Chapter 1. Measuring the impact of social protection on inclusive growth

Over the past years, social protection has gained an ever-greater recognition on the global and national development policy agendas as not only a fundamental human right but also an effective way to tackle poverty and vulnerability. This focus has been largely influenced by overwhelming evidence that social protection schemes can deliver real results in terms of poverty reduction and progress towards improving job quality. Yet, the economic impact of social protection investments remains overall poorly documented. To a large extent, this has to do with the complexity of measurement. This chapter proposes a methodological framework to capture linkages between social protection and inclusive growth. It first outlines definitions and measures of social protection and inclusive growth, then presents a new conceptual and measurement framework to assess the impacts of social protection on inclusive growth.

Inclusive growth and social protection

Inclusive growth

The current international development agenda highlights the need to shift focus from economic growth to inclusive growth, which emphasises distribution and the ability of vulnerable groups to participate in the growth process (OECD, 2018[1]; Mathers and Slater, 2014[2]). Despite unprecedented levels of wealth globally, 896 million people lived in extreme poverty and 2.1 billion lived in extremely vulnerable conditions in 2012 (UNDP, 2017[3]). Economic growth on its own is not sufficient to increase living standards, reduce inequalities and foster development. Large and persistent inequality may hamper economic growth, as it undermines the ability of the poor and most vulnerable to invest in education, affecting the opportunities and productivity of current and future generations (OECD, 2018[1]). Tackling inequalities is thus central to sustainable and inclusive development. According to the International Monetary Fund, inequality reduction resulting from redistributive policies in the form of taxes and transfers goes hand in hand with increased and sustained economic growth (Ostry, Berg and Tsangarides, 2014[4]).

Inclusive growth, defined as improvement of living standards and shared prosperity across all social groups, focuses on the pace and structure of growth. The concept of inclusive growth has gained recognition in development circles because it has broadened the discourse beyond a focus on the extreme poor, and increasingly shifted policy focus from poverty reduction to determining how growth can be made more equitable and more inclusive (UNDP, 2017[3]).

In response to increasing wealth, income and opportunity inequalities in many member countries, the Organisation for Economic Co-operation and Development (OECD) launched the OECD Inclusive Growth Initiative in 2012 (Box 1.1). It sought to develop a “people-centred growth model” that allowed everyone to participate in the growth process and get a fair share of its benefits (OECD, 2018[1]).

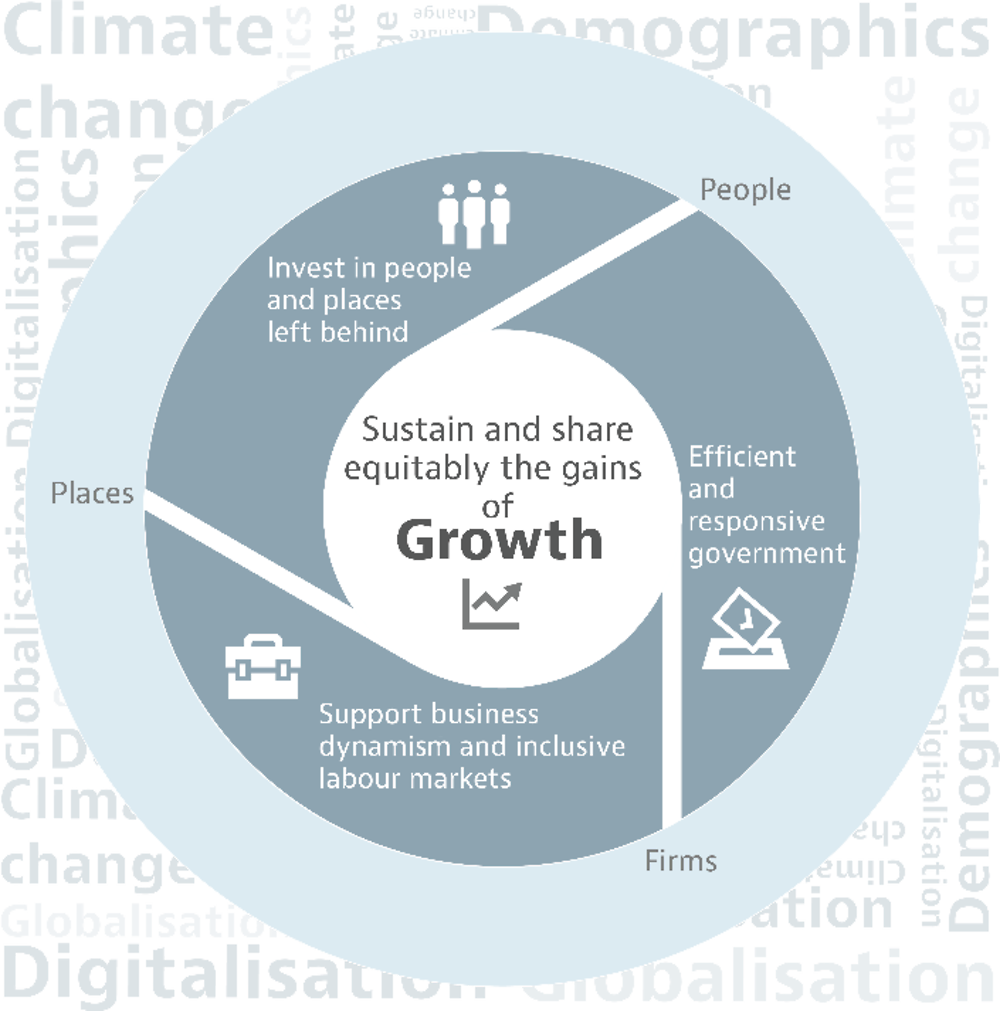

The OECD launched its Inclusive Growth Initiative in 2012 to help governments address the challenge of persistent and increasing inequality in income, wealth and opportunities. Across the OECD, the richest 10% own around half of all household assets, while the bottom 40% hold only 3%. Similarly, at the global level it is estimated that the poorest 50% of the world’s population receives only 9% of world income, while the richest 1% receives 20%.

