Chapter 2. An overview of project pipelines

This chapter explores “project pipelines”, a common concept used in infrastructure planning and investment discussions and government strategies to engage private sector stakeholders and mobilise finance. To begin, the chapter examines what is meant by project pipelines in the context of climate objectives to scale-up investment in low-carbon infrastructure. Important to these objectives is how project pipelines relate to government’s wider investment policy framework and the tools, activities and processes with which governments: disseminate information; highlight investment opportunities; and encourage market actors to engage, commit funding and devote time to executing infrastructure investments. To close, the chapter explores what concrete actions governments can take to build robust pipelines and what factors governments can consider when building such pipelines – the focus of Chapter 3 which includes case studies of emerging good project pipeline practices.

2.1. Introduction to project pipelines

Pipelines of infrastructure projects – or simply “project pipelines” for the purposes here – are a common concept in infrastructure planning and investment literature (see, for instance, OECD (2015[1]; 2017[2]; 2017[3]) and others including Mercer and Inter-American Development Bank (2016[4]), Nassiry, Nakhooda and Barnard (2016[5]) and Kortekaas (2015[6]). Pipelines are often used in these discussions to emphasise specific, upcoming investment opportunities in infrastructure assets, such as prospects to develop large-scale renewable energy projects in a country over the next decade. As such, project pipelines have become a key focal point in countries’ efforts to implement their climate and development commitments, including the Nationally Determined Contributions (NDCs).

Meeting climate mitigation objectives requires pipelines of many thousands if not millions of low-carbon infrastructure projects throughout the world. Public finance on its own will be insufficient. The private sector, therefore, will need to invest, build and support the development, operation and maintenance of those projects in the pipelines, as well as the retrofit or decommissioning of existing infrastructure to align it with mitigation and other sustainability objectives. Clear policy objectives and commitments are important to investors since they often look to government strategies as important signals of intent, which can be a critical factor in decision-making and trigger actual low-carbon investment. The following section gives more information on how much infrastructure investment is required and which sectors are covered in this report.

Governments (of all levels, national or otherwise) are best-placed to promote and develop project pipelines to foster private sector investment in projects and achieve their policy objectives and commitments, like the NDCs or the longer term 2050 low-emissions development strategies. The NDCs, for instance, provide and serve as a framework for national low-carbon investment priorities in countries that ratified the Paris Agreement. To meet their NDCs, countries will need to have a pipeline of suitable investment-ready infrastructure projects.

There is no one-size-fits-all method to promote and build infrastructure project pipelines. To date, no formal definition exists for pipelines nor has there been a comprehensive examination of the pipeline concept and its role in planning for or meeting climate objectives. Infrastructure planning efforts vary greatly in scope and scale and very much depend on specific country or regional contexts and their infrastructure “starting points”. There is, however, significant potential for governments to share and learn from good practices and approaches taken to build project pipelines, as discussed in this chapter.

The remainder of this chapter examines the following questions: What infrastructure investment is needed to meet climate objectives? (section 2.2); What is meant by project pipelines in the context of climate objectives? (section 2.3); What concrete actions can governments take to build robust pipelines and what factors can governments consider when building such pipelines? (section 2.4). Chapter 3 examines these approaches in more detail through case studies of governments and other public actors developing project pipelines to meet climate objectives.

2.2. Infrastructure investment needs to meet climate objectives and scope of report

The challenge to meet climate objectives is to both scale up finance for long-term investment in infrastructure and shift investments towards low-carbon alternatives (OECD, 2015[7]). Low-carbon infrastructure has been deployed in rapidly increasing volumes with decreasing costs, particularly in the energy sector. The ramifications of these low-carbon technologies and improved operational experience have been felt globally, and many countries now have access to new and increasingly affordable low-carbon sources of energy and clean transportation.

Despite these significant advances, estimates of what is planned continue to significantly lag behind estimates of what is needed, despite new commitments such as the NDCs. Investment in low-carbon infrastructure, for instance, needs to occur at volumes well above current levels. While estimates of investment needs differ, they all point to a significant infrastructure investment gap of trillions of dollars per year to meet climate and sustainable development objectives.1 For instance, latest figures suggest that total current infrastructure investment is around USD 3.4–4.4 trillion globally per year (OECD, 2017[3]), but the gap to meeting climate and development objectives may be an additional USD 2.5 trillion per year to 2030 (when compared to the estimated investment needs of USD 6.3–6.9 trillion per year2).

The current set of NDCs do not put global emissions on a pathway to meet the temperature goals implicit in the Paris Agreement (UN Environment, 2017[8]). All sectors will be affected by the investments required to meet long-term climate objectives, including the reorientation of existing infrastructure or deployment of new low-carbon and climate-resilient assets:

-

energy, e.g. renewable energy technologies

-

transport, e.g. public transport options like bus rapid transit and electric vehicles (ITF, 2017[9])

-

industry, e.g. improved process efficiencies

-

housing, e.g. efficiency measures such as insulation and deep retrofitting

-

water, e.g. water supply and sanitation, flood protection, water storage and conveyance

-

food and sustainable agriculture, e.g. irrigation, resilience to extreme changes in climate

-

forestry, e.g. reforestation

-

resilience infrastructure, e.g. to protect assets from potential storm damage.

2.1.1. Scope and focus of report

The focus in this report is on low- or zero-carbon, mitigation projects such as renewable electricity generation, energy efficiency, public transportation and electric vehicles. Despite this particular focus, the examples of good practice in this report for building low-carbon project pipelines are potentially applicable to other types of infrastructure projects. At the same time, good practices based on an examination of other types of infrastructure projects (or aspects of infrastructure projects, e.g. resilience) are also relevant to low-carbon infrastructure projects. For example, adding resilience measures in the design of these projects, which is essential to their durability, needs to be considered for low-carbon infrastructure upfront and systematically, although such measures may add to the complexity of structuring projects and increase costs (see Box 2.1 for work on resilience infrastructure investment).

The development of project pipelines aligned with long-term climate mitigation objectives will need to be supportive of such important infrastructure sectors as water supply or flood protection (Section 3.7 in Chapter 3 examines in more detail water infrastructure and approaches taken by the Netherlands and the United Kingdom). Lessons from work on water infrastructure also can apply to developing low-carbon infrastructure. In particular, the consideration of long-term strategic pathways, avoiding path dependencies and expensive lock-ins are important to ensure infrastructure investment remains aligned with long-term policy objectives.

The physical impacts of climate change, such as changes in temperatures, changes in rainfall patterns and sea-level rise, will affect all types of infrastructure investments. Potential threats include reduced asset lifetimes, increases in operational expenditure, the need for additional capital expenditure, and increased risks of environmental damage and litigation. Decisions taken now about the location, construction and operation of infrastructure will determine future resilience. Adopting a resilient approach to respond to climate change also means accepting that some disruptions are occasionally unavoidable.

Improving the climate resilience of new or existing infrastructure can be achieved by reducing exposure or sensitivity to climate-related hazards through a wide range of context-specific adaptation responses. Adaptation measures may require implementing “hard” civil engineering measures to protect assets, or “soft” measures, which include modifying maintenance routines or information-sharing practices. Innovative solutions can also be used, such as working with nature. These measures can have very different costs, both in absolute and relative terms with respect to an overall construction or retrofitting project.

National governments have the opportunity to ensure that future investment supports resilience and avoids locking-in vulnerability. Vallejo and Mullan (2017) identified four areas in which governments can focus their efforts to facilitate climate-resilient infrastructure:

-

1. Improving risk assessment and information to support decision making. Ensuring data on projected natural hazards is available and accessible, raising awareness, and building the capacity of relevant decision makers all contribute to better decision-making. High–level risk assessments should also be undertaken to identify the exposure of existing infrastructure.

-

2. Screening and factoring climate risks into public investments. When investing in or commissioning infrastructure, governments can require contractors and suppliers to demonstrate they have considered climate risks.

-

3. Enabling infrastructure resilience through policy and regulation. Governments can support climate-resilient infrastructure by removing regulatory distortions, or adding regulatory requirements to consider physical climate risks.

-

4. Encouraging climate risk disclosure. The disclosure of physical risks can encourage action to manage those risks, as well as revealing interdependencies and supporting the design of public policy.

