Chapter 8. Fostering market openness

The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law.

Prepare for digital technologies to continue reshaping international trade

-

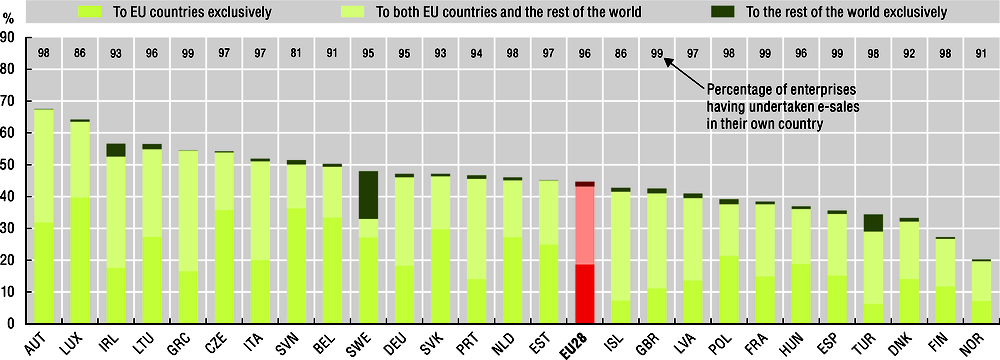

E-commerce is expanding across borders, with 45% of EU firms having undertaken cross-border e-commerce sales in 2016, up from 42% in 2010.

-

Trade restrictions on services that enable digital delivery primarily take the form of measures that affect infrastructure and connectivity (e.g. inefficient regulations on interconnection).

-

As digital technologies affect international trade, market openness policies must be holistic. Multi-stakeholder dialogue to ensure interoperability across regulatory regimes, including for cross-border data flows and related privacy and security considerations, is needed.

Reduce barriers to investment and promote open financial markets

-

Investment regimes that mobilise investment in communications infrastructures, digital technologies and knowledge-based capital (KBC) (e.g. business models, software, data), coupled with open financial markets, drive inclusive growth.

Monitor changing competitive dynamics

-

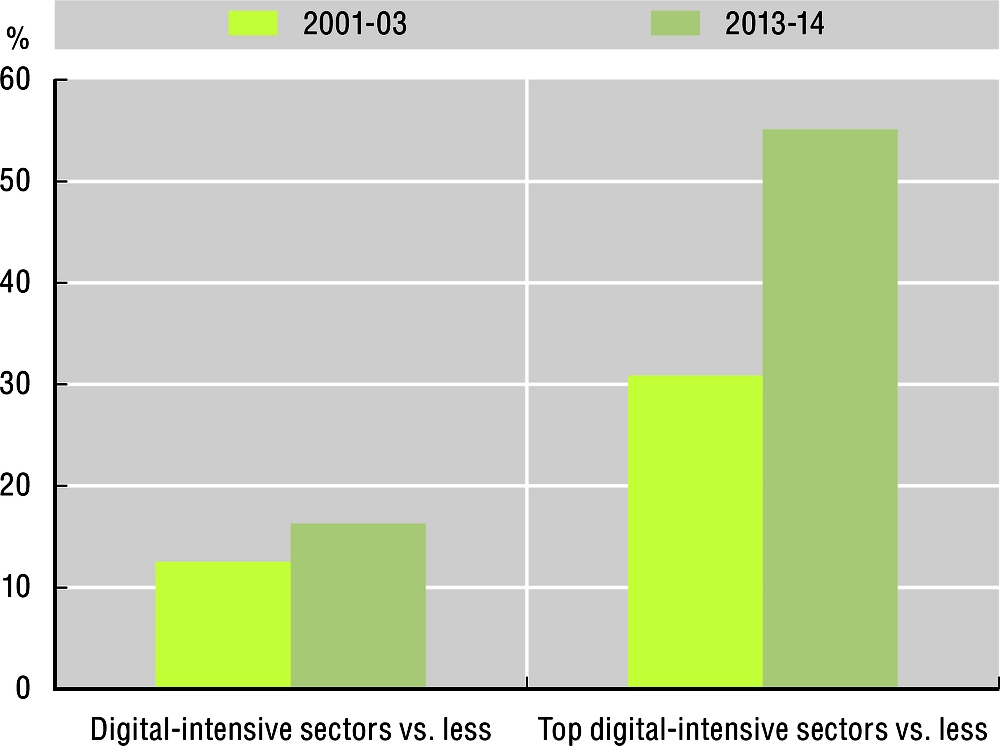

Global acquisitions of digital-intensive firms grew by more than 40% over 2007-15, compared to 20% growth for acquisitions in less digital-intensive sectors. Firms in the most digital-intensive sectors enjoy a 55% higher mark-up than firms operating in less digital-intensive sectors. Competition authorities should consider these and related trends when assessing dominance.

