4. Australia

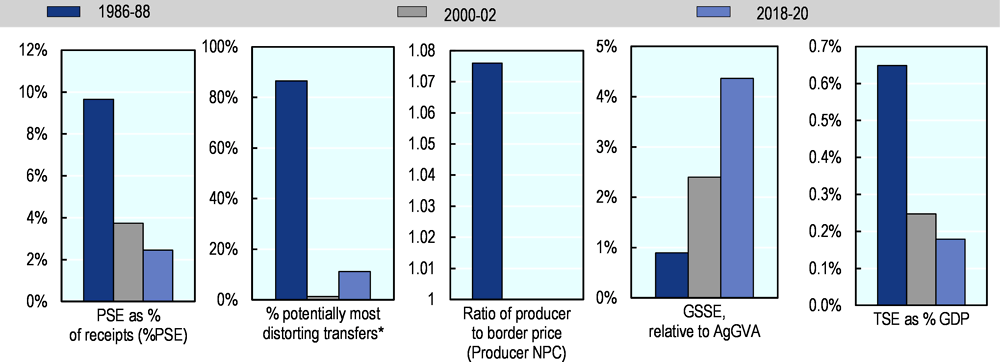

Australia’s support to agricultural producers is among the lowest in the OECD area, estimated around 2% of gross farm receipts for 2018-20, with total support to agriculture (TSE) representing around 0.2% of GDP. Over time, the composition of the TSE moved away from producer support (PSE), and the share of general services support (GSSE) in total support increased from less than 10% in the late 1980s to 55% in 2018-20.

Market price support to producers ended in 2000 and domestic prices for Australia’s main agricultural outputs are at parity with world prices since then. Around 48% of support provided to producers in 2018-20 was input subsidies. Much of these went to on-farm investments, including in response to adverse events. The bulk of remaining producer support (about 30% of the PSE) went towards income-smoothing programmes that address cashflow fluctuations, such as the Farm Management Deposits and income tax averaging arrangements. Notwithstanding and in addition to these programmes, disaster payments occurred in the recent period.

Approximately one-third of total public expenditure for agriculture is support for research, development and extension services, and Australia has an extensive agricultural knowledge and innovation system. Public expenditure on biosecurity inspection and control services, and to develop and upgrade infrastructure (mostly hydrological) represents the bulk of the remaining expenditure on general services.

Recent policy developments relate to adverse events: droughts, wildfires and the COVID-19 pandemic. Drought response programmes introduced in 2020 were funded through the Future Drought Fund. Programmes strengthened on-farm capacity and public investment in research and development, and improved access to climate information systems. The programmes channel public funds to region-based innovation generation and adoption, and to farms to develop strategic management skills and support the development of Farm Business Plans, among other activities. Innovation generation and adoption are also at the centre of the Agricultural Innovation Agenda. The agenda offers a regulatory environment enabling greater private sector participation in the innovation system.

The National Bushfire Recovery Fund formalised wildfire-recovery programmes that, while they place greater emphasis on the forestry sector, also support farm clean up and emergency response activities. The fund provides low-interest loans to affected farmers for working capital or larger investments. It also supports the Rural Financial Counselling Service providers in bushfire-affected regions, and industry-specific support to apple growers and wine grape producers.

Trade developments mainly relate to progress in trade agreements and facilitating access to export markets in the COVID-19 context. Trade agreements with Hong Kong, China; Peru; and Indonesia entered into force in 2020, in addition to the Pacific Agreement on Closer Economic Relations Plus (PACER Plus). The Regional Comprehensive Economic Partnership (RCEP) agreement between the Association of South East Asian Nations (ASEAN), Australia, the People’s Republic of China (hereafter “China”), Japan, Korea and New Zealand was signed on 15 November 2020. These include food and agriculture.

Australia is in separate FTA negotiations with the European Union and the United Kingdom. Negotiations have been on-going for an extended period with India, and with the Gulf Cooperation Council (GCC) and the Pacific Alliance Free Trade Agreement. Australia is also in the Environmental Goods Negotiations (undertaken in conjunction with 45 other WTO member countries) and the Trade in Services Agreement (TiSA) also undertaken with a sub-group of WTO members (DFAT, 2021[1]).