Source and further reading: Vallejo, L. & M. Mullan (2017), "Climate-resilient infrastructure: Getting the policies right", OECD Environment Working Papers, No. 121, OECD Publishing, Paris. https://doi.org/10.1787/02f74d61

2.3. An overview of project pipelines: Meaning and context

The importance of project pipelines is evident from a body of literature (summarised in Annex 2.A) which recommends that governments develop and manage them as a means to improve transparency and offer long-term credibility, predictability and vision. Pipelines are recommended largely because investors’ abilities to identify and assess low-carbon infrastructure investment opportunities are greatly helped if pipelines are clearly described and promoted by governments (Kortekaas, 2015[6]).

Yet, in the context of scaling up infrastructure investment for climate objectives, few reports go beyond this generic recommendation to explore how to characterise or identify good project pipeline practices, or what concrete steps governments can take to develop more robust project pipelines and thereby scale-up investment in low-carbon infrastructure. To shed more light on these issues, this section explores project pipelines in the context of meeting climate objectives and examines the following questions:

-

What is meant by project pipelines in the context of climate objectives? (Section 2.3.1)

-

How do project pipelines relate to the government’s wider investment policy framework to mobilise private finance? (Section 2.3.2)

-

How does this report help shift the current discussions of project pipelines from concept to actions? (Section 2.3.3)

2.3.1. What is meant by project pipelines in the context of climate objectives?

No formal definition of a project pipeline has been agreed for infrastructure projects generally, let alone one which is aligned to meeting long-term climate objectives. Based on expert interviews, discussions and review of literature, the predominant view amongst governments and the investment community appears to be that a project pipeline is manifested in the form of a list of projects at an advanced stage in the development process and that it should be published or communicated publicly in some way.

Based on this common view, a low-carbon and climate-aligned project pipeline could be described as “a set of infrastructure projects and assets (accounting for the existing stock of assets), and future assets in early development and construction stages prior to project commissioning, typically presented as a sequence of proposed investment opportunities over time that align with and are supportive of long-term climate and development objectives.”

Despite the absence of a commonly used formal definition, examples of project pipelines from governments, development banks and international initiatives have tended to be fairly consistent with the description of pipelines provided above. These public institutions invariably aim to generate lists of tangible, future assets that will be added to or replace the existing infrastructure stock. One such example explored in Chapter 3 is the Clean Technology Fund of the Climate Investment Funds (CIF). The CIF works in 72 developing and emerging economies to assist governments with country assessments of their low-carbon and climate-resilient infrastructure needs and develops a number of near-term and tangible investment opportunities.3 See Chapter 3 for several other examples of efforts to build project pipelines.

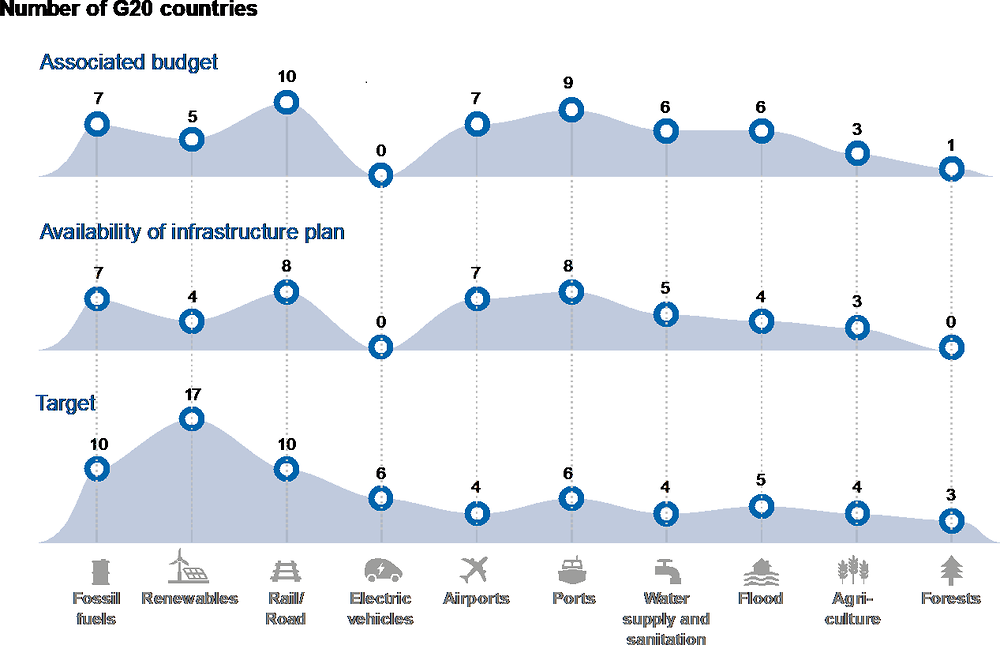

The OECD recently examined national-level, infrastructure investment plans for the Group of 20 (G20) countries (OECD, 2017[3]).4 Figure 2.1 shows an overview of these G20 infrastructure plans, taken from OECD (2017[3]). The plans cover ten infrastructure sectors from fossil fuel to flood prevention, and were filtered according to a number of criteria: whether a target or objective was in place (e.g. to increase the number of electric vehicles to 1 million by 2025); if a public budget was available to support investment (e.g. there is a public fund of EUR 300 million available to de-risk investments); or if information was publicly available on individual projects (e.g. typically a list of all or, more often, a subset of the projects included in the plan, presented online or otherwise).

Note: This figure shows the number of G20 countries that, as of early 2017, had sector targets (bottom graph), plans of projects (middle), and associated budgets to support their development (top).

Source: OECD (2017[3])

The analysis revealed inconsistencies across the G20 countries by sector and by level of detail in the project pipeline (according to analysis of infrastructure budgets, plans and targets in early 2017). The study found that while 17 countries had set a renewable energy target, for instance, only four (Argentina, Brazil, Mexico and the United Kingdom) had an associated infrastructure plan that outlined the projects involved. Indeed, few countries had a budget or plan for the development of important infrastructure sectors like agriculture, sanitation, flood prevention or forestry. Likewise, while six countries had a target for deploying electric vehicles, no country had a plan or budget to reach it.5

The OECD (2017[3]) report found that there are gaps in the consideration of climate change mitigation and adaptation objectives, and challenges to determine the extent and nature of project pipelines. Only five of the 20 countries studied, for instance, mention climate mitigation or adaptation measures within their infrastructure planning processes. The report also recognised that very few countries have so far developed 2050 low-emission development strategies,6 and strongly urged others to rapidly scale up investment in low emissions infrastructure by developing a prioritised and “[publicly available] pipeline of infrastructure projects.”

Similar messages are also found in a forthcoming OECD paper (Mirabile and Calder, 2018 forthcoming[10]) which attempts to ‘quantify’ the project pipeline in the global power sector. This study, summarised in Box 2.2, compares global electricity generation capacity (under construction and planned over the next five years) against low-carbon scenarios to test for misalignment. It finds that the current building and planned construction of coal capacity over the next five years are incompatible with long-term climate ambitions. Renewable energy deployment, on the contrary, appears to be going in the right direction, but needs to be accelerated.

Many countries will soon begin or have already begun to include their NDCs or other forms of climate targets in their long-term infrastructure planning and policy-making processes. These processes are country and context specific. Nevertheless, the ability to identify and compare common or good practices for project pipeline planning and development may prove beneficial to other countries. What constitutes good project pipeline practice is the focus of the next section and Chapter 3.

With 40% of energy emissions accounted for by the electricity sector – themselves representing 68% of global greenhouse gas emissions – decarbonising electricity infrastructure is essential if climate goals such as the Paris Agreement are to be achieved. This study establishes whether electricity generation infrastructure under construction and planned in the next five years – the “pipeline” – is in line with a low-carbon scenario.

Results indicate that globally, there are approximately 6 300 GW of power capacity in operation, 1 200 GW currently under construction (to become operational in the next five years). An analysis of this pipeline indicates that renewable energy technology is expanding rapidly: it represented only 34% of the installed capacity in 2017 yet accounts for 62% of the plants under construction (mostly from wind and solar power). In contrast, the development of new coal power plants is slowing: currently representing 31% of total installed generation capacity, coal power represents 23% of electricity capacity under construction.

