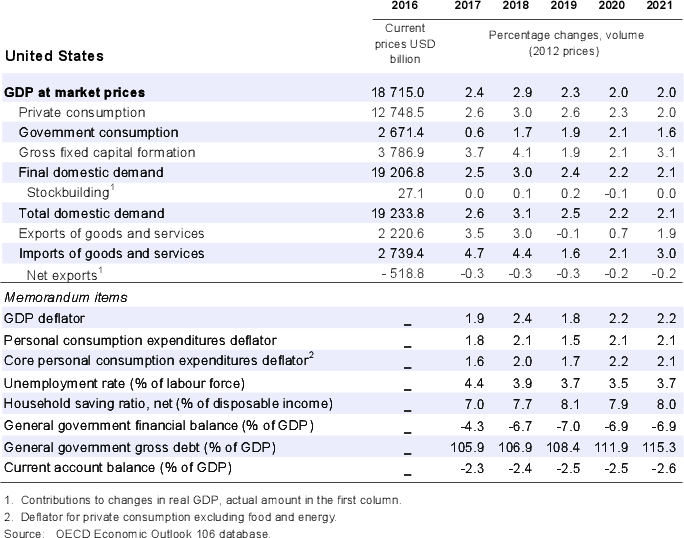

copy the linklink copied!United States

The current economic expansion has become the longest on record but economic growth is now slowing, partly due to increased tariffs on imported goods and high trade tensions. The labour market has created many new jobs and unemployment has fallen to historically very low rates. Rising real wages and high asset prices are supporting average household income and consumption growth. On the other hand, in addition to intense trade tensions and uncertainty, the combined effects of a waning fiscal impulse, weaker growth in trading partners, and demographic pressures are weighing on confidence and activity.

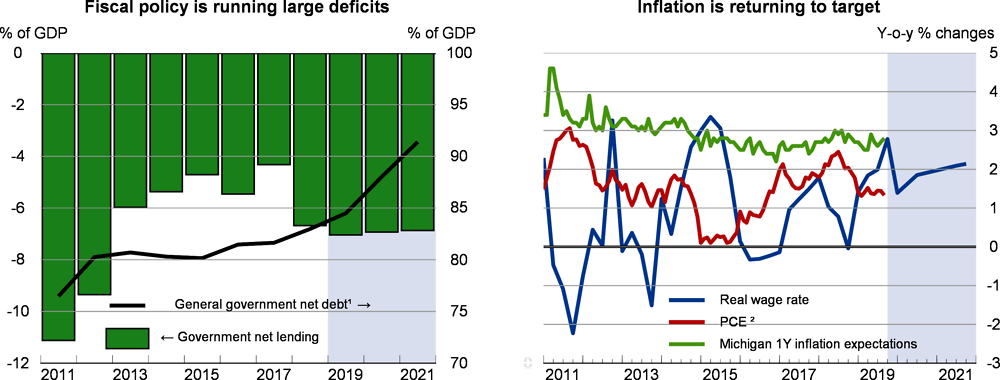

The Federal Reserve has acted to meet its dual employment and inflation mandate. With inflation returning to target only slowly and inflation expectations slipping, no changes to interest rates are projected, which may help meet the inflation target symmetrically. With large budget deficits and unsustainable long-run fiscal trends, the federal government has limited space to support the economy. Reducing barriers to finding jobs would help boost labour supply and productivity.

The economy is slowing

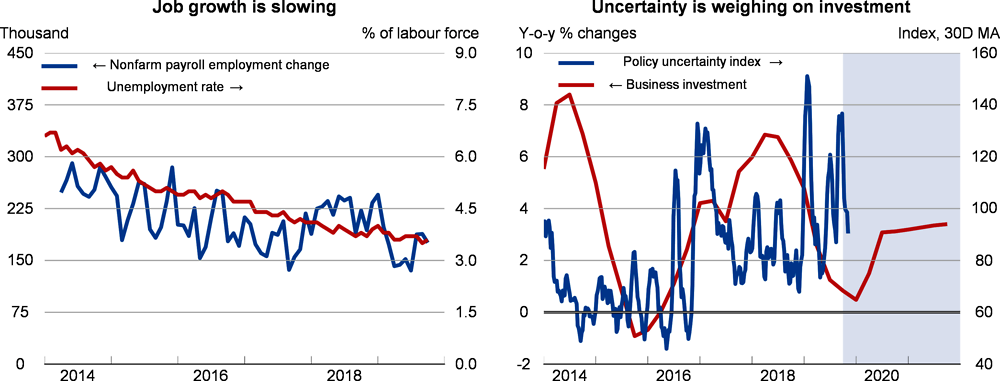

Investment and trade are slowing due to heightened uncertainty and weak demand from foreign markets, denting growth prospects. New trade measures implemented in September and those scheduled to be introduced in December 2019 on USD 300 billion imports from China have increased uncertainty, which is weighing on confidence, business investment and industrial production. The effect of new trade measures will also depress consumption growth and temporarily boost inflation. These effects are compounded by weak demand from trading partners.