Several schemes aim to facilitate access to export markets through simplified regulations, digital tools, export market diversification and logistics support. The Busting Congestion for Agricultural Exporters package aims to simplify export regulations, limit export costs and accelerate exporters’ use of digital services. It includes sector-specific support to seafood and live-animal exporters to transition towards data- and technology-enabled ways of meeting regulatory standards, improve the export regulatory environment of the meat industry and simplify plant exports.

The Agri-Business Expansion Initiative funds the Australian Trade and Investment Commission (Austrade) and the Australian Department of Agriculture, Water and the Environment (DAWE) to support farming, forestry and fishing exporters to expand and diversify export markets. The initiative also expands the Agricultural Trade and Market Access grant programme (ATMAC) through partnerships with industry associations. The International Freight Assistance Mechanism (IFAM) was established in April 2020 to help keep international supply chains open during COVID-19. Support is available to domestic connections for producers and growers in regional and rural areas that rely on airfreight.

Together with the enhanced use of digital technology, simplified regulations aimed to accelerate export processes under COVID-19 conditions. Industry-specific support was also introduced to ease the transition in industries exporting live animals and seafood, meat and plants.

Australia provides low levels of support to its agricultural sector. In recent years, public expenditure on services that support the sector as a whole exceeded support to individual farmers.

Farm support comes through subsidised inputs and loans, and advisory and biosecurity services, together with financial risk management tools. Decline in farm income as a result of natural hazards is compensated at times through ad hoc grants, as was the recent case with challenging farming conditions caused by continued drought, wildfires and the COVID-19 pandemic. Concessions on credit, water rates, fodder transport subsidies and additional ad hoc payments were used. These policies contrast with past approaches that aimed to strengthen farm resilience to drought as a normal farming condition, and may encourage risk-taking by producers and disincentivise the sector’s adaptation and transformation to future risks.

Research and development are a major component of general services provided to the sector, while extension and education services receive smaller funding. Recent programmes increased funding to advisory services networks. The Future Drought Fund and Agricultural Innovation Agenda both encompass innovation generation and adoption. Knowledge transfer services should receive continued consideration, as they facilitate farmers’ innovation take-up, which increases productivity and sustainability, and can build on-farm capacity to manage risks.

Ensuring farm economic viability in the face of resource constraints – particularly with respect to water – remains the greatest challenge to Australia’s agricultural sector. Reforms initiated water pricing mechanisms that help improve the alignment of incentives for water use with scarcity conditions in the Murray-Darling Basin (MDB). Investments support water use efficiency at both the farm level and in wider water management basins. Policymakers should continue to evaluate existing policies and future projects to develop new sources of water outside of the MDB to ensure that they take longer-term climatic projections into account and do not incentivise behaviour that may worsen conditions for the sector’s future.

Despite wide acknowledgement that the changing climate affects Australia’s farmers, the sector’s role in contributing to climate change through emissions remains overlooked in terms of policy response. Information on the sector’s emissions should be improved by the release of a new version of the FullCAM modelling tool. Improved evidence offers an opportunity to develop a more systematic and sector-wide approach in anticipation of future climate policies that may impact the sector to a greater extent than in the past. The FullCAM model is also to be used for calculations under the Emissions Reduction Fund (ERF).

Note: * Share of potentially most distorting transfers in cumulated gross producer transfers.

Source: OECD (2021), “Producer and Consumer Support Estimates”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-pcse-data-en.

Source: OECD (2021), “Producer and Consumer Support Estimates”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-pcse-data-en.

Overview of policy trends

Before the 1980s, Australian agriculture was supported by a range of measures designed to maintain and stabilise farm income, and to provide farmers with market power to offset the perceived disadvantages of remoteness. In 1980, Australia had 65 statutory marketing boards that used border protection through tariffs and import controls to divide domestic and international markets, and set higher prices in domestic markets (Table 4.2).