While these results provide encouraging signs that the decarbonisation of the energy sector is in motion, data suggest that coal will still be the main source of electricity output by 2022. Solar power – while being deployed widely – still only accounts for 1% of electricity generation (IEA, 2017[11]). To be in line with 2020–30 energy scenarios that provide pathways to reach the Paris Agreement temperature goal of limiting global temperature rise to well below 2°C, not only should the installed capacity of coal stall, global coal capacity should decrease by 2% per year in the next ten years (compared to a 3% increase in the last ten years). The current building of coal capacity and planned construction in the next five years are not compatible with staying on an emissions scenario of below 2°C. Renewable energy deployment, on the contrary, appears to be going in the right direction, but needs to be accelerated.

This study indicates that a number of changes need to take place in the electricity sector to meet the Paris Agreement’s mitigation goals. In addition, the implied transition brings with it a number of challenges and opportunities that governments need to consider, such as: addressing air quality and climate issues simultaneously; ensuring a just and inclusive transition; managing stranded assets; arranging alternative government revenues (including from carbon pricing).

Source and further reading: Mirabile and Calder (2018 forthcoming[10]).

2.3.2. How do project pipelines relate to the government’s wider investment policy framework to mobilise private finance?

Governments as a whole, and specific public agencies and institutions, strongly influence the development of domestic project pipelines by signalling intent, setting policies and regulations, establishing promotional institutions and planning infrastructure. Public actors have a suite of available tools and levers to involve themselves in infrastructure investments. They can, for instance: fund projects directly from public budgets; lead public-private partnerships; employ risk mitigants like public guarantees; or set policy incentives for specific sectors or technologies (see Annex 2.B for more information).

High-level objectives and policy frameworks

The NDCs are an important example of government efforts to set high-level national mitigation objectives. They could influence policy frameworks, infrastructure investments and the associated project pipelines in almost all countries to the period to 2025–30. Yet, even where the NDCs have clear goals, their implementation, as manifested in changes in the domestic policy framework, is still at an early or basic stage in many countries. The lack of detailed infrastructure investment plans and integration of these plans into national policy contexts means it is not always clear what and where project investments are needed, or how to finance them. Importantly, poorly defined infrastructure planning and lack of policy links could open the door to investments that should not be made, such as those which result in expensive lock-in or path dependencies and those which are incompatible with climate objectives.

By using the various policy tools available to them (see, for instance, Annex 2.B), a range of public institutions can shape how project pipelines and efforts to develop pipelines relate to the wider policy framework and the investment-enabling environment.7 For instance, subnational and local governments set policies specific to their local needs (see Annex 2.C). Regulators set expectations for financial returns from infrastructure assets in sectors that may inherently lack competition but where investments are often undertaken by the private sector, such as electricity grids and transport networks. Development banks employ technical capacity and local knowledge to promote and support infrastructure investment in emerging and developing economies (see Annex 2.D and section 3.3 in Chapter 3). Lessons from these activities and institutions, such as what works and what does not, can feed back into policy-making processes and improve understanding of investment obstacles or gaps (and how to overcome those).

Mobilising private sector investors

Private sector investors and project developers, who are expected to provide up to three-quarters of green infrastructure investment (WEF, 2013[12]), have at their disposal numerous channels through which to invest and to assess projects, take positions and secure attractive returns on their investments.8 Governments can foster such channels and maintain relevant funding activities (see, for example. OECD (2016[13]; 2015[1])) including ensuring that, to the best of their abilities, projects are investment-ready and attractive (see the next section).

Investors (and project developers) want to identify and source investment opportunities that match their needs from the available options, which are usually driven by government policy and goals. Long-term investors, like pension funds or insurance companies, are typically less interested in one-off investments than in the possibility of an attractive, enduring portfolio of bankable projects with the right risk-return profile and track record of various actors involved. Meanwhile, private equity and early-stage investors are typically interested in higher risk-return profiles (particularly important in low carbon investments in developing countries). In both cases, investors often compare and evaluate investment options across countries and sectors to find suitable opportunities. Annex 2.E discusses the role of better infrastructure data and more transparency in project pipeline development processes.

A key motivation for examining project pipelines more comprehensively is the general lack of knowledge on what effective approaches and efforts to build project pipelines look like. This situation presents challenges to investors and, from an investor or project developer perspective, may ultimately constrain investment. OECD (2017[3]) warned that “[project pipelines] that are inaccessible, incomplete or poorly aligned with long-term climate mitigation and adaptation goals are likely to hinder the flow of infrastructure investment in support of climate goals”. Expert interviews and discussions undertaken for this report reached similar conclusions: project pipeline approaches, as implemented to date, vary in their use and application; the range of pipeline practices are too varied and dissimilar to allow conclusions to be made on what works best; and the lack of clarity in pipeline development practices hampers investors’ efforts to identify such opportunities.

2.3.3. How does this report help shift the current discussions of project pipelines from concept to concrete actions?

By providing an in-depth exploration of what is involved in building project pipelines in the context of meeting climate objectives, this report aims to move discussions on pipelines beyond high-level assessments of project pipelines. The next section examines what concrete actions governments can take to build robust project pipelines and Chapter 3 explores a set of case studies to identify good practices in this area.

This report aims to complement and expand on other examinations of pipelines completed to date, which have focused on such topics as:

-

reviewing available data and studying government reports and publications (e.g. the approach taken by OECD (2017[3])

-

analysing planned investments in one sector (e.g. power sector analysis presented in Box 2.2)

-

building an online tool for hosting projects that are in later stages of development but do not account for climate or sustainability factors (e.g. see the Global Infrastructure Hub presented in Annex Box 2.E.1)

-

targeting the preparation of individual projects to be added to a national project pipeline (e.g. within Multilateral Development Banks)

-

summarising infrastructure initiatives in general (e.g. a survey by Mercer and the Inter-American Development Bank (2016[4])).

2.4. Robust project pipelines and effective efforts to develop them

Governments can take action in a number of areas to make their project pipelines robust in the context of meeting climate objectives. The process to “translate” such objectives into a tangible set of projects involves collective action from a range of actors. Governments (of all levels, national or otherwise) are best-placed to support the development of robust project pipelines through various activities, processes and practices.

Based on expert interviews and a review of literature and existing pipeline practices, a national project pipeline aligned to climate objectives can be developed. However, such a pipeline can only be as robust as the (investment-ready and bankable) projects that constitute it and as effective as the institutions that deliver it. In addition, such a pipeline will only be as ambitious as the government objective to which it is linked. In the context of low-carbon project pipelines, ambition can refer to the stringency of mitigation action implied in the NDCs and the way in which the target is expressed (e.g. absolute emissions reduction, renewable energy target and others).

The following subsections look at key areas of government efforts to build project pipelines and ultimately ensure that they are robust and fit-for-purpose.

-

Influencing the bankability of projects in the pipeline (Section 2.4.1)

-

Characterising robust project pipelines (Section 2.4.2).

-

Highlighting effective efforts to develop robust project pipeline (Section 2.4.3).

2.4.1. Influencing the bankability of projects in the pipeline

A commonly proposed but vague solution to the lack of bankable and investment-ready projects is for governments to have “better pipelines”. This prescription fails to consider that there is a lack of easily identifiable, bankable projects at the volumes, scales and risk-return profiles that interest investors. The notion of having better pipelines should, therefore, account for these demands and other country needs, which make the task of developing and delivering better pipelines, and the associated projects, much more complex than the simple phrase (“better pipelines”) would suggest. This concern points to two items of importance, 1) how to ensure projects within the pipeline are bankable, and 2) what actions governments can take to support them.

Governments sometimes lack the capacity and knowledge to convert project proposals into economically attractive investment opportunities. To that end, project preparation facilities (PPFs) are increasingly offered by public institutions to assist the development of projects to reach investment-ready states (see Annex 2.F for more information on PPFs and project bankability). An increasing amount of emphasis is being placed on these facilities, particularly in developing and emerging economies; the costs for global project preparation activities have been estimated between 2.5% and 10% of total infrastructure investment (GCEC, 2016[14]; Kortekaas, 2015[6]) or up to USD 690 billion per year.9

The amount of preparation needed depends on the sector and type of infrastructure. In designing PPFs, governments play a key role in ensuring projects are in line with the country’s strengths. For instance, the rapid cost reductions witnessed in some areas such as renewable energy sources like wind and solar energy mean that identifying bankable electricity generation projects is becoming less of a challenge than in other sectors, noting that even solar energy projects face significant barriers in many sun-rich countries. The reducing sizes of “average” infrastructure projects (e.g. small-scale energy efficiency, demand-side technologies, and distributed renewable energy) mean many millions of new, and often discrete, projects will be required globally. Of course, since infrastructure normally lasts for decades, bankable projects will need to be adequately resilient to future changes in environmental conditions (see Box 2.1 for information on resilience).

