5. The taxation of self-employed individuals

This chapter focuses on the taxation of self-employed individuals in Lithuania. The chapter begins by considering self-employment trends, the tax rules on self-employment and the characteristics of the self-employed. Next, the tax design and tax burdens of the business certificate and individual-activity regimes are evaluated against each other and standard employment and options for tax reform are presented. Finally, incorporated self-employment under different CIT rates is compared against standard employment and the individual-activity regime.

This chapter provides observations on the tax design and options for tax policy reforms in unincorporated and incorporated business regimes in Lithuania. The unincorporated regimes focus on the business certificate (BC) regime and the individual-activity (IA) regime (the taxation of self-employed farmers is briefly reviewed separately). The regimes are evaluated in terms of their tax design, tax rates and tax burdens, tax-induced incentives between organisational forms (including standard employment), interaction (i.e. migration between them) and adherence to principles of good tax policy (i.e. horizontal equity and tax neutrality). The incorporated business regime section focuses on owner managers of closely-held corporations and the tax-induced incentives between distributing profits as dividends and drawing a salary as an employee under both standard and reduced CIT rate regimes. The chapter is based on analysis using a representative sample of the tax record microdata in 2019. The chapter draws from a forthcoming OECD paper on the design of presumptive tax regimes ( (Mas-Montserrat et al., forthcoming[1])) The self-employment tax rules refer to the year 2021, unless otherwise stated. For simplicity, the following shorthand acronyms are used regularly throughout this chapter:

Self-employment trends

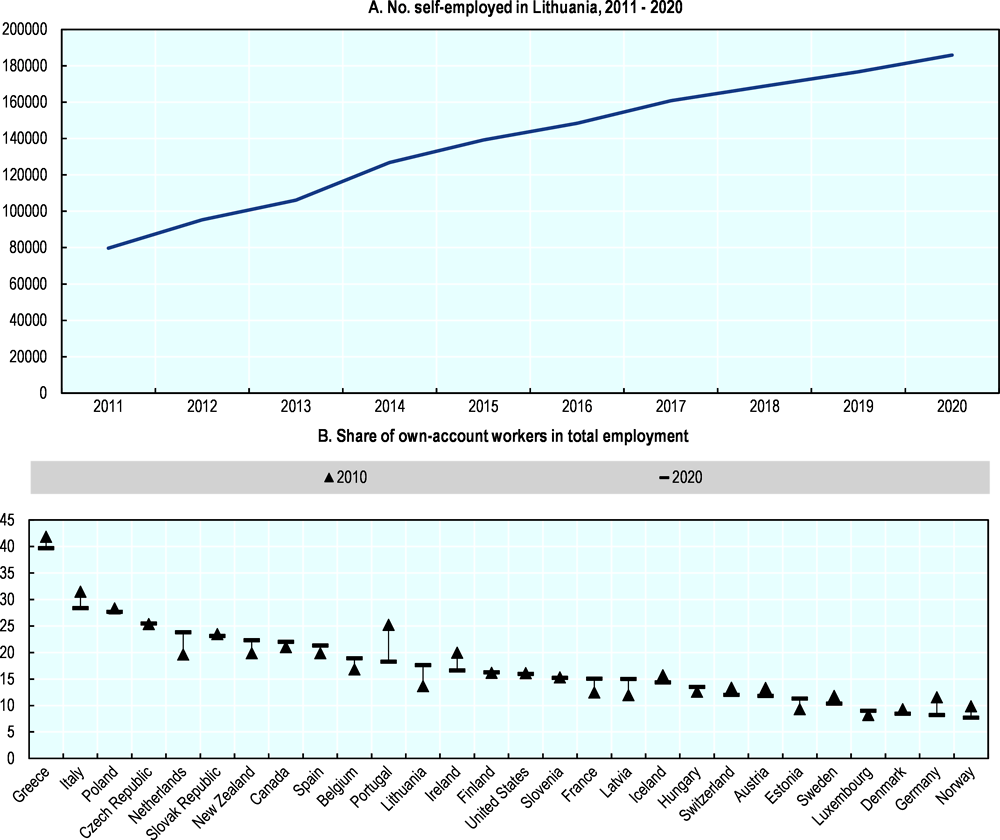

Self-employment has continued to grow (Figure 5.1, Panel A). Own-account workers represent 17.6% of total employment in 2020, which places Lithuania in the middle range of OECD countries (Figure 5.1, Panel B). While there has been no clear trend across the OECD in the share of own-account workers in total employment between 2010 and 2020, there has been a significant increase in Lithuania.

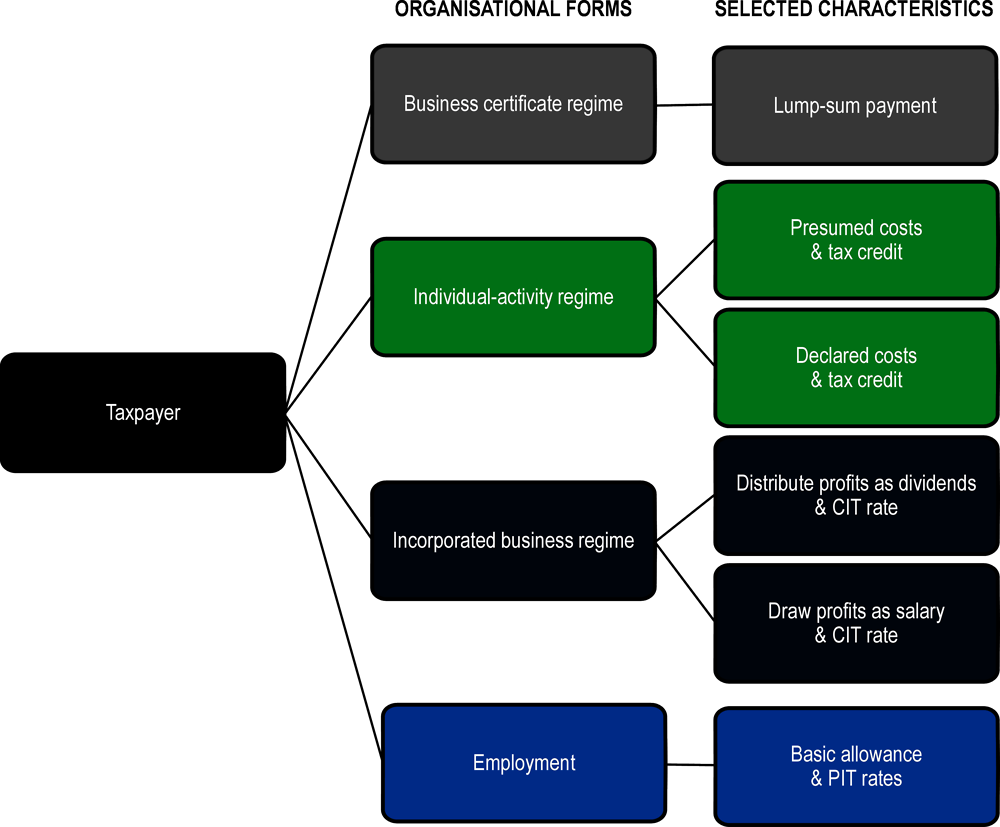

Self-employment numbers are significant. Individual activity in Lithuania refers to unincorporated self-employment (SE) activity from which income is received regularly. There are two main ways of taxing individual SE activity in Lithuania. They are the individual-activity certificate regime (IA regime) and the business certificate regime (BC regime). The number of individuals in the BC regime represents about half of the IA regime in 2019 (88,208 individuals declared having income under the BC regime and 174 124 declared having income under the IA regime).1 In the IA regime, about one-third of individuals are farmers (116 680 related to non-agricultural income and 57 444 relate to agricultural income). Individuals in the IA and BC regimes combined comprise 18% of employees (there are a total of 1 434 240 individuals with employment income in 20192). Lithuania has a wide range of other categories which do not belong to self-employed or employed categories, which are outside the scope of the current review. Figure 5.3 provides a stylised overview of the organisational forms considered.

Self-employment PIT revenues

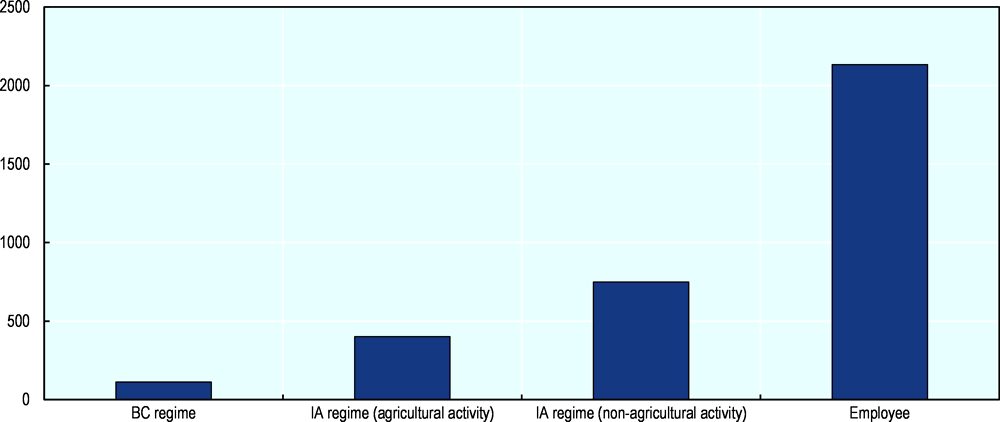

PIT revenues from self-employment are low compared to standard employment. The average PIT paid per person is lowest in the BC regime, followed by agricultural activity in the IA regime and then non-agricultural activity in the IA regime (Figure 5.2). The average PIT paid is significantly lower in all of the SE regimes compared to standard employment.

Note: In chart A, self-employed defined as persons carrying out economic activity by certificate and individual enterprises are public and private companies, state-owned and municipal enterprises, foreign affiliates, agricultural and cooperative partnerships, public bodies. In chart B, only countries for which are data are available are shown.

Source: Statistics Lithuania. OECD Gender – Entrepreneurship database.

Note: PIT paid is based on both declarations filed by individuals and on behalf of individuals. BC regime refers to income from individual activities under a business certificate. IA regime (agricultural activity) refers to income from agricultural individual activity under an individual activity certificate. IA regime (non-agricultural activity) refers to Income from non-agricultural individual activity under an individual activity certificate. Employees refer to payments made in connection with employment relations or relations in their essence corresponding to employment relations, except certain other payments.

Source: OECD analysis of microdata.

Principles of tax policy design for self-employment

The principle of horizontal equity says that tax and benefit treatment should be aligned across employment forms, but rationales exist for departure from the principle. Equity is the aim that taxation is fair for all taxpayers. Equity can be broken into vertical equity (how individuals with a greater ability to pay should bear proportionately higher tax burdens) and horizontal equity (how similar individuals should face similar tax burdens). This chapter focuses mainly on the latter. The principle of horizontal equity states that tax treatments and benefit entitlements should be broadly aligned across different employment forms (e.g. between employees and the self-employed). However, arguments have been made to justify departures from the principle of horizontal equity in tax treatment beginning with the notion that employment forms face different economic realities in terms of agency over their work, social protections they are afforded and the risk they bear. For example, the job uncertainty, investment loss and competitive pressure of self-employed compared to employment may justify lower tax burdens on the self-employed (Milanez and Bratta, 2019[2]). Similarly, reduced employment rights and different entitlements may justify lower tax burdens.