Price stabilisation schemes assisted export industries such as wheat, manufactured dairy products, sugar and dried vine fruit. Other policy measures included fertiliser subsidies, income tax incentives, rural credit for and subsidies to agricultural research and extension, and public investment in land and water development and rural infrastructure.

Agricultural policy evolved significantly from the mid-1980s. Competition policy reforms in the 1980s and 1990s led to removing policies that distort agricultural production and trade. The National Drought Policy introduced in 1992 formalised the transfer of drought risk management to farmers and repurposed government support towards resilience-strengthening activities. Trade practices and anti-dumping legislation ensured competitive markets across the whole economy, reducing the need for sector-specific measures. Price stabilisation policies were relaxed, price and output controls removed and centralised marketing schemes gradually dismantled (Gray, Oss-Emer and Sheng, 2014[2]). Tariffs were reduced. Floating exchange rates and trade liberalisation reduced price volatility in agricultural commodities.

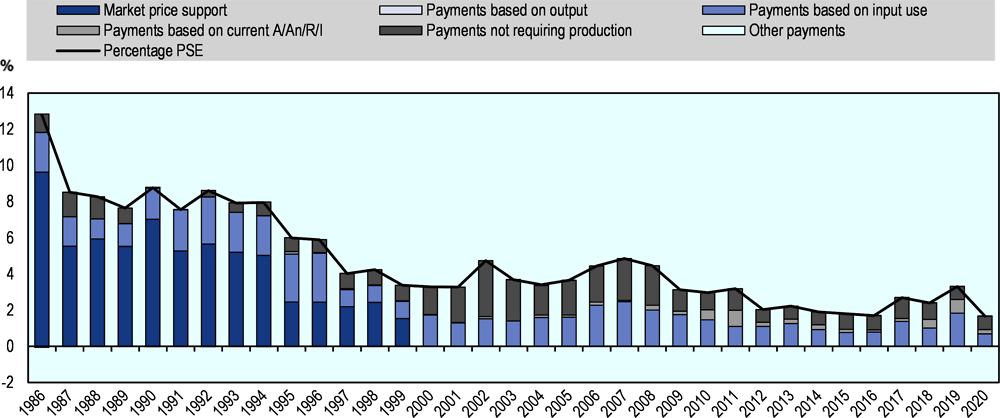

In Australia, total support to the sector is composed of general services and budgetary payments to producers; market price support disappeared since the late 1990s (Figure 4.1). PSE or support to producers was reduced to one of the lowest in OECD. It is mostly delivered through input use support and payments not requiring production.

Note: A/An/R/I:Area planted/Animal numbers/Receipts/Income.

Payments not requiring production include Payments based on non-current A/An/R/I (production not required) and Payment based on non-commodity criteria. Other payments include Payments based on non-current A/An/R/I (production required) and Miscellaneous payments.

Source: OECD (2021), “Producer and Consumer Support Estimates”, OECD Agriculture statistics (database), https://doi.org/10.1787/agr-pcse-data-en.

Main policy instruments

Australia’s agricultural sector is market oriented, with domestic and international prices generally aligned. Support to agriculture comprises a mix of direct budgetary outlays, concessional loans and tax concessions. Direct support is provided to upgrade on-farm infrastructure that aims to improve natural resource use. Several programmes support the development and uptake of farming practices to enhance sustainability,1 including through innovation take-up and pilot testing of certification schemes.2

Concessional loan schemes incentivise investments in weather and market risks preparedness. Income stabilisation tools such as the Farm Management Deposits scheme and income tax averaging arrangements further strengthen farm preparedness. These are supplemented with natural disaster payments and farm household income support during periods of hardship. Public funding is planned through the Disaster Recovery Funding Arrangements that came into force in 2018. The Drought Response, Resilience and Preparedness Plan was released in November 2019 and initially allocated AUD 3.5 billion (USD 2 billion). The Plan’s FarmHub supports farmer access to weather information and improved weather information collection and dissemination. (Department of Agriculture, 2019[3]). Central and regional funding support large scale water infrastructure investments. Programmes also support farmers and land managers in pests and weeds control during drought.

