Annex A. Country profiles

This annex provides detailed information about how OECD and selected non-OECD countries design financial incentives to promote savings for retirement. Each country profile includes the following sections: i) the structure of the funded private pension system; ii) the tax treatment of retirement savings (contributions, returns on investment, funds accumulated and pension income); iii) the description of non-tax incentives; iv) the social treatment of contributions and benefits; v) the tax treatment of pensioners; and vi) the incentives for employers.

Australia

Structure of the funded private pension system

Tax treatment of contributions

Contributions are taxed, but usually at a lower rate than the individual’s marginal income tax rate. There are two main types of contributions with different tax treatments: “concessional” or before-tax contributions and “non-concessional” or after-tax contributions.1 The government also makes tax-exempt contributions to eligible individuals.

Concessional contributions

Concessional contributions include mandatory employer contributions (“superannuation guarantee” contributions), employee “salary sacrifice” contributions and voluntary deductible contributions.2 The superannuation guarantee contribution is paid regardless of age. However, individuals between 65 and 74 years of age may only make voluntary deductible contributions if they satisfy a “work test”. Individuals aged over 75 cannot make voluntary deductible contributions.

Concessional contributions are taxed at 15% on amounts up to the concessional contributions cap. In 2017-18, this cap is AUD 25 000. It is indexed to wages. From 1 July 2018 it is possible for individuals with balances of less than AUD 500 000 to carry-forward up to 5 years unused concessional cap space.

Contributions over the concessional contributions cap are taxed at the individual’s marginal income tax rate. The individual also has to pay the excess concessional contribution (ECC) charge on the increase in the tax liability to neutralise the benefit of having excess contributions in the concessionally taxed environment. To reduce the tax liability, the individual receives a non-refundable tax offset equal to the 15% tax already paid by the fund on the excess amount. Any contributions over the cap count towards the individual’s non-concessional contributions. The individual may choose to withdraw up to 85% of the excess concessional contributions from the superannuation fund to help pay the income tax. Any excess concessional contributions withdrawn no longer count towards non-concessional contributions cap.

For high-income earners, with an adjusted taxable income of more than AUD 250 000, the tax rate on concessional contributions that are considered above the AUD 250 000 threshold is 30% instead of 15%. The additional tax is imposed on the whole amount of the contributions, up to the concessional cap, if salary and wages are above the threshold. Otherwise, the additional tax is only imposed on the portion of the contribution that takes the individual over the threshold. If the adjusted taxable income is less than AUD 250 000, but adding concessional contributions brings the total above that threshold, the 30% tax rate applies only to the part of the contribution above the threshold. For example, if your income is AUD 230 000 and your concessional contributions are AUD 25 000, you only pay the 30% tax rate on AUD 5 000.

Non-concessional contributions

Non-concessional contributions primarily include personal voluntary contributions (which can be made as after-tax additional contributions), spouse contributions and other contributions made by one person on behalf of another person where there is no employment relationship. Excess concessional contributions not withdrawn from the fund are also included in the calculation of non-concessional contributions.

Non-concessional contributions are not taxed upon entry into the fund because they are made from money on which the individual has already been taxed at his/her marginal rate. The non-concessional contributions cap is the limit on the amount of non-concessional contributions an individual can make each year before paying extra tax. In 2017-18, this cap is AUD 100 000. Only individuals with a total superannuation balance of less than AUD 1 600 000 are permitted to make non-concessional contributions. The cap is indexed to wages.

Any non-concessional contributions above the cap in a given year automatically bring forward the next two years’ non-concessional contributions cap for people under 65 years old. This means that an eligible individual can contribute up to AUD 300 000 over a three-year period without paying the excess contributions tax. Any contributions above AUD 300 000 in that three-year period can remain in the superannuation fund and be taxed at 49%, or be withdrawn from superannuation to avoid that additional tax, and only pay tax at an individual’s own marginal tax rate on an earnings amount associated with the excess contributions.

Individuals aged between 65 and 74 are eligible to make annual non-concessional contributions of AUD 100 000 if they meet the work test (that is, they work 40 hours within a 30 day period each income year), but are not able to access the bring-forward of contributions.

A tax offset (called Spouse Super Contribution Tax Offset) may apply to after-tax contributions made on behalf of non-working or low-income-earning spouses.3 It is payable to the contributor (not the spouse). The tax offset is calculated as 18% of the lesser of:

-

AUD 3 000, reduced by one dollar for every dollar that the sum of the spouse’s income, total reportable fringe benefits and reportable employer superannuation contributions exceeds AUD 37 000; and

-

the total amount of contributions paid.

State contributions

The government provides a low-income super tax offset (LISTO) of up to AUD 500 annually for eligible individuals on adjusted taxable income of up to AUD 37 000. The amount payable is calculated by applying a 15% match rate to concessional contributions made by, or for individuals (it is effectively a refund of the tax paid on concessional contributions). This contribution is tax exempt.

Tax treatment of returns on investments

Investment earnings on superannuation assets in the accumulation phase are taxed at a rate of 15%.

People who have reached preservation age but are under 65 and not retired can still access a transitional super income stream (TRIS) but earnings on the amount supporting it will be taxed at 15%.

Funds are eligible for imputation credits for dividend income and a one-third capital gains tax reduction on assets held for at least 12 months.

Tax treatment of funds accumulated

From 1 July 2017, the transfer balance cap imposes a lifetime limit of AUD 1 600 000 on the amount of superannuation assets that may be transferred to a retirement phase account (i.e. an account supporting retirement income streams) with tax-free investment earnings. Assets in excess of the AUD 1 600 000 transfer balance cap must be rolled back to an accumulation phase account (where investment earnings will be taxed at 15%) or withdrawn from superannuation. The transfer balance cap is indexed in line with the consumer price index and increases in AUD 100 000 increments. The transfer balance cap applies only to the amount of assets that may be transferred into a retirement phase account. The value of retirement phase accounts may grow above AUD 1.6 million if future earnings exceed withdrawals.

Transfers in excess of AUD 1 600 000 are subject to excess transfer balance tax. This is a tax on notional earnings attributed to the excess. The tax is 15% in 2017-18. From 2018, the rate is 15% the first time an individual has an excess transfer balance and 30% for second and subsequent breaches.

Tax treatment of pension income

Benefits withdrawn from a superannuation fund have three components: a tax-free component, a taxed element and an untaxed element. Non-concessional (after-tax) contributions are tax-free when withdrawn from the superannuation account. Concessional (before-tax) contributions are taxable when withdrawn. If the superannuation fund has paid taxes on those contributions (as described earlier), this corresponds to the taxed element. If the fund has not paid taxes, this corresponds to the untaxed element.

Individuals do not pay tax on the tax-free component when they withdraw it, regardless of their age or the type of withdrawal. The tax treatment of the taxable component (taxed element and untaxed element) depends on the age at which the individual retires and the type of withdrawal, as described in the tables below. The preservation age is the age at which individuals can access their superannuation assets if they are retired. It depends on the date of birth (55 years old for people born before 1 July 1960, increasing gradually to 60 for people born from 1 July 1964).

Non-tax incentives

The state helps low-to-middle income earners to boost their retirement savings through the “super co-contribution”. This contribution is tax-exempt. The super co-contribution is a government matching contribution for eligible individuals. Individuals younger than 71 are eligible for a super co-contribution if they make a voluntary non-deducted contribution (in their own name) in the income year, have a total income lower than the higher income threshold (AUD 51 813 for 2017-18), at least 10% of their total income is from employment or business and their total superannuation balance is less than AUD 1 600 000. The match rate is up to 50%. Individuals with an income below the lower income threshold (AUD 36 813 for 2017-18) can get 50 cents for each dollar contributed, up to the full maximum entitlement (AUD 500 for 2017-18). For every dollar that the individual earns above the lower income threshold, the maximum entitlement is reduced by 3.333 cents.

Social treatment

Social contributions are not levied on mandatory pension contributions.

Withdrawals from the taxed and untaxed elements before 60 years old are subject to Medicare Levy (2% since July 2014). After 60 years old, only withdrawals from the untaxed element are subject to Medicare Levy.

Tax treatment of pensioners

The public pension (Age Pension) is included in taxable income. The Age Pension is paid to people who meet age and residency requirements, subject to a means test.

