Assessment and recommendations

While the long-term impacts of the COVID-19 pandemic still remain uncertain at the time of writing this report, the crisis has brought to the fore many of the longstanding issues that the Czech Republic was facing in the field of housing, such as housing insecurity, homelessness and inequalities, as observed in many other OECD countries (OECD, forthcoming[1]). Such challenges are even more acute in cities and urban areas, where property and rental prices have often increased faster than in the Czech Republic in general and the share of households overburdened by housing costs or the share of those who live in overcrowded dwellings are higher. To enrich the analysis, the OECD, in co-operation with the Ministry of Regional Development of the Czech Republic or Ministerstvo pro místní rozvoj (MMR), carried out a survey of 1 877 Czech municipalities in August/September 2020 to collect data on the housing market and housing policies at the municipal level. The survey will hereinafter be referred to as the OECD-MMR housing survey. The survey covered all municipalities within functional urban areas (FUAs) of more than 50 000 inhabitants in the Czech Republic, as well as the municipalities within the FUAs of Jablonec and Mladá Boleslav (see Annex A for further details on the administration of the survey).

Following the post-1989 massive privatisation of the housing stock, including at the municipal level, homeownership is the main type of housing tenure in the Czech Republic

Following the transition from the communist regime to a market economy starting from 1989, the housing stock in the Czech Republic went through a massive movement of privatisation. Faced with strict rent regulation and a lack of financial and human resources for housing maintenance, municipalities privatised a major part of the housing stock that had been transferred to them. As a result, as in many other former communist countries in Central and Eastern Europe, homeownership has been the dominant type of tenure in the Czech Republic, with 75% of Czech households owning their accommodation (well above the OECD average of around 43%). The private rental market is relatively limited, with only 18% of Czech households renting their dwelling from the private rental sector (compared with 25% in OECD countries on average (OECD, 2020[2])). The share of households that rent their dwelling from the subsidised market (state-owned or other) is also very low, at only 1.4% of all households. Social rental dwellings only account for 0.4% of the total number of dwellings in the Czech Republic – a very low share compared with other OECD countries (e.g. 20% in Austria, 7.6% in Poland and 4.0% in Hungary (OECD, 2020[2])).

Many Czech households are struggling to access affordable housing, especially in cities

House prices have increased faster than household disposable income

Since reaching their lowest post-financial crisis levels in 2013, house prices in the Czech Republic have increased sharply and now largely exceed their pre-crisis level. Between the first quarter of 2013 and the second quarter of 2020, real house prices rose by 43.1%, a much higher growth rate than in OECD countries, where, on average, real house prices increased by 24.9% over the same period. In 2018 alone, house prices increased by 7.1% in the Czech Republic – one of the highest growth rates among EU countries (just below the growth rates observed in Hungary, Latvia and Portugal). Estimates from the Czech National Bank indicate that the Czech housing market was overvalued by around 25% at the end of 2019 (CNB, 2020[3]).

House prices in the Czech Republic have soared faster than household disposable income, making housing increasingly unaffordable for first-time buyers, renters and those who have to move from cheap areas into more expensive ones for work reasons for example. Czech households need to save more than 11 years of gross annual salaries to buy a standardised new dwelling of 70 square metres, compared to approximately 9 years in Latvia and 7 years in Hungary and Poland (Deloitte, 2020[4]).

House prices have risen faster in cities than in the rest of the Czech Republic

While house price growth has varied considerably across regions, it has generally been higher in cities than in the rest of the Czech Republic. Across the Czech Republic, the larger the municipalities in terms of population size, the more expensive the housing, suggesting that there is a price premium for living in cities. In all 13 regions of the Czech Republic, house prices are consistently higher in municipalities that have more than 50 000 inhabitants than in smaller municipalities. Prague is the most expensive city in the Czech Republic and according to the Czech Statistical Office, Prague also recorded the strongest price growth (41.7%) since 2010 for all types of real estate among all regions in the Czech Republic. Following Prague, Brno is the second most expensive regional capital, followed by Ceske Budejovice, Hradec Kralove and Pilsen.

The private rental market offers few housing alternatives due to increases in rental prices

While the rise in house prices may benefit the large share of Czech households that own their dwelling (due to the rise in the value of their assets), it means that purchasing a home remains out of reach for most newcomers to the housing market. As rents have also been increasing, the private rental market offers few alternative options to homeownership. Between the second quarter of 2019 and the second quarter of 2020, rent prices in the Czech Republic increased by 3.7%, which is lower than the 4.3% increase in house purchase prices over the same period but remains one of the highest growth rates among European and OECD countries.

Living in cities imposes a heavy financial burden on Czech households

Housing-related expenditure is the single-largest expenditure of Czech households for all income groups. In 2018, Czech households spent on average 26.5% of their total expenditure on housing – which is higher than the OECD average of 22.3% and one of the highest shares among all OECD countries. According to the European Union Statistics on Income and Living Conditions (EU-SILC), the financial burden of housing costs for Czech households is particularly high for vulnerable groups: households at risk of poverty (i.e. those with an income below 60% of the median national income), single people, people aged 65 and above, and single parents. Two in 3 low-income renters in the Czech Republic spend more than 40% of their disposable income on housing-related costs (the so-called “housing cost overburden rate”), often due to high costs of utilities (electricity, gas, water, etc.) (OECD, 2020[2]). The share of households overburdened by housing is also higher in cities than in the rest of the country, with the overburden rate increasing with the degree of urbanisation.

Drivers pushing housing demand up in Czech cities are likely to withstand the COVID-19 crisis

Many factors have been driving the demand for housing in cities

Strong demand for housing in Czech cities has been driven by many factors, including: strong economic growth and rising real wages until 2020; favourable lending conditions; changes in household composition; and population ageing. While such factors influencing house prices are national, housing markets are by definition influenced by their location and involve a range of specific local factors. Cities are popular locations and attract people who want to benefit from the availability of jobs, education, lifestyle and cultural opportunities, as well as urban infrastructure, public goods and services.