Since 2018, the Regional Investment Corporation (RIC) administers farm business loans and support to States and Territories for water infrastructure projects. Changes to the portfolio of concessional loans are described in Domestic policy developments.

Given the low level of direct government support to farmers, research and development (R&D) programmes are a major component of Australian support to agriculture. A smaller portion of public expenditure goes to development and maintenance of large infrastructures and inspection services, including pest and disease control activities. Industry and governments cost-share the eradication of outbreaks, while trade-related costs of biosecurity and food safety inspection services are covered by industry.

Rural research and development corporations (RDC) are the Australian Government’s primary vehicle to support rural innovation. RDCs are a partnership between the government and industry created to share funding and strategic direction-setting for primary industry R&D, investment in R&D and subsequent adoption of R&D outputs. A levy system collects contributions from farmers to finance RDCs, and the Australian Government provides matching funding for the levies, up to legislated caps.

Improving market transparency is also part of the government’s assistance to the food sector. One example is the mandatory dairy code of conduct under the authority of the Australian Competition and Consumer Commission, which came into force in January 2020 (ACCC).3

The Australian Climate Change policy directed towards agriculture seeks to address both adaptation and mitigation while, at the same time, developing responses that maintain and enhance productivity, profitability and food security. The policy was reviewed in 2017 and implementation of review outcomes began in 2019.

Australia’s agricultural sector contributes as part of the land-based sectors to the country’s response to the 2016 Paris Agreement on Climate Change. This includes a commitment to reduce the sector’s greenhouse gas (GHG) emissions by between 26% and 28% in 2030 compared to 2005 levels, as defined in the Australian Nationally Determined Contribution (NDC).

Australia’s Direct Action Plan supports whole-of-economy emissions cuts through government purchase of emission reductions by the Emission Reduction Fund (ERF). The ERF is a voluntary scheme, open to all sectors, to undertake emission reductions and carbon sequestration (capture and storage) projects that meet strict integrity requirements, including in relation to additionality. For agriculture, the Direct Action Plan builds on the Carbon Credits (Carbon Farming Initiative) Rule 2015, now integrated in the ERF. Under the scheme, landowners and farmers can earn alternative and additional income through sales of generated Australian Carbon Credit Units to the government or third parties. The scheme is amended periodically,4 offering space for improving issues identified. These include the ability of the scheme to deliver additional carbon abatement relative to what may have occurred anyway (Burke, 2016[4]; Freebairn, 2016[5]), and for the funded projects to deliver on their intended reductions.

Australia’s agriculture is trade oriented with fifteen comprehensive regional or bilateral free trade agreements in force.5 Policies support access to export markets, including helping small exporters overcome market access barriers and costs associated with exports registration. While imports of agriculture and food products, on average, face lower tariff rates than non-agricultural goods,6 a number of SPS measures are in place to manage pest and disease risks that could harm the sector. These SPS arrangements mean that a number of import restrictions are in place for imports of agricultural products from certain regions.

Domestic policy developments in 2020-21

Recent policy developments were mostly related to adverse events; droughts, wildfires and the COVID-19 pandemic that affected Australia’s economy and farm sector. Building on the current menu of policy tools, support was deployed at farm and sector levels.

The eight programme headings under the AUD 5 billion (USD 3.4 billion) Future Drought Fund were announced in July 2020. The largest envelopes are for the Drought Resilience Research and Adoption Program (AUD 86 million or USD 59 million over four years) in the form of grants provided to eight region-based Adoption and Innovation Hubs; and for the Farm Business Resilience Program (AUD 20 million or USD 14 million) for farmer training to develop strategic management skills and support the development of a Farm Business Plan. Other headings support Regional Drought Resilience Planning with a focus on cross territorial collaboration and stakeholder participation; a digital Climate Service for Agriculture platform targeted to farmers’ drought and climate decision making needs; and Natural Resource Management programmes available to regional resource management bodies for landscape related actions that improve drought resilience, and to farmers and farmer groups to build resilience through management practices. Government support under the programme also goes to the development of an online Drought Resilience Self-Assessment Tool for farmers. The tool will be developed with end-users and is expected to help farmers assess their exposure to drought and other climate risks, based on economic, social and environmental indicators.

