1. Digital tools and practices: SME access and uptake

The digitalisation of businesses has continued apace in recent years, but SMEs lag in thetransition, despite potentially tremendous benefits. The stake are high because the SME digital gap has proved to weigh down on productivity and to increase inequalities among people, firms and places. This chapter explores trends and patterns in SME digital uptake, and policies in place to support SMEs in adapting business practices. A first section analyses trends in diffusion across OECD countries prior to the COVID-19 crisis. A second section looks at the impact of the COVID-19 crisis on SME digital transformation, with early evidence and business cases. The last section considers how governments have intended, before and during the COVID-19 crisis, to support SMEs in going digital.

The digitalisation of businesses has continued apace in recent years. All sectors and firms of all sizes are increasingly equipping their staff with computer and Internet access, although smaller firms do so more slowly, and some sectors do so more quickly (e.g. construction, logistics or retail trade).

Digitalisation is multi-faceted, and involves the use and applications of a broad range of technologies, for different purposes.

In addition, there are complementarities in digital diffusion: The adoption of a technology A rises with the adoption of a technology B. This complementarity increases as firms grow in size and scale (increased elasticity), which can contribute to further enlarge digital divides, and exacerbate the risks of seeing the benefits of the digital transformation accruing to early adopters.

SMEs lag in digital adoption, in all technology areas, but tend to digitalise some business functions first: general administration and marketing operations. The digital gap is smaller between SMEs and large firms in their business-to-government interactions, in using electronic invoicing or social media, or in selling online.

SME gap in adoption increases when technologies become more sophisticated or mass matters for implementation. For instance, for enterprise resource planning software, a critical size is required to deal with the complexity and the significant amount of resources needed.

Micro-firms go under the radar, i.e. about 90% of the business population in OECD countries are not covered by international statistics on digital uptake by businesses.

Cross-industry differences in diffusion are marked. Some technologies are more relevant to digitalisation in some sectors, and more closely related to value creation in these sectors. For instance, high-speed broadband connection in accommodation and food services, or e-sales in the wholesale and retail trade. This advocates for adopting a differentiated policy approach towards SME digitalisation by industry but also business functions.

There has been a sharp increase in the digital uptake and online sales by SMEs since the beginning of the COVID-19 pandemic. As the crisis continues, those changes are poised to last, some investments being irreversible and the demonstration made.

There is a broad-based focus among OECD countries on accelerating digital innovation diffusion to SMEs. However, there is a large mix of approaches and, in some areas, diverging viewpoints on how to do so, considering the heterogeneity of the SME population and the diversity of their business ecosystems. While some countries seek to mainstream SME policy considerations in other policy agendas, others target SMEs with tailor-made instruments, often combined with place-based or sector-wide policy mixes.

Governments implement a mix of policy approaches: from technology support programmes, to skills development, to alternative sources of finance and Fintech, to improving SME capacity to manage and protect their data, or to adopt sound digital security practices, to promoting e-government as a lever of business adoption, to deploying high-quality infrastructure, and networking platforms and facilities, etc.

SMEs lag in the digital transition, despite potentially tremendous benefits to be reaped from new digital-enhanced tools, services and practices (OECD, 2019[1]). Digitalisation creates unprecedented opportunities for smaller businesses to overcome the size-related barriers they typically face in innovating, going global and growing (Box 1.1). As their size limits the scope for generating economies of scale, SMEs tend to rely on product differentiation and network and agglomeration effects to compete (OECD, 2019[1]).

Combined together, the Internet of Things (IoT), data analytics and cloud computing are likely to increase firms’ capacity for simulation, prototyping, decision making and automation (OECD, 2017[2]). IoT supports machine-to-machine communication and enables the generation of an unprecedented volume of data through the hyper-connectivity of devices, sensors and systems. Data analytics leverages machine learning and new algorithms for data exploration and market intelligence. Cloud computing allows storing and processing more information, at a more affordable cost. Emerging digital technologies can help reduce operation costs along the internal value chain of the firm and generate productivity gains, without additional mass (Chapter 5 on AI). Digital technologies can help increase SME capacity for product differentiation and market segmentation (ibid). They can also increase SME customer base and the firm’s regional and global reach through network effects (Chapter 3 on SMEs and digital platforms), or help reduce information asymmetry on markets (Chapter 4 on Blockchain ecosystems for SMEs).

Yet, SMEs lag the capacity to undertake this digital transformation. The smaller, the less likely a company is to adopt new digital business practices. The digital uptake is to a large extent still confined to basic services, and adoption gaps compared to large firms increase as technologies become more sophisticated (OECD, 2019[1]). Although the majority of businesses are connected, information and communication technologies (ICT) are still primarily seen as a communication tool. Having a website has become a common practice and using social media for business purposes is frequent. Firms performing data analytics are conversely less widespread.

SMEs must be better prepared for the digital transition. (Brynjolfsson and McElheran, 2016[3]) estimate that timing is essential as leading adopters of data analytics are receiving the biggest gains, while laggards that reach the frontier later tend to have lower net benefits, or not at all. Back in the early 1960s, the diffusion theory already introduced the idea of a threshold beyond which late adopters of an innovation might capture decreasing returns (in terms of market shares) as compared to earlier adopters (Rogers, 1962[4]). Business strategies that aim to move faster to commercialisation, through sometimes beta versions of products, also illustrate the existence of a first-mover (or second-mover) advantage. This is particularly true in sectors where network effects are important, and where early innovators can raise visibility, set industry standards, and increase user costs of switching to alternative models or branding (OECD, 2019[1]). The acceleration of technological change and innovation also contributes to widen gaps. Digital technologies in particular allow small differences in skill, effort or quality to yield large differences in returns, in part by increasing the size of the market that can be served by a single person or firm (OECD, 2015[5]).

The stakes are high, not only because SMEs make the most of the business and industrial fabric in most countries and regions, but also because they are strategic actors in large firms’ supply chains and play a key role in building inclusive and resilient societies. At an aggregate level, the SME digital gap has proved to weigh down on a country’s productivity performance and to contribute to increasing inequalities among individuals, firms, communities and places.

The COVID-19 outbreak is providing a striking example of the role SMEs play in ensuring resilience and sustainability, and how digitalisation can help them improve business processes and offer. Many SMEs have been experimenting with innovative forms of production and sales, often leveraging digitalisation to develop working methods that could help them cope with containment and social distancing measures (OECD, 2020[6]). Business surveys conducted worldwide since the beginning of the COVID-19 pandemic converge in highlighting a rapid uptake of teleworking and digital sales channels among SMEs, also signalling an acceleration in their digital transformation.

This chapter explores trends and patterns in SME digital uptake and policies in place to support SMEs in the transition. A first section analyses patterns and trends in digital technology diffusion across OECD countries prior to the COVID-19 crisis, with a focus on cross-country, cross-industry and cross-technology differences in diffusion, based on internationally comparable data and statistical analysis. A second section looks at the impact of the health and economic crisis on SME digital uptake and transition, with early evidence and business cases. The last section considers how governments have intended, before and during the COVID-19 crisis, to support SMEs in going digital.

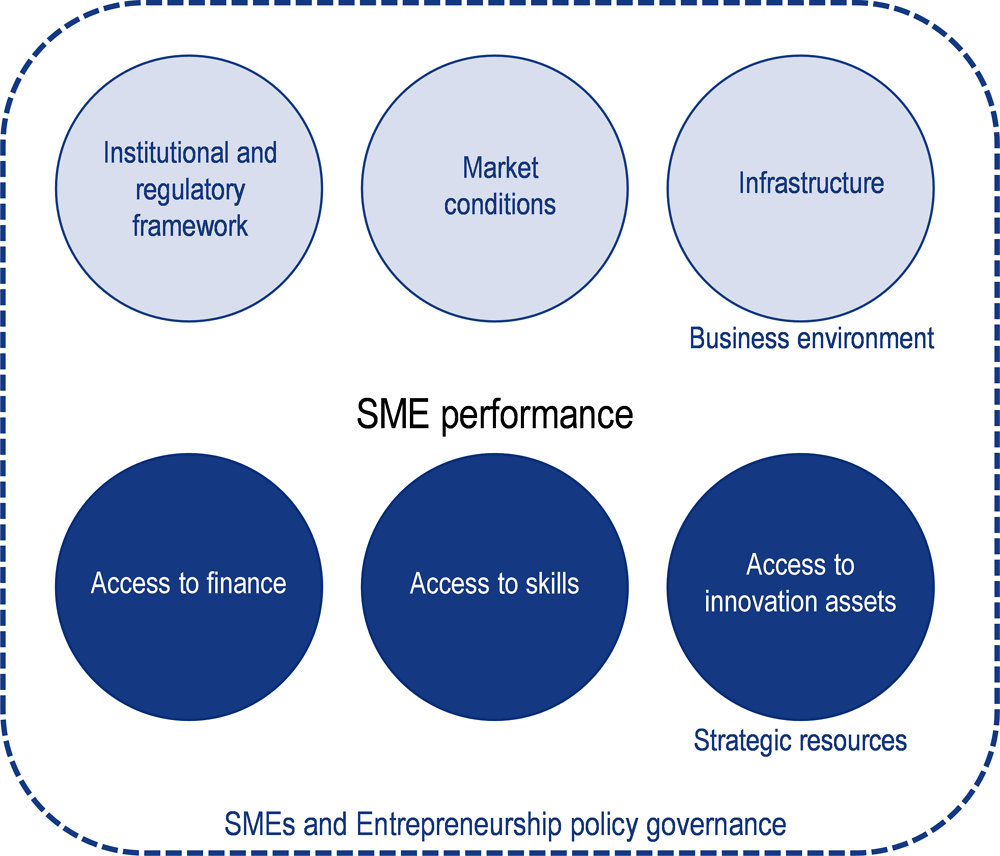

Digitalisation alters the business conditions under which SMEs do business and perform (Figure 1.1).

