Chapter 2. Strengths, gaps and weaknesses in Korea’s income and employment support measures

This chapter looks at the development, take-up and effectiveness of the main systems in place in Korea to support jobseekers and the working poor in finding employment and earning a decent income. The discussion focuses on four schemes: the Employment Insurance (unemployment benefit), the Basic Livelihood Security Programme (social assistance), the Employment Success Package Programme (employability support) and the Earned Income Tax Credit (in-work support). The chapter also discusses how the programmes are administered and delivered. It concludes that better enforcement of the systems already in place could go a long way in closing the social protection gaps as Korea strives to create a more robust and mature welfare state.

The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law.

The development of the Korean welfare state

Over the past few decades, Korea has not only seen fast economic growth and transformation but also rapid social development and eventually, since the mid-1980s, the construction and gradual expansion of a social protection system that better aligns with the country’s state of development. There is still a long way to go for Korea to achieve a mature and effective benefit system and employment service. In the years to come it will be important to take the right decisions on which parts of the system to expand, which new elements to introduce, if any, and how to better enforce the system and regulations currently in place. This chapter discusses this process and in particular the extent to which the main components of Korea’s social protection system succeed in providing adequate income and employment support to low-income jobseekers and the working poor.

Towards effective social security and activation

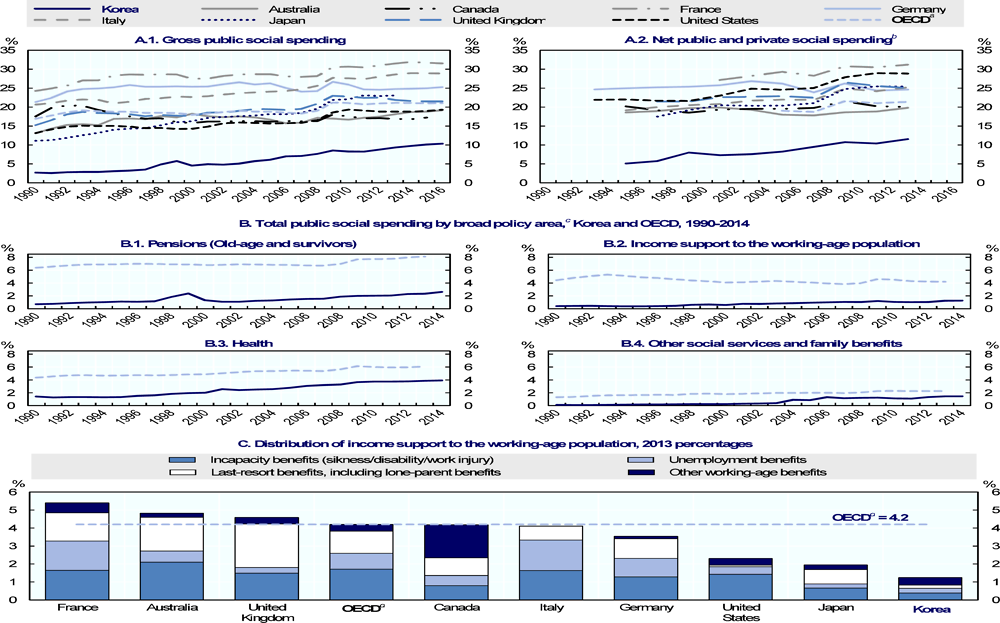

Public social spending as a percentage of GDP is still low in Korea, compared with other OECD countries, but has increased continuously since the Asian financial crisis in the late 1990s. In 2016, gross public social spending stood at 10.4% of GDP – the second lowest in the OECD (after Mexico), well below the OECD average of 21.0% and only one-third of the level in many European countries, including France and Italy (Figure 2.1, Panel A1). The gap with the OECD average is slightly smaller when also including private social spending, mandatory or voluntary, and looking at net spending which takes into account the extent to which social benefits are taxed away. Because of the low tax burden in Korea, total public and private net social spending is about two percentage points higher, each year, measured as a share of GDP (Figure 2.1, Panel A2).

Korea is among the few OECD countries still expanding their social protection system. This is reflected in the continuous growth in public social spending which more than doubled since 2000. The increase in real terms outpaced the growth rate in most OECD countries. The introduction of a public pension system (in 1988), universal health insurance (in 1989), mandatory employment insurance (in 1995) and a national social assistance programme (in 2000) all contributed to this increase. Also the increase since 2000 in the absolute share of GDP allocated to public social spending – almost six percentage points in the case of Korea – was larger than in most countries.

Rapid population ageing is the biggest factor in recent years in social spending increases in other OECD countries, more influential than system reform. This factor will be a key driver of further change in the coming years in Korea’s rapidly ageing society: social expenditure in Korea is projected to increase rapidly to at least 26% of GDP by 2050, even without further social benefit reform, because of the shift in the age structure and the gradual maturing of the current social protection system (Won and Kim, 2013[1]).

Note: GDP: Gross domestic product.

a. For gross and total public social spending: unweighted average of the 35 OECD countries; 1990-99 data are trended from 23 countries (Panel A1 and Panel B). For net public and private social spending: unweighted average of 27 OECD countries for which data are available from 2005 onwards (Panel A2).

b. Net public and private social spending are reported only for odd years. For even years, data have been interpolated from data related to odd years, for all countries and the OECD.

c. Data do not include spending on Active Labour Market Programmes which cannot be split into cash and service spending.

d. Unweighted average of the 35 OECD countries.