In response to the continued effects of droughts, the government widened and reinforced the range of existing programmes and introduced new measures at the farm and sectoral levels. Drought response measures include loans, water infrastructure support, advisory services, as well as research and development and improved access to specialised weather information. The government increased by AUD 2 billion (USD 1.4 billion) the budget for concessional loans available to farm businesses and managed through the Regional Investment Corporation (RIC), and made available two-year interest free terms to eligible applications up to 30 September 2021. RIC’s farm business drought loans support farm businesses to recover, manage through or prepare for droughts. Their eligibilty was widened to cover more areas. In addition, small businesses that directly provide primary production related goods and services to farm businesses in specific geographic areas have access to the preferential conditions of the AgBiz Drought loan (OECD, 2020[6]). The Rural Financial Counselling Service (RFCS) was attributed AUD 62 million (USD 43 million) for the period from July 2021 to June 2024.

On-farm support is provided for water infrastructure as well as pest and weed control. The on-farm Emergency Water Infrastructure Rebate Scheme foreseen under the Drought Response, Resilience and Preparedness Plan was reinforced to reach AUD 100 million (USD 60 million). The scheme supports the purchase and installation of on-farm water infrastructure for permanent plantings and livestock farmers.

Response to the 2019-20 wildfires is delivered through the AUD 2.1 billion (USD 1.4 billion) National Bushfire Recovery Fund, announced in January 2020. Low interest loans are available since January 2020 to affected farmers for up to AUD 500 000 (USD 344 000), with varying amounts and duration for working capital or larger investments.7 A two-year interest free repayment deferral period applies to these loans. Agriculture related measures under the fund consist of clean-up and emergency response activities. Sectoral subsidies are provided to apple growers to assist them to re-establish their apple orchards and to wine grape producers whose losses are not covered by the Disaster Recovery Funding Arrangement. The fund also supports the Rural Financial Counselling Service providers in bushfire-affected regions.

A new concessional loan product was introduced through the RIC in January 2021. The AgriStarter loan supports sector entry as well as farm succession arrangements with loans of up to AUD 2 million (UD 1.4 million) from the overall AUD 75 million (USD 52 million) budget.

The National Agricultural Innovation Agenda was announced in September 2020 and its implementation is planned to begin in 2021. The agenda considers innovation generation and adoption, and foreshadows the regulatory environment enabling greater private sector participation in the innovation system.

Funds attributed to the Emissions Reduction Fund were increased to AUD 4.6 billion (USD 3 billion) with an additional AUD 2 billion (USD 1.4 billion) made available to farmers from the Climate Solutions Fund,8 for projects relating to land and water quality improvements and adaptation to drought.

Trade policy developments in 2020-21

Australia’s trade policy seeks further market opening through multilateral, bilateral and regional trade agreements (DFAT, 2021[1]). Recent developments were mainly related to progress in trade agreements and facilitating access to export markets in the COVID-19 context.

Four free trade agreements came into force in 2020 and one was signed that is not yet in force. The Australia-Hong Kong, China Free Trade Agreement entered into force on 17 January 2020. At this date, custom duties were eliminated for all goods including food and agriculture, while special provisions apply to imports into Australia. On 11 February 2020, the Peru-Australia Free Trade Agreement (PAFTA) entered into force. At this date, most duties on food and agricultural goods were eliminated and the elimination of remaining duties is scheduled during the subsequent four-year period. The Indonesia-Australia Comprehensive Economic Partnership Agreement (IA-CEPA) entered into force on 5 July 2020.

