Iceland

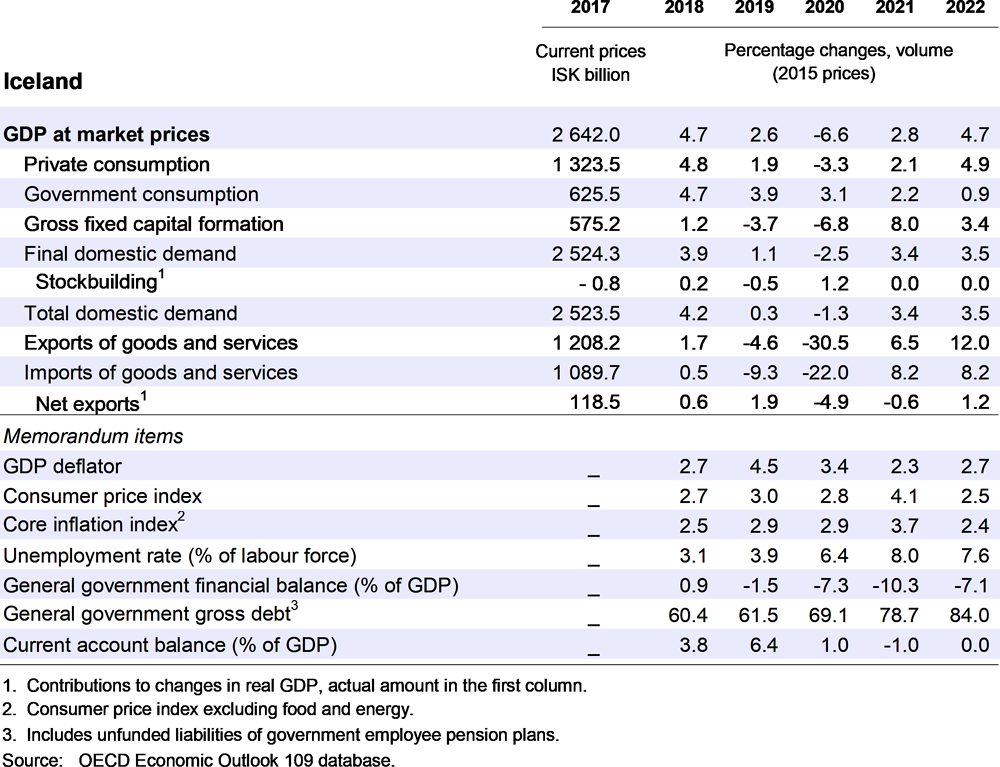

GDP is projected to grow by 2.8% in 2021 and 4.7% in 2022, driven by a rebound of foreign tourism and strong fisheries and services exports. Household consumption will rise as precautionary savings are reduced and confidence strengthens. Business investment will grow supported by improved financial conditions and the realisation of pent-up demand for infrastructure.

Monetary policy remains accommodative notwithstanding the mid-May increase in the policy interest rate. Short-term inflation expectations have risen above the central bank’s inflation target, despite a gradual appreciation of the krona since late 2020. Fiscal policy should focus on vulnerable households, and the government should implement the planned investment and recovery programme. Strengthening competition and skills would help underpin a sound recovery.

The health situation is improving

Iceland’s COVID-19 situation is improving thanks to an effective testing, tracing and tracking strategy, a well-functioning health system and targeted containment measures. The number of new infections has steadily declined since the end of last year except for a few weeks in spring 2021. Containment measures, which were less restrictive than in most countries, are being relaxed further. Vaccination is progressing well. Schools and universities have operated almost without interruption. After a temporary tightening in end-March, border restrictions are gradually being lifted.

Source: OECD Economic Outlook 109 database; Statistics Iceland; and Central Bank of Iceland.

The economy is recovering

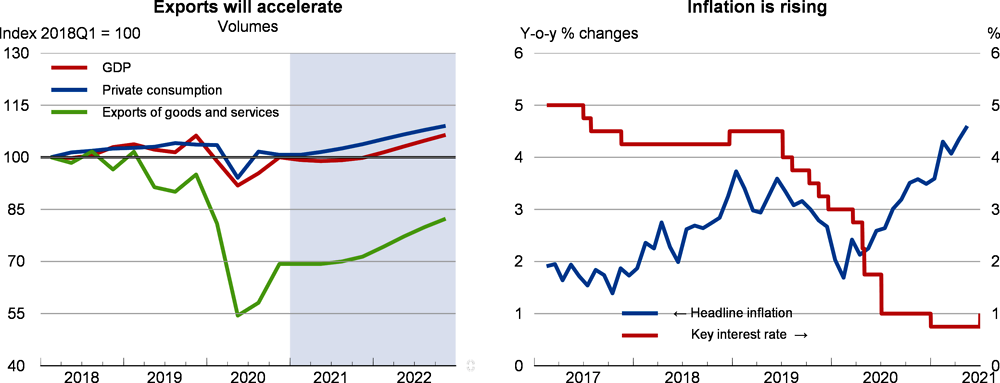

After the sharp contraction in output in the first half of 2020 and a modest recovery since then, economic momentum is returning. Tourism is recovering after the easing of external border checks. Fisheries’ exports remain strong, especially of higher-value fresh seafood and aquaculture. Some sectors, like pharmaceuticals and data storage and processing, continue to grow fast. Household consumption remains robust, based on rising wages and policy support measures. The unemployment rate hovered at around 8% of the labour force since late 2020 but has begun to recede. Immigration has declined sharply, while emigration also slowed as the employment outlook is not better abroad.

Policy remains accommodative

Policy remains accommodative. In mid-May, the central bank raised the policy interest rate by 0.25 percentage point to 1%. The króna has appreciated by around 5% over the past few months, yet inflation has risen to 4¼ per cent on the back of considerable wage growth and an increase in commodity prices. Short-term inflation expectations exceed the central bank’s target. Fiscal policy remains expansionary. Most government support has been extended until end-2021, and households may continue to draw on third-pillar retirement savings. The government should focus direct support on households in need. Public investment, especially in green transport infrastructure, digitalisation and research and innovation, should expand as planned by the government.

The recovery is set to accelerate

GDP is projected to grow by 2.8% in 2021 and 4.7% in 2022. Tourism will rebound in the second half of 2021 following vaccination and the easing of containment measures worldwide. Fisheries and service exports are set to remain strong. Business investment will recover as pent-up demand for accommodation infrastructure will be realised. Household consumption will rise thanks to regained confidence and reduced saving. Public investment, as planned by the government, will add to momentum. As the government-supported short-term work scheme ends, the unemployment rate will average 8% in 2021 but will edge down in 2022. The budget deficit will reach around 10% of GDP in 2021 and then decline to 7% of GDP in 2022, which is appropriate. Gross public debt will climb to nearly 85% of GDP in 2022. The projections are subject to substantial uncertainty and risks. The recovery of tourism relies strongly on foreign arrivals and hence on economic and health conditions overseas. The disappearance of specific fishing stock would dent exports.

Strengthening competition and upgrading skills would underpin the recovery

Structural reforms could help accelerate the reallocation of labour and foster an inclusive recovery. Strengthening competition, in particular in the construction and tourism sectors, and opening the network industries to foreign firms could help create new businesses, facilitate technology transfer, and diversify the economy. Strengthening skills, by better aligning tertiary education with labour market needs, improving collaboration between universities and firms, and upgrading vocational education and training could reduce labour market mismatch and help workers venture into new sectors and activities.