Source: OECD (2019[1]), OECD SME and Entrepreneurship Outlook 2019, OECD Publishing, Paris, https://dx.doi.org/10.1787/34907e9c-en.

Emerging technologies, such as big data analytics, artificial intelligence (AI), blockchain and 3D printing, enable greater product differentiation, better integration of supply chain systems and new business models that leverage shorter distance and time to markets, at the same time creating a better-informed and more differentiated demand that requires more flexibility and reactivity in supply. These changing market conditions are likely to benefit smaller and more responsive businesses. In fact, digitalisation has durably altered market conditions by reducing the efficient firm size. Digitalisation enables a reduction in transaction costs associated with market activities, i.e. access to information, communication and networking, reducing de facto incentives for firms to internalise such activities.

Digitalisation can also help SMEs integrate to global markets, as it reduces the costs associated with transport and border operations, increases the tradability of many services (where SMEs are majority), and reduces some hidden costs that fragmented global value chains (GVCs) raise (additional management, logistics and operations) (Contractor et al., 2010[7]).

Digitalisation changes conditions under which SMEs access strategic resources. It creates a range of innovative financial services for businesses that traditionally face greater difficulties in accessing finance. From peer-to-peer lending, to alternative risk assessment tools, to Initial Coin Offerings (ICOs) issuing crypto-assets, blended financing models are on the rise, Fintech becoming increasingly central in the SME finance landscape and established market players increasingly adopting Fintech instruments. Digitalisation also eases SME access to skills through job recruitment platforms, outsourcing and online task hiring, or by connecting them with knowledge partners.

Digitalisation supports open sourcing and open innovation, and greater access to innovation assets, such as technology itself, data or knowledge networks. For instance, multinational enterprises (MNEs), through their international production networks, have long served as “internalised” cross-border transmission channels for goods and services, financial flows, and intellectual property. They increasingly serve as vehicles for the diffusion of digital technologies globally (Gestrin and Staudt, 2018[8]). Several factors mediate the extent to which SMEs can translate collaboration with MNEs into productivity gains (OECD, 2016[9]), physical distance being one. Knowledge spill overs from MNEs are the strongest up to 10 km from the lead firm, and progressively decay, partly reflecting production linkages. Increased digitalisation may reduce the importance of distance.

Digitalisation is also transforming the institutional framework. E-government and online platforms are facilitating consultations and public service delivery to SMEs. Digital applications are already spreading across a broad range of areas, from business development services, to license systems, to tax compliance, to courts.

In parallel, greater data availability, combined with behavioural insights, is enabling governments to better adapt their services to user preferences, and creates room for policy experimentation (e.g. tax compliance by design), overall improving SME policy efficiency.

Source: OECD (2019[1]), OECD SME and Entrepreneurship Outlook 2019, OECD Publishing, Paris, https://dx.doi.org/10.1787/34907e9c-en.

Digital technologies diffuse quickly but differently across firms, countries and industries. This chapter explores patterns and trends in diffusion across OECD countries. It aims to identify SME gaps as compared to large firms, and better understand cross-country, cross-industry and cross-technology differences in diffusion. It intends to seize the connectivity gap and explore issues such as the degree of sophistication of digital technologies, industrial structure, or the co-diffusion of technologies.

The analysis is mainly data-driven and based on the most recent data on business use of ICT, drawn from the OECD ICT Access and Usage by Businesses Database and Eurostat database on the Digital Economy and Society (Eurostat, 2020[10]) (OECD, 2020[11]). These databases are the largest repositories of internationally comparable indicators on firms’ connectivity, uptake of digital technologies, and integration of ICT specialists. The dataset covers 45 European and OECD countries (plus Brazil), and data are available back to the early 2000s, depending on the indicators. However, the dataset presents some limitations that are specific to survey data, i.e. issue of comparability and coverage across countries with different surveys or collection systems, or the level of stratification that could be reached; for instance, data cannot be disaggregated at both firm-size and industry levels, or break in series, etc. (Box 1.2).

Trends and patterns as described in this section are anterior to the COVID-19 crisis.

Characteristics

The ICT Access and Usage by Businesses database provides access to a selection of 51 indicators, based on the second revision of the OECD Model Survey on ICT Access and Usage by Businesses. The survey was first launched in 2001 with a view to creating international standard metrics that capture digital uptake, and trends in digital tool adoption, from businesses of all sizes across OECD countries and sectors.

Core indicators are organised in nine categories: connectivity (A); websites (B); information management tools (C); e-commerce (D); digital security (E); e-government (F); use of cloud computing (G); ICT skills (H); and use of social media (I).

The indicators originate from two sources: 1) an OECD data collection (Australia, Brazil, Canada, Colombia, Japan, Korea, Mexico, New Zealand, Switzerland and the United States); and 2) Eurostat Statistics on Businesses for the OECD countries that are part of the European Statistical system. Survey data are collected through different means across countries. Most OECD countries (e.g. those abiding by the regulation of the European Statistical System) undertake the survey on annual basis, while a few do it on multi-annual or occasional basis, or collect essential data (e.g. e-commerce in the United States) by means of other surveys.

Statistics are computed as percentage values. Data are disaggregated by firm size or industry level. The stratification by firm size is based on the number of persons employed, in general using the following thresholds: 10 to 49 (small), 50 to 249 (medium), 250 and over (large). The stratification by industry is based on the International Standard Industrial Classification of All Economic Activities (ISIC Rev.4) at one digit.

Limitations in coverage and interpretation

Micro-enterprises (0-9) are not covered, since historically not included in the European regulation. International practice also tends to exclude agriculture (notable exceptions are Australia, Chile and New Zealand) and, in some cases, construction and personal services. Always excluded are the economic activities of households and the whole of the public administration, for which other types of survey are better suited. The European Statistical System (ESS) also excludes enterprises in the financial sector and in the past network industries (e.g. Electricity, Telecommunications).

Diffusion rates may vary substantially for one single country and one single technology, from one year to another, making comparisons over time difficult.

Data cannot support a cross-analysis of firm size and industry together.

Source: OECD (2020[11]), OECD ICT Access and Usage by Businesses Database, www.oecd.org/sti/ieconomy/ICT-Model-Survey-Usage-Businesses.pdf (accessed on 25 November 2020).

The digitalisation of businesses has continued apace

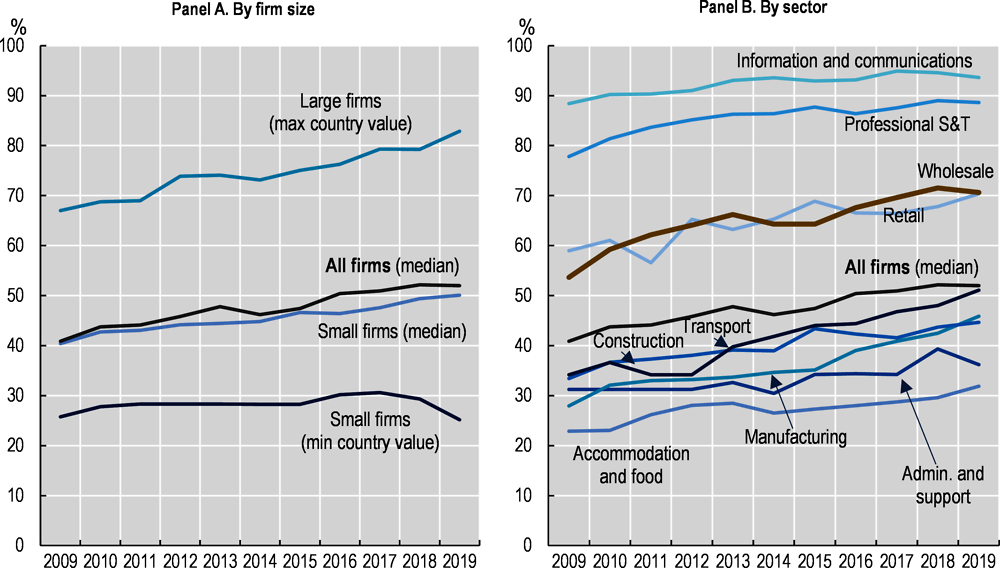

The digitalisation of businesses has continued apace in recent years, with wide country disparities (OECD, 2020[12]). A first exploration of ICT use data, drawing on the percentage of persons employed using a computer with an Internet connection, gives some insights on the extent -and speed - at which ICTs have been embedded throughout business activities (OECD, 2020[12]). The share of employees using computers with Internet access has significantly increased across OECD countries during the last decade (Figure 1.2). In 2019, the median share of connected employees in the area (all firms) was 52%, up from 41% in 2009. However, these numbers hide wide cross-country disparities, e.g. from 24.8% in Turkey to 81.7% in Sweden (2019).

Small and large firms alike increasingly equip their staff with computer and Internet access, but the smaller ones less rapidly. The median share of employees having access to a computer with an Internet connection in OECD countries has increased more slowly in firms with 10-49 employees than in the rest of the business population since 2009. In addition, small firms in lagging countries (Greece, Hungary, Poland, Portugal and Turkey at 40% or below) are at stall, while large firms in frontier countries (Denmark, Finland, Sweden at about 80% or above) have shown rapid progress over the period (Figure 1.2).