Even though the Czech Republic is less urbanised than high-income countries on average (22% of the population lives in cities, 37% in towns and semi-dense areas and 41% in rural areas, compared with 49%, 27% and 24% respectively in high-income countries on average) (OECD/EC, 2020[5]), the Czech Republic has continued to urbanise over the past decade. Its population living in FUAs, i.e. a city and its commuting zone, has increased faster than in the country overall (+4.5% between 2009 and 2019 compared to 1.8% in the Czech Republic over the same period). Faster population growth in Czech cities is due to inflows from rural areas to the main cities, as well as inflows of migrants from abroad who tend to settle in urban areas and students – both Czech and from abroad – who come to study in renowned universities. Some Czech cities are also very attractive to investors and the increase in tourism and intensified use of short-term rental platforms have put more pressure on house prices in the past few years. While the COVID-19 crisis put a sudden halt to touristic activities in the Czech Republic, most drivers pushing housing demand up in Czech cities are likely to withstand the crisis, since structural drivers such as demographic trends and attractiveness of urban areas continue to be prevalent and economic growth is expected to resume in 2021.

Housing demand has been increasing faster in urban peripheries than in urban centres

While the population has been increasing faster in FUAs than in the rest of the Czech Republic, this has been driven by an increasing share of the urban population living outside urban centres. Between 2009 and 2019, in all Czech FUAs except for the city of Most, the population increased faster in the commuting zones of the FUAs than in their core cities, indicating a phenomenon of urban sprawl. This has significant environmental, economic and social consequences, including higher emissions from road transport (as sprawling cities are characterised by larger distances between homes and jobs, more likely to be covered by car) and higher costs of providing key public services (such as water supply, electricity and public transport, which are more expensive to provide in sprawling rather than compact areas).

Czech cities face a shortage of housing supply

Construction activity has not caught up with previously high levels from before the 2009 financial crisis

Such high and growing demand for housing in Czech cities has not been met by a sufficient increase in housing supply. Construction activity (measured by the number of started and completed dwellings) declined after the financial crisis and has yet to recover. Furthermore, according to calculations from the MMR, the housing stock decreased between 2011 and 2017, as the number of new dwellings did not compensate for the wear and tear of old buildings or the change from residential to commercial use. According to the 2020 OECD-MMR housing survey, about a third of municipalities that responded built no new housing over the past five years. Furthermore, the COVID-19 pandemic put a halt to all construction projects in the spring of 2020, which will lead to a sharp decrease in completed dwellings for the year of 2020 compared to previous years.

Construction activity does not happen where it is most needed, while zoning and land use planning do not steer development towards urban areas where housing demand is high

The OECD-MMR housing survey shows that housing construction does not focus on high-priced areas, where it would be most needed. There is no indication that municipalities with higher price levels have increased construction activity, which suggests that the growth in demand (reflected in higher prices) has not been buffered by an increase in supply. In contrast, many municipalities with low price levels experienced considerable housing development. In these municipalities, there is therefore a risk that this excess in housing development creates undesired side-effects in terms of vacancy rates and urban sprawl.

In several OECD countries, local zoning and land use planning policies often hamper housing construction and limit housing supply, contributing significantly to high housing costs (OECD, forthcoming[1]). In the Czech Republic, however, there is little indication of that happening, since municipalities have zoned large areas of undeveloped land for residential development. In municipalities covered by the OECD-MMR housing survey, an average of 79 m²/inhabitant of greenfield land is zoned for development in local master plans. This corresponds to approximately 15% of the current built-up area of the municipalities covered by the survey. Yet, the Czech planning system does not seem to contribute to steering housing development in areas with high prices. There is no relationship between the amount of greenfield land per inhabitant within a municipality that is zoned for development and the level of house prices. On average, municipalities with very low price levels have zoned the same amount of land for development as municipalities with very high housing price levels, which suggests that the planning system does not contribute to reversing the pattern of untargeted housing development. This lack of planning direction is also apparent when considering that the average amount of undeveloped land suitable for development owned by municipalities is significant. According to the OECD-MMR housing survey, municipalities own about 51 m²/inhabitant of undeveloped land that is suitable for housing construction, which is equivalent to approximately 9% of their built-up area.

Private sector housing supply faces several constraints

Other factors may explain the shortage of housing supply, including a shortage of qualified construction workers and managers, making it difficult for developers and local governments to find contractors and led to lengthy construction times and higher construction costs. Furthermore, the complex building permit process generates delays in obtaining building permits and licences, creating bottlenecks in housing construction. The Czech Republic ranks 157th out of 190 countries surveyed in the World Bank’s Doing Business 2020 survey in terms of “dealing with construction permits”. It takes 21 procedures and 246 days to build a warehouse in the Czech Republic, whereas in OECD countries on average, it takes 12.7 procedures and 152.3 days (World Bank, 2019[6]). According to the OECD-MMR housing survey, municipalities responded that the main constraints for private developers were the cost of infrastructure provision, the lack of available land and the lack of infrastructure capacity. In line with the aforementioned World Bank data, the complicated and lengthy building permit process also ranked high on the list of constraints.

The housing stock in Czech cities is often old and needs energy efficiency improvements

Almost all Czech households have access to basic facilities since 99.3% of dwellings in the Czech Republic offer private access to an indoor flushing toilet, which is more than the OECD average of 95.6%. The Czech Republic also fares relatively well compared with other European countries when it comes to the basic quality of dwellings.

However, people living in cities tend to have less space than people who live in rural areas or towns and suburbs. In 2018, the average number of rooms per person was 1.4 in cities, compared with 1.5 in towns and suburbs and 1.6 in rural areas. This was slightly lower than the European average of 1.6 rooms per person who lives in a city. A relatively high share of Czech households also lives in overcrowded dwellings: 12.2% of the Czech households, slightly above the OECD average rate of 10.9%. Tenants are also much more likely to live in overcrowded housing than homeowners (OECD, 2020[2]).