-

Digital technologies and data lead to greater competition in many markets, but can tilt others towards greater concentration, market power and dominance. Competition authorities must be prepared with flexible tools and co-operate across borders to address transnational competition issues.

Address tax challenges arising from the digitalisation of the economy

-

Ensuring that tax systems are fit-for-purpose in the digital age requires continued international co-operation towards a consensus-based, global solution.

Digital technologies are transforming the environment in which firms compete, trade and invest. Market openness enables digitalisation to flourish by creating a business-friendly environment that allows foreign and domestic firms to compete on an equal footing and without excessive restrictions or burdensome conditions (OECD, 2010[1]). Open trade and investment regimes can create new avenues to rapidly upgrade technologies and skills, and increase specialisation, as frontier technologies, applications and processes diffuse through open markets (Andrews, Criscuolo and Gal, 2015[2]). Market openness also fosters competition and helps firms, domestic and foreign, reap the benefits of trade and investment, contributing to economic growth (Romalis, 2007[3]).

Prepare for digital technologies to continue reshaping international trade

Digital technologies and data profoundly impact international trade by reducing trade costs; facilitating the co-ordination of global value chains (GVCs); diffusing ideas and technologies across borders; and connecting greater numbers of businesses and consumers globally, all of which push out the trade frontier. New technologies and an open, non-fragmented Internet ecosystem are potentially creating new opportunities for trade, enabling new value chains with new players and new business models, and spurring innovation.

Innovative business models that use digital technologies and services like digital matching services, logistical support and secure online payment systems are providing solutions that enable firms to sell their products online and in new markets (OECD, forthcoming[4]). For instance, online platforms have lowered barriers to entry for firms to trade, including by allowing smaller firms to pay for and use the platform’s logistics and customer service infrastructure to sell in global markets. Other digital-intensive firms combine their online services with local or offline activities to profitably sell new types of products globally (OECD, forthcoming[4]). This can also affect outsourcing and offshoring dynamics.

As digital transformation has accelerated, the cross-border e-commerce landscape, a key component of digital trade, has become increasingly dynamic. E-commerce transactions are progressively taking place across borders, with 45% of EU firms having undertaken cross-border e-commerce sales in 2016, up from 42% in 2010 (Figure 8.1). But there are differences across countries, which underscores the importance of better understanding the drivers of e-commerce, and digital trade more specifically, in view of boosting growth and consumer welfare.

Notes: StatLink contains more data. See Chapter notes.1

← 1. Figure 8.1: For Iceland, data refer to 2012. For Turkey, data refer to 2014.

Source: OECD (2019[5]), Measuring the Digital Transformation, https://dx.doi.org/10.1787/9789264311992-en, based on Eurostat[6], Digital Economy and Society Statistics (database), https://ec.europa.eu/eurostat/web/digital-economy-and-society/data/comprehensive-database (accessed September 2018).

Digitalisation has allowed trade to take place through digital means entirely, increasing exports of digitally deliverable services, and enabled more traditional trade, especially in more complex manufactures but also in agricultural goods (López González and Ferencz, 2018[7]). Across the OECD, trade in digitally deliverable services represents 23% of total services imports and 28% of total services exports (Figure 8.2).

Notes: StatLink contains more data. See Chapter notes.1

← 1. Figure 8.2: This figure covers the EBOPS items SF: Insurance and pension services; SG: Financial services; SH: Charges for the use of intellectual property not included elsewhere; SI: Telecommunications, computer and information services; and the sub-item SK1 Audiovisual and related services. For Chile, China, Indonesia, Mexico, New Zealand and Switzerland, Audiovisual and related services include Other personal, cultural, and recreational services.

Source: OECD (2019[5]), Measuring the Digital Transformation, https://dx.doi.org/10.1787/9789264311992-en, based on OECD calculations based on OECD, International Trade in Service Statistics (database), http://www.oecd.org/sdd/its/international-trade-in-services-statistics.htm; EBOPS 2010, https://www.oecd.org/sdd/its/EBOPS-2010.pdf; WTO, Trade in Commercial Services (database), https://www.wto.org/english/res_e/statis_e/tradeserv_stat_e.htm (accessed October 2018).

Digital transformation has not only changed how we trade but also what we trade: a larger number of smaller and low-value packages of physical goods, as well as digital services, are now crossing borders; goods are increasingly bundled with services; and new and previously non-tradable services are now being traded across borders. The rise of services in international cross-border trade is closely linked to rapid technological developments. Services that traditionally required close proximity to customers now can be traded at a distance, allowing firms to reach global markets at lower costs.