Most senior Australians receive tax relief through the seniors and pensioners tax offset (SAPTO). SAPTO is available to taxpayers in receipt of a taxable Australian Government pension, as well as to Australians who are of Age Pension age and who meet all of the Age Pension eligibility criteria except the means test. In 2017-18, it is worth a maximum of AUD 2 230 for a single senior and AUD 1 602 for each member of a senior couple. It builds on the statutory tax-free threshold and the low income tax offset to ensure that eligible single senior Australians with a rebate income up to AUD 32 279 in 2017-18 (or AUD 28 974 for each member of a couple) pay no income tax or the Medicare levy. The tax offset cannot exceed the total tax paid.4

-

For single individuals: the maximum offset is reduced by 12.5 cents for each dollar of rebate income in excess of AUD 32 279, cutting out at a rebate income of AUD 50 119.

-

For couples: the maximum offset is reduced by 12.5 cents for each dollar of rebate income in excess of AUD 28 974 (AUD 57 948 of combined income), cutting out at a rebate income of AUD 41 790 (AUD 83 580 of combined income).

Incentives for employers to set up or contribute to a funded private pension plan

Employer superannuation guarantee contributions are deductible against corporate income tax.

Employers who fail to make the required contributions are subject to additional tax and penalties. This additional tax is the superannuation guarantee charge. It is paid to employees to compensate for non-payment of compulsory superannuation. The charge is higher than the basic superannuation requirement as it includes interest and administrative components. It is not deductible.

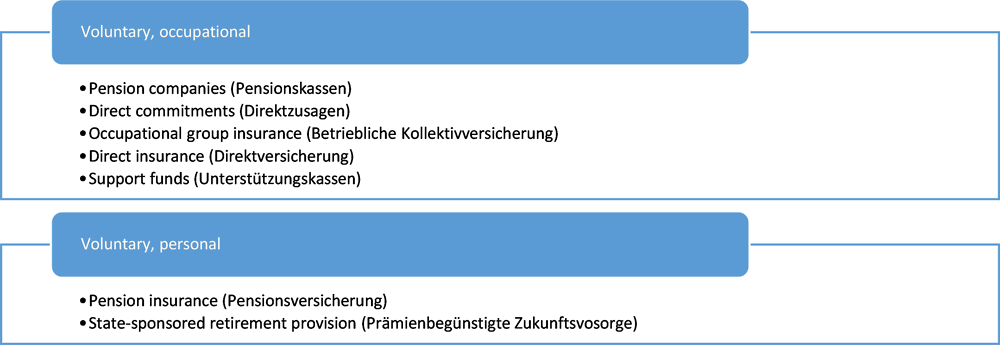

Austria

Structure of the funded private pension system

Tax treatment of contributions

Pension companies and occupational group insurance

Employee contributions are taxed at the individual’s marginal income tax rate. They cannot exceed the sum of annual employer contributions (although an employee can contribute up to EUR 1 000 even when the employer contributes less than EUR 1 000 per year). These contributions are treated as special expenses.

25% of an individual’s special expenses (individual private pension contributions plus other special expenses) are tax-deductible up to the limit of EUR 2 920 per year for a single person and EUR 5 840 if the spouse’s income does not exceed EUR 6 000. If the annual salary exceeds EUR 36 400 these limits are gradually decreased and no tax-deductible special expenses can be claimed if the annual salary exceeds EUR 60 000. From 2016, special expenses are no more deductible for new pension contracts. For contracts concluded before 1 January 2016, the deductions continue to be applicable for a maximum period of 5 years.

Employer contributions are not considered as income for the employee.

An extra 2.5% insurance tax is levied on both employee and employer contributions.

Direct insurance

Employee contributions are taxed at the individual’s marginal income tax rate. They cannot exceed the sum of annual employer contributions (although an employee can contribute up to EUR 1 000 even when the employer contributes less than EUR 1 000 per year). Contributions exceeding EUR 1 000 are treated as special expenses. From 2016, special expenses are no more deductible for new pension contracts. For contracts concluded before 1 January 2016, the deductions continue to be applicable for a maximum period of 5 years.

Employer contributions up to EUR 300 per year are tax-free for the employee. Contributions in excess of EUR 300 are considered as taxable income for the employee and can be considered as special expenses.

An extra 4% insurance tax is levied on both employee and employer contributions.

Direct commitments and support funds

Employees do not contribute. Employer contributions are not considered as income for the employee. The 4% insurance tax applies to support funds but not to direct commitments.

Personal pension plans

Contributions to personal pension plans are done from after-tax income (therefore they are taxed at the individual’s marginal rate of income tax). These contributions are treated as special expenses and attract a 25% tax relief up to a limit. From 2016, special expenses are no more deductible for new pension contracts. For contracts concluded before 1 January 2016, the deductions continue to be applicable for a maximum period of 5 years.

There is no tax relief for state-sponsored retirement provision plans.

An extra 4% insurance tax is levied on individual contributions.

Tax treatment of returns on investments

Investment income is tax-exempt for pension companies, occupational group insurance, direct insurance, support funds and personal pensions.

Investment income is considered as company profit and subject to profit tax for direct commitments.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

The tax treatment of pension income depends primarily on the type of plan:

-

Pension companies and occupational group insurance: Pensions are taxed as earned income at the individual’s marginal rate of income tax. The portion of pension accrued by employer contributions is fully taxed. Only 25% of the portion of pension accrued by employee contributions is taxed.

-

Direct insurance and personal pension insurance: Pensions are taxed as earned income at the individual’s marginal rate of income tax from the moment the total value of benefits paid exceeds the capital value of the pension at retirement. It means that pension benefits are tax-free until that point in time.

-

Direct commitments and support funds: Pensions are taxed as earned income at the individual’s marginal rate of income tax.

-

State-sponsored retirement provision: Withdrawals are tax-exempt if the entitlements are transferred to an occupational or personal pension plan or used to buy an annuity. If they are paid-out as a lump sum, the individual has to pay back 50% of the government subsidies and a 27.5% tax on capital gains.

Lump sum payments are taxed as ordinary income unless the payment does not exceed the amount of EUR 12 000. In this case, only 50% of the normal tax rate has to be paid. This applies to all lump sum payments which result from terminations of pension plans.

Non-tax incentives

The minimum term of a state-sponsored retirement provision plan is 10 years and only individuals not yet receiving social security pension benefits can open such plans. The plan must provide a capital guarantee. Personal contributions to a state-sponsored retirement provision plan can attract government matching contributions. The matching contribution rate corresponds to a fixed rate of 2.75% plus a variable rate depending on the annual general level of interest rate. For 2018, the variable rate is 1.5% (thus the total matching rate is 4.25%). As of 1 January 2018, the maximum personal contributions considered to calculate the government contribution is EUR 2 825.60 (thus the maximum government matching contribution for 2018 is EUR 120.09). No tax is levied on matching contributions. If the individual takes the benefits as a lump sum payment, s/he has to pay back 50% of the government subsidy and pay an additional 27.5% tax on the capital gains with retro-active effect.

It is also possible to get government matching contributions for employee contributions to direct insurance plans. The match rate is 2.75% plus a variable rate depending on the annual general level of interest rate for contributions up to EUR 1 000.

Social treatment

Social contributions are levied on employee/individual contributions but not on employer contributions.

Pensioners do not pay most social contributions but do pay for sickness insurance (5.1%).

Tax treatment of pensioners

Old-age public pension is considered as an income and subject to the individuals’ marginal income tax rate.

Retired persons are entitled to a tax credit. For couples, the tax credit amounts to EUR 764 for sole earners with income up to EUR 19 930 and if the spouse’s income does not exceed EUR 2 200. Otherwise the tax credit is EUR 400. The tax credit is linearly reduced to 0 between EUR 17 000 (EUR 19 930 for sole earners) and EUR 25 000 of income.

Additional voluntary contributions are possible in the public pension system (Höherversicherung) and lead to benefits taxed differently. Everyone with a public pension scheme can make additional contributions. Contributions can be defined by the individual. The contribution limit for 2018 is EUR 10 260. The contributions are deductible as special expenses up to the individual’s personal limit. The additional amount granted in pension benefits by these additional contributions depends on the amounts contributed, gender, age at the time of the contribution and the age at retirement. 75% of these additional benefits are tax-exempt. 25% are taxed at the individual’s marginal rate of income tax. Under certain conditions, benefits resulting from these contributions can be fully tax exempt, if they result from contributions up to EUR 1 000.

