment options within reasonable commuting distance, i.e. if local employment is highly concentrated. The resulting redistribution of income from workers to company owners hurts workers and reduces overall economic efficiency, as companies paying low wages generally employ fewer workers and curtail output. In many OECD countries, industry sales have become more concentrated (Bajgar et al., 2019[1]) while the share of wages in total income has declined (Autor et al., 2017[2]; Schwellnus et al., 2018[3]), raising the question whether increased sales concentration has gone together with increased labour market concentration and wage-setting power.

This chapter analyses the links between labour market concentration, wages and inequality. The analysis is based on linked employer-employee data from seven OECD countries for which relevant and comparable measures of labour market concentration can be constructed.2 The main focus is on labour market concentration at the level of detailed industries and regions. The paper presents comparable descriptive evidence on the degree of local labour market concentration across industry groups (manufacturing and services), geographical areas (rural and urban areas) and worker groups (low- and high-qualified workers), as well as its changes over time. It further presents econometric evidence on the causal effect of labour market concentration on wages, distinguishing between low- and high-qualified workers and testing whether the wage effects have changed over time.

A growing literature studies wage-setting power in single-country contexts, but comparable estimates of wage-setting power and its implications for wage growth and wage inequality across OECD countries are still missing. One strand of the literature analyses concentration in local labour markets and its relation to wages in the United States (Rinz, 2020[4]; Benmelech, Bergman and Kim, 2020[5]), France (Marinescu, Ouss and Pape, 2020[6]), the United Kingdom (Abel, Tenreyro and Thwaites, 2018[7]), Austria (Jarosch, Nimczik and Sorkin, 2019[8]), and Portugal (Martins, 2018[9]).3 Some recent studies have pointed to the key role of job mobility in shaping workers’ outside options and thus the relationship between concentration and wages (Caldwell and Danieli, 2018[10]; Jarosch, Nimczik and Sorkin, 2019[8]; Schubert, Stansbury and Taska, 2020[11]; Berger, Herkenhoff and Mongey, 2019[12]).A limitation of these studies is the lack of a unified definition of local labour markets and concentration measures, which limits cross-country comparability.4 A second strand of literature attempts to estimate the labour supply elasticity to the individual firm, a key theoretical determinant of wage-setting power (Sokolova and Sorensen, 2020[13]; Manning, 2011[14]; Bassier, Dube and Naidu, 2021[15]). While most empirical estimates of the labour supply elasticity to the individual firm suggest significant potential wage-setting power, the extent to which firms actually exercise it has not yet been clearly established (Manning, 2020[16]).

This chapter makes three main contributions. First, it analyses developments in labour market concentration since the early 2000s from a cross-country perspective, drawing on comprehensive administrative data. The data treatment and the definitions of wages and local labour market concentration are harmonised across countries as much as possible, improving comparability. Second, the chapter provides econometric estimates of the impact of labour market concentration on wages based on instrumental variable techniques, holding constant a large number of potential confounding factors, including unobserved productivity differences between local labour markets. Third, the chapter puts the analysis of labour market concentration into the broader context of firms’ wage-setting power (by providing estimates of the labour supply elasticity to the individual firm) and recent trends in product markets (by providing evidence on the links between sales and employment concentration).

The main results of the chapter are as follows. On average across the covered countries, around 20% of the workforce is employed in highly concentrated local labour markets, with the share being even higher for rural and manufacturing workers. The consequent reduction in workers’ job options puts significant downward pressure on wages, especially those of low-qualified workers, thus raising overall wage inequality. However, local labour market concentration has tended to slightly decline over the period 2003-17 despite rising sales concentration. These results imply that labour market concentration is a relevant issue from the perspective of public policies aiming to address inequality but cannot explain broader economic trends related to wage stagnation and the decline in the labour income share experienced by number of countries over the past two decades.

Wage-setting institutions such as minimum wages and collective bargaining can counter-balance negative wage effects from labour market concentration, and integrating labour market power considerations into merger control can prevent firms from reaching dominant positions in the first place. In many cases, reforming policy settings in product and labour markets that limit competition would curb market income inequality while at the same time raising economic growth and employment. For instance, reducing regulatory barriers to worker mobility (such as professional licencing or non-compete clauses) and business dynamism (such as regulatory obstacles to firm entry and growth) would raise workers’ wages relative to productivity while allowing high-performing firms to expand more easily.

The next Section describes a conceptual framework linking public policies, wage-setting power and wages. Section 4.3 describes the linked employer-employee data used in the empirical analysis, as well as the methodology used to construct the measures of labour market concentration used in the descriptive and econometric analysis. Section 4.4 reports the descriptive evidence on labour market concentration across countries, industries, geographical areas and worker groups and over time. Section 4.5 presents the econometric results on the effects of labour market concentration on wages across worker groups and over time. Section 4.6 concludes and discusses the implications of the analysis for public policy.

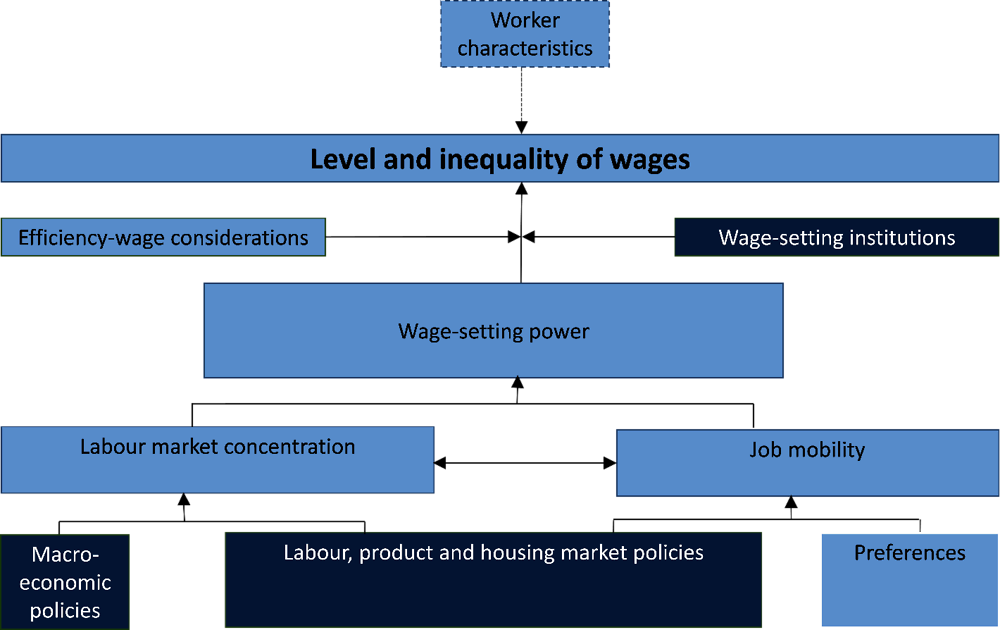

Workers’ wages are determined by their individual characteristics, such as qualifications, experience and gender, but also by the degree of firms’ wage-setting power (Figure 4.1). Wage-setting power arises when workers have only limited job options due to a lack of available jobs in their relevant labour market and/or when there is limited labour mobility. A lack of available jobs may arise when hiring is concentrated among a small number of potential employers, or potential employers post few vacancies relative to the number of job seekers, for example during economic downturns. Even when there is no lack of job vacancies, workers may nonetheless have little options outside their current job if there is low job mobility. Job mobility may be limited for different reasons, e.g. because workers incur monetary costs (including search costs related to gathering information on job opportunities and their suitability) or due to preference-related non-monetary costs from moving to a different firm, occupation, industry or region. Firms with wage-setting power can afford paying workers lower wages than other firms because only a fraction of its workers would quit to take up higher-paying jobs. This reduces average wages and can contribute to wage inequality.

While limited job availability and/or labour market frictions give employers the power to set wages, they may choose or be legally constrained not to exercise it. For instance, firms may anticipate that employees perceive low wages as unfair and that they may consequently cut back on effort. This would reduce the firm’s output and limit the gains from paying lower wages. In other words, the firm may not fully exercise its wage-setting power out of efficiency-wage considerations (Akerlof and Yellen, 1990[17]). Even if setting wages below workers’ (marginal) productivity is optimal from the firm’s point of view, institutional constraints such as minimum wages or collectively-agreed wage floors may prevent it from doing so (Azar et al., 2019[18]).5 The measurement of wage-setting power thus faces the challenge of distinguishing between firms’ potential to set wages below marginal productivity and the extent to which they actually use it.