2.4.2. Characterising robust project pipelines

The preceding discussion suggests that governments can develop robust project pipelines to highlight the scale and scope of investment opportunities and communicate the available tools and policies. Efforts to develop robust pipelines ultimately need to: promote investment in “good projects”,10 across a variety of sectors, of different scales; accommodate the requirements of investors; and allocate preparatory support to certain projects that may help a country achieve objectives like the NDCs, but which are not yet bankable.

Literature review and discussions with experts suggest that, with respect to aligning infrastructure to long-term climate objectives, governments can develop robust pipelines of projects if they:

-

link policy making to forward-looking objective setting and the programmes and institutions to deliver them, providing overall co-ordination and leadership to champion project pipelines

-

focus on strengthening the interface and mechanisms that governments employ to disseminate information and convene actors, offering transparent processes and communicating relevant information on projects and the pipeline with the financing and investment community

-

take a holistic, whole-of-government approach to infrastructure planning and investment, feeding lessons back into policy-making processes to bolster the investment-enabling environment and providing funding or institutional support to projects when appropriate

-

fast-track suitable infrastructure project investment in a way that brings the carbon and energy intensities of the country’s economy to target levels, prioritising the deployment of “high-value” and strategically important projects and sectors

-

foster the development of a diverse set of bankable projects and promote business models suitable for private sector needs, setting strong eligibility criteria to determine which projects should be built and supported and which should not

-

increase country resilience to changes in climate and development needs, deploying infrastructure that remains pertinent and relevant over time and tailored to changing external conditions, and avoiding expensive path dependency or lock-in.

2.4.3. Highlighting effective efforts to develop robust project pipelines

Building from the above analysis, and based on a thorough review of project pipeline efforts across many countries, a number of policy and institutional factors have been identified which are common to effective government efforts to develop robust pipelines. Through a series of case studies, Chapter 3 examines each of the following six factors in the context of a country’s or region’s efforts to build robust project pipelines. Each case study, therefore, explores the various attributes and important applications of the factor and highlights emerging good practices of its use.

-

1. Leadership relates to governments as a whole, or specific agencies, championing the development of a robust project pipeline. It is manifested when these government actors possess and use authority to oversee policy actions, co-ordinate and mobilise public and private actors, signal investment needs, devote time and cater to national and international priorities, and disseminate information. Governments can also help direct actors to scale up activities in certain areas such as technology manufacturing or research by providing a vision of future investment needs and direction. See section 3.2 in Chapter 3.

-

2. Transparency relates to having transparent approaches to developing sectoral infrastructure investment plans, sourcing projects, providing targeted funds and using data management processes that foster investment. Lack of transparency is a major barrier to mobilising project developers and investment decision makers. Improved transparency, on the other hand, equips investors with information they can use to justify subsequent commitments and positions in one or more pipelines or develop exit strategies. See section 3.3 in Chapter 3.

-

3. Prioritising, expediting or optimising strategically valuable projects – and shepherding them through development processes – constitutes a critical step in building robust pipelines aligned to long-term climate objectives. Developing and implementing low-carbon projects at scales and rates far beyond current volumes, including projects involving more than one country, is often hindered by complex institutional arrangements and misaligned regulatory processes. See section 3.4 in Chapter 3.

-

4. Project support refers to various elements of the investment-enabling environment that affect the risk-return profiles of projects such as efforts by governments to: bridge investment gaps, overcome investment barriers, unlock important but challenging sectors or technologies, and mobilise actors. These include policy incentives, the supply of public funds and institutional support, and the provision of effective and efficient project preparation facilities where needed. See section 3.5 in Chapter 3.

-

5. Eligibility criteria ensure a pipeline of projects is properly aligned to or in support of long-term climate objectives. Such criteria necessitate strong systems to assess which projects should be promoted and set conditions of how strategies like the NDCs are “translated” into project pipelines. They can provide guidance on, for instance, which projects should be built and supported and which should not (such as to avoid expensive economic stranding of assets). Each of the case studies presented in Chapter 3 includes, to some extent, systematic processes for identifying eligible projects and supporting them.

-

6. Dynamic adaptability describes the capacity of governments to keep project pipelines aligned with policy objectives over time, to be pertinent and relevant in the long-term, and tailored to changing external conditions, avoiding expensive path dependency or lock-in. To develop project pipelines that are dynamic and adaptable, governments should make efforts to ensure pipelines are informed by long-term strategic planning of investment pathways. See section 3.7 in Chapter 3.

Many of these factors and the associated approaches are already applied, to some extent, by governments and public institutions aiming to mobilise private sector investment. The case studies and factors were specifically chosen to be widely applicable beyond the country or region in question. The factors are well understood solutions to common infrastructure investment barriers (see, for instance Annex Table 2.B.1 in Annex 2.B): including: the existence of clear leadership structures, methods to prioritise important projects or ensuring infrastructure plans are kept pertinent to changing environmental conditions over time.

The case studies show that important actions to develop project pipelines are already being taken by policy makers in a range of settings. These examples (and others summarised throughout Chapter 3) offer lessons to other countries on what worked, what did not, and other good project pipeline practices.

References

[32] Abramskiehn, D. et al. (2017), Supporting National Development Banks to Drive Investment in the Nationally Determined Contributions of Brazil, Mexico, and Chile, Inter-American Development Bank, Washington DC, https://publications.iadb.org/bitstream/handle/11319/8520/Supporting-National-Development-Banks-to-Drive-Investment-in-the-Nationally-Determined-Contributions-of-Brazil-Mexico-and-Chile.PDF?sequence=1&isAllowed=y (accessed on 16 October 2017).

[33] ADB (2017), Catalyzing Green Finance: A Concept for Leveraging Blended Finance for Green Development, Asian Development Bank, Manila, Philippines, https://www.adb.org/sites/default/files/publication/357156/catalyzing-green-finance.pdf (accessed on 05 October 2017).

[27] Bhattacharya, A. et al. (2016), Delivering on sustainable infrastructure for better development and better climate, Brookings Institution, http://www.lse.ac.uk/grantham/ (accessed on 04 October 2017).

[28] Bielenberg, A. et al. (2016), Financing change: How to mobilize private-sector financing for sustainable infrastructure, McKinsey & Company, London, http://newclimateeconomy.report/workingpapers/wp-content/uploads/sites/5/2016/04/Financing_change_How_to_mobilize_private-sector_financing_for_sustainable-_infrastructure.pdf (accessed on 04 October 2017).

[17] BIS (2014), “Understanding the challenges for infrastructure finance”, Bank for International Settlements, http://www.bis.org/publ/work454.pdf (accessed on 04 October 2017).

[45] Boyd, R. et al. (2017), The Productivity of International Financial Institutions' Energy Interventions, Climate Policy Initiative, San Francisco, https://climatepolicyinitiative.org/wp-content/uploads/2017/03/The-Productivity-of-International-Financial-Institutions%E2%80%99-Energy-Interventions.pdf (accessed on 05 November 2017).

[39] Corfee-Morlot, J. et al. (2012), “Towards a Green Investment Policy Framework: The Case of Low-Carbon, Climate-Resilient Infrastructure”, OECD Environment Working Papers, No. 48, OECD Publishing, Paris, https://doi.org/10.1787/5k8zth7s6s6d-en.

[18] G20 Leaders (2014), G20 Leaders' Communiqué, Brisbane Summit, 15-16 November 2014, http://www.g20.utoronto.ca/2014/brisbane_g20_leaders_summit_communique.pdf (accessed on 12 January 2018).

[14] GCEC (2016), The Sustainable Infrastructure Imperative: Financing for Better Growth and Development - The 2016 New Climate Economy Report, Global Commission on the Economy and Climate, http://newclimateeconomy.report/2016/wp-content/uploads/sites/4/2014/08/NCE_2016Report.pdf (accessed on 04 October 2017).

[35] GCEC (2014), Better Growth Better Climate: The 2014 New Climate Economy Report, Global Commission on the Economy and Climate, http://newclimateeconomy.report/2016/wp-content/uploads/sites/2/2014/08/NCE-Global-Report_web.pdf (accessed on 04 October 2017).