13th and 14th month pensions (Sonderzahlungen) attract a particular tax treatment. They are tax free up to an amount of EUR 620 per year. If the received amount is between EUR 621 and the value of 2 times the average monthly gross pension income (max. EUR 2 100), there is no tax levied. If the value of 2 times the average monthly gross pension exceeds EUR 2 100, the amount between EUR 621 and EUR 2 100 is taxed at a fixed rate of 6%. If the amount received exceeds 2 times the average monthly gross pension, the excess amount is taxed at the individual’s marginal income rate.

Incentives for employers to set up or contribute to a funded private pension plan

Pension companies and occupational group insurance: Employer contributions are tax-deductible company expenses, up to 10% of salary, provided that the total benefit target including social security benefits does not exceed 80% of current salary.

Direct insurance: Employer contributions up to EUR 300 per year are exempt from non-wage labour costs.

Direct commitments and support funds: Allocations to internal reserves are tax-deductible against income and corporation tax, up to 10% of salary, if the total benefit target including social security benefits does not exceed 80% of current salary.

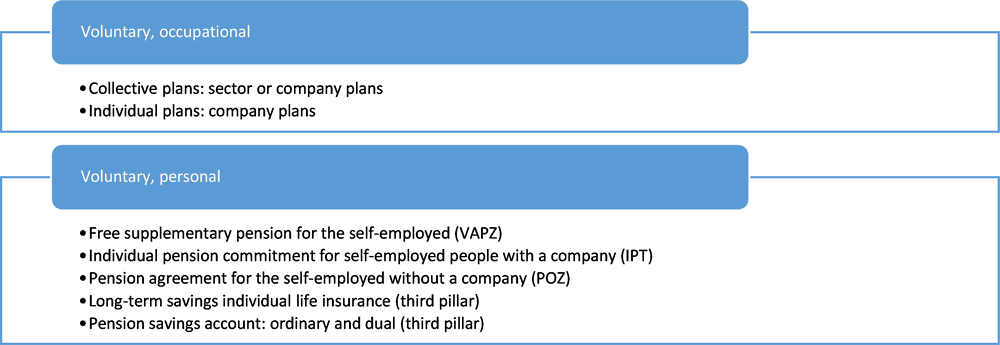

Belgium

Structure of the funded private pension system

Tax treatment of contributions

Occupational pension plans

Employer contributions to an occupational pension plan are not considered as taxable income for the employee.

Employee contributions to an occupational pension plan are rare. They are eligible for a non-refundable tax credit of 30% of the amount contributed.5

Employee and employer contributions enjoy tax relief only to the extent that total retirement benefits, including the statutory pension, do not exceed 80% of the last gross annual salary.6

The employer must pay an annual 4.4% tax on the total contributions paid (employer plus employee) under group life insurance contracts. This tax is not due in the case of a “social” pension scheme (i.e. a plan with solidarity components).7 It is not due either under institutions for occupational retirement provision (IORP).

Personal pension plans for the self-employed

There are three types of personal pension plans for the self-employed. VAPZ plans can be opened by any self-employed person. By contrast, only the self-employed with a company can open an IPT plan, while only those without a company can open a POZ plan.

Contributions to VAPZ plans are deductible from professional income. Contributions to VAPZ plans cannot exceed 8.17% of professional income, up to EUR 3 187.04 in 2018 (respectively 9.40% of professional income for “social” VAPZ plans, up to EUR 3 666.85).

Contributions to IPT plans are deductible from taxable income only to the extent that total retirement benefits, including the statutory pension, do not exceed 80% of the last gross annual salary. The self-employed individual must pay an annual 4.4% tax on the total contributions paid.

Contributions to POZ plans are eligible for a non-refundable tax credit of 30% of the amount contributed. The self-employed individual enjoys tax relief only to the extent that total retirement benefits, including the statutory pension, do not exceed 80% of the last gross annual salary. The self-employed individual must pay an annual 4.4% tax on the total contributions paid.

Third pillar personal pension plans

Individual contributions to third pillar pension plans are eligible for a non-refundable tax credit of 30% of the amount contributed.

In the case of pension savings accounts, the maximum contribution is EUR 960 per year in 2018. Alternatively, the individual may opt for a dual account, allowing for contributions up to EUR 1 230, with a tax credit of 25% (instead of 30%). The pension savings account shall have been subscribed by an individual aged 18 or over, but less than 65, and for at least 10 years.

In the case of long-term savings individual life insurance, contributions cannot exceed 6% of professional income, up to EUR 2 310 in 2018 (respectively 15% of professional income when professional income is no more than EUR 1 920 in 2018). The individual must pay an annual 2% tax on the total contributions paid. The insurance contract shall have been subscribed by an individual younger than 65, and for at least 10 years.

Tax treatment of returns on investments

Pension plans directly withhold a 9.25% profit sharing tax from the pension account. Pension savings accounts (third pillar) are exempted from profit sharing tax.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

Occupational pension plans

The tax treatment of occupational pension income depends on the form of the pay-out option and the source of the contributions. In the case of a lump sum capital payment, the part of the capital that has accrued in respect of the employer’s contributions is generally taxed at 16.5% (plus municipal tax). In case the individual withdraws from the statutory age of retirement (65 years old increasing gradually to 67) and remained active until that age, the tax rate is reduced to 10% (plus municipal tax).

The part of the capital that has accrued in respect of the employee’s contributions is taxed at 10% (plus municipal tax) if withdrawn following death or retirement, and at age 62 (63 as of 2019) at the earliest (16.5% for the capital that has accrued in respect of contributions made before 1993).

Annuities are taxed at the individual’s marginal rate of income tax. Annuities are rare in practice. Programmed withdrawals are not allowed in Belgium.

Personal pension plans for the self-employed

Upon withdrawal from VAPZ plans (from age 62 or 63 as of 2019), the accumulated capital is converted into a virtual income for tax purposes. The virtual income is then taxed at the individual’s marginal income tax rate. The virtual income is determined by applying a conversion rate to the accumulated capital (between 4% and 4.5%) and has to be declared during a certain period (13 years, except when the individual withdraws from age 65, in which case, the declaration duration is only 10 years).

Withdrawals from IPT plans are generally taxed at 16.5% (plus municipal tax). In case the individual withdraws from the statutory age of retirement (65 years old increasing gradually to 67) and remained active until that age, the tax rate is reduced to 10% (plus municipal tax).

Withdrawals from POZ plans are taxed at 10% (plus municipal tax) if withdrawn following death or retirement, and at age 62 (63 as of 2019) at the earliest.

Third pillar personal pension plans

Third pillar pension plans are paid as a lump sum. That lump sum is taxed at the rate of 8% for pension savings accounts and 10% for long-term savings individual life insurance (no municipal tax). If the pension plan has been opened when the individuals was younger than 55, the tax is calculated on the capital accumulated until age 60. If the pension plan has been opened when the individuals was 55 or older, the tax is calculated on the capital accumulated when the contract reaches 10 years. Individuals can choose to withdraw the money when the anticipated tax is due, or to delay withdrawal and the payment of the tax when they get entitled to a pension (62 or 63 as of 2019). In the latter case, individuals can continue contributing after age 60 with no further tax due on the additional capital accumulated.

Non-tax incentives

No such incentives.

Social treatment

Employers must pay social contributions at the rate of 8.86% on their contributions to an occupational pension plan, which is lower than the usual rate for social contributions.

For the self-employed, social security contributions are not levied on contributions to IPT plans. They are levied on contributions to POZ plans. VAPZ contributions are considered as social contributions.

There is a special social contribution of 3% on the portion of contributions exceeding EUR 32 472 (for 2018) per year (so-called Wyninckx contribution). This applies to all plans except third pillar plans, but is mostly relevant for IPT plans.

Employee contributions to occupational plans and individual contributions to third pillar plans are treated in the same way as salary and are thus subjected to the same social contributions (13.07%).

Third pillar lump sums are not subject to social contributions.

Pensioners with a pension above a minimum threshold pay a social contribution of 3.55% for health and disability insurance. The minimum threshold is EUR 1 306.12 since 1 September 2010 for a single pensioner without dependents (EUR 1 517.60 for pensioners with dependents). The effect of the contribution cannot lead to a pension payment inferior to this monthly amount.

There is also a “solidarity” contribution levied on pension income exceeding EUR 2 478.95 per month. This contribution ranges from 0% to 2% of the gross pension.

Tax treatment of pensioners

Public pension income is taxed at the individual’s marginal rate of income tax.

