Chapter 5. Reset the financial system in line with long-term climate risks and opportunities

There is an urgent need to mobilise all sources of private finance to scale up and shift infrastructure investment towards low-emission, resilient projects. An array of rules governing the financial system favours the status quo and stands in the way of the necessary reallocation of capital. Decision-making processes are distorted by inadequate climate risk pricing, capabilities and biased incentives in the investment value chain. This chapter reviews the barriers linked to a radical reallocation of capital to low-emission, resilient infrastructure, and proposes three priority actions to scale up and shift investment at scale: integrate climate impacts in investment decisions and strategies, increase transparency and disclosure of climate-related risks and opportunities in financial markets, and bolster the role of financial supervisory authorities to ensure a stable and sustainable financial system.

There is an urgent need to mobilise all sources of private finance to scale up and shift infrastructure investment towards low-emission, resilient projects. An array of rules governing the financial system favours the status quo and stands in the way of the necessary reallocation of capital. Decision-making processes are distorted by inadequate climate risk pricing, capabilities and biased incentives in the investment value chain. The following actions will help move sustainable finance from momentum to transformation:

-

Encourage the integration of climate impact into investment decisions and strategies to improve climate-risk management strategies.

-

Incentivise the disclosure of climate-related risks and opportunities for investors to increase transparency in financial markets.

-

Support financial supervisory authority to better assess and manage climate-related risks that could threaten the financial stability of the system in the short and long term.

Why is resetting the financial system transformative?

Infrastructure worldwide has suffered from chronic underinvestment for decades, and current global investments fall short on delivering the services needed for sustainable development. Significant levels of infrastructure investment are needed to maintain and upgrade ageing infrastructure, particularly in high-income countries, as well as to support development and the achievement of the Sustainable Development Goals (SDGs) in developing economies. All sources of finance – public and private – need to be mobilised.

The OECD report Investing in Climate, Investing in Growth estimates that USD 6.9 trillion of investment in infrastructure is required annually on average between 2016 and 2030 to meet development and climate needs globally (OECD, 2017[1]). Current spending falls short of this figure; it amounts to only USD 3.3-4.4 trillion dollars annually. Two-thirds of the required infrastructure investments are expected to take place in developing and emerging economies (New Climate Economy, 2016[2]). The additional costs of investing in low-emission, resilient infrastructure are offset by potential fuel savings, and are marginal compared to other infrastructure cost drivers (e.g. corruption levels, efficiency of infrastructure delivery). Developments in low-emission technologies and in the digital economy could actually reduce the demand for infrastructure, and make many low-emission, resilient infrastructure investments cheaper than traditional infrastructure systems.

Making infrastructure compatible with a low-emission, resilient future is therefore not more expensive, but it does require a significant reallocation of capital away from fossil fuel-intensive activities towards infrastructure projects supporting low-emission and resilient energy, transport, land-use and urban systems.

Given the considerable need for long-term infrastructure investment, all sources of finance need to be mobilised. Countries need to improve the efficiency of public investment while mobilising private investment at scale and at pace. Innovative financial instruments, supported by digitalisation, can create new opportunities for diversification of financing sources. They can also help align public and private sector interests in infrastructure provision and management, while optimising the capital structure and reducing the cost of capital for the public sector (OECD, 2017[3]).

What is the state of play?

There is some progress in incentivising private investment in sustainable, low-emission and resilient infrastructure. Carbon pricing policies and targeted incentives to change the relative prices, risks and returns of low-emission, resilient projects have induced visible and dramatic changes in the energy sector. The falling costs of some renewable energy technologies mean that they are now competitive with emissions-intensive alternatives. Many innovative financing mechanisms have been implemented to blend public finance, limit the risk for private actors, and subsidise and incentivise private lending, investments and insurance. For instance, the green bond market increased from just USD 3 billion in 2011 to USD 163 billion in 2018, or to USD 895 billion when including climate-aligned bonds (Climate Bonds Initiative, 2018[4]). International financial institutions are also increasingly using their balance sheets to leverage private capital, alongside measures to de-risk investments by providing capacity building in countries (see Chapter 6).

There is increasing momentum for change in the financial system, with a growing number of initiatives to harness finance to drive the low-emission transition (Maimbo et al., 2017[5]; UNEP Inquiry, 2018[6]). Globally, the number of sustainable finance measures doubled between the end of 2013 and the end of 2017, and international initiatives to promote sustainable finance have quadrupled (UNEP Inquiry, 2018[7]). Notable examples include the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD) and the G20’s Sustainable Finance Study Group and Sustainable Insurance Forum (SIF).

However, available indicators show that progress has been patchy and incremental. Overall, infrastructure financing levels remained stable between 2010 and 2016. Institutional investments in low-emission infrastructure are a fraction of the assets under management by institutional investors – amounting to USD 84 trillion in OECD countries. Looking just at large pension funds surveyed by the OECD, direct equity investment in unlisted infrastructure projects of all types accounted for only 1% of their asset allocation in 2015, and green infrastructure accounted for only a fraction of that 1% (OECD, 2017[8]).

The failure to align private investment with a well-below 2°C pathway creates risks for the financial system and the global economy as a whole. In the financial system, investments in emission-intensive projects risk becoming stranded assets in a future with net-zero emissions, or vulnerable to physical damage from climate change and weather-related events. For the global economy, continued investment in assets that are incompatible with well-below 2°C pathways could put the climate objectives of the Paris Agreement out of reach.