The principle of tax neutrality says that tax should not be a factor in organisational form decisions, but non-neutral policies can have justifications. Tax treatment is neutral when similar individuals face the same tax burden and tax is not a factor in the organisational form decision. Neutrality implies that decisions are made on economic merit and not for tax reasons. Departures from horizontal equity tax treatment can have implications for neutrality. For example, greater allowable deductions for self-employed workers relative to employed workers (which is commonly the case across countries including in Lithuania) could lead to false self-employment and inflated deductions. Similarly, lower tax rates on capital income relative to labour income (which is commonly the case across countries including in Lithuania) can encourage the self-employed to incorporate their business and re-characterise labour income as capital income (Milanez and Bratta, 2019[2]). Non-neutral policies such as these can however be justified for example on the basis of encouraging economic growth and job creation.

Source: OECD analysis.

This section provides an overview of the tax rules for self-employment in the BC and IA regimes compared with standard employment for both PIT and SSCs. The analysis presented for the IA regime includes self-employed farmers and non-farmers. Since the tax rules differ for farmers, farmers are briefly discussed separately at the end of the IA regime section.

PIT rules

Taxpayers in Lithuania can simultaneously belong to several different organisational forms including two self-employment regimes (IA and BC regimes), a standard employment and incorporation (at a standard or reduced CIT rate and then with a choice to pay profits in dividends, in salary or retain in the company). The organisational forms differ in several respects including how income is taxed, deductions, eligibility criteria, record-keeping requirements and the level of government at which taxes are set and collected (Table 5.1). The tax rules described in this section refer to the year 2021. There are other types of self-employment income that exist but which are not considered for the purposes of this report.

In the IA regime, the PIT rate is increasing. Under the IA regime, the PIT rate is applied to taxable income. The PIT rate ranges from 5% for taxable incomes up to EUR 20 000 to 15% for taxable incomes above EUR 35 000 (Table 5.1). The average effective PIT rate increases between taxable income of EUR 20 000 and EUR 35 000 as a result of the design (discussed later, see Figure 5.15).

In the IA regime, individuals can choose between declaring expenses and a presumed cost deduction. When taxing IA, all incomes related to IA are combined. Taxable IA income is calculated by deducting IA-related deductions. Deductions include IA-related expenses, non-taxable income, previous losses and SSCs (including health SSCs). Furthermore, IA taxpayers can choose between declaring actual expenses and opting for a presumed cost deduction of 30% of IA income (which includes SSCs and health SSCs).

In the IA regime, SSCs are deductible from the PIT base. For Lithuanian employees, SSCs are not deductible from the PIT base (in contrast to most OECD countries). For IA taxpayers, SSCs are deductible. For BC taxpayers, SSCs are not deductible (as are any other expenses for BC activities).

In the BC regime, individuals pay a fixed lump-sum payment. The tax liability is a fixed lump-sum PIT payment that is paid in advance when a taxpayer purchases the business certificate.

In the BC regime, the municipalities set the lump-sum payment and receive the PIT revenues. The amount of the lump-sum payment under the BC regime is set by the municipalities and is allocated to municipality budgets. In contrast, PIT revenues on other SE and employment income are set by central government (and allocated between central and local government).

The BC regime has an annual revenue cap. To be eligible for the BC regime, taxpayers must have annual revenues below EUR 45 000. Annual revenue exceeding the cap is taxed under the IA regime. The cap is equal to the VAT threshold in Lithuania so BC taxpayers usually do not have to register for VAT. Annual revenues include income from all activities with business certificate combined, except for rent from residential property, which is calculated separately.

Eligibility for the BC regime is limited to certain activities. To be eligible for the BC regime, taxpayers must operate in a specified list of activities set periodically by the government. Each activity requires a separate business certificate. The certificate is only valid for a specified location and time.

SSC rules

SSC rates for the self-employed are lower than for employees, particularly for the business certificate regime. Total SSC rates are highest for employees (21.29%), IA taxpayers (19.5%) followed by BC taxpayers (15.7%) (Table 5.2). When employer SSCs are excluded (which relate to unemployment, occupational accident and diseases and social tax), SSC rates are the same for employees and IA taxpayers. For BC taxpayers, SSC rates are lower as sickness and maternity SSCs are not included.

The SSC base for the self-employed is narrower than for employees, particularly for the business certificate regime. SSCs due are calculated by applying SSC rates (Table 5.2) to the SSC base. The SSC base is insurable income and differs by organisational form (Table 5.3). In the IA regime, the SSC base is 90% of taxable IA income (before SSCs are deducted). For health SSCs in the IA regime, there is an SSC floor so that insurable income cannot fall below the MMW. In the BC regime, insurable income is set at the MMW for pension SSCs and health SSCs (i.e. these are the only two SSC rates that apply to the BC). An SSC floor and ceiling apply to employees but not to the SE regimes (except for the health SSC in the IA regime).

Before considering the BC and IA regime in detail, this section provides an overview the income distributions and demographic characteristics across the regimes based on the microdata.

Applying the microdata to self-employment

Self-employed taxpayers are defined in the microdata as those with meaningful self-employment activity. To identify taxpayers with meaningful self-employment activity, self-employed taxpayers (SE) are defined as are non-pensioners (i.e. have no pension income) with SE income representing at least 15% of employment wage income plus SE income (Table 5.4). On this basis, there are 5,660 SE (8% of the three categories of taxpayers). Of these, 62% derive all of their income from SE and 38% from a combination of SE income and employment income. The SE group is further divided into the IA regime (64%) and BC regime (36%).

Comparing single income source groups is a useful empirical simplification. Since PIT applies to a wide range of incomes (e.g. employment, self-employment, dividends etc), a useful empirical simplification is to compare taxpayer groups with a single income source such as comparing ‘pure employees’ (i.e. employees with only employment income) with ‘pure self-employed’ (i.e. self-employed with only self-employment income).

Self-employed incomes

Incomes are higher in the individual-activity regime than the business certificate regime due the cap on business certificate income. The income distribution of the two SE regimes is similar for most of the distribution but diverge at the highest incomes (Figure 5.4, Panel A), reflecting the smaller number of outlying high incomes in the BC regime (this is ensured by the BC regime annual revenue cap). Below the cap, BC taxpayers have modestly higher incomes for most of the distribution (Figure 5.4, Panel B). The IA regime has higher income inequality, reflected in a higher P80/20 ratio of 14 compared to 9 in the BC regime. IA and BC income refer to SE income derived under those regimes respectively and employee income refers to gross wage employment income.

However, when an adjustment is made for outliers and time spent working, business certificate taxpayers have higher self-employment income on average than individual activity taxpayers. IA taxpayers have higher mean SE income than BC taxpayers (+64%). A more appropriate comparison across the two regimes using median income shows that ‘pure’ BC taxpayers (i.e. SE income derived only from the BC regime) have 30% higher income than ‘pure’ IA taxpayers (i.e. SE income derived only from the IA regime). Furthermore, adjusting for the fact that BC taxpayers work about one-third less than the IA self-employed throughout the year (as proxied by the median number of months worked, see note Table 5.5), BC incomes are almost twice as high (+95%).

Compared to business certificate taxpayers, individual activity taxpayers earn higher average incomes from other sources such as employment and capital income. Other income sources tend to be higher on average in the IA regime including employment income (+23%) and dividends, interest and royalty income (+39%).

Note: Mean value calculated in each percentile so the figures do not correspond precisely to Table 5.5.

Source: OECD analysis of microdata.

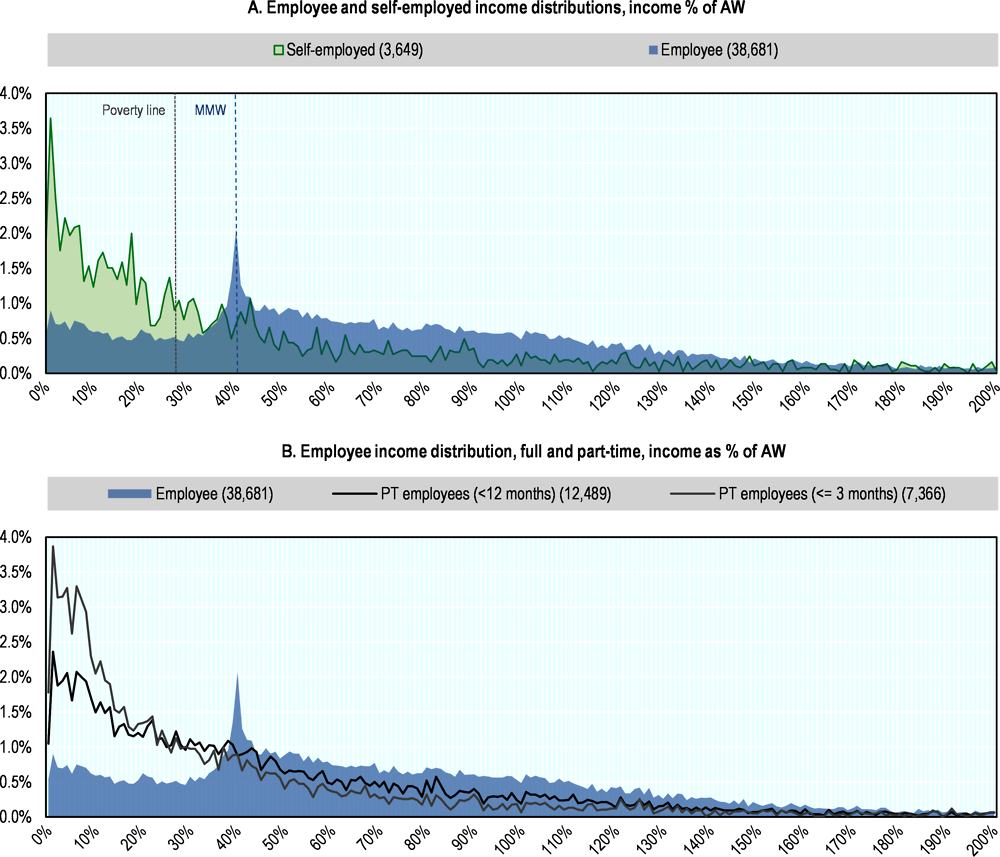

A high share of SE may be at risk of poverty. The IA taxpayer income distribution is positively skewed with many SE earning low incomes (Figure 5.5, Panel A). IA incomes are significantly below employee incomes. Half of IA taxpayers (54%) earn below the MMW compared to just one-quarter (25%) of employees. There is income bunching among employees at the MMW (Figure 5.5, Panel A).

A high share of part-time employees report very low incomes. Part-time (PT) employees3 working less than 12 months of the year and 3 months or less of the year earn much less than employees generally (Figure 5.5, Panel B). The share of PT employees in the former and latter groups earning below 10% of the AW is 20% and 32% respectively. Of taxpayers with both employment and SE income, about in 1 in 5 are PT employed (19%) according to the microdata. 2% are employed for 3 months of the year and have average income of EUR 753 (employment and SE income) vs EUR 2,187 for FT (i.e. 12 months of the year).

Note: The minimum monthly wage (MMW) is EUR 555 in 2019. The average wage refers to the gross average wage from employment in 2021 calculated by the OECD secretariat. The self-employed and employee income distribution refers to total self-employment income and gross employment income respectively. The self-employed and employee groups are as defined in Table 5.5. The part-time employee groups refer to employees who work a number of months in the year which is less than 12 and 3 or less respectively.

Source: OECD analysis of microdata.

Self-employed demographics

Compared to employees, the self-employed are more likely to be male and married. Compared to employees, the SE are on average more likely to be male (+7% p.p.) and married (+9% p.p.) (Table 5.6). The age distribution and family structure between SE and employment are broadly similar.

The two self-employment regimes are broadly demographically similar, although business certificate taxpayers are more likely on average to be older, female, married and work part-time. Comparing between the two SE regimes, BC taxpayers are modestly more likely than IA taxpayers to be female (+4% p.p.) and married (+5% p.p.) (Table 5.6). BC taxpayers are more likely to work part-time (a median of 8 months annually compared to 12 months in the IA regime, see note from Table 5.5). BC taxpayers are older on average as group because there are less BC taxpayers under the age of 35 compared to the IA regime. The demographic characteristics of the SE regimes, and particularly the BC regime, have some similarities to the typical demographics of second-earners (as discussed previously, second-earners in Lithuania have strong work incentives at long-unemployment spells beyond 12 months). There is little statistical difference in family size and the prevalence of reported disability between the two SE regimes.