All sectors are also providing broader computer and Internet access to their staff, some quicker than others. In the most digital-intensive services, the deployment of computers with Internet connection is almost reaching a full completion. In 2019, a median of 93.6% of persons employed in information and communication services, and 88.6% of those employed in professional, scientific and technical services, have computer and Internet connection. Despite steady progress over the decade, the least digitalised sectors, i.e. administration and support services (median 36.2%) and accommodation and food services (31.8%), remain at the end of the tail. The use of computers and Internet has however taken off in construction (median 45.9%), transportation and storage (51.1%), and wholesale (70.6%) and retail trade (70.3%) services.

Note: Minimum, maximum and median country values take into account OECD countries for which minimum time series are available (excluding Iceland and Switzerland). Percentages by industry are median values. The drop observed between 2018 and 2019 in the minimum country share of employees with computers and Internet access in small firms is due to a decrease in numbers in Turkey. Turkey aside, the trend remains relatively stable, as in previous years.

Source: OECD calculations based on OECD (2020[11]), OECD ICT Access and Usage by Businesses Database, www.oecd.org/sti/ieconomy/ICT-Model-Survey-Usage-Businesses.pdf (accessed on 25 November 2020).

Digitalisation is multi-faceted

Digitalisation is multi-faceted. It involves the use and applications of a broad range of technologies, for different purposes, e.g. from enabling greater access to markets and end-users, to achieving greater integration of business processes, or to scaling up corporate IT capacity, etc. (OECD, 2014[13]) (OECD, 2019[1]) (Eurostat, 2020[14]).

Enterprise resource planning (ERP) systems enhance back-office efficiency and strategic planning. ERP systems are software-based tools for managing and integrating internal and external information flows, from material and human resources to finance, accounting and sales, and automates planning, inventory, purchasing and other business functions (OECD, 2014[13]) (OECD, 2017[15]; Andrews, Nicoletti and Timiliotis, 2018[16]).

Radio Frequency Identification (RFID) technologies help enhance efficiency in production and logistics. RFID technologies allow near-field communication and are used for product identification, person identification or access control, for monitoring and control of industrial production, supply chain and inventory tracking and tracing, for service and maintenance information management or for payment applications (e.g. highway tolls, passenger transport) (Eurostat, 2020[17]).

Customer Relationship Management (CRM) and Supply-Chain Management (SCM) software help enhance front-office integration and supply chain operations. CRM and SCM software are used for managing a company’s interactions with its customers, clients, prospects, employees and suppliers (OECD, 2014[13]) (Andrews, Nicoletti and Timiliotis, 2018[16]).

Cloud computing help enhance IT systems and capacity. Cloud computing (CC) refers to ICT services accessed over the Internet, including servers, storage, network components and software applications (OECD, 2014[13]). CC offers opportunities for SMEs to access online extra processing power or storage capacity, as well as databases and software, in quantities that suit and follow their needs. In addition to its flexibility and scalability, CC reduces costs of technology upgrading by exempting firms of upfront investments in hardware and regular expenses on maintenance, IT team and certification. In fact, higher adoption rates of cloud computing are associated with lower intensities of ICT investment in equipment, firms moving towards an ICT management model that is more based on software acquisition and digital connectivity (OECD, 2019[1]).

Big data analytics could find a broad range of applications within the firm, supporting efficiency gains in decision making and strategic planning, general administration, production, pre-production and logistics, or marketing, advertising and commercialisation (Chapter 5 on AI: Changing landscape for SMEs). Data analytics refers to the use of techniques, technologies and software tools for the analysis of vast amounts of data generated by activities carried out electronically and through machine-to-machine communications (OECD, 2014[13]; OECD, 2020[12]).

Social media help increase SME customer base, business visibility and outreach. Social media are primarily used for external interactions including developing the enterprises’ image and marketing products, as well as to obtain or respond to customers' opinions, reviews and questions (OECD, 2020[12]). Social media are also used to collaborate with business partners or to recruit employees.

E-commerce help SMEs increase customer and supplier base, and reach markets beyond traditional boundaries, in regions or abroad. E-commerce describes the sale or purchase of goods or services conducted over computer networks by methods designed specifically for the purpose of receiving or placing orders (i.e. webpages, extranet or electronic data interchange) (OECD, 2011[18]). E-booking and orders are more advanced forms of e-sales. E-commerce takes place through a range of different commercial relationships, involving any possible pairing of consumers (C), businesses (B) or governments (G) (OECD, 2019[19]). These include classical B2B transactions, which still account for the lion’s share of turnover resulting from private sector e-commerce, as well as business-to-government (B2G) transactions (e.g. government procurement). E-commerce transactions increasingly involve consumers directly, most notably business-to-consumer (B2C) transactions. Additionally, emerging business models involve consumer-to-business (C2B) and peer-to-peer relationships, which take place between two or more individuals.

B2G applications help cut the red tape and level the playing field in government-SME interactions, while providing SMEs with incentives for further technology adoption (see Section 3 on policy considerations).

Electronic invoicing supports compliance-by-design approaches and helps reinforce the integration of accounting systems and tax rules, ultimately alleviating administrative burden on SMEs. Electronic invoicing supports more secure chains of information between businesses and the public administration, and the deployment of pay-as-you-earn arrangements for business withholding and reporting to tax authorities (OECD, 2019[20]). E-invoicing systems allow for instance tax administrations to go beyond personal income tax returns and (fully) pre-fill corporate income tax and value-added tax returns.

High-speed broadband is a prerequisite for SME digital transformation. High-speed fixed broadband is defined herein as having download speed of at least 100Mbit/s (i.e. fibre). Adequate network access speed is essential to fully exploit existing services over the Internet and to foster the diffusion of new ones (OECD, 2017[21]). Differences in speed levels are important for customers. For example, high-speed broadband subscribers can download a high-quality movie (1.5 GB) in less than 22 minutes, while the same process takes at least 52 minutes for low-speed subscribers.

Some indicators of business ICT use can therefore be used to monitor more specifically the digitalisation of some SME business functions (Table 1.1).

SMEs have specific digital journeys

SMEs lag in digital technology adoption, in all digital technology areas. The gap in SME diffusion rates as compared to large firms is a recurrent feature across all technologies for which data are available (Figure 1.3). Small firms remain less digitalised than medium-sized firms, and medium-sized firms less than large firms. In fact, overall, diffusion patterns are relatively similar between small, medium-sized and large firms, the larger moving just faster along the diffusion curve (Rogers, 1962[4]).

SMEs tend to digitalise general administration and marketing operations first. There is comparatively little difference in the prevalence of B2G interactions between small, medium-sized or large firms (Figure 1.3). Adoption rates are higher among SMEs for social media or supply-customer management software. The gaps across firm sizes are also smaller when it turns to use electronic invoicing or participating in e-commerce (although diffusion rates for the latter are also smaller).

Note: Values represent the median of diffusion rates in countries for which data are available. Country diffusion rates are average rates calculated over the period 2015-18. This approach helps avoid distortions in time or in a single year, but may tend to underestimate the diffusion rates of technologies that are diffusing quicker.

Source: OECD calculations based on OECD (2020[11]), OECD ICT Access and Usage by Businesses Database, www.oecd.org/sti/ieconomy/ICT-Model-Survey-Usage-Businesses.pdf (accessed on 25 November 2020).

SMEs gap in adoption increases when technologies become more sophisticated or mass matters. Small firms are particularly less likely to use ERP systems than large firms. Firms adopt ERP systems when they reach a critical size that allows them to deal with the complexity and the significant amount of time, financial resources and reskilling required for ERP implementation (Andrews, Nicoletti and Timiliotis, 2018[16]). Consequently, the ERP diffusion gap is significantly larger between medium and small firms than between large and medium-sized firms. The reverse is true for SCM software or big data analytics for which the digital gap enlarges between medium and large firms. Conversely, large firms have invested more intensively in the integration of their business processes (ERP, CRM, SCM), tools for strategic planning, and tools for production and logistics management (RFID).