Yet services regulations remain fragmented by borders, and regulatory frictions create trade costs for services providers, particularly for small and medium-sized enterprises (SMEs). As a result, the benefits of digital technologies may be diminished by existing and emerging trade barriers that hold back innovation and create obstacles to the movement of services that enable digital delivery across borders.

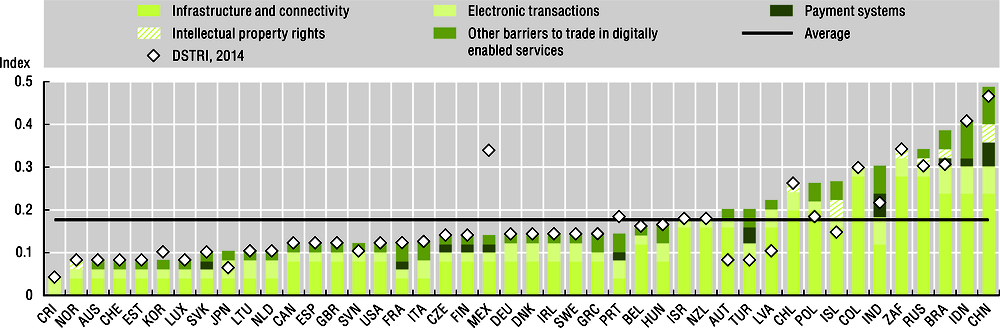

Recent data suggest that trade restrictions on services that enable digital delivery are primarily due to measures that affect infrastructure and connectivity (e.g. inefficient regulations on interconnection and restrictions on cross-border data flows beyond those imposed to ensure the protection and security of personal data) (Figure 8.3). Other measures restricting trade in such services include restrictions on electronic transactions (e.g. discriminatory measures affecting licenses for e-commerce) and payment systems (restrictions on electronic signatures), among others.

Notes: The Digital Services Trade Restrictiveness indices take values between zero and one, with one being the most restrictive. StatLink contains more data. See Chapter notes.1

← 1. Figure 8.3: The STRI indices are calculated on the basis of the STRI regulatory database which records measures on a most-favoured-nation basis. Preferential trade agreements are not taken into account.

Source: OECD (2019[5]), Measuring the Digital Transformation, https://dx.doi.org/10.1787/9789264311992-en, based on OECD, STRI (database), http://oe.cd/stri-db (accessed December 2018).

Digital trade transactions, be they in relation to goods or services, have been part of the landscape for many years and often raise the same, or similar, issues as non-digital transactions. This is because digital trade is not just about digitally deliverable services, but also about more traditional – including supply-chain – trade enabled by growing digital connectivity. What is new in digital trade is the scale of transactions and the emergence of new (and disruptive) players transforming production processes and industries, including many that were previously little affected by globalisation.

While all digital trade is enabled digitally, not all digital trade is digitally delivered. Digital trade also involves digitally enabled but physically delivered goods and services (such as a purchase of a good on an online marketplace or the booking of a hotel through a matching service).

While there is no single recognised and accepted definition of digital trade, there is a growing consensus that it encompasses digitally enabled transactions in trade in goods and services, whether digitally or physically delivered. This characterisation, drawing on the OECD’s (OECD, 2011[8]) and the World Trade Organization’s (WTO, 1998[9]) definition of an e-commerce transaction, lends itself to decomposing the digital trading environment into a number of distinct categories of transactions each of which raises different questions for trade and investment policy as well as for measurement.

Source: López González and Ferencz (2018[7]), “Digital trade and market openness”, https://doi.org/10.1787/1bd89c9a-en.

While digital trade was introduced into the World Trade Organization (WTO) as early as 1998 through the work programme on e-commerce (WTO, 1998[9]), progress has been slow apart from a temporary moratorium on imposing customs duties on electronic transmissions. At the 11th Ministerial Conference in Buenos Aires in 2017, WTO members agreed to “maintain the current practice of not imposing customs duties on electronic transmissions” until the next ministerial (WTO, 2017[10]). A group of 71 members further agreed to “initiate exploratory work together towards future WTO negotiations on trade-related aspects of electronic commerce” (WTO, 2017[11]).

Existing multilateral trade rules were negotiated when digital trade was in its infancy and, even if conceived to be technologically neutral, questions have arisen as to whether they might require clarifications to reflect new forms of, and issues raised by, digital trade. For example, trade rules are traditionally predicated on identifying whether products are goods or services and the borders they cross, but new business models and the global nature of the Internet blur these distinctions. Firms can flexibly service markets from different locations and the products they sell bundle goods with services (such as a fitbit or a smart speaker). This makes it increasingly difficult to identify the particular trade rules that apply to specific transactions (López González and Ferencz, 2018[7]).