Source: OECD Social Expenditure Database, www.oecd.org/social/expenditure.htm.

The importance of population ageing for the cost of social protection is also reflected in the structure of public social spending. The largest and fastest increasing components of Korea’s social expenditure are pensions (which target older people only) and health care (which targets older people predominantly). This is similar in most OECD countries (Figure 2.1, Panel B) but the situation in Korea is exceptional in several ways, as emphasised in earlier OECD work (OECD, 2013[2]):

-

Pension spending, although increasing continuously since 1990, is still relatively low – around 2.6% of GDP in 2014 – because the system has yet to mature fully but also because entitlements are lower than in many other OECD countries.

-

Health spending which more than doubled in the same period, to around 4% of GDP in 2014, is predominantly in the form of services because contrary to other OECD countries Korea does not have statutory sickness benefit insurance.

-

Korea’s outlays on income support to the working-age population (unemployment benefits, incapacity benefits and last-resort benefits),1 at 1.3% of GDP in 2014, are among the lowest in the OECD area, less than one-third of the OECD average of 4.2%. This is only partly explained by the low unemployment rate in Korea.

-

Within the latter group, Korea spends much less than other OECD countries on all risks that the working-age population is possibly facing: unemployment, poor health and low income (Figure 2.1, Panel C).

Comparative OECD statistics also reveal some of the strengths of the Korean social protection system: a system which was built much later than in other countries and thereby avoided some of the mistakes of “early” welfare states. Most importantly, Korea avoided creating a social protection system with strong disincentives to work and high benefit dependence through a combination of three factors: a) a focus on activating jobseekers and the provision of active labour market programmes (ALMP), including training; b) relatively modest benefit levels and relatively strict entitlement conditions; and c) low tax rates which contribute to making work pay.

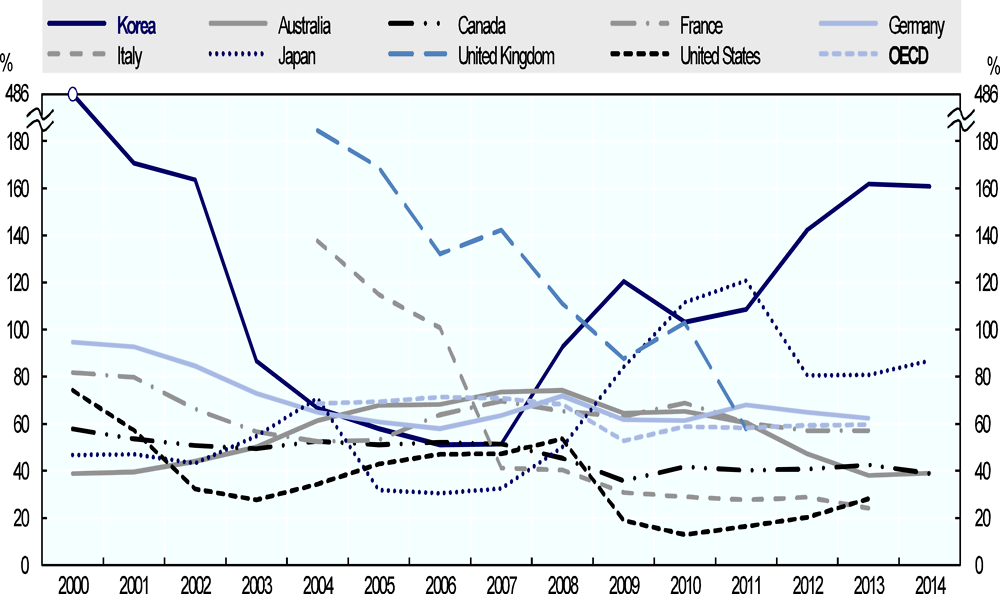

Since 2009, ALMP spending in Korea has been higher than the country’s spending on unemployment benefits (as was also the case until 2002). This is different from most other OECD countries. On average across the OECD, ALMP spending equals only around 60% of a country’s unemployment benefit spending, with some countries showing shares much lower than this (e.g. 20% in Italy and the United States or 40% in Australia and Canada). In most countries the ratio of active to passive spending dropped after the global financial crisis in 2008-09, because of the sharp rise in unemployment and corresponding spending on unemployment benefits. Korea and, to a lesser extent, also Japan, are exceptions to this trend: ALMP spending was increased after the crisis, initially through a stronger focus on job creation and more recently in the case of Korea through business start-up incentives and more investment in training. A similar picture emerged in Korea in the aftermath of the Asian crisis in the late 1990s, while in the period 2003-08 total ALMP spending was below the country’s total unemployment benefit spending (Figure 2.2). The relatively high level of active spending, relative to passive spending, is a good starting point for achieving strong reemployment outcomes for jobseekers in Korea.

to the country’s unemployment benefit spending

Note: ALMP: Active labour market programmes. Unweighted average of OECD countries for which ALMP spending for active measures (Categories 1 to 7) are available from 2004 onwards. For unemployment benefit spending, unweighted average of the 35 OECD countries; 1980-99 data are trended from 23 countries, as information for Chile, the Czech Republic, Estonia, Hungary, Iceland, Israel, Korea, Mexico, Poland, the Slovak Republic and Slovenia is not available from 1980.