[25] Gouldson, A. et al. (2015), “Accelerating Low-Carbon Development in the World's Cities”, Global Commission on the Economy and Climate, http://newclimateeconomy.report/workingpapers/wp-content/uploads/sites/5/2016/04/NCE2015_workingpaper_cities_final_web.pdf (accessed on 30 November 2017).

[11] IEA (2017), World Energy Balances 2017: An Overview Global trends, International Energy Agency, Paris, http://www.iea.org/publications/freepublications/publication/WorldEnergyBalances2017Overview.pdf (accessed on 15 June 2018).

[22] International Energy Agency (IEA) and International Renewable Energy Agency (IRENA) (2017), Perspectives for the Energy Transition: Investment Needs for a Low-Carbon Energy System, http://www.energiewende2017.com/wp-content/uploads/2017/03/Perspectives-for-the-Energy-Transition_WEB.pdf (accessed on 04 October 2017).

[23] IRENA (2017), “Stranded Assets and Renewables: How the energy transition affects the value of energy reserves, buildings and capital stock - a REmap working paper”, International Renewable Energy Agency, http://www.irena.org/DocumentDownloads/Publications/IRENA_REmap_Stranded_assets_and_renewables_2017.pdf (accessed on 01 November 2017).

[9] ITF (2017), ITF Transport Outlook 2017, OECD Publishing, Paris, https://doi.org/10.1787/9789282108000-en.

[38] Kennedy, C. and J. Corfee-Morlot (2012), “Mobilising Investment in Low Carbon, Climate Resilient Infrastructure”, OECD Environment Working Papers, No. 46, OECD Publishing, Paris, https://doi.org/10.1787/5k8zm3gxxmnq-en.

[6] Kortekaas, B. (2015), Infrastructure Finance in the Developing World: Infrastructure Pipeline and Need for Robust Project Preparation, Group of 24 (G24), Washington DC, https://www.g24.org/wp-content/uploads/2016/05/MARGGK-WP04.pdf (accessed on 04 October 2017).

[41] McNicoll, L. et al. (2017), “Estimating Publicly-Mobilised Private Finance for Climate Action : A South African Case Study”, OECD Environment Working Papers, No. 125, OECD Publishing, Paris, https://doi.org/10.1787/a606277c-en.

[4] Mercer and Inter-American Development Bank (IDB) (2016), Building a Bridge to Sustainable Infrastructure: Mapping the Global Initiatives, https://doi.org/10.18235/0000674.

[10] Mirabile, M. and J. Calder (2018 forthcoming), “Clean Power for a Cool Planet: Electricity infrastructure plans and the Paris Agreement”, OECD Environment Working Papers, OECD, Paris.

[5] Nassiry, D., S. Nakhooda and S. Barnard (2016), Finding the pipeline: Project preparation for sustainable infrastructure, Overseas Development Institute, https://www.odi.org/sites/odi.org.uk/files/resource-documents/11075.pdf (accessed on 04 October 2017).

[2] OECD (2017), Getting Infrastructure Right: A framework for better governance, OECD Publishing, Paris, https://doi.org/10.1787/9789264272453-en.

[3] OECD (2017), Investing in Climate, Investing in Growth, OECD Publishing, Paris, https://doi.org/10.1787/9789264273528-en.

[21] OECD (2017), Selected Good Practices for Risk Allocation and Mitigation in Infrastructure in APEC Economies, OECD, Paris, http://www.oecd.org/daf/fin/private-pensions/Selected-Good-Practices-for-Risk-allocation-and-Mitigation-in-Infrastructure-in-APEC-Economies.pdf (accessed on 11 January 2018).

[13] OECD (2016), G20/OECD Support Note on Diversification of Financial Instruments for Infrastructure, OECD, Paris, https://www.oecd.org/g20/topics/financing-for-investment/G20-OECD-Support-Note-on-Diversification-of-Financial-Instruments-for-Infrastructure.pdf (accessed on 04 October 2017).

[7] OECD (2015), Aligning Policies for a Low-carbon Economy, OECD Publishing, Paris, https://doi.org/10.1787/9789264233294-en.

[1] OECD (2015), Mapping Channels to Mobilise Institutional Investment in Sustainable Energy, Green Finance and Investment, OECD Publishing, Paris, https://doi.org/10.1787/9789264224582-en.

[43] OECD (2015), Overcoming Barriers to International Investment in Clean Energy, Green Finance and Investment, OECD Publishing, Paris, https://doi.org/10.1787/9789264227064-en.

[37] OECD (2015), Policy Guidance for Investment in Clean Energy Infrastructure: Expanding Access to Clean Energy for Green Growth and Development, OECD Publishing, Paris, https://doi.org/10.1787/9789264212664-en.

[42] OECD (2008), Public-Private Partnerships: In Pursuit of Risk Sharing and Value for Money, OECD Publishing, Paris, https://doi.org/10.1787/9789264046733-en.

[26] OECD/United Cities and Local Government (2017), Subnational Governments Around the World: A First Contribution to the Global Observatory on Local Finances, OECD, Paris, https://www.oecd.org/regional/regional-policy/Subnational-Governments-Around-the-World-%20Part-I.pdf (accessed on 22 November 2017).

[40] Prag, A., D. Röttgers and I. Scherrer (2018), “State-Owned Enterprises and the Low-Carbon Transition”, OECD Environment Working Papers, No. 129, OECD Publishing, Paris, https://doi.org/10.1787/06ff826b-en.

[44] Rohde, N. (2015), Assembly Lines for Project Development: The Role of Infrastructure Project Preparation Facilities (PPFs), Heinrich Böll Stiftung: North America, Washington DC, https://us.boell.org/sites/default/files/2-10-14_nora_rohde_project_preparation_facilities.pdf (accessed on 06 October 2017).

[19] Rydge, J., M. Jacobs and I. Granoff (2015), “Ensuring new infrastructure is climate-smart”, The Global Commission on the Economy and Climate, http://newclimateeconomy.report/2015/wp-content/uploads/sites/3/2015/10/Ensuring-infrastructure-is-climate-smart.pdf (accessed on 05 October 2017).

[24] Stadelmann, M., G. Frisari and A. Rosenberg (2014), The Role of Public Finance in CSP: Lessons Learned, Climate Policy Initiative, Venice, Italy, https://climatepolicyinitiative.org/wp-content/uploads/2014/06/The-Role-of-Public-Finance-in-CSP-Lessons-Learned.pdf (accessed on 10 October 2017).

[30] Trabacchi, C. et al. (2016), The Role of the Climate Investment Funds in Meeting Investment Needs, Climate Policy Initiative, San Francisco, https://climatepolicyinitiative.org/wp-content/uploads/2016/06/The-role-of-the-Climate-Investment-Funds-in-meeting-investment-needs.pdf (accessed on 05 October 2017).

[8] UN Environment (2017), The Emissions Gap Report 2017: Synthesis Report, UN Environment, https://wedocs.unep.org/bitstream/handle/20.500.11822/22070/EGR_2017.pdf?sequen%E2%80%A6 (accessed on 01 November 2017).

[20] UN Environment and Italian Ministry of Environment (2016), Financing the Future: Report of the Italian National Dialogue on Sustainable Finance, UN Environment, https://wedocs.unep.org/bitstream/handle/20.500.11822/16801/Financing_the_Future_EN.pdf?sequence=1&isAllowed=y (accessed on 05 October 2017).

[36] UNCTAD (2014), World Investment Report 2014: Investing in the SDGs - An Action Plan, http://unctad.org/en/PublicationsLibrary/wir2014_en.pdf (accessed on 04 October 2017).

[16] UNFCCC (2015), Enhancing Access to Climate Technology Financing: Technology Executive Committee Brief #6, http://unfccc.int/ttclear/misc_/StaticFiles/gnwoerk_static/TEC_documents/204f400573e647299c1a7971feec7ace/ea65db0ca9264cdbaefeb272dd30b34c.pdf (accessed on 04 October 2017).

[12] WEF (2013), The Green Investment Report: The ways and means to unlock private finance for green growth, World Economic Forum, Geneva, http://www3.weforum.org/docs/WEF_GreenInvestment_Report_2013.pdf (accessed on 04 October 2017).