Incentives for employers to set up or contribute to a funded private pension plan

Employer contributions to an occupational pension plan are deductible as business expenses to the extent that total retirement benefits, including the statutory pension, do not exceed 80% of the last gross annual salary.

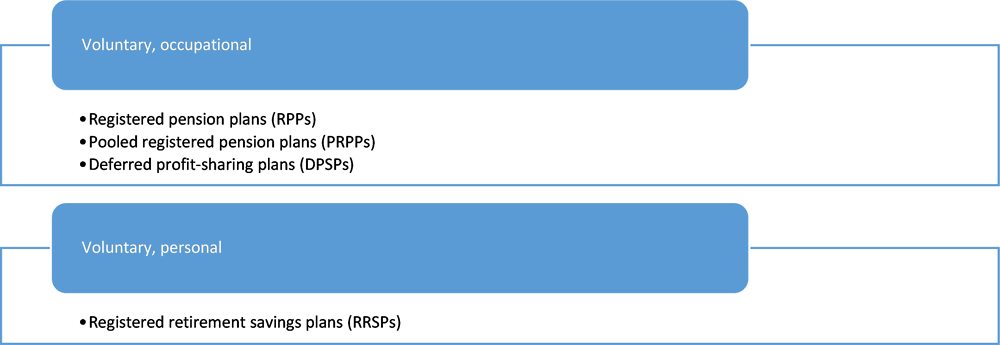

Canada

Structure of the funded private pension system

Tax treatment of contributions

Pension contributions made within the applicable limits are deductible from income.

There is a penalty tax of 1% per month for excess over-contributions made to an RRSP or a PRPP (i.e. contributions in excess of CAD 2 000 over the applicable RRSP/PRPP limit). Over-contributions, including those made within the CAD 2 000 over-contribution allowance, are not deductible from income.

Limits apply to contributions to RRSPs, PRPPs, DPSPs and defined contribution RPPs. Limits apply to pension benefits provided under a defined benefit RPP:

-

Annual contributions of 18% of earnings are permitted to be made to an RRSP and defined contribution RPP, up to a specified dollar limit (CAD 26 230 and CAD 26 500 respectively for 2018).

-

Defined benefit RPPs are permitted to provide pension benefits of 2% of earnings per year of service, up to 1/9th of the DC RPP limit per year of service (CAD 2 944 for 2018).

-

Annual contributions to a DPSP are limited to 18% of earnings up to one-half of the defined contribution RPP limit (CAD 13 250 for 2018).

-

The RPP and RRSP dollar limits are indexed to average wage growth.

The RPP and RRSP limits are integrated in order to provide comparable retirement savings opportunities whether an individual saves in an RPP, an RRSP, a PRPP, a DPSP or a combination of these plans. This is achieved through the pension adjustment (PA), which reduces an RPP or DPSP member’s annual RRSP limit by the amount of annual RPP and/or DPSP saving.

-

For defined contribution RPP members and DPSP members, the PA is equal to the sum of employer and employee contributions.

-

For defined benefit RPP members, the PA is an estimate of the contributions needed to fund the annual benefit accrued under the plan (based on a pension cost factor of 9 multiplied by the annual benefit accrued under the plan).

-

PRPP contributions must be made within an individual’s available RRSP limit.

Unused RRSP room is carried forward to future years.

In general terms, contributions to (or benefit accruals under) these plans must cease and payments/withdrawals must commence by or after the end of the year in which the plan member attains 71 years of age. In particular, an RRSP must be converted to a Registered Retirement Income Fund (RRIF) for this purpose. While defined benefit RPP members may not accrue pension benefits after the year in which they attain 71 years of age, employers may make any necessary contributions to a defined benefit RPP that are required to ensure the plan is fully funded in respect of all members and retirees, including those over age 71.

An individual who is 72 years of age or older, may, based on the individual’s accumulated unused RRSP room, contribute to a spousal RRSP until the end of the year in which the spouse reaches 71 years of age.

Tax treatment of returns on investments

Returns on investments are not taxed.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

Payments and withdrawals from pension and retirement savings plans are included in income for regular tax purposes and taxed at the applicable rate. Income tax is generally withheld on such payments and withdrawals.

Lump sum payments from an RPP, where they are permitted, generally are not treated differently than periodic pension payments for tax purposes (i.e., they are included in income and taxed at the applicable rate) except for the purposes of the Pension Income Credit and pension income splitting (lump sum amounts are not eligible). Where a lump sum amount is permitted to be transferred to another registered plan or used to purchase an annuity (e.g., where a member terminates their membership in, or retires under, an RPP), the transfer is tax-free (i.e. there are no immediate tax consequences). The transferred amounts would be included in income for tax purposes when withdrawn from the receiving registered plan or when received as annuity payments.

The Pension Income Credit (PIC) is a non-refundable tax credit provided on the first CAD 2 000 of eligible pension income. The credit rate is 15% federally.

A pension income splitting measure permits seniors and pensioners to allocate up to one-half of their eligible pension income to their spouse or common-law partner for tax purposes.

Eligible pension income for the Pension Income Credit and pension income splitting includes periodic pension payments from an RPP, regardless of the recipient’s age, and other types of pension income (i.e., income from an RRSP annuity, RRIF, PRPP and DPSP annuity) as of age 65.

Generally, pension and RRSP assets may not be withdrawn tax-free, either in a lump-sum or on a periodic basis. However, tax-free withdrawals from an RRSP may be made by first-time home buyers for the purchase of a home or by those pursuing qualifying education or training programs, under the Home Buyers’ Plan (HBP) and the Lifelong Learning Plan (LLP) respectively. Withdrawals are limited to CAD 25 000 under the HBP and CAD 20 000 under the LLP. HBP and LLP withdrawals must be repaid to an RRSP in regular repayments over a specified period, otherwise the repayment amount is included in income for tax purposes.

Non-tax incentives

No such incentives.

Social treatment

Social programme contributions (Canada Pension Plan contributions and Employment Insurance premiums) are not levied on employer contributions to an RPP, PRPP or DPSP, since employer contributions to these plans are excluded from an employee’s earnings. Employee contributions to an RPP or PRPP attract social programme contributions since such contributions are made out of an employee’s earnings. Contributions to an RRSP, which are generally made out of employment or self-employment earnings, attract social programme contributions.

Social programme contributions are not levied on pension income.

Tax treatment of pensioners

Public pension benefits (Canada Pension Plan and Old Age Security (OAS) benefits) are included in income for regular tax purposes and taxed at the applicable rate, with the exception of the Guaranteed Income Supplement (GIS), which is a non-taxable supplement to OAS provided to low-income seniors.

The Age Credit is a non-refundable tax credit provided to individuals age 65 and over on an amount of CAD 7 333 for 2018. The credit amount is reduced by 15% of income over a threshold of CAD 36 976 (for 2018) and is eliminated when income exceeds CAD 85 863 (for 2018). Both the credit amount and the income threshold are indexed to inflation annually.

Incentives for employers to set up or contribute to a funded private pension plan

Employer contributions to an RPP, a PRPP or a DPSP are deductible for the employer for income tax purposes.

Social programme contributions (Canada Pension Plan contributions and Employment Insurance premiums) are not levied on employer contributions to an RPP, PRPP or DPSP, since employer contributions to these plans are excluded from an employee’s earnings.

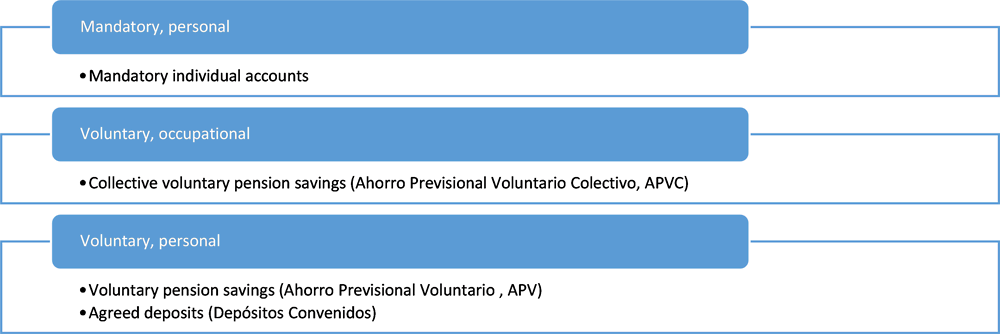

Chile

Structure of the funded private pension system

Tax treatment of contributions

Members of the pension system contribute 10% of their salary to mandatory personal accounts. These contributions are tax-exempt. There is an upper limit for the salary taken into account for contributing to the system of 78.3 UF.8

Members may also contribute to voluntary accounts. These contributions are tax-exempt up to a certain limit. Regarding contributions to APV or APVC, there are two tax regimes available for members:

-

Regime B: contributions are tax-exempt, up to a limit of 50 UF per month or 600 UF per year. Under this regime, voluntary contributions are deducted before taxation.