An additional issue related to housing quality in cities in the Czech Republic lies in the physical deterioration of real estates, including buildings and neglected public spaces. According to the 2011 Population and Housing Census, the average age of occupied residential buildings in the Czech Republic was 52.4 years for multi-unit buildings and 49.3 years for family houses, which is older than the average age of buildings in the EU (Office of the Government, 2019[7]). Although the State Investment Support Fund has implemented several programmes to encourage repairs and modernisation of housing, the number of dwellings for which renovation (requiring building permits) has started or been completed has been decreasing over the past decade.

Renovation to improve dwellings’ energy efficiency is another key dimension of housing quality, which can have a substantial impact on housing affordability. While energy efficiency improvements have occurred in the past years (mostly due to improvements in insulation of buildings, refurbishment of old buildings and improvements in heating equipment), energy intensity per floor area of residential space heating (i.e. the energy used to heat one square metre) is still high and remains one of the highest among OECD countries (after correcting for temperatures).

Barriers to the housing market leave some social groups in substandard housing

As private rental accommodations rented at market prices have become financially inaccessible for many Czech households and availability of municipal social housing is limited, many households have no choice but to turn to substandard housing, such as dormitories. Dormitories are flats or rooms, most often in private buildings, where residents do not have standard rental contracts, do not receive a local residence permit and frequently pay overpriced rents for small and low-quality spaces (e.g. shared kitchen, shared sanitation facilities, overcrowding, badly insulated with energy leaks), poorly maintained by their private owners. People who have been living in this type of alternative housing often face stigma and discrimination when they later attempt to access the private rental market, which locks them in precarious housing in the long term. These facilities frequently provide housing to migrant workers and marginalised population groups, such as the Roma, who are often excluded from regular housing markets.

Within the 758 municipalities that provided information on dormitories as part of the OECD-MMR housing survey, there are 555 privately-run dormitories, which are home to approximately 0.7% of the population in these municipalities. However, these numbers could be underestimated given the difficulties in collecting reliable data on dormitories, in particular due to their complicated ownership structures

In addition to people living in substandard conditions or inadequate housing, there are also a number of people who are either homeless or at risk of becoming homeless. According to the Ministry of Labour and Social Affairs, in 2016, there were around 68 500 homeless people (of which 21 230 adults and 2 600 minors are “roofless”, according to the 2019 census) and 119 000 are at the risk of becoming homeless across the Czech Republic.

Social housing provision does not meet the needs of all low-income and vulnerable households

The social housing stock in the Czech Republic is too small to meet the demand of all low-income and vulnerable households

In the Czech Republic, social housing is understood as municipally owned housing that is allocated based on criteria decided by the municipality. As discussed previously, the social housing stock in the Czech Republic is very small, accounting for only 0.4% of the total number of dwellings in the country – a very low share compared with other OECD countries. However, this very low number could well be the consequence of an unclear definition of what constitutes social housing in the Czech Republic. Even after excluding outliers, municipalities participating in the OECD-MMR housing survey indicated that they own 8.7% of their total housing stock and provide it to residents at below-market rates. Social housing provision by non-governmental organisations also remains very rare. It exists only in 5% of all surveyed municipalities and the number of housing units provided tends to be low (3.6 housing units per 10 000 inhabitants). Approximately half of these units were built in the past five years, indicating that this is a relatively novel approach that could have the potential to grow in the future.

According to the OECD-MMR housing survey, more than half of the municipalities covered by the survey own housing (57%). However, this percentage varies significantly according to the size of the municipality, ranging from less than 40% among very small municipalities to close to 90% of large municipalities. Furthermore, more than 90% of municipalities that own housing make at least part of their housing stock available as social housing and 73% provide their entire housing stock at below-market rents.

The shortage of social housing is visible in the long waiting lists of aspiring tenants who apply for social housing. Among municipalities that allocate access to social housing through waiting lists, the median wait time is 24 months but, in 18% of municipalities, it can even reach 60 months or longer. In light of such a shortage of social housing, it comes as no surprise that 35% of municipalities that responded to the OECD-MMR housing survey indicate that increasing the stock of social housing is a policy priority. However, only 15% of all municipalities built any housing between 2015 and 2019.

Allocation of social housing varies across municipalities

Social housing in the Czech Republic is mostly provided by municipalities, which have complete autonomy in deciding how to use the housing stock that they own. They can choose to rent it out at market rates, just as any private rental housing provider, or to provide social housing at reduced rents to specific population groups. If municipalities choose the latter option, they set eligibility criteria autonomously and determine the conditions at which they rent it out (such as rent levels, deposit requirements, etc.). Municipalities are not only free to choose how much social housing they provide and at what price, they can also determine who is eligible and how to allocate housing within the eligible population. In the absence of national binding guidelines, the allocation of social housing to households in need by individual municipalities is sometimes opaque and can prevent some households that need it the most from accessing social housing. Selection criteria may include: time spent on a waiting list; social criteria such as age, family size, single-parent households and people belonging to specific marginalised communities such as the Roma community; special arrangements for the disabled and elderly; and the amount of a contribution tenants make to the municipality, without a clear and systematic record system of these contributions.

Beyond designating eligible groups for social housing, municipalities can introduce further requirements that can limit access to social housing for some population groups. Especially relevant in this context are deposit requirements and a ban on individuals who have a debt with the municipalities. Both requirements can prevent very low-income households from accessing social housing even though they are most urgently in need.

Municipalities face obstacles in the development of social housing

According to the OECD-MMR housing survey, local governments own considerable amounts of undeveloped land that is suitable for housing development (approximately 9% of their built-up area). Although Czech municipalities own significant amounts of developable land, there is a lack of investment in new social housing in general in the Czech Republic. In 2018, central government spending on social rental housing (encompassing both direct provision of social rental housing and subsidies to non-governmental social rental housing providers) in the Czech Republic was only 0.01% of gross domestic product (GDP) – this is about 10 times less than the average of public spending by national governments of OECD countries for which data is available (OECD, 2020[2]).