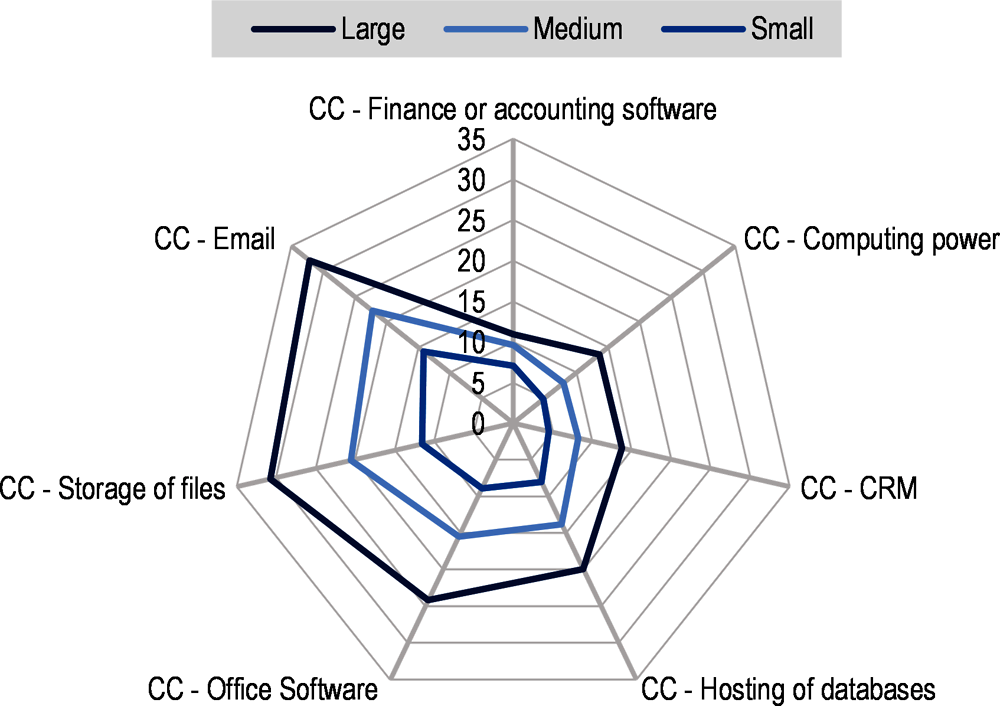

Large firms are consolidating their IT systems through external CC services. Overall, the first uses for which firms turn towards CC are email services and storage capacity, then accessing office software and hosting databases (OECD, 2017[22]). The same stands for small firms, as well as for medium-sized or large firms, but larger firms have been more proactive in externalising the development and maintenance of their IT systems than smaller firms (Figure 1.4).

Source: OECD calculations based on OECD (2020[11]), OECD ICT Access and Usage by Businesses Database, www.oecd.org/sti/ieconomy/ICT-Model-Survey-Usage-Businesses.pdf (accessed on 25 November 2020).

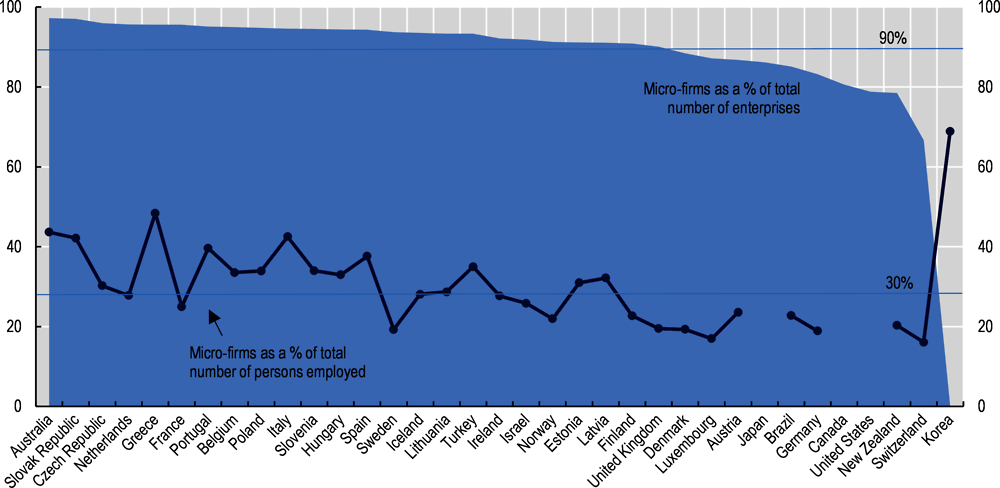

Micro-firms go under the radar

There is a lack of internationally comparable evidence on the digitalisation of micro-firms. Firms with less than 10 employees, as well as self-employed, are not covered by the OECD and Eurostat ICT Use by Business surveys (Box 1.2). Yet, micro firms account for over 90% of the total business population in most OECD countries (Figure 1.5). They employ on average one person out of three in the area (OECD, 2019[1]) and over 40% of total persons employed in Korea (68.8%), Greece (48.4%) Australia (43.6%), Italy (42.5%) or the Slovak Republic (42.1%) (OECD, 2020[23]).

Note: Total employment data for Japan, Canada and the United States are not available. The number of enterprises for Korea is not available either.

Source: OECD (2020[23]), OECD Structural Business Statistics (accessed 29 November 2020).

Anecdotal evidence points to a digitalisation process at play also within the micro firm population, although it remains difficult to seize its magnitude and to understand its specificities without comparable data. A 2015 private survey conducted on small businesses with less than five employees in Australia, Brazil, Canada, India, Turkey, the United Kingdom and the United States, showed that over half of businesses did not have a website, but some form of web presence through social media platforms.1 These businesses, in addition to being small by their employee payroll, were also small by their customer base, which limited the opportunity cost of having their own website. 22% had no online presence at all. A recent European Investment Bank survey underlines that less than 30% of micro firms have implemented at least one digital technology, as compared to around 80% of large firms (European Investment Bank, 2020[24]).

By extrapolation, trends on digital platforms can provide some insights on the digitalisation of micro-firms. Indeed, new forms of e-commerce supported by online platforms (e.g. Amazon) offer micro-firms an unprecedented opportunity to increase their customer base and outreach, create economies of scale through network effects, and access business intelligence services at low cost (see Chapter 3 on SMEs and digital platforms). More broadly, digital platforms can help micro-firms improve cost efficiency in a broad range of business functions, from marketing, to sourcing, to innovation, to financing, etc. Micro-firms could achieve a more rapid shift towards digital platforms and these new business models, as they tend to be more agile and flexible than larger organisations.

Noteworthy, in micro-firms, digital uptake relies heavily on his/her entrepreneurial orientation, innovative capacity (skills and awareness) and perception of potential risks and benefits. Therefore, the business owner/manager’s skills and his/her understanding of the benefits and implications of the digitalisation process could positively leverage digital uptake among micro-firms (Al-Awlaqi, Aamer and Habtoor, 2018[25]).

Technology supports further technology adoption

There are complementary dynamics in digital technology diffusion. Figure 1.6 represents the diffusion rates of CC, CRM, SCM, ERP and big data analytics by pair in each country for which data are available. Among small, medium-sized or large firms alike, the adoption of a technology A increases with the adoption of a technology B. The complementarity in diffusion is also likely to increase as firms grow in size and scale, as reflected by increasing elasticity between diffusion rates from one population to another.

Note: CC stands for cloud computing services; SCM stands for supply-chain management; CRM for customer relationship management, ERP for enterprise resource planning. The diffusion rate refers to the percentage of firms using this software in 2019. The lines suggest the elasticity between the diffusion rate of a technology A and the diffusion rate of a technology B.

Source: OECD (2020[26]), OECD Database on ICT Access and Usage by Businesses, http://stats.oecd.org/Index.aspx?DataSetCode=ICT_BUS (accessed 23 November 2020).

This technology complementarity could contribute to further enlarge digital divides, as smaller businesses are trapped into a vicious circle, and larger and more digital-savvy firms are more easily able to step up to new technology environment and digital practices. This complementarity also exacerbates the risks of seeing the benefits of the digital transformation accruing to early adopters.