What are the opportunities and barriers for change?

Governments have a central role to play in steering financial markets towards better pricing of climate-related risks and opportunities. It is essential that countries improve the overall business and investment environment and develop strong and stable climate policy frameworks to orient their economy away from emissions-intensive activities and level the playing field between low- and high-emission alternatives. However, these changes on their own are not enough (see Chapter 1). It is also essential for investors to have a number of de-risking financial tools and instruments at their disposal, such as public guarantees or blended finance mechanisms proposed by development finance institutions (see Chapter 6). A number of obstacles embedded in current financial systems and regulations are preventing the re-allocation of finance to long-term low-emission infrastructure investments at the pace and scale needed.

The way climate risks and opportunities are managed, disclosed and mitigated in financial systems remains a key obstacle to developing better risk management strategies. The following are key barriers to a better pricing of climate-related risks and opportunities (UNEP Inquiry, 2015[9]; Maimbo et al., 2017[5]; UN Environment, 2018[10]):

-

Risk pricing: Risk pricing is currently disconnected from climate-related factors, since the financial system lacks comparable climate-related data and metrics; clear standards and definitions of low-emission, resilient infrastructure; and a financial data or a detailed track record on the financial performance of low-emission, resilient infrastructure projects.

-

Capabilities: Investors tend to invest in what is familiar to them. Climate-related capabilities need to be enhanced to better handle decision making under uncertainty all along the investment value chain and to break behavioural biases.

-

Biased incentives: Incentives, institutional norms and regulations that still favour short-termism and the status quo need to be shifted to increase the rate of adoption of low-emission technologies and infrastructure projects.

Now is the time to capitalise on the growing momentum to transform the financial sector, but these barriers must be overcome. It is necessary to break the silos between climate and finance communities to fix incentives, capabilities and climate risk pricing, and embark on local, national and international initiatives that aim to mobilise long-term investment on the one hand, and shift investment towards sustainable infrastructure on the other (see Box 5.1). This collaboration is a necessary condition to create the financial system needed for development in line with climate goals.

Over the past decade institutional investors, such as pension funds, insurers and sovereign wealth funds, have been looking for new sources of long-term, inflation-protected returns. Increasing numbers of institutional investors are recognising the potential for infrastructure investment to deliver inflation-linked, long-term and stable cash flows. A growing number of investors are also concerned with the potential impact of climate change on their long-term financial performance, and have begun integrating environmental, social and governance considerations into their investment processes. But long-term investors approaching infrastructure face an “information gap”, and improved data and information are necessary through the following actions:

1. Mapping finance and risk allocation in infrastructure

-

Map investment and financing channels for sustainable infrastructure.

-

List instruments and levels of public financial support.

-

Create a database of stock and flows of infrastructure projects.

For instance, the OECD-led Research Collaborative on Tracking Private Climate Finance monitors flows of private and public climate finance in an effort to measure the extent to which current financial flows are aligned with the goals of the Paris Agreement.

2. Defining the investment characteristics of infrastructure as an asset class

-

Promote a definition of sustainable and quality infrastructure to facilitate data collection on performance and sustainability.

-

Promote standardisation and harmonisation of project documentation and disclosure.

-

Support initiatives to create infrastructure benchmarks.

The G20 has catalysed efforts to address the information gap. In 2014, for example, the G20 launched the Global Infrastructure Hub (GIH), which aims to provide the private sector with free information about government infrastructure projects. However, to date the GIH has failed to collect data related to the sustainability and the climate impacts of infrastructure projects, contributing to the ‘silos’ within the G20 process and at the national level. These silos are the result of a lack of communication between communities involved, on the one hand, in infrastructure and finance and, on the other, in sustainability.

3. Mobilising private sector investment in developing countries

-

Define measurements and criteria to assess the impact of initiatives that leverage private sector capital in low-emission infrastructure.

-

Measure governments’ instruments and techniques to attract private sector refinancing in low-emission infrastructure.

-

Promote the setting of objectives for using national and multilateral development banks’ balance sheets to catalyse investment (see Chapter 6).

Source: OECD (2017[3]), Breaking Silos: Actions to Develop Infrastructure as an Asset Class and Address the Information Gap; OECD (2017[1]), Investing in Climate, Investing in Growth.

5.1. Encourage the integration of climate impacts into investment decisions and strategies

Given the growing threats from climate change, understanding, quantifying and actively managing business exposure to climate-related risks should be an important part of risk management practices in companies’ activities and investors’ portfolios. There are some encouraging signals from investors that a transition towards more sustainable investments is under way. Many investors have started implementing a variety of measures to adapt their investments to climate risks and benefit from climate-related opportunities (Ang and Copeland, 2018[11]), including:

-

Environmental, social and governance (ESG) integration with a strong emphasis on climate change. For instance, investors representing over USD 70 trillion have become signatories to the UN Principles of Responsible Investment (UN PRI[12]).

-

Thematic investment, which refers to investment in thematic funds that are aligned with a low-emission transition, or directly in assets.

-

Best-in-class climate investing, which only targets investment in the best performing companies within each sector or industry.

