France

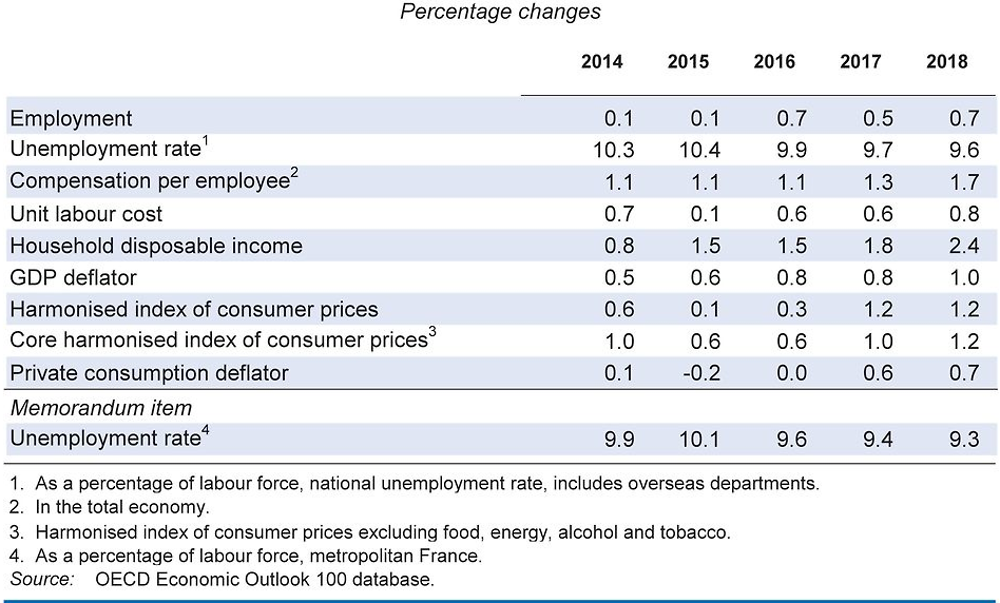

GDP growth is projected to edge up to 1.6% by 2018, as tax cuts and faster job growth support stronger private consumption. Business investment should also pick up owing to tax reductions and low interest rates. In turn, the unemployment rate should continue to gradually fall, thanks to lower social security contributions, hiring subsidies and significant upscaling of training available to jobseekers. Inflation will remain low, as slack persists.

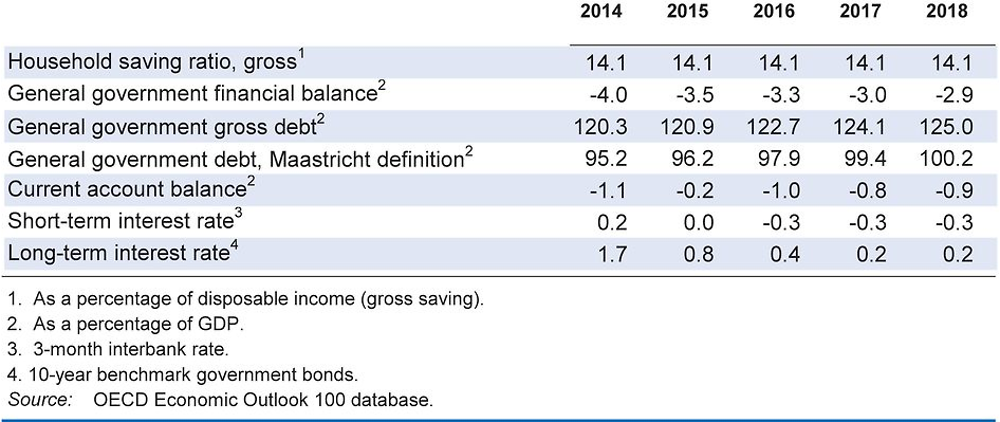

A continued reduction in debt servicing costs and some spending restraint is projected to bring the fiscal deficit down to just below 3% of GDP in 2018. Tax and social security cuts have reduced labour costs and improved the investment climate. A recent labour law reform clarifies conditions for dismissals and gives more importance to firm-level agreements on working time.