The literature has traditionally measured wage-setting power by the labour supply elasticity to the individual firm. The rationale is that firms ultimately derive their wage-setting power from the fact that workers do not switch jobs in response to small wage differentials between firms. The labour supply elasticity encompasses both wage-setting power deriving from a limited number of employers in a given labour market (“classical monopsony”) and from frictions in labour markets related to search and hiring costs (“modern monopsony”) (Manning, 2020[16]). When there is a large number of effectively available employers, i.e. employment is not concentrated among a small number of firms and frictions are low, the labour supply elasticity is expected to be high, theoretically approaching infinity in the case of a perfectly-competitive labour market without frictions. By contrast, a much smaller labour supply elasticity is expected when there is only a small number of effectively available employers, indicating the presence of wage-setting power. On average across countries where data to estimate the labour supply elasticity are available, its estimated value is around 2, which is consistent with estimates from previous studies (Sokolova and Sorensen, 2020[13]) and implies significant wage-setting power (Annex Figure 4.B.1). However, estimates of the labour supply elasticity to the individual firm may be affected by significant measurement and endogeneity issues.

Complementing the traditional approach based on the labour supply elasticity, an emerging literature has approximated firms’ wage-setting power by local labour market concentration (Schubert, Stansbury and Taska, 2020[11]; Azar et al., 2020[19]; Marinescu, Ouss and Pape, 2020[6]; Rinz, 2020[4]). Unlike the labour supply elasticity, labour market concentration is a partial measure of wage-setting power that does not account for search and hiring frictions. However, it can be directly observed in the data and allows analysing whether wage-setting power is actually exercised by employers by relating concentration to wages at the local labour market level, which is infeasible using the labour supply elasticity.6 The remainder of the chapter therefore focuses on local labour market concentration.

4.3.1. Methodology

Measuring labour market concentration

In contrast to product market concentration, which is often measured at the national level, labour market concentration is typically measured at the local level (Rinz, 2020[4]). Adding the geographical dimension accounts for the fact that there are large barriers to worker mobility across regions, with workers typically searching for new jobs in a local area within commuting distance from their home (Manning and Petrongolo, 2017[20]). By contrast, competition in product markets often takes place at the national or international levels. Indeed, in most OECD countries even local services (e.g. physical retail; hotels and restaurants) are often provided by national and multinational chains.7

The definition of a local labour market is too narrow if many workers can find alternative employment in another labour market (i.e. there is a high degree of worker mobility across local labour market boundaries), whereas it is too broad if many jobs within the local labour market are actually not accessible to workers. Ideally, boundaries of local labour markets are defined such that most jobs inside the same market are available to all workers in the market, while worker flows across markets are minimal (Nimczik, 2020[21]). Most of the literature has defined the relevant labour market at the level of occupation by commuting zone (Martins, 2018[9]; Marinescu, Ouss and Pape, 2020[6]; Schubert, Stansbury and Taska, 2020[11]) – the rationale being that there are fewer barriers to job mobility within occupations and within commuting zones. Another common definition of the local labour market is at the level of industries by commuting zones (Benmelech, Bergman and Kim, 2020[5]; Rinz, 2020[4]), reflecting the fact that worker mobility is typically much higher within industries than between them.8

The preferred definition of the local labour market used in this chapter is at the level of 3-digit industries (around 230) and TL3 regions (generally comparable to French départements or Spanish provincias). TL3 regions overlap with commuting zones but do not always coincide with them. The chosen definition of the local labour market represents a compromise between country coverage and a sufficiently narrow definition of local labour markets (Box 4.1). The main measure of local labour market concentration used in the analysis is the Herfindahl-Hirschman-Index (HHI).9 The HHI can take values between 0 (when a large number of small firms accounts for very small shares of total hiring) and 10,000 (in the extreme case when a single firm dominates the entire market). Larger values thus indicate higher levels of concentration, with values above 2500 typically considered as indicating high concentration (Marinescu and Hovenkamp, 2019[22]; OECD, 2020[23]; OECD, 2019[24]).10

While job-to-job mobility is systematically higher within industries than between them, a disadvantage of focusing on industries rather than occupations is that the local labour market definition may be too broad, since workers might not have the required specialised skills or experience to access all occupations within an industry. For instance, not all jobs within a local manufacturing industry may be equally relevant for a machine operator and an engineer.

By contrast, local labour market definitions based on occupation may be too narrow, since relevant outside job opportunities can also arise outside a worker’s current occupation. For instance, promotions often imply a change of occupational code but may nonetheless be available to workers at a lower level in the occupational hierarchy.

Ultimately, the quality of approximation of labour market boundaries by occupations or industries is an empirical question. Mobility within industries as a share of total job-to-job mobility is broadly similar to mobility within occupations, suggesting that industry and occupation-based definitions of local labour market concentration yield broadly similar approximations.1 Moreover, for some occupations, industry and occupation-based definitions would yield very similar local labour markets (e.g. medical staff or teachers).

In terms of the geographical dimension, TL3 regions overlap with commuting zones but do not always coincide with them. However, working with TL3 regions has advantages especially for cross-country comparisons, as they are based on an internationally harmonised territorial grid. Given that TL3 regions generally correspond to lower-level national administrative boundaries (or groups thereof), they are available in most linked employer-employee datasets. Forming geographical boundaries along TL3 regions also has the advantage of allowing comparisons with the literature, which draws on region boundaries at similar levels.2

The analysis in this chapter mainly focuses on hiring concentration rather than employment concentration. Concentration in new hires (defined as workers who were not employed by the firm in the previous year) accurately reflects workers’ current job options and bargaining position. By contrast, concentration in employment largely reflects past job options given that only a small minority of workers switch jobs every year, especially in relatively rigid labour markets (Marinescu, Ouss and Pape, 2020[6]).

Various alternative measures or extensions of the preferred definition of local labour market concentration are reported. This includes employment rather than hiring-based local labour market concentration and an alternative definition of the local labour market at the coarser 2-digit industry level but that allows concentration to vary by qualification level.3

← 1. On average across the countries covered in this chapter, the rate of job switchers who remain within their industry is around 30% and the rate of those who remain within their occupation around 40%. Bassanini (2022[25]) use detailed occupations to define local labour markets and obtain similar estimates for the effect of labour market concentration on wages as the ones obtained in this chapter.

← 2. For example, Rinz (2020[4]) uses commuting zones with an average population of 450,000 for the United States. Martins (2018) uses districts with an average population of 340,000 for Portugal, which roughly correspond to TL3 regions.

← 3. Managers, Professionals, Technicians and Associate Professionals are mapped to high-skilled; Clerical Support Workers, Services and Sales Workers, Skilled Agricultural, Forestry and Fishery Workers, Craft and Related Trades Workers, Plant and Machine Operators, and Assemblers are classified as middle-skilled; and elementary occupations are mapped to low skilled.

Estimating the effect of labour market concentration on wages

In order to analyse the degree to which firms exercise their potential wage-setting power, wages are related to local labour market concentration based on the following equation:11

where w denotes wages; HHI the Herfindahl-Hirschman index of local labour market concentration; and the error term. Subscripts i, j, m and t denote, respectively, workers, firms, local labour markets and years; and year fixed effects. Worker fixed effects control for all time-invariant, individual determinants of wages, both observable and unobservable. This ensures that the estimated can be interpreted as the effect of concentration on the wages of similar workers. It further removes any potential endogeneity arising from a correlation between worker characteristics and concentration, such as a higher prevalence of low-qualified workers in highly concentrated regions and industries.12

Another econometric concern that needs to be addressed is the possible spurious correlation between concentration and wages at the level of local labour markets. For example, urban areas might attract a larger number of firms – leading to lower concentration – and may at the same time be more productive, for instance due to agglomeration effects (Glaeser, 2010[26]). The inclusion of local labour market fixed effects allows controlling for time-invariant omitted factors that may be correlated with both wages and concentration at the local labour market level. In other words, labour market fixed effects allow isolating the pure market power effect of labour market concentration from the effect of other factors that may be correlated with concentration and also affect wages, such as average productivity or average firm size in the local labour market.

By construction, the inclusion of local labour market fixed effects cannot address endogeneity issues related to time-varying omitted factors, such as productivity shocks (rather than productivity levels) that may be correlated with both concentration and wages at the local labour market level. For instance, an unobserved positive productivity shock in a local labour market may lead to market entry of new firms, reduce concentration and raise wages. This would bias the estimated coefficient on local labour market concentration down, leading to an estimated coefficient that is more negative than the true wage effect of concentration and thus overstating the effect of concentration on wages.

