1. Designing Policies for Efficient, Inclusive and Sustainable Housing

Housing has become an increasingly pressing economic, social and environmental challenge in OECD countries. Rising house prices and rents have undermined affordability and resulted in social exclusion. This chapter documents these trends and discusses their main drivers by pulling together key findings from the OECD Horizontal Project on Housing. It shows that inefficiencies in housing markets can have adverse consequences for the economy at large, including macroeconomic instability and impaired labour mobility. Cost pressures also exacerbate the challenge of upgrading the housing stock to comply with environmental objectives. The chapter concludes by reviewing the evidence on policy instruments that can improve housing outcomes and describing the policy indicators used to assess progress and gauge the scope for further policy action. An online dashboard and country snapshots provide easy ways to compare indicators of outcomes and policy settings across countries. The conclusion summarises synergies and trade-offs of different policy interventions with respect to the objectives of housing inclusiveness, efficiency and sustainability.

Households in many OECD countries have found it increasingly difficult to access quality, affordable housing. House prices have typically risen faster than average incomes, and households have borrowed more and more to buy their home, so that the burden of mortgage servicing has become heavier for many households despite lower interest rates. Rents have often gone up faster than inflation. Housing costs overall have been on a steep rising trend. Affordability has been particularly challenging for households on low incomes or those that have faced adverse income shocks or job losses, notably as a result of the COVID-19 pandemic. Increasing awareness of the negative externalities arising from commuting by private automobiles has further put a strain on the capacity of housing markets to deliver affordable housing while reducing environmental and health costs for current and future generations. Housing markets and policies also affect overall economic performance and living standards as they can influence if and when households move, how they use their savings and how they accumulate wealth.

The COVID-19 crisis is exacerbating many of these challenges (see Box 1.1). They will have to be addressed at the same time as an unprecedented effort is required to renew and upgrade the housing stock to improve energy efficiency and facilitate the transition to a low-carbon economy. Indeed, the reallocation of resources that will be needed to underpin the recovery post-COVID-19 provides an opportunity to accelerate this transition.

Buildings, structures and dwellings have a long life span, lasting for about a whole generation. As a result, policies that shape housing demand and supply need to be forward-looking and anticipate changes in the population’s needs, preferences and behaviours, as well as “megatrends” that affect economies and societies. To the extent possible, policies and regulations also need to foresee and respond to technological changes that affect the construction, use and maintenance of structures. The COVID-19 crisis, along with digitalisation, climate change and population ageing, will most likely have long-lasting, yet uncertain, effects on housing demand and supply, including both the residential and commercial market segments.

COVID-19

The COVID-19 crisis may trigger changes in preferences and behaviour that are likely to influence housing demand over the longer term. For example, if teleworking becomes more prevalent, housing demand may shift durably away from city centres towards rural and peri-urban areas, and away from apartments to single-family accommodation. Such a change would impinge on the need for some urban amenities, transport infrastructure and social services. An associated relief on property prices in urban centres would likely be accompanied by pressure elsewhere with an uncertain net effect on affordability, unless supply adjusts in tandem. Teleworking will also have a bearing on the demand for office space, putting downward pressure on commercial property prices in central business districts. If the fear of infectious diseases lingers, there could also be an increase in demand for larger offices to allow for effective physical distancing, which could somewhat offset the downward trend in demand due to teleworking.

Where these shifting demand patterns lead to a hollowing-out of city centres, there will be increased risk of urban decay and a loss of dynamism in areas where productivity tends to be highest. Alternatively, changing attitudes and work practices may create new opportunities for social and economic transformation in metropolitan areas that have become increasingly polycentric.1 At the same time, as density gives way to sprawl, the environmental footprint of cities will need to be reassessed, with implications for policy aimed to improve the environmental sustainability of the world’s metropolitan areas.

Digitalisation

Digitalisation, beyond its effect through teleworking, affects the housing outlook in several ways and has considerable further transformative potential. For example, the expansion of short-time accommodation digital platforms has put pressure on rental markets in many cities worldwide, a trend that may well continue when the tourism and hospitality industries recover from the COVID-19 crisis. On the other hand, the decline in short-term rentals (such as Airbnb) during the COVID-19 crisis could be long-lasting and free up rental housing for residents and hence support affordability.

Digitalisation is also re-shaping the “high street” with attendant changes in commercial property demand as in-person shopping is replaced by on-line retail trade. This phenomenon adds to the downward pressure on office space demand in central business districts associated with more widespread teleworking. Where regulations allow it, flexibility to convert commercial property for residential use will facilitate the reallocation of housing capital to evolving demand for different uses, potentially making housing more affordable. However, there could be a risk of disaffection for city centres giving rise to housing segregation as the better-off moves away with effects on the provisions of public services. These trends would pose challenges for urban planning and the design of land-use and zoning regulations.

Moreover, digitalisation offers several options for technological change and innovation in construction and “smart” management of buildings, not least through artificial intelligence and the internet of things. Innovations in urban planning and management are already taking place and can improve traffic management, urban amenities and infrastructure, and energy efficiency of buildings and cities at large. These developments can make cities more attractive and counter the centripetal forces associated with digitalisation and COVID-related behavioural changes.

Yet another aspect of digitalisation is the scope for expanding fintech to offer a broader range of finance for investment in real estate. To the extent that these activities are regulated appropriately and financial stability is safeguarded, the entry of new participants in real estate markets can enhance competition, reduce borrowing costs and facilitating access to finance for those that currently struggle to do so. Investment in the energy efficiency of buildings can lower housing costs further as it reduces household spending on energy and improves their creditworthiness. Ultimately, more flexible housing finance could facilitate the adjustment of supply to changes in the demand for both residential and commercial property after the crisis, facilitating housing capital reallocation.

Digitalisation could also improve the matching of supply and demand for dwellings. The rise of digital showings of properties during the COVID-19 crisis is likely to remain at least in part permanent, allowing for a better filtering of costly physical visits and ultimately more and better matches.

Population ageing and climate change

Housing will also be shaped by trends related to pre-crisis population ageing and climate change. Changes in demographics have highly asymmetric effects on housing markets, with falling demand in remote areas that puts downward pressure on prices, at the same time as changing needs and preferences elsewhere that require the retrofitting of buildings, a reconfiguration of living spaces and investment in adapted urban infrastructure. The implications of population ageing for policy go beyond housing and include urban planning and regional development considerations.

Climate change raises the risk of natural disasters and capital depletion in coastal areas exposed to rising sea levels, just to cite a few. It influences construction patterns and the use of materials in buildings, as well as calling for innovation to improve energy efficiency in response to changing weather conditions. It also has a bearing on the design, maintenance and upgrade of urban infrastructure. The attendant economic (private and public) costs need to be taken into account and pose challenges for urban planning and regional development, as well as disaster risk management and insurance.

Flexible land-use policies as facilitators

Flexible land-use policies are key to accommodate the above described permanent changes in real estate demand that may stem from the COVID 19 crisis without entailing unnecessary costs. Flexible settings indeed reduce the risk that structural demand shifts, such as greater appetite for larger, more peripheral homes, trigger price spikes and speculative bubbles that could, in turn, entrench restrictive land-use regulations. Flexible settings can also provide the required fluidity in converting real estate between commercial, office and residential uses for areas to adapt to changes in preferences so that buildings that become vacant are quickly repurposed rather than risking to become abandoned with negative spillovers. In particular, flexible settings would facilitate the conversion of retail and office space into dwellings, contributing to ease the housing crisis.

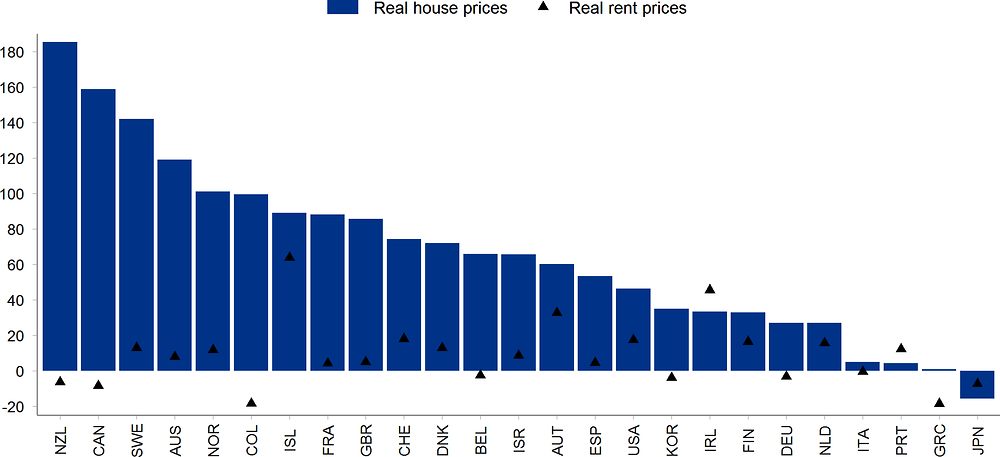

Housing costs have risen faster than other consumption expenditures

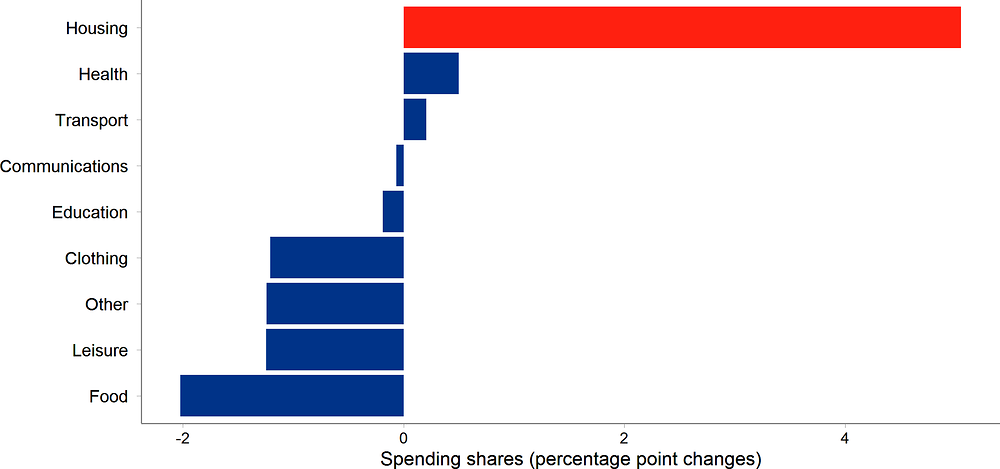

Access to high-quality housing has become increasingly difficult in many OECD countries over the past decades. House prices and rents have risen faster than general inflation across OECD countries undermining housing affordability (Figure 1.1). The reduction in real interest rates has only partly buffeted the impact of higher house prices. The increase in real housing costs has been particularly sharp in urban areas, where the housing stock and undeveloped land is in short supply. In fact, between 2005 and 2015 alone, the share of middle-income households’ (i.e. households earning between 75% and 200% of median incomes) income spent on housing rose by as much as five percentage points on average in OECD countries (Figure 1.2).

Source: OECD Analytical House Price Database.

Note: Unweighted average of 23 OECD countries (Austria, Belgium, Chile, Czech Republic, Germany, Finland, Greece, Hungary, Ireland, Lithuania, Luxembourg, Latvia, Mexico, Netherlands, Norway, Poland, Portugal, Slovak Republic, Slovenia, Spain, Turkey, United Kingdom and United States). Data refers to middle-income households (75% to 200% of median earnings).

Source: Under Pressure: The Squeezed Middle Class (OECD, 2019[1]).