Several reasons could explain the low level of investment in new social housing. First, much of the municipally owned land suitable for development is located in small municipalities. According to the OECD-MMR housing survey, 71% of all municipally owned land belongs to municipalities that have less than 1 000 inhabitants. Such small municipalities might not have the capacity needed to provide affordable housing on the land. Moreover, house prices in municipalities that own larger amounts of land per capita tend to be lower than house prices in municipalities that own less land, reducing the incentives to build more affordable housing. Furthermore, the current legislative framework in the Czech Republic puts the responsibility of providing affordable housing and allocating social housing on municipalities, which may deter municipalities from making politically risky and unpopular decisions. When municipalities do intend to develop social housing, they are faced with a number of obstacles, the most important bottleneck being the shortage of funds (both from their own financial resources and from the national state).

The Housing Policy Strategy provides a dedicated national framework for housing affordability policy in the Czech Republic

The Czech Republic has a specific national housing policy in place, called the Housing Policy Strategy in the Czech Republic Till 2020 (hereinafter the Housing Strategy). The Housing Strategy focuses on three priorities: i) affordability of adequate housing; ii) stability of the housing market; and iii) quality of housing (Ministry of Regional Development, 2011[8]). This framework offers a comprehensive outline of the policy instruments available in the Czech Republic, including support for homebuyers and homeowners (subsidies to households to facilitate homeownership, tax relief for access to homeownership, support to finance housing regeneration), the housing allowance for tenants and homeowners, the housing supplement for social assistance recipients and subsidies for the development of affordable rental housing. Initially established in 2011 and set to be renewed in 2021, it follows a clear time horizon and is updated on a regular basis to keep abreast of new trends and developments on the housing market. Furthermore, its focus on housing quality as well as quantity constitutes an important effort to adopt a holistic approach to housing affordability, especially as the housing stock in Czech cities is often old and in need of energy efficiency improvements.

However, its implementation faces legal, institutional and financial challenges

Despite the existence of this concrete national housing policy framework, some limitations are hampering its effective implementation. One major limitation to the Housing Strategy is the lack of legal definition for terms as important as “social housing”, which has led to an “underregulated” and inefficient social housing sector (de Boer and Bitetti, 2014[9]). A national framework for social housing does exist, in the form of the Social Housing Policy Strategy of the Czech Republic 2015-2025, which was approved in 2015 and is under the responsibility of the Ministry of Labour and Social Affairs. While it outlines the objectives of the Czech government in terms of social housing, it does not constitute legislation on social housing, it is distinct from the Housing Strategy with no clear and systematic connection with it and the term “social housing” remains used in different ways throughout official documents.

Furthermore, the high number of actors within the system complicates the national housing policy framework. At the national level, housing policy is primarily led by the Ministry of Regional Development. However, other ministries administer certain housing benefits and related programmes without clear co-ordination mechanisms. For example, prominent actors include the Ministry of Labour and Social Affairs (social security allowance for housing, contribution for renovations for disabled people), the Ministry of Finance (building savings scheme, tax relief measures), the Ministry of the Environment (energy efficiency renovations scheme) and the Ministry of the Interior (integration of asylum seekers). At the local level, municipalities are responsible for housing provision, including affordable and social housing. They also have competency over grant allocation and distribution, urban planning and zoning.

Another obstacle is a lack of financial resources, both at the national and local levels. The government’s spending to support housing affordability in the Czech Republic is generally low compared to other OECD countries. In 2017, state expenditure on housing was only 0.39% of GDP, including about 0.18% spent on housing allowances (below the OECD average of 0.25%).

Direct policy instruments to support housing affordability exist but have limitations

Two main housing policy instruments in the Czech Republic are: i) the housing allowance, paid to low-income families and individuals who cannot afford housing at market prices (i.e. housing costs exceed 30% of the household’s sum of incomes after deduction of contributions to health and social insurance and income tax); and ii) the housing supplement, paid to the lowest-income households. These are both distributed by the Ministry of Labour and Social Affairs. However, unawareness of the benefit, the complicated administrative process to receive it and recent adjustments to the formula determining the income taken into account to assess eligibility resulting in more complexity can lead to some “non-uptake” of the housing allowance among eligible households.

Multiple policy instruments encourage homeownership, mostly via demand-side subsidies, including grants and tax reliefs, buy-to-rent schemes and relief for distressed mortgages, with several programmes targeting specific groups run by the State Investment Support Fund (former State Housing Development Fund). However, supporting homeownership may not solve the affordability issue for low-income families, and some policies to encourage homeownership may in fact be counterproductive. For example, mortgage interest tax deductions for homeownership may disproportionately benefit high-income households. Furthermore, homeownership can hinder labour mobility and be a driver of structural rigidities, partly because high transaction costs associated with the purchase or sale of property result in homeowners being less mobile than renters. This can be an issue especially in the current context of the economic fallout from the COVID-19 crisis and the rise in unemployment.

Municipalities tend to lack a housing policy framework and intermunicipal co-ordination on housing policy remains limited

At the local level, Czech municipalities generally lack a housing policy framework. A comprehensive and solid housing policy framework is important to set strategies that address housing shortages, monitor local housing construction trends and prices, as well as to set explicit targets for housing development. According to the OECD-MMR housing survey however, 63% of municipalities that answered the survey indicated they had no housing strategy. Another 70% of municipalities had no explicit quantitative and/or qualitative targets for housing development in place and 75% failed to monitor housing prices on a regular basis. Finally, over one-third (36%) of municipalities did not monitor local housing construction trends. Even when there is a housing strategy, it is not embedded within a broader spatial planning framework. In addition, 89% of municipalities indicated that there was no intermunicipal co-ordination on housing policies.

This lack of intermunicipal co-ordination on housing policies may be related to the lack of incentives for co-operation in the subnational financial framework in the Czech Republic. Subnational governments in the country are mostly financed through a mix of shared taxes (personal and corporate income tax, and value added tax), as well as grants and transfers from the central government. Although progressive decentralisation from 1989 onwards has given Czech municipalities more competencies, municipalities have little fiscal autonomy compared to other OECD countries. Since population size is the main determinant of the revenues that municipalities receive from the national government through the tax-sharing formula, municipalities in the Czech Republic tend to compete with one another for the population in order to increase their revenue base and the size of government transfers. This may lead to suboptimal land uses such as the promotion of sprawling housing developments for which it is costly to provide services and deliver and maintain infrastructure (OECD, 2017[10]).