-

Regime A: contributions are not deducted before taxation.

Agreed deposits are contributions settled between the employer and the worker. These savings may only be withdrawn upon retirement and they are not subject to taxation up to a maximum of 900 UF. Contributions above this limit are taxed at the individual’s marginal rate of income tax.

Tax treatment of returns on investments

Returns on investments are not taxed in general.

Workers making voluntary contributions under regime A, withdrawing the funds and not using them to complement the mandatory pension, pay taxes upon withdrawal on the yield obtained from the amount withdrawn, at the individual’s marginal rate of income tax.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

Pension income is subject to income tax.

Upon retirement, pensioners who can finance a pension greater than 100% of the maximum pension with solidarity payment and greater than 70% of the average monthly taxable wage over the last ten years, are entitled to withdraw the surplus as a lump-sum payment (i.e. funds remaining in the individual account after calculating the necessary savings to obtain the aforementioned pension). This available surplus is tax-exempt up to a maximum annual amount equivalent to 200 UTM, and the total exemption may not exceed 1 200 UTM.9 If members choose to withdraw the entire surplus in one year, the maximum exemption is 800 UTM. This exemption applies to all savings (mandatory and voluntary) done at least 48 months prior to retirement. In the case of agreed deposits, if an individual withdraws more than 900 UF but less than the limit of the surplus, the return on investment over the excess of 900 UF is taxed.

Workers may fully or partially withdraw the balance accumulated through voluntary contributions at any time, not only upon retirement. If the worker used regime B, these funds are subject to a special additional tax and are considered income for the year the withdrawals were made. The special additional tax is calculated differently depending on when the withdrawal is made:

-

Withdrawal before meeting the conditions for retirement: The withdrawal is subject to one-off additional tax at the time of withdrawal at a rate between 3% and 7%. This rate is calculated as 0.03 + [1.1 × (ICR - ISR)/R] where ICR corresponds to the amount of income tax that the individual would have to pay by adding the withdrawal to other taxable income for the fiscal year; ISR corresponds to the amount of income tax that the individual would have to pay if no withdrawals were made; R corresponds to the amount of the withdrawal.

-

Withdrawal for pensioners or those who meet requirements for retirement: The withdrawal is subject to one-off additional tax at the time of withdrawal at a rate calculated as (ICR - ISR)/R.

If the worker used regime A, s/he does not have to pay the additional tax described above. In the case of withdrawal of funds before retiring, the worker loses the government matching contribution and pays tax on the return on investment. If voluntary contributions under regime A are used to complement the mandatory pension, the part of the pension financed with these voluntary savings is deducted before taxation.

Non-tax incentives

Workers between 18 and 35 years old with an income lower than 1.5 times the minimum wage are entitled to a government matching contribution for the first 24 contributions to the pension system. This contribution consists in two payments: a subsidy to employers for hiring this type of workers and a direct contribution to the worker’s pension account of the same amount. The matching contribution is equivalent to 50% of the mandatory contribution of the worker if the wage is lower than or equal to the minimum wage; or 50% of the mandatory contribution over the minimum wage if the wage is greater than the minimum wage and lower than 1.5 times the minimum wage.

Women aged 65 or older are entitled to a government subsidy for each child alive at birth. The subsidy is equivalent to 18 months of contributions over the current minimum wage at the moment of the birth of the child, invested in fund type C since 2009 or since the birth of the child, whichever is later.

Workers making voluntary contributions under regime A (usually low-earnings workers whose wages are either exempted from income tax or have a low income tax rate) are entitled to a government matching contribution, corresponding to 15% of the amount saved annually, subject to a limit. These funds are added to the individual account each year but have a separate accounting. For each calendar year, the government matching contribution is limited to 6 UTM. If the member withdraws the funds instead of using them for retirement, the matching contribution is lost. It is not required to contribute to the mandatory system to get the matching contribution but only members of the pension system may contribute to voluntary accounts.

Social treatment

Social contributions (pension 10%; healthcare 7%; unemployment insurance 3% - of which 0.6% is paid by the employee and 2.4% by the employer - ; insurance for work-related accidents and occupational diseases 0.95%; disability and survivor insurance 1.41%) are levied over the gross salary. There is a maximum salary for social contributions of 78.3 UF. Pension contributions are part of the social security contributions.

Pensioners pay 7% of pension income for health coverage. Since 2011, pensioners eligible for a solidarity pension (who must belong to the 60% poorest population, among other requirements) are exempted to pay contributions for health insurance. Between 2012 and 2016, pensioners that belonged to the 80% poorest population and were not eligible for a solidarity pension, benefited from a reduction in the contribution for healthcare. Since November 2016, this latter group of pensioners is exempted to contribute for healthcare.

Tax treatment of pensioners

The basic solidarity pension and the pension supplement are taxed at the individual’s marginal rate of income tax. In practice however, they are tax exempt, because the beneficiaries are in the lower part of the income scale.

Incentives for employers to set up or contribute to a funded private pension plan

Agreed deposits and contributions in APVC are considered as an expense for the employer and therefore reduce corporate income tax.

Czech Republic

Structure of the funded private pension system

Tax treatment of contributions

Individuals’ contributions into supplementary pension insurance plans are paid from after-tax income. Contributions of and below CZK 1 000 a month are matched by government contributions. Contributions above CZK 12 000 a year are tax-deductible up to CZK 24 000 a year.

Employer contributions into supplementary pension insurance plans are not considered as taxable income for the employee up to CZK 50 000 a year. Above they are taxed as income

Tax treatment of returns on investments

Returns on investment are not subject to income tax during participation in the system but taxed according the rules described below in out payments from the system.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

If the participant would like to withdraw money and the conditions for lump sum or pension are not met, this closes the contract and any government contributions are returned to the government, and if the participant in such a case used tax incentives, the amount previously deducted must be taxed.10 In addition, the returns on investments and employers contributions are taxed at 15%.

Annuities are tax-free, including when withdrawn up to 5 years before the official retirement age. Programmed withdrawals for more than 10 years are tax-free. They are otherwise taxed as income. Lump sums are taxed at 15% but the tax base consists only of the returns on investments and employer’s contributions payed after January 2000.

Non-tax incentives

Individuals’ contributions made into supplementary pension insurance plans are matched each month by the government according to the following scale:

-

CZK 230 if the individual contributes at least CZK 1 000.

-

CZK 210 if the individual contributes between CZK 900 and CZK 999.

-

CZK 190 if the individual contributes between CZK 800 and CZK 899.

-

CZK 170 if the individual contributes between CZK 700 and CZK 799.

-

CZK 150 if the individual contributes between CZK 600 and CZK 699.

-

CZK 130 if the individual contributes between CZK 500 and CZK 599.

-

CZK 110 if the individual contributes between CZK 400 and CZK 499.

-

CZK 90 if the individual contributes between CZK 300 and CZK 399.

-

Nothing if the individual contributes less than CZK 300.

Employer contributions cannot be matched. The government contributions are not subject to income tax and social contributions.

Social treatment

Individuals’ contributions above CZK 12 000 per year and up to CZK 24 000 are not included in income subject to social contributions.

Social contributions are not levied on employer’s contributions up to the limit of CZK 50 000 per year.

Social contributions are not levied on pension income.

Tax treatment of pensioners

Old-age public pay-as-you-go pensions are not taxed up to a value of 36 times the minimum wage.

Taxpayers can claim a tax credit of CZK 24 840 per year. Since 2014, the tax credit can also be claimed by individuals receiving an old-age public pension.

Incentives for employers to set up or contribute to a funded private pension plan

Employer contributions into supplementary pension insurance plans are deductible from corporate tax - more precisely they constitute expenses for tax purposes.

Social contributions are not levied on employer’s contributions up to the limit of CZK 50 000 per year.