The Inclusive Growth Initiative focuses on putting people at the centre of policy with the aim of ensuring (i) that economic growth translates into improved living standards as measured by a range of well-being outcomes that matter to people; and (ii) that these improvements benefit all segments of the population. In 2018, the OECD developed the Framework for Policy Action on Inclusive Growth as a tool to assess policies ex-ante in terms of their effects on economic growth and social inclusion and help governments design integrated strategies that combine greater efficiency and equity (OECD, 2018[1]).

The Framework for Policy Action highlights three priority areas through which governments can sustain and more equally share the benefits of economic growth:

-

1. Invest in people and places left behind, providing more equal opportunities through early-life interventions that compensate for initial disadvantage; life-long skills acquisition; and the construction of comprehensive economic and social networks.

-

2. Support business dynamism and inclusive labour markets through the diffusion of technology and innovation; the promotion of entrepreneurship, particularly for women and under-represented groups; effective competition policies and strong social protection systems that facilitate the creation and retention of quality jobs while enhancing resilience to the Future of Work.

-

3. Build efficient and responsive governments through integrated policy packages, whole of government responses and inclusive forms of policy-making that restore trust in public governance by fostering high levels of integrity and accountability.

The Framework for Policy Action builds on data, evidence and policy insights from a range of OECD strategies and projects, including the Productivity-Inclusiveness Nexus, the Jobs Strategy, Skills Strategy, Innovation Strategy, Going for Growth Strategy, the Going Digital project and the Green Growth project. Supported by a dashboard of 24 indicators to monitor progress over time on the key outcomes and drivers of inclusive growth, it is a non-prescriptive tool that can be applied in different contexts taking account of country-specificities and social preferences. The OECD is currently piloting the Framework for Policy Action through adapted country reviews.

Source: OECD (2018[1]), Opportunities for All: A Framework for Policy Action on Inclusive Growth, https://doi.org/10.1787/9789264301665-en.

Social protection

Social protection refers to policies aimed to prevent and reduce poverty, vulnerability and social exclusion throughout the lifecycle (UN DESA, 2018[5]; Mathers and Slater, 2014[2]). Social protection systems often provide benefits to individuals or households to guarantee income security and access to health care. Measures such as cash benefits, old-age pensions, in-kind transfers and disability benefits were instrumental in cushioning the impact of the global financial crisis among the most vulnerable, while serving as a macroeconomic stabiliser and enabling people to overcome social exclusion and poverty in both developed and developing countries (ILO, 2011[6]).

Social protection can also stimulate demand and boost consumption, and hence contribute to economic growth. During recessions, social protection spending can help revive economies and stimulate employment (UN DESA, 2018[5]).

Social protection instruments are commonly classified into three categories: 1) social assistance; 2) social insurance; and 3) labour market programmes. They vary in aspects of design, coverage and funding arrangements Box 1.2, which may have implications for their impact on growth and equality. This report focuses on social assistance and social insurance programmes directed at all lifecycle stages. It does not consider labour market programmes, which have a narrower target base but may also significantly affect inclusive growth, e.g. training schemes implemented as part of activation strategies to increase employability of the unemployed, or public works programmes targeted at long-term unemployed and other vulnerable groups. Other social policies, such as early childhood development (ECD), are also beyond the scope of this report.

Social assistance is defined as non-contributory social protection, usually financed through taxes and targeted at low-income households and vulnerable groups (UN DESA, 2018[5]). Examples include cash or in-kind social transfers, fee waivers, subsidies and child benefits, all of which are means tested. Cash transfers have proliferated, particularly in low- and middle-income countries; over 130 countries use direct, regular and non-contributory cash payments as income support and poverty reduction strategies central to their social protection systems (Bastagli et al., 2016[7]). It is estimated that, on average, countries spend 1-2% of gross domestic product on social assistance transfers (DFID, 2011[8]). These can be unconditional or conditional on school attendance, health or job requirements (Baird et al., 2013[9]). Social assistance schemes cover approximately 31% of the world’s population and have had a positive effect in reducing income inequality.

Social insurance refers to contributory programmes that protect against certain life contingencies through a risk-pooling insurance mechanism dependent on prior contributions (Mathers and Slater, 2014[2]). Old-age pensions are the most common example: employer and/or employee contributions consolidate pension funds, which finance retirement benefits. Currently, pension schemes receive contributions from 35% of the world’s labour force and provide benefits to 68% of the elderly (ILO, 2017[10]). Unemployment benefit programmes are another, less widespread example that target the working-age population. Social insurance programmes also provide a proven equalising effect which, in certain contexts, is greater than that of social assistance. In middle- and high-income countries where coverage is widespread, as in Eastern Europe and Central Asia, social insurance has reduced the Gini coefficient by 16%.