-

Exclusionary screening in the due diligence process, which blacklists sectors or companies based on their carbon footprint. For instance, the Powering Past Coal Alliance brings together over 60 national and regional governments, as well as businesses and organisations, who have collectively agreed to phase out existing coal power and place a moratorium on any new traditional coal power stations without carbon capture and storage (UNFCCC, 2017[13]; Government of Canada, 2018[14]).

-

Divestment, which is the action of selling off subsidiary business interest or investments because of climate risks (Baron and Fischer, 2015[15]). In 2016, total divestment from fossil fuels represented USD 5 trillion across 76 countries (Arabella Advisors, 2016[16]).

-

Active ownership, in which equity investors use their ownership stake in a company to influence its decision making.

There are still many uncertainties over the impact of such strategies on aggregate levels of funding. Investment strategies such as best-in-class investing, exclusionary screening or divestment may not necessarily translate into lower investment in emissions-intensive assets, as other financiers may still finance them. Active ownership may contribute more directly to mitigation objectives and have a clearer impact on the real economy (see Box 5.2).

“A 4°C world is not insurable.” – Thomas Buberl, CEO of AXA

Insurance companies are at the forefront of the thinking on how to integrate climate-related risks and opportunities in investment decisions.

At COP 21 in 2015, AXA committed to divesting EUR 500 million from the coal industry. At the One Planet Summit in December 2017, it introduced a policy to stop insuring new coal construction projects or businesses, and pipelines associated with the extraction of tar sands. It increased its divestment objectives to EUR 700 million from oil sands producers and EUR 2.4 billion from the coal industry. It also announced that by 2020 it would seek to increase its green investments from its 2015 goal of EUR 3 billion to EUR 12 billion. In co-operation with the International Finance Corporation (IFC), AXA has launched a USD 500 million facility supporting climate-related infrastructure projects in emerging economies.

The Allianz Group has also made divestment from coal a central part of its climate action. The group withdrew from insuring coal-fired power plants as well as planned and operating coal mines. Its goal is to phase out all investment and insurance coverage of coal companies by 2040. As of November 2018, the group had divested EUR 265 million in equities and EUR 4.8 billion in run-off assets. Like AXA, it currently targets energy and mining companies with 30% or more of their revenues derived from coal, and it will reduce the threshold by 5% increments to reach 0% by 2040.

Limiting insurance coverage, divestment and green investments are important tools at insurers’ disposal to take action on climate change, but they can also share their expertise and help companies prepare for a future with lower emissions. AXA, for example, engages directly with companies in key industries such as oil and gas (e.g. BP, Eni, Royal Dutch Shell, Lukoil), utilities (e.g. EDF, GDF Suez, RWE, E. ON), mining (e.g. Rio Tinto, Glencore Xstrata, BHP Billiton) and automotive manufacturing (e.g. BMW, Renault, Toyota, Volkswagen). It encourages them to improve disclosure of climate-related risks and develop strategies to manage the global transition towards a low-emission, resilient future.

Source: AXA (2018[17]), “Active engagement: Initiatives 2017/18”, AXA website, 3 April 2018; AXA (2017[18]), Integrated Report 2017; Allianz (2018[19]), “Allianz is driving change toward a low-carbon economy with an ambitious climate change package”, Allianz website, 4 May 2018.

Mainstreaming climate considerations in investment decisions and strategies across the entire financial system requires action on different fronts: enhancing market transparency; developing benchmarks and metrics of success; valuing risk in the financial system; mapping investments; and harnessing digital finance.

Enhancing market transparency and improving data

Enhancing greater market transparency and improving data on performance, risks and costs and opportunities of low-emission and resilient investments across available channels is essential for promoting sustainable infrastructure as an asset class and leveraging long-term investment (OECD, 2017[3]). The deployment of blockchain technologies could help enable this transparency, provided that the right regulations are in place (see Box 5.3).

A number of digital innovations are emerging in the infrastructure space, which offer the potential to transform how physical systems operate by making infrastructure more connected, intelligent and efficient, including blockchain. Blockchain is one of such technologies that can be used for record keeping, automation of processes and transactions, and transferring value through cryptocurrencies or tokens without requiring a central entity to validate transactions.

When thinking about blockchain, carbon neutrality is not the first thing that comes to mind and there are concerns around the technology’s CO2 impacts as vast amounts of energy are required to sustain the network. However, blockchain can also help fight climate change. It can help unlock new sources of financing, serve as a clean energy trading platform, and address key issues along the infrastructure value chain:

-

Greater contractual and financial standardisation during the bidding and procurement stages of infrastructure projects can reduce costs and complexity, facilitate comparability of projects, and help financial allocations by investors.

-

Enhanced data availability, transparency, privacy and quality can support well-informed investment decisions. Coupled with Artificial Intelligence (AI) technologies for example, blockchain can improve data analytics of infrastructure systems and provide global visibility over climate actions, help track climate financing flows, and encourage greater alignment of these flows.

-

Better data on the identification, measurement and management in investment risks can improve risk mitigation.

Some concrete applications of blockchain technologies can help progress towards the goals of the Paris Agreement. For example, as a decentralised financing infrastructure, blockchain-based platforms can enable a wide spectrum of investors to invest directly in low-emission projects. Blockchain can also improve the way emissions trading systems work, by strengthening data transparency and reliability (e.g. on quotas and certificates circulation) and by automating transactions and price discovery. Contract management systems that rely on blockchain can also be applied to keep track of the validity of legally-binding contracts in infrastructure projects, which is particularly appealing with multi-party contract agreements.