Steer housing development toward urban areas where demand for housing is high

Provide clear national and regional guidance to local planning policies

In order to increase affordable housing in urban areas where it is most needed and reduce vacant housing in areas where demand for housing is low, housing development needs to target urban areas where housing demand is high. This requires national, regional and local action. National planning frameworks need to provide clear regulation to guide local planning policies on where housing development should occur or not. Where necessary, these guidelines should also have binding power on local governments. In turn, municipalities should strive to adapt their planning policies more effectively to local housing markets. Where demand for housing is high, planning policies should encourage high-density housing development. Where housing demand is low, local zoning should be more restrictive to prevent overdevelopment and its associated negative fiscal and environmental consequences.

Use local land use planning instruments to encourage private sector construction of affordable housing

The use of developer obligations within local land use planning policies could be broadened. In particular, many OECD countries have successfully used inclusionary zoning (i.e. the requirement on developers to provide a share of housing units in new developments as affordable rental units) to improve housing affordability in the most expensive cities. For example, most major cities in Germany use inclusionary zoning and related instruments extensively. In 2020, the city of Frankfurt passed a new regulation that not only requires the provision of 30% affordable rental units in greenfield developments but also the provision of 10% affordable owner-occupied units, 15% co-operative units and 15% free-market rental units.

While such regulation is especially suitable for urban areas where housing demand is high, it needs to be used more carefully in contexts where housing demand is less high, as it may stifle housing supply and increase prices if it reduces incentives for developers to build housing. In cities with lower housing demand levels, requirements such as those introduced by Frankfurt could obstruct new housing development. To avoid such unintended consequences, it is important that inclusionary zoning and similar requirements are adapted to the local context.

To enable local governments to use inclusionary zoning, the national government needs to provide the corresponding legal framework. Local governments, in turn, need to develop the expertise and build up the administrative capacity within their planning departments to use the instruments at their disposal effectively. In particular, local governments will need to strengthen their capacity to develop effective regulatory plans and use their planning powers to engage proactively with developers to steer housing development in the desired direction.

Minimum parking requirements should also be abolished to reduce construction costs and encourage housing construction within urban centres. Such requirements tend to drive construction costs up, especially in densely populated city centres where the cost of providing the parking space often exceeds the price of the car that uses it (Litman, 2016[11]). They also generate high social costs as they take up valuable public space and encourage car use over public transport (Shoup, 2005[12]).

Ensure compact, transport-oriented development to reduce auxiliary costs of housing in cities

Transport-oriented development offers an important tool to reduce the auxiliary costs of housing. Housing that is located far away from city centres and disconnected from public transport networks requires long car commutes. The costs associated with these commutes can outweigh cheaper housing costs associated with more peripheral locations.

One option to steer housing location towards transport-oriented development is the use of integrated indices that take both housing and transport costs into account, such as the Housing and Transportation (H+T) Affordability Index used in the United States. Planners can use such an index to encourage the construction of affordable housing in neighbourhoods with higher land costs but lower transport costs, and to target public transport investments (Guerra and Kirschen, 2016[13]). The index can also help individuals make informed decisions about where to find the most affordable housing, taking into account transport costs.

Beyond improving housing affordability, transport-oriented development yields a range of other benefits for low-income households. For example, it can contribute to avoiding segregation and facilitating access to public services and economic opportunities that might otherwise remain out of reach for these households due to a lack of suitable transport options.

Manage publicly owned land strategically to provide affordable housing where possible

In places where housing demand is already high, municipalities should aim at using this land for the provision of affordable housing, for example by entering into joint development agreements with private developers or not-for-profit housing providers. Where housing demand is currently low or where publicly owned land cannot be developed for other reasons, municipalities should treat publicly owned land as a strategic resource that can help them provide affordable housing in the future. Where possible, infrastructure investments and other urban planning decisions should help enable the future use of municipal land for affordable housing development. Likewise, decisions to sell public land should be made only after taking a long-term perspective on the potential value of the land for the municipality.

Monitor the effectiveness of the national reform of the building permit process

The complexity and time-consuming process for obtaining a building permit in the Czech Republic is an obstacle to more housing development. The current ongoing reform of the Building Act and related laws (which are expected to take effect in 2023) is an attempt to alleviate such challenges and accelerate the building process, especially by integrating separate processes (including the issuance of binding opinions, zoning decisions and building permits) into a single procedure managed by a one-stop-shop regional building and construction authority. The renewed building permit process aims to give citizens the opportunity to obtain a building permit within one year of submitting an application, including a possible appeal against a decision and judicial review. While this reform is expected to accelerate and streamline the permit-granting procedures for the average citizen and the larger investor, the planned change will be demanding on the management and internal organisation of work within the regional building and construction authorities. A key condition for the successful setup and operation of the new system is the overall digitisation of administrative proceedings and documents for issuing decisions. The impact of this reform should be monitored to make sure the procedures are accelerated and streamlined, both for individual citizens and for large developers.