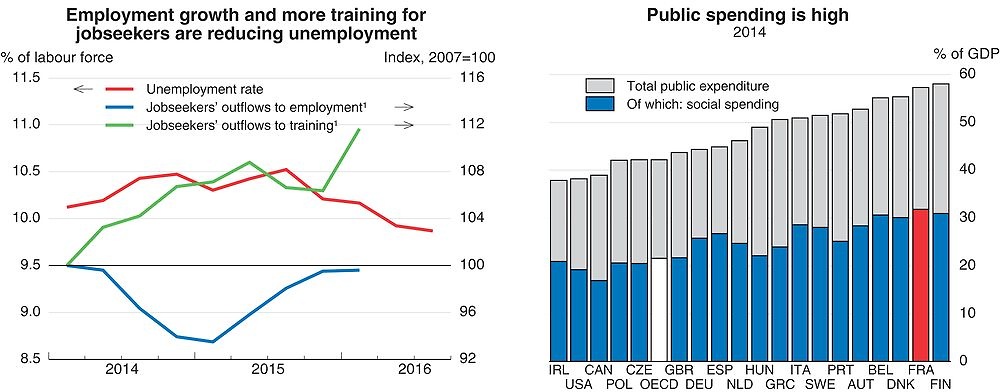

At 57% of GDP, France has one of the highest public spending ratios in the OECD, and high taxes are needed to finance it. The overall fiscal stance is largely neutral over the projection period. However, further tax and social security contribution cuts should be pulled forward to stimulate the economy and reduce unemployment faster. In the longer term, to lower the high tax burden, the government should continue to reduce spending, focussing more on limiting inefficiencies and non-priority areas. This requires continued efforts to better target social spending, reduce the number of sub-central governments and the overlaps in their competencies.

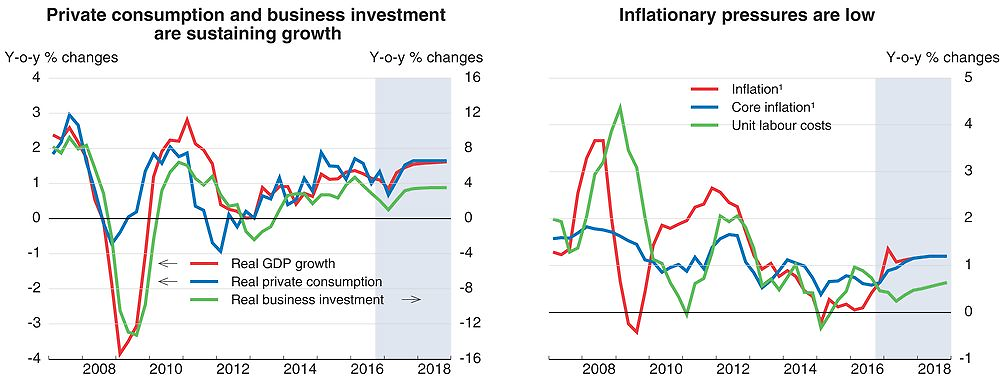

A gradual recovery has taken hold

Tax cuts and low energy prices have bolstered real wages and helped companies restore their profit margins, supporting a strong rebound in consumption and business investment. The economy hit a soft patch in mid-2016, but recent indicators suggest growth has resumed. The fall in residential investment has started to level off. Public investment has returned to growth after local governments had sharply cut back their investment in response to lower central government transfers.