Source: OECD/Eurostat Labour Market Programme Database, https://doi.org/10.1787/data-00312-en for ALMP and OECD Social Expenditure Database, www.oecd.org/social/expenditure.htm for unemployment benefit spending.

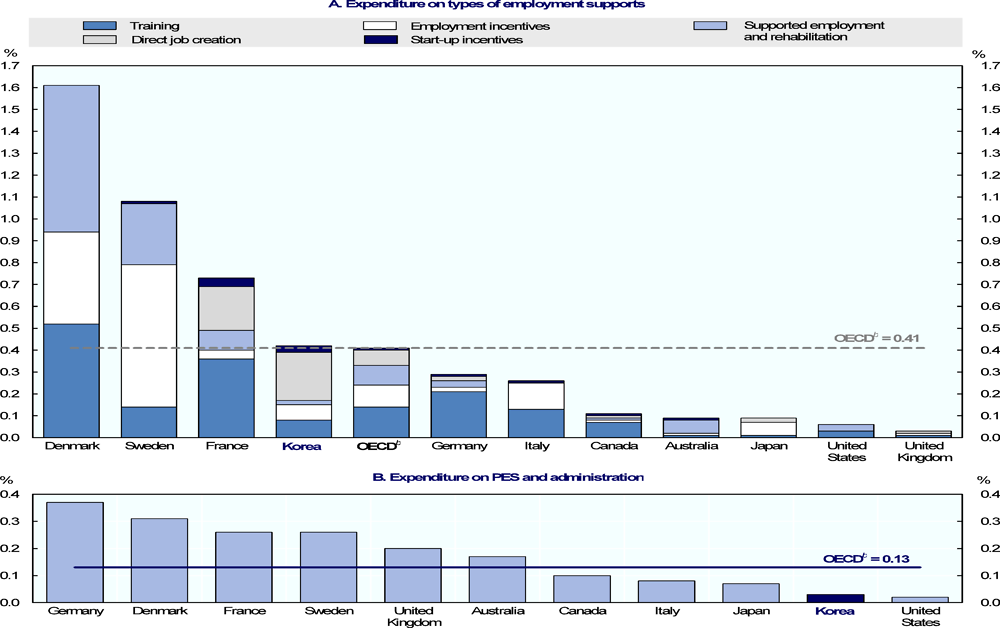

However, the composition of Korea’s ALMP spending is lagging behind the developments in many of the OECD countries which are in the forefront of labour market policy. Total spending on ALMP, at 0.42% of GDP, is at the OECD average. However, spending in Korea is still largely concentrated on direct job creation in the public sector (Figure 2.3, Panel A). Most OECD countries have downsized considerably such community employment programmes which were popular especially in the 1990s as these programmes failed to bring people back into the regular labour market. Spending on training, employment incentives and other programmes to help jobseekers of all ages improve their employability and find stable employment in the private sector is lower in Korea than in the average OECD country.

There is another factor which reduces the actual impact of ALMP spending in Korea on employment. According to administrative data, almost 80% of direct job creation is targeted at workers above the retirement age of 65 years. This type of social spending, which can be seen as a welfare programme for older workers to tackle the high poverty rates of this group, comprises roughly 40% of Korea’s total ALMP spending. Effective ALMP spending for the working-age population is therefore much lower. Would Figure 2.2 be adjusted accordingly, by removing ALMP spending for workers above age 65, Korea’s ratio of active spending to passive spending for 2014 would drop from 160% to just 100% – which is still above but much closer to the OECD average.

selected OECD countries, 2014a

Note: GDP: Gross domestic product; PES: Public Employment Service. Countries are ranked in decreasing order of expenditure in each respective panel.

a. FY 2011/12 for the United Kingdom.

b. Weighted average of the 35 OECD countries.

Source: OECD/Eurostat Labour Market Programme Database, https://doi.org/10.1787/data-00312-en.

Moreover, Korea spends comparatively little – merely 0.03% of its GDP which is less than 10% of the entire ALMP budget – on the administration of its Public Employment Service (PES) and on counselling and case-managing of jobseekers. Partly this is due to the relatively low level and short average duration of unemployment. However, low spending on administering employment services limits the effectiveness of the PES as research from around the world has shown: intense counselling of jobseekers (Crépon, Dejemeppe and Gurgand, 2005[3]; Pedersen, Rosholm and Svarer, 2012[4]), regular monitoring of their job-search requirements (Klepinger et al., 2002[5]; Borland and Tseng, 2007[6]; McVicar, 2008[7]) and low clients-per-counsellor caseloads (Hainmueller et al., 2011[8]; Hofmann et al., 2012[9]) are very effective means to achieve sustained reemployment. Most OECD countries use much larger parts of their ALMP budget to manage the PES and its clients, sometimes as much as 50% of the total funds or even more than this, like in Australia, the United Kingdom or the United States, and typically around 25% (Figure 2.3, Panel B).

