Greece

Growth is projected to turn positive in the second half of 2016, after a deep and prolonged recession, as recovering confidence boosts investment and consumption and improved competitiveness raises exports. Unemployment is still very high, which is causing serious social problems, but is now gradually receding. The huge public debt burden is undermining investment and confidence, making some form of additional debt relief (for example, extending maturities) crucial.

The pace of fiscal consolidation has slowed. This is appropriate given the need for growth and rising fiscal pressures, including from the refugee crisis. The implementation of policies such as the Guaranteed Minimum Income and school meal and housing programmes will reduce poverty and inequality, which rose sharply during the crisis. Fighting tax evasion would increase fairness and raise the revenues needed to deal with social problems. Dealing with the large stock of non-performing loans in banks is a priority to restore the availability of credit for investment.

Persistently weak productivity performance accounts for a significant part of the decline in output since the onset of the crisis. The full implementation of structural reforms will boost productivity and growth. Labour market reforms have improved flexibility and thereby productivity. Productivity growth will also be boosted by easing the regulatory burden and barriers to competition further, especially in network industries and protected professions, and increasing the efficiency of bankruptcy procedures.

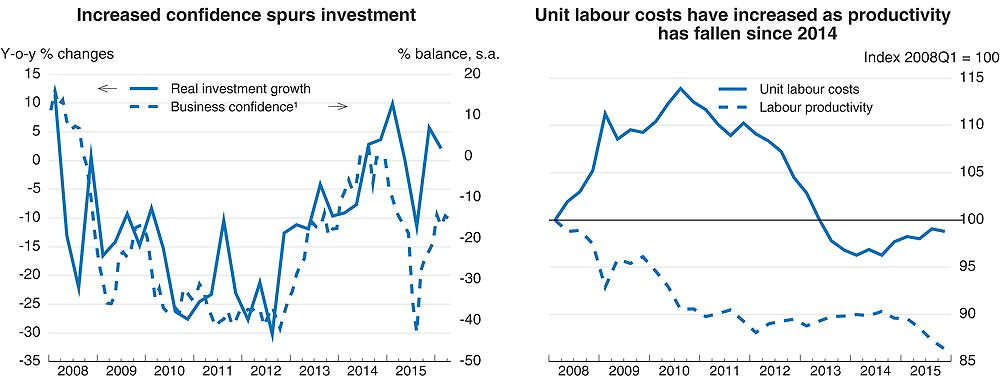

The economy is recovering gradually from a deep recession

The financing programme agreed with the European Stability Mechanism in August 2015 has reduced uncertainty and, together with the gradual softening of capital controls, boosted confidence and growth. Investment rebounded in the last quarter of 2015. Job creation improved and the high unemployment rate declined further. The inadequate social safety net has been unable to stem the rise in poverty. Inflation was still negative at the end of 2015 due to large spare capacity and falling oil prices.

1. Unweighted average of data for manufacturing industry, construction, trade and business-related services.

Source: OECD Economic Outlook 99 database; and OECD National Accounts Database.

Despite the recapitalisation of banks last December credit conditions are still sluggish due to large non-performing loans. Due to continuing fiscal consolidation, the primary balance became positive at 0.7% of GDP in 2015, outperforming the target of -0.25% of GDP. Public debt is still very high, however, bearing on investment and confidence.

Policies to reduce poverty and structural reforms are needed for more inclusive growth

The slower pace of consolidation set out in the August agreement is appropriate. The implementation of planned social policies, such as the Guaranteed Minimum Income, would alleviate poverty and help to deal with the high social costs of the crisis. The modernisation of the public employment service and the expansion of active labour market policies would reduce unemployment. Fighting tax evasion and rationalising the pension system will raise revenues to finance these policies.

The full implementation of the structural reforms agreed under the August agreement will significantly boost output over the next decade. Further reforms are needed to shift the economic structure towards exports and the expansion of new enterprises. Easing regulation in network industries will increase competitiveness and enhance exports. Further reducing regulatory procedures and administrative burdens on firms will enhance productivity and investment.

The recovery is expected to gain strength but uncertainty remains high

Output growth is projected to turn positive only in the second half of 2016 but the economy should recover in 2017 as structural reforms spur domestic demand and stronger external demand enhances exports. Increases in VAT will raise headline inflation temporarily in 2016, but inflation will stay negative or close to zero given the large economic slack. Unemployment will continue to decline alleviating poverty further.

Successful negotiations to lower the gross financing needs of the public sector could significantly improve the medium-term outlook by addressing debt sustainability risks. Full and swift implementation of structural reforms would boost confidence and lead to a stronger and faster economic recovery; but slippage in this area will be harmful for growth. Rising global risks such as weaker global trade, low oil prices and weaker growth in China and the euro area would reduce Greek exports. The cost of the refugee crisis, estimated at 0.4% of GDP for 2015, could be higher in 2016.