The Pacific Agreement on Closer Economic Relations Plus (PACER Plus) entered into force on 13 December 20209. Beyond its free trade dimension covering sanitary and phytosanitary (SPS) measures, rules of origin, customs, trade in goods and services and investment; PACER Plus provides for AUD 19 million (USD 13 million) to support Pacific Island parties with the implementation of the trade agreement and benefit from regional and global trade more generally (DFAT, 2021[1]). It will also help support the region’s economic recovery from the COVID-19 pandemic.

The Regional Comprehensive Economic Partnership (RCEP) agreement between Australia, the Association of South East Asian Nations (ASEAN) member states and China, Japan, Korea and New Zealand was signed on 15 November 2020. The agreement includes agriculture and will enter into force 60 days after six ASEAN members and three non-ASEAN members have ratified the agreement.

Australia is currently engaged in FTA negotiations with the European Union (launched in 2018), and with the United Kingdom (launched in 2020). Negotiations have been on-going for an extended period with India, with the Gulf Cooperation Council (GCC), and the Pacific Alliance Free Trade Agreement. Australia also engages in the plurilateral Environmental Goods Negotiations (undertaken in conjunction with 45 other WTO member countries) and the Trade in Services Agreement (TiSA) also undertaken with a sub-group of WTO members (DFAT, 2021[1]).

Standards that apply to exports of livestock, the Australian Standards for the Export of Livestock (ASEL), are reviewed every three years to ensure that the standards remain fit for purpose and reflect the latest science. The latest version of the ASEL (ASEL 3.1) was published in March 2021.

The enactment of the Biosecurity Amendment (Traveller Declarations and Other Measures) Act 2020 increases penalties and extends the biosecurity-related visa cancellation grounds from 1 January 2021 to travellers who fail to declare high risk goods identified in a pre-established list including live animals, meat and meat products, seeds and live plants.

Trade policy responses to the COVID-19 pandemic

The Busting Congestion for Agricultural Exporters package was announced in 2020 with AUD 328 million (USD 226 million) over four years. It aims to simplify export regulations, limit export costs and accelerate exporters’ use of digital services. It includes sector specific support to help seafood and live animal exporters transition toward data and technology enabled ways to meet regulatory standards, to improve the export regulatory environment of the meat industry and to simplify plant exports.

Government support to access export markets was reinforced subsequently with several programmes. The Agri-Business Expansion Initiative was announced in December 2020, more than half of the AUD 73 million (USD 50 million) under this initiative is attributed to Austrade to support farming, forestry and fishing exporters to expand and diversify their export markets in 2021. The initiative also expands the Agricultural Trade and Market Access grant programme (ATMAC) through an additional AUD 18.4 million (USD 13 million) in funding over two years. The revised programme enables government to develop strategic partnerships with industry to support the agriculture, fisheries and forestry sectors’ efforts to improve and diversify access to overseas markets by mobilising research, training, and capital works that support market diversification among other actions. The International Freight Assistance Mechanism (IFAM) was established in April 2020 to help keep international supply chains open during COVID-19. Its initial budget was increased in July and October 2020 and March 2021 to total AUD 782 million (USD 538 million). The funding also supports domestic connections for producers and growers in regional and rural areas that rely on airfreight to get their products to existing markets. The Package Assisting Small Exporters (PASE) helps small exporters to overcome market access barriers and costs associated with exports registration, it is in place four years up to 2022 with a total budget of AUD 5 million (USD 3 million).