An increasing number of countries have consolidated social protection systems to tackle development challenges, especially under the 2030 Agenda framework, which recognises the right to social security (UN DESA, 2018[5]). However, only 45% of the world’s population is covered by at least one social protection benefit, and coverage varies widely by population group. Worldwide, 35% of children, 22% of the unemployed and 68% of the elderly benefit (ILO, 2017[10]). Although there is a long way to go to achieve the UN Sustainable Development Goal 1.3 to “implement nationally appropriate social protection systems and measures for all”, a number of developing countries in all regions are close to or have reached universal pension coverage.

Social protection coverage also varies across regions (Table 1.1). Social insurance varies from 4% of the population in sub-Saharan Africa to 47% in Europe and Central Asia. Social assistance has higher coverage than social insurance in most regions. The Middle East and North Africa region shows the largest difference: social assistance covers about 55% of the population, while social insurance covers 14%. In Europe and Central Asia, social assistance and insurance cover about the same share (47%).

Coverage also varies across income quintiles. Social assistance has higher coverage among poorer populations; social insurance has higher coverage among richer populations. For instance, in Latin America, social assistance covers 67% of the poorest and 10% of the richest quintiles, while social insurance covers 9% of the poorest and 40% of the richest quintiles. The nature and coverage of programmes matter to their influence, for instance, on inequalities (Box 1.2).

Linkages between social protection and inclusive growth

Numerous studies focus on how social protection can reduce poverty and vulnerability and enhance household welfare, but few investigate programmes’ potential impact on growth patterns. Social protection programmes can particularly affect the poor, as many low-income households are locked in poverty traps of low income, credit constraints and limited opportunities.

Economic development haves traditionally been seen as a trade-off between equity and efficiency. However, evidence strongly suggests that income inequality has a sizeable negative impact on economic growth, as it hinders investments in human capital (OECD, 2015[12]; ILO, 2011[6]). Consequently, social protection systems can also encourage growth. Past studies have already shown how social safety nets have the potential to overcome constraints on growth linked to market failures without eliminating, however, the trade-off between the dual objectives of equity and growth (Alderman and Yemtsov, 2013[13]; Alderman and Hoddinott, 2020[14]); Social accountability mechanisms matter for effective social protection as they contribute to improving both service delivery and state-citizen relations, as evidenced for instance by case studies in Ethiopia and Nepal (Ayliffe, 2018[15]; Schjødt, n.d.[16]).

Figure 1.1 summarises linkages and the three main channels through which social protection may affect inclusive growth:

-

Lift credit constraints and encourage investments. Social protection can alleviate credit constraints by facilitating access to bank loans and extending credit to low-income households.

-

Provide greater security and certainty. Social protection can help households cope with risks and protect their consumption and assets against adverse shocks, which leads to a more efficient use of resources.

-

Improve household resource allocation and dynamics. Social protection can affect household time and resource allocation, which has implications for income growth related to changes in intra-household bargaining power, investments in education or child labour, household labour allocation and migration decisions.

These channels may operate on three levels: 1) individual and household (micro); 2) community (meso); and 3) national (macro).

Note: (+) indicates an expected positive impact; (−) indicates an expected negative impact.

Source: Authors’ elaboration based on Barrientos and Scott (2008[13]), Social Transfers and Growth: A Review, and Mathers and Slater (2014[2]), Social Protection and Growth: Research Synthesis.

Micro linkages

Growth effect

At the individual and household level, social protection policies can a priori affect economic growth through five main effects: 1) accumulation of productive assets; 2) preventing the loss of productive capital; 3) stimulating innovation and entrepreneurship; 4) altering labour market participation and savings; and 5) stimulating investments in human capital such as education and health. While most effects are expected to have a positive impact on inclusive growth, the impact on labour force allocation is ambiguous and the impact on savings is a priori negative.

These elements are captured in the first two pillars of the OECD Framework for Policy Action on Inclusive Growth: 1) invest in people and places left behind, providing equal opportunities; and 2) support business dynamism and inclusive labour markets (OECD, 2018[18]). According to the first pillar, the key dynamics for governments and the private sector to sustain are promoting life-long learning and acquisition of skills, especially in relation to the future of work; increasing social mobility; improving health and enhancing access to affordable housing; promoting regional catch-up; and investing in communities’ well-being and social capital. As for the second pillar, the key dynamics for policies to catalyse are boosting productivity growth and business dynamism, while ensuring adaptation and diffusion of technologies across the board – in particular for small and young firms; achieving inclusive labour markets; and optimising natural resource management for sustainable growth.

Beyond social protection, potential policies for growth and inclusiveness include education and skills policies; labour market policies and employment protection; health policies; investment policies; taxes and transfers; territorial policies; structural and regulatory policies; data exchange, trade and competition policy enforcement; and policies supporting a low-carbon and resource-efficient economy (OECD, 2018[18]). In particular, social protection systems need to adapt to changes in family structures and living arrangements; health policies to address the wide range of social determinants of health inequalities and expand spending allocated to prevention targeted at key risk factors and population groups, especially for children; and labour market policies to coordinate with product market regulations to lower barriers to mobility of labour and reducing discrimination.

Social protection can enable low-income households to accumulate productive assets by increasing access to credit, supporting investments or facilitating assets accumulation directly (Mathers and Slater, 2014[2]). This increases consumption and enables investments in livelihoods (IEG, 2011[14]).

Social protection can have a positive direct impact on growth by preventing the loss of productive capital after a shock (Mathers and Slater, 2014[2]). By supplementing or increasing vulnerable households’ ability to cope with shocks, social protection programmes reduce the need to sell productive assets, such as livestock, or to adopt harmful coping mechanisms that deteriorate human capital, such as reducing food consumption or interrupting children’s education.