Market openness therefore needs to be approached more holistically. For example, Internet access may be a necessary but not sufficient condition for digitally enabled trade in goods to flourish. If logistics services in the receiving (or delivering) country are costly due to service trade restrictions increasing prices, or if goods are held up at the border by cumbersome procedures, then the benefits of digital transformation may not materialise. Platform-enabled trade transactions might be curtailed or might not take place at all.

The nature of the measures that affect how modern firms engage in digital trade is changing – some relate to accessing and using digital networks or supporting digital services; others are old trade issues with new consequences; and some are new measures which raise new issues. For instance, digital trade can change or amplify the importance of “old” issues. Trade in low-value goods ordered online is still subject to traditional physical connectivity constraints. However, since trade costs can represent a sizeable share of the value of small consignments, how fast and at what cost a physical good can clear customs is especially important. At the same time, growing trade in digitally ordered parcels poses new challenges for customs authorities and other border agencies, from workload to adapting clearance and risk management processes, to revenue issues related to tariffs or the collection of value-added tax.

Cross-border data flows support trade transactions. They underpin trade by enabling control and co-ordination along GVCs, or by enabling implementation of trade facilitation measures. Reaping the benefits of digital trade requires multi-stakeholder dialogue on regulatory approaches that ensure the interoperability of differing regulatory regimes, particularly for transversal issues such as cross-border data flows (see Chapter 7). On the one hand, emerging measures impacting cross-border data flows raise concerns for business activity and the ability to benefit from digital trade; on the other hand, important public policy objectives, such as the protection of privacy, security and intellectual property rights, must be taken into account. The challenge is to address public policy objectives in a manner that is not arbitrary or discriminatory so as to preserve the significant economic and trade benefits flowing from data-enabled trade. To support this dialogue one important step will be to better understand the nature and composition of data flows which are highly heterogeneous, as well as the scope of the public policy objectives being pursued.

Trade agreements – multilateral, plurilateral and bilateral – offer some useful insights into managing exchanges across countries with different standards, reflecting different cultural and political contexts. In trade agreements, and as reflected in market openness principles, combining the benefits of trade with countries’ right to regulate has rested on principles that: 1) standards are transparent; 2) these standards are applied to everyone in the same way (i.e. that they are non-discriminatory); and 3) in achieving their legitimate public policy objectives, countries do not use measures that restrict trade more than is necessary to achieve the objective.

Reduce barriers to investment and promote open financial markets

Investment regimes that mobilise private investment in communications infrastructures, technologies and KBC (e.g. business models, software, data), coupled with open financial markets, attract foreign direct investment (FDI) and underpin digital transformation as a driver of inclusive growth. They also help channel resources to more productive uses and, through competitive pressure and the discipline imposed by shareholders and creditors, ensure that all firms strive to improve their efficiency and allow inefficient firms to exit (OECD, 2015[12]).

Reducing barriers to international investment is thus important to supporting the broader digital transformation. The OECD FDI Regulatory Restrictiveness Index (RRI) measures statutory barriers to foreign investment in a range of countries. While it focuses on regulatory barriers to FDI on the books, and not at how rules are implemented, it provides a useful – albeit partial – indication of how global policy trends are affecting foreign investment (Thomsen and Mistura, 2017[13]). Over time and across countries, policies have tended to move towards greater openness for foreign investors (Thomsen and Mistura, 2017[13]).

Overall, FDI restrictiveness still varies greatly across countries and regions (Figure 8.4). Both OECD and non-OECD countries in the Asia-Pacific region tend to have higher FDI RRI scores, with a greater propensity to screen inward investment and more frequent use of foreign equity limits at a sectoral level. EU countries show relatively fewer restrictions and large countries – with their big domestic markets – can afford to impose more and broader restrictions than smaller countries. Across the OECD, the communications component of the RRI is higher (more restrictive) than the average RRI score.

Notes: The FDI RRI take values between zero and one, with one being the most restrictive. StatLink contains more data. See Chapter notes.1

← 1. Figure 8.4: The FDI RRI measures statutory restrictions on FDI in 68 countries, including all OECD and G20 countries, and covers 22 sectors. Four types of measures are covered: (i) foreign equity restrictions, (ii) screening and prior approval requirements, (iii) rules for key personnel and (iv) other restrictions on the operation of foreign enterprises. The score for each sector is obtained by adding the scores for all four types of measures, and re-scaling this to a maximum value of 1. The 22 sector scores are then averaged to yield the overall score for each country. The main source of information is the list of countries’ reservations under the OECD Code of Liberalisation of Capital Movements and their lists of exceptions and other measures reported for transparency under the National Treatment instrument (NTI). Additional sources include official national publications and information gathered by the Secretariat in the preparation of OECD Investment Policy Reviews, as well as by other international organisations.