1. Harmonised consumer price index, excluding energy, food, alcohol, and tobacco for core inflation.

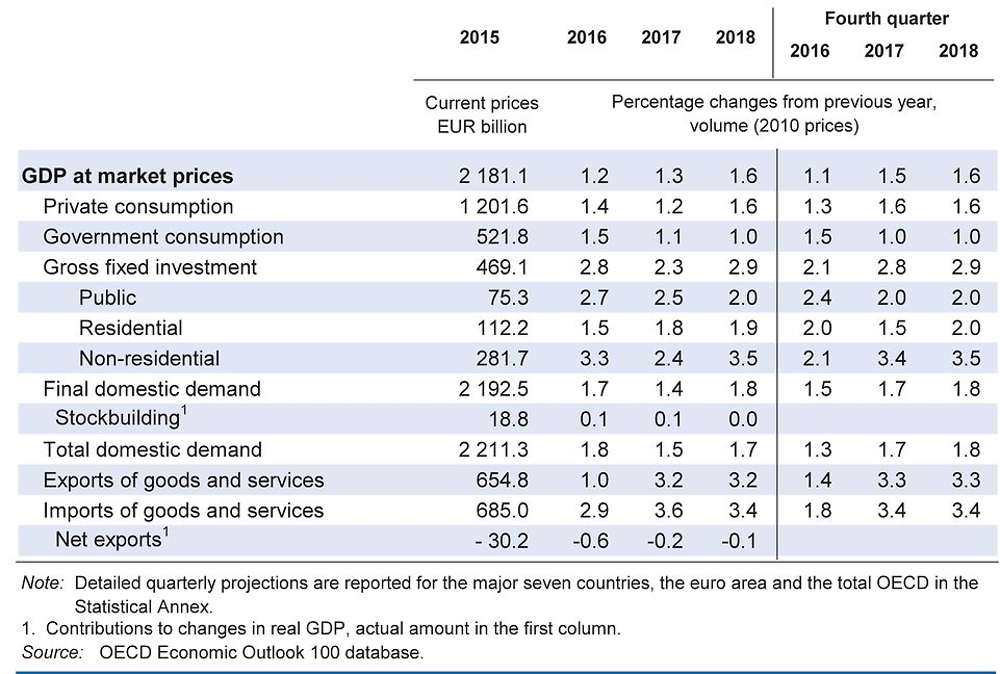

Source: OECD Economic Outlook 100 database; and INSEE.

The unemployment rate has edged down, thanks to stronger economic growth in combination with tax reductions and hiring subsidies, which has spurred hiring. In addition, the expansion of training programmes for the unemployed has temporarily drawn people out of the labour force. Headline inflation has turned positive again, as energy prices have stopped declining, but core inflation continues to be low as unemployment remains high and there is still ample spare capacity.

Further tax reductions should be pulled forward, but well-designed spending cuts are needed thereafter

Sharp cuts in local government investment reduced the general government deficit to 3.5% of GDP in 2015, which was lower than expected. The ongoing series of tax cuts will continue to reduce revenues, and the 2017 draft budget includes additional spending on employment, education and security. Yet, spending restraint in other areas, stronger growth and lower debt service, which is projected to fall by a full percentage point of GDP from 2012 levels by the end of the projection period, will help cut the deficit gradually to 2.9% of GDP in 2018.

1. Quarterly cumulated outflows of jobseekers, registered with Pôle Emploi in categories A, B and C, to employment or training schemes; three-month moving average.

Source: OECD Economic Outlook 100 Database; OECD Social Expenditure (SOCX) Database; and DARES.

France’s very high public spending means a heavy tax burden, which hurts employment and investment. To help France escape from its low-growth trap and ensure durable reductions in unemployment, planned tax cuts should be pulled forward. However, reducing the tax burden will require controlling spending through reforms that are sustainable in the long term. After years of across-the-board expenditure restraint and a partial public-sector wage freeze, the authorities need to focus more on inefficiencies and identify non-priority areas for cuts.

Further efforts are needed to better target France’s relatively high and rising social spending on the poor, contain spending on pensions and increase the effective retirement age, including by aligning older workers’ unemployment benefit entitlements with those of younger workers. Such measures would make room for better supporting children and young adults, who are too often harmed by high unemployment and poverty. Building on recent sub-central government streamlining, further reforms are needed to reduce the large number of municipalities and eliminate overlaps in competencies across different levels of government. Education spending is broadly appropriate but needs to be better targeted at weak students. The quality of infrastructure is high overall, but the recent consolidation focussed too much on public investment cuts, and this needs to be reversed, while better targeting poor neighbourhoods.

Growth is projected to increase gradually

The modest pick-up in output growth, along with continued tax cuts and new hiring subsidies, is projected to support gradual employment gains and a further small decline in the unemployment rate. The extension of the accelerated depreciation allowance into 2017 and additional reductions in social contributions and business taxes will contribute to stronger business investment. The gradual recovery in residential investment is projected to continue, and public investment should grow moderately. The prospect of the United Kingdom leaving the European Union is projected to hold back France’s exports. The current account deficit will stay largely stable at around 1% of GDP. Owing to persistent substantial slack, core consumer price inflation is not expected to accelerate.

The 2017 presidential elections create considerable uncertainty, as candidates’ economic programmes differ widely. Adverse developments in emerging markets, China in particular, would also have negative repercussions. If the nature of the United Kingdom’s exit from the European Union were to be clarified faster than expected and turned out to involve a more favourable trade regime with EU countries, such as continued adherence to the single market, French exports and investment could be stronger than under the baseline assumptions. Moreover, the medium-term effects of lower taxes and social charges on business sentiment could be larger than expected, leading to stronger investment, employment and consumption. Also, households have not yet spent all their energy-related savings but could do so in the future.