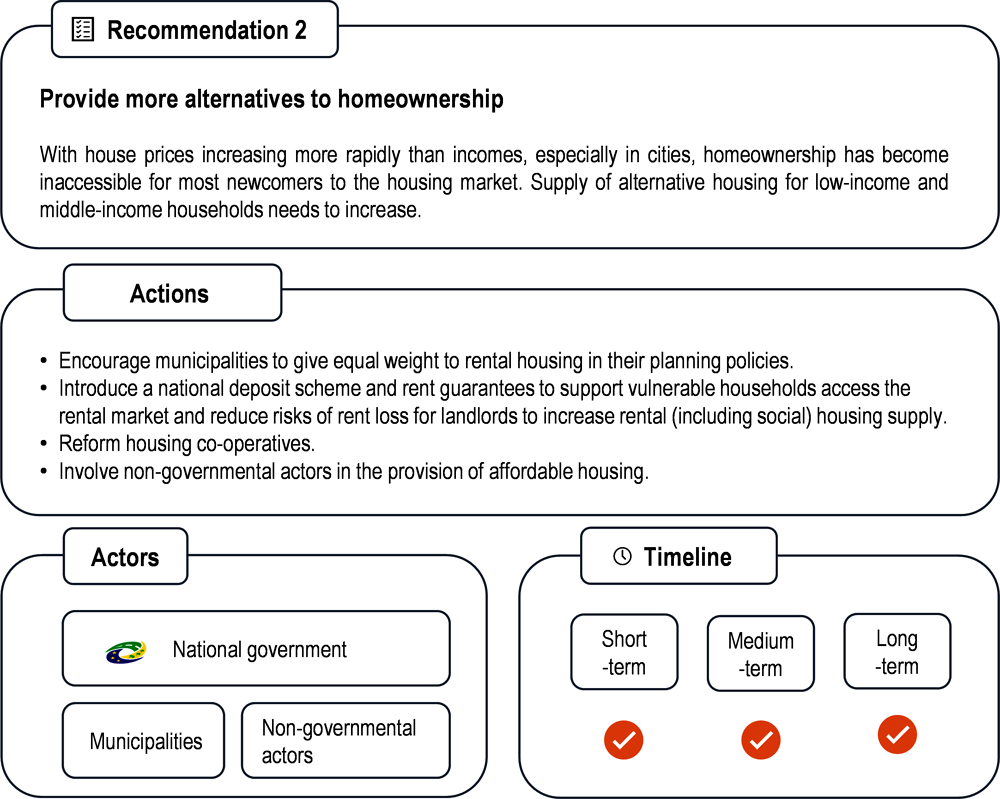

Provide more alternatives to homeownership

Encourage municipalities to scale up rental housing in their planning policies

Sufficient stock of affordable rental housing is a key component of an affordable housing market. Rental housing is the only solution for low-income households and for the “squeezed” middle class that do not have access to social housing but are unable to afford mortgages to purchase housing. Moreover, rental housing is usually available at much shorter notice than owner-occupied housing and social housing.

Although the stock of rental housing in the Czech Republic is low by international standards, municipalities give the provision of rental housing a very low priority. Only 11% of all surveyed municipalities indicated that increasing the stock of rental housing is a policy priority, even though 46% of all municipalities were in favour of increasing the supply of privately built housing.

Given the importance of rental housing for low-income and middle-income households and the low stock of rental housing in the Czech Republic, public policies at all levels of government should encourage the construction and provision of rental housing. National incentives to increase the stock of rental housing must be better structured to allow municipalities to leverage them. Municipalities often lack the resources to take advantage of existing programmes (such as the Guarantees programme for rental apartment development) as they cannot fund construction upfront.

The Czech Republic could take further inspiration from many OECD countries where national governments have implemented specific measures to support the rental market. Such measures include rent guarantee and deposit schemes, and minimum quality regulations for rental dwellings. For example, rent guarantees and deposits can be structured to reduce risks of rent loss for landlords in order to increase the supply of private rental housing or to support tenants who cannot afford to pay the initial deposits for rentals. Given the inability of some low-income households to pay such deposits, national deposit schemes could play an important role, in particular by supporting households currently living in dormitories to move into regular housing.

Reform housing co-operatives and engage non-governmental actors to reach housing affordability objectives

Housing co-operatives became popular in the post-war Czech Republic because most construction costs could be financed by state loans and more efficient housing structures (i.e. multi-unit buildings, prefabricated buildings) could be constructed by several households pooling resources rather than by any one household alone. Today, residents are legally allowed to sell the right to live in housing co-operatives. This is due to provisions enacted to curb the grey market trading of housing shares.

EU state aid rules in relation to the support of housing outside of social housing are rather strict, complicating the ways the national government can support non-governmental actors in the provision of affordable housing. The EU Urban Agenda Housing Partnership’s guidance paper on EU regulation and public support for housing stipulates that “non-financial measures are also available to authorities to support investments in affordable, adequate and social housing without being labelled as state aid under EU rules. E.g.: Support the creation and capacity of institutions and organisations that will contribute to social and affordable housing such as not-for-profit investors, Community Land Trusts, housing cooperatives and public companies” (2017[14]). Such non-financial measures like supporting non-profit organisations as housing providers could be leveraged to promote further the co-operative housing sector.

Reinforce the supply of social housing

Increase public investment in social housing

Reducing the shortage of social housing will require greater public investment by the national and local governments. Currently, municipal housing construction is low, even though it is a political objective for many municipalities to increase social housing provision. As a consequence, long waiting lists for social housing persist and a significant number of people have little choice but to live in dormitories and other forms of substandard accommodation. Additional financial support from the national government for social housing development is critical to provide more affordable housing. National support to municipalities should also be made available ahead of construction to avoid that short-term financing constraints deter municipalities from undertaking social housing development.

Introduce a national social housing legislative framework that guides municipal housing

In addition to the objectives already set out in the Social Housing Policy Strategy of the Czech Republic 2015-2025, clear national legislative guidelines on social housing could help better co-ordinate social housing policies conducted by municipalities. The current lack of national guidelines has created an uneven landscape across the Czech Republic, in which social housing stocks, prices and eligibility requirements vary widely among municipalities. National guidelines can help steer a more equitable distribution of the available social housing stock and give priority to those who need it the most. Such guidelines should include a legal definition of social housing that enables all levels of government to regulate social housing effectively. Moreover, they should ensure co-ordination across municipalities within FUAs (see OECD definition of FUAs (Dijkstra, Poelman and Veneri, 2019[15])) to take into account the fact that the need for and availability of social housing are uneven across municipalities. Lastly, national guidelines should provide municipalities with financial incentives to continuously enlarge their social housing stock.