Korea will have to make critical choices when further expanding its welfare state, especially the part directed to the working-age population. A main challenge will be to expand the system while keeping work incentives and the activation orientation high. Finding the right balance between entitlements and obligations and between benefits and work incentives has shown to be a challenge in many countries, especially for low-income groups. Any easing of eligibility criteria; any increase in payment levels; and any introduction of new system components to close current gaps in the system must, therefore, go hand-in-hand with expanded and strengthened activation efforts to avoid undesirable benefit dependence and assure high and sustained rates of employment and reemployment of low-income jobseekers and the working poor.

Key outcomes delivered by the social protection system

Expanding social protection will be necessary for Korea to make sure jobseekers receive the employment and income support they need to make ends meet and to find adequate and sustained employment. There are gaps in the Korean system – in the Korean literature commonly referred to as “blind spots” (Yoo, 2013[10]) – which must be fully understood and addressed in an effective and efficient way. Not all groups of people are well included in the labour market, some groups of jobseekers are poorly supported when out of work and in-work poverty is also a prevalent phenomenon to be tackled.

Job quality and labour market inclusiveness

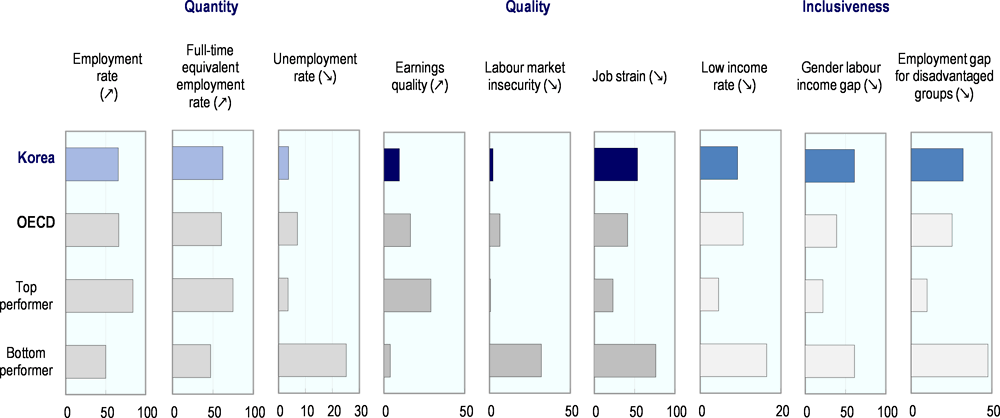

In a nutshell, the Korean labour market is characterised by low unemployment but only average levels of employment due to relatively poor labour market integration of disadvantaged groups as well as women (Figure 2.4). Moreover, many workers work in poor-quality jobs with high levels of job strain and rather low earnings. Income security in case of job loss appears to be high but this is only true for people who are entitled to unemployment benefits and many in the Korean workforce are not.

In other words, there is significant room for improvement in labour market outcomes in various areas. Governments have a number of tools at hand to influence labour market developments, many of which are not the main focus of this report. Solid social protection that allows jobseekers to find a good-quality job that matches their skills is one such tool which could be effective if complemented by well-targeted support to improve jobseekers employability and enable them to find a new job. The low social and labour market spending of the Korean government directed towards the working-age population hinders these labour market institutions from unfolding their full potential. Consequently, for many Koreans good-quality employment remains unachievable.

Note: An upward ↗ (downward ↘) pointing arrow for an indicator means that higher (lower) values reflect better performance.

Definitions: Earnings quality: Gross hourly earnings in USD adjusted for inequality. Labour market insecurity: Expected monetary loss associated with becoming unemployed as a share of previous earnings. Job strain: Percentage of workers in jobs characterised by a combination of high job demands and few job resources to meet those demands. Low income rate: Share of working-age persons living with less than 50% of median equivalised household disposable income. Gender labour income gap: Difference between average per capita annual earnings of men and women divided by average per capita earnings of men. Employment gap for disadvantaged groups: Average difference in the employment rate for prime-age men and the rates for five disadvantaged groups (mothers with children, youth who are not in full-time education or training, workers aged 55-64, non-natives, and persons with disabilities) as a percentage of the employment rate for prime-age men.

Source: OECD calculations using data for 2015 or latest year available from multiple sources. See OECD Employment Outlook 2017, https://doi.org/10.1787/empl_outlook-2017-en, Table 1.2, https://doi.org/10.1787/888933478165 for further details.

Take-up of working-age benefits

The availability of effective income and employment support is important, for at least two reasons: First, people outside the social benefit system rarely receive, or seek, targeted employment support, in Korea as much as in other OECD countries. Second, to make ends meet jobseekers not entitled to any support will have to accept jobs of any quality or will be pushed into low-quality self-employment. This is certainly happening in Korea.

In all OECD countries, including Korea, there is a big discrepancy between being unemployed and actually receiving income support and, possibly, employment support. There are many reasons why unemployment benefit take-up tends to be low: i) eligibility criteria that, legally or effectively, exclude self-employed people and certain groups of workers depending on firm size or type of contract; ii) non-eligibility in many countries for all those who quit their job voluntarily; iii) strict entitlement conditions which exclude some of those who would otherwise be eligible for support but have not been in their job long enough; iv) a mismatch between regulations and actual enforcement of legislation; and v) people’s own behaviour when temporarily unemployed, such as not claiming a benefit because people found a new job quickly or thought they will find one easily.