The potential bias from unobserved productivity shocks is addressed by using an instrumental variable for local labour market concentration. Following seminal studies in the academic literature (Martins, 2018[9]; Marinescu, Ouss and Pape, 2020[6]; Azar et al., 2019[18]), the average inverse number of firms in the same year and industry but in other regions, weighted by industry-employment shares of each region, is used as an instrumental variable. The rationale is that the number of firms in a market is strongly and inversely related to concentration but unrelated to productivity shocks to individual firms. Unlike potential instrumental variables that are a function of firm size (such as average concentration in the same industry but other regions), this variable has the advantage of being invariant to productivity shocks to individual firms.13

The analysis is conducted separately on individual-level data for each country in a distributed micro data approach. In contrast to individual-level data that are subject to strict confidentiality restrictions in many countries, aggregate and semi-aggregate descriptive statistics and regression results based on the micro data can generally be distributed. Country-level estimates are averaged following established procedures for the statistical aggregation of regression estimates.14

4.3.2. Data

The analysis in this paper is based on a newly created harmonised cross-country dataset based on linked employer-employee data that provide information on employees and the firms where they work. The data cover the universe of workers (or a large representative sample) in each country and are of very high quality (Criscuolo et al., 2020[27]), which allows calculating precise measures of labour market concentration. The availability of employee information furthermore allows controlling for worker characteristics when estimating the effect of concentration on wages. In particular, linked employer-employee data allow accurately measuring concentration not only in employment but also in hiring, which is not possible with firm-level data alone.15 New hires are identified from workers switching firms for their main job. All country datasets contain a core set of comparable information on workers (wage, gender, age and location) and firms (industry and size). Most datasets also contain a number of additional relevant variables, such as hours worked, occupation and education, but there are large differences in availability and detail. The main results presented in this paper rely on the core set of comparable characteristics. Additional analysis as well as a large set of robustness checks exploit the more detailed information for different subsets of countries.

The analysis requires making a number of data harmonisation choices. A basic prerequisite for measuring labour market concentration in a specific local labour market is the availability of information on the firm’s industry (at the 3-digit level) and information on the location of the worker at the level of TL3 regions, corresponding roughly to provinces (e.g. provincias in Spain or départements in France) or groups of smaller units such as counties or districts (e.g. in Austria).16 The wage regressions are based on monthly wages.17

The main analysis based on the local labour market definition at the 3-digit industry and TL3 region level covers seven countries over a period from the early 2000s up to 2017.18 Where these detailed levels are unavailable, a number of descriptive results are reported at a coarser level of aggregation (2-digit industry or TL2 region) for a maximum of 11 countries.19 The analysis covers dependent employees in all sectors of the private economy other than agriculture, mining and utilities. This covers on average 97% of total private sector employment.20 Industries are classified according to the International Standard Industrial Classification (ISIC), revision 4. TL3 regions are classified into rural and urban according to a harmonised classification by Fadic et al. (2019[28]).21

4.4.1. A snapshot of labour market concentration across countries

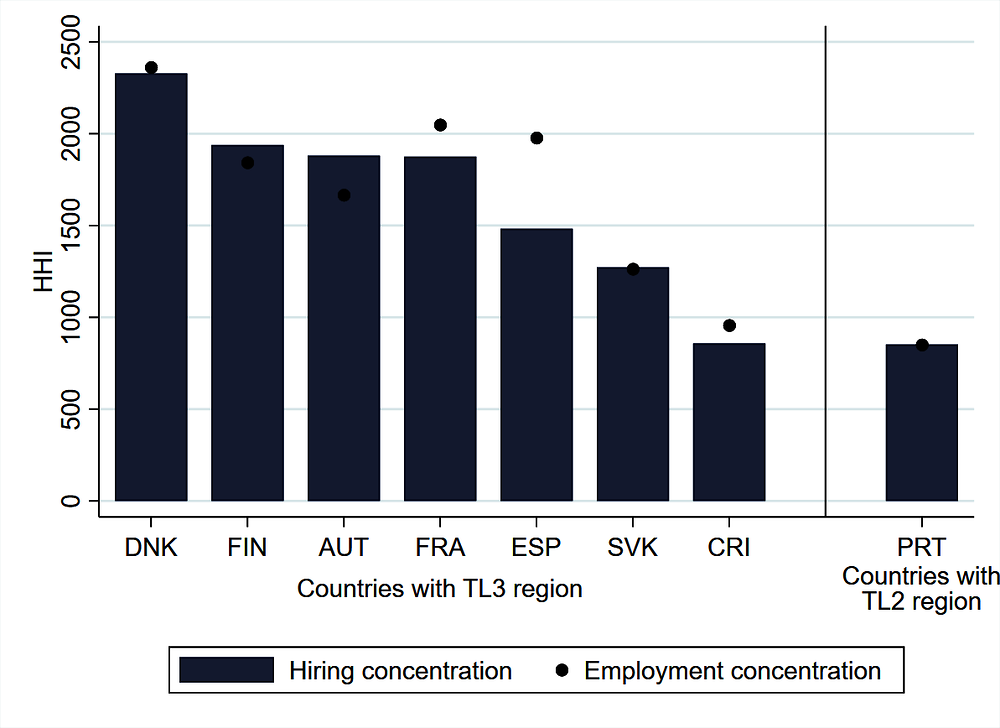

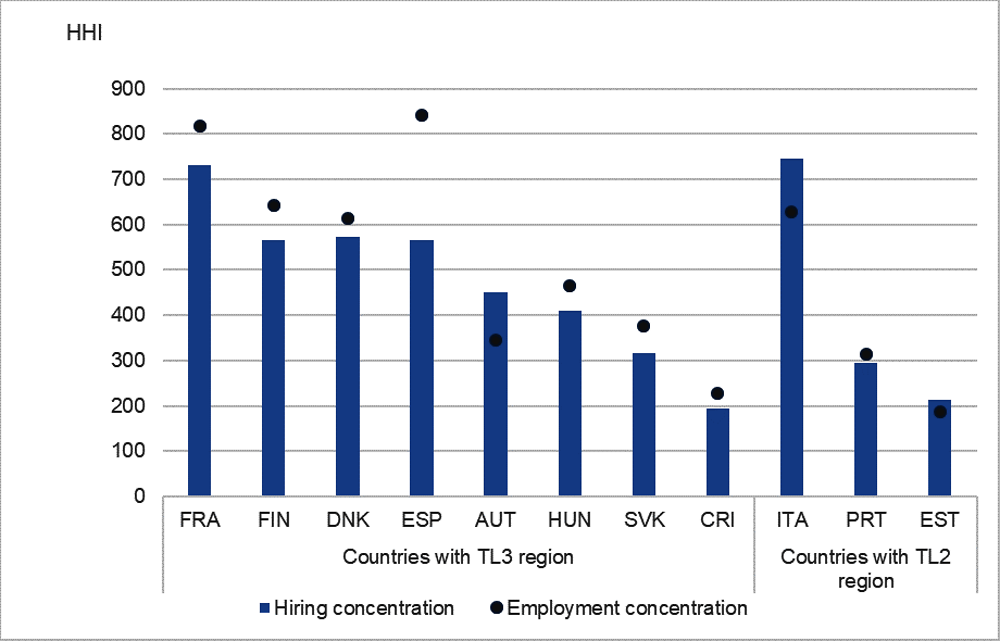

On average across countries, local labour markets are moderately concentrated but around 20% of workers are employed in markets with high levels of concentration (Figure 4.2). The cross-country average of local labour market concentration for the average worker as measured by the employment-weighted HHI is around 1600 (Panel A), which is the threshold conventionally used in merger reviews to indicate moderate sales concentration (US Justice Department and the Federal Trade Commission, 2010[29]). Moreover, around 20% of workers are employed in highly concentrated labour markets (based on the conventional threshold of an HHI above 2500). This share is substantially higher in Austria, Denmark, Finland and France (Panel B).

Note: The Figure shows statistics based on the HHI in hiring in 2015 at the level of local labour markets defined by 3-digit industries and TL3 regions. Panel A shows the average employment-weighted HHI. Panel B shows the share of workers in markets with an HHI above 2,500. The primary and utilities sectors, public administration and defence are excluded. Data for the USA refer to the weighted average HHI of employment concentration in local labour markets defined by 4-digit NAICS industries and commuting zones. The share of workers with HHI above 2,500 is not available for the United States.

Cross-country differences in local labour market concentration can reflect structural differences between countries, but may also be due to differences in the average size of TL3 regions. For instance, in some countries, such as Austria and Finland, average employment of TL3 regions is lower than in other European countries; whereas in Costa Rica, it is higher. This may introduce an upward bias in measured concentration in Austria and Finland relative to the other countries. Given the measurement challenges characterising cross-country comparisons of concentration levels, the remainder of the paper focuses on within-country differences in concentration across geographical areas, industries, worker groups and over time rather than on cross-country differences in local labour market concentration.