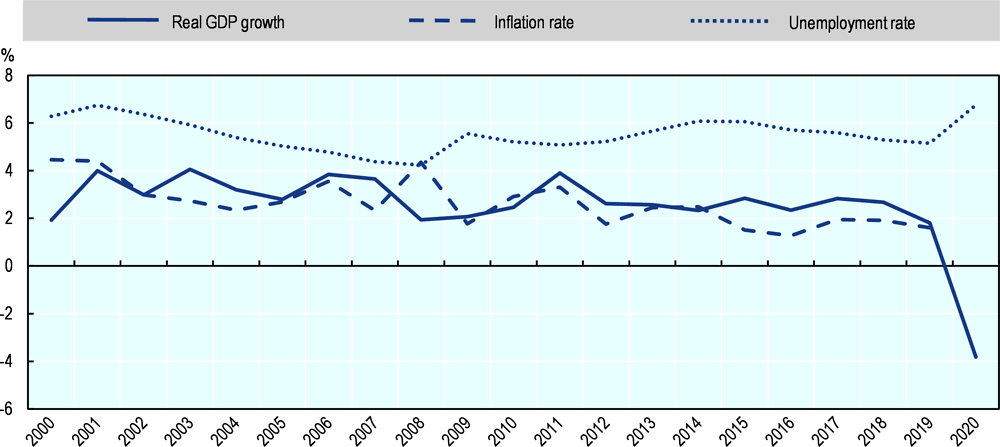

Australia is the world’s 14th largest economy (in 2019) and the sixth largest country by land area, accounting for 12% of all agricultural land in the countries included in this report but only 0.5% of the population. The country’s GDP per capita is more than twice the average of the countries covered in this report (Table 4.3). Agriculture represents a small share in the economy, but contributes significantly to total exports. Australia is an important producer and exporter of agricultural products, making the country a key supplier to world markets for agricultural products.10

Years of consistent positive economic growth came to a halt in 2020 when the economy shrunk by 4% and unemployment rose by 30% to 7% as a consequence of the COVID-19 pandemic and related restrictions (Figure 4.4).

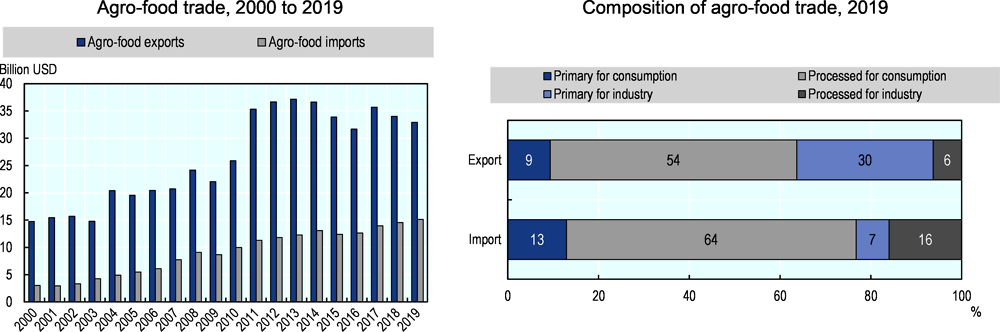

Australia’s agro-food sector is well integrated into world markets; imports are sizeable as are exports and the country is a consistent and significant net exporter. Processed goods for final consumption and further processing make up 60% of the country’s agro-food exports. Approximately three-quarters of Australia’s agro-food imports go to domestic final consumption and the remaining share (23%) is destined for the processing industry (Figure 4.5).

Sources: OECD statistical databases; World Bank, WDI; and ILO estimates and projections.