All these reasons play a role in Korea in explaining why only very few people who lose or leave their job actually receive any benefits, and some of them play a bigger role than in other countries. For instance, the size of the groups effectively excluded is large; the exclusion of voluntary job leavers is strict; and the enforcement of legislation is weak.

Estimating the share of job changers and job losers who access unemployment benefits is not straightforward and only possible with the use of panel survey data. Analysis based on the Korea Labour and Income Panel Survey (KLIPS) suggests that about one in ten Koreans who lost or changed a job in a given year or had an intermittent period of non-employment during that year actually received unemployment benefit.2 This is lower than corresponding benefit take-up rates in other OECD countries for which comparable data are available. For instance, in Canada and the United States where voluntary job leavers are also excluded from unemployment benefits the corresponding take-up rates are just over 30% and just below 20%, respectively. Also the figure for Australia, at close to 18%, is above the take-up figure for Korea although the Australian unemployment benefit is entirely means-tested; however, in Australia people leaving their job voluntarily can claim unemployment benefit after a period of around ten weeks of unemployment.

KLIPS analysis further suggests that also the take-up of social assistance benefits is low for the same group of people losing or changing their job in a given year. At 1.25%, the share receiving social assistance is lower than in most other OECD countries because in Korea people with work capacity hardly ever access such payments.

Poverty outcomes for the working-age population

While trying to keep a balance between the provision of income and work incentives, one critical role of a country’s benefit system is to prevent people from falling into poverty when losing their job. Comparing various Korean data sources (Survey of Household Finance and Living Conditions, Household Income and Expenditure Survey, KLIPS) with data for OECD countries, Korea finds itself in a rather unique position in regard to poverty outcomes, in several ways.

-

First, overall poverty rates of the Korean working-age population are very similar to the OECD average rate of 16%.

-

Second, the labour force status distribution of poverty deviates strongly from that of other countries. Korea has a relatively high rate of poverty among employees – explaining the in-work poverty discussion in the country – but a low poverty rate for unemployed and inactive people. Like in most OECD countries, unemployed people in Korea face higher poverty rates than inactive people.

-

Third, the small difference in poverty rates between employed and unemployed people in Korea is not a result of the transfer system: Contrary to most other OECD countries, in Korea the benefit system has relatively little impact on ultimate poverty outcomes.

The rather limited impact of the benefit system in Korea on people’s household income situation, which was already discussed in earlier OECD publications (OECD, 2013[2]), partly reflects the low take-up of social benefits among working-age individuals and Korea’s low overall level of public social spending. In the typical OECD country, the tax and transfer system through redistribution eliminates around half of the poverty level that the market income distribution alone would create. This is not the case in Korea where, on the other hand, the market income distribution of households seems to be flatter than in other OECD countries.

This is surprising at first sight because of the large difference in Korea in job quality and earnings between regular and non-regular employees and the large gender wage gap. Data from the Survey of Household Finance and Living Conditions for example suggest that market income poverty rates for those in employment range from only 5% for regular workers to almost 30% for daily workers. However, market income differences seem to be compensated to a considerable extent by the composition of households. After all, it is women who are highly over-represented among those working under precarious employment conditions. Many of them are second earners who live in a household with a first earner who is in regular employment. In turn, the ongoing trend in Korea towards smaller households and less stable family relations is likely to have a considerable impact in the medium term on income distribution and poverty outcomes.

The special situation of people with health problems

One group of people in Korea seems to suffer a much greater poverty risk: people with health problems. KLIPS data suggest that their poverty risk is almost twice as high as for people in good health. This is also the case in some other OECD countries, such as Australia, Belgium, France, Slovenia and the United States, but different from the situation in most OECD countries in which poverty risks for people in bad health are typically only slightly higher than for their healthy peers.

The poverty outcome for people with bad health might be related to the accessibility of a country’s benefit system. Across OECD countries, people in bad health tend to depend on social benefits to a larger extent, with their more frequent benefit take-up partly compensating their lower employment rate although this also depends on the value of the benefits available to this group. In Korea, social benefit take-up hardly varies by health status; people in bad health have a less comprehensive, less mature safety net available in case of unemployment or incapacity. This issue deserves special attention.

The main elements of Korea’s support system for the working-age population

Four pillars to support the unemployed and the working poor

Korea can do more to support unemployed people but also those who have a job but do not earn enough to sustain a living above the poverty threshold. Korea has four main support systems in place to assist the unemployed and the working poor:

-

Unemployment benefit provided by the Employment Insurance (EI);

-

Social assistance provided by the Basic Livelihood Security Programme (BLSP);

-

Employability support with a benefit component provided under the Employment Success Package Programme (ESPP); and

-

In-work support provided through the Earned Income Tax Credit (EITC).