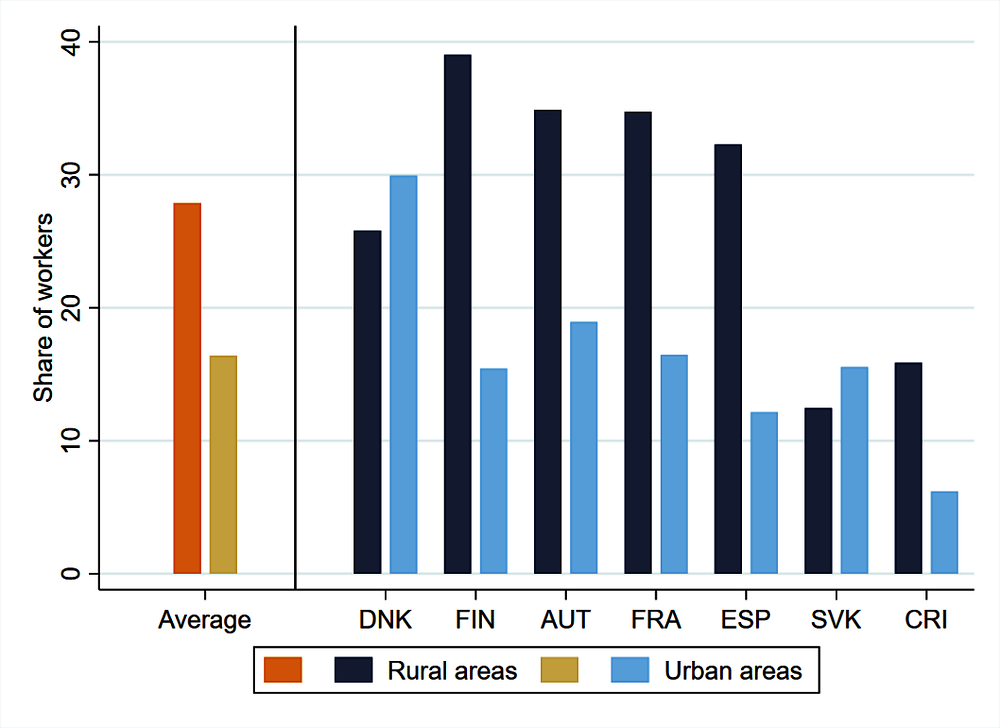

The share of workers exposed to high local labour market concentration in rural areas (around 30%) is twice as large than in urban ones (around 15%) (Figure 4.3). In rural areas, there are fewer job opportunities for workers in any given industry due to a limited number of potential employers. In urban areas, there are significantly more job opportunities, as firms generally tend to locate close to large population centres to access a larger pool of workers and consumers and benefit from agglomeration economies (Glaeser, 2010[26]). In some industries, firms also tend to co-locate with firms in the same or closely related industries, generally in urban areas, thereby expanding job opportunities for workers with industry-specific skills (Moretti, 2013[30]). While the rural-urban differential in local labour market concentration holds for most countries covered by the analysis, in Denmark and in the Slovak Republic concentration is lower in rural than urban areas. This may reflect the fact that in these countries a number of very large employers, in particular multi-national firms, account for a very large share of employment in the capital region.

Note: Local labour markets are defined by new hires in 3-digit industries and TL3 regions. The urban vs. rural classification follows Fadic et al. (2019[28]). The primary and utilities sectors, public administration and defence are excluded.

A significantly higher share of manufacturing workers (around 40%) than services workers (around 15%) is employed in highly-concentrated labour markets (Figure 4.4). Manufacturing is generally more geographically concentrated than services, which can be explained by larger scale economies in manufacturing and higher tradability (Gervais and Jensen, 2019[31]). For instance, the benefits for an automobile firm to locate close to its customers is small since scale economies are large and automobiles can be shipped to the location of final demand at low cost. By contrast, even though in some digitally-intensive services sectors economies of scale are becoming increasingly important and remote provision is becoming more feasible, in many services sectors economies of scale remain limited and provision still requires physical presence.22

The rural-urban differential in local labour market concentration holds within industries and the manufacturing-services differential holds within regional groups (Annex Figure 4.A.1). This suggests the concentration differentials reported above cannot be explained by a higher tendency of manufacturing firms to locate in rural areas with higher levels of concentration.

Note: Local labour markets are defined by new hires in 3-digit industries and TL3 regions. The primary and utilities sectors, public administration and defence are excluded.

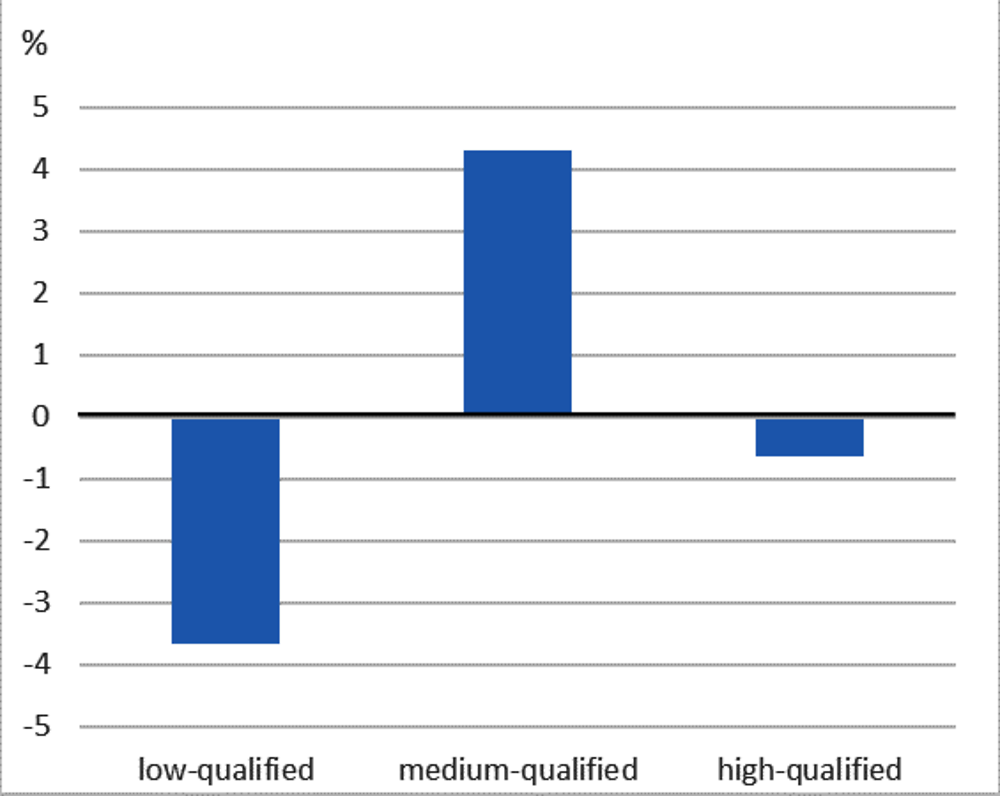

Low-qualified workers tend to face significantly higher concentration within their local labour markets (Figure 4.5).23 The lack of a link between a local labour market’s workforce composition and its degree of employer concentration partly reflects the fact that a high share of low-qualified workers are employed in low-concentrated urban services sectors. By contrast, within their local labour markets, i.e. within a given industry and geographical area, low-qualified workers generally have a smaller number of job options than their medium and high-qualified peers. Exposure to local labour market concentration appears to be lowest for medium-qualified workers. The ratio of concentration for low-qualified workers relative to the mean reported in Figure 4.5 implies that the average low-qualified worker is employed in a moderately concentrated labour market with an HHI of around 2400, whereas the average medium-qualified worker is employed in a low-concentrated local labour market with an HHI of around 1300.24

Note: For the purpose of this analysis, local labour markets are defined at the 2-digit industry by TL3-level by worker qualification level, i.e. bars can be interpreted as deviations from the employment-weighted average of hiring concentration within local labour markets defined at the 2-digit industry by TL3-level. Deviations due to differences in employment shares of different qualification groups between local labour markets, i.e. workforce composition effects, are around one order of magnitude smaller and reported in Annex Figure 4.A.6.The analysis cannot be conducted at the 3-digit industry by TL3 by worker qualification level due to confidentiality restrictions related to excessively small 3-digit-TL3-qualification cells in a number of countries. Qualification groups are based on occupation or education. Included countries: Costa Rica, Finland, Spain, France and Slovakia (Information on worker qualification is unavailable for Austria).

The patterns in local labour market concentration documented at the 3-digit industry by TL3 region local labour market level are robust to alternative definitions. Defining local labour markets in terms of employment rather than hiring has no quantitative effect of at the level of concentration (Annex Figure 4.A.5). Data available for less detailed aggregations of industry and/or region for a larger sample of 11 countries are reported in Annex Figure 4.A.6. While the cross-country pattern of concentration documented above is broadly similar to the one in Figure 4.2, the measured levels of the HHI decrease at this more aggregate local labour market definition, reflecting a mechanical increase in the number of firms when regions or industry boundaries are expanded.