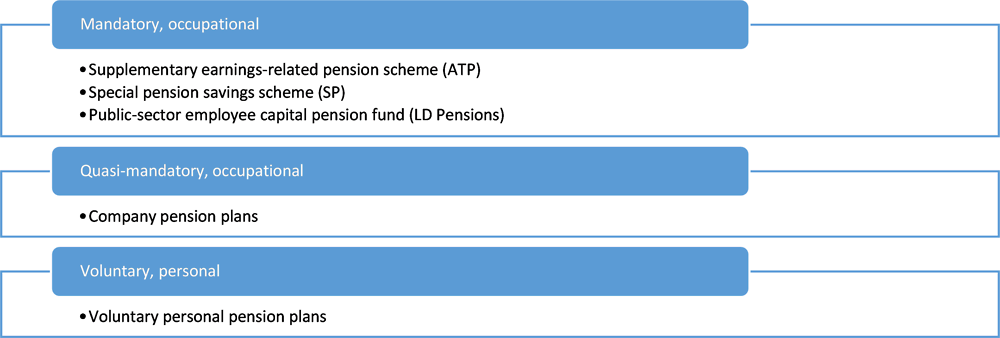

Denmark

Structure of the funded private pension system

Quasi-mandatory occupational plans and voluntary personal plans can run three different kinds of scheme: age savings (Aldersopsparing), programmed withdrawal (Ratepension/Ophørende livrente) or life annuity (Livrente).

Tax treatment of contributions

Employer contributions are not considered as taxable income to the employee.

In age savings, individual contributions are subject to labour market tax and income tax. There is a contribution limit of DKK 5 100 in 2018. The last five years before retirement age, the contribution limit is increased to DKK 46 000 per year.

For all the other plans, employee/individual contributions are deductible from income tax but still subject to the labour market tax (this tax is paid by the pension institutions):

-

ATP: contributions are tax-exempt.

-

Programmed withdrawal: contributions are tax-exempt up to DKK 54 700.

-

Life annuity: contributions are tax-exempt.

-

LD pensions: the scheme has not received contributions since 1980.

-

SP: the scheme has not received contributions since 2010.

Tax treatment of returns on investments

Returns are subject to taxation, regardless of the form of the pension scheme. Returns are taxed yearly at a fixed rate of 15.3%. Returns include dividends, interests and changes in the market value of the assets.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

For ATP, programmed withdrawal and life annuity schemes, pension income is subject to personal income tax (but not to labour market tax).

Pension income from age savings schemes is tax-exempt and does not affect entitlements for the housing support and public pensions.

If an individual chooses to withdraw assets from programmed withdrawal or life annuity schemes before retirement age, the sum will be taxed at a fixed rate of 60%. Many occupational plans do not however offer this opportunity of early withdrawal.

Non-tax incentives

No such incentives.

Social treatment

No such contributions.

Tax treatment of pensioners

Public basic old-age pension is subject to personal income tax (but not to labour market tax).

Incentives for employers to set up or contribute to a funded private pension plan

Contributions made by employers are, like other parts of salaries, fully tax deductible as expenses.

Estonia

Structure of the funded private pension system

Tax treatment of contributions

In mandatory pension plans, only employee contributions and government matching contributions are possible. Employee contributions (2% of the gross salary withheld by the employer) are fully tax-deductible. Government matching contributions (4% of the gross salary) are not considered as taxable income to the employee. They are paid from the employer’s social contributions (20% for pension insurance and 13% for health insurance).

Individuals receive a non-refundable tax credit on their contributions to voluntary pension plans corresponding to 20% of the contributions made during the year, up to 15% of gross income or EUR 6 000. The EUR 6 000 limit applies to the total employee and employer contributions. Contributions are otherwise taxed at the fixed income tax rate (20% in 2018). The tax credit only applies to contract opened for at least 5 years when the individual reaches 55.

Employer contributions to voluntary pension plans are considered as a part of the employee’s salary and are not subject to personal income tax as long as they do not represent more than 15% of individual contributions, up to EUR 6 000. As the EUR 6 000 limit is common to employee and employer contributions, any employer contribution reduces the available room for individual contribution entitled to the tax credit.

Tax treatment of returns on investments

Returns on investments are not taxed.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

Pension payments from the mandatory funded pension system and the pay-as-you-go public pension system are treated together in terms of taxation. An annual basic exemption is available to all Estonian residents who receive taxable income below EUR 25 200, and pension income exceeding the limit is taxed as income at the fixed income tax rate (20% in 2018).

The taxation of pension payments from voluntary pension plans depends on when the individual withdraws money and the form of pension payments.

-

Early withdrawals (before age 55) are taxed at a rate of 20% except if the person has become fully and permanently disabled. For disabled people, lump sums are taxed at a rate of 10%, while life annuities are tax-free.

-

Withdrawals from the age of 55 are taxed at a rate of 10% for fixed-term annuities and tax free for life annuities, provided that more than 5 years have passed since the conclusion of the contract. Withdrawals are taxed at a rate of 20% if less than 5 years have passed since the conclusion of the contract.

-

All taxed withdrawals should be taken into account in yearly income when calculating the basic tax exemption.

Non-tax incentives

No such incentives.

Social treatment

Employees pay 1.6% of their earnings in contributions for unemployment insurance. The taxable base is the total amount of the gross wage or salary.

Social contributions are also paid by employers on the same taxable base than employees’. The social tax is 33% of gross salary. There is a minimum lump sum payment for each employee of EUR 155.10 (in 2018). In addition, employers pay the unemployment insurance premium at a rate of 0.8% of gross salary monthly.

Social contributions are not levied on pension income.

Tax treatment of pensioners

Pension payments from the mandatory funded pension system and the pay-as-you-go public pension system are treated together in terms of taxation. Pension income exceeding the annual basic exemption is taxed as income at the fixed income tax rate (20% in 2018).

Incentives for employers to set up or contribute to a funded private pension plan

Contributions to voluntary pension plans made by the employer are classified as expenses related to business. These expenses may be deducted from the employer’s business income.

Finland

Structure of the funded private pension system

Tax treatment of contributions

Mandatory occupational plans: Employee contributions are fully tax-deductible from earned income. Employer contributions are not considered as taxable income to the employee.

Voluntary occupational group plans: Employee contributions are deductible from the employee’s earned income up to the lesser of (i) 5% of salary or (ii) EUR 5 000 per year. If the employee contributes more than the employer does, the excess amount is not deductible. For voluntary occupational plans opened before 06/05/2004, employees’ contributions are fully deductible. Employer contributions are not considered as taxable income to the employee.

If the employee contributes to the occupational group plan, the retirement age cannot be lower than the maximum statutory age (currently varying between 68, 69 and 70 years depending on the age of the insured person) to be eligible for tax relief.11 If the employee does not contribute to the plan, in practice a minimum retirement age of 55 years has been applied.

Voluntary personal plans set up by the employer: Employee contributions are not tax-deductible for the employee. Employer contributions are not considered as taxable income to the employee if they do not exceed a limit of EUR 8 500 per year. Excess contributions count as employee’ salary and are taxed at his/her marginal income tax rate.

Voluntary personal plan taken by the employee: Individual contributions are deductible from capital income up to EUR 5 000 per year. If the capital income earned in the year is lower than the amount of deductible contributions, the difference is used to calculate a tax credit applicable to earned income tax. For example, if an individual contributes EUR 5 000 to a personal plan and has EUR 3 000 of capital income, the first EUR 3 000 of contributions are used to reduce capital income to zero. The tax credit is then calculated as 30% of the remaining EUR 2 000, i.e. EUR 600. Employer contributions are considered as taxable income to the employee. If the employer provides a voluntary personal plan for its employees, each year the employer contributes to it, the tax-deductible amount of contributions to a voluntary personal plan taken by the employee declines to EUR 2 500. If the voluntary personal plan was opened before 06/05/2004, contributions paid before 2006 were deductible from earned income.

For members of voluntary personal plans since 2013, the retirement age cannot be lower than the maximum statutory age (currently varying between 68, 69 and 70 years depending on the age of the insured person) to be eligible for tax relief. In addition, early withdrawal of pension assets is possible only under strict conditions (unemployment, disability, divorce and death of a spouse). Furthermore, the minimum withdrawal period has to be 10 years.

Tax treatment of returns on investments

Returns on investments in pension plans are not taxed during the saving time until pension is actually paid out.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

Pension benefits received from mandatory occupational plans, voluntary occupational plans and voluntary personal plans provided by the employer are taxed as earned income, as part of the taxpayer’s total earned income.