However, blockchain’s ultimate impact will depend on the ability of governments to develop the right policies to extract its potential benefits and mitigate environmental impacts, while also addressing risks and potential for misuse. Several areas are calling for greater attention:

-

Encouraging collaboration and innovation: Governments, international organisations, such as the United Nations Framework Convention on Climate Change (UNFCCC), technology providers and academia could form dedicated working groups to support the development of technical standards related to blockchain technologies, building on existing industry alliances.

-

Supporting education: More research and outreach on blockchain could be supported to develop low-emission related solutions, raise awareness on the technology (e.g. energy consumption, scalability drawbacks), help overcome knowledge gaps, and encourage greater trust in incorporating the technology into current systems.

-

Mitigating environmental impacts: Governments need to engage with industry to ensure that the protocols and network designs they develop are as energy efficient as possible, and green applications of blockchain technologies (e.g. in energy, transport, trade and agriculture sectors) are playing their role in the low-emission transition.

-

Ensuring supportive regulatory environments: The regulations that apply to blockchain technologies vary from country to country, and because of the distributed nature of networks, many legal questions are still open. For example, issues related to liability, intellectual property or data privacy are yet to be resolved, and call for careful government attention.

Source: OECD (2018[22]), Blockchain, infrastructure and the low-emission transition (forthcoming), Financing Climate Futures Case Studies.

Developing benchmarks and metrics of success

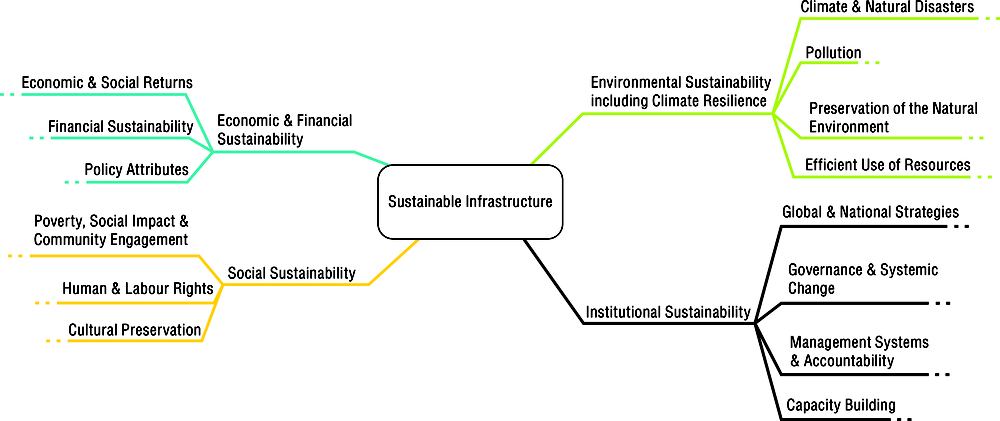

Developing benchmarks and metrics of success could facilitate due diligence of low-emission infrastructure and asset allocation modelling (OECD, 2015[20]) and measure performance to feed into the asset allocation process. Establishing a harmonised definition of sustainable infrastructure could be essential to ensure consistency of data collection and help harmonise project preparation. For example, this could be done through SOURCE, an online platform developed by the multilateral development banks (MDBs) to present sustainable, bankable and investor-ready infrastructure projects and improve project preparation.

In 2017, G7 world leaders endorsed the Ise-Shima principles for promoting quality infrastructure investment, and encouraged all actors in the value chain to align their infrastructure investment and assistance with the principles. Building on these principles, the Inter-American Development Bank (IDB) developed a framework for sustainable infrastructure to attempt to harmonise existing definitions of sustainable infrastructure (see Figure 5.1).

Source: IDB (2018[21]), What is Sustainable Infrastructure? A Framework to Guide Sustainability Across the Project Cycle.

Valuing risk in the financial system

Ensuring that investors take climate-related risks and opportunities into account is a critical step in shifting financial flows. This will require a range of interventions to value risks, including broadening concepts of risk and the time horizons over which they are assessed, embedding climate considerations into incentive structures and the key performance indicators of financial decision makers, and mainstreaming related concepts into professional education programmes. Regulators have a key role to play in this regard (see Section 5.3).

Mapping investors channels

Improving the understanding of how financial policies and regulations affect low-emission, resilient infrastructure investment patterns is key. This includes developing better classification systems for financial measures, effective frameworks to measure impact, and enhanced understanding of the transferability of measures across countries at different stages of development and with different financial systems (UNEP Inquiry, 2018[7]).

Harnessing digital finance

Harnessing the new opportunities created by digital finance could also transform the infrastructure investment value chain, enable citizens to participate more directly in investment and unlock new sources of finance for infrastructure. Chapter 3 has already discussed the example of the M-Akiba retail bond issued by the Government of Kenya, which offers Kenyan citizens the opportunity to invest directly in new and ongoing infrastructure development projects through their mobile phones (see Chapter 3).