This section provides discussion, observations and recommendations on the design of the business certificate (BC) regime and its interaction with the individual-activity (IA) regime and standard employment. Its adherence to tax policy principles is discussed followed by the design of eligibility criteria, the determination of the tax liability, the role of migration from the regime and tax rate design. This section draws from a forthcoming OECD paper on the design of presumptive tax regimes ( (Mas-Montserrat et al., forthcoming[1])).

Eligibility design

The business certificate regime is a presumptive tax regime since it is not based on actual taxable income but rather on a presumed tax base. Presumptive tax regimes differ on the method used to make that presumption. In general, presumptive tax regimes do not aim to raise significant amounts of tax revenues but instead to improve tax compliance over the long term. This may justify tax revenue collection costs that exceed the tax revenues collected in the short term (Engelschalk, 2007[3]).

Revenue eligibility caps keep compliance costs low for taxpayers and enforcement costs low for tax admins but revenue measures can be relatively easily manipulated. Presumptive regimes commonly operate eligibility caps based on revenues (Thuronyi, 2004[4]). The design of revenue caps are simple, which keep compliance costs low for taxpayers and enforcement costs low for the tax admin. On the other hand, reported business revenues are relatively easy for taxpayers to manipulate.

The revenue cap influences the numbers of taxpayers in the self-employment regimes which in turn affects the levels of tax revenues and tax transparency for the authorities. Since SE move between regimes, the level at which the revenue cap is set will influence the numbers of SE in each regime, which in turn has tax policy implications. A high cap mechanically implies more BC taxpayers which means lower tax and compliance burdens for SEs but reduced tax revenues and information available for the authorities (Table 5.7) (BC taxpayers do not have to report costs reducing transparency and monitoring capabilities for the tax administration). Inversely, a lower cap implies more IA taxpayers which means higher tax and compliance burdens for SEs and increased tax revenues and transparency for the authorities (Table 5.7).

The revenue cap should be aligned and evolve with the capacity of the tax admin. From a tax admin perspective, the tax affairs of IA taxpayers are likely to have greater complexity and administrative burden than BC taxpayers (e.g. they report more information such as business costs on a more regular basis). Therefore, policies that shift the SE from the BC to the IA regime may increase the administrative burden on the tax admin (and vice versa). An example of such a policy is reducing the BC regime revenue eligibility cap (Table 5.7). Consequently, policies that shift the SE to the IA regime should be done with regard to the current and evolving capacity and capability of the tax admin to effectively manage and monitor the expected increase in the number of IA taxpayers arising from that policy.

The revenue cap may be too high, resulting in too many business certificate taxpayers and too few individual activity taxpayers (and lost tax revenues). The BC regime revenue cap is high in the context of the SE income distribution. 92% of IA regime SE have incomes below the cap and by design 100% of BC regime SE have incomes below the cap (Figure 5.6). Compared to selected presumptive regimes internationally (in USD PPP), the cap for the BC regime (USD 97 826) is above comparable regimes for unincorporated self-employed in Hungary (KATA regime, USD 77 499), similar to Italy (régime forfaitaire, USD 99 335) but below France (régime du micro-entrepreneur, USD 242 926). If the cap were cut to EUR 20000, about 20% of BC taxpayers would enter the IA regime (assuming no income responses to the cut). Given the wide tax burden gap between regimes (Figure 5.10), the cap should not be set too high as it extends BC eligibility too widely and reduces the standard IA regime thus undermining horizontal equity and tax revenues.

A high share of low-income SE in the IA regime may raise design rationale questions for the BC regime. Over half of IA taxpayers (54%) have incomes of 30% of AW or less. This may raise questions of the design rationale and targeting of the BC regime to the extent that it is aimed at supporting low-income SE in entering SE and growing as businesses with the eventual intention of migrating to the IA regime. Income comparisons between the regimes will also be affected by the BC regime being restricted to certain activities.

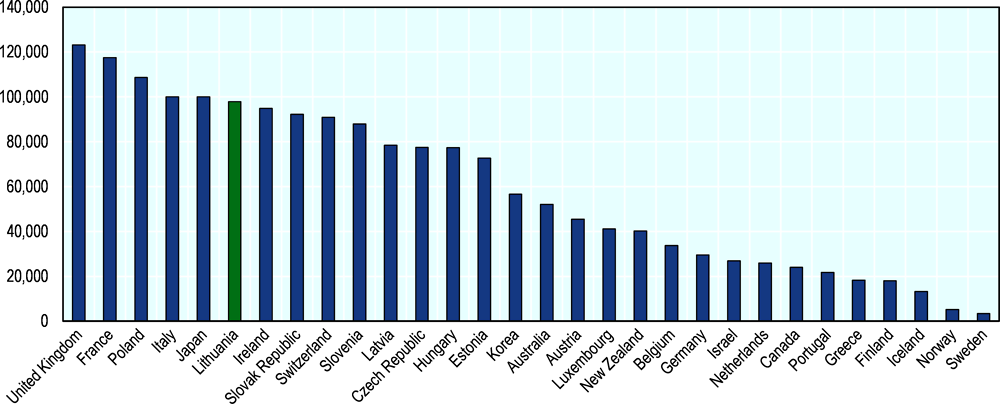

The alignment of the business certificate cap with the VAT threshold comes with advantages and drawbacks. The VAT registration threshold in Lithuania is high in international comparison (Figure 5.7). A case for alignment is that SE that have the capability to comply with VAT-related accounting and administration should also be able to maintain records and calculate their taxable profits under a standard regime (i.e. the IA regime). However, alignment implies that changes to PIT and VAT policy can jointly impact the regime. For example, VAT or PIT simplification measures or improvements in VAT refunds could make the IA regime more attractive, thus likely reducing the number of SE opting for the BC regime.

The business certificate sector eligibility criteria has the potential to produce vertical and horizontal inequities that might introduce competitive distortions. The BC regime is only available to SE operating in certain specified business activities, which could produce inequities. First, BC taxpayers with different turnover and costs but in the same sectors will face the same tax liability (‘vertical inequity’). Second, IA taxpayers that perform similar activities to BC taxpayers that are ineligible for the BC regime might have similar profits but face different tax burdens (‘horizontal inequity’). Third, taxpayers with similar profits just above and below the revenue cap but in different regimes would face different tax burdens (‘horizontal inequity’) (see Figure 5.9). An estimation of the extent of taxpayers that would be exposed to these various inequity risks could be investigated in the microdata.

Good practice suggests that revenue caps should generally be inflation-indexed. When the eligibility criteria is revenue, good practice is to index the cap to inflation to prevent erosion over time (Thuronyi, 2004[4]) (Bird and Wallace, 2004[5]) . Given currently high levels of inflation, non-indexation will shift SE from the BC to the IA regime. As this report recommends to lower the revenue eligibility cap, the cap could be lowered and subsequently inflation-indexed.

Tax liability design

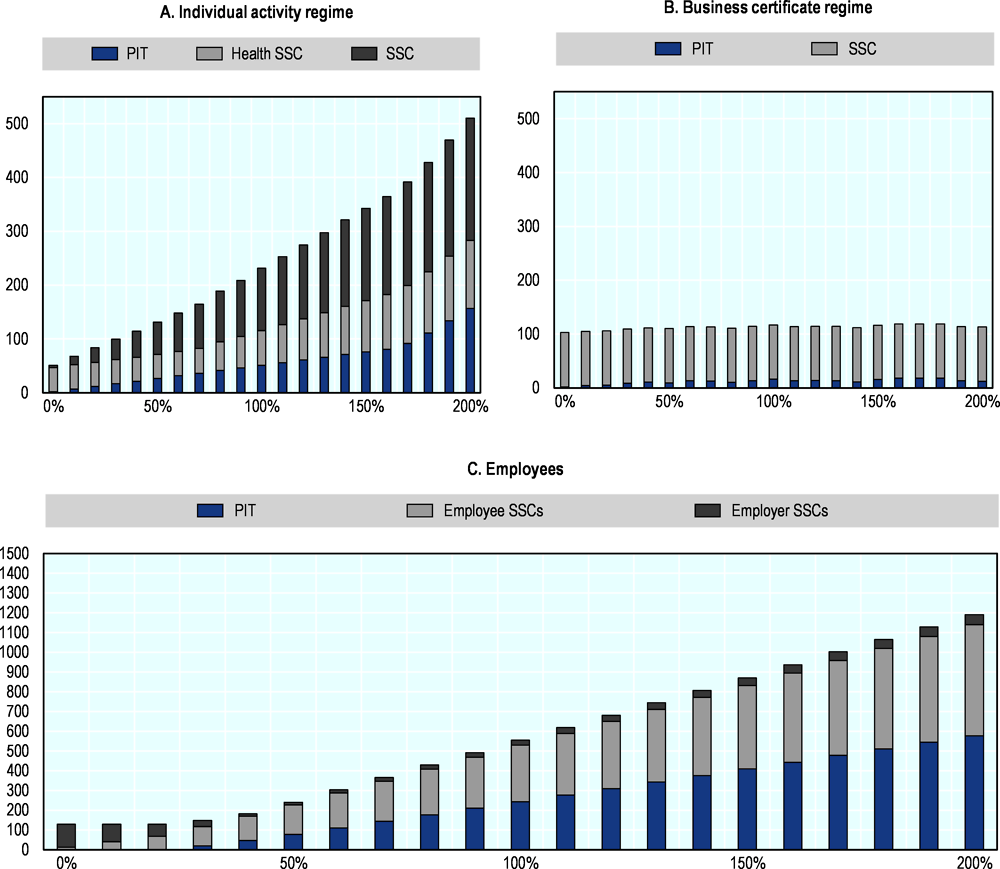

The business certificate’s lump-sum payment has advantages, principally its simplicity. There are several approaches to determining the tax liability in presumptive tax regimes including applying lump-sum payments and tax rates. The lump-sum payment operated in the BC regime has several advantages (Figure 5.11) as follows:

1. It is transparent and predictable, resulting in low compliance costs for taxpayers and low enforcement costs for the tax admin.

2. It is a low payment in relative and absolute terms, which helps encourage informal workers to enter the regime and to ensure voluntary compliance.

3. Since the tax is set by the municipalities, there is no computation cost for BC taxpayers.

4. Since BC taxpayers do not have to declare costs (only turnover), the administrative costs of record-keeping and accounting are low.

5. It avoids creating disincentives for businesses to grow since the tax payment remains fixed as income increases.

The lump-sum payment has several drawbacks, particularly its regressivity.

1. It is regressive and places a higher tax burden on the poorest SE by treating all taxpayers equally regardless of their income and ability to pay.

2. It is regressive relative to alternative approaches to determining tax liability in presumptive regimes. A lump-sum payment is regressive relative to a lump-sum payment that is differentiated by sector of activity or within turnover bands. It is also regressive relative to proportional or progressive tax rates levied on turnover. While such alternatives can improve progressivity they also come with several drawbacks including increased complexity.

3. A fixed amount may not allow for the tax burden to fluctuate when economic activity and incomes drops thus creating cash flow challenges (ILO, 2021[6]). However, the government can opt to make periodic adjustments to the amount.

4. It may create an entry barrier for businesses that do not make profits as losses cannot be offset against future liabilities.

5. Given the population of lump-sum payments in countries that implement them, they may be difficult to abolish (Bucci, 2020[7]).