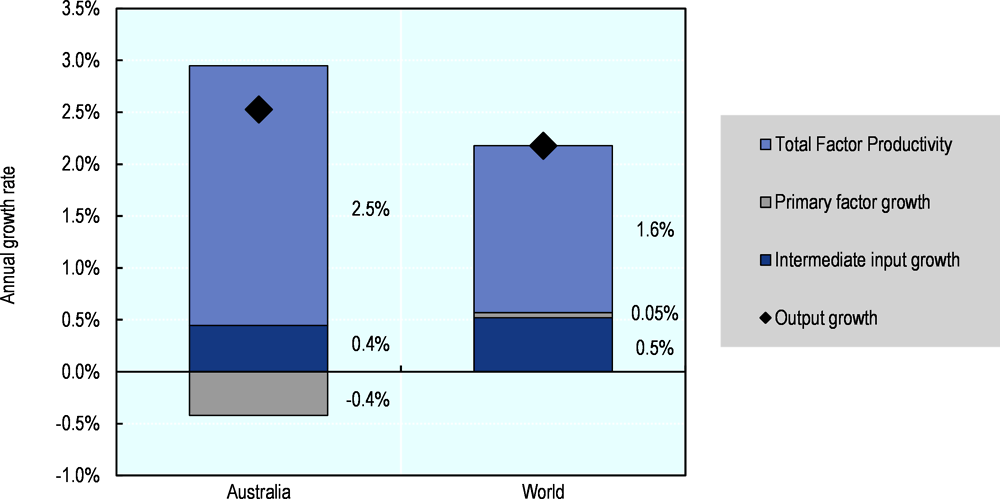

Over the 2007-16 period, total factor productivity (TFP) growth in Australia (2.5% per year) outpaced the world average, driven by continued structural adjustment and the uptake of innovative technologies and practices in the sector (Figure 4.6). Average TFP growth slowed compared to 1991-2000 partly due to challenging climate conditions (Table 4.4). Water availability and competition with other sectors is a particularly limiting factor, which may be exacerbated by climate change.

References

[7] Australian Bureau of Meteorology (2020), Water in Australia 2018-19, Bureau of Meteorology, http://www.bom.gov.au/water/waterinaustralia/files/Water-in-Australia-2018-19.pdf.

[4] Crawford School of Public Policy, T. (ed.) (2016), “Undermined by Adverse Selection: Australia’s Direct Action Abatement Subsidies”, CCEP Working Paper No. 1605, https://doi.org/10.2139/ssrn.2783542.

[3] Department of Agriculture (2019), Australian Government Drought Response, Resilience and Preparedness Plan, http://agriculture.gov.au/drought-preparedness-resilience.

[1] DFAT (2021), Australia’s free trade agreements (FTAs), https://www.dfat.gov.au/trade/agreements/Pages/trade-agreements (accessed on 30 March 2021).

[5] Freebairn, J. (2016), “A Comparison of Policy Instruments to Reduce Greenhouse Gas Emissions”, Economic Papers: A journal of applied economics and policy, Vol. 35/3, https://doi.org/10.1111/1759-3441.12141.

[2] Gray, E., M. Oss-Emer and Y. Sheng (2014), Australian agricultural productivity growth: past reforms and future.

[6] OECD (2020), Agricultural Policy Monitoring and Evaluation 2020, OECD Publishing, Paris, https://dx.doi.org/10.1787/928181a8-en.

Notes

← 1. The Smart Farms Program (Agriculture) and Regional Land Partnerships under the second phase of the National Landcare Program 2019-23 http://www.nrm.gov.au/national-landcare-program.

← 2. The Agriculture Stewardship Package https://www.agriculture.gov.au/about/reporting/budget/sustaining-future-australian-farming.

← 3. https://www.legislation.gov.au/Details/F2019L01610

← 4. Last updated in April 2019 https://www.legislation.gov.au/Series/F2015L00156.

← 5. These include with New Zealand (ANZCERTA 1983), Singapore (SAFTA 2003), Thailand (TAFTA 2005), the United States (AUSFTA 2005), Chile (AClFTA 2009), the ASEAN-Australia-New Zealand Free Trade Area (AANZFTA 2010), Malaysia (MAFTA 2013), Republic of Korea (KAFTA 2014), Japan (JAEPA 2015), the People’s Republic of China (ChAFTA 2015), the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP 2018), Australia-Hong Kong (A-HKFTA 2020), Peru-Australia (PAFTA 2020), Indonesia-Australia Comprehensive Economic Partnership Agreement (IA-CEPA 2020) and the Pacific Agreement on Closer Economic Relations (PACER Plus 2020).

← 6. https://www.wto.org/english/res_e/statis_e/daily_update_e/tariff_profiles/NZ_E.pdf.

← 7. https://www.raa.nsw.gov.au/disaster-assistance/special-disaster-loan-bushfires

← 8. https://www.environment.gov.au/climate-change/climate-solutions-package.

← 9. The eight participating countries include Australia, Cook Islands, Kiribati, New Zealand, Niue, Samoa, Solomon Islands and Tonga.

← 10. Based on UN Comtrade data, Australia ranked 6th world exporter of agro-food products in the 2017-19 period.