4.4.2. Trends in labour market concentration

There is no evidence of an increase in local labour market concentration over the period 2003-2017. Averaging across countries, there is a slight decline until 2008 and a broadly stable trend since (Figure 4.6). The initial decline in local labour market concentration is mainly driven by Finland and Spain, which may partly be explained by the rapid shift from manufacturing to lower-concentrated services in these countries in the run-up to the global economic crisis of 2008-09. But changes in industry composition do not appear to be the sole explanation for this initial decline, given that concentration has declined even within services.25

Note: The lines are based on the simple average of country-level growth rates in the HHI (rather than levels) to account for changes in country composition over time. Local labour markets are defined by new hires in 3-digit industries and TL3 regions. Included countries: Austria, Denmark and Spain (2003-17); Costa Rica (2007-17); Finland (2005-16); France (2003-16); United States (2003-15). The Slovak Republic is not included in the figure due to insufficient year coverage (2014-2017). For detailed definition in the USA, see note of Figure 4.2.

The trend decline in local labour market concentration has occurred despite an increase in sales concentration over the past two decades. Available measures of sales concentration typically refer to industry sales at the national level, whereas local labour market concentration is measured as hiring or employment. This suggest that there are two possible explanations for the observed decoupling of local labour market concentration from national sales. Firstly, national employment concentration may have decoupled from national sales concentration if firms are increasingly able to scale up production without increasing employment, including through domestic and international outsourcing. Secondly, local employment concentration may have decoupled from national employment concentration, which may for instance be the case if large national employers increasingly enter each other’s local labour markets (Rinz, 2020[4]).26 Box 4.2 suggests that the main explanation is the decoupling of national employment concentration from national sales concentration.

The evidence reported above suggests that local labour market concentration has tended to decline over the past 20 years despite existing evidence of an increase in sales concentration (Bajgar et al., 2019[1]). There are several possible explanations for this decoupling.

One possible explanation is that sales concentration is typically measured as a concentration ratio at the national level, e.g. the ratio of sales of the eight largest firms in an industry relative to all firms, whereas employment concentration in this chapter is measured as the HHI at the local labour market level. However, re-expressing labour market concentration as a concentration ratio and distinguishing between national and local concentration suggests that the decoupling has mainly occurred at the national level, especially in services (Figure 4.7, Panel A).

Note: Sales and employment concentration are measured by the CR8, i.e., the concentration ratio measuring the sum of the market share (in sales and employment) held by the largest eight firms in an industry. The CR8 is measured at the 2-digit industry level (2-digit industry by TL3 region for local labour market concentration) to maintain consistency in measurement between employment and sales concentration, for which other measures of concentration are unavailable. The data are unweighted averages across industries and countries (local labour market concentration has been averaged across regions using employment weights within industries in a first step). Time series have been normalised to 100 in 2002. Included countries: Denmark, France, Hungary, Italy, Portugal and Spain.

Source: Bajgar et al. (2019[1]).

The decoupling of employment concentration from sales concentration at the national level could reflect the fact that the top eight firms in terms of employment are not necessarily the same as the top eight firms in terms of sales. High-sales firms tend to have higher labour productivity and thus smaller workforces at any given level of sales (Autor, Katz and Van Reenen, 2020[32]; Andrews, Criscuolo and Gal, 2016[33]). Consequently, an expansion of sales of the top eight firms in terms of sales does not necessarily translate into an expansion of employment of the top eight employers, especially in sectors where sales can be scaled up without expanding employment, which tends to be the case in a number of intangible- and digitally-intensive services industries.

Another possible explanation of the decoupling of national employment concentration from national sales concentration is related to the degree to which leading firms may domestically or internationally outsource activities to other firms. Removing labour-intensive tasks from firms’ production processes effectively decouples developments in sales from employment.

Sales and employment concentration are more closely linked in manufacturing than in services (Figure 4.7, Panels B and C). This is consistent with evidence of a robust productivity-size premium in manufacturing despite increased domestic and international outsourcing but a weaker (and weakening) productivity-size premium in services (Berlingieri, Calligaris and Criscuolo, 2018[34]).

Local labour market concentration has a significantly negative effect on wages, even after accounting for differences in workforce composition and productivity across local labour markets (Figure 4.8). In other words, a worker employed in a highly-concentrated local labour market earns a significantly lower wage than a worker with similar characteristics in a low-concentrated market with similar average productivity. On average across countries, the mean reduction in wages from a 1,000 point increase in the HHI is around 2%, which is broadly in line with existing estimates from country-level studies relying on occupation-by-region based local labour market definitions (Martins, 2018[9]; Marinescu, Ouss and Pape, 2020[6]).27 While all country-level coefficients estimated from Equation 4.1 are negative as predicted by theory, some of them are estimated with large error, which precludes direct cross-country comparisons.28 Consequently, the remainder of the section focuses on the average cross-country effect.

Based on the estimated average cross-country effect of concentration, wages at the 90th percentile of employment-weighted local labour market concentration (i.e. the 90th percentile of workers rather than the 90th percentile of local labour markets) are 7% lower than at the 10th percentile (Annex Table 4.A.2). On average across countries, for workers at the 90th percentile the value of the HHI is about 4000, whereas for workers at the 10th percentile it is around 150. Based on the average wage effect reported in Figure 4.8, this difference in labour market concentration translates into an economically significant wage difference of 7%. The implied wage difference would be even larger (around 16%) between workers at the 90th and 10th percentiles of the unweighted concentration distribution, given that concentration is typically highest in small markets with low employment.

Note: Light blue bars represent country-level point estimates of an instrumental variables regression of log wages on local labour market concentration (Equation 4.1). Preferred estimates correspond to column 3 (AUT), column 7 (CRI), column 11 (ESP), column 16 (FIN), column 19 (FRA) and column 23 (DNK) of Annex Table 4.A.1. The Slovak Republic is not included in the wage regressions due to insufficient year coverage (2014-2017). All estimated models include local labour market, worker fixed and year fixed effects. The estimated model for Finland additionally includes firm fixed effects to control for omitted firm-level factors that may be correlated with concentration even after controlling for market fixed effects, such as firm-level productivity (in the other countries, including firm fixed effects yields virtually identical estimates as excluding them). The aggregate coefficient (-0.018) is a weighted average of the individual country-level estimates, with weights taking into account both the estimation error within each country, and the between-country variation in estimates (Stanley, 2001[35]). The whiskers correspond to 95% confidence intervals, the horizontal grey band corresponds to the 95% confidence interval of the aggregate coefficient [-0.028 -0.007]. The aggregate coefficient implies that a 1,000 point increase in the HHI reduces wages by 1.8%.

The wage effects of local labour market concentration tend to be driven by low-qualified workers (Annex Table 4.A.3). On average across the three countries for which disaggregated coefficients by skill group can be estimated, the wage effect for low- and medium- qualified workers of a 1,000 point increase in the HHI is about 2% whereas the effect for high-skilled workers is close to zero.29 At the same time, low-qualified workers face about 40% higher local labour market concentration than high-qualified ones. Combining the effects on low-qualified workers’ wages from the stronger wage response to concentration with the higher exposure to concentration suggests that labour market concentration reduces low-qualified workers’ wages by around 6% relative to those of high-skilled ones.

The negative wage effect of labour market concentration has tended to become stronger over time (Figure 4.9). The estimated wage effect is about twice as strong in 2015-2017 than in 2003-2005, with the difference being statistically significant at the 5% level. The increasingly negative wage response to concentration suggests that firms are increasingly exercising their wage-setting power. To some extent, this could reflect the weakening of workers’ bargaining position due to changes in wage-setting institutions such as minimum wages and collective bargaining, or increased exposure to domestic and international outsourcing (Abel, Tenreyro and Thwaites, 2018[7]).

Note: Each bar represents the average of year-by-year country level estimates of the semi-elasticity of concentration on wages, for a block of four years each (3 years for the final block). The aggregate coefficient is a weighted average of the individual country-level estimates, with weights taking into account both the estimation error within each country, and the between-country variation in estimates (Stanley, 2001[35]). Each regression uses a cross-section of worker-firm data and controls separately for region, industry and year fixed effects. The 90% confidence intervals take into account both the estimation error within each country, and the between-country variation in estimates. Included countries: Austria, Costa Rica, Denmark, Finland, France and Spain.

The analysis in this chapter covers the degree of labour market concentration, the extent to which it varies across different segments of the labour market and over time, as well as its effects on wages. The main results are that (1) on average across the covered countries a significant share of workers (around 20%) are employed in highly-concentrated labour markets, especially in manufacturing and rural areas; (2) labour market concentration has negative effects on wages; (3) wage effects from labour market concentration tend to be particularly negative for low-qualified workers; and (4) wage effects have tended to become more negative over time. These results can potentially inform a range of public policy areas.

The high degree of labour market concentration for a significant share of workers and the increasingly negative effect of concentration on wages suggest that wage-setting policies may play a useful role in counter-balancing wage-setting power. In a labour market where firms have a high degree of wage-setting power, statutory or collectively-bargained wage floors can increase wages without reducing employment by limiting firms’ scope to reduce wages below workers’ reservation wages (Card and Krueger, 1994[36]; Manning, 2020[16]; OECD, 2019[37]; OECD, 2018[38]).30 In a number of OECD countries, the real value of the minimum wage and the share of workers covered by collective bargaining agreements have tended to decline over the past decades, suggesting room for policy action.