Source: OECD (2019[5]), Measuring the Digital Transformation, https://dx.doi.org/10.1787/9789264311992-en, based on OECD, FDI Regulatory Restrictiveness Index (database), http://www.oecd.org/investment/fdiindex.htm (accessed December 2018).

In addition, multinational enterprises – which by definition operate across borders – can make extensive use of digital technologies and data to organise their business operations and improve processes and procedures (see Chapter 3). Use of such technologies also promotes market-based international technology transfer, although knowledge-related spillovers from FDI vary across sectors, with services sectors enjoying the strongest productivity-enhancing effects of FDI (Lesher and Miroudot, 2008[14]).

Intensive use of digital technologies and data may also impact a firm’s decision of whether to export or establish a local presence insofar that exporting may become more attractive if products are relatively easily delivered digitally (UNCTAD, 2017[15]). Moreover, as digital technologies have helped support the spread of GVCs (De Backer and Flaig, 2017[16]), the infrastructures and services needed to support GVCs may become a new variable in a firm’s decision of whether and where to invest (Gestrin and Staudt, 2018[17]).

Investment regimes also need to facilitate investment in KBC – such as business models, software, data, intellectual property, economic competences (e.g. firm-specific skills such as management, brand management, new organisational processes and structures) and skills (see Chapters 3 and 4). Such investment is now larger than investment in machinery and equipment in many OECD countries (OECD, 2017[18]). Business investment in KBC not only helps boost both growth and productivity (OECD, 2013[19]), but it also supports the broader digital transformation by promoting market innovation.

Open financial markets facilitate investment

Efficient, stable and open financial markets, based on high levels of transparency, confidence and integrity, help allocate financial resources to firms investing in digital transformation. Open financial markets also ensure that domestic financial services firms remain competitive in the face of foreign competition. Increased competition should make domestic firms more efficient and transparent. Financial flows can lower the cost of capital for firms in countries in which capital is scarce, which in turn can raise investment in digital technologies and data.

Regulatory frameworks that are sector-based (e.g. bank-focused) can present barriers for more targeted services (e.g. payments) to enter the market. Regulators and supervisors need to build capacity to align to the objective of promoting safe and beneficial digitalisation of financial services. In this respect, inter-sectoral and international regulatory co-operation is needed for consistent regulation and information sharing.

Digital technologies also underpin new forms of external funding, the most prominent of which is crowdfunding, whereby external finance is raised through online platforms from a relatively larger pool investors. Although it still represents a minor share of all business financing (and serves to finance specific projects rather than enterprises as a whole), crowdfunding may play a growing role, including for the financing of innovative ventures, as online interactions with large numbers of customers may help entrepreneurs to validate untested products. In addition, venture capital investors, business angels and institutional investors are increasingly finding investment opportunities through crowdfunding platforms, usually through the largest and more developed platforms (see Chapter 4) (OECD, 2017[20]).

Monitor changing competitive dynamics

Strengthening competition, including by opening access to markets, benefits consumers through lower prices and a greater variety of goods and services, and supports trade and investment. Competitive markets also underpin digital transformation by spurring innovation, new business models, business dynamism and productivity, driving structural change across the economy.

Digital transformation promotes greater competition in a large variety of product and service markets, both domestically and internationally. In the digital age, geographic market boundaries matter less because the Internet has facilitated the entry and growth of digitally based suppliers and retailers (e.g. Amazon, Rakuten, Alibaba) that do not need to have a physical presence in all markets in which they sell, which has helped increase competition and expand GVCs. In turn, digitally enabled business models have increased competitive pressure on offline incumbents.

Digital technologies enable new types of products and services to compete with existing ones (e.g. services that stream television content over the Internet versus cable and satellite TV providers, online-only publications versus traditional print media, etc). In some cases, these new products and services have greatly reduced prices (e.g. financial and brokerage services) and improved services (e.g. movie rentals). Occasionally, digital technologies and data have helped to make possible new products and services that disrupt well-established markets (e.g. film cameras replaced by digital cameras, digital cameras supplanted by smartphones, compact discs superseded by digital downloads and streaming).

But even as digital technologies and data lead to greater competition in many markets, they have also demonstrated a potential to tilt others towards greater concentration, market power and even dominance. For instance, in online platform markets, network effects and the possibility to achieve “scale without mass” can drive winner-take-all or winner-take-most outcomes. While network effects – the phenomenon that some products, such as the telephone, become more useful as the number of users increases – are widely understood, scale without mass refers to a feature of many digital markets that allows companies to add new users at virtually no cost (see Chapter 1).