Rising housing costs put a disproportionate burden on low-income households

Whereas households throughout the income distribution face rising housing costs, the less affluent ones typically spend a higher share of their income on housing (Figure 1.3). The provision of social housing and housing-related benefits can help alleviate the pressure on the most affected social groups. Still, they need to be well designed to ensure that scarce resources reach those in need without hindering their mobility or resulting in residential segregation (OECD, 2020). The COVID-19 crisis, which has created large employment and income losses that are concentrated on the most vulnerable groups,2 exacerbates the difficulties in ensuring access to quality, affordable housing.

Note: In Chile, Mexico, Korea and the United States gross income instead of disposable income is used due to data limitations. No data on mortgage principal repayments are available for Denmark due to data limitations. Income quintiles for Canada are based on adjusted after-tax household income.

Source: OECD Affordable Housing Database (http://www.oecd.org/housing/data/affordable-housing-database/housing-conditions.htm), indicators HC1.2.

Supply has not kept up with demand

There are many reasons why housing costs have increased over the past two decades. Key housing market outcomes, such as house prices and construction, result from the interplay of demand and supply. On the demand side, economic expansion has contributed to household income growth. Demographic developments, such as population ageing and migration are key drivers of the level of demand as more people are looking for homes. At the same time, changes in household structure towards smaller households have not been accompanied by similar changes in the type of housing demanded, since people tend to live in bigger homes as documented by an increase in the average floor area per person in the past decade (IEA, 2020). Mortgage credit became more available and more affordable following financial deregulation during the period of relative macro-economic stability from the mid-1990s to the mid-2000s, a development further spurred by quantitative easing and ultra-lax monetary policy in the aftermath of the great financial crisis. Many countries also have favourable tax treatment of owner-occupied housing via mortgage interest deductibility, which further spurs house prices (Chapter 4).

On the supply side, low responsiveness of new housing has exacerbated the price effects of housing demand changes. Supply tends to be more “sticky” than demand, because it takes time to plan and build new structures so that weak supply adjustment allows price pressures to build up. Additionally, rising construction costs have contributed to declining housing affordability in many countries, in part due to increasingly stringent energy efficiency and environmental sustainability regulations (Chapters 4 and 7).

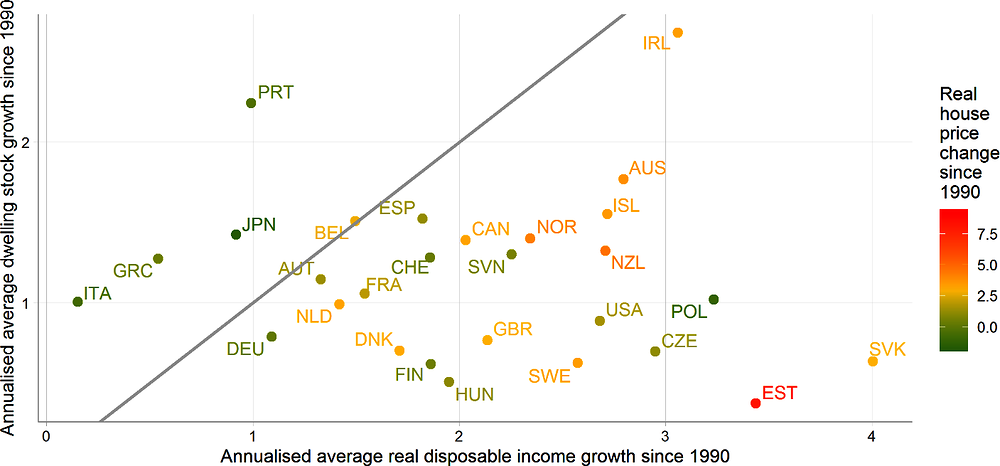

Housing supply responds to changes in demand, such as from income growth, quite differently across countries (Figure 1.4).

Note: This chart shows that housing supply, measured by the number of dwellings, has expanded much more slowly than aggregate household disposable income in many countries. It also illustrates that real house prices have broadly tended to increase more in countries where supply growth has not kept up with income growth (below the 45° line) by comparison with countries where supply has expanded faster than incomes (above the 45° line).

Source: OECD Economic Outlook database, Cavalleri, Cournède and Ziemann (2019[2]) and OECD calculations.

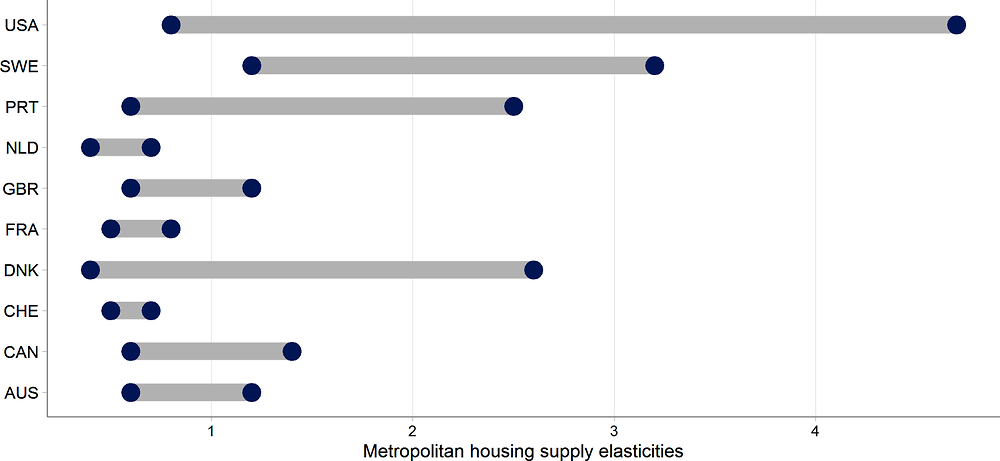

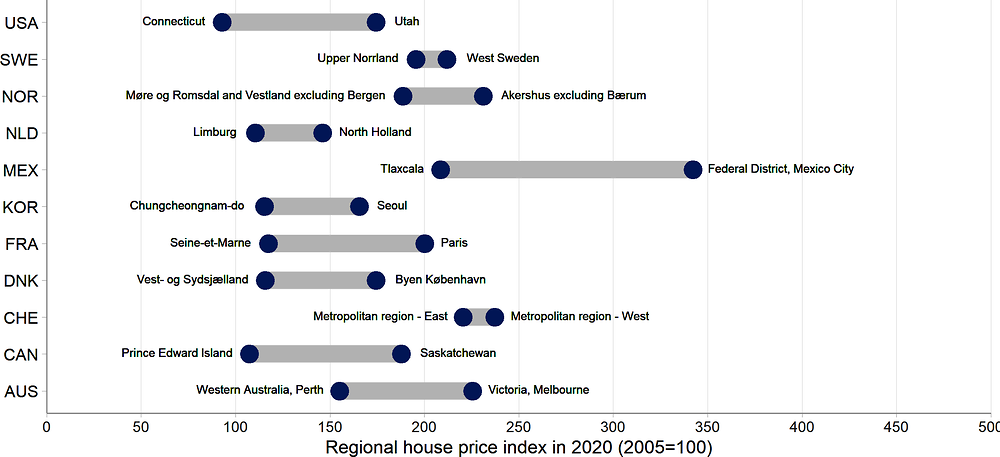

The responsiveness of supply to price changes triggered by stronger demand indeed has been found to vary a lot across and within countries (Figure 1.5, Figure 1.6). The differences have been empirically related to a range of geographical, historical and policy drivers.3 These factors include: Is the area easily amenable to construction? What is the urban form inherited from the past? How conducive is the policy environment to homebuilding? These factors vary a lot across but also within countries: one manifestation of this variation, together with geographic differences in demand, has been strongly diverging house price changes within many OECD countries (Figure 1.6). Housing supply conditions can further affect the economic incentives to inter-regional migration and, consequently, the spatial allocation of workers within countries (Causa, Abendschein and Cavalleri (2021[3]); Causa, Cavalleri and Luu (2021[4]). A flexible housing supply enhances the responsiveness of internal migration to both local income and employment conditions, and this spatial reallocation can help to absorb adverse local shocks.

The heterogeneity of price developments underscores the importance of spatially aligning demand and supply, meaning construction should occur where it is most demanded. The need for flexible supply responses is even more critical as ongoing megatrends, such as population ageing and digitalisation, as well as the recent COVID-crisis, are weighing on demand patterns (cf. Box 1.1). But, new construction is not the only way to bring supply in line with demand. For instance, the renovation and upgrading of the dwelling stock can help match demand and reduce vacancy rates. Besides, taxing vacant homes encourages greater use of existing housing assets. Making sure that taxation and regulation of short-term rentals are neutral by comparison with hotels or touristic residences can also help to avoid an excessive conversion of dwellings away from long-term residential uses.

Note: The segments represent the range of regional house price indices between the lowest and the highest observation as of 2020.

Source: OECD Database on National and Regional House price indices (http://stats.oecd.org/Index.aspx?DataSetCode=RHPI).

Governments are investing less in housing development

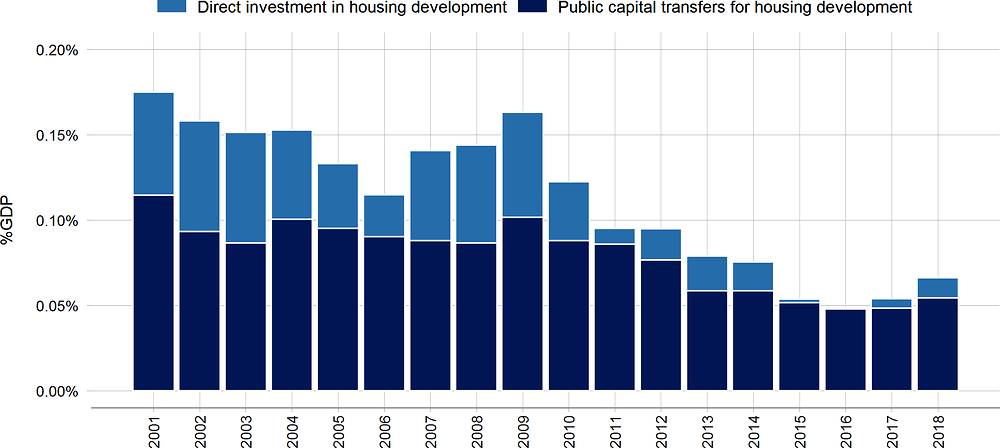

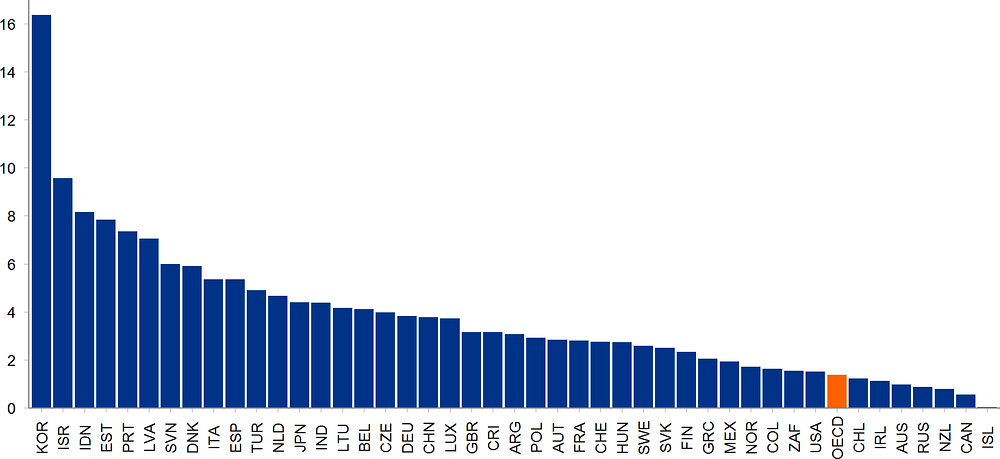

Another factor contributing to supply gaps is the decline in government investment in housing development, as well as a drop in the relative size of the social housing stock in most OECD countries. Over the past two decades, public investment in housing construction has dropped by more than one half on average across the OECD. In particular, direct public investment in dwellings has plummeted since the Global Financial Crisis, amounting to less than 0.01% of GDP in 2018 (Figure 1.7). In parallel, relative to the total dwelling stock, the share of social housing has declined in all but six OECD countries since 2010, further reducing the affordable housing supply for low-income households.4

Note: The OECD average is the unweighted average across the 25 OECD countries with capital transfer and gross capital formation data available from 2001. It excludes Australia, Canada, Chile, Iceland, Israel, Japan, Korea, Lithuania, New Zealand, Turkey and the United States. See the source for additional details.