An alternative to the lump-sum payment approach is a proportional tax rate on turnover. Compared to the lump-sum payment, a proportional tax rate results in a tax liability that is linear relative to revenue, making it less regressive than the lump-sum payment. Since taxpayers in the BC regime already declare turnover (but not costs), the operation of a proportional tax rate on turnover would add a minimal tax compliance burden in terms of computing the tax liability. However, proportional tax rates have drawbacks including that reported turnover measures are relatively easy to manipulate, which introduces non-compliance risk.

The proportional tax rate on turnover could vary by business sector profitability. Differentiated tax rates across sectors would allow levying a higher rate on the activities that are on average more profitable. This would prevent highly profitable businesses facing a low presumptive tax burden who would face a tax-induced incentive to remain in the BC regime and not migrate into the IA regime. On the other hand, differentiated sector tax rates are based on average profitability rates which means that high profit business in a sector with low average profits will not be highly taxed. Differentiated sector tax rates also produce a tax-induced incentive for businesses to reclassify their sectoral status to more lightly taxed sectors.

Migration from the business certificate regime

The design of the tax system should provide businesses with an incentive to migrate from the business certificate to the individual-activity regime. A smooth transition from a presumptive to a standard regime might be achieved by introducing simplified tax provisions and administrative procedures in the standard regime (e.g. reduced rates, simplified accounting, simplification of VAT-related administrative procedures) (Engelschalk, 2007[3]). However, such features might need to be time-limited to prevent potential disadvantages such as bunching effects and artificial closing and reopening of business activities.

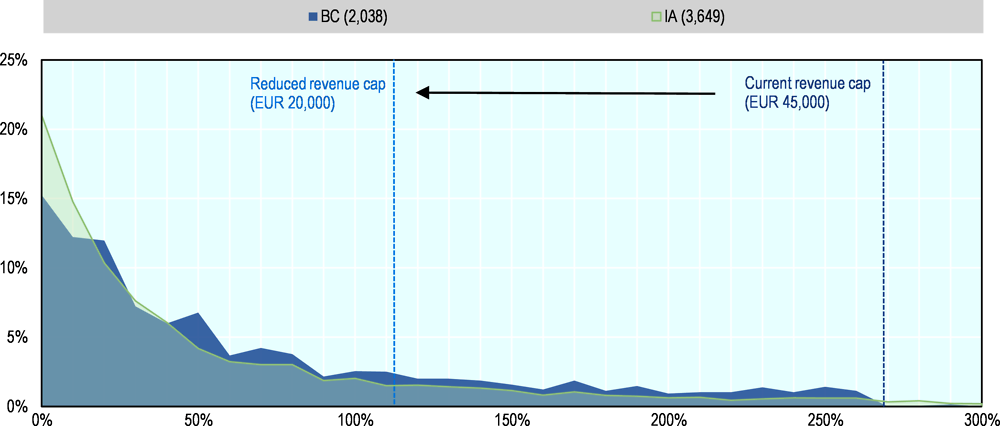

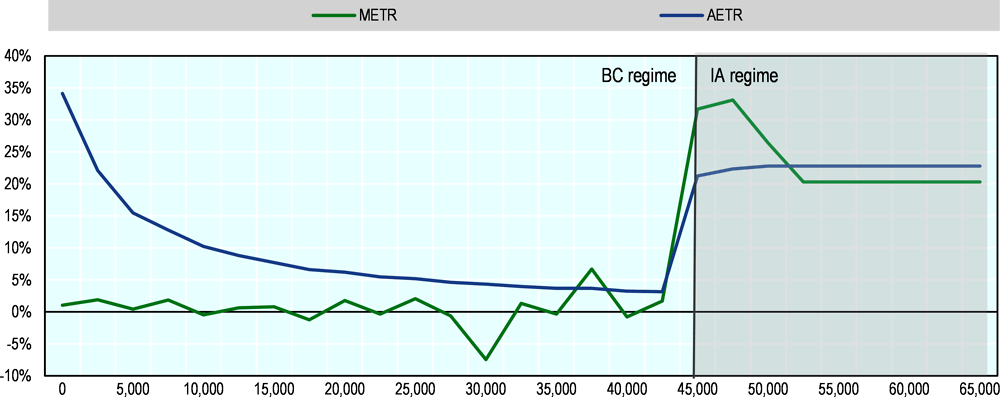

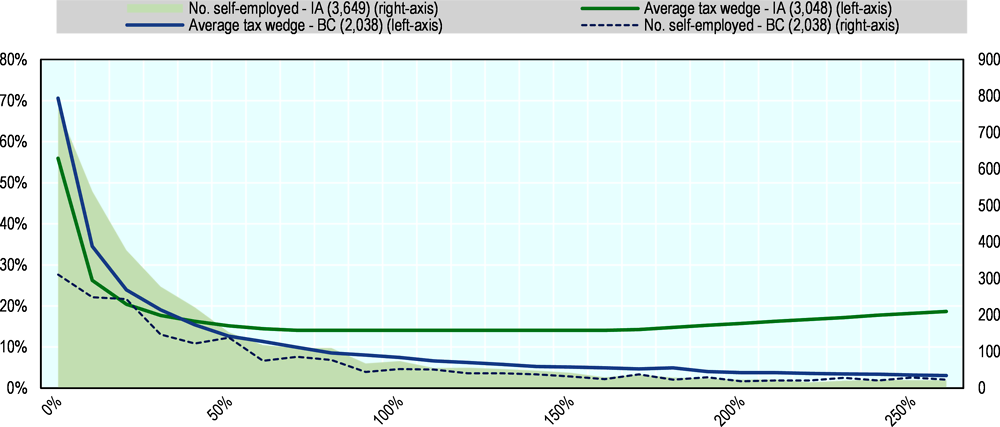

However, a sharp rise in the marginal tax wedge as taxpayer’s transition to the individual-activity regime is likely to deter migration. Up to the BC regime eligibility cap, METRs remain flat and close to zero as taxes remain unchanged with higher incomes (Figure 5.8) (the fluctuation in the METRs is due to fluctuations in the average PIT reported on the tax records within the income bands and sample size issues). Once the cap is reached, the SE enter the IA regime and then face higher METRs (Figure 5.8) due to higher SSCs and a progressive PIT (see Figure 5.10).

Note: Marginal and effective tax rates are calculated for the BC and IA regimes below and above the EUR 45 000 revenue cap respectively. Self-employment incomes are shown in bands of EUR 2 500. The hypothetical IA regime average effective tax wedges (AETR) and marginal effective tax wedges (METR) are calculated based on the tax rules using IA self-employment income from the tax records for taxpayers who opt for the presumed cost deduction and have only self-employment income. In the BC regime, the AETR and METR are calculated using business certificate PIT paid and business certificate income on the tax records in addition to a hypothetical calculation of SSCs.

Source: OECD analysis of microdata.

Income bunching below the business certificate eligibility cap reflects the disincentive to migrate to the individual-activity regime and the administrative burden of VAT registration. The share of BC self-employed spikes just below the BC regime cap and VAT threshold of EUR 45 000 (Figure 5.9). This suggests that some BC taxpayers may be under-reporting incomes to avoid VAT registration or the IA regime or a combination of both. BC taxpayers that exceeded the threshold would migrate to the IA regime and face higher average and marginal tax burdens in this income range (Figure 5.8) in addition to higher administrative burdens associated with VAT compliance. If taxpayers were to supress reported incomes, which they have an incentive to do, there could be additional undetected income bunching. The sample tax record data indicate that 3.9% of BC report SE income between EUR 40 000 and EUR 45 000, which implies approximately 3 500 taxpayers nationally in that income range.4 The share of IA taxpayers is greater between EUR 40 000 and EUR 45 000 than it is between EUR 45 000 and EUR 50 000 (Figure 5.9), suggesting that some IA taxpayers could be misreporting incomes to avoid VAT registration. These interpretations remain suggestive rather than conclusive in the absence of the larger sample size of the full tax record data and multivariate analysis that controls for multiple variables. As further work, longitudinal tax record data could be employed to track and identify the type of self-employed that switch from the BC to the IA regime (and vice versa) and the role of the tax burden in that decision.

The tax burden in the business certificate regime is low relative to standard employment and individual activity (except at low incomes)

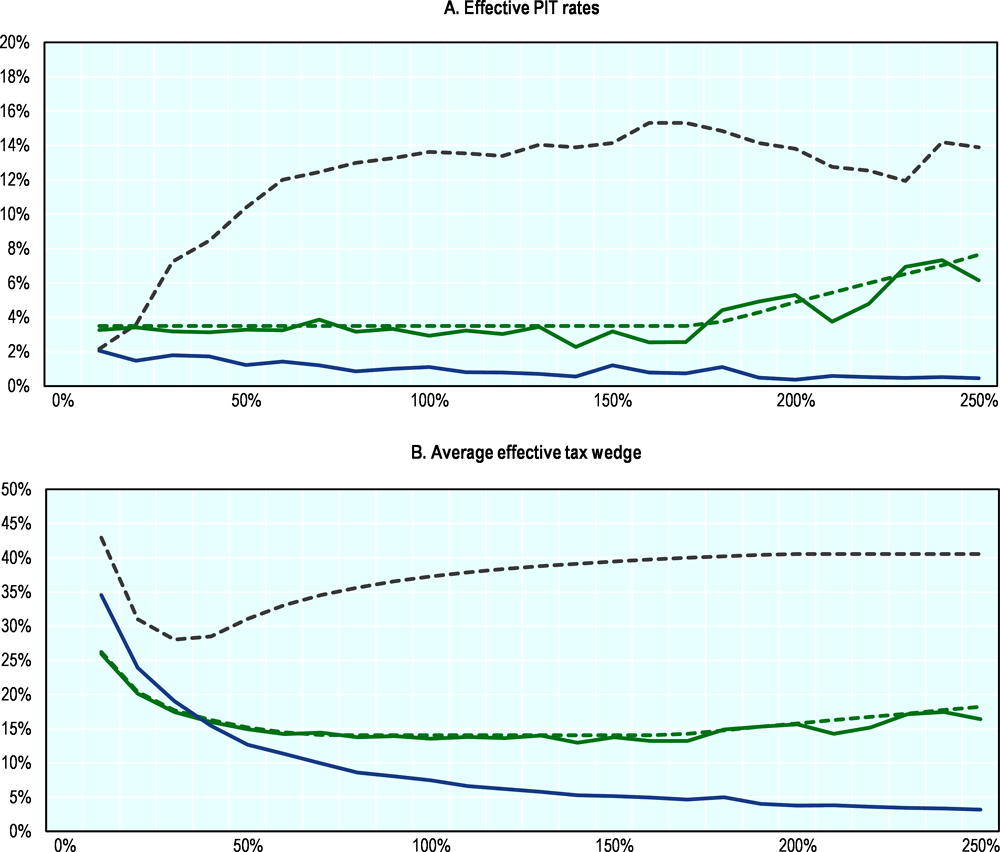

Effective PIT rates in the business certificate regime are below those in the individual activity regime across the income distribution based on the tax record data. In the BC regime, average effective PIT rates (i.e. business certificate PIT paid as a share of business certificate income on the tax records) are lower than the IA regime across all gross incomes (Figure 5.10).

However, a relatively high SSC floor in the business certificate regime implies that low-income self-employed could prefer the individual activity regime. Due to a relatively high SSC floor in the BC regime (the base is set at the MMW), the average tax wedge under the BC regime is higher than under the IA regime at low incomes (below 30% of AW) but becomes progressively lower at higher incomes (comparing Figure 5.10, Panels A and B) (note that very low incomes are not shown but examined later in Figure 5.12). This occurs because SSCs are calculated as a share of income in the IA regime and PIT rates increase at higher incomes whereas SSCs and PIT remain flat in the BC regime leading to a decline in the average tax wedge. These tax burdens imply that the self-employed may prefer the IA regime at low incomes and the BC regime at middle and higher incomes up the revenue cap of EUR 45 000. Since many SE earn low incomes (47% of IA SE earn incomes less than 30% of the employee AW based on the microdata), a significant share of low-income SE may prefer the IA regime at low incomes. In the IA regime, both hypothetical and empirical PIT and average tax wedges are calculated for robustness based on the tax rules and the tax record data respectively (see note in Figure 5.10). The IA regime calculations are based on self-employed who opt for the presumed cost deduction (see note in Figure 5.10).