Social protection can foster economic growth by enabling innovation and entrepreneurship, as long-term and predictable income support unlocks innovation and risk taking for the vulnerable or poor, who otherwise could not afford potential failure (Mathers and Slater, 2014[2]). The certainty of future transfers, which guarantee consumption levels and protect productive assets, diversifies livelihoods and reallocates labour to more profitable activities (Alderman and Yemtsov, 2014[15]).

Social protection can affect growth through its direct impact on labour market participation and savings. The employment effect can be either positive by leading to better employment opportunities or negative by creating dependency and adverse incentives (Mathers and Slater, 2014[2]). For instance, in the short term, unemployment benefits tend to increase unemployment duration and spells, contributing to higher unemployment. However, unemployment benefits allow individuals to improve job search and find jobs that better match their skills and aspirations, ultimately leading to better labour market outcomes and attachment, and a reduced risk of falling back into unemployment. Whether or not social protection has a growth-inducing effect on labour supply depends on the design and type of programmes implemented. Some unconditional cash transfers, conditional cash transfers (CCTs) and food transfers in Brazil have been shown to facilitate better employment opportunities (ODI, 2011[16]), while free health provision in Mexico has created incentives for informality (Alderman and Yemtsov, 2014[15]). The effect on savings is a priori negative, as social protection reduces the need for precautionary savings.

Last, social protection can affect investments in human capital. Social assistance programmes often include conditions requiring human capital investments, such as sending children to school and visiting health clinics (Barrientos and Scott, 2008[13]). Even without conditionalities, social protection may spur investments in human capital through effects on liquidity constraints, a lead cause of underinvestment in human capital, especially among poorer households. Higher educational attainment is closely correlated with future labour market opportunities. Social protection investments that lead to human capital accumulation are therefore likely to spur growth outcomes.

Overall, social protection can be a determinant of growth at the individual and household level. However, despite their common aim, not all social protection programmes are expected to affect growth equally. Social protection investments cover a range of social insurance and assistance schemes with characteristics and design features that affect growth to varying degrees in various ways (Arjona, Ladaique and Pearson, 2001[17]).

Effect on inequality reduction

As social protection policies often aim to address poverty and vulnerability, they also have an effect on inequality. Tackling inequality is important, as it hinders poorer individuals and households from making investments in human capital, for instance, and reaching their full potential, which has negative impacts on individuals and the economy as a whole (OECD, 2015[12]).

Social protection programmes, particularly social assistance programmes, are often explicitly designed to reduce inequalities by promoting equal opportunities throughout the lifecycle (OECD, 2018[1]). Although their impact varies by design, adequacy and implementation, evidence shows that they can reduce inequalities (UN DESA, 2018[5]). At a micro level, social protection systems can reduce inequalities through two main complementary paths.

First, these programmes guarantee a minimum level of economic and social well-being, serving as safety nets for low-income and vulnerable households and individuals to mitigate the risk of poverty, and as spring boards that enable social mobility and help close inequality gaps (Ali, 2007[18]).

Second, social protection programmes can enable equal access to opportunities by overcoming the savings and credit constraints that prevent human capital investments and disruption of intergenerational poverty (Mathers and Slater, 2014[2]). For instance, by addressing demand-side barriers to nutritious food, health services and education (UN DESA, 2018[5]), programmes can contribute to lower rates of malnutrition and increased rates of school enrolment and attendance, thereby reducing opportunity inequalities. Social protection policies can also support higher educational attainment (Ali, 2007[18]), which improves productive capacity and employment prospects (UN DESA, 2018[5])and indirectly affects economic growth, as it enhances productivity and human capital (Mathers and Slater, 2014[2]).

Meso and macro linkages

Growth effect

Social protection can also affect growth outcomes at community and national levels. At the meso level, social protection investments can generate multiplier effects from increased local consumption and production, and enable accumulation of productive assets at the community level. The extent of these multiplier effects depends on the nature and size of the social protection transfers and their coverage (Mathers and Slater, 2014[2]). There may also be an inflation effect on local wages, as social protection programmes, particularly labour market programmes, can push up costs of labour.

At the macro level, social protection can have significant and broad effects on economic growth. It may increase aggregate household productivity and stimulate aggregate demand, particularly through counter-cyclical spending during economic downturns, thus increasing employment and revenue collection. However, a negative growth effect may also be expected through greater dependency and lower investment due to a decline in labour force participation and reduced savings. Indirect effects, such as facilitating economic reforms, building human capital, enhancing social cohesion and influencing fertility can further spur growth (Mathers and Slater, 2014[2]).

Effect on inequality reduction

Social protection can have sizeable effects on inequality at the meso and macro levels. Social protection policies can contribute to equal access to opportunities, reducing inequalities of outcomes (Ali, 2007[18]). Social protection programmes also contribute, to varying degrees, to reduced income inequality. Social protection systems worldwide reduced the Gini coefficient by 1.8% in 2016 (World Bank, 2018[11]). Moreover, by reducing inequalities, social protection schemes foster social cohesion and have a significant indirect positive impact on economic growth (Mathers and Slater, 2014[2]).