5.2. Encourage the disclosure of climate-related risks and opportunities in financial markets

There is a growing awareness that inadequate disclosure of climate-related risks and opportunities can lead to a mispricing of assets and capital. For instance, investors with some fossil fuel assets might not be able to recover their investment fully due to more stringent climate regulations, but this is not properly accounted for in financial actors’ allocation decisions. Three types of climate-related risks could inflict potential losses on investors, and eventually challenge the stability of the financial system (Carney, 2018[23]):

-

Physical risks related to the increased frequency and severity of climate- and weather-related events could damage property and disrupt trade (see Chapter 1). There is growing evidence suggesting that developing countries vulnerable to climate change are experiencing a higher sovereign cost of debt due to climate factors, and that this might increase in the future (Buhr et al., 2018[24]).

-

Liability risks arising if those suffering from climate change losses seek compensation from those they hold responsible. For instance in October 2018 a court in The Hague upheld a historic legal order urging the Dutch government to accelerate carbon emissions cuts (Nelsen, 2015[25]).

-

Transition risks caused by the revaluation of assets in a lower-emission economy. Building more fossil fuel dependent infrastructure will result in stranded assets, defined as assets that are “unable to recover their investment cost as intended, with a loss of value for investors” (Baron and Fischer, 2015[15]). This risk is particularly acute for investors that are closely linked to coal mining or energy production from coal.

Inadequate disclosure could also hide some opportunities to invest in profitable projects created by the low-emission transition. The International Finance Corporation (IFC) estimates that the Paris Agreement could help open up nearly USD 23 trillion in opportunities for low-emission, resilient investments in emerging markets between now and 2030 (IFC, 2016[26]). Such opportunities range from green buildings in East Asia (USD 16 trillion), sustainable transport in Latin America (USD 2.6 trillion), renewables in the Middle East and North Africa, climate-resilient infrastructure in South Asia (USD 2.2 trillion), clean energy in Africa (USD 783 billion) and energy efficiency and transport in Eastern Europe (USD 665 billion) (IFC, 2016[26]).

Measuring and disclosing adequate climate-related information is a first step in making markets more efficient and economies more resilient. Private investors and governments alike can make better decisions with improved transparency and access to information on the climate-related performance and exposure of assets and businesses, as well as financial systems as a whole. In fact, not disclosing climate-related financial information would amount to knowingly excluding key information on risk factors that would lead to mispricing, biased investment decisions and suboptimal investment outcomes.

Many investors and corporations are actively advancing the climate-related disclosure agenda. For instance, at the One Planet Summit in 2017 (see Box 5.4), the Climate Action 100+ coalition, representing 225 investors with USD 26.3 trillion of assets under management, committed to engage with the 100 most polluting corporations, responsible for about two-thirds of worldwide industrial emissions, and to step up their ambition on climate action (Ang and Copeland, 2018[11]). At the same event, financial institutions responsible for managing USD 80 trillion of assets – equivalent to annual global GDP – publicly supported the Task Force on Climate-related Financial Disclosures (TCFD) (see Box 5.5).

In December 2017, leaders from around the world gathered in Paris, France for the first One Planet Summit to speed up the global transition to a low-emission economy. The summit resulted in twelve climate commitments:

Stepping up for finance adaptation and resilience to climate change:

-

1. Responding to extreme events in island states

-

2. Protecting land and water against climate change

-

3. Mobilising researchers and young people to work for the climate

-

4. Public procurement and access for local governments to green financing

Accelerating the transition towards a decarbonised economy:

-

5. Zero-emissions target

-

6. Sectoral shifts towards a decarbonised economy

-

7. Zero-pollution transport

-

8. Towards a carbon price compatible with the Paris Agreement

Anchoring climate issues at the centre of the decisions of finance and its actors:

-

9. Actions of central banks and businesses

-

10. International mobilisation of development banks

-

11. Commitment by sovereign funds

-

12. Mobilising institutional investors

Source: One Planet Summit (2017[28]), “Commitments”, One Planet Summit web site, https://www.oneplanetsummit.fr/en

The Task Force on Climate-related Financial Disclosure (TCFD) was established by the Financial Stability Board (FSB) in response to a call from G20 Leaders. It has designed a set of recommendations to “shift financial flows towards a low-carbon economy and to avoid stranded assets, reduce or better manage climate-related risks for individual investors, corporates and reduce climate-related risks for the financial system as a whole”. It delivered recommendations for voluntary disclosures of material, decision-useful climate-related financial risks for the G20 Summit in Hamburg in 2017.

The recommendations promoted by the TCFD are articulated around the disclosure of four essential elements:

-

Governance: disclosing the governance of climate-related risks and opportunities;

-

Strategy: disclosing actual and potential impacts of climate-related risks and opportunities on the organisation’s businesses, strategy and financial planning where such information is material;

-

Risk management: disclosing risk management arrangements for how the organisation identifies, assesses and manages climate-related risks; and

-

Metrics and targets: disclosing metrics and targets used to assess and manage relevant climate-related risks and opportunities, where such information is material.

The task force also encourages companies to carry out scenario analysis: while some are already affected by risks associated with climate change today, for many the most significant effects of climate change are likely to emerge over the medium to longer term and their timing and magnitude are uncertain. To appropriately incorporate the potential climate effects in their planning processes, companies need to consider how their climate-related risks and opportunities may evolve under different plausible futures.

Source: TCFD (2017[29]), Recommendations of the Task Force on Climate-related Financial Disclosures.