Source: OECD Affordable Housing Database (http://oe.cd/ahd), indicator PH1.1.

Housing markets play a paramount role in the economy

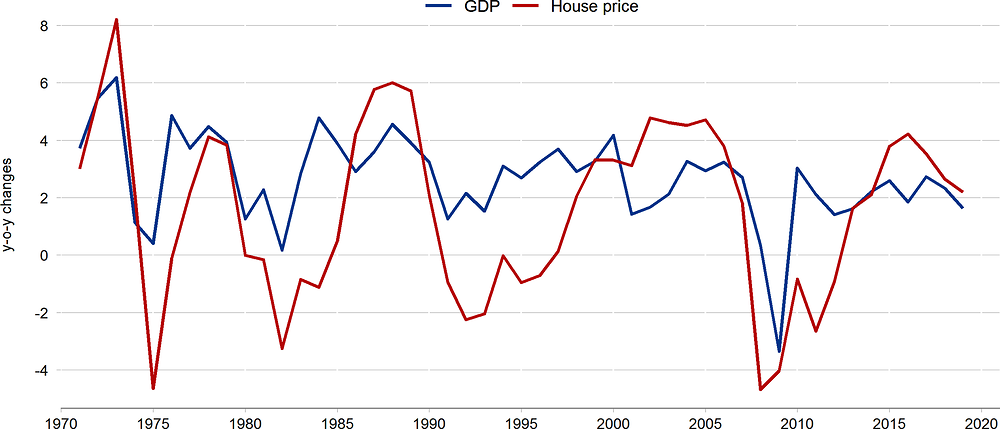

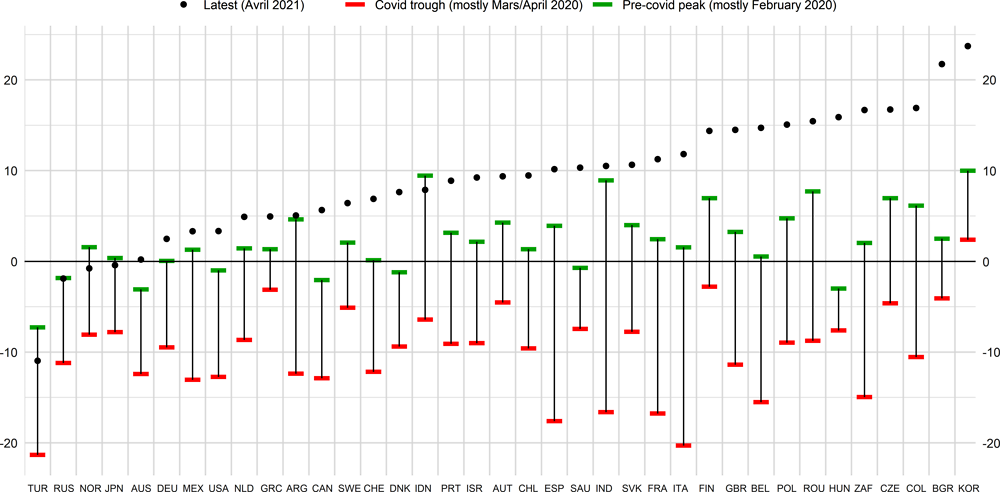

Housing accounts for a sizeable share of output. Construction makes up about 6% of GDP on average across OECD countries. Investment in dwellings alone accounts for about 20% of gross fixed capital accumulation. As a result, fluctuations in housing-related activities and house prices have strong effects on the business cycle (Figure 1.8). Understanding the drivers of these fluctuations is paramount to prevent the propagation and limit the amplification of housing shocks, thereby enhancing economic resilience. Housing and business cycles are indeed related: countries that observed larger corrections in real house prices during the Global Financial Crisis also suffered larger declines in economic activity. The unfolding COVID-19 crisis has had a major impact on construction and other housing-related activity (Box 1.2). Moreover, house price cycles tend to lead economic cycles. Peaks and trough in house prices occur before turning points in the business cycles, making them an important leading indicator of fluctuations in economic activity (Chapter 3).

Source: OECD Economic Outlook database and OECD Analytical House Price database.

The spread of the COVID-19 pandemic affected the housing sector throughout the world. Containment measures involved total or partial shutdowns of construction sites in many countries, as well as housing-related activities more generally. Indeed, internet searches related to real estate markets correlate strongly with the construction Purchasing Managers Indicators (PMIs) which allows the construction of construction confidence benchmarks for a wide range of countries (OECD, 2020[6]). Figure 1.9 illustrates the sharp declines in construction sectors' confidence as the first COVID wave hit in early 2020. While confidence had rebounded swiftly in most countries, the re-emergence of the virus in the second half of 2020 and first quarter of 2021 undermined the sector yet again in some countries.

Note: The indicator ranges from -50 by 50. Positive numbers mean expansion and negative ones contraction. The chart shows countries where the Google Trends data are available and the 2018 population exceeded 10 million.

Source: Update of OECD (2020[6]).

Greater access to housing finance creates opportunities and risks

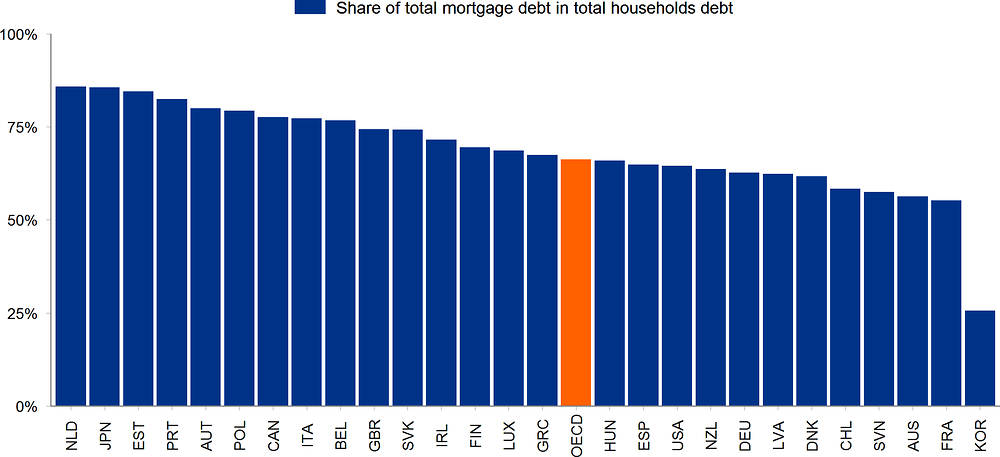

Financial and mortgage markets play a key role in housing markets since most households finance their home with debt financing (Figure 1.10). Housing finance has changed significantly over the past decades, which has lowered the borrowing cost for housing, leading to an expansion in the supply of mortgage loans. Financial and mortgage market innovations have helped lower-income households to become homeowners, as these changes have made it easier for them to take housing loans. However, excess leverage can pose risks for macroeconomic stability and long-term economic performance if policy changes trigger a significant relaxation in lending standards, a subsequent increase in non-performing loans and credit misallocation.5 Macro-prudential regulations but also housing policies can foster economic resilience by mitigating the build-up of vulnerabilities, reducing the transmission and hence the severity of crises and fostering an economy’s capacity to recover from them.

Source: OECD Wealth Distribution Database (oe.cd/wealth), HFCS database.

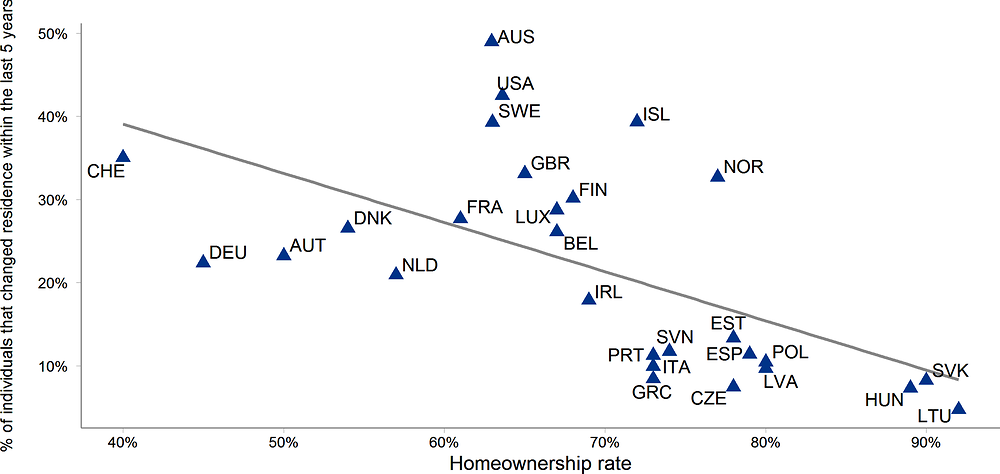

Residential mobility yields important benefits but may be hindered by poorly functioning housing markets

Several factors influence people’s decision to move. Preferences and needs, including due to changing family circumstances, play an important part, but so do policy choices that may create obstacles to mobility and make it difficult for people to move in search of better jobs. Residential mobility can help overcome interregional inequalities, improve job matching and thereby lift aggregate productivity and social mobility.

Among the key determinants of residential mobility are homeownership and social-housing tenure, since homeowners and social-housing tenants usually are not as mobile as private-market renters (Figure 1.11 and (OECD, 2020[7])). Furthermore, rising housing costs and rising regional differences in housing costs constrain the ability of lower-income individuals to move to areas where there are jobs or better jobs available but where they cannot afford the housing cost, with adverse implications for labour mobility and reallocation.6 Well-designed housing and labour market policies can facilitate residential mobility by improving the matching of workers with jobs across the territory. Removing policy-related obstacles to mobility and ensuring sufficient supply in high-demand areas can speed up the reallocation process in the wake of the COVID-19 crisis and help the labour market to recover.

Source: OECD Calculations based on 2012 EU SILC Data for EU countries; AHS 2013 for the United States; HILDA 2012 for Australia. Homeownership rates from the OECD Affordable Housing Database.