Cross-country differences are significant in accessing infrastructure

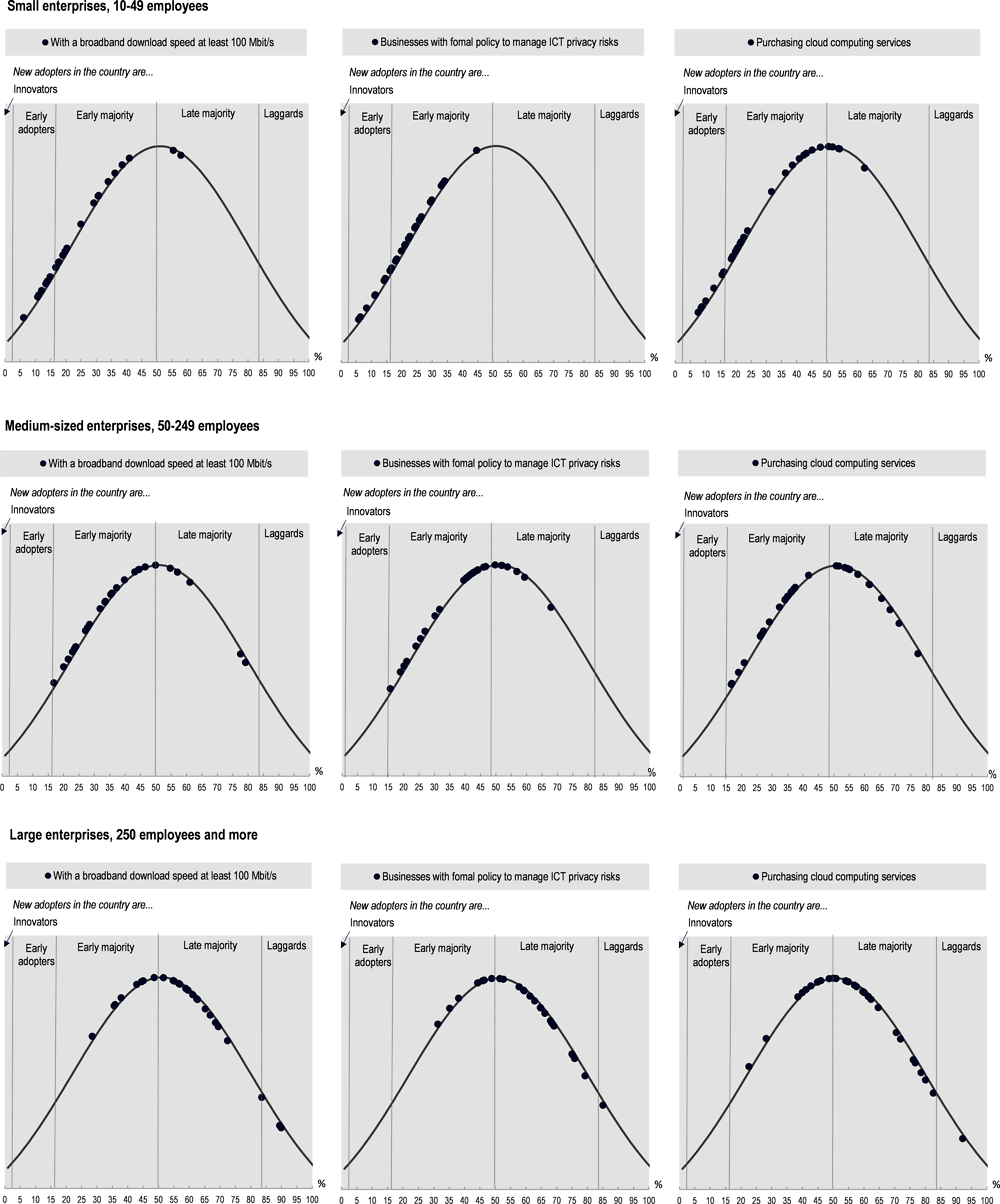

There are large cross-country differences in the way the business population accesses digital infrastructure and builds IT capacity (Figure 1.7). The literature suggests growing potential benefits in adoption by earlier adopters, and decreasing benefits after a majority of firms have moved to the new technology. Adoption rates and potential benefits could be represented as following a bell-shaped diffusion curve where first adopters are innovators, last adopters are laggards, and in-between, new adopters are early majority or late majority, according to the share of firms that have already implemented the technology. For instance, in Denmark and Sweden, more than half of small enterprises are connected to high-speed broadband, which makes new adopters a late majority, with potentially decreasing benefits. In France, Greece or Italy, they are hardly 10%, or even less, in this case, which makes them early adopters. Likewise, in Denmark and Sweden, new adopters among large firms are laggards, with almost 90% of large firms already connected in these two countries. As a comparison, in Greece, the Slovak Republic and Turkey, new adopters among large firms are early majority, with 35% or less of large firms connected. Overall, there are more small firms connected to high-speed broadband in Denmark and Sweden than large firms connected in Greece, the Slovak Republic and Turkey. The same stand where looking at digital security practices or the purchase of cloud computing services.

Cross-country differences in digital infrastructure have inevitably an impact on SME digital adoption, increasingly as emerging cloud-based solutions require quality digital network to transfer data and robust digital security practices to protect codes and systems (see Chapter 2 on SMEs and digital security) (Box 1.3).

The Building Workshop is an architecture and design firm located in Angus in the North Eastern part of Scotland. The Building Workshop is a family business, founded in 2009. Digital technology has been instrumental to business development since its inception. The use of building information modelling (BIM) software and a 3D model approach, as well as social media, cloud storage and video conferencing have been key to overcome the challenges related to the firm’s rural location. The Building Workshop now works on projects and services clients based in different areas across the United Kingdom, widening its potential customer base and allowing the firm to grow.

Limitations to doing and growing business were related to weak broadband connectivity in the area, sometimes requiring owners to physically relocate to a family home in the neighbourhood during working hours for accessing more reliable and stable broadband connection in order to back up data to the cloud.

Source: OECD Global Digital for SMEs Initiative (D4SME), Databank.

Note: Diffusion rates are the percentage of enterprises of a firm size class that use a particular technology. The diffusion rates of each country are plotted along a stylised diffusion curve that features higher potential benefits in adoption by earlier adopters. The thresholds between different categories of adopters are drawn from (Rogers, 1962[4]). Innovators are technology adopters that account for 2.5% of total business population. Early adopters account for an additional 13.5% of the total population, the early majority for additional 34%, the late majority for additional 34% and the latest 16% of adopters are laggards.

Source: Data are drawn from the OECD database on business ICT use and refer to 2019 or the latest year available OECD (2020[26]), OECD Database on ICT Access and Usage by Businesses, http://stats.oecd.org/Index.aspx?DataSetCode=ICT_BUS (accessed on 23 November 2020).

Cross-industry differences are even larger

Differences in digital diffusion seem more pronounced across industries than across firm sizes. While the patterns of digital diffusion remain relatively the same among small, medium-sized or large firms – the shape of diffusion charts are very similar in Figure 1.3 across the three firm size classes – cross-industry gaps emerge more prominent (Figure 1.8).

Note: ACC: accommodation and food services; ADM: administrative and support services; CON: construction; lNF: information and communication services; PRO: professional, scientific and technical services; MAN: manufacturing; RET: retail trade services; WHO: wholesale trade; TRA: transport and storage services.

Source: OECD (2020[26]), OECD Database on ICT Access and Usage by Businesses, http://stats.oecd.org/Index.aspx?DataSetCode=ICT_BUS (accessed 23 November 2020).

Firms in IT services have a more intensive use of all types of digital technologies, especially cloud computing, CRM and social media. The cloud computing is also more popular in professional scientific and technical services, construction, or administrative and support services. In manufacturing and wholesale trade, more firms are using ERP software. In the wholesale trade, CRM software as well.

A more in-depth analytical work was conducted with a view to identifying cross-country and cross-industry patterns in digital technology diffusion, also accounting for the great variety of digital technologies and transformations at play, and for the limitations in data (Box 1.2). It aims to identify the most relevant variables that summarise the variability of digital uptake at sectoral level and explore their link with value creation (Box 1.4).

Digital technologies diffuse differently across sectors. An analytical work was conducted with a view to identifying cross-industry patterns in digital technology diffusion, also accounting for the great variety of digital technologies and transformations at play, and for the limitations in data. The objective of the research was to identify the most relevant variables that summarise the variability of digital uptake at sectoral level and explore their link with value creation.

First, computing a principal component analysis (PCA) aimed to identify and select the variables, i.e. the one or two technologies that best capture overall variability in digital uptake at sector level, based on the OECD dataset of ICT use indicators. The work was conducted, along the nine categories of technologies, as defined in the database: connectivity (A); websites (B); information management tools (C); e-commerce (D); digital security (E); e-government (F); use of cloud computing (G); ICT skills (H); and use of social media (I). Were excluded the categories where the number of indicators was not technically sufficient to conduct a PCA.

The second step aims to study the link between digital uptake and an output production metric. (Carini et al., 2017[27]) and (Ilic, 2010[28]) identify the value-added as an efficient performance metrics. The creation of value at the sectoral level is proxied by the sectoral value-added rate, i.e. the sectoral value-added as a share of sectoral turnover (to control for size effect). Value-added and turnover data were drawn from OECD Structural Business Statistics (SDBS) databases. This second step consists in building a correlation matrix between these “best summarising” technologies, i.e. those that best explain cross-country cross-industry gaps in digital uptake, and the sectoral value-added.

Lastly, the analysis looks at possible complementarities between different digital tools, through simultaneous uptake, and of which technologies, and for which relative value creation.

Table 1.2 summarises the methodological steps.

Some similarities exist in digital diffusion across industries, and infrastructure is a key enabler. The results of the statistical analysis show that, regardless of the sector, there is a positive and significant correlation between sectoral value-added and (1) connectivity (2) the use of cloud computing services (3) ICT skill training and (4) the E-commerce.

Sectoral value added increases particularly with connectivity in the accommodation, administrative and support services, and manufacturing sector, and with CC adoption in the accommodation, real estate, retail and wholesale services sectors.

Sectoral value added increases with the training of ICT specialists in administrative and support services, construction and wholesale services.

In real estate sector, the training of both ICT and non-ICT specialists is relevant.

Beyond these preliminary commonalities, there are substantial sectoral differences in digital diffusion, pointing out different paths towards value-added creation. For instance, infrastructure appears to be positively linked to the value-added rate (i.e. value-added as a share of turnover). However, while high-speed broadband connections are highly relevant to value creation in accommodation and food services (0.4588), it is the use of portable devices that arises as prominent in the construction (0.4302), and administrative and support services (0.4347).

There are different uses of cloud computing software across sectors.

In the accommodation and food services sector, the purchase of cloud computing aims specifically to the storage of files, highlighting the importance of the mobility-enhancing features, e.g. out-of-office access to information, or regulatory compliance with consumer data. The sector is also characterised by an increasing availability of business-related data and the complementarity between cloud technologies and big data analytics. A similar trend is observed for the real estate sector (Mladenow, 2015[30]).

In the construction, transport and storage services, and wholesale sectors, cloud computing purchases target the hosting of databases. In the construction sector, this responds to the need for a greater transparency in data exchange between actors along the building process, and better control of the supply chain (McKinsey Global Institute, 2017[31]), as well to the need of optimising the management of assets (e.g. rental of construction equipment).

This section looks at the impact of the COVID-19 crisis on SME digital uptake, and exemplifies the speed of transformation with some SME business cases drawn from the databank of the OECD Global Digital for SMEs (D4SME) Initiative (OECD, 2020[32]) (Box 1.5).