Pension benefits received from voluntary personal plans taken by employees are taxed as capital income. Capital income is taxed at a fixed rate of 30% up to EUR 30 000. The excess amount is taxed at 34%.

Non-tax incentives

No such incentives.

Social treatment

Employer health insurance contribution is payable by the employer on salary income, and if e.g. pension insurance contributions constitute taxable salary, the employer and employee health insurance contributions need to be collected. The average contribution in 2018 is 0.86% of salary paid. A so-called employee per diem contribution also needs to be collected from income taxable as salary income, the rate of this contribution is 1.53% during 2018.

Similarly, if e.g. employer contributions to pension insurance are considered taxable salary income for the employee, mandatory unemployment and pension insurance contributions need to be collected.

The employer withholds the mandatory unemployment contribution from the employee’s salary, and forwards both the employer’s (in 2018, up to 2.6% of salary paid) and employee’s (in 2018, 1.9% of salary received) contribution to the Unemployment Insurance Fund (TVR).

The average mandatory pension insurance contribution rate applicable for employer is 17.75% during 2018 on salaries paid. The mandatory pension insurance rate applicable for employees depends on the age of the employee and varies between 6.35% and 7.85%.

Pension income does not form a basis for pension or unemployment insurance contributions.

There is a separate health care contribution for pension income taxable as earned income. The health care contribution rate is 1.53% for pension income in 2018.

Tax treatment of pensioners

Public pension income is subject to taxes as earned income. However, pensions are entitled to a special pension deduction. The deduction ensures that persons who only receive a small, usually public, pension get their pension tax free.

Some public pensions and add-ons are always tax free, e.g. some war related pensions and state artist pensions.

Incentives for employers to set up or contribute to a funded private pension plan

From the point of view of corporate income tax, the employer contributions to e.g. pension insurances can be deducted in the taxation of the employer, similarly to salary expenses. However, as such, there is no extra benefit in using these plans from the point of view of corporate income taxation.

As explained above, some employer (or employee) social contributions are not payable on e.g. voluntary pension insurances, if conditions are met.

France

Structure of the funded private pension system

Tax treatment of contributions

Personal income tax system

Employer contributions to all occupational pension plans (except article 82) are not considered as taxable income for the employee.

Employee contributions to occupational (except PERCO and article 82) and personal pension plans are tax deductible from income (or from taxable profit in case for Madelin contracts) up to specific limits. Contributions above the limits are taxed at the individual’s marginal rate of income tax. The following limits apply:

-

Article 39: No limit for the tax-exemption of employer contributions.

-

Article 83 and PERE: Mandatory employer and employee contributions are tax-exempt up to a limit of 8% of the annual gross wage of the employee, with the annual gross wage capped at 8 times the annual social security ceiling. The contribution limit is reduced by tax-exempt employer or employee contributions into PERCO.

-

Article 83, PERE, PERP and PREFON: The tax deduction limit for voluntary contributions is common for these four types of plan. The ceiling for a year is 10% of gross earnings of the previous year. This ceiling cannot be lower than 10% of the annual social security ceiling (EUR 3 973 in 2018) or greater than 8 times 10% of the annual social security ceiling (EUR 31 785 in 2018). This ceiling is reduced by the following contributions made in another retirement savings plan the same year:

-

Employer contributions and mandatory employee contributions into article 83 and PERE;

-

Employer contributions into PERCO;

-

Tax deductible contributions into Madelin contracts.

-

The final cap for one year is the ceiling of that year plus unused ceilings of the three previous years.

-

-

Madelin contracts: The tax deduction limit for contributions depends on the taxable profit. If the taxable profit is lower than the annual social security ceiling (EUR 39 732 in 2018) then the tax deduction is capped at 10% of the annual social security ceiling. If the taxable profit is between 1 and 8 times the annual social security ceiling, the cap is equal to 10% of the taxable profit plus 15% of the taxable profit above the annual social security ceiling. If the taxable profit is greater than 8 times the annual social security ceiling, the cap is equal to 10% of 8 times the annual social security ceiling plus 15% of 7 times the annual social security ceiling.

Employer contributions on behalf of employees into article 82 occupational plans are considered as taxable income for the employee and are not tax deductible.

Voluntary employee contributions into PERCO are not tax-deductible. However, profit-sharing contributions into PERCO are not considered as taxable income for the employee. Employer contribution into PERCO cannot exceed 16% of the annual social security ceiling and 3 times employee contributions (voluntary contributions and profit sharing contributions). Employee contributions into PERCO (voluntary contributions and profit sharing contributions) cannot exceed a quarter of the employee’s gross earnings of the past year. The cap for employee contributions into PERCO includes any contributions made into company savings plan (PEE) or intercompany savings plan (PEI).

Social taxes

So-called “social” taxes are levied on employer and employee contributions to occupational pension plans (except article 39) and on individual contributions to personal pension plans: the General Social Contribution (CSG) at the rate of 9.2% and the Social Debt Reimbursement Contribution (CRDS) at the rate of 0.5%.12 These social taxes are withheld from the salary. Part of the CSG is deductible from income tax (6.8%). Social taxes are not levied on contributions to article 39.

Tax treatment of returns on investments

For article 39, article 83, PERE and PERP, return on investment is exempt from income tax and social taxes.

Return on investment into PERCO and article 82 is not considered as taxable income during the accumulation phase. However, in case of a lump sum withdrawal, it is subject to social taxes at the rate of 17.2% (PERCO) or income and social taxes (article 82). Part of the CSG is deductible from income tax (6.8%).

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

Annuities

Annuities paid by article 39, article 83, PERE, PREFON, Madelin and PERP are subject to the same social and income taxes as public pensions. These pensions are taxed at the individual’s marginal rate of income tax after a 10% deduction. This deduction cannot be lower than EUR 383 per pensioner or greater than EUR 3 752 per household. If the individual’s pension is lower than EUR 383, then the tax deduction is equal to the pension. These pensions are also subject to CSG (8.3%), CRDS (0.5%), health contribution (1%) and the solidarity contribution for autonomy - CASA - (0.3%). Part of the CSG is deductible from income tax (5.9%).

An additional tax applies to annuities paid by article 39. The tax scale depends on the date when the annuities have begun:

-

If the annuities have begun before 1 January 2011, the part of the monthly pension below EUR 500 is not taxed, the part between EUR 500 and EUR 1 000 is taxed at 7% and the part above EUR 1 000 is taxed at 14%.

-

If the annuities have begun after 1 January 2011, the part of the monthly pension below EUR 400 is not taxed, the part between EUR 400 and EUR 600 is taxed at 7% and the part above EUR 600 is taxed at 14%.

The part of the additional tax covering the first EUR 1 000 of pension payment is tax-deductible.

Annuities paid by PERCO and article 82 are partially taxed at the individual’s marginal income tax rate and subject to social taxes (17.2%), depending on the claiming age. If the individual claims the annuity before age 50, 70% of the pension is subject to income and social taxes. If s/he claims the annuity between age 50 and age 59, 50% of the pension is subject to income and social taxes. If s/he claims the annuity between age 60 and age 69, 40% of the pension is taxed. If s/he claims the annuity from age 70, 30% of the pension is taxed.

Lump sums and programmed withdrawals

Lump sums or programmed withdrawals are not allowed for article 39, article 83, PERE and PREFON. They are not allowed either for Madelin contracts, except if the pensioner buys his/her permanent residence.

In case of a lump sum withdrawal after 8 years from article 82, the payment is divided between a capital component and a return on capital component. Only the return on capital component above EUR 4 600 (for singles) is subject to taxes, as follows:

-

if total premiums are lower than EUR 150 000, a single tax of 7.5% (or income tax at the individual’s marginal tax rate), and social taxes;

-

if total premiums are higher than EUR 150 000, a single tax of 30% (12.8% for income tax and 17.2% for social taxes) or income tax at the individual’s marginal tax rate and social taxes.

Lump sums paid by PERCO are divided into a capital component and a return on capital component. Only the return on capital component is subject to 17.2% social tax. The lump sum is not considered as taxable income.

Pensioners can withdraw up to 20% of their PERP as a lump sum. In this case, pensioners can choose between three fiscal options:

-

The lump sum is taxed at the individual’s marginal rate of income tax after a deduction of 10%. The lump sum is also subject to CSG (8.3%) and CRDS (0.5%). CSG is partially tax deductible (5.9%).