In total (if only considering recipients of working age) these four systems catered for 3.88 million people in 2015, which corresponds to around 10% of the working-age population. This is one million more than just four years ago, in 2011, largely because of the expansion and maturing of EITC and ESPP. Total annual spending on these four support programmes was over 10 trillion KRW in 2015, up from around 8 trillion in 2011 (Table 2.1).3

In short (with more details below), EI provides support and income replacement benefits for workers who lose their job involuntarily, provided they are insured and eligible for payments. BLSP provides a means-tested safety net for people living below the poverty line, provided they fulfil all entitlement conditions. Given the strictness of both EI and BLSP criteria, many Koreans will not be eligible for payments from either of the two support programmes. ESPP covers some of this gap for a small number of jobless people needing particular help to access the labour market. EITC covers some of the income gap for workers who earn too little to support their families. The size of the non-protected group, however, remains large.

Table 2.1 also shows that the size and weight of the four schemes in the overall policy package has changed considerably. EITC, after a large expansion in the past few years, now has the largest number of participants but, because spending per participant is low, EITC spending is only about 10% of the total spending on these four programmes. BLSP has the highest per-recipient cost and is therefore the largest programme in terms of total costs (again, only including BLSP recipients of working age). EI has more participants than BLSP but per-recipient spending is lower and so is total EI spending. ESPP, finally, despite its recent expansions still plays a minor role in terms of both recipients and spending. In the coming years, ESPP and EITC recipient numbers will probably increase further but the overall spending composition will change little without further reform.

Protecting the unemployed: Employment Insurance

Korea introduced its EI programme in mid-1995; much later than most other OECD countries and also considerably later than its own Industrial Accidents Compensation Insurance (IACI), which was introduced 30 years earlier. EI is a comprehensive labour market and social security measure including i) the employment security and vocational skills development programmes aimed at preventing joblessness, promoting employment and improving workers’ vocational skills; and ii) the unemployment insurance component providing income support to displaced workers (see Box 2.1 for more details on some of the key characteristics of Korea’s EI).

Benefit coverage

Eligibility: EI in principle covers all employees on a mandatory basis, except for most persons working less than 60 hours a month or 15 hours a week, and family labour. Most self-employed can opt in on a voluntary basis. Entitlement: a beneficiary must have at least 180 days of coverage during the last 18 months, be registered at an employment security office, capable of work and available for work. Unemployment must not be due to voluntary leaving, misconduct, a labour dispute, or the refusal of a suitable job offer.

Benefit level and duration

EI beneficiaries receive 50% of their previous average gross wage. EI benefits are paid in instalments of 14 days, every two weeks. The minimum daily benefit is set at 90% of the minimum wage, whereas the monthly maximum was originally fixed at a constant level of KRW 40 000 but increased to KRW 43 000 in 2015 and KRW 50 000 as of April 2017. When EI was first introduced, the minimum benefit was around a fifth of the maximum but as the minimum grew rapidly, in line with increases in the minimum wage, and the maximum remained largely untouched, this is no longer the case.

The EI payment duration has not changed since the introduction of the system. Payment duration increases with age at the time of job loss and the length of the insurance record, ranging from 90 days for people insured for less than a year, irrespective of age, to 180 days for people under age 30 who are insured for 10 or more years (or 210 days if aged 30-49 and 240 days if aged 50 or older or if having a recognised disability).

Special benefits

Extended EI benefits exist in several forms. Individual extended benefits are offered to jobseekers who, after having been referred to job vacancies three or more times by a Job Centre, fail to gain employment and are considered needy. They can receive 70% of their previous EI benefit for an additional period of 60 days. Benefits for extended training are offered to jobseekers with difficulties in finding work because of a lack of skills. Such individuals are ordered to take training and can receive 100% of their previous EI benefit for a period of up to two years, as long as they receive training. Special extended benefits are offered to jobseekers whose unemployment benefit period has expired and who have difficulties in finding new employment due to a sudden rise in unemployment, during a period designated by the Minister of Employment and Labour. These beneficiaries can receive 70% of their previous EI benefit for an extended period of up to 60 days. Such benefits were provided three times during the crisis of 1998, but have not been offered since. Finally, a beneficiary who falls ill can receive 100% of the EI entitlement until being well enough to resume job search, up to a maximum of four years.

Funding mechanism

The EI system is co-funded from employee and employer contributions. Unemployment benefits are funded by 1.3% of the worker’s gross wage, with the cost shared equally by employer and employee. Depending on firm size, employers have to pay an additional contribution ranging from 0.25% of the wage sum (less than 150 employees) to 0.85% of the wage sum (over 1 000 employees) to cover the cost of the employment security and vocational skills development programme. (For comparison, industrial accident insurance is fully covered by employers who pay a risk-rated premium ranging from 0.70% to 32.3% of the wage sum – the average being 1.70%). The EI contribution for voluntarily insured self-employed is equal to 2.25% of a self-chosen monthly remuneration level.

EI covers most salaried workers on a mandatory basis and they are entitled to payments if they have been dismissed involuntarily and paid contributions for at least 180 days out of the past 18 months. EI is co-funded by employer and employee premiums. At around 2% of the wage, total EI contributions in Korea are lower than in other OECD countries with an (un)employment insurance, with premium rates typically in the order of 4-8%.