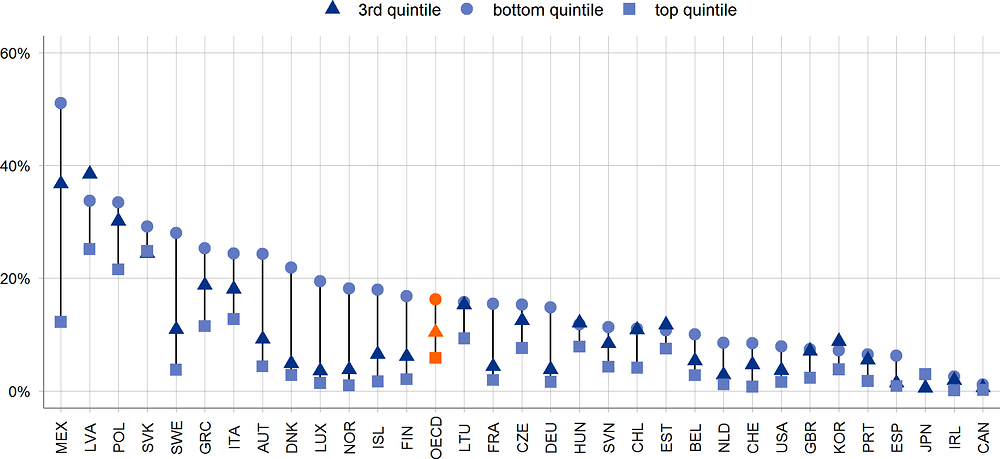

Lack of access to quality housing can have lasting distributional effects

As previously discussed, low-income households are spending a larger share of their income on housing: in addition to being more likely to be overburdened by housing costs, they are also more likely to live in poor-quality dwellings (Figure 1.12). They may not be able to afford regular maintenance or improvements to their dwellings, while at the same time finding it too expensive to move to better-quality housing. Lack of access to quality housing are often associated with poor access to health, education, broadband internet and good job opportunities (OECD, 2014[8]). This can have long lasting effects including on the lifelong income of young people who grow up in housing of poor quality or limited access to education or health services. The COVID-19 pandemic renewed concerns among policymakers about overcrowding, because overcrowded conditions make it more difficult for inhabitants to effectively self-isolate, putting people at greater risk of contracting and spreading infectious diseases (OECD, 2020[9]). The COVID-19 crisis has also exacerbated the impact of the digital divide in housing, as households without internet access have greater difficultly in working from home or participating in distance learning.

Note: See section "Data and comparability issues" of Indicator HC2.1 on limits to comparability across countries due to the definition of rooms.

Source: OECD Affordable Housing Database (http://www.oecd.org/housing/data/affordable-housing-database/housing-conditions.htm), indicator HC2.1.

Housing is an integral part of household wealth

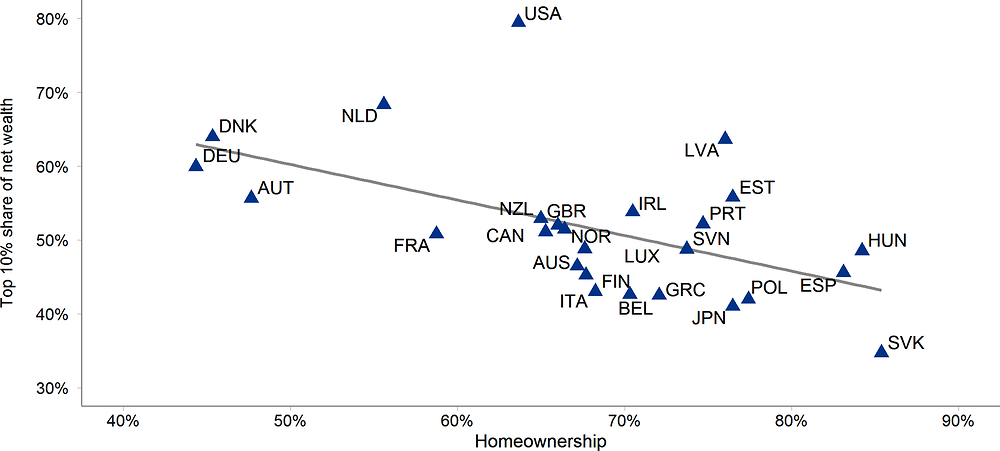

Rising house prices means that many households are missing out on the benefits of owning a home. Developments in housing markets have repercussions for household consumption and the macroeconomy via wealth effects. Rising house prices also have implications for wealth inequality (Chapter 5). Indeed, housing is an essential part of wealth as it is the single and biggest asset for a majority of households. Changes in house prices translate into changes in household wealth and this can in turn redistribute wealth between different types of households such as renters and homeowners. Given the importance of housing in household balance sheets, especially for the middle class, housing contributes to equalise the net wealth distribution (Figure 1.13). This is because housing seems to be more equally distributed than other assets, such as financial assets.

Source: OECD Wealth Distribution Database (oe.cd/wealth).

Housing accounts for a substantial share of global CO2 emissions

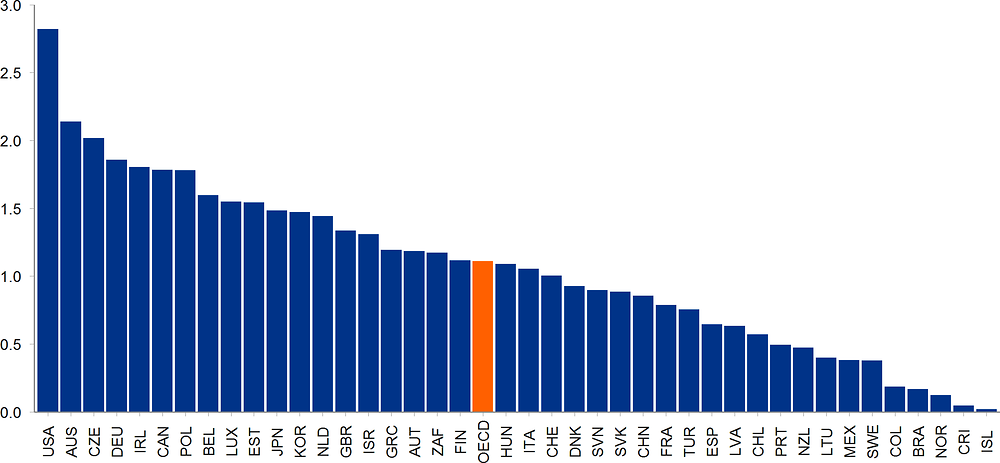

Housing is energy-intensive. The residential sector (buildings and construction) accounts for 28% of global final energy consumption and 17% of total CO2 emissions. Housing-related emissions are very different across countries (Figure 1.14). These large gaps reflect considerable cross-country differences in the degree to which public policies effectively price CO2 emissions from the residential sector, pointing to ample room for reducing emissions in many countries, although non-policy factors such as temperature patterns are also at play (Figure 1.15).

The use of environmental-friendly materials and improvements in isolation and heating systems have great potential to make housing more energy-efficient and help meeting agreed emission targets. Yet, in 2018, two-thirds of countries still lacked mandatory building energy codes.7 High-performance buildings, such as near-zero energy buildings, still make up less than 5% of new construction. Implementing and enforcing regulation to meet building envelope objectives also means that existing buildings require renovation and maintenance. However, environmental regulation increases construction costs and administrative burdens on the supply of residential structures. Policy simulations show that the carbon transition could put sizeable additional pressure on house prices (Chapter 4). Ensuring both affordability and sustainability is, therefore, an important policy challenge.

Source: OECD Environment Database (2020).

Complex links tie housing and environmental quality

In addition to emissions, housing has environmental impacts through land and material use as well as the transportation patterns that urban form generates. These impacts can differ across countries, as in the case of land-use (Figure 1.16). Furthermore, the effects of housing can sometimes be different across environmental objectives: for example, urban sprawl translates into higher transportation needs, greater difficulty in deploying public transport and higher greenhouse gas emissions as well as greater use of rural or natural land. On the other hand, lower density reduces exposure to local air pollutants that are more concentrated in higher density areas. Some environmentally-related policies can put a strain on the near-term affordability of housing. Nonetheless, frontloading the pricing of environmental externalities yields important benefits as it reduces the extent of such externalities, thereby contributing to environmental sustainability and intergenerational justice.

Source: OECD, “Land cover change”, https://dx.doi.org/10.1787/3dee7330-en.

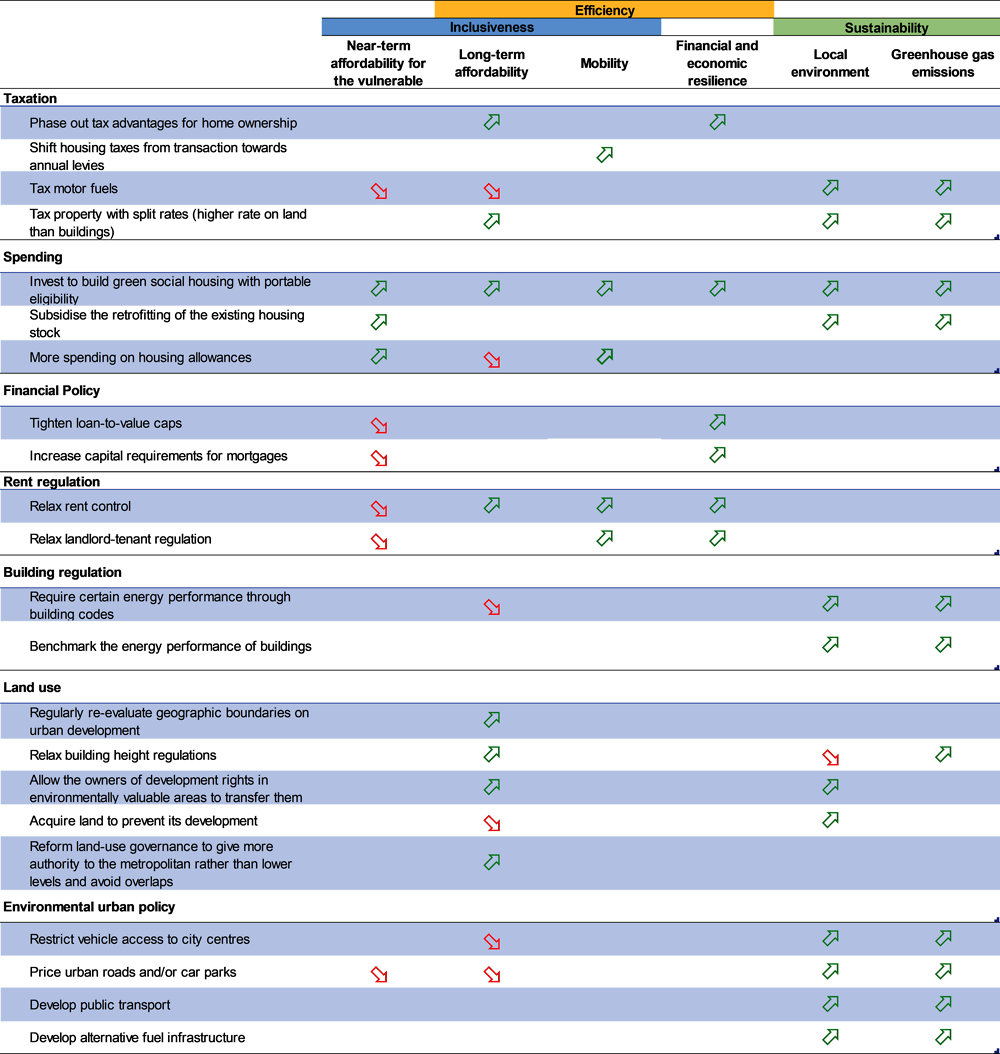

Policy action in multiple areas, ranging from housing policies to government spending and taxation, influences housing outcomes. Reforms can aim at multiple objectives: making the housing market more efficient, more inclusive or more sustainable (Box 1.3). National preferences can considerably vary across these objectives, which can warrant contrasted policy choices across countries. Furthermore, the legacy of past choices strongly shapes today’s needs and possibilities in a sector where path dependency is very strong due to the slow renewal of the housing stock.