Remove barriers to access to social housing

Deposit requirements and restrictions on debt prevent some eligible households from accessing social housing, thereby excluding many of the poorest households that would need access to social housing most urgently. In order to prevent households living in social housing from persistently failing to pay their rent, other options should be explored. For example, the national government could create a legal basis that allows municipalities to withhold rent payments from the housing allowance if social housing tenants repeatedly fail to pay their rents.

Ensure the most vulnerable households have access to adequate housing

Simplify the application process for housing allowances and subsidies, and ensure it remains accessible to those who need them the most

The complex administrative procedures to access housing allowances and subsidies can be prohibitive for some households. Simplifying the housing allowance system to reach more people is, therefore, a positive step. However, to be eligible for such benefits, households must have already established a residence for a number of months, which means that those who are unable to access such housing in the first place often remain out of the system even though they are the most vulnerable (e.g. those living in temporary accommodation, including dormitories). The simplification of the housing allowance system must therefore be part of a broader package of measures to protect the most vulnerable households.

Strengthen the regulation of dormitories to better protect residents

National regulations of dormitories should be strengthened to better protect residents and improve their living conditions. Although tenants in rental housing are typically granted some statutory protections, people living in dormitories usually do not benefit from them. Not only do tenants of dormitories lack security of tenure but there is a higher risk of eviction for groups such as the Roma community in particular.

While national and local governments should ultimately aim at eliminating the need for dormitories altogether, short-term regulations have to strike a balance between increasing the protection of residents and avoiding the closure of dormitories. As dormitories often constitute a last-resort option for residents, regulations that would lead to their closure would leave residents worse off unless viable alternative forms of accommodation exist. National regulations of dormitories should therefore include provisions on minimum quality requirements (e.g. number of residents per room, number of bathrooms, etc.) and provide increased statutory protection for residents.

Adopt a metropolitan-area approach to housing (including social housing), transport and spatial planning

Housing and land use planning policies should be co-ordinated at the level of the FUA. Municipalities within the Czech Republic are very small by international standards. This limits the administrative capacity of municipalities and increases the need for co-ordination across municipal boundaries. While a wide range of tools for intermunicipal co-operation exists in the Czech Republic, few concern the housing sector.

Developing joint housing, transport and spatial plans at the metropolitan level can help overcome the consequences of administrative fragmentation and steer housing development to locations that are well connected to public transport and close to employment centres. The national government should continue to support intermunicipal co-operation and joint service provision, including by providing financial incentives for it.

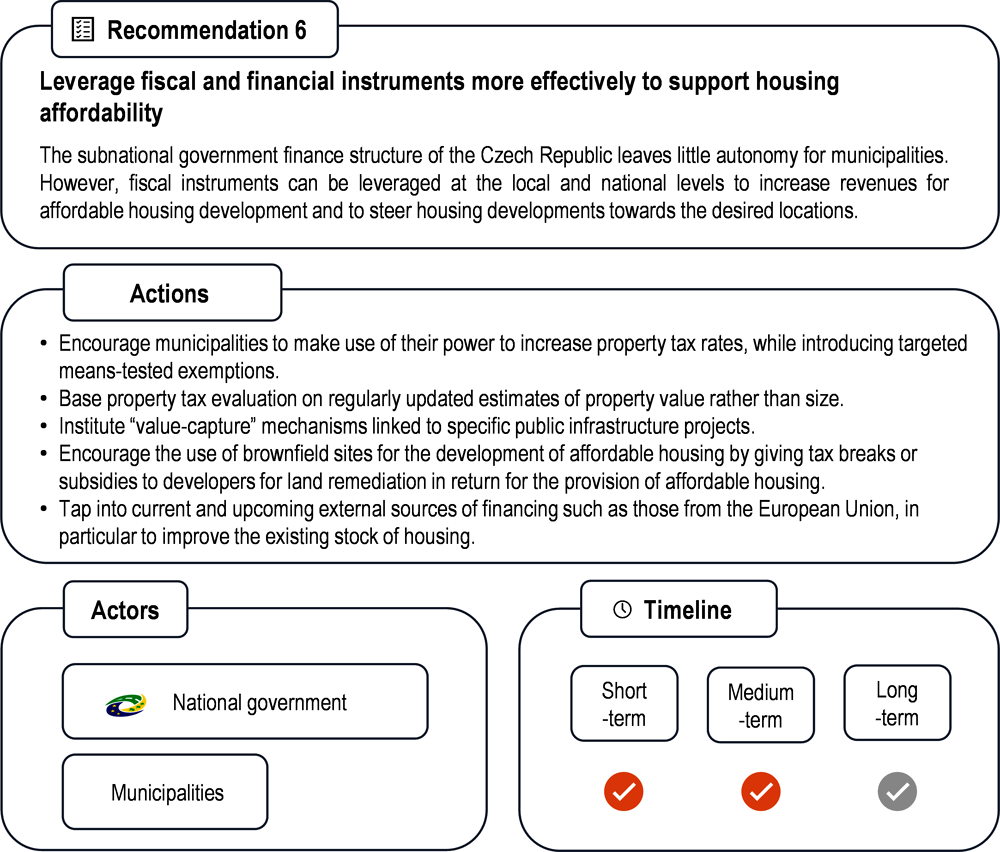

Leverage fiscal and financial instruments more effectively to support housing affordability

Due to their low level of fiscal autonomy, Czech municipalities tend to compete with one another to attract the population and increase their share of government transfers. As indicated in several OECD reports (Blöchliger, 2015[16]; OECD, 2020[17]), the Czech Republic is not using property tax to its full advantage. At 0.6% of total government tax revenue in 2018, the recurrent tax on immovable property is very low compared to the OECD average of 3.1%. The same holds true for the subnational level: property tax on land and buildings accounts for 4.3% of subnational government tax revenue, 2% of total consolidated subnational government revenue and 0.2% of GDP, which is well below the OECD average of 1.1% of GDP. The base rate is set centrally and municipalities can raise the rate to five times the minimum threshold amount. However, most municipalities tend to set their local property tax rate at the lowest level. Only 7% of municipalities have made use of the possibility to increase tax rates (Janouskova and Sobotovicova, 2016[18]). If more municipalities used their power to increase property tax rates, this could directly augment municipalities’ tax revenue, thus enabling them to invest more money in housing. To avoid resistance from municipalities to the tax and unintended consequences (e.g. in terms of increasing the housing burden for low-income households), targeted means-tested exemptions could be introduced, such as exemptions for low-income households.