Source: OECD Economic Outlook 106 database; US Bureau of Labor Statistics; and Refinitiv.

1. General government shows the consolidated (i.e. with intra-government amounts netted out) accounts for all levels of government (central plus state/local) based on OECD national accounts. This measure differs from the federal debt held by the public, which was 77.8% of GDP for the 2018 fiscal year.

2. Personal Consumption Expenditures price index.

Source: OECD Economic Outlook 106 database.

Strong job growth has helped drive down unemployment to rates that have not been seen since the 1960s. Wage growth has picked up, although somewhat hesitantly, which coupled with strong asset prices has helped support average household income and consumption growth. However, more recently job growth has been slowing towards rates that are more consistent with underlying labour force growth.

Policies to address weakening growth are needed

Heightened policy uncertainty about international trade is weighing on activity and investment decisions. Exporters have been hit by retaliatory measures and consumers are facing higher prices due to the tariff increases. Measures to reduce trade tensions and accompanying uncertainty, such as reaching agreement with China, would help bring forward investment from firms currently waiting before committing. The projections assume that trade measures remain unchanged after the introduction of the new tariff measures already announced for December. On that basis, increased US tariffs and associated retaliation may reduce US GDP by ½ percentage point by 2021.

Monetary policy has faced communication challenges as uncertainty about the outlook has increased and criticism of monetary policy has become more voluble. Given low inflation expectations monetary policy needs to ensure that the inflation target is met symmetrically. The Federal Reserve has undertaken three interest rate cuts as the international outlook deteriorated and as uncertainty has risen. If growth falters significantly, monetary policy may need to augment interest rate cuts with extended forward guidance and additional balance sheet operations. On the other hand, if economic conditions prove to be stronger than anticipated, a resumption of monetary policy normalisation would be appropriate.

The government is running substantial budget deficits, which are projected to rise to nearly 7% of GDP in 2021. To the extent possible, federal, state and local governments should reorient spending to areas such as infrastructure that would support productivity in the longer run. However, fiscal policy is unsustainable if sizeable deficits continue and long-term fiscal spending pressures mount. This leaves limited room for the federal government to react in the event of a sizeable downturn. Rebuilding fiscal buffers and preparing contingency plans would help prepare for possible shocks.

Part of the projected slowdown is structural, driven by demographic pressures leading to lower labour force growth. Some evidence is showing that strong job growth has drawn in workers who have tended to remain on the margins of the labour market. In addition, efforts to reduce opioid addiction appear to be bearing fruit, which will likely reduce death rates and support higher labour force participation. Continuing to help individuals back to the labour market and into jobs would help offset some of the employment slowdown while at the same time boosting productivity. Easing occupational licensing requirement and zoning restrictions would help workers find more productive jobs. These effects would help boost household incomes and help many low-income families.

Risks abound around projected slowing economic growth

Against a background of slowing economic growth due to demographic pressures, increased trade restrictions and policy uncertainty are further depressing activity. Investment growth remains modest as uncertainty remains high and trade growth fails to recover. Partly in reaction to the weaker outlook, monetary policy remains accommodative over the projections, and with new tariff rates coming into play inflation is projected to pick up to slightly above the Federal Reserve’s target.

There are substantial downside risks to the projection if trade tensions continue to escalate, especially if disputes spread to the automobile sector, intensifying uncertainty even more, further depressing investment and holding back a recovery of world trade. Domestic risks are also mounting, notably borrowing by the non-financial corporate sector. Limited space for fiscal and monetary policies to react to a sharp slowdown makes building up buffers and avoiding further disruption important. For monetary policy to remain effective, political interference should be avoided as it blurs communication, in particular concerning forward guidance. Working with trading partners in multilateral institutions would help relax tensions and give greater certainty to companies. On the other hand, a stronger international outlook, reduced trade tensions, building on the recent agreement with China to reach a wider-ranging deal, and stronger productivity growth could boost growth and inflation.

Metadata, Legal and Rights

https://doi.org/10.1787/9b89401b-en

© OECD 2019

The use of this work, whether digital or print, is governed by the Terms and Conditions to be found at http://www.oecd.org/termsandconditions.