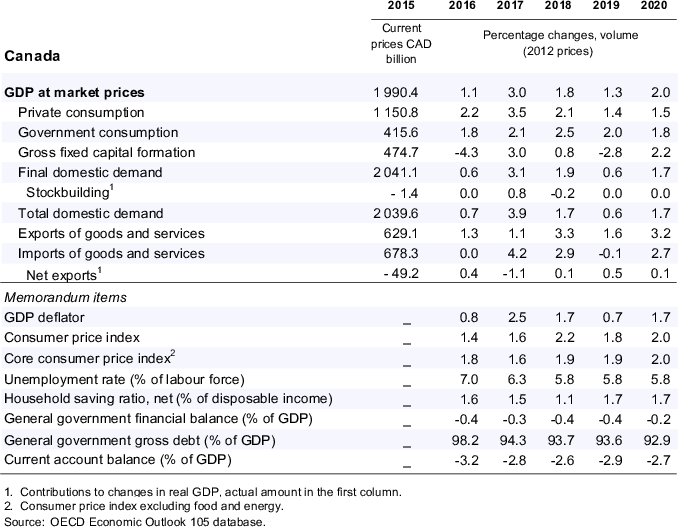

copy the linklink copied!Canada

Growth is projected to recover to around 2% (annualised rate) in the second half of 2019. Exports will strengthen in response to an easing in Alberta’s mandatory oil production cuts and higher export market growth. Business investment will rise as firms move to increase capacity and productivity and in response to new tax incentives. Employment growth is on course to slow, but the unemployment rate should remain near record lows.

The Bank of Canada is likely to maintain the current degree of monetary stimulus, which should be sufficient to keep inflation near the mid-point of its 1-3% medium-term target band. The fiscal policy stance is set to remain broadly neutral and, with small budget deficits, the debt-to-GDP ratio should continue to edge down. Macroprudential measures have helped take the steam out of the housing market and reduced lending to high-risk borrowers. The supply of affordable housing should be increased and social housing should be better maintained and targeted.

Economic growth has slowed

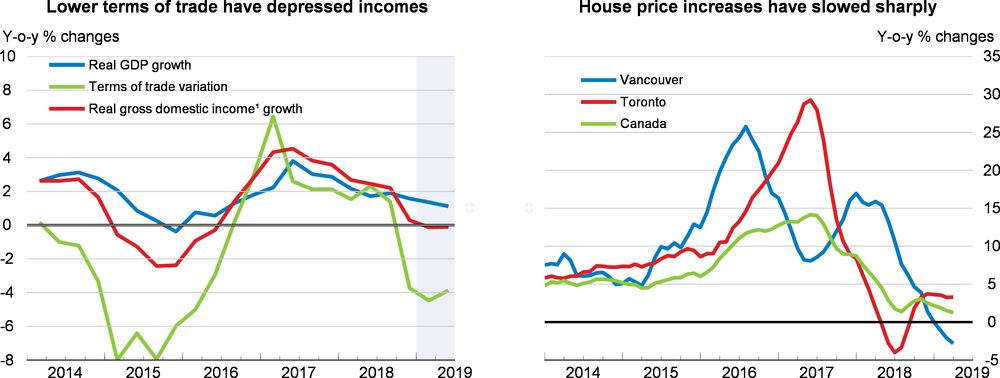

Economic growth has slowed as households have adjusted consumption expenditure to moderating income growth and higher interest rates, and businesses have cut investment in response to greater global trade policy uncertainty. Growth has also been weighed down by a sharp fall in oil export prices in late 2018, which has reduced domestic incomes, and by mandatory oil production cuts in Alberta. In addition to these cuts, slowing import demand growth in the United States has contributed to the fall in export growth.

1. Real gross domestic income equals real GDP adjusted for changes in the terms of trade.

Source: OECD Economic Outlook 105 database; Teranet; and Bank of Canada.

1. Includes oil and gas. Also includes some engineering structures investment that may relate to other sectors.

2. Percentage of firms expecting higher investment (/levels of employment) minus the percentage expecting less investment (/lower levels of employment).

Source: Bank of Canada (2019), Business Outlook Survey, Spring; OECD Economic Outlook 105 database; and Statistics Canada, Table 36-10-0108-01.