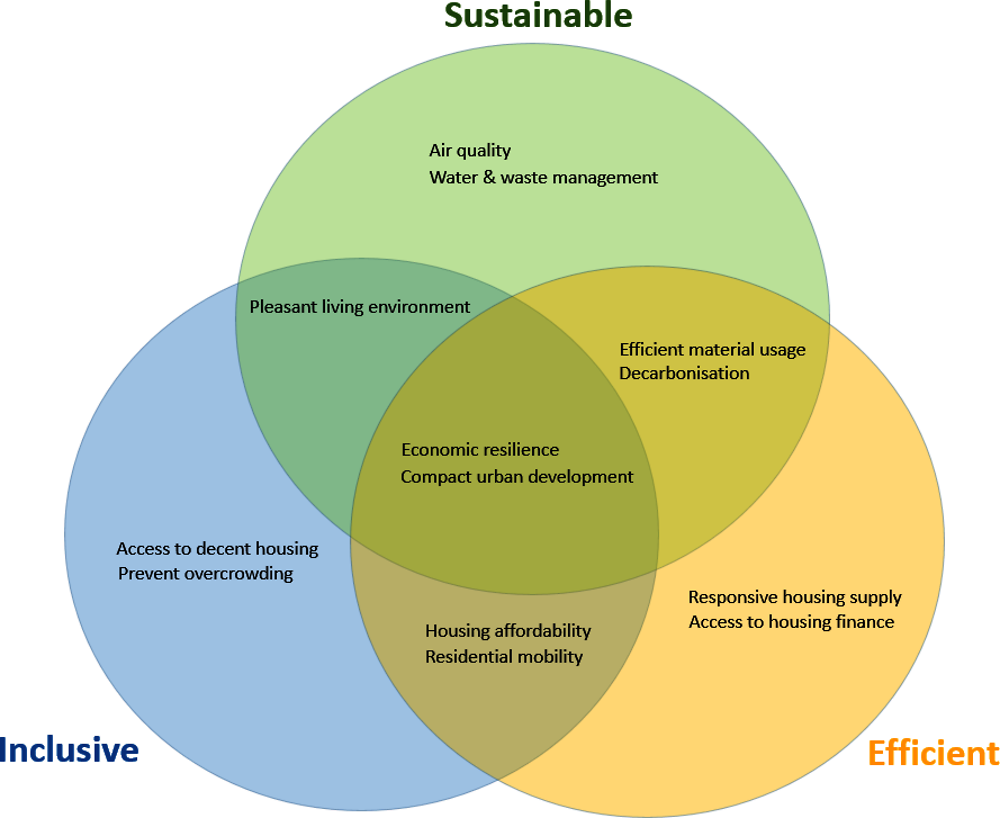

Three key dimensions underpin the OECD Horizontal Project on Housing: Inclusiveness, efficiency and sustainability (Figure 1.17). Inclusiveness relates to the possibility for low-income households and other vulnerable groups, such as people with unstable jobs, to live in good-quality dwellings that serve their needs, including access to labour markets, schools and amenities. Efficiency describes the capacity of the sector to supply housing that matches demand both quantitatively and qualitatively without unnecessary costs. Sustainability refers to the compatibility of residential construction and housing use with high local environmental quality and climate objectives.

As in other policy areas, where multiple objectives can be pursued, there is a need to assess possible synergies, trade-offs and unintended consequences that different policy tools may involve. When trade-offs arise, it is also essential to identify the extent to which compensatory measures can alleviate adverse effects induced by specific policy initiatives. Table 1.1 summarises the key policy synergies and trade-offs among housing objectives based on the empirical evidence reported in this Synthesis. Two caveats apply. First, it relates to typically expected effects; different consequences may arise in practice depending on the country-specific environment. Second the table summarises the available empirical evidence regarding impacts on housing objectives, but the policy interventions can also have effects in other areas such as government budgets. The OECD Housing Policy Dashboard (Box 1.4) gathers outcomes and policy indicators drawn from the report and aims to assist policymakers in making informed policy choices when designing national housing strategies.

Table 1.1. Most policy interventions have effects that cut across multiple dimensions |

|---|

|

Note: A green upwards-pointing arrow means that the policy reform in the row supports the objective in the column. A red downward-pointing arrow means that it detracts from it. Blanks indicate that there is no known systematic effect. Indicators to measure outcomes and policy stances are summarised in Box 1.4. The depicted impacts reflect the empirical evidence reported throughout the present report. Real consequences may depend on the country-specific context and can differ from the expected effects shown in the table. The columns cover housing-related objectives, but the policy interventions in the rows can have effects on other areas such as government expenditure or revenue. |

Source: Chapters 2-9. |

A set of indicators to inform policy choices

A better understanding of the linkages between policies and outcomes along the three dimensions of efficiency, inclusiveness and sustainability requires the use of indicators. A dedicated Housing Dashboard provides policymakers with a set of key indicators that should help to make informed policy choices (Figure 1.18). It is available at http://bit.ly/housingtoolkitpreview.8

Because housing is a complex policy area, many outcome indicators could point to weaknesses in policy settings associated with one or more policy objectives. For instance, sustained increases in house price-to-income ratios point to deteriorating housing affordability, which poses challenges for inclusiveness and could signal at the same time a lack of efficiency in the way housing markets operate. As a result, in many cases there is no one-to-one correspondence between outcomes and policy objectives, and some judgement is therefore needed to link outcome indicators to policy objectives.

Policy indicators to compare policy stances with other countries

Along with outcome indicators, policy choices can be informed by a comparison of the policy stance and key features of policy interventions pursed in different countries and over time. To make progress in this area, the OECD has been investing in the collection of data and construction of policy indicators spanning the range of areas that are relevant for housing (Figure 1.18). By allowing benchmarking with other countries, these policy indicators provide indications about the scope for action regarding the reform options listed in Table 1.2.

An important source of information about policy settings is the 2019 OECD Questionnaire on Social and Affordable Housing (QuASH). It includes information on social housing policy, rental market regulation, land-use governance and mortgage regulation. Information is also available from other OECD workstreams, such as the measurement of effective housing taxation and mortgage interest relief, which comes from the OECD work on the Taxation of Household Savings (Brys et al., 2021[10]). External sources have also been used (see Annex 1.A1)

Given the interlinkages between outcomes and policy objectives, a policy dashboard (available online) allows policymakers to access information on the relevant outcome and policy indicators for a given country but also to compare settings across countries and over time. The dashboard can also be used to present snapshots of the situation in each country (“country fiches”) by highlighting selected key indicators in each dimension in comparison with peer countries.

Building on complementarities among policy objectives

Several policy initiatives can bring simultaneous progress in inclusiveness, efficiency and sustainability (Table 1.1). They include more provision of social housing, greater reliance on recurring taxes on immovable property and land, and various regulatory changes in land-use (Table 1.1).

Well-designed social housing can improve affordability along with other policy objectives.

Investment in social housing – directly or indirectly through non-profit or reduced-profit associations (Box 1.5) – contributes to increasing housing supply. As such, it not only results in greater affordability for eligible low-income tenants but also for the rest of the housing market. Importantly, eligibility for social housing should be portable across cities and regions to ensure low-income workers' mobility. Removing obstacles for people to follow jobs is an essential aspect of resource reallocation and particularly vital in the post-COVID-19 era (Box 1.2).

Moreover, providing social housing that is developed or refurbished in line with high energy efficiency standards contributes to reducing the housing sector's carbon footprint. It can also contribute to reducing energy poverty among social housing tenants. Doing so can have a demonstration effect, easing the broader deployment of environmentally ambitious building standards and facilitating the transition of the entire economy towards the attainment of agreed emissions objectives. Finally, if social housing investment is well integrated into environmentally and socially ambitious urban strategies, it also contributes to improving the quality of the local environment and to the development of inclusive, socially mixed neighbourhoods.

Austria has the third-highest share of social housing in its total dwelling stock among OECD countries at 24% in 2019 (OECD, 2020[11]). This high average ratio across the country masks the even greater importance of social housing in the capital city, Vienna, where the share is 43%. This performance results from a specific way of supplying and managing social housing, which involves municipalities and limited-profit housing associations. Both pillars of the system matter: for instance, in Vienna, 22% of households live in social housing provided by the municipal government and 21% in social housing provided by the limited-profit housing associations.

Across Austria, limited-profit associations manage more than two-thirds of the social housing stock. They generally provide high-quality housing at a below-market rate to low and medium-income households. They operate over 900 000 social housing units (two-thirds of which are designated for tenants) and build between 12 000 to 15 000 new homes every year, equivalent to 25-30% of total residential construction. Rents, which are cost-based, are on average 23% lower than for-profit sector rents. Abstracting from the opportunity cost of not renting at the market rate, budgetary costs for taxpayers and municipalities are limited: the funding of projects relies on private and public loans and equity of the housing association, which collects tenant contributions. The unique business model of housing associations mainly relies on funding loans, cost-based rents and the direct reinvestment of the surplus in construction and renovation of dwellings once loans are paid back. Furthermore, part of the rent goes into a rehabilitation fund dedicated to the renovation of buildings (more details on the social housing funding model in Austria can be found in Box 2.4). Thus, the quality of housing is maintained over time. Strict regulations on the quality of the building, both social and environmental, also ensure the high quality of affordable housing.

Source: OECD (2019[12]; OECD, 2020[11]).

Unlike the provision of social housing with limited benefit portability, housing allowances do not in principle restrict residential and job mobility (Chapter 6). However, a critical difference between the provision of social housing and housing allowances is that the latter supports demand while the former contributes to expanding supply. Where supply is rigid, an increase in housing allowances may have the unintended consequence of putting upward pressure on house prices and rents.9 This pressure can offset the intended effect of allowances on affordability for beneficiaries while making housing more expensive for households who are not receiving them. Dealing with this trade-off calls for complementary measures (discussed below) to enhance housing supply responsiveness to changes in demand associated with an increase in housing allowances.

Tax reforms can bring economic, social and environmental benefits

Shifting housing taxation away from transaction-based levies towards annual taxes would enhance housing market efficiency. Recurrent taxes on immovable property, as opposed to levies on housing transactions, have the added advantage of not discouraging residential mobility, which is closely linked to job mobility. Recurrent property taxes have also empirically been found to be comparatively supportive of economic growth, by comparison with other taxes, especially transaction-based levies; many countries are raising very litlle revenue from recurring property taxes, a situation that offers scope to make greater use of them.10 In countries where the valuation of the property, for tax purposes, lags well behind the market value, there is also scope to align the valuation for tax purposes with the market value (Chapter 8).

In addition, a rebalancing of the recurring property tax basis towards land, rather than structures, would have the benefit of encouraging more efficient uses of land and therefore greater environmental quality (Chapter 7). By reducing the extent to which recurring housing taxes discourage investment in dwellings, such a shift should also make the supply of housing more responsive to changes in demand. Nevertheless, some caution is warranted, since land-use regulation can limit the benefits that can be reaped through more efficient property taxes (Chapter 8).