Some governments are expanding the disclosure requirements for private and long-term investors. A study by the Cambridge Centre for Sustainable Finance estimates that two thirds of G20 member states have engaged with the TCFD recommendations in some form, mainly through statements of support for the aims and recommendations of the Task Force (CISL, 2018[27]). Australia, Canada, the EU, Italy, Japan, South Africa, Turkey and the United Kingdom have conducted (or are in the process of conducting) consultations with the private sector on sustainable finance generally and on disclosure requirements as an important building block of sustainable finance more specifically. Japan has issued voluntary disclosure guidelines and the EU has put together a firm action plan on how to incorporate the recommendations into existing disclosure frameworks.

In a parallel development to the TCFD, France has required asset owners and investment managers to disclose climate-related financial risks. Under Article 173-VI of the Energy Transition Act, institutional investors must provide information not only on how they integrate ESG factors in their investment and voting decisions, but also on the climate risks they face and how their portfolio’s makeup contributes to the transition to a low-emission economy (CISL, 2018[27]). In South Africa, investors must consider how environmental factors can affect long-term performance as per the South African Pension Act (Maimbo et al., 2017[5]).

An important element of the disclosure agenda is the necessity to change the paradigm surrounding disclosure. Instead of disclosing and measuring emissions with static foot-printing techniques, the TCFD encourages the use of scenario analysis to consider dynamically the potential impact of the risks and opportunities of the transition to a low-emission economy on strategy and financial planning.

Reporting practices could move towards the measurement of the emissions embedded in coal, oil and gas reserves and resources. They could include scenario analysis to stress-test investors and companies’ portfolios against decarbonisation scenarios and track progress of companies towards science-based targets. Such disclosure would help to better understand the risks for investments that are misaligned with climate goals, differentiated into financial risks and impact risks. Such practices would trigger the behavioural change needed by investors and financiers, and help move away from incremental progress to the radical reallocation needed (TCFD, 2017[29]).

Building climate-related capacity among investors and private firms is an essential factor of success. Low-emission, resilient strategies and science-based targets need to be developed, data on climate-related risks and opportunities of businesses and portfolios need to be collected and reporting on climate-related risks will need to broaden and improve. Regulators and standard-setters could provide guidance to ensure the credibility and comparability of commitments.

Improving climate-related risk assessment and disclosure may not necessarily lead to the desired behavioural change in cases where such risk is still considered acceptable. Such measures should be part of a set of policies that make climate-related risk of material relevance to investors, and a broader disclosure agenda that could encourage more transparency about the financial flows themselves. Improving transparency on financial flows that contribute to the desired transition, as well as on flows that potentially undermine it, could help governments measure progress towards aligning all flows with a low-emission future.

5.3. Rethink financial supervision in light of climate imperatives

Financial stability is a prerequisite to any type of investment, including investment in low-emission, resilient infrastructure, and the primary role of financial regulators is to ensure the stability of the financial system. There is a growing awareness among regulators and financial supervisors that success in transitioning to a world with manageable levels of climate change is a determinant of financial stability in the long run. The G20 sustainable finance study group stated that “a proper framework for sustainable finance development may also improve the stability and efficiency of the financial markets by adequately addressing risks as well as market failures such as externalities” (G20 Green Finance Study Group, 2016[30]). As a first step, climate considerations need to be integrated into the rules and regulations that support the stability of the financial system.

Progress on this front has already been made. The European Commission’s High-Level Expert Group has recommended integrating sustainability into the European Union’s regulatory and financial policy framework (see Box 5.6). At the One Planet Summit in December 2017, central banks and supervisors from three continents, including the Bank of England, Banque de France, De Nederlandsche Bank, Deutsche Bundesbank and the Federal Financial Supervisory Authority of Germany BaFin, created the network for “greening the financial system”, an initiative to help accelerate climate mainstreaming in financial supervision and in the refinancing of secondary markets to promote an orderly development of green finance (One Planet Summit, 2017[27]). The network’s ambition is to exchange experiences, share best practices, contribute to the development of environment and climate risk management in the financial sector and mobilise mainstream finance to support the transition towards a sustainable economy, on a voluntary basis.

In September 2016, the European Commission launched the industry-led High-Level Expert Group (HLEG) on Sustainable Finance to examine how to integrate sustainability considerations into the European Union’s financial policy framework.

The HLEG’s interim report (June 2017) recommended integrating sustainability into the EU’s regulatory and financial policy framework, including through climate disclosure, accounting, fiduciary duties, corporate governance and reporting, and stewardship codes. Its final report stressed that moving towards sustainable finance involves two imperatives: (1) improving the contribution of finance to sustainable and inclusive growth and the mitigation of climate change; and (2) strengthening financial stability by incorporating environmental, social and governance (ESG) factors into investment decision making. The report lays out 30 proposals, including 8 key recommendations.

Building on the recommendations provided in the HLEG’s final report, in March 2018 the European Commission launched a broad Action Plan on Financing Sustainable Growth, laying down the roadmap to integrating sustainability in the financial system at the EU level. This involved 10 main actions:

-

Establishing an EU classification system for sustainable activities

-

Creating standards and labels for green financial products

-

Fostering investment in sustainable projects

-

Incorporating sustainability when providing financial advice

-

Developing sustainability benchmarks

-

Better integrating sustainability in ratings and market research

-

Clarifying institutional investors’ and asset managers’ duties

-

Incorporating sustainability in prudential requirements

-

Strengthening sustainability disclosure and accounting rule-making

-

Fostering sustainable corporate governance and attenuating short-termism in capital markets.