Although social protection can reduce inequalities, its redistributive effect depends on country context and programme type. Inequality reduction through social insurance, which does not explicitly target vulnerable groups, is seems highly dependent on the extent of coverage. In middle- and high-income countries, where coverage rates are high, social insurance has a significant effect on income inequality: in eastern Europe and Central Asia, the Gini coefficient fell by 16% due to investments in social insurance (UN DESA, 2018[5]). Social protection systems in low-income countries tend to be less extensive and have limited coverage due to informality and lack of financing. Because of low coverage, social assistance programmes in sub-Saharan Africa and East Asia have proven less effective in reducing inequalities (World Bank, 2018[11]).

Micro-level impacts of social protection on inclusive growth

The conceptual framework developed in this report shows that social protection investments have multiple micro-, meso- and macro-level effects on growth and inequality. Measuring these effects, however, is often a challenge. Key challenges include heterogeneity of social protection investments, multiplicity of possible effects that may cancel each other out, presence of endogeneity, the difficulty to measure some effects in traditional household surveys, in particular health outcomes that require specific health surveys or modules, and, concerning macro effects, scarcity of internationally comparable data on social protection investments by programme type.

This report adopts a careful approach, focusing on the micro determinants of inclusive growth that have a theoretical link with social protection investments and that can be measured in standard household surveys. It therefore consider only those more direct effects of social protection investments that are more straightforward to measure empirically in standard household surveys that are used for the empirical analysis. For this reasons, health outcomes, that are another major channel through which social protection can spur inclusive growth, are not covered in the empirical part of this report.

The measurement framework further identifies a number of micro determinants of inclusive growth, or outcome variables, that operate throughout the lifecycle and which are, in theory, likely to be influenced by social protection investments (Table 1.2). Outcomes of interest typically refer to education, early pregnancy, fertility, child labour, employment, migration, consumption and savings. Annex 2.A and Annex 3.A detail methodological approaches for social assistance and social insurance, respectively.

The choice of outcomes variables has a strong theoretical justification. The following section outlines the theoretical underpinning of the micro-level impact of social protection investments.

Social protection can support consumption and alter savings patterns

Adequate non-contributory, rights-based social assistance benefits can prevent major fluctuations in household income and smooth household consumption but have a negative impact on precautionary savings. They target vulnerable populations with a high marginal propensity to consume and lower ability to save. Social assistance programmes are therefore expected to have a positive impact on consumption and a neutral or slightly negative effect on saving (Kabeer and Waddington, 2015[19]). Any form of family allowance or child benefits may also negatively affect aggregate household saving, as they target young households that tend to save less than middle-aged ones (Cigno, Casolaro and Rosati, 2002[20]).

Likewise, social insurance is expected to erode precautionary savings and increase household consumption (Feldstein and Liebman, 2002[21]). An actuarially generous social insurance system (i.e. contributions are less than expected compensation) would further incentivise present consumption and disincentivise savings (Cigno, Casolaro and Rosati, 2002[20]; CBO, 1998[22]). The effects of pensions in particular are assumed to last throughout the lifecycle. At working age, when contributions are paid, pension wealth is accumulated and tends to crowd out voluntary retirement saving; at old age, when benefits are received, the limited impact of social risks (e.g. sickness) on household income reduces the need for precautionary savings (Mu and Du, 2017[23]).

Social protection appear to have mixed effects on labour supply

The effect of social assistance on labour supply may vary, depending on aim and targeted population. Cash transfers aimed to reduce poverty are often means tested and target working-age populations. They can reduce labour supply through two main channels: 1) a direct additional income effect that reduces the need to work; and 2) a tax effect as additional income from work becomes less rewarding in a system with progressive marginal tax rates.

The tax effect is likely to be stronger the higher the marginal tax rates (Borjas, 2005[24]). However, if the costs of looking for a job and household credit and liquidity constraints are taken into account, social assistance may have a positive effect on labour supply. Providing cash transfers to resource-poor households can free up time and allow a part of the transfer to be invested in job-seeking activities, improving employment opportunities. Programmes, such as social pensions, to support particularly vulnerable groups with less ability to work may reduce labour supply (due to, for instance, sickness or old age), which is both expected and desired.

Under social insurance, pensions are expected to affect labour supply negatively (Krueger and Meyer, 2002[25]), especially among low-skilled workers whose income replacement rates tend to be higher (Lalive and Parrotta, 2017[26]). Contributions act as an implicit tax on labour income and, as such, can disincentivise enrolment in a pension scheme and, after a certain age, accelerate retirement through a substitution effect (French and Jones, 2012[27]). However, actuarially fair pensions, which equalise at present value lifetime individual pension entitlements (pension wealth) to lifetime individual pension contributions, can encourage workers to postpone retirement, as they reduce disincentives to working beyond retirement age (OECD, 2017[28]). Pension wealth and retirement decisions also particularly depend on individual discount rates or myopia regarding future benefits (opportunity cost of delaying consumption). Individuals with low discount rates (i.e. whose future benefit increases outweigh current benefits foregone) are more prone to remain employed and postpone retirement. In turn, unemployment insurance is expected to raise the reservation wage and lengthen unemployment spells, thereby driving down employment, at least in the short term.

Social protection seems to improve education outcomes in poorer households

Social assistance can have a positive impact on education spending in a context of liquidity and credit constraints, as beneficiary households can afford to spend more on education. CCTs are likely to have a particularly strong effect on education outcomes, since they often focus on education and are conditional on school attendance (Bastagli et al., 2016[7]; Baird et al., 2013[9]). Social pensions, like old-age grants, are also expected to have a positive impact on education expenditure, as they enable three-generation households to overcome liquidity constraints through resource pooling (Bastagli et al., 2016[7]). While this report focuses on social protection programmes, ECD, which can be considered part of social welfare policies, has clear implications for education outcomes.