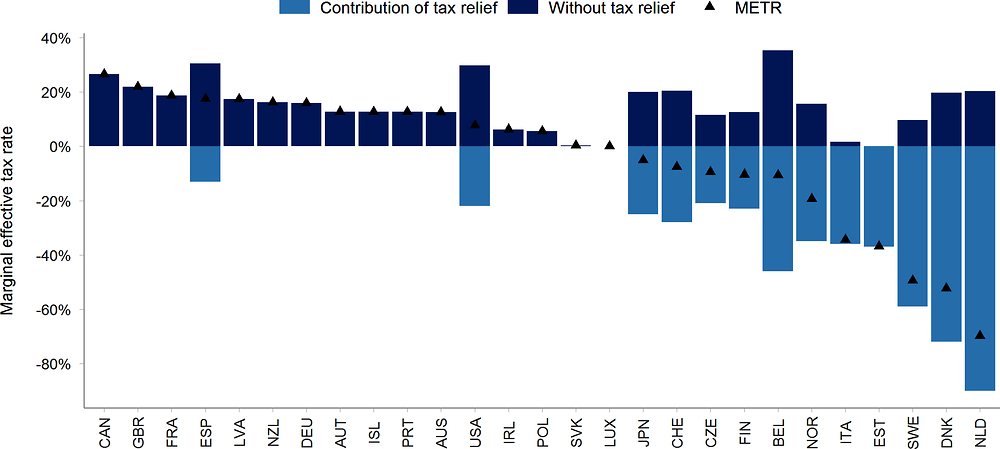

Phasing out mortgage interest relief can reduce house prices by substantial amounts in countries where supply lacks flexibility (see Chapter 4). The reason is that much of the value of mortgage interest relief gets capitalised into land prices in areas where supply is rigid. Gruber, Jensen and Kleven (2021[13]) find that scaling back mortgage interest rate deduction in Denmark has reduced equilibrium house prices and household indebtedness.11 In the long term, lower house prices make housing markets more inclusive by facilitating homeownership to a more significant share of the population and by driving down rents. In the medium term, before prices adjust, phasing out mortgage interest relief comes at a loss to the households who would otherwise have benefited from the tax advantage. The resulting political economy challenge means that countries that have eliminated or reduced mortgage interest relief have typically done so gradually (France, Netherlands, United Kingdom). This does not raise a pressing distributional issue, however, since mortgage interest relief primarily benefits higher-income groups.12 Furthermore, because mortgage interest relief does not remove primary barriers to first buyers such as downpayments and credit scores, its reform is also likely to have limited effects on homeownership even over the medium term.13 Increasing the effective taxation of residential property through the removal of mortgage interest relief or other advantages offers the additional benefit of contributing to smooth housing cycles (Figure 1.19; Chapter 3). The tax reforms that the Netherlands implemented in the 2010s are an example of a strategy that combined a shift in the burden of property taxation from a transaction-based to recurrent taxes with a reduction in the mortgage relief rate (Box 1.6).

Another avenue for tax reform that can improve both affordability and efficiency is to shift the burden of property taxation from transaction-based to recurrent taxes. Doing so removes an important obstacle to mobility (Chapter 6) and better aligns the tax with the services received (Chapter 8).

The Dutch tax system was long offering exceptionally favourable conditions to homeowners with large mortgages while applying substantial levies on housing transactions. This combination was identified as offering considerable scope for reform packages with multiple benefits (OECD, 2010[14]). First, reducing the highly favourable tax treatment of mortgage-funded homeownership can be expected to reduce levels of household indebtedness, contributing to greater economic stability and resilience (see Chapter 3), while also curbing house price increases (see Chapter 4). Second, lowering transaction taxes makes the housing market more fluid, facilitating residential mobility (see Chapter 6) and labour reallocation. These two reforms go well together in a tax package, as they have opposite effects on overall tax revenues.

This diagnosis, well recognised and accepted in the aftermath of the Global Financial Crisis, has been followed by a series of reforms. The transaction tax was reduced from 6% to 2% in 2011, first temporarily as a way of stimulating the market, but then from 2012 permanently as a way of facilitating residential mobility (OECD, 2012[15]). Besides, a series of measures have gradually narrowed the favourable treatment of mortgage borrowing under personal income tax. A significant first step taken in 2013 was to restrict interest relief to mortgages that are fully amortisable: this change excluded “balloon mortgages”, i.e. mortgages for which much or all of the principal is repaid at the term in a lump sum. Such balloon mortgages were previously widespread in the Netherlands, contributing to very high household indebtedness. An important further reform in 2014 launched a gradual reduction in the maximum mortgage relief rate by 0.5 percentage point a year until 2040 (from a starting point of 52% in 2014). In 2017, the government decided to accelerate this phase-out, taking it to 3 percentage points a year from 49% in 2020 to 37% in 2023 (OECD, 2018[16]).

Source: (OECD, 2010[14]; OECD, 2012[15]; OECD, 2018[16]).

Reforming land-use regulations can yield multiple benefits

Permitting the transfer of vested development rights from environmentally highly valuable areas to other places improves environmental quality while easing supply constraints where housing is in high demand. To the extent that greater supply responsiveness reduces upward pressure on prices, these reforms also have the potential of improving affordability along with improving efficiency in housing markets and contributing to environmental sustainability. Combining these regulatory reforms with stricter energy efficiency standards could improve the environmental impact of housing policies by paving the way for faster progress in the energy transition of the housing stock.

Furthermore, reforming land-use regulations can have broader positive consequences for the economy. Flexible land-use regulation within integrated planning frameworks that incorporate environmental objectives can facilitate the efficient reallocation of labour and capital by allowing housing supply to adjust to the demand for relocation to high-productivity areas: such flexibility boosts investment and aggregate productivity and economic growth.14

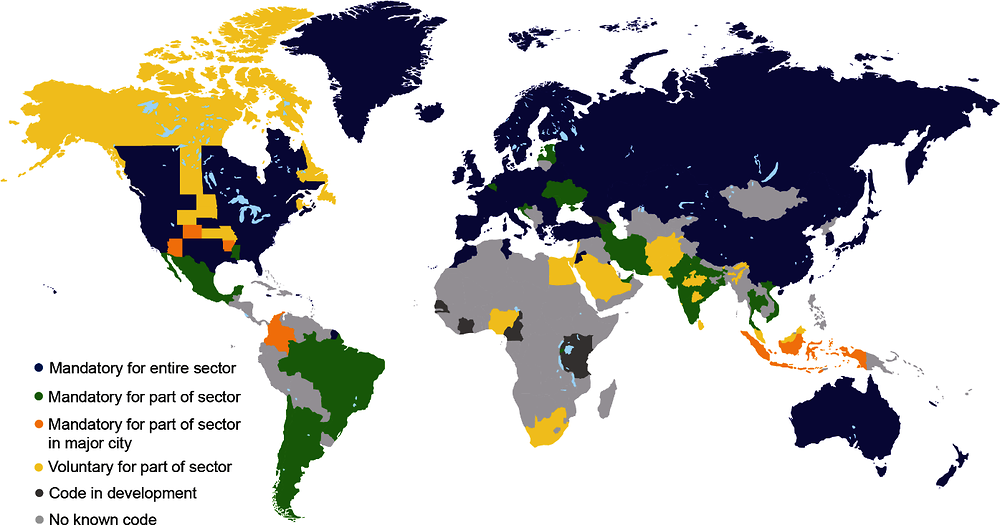

One way of doing so is to regularly revisit the geographic boundaries for urban development to accommodate city growth while ensuring forms of expansion compatible with environmental objectives (Chapter 7). Moreover, land-use governance arrangements that avoid overlap in the allocation of housing policy functions across the different levels of administration and favour planning at the metropolitan level rather than lower levels of government (Figure 1.20) can facilitate the matching of supply and demand within broader catchment areas. This can potentially increase the responsiveness of supply to evolving demand, mitigating upward pressure on prices and making housing more affordable (Chapter 4).15

Note: The governance of land-use regulations indicator ranges from 0 (least efficient, meaning most fragmented and overlapped) to 30 (most efficient meaning least fragmented with little overlapping responsibilities across levels of government) according to answers to the 2019 OECD Questionnaire on Affordable and Social Housing.

Source: OECD calculations.

Urban renovation policies are important for environmental and social objectives

The subsidisation of energy-efficient renovation of old buildings, which may be underutilised as a result of poor building standards, can expand the use of housing stock and its energy performance while easing the near-term pressure on affordability from the cost of energy-efficiency upgrading. Over time, the affordability benefits of such subsidies are likely to diminish, however, as the value of the upgrading gets capitalised into house prices.16

Managing trade-offs and unintended policy effects

Some trade-offs involve balancing short- against long-term affordability

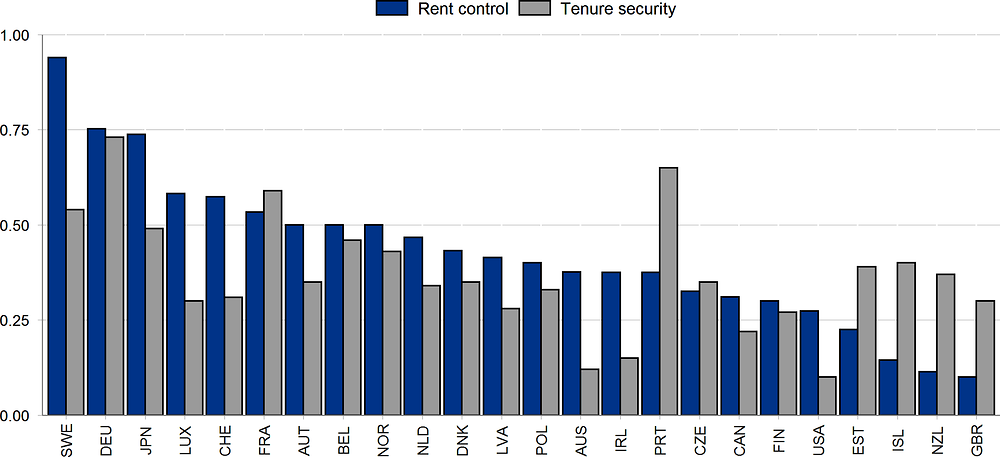

Making rental market regulations such as rent control and tenure security (Figure 1.21) more flexible, in combination with reforms to allow more responsive supply, have the potential to make housing markets more efficient and affordable in the long term. Still, they could undermine affordability for some households in the short term, especially for incumbents, as stringent rent controls reduce the rates of return on real estate investment. The related uncertainty discourages developers and lenders from investing in real estate, making the supply of housing considerably less responsive to changes in demand (Chapter 4). At the same time, tight rental contract restrictions could also affect vulnerable renters adversely, which poses obstacles for residential and labour mobility (Chapter 6). Indeed, excessive protection of tenants often implies that renters with uncertain labour market prospects, such as low-wage or non-standard workers, find it difficult to sign a lease, because landlords, who anticipate a difficult eviction in case of non-payment, require evidence about the stability of tenants’ income. There nonetheless remains a case for providing tenants with reasonable security over tenure and rent levels: a compromise can be a system of rent stabilisation, whereby rents can be varied for new contracts and renewals but regulated in line with market developments during the duration of the contract.

Note: The rent control and tenure security indices range from 0 (no restrictions) to 1 (all types of restrictions) according to answers to the 2019 OECD Questionnaire on Affordable and Social Housing.

Source: OECD calculations.

By potentially resulting in supply-demand mismatches, overly tight rental market regulations may also exacerbate speculative housing bubbles and excess accumulation of household debt, undermining economic resilience. Indeed, tight rental market regulations are associated with a higher probability of incidence of financial crises and more severe cyclical downturns in economic activity (Chapter 3). The unintended consequences associated with a tightening of rental market regulations can be mitigated at least in part through greater reliance on social housing and household allowances, which can be targeted to vulnerable renters, as well as by relaxing overly restrictive land-use regulations that inhibit supply responses where housing is in high demand.

The measures taken by several countries to shield renters from the hardships associated with the COVID-19 crisis are a case in point (Box 1.7). For example, rental market restrictions were introduced in many countries at the onset of confinement to help vulnerable households in the short term and provide a degree of income protection for existing renters. However, the obstacles imposed by tight landlord-tenant obligations to residential and consequently labour mobility can over time become particularly unwelcome in post-COVID-19 economies, given the need to adjust and facilitate the reallocation of labour and capital towards sectors and activities with promising economic prospects.