Mark-ups – the wedge between the price a firm charges for its output on the market and the cost the firm incurs to produce one extra unit of output – are one indication of the level of competition in a particular market. Mark-ups have been increasing on average across firms and countries, especially for firms at the top of the mark-up distribution and those in digital-intensive sectors (Figure 8.5). On average, firms in the most digital-intensive sectors enjoy a 55% higher mark-up than firms operating in less digital-intensive sectors all else equal (elaboration based on Calligaris, Criscuolo and Marcolin, 2018[21]). This gap is persistent, even after controlling for productivity and firm patent stock.

Note: See Chapter notes.1

← 1. Figure 8.5: The figure reports the estimates of a pooled OLS regression explaining firm log-mark-ups in the period, on the basis of the firm’s capital intensity, age, productivity and country-year of operation, as well as a dummy variable with value 1 if the sector of operation is digital-intensive vs less digital-intensive (specifications on the left in the graph), or if the sector of operation is among the top 25% of digital-intensive sectors vs not (specifications on the right in the graph). Sectors are classified as “digital-intensive” or “highly digital-intensive” according to the taxonomy developed in Calvino et al. (2018[27]). Estimates using mark-ups based on a Cobb Douglas production function. With respect to Calligaris et al. (2018[21]), in this elaboration the parameters of the production function have been estimated at the 3-digit industry level (rather than 2-digit), and including year dummies. Moreover, mark-ups lower than 1 but greater than 0.95 have been winsorized (rather than trimmed) to 1. Standard errors are clustered at the company level. All coefficients are significant at the 1% confidence level.

Source: Elaboration based on Calligaris S., C. Criscuolo and L. Marcolin (2018[21]), “Mark-ups in the digital era”, https://doi.org/10.1787/4efe2d25-en, based on Orbis® data (accessed July 2018).

Industry concentration – while imperfect – can serve as a proxy to help understand the degree of competition in a given sector or market, as well as changes in the structure of industries. Mergers and acquisitions are associated with increases in industry concentration. Over 2003-15, the number of global mergers and acquisitions doubled, with a strong increase in cross-border mergers and acquisitions of firms in digital-intensive sectors (Bajgar et al., forthcoming[22]). The number of cross-border acquisitions of digital-intensive firms grew by more than 40% over 2007-15, compared to 20% growth of acquisitions of less digital-intensive firms (Bajgar et al., forthcoming[22]). These developments may not necessarily be a source of concern, as they may be inherent to the nature of digital transformation, but they should be further examined and considered by policy makers.

Ensuring a competitive environment for both domestic and cross-border transactions is essential. In the cross-border context, regulatory restrictions on products can be assessed for being excessive or insufficient compared to restrictions on domestically supplied products (OECD, 2018[23]). Such an assessment may consider whether national standards are followed by products sold across borders and ensure that illegal products are not made available (OECD, 2018[23]). Competition in the cross-border context includes single firms seeking to sell products across a border and limits on rivalry by a dominant firm or cartels.

The absence of regulation may also discourage digital innovation. Truly new and innovative business models may emerge in between traditional sector delineations, or transform the relationships among different actors. In the absence of adequate regulation, outlining basic minimum requirements for such business models may discourage investors as well as first-to-market innovators. Similarly, a common understanding of the rights and responsibilities of parties to a transaction might be beneficial for transactions taking place between “peers” in the platform economy (OECD, 2016[24]). “Free” transactions, whereby consumers receive goods and services in exchange for use of their personal data (including for advertising purposes and to provide customised content), may be considered less reliable in the absence of suitable redress mechanisms for those who may encounter a problem with such transactions (OECD, 2016[24]). In cases like these, the absence of some kinds of horizontal regulations, including consumer safety and consumer protection, could restrict the emergence of innovative products or business models.

As digital transformation continues to affect competition, it may lead to some new challenges for competition policy frameworks that were designed with traditional products in mind. One such challenge is that digitalisation may introduce new dimensions of competition in markets, as well as new ways to achieve anticompetitive outcomes, such as the use of algorithms to collude. In addition, a range of issues will require competition authorities to enhance their advocacy efforts and deepen their co-operation with consumer protection, data protection and other regulators. These include the use of consumer data under the relevant data protection safeguards as a competitive asset when providing products at no cost, or when developing personalised prices.

Co-operation may be needed across borders to ensure that common standards are applied and that information is available to regulators. Bilateral and regional enforcement may also be useful, for example joint decision making between jurisdictions, although it is important that clear rules exist to indicate how enforcement actions are to be addressed if there are bodies with overlapping responsibilities.

Address tax challenges arising from the digitalisation of the economy

The taxation system is an important factor firms consider when deciding whether to invest domestically or abroad, and can distort competition and resource allocation if cross-border firms have a competitive advantage over domestic firms through international tax planning. Digital transformation has a wide range of implications for taxation, impacting tax policy and tax administration at both the domestic and international levels, offering new tools and introducing new challenges for policy makers. As a result, the digitalisation of the economy has been at the centre of the recent global debate over whether current international tax rules continue to be “fit-for-purpose” in an increasingly global business environment.