Note: Note that the tax wedges are based on gross income for employees and self-employment income for the self-employed. Incomes are shown as a share of the employee AW in 2021 and are divided down into 10% bands. Incomes start at 10% of the AW. The employee PIT rate is calculated as PIT as a share of total employment wage income based on the tax records. The employee average tax wedge is calculated using the Taxing Wages 2021 model as employee SSCs are not available in the tax record data. The hypothetical individual activity self-employment PIT rate and average tax wedges are calculated based on the tax rules using self-employment income from the tax records and for those who opt for the presumed cost deduction. The empirical individual activity self-employment PIT rate and average tax wedge are based on the PIT variable in the tax records (SSCs are not available in the tax records so the SSC rules are used) for those who opt for the presumed cost deduction and with self-employment income. In the BC regime, the effective PIT rate is the business certificate PIT paid on the tax records as a share of income from business certificate income. In the IA and BC regime, the PIT rate is calculated using the ‘tin’ and ‘tbl’ variables as a share of individual activity and business certificate income respectively. In a small number of cases in the business certificate regime, the sample size is too small to calculate the average tax rate within an income band so the average tax rate is assumed that of the previous band.

Source: OECD analysis of microdata.

The average effective tax wedge in the business certificate is far below that of employees at all incomes. The average effective tax wedge for employees always exceeds those of both self-employment regimes driven by higher employee and employer SSCs at low incomes (Figure 5.10, Panel C) and significantly higher PIT rates (Figure 5.10, Panel A).

Average effective tax wedges are high at very low incomes across several organisational forms driven by different SSC floors. At very low incomes between 0 - 10% of AW (not shown in Figure 5.10), the average tax wedges are similarly high across all organisational forms due to different SSC floors. In the BC regime, the average tax wedge is 71% (due to the minimum SSC base set at MMW and the lump-sum payment), in the IA regime 63% (due to the minimum health SSC floor) and for employees 70% (due to the employer SSC floor). Note that the employer SSC floor does not apply to all SE because not all SE are obliged to pay SSCs (e.g. SE that have reached retirement age, SE receiving the social insurance old-age pension).

Note: Notes for Figure 5.10 apply. In charts A and B, PIT reported on the tax records are used. In chart C, PIT is calculated using Taxing Wages 2021 model.

Source: OECD analysis of microdata.

The income distribution shows that the lowest income self-employed prefer the standard individual-activity regime to the business certificate regime. As shown in Figure 5.12, the higher average tax wedge in the BC regime relative to the IA regime at low incomes could lead to the lowest income SE preferring the standard IA regime to the presumptive BC regime. When the income distribution of the IA and BC regimes is overlaid alongside the average tax wedges in the two regimes, a high share of the lowest income self-employed are in the IA regime both in absolute terms and relative to the numbers in the BC regime (Figure 5.12). This may suggest that some SE are choosing the IA regime over the BC regime to avail of a lower tax burden. A range of other factors may play a role in the low-income SE opting for the IA regime including restrictive eligibility criteria for entering the BC regime such as the list of eligible activities.

The tax burden on the lowest income self-employed is high relative to reported self-employment incomes. Although the tax wedge is higher in the BC than the IA regime at low incomes, it remains high in both regimes, which could produce a disincentive for the SE to formalise their business in either regime. There is however a tax vacation for new IA taxpayers to encourage formal work. The high tax wedges may also be a result of low reported SE incomes. The absolute PIT and SSCs are quite low. If the true incomes of the SE were higher than those reported, which could be the case in some cases given relatively high reported informality in Lithuania generally, the true tax burdens faced by the SE would be lower.

Source: OECD analysis of microdata.

Illustrative simulations of reform options

Aligning the average PIT rates in the business certificate regime with those in the individual-activity regime would raise average effective PIT rates and PIT revenues. An illustrative indication of PIT revenues in the BC regime can be estimated across the income distribution by applying the average PIT rates in Figure 5.12 to the total BC income of EUR 823 million in 2019 (see note in Figure 5.13). This approach gives a reasonable estimated PIT revenues of EUR 7.8 million compared to actual BC PIT revenues of EUR 8.5 million in 2019. To give an indication of aligning the tax burden between regimes, the average effective PIT rates in the IA regime can be applied to total BC income by income band, which shows that average PIT rates would increase across the income distribution and PIT revenues would increase by a factor of 4.7 (Figure 5.13).

An illustrative simulation of a low proportional tax rate on turnover in the business certificate regime serves to highlights that the existing lump-sum payment amount produces very low tax effective rates in the regime. To illustrate the proportional tax rate approach in the BC regime, a 3% tax rate levied on BC turnover would raise the effective PIT rate on BC taxpayers across all incomes and increase PIT revenues by a factor of over 3 (Figure 5.13) (note that PIT revenues are not increasing with higher average PIT rates at higher incomes due to fewer BC taxpayers at higher incomes). The proportional tax rate on turnover serves to highlight how even a low proportional tax rate on turnover would substantially increase effective PIT rates and PIT revenues compared to the existing approach.

Note: Since the tax record data is based on a sample, BC incomes are ‘grossed-up’ to the national level using the total BC income of EUR 823 million in 2019 based on the Budget Revenue Report 2021. First, to estimate PIT revenues in the BC regime, average PIT rates in Figure 5.12 are applied to the BC income by income band for incomes between 0 and 260% of AW (which represents 97% of BC income; sample size restricts average PIT rates above 260% of AW). PIT revenues in the BC regime are estimated at EUR 7.8 million compared to actual PIT revenues of EUR 8.5 million in 2019. Second, average PIT rates in the IA regime in Figure 5.12 are applied to BC income across the same income bands (e.g. for many income bands at a rate of 3.5% as PIT is calculated on taxable income and assuming a presumed cost deduction of 30%). Third, a 3% turnover rate is applied to BC income.

Source: Budget Revenue Report 2021, Ministry of Finance of the Republic of Lithuania. OECD analysis of microdata.

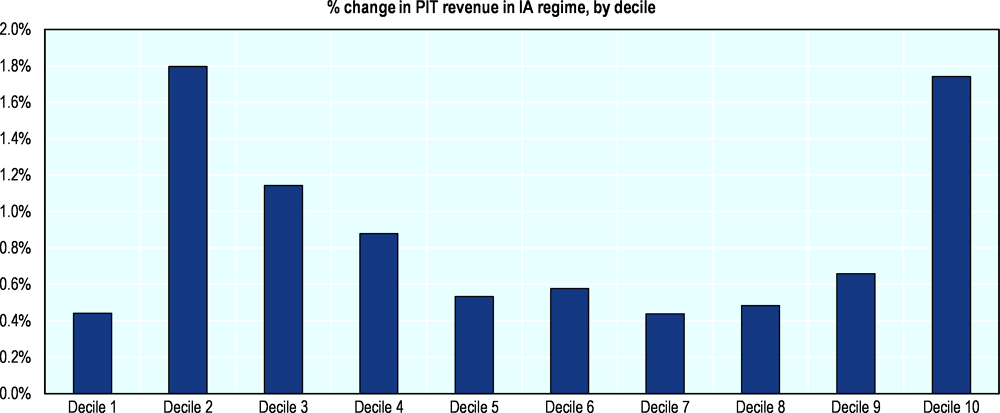

Replacing the fixed lump-sum payment in the BC regime with a 3% proportional tax rate on turnover would increase total PIT revenues by 0.5%. According to modelling in EUROMOD, the reform would produce relatively high increases in PIT revenues in lower equivalised household disposable income deciles (Figure 5.14). This is partly because most BC taxpayers earn very low incomes and pay very low PIT. The reform would increase income inequality by 0.0556 percentage points as measured by the S80/S20 ratio.

Note: Deciles refer to equivalised total household disposable income. PIT refers to total PIT paid from all income sources (i.e. including employment income and SE income).

Source: Simulations performed by the EUROMOD team of the European Commission’s Joint Research Centre (JRC).

Adherence of the business certificate regime to tax policy principles and tax liability reform options

The business certificate regime violates the principle of horizontal equity. The BC regime has very low tax burdens on taxpayers with similar incomes relative to the IA regime (Figure 5.10). This violates the principle of horizontal equity which states that similar (in this case, on the basis of income) SE taxpayers should be taxed similarly. The departure from the horizontal equity principle in the BC regime requires a justifying rationale. It follows that the significant tax burden differential between the regimes requires a correspondingly significant justifying rationale. A rationale may be that BC taxpayers face different economic realities to other SE forms that justify a lower tax burden. However, this does not seem to be supported based on broadly similar demographic characteristics between the SE regimes (Table 5.5 and Table 5.6) and higher median incomes in the BC regime when adjustments are made for time spent working (Table 5.4).

The departure from horizontal equity has implications for tax neutrality. The current design of the BC regime is likely to violate the principle of tax neutrality by influencing organisational form decisions. IA taxpayers have a tax-induced incentive to reclassify their sector of activity to fit those eligible for the BC regime and to supress their income below the BC cap. Employees have a tax-induced incentive to reclassify as SE and enter the BC regime. These tax arbitrage opportunities risk higher numbers of taxpayers entering the BC regime than would otherwise be the case, which could undermine tax revenues and equity by placing a higher tax burden on employees. The costs of this tax arbitrage produced by the BC regime design should be weighed against the justification for non-neutrality including encouraging the growth of small business and formality.

The revenue eligibility cap could be reduced to target only micro-businesses. The revenue cap is high relative to SE incomes. 92% of IA regime SE have incomes below the cap and by design 100% of BC regime SE have incomes below the cap (Figure 5.6). For example, a reduced cap to EUR 20 000 would narrow the scale of the BC regime (improving horizontal equity) and could mechanically migrate about 20% of higher-income BC taxpayers to the IA regime (an even lower cap could also be considered based on the income distribution). This would raise PIT and SSC revenues and increase transparency for the tax admin (i.e. as costs are not reported in the business certificate).

There are several reform options for raising taxes in the business certificate regime including the following.

1. Increase the lump-sum payment. The existing tax liability approach used in the BC regime of a lump-sum PIT payment set by the municipalities could be increased at the level of the municipalities. In this case, the current design would be retained and only the PIT payment would be increased.

2. Increase the lump-sum payment and incorporate SSCs within the payment, although this approach has limitations. In presumptive regimes, a single tax payment often incorporates SSCs. Including SSCs in a single payment can reduces administrative costs and support tax compliance. Empirical evidence has found that a presumptive tax regime can induce businesses to formalise with the tax administration without necessarily formalising its employees in the social security system (Teixeira, 2021[8]) (Díaz et al., 2018[9]). In the BC regime, the lump-sum payment does not include SSCs, which are calculated separately. As part of increasing the lump-sum PIT payment, the SSC contributions for the BC regime could be consolidated within the lump-sum tax payment. This would have the advantage of simplifying the compliance burden on BC taxpayers. On the other hand, including SSCs within the lump-sum payment would more explicitly break the link between SSCs paid and benefits received, which is an argument for keeping SSCs outside of the presumptive regime. This approach would also raise the question of whether the SSCs should be collected at the local or government level.