Wage-setting policies may become particularly relevant in the context of the emergence of digital platforms that have gained dominant positions in some local labour markets. Many digital platforms, including in ride-hailing, food delivery and retail, rely mainly on low-skilled self-employed workers for whom the wage effects of local labour market concentration are particularly negative.31 Collective bargaining over wages and working conditions on the part of these self-employed workers should not be prevented by the undue application of non-collusion clauses in competition law (OECD, 2020[23]).

A high degree of wage-setting power may also indicate the need for public policies to directly address labour market concentration, especially in a context where collective bargaining is under pressure, trade union density is declining and “winner-takes-most” dynamics are emerging in some sectors of the economy. In many jurisdictions, competition authorities already have the legal mandate to include labour market power as a consideration in reviews of mergers and acquisitions (OECD, 2020[23])). One way to operationalise labour market power in merger reviews is to define a threshold above which a labour market is considered to be highly concentrated, which would then trigger further investigation (Marinescu and Hovenkamp, 2019[22]). Even though the analysis in this chapter suggests that increasing product-market concentration does, on average, not imply higher labour market concentration, anecdotal evidence nonetheless suggests that, in some sectors of the economy, increased product market concentration has been associated with increased labour market concentration. For instance, large digital platforms in the transport and retail sectors have become dominant employers in some local labour markets.

Excessive wage setting power may further be tackled by policies to promote voluntary job mobility, which would increase the job options effectively available to workers. While job mobility is partly determined by individual preferences over non-wage job characteristics, monetary costs to mobility can be influenced by public policies. Such costs could, for instance, be reduced by strengthening active labour market policies; improving the portability of benefits; regulatory action that reduces legal or contractual barriers to job mobility (occupational licensing, non-compete and non-poaching agreements, portability of workers’ ratings across digital platforms); and through housing and transport policies. The uptake of telework has effectively expanded the geographical boundaries of worker’s job options but teleworkable jobs and occupations are typically located at the top of the skill distribution (OECD, 2021[39]; Espinoza and Reznikova, 2020[40]). While policies to support telework would thus tend to raise average wages, they may further widen the gap between workers at the top and the rest of the wage distribution.

References

[7] Abel, W., S. Tenreyro and G. Thwaites (2018), Monopsony in the UK, https://ssrn.com/abstract=3270944.

[41] Abowd, J., F. Kramarz and D. Margolis (1999), “High Wage Workers and High Wage Firms”, Econometrica, Vol. 67/2, pp. 251-333, https://about.jstor.org/terms (accessed on 2 December 2019).

[17] Akerlof, G. and J. Yellen (1990), “The Fair Wage-Effort Hypothesis and Unemployment”, The Quarterly Journal of Economics, Vol. 105/2, p. 255, https://doi.org/10.2307/2937787.

[33] Andrews, D., C. Criscuolo and P. Gal (2016), The Best versus the Rest, https://doi.org/10.1787/63629cc9-en.

[14] Ashenfelter, O. and D. Card (eds.) (2011), Imperfect Competition in the Labor Market, Elsevier.

[2] Autor, D. et al. (2017), “Concentrating on the Fall of the Labor Share”, American Economic Review, Vol. 107/5, pp. 180-185, https://doi.org/10.1257/aer.p20171102.

[32] Autor, D., L. Katz and J. Van Reenen (2020), “The Fall of the Labor Share and the Rise of Superstar Firms”, The Quarterly Journal of Economics, Vol. 135, pp. 645–709, https://doi.org/10.1093/qje/qjaa004.

[18] Azar, J. et al. (2019), Minimum Wage Employment Effects and Labor Market Concentration, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w26101.

[42] Azar, J., I. Marinescu and M. Steinbaum (2019), “Measuring Labor Market Power Two Ways”, AEA Papers and Proceedings, Vol. 109, pp. 317-321, https://doi.org/10.1257/pandp.20191068.

[19] Azar, J. et al. (2020), “Concentration in US labor markets: Evidence from online vacancy data”, Labour Economics, Vol. 66, p. 101886, https://doi.org/10.1016/j.labeco.2020.101886.

[1] Bajgar, M. et al. (2019), “Industry Concentration in Europe and North America”, OECD Productivity Working Papers, No. 18, OECD Publishing, Paris, https://dx.doi.org/10.1787/2ff98246-en.

[25] Bassanini, A. et al. (2022), Labour market concentration in Europe.

[15] Bassier, I., A. Dube and S. Naidu (2021), “Monopsony in Movers: The Elasticity of Labor Supply to Firm Wage Policies”, Journal of Human Resources, pp. 0319-10111R1, https://doi.org/10.3368/jhr.monopsony.0319-10111r1.

[5] Benmelech, E., N. Bergman and H. Kim (2020), “Strong Employers and Weak Employees: How Does Employer Concentration Affect Wages?”, Journal of Human Resources, pp. 0119-10007R1, https://doi.org/10.3368/jhr.monopsony.0119-10007r1.

[12] Berger, D., K. Herkenhoff and S. Mongey (2019), Labor Market Power, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w25719.

[34] Berlingieri, G., S. Calligaris and C. Criscuolo (2018), “The Productivity-Wage Premium: Does Size Still Matter in a Service Economy?”, AEA Papers and Proceedings, Vol. 108, pp. 328-33, https://doi.org/10.1257/pandp.20181068.

[49] Bound, J., D. Jaeger and R. Baker (1995), “Problems with Instrumental Variables Estimation When the Correlation Between the Instruments and the Endogeneous Explanatory Variable is Weak”, Journal of the American Statistical Association, Vol. 90/430, p. 443, https://doi.org/10.2307/2291055.

[10] Caldwell, S. and O. Danieli (2018), Outside Options in the Labor Market.

[36] Card, D. and A. Krueger (1994), “Minimum Wages and Employment: A Case-Study of the Fast-Food Industry in New Jersey and Pennsylvania”, American Economic Review, Vol. 84/4, pp. 772-793, https://www.jstor.org/stable/2118030.

[48] Causa, O., N. Luu and M. Abendschein (forthcoming), Labour market transitions across OECD countries: stylised facts.

[27] Criscuolo, C. et al. (2020), “Workforce composition, productivity and pay: the role of firms in wage inequality”, OECD Economics Department Working Papers, No. 1603, OECD Publishing, Paris, https://dx.doi.org/10.1787/52ab4e26-en.

[50] DerSimonian, R. and N. Laird (1986), “Meta-analysis in clinical trials”, Controlled Clinical Trials, Vol. 7/3, pp. 177-188, https://doi.org/10.1016/0197-2456(86)90046-2.

[43] Dube, A., A. Manning and S. Naidu (2018), Monopsony and Employer Mis-optimization Explain Why Wages Bunch at Round Numbers, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w24991.

[40] Espinoza, R. and L. Reznikova (2020), “Who can log in? The importance of skills for the feasibility of teleworking arrangements across OECD countries”, OECD Social, Employment and Migration Working Papers, No. 242, OECD Publishing, Paris, https://dx.doi.org/10.1787/3f115a10-en.

[28] Fadic, M. et al. (2019), “Classifying small (TL3) regions based on metropolitan population, low density and remoteness”, OECD Regional Development Working Papers, No. 2019/06, OECD Publishing, Paris, https://dx.doi.org/10.1787/b902cc00-en.

[31] Gervais, A. and J. Jensen (2019), “The tradability of services: Geographic concentration and trade costs”, Journal of International Economics, Vol. 118, pp. 331-350, https://doi.org/10.1016/j.jinteco.2019.03.003.

[26] Glaeser, E. (ed.) (2010), Agglomeration Economics, The University of Chicago Press, http://www.nber.org/books/glae08-1.

[46] Haltiwanger, J. (2021), Rising between Firm Inequality and Declining Labor Market Fluidity: Evidence of a Changing Job Ladder, National Bureau of Economic Research.

[8] Jarosch, G., J. Nimczik and I. Sorkin (2019), Granular Search, Market Structure, and Wages, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w26239.

[47] Langella, M. and A. Manning (2021), The measure of monopsony, https://cep.lse.ac.uk/pubs/download/dp1780.pdf.

[16] Manning, A. (2020), “Monopsony in Labor Markets: A Review”, ILR Review, Vol. 74/1, pp. 3-26, https://doi.org/10.1177/0019793920922499.

[45] Manning, A. (2003), Monopsony in Motion, Princeton University Press, https://doi.org/10.1515/9781400850679.

[20] Manning, A. and B. Petrongolo (2017), “How Local Are Labor Markets? Evidence from a Spatial Job Search Model”, American Economic Review, Vol. 107/10, pp. 2877-2907, https://doi.org/10.1257/aer.20131026.