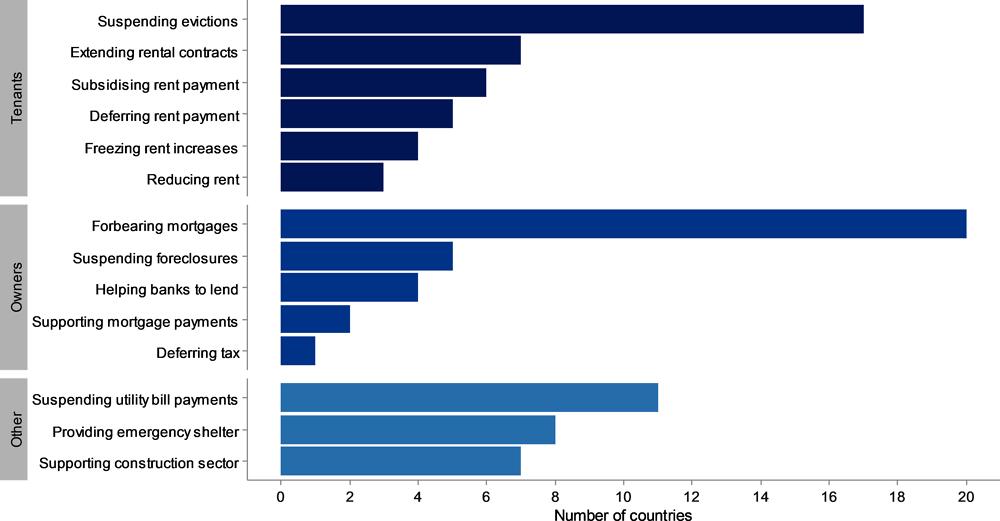

With the onset of the COVID-19 crisis, governments responded with a host of specific measures to protect mortgage-holders and tenants in addition to the support from social safety nets. A number of countries also intervened to help the post-crisis recovery of the construction sector (Figure 1.22). In most countries, emergency support involved a suspension of eviction procedures, temporary forbearance of rent and mortgage payments, and in some cases moratoria on utility payments. Most governments, at both national and local levels, also took specific steps to shelter the homeless during the lockdown.

Countries implemented several specific policies to support tenants in addition to letting social safety nets play their role. Many countries introduced moratoria on rent payments for economically distressed tenants. Some governments also provided specific financial support to tenants unable to honour rent payments as a result of the crisis. Rental market regulations were also adjusted, at least temporarily in some countries: rent freezes have been common for contracts coming up for renewal; rental contracts were made more flexible, by allowing tenants to terminate their contracts prematurely or to extend them so that they could more easily adjust to the needs prompted by the pandemic. Steps have also been taken to protect mortgage-holders and homeowners more generally. Several countries suspended foreclosure procedures during the period of confinement. Others authorised owners to defer the payment of their real estate taxes. Other measures aimed at supporting housing finance directly. In some countries, liquidity was provided directly to banks and mortgage lenders and, in some cases, by temporarily relaxing macro-prudential regulations imposed on banks.

Some of the response measures involve trade-offs between short and long-term objectives. Stronger tenant protection, regulatory forbearance and financial support for mortgage borrowers and lenders all reduce the short to medium-term adverse impact of the crisis on households and lenders, including an increase in evictions, foreclosures and homelessness. Moreover, such protections also helped to ensure that households could safely shelter in place and, when necessary, quarantine during the pandemic. However, as discussed in the main text, these measures can in the medium-term bear on supply, hinder mobility and diminish resilience to future crises (Table 1.1). As the recovery unfolds it will become increasingly important to balance short-term concerns against the longer-term needs of a well functioning housing sector.

Other crisis-response measures however do not involve such trade-offs. Expanding the supply of social housing contributes to the recovery in activity while, over the medium to long term, expanding supply and facilitating access to housing by low-income households. It is important to ensure portability of social housing rights to avoid creating obstacles to mobility. Easing land-use rules to facilitate construction, within the framework of urban planning strategies and building codes that are compatible with environmental objectives, would boost the recovery of the construction sector over the medium term. Such initiatives would also make the housing market more efficient over the long term.

Some macro-prudential measures raise challenges for particular groups

Macro-prudential measures to limit borrowers’ exposure to housing indebtedness also involve trade-offs, especially as regards access to housing finance by specific social groups. Tightening macro-prudential policy settings helps to curb housing market excesses (Box 1.8) and protect macroeconomic stability (Chapter 3). However, interventions such as limits on mortgage amounts relative to the value of the property (loan-to-value LTV caps) make dwelling purchases more difficult for young households with limited savings. Where appropriate, this trade-off can be mitigated at least in part by targeting support to first-time home-buyers through tax-favoured savings plans that help them accumulate their upfront payment. Another option is for macro-prudential policy to rely more on debt-service-to-income caps, which also mitigate risk without requiring the accumulation of a downpayment in the same way as LTV caps do.

Facing fast increases in house prices, Sweden tightened LTV-based measures in 2016 using amortisation as a tool. It required minimum amortisation of 1% per year for mortgages with LTVs between 50 and 70% and 2% per year if the LTV is above 70%. Since 2018, this LTV-based set of measures was supplemented by a policy relying on the debt-to-income (DTI) ratio: loans with a DTI above 4.5 must have an amortisation of at least 1% per year. These requirements, which have the effect of discouraging high borrowing relative to the value of the house and the level of income, have been successful at curbing house price increases.

Also in response to rapidly rising house prices, especially in Vancouver and Toronto, Canada tightened its LTV cap from 95% to 90% for homes above CAD 0.5 million. This move was complemented by tightening compliance with the cap on the debt-service-ratio: while the ratio was previously computed with the effective interest rate at which the mortgage is issued, after the move it had to use a conventional interest rate defined by the Bank of Canada. Access to government insurance was also tightened for high-LTV mortgages in 2016 and again in 2018. The tightening in macroprudential policy was followed by more muted house price developments, including a decline in Vancouver and stabilisation in Toronto.

Sources: (OECD, 2019[17]; Duprey and Ueberfeldt, 2020[18]; OECD, 2018[19]).

Efforts to improve the environmental sustainability of housing can entail costs

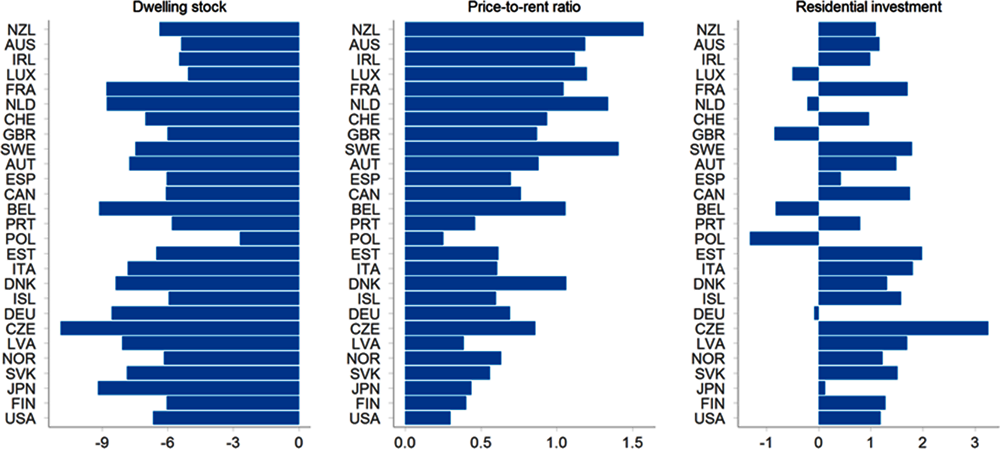

The costs arising from compliance with stricter energy efficiency and other regulations that can improve the environmental sustainability of buildings and structures can undermine affordability. Of course, these costs may not be passed on in full to house prices, especially where construction and home improvements may be subsidised, at least in part. Also, efforts to increase the energy efficiency of dwellings may result in lower energy costs to be borne by homeowners or renters. These improvements can also lower borrowing costs or improve credit terms for mortgage-holders to the extent that lower utility bills and better long-term valuation prospects for high-efficiency homes reduce credit risk (Box 1.9). However, upward pressure on house prices may be substantial where sizeable investments are needed to replace or upgrade the housing stock: illustrative simulations with stylised assumptions suggest that the attendant house price increase could be equivalent to more than half a year of disposable income in many OECD countries (Figure 1.23).

Several policies to improve the environmental performance of cities can have adverse implications for housing supply and affordability. Government acquisition of land to prevent development, as in the case of green belts around urban areas, directly limits supply. More indirectly, policies to restrict car access to city centres, price urban roads or increase car park fares have also been empirically found to raise house prices in cities by reshaping housing demand towards city centres, where house prices are typically higher (Chapter 7). There is also evidence that expanding public transport networks typically results in higher house prices, although doing so enhances labour-market and broader social inclusion by facilitating commuting and exchanges within urban areas. The potential negative effects of higher house prices on affordability and inclusiveness can be countered by policies to provide social housing and make land available for construction in the areas for which these policies are boosting housing demand.

StatLink https://stat.link/oftw8c

Note: Changes to baseline are shown (percentage points for dwelling stocks and residential investment; the number of years of disposable income to purchase the average 100m2 dwelling for the price-to-rent ratio). Environmental regulation to move towards carbon neutrality assumes an immediate increase of 10% in construction costs as well as a gradual increase in the heavy renovation rate of one percentage point from baseline heavy renovation rate (varies by country) until 2035. After 2035, the heavy renovation rate declines uniformly towards 1% per year by 2050.

Source: Cournède, De Pace and Ziemann (2020[20]).

Energy efficient, or “green”, mortgages can be an important funding source for the considerable investment required to bring the energy efficiency of dwellings in line with climate targets. An energy efficient mortgage is a housing loan that incorporates incentives for existing homeowners to improve the energy efficiency of their dwelling or for buyers to acquire energy efficient properties. The incentives can be favourable financing conditions or an increased loan amount. The assessment of energy efficiency relies on an energy performance certificate (EPC).

The rationale behind energy efficient mortgages comes from their advantages for lending institutions, borrowers and policymakers; namely, they are expected to reduce the owners’ payment disruption risk and improve their disposable income, increase property value, and, as a result, reduce credit risk for banks and financial institutions. Recent empirical analysis identified a negative correlation between building energy performance and credit risk (Billio et al., 2020[21]). The associated portfolio analysis shows a concentration of default in less efficient properties. The degree of energy efficiency also matters: more energy efficient buildings are associated with relatively lower risk of default, suggesting that energy efficient investments tend to improve borrowers’ solvency.

In addition, investor preferences and prudential perspectives could play a significant role in encouraging banks to support the transition to a low-carbon economy. Indeed, the origination of green mortgages allows banks to issue green bonds. The constitution of “green” portfolios based on a green retail strategy is an essential precondition for banks to develop green and Environmental, Social and Governance (ESG) funding instruments, which could support reductions in financing costs and diversification of funding bases by attracting ESG investors. At the same time, regulatory and supervisory requirements are changing rapidly, making ESG compliance a new priority for banks.

In Europe, the European Mortgage Federation-European Covered Bond Council (EMF-ECBC) launched an Energy Efficient Mortgages Initiative (EEMI) in 2015 with the aim of: (1) promoting energy efficiency investment in buildings, (2) creating a standardised green mortgage to facilitate the acquisition of energy efficient properties and the renovation of those not aligned with energy efficiency norms, and (3) evaluating the availability of energy efficient mortgage data across EU Member States, as well as gathering large-scale datasets to investigate the links between buildings’ energy efficiency features, their market value and loans’ probability of default and loss-given-default.