Co-organised by the OECD and by Business at OECD, the OECD Digital for SMEs Global Initiative (D4SME) intends to promote knowledge sharing and learnings on how different types of SMEs can seize the benefits of digitalisation, and on the role of government, regulators, business sectors and other institutions in supporting SME digitalisation. The Initiative aims to promote knowledge sharing and learning on how to enable all SMEs to make the most of the digital shift, placing specific emphasis on the diverse opportunities and needs of the large “missing middle” of SMEs and entrepreneurs and on their role for an effective, inclusive and sustainable digital transition

The D4SME Initiative is a response to a call from Ministers and high-level representatives from over 50 countries and 12 international organisations at the OECD Ministerial Conference on Strengthening SMEs and Entrepreneurship for Productivity and Inclusive Growth (Mexico City, 22-23 February 2018). At the Conference, Ministers stressed the importance of “fostering conditions for SME adoption and diffusion of innovative and digital technologies, investment in complementary knowledge-based assets and digital security.” In particular, they asked the OECD to strengthen multi-stakeholder dialogue to inform policies that shape conducive framework conditions and remove obstacles to SME digitalisation.

Source: OECD (2020[32]), OECD Digital for SMEs Global Initiative, www.oecd.org/going-digital/sme/ (accessed on 29 November 2020).

The OECD Centre for Entrepreneurship, SMEs, Regions and Cities has monitored since February 2020 over 100 surveys conducted on SMEs in 31 countries.2 The surveys give insight into SME perspectives on the impact of the COVID-19 pandemic, their efforts to cope with that and their expectations for the future. Survey results differ across countries, reflecting the timing and severity of the COVID-19 pandemic and containment measures, but follow a comparable pattern. Insights on SME digitalisation from this work are provided below (OECD, Forthcoming[33]).

Up to 70% of SMEs are making more use of digital technologies due to COVID-19

The business surveys conducted in the course of 2020 worldwide document the increase in the uptake of digital technologies and online sales by SMEs from May 2020 onwards. Surveys show that since the start of the COVID-19 pandemic, up to 70% of SMEs are making more use of digital technologies, although substantial differences exist between countries. However, the difference between SMEs – and in particular small firms – and large firms continues to be significant, with the uptake of digital technologies by SMEs being only half of that by larger firms.

As the crisis continues, those changes are poised to become structural and last. Most investments will be irreversible. The crisis may have also served for demonstration effect.

A survey by the United States Chamber of Commerce (5 May) shows an acceleration in digitalisation trends. Over April-May, the share of small businesses transitioning some or all of their employees to teleworking increased from 12% to 20%, and small businesses that had begun moving the retail aspect of their business to digital means increased from 10% to 17%.3

A survey carried among 1 128 SMEs in Brazil (June) finds that almost 50% of them were more digitally enabled in June than before the COVID-19 pandemic. Improvements in customer relationships, as well as process agility and customer acquisition were cited as key benefits of digitisation by 55% of the SMEs surveyed, followed by the ability to operate remotely, cited by 53.5% of those polled.4

A study by CISCO (June) among SMEs in eight countries shows that 70% of SMEs are accelerating their digitalisation efforts because of COVID-19.5

A study by the Business Development Bank of Canada among 1 000 SMEs in the country (June) shows that 21% of small SMEs did not intend to make any change to their business practice, as compared to 4% of larger SMEs. 60% of SMEs would make telework a business practice, whereas 40% intended to consolidate their financial position and increase their investment in technology.6

A survey held in the United Kingdom by CEP/CBI on technology adoption in response to COVID-19 (July) shows that 75% of respondents had moved to remote working. In the period from late March to late July 2020, over 60% of firms adopted new digital technologies and management practices; and around a third invested in new digital capabilities. Nearly half of the respondents have introduced new products or services.7

Research by Sage on placing SMEs at the heart of the UK recovery (mid-July) indicates that 80% of SMEs think digital adoption will be critical for an enterprise-led recovery and job creation, but only a small proportion (33%) have the bandwidth to invest in technology across key business processes.8

A survey by Visa among SMEs in 8 countries (early August) indicates 67% have undertaken steps towards digitalisation. More than a quarter of SMEs have tried targeted advertising on social media or sold products or services online. Another 20% have adopted contactless payments and a third say they have accepted less, or stopped accepting, cash.9

A survey by GoDaddy among 5 265 small business owners in Australia, Canada, Germany, India, Mexico, Philippines, Spain, Turkey, the United Kingdom, and the US (19 August) highlights that 40% of respondents have a business website. Among owners that did have a website, more than half increased their online presence during the COVID-19 pandemic by adding content, creating an online store, and increasing digital marketing. American companies were most likely to handle their own tech needs at 66% compared to 54% globally. Only 19% of businesses report budgeting more money on building an online presence with 53% reporting that their online budget stayed the same.10

A survey by Allianz in Australia (27 August) reports that 20% of small businesses changed their policy completely during the COVID-19 pandemic, with 18% focusing on digitalisation.11

An American Express Small Business research survey (late August) shows that for 24% of surveyed businesses, online sales will account for at least half of their sales within the next year while 18 % say they already do. 39% of the businesses surveyed say the most helpful type of assistance they could receive to help run their businesses while COVID-19 is digital training.12

A survey by Hewlett Packard in several Asian-Pacific countries (early September) shows that where SMEs know digital adoption is very important to their recovery, they are currently focused on managing their cash flow (Hewlett Packard, 2020[34]).

According to a report on small business digitalisation by the Connected Commerce Council (10 September), 72% of small businesses have increased the use of digital tools during the COVID-19 pandemic. The report distinguishes between different types of SMEs. Digital Drivers (35%) consider digital tools essential and used these already before COVID-19. Digital Adopters use some digital tools but are not fully committed to digital. And Digital Maintainers are generally sceptical about the use of digital tools.13

A Salesforce survey in Spain (29 October) shows that, during the COVID-19 pandemic, SMEs have opted for digital marketing strategies that allow them to reach their customers through these new channels, despite the mobility restrictions. 7 out of 10 businesses in Spain have been digitised in response to COVID-19 pandemic, and digital marketing spending relative to total company budgets increased to 12.6% of company budgets on average from May, the highest recorded in the report, up from 11.3% in February).14

A study by Paypall among small businesses in Canada about how dramatically the COVID-19 pandemic has accelerated digital commerce for them (November) reports that 67% of small businesses accept now payments online and 47% of them only started doing so this year. Of all small businesses selling online, 34% turned to digital payments only after COVID-19 was declared a global pandemic in March. The majority of online small business owners (72%) believe e-commerce is now necessary in order to have a successful business. In fact, 69% of online small business owners said selling online has made them more successful, and without this possibility, 58% of small business owners said their business would not survive the COVID-19.15

A survey by Hewlett Packard to 1 600 businesses in Viet Nam and seven neighbour countries, Australia, India, Indonesia, Japan, Singapore, South Korea, and Thailand (16 November) shows that Vietnamese SMEs are the most optimistic in the Asia-Pacific region about the post-COVID-19 scenario. In Viet Nam, 41% of firms surveyed expect to see growth next year, against the regional ratio of only 16%, with 47% of them believing digital adoption held the key to post-pandemic growth.16

A survey by KOSGEB, the Turkish Small and Medium Enterprises Development Organisation, to SMEs (December) showed that 32.6% of respondents had already moved their business to the digital environment with the pandemic, and 21.8% of those which have not yet, plan to do so.

SMEs have transformed business operations in the most affected sectors

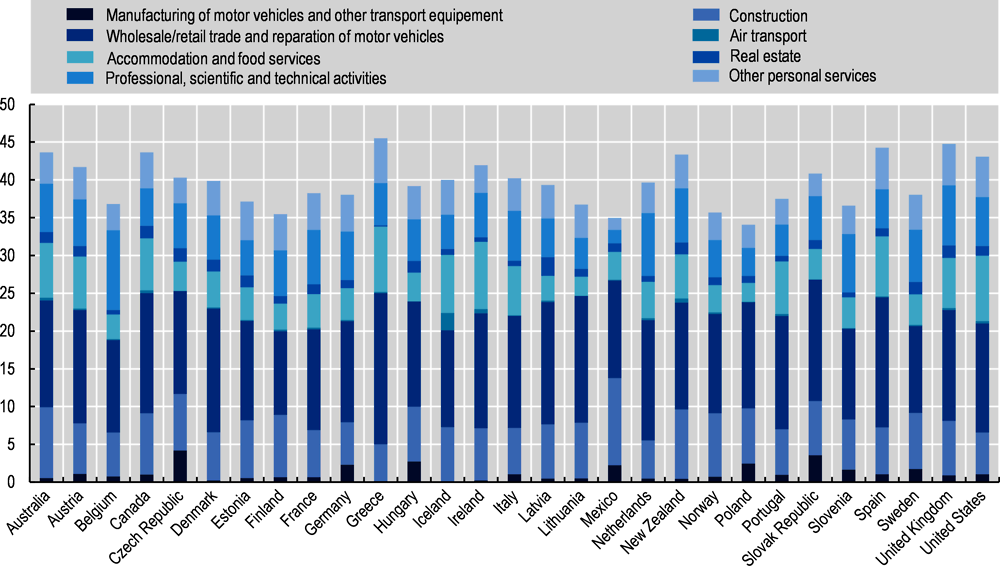

Most affected sectors by the COVID-19 pandemic are those where constraints regarding physical and social distancing, disruptions in supply chains, and interruptions of activities have been the hardest. These are also sectors where teleworking and smart working arrangements or digital solutions were less easy to implement. Overall, they account for 35-45% of total employment in OECD countries (Figure 1.9).

Note: Economic sectors are defined using the ISIC rev.4 classification: manufacturing of motor vehicles and other transport equipment (29-30); construction (41-43); wholesale/retail trade and repair of motor vehicles (45-47); air transport (51); accommodation and food service activities (55-56); real estate activities (68); professional, scientific and technical activities (69-75); arts, entertainment and recreation (90-93); and other service activities (94-96). The latter two are grouped together as other personal services in the Figure.