3. Replace the lump-sum payment with a proportional tax on turnover and align the tax burden with the individual-activity regime. The lump-sum PIT amount could be replaced with a proportional tax on turnover over the medium-term. The tax burden could be more closely aligned with the tax burden in the IA regime to reduce vertical inequity and arbitrage opportunities. The tax burden would not necessarily need to be exactly aligned with that of the IA regime but reducing the tax burden gap would reduce tax arbitrage opportunities. The appropriate tax burden and tax rates could be set based on an evaluation of the profitability of SE businesses in Lithuania. If profitability differs across sectors, a sector-based approach could be considered.

4. Administrative and accounting training may help to smooth the transition to the individual-activity regime. The BC regime is only valid for a specific time. A BC can be issued for a maximum of one year but can be as short as 5 days. Business certificates can then be renewed. When regimes have eligibility periods such as the BC regime, providing supports such as book-keeping or accounting training may help taxpayers to transition to the IA regime (Engelschalk, 2007[3]).

This section provides discussion, observations and recommendations on the design of the individual-activity (IA) regime and its interaction with standard employment. Its adherence to tax policy principles is discussed followed by the design of eligibility criteria, the determination of the tax liability, the role of migration from the regime and tax rate design. The analysis presented for the IA regime includes self-employed farmers and non-farmers. Since the tax rules differ for farmers, farmers are briefly discussed separately at the end of this section.

Design of the tax credit

In the IA regime, a tax credit is available that cuts the effective PIT rate, particularly for those on lower and middle incomes. Under the IA regime, a tax credit is available based on taxable IA income where there is a legal distinction between taxable income and taxable IA income. The latter is more narrowly defined to include only income and exemptions related specifically to IA (i.e. other income such as income from BC and other exemptions unrelated to IA are excluded). The formula for calculating the tax credit (see equation 1) includes which is annual IA taxable income and which is an identifier set equal to 1 if exceeds EUR 20 000 and 0 otherwise. As a share of IA taxable income, the tax credit is 10% for taxable incomes up to EUR 20 000 and steadily reduced thereafter until it no longer applies at EUR 35 000. Without the tax credit, an IA taxpayer pays an effective tax rate of 15% on taxable IA income. For those with taxable income below EUR 20 000 where the full tax credit applies, the effective tax rate is reduced to 5%. For those with higher taxable income between EUR 20 000 and EUR 35 000, the effective tax rate is higher ranging from 5 to 15%.

Source: Lithuania Ministry of Finance.

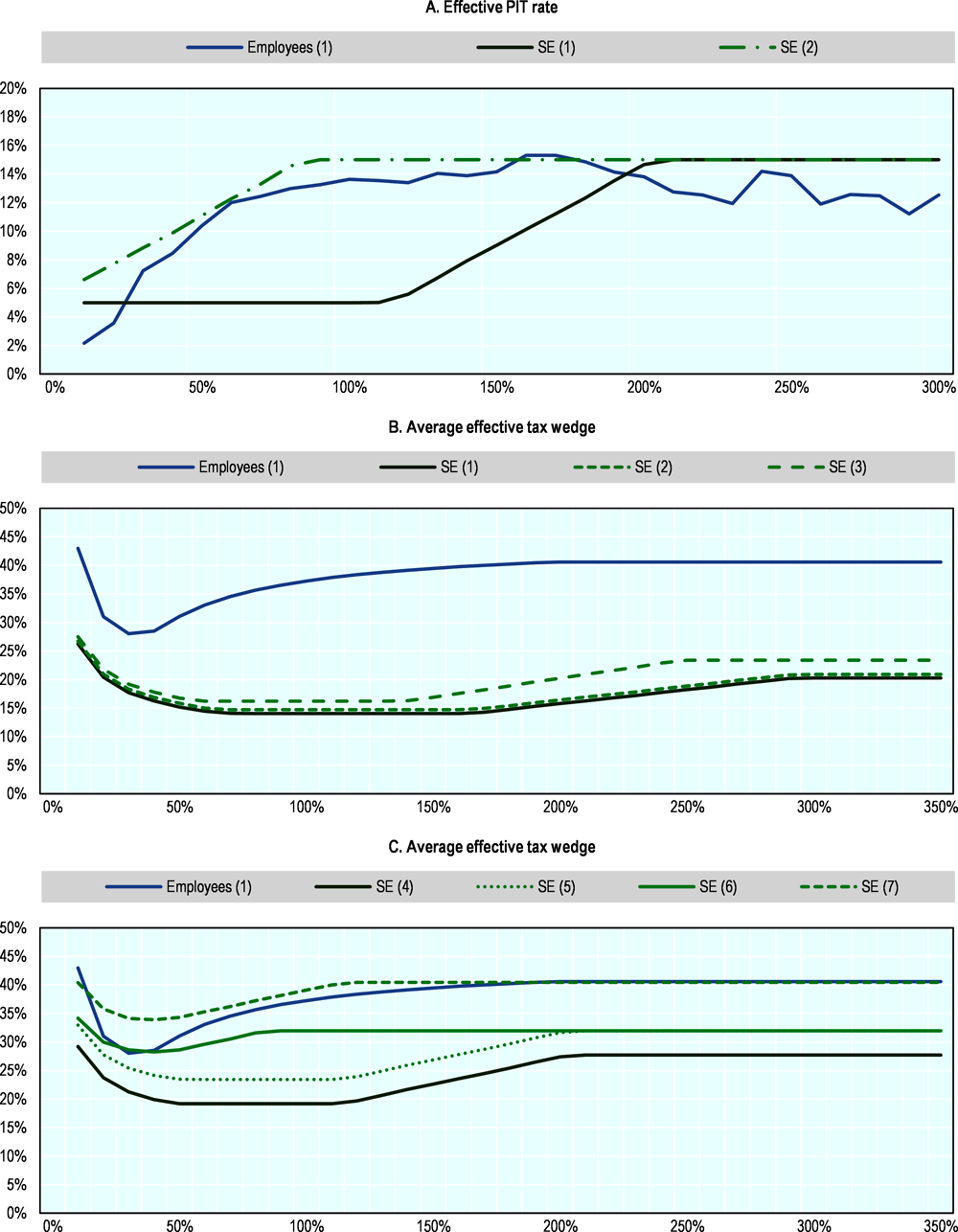

In the IA regime, statutory PIT rates are always lower than in standard employment. As a result of the tax credit, the statutory PIT rate in the IA regime ranges from 5% for incomes up to EUR 20 000 to 15% for incomes above EUR 35 000. Statutory PIT rates for employees are always higher at 20% up to 60 monthly AW (i.e. EUR 104 278 in 2020) and 32% above that. Effective PIT rates on IA taxpayers are also lower at most incomes (see Figure 5.17, Panel A).

The IA regime PIT design will produce rising METRs. As the tax credit is tapered in the IA regime, increasingly higher effective PIT rates are paid on total taxable income (up to the max PIT rate of 15%). As a matter of design, this is unlike in a standard progressive PIT system where a higher PIT rate is levied only on that part of income above a higher PIT bracket. Consequently, the tax credit design will produce rising METRs for IA taxpayers because earning an additional euro of income faces a higher statutory tax rate that applies to the entire taxable income (rather than just the part of income above a higher PIT bracket).

Design of presumptive cost deduction

The presumed cost deduction does not appear to be sufficiently generous to be preferred to declaring actual costs. The presumed cost deduction includes SSC payments that IA taxpayers are required to pay. IA regime SSC rates of 19.5% levied on 63% of gross earnings imply effective SSC rates of 12.3% on gross income. Consequently, the presumptive cost deduction can be represented in two separate deduction components - SSCs (12.3% of gross income) and a standard deduction (17.7% of gross income). The latter deduction component corresponds to the input costs of operating a business. Actual costs faced by small individual SE may exceed 17.7% of income. Indeed, a 30% presumptive cost deduction is low when compared with selected OECD countries (it ranges from 34 – 70% in France and from 14 – 60% in Italy conditional on economic activity5).

However, a majority opt for the presumed cost deduction, which presents a puzzle. Take-up of the presumed cost deduction is high among IA taxpayers (83%) compared to those opting for declaring deductions (17%). One reason could be the increased admin and compliance costs associated of maintaining tax and accounting records that can be disproportionately burdensome for smaller SEs. A further reason is that a majority of IA taxpayers are non-VAT registered (over 9 in 10 report income below the VAT threshold) and therefore cannot benefit from VAT deductions by declaring deductions. Indeed, IA taxpayers with incomes above the VAT threshold opt for the presumed cost deduction less on average. Additionally, few SEs may make tax losses that can then be carried forward to reduce future taxes, which would increase the incentive to declare actual costs. From a non-compliance perspective, it is possible that the presumed cost deduction is chosen as a means to under-report income and minimise information provided to the tax admin instead of declaring actual costs and invoices which would increase information available to the tax admin and might allow for detecting such sales suppression. As a stylised example, if an SE opts for the presumed cost deduction and suppresses sales at the same rate as shadow economy as a share of GDP (i.e. 23% in 2021),6 taxable income would be the same as if they declared actual costs of 46% of gross income. Therefore, in a high informality SE environment reflected in sales suppression, the presumed cost deduction provides an effective deduction that exceeds 30% of income.

Design of SSCs

IA taxpayers can deduct SSCs to reduce their tax burden whereas employees cannot deduct SSCs. The non-deductibility of SSCs from the PIT base for employees implies that employees face higher tax burdens relative to IA taxpayers who can deduct SSCs from gross income (either implicitly through the presumed cost deduction or explicitly by declaring actual costs).

IA taxpayers face the same statutory SSC rates as employees. In the IA regime, the total SSC rate is 19.5%, which is comprised of a general SSC rate of 12.52% (that covers pension, sickness and maternity) and a health SSC rate of 6.98% (Table 5.2). The IA SSC rate is above the BC regime (15.7%) and the same as for employees when employer SSCs are excluded (i.e. 19.5%).

However, IA taxpayers face a narrower SSC base than employees which results in significantly lower effective SSC rates. In the IA regime, the SSC base is 90% of taxable IA income (before SSCs are deducted). For IA taxpayers that claim the presumed cost deduction of 30%, which is most IA taxpayers (83%), the effective SSC base is then 63% of gross income. For IA taxpayers that opt to declare expenses the effective SSC base could be even lower. By contrast, employees pay employee SSCs on 100% of their gross income. The employee SSC base is not reduced by the BA that employees claim.

Compared to employees, the SSC ceiling for IA taxpayers is introduced at a lower income and is more broadly applied (it covers health SSCs) which cuts the tax burden on high-income self-employed relative to high-income employees. For employees, the employee SSC ceiling is 5 annual AW since 2021 and the ceiling excludes health SSCs. In the IA regime, the SSC ceilings is lower at 3.6 annual AW in 2022 and the ceiling applies to health SSCs (unlike for employees) (note that the SSC ceiling cannot apply to the BC regime as it exceeds the BC regime income eligibility cap). For IA taxpayers, the SSC ceilings produce a gradual reduction in the AETR and a sharp fall in the METR at about 384% of the AW which would not occur in the absence of the SSC ceilings. For employees, the SSC ceiling occurs later at 482% of AW and does not change the AETR because it coincides with the simultaneous introduction of the top PIT rate.

Note: There are 3 649 individual activity self-employed in the sample in total and 178 in the above income range.

Source: OECD analysis of microdata.