Theoretical expectations concerning contributory old-age pensions and education expenditures are less clear. From a macroeconomic perspective, population ageing increases the political power of older people, which could lead governments to shift public expenditures from education to pensions (Ono and Uchida, 2016[29]). Nonetheless, pay-as-you-go pension systems can incentivise the ageing working population to invest in public education, as they would reap more benefits from increased future productivity and the resulting higher income and tax contributions (Michailidis, Patxot and Solé, 2016[30]). From a microeconomic perspective, if receiving pensions and having children are considered alternative old-age insurance strategies, pension contributors would tend to invest little in child education (Meier and Wrede, 2005[31]; Mu and Du, 2017[23]). However, as parents are assumed to be altruistic and pensions reduce the need to save for retirement, underinvestment in the formation of children’s human capital is most likely to occur in liquidity- and credit-constrained households (Lambrecht, Michel and Vidal, 2005[32]; Mu and Du, 2017[23]).

Social protection can foster innovation and investments among the poor

Social protection benefits can play a significant role in lifting credit constraints and reducing risk aversion, which would encourage productive investments and adoption of innovative technologies (ILO, 2010[33]; Barrientos, 2012[34]; Covarrubias, Davis and Winters, 2012[35]). However, as wealthier people face lower barriers to investments, this applies mainly to the poor. Low-income households have a lower marginal propensity to save and invest; are disproportionately credit-constrained owing, in particular, to lack of collateral; and are, in addition, liquidity constrained. They may therefore favour occasional savings to cope with potential economic shocks at the expense of productive investments, and are less inclined to adopt technologies with high return but which involve more risk (Deaton, 1990[36]; ILO, 2010[33]; Barrientos, 2012[34]; Stoeffler, Mills and Premand, 2016[37]) . Social protection, particularly social assistance, that targets the poor and often involves cash transfers, can help households overcome risks and spur innovation, entrepreneurship and investments in, for instance, business activities.

Social protection tend to lower fertility rates

Fertility rates are a strong determinant of economic growth. While declining fertility slows growth through decreased labour supply (Prettner, Bloom and Strulik, 2012[38]), in developing countries with high fertility prevails, reduced fertility can spur economic growth (Ashraf, Weil and Wilde, 2013[39]).

Social protection can affect decisions about household composition, such as fertility. Conditional cash transfers, which are often targeted, very modest and not rights based and without limit to number of beneficiary children – are expected to reduce fertility. They are mostly paid to women and require periodic visits to medical centres, potentially empowering women’s family planning decisions and providing information and access to contraceptives (Bastagli et al., 2016[7]). Conditionalities also add a price effect to the income effect of the benefit, reducing the cost of education: if households substitute “quantity for quality” in their fertility decisions, CCTs could have a positive effect on human capital investments and a negative effect on the number of children (Simões and Soares, 2012[40]). Social assistance in the form of child-related benefits reduce the marginal cost of children and could have a positive effect on fertility, but the benefits would need to cover the high costs of bearing and raising children.

Mandatory social insurance and benefits could have a negative effect on fertility if children are considered part of the household old-age insurance strategy (Mu and Du, 2017[23]). Social insurance may also reduce fertility through its effects on access to contributory social insurance systems (OECD, 2017[41]). Social insurance is often earnings-related; children can affect permanence in the labour market, prospects of future earnings, and access and level of contribution to contributory insurance systems, such as pensions, acting as an implicit tax on childbearing (Cigno, Casolaro and Rosati, 2002[20]).

Social protection seems to have mixed effects on migration

Migration is another channel through which social protection can indirectly affect inclusive growth. With regard to social assistance, cash transfers can affect migration decisions directly, by providing the means for a household member to migrate internally or internationally, or indirectly, by providing collateral to obtain credit to finance migration. However, if transfers substitute for potential remittances from migrants, they may render migration unnecessary and reduce migration (Hagen-Zanker and Himmelstine, 2013[42]). Programme design matters as well. Recent evidence shows indeed that the impacts of cash transfers on domestic and international migration hinge on whether programmes were designed to implicitly or explicitly inhibiting or facilitating mobility (Adhikari and Gentilini, 2018[48]). Place-based programmes implicitly deter migration, in contrast with social assistance that is explicitly conditioned on spatial mobility or that contribute to relax liquidity constraints and reduce transaction costs thereby implicitly facilitating migration.

Social insurance effects on migration depends on the portability of benefits and contributions (Hagen-Zanker, Mosler Vidal and Sturge, 2017[43]). Benefits, particularly pension income, can be expected to reduce liquidity constraints and consequently facilitate financing of migration. However, the effect is neutralised if social insurance benefits have limited or no portability, i.e. the transfer could be lost when migrating, raising the costs of and disincentivising migration (Hagen-Zanker and Himmelstine, 2013[42]). In the absence of effective retirement provisions, savings derived from migration may also be seen as a substitute for formal pensions (Sana and Massey, 2000[44]).

Social protection programmes have a number of positive and negative effects on inclusive growth in theory; assessing their role in inclusive growth remains an empirical question. Subsequent chapters look at recent and new empirical evidence, drawing on an in-depth survey of the empirical literature and new empirical evidence from four countries at various stages of development: Brazil, Germany, Ghana and Indonesia.

References

[15] Alderman, H. and R. Yemtsov (2014), “How can safety nets contribute to economic growth?”, World Bank Economic Review, Vol. 28/1, Oxford University Press, Oxford, England, pp. 1-20, https://doi.org/10.1093/wber/lht011.