Source: OECD (2020[35]), Statistical Insights: Small, Medium and Vulnerable, www.oecd.org/sdd/business-stats/statistical-insights-small-medium-and-vulnerable.htm (accessed on 29 November 2020); OECD calculations based OECD Annual National Accounts database.

E-commerce has experienced simultaneous shocks in demand and supply. As people avoided crowds and malls, and retail stores closed doors, consumers have turned towards home delivery. E-sales have increased worldwide but unevenly across product lines, more orders being passed for food, essential consumer goods or home item and appliances (e.g. printers or fridges), while demand for traditionally top online sale products (e.g. clothing or electronics) was at half-mast. Conversely, sellers on digital marketplaces have shown unusual delivery delays or failed supplying, due to major disruptions in logistics chains and transport systems.

Circus bakery, a French SME, launched a retail website 24 hours after the closure of its sole shop. Its website offers delivery and “click & collect” services, enabling the bakery to continue operating during the crisis.

Five Way Cellars, an Australian wine & liquor retailer, launched its retail website in 2019, after 30 years in the industry, in order to complement the activities of its “brick and mortar” store. During the lockdown, it used this digital platform as its primary source of business. The brand has also engaged on social media (Instagram, Facebook) for the first time in order to promote its products and in an attempt to compete with larger distributors who are able to heavily discount prices.

Natoora, a UK wholesaler of fresh produce, has radically changed its business model from business-to-business (B2B) to business-to-consumer (B2C), because it could no longer sustain activities as a wholesaler to restaurants and businesses, many of which had to shut down due to containment restrictions. Using a newly launched website, the company has delivered its product to households and individual customers.

The leisure and entertainment industry has developed new markets in response to social distancing. Dancing, relaxation or cooking classes are moving online. Museums are putting forward their virtual reality tours (OECD, 2020[36]). Providers of video streaming services and Internet access have been boosting their subscriptions, proposing free access to on-demand TV or complimentary online services.

SkyTing Yoga is a New York based yoga studio. Earlier in 2020, the studio launched its digital platform, “SkyTing TV” as a complementary service. This has become its main source of revenue along with a new offering in which the firm streams classes via Instagram for a donation using the payment platform Venmo.

Boiler Room, the music production and events company, instead of cancelling 40 upcoming concerts have lived streaming the events via their internet platform from the artists’ homes and private spaces.

The e-banking and mobile payment industries have adapted to new market conditions, whereas businesses were forced to go online for selling, consumers and businesses looked for solutions to avoid contact with banknotes (some stores limiting payments to credit cards only), and the banking system intended to maintain cash access. Commercial banks have encouraged customers to use online and app-based banking services, eventually closing proximity agencies, while central banks in Korea, China (People’s Republic of) and the United States, quarantined physical bills.

E-learning services have spread widely. Education systems have massively moved to e-learning, as more than 900 million children and youth in more than 102 countries were locked down at home due to school closures (OECD, 2020[37]). Large universities cancelled in-person classes for shifting towards virtual training. In a very short time, digital-enabled approaches to learning have become a temporary alternative to traditional face-to-face methods. The digital turnaround has also affected business education services.

Smart working solutions have bloomed to tackle the almost-total disappearance of face-to-face and on-site business activities. The cancellation of trade shows, exhibitions and conferences has raised a major challenge for firms that use these B2B channels for building professional networks and getting new clients. This is especially true for smaller businesses that count more on word-of-mouth and reputation for networking, or in professional and consulting services, where on-site visits could be an essential part of the job. Some large digital firms, and SMEs as well, have been able to deploy a range of digital solutions. From voice and video calling, to teleconferencing to live-streaming webinars, to teleworking, examples include:

IBM hold its “Think 2020” client and developer conference and its “PartnerWorld” partnering conference as global digital events by combining live-streamed content, interactive sessions, certification, and locally hosted events.

Google changed its Cloud Next event to a digital-only conference this year.

Wolf PR, an Israeli media & advertising SME, has implemented a work-from-home policy for its team of 20 people. Whilst staff work remotely, employees use the teleconferencing platform Zoom to stay connected and the Microsoft Office cloud platform to share information.

Hylton and Company Realty, is a real-estate SME in the US. Much of the business was already digital, through a website that was the main point of contact for customers. To respond to the challenge of working from home, ‘open houses’ have been showcased online using cameras, virtual tours and drone videos to display properties.

At the extreme, some firms have radically changed their business models with the help of digital tools.

Older, an Italian textile SME producing uniforms for the hospitality industry, has responded to the decrease in demand by changing its business model in order to produce face masks. The company has been using its website and Instagram for processing orders.

Peppe’s Sydney, an Australian restaurant, has responded to the COVID-19 restrictions by changing its business model, from a fine dining restaurant, to a take-away service, using delivery platforms such as Uber Eats for the first time.

The SME digital lag arises from a range of factors and barriers, including SME lack of information and awareness, skills gaps, insufficient capital or missing complementary assets such as technology itself or organisational practices (OECD, 2019[1]). Smaller businesses often face more difficulties in adapting to changing regulatory frameworks, dealing with digital security and privacy issues or simply accessing quality digital infrastructure.

There is a broad-based focus among OECD countries on accelerating digital innovation diffusion to SMEs and ensuring they keep pace with the digital transformation (OECD, 2019[1]) (OECD, 2020[6]). However, there is a large mix of approaches and, in some areas, diverging viewpoints on how to unleash SME and entrepreneurs’ digital potential, and account for the great heterogeneity of the SME population and the diversity of their business ecosystems. While some countries have sought to mainstream SME policy considerations in other policy agendas, others specifically target SMEs with tailor-made instruments, often combined with place-based or sector-wide policy mixes.

Providing SMEs with technology support and assistance

Small enterprise owners are often unaware of the potential new digital tools could offer for improving their business or they consider the upfront costs of upgrading towards more sophisticated digital technologies as too high (OECD, 2017[38]).

Policy makers have been active in providing SMEs targeted financial support and technical assistance in conducting technology and problem-solving diagnosis, or implementing new e-business solutions, often in the form of small-scale and place-based initiatives. In some cases, financial and technical support is supplemented with training and guidance on the skillset and organisational changes that are required to support technological change (Table 1.4).

Government-funded technology extension programmes seek to expand the absorption and adaptation of existing technologies (e.g. equipment, new managerial skills) in firms, and to increase their absorptive capacity (Box 1.6). While this type of support is not new, the use of technology extension programmes that are targeted at SMEs has expanded over the last decades (Shapira, Youtie and Kay, 2011[39]).

Technology extension programmes typically start with an assessment of the firm’s operations and processes, followed by a proposed plan for improvement and implementation assistance. Key services include information provisions (e.g. to improve use of existing technologies, trends, best practices); benchmarking to identify areas for improvements; technical assistance and consulting; and training.

Technology extension services are often offered by networks of technical specialists (e.g. engineers) who proactively reach out to firms to organise visits and consultations. However, firms can also reach out for assistance to technology extension programmes.

This type of support is typically offered individually to interested firms, but may also be provided simultaneously to groups of firms with common needs. The first stages of review and diagnosis are generally free of charge, while more intensive projects often require co-financing by the firm, although at lower than market prices for consulting services.

As part of their responses to the COVID-19 crisis, governments have intensified efforts towards SME digitalisation, sometimes through new schemes, sometimes in reinforcing existing schemes. In addition, some had to adjust regulatory framework and legislation in order to create room for new working arrangements and business models to be deployed. Chile made changes to its Labour Code for regulating teleworking (OECD, 2020[6]).

Encouraging SME training and upskilling

SMEs typically have greater difficulty in attracting and retaining skilled employees than large firms because they tend to lack capacity and networks to identify and access talent, but more importantly, they tend to offer less attractive remuneration and working conditions (Eurofound, 2016[40]). SMEs also offer fewer training and development opportunities (OECD, 2013[41]), often due to the lack of internal training or Human Resources departments to organise and co-ordinate training, and lower levels of management skills to anticipate needs (OECD, 2015[42]). In addition, financial costs of tailored training are relatively higher for SMEs because they have less employees to distribute the fixed training costs over, and less scope to release people from revenue-generating activities for training. Furthermore, SMEs tend to experience higher job turnover, which constrains their capacity and willingness to invest in skills development when there is a risk that an upskilled employee will leave shortly after training (OECD, Forthcoming[43]).

Engaging SMEs in training and education

There are several types of policy initiatives that can be deployed to support the development of workforce skills in SMEs (OECD, 2012[44]), mainly focusing on reducing training costs for firms and promoting the benefits of workplace training.

Many OECD countries offer tax incentives to reduce the cost firms incur for training their employees. Training costs can be, partially or fully, deductible from annual corporate profits in the form of tax exemptions. Such schemes may specifically target smaller firms by offering them enhanced deductions. Smaller firms are also frequently targeted by direct training subsidies schemes. Training vouchers, for example, help SMEs purchase training hours from accredited individuals or institutions.

Countries aim to raise awareness of the importance of training and skills development in SMEs through various channels, including public and stakeholder organisations. An option is to leverage local employer networks to promote skills upgrading in the workplace. Employer networks and associations can foster trust-based relationships between firms that support knowledge-sharing and pooled investments in training. Collaborations across firms can also foster innovative diffusion within regional supply chains, potentially integrating firms into GVCs, which also reduces regional vulnerability to automation (OECD, 2018[45]).