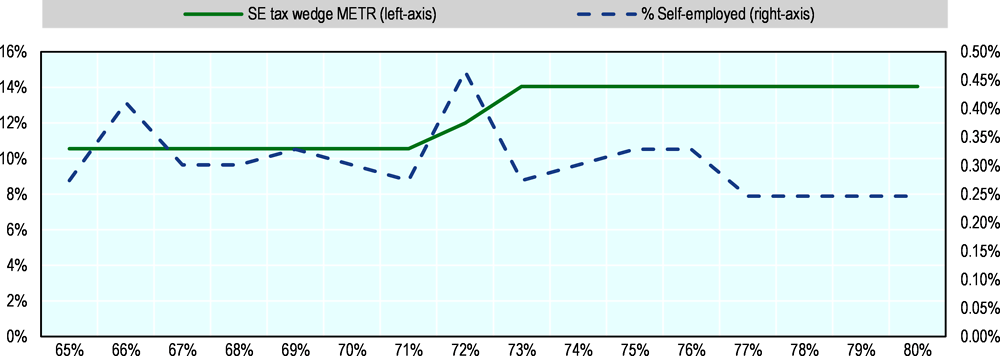

The expiration of the health SSC floor produces an increased marginal tax wedge but few IA taxpayers appear to respond to it. As the health SSC floor is lifted in the IA regime and there is an increase in the marginal tax wedge, there is some evidence of SE income bunching but it is very limited in terms of the share of SE (Figure 5.16).

There may be scope to harmonise SSC and health SSC payments on a monthly basis in the IA regime. IA taxpayers currently pay SSCs on an annual basis and health SSCs on a monthly basis. Converting the annual SSC payment to a monthly payment (assuming automated or directly deducted payments with no additional tax compliance burden for taxpayers) would have the advantage of reducing the risk of SSC arrears to the tax admin and providing taxpayers with a clearer picture of their financial situation throughout the year as payments are made monthly.

The tax burden in the IA regime is low relative to employment

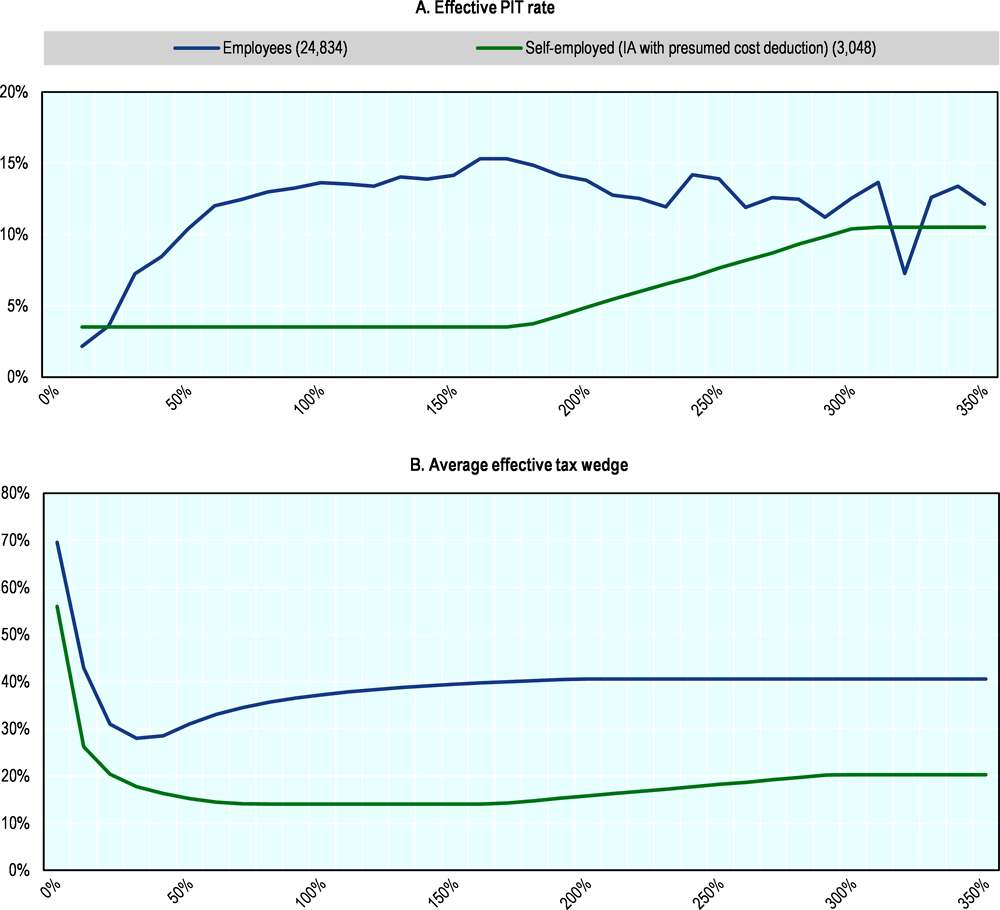

Most IA taxpayers face an effective PIT rate of 3.5%, far below that of employees. With regard to the PIT base, IA taxpayers pay PIT on taxable income reduced by deductions (presumptive or declared) whereas employees pay PIT on gross income reduced by the basic allowance. This results in IA taxpayers having higher effective PIT rates than employees at low incomes below about one-third of AW (i.e. the BA means low-income employees pay no PIT) but higher effective PIT rates above that (Figure 5.17, Panel A). Most employees across the income distribution face high and flat effective PIT rates (Figure 5.17, Panel A). For example, effective PIT rates for employees are 9% at 1/2 the AW, 16% at the AW and 20% at twice the AW (Figure 5.17, Panel A). With the exception of low incomes where the BA exempts employees from paying any PIT, IA taxpayers face significantly lower effective PIT rates at all incomes.

IA taxpayers face an average effective tax wedge lower than employees at all incomes. While the shape of the average tax wedge across the income distribution is similar between IA and employees (i.e. it is relatively compressed and flat), it is significantly lower for IA, particularly at incomes above half the AW. The IA tax wedge ranges from about 1/3 to 2/3 of the employee tax wedge for most of the distribution (Figure 5.17, Panel B). In other words, between 50% and 150% of the AW, the employee tax wedge is about 21 percentage points higher than the IA tax wedge. At low incomes, the IA tax wedge is relatively higher due to the health SSC floor but it remains below that of employees. Due to the BA and the exclusion of employer SSCs, the net personal average tax rate (NPATR) for employees is below the IA average tax wedge up to about 1/4 of the AW.

The microdata confirm that PIT rates and average effective tax rates are lower for IA taxpayers than employees. Compared to the previous hypothetical models (Figure 5.17), when microdata is used to calculate the effective PIT rate and AETR (average effective tax wedge as calculated in Figure 5.18) similar patterns emerge – IA taxpayers face lower tax burdens than employees (Figure 5.18) (for the purposes of the analysis, only 84% of IA that opt for the presumed cost deduction are included and the AETR for employees is calculated using Taxing Wages 2021, see note (Figure 5.18).

High-income IA taxpayers face rising METRs as the tax credit tapers. For employees, the first spike in the METR (marginal tax wedge as calculated in Figure 5.18) occurs as employees first start to pay PIT and the second spike occurs as the max BA starts to taper-out. Since many employees earn incomes at 1/3 and 1/2 the AW, the income-bunching risk from high METRs is greater. For the IA, over the same income range, the METR is by contrast relatively flat (with a modest increase as the health SSC floor expires) suggesting limited incentives to distort behaviour (Figure 5.17, Panel C). At higher incomes however, the design of the SE regime produces elevated METRs. As the tax credit is tapered at taxable income of EUR 20 000 (i.e. 170% of AW), the IA METR jumps and steadily rises before dropping as the tax credit expires (at EUR 35 000 i.e. 297% of AW). The METR drops further at 384% of AW as the SSC ceiling is introduced.

Note: The average wage refers to the gross average wage from employment in 2021 calculated by the OECD secretariat. Chart B starts at 10% of AW due to very high AETRs for the self-employed due to health SSC floor. SSC and health SSC ceilings for the individual activity SE are 3.6 annual AW in 2022 and 5 annual AW since for employees since 2021 (excluding health SSCs). For both employees and IA, the PIT rate is calculated as PIT as a share of gross income. For IA, total SSCs include SSCs plus health SSCs. For IA, the average tax wedge is calculated as PIT and total SSCs divided by total labour costs (i.e. gross income plus total SSCs). For employees, the average tax wedge is calculated as PIT, employee SSCs and employer SSCs divided by total labour costs (i.e. gross income plus employer SSCs). For employees, the net personal average tax rate (NPATR) is calculated as PIT and total SSC divided by gross income. For SE, the marginal effective tax wedge (METR) is calculated as the part of the increase of labour costs (gross income plus total SSCs) that is paid in PIT and total SSCs. The increase refers to a one percentage-point increase in gross income as a share of AW. The SE income distribution refers to a tax record sample of 3,649 taxpayers in 2019 (including those with incomes from sources other than self-employment).

Source: OECD hypothetical model of self-employment; OECD Taxing Wages; OECD analysis of microdata.

Note: The average wage refers to the gross average wage from employment in 2021 calculated by the OECD secretariat. For employees, the PIT rate is based on the PIT variable in the tax record data as a share of total employment income. For employees, the average tax wedge is calculated hypothetically using OECD Taxing Wages (as some SSCs are unavailable in the microdata). For employees, the average tax wedge is calculated as PIT, employee SSCs and employer SSCs divided by total labour costs (i.e. gross income plus employer SSCs). For SE, the average tax wedge is calculated as PIT and total SSCs divided by total labour costs (i.e. gross income plus total SSCs). Based on 24,834 employees. Based on 3,048 individual activity self-employed that opt for the presumed cost deduction. Of these, 84% avail of the presumed cost deduction. When the self-employed not availing of the presumed deduction are included, the effective PIT rate is more variable owing to higher costs (which could be due to losses, inter alia). Individual activity self-employed have income sources other than self-employment.

Source: OECD analysis of microdata.

The IA regime design and the self-employment income distribution

Few IA taxpayers will face high METRs so disincentives to progress in work will be limited. The increasing METRs in the IA regime will reduce incentives to progress in work. However, few IA taxpayers earn incomes within the income range where METRs are high (Figure 5.18) so the negative impacts will be limited.

Similarly, as few higher income SE earn sufficient income to face higher PIT rates, the progressivity introduced by the tax credit will be limited. The tax credit design cannot achieve the goal of promoting progressivity because it does not appear to have been designed to reflect the actual IA income distribution (Figure 5.18). In the IA regime, a majority (85%) face an effective PIT rate on gross income of 3.5% with only a minority (4%) facing the 10.5% PIT rate on gross income or a rate in-between (8%) (Figure 5.18, Panel A).7

Adherence of the individual-activity regime to tax policy principles

The IA regime design may produce horizontal inequity (i.e. IA taxpayers with similar incomes to employees face lower tax burdens). The lower IA tax burden is driven by a range of tax design features that advantage SE over employment. These include lower statutory PIT rates, narrower PIT and SSC bases, deductible SSCs and a lower and broader SSC ceiling. These design features violate the principle of horizontal equity by taxing similar taxpayers differently. In the absence of a strong rationale, they may be unequitable.

The IA regime may not be tax neutral (i.e. it may encourage tax arbitrage from employment to SE). The aforementioned design features of the IA regime may violate tax neutrality as the tax design encourages employees to reclassify as SE to avail of a reduced tax burden. For example, an employee may be able to do the same work for their employer at a reduced tax burden by incorporating as an IA taxpayer. This tax arbitrage opportunity risks higher numbers of employees entering the IA regime than would otherwise be the case, potentially undermining tax revenues by placing a higher tax burden on the employee taxpaying population.

Justifying rational exist for some departure from these principles for the SE but they should be weighed against arbitrage and tax revenue risks. Justifying rationale for why SE may be taxed lower than similar income employees could include that the authorities prefer to encourage small business growth, SE face greater job uncertainty in addition to reduced employment and entitlement rights. These rationale should be weighed against the likelihood and tax revenue risks of tax arbitrage opportunities produced by the tax burden differentials between the organisational forms.