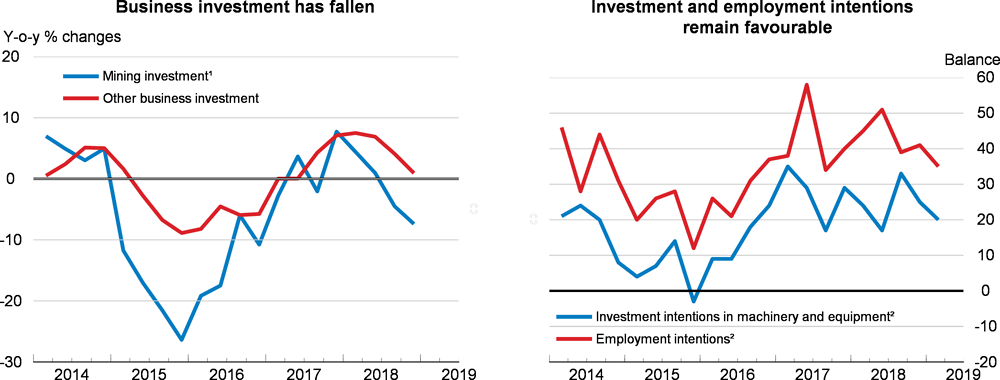

A weakening housing market has depressed residential investment and compounded the slowdown in consumption expenditure. Consumer and business confidence indicators have fallen, pointing to weak economic activity in the coming months. Nevertheless, business investment and employment intentions remain healthy outside the energy sector. The mandatory oil production cuts have markedly reduced the discount on Canadian oil in recent months, increasing incomes and paving the way for an easing in the cuts.

Employment growth has picked up markedly and the unemployment rate has remained below 6%, near a 40-year low. Wage growth has slowed from an already modest pace, driven by developments in the oil-producing provinces. Job churn has increased, pointing to stronger future wage growth. Consumer price inflation has receded due to falling energy prices. The average of the Bank’s preferred underlying inflation measures has edged down to 1.8%. Expected inflation has declined, with a majority of businesses now anticipating inflation to be in the lower half of the 1-3% medium-term target band over the next two years, and most of the remaining ones expecting inflation to be 2-3%.

The macroeconomic policy stance will gradually move towards neutral

In response to the tightening of macroprudential policy, provincial measures to reduce housing demand (notably foreign buyer transaction taxes in Vancouver and Toronto and a speculation and vacancy tax in major urban areas of British Columbia) and rising mortgage interest rates, the housing market appears to have achieved a soft landing, although there are large regional differences in conditions. Nationwide house prices stabilised (year-on-year) in early 2019, largely reflecting price growth of around 3% in Toronto, Canada’s largest housing market, declines in Vancouver (the second largest market) and Calgary and small increases in most other large urban markets. In Vancouver, adjustment is still occurring to the measures aimed at slowing the market and considerable housing supply is in the pipeline, pointing to further easing, while in Calgary prices should stabilise once adjustment to the fall in oil prices is complete. A housing market soft landing will support gradual deleveraging by households, a process that is already underway; household credit growth has slowed to low rates. No further tightening in macroprudential policy is called for at this time. To counter low housing affordability and long waiting lists for social housing, the supply of affordable housing should be increased and the stock of social housing should be better maintained and targeted.

The gradual withdrawal of monetary policy stimulus underway since mid-2017 has paused since late 2018 in response to slowing growth and a deteriorating global economy. With core inflation slightly below the mid-point of the target band and subdued wage pressures, the official rate is likely to remain unchanged until late 2020 and then to be raised to 2.0%, still below the Bank’s estimate of the neutral rate (2.25-3.25%). Long-term rates should increase moderately in response to rising global rates.

The fiscal policy stance is projected to remain broadly neutral in 2019-20, with the underlying primary balance set to be approximately stable as a percentage of potential GDP. This reflects a small easing at the federal level and tightening in Ontario, where the budget deficit is set to fall by 0.3% of national GDP over the next two years.

Growth is projected to strengthen

Many of the factors that have depressed growth in recent months – notably falling oil prices, mandatory oil production cuts, tightening macroprudential policies and rising interest rates - will have played out by mid-2019, laying the ground for an increase in growth to around 2%. In addition to an easing in the mandatory oil production cuts, stronger export market growth will support a pick-up in export growth. Business investment should also gather steam as firms seek to expand capacity, increase productivity and benefit from accelerated depreciation allowances following weak investment in recent years. While growth in private consumption will strengthen, it will nevertheless remain somewhat weaker than in recent years, consistent with gentle deleveraging. The unemployment rate is projected to remain around the current lows and real wage growth to edge up but to remain moderate.

A major downside risk is a greater-than-expected increase in mortgage rates, which could impair many households’ ability to service their mortgages, leading to a housing market correction and lower consumption expenditure. Another risk is that the United States-Mexico-Canada Agreement is not ratified or that access to the US market becomes less favourable even if it is ratified. On the upside, an increase in oil prices would boost incomes, as would a resolution of the regulatory difficulties of increasing oil pipeline capacity.