Countries are also investing more in “brokers” or intermediator bodies such as group or collective training offices to organise training for groups of SMEs to shift the burden away from individual employers. These organisations often sign apprenticeship contracts with government while also providing pastoral care and practical assistance to individual apprentices (Box 1.7). They are particularly useful for SMEs who would not otherwise be able to meet the national minimum standards for training apprentices and upholding apprenticeship training quality standards.

Finally, regulation can encourage skills development. Some countries have introduced statutory rights for employees for training leave. However, their take-up is generally not high (less than 2% of employees benefitting from the measure).

Many OECD countries are examining the role of apprenticeship programmes as a means of better linking the education system to the world of work. Apprenticeship programmes combine both school-based education and the on-the job training and result in a formal qualification or certificate (OECD/ILO, 2017[46]) ]. Many SMEs use apprenticeship programmes because of their benefit in stimulating company productivity and profitability. In countries for which data are available, more than 50% of all apprentices work in companies with 50 employees or fewer (OECD, 2016[9]). Apprenticeships are more common in manufacturing, construction and engineering sectors, where employers (and often unions) are well represented and organised (Kuczera, 2017[47]).

Source: OECD/ILO (2017[46]), Engaging Employers in Apprenticeship Opportunities: Making It Happen Locally, OECD Publishing, Paris, https://doi.org/10.1787/9789264266681-en; OECD (2016[9]), Increasing Productivity in Small Traditional Enterprises: Programmes for Upgrading Managerial Skills and Practice; Kuczera (2017[47]), “Striking the right balance: Costs and benefits of apprenticeship”, OECD Education Working Papers, No. 153, OECD Publishing, Paris, https://doi.org/10.1787/995fff01-en.

Strengthening management skills in SMEs

Governments have several tools at their disposal to help build management skills in SMEs, ranging from the provision of digital diagnostic tools to help SMEs identify their management deficiencies, training and workshops, and more intensive approaches such as management coaching. Most programmes and initiatives tend to cover business strategy, operating models, process management, performance management, leadership, governance, agility, and innovation. An important component of management skills is financial planning and management (G20/OECD, 2015[48]). This includes the ability to conduct risk planning, and provide relevant financial information in business plans and investment projects.

One of the greatest challenges for governments is to create a demand for existing support services since many programmes have low take-up rates due to a lack of awareness of existing programmes; legitimacy issues around public support operators; doubts on the usefulness of the advice; and limited ambitions for business development and growth.

Leveraging Fintech and alternative sources of finance for SMEs

Across all stages of their life cycle, SMEs face structural barriers in accessing appropriate sources of finance that are critical to innovation and growth (OECD, 2019[1]). Internal barriers include a lack of collateral to be provided to funders and investors as guarantees, insufficient financial skills of small business owners and managers, and a lack of knowledge and awareness about funding options and alternatives. Market barriers include information asymmetries between financial institutions and the SME management, and relatively higher transaction and borrowing costs for funding institutions to serve SMEs. The above challenges are typically more pronounced in some segments of the business population, especially new firms, start-ups, and innovative ventures with high growth potential, in remote and rural areas, or in groups under-represented in entrepreneurship, such as women, youth, seniors and migrants (OECD/European Union, 2017[49])).

Online alternative finance activity has been increasingly included in SME finance policies (OECD, 2020[50]). Using technologies such as digital ID verification, distributed ledger technologies (DLT), big data and marketplace lending, finance suppliers are offering an array of innovative services with the potential to revolutionise SME finance markets. Mobile banking, (international) mobile payments and the use of alternative data for credit risk assessment can significantly reduce information asymmetries and transaction costs, tackling SME structural barriers in accessing finance.

Fintech, defined as technology-enabled innovation in financial services, is becoming more and more important in offering more convenient and accessible services, more effective credit risk assessments and lower transaction costs. These instruments can be a unique opportunity for projects that are too small, too risky, or have a social purpose (OECD, 2018[51]), and their strong expansion in particular in the early 2010s has prompted regulators to intervene.

In the context of the exercise to identify Effective Approaches for implementing the G20/OECD High Level Principles on SME Financing, a large majority of countries reported supporting the development of Fintech solutions (27 out of 38). Regulatory initiatives comprised 19 out of these 27 measures. In addition, platforms to inform and connect SMEs to Fintech companies, workshops and the creation of Fintech association were also mentioned (Koreen, Laboul and Smaini, 2018[52]).

The COVID-19 pandemic has provided further incentive to develop alternative sources of finance for SMEs and entrepreneurs. In Latvia and Mexico, Fintech initiatives are being implemented to support SME finance in the context of the crisis (OECD, 2020[6]).

Improving SME capacity to manage and protect their data and IPRs

SMEs tend to privilege trade secrecy as their default mode of data protection. Past surveys have showed that small firms consider trade secrecy as an important means for protecting innovation (Cohen, Nelson and Walsh, 2000[53]; Jankowski, 2012[54]; Hall et al., 2014[55]), with the lead time advantage -that is a primary mechanism of IP appropriation in some industries- and on-purpose complex product design -that aims to discourage competitors from engaging in counterfeiting (Rujan and Dussaux, 2017[56]; Hughes and Mina, 2011[57]). However, the protection of trade secrets is becoming increasingly difficult. Digitalisation and the revolution in data codification, storage and exchange (i.e. cloud computing, emails, USB drives) are prime drivers of a rise in trade secret infringements. Increasing value given to IP (and de facto its misappropriation), staff mobility and changing work culture and relationships (e.g. temporary contracts, outplacement, teleworking) or the fragmentation of global value chains (with more foreign parties involved within more diverse legal frameworks and uneven enforcement conditions) also contribute to increase exposure and risk of disclosure (Almeling, 2012[58]).

Trade secrecy is confidential business information that can cover new manufacturing processes, improved recipes, business plans or commercial information on whom to buy from and whom to sell to (e.g. customer list). Unlike patents, trade secrets are protected by law on confidential information, e.g. confidentiality agreement, or non-disclosure or covenant-not-compete clauses.

Trade secret popularity holds on its relative ease of use (due to low technicity and the absence of formal registration requirements), lower costs incurred for administration and the absence of definite term of protection. Trade secrets apply to a range of approaches used by SMEs and can help them capture the value of their innovations, reinforce strategies such as lead-time, product complexity and customer-driven innovation, or support innovation modes emphasising incremental change and open collaboration (Brant and Lohse, 2014[59]).

In fact, trade secrecy and patents complement each other. Trade secret law “plugs several holes in the patent statute” (Friedman, Landes and Posner, 1991[60]) and both offer SMEs distinct tools for a comprehensive IP protection. Trade secrets are more likely to be used (often without patents) for process innovation and for innovations in services (where SMEs are majority) while patents are more likely to be used (alone or in combination with trade secrets) when the innovative product is a physical good (EUIPO, 2017[61]). Trade secrets can also be more suitable for inventions that do not meet the criteria for patentability, especially in profitability terms and at the early stages of product development. On the downward side, trade secret law is more difficult to enforce than a patent; it does not protect from fair discovery or reverse engineering and the secret is lost when disclosed. Also, trade secret laws are set within national legal frameworks limiting transnational knowledge transfers.

Source: Brant and Lohse (2014[59]), “Trade Secrets: Tools for Innovation and Collaboration”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.2501262; Friedman, Landes and Posner (1991[60]), “Some Economics of Trade Secret Law”, Journal of Economic Perspectives, https://doi.org/10.1257/jep.5.1.61; EUIPO (2017[61]), Protecting Innovation Through Trade Secrets and Patents: Determinants for European Union firms, https://euipo.europa.eu/tunnel-web/secure/webdav/guest/document_library/observatory/ documents/reports/Trade%20Secrets%20Report_en.pdf.

SME data protection is being reinforced while efforts are made to harmonise legislation across jurisdictions and help smaller firms navigate through different regulatory frameworks. Trade secrets have been the subject of increased domestic and international policy attention and trade secret laws have been strengthened in Europe and the United States.

The European Trade Secrets Directive aims to standardise existing and diverging national laws against the unlawful acquisition, disclosure and use of trade secrets (European Commission, 2016[62]). The Directive was brought into force in 2018 in order to enable companies to exploit and share their trade secrets with privileged business partners across the Internal Market. For instance, registering trade secrets on the blockchain could be considered as a “reasonable step (…) to keep [the information] secret”.

The US Defend Trade Secrets Act 2016 aims to strengthen trade secrecy protection. It creates federal civil cause of action and provides a choice between treating localised disputes under state laws or treating disputes under federal law (US Patent and Trademark Office, 2017[63]). Courts can protect trade secrets by enjoining misappropriation, ordering parties that have misappropriated a trade secret to take steps to maintain its secrecy, or ordering payment of royalties, award damages, court costs and attorneys' fees.

The European Union is also engaging reforms of intellectual property rights (IPRs) laws as part of its package of measures for creating a Digital Single Market. The Copyright Reform aims in particular at more cross-border access to content online, wider opportunities to use copyrighted materials in education, research and cultural heritage and a better functioning copyright marketplace. The planned Unitary Patent will offer uniform protection in up to 26 EU member states, and enact for patent holders an alternative pathway to the existing European and national patent systems, a centralised procedure at the European Patent Office (EPO) and a uniform litigation system (Unified Patent Court) that is poised to increase legal certainty at reduced costs.