Under the auspices of the OECD/G20 Base Erosion and Profit Shifting (BEPS) Project and the Inclusive Framework on BEPS, work has been undertaken that recognises that digitalisation and some of the business models that it facilitates present important challenges for international taxation (OECD, 2015[25]). This analysis acknowledges that it would be difficult, if not impossible, to “ring-fence” the digital economy from the rest of the economy for tax purposes because of the increasingly pervasive nature of digitalisation.

This work has also identified a number of key features of digitalisation that are potentially relevant from a tax perspective. There was recognition that digitalisation has also accelerated and changed the spread of GVCs in which multinational enterprises integrate their worldwide operations. More specifically, new phenomena such as the collection and exploitation of data, network effects and the emergence of new business models, such as multi-sided platforms, were identified as presenting additional challenges to the existing tax rules (OECD, 2018[26]).

Building on the 2015 Action 1 Report, an Interim Report on the Tax Challenges Arising from Digitalisation was delivered to the G20 Finance Ministers in March 2018. The interim report presents an in-depth analysis of value creation across different digitalised business models, and describes the main characteristics of digital markets (OECD, 2018[26]). These have significantly evolved, especially for some enterprises. In particular, it identified three characteristics that are frequently observed in certain highly digitalised business models: 1) scale without mass; 2) reliance on intangible assets; and 3) reliance on data and user contributions. Further, it was acknowledged that these characteristics are expected to become common features of an even greater number of businesses as digitalisation progresses.

The interim report highlighted the importance of considering the implications of these three characteristics for the international tax system. They raise important issues concerning the rules relating to the allocation of taxing rights between jurisdictions (the “nexus” rules) and on the determination of the relevant share of a multinational enterprise’s profits that will be subject to tax in a given jurisdiction (the “profit allocation” rules). There is a question whether the existing nexus rules, which govern the extent of a jurisdiction’s right to tax a non-resident enterprise, may be outdated as an enterprise can now be heavily involved in the economic life of a jurisdiction but with a presence that, under existing tax rules, attracts only minimal or no taxing rights for that jurisdiction.

The rules relating to “profit allocation” are based on the “arm’s-length” principle, described in the OECD Transfer Pricing Guidelines, and focus on the functions performed, assets used and risks assumed by each entity. There is a question of whether, and the extent to which, the existing profit allocation rules continue to produce appropriate results, including in cases where some or all of the three characteristics mentioned are present.

While work on a global, consensus-based solution is underway, a number of jurisdictions are considering the introduction of interim measures. In the Inclusive Framework on BEPS, there is no consensus on either the merit or need for interim measures and the interim report does not make a recommendation for their introduction. A number of countries consider that an interim measure will give rise to risks and adverse consequences irrespective of any limits that may be imposed on the design of such a measure and, therefore, oppose such a measure.

Other countries acknowledge these challenges, but consider that they do not outweigh the need to ensure that tax is paid in their jurisdictions on certain digital services supplied in their jurisdictions and consider that at least some of the possible adverse consequences can be mitigated through the design of the measure. This latter group of countries is of the view that a proliferation of different types of interim measures would be undesirable and, therefore, the interim report sets out guidance agreed by those countries on the design considerations that need to be taken into account when considering the introduction of interim measures.

Ensuring that tax systems are ready to meet the changes brought about by the increasingly global business models enabled by digitalisation, as well as to leverage opportunities and provide protection from potential risks, is a critical challenge. The impact of digitalisation on the international tax system will be a significant component of this work, and has important ramifications for multinational enterprises and governments, as well as the future of tax systems. Members of the Inclusive Framework on BEPS have agreed to undertake a coherent and concurrent review of the two key aspects of the existing tax framework – the profit allocation and nexus rules – that would consider the impacts of digitalisation on the economy, relating to the principle of aligning profits with underlying economic activities and value creation.

Since publication of the interim report in March 2018, the more than 120 members of the Inclusive Framework on BEPS have made significant progress to bridge the gaps in their positions with a number of countries bringing forward new proposals. By the end of 2018, the dynamic of the discussions shifted, with a renewed impetus for a potential agreement. The challenge now is to identify how the various proposals intersect – finding a solution that incorporates elements of these proposals could have a mutually reinforcing effect. The Inclusive Framework will meet again in 2019 to take these proposals forward, and a strong showing of unity and commitment to work together at the highest political level will be a key ingredient in finding common ground. It is hoped that there could be agreement on the sense of direction by then so that technical work on agreed solutions could be delivered by the end of 2020.