In the current blind-spots discussion in Korea, the benefit side of EI dominates the debate, for obvious reasons. EI benefits have long suffered from the low coverage of the programme and more recently face the additional challenge of having turned over time into a relatively low and de-facto flat-rate payment. Both EI coverage and EI payment levels will have to be addressed vehemently in the coming years.

Despite a series reforms, EI coverage issues remain urgent

Despite continuous expansion of the programme since its introduction, the biggest problem of Korea’s EI scheme remains the low number of workers insured and the low number of jobseekers entitled to a benefit. Korean governments at all times tried to tackle this weakness. In the late 1990s, legal coverage was gradually extended from companies with 30 and more ordinarily employed workers to all companies, irrespective of the number of workers employed. In the 2000s, coverage was extended to include not only regular but also most groups of non-regular employees, including part-time workers and daily workers. And most recently, since 2012, own-account workers and employers with less than 50 employees can also choose to be insured on a voluntary basis.4

EI take-up, however, remains low, for a number of reasons. First, there are still certain groups of salaried workers legally excluded from EI. This includes: a) employees who work less than 60 hours per month or 15 hours per week; b) businesses with less than five employees in the agricultural, forestry, fishery and hunting industries; c) most foreign workers; and d) workers aged 65 and over.5 Second, while self-employed workers can in principle choose to opt-in they almost never do so in practice – despite the high flexibility of the regulation and affordable premium rates.6 This is very important in a country where self-employment accounts for roughly one quarter of the total workforce and where many jobless people have no other choice than own-account work to make a living. Third, while EI is legally mandatory for all groups of employees not explicitly excluded, many of these employees are not insured, especially when they work in very small businesses with less than five employees (see below); again, this is a very strong limiting factor in a country dominated by such micro-businesses.