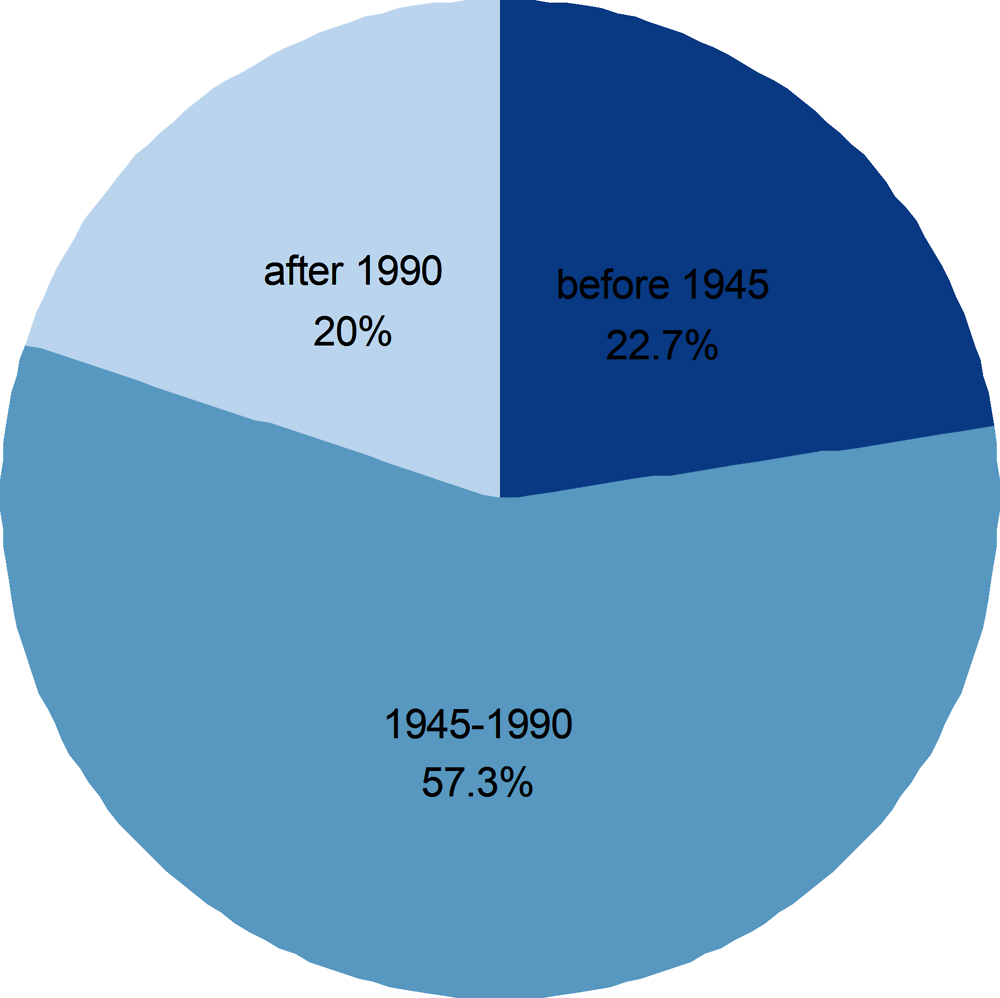

Since the introduction of Energy Performance Certificates (EPC) in 2010, mortgage markets appear to be increasingly sensitive to the energy performance of buildings and mortgage parameters are aligning to EPC classes. The challenge remains to support and scale up the renovation of the existing buildings that have poor energy efficiency performance. In Europe, about 80% of the building stock was built before 1990 (Figure 1.24), making it important to incorporate the renovation of existing building in energy efficient mortgage strategies. Poorly insulated dwellings can have dire consequences for households: 7% of Europeans and nearly 20% of the less affluent ones (defined as those living in households earning below 60% of median national income) reported that they are unable to keep their homes adequately warm in 2018. The potential for mobilising the mortgage market is considerable, because the outstanding stock of mortgages accounts for 44% of GDP in the European Union.

Efforts to improve the energy efficiency of buildings also need to reflect local conditions, given the diversity of climate across regions. For example, in Europe nearly 65% of the energy consumption of an average household is related to heating and cooling. Assessing the actual needs of households according to their place of residence therefore also gives an important indication of realistic goals in reaching energy efficiency, while at the same time providing a common set of framework conditions to identify the features a dwelling needs to possess in order to be energy efficient in a certain climate zone.

Source: European Mortgage Federation.

Against this background, business-led initiatives are under way to establish a European standard for green mortgages. The EMF-ECBC in February 2021 launched the “Energy Efficient Mortgage” (EEM) label to facilitate further data collection to inform analysis of the performance of green mortgages on an ongoing basis and secure quality and transparency for market stakeholders in the gathering, processing and disclosure of EEM data. The label is expected to underpin the business case and stimulate EEM market development. In this perspective, the collection of mortgage-specific data, including on the energy efficiency parameters of the underlying dwelling, is essential to assess the “greenness” of the labelled product.

Initiatives to develop energy efficient mortgages are not limited to Europe. Efforts are under way to coordinate standards globally through an advisory council attached to the European Efficient Mortgage Initiative. In Japan, the government-owned Japan Housing Finance Agency (JHF) has been promoting energy efficiency through its mortgage programme “Flat35S”, which was launched in 2005. As Japan is geographically distributed from subarctic to subtropical, the energy efficient labelling standard varies between 8 regions due to different climate conditions. The share of Flat35S financing energy efficient dwellings was about 47% of JHF’s securitisation support business in 2019 or around 10% of Japan’s total gross mortgage lending.

In Mexico, the Institute of the National Housing Fund for Workers (Infonavit) started issuing green mortgages in 2007. These mortgages include a top-up to the loan to allow the borrower to invest in energy-efficiency improvements. In 2014, Infonavit decided to originate only green mortgages. The impact on the market is substantial, because the number of mortgages issued by Infonavit each year (311 000 in 2019) is roughly equivalent to one-half of the net increase in the number of dwellings.

Source: European Mortgage Federation-European Covered Bond Council (EMF-ECBC); Japan Housing Finance Agency (JHF); Mexican Institute of the National Housing Fund for Workers (Infonavit).

Increases in motor fuel taxes, which reduce pollution in cities and beyond, potentially have the same upward effect on house prices over the medium term. However, this adverse impact subsides over time as the car fleet gradually becomes more fuel-efficient in response to higher fuel taxes (Chapter 7).

Improve housing policy governance to facilitate integrated responses to trade-offs

The governance of housing-related policies, from social housing to land-use to taxation, tends to be fragmented across government levels and sometimes across ministries or government agencies. This situation can complicate reforms, if public bodies with responsibility over one area, for instance land-use regulation, do not have authority in other areas, such as taxation or social housing that would allow them to design integrated reform packages. Difficulties of this nature can be tackled by reviewing the assignment of responsibilities and ensuring proper coordination across government layers and functions (Chapter 8). Integrated governance is important to provide urban policy making that is nimble and aware of linkages so that it can respond well to the lasting changes that are likely to arise in the future (see Box 1.1).

References

[5] Bétin, M. and V. Ziemann (2019), “How responsive are housing markets in the OECD? Regional level estimates”, OECD Economics Department Working Papers, No. 1590, OECD Publishing, Paris, https://dx.doi.org/10.1787/1342258c-en.

[21] Billio, M. et al. (2020), Final Report on Correlation Analysis Between Energy Efficiency and Risk, https://eedapp.energyefficientmortgages.eu/wp-content/uploads/2020/08/EeDaPP_D57_27Aug20-1.pdf.

[10] Brys, B. et al. (2021), Effective Taxation of Residential Property, forthcoming.

[3] Causa, O., M. Abendschein and M. Cavalleri (2021), The laws of attraction: economic drivers of inter-regional migration,housing costs and the role of policies, OECD, Economics Department Working Papers, forthcoming.

[4] Causa, O., M. Cavalleri and N. Luu (2021), Migration, housing and regional disparities: a gravity model of inter-regional migration with an application to selected OECD countries, OECD, Economics Department Working Papers, forthcoming.

[2] Cavalleri, M., B. Cournède and V. Ziemann (2019), “Housing markets and macroeconomic risks”, OECD Economics Department Working Papers, No. 1555, OECD Publishing, Paris, https://dx.doi.org/10.1787/737133d8-en.

[20] Cournède, B., F. De Pace and V. Ziemann (2020), The Future of Housing: Policy Scenarios.

[18] Duprey, T. and A. Ueberfeldt (2020), Managing GDP Tail Risk, Bank of Canada.

[13] Gruber, J., A. Jensen and H. Kleven (2021), “Do People Respond to the Mortgage Interest Deduction? Quasi-Experimental Evidence from Denmark”, American Economic Journal: Economic Policy 2021, Vol. 13/2, pp. 273-303, https://doi.org/10.1257/pol.20170366.

[11] OECD (2020), Affordable Housing Database, http://oe.cd/ahd.

[6] OECD (2020), Housing Amid COVID-19: Policy Responses and Challenges, https://www.oecd.org/coronavirus/policy-responses/housing-amid-covid-19-policy-responses-and-challenges-cfdc08a8/.

[9] OECD (2020), OECD Employment Outlook 2020: Worker Security and the COVID-19 Crisis, OECD Publishing, Paris, https://dx.doi.org/10.1787/1686c758-en.

[7] OECD (2020), Social housing: A key part of past and future housing policy, OECD Publishing, http://www.oecd.org/social/social-housing-policy-brief-2020.pdf.

[12] OECD (2019), OECD Economic Surveys: Austria 2019, OECD Publishing, Paris, https://dx.doi.org/10.1787/22f8383a-en.

[17] OECD (2019), OECD Economic Surveys: Sweden 2019, OECD Publishing, Paris, https://dx.doi.org/10.1787/c510039b-en.

[1] OECD (2019), Under Pressure: The Squeezed Middle Class, OECD Publishing, Paris, https://dx.doi.org/10.1787/689afed1-en.

[19] OECD (2018), OECD Economic Surveys: Canada 2018, OECD Publishing, Paris, https://dx.doi.org/10.1787/eco_surveys-can-2018-en.

[16] OECD (2018), OECD Economic Surveys: Netherlands 2018, OECD Publishing, Paris, https://dx.doi.org/10.1787/eco_surveys-nld-2018-en.

[8] OECD (2014), Society at a Glance 2014: OECD Social Indicators, OECD Publishing, Paris, https://dx.doi.org/10.1787/soc_glance-2014-en.

[15] OECD (2012), OECD Economic Surveys: Netherlands 2012, OECD Publishing, Paris, https://dx.doi.org/10.1787/eco_surveys-nld-2012-en.

[14] OECD (2010), OECD Economic Surveys: Netherlands 2010, OECD Publishing, Paris, https://dx.doi.org/10.1787/eco_surveys-nld-2010-en.

Notes

← 1. See for instance OECD (2018[93]).

← 2. (OECD, 2020[9]).

← 3. (Bétin and Ziemann, 2019[5]; Cavalleri, Cournède and Özsöğüt, 2019[29]).

← 4. (OECD, 2020[28]).

← 5. See Chapter 3 for impacts on resilience and Cournède, Denk and Hoeller (2015[210]) for effects on long-term economic performance.

← 6. (Bayoumi and Barkema, 2019[211]; Causa et al., 2021[222]).

← 7. Source : https://www.iea.org/reports/building-envelopes.

← 8. User name : delegate. Password : OECDHorizontalProject.

← 9. (Fack, 2006[214]; Grislain-Letrémy and Trevien, 2014[215]; Susin, 2002[216]).

← 10. See Akgun, Cournède and Fournier (2017[206]) and Arnold et al. (2011[220]).

← 11. Similarly, a recent study by Sommer and Sullivan (2018[51]) shows that eliminating mortgage interest relief reduces house prices and increases homeownership in the Unites States.

← 12. (Matsaganis and Flevotomou, 2007[207]; Jahoda and Godarovo, 2014[208]; Figari et al., 2017[209]; Justo et al., 2019[213]).

← 13. (Matsaganis and Flevotomou, 2007[207]; Jahoda and Godarovo, 2014[208]; Figari et al., 2017[209]; Justo et al., 2019[213]).

← 14. (Herkenhoff, Ohanian and Prescott, 2018[192]; Hsieh and Moretti, 2019[217]).

← 15. (Bétin and Ziemann, 2019[5]; Cavalleri, Cournède and Özsöğüt, 2019[29]).

← 16. (Taruttis and Weber, 2020[130]).