[29] Woetzel, J. et al. (2016), Bridging Global Infrastructure Gaps, McKinsey Global Institute (MGI), https://www.mckinsey.com/industries/capital-projects-and-infrastructure/our-insights/bridging-global-infrastructure-gaps.

[31] World Bank Group (2015), Principles to Mainstream Climate Action within Financial Institutions: Five Voluntary Principles, World Bank Group, http://www.worldbank.org/content/dam/Worldbank/document/Climate/5Principles.pdf (accessed on 05 October 2017).

[15] World Bank Group and International Monetary Fund (2014), Statement by the Heads of the Multilateral Development Banks and the IMF on Infrastructure, http://www.worldbank.org/en/news/press-release/2014/11/13/statement-heads-multilateral-development-banks-imf-infrastructure (accessed on 04 October 2017).

[34] World Bank Group et al. (2013), “Long-Term Financing of Infrastructure: A Look at Non-Financial Constraints”, G20, http://g20india.gov.in/pdfs/6_Non-financial_constraints_to_LT_infra_financing_FINAL.pdf (accessed on 06 October 2017).

Governments have widely recognised the importance of green,11 low-carbon infrastructure to help establish strong economic growth and deliver low-carbon pathways (OECD, 2017[3]). In addition, the associated infrastructure projects that constitute the pipeline can themselves be an enabler for development and social progress (Nassiry, Nakhooda and Barnard, 2016[5]), so governments would do well to ensure such project pipelines are robust and effective in delivering the desired objectives. Project pipelines are mentioned often in contexts related to infrastructure investment in general, and to governments meeting their climate and development objectives specifically – and can be summarised across three themes below.

The apparent gap between available capital and investment-ready, bankable projects. The apparent investment gap is driven not by the availability of private capital (there is an oversupply of capital seeking bankable projects), but the lack of available and suitable bankable or investment-ready projects (Mercer and Inter-American Development Bank (IDB), 2016[4]; Nassiry, Nakhooda and Barnard, 2016[5]; Kortekaas, 2015[6]). A bankable or investable project is one that offers a level of returns commensurate with the risk appetite of private investors, thus making it attractive for them to invest or commit financial positions.12

The lack of available projects is not a problem restricted to climate and development investment alone, on which there is a great deal of literature (World Bank Group and International Monetary Fund, 2014[15]; UNFCCC, 2015[16]; OECD, 2017[3]). It applies equally to infrastructure investment in general and remains one of the primary impediments to bridging the evident gap between infrastructure investment demand and the supply of infrastructure finance (BIS, 2014[17]). See Annex 2.F for information on facilities to prepare projects to a bankable or investment-ready state.

Long-term vision and clarity to mobilise private finance. A number of OECD reports recommend that governments follow better practice related to infrastructure planning and investment, taking a long-term perspective, and consider developing robust project pipelines as an important means to mobilise finance and send signals of intent to investors. For instance, the OECD (2015[1]) recommends that governments establish “a national infrastructure strategy and roadmap with project pipeline” including detailing the timing, capacity needs, locations of investment, and available policy support. The OECD (2017[2]) also proposes that governments to set infrastructure objectives relevant to project pipelines such as “a national long-term strategic vision”, “clear criteria to guide the choice of delivery”, “review existing infrastructure resilience in the face of evolving natural and manmade risks and develop guidelines to future proof new infrastructures.”

International fora such as the Group of 20 countries (G20) have also recognised the importance of project pipelines in aligning investment and private sector action (OECD, 2016[13]) and, during the 2014 G20 Summit, leaders agreed that “to help match investors with projects, [they would] address data gaps and improve information on [infrastructure] project pipelines” (G20 Leaders, 2014[18]). The Global Infrastructure Hub, for instance, was established by the G20 in the same year to deliver its multi-year Global Infrastructure Initiative. Launched with a mandate to provide support for a global pipeline of bankable projects, the Global Infrastructure Hub offers a suite of tools to help investors navigate investment decision making and identify the most appropriate opportunities.

Mainstream climate considerations into investment decisions. Rydge, Jacobs and Granoff (2015[19]) pointed to the need to ensure climate concerns are properly accounted for within infrastructure investments. They suggest infrastructure and climate policies “[too often] exist in separate silos.” A joint report by UN Environment and the Italian Ministry of the Environment (2016[20]) highlights that public and private support for infrastructure is “de-linked from sustainability priorities.”

Furthermore, the OECD found that only nine of the G20 countries integrated both mitigation and adaptation considerations into infrastructure planning (OECD, 2017[3]). Not only does this de-linking impact negatively on the quality of service provided by infrastructure. it may overlook valuable co-benefits (such as cleaner air and reduced traffic congestion) and could potentially lock-in vulnerability to or future damage from the impacts of climate change. The inclusion of future damages in projects could help make projects that avoid these damages more attractive investment opportunities.

Governments have a suite of tools and institutional arrangements available to mobilise investment and overcome common barriers to infrastructure investment (as highlighted in Annex Table 2.B.1). They can, for instance:

-

procure goods and services and fund large capital projects such as transport and energy infrastructure directly from public budgets

-

direct or influence investment decisions of state-owned enterprises, which are important actors in many developing and emerging economies, particularly in the energy sector13

-

lead public-private partnerships and other initiatives often used to anchor large bulky infrastructure projects and encourage effective co-investment by public and private actors14

-

employ public instruments (risk mitigants and transaction enablers) such as guarantees that reduce or mitigate investment risks or allocate them to those actors able and willing to manage them (OECD, 2017[21])

-

support research into innovative technologies or solutions; or design policies and plans to support climate objectives and ensure domestic policies are cost-effective and well-aligned across the economy and at different levels of government (OECD, 2015[7])

-

support the development of innovative financial instruments and project finance structures to help avoid costly and burdensome administrative approaches and lower transaction costs. These include, for instance: standardising contracts, methods and processes, like those applied by the Climate Investment Funds in over 70 emerging and developing countries (see section 3.3 in Chapter 3); and encouraging the securitisation or warehousing of aggregate smaller assets into larger investment tickets (often attractive to long-term investors like pension funds).

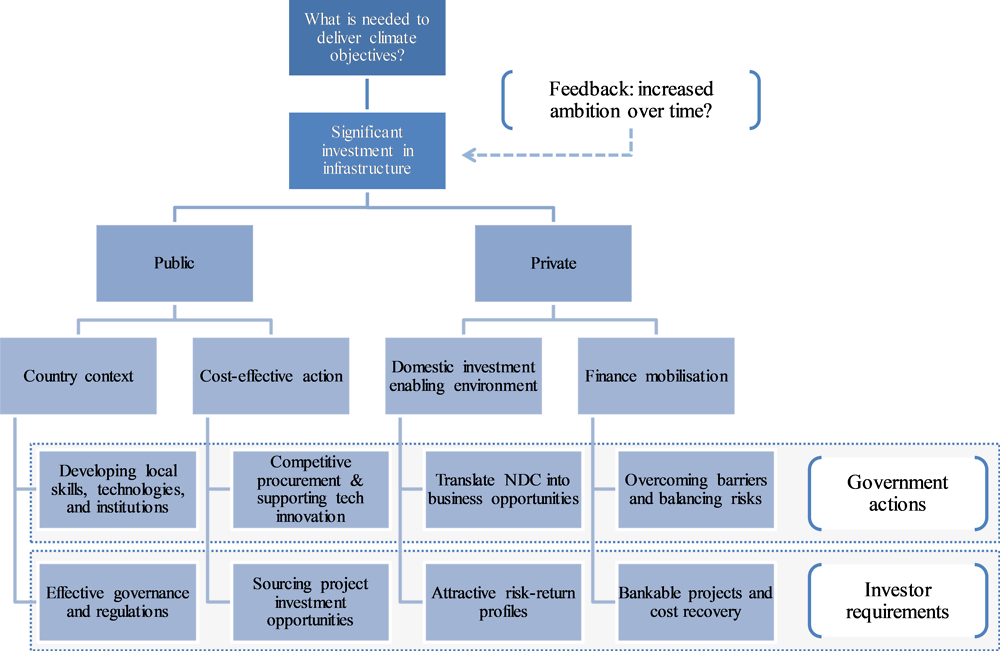

The high-level linkages between government actions and private investment needs and expectations are shown in Annex Figure 2.B.1. It highlights the various but specific roles governments have to foster, scale-up and accelerate infrastructure investment to meet long term climate objectives, like the Nationally Determined Contributions (with relevant feedback to increase ambition over time).