Reform options

A number of tax policy reforms could be considered. To mitigate against the aforementioned challenges of horizontal inequity and tax non-neutrality between the IA regime and employment, there is a scope for tax policy reform. While perfect alignment of the tax burden between the IA regime and employment may not be preferable (given justifying rationale for lower burdens on SE) or indeed politically feasible, tax policies that reduce misalignment will reduce the challenges of horizontal inequity and tax non-neutrality. A number of such tax policy reforms that could be considered are as follows:

1. Raise the PIT rate in the IA regime to better align with the PIT rate faced by employees. Statutory PIT rates in the IA regime are always lower than PIT rates on employees. Effective PIT rates in the IA regime are lower than on employees at most incomes. To support fairness and reduce tax arbitrage between employment and SE, the IA PIT rate could be aligned with the standard 20% PIT rate for employees. This could be achieved by reforming the tax credit design by cutting the tax credit threshold (i.e. currently EUR 20 000) or the tax credit (i.e. currently 10%).

2. The appropriate PIT rate could set based on an evaluation of profits in the IA regime, but the data availability for a rigorous evaluation may be lacking. An evaluation of profitability or the ability to pay might be challenging given the high take-up of the presumptive cost deduction which, from the perspective of data availability, implies that the tax admin likely has limited tax record information on the costs of business operations in the IA regime. An analysis of IA taxpayers that do declare actual tax returns is likely to suffer from selection bias so that a representative evaluation would be challenging.

3. Broaden the SSC base in the IA regime to better align with that of employment. IA taxpayers face a narrower SSC base (of 63% of gross income under the presumed cost deduction) than employees (of 100% of gross income). The IA SSC base could be broadened to better align with the employee SSC base. One option could be to set the IA SSC base at 100% of taxable income instead of 90% of taxable income so that the effective SSC base becomes 70% of gross income. In this case, IA taxpayers would continue to pay lower SSCs as they face the same statutory SSC rates as employees.

4. Align the SSC deductibility rules between the IA regime and employment. To reflect the costs of inputs in operating a business, IA taxpayers can deduct costs. The employee equivalent is the costs of going to work which form part of the rationale for a basic allowance. However, IA taxpayers can further deduct SSCs (presumed or declared) whereas employees cannot, which implies reduced tax burdens for IA taxpayers. In the absence of a justifying rationale, SSC deductibility could be afforded to employees and SEs more equally. This could be achieved directly by disallowing IA taxpayers from deducting pension SSCs. The SSC pension benefits of employees could continue to remain untaxed (as employees have effectively already been taxed through higher PIT).

5. The SSC ceiling design between SE and employees could be equalised to reduce tax arbitrage opportunities. There does not appear to be a strong rationale for lower SSC ceilings on IA which imply that high-income IA benefit from reduced SSC burdens. Raising the IA SSC ceiling to align with that of employees would increase the SSC burden on high-income IA and raise SSC revenues, albeit the SSC revenue impact would be limited as few IA have very high incomes. Aligning the SSC ceiling would reduce arbitrage opportunities for high-income employees to incorporate as SE to reduce their tax burden. Aligning the scope of the SSC ceilings (i.e. the employee SSC ceiling excludes health SSCs but the SE ceiling includes health SSCs) would similarly reduce tax arbitrage opportunities. SSC ceilings should be applied on a combined income, irrespective of the type of activity form which the income is derived.

6. The IA regime tax credit design should be aligned with the SE income distribution in mind. The tax credit in the IA regime could be better designed. From the perspective of achieving PIT progressivity, too few IA taxpayers report incomes within the income range where it has been set. From the perspective of incentives, of the few taxpayers that it affects, a rising METR may discourage business growth.

7. Consideration could be given to abolishing the presumptive cost deduction as it weakens the tax admin’s capacity to successfully monitor and enforce compliance. Despite the presumed cost deduction seeming insufficiently generously to be preferred to declaring actual costs, more than 4 in 5 IA taxpayers (83%) opt for it based on an estimate from the microdata. There are advantages to a presumed cost deduction including simplicity for taxpayers and the tax admin. However, a main drawback of a majority of IA taxpayers opting for the presumptive cost deduction is that the tax admin has limited transparency on the actual operations and costs of business within the IA regime. On top of limited transparency in the IA regime, Lithuania operates a presumptive BC regime where costs are not required to be reported. Taking the two unincorporated SE regimes together, this implies that the tax admin has cost information on only about 1 in 10 businesses (13%8). This lack of information may weaken the tax admin’s capacity to successfully monitor and tackle compliance in the IA regime.

8. There may be a tax-induced incentive to switch from employment to self-employment as incomes increase. If taxpayers responded to the net personal average tax rate (Figure 5.17, Panel B), they would face a tax-induced incentive to be employed at incomes up to about 1/4 of the AW and to enter the IA regime once income increased beyond that. The income distribution data show significant shares of part-time (PT) employees in this income range (Figure 5.5). Although a high share of PT employees report very low incomes, this does not necessarily imply that they face poverty risks as they have high incomes on per month basis. For example, it could be speculated that some employees intentionally work PT and report low incomes to avail of a lower tax burden and then switch to more lightly taxed SE when income rises. Such an organisational arrangement is made possible by the tax rules which allow individuals to simultaneously be employed, have a business certificate and an individual certificate. However, the extent of this arbitrage behaviour remains unclear in the absence of a more comprehensive analysis of switching between organisational forms using longitudinal microdata. We leave this for future work.

Simulating reforms

The tax burdens in the IA regime can be simulated and compared with employment for several potential tax reforms by applying the SE tax rules to income and taxes on the microdata. SE face lower tax rates than employees because they can deduct business costs from their income (for employees, the costs are already borne by their employer). To account for this difference methodologically and improve comparability, IA costs are set at zero (i.e. the presumed cost deduction is reduced from 30% to 0%. Note that this raises the tax burden on IA thus narrowing the gap with employees). The simulation informs the extent of the tax burden alignment between IA taxpayers and employees on several tax reform options as follows:

1. Cutting the tax credit threshold to zero would broadly align the PIT burden with employees. The effective PIT rate for the IA would broadly align with employees if the tax credit (TC) threshold was reduced from EUR 20 000 to EUR 0 (Figure 5.19, Panel A). This occurs as a TC threshold of zero corresponds to a PIT rate of 5% from when income is first earned that then steadily increases up to a PIT rate of 15% (if the TC were not set to zero, the PIT rate is flat at 5% up to 170% of the AW).

2. Removing the deductibility of SSCs from the IA regime would modestly raise the tax burden, particularly on high earners. Employees cannot deduct SSCs from the PIT base. If non-deductibility of SSCs were extended to IA taxpayers that opt for the presumptive cost deduction (i.e. implying a presumptive cost deduction of 17.7%), it would modestly raise the IA tax burden across the income distribution, notably at higher incomes when the health SSC floor has expired (Figure 5.19, Panel B, SE (3), see Figure notes).

3. Broadening the IA SSC base would not alter the tax burden significantly. If the IA SSC base was broadened from 90% to 100% of taxable income, the tax burden would increase but only very modestly (Figure 5.19, Panel B, SE (2), see Figure notes).

4. Aligning the IA PIT rate with the employee PIT rate would meaningfully shift the IA tax burden upwards but it would remain below that of employment. Increasing the PIT rate to 20% would shift the IA tax burden upwards relatively uniformly across the income distribution (Figure 5.19, Panel C, SE (5), see Figure notes) (following the methodology to increase comparability in chart A, chart C sets the presumptive cost deduction to zero, SE (4)). The distributional pattern of the tax burden would remain similar.

5. Aligning the IA PIT rate and simultaneously cutting the tax credit threshold to zero would better align the tax burden and the tax burden distributional shape with that of employment. Increasing the PIT rate to 20% and simultaneously cutting the TC threshold to zero (Figure 5.19, Panel C, SE (6), see Figure notes) would better align the distributional shape of the tax burden with employees. On top of the PIT rate increase, the TC threshold cut raises the tax burden between about 50% and 150% of AW. This tax reform would reduce tax arbitrage opportunities between the IA regime and standard employment.

6. Aligning the tax burden with employees might require substantial increase in PIT rates which may not be desirable. Increasing the PIT to 30% and cutting the TC threshold to EUR 5 000 is one option for broadly align with the tax burden for employees. A higher PIT rate is needed to compensate for the tax credit of 10% (even when the tax credit threshold is cut to zero). However, exact alignment may not be desirable (given justifying rationale for lower tax burdens among the self-employed).

Note: In all charts, employees refer to employees with only employment income (24,834 taxpayers in the microdata) and SE refers to individual-activity self-employed who opt for the presumed cost deduction (3,048 taxpayers). In chart A, the employee PIT rate is PIT as a share of total employment income in the microdata. In charts B and C, the employee average effective tax wedge (AETR) is calculated using the OECD Taxing Wages model (since employee SSCs are not available in the microdata).

Simulation parameters: Chart A: SE (1) sets the presumed cost deduction (PCD) to 0. SE (2) sets PCD to 0, the PIT rate a 15% and the tax credit threshold (TC) to 0. Chart B: SE (1) sets PCD at 30%. SE (2) sets PCD at 30% and the SSC base at 100% of taxable income. SE (3) sets PCD at 17.7%. Chart C: SE (4) sets PCD at 0%. SE (5) sets PCD at 0%, PIT rate at 20% & TC at EUR 20,000. SE (6) PCD at 0%, PIT rate at 20% & TC at EUR 0. SE (7) PCD at 0%, PIT rate at 30% & TC at EUR 5 000.

Source: OECD analysis of microdata.

Hypothetical modelling applying the SE tax rules confirms that raising the PIT rate and cutting the tax credit threshold would significantly reduce the tax burden gap with employment. Using the same methodology from Figure 5.19 to improve comparability between the IA regime and employment (i.e. setting presumptive cost deduction to zero) but applying a hypothetical modelling analysis using the SE tax rules shows that raising PIT to 20%, cutting the TC threshold to EUR 5 000 and aligning the SSC ceilings would significantly reduce the tax burden gap with employment (Figure 5.20). The reform does not significantly change the magnitude of the METRs but rather shifts them to different income levels.

Note: The hypothetical model follows the same approach as described in the notes in Figure 5.17. The hypothetical model has the advantage of modelling the SSC ceilings at higher incomes as it is not restricted to the sample microdata which is limited by sample size. It is also suitable to model METRs. PCD set at 0% for comparability. SE (1) shows PIT rate of 15% and TC threshold at EUR 20 000. SE (2) shows PIT rate at 20% and TC threshold at EUR 5 000. The SSC ceiling for SSCs and health SSCs used is EUR 64 676 in 2022.

Source: OECD hypothetical SE model.

Increasing the PIT rate in the IA regime from 15% to 20% and simultaneously cutting the tax credit threshold from EUR 20 000 to EUR 5,000 would raise total PIT revenues by about 1% and modestly reduce income inequality (by 0.0123 percentage points based on the S80/S20 ratio). According to modelling using EUROMOD, the reform would produce relatively high increases in total PIT revenues in both the bottom and top equivalised household disposable income deciles (Figure 5.21). The result reflects the low PIT paid by many IA taxpayers and the IA regime income distribution whereby most SE earn low incomes in the lower deciles, and a few earn very high incomes in the top deciles.

Note: Deciles refer to equivalised total household disposable income. PIT refers to total PIT paid from all income sources (i.e. including employment income and SE income).

Source: Simulations performed by the EUROMOD team of the European Commission’s Joint Research Centre (JRC).

Self-employed farmers

This section briefly describes the taxation of self-employed farmers. SE farmers are defined as persons working under agricultural individual activity income. SE farmers comprise 1/3 of IA taxpayers in 2019. A detailed examination of the taxation of SE farmers goes beyond the scope of this report, which we leave for future work.

Self-employed farmers have relatively high and varied income sources compared to non-farmer SE. Farmers have higher average SE income and, as such, are more likely to be VAT registered than non-farmer SEs (Table 5.9).