A differentiated property tax could also be used to incentivise more efficient land use through higher-density housing development, discourage low-density housing and promote brownfield developments. Such instruments are currently underused by Czech municipalities and constitute a missed opportunity. In particular, property tax does not capture changes in market value as the calculation of the tax is based on the size of property rather than its value. The tax evaluation should be based on regularly updated estimates of property value rather than size, as is currently the case. Rather than allowing private individuals and businesses to retain the entire market value benefit from increased property values attributable to public spending and investment, municipalities in the Czech Republic could take steps to “capture” a portion of the increases in value. A shift to a value-based property tax and/or the implementation of various “value-capture” mechanisms linked to specific public infrastructure projects would help achieve such an objective.

In addition to residential developments, commercial and industrial developments often occur on greenspace. Complicating the issue of new development are the many old industrial or brownfield sites in the Czech Republic. Even though these sites represent potential development sites and their redevelopment should be encouraged, they can be very difficult to revitalise. The remediation required by brownfield sites poses an obstacle to their use as municipalities may lack the funds that would be necessary for their rehabilitation. In order to use brownfield sites while encouraging the development of affordable housing, programmes giving tax breaks or subsidies to developers for land remediation in return for the provision of affordable housing could be considered.

Czech local and national governments could tap into current and upcoming sources of financing, such as those offered by the EU in the context of the recovery package and the Renovation Wave,1 and especially the Affordable Housing Initiative (AHI).2 This initiative will provide support, knowledge and expertise to local industrial partnerships with the ambition to pilot lighthouse renovation neighbourhoods, putting liveability, sustainability and socially responsible business models at the forefront. Given the labour-intensive nature of the building sector, improving the existing housing stock, including in terms of energy efficiency, could also foster post-COVID-19 recovery in the Czech Republic.

References

[16] Blöchliger, H. (2015), “Reforming the Tax on Immovable Property: Taking Care of the Unloved”, OECD Economics Department Working Papers, No. 1205, OECD Publishing, Paris, https://doi.org/10.1787/5js30tw0n7kg-en.

[3] CNB (2020), Financial Stability Report 2019/2020, Czech National Bank, https://www.cnb.cz/export/sites/cnb/en/financial-stability/.galleries/fs_reports/fsr_2019-2020/fsr_2019-2020.pdf.

[9] de Boer, R. and R. Bitetti (2014), “A Revival of the Private Rental Sector of the Housing Market?: Lessons from Germany, Finland, the Czech Republic and the Netherlands”, OECD Economics Department Working Papers, No. 1170, OECD Publishing, Paris, https://dx.doi.org/10.1787/5jxv9f32j0zp-en.

[4] Deloitte (2020), Property Index: Overview of European Residential Markets.

[15] Dijkstra, L., H. Poelman and P. Veneri (2019), “The EU-OECD definition of a functional urban area”, OECD Regional Development Working Papers, No. 2019/11, OECD Publishing, Paris, https://dx.doi.org/10.1787/d58cb34d-en.

[14] EU Urban Agenda Housing Partnership (2017), EU Urban Agenda-Housing Partnership Guidance Paper on EU Regulation & Public Support for Housing, https://ec.europa.eu/futurium/sites/futurium/files/housing_partnership_-_guidance_paper_on_eu_regulation_and_public_support_for_housing_03-2017.pdf.

[19] European Commission (2020), COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS: A Renovation Wave for Europe - greening our buildings, creating jobs, improving lives, https://ec.europa.eu/energy/sites/ener/files/eu_renovation_wave_strategy.pdf.

[13] Guerra, E. and M. Kirschen (2016), “Housing Plus Transportation Affordability Indices: Uses, Opportunities, and Challenges”, International Transport Forum Discussion Papers, No. 2016/14, OECD Publishing, Paris, https://dx.doi.org/10.1787/a1fc9b79-en.

[18] Janouskova, J. and Š. Sobotovicova (2016), “Immovable property tax in the Czech Republic as an instrument of fiscal decentralization”, Technological and Economic Development of Economy, Vol. 22/6, pp. 767-782, https://doi.org/10.3846/20294913.2016.1236355.

[11] Litman, T. (2016), Transportation Cost and Benefit Analysis (second edition), Victoria Transport Policy Institute.

[8] Ministry of Regional Development (2011), Housing Policy Concept of the Czech Republic Till 2020, State Housing Development Fund, Ministry of Regional Development of the Czech Republic, https://www.bmszki.hu/sites/default/files/fajlok/node-293/housing_policy_concept_till_2020.pdf.

[2] OECD (2020), Affordable Housing Database, OECD, Paris, http://oe.cd/ahd.

[17] OECD (2020), OECD Economic Surveys: Czech Republic 2020, OECD Publishing, Paris, https://doi.org/10.1787/1b180a5a-en (accessed on 29 January 2021).

[10] OECD (2017), The Governance of Land Use in the Czech Republic: The Case of Prague, OECD Publishing, Paris, https://doi.org/10.1787/9789264281936-en.

[1] OECD (forthcoming), Housing Synthesis Report, OECD Publishing, Paris.

[5] OECD/EC (2020), Cities in the World: A New Perspective on Urbanisation, OECD Urban Studies, OECD Publishing, Paris, https://dx.doi.org/10.1787/d0efcbda-en.

[7] Office of the Government (2019), 2019 European Semester: National Reform Programme of the Czech Republic 2019, https://ec.europa.eu/info/sites/info/files/2019-european-semester-national-reform-programme-czech-republic_en.pdf.

[12] Shoup, D. (2005), The High Cost of Free Parking, American Planning Association.

[6] World Bank (2019), Doing Business 2020, World Bank, Washington, DC.