Note: The figure provides a simplified and illustrative overview of the various government actions and investor requirements. Relationships may not always be a one-way process between one level (e.g. private finance mobilisation) and the next (e.g. governments acting to overcome barriers). There, of course, may be feedback within levels (e.g. the domestic investment-enabling environment may also influence the extent of private finance mobilisation). NDC: Nationally Determined Contribution.

Countries’ approaches to investment planning and designing project pipelines take inputs from various areas of government, from sub-national, local regions and cities to federal ministries, agencies and regulators. Private actors carry out the majority of the investments in many countries and thus have a role in also developing project pipelines themselves.

National governments often take the lead to develop and cultivate pipelines of projects at the national level, but pipelines can of course extend to other levels of government. Local governments and cities in particular have, to various extents, their own competencies and capacities to design, develop and fund infrastructure projects.

These subnational actors are important for meeting long-term climate objectives and pledges. Cities, for instance, host more than half of the world’s population, use more than 70% of the world’s energy and emit around the same share of global greenhouse gases, and contribute the vast majority of global economic flows (e.g. 85% of global gross domestic product (GDP) was generated in cities in 2015) (Gouldson et al., 2015[25]). In December 2017, over 2 500 cities from around the world have submitted non-state actor climate pledges to the United Nations Framework Convention on Climate Change (see http://climateaction.unfccc.int for information). Indeed, a recent review of the activities of subnational governments in 100 countries, found that they were responsible for 25% of public expenditure worldwide (equivalent to 9% of global GDP) and 40% of public investment (60% in OECD countries) (OECD/United Cities and Local Government, 2017[26]).

Project pipelines will depend on many interconnected political, institutional and economic factors that affect the short- to long-term infrastructure investment and planning priorities. The resulting route to delivering mitigation objectives under the long-term climate objectives will be different for each country given the various drivers and infrastructure “starting points” including, but not limited to:

-

level of economic development and growth expectations

-

urbanisation and population growth

-

previous infrastructure investment and expected future needs

-

maturity and composition of financial capital markets

-

ambition of plans in terms of quality and scale of green infrastructure deployed

-

level of coherence and co-operation within the government and across public agencies, and between the government and private sector

-

capacities of sub-national governance (e.g. degree of autonomy of cities, states from central government)

-

government support available to foster a favourable regulatory and investment environment, creating markets to engage the private sector domestically and internationally

-

availability of local skills and technologies.

The demand for new infrastructure and corresponding investment gap as noted in section 2.2 will be higher in emerging and developing economies (Bhattacharya et al., 2016[27]; Bielenberg et al., 2016[28]; Woetzel et al., 2016[29]; GCEC, 2016[14]). In many of these countries, climate considerations may need active institutional and technical support if they are to be mainstreamed into public and private sector activities.

Public financial institutions such as national and Multilateral Development Banks (MDBs) bring important experience in supporting the design and development of national infrastructure investment plans and project pipelines. Mainstreaming climate investment considerations in national infrastructure planning and the operations of development banks remains a key research and operational priority for MDBs (Trabacchi et al., 2016[30]; World Bank Group, 2015[31]; OECD, 2017[3]) and also national development banks (Abramskiehn et al., 2017[32]).

To address investment barriers, the Asian Development Bank (ADB) recently proposed that governments consider setting up a national facility to scale-up investment in green infrastructure projects bridging gaps that hinder the sourcing of investment-grade projects (ADB, 2017[33]). The ADB Green Finance Catalyzing Facility is based on the principle that risk should be, but is often not, allocated to the parties best-suited to manage them, and proposes using concessional finance to mitigate key project risks and costs in certain situations. The provision of such finance will be ultimately conditional upon governments developing project “roadmaps” and indicators to check progress on achieving objectives.

MDBs have also supported the SOURCE platform (https://public.sif-source.org),15 which provides, inter alia, a comprehensive and harmonised compendium of climate considerations and principles to be used in investment decision making. It is available for free for government agencies in emerging countries and offers templates for the preparation of projects, including governance, technical, legal, financial, economic, environment and social aspects. Templates are further adapted to adjust to sector requirements and different project stages. SOURCE also generates data (from the project portfolio, national and/or global levels) which can be assessed to develop analytics, benchmarks and indicators on the performance and sustainability of infrastructure projects. In addition, SOURCE provides guidance to governments in the project preparation process and allows them to identify barriers to project bankability and provides an entry-point for investors to procure projects or find answers to queries (see Annex 2.F for the role of project preparation facilities).

Investors are often hampered by the lack of data and information on projects. According to discussions with experts undertaken for this report, however, government efforts to build project pipelines need to be (but currently are not often) communicated using parameters that investors work with or with the appropriate “presentation” medium that balances transparency and confidentiality.16

Better data and availability of information offer the opportunity to develop robust cross-country assessments of infrastructure gaps. As suggested by OECD (2017[3]), project pipelines not only improve information on future needs (e.g. what projects are needed later?), but also provide better information and data dissemination tools (e.g. what projects or processes are working now or have worked in the past, and what could be improved?).

In turn, better data and knowledge helps inform policy-making, providing valuable policy feedback and better investment planning as governments take steps to turn low-carbon objectives into investible business plans and establish markets for infrastructure investment. See also efforts to increase transparency in section 3.3 in Chapter 3. Examples of efforts to improve infrastructure data include, but are not limited to:

-

The OECD, European Investment Bank, Global Infrastructure Hub and the Club of Long Term Investors together launched the “Infrastructure Data Initiative” in 2017 to address the issue of establishing infrastructure as an asset class through data collection and improving the availability of infrastructure investment data (see Annex Box 2.E.1 for information on the Global Infrastructure Hub).

-

The SOURCE platform (introduced in Annex 2.D) is an online infrastructure project preparation and data management platform, led by Multilateral Development Banks (MDBs) and managed by the not-for-profit, Sustainable Infrastructure Foundation. To date, SOURCE hosts more than 1 700 users across 44 countries, and is supporting the development of 198 infrastructure projects globally.

The Global Infrastructure Hub (Hub) was established by the G20 in 2014 to support its multi-year Global Infrastructure Initiative. Launched with a mandate to provide a global pipeline of bankable projects, the Hub offers a suite of tools to help investors navigate investment decision making and identify the most appropriate opportunities. It fosters a network among governments, the private sector and multilateral organisations to identify best practices, develop knowledge tools to bridge data gaps, address information asymmetry, improve the policy environment, and allow visibility for projects to an international audience of investors.

At the heart of the Hub is the Global Infrastructure Project Pipeline, designed to afford governments an opportunity to tap into a wide pool of international capital. The pipeline provides prospective investors with all relevant information, in a lucid format. Investors can access project profiles in a personalised dashboard and contact the relevant authority to invest with the click of a button. Projects are categorised under eight progressive stages of development based on first-hand data from governments. The global pipeline is linked to the databases of governments and MDBs, to match investors with projects of interest, and is regularly updated. Presently, the Hub lists 298 projects across 34 countries.

Analytical tools supplement the pipeline to support investors and policymakers. For instance the InfraCompass, based on an in-house capability framework developed by the Hub, assesses the capacity of 49 countries to deliver “quality” infrastructure* and evaluates the strength of their policy, legal and financial environment. An annotated matrix of risks associated with public-private partnership (PPP) projects is provided by the PPP risk allocation tool. To further its objectives, the Hub has also partnered with the OECD, World Bank Group and other multi-lateral organisations.

Together, these digital tools allow the investment community to interface with the governments and relevant authorities, allow information symmetry and channel the cross-border flow of capital to infrastructure projects.

* Noting that InfraCompass does not account for climate or sustainability factors within its definition of “quality” infrastructure.