[18] Ali, I. (2007), “Inequality and the imperative for inclusive growth in Asia”, Asian Development Review, Vol. 24/2, Asian Development Bank, Mandaluyong, Philippines, pp. 1-16, http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.177.3089&rep=rep1&type=pdf.

[17] Arjona, R., M. Ladaique and M. Pearson (2001), “Growth, inequality and social protection”, OECD Labour Market and Social Policy Occasional Papers, No. 51, OECD Publishing, Paris, https://dx.doi.org/10.1787/121403540472.

[39] Ashraf, Q., D. Weil and J. Wilde (2013), “The effect of fertility reduction on economic growth”, Population and Development Review, Vol. 39/1, Wiley-Blackwell, Hoboken , NJ, pp. 97-130, https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1728-4457.2013.00575.x..

[9] Baird, S. et al. (2013), “Relative Effectiveness of Conditional and Unconditional Cash Transfers for Schooling Outcomes in Developing Countries: A Systematic Review”, No. 8, Campbell Systematic Reviews, The Campbell Collaboration, Oslo, https://doi.org/10.4073/csr.2013.8.

[34] Barrientos, A. (2012), Social transfers and growth: What do we know? What do we need to find out?, Elsevier Ltd., Amsterdam, https://doi.org/10.1016/j.worlddev.2011.05.012.

[13] Barrientos, A. and J. Scott (2008), “Social transfers and growth: A review”, Brooks World Poverty Institute Working Paper , No. 52, University of Manchester, Manchester, England, https://doi.org/10.2139/ssrn.1297185.

[7] Bastagli, F. et al. (2016), Cash Transfers: What Does The Evidence Say? A Rigorous Review of Programme Impact and of the Role of Design and Implementation Features, Overseas Development Institute, London, https://doi.org/10.13140/RG.2.2.29336.39687.

[24] Borjas, G. (2005), Labour Economics, 3rd Edition, McGraw-Hill/Irwin, New York, https://trove.nla.gov.au/work/6075113?q&sort=holdings+desc&_=1545299388611&versionId=35025818.

[22] CBO (1998), Social Security and Private Saving: A Review of the Empirical Evidence, Congressional Budget Office, Washington, DC, http://www.cbo.gov/publication/11011 (accessed on 13 November 2018).

[20] Cigno, A., L. Casolaro and F. Rosati (2002), “The impact of social security on saving and fertility in Germany”, Vol. 59/2, Mohr Siebeck GmbH & Co., Tübingen, Germany, pp. 189-211, https://doi.org/10.2307/40912996.

[35] Covarrubias, K., B. Davis and P. Winters (2012), “From protection to production: Productive impacts of the Malawi Social Cash Transfer scheme”, Journal of Development Effectiveness, Vol. 4/1, Taylor & Francis, Abingdon-on-Thames, England, pp. 50-77, https://doi.org/10.1080/19439342.2011.641995.

[36] Deaton, A. (1990), On risk, insurance, and intra-village consumption smoothing, Research Paper, Princeton University, Princeton, NJ, https://scholar.princeton.edu/deaton/publications/risk-insurance-and-intra-village-consumption-smoothing.

[8] DFID (2011), Cash Transfers Evidence Paper, Department for International Development, London, https://webarchive.nationalarchives.gov.uk/+/http:/www.dfid.gov.uk/Documents/publications1/cash-transfers-evidence-paper.pdf..

[21] Feldstein, M. and J. Liebman (2002), “Social security”, Handbook of Public Economics, Vol. 4, A. J. Auerbach and M. Feldstein (eds), North Holland Publishing Co., Amsterdam, pp. 2245-2324, http://www.elsevier.com/books/handbook-of-public-economics/auerbach/978-0-444-82315-1.

[27] French, E. and J. Jones (2012), “Public pensions and labor supply over the life cycle”, International Tax and Public Finance, Vol. 19/2, Springer US, New York City, NY, pp. 268-87, https://doi.org/10.1007/s10797-011-9184-x.

[42] Hagen-Zanker, J. and C. Himmelstine (2013), “What do we know about the impact of social protection programmes on the decision to migrate?”, Migration and Development, Vol. 2/1, Taylor & Francis, Abingdon-on-Thames, England, pp. 117-31, https://doi.org/10.1080/21632324.2013.778131.

[43] Hagen-Zanker, J., E. Mosler Vidal and G. Sturge (2017), Social protection, migration and the 2030 Agenda for Sustainable Development, Briefing paper, Overseas Development Institute, London, http://www.odi.org/publications/10822-social-protection-migration-and-2030-agenda-sustainable-development.

[14] IEG (2011), Evidence and Lessons Learned from Impact Evaluations on Social Safety Nets, Independent Evaluation Group, World Bank Group, Washington, DC, http://www.worldbank.org.

[10] ILO (2017), World Social Protection Report 2017- 19: Universal Social Protection to Achieve the Sustainable Development Goals, International Labour Organization, Geneva, Switzerland, http://www.ilo.org/global/publications/books/WCMS_604882/lang--en/index.htm.

[6] ILO (2011), Social Protection Floor for a Fair and Inclusive Globalization, International Labour Organization, Geneva, Switzerland, http://www.ilo.org/global/publications/ilo-bookstore/order-online/books/WCMS_165750/lang--en/index.htm.

[33] ILO (2010), Effects of Non-contributory Social Transfers in Developing Countries: A Compendium, International Labour Organization, Geneva, Switzerland, http://www.ilo.org/publns.