The European Commission announced its first four proposals to support sustainable finance in the European Union in May 2018, and proposed legislation on benchmarks, green definitions, investor duties and retail investing.

Sources: EU High-Level Expert Group on Sustainable Finance (2017[33]); Financing a Sustainable European Economy: Interim Report; EU High-Level Expert Group on Sustainable Finance (2018[34]), Financing a Sustainable European Economy: Final Report; European Commission (2018[35]), Action Plan: Financing Sustainable Growth.

While recognising that national circumstances matter and that there is no one-size-fits-all approach, governments, financial regulators and climate policy makers can act on a variety of levels (Maimbo et al., 2017[5]):

-

Support the growth of low-emission, resilient investment market through the development of standards and policy frameworks that promote the issuance of low-emission, resilient financial products and the emergence of new market platforms. Policy banks and state-controlled financial institutions, including sovereign wealth funds, could be harnessed more effectively (see Chapter 4).

-

Continuously monitor the potential unintended consequences of financial regulations and regulatory reforms on the supply of long-term investment financing for climate (Ang, Röttgers and Burli, 2017[31]). This could include preserving the integrity of standards for “low-emission” labels and markets or initiatives such as the emerging global dialogue on capital risk weightings.

-

Promote transparency in the financial system, through policies and regulations that support the disclosure of risks and opportunities associated with climate change, disclosure of financial flows, and developing climate-scenario analysis for insurance companies and banks. These scenarios could be a strategic tool for policy making.

-

Clarify legal frameworks and mandates for instance on the interpretation of long-term investor obligations and responsibilities in the context of climate change or how climate considerations can be interpreted within the existing mandates of supervisory bodies. For instance, the Central Bank of Brazil has published guidelines for the social and environmental responsibility of financial institutions (Resolution no. 4327 of 2017) (Maimbo et al., 2017[5]; OECD, 2017[32]).

References

Allianz (2018), Allianz is driving change toward a low-carbon economy with an ambitious climate protection package, Allianz Web Portal, https://www.allianz.com/en_GB/press/news/business/insurance/180504-allianz-announces-climate-protection-package.html (accessed on 19 October 2018). [19]

Ang, G. and H. Copeland (2018), Integrating Climate Change-related Factors in Institutional Investment, OECD Publishing, Paris, https://www.oecd.org/sd-roundtable/papersandpublications/Integrating%20Climate%20Change-related%20Factors%20in%20Institutional%20Investment.pdf (accessed on 26 July 2018). [11]

Ang, G., D. Röttgers and P. Burli (2017), “The empirics of enabling investment and innovation in renewable energy”, OECD Environment Working Papers, No. 123, OECD Publishing, Paris, https://doi.org/10.1787/67d221b8-en. [31]

Arabella Advisors (2016), The Global Fossil Fuel Divestment and Clean Energy Investment Movement, https://www.arabellaadvisors.com/wp-content/uploads/2016/12/Global_Divestment_Report_2016.pdf (accessed on 27 July 2018). [16]

AXA (2018), Active engagement: Initiatives 2017/18, AXA Web Portal, https://www.axa-im.com/en/content/-/asset_publisher/alpeXKk1gk2N/content/insight-annual-report-active-engagement/23818 (accessed on 19 October 2018). [17]

AXA (2017), Integrated Report 2017, AXA, https://www-axa-com.cdn.axa-contento-118412.eu/www-axa-com%2F2d414b6f-ac38-44ad-bf1d-0fc4b2a231f2_axa-ra2017-en-pdf-e-accessible_03.pdf (accessed on 19 October 2018). [18]

Baron, R. and D. Fischer (2015), Divestment and Stranded Assets in the Low-carbon Transition, OECD Publishing, Paris, https://www.oecd.org/sd-roundtable/papersandpublications/Divestment%20and%20Stranded%20Assets%20in%20the%20Low-carbon%20Economy%2032nd%20OECD%20RTSD.pdf (accessed on 19 October 2018). [15]

Buhr, B. et al. (2018), Climate Change and the Cost of Capital in Developing Countries, Imperial College Business School and SOAS University of London, https://imperialcollegelondon.app.box.com/s/e8x6t16y9bajb85inazbk5mdrqtvxfzd (accessed on 27 July 2018). [24]

Carney, M. (2018), A Transition in Thinking and Action, https://www.bankofengland.co.uk/-/media/boe/files/speech/2018/a-transition-in-thinking-and-action-speech-by-mark-carney.pdf (accessed on 14 September 2018). [23]

CISL (2018), Sailing from different harbours: G20 approaches to implementing the recommendations of the Task Force on Climate-related Financial Disclosures, University of Cambridge Institute for Sustainability Leadership (CISL), Cambridge, https://www.cisl.cam.ac.uk/resources/publication-pdfs/cisl-tcfd-report-2018.pdf (accessed on 25 October 2018). [27]

Climate Bonds Initiative (2018), Green Bond Highlights 2017, https://www.climatebonds.net/files/reports/cbi-green-bonds-highlights-2017.pdf (accessed on 24 July 2018). [4]