[22] Marinescu, I. and H. Hovenkamp (2019), “Anticompetitive Mergers in Labor Markets”, Indiana Law Journal, Vol. 94, p. 1031.

[6] Marinescu, I., I. Ouss and L. Pape (2020), Wages, Hires, and Labor Market Concentration, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w28084.

[9] Martins, P. (2018), Making their own weather? Estimating employer labour-market power and its wage effects.

[30] Moretti, E. (2013), The New Geography of Jobs.

[21] Nimczik, J. (2020), Job Mobility Networks and Data-driven Labor Markets.

[51] Nordhaus, W. and A. Moffat (2017), A Survey of Global Impacts of Climate Change: Replication, Survey Methods, and a Statistical Analysis, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w23646.

[39] OECD (2021), Inclusiveness during the Pandemic: Gender and Skills Differences in Exposure to Employment Effects, OECD Publishing, Paris.

[23] OECD (2020), Competition in Labour Markets, https://www.oecd.org/daf/competition/competition-in-labour-markets-2020.pdf.

[24] OECD (2019), Labour market regulation 4.0: Protecting workers in a changing, OECD Publishing, Paris, https://doi.org/10.1787/9ee00155-en.

[37] OECD (2019), Negotiating Our Way Up, OECD, https://doi.org/10.1787/1fd2da34-en.

[38] OECD (2018), Good Jobs for All in a Changing World of Work: The OECD Jobs Strategy, OECD Publishing, Paris, https://doi.org/10.1787/9789264308817-en.

[4] Rinz, K. (2020), “Labor Market Concentration, Earnings, and Inequality”, Journal of Human Resources, pp. 0219-10025R1, https://doi.org/10.3368/jhr.monopsony.0219-10025r1.

[44] Rossi-Hansberg, E., P. Sarte and N. Trachter (2021), “Diverging Trends in National and Local Concentration”, NBER Macroeconomics Annual, Vol. 35, pp. 115-150, https://doi.org/10.1086/712317.

[11] Schubert, G., A. Stansbury and B. Taska (2020), “Monopsony and Outside Options”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.3599454.

[3] Schwellnus, C. et al. (2018), “Labour share developments over the past two decades: The role of technological progress, globalisation and “winner-takes-most” dynamics”, OECD Economics Department Working Papers, No. 1503, OECD Publishing, Paris, https://dx.doi.org/10.1787/3eb9f9ed-en.

[13] Sokolova, A. and T. Sorensen (2020), “Monopsony in Labor Markets: A Meta-Analysis”, ILR Review, Vol. 74/1, pp. 27-55, https://doi.org/10.1177/0019793920965562.

[35] Stanley, T. (2001), “Wheat From Chaff: Meta-Analysis As Quantitative Literature Review”, Journal of Economic Perspectives, Vol. 15/3, pp. 131-150, https://doi.org/10.1257/jep.15.3.131.

[29] US Justice Department and the Federal Trade Commission (2010), Horizontal Merger Guidelines, https://www.justice.gov/atr/horizontal-merger-guidelines-08192010#5c.

[52] Yeh, C., C. Macaluso and B. Hershbein (2021), Monopsony in the U.S. Labor Market.

Note: The Figure shows the share of workers in local labour markets with an HHI above 2,500. Local labour markets are defined by 3-digit industries and TL3 regions. Markets are grouped by the broad sector to which the underlying 3-digit industry belongs, and by the rural/urban status of the region the market is located in. Average across six OECD countries: Austria, Costa Rica, Finland, France, Spain, Slovakia. Denmark is not included as data at the industry-by-region level are unavailable due to confidentiality restrictions. The primary and utilities sectors, public administration and defence are excluded.

Note: The bars show deviations from average local labour market concentration that are due to differences in employment shares of different qualification groups between local labour markets (3-digit industry by TL3 region) assuming that there are no differences in concentration within local labour markets. In this sense, they can be interpreted as the between local labour market component of differences in exposure to concentration between skill groups. The within component is reported in Figure 4.5. Included countries are Costa Rica, Finland, France, Slovakia and Spain (Information on worker qualification is unavailable for Austria).

Note: This Figure shows the average evolution between 2006 and 2015 of the HHI in hiring across 5 countries where concentration at the 3-digit industry by TL3 region level is available by sector and region: Austria, Costa Rica, Denmark, Finland, France, and Spain. Each diamond shows the HHI in a synthetic country where concentration follows the same time trend and has the same 2015 average as this group of countries. Rural and urban regions are defined as in Figure 4.2. Data for Austria, Denmark and Spain cover the whole period; Costa Rica is 2007-2017, Finland 2005-2016, France 2003-2016. The Slovak Republic is not included in the figure due to insufficient year coverage (2014-2017); the United States are not included because labour market concentration has not been disclosed at the level of individual regions for all years.

Note: This Figure shows the average evolution between 2001 and 2015 of the HHI in hiring across all countries where data are available, and for the balanced country sample shown in Figure 4.5. Each time series is normalised in 100 in 2003 to facilitate comparison of trends. Periods covered: 2001-2018 (Austria), 2007-2018 (Costa Rica), 2003-2017 (Denmark), 2005-2016 (Finland), 2002-2017 (France), 2003-2017 (Portugal), 2002-2018 (Spain), 2015-2018 (Slovak Republic), 2001-2015 (United States).

Note: This Figure shows the average of the HHI in hiring and employment across all countries where data are available. In Portugal, only large TL2 regions are available. Data for Austria, Costa Rica, Denmark, Finland, Portugal and the Slovak Republic comprise the population of all workers and hires; representative samples of workers are drawn in France (8.4% random sample) and Spain (4%).

Note: This Figure shows the average of the HHI in hiring and employment across all countries where data are available, for local labour markets defined by 2-digit industries and regions. For countries where the more detailed regional grid (TL3-level) is unavailable (Estonia, Italy, and Portugal), concentration is calculated over the smallest regional grid available in the data. This is the TL2-level for Portugal, Italy, and Estonia (where the TL2 level corresponds to the national level).

[TABLE CONTINUED ON NEXT PAGE]

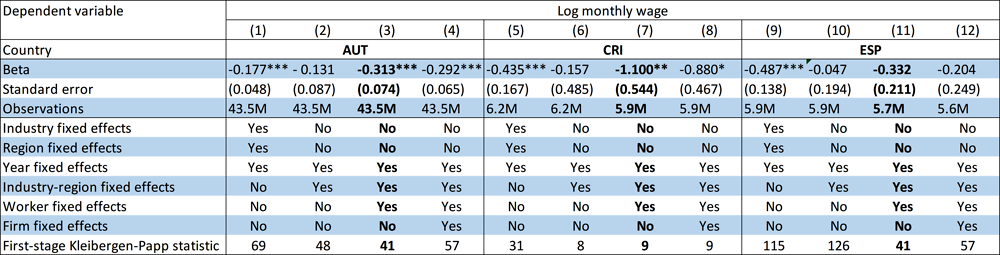

Note: This table shows the results from instrumental variables regressions of log monthly wages on local labour market concentration (the HHI in hiring of 3-digit industries and TL3 regions) using the regression model in equation (1). Concentration is instrumented with the inverse average number of firms in the same industry but in other regions. Reported are specifications with different fixed effects structures which are detailed in the table. Robust standard errors are clustered at the local labour market (industry-by-region) level. ***, ** and ** denote statistical significance at the 1%, 5% and 10% levels of significance, respectively. Columns with the preferred specification for each country are highlighted in bold

Note on preferred specifications: In general, the preferred specification corresponds to Equation 4.1 which controls for worker, year, and industry-region (market) fixed effects, and is shown as the 3rd column for each country. For comparison, two specifications with a less demanding fixed effects (FE) structure are shown on its left; and a specification with an additional firm FE is shown on its right. In most cases, adding firm FE in addition to industry-region, worker and time FE makes little difference, since industry-region FE already should capture most pay and productivity differences between establishments. Additional inclusion of firm FE will only matter for multi-establishment firms (since FE of single-establishment firms are already nested in industry-region FE). Only in Finland there is a material difference, which suggests that market FE are not sufficient to capture all relevant productivity differences on the firm side, possibly owing to the influence of multi-establishment firms. For this reason, the preferred specification in Finland includes firm FE. However, the result in Figure 4.8 is robust to choosing the specification that includes firn FE as preferred specification for all countries.

Note: This table shows the implied wage effects of moving from the 10th to the 90th percentile of concentration, based on the aggregate semi-elasticity reported in Figure 4.8. The upper part shows the effects of moving between points in the unweighted distribution of concentration (local labour markets), the lower part shows the effects of moving between respective points in the employment-weighted concentration. Concentration in all countries refers to 3-digit industry by small TL3 region for all countries.