Sources: https://www.gihub.org/; http://www.g20.utoronto.ca/2014/2014-1116-communique.html; http://www.mofa.go.jp/files/000059859.pdf [PDF]

Governments can procure or direct project development and project pipelines to help facilitate private investment. In some cases additional public support may be required to get projects “over the line” to reach an investment-ready or bankable state.17 Improving the bankability of projects in the pipeline is an important and often cited step to increase the flow of capital towards low-carbon infrastructure projects. A project preparation facility (PPF) is an entity that supports infrastructure investment by channelling a small amount of finance to overcome technical and financial barriers that prevent the project from being bankable or investable to the investment community.18, 19

Project preparation is not a pre-set activity, but rather a dynamic concept that adapts and evolves according to the needs of a country, sectors and individual projects, with the ultimate aim of reaching bankability; from supporting engineering design plans, enhancing feasibility studies, or fast-tracking government investment and procurement processes in the preparation of technical and financial documents. Pipelines are often associated with PPFs because sourcing finance and building a bankable project pipeline is made simpler when the projects are well-structured and have detailed demand, engineering, and cost analyses that highlight potential gaps (Kortekaas, 2015[6]).

Governments have an interest in ensuring projects aligned to the climate objectives are attractive to investors, added to the pipeline, and not held up before deployment. The need for PPFs varies depending on sector and country context but is a rapidly growing area of concern since the costs for global project preparation activities have been estimated at 2.5–10% of total infrastructure investment (GCEC, 2016[14]; Kortekaas, 2015[6]) or up to USD 690 billion per year.20

Discussions with experts for this report suggest that these preparation facilities will be supported with public funds. In other words, investors may rely on government support before committing their own funds to project investments. As a result, governments should properly consider and account for these costs when translating national objectives like the Nationally Determined Contributions into granular investment plans. Given their magnitude, the costs would significantly affect the overall returns on investment from designing and developing a pipeline of successful projects. They could also be a significant challenge for smaller governments or those in emerging and developing economies, and risk adding a layer of complexity when implementing low-carbon ambitions.

On their own, PPFs are not expected to overcome the wide range of non-financial constraints common to infrastructure investment, and will struggle to do so. The World Bank with others (World Bank Group et al., 2013, p. 3[34]) warns that “the same lack of skills and experience in the public sectors of developing countries vis-à-vis developing PPPs constrains the ability of PPFs to deliver results on the ground.” These possible constraints include (World Bank Group et al., 2013[34]):

-

an absence of credible partnerships between public and private actors (e.g. public-private partnerships, to the extent that this model is used)

-

insufficient capacity for project design and implementation

-

poor accountability, performance- and contract-management, or lack of co-ordination across actors

-

other considerable market and non-market barriers are also prevalent – such as high interest rates, external debt accumulation, geo-political situations (especially for cross-border or transboundary infrastructure projects), trade-offs with other policy agendas (e.g. food and water security or biodiversity protection) and so on.

PPFs provide investors with an entry point into pipeline and project procurement, a means to find answers to queries, and ways to identify investment opportunities suited to their individual requirements and appetites. Approaches to support and finance projects on a project-by-project basis may be administratively burdensome and costly for the institutions involved. Standardisation of contracts and processes, for instance, is one such method to lower these transactions costs. Given infrastructure needs and the diminishing size of projects (e.g. towards decentralised as opposed to centralised energy sources), however, many thousands, if not millions, of new and discrete projects will be required globally, with the majority located in developing and emerging economies.

A more holistic approach to project and pipeline development, including the securitisation and aggregation of smaller assets, would bring advantages if it creates a two-way exchange between investors and policy-makers to identify investment barriers and ensure possible gaps are understood earlier on in the project development cycle. This would include the government’s interface through which it engages and encourages investment from private sector actors.

Notes

← 1. See Section 3 and Box 3.1 in OECD (2017[3]) for a discussion on and the challenges related to estimating infrastructure investment, including estimates from the Global Commission on the Economy and Climate (GCEC, 2014[34]), Bhattacharya et al. (2016[26]) and UNCTAD (2014[35]).

← 2. OECD (2017[3]) suggests that, to meet development needs, investment in new infrastructure could reach USD 6.3 trillion per year over the period 2016–30, even before governments consider climate change concerns. A further 10%, around USD 0.63 trillion, may be necessary to put emissions on a pathway in line with a well-below 2°C scenario, notably including increased demand-side investments in energy. The difference between these estimates and current investment volumes (USD 3.4-4.4 trillion per year) is approximately USD 2–3 trillion per year.

← 3. The CIF is examined in more detail in section 3.3 in Chapter 3 in the context of supporting clean transport investment in cities in Viet Nam.

← 4. Argentina, Australia, Brazil, Canada, the People’s Republic of China (China), France, Germany, India, Indonesia, Italy, Japan, Korea, Mexico, the Russian Federation (Russia), Saudi Arabia, South Africa, Turkey, the United Kingdom and the United States, plus the European Union.

← 5. Since publication of the report (OECD, 2017[3]), the United Kingdom released its July 2018 “Road to Zero” strategy which sets out in detail the ambition for at least 50% of cars to be ultra low-emission by 2030. For more details, see: www.gov.uk/government/news/government-launches-road-to-zero-strategy-to-lead-the-world-in-zero-emission-vehicle-technology.

← 6. Nine at the time of writing and most from developed economies. See unfccc.int/focus/long-term_strategies/items/9971.php for more information.

← 7. The investment-enabling environment is where, as discussed by the OECD (2015[36]), governments establish strong policy and institutional frameworks (including core climate policies like carbon pricing, fossil fuel subsidy reform), and provide support to low-carbon alternative sources of energy like renewable energy.

← 8. Private sector actors are multifaceted and have fundamentally important roles in delivering project pipelines: project developers to build and operate these infrastructure projects, and prepare projects for implementation and thus foster involvement of other actors through various channels; investors to provide capital and take ownership of projects and can also bring technical and management capabilities; and supply chain actors to provide skills and manufacturing capabilities. Investors can structure project financing by taking equity or mezzanine positions, commercial loans for capital-intensive construction phases or refinancing those projects that are already operational.

← 9. When applied to the OECD estimates of annual global infrastructure needs at USD 6.9 trillion for the 15-year period to 2030 (OECD, 2017[3]).

← 10. Governments will also need to have the foresight to look to the development of “better projects” in the future; those that are more suitable to the longer term climate objectives, resilient to future changes in environmental conditions, without risk of stranding assets, and also bankable by nature.

← 11. The OECD (Kennedy and Corfee-Morlot, 2012[37]; Corfee-Morlot et al., 2012[38]) defines green infrastructure as “low-carbon, climate-resilient infrastructure projects [that] either mitigate greenhouse gas emissions and/or support adaptation to climate change in the area of transport, energy or buildings.”

← 12. Nassiry, Nakhooda and Barnard (2016[5]) explain that bankability itself is dependent on a number of important factors such as: domestic capacities to structure and negotiate projects; processes for proponent/beneficiary engagement; policy and regulatory environment; revenue generation; technology and project feasibilities; and cost or risk-return tolerance.

← 13. In China, for example, of the eight largest Chinese power companies, accounting for more than 50% of China’s generation capacity, seven are state-owned (Prag, Röttgers and Scherrer, 2018[39]). In South Africa, state-owned energy utility Eskom generates over 95% of electricity in the country (see McNicoll et al. (2017[40])).

← 14. PPPs are defined as collaboration between public and private entities in which risks, returns and financing are negotiated between the partners where the private entity provides public services for a financial return – see OECD (2008[41]) for definitions.

← 15. SOURCE is funded primarily by International Financial Institutions and led by Multilateral Development Banks, which approve the platform’s strategic direction and annual budget. The Sustainable Infrastructure Foundation (SIF), a not-for-profit organisation established in 2014 in Switzerland, manages the implementation of SOURCE platform development and delivery.

← 16. Private sector companies will likely not “publish” full project pipeline data due to the confidential nature of the project-level information and financial details, but they can provide governments with metadata that is relevant to meeting long-term climate objectives (e.g. capacity installed, emissions avoided per year).

← 17. Bankable means, from an investor perspective, that the project investment offers an appropriate return profile for the risk they take. Project preparation requires a wide array of actors to work together to bridge knowledge or capacity gaps, from legal experts to technical advisors.

← 18. Common reasons for projects to leave or drop from the project pipeline include but are not limited to: policy or regulatory risks; technology risks; supply chain constraints; lack of developer track record; or lack of affordable financing options. However, the barriers are likely linked to the underlying domestic policy framework such as presented in (OECD, 2015[42]). The aim of project preparation is to develop projects to a point where they attract sufficient interest from investors (Rohde, 2015[43]), and are intended to “translate demand for infrastructure into bankable projects” (Kortekaas, 2015[6]).