-

The income tax due for the lump sum is equal to 4 times the additional tax that would be generated by a quarter of the lump sum being taxed at the marginal rate of income tax. The lump sum is also subject to CSG (8.3%) and CRDS (0.5%). CSG is partially tax deductible (5.9%).

-

The lump sum is entirely taxed at the rate of 7.5% and subject to CSG (8.3%) and CRDS (0.5%). In this option, there is not deductible CSG. This option is only available if it is not possible to withdraw another lump sum from the same contract in the future.

Non-tax incentives

No such incentives.

Social treatment

Contributions into article 39 plans are not subject to social contributions. More precisely, three types of employer contribution are possible and depend on employer’s choice. If the article 39 management is not delegated to an insurance company, social contributions are taxed at 48% of the insurance premium. However, in case of delegated management, the rate is 24%. Employer may choose pensions as tax base with a rate of 32%.

Employee and employer contributions into article 83 and PERE are subject to employee social contributions. Employer contributions within limits are subject to a fixed social fee of 20% instead of usual employer social contributions. The contribution limit is the highest of 5% of the annual gross wage (with the annual gross wage capped at 5 times the annual social security ceiling) or 5% of the annual social security ceiling. The limit is reduced by employer contributions into PERCO. Any contributions above the limit are subject to usual employer social contributions.

Employer contributions into article 82 are subject to social contributions.

Employee contributions (except profit-sharing contributions) into PERCO are subject to social contributions. Employer contributions are subject to a fixed social fee of 20% instead of usual employer social contributions, lowered to 16% on two conditions.

Contributions to PERP and “Madelin” contracts are subject to social contributions.

Social contributions are not levied on pension income.

Tax treatment of pensioners

Public pensions are taxed at the individual’s marginal rate of income tax after a 10% tax deduction. This deduction is computed on public pensions and some private pensions (article 39, article 83, PERE, PREFON, Madelin contracts and PERP). It cannot be lower than EUR 383 per pensioner or greater than EUR 3 752 per household. If the individual’s pension is lower than EUR 383, then the tax deduction is equal to the pension.

Pensioners with low “fiscal reference income” are partially or fully exempt from social taxes. The value of the income thresholds in Table A A.4 depends on the family composition and on whether the individual leaves in metropolitan France or in Overseas Departments of France.

Incentives for employers to set up or contribute to a funded private pension plan

Employers contributions to occupational private pension plans (article 39, article 83, PERE and PERCO) are deductible from corporate tax. Regarding social contributions, the social treatment described above is also an incentive for employers to set up or contribute to a funded private pension plan.

Germany

Structure of the funded private pension system

Since 1 January 2018, social partners can agree to introduce occupational defined contribution schemes per collective agreement. These plans can be offered by life insurers and pension funds.

Tax treatment of contributions

Pension funds and direct insurance: Employer and employee contributions are tax exempt, up to 8% of the social security contribution ceiling (EUR 78 000 per year in 2018). If total contributions exceed the limit, they are taxed at the individual’s marginal rate of income tax. For members who joined the plan before 2005, in certain cases, total contributions up to EUR 1 752 could be subject to a 20% fixed tax rate (plus solidarity and church tax), provided this rate is more beneficial than the employee’s personal income tax rate and that the 8% tax deduction rule would not be used.

Direct commitments: Employer and employee contributions are tax free and no ceiling applies.

Riester pensions: Riester pensions are available only to individuals who are actively compulsorily insured in a pension system, where the benefits were reduced by the legislation in or after 2002 (i.e. employees, civil servants, unemployed in receipt of unemployment benefits, recipients of disability pensions). Riester pension plans and the corresponding incentives are also generally available to spouses and partners of civil partnership if both partners live in the European Union, are not separated from each other, make the minimum payment and conclude a Riester contract. Plan members can receive a government subsidy and pay contributions net of those subsidies. Their gross contributions (including the subsidy) can be deducted from income tax up to EUR 2 100. From a technical point of view, the government subsidy can be seen as an advance on the subsequent tax relief.13 To be incentivized, contributions must be paid to an officially certified Riester pension contract. Important certification criteria are the following. The pension has to be paid in the form of a life annuity and if the contract was signed after 2011, the payment must not occur before age 62.14 Alternatively, income drawdown until age 85 with a subsequent lifetime annuity from age 85 onwards is permitted.

Basisrente pensions: Contributions to Basisrente pensions are partly taxed at the individual’s marginal income tax rate. From a tax perspective, Basisrente pension plans are treated like pillar one pensions (mandatory state pension plan and collective retirement schemes for selected professions). These pensions are in a transition period regarding taxation. Contributions to pillar one pensions (including Basisrente contributions) are partly taxed, the exempt part growing by 2 percentage points every year, starting from 60% in 2005. This means that in 2018, 86% of a maximum EUR 23 712 for single individuals (EUR 47 424 for married couples) of contributions can be deducted from taxable income. Contributions will be fully tax exempt from the year 2025, up to a maximum equal to the maximum contribution to the miners’ statutory pension scheme (Knappschaft). The limit counts for the total contributions to mandatory state pension, collective retirement schemes for selected professions and Basisrente pensions. For contributions to Basisrente pensions to be tax-incentivized, they must be paid to an officially certified Basisrente contract. Important certification criteria are the following. The benefit payment of a Basisrente scheme must be under the form of a life annuity and if the contract was signed after 2011, the payment must not occur before age 62. The savings cannot be inherited by someone else, must be non-transferable, cannot be used as collateral, cannot be sold and cannot be subject to capitalization.

Private pension insurance: No tax relief on contributions.

Tax treatment of returns on investments

Returns on investments are not taxed.

Tax treatment of funds accumulated

There is no ceiling on the lifetime value of private pension funds. No tax applies on funds accumulated.

Tax treatment of pension income

In general, pension income is taxed at the individual’s marginal rate of income tax.

Direct commitments: Direct commitments are in transition period regarding the taxation of pension income. The tax-free allowance on benefits will be gradually phased-out from 40% of pension income up to EUR 3 000 in 2005 to 0% by the year 2040. If the payment of the benefits starts in 2018, 19.2% of pension income is tax-free, up to EUR 1 440.

Pension funds, direct insurance and Riester pensions: If the benefits of tax-deducted contributions are paid as annuities or a maximum of 30% as a lump sum, they are taxed at the individual’s marginal rate of income tax. If the annuity is lower than EUR 28.35 per month then the whole benefits can be paid as a lump sum and are also taxed at the individual’s marginal rate of income tax. Programmed withdrawals with subsequent annuitisation from age 85 from Riester plans are also taxed at the individual’s marginal tax rate. If the benefits of non-tax-deducted contributions (e.g. contributions exceeding tax limits or paid without being entitled to Riester subsidy) are paid as annuities, then only an age-dependent percentage of the pension is liable for taxation (see description below for private pension insurance).

Basisrente pensions: Due to the transitional regime, the taxation of pension income depends on the date of retirement. If the payment of the benefits started in 2005 or earlier, 50% of the benefits are subject to taxation at the marginal income tax rate of the pensioner. The taxable portion increases annually by 2 percentage points until 2020. Between 2020 and 2040, the taxable portion increases annually by 1 percentage point until reaching 100%. Therefore, pensions withdrawn on or after 2040 will be fully taxed. The tax-exempt part of the pension is determined in the year after the retirement (based on the rate applicable in the year of retirement) and is kept constant in nominal terms for the remaining lifetime of the retiree. If the payment starts in 2018 the taxation rate of the pension is 76%. The annual amounts are taxed at the individual’s marginal rate of income tax.

Private pension insurance: Because for these products, in general, contributions are not tax-favoured, some special tax rules regarding the benefits apply. Withdrawals before age 62 are not allowed for contracts signed from 2012.

-

For life-time annuities, only the so-called “income part” (i.e. returns on investment) will be taxed at the individual’s marginal rate of income tax. This income part is determined by the age at which the retiree receives the pension for the first time. For example, if the recipient receives his/her pension for the first time at age 65, the taxable income part is 18% of the annual pension. For age 60 (respectively age 67) it is 22% (respectively 17%). This amount will be taxed at the individual’s marginal rate of income tax.

-

The taxable income in case of a lump sum payment is calculated as follows. The income part is the insurance benefit in the event of survival minus the paid-in contributions. If the lump sum is paid after holding the contract at least 12 years and the recipient is 60 years or older (if the contract was signed from 2012, the payment must not occur before age 62) half of the income part will be taxed.

Non-tax incentives

Riester plans