Note: This table shows the results from instrumental variables regressions of log monthly wages on local labour market concentration (the HHI in hiring of 3-digit industries and TL3 regions), where concentration is interacted with a dummy for high skilled workers (the omitted category pools low and medium-qualified workers). Concentration is instrumented with the inverse average number of firms in the same industry but in other regions. Reported are specifications with different fixed effects structures which are detailed in the table. Robust standard errors are clustered at the local labour market (industry-by-region) level. ***, ** and ** denote statistical significance at the 1%, 5% and 10% levels of significance, respectively. Column 5 contains the aggregate coefficients, obtained using a random effects meta-aggregation procedure (Stanley, 2001[35]).

Note: The simulations assume that the concentration differentials between qualification groups observed at the 2-digit industry*TL3-region are similar at the 3-digit industry*TL3 level. The estimated wage effect for low- and medium-qualified workers is constrained to be equal (see Table 4.A.4.). Included countries: Costa Rica, Spain, Finland, France, and Slovakia (Information on worker qualification is unavailable for Austria).

The labour supply elasticity to the individual firm can be obtained empirically by estimating the elasticity of job separations to wages, where wages relate to the component of wages that is due to pay differences between firms for similar workers (Manning, 2011[14]). Following Bassier, Dube and Naidu (2021[15]), the labour supply elasticity is estimated in two stages. The first stage isolates the firm component of wages from other worker-related components by estimating a two-way fixed effects model based on Abowd, Kramarz and Magnolis (1999[41]):

where is the wage of individual i in firm j in year t; is a firm fixed effect; is a worker fixed effect; is the error term; and are time-varying worker control variables.32 Based on the results from the first stage, the second stage then estimates the elasticity of worker separations to the firm component of wages:

where is a dummy indicating separation of worker from firm in year ; is the estimated firm fixed effect; is the elasticity of separations to wages; and is the error term.33 The fact that separations are estimated using only the component of wages that corresponds to firm pay premia (see Chapter 2) and not the component that corresponds to worker characteristics mitigates concerns of endogeneity of wages to the quit rate.34

On average across the covered countries, of which only Costa Rica is non-European, the estimated labour supply elasticity is around 2 (Annex Figure 4.B.1). This translates into a potential wage loss of about 30% compared to a worker’s market wage in the absence of wage-setting power.35 To some extent, the cross-country pattern of the estimated labour supply elasticity may reflect structural differences, e.g. related to cross-country differences in job mobility. But it may also be explained by differences in measurement error or the severity of endogeneity issues related to omitted factors that influence both wages and quit rates. For instance, higher-paying firms may be more likely to offer better non-wage working conditions (e.g. flexible hours, telework) that would have a direct effect on the quit rate. But firms may also pay higher wages to compensate workers for difficult or harsh working conditions. The severity, direction, and relative importance of such endogenous non-wage determinants of quits could additionally vary across countries, implying that care needs to be taken when interpreting the cross-country pattern in Annex Figure 4.B.1.

Note: The aggregate coefficient is a weighted average of the individual country-level estimates, with weights taking into account both the estimation error within each country, and the between-country variation in estimates (Stanley, 2001[35]). Since no information on workers’ location is needed to estimate the labour supply elasticity, the analysis can be conducted on a somewhat broader country sample than the analysis of labour market concentration. Included countries: Austria, Costa Rica, Estonia, Finland, France, Hungary, Italy, Portugal, Spain, and Slovak Republic.

Overall, these results suggest a substantial degree of potential wage-setting power. However, they do not address the question of the extent to which firms actually exercise their power. This question is addressed using local labour market concentration as a partial indicator of wage-setting power.

Notes

← 1. This chapter has been written by an OECD team consisting of Michael Koelle, Nathalie Scholl and Cyrille Schwellnus with contributions of: Antoine Bertheau (University of Copenhagen, DENMARK), Chiara Criscuolo (OECD), Antton Haramboure (OECD), Alexander Hijzen (OECD), Balazs Murakőzy (University of Liverpool, HUNGARY), Satu Nurmi (Statistics Finland/VATT, FINLAND), Vladimir Peciar (Ministry of Finance of the Slovak Republic, SLOVAK REPUBLIC), Kevin Rinz (US Census Bureau, UNITED STATES), Catalina Sandoval and Jonathan Garita (Costa Rica Central Bank, COSTA RICA). Matej Bajgar, Chiara Criscuolo and Jonathan Timmis kindly provided the sales concentration data. For details on the data used in this chapter please see the standalone Data Annex and Disclaimer Annex.

← 2. The seven OECD countries that form the core of the analysis are Austria, Costa Rica, Denmark, Finland, France, Slovak Republic, and Spain. Comparable labour market concentration measures from the United States (based on establishment-level employment data) are additionally available for part of the descriptive analysis. Data for the Slovak Republic are available only for a short timespan (2014-2017), precluding any analysis which relies on the time series dimension of the data (including wage regressions).

← 3. Early studies on labour market concentration studied particular non-standard market niches, such as postings on online job boards (Azar, Marinescu and Steinbaum, 2019[42]; Azar et al., 2020[19])

← 4. A notable exception is ongoing work by Bassanini et al. (2022[25]) that analyses labour market concentration in a number of European countries.

← 5. Firms may also refrain from exercising wage-setting power because of costs related to setting optimal wages. Dube, Manning and Naidu (2018[43]), for instance, find strong evidence for bunching of wages at round numbers, suggesting the presence of optimisation costs.

← 6. Estimating the labour supply elasticity at the level of a narrowly defined local labour market is challenging due to the limited number of worker transitions observed in smaller partitions of the data. A sufficiently high number of separations – i.e., workers switching between different firms – is crucial for the precise estimation of firm pay premia and the elasticity of separations to cross-firm wage differences. Previous work relating wages to estimated labour supply elasticities did so either for larger labour markets (such as the entire US state of Oregon (Bassier, Dube and Naidu, 2021[15])) or for elasticities of online job applications to wages rather than actually observed separations (Azar, Marinescu and Steinbaum, 2019[42]).

← 7. However, trade costs may also imply that product markets, at least in some industries, are local (Rossi-Hansberg, Sarte and Trachter, 2021[44]).

← 8. A third approach to measure firms’ wage-setting power that is not further explored in this chapter relies on firm-level data and the estimation of firm-level production functions to infer the mark-down of wages below marginal costs (Yeh, Macaluso and Hershbein, 2021[52]). The drawback of this approach is that firm-level data generally do not allow to control for workforce composition and the inference of mark-ups relies on a set of theoretical assumptions.

← 9. The HHI consists in the sum of the squared market shares (in percent) of individual firms: .

← 10. When reporting the average of local labour market concentration at the national or industry level, each local labour market is weighted by its employment, such that national averages reflect the concentration faced by the average worker in the economy rather than concentration in the average local labour market.

← 11. The analysis is done at the preferred level of local labour markets, i.e. 3-digit industry by TL3-region, but is tested on a smaller subset of countries also for alternative labour market definitions for robustness.

← 12. Such sorting could arise either as an optimal worker response to wage penalties from concentration – with high-skill, high-wage workers more likely to overcome costs to mobility – or it could be driven by a third factor, such as the sorting of high-skilled workers to cities, where concentration is lower because of the higher density of markets. In some alternative specifications reported in Annex Table 4.A.1, observable worker characteristics (flexible gender-age interactions and a dummy for marginal workers) substitute for worker fixed effects.

← 13. This instrumental variable identifies the causal of effect of concentration under the assumption that changes in the average number of firms in other regions affect wages only through their effect on concentration, which may for instance be the case of changes in regulatory barries to entry.

← 14. Aggregation of estimates of single studies follows the methodology of “meta analysis” that is commonly used in economics (Stanley, 2001[35]; Nordhaus and Moffat, 2017[51]). It follows long-established statistical procedures that originate from applications in public health, medical science and adjacent fields (DerSimonian and Laird, 1986[50]). The aggregate coefficient is a weighted average of the individual country-level estimates, with weights taking into account both the estimation error within each country, and the between-country variation in estimates (so-called random effects meta analysis).

← 15. It is not possible to study labour market concentration from worker-level data, such as labour force surveys (LFS), due to lack of information that would allow grouping workers in the same firm. Firm-level data provide information on total employment at the firm level, which allows measuring firm-level employment concentration if sufficiently large and representative samples are available. But firm-level data lack information on individual workers, which precludes the measurement of concentration in hiring for different types of workers. Firm-level data also lack information on individual wages.

← 16. If a dataset does not provide information on worker location, establishment location is used instead.

← 17. Wages can be harmonised to the hourly level in about half of all countries where information on hours worked or equivalent (e.g. full-time equivalent rates) is available, which allows checking the robustness of the results obtained with monthly wages.

← 18. In many countries, the first year of observation is 2002, which implies that hiring concentration (which requires observing worker transitions between firms) is available from 2003.