EU High-Level Expert Group on Sustainable Finance (2018), Financing a Sustainable European Economy: Final Report, European Commission, https://ec.europa.eu/info/sites/info/files/180131-sustainable-finance-final-report_en.pdf (accessed on 05 July 2018). [34]

EU High-Level Expert Group on Sustainable Finance (2017), Financing a Sustainable European Economy: Interim Report, European Commission, https://ec.europa.eu/info/sites/info/files/170713-sustainable-finance-report_en.pdf (accessed on 13 September 2018). [33]

European Commission (2018), Action Plan: Financing Sustainable Growth, http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1483696687107&uri=CELEX:52016SC0405 (accessed on 05 July 2018). [35]

G20 Green Finance Study Group (2016), G20 Green Finance Synthesis Report, G20 Green Finance Study Group, http://www.g20.utoronto.ca/2016/green-finance-synthesis.pdf (accessed on 12 September 2018). [30]

Government of Canada (2018), Power Past Coal Alliance Declaration, https://www.canada.ca/en/services/environment/weather/climatechange/canada-international-action/coal-phase-out/alliance-declaration.html (accessed on 20 July 2018). [14]

IDB (2018), What is Sustainable Infrastructure? A Framework to Guide Sustainability Across the Project Cycle, Inter-American Development Bank, https://publications.iadb.org/bitstream/handle/11319/8798/What-is-Sustainable-Infrastructure-A-Framework-to-Guide-Sustainability-Across-%20the-Project-Cycle.pdf?sequence=1&isAllowed=y (accessed on 24 July 2018). [21]

IFC (2016), Climate Investment Opportunities in Emerging Markets, International Finance Corporation, Washington, DC, https://www.ifc.org/wps/wcm/connect/51183b2d-c82e-443e-bb9b-68d9572dd48d/3503-IFC-Climate_Investment_Opportunity-Report-Dec-FINAL.pdf?MOD=AJPERES (accessed on 19 October 2018). [26]

Maimbo, S. et al. (2017), “Roadmap for a Sustainable Financial System”, No. 121283, World Bank Group and UNEP Inquiry, Washington, DC, http://documents.worldbank.org/curated/en/903601510548466486/Roadmap-for-a-sustainable-financial-system. [5]

Nelsen, A. (2015), “Dutch government ordered to cut carbon emissions in landmark ruling”, The Guardian, https://www.theguardian.com/environment/2015/jun/24/dutch-government-ordered-cut-carbon-emissions-landmark-ruling (accessed on 19 October 2018). [25]

OECD (2018), “Blockchain, infrastructure and the low-emission transition (forthcoming)”, Financing Climate Futures Case Studies, OECD Publishing, Paris. [22]

OECD (2017), Breaking Silos: Actions to Develop Infrastructure as an Asset Class and Address the Information Gap, OECD Publishing, Paris, http://www.oecd.org/daf/fin/private-pensions/Breaking-Silos%20-Actions-to%20Develop-Infrastructure-as-an-Asset-Class-and-Address-the-Information-Gap.pdf (accessed on 20 July 2018). [3]

OECD (2017), Investing in Climate, Investing in Growth, OECD Publishing, Paris, https://doi.org/10.1787/9789264273528-en. [1]

OECD (2017), Investment governance and the integration of environmental, social and governance factors, OECD Publishing, Paris, https://www.oecd.org/investment/Investment-Governance-Integration-ESG-Factors.pdf (accessed on 13 September 2018). [32]

OECD (2017), OECD Business and Finance Outlook 2017, OECD Publishing, Paris, https://doi.org/10.1787/9789264274891-en. [8]

OECD (2015), Mapping Channels to Mobilise Institutional Investment in Sustainable Energy, Green Finance and Investment, OECD Publishing, Paris, https://doi.org/10.1787/9789264224582-en. [20]

One Planet Summit (2017), Commitments, One Planet Summit Web Portal, https://www.oneplanetsummit.fr/en/commitments-15 (accessed on 19 October 2018). [28]

TCFD (2017), Recommendations of the Task Force on Climate-related Financial Disclosures, https://www.fsb-tcfd.org/wp-content/uploads/2017/06/FINAL-TCFD-Report-062817.pdf (accessed on 12 September 2018). [29]

UN Environment (2018), Shifting the Lens (forthcoming), UN Environment, https://www.unepinquiry.org. [10]

UN PRI (n.d.), About the PRI, PRI Web Portal, https://www.unpri.org/pri (accessed on 19 October 2018). [12]

UNEP Inquiry (2018), “Greening the Rules of the Game: How Sustainability Factors Are Being Incorporated Into Financial Policy and Regulation”, Inquiry Working Paper, No. 18/01, UN Environment, http://unepinquiry.org/wp-content/uploads/2018/04/Greening_the_Rules_of_the_Game.pdf (accessed on 13 September 2018). [6]

UNEP Inquiry (2018), Making Waves: Aligning the Financial System with Sustainable Development, UN Environment, Geneva, http://unepinquiry.org/making-waves/. [7]

UNFCCC (2017), More than 20 Countries Launch Global Alliance to Phase Out Coal, https://unfccc.int/news/more-than-20-countries-launch-global-alliance-to-phase-out-coal (accessed on 20 July 2018). [13]