References

Andrews, D., C. Criscuolo and P. Gal (2015), “Frontier firms, technology diffusion and public policy: Micro evidence from OECD countries”, OECD Productivity Working Papers, No. 2, OECD Publishing, Paris, https://dx.doi.org/10.1787/5jrql2q2jj7b-en. [2]

Bajgar, M. et al. (forthcoming), “Acquiring innovation in the digital economy”, OECD Productivity Working Paper, OECD Publishing, Paris. [22]

Calligaris, S., C. Criscuolo and L. Marcolin (2018), “Mark-ups in the digital era”, OECD Science, Technology and Industry Working Papers, No. 2018/10, OECD Publishing, Paris, https://dx.doi.org/10.1787/4efe2d25-en. [21]

Calvino, F. et al. (2018), “A taxonomy of digital intensive sectors”, OECD Science, Technology and Industry Working Papers, No. 2018/14, OECD Publishing, Paris, https://dx.doi.org/10.1787/f404736a-en. [27]

De Backer, K. and D. Flaig (2017), “The future of global value chains: Business as usual or ‘a new normal’?”, OECD Science, Technology and Industry Policy Papers, No. 41, OECD Publishing, Paris, https://dx.doi.org/10.1787/d8da8760-en. [16]

Eurostat (2018), Digital Economy and Society Statistics (database), https://ec.europa.eu/eurostat/web/digital-economy-and-society/data/comprehensive-database (accessed December 2018). [6]

Gestrin, M. and J. Staudt (2018), The Digital Economy, Multinational Enterprises and International Investment Policy, OECD, Paris, http://www.oecd.org/investment/the-digital-economy-mnes-and-international-investment-policy.htm. [17]

Lesher, M. and S. Miroudot (2008), “FDI spillovers and their interrelationships with trade”, OECD Trade Policy Papers, No. 80, OECD Publishing, Paris, https://dx.doi.org/10.1787/235843308250. [14]

López González, J. and J. Ferencz (2018), “Digital trade and market openness”, OECD Trade Policy Papers, No. 217, OECD Publishing, Paris, https://dx.doi.org/10.1787/1bd89c9a-en. [7]

OECD (2019), Measuring the Digital Transformation: A Roadmap for the Future, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264311992-en. [5]

OECD (2018), Maintaining Competitive Conditions in Era of Digitalisation, OECD, Paris, http://www.oecd.org/g20/Maintaining-competitive-conditions-in-era-of-digitalisation-OECD.pdf. [23]

OECD (2018), Tax Challenges Arising from Digitalisation – Interim Report 2018: Inclusive Framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264293083-en. [26]

OECD (2017), Financing SMEs and Entrepreneurs 2017: An OECD Scoreboard, OECD Publishing, Paris, https://dx.doi.org/10.1787/fin_sme_ent-2017-en. [20]

OECD (2017), OECD Science, Technology and Industry Scoreboard 2017: The Digital Transformation, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264268821-en. [18]

OECD (2016), OECD Recommendation of the Council on Consumer Protection in E-Commerce, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264255258-en. [24]

OECD (2015), Addressing the Tax Challenges of the Digital Economy, Action 1 – 2015 Final Report, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264241046-en. [25]

OECD (2015), Policy Framework for Investment, 2015 Edition, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264208667-en. [12]

OECD (2013), Supporting Investment in Knowledge Capital, Growth and Innovation, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264193307-en. [19]

OECD (2011), OECD Guide to Measuring the Information Society 2011, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264113541-en. [8]

OECD (2010), OECD Market Openness Principles, OECD Innovation Policy Platform, OECD, Paris, http://www.oecd.org/innovation/policyplatform/48137680.pdf. [1]

OECD (forthcoming), A Dynamic E-commerce Landscape: Developments, Trends and Business Models, OECD Publishing, Paris. [4]

Romalis, J. (2007), “Market access, openness and growth”, NBER Working Paper No. w13048, https://doi.org/10.3386/w13048. [3]

Thomsen, S. and F. Mistura (2017), Is Investment Protectionism on the Rise?, OECD, Paris, http://www.oecd.org/investment/globalforum/2017-GFII-Background-Note-Is-investment-protectionism-on-the-rise.pdf. [13]

UNCTAD (2017), World Investment Report 2017: Investment and the Digital Economy, United Nations Conference on Trade and Development, Geneva, http://unctad.org/en/PublicationsLibrary/wir2017_en.pdf. [15]

WTO (2017), Joint Statement on Electronic Commerce, World Trade Organization, Geneva. [11]

WTO (2017), Work Programme on Electronic Commerce: Draft Ministerial Decision of 13 December, World Trade Organization, Geneva. [10]

WTO (1998), Work Programme on Electronic Commerce, World Trade Organization, Geneva, https://www.wto.org/english/tratop_e/ecom_e/wkprog_e.htm. [9]