[19] Kabeer, N. and H. Waddington (2015), “Economic impacts of conditional cash transfer programmes: A systematic review and meta-analysis”, Journal of Development Effectiveness, Vol. 7/3,Taylor & Francis, Abingdon-on-Thames, England, https://doi.org/10.1080/19439342.2015.1068833.

[25] Krueger, A. and B. Meyer (2002), “Labor supply effect on social insurance”, in Auerbach and Feldstein (ed.), Handbook of Public Economics, North-Holland Publishing Co., Amsterdam, http://www.elsevier.com/books/handbook-of-public-economics/auerbach/978-0-444-82315-1 (accessed on 13 November 2018).

[26] Lalive, R. and P. Parrotta (2017), “How does pension eligibility affect labor supply in couples?”, Labour Economics, Vol. 46, Elsevier B.V, Amsterdam, pp. 177-88, https://doi.org/10.1016/j.labeco.2016.10.002.

[32] Lambrecht, S., P. Michel and J. Vidal (2005), “Public pensions and growth”, European Economic Review, Vol. 49, Elsevier B.V, Amsterdam, pp. 1261-81, https://doi.org/10.1016/j.euroecorev.2003.09.009.

[2] Mathers, N. and R. Slater (2014), Social Protection and Growth: Research Synthesis, Department of Foreign Affairs and Trade, Commonwealth of Australia, Canberra, https://dfat.gov.au/about-us/publications/Pages/social-protection-and-growth-research-synthesis.aspx (accessed on 19 September 2018).

[31] Meier, V. and M. Wrede (2005), “Pension, fertility and education”, Public Finance Working Paper 1521, Center for Economic Studies and Institute for Economic Research , Munich, Germany, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=812306 (accessed on 13 November 2018).

[30] Michailidis, G., C. Patxot and M. Solé (2016), “Do pensions foster education? An empirical perspective”, UB Economics Working Papers, Vol. 16/344, Universitat de Barcelona School of economics, Barcelona, Spain, https://doi.org/10.2139/ssrn.2791408.

[23] Mu, R. and Y. Du (2017), “Pension coverage for parents and educational investment in children: Evidence from urban China”, World Bank Economic Review, Vol. 31/2, Oxford University Press, Oxford, England, pp. 483-503, https://doi.org/10.1093/wber/lhv060.

[16] ODI (2011), Social protection in Brazil: Impacts on poverty, inequality and growth, Overseas Development Institute.

[1] OECD (2018), Opportunities for All: A Framework for Policy Action on Inclusive Growth, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264301665-en.

[28] OECD (2017), Pensions at a Glance 2017: OECD and G20 Indicators, OECD Publishing, Paris, https://dx.doi.org/10.1787/pension_glance-2017-en.

[41] OECD (2017), Social Protection in East Africa: Harnessing the Future, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264274228-en.

[12] OECD (2015), In It Together: Why Less Inequality Benefits All, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264235120-en.

[29] Ono, T. and Y. Uchida (2016), Pensions, education, and growth: A positive analysis, Elsevier Inc, Amsterdam, https://doi.org/10.1016/j.jmacro.2016.03.005.

[4] Ostry, J., A. Berg and C. Tsangarides (2014), Redistribution, Inequality, and Growth, International Monetary Fund, Washington, DC, http://www.imf.org/en/Publications/Staff-Discussion-Notes/Issues/2016/12/31/Redistribution-Inequality-and-Growth-41291.

[38] Prettner, K., D. Bloom and H. Strulik (2012), “Declining fertility and economic well-being: Do education and health ride to the rescue?”, Program on the Global Demography of Aging Working Paper Series, No. 84, Elsevier, B.V, Amsterdam, https://doi.org/10.1016/j.labeco.2012.07.001.

[44] Sana, M. and D. Massey (2000), “Seeking social security: An alternative motivation for Mexico-US migration”, International Migration, Vol. 38/5, Wiley-Blackwell, Hokoben, NJ, pp. 3-24, https://doi.org/10.1111/1468-2435.00125.

[40] Simões, P. and R. Soares (2012), “Efeitos do Programa Bolsa Família na fecundidade das beneficiárias”, Revista Brasileira de Economia: RBE, Vol. 66/4, Associação Brasileira de Estatística, São Paulo, pp. 533-56, https://doi.org/10.1590/S0034-71402012000400004.

[37] Stoeffler, Q., B. Mills and P. Premand (2016), “Poor households' productive investments of cash transfers Quasi-experimental evidence from Niger”, Policy Research Working Paper, Impact Evaluation Series, No. WPS 7839, World Bank Group, Washington, DC, http://econ.worldbank.org..

[5] UN DESA (2018), Promoting Inclusion through Social Protection: Report on the World Social Situation 2018, United Nations Department of Social and Economic Affairs, New York City, NY, https://www.un.org/development/desa/dspd/report-on-the-world-social-situation-rwss-social-policy-and-development-division/2018-2.html.

[3] UNDP (2017), Strategy for Inclusive and Sustainable Growth, United Nations Development Programme, New York City, NY, http://www.undp.org/content/dam/undp/library/Poverty%20Reduction/UNDPs%20Inclusive%20and%20Sustainable%20Growth-final.pdf.

[11] World Bank (2018), ASPIRE: The Atlas of Social Protection- Social Safety Net Expenditure Indicators (database), World Bank Group, Washington, DC, http://datatopics.worldbank.org/aspire/indicator/social-expenditure (accessed on 01 August 2018).