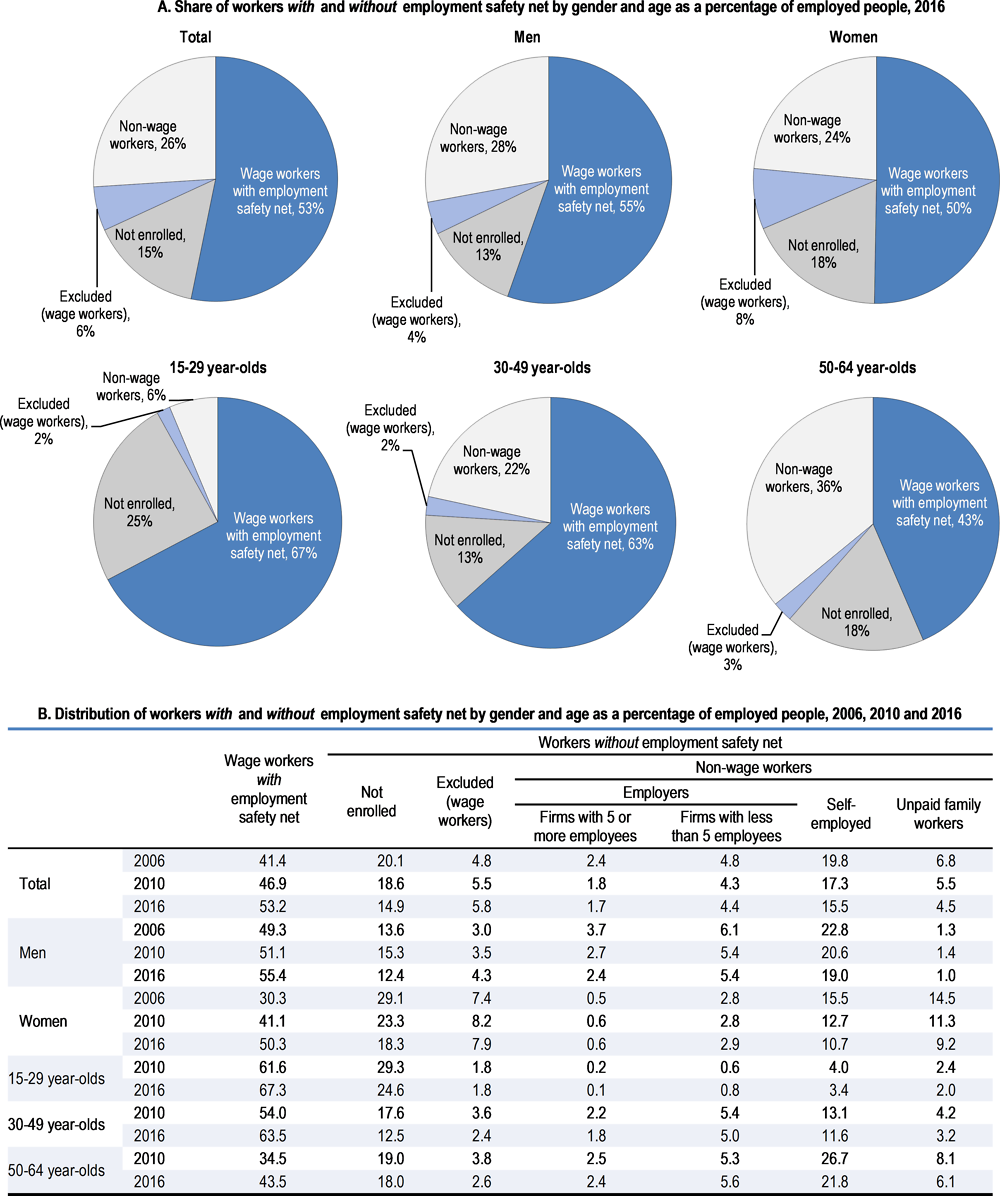

Figure 2.5 shows the blind spots of EI enrolment in Korea in more detail. Overall, in 2016 only just over half, or 53.2%, of the employed population in Korea had access to an unemployment safety net, either through EI (47.6%) or through other schemes for special groups of (public) workers (5.6%). Of the remainder, 14.9% were wage workers not enrolled in EI although they should be enrolled; 5.8% were excluded wage workers (mostly workers over age 65 or non-standard contracted workers); and the remaining 26% were non-enrolled self-employed (mostly own-account workers but also employers and unpaid family workers). In other words, many Koreans are still excluded despite a drop in the excluded share from 58.5% in 2006 to 53% in 2010 and 47% in 2016. In the period 2006-10, most of the improvement resulted from structural labour market changes (i.e. a decline in self-employment and unpaid family work over this period). In the period 2010-16, over half of the improvement was due to a decline in non-enrolment, and the rest was due to structural change.

Note: This figure adapts and updates a similar figure published in KDI Focus by Yoo (2013[10]).

Source: Supplementary results of the Economically Active Population Survey by employment type in August 2006, August 2010 and August 2016.

There are significant age and gender differences in non-enrolment. First, women are more likely than men to be excluded from EI although this gender gap is closing rapidly both because of a larger drop for women in EI non-enrolment – from 29% in 2006 to 18% in 2016 – and the drop in the number of unpaid family workers who are women in most cases. Second, workers over the age of 50 are less likely than their younger peers to be covered by EI – 43% of the 50-64 year-olds have a safety net compared with 67% of the 15-29 year-olds. The age gap in non-coverage is also closing but only very slowly: EI non-enrolment has fallen much faster for workers under age 50 while the decline in self-employment has affected workers over age 50 more than other age groups.

Lowest coverage for non-regular workers in micro-businesses

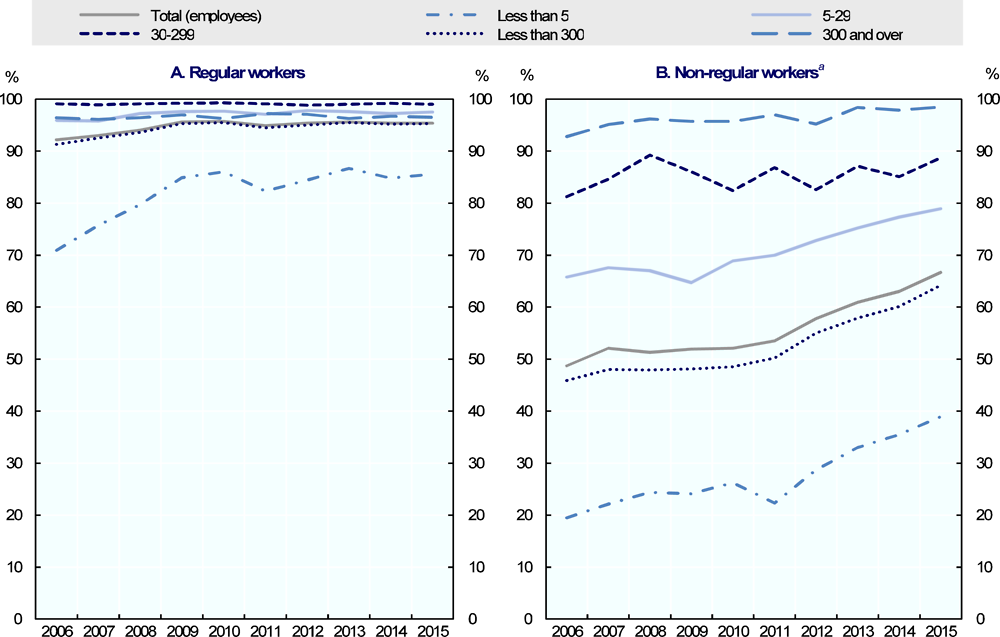

Two characteristics of the Korean labour market explain much of the low EI coverage: non-regular work and work in micro-businesses with less than five workers. Both forms of work are widespread in Korea, with one in three salaried workers having a non-regular work contract and four in ten working in a micro-business (see Chapter 1).

EI coverage for regular workers reached over 90% more than ten years ago and is now at around 95%. But among non-regular workers, even in 2015 only about two-thirds are covered by EI despite a continuous increase in this share which stood at only 50% of all non-regular workers ten years ago (Figure 2.6).

face the lowest employment insurance coverage

a. Excluding independent contract workers.

Source: Ministry of Employment and Labor, Survey on Labor Conditions by employment type, 2006-15.

Comparable inequality in EI coverage is found by firm size. Workers employed in large companies with more than 300 employees have EI coverage rates near to 100%, irrespective of whether they have a regular or non-regular work status. Similarly, the type of employment has a limited impact in firms with 30-299 employees in which also among non-regular workers around 90% are covered by EI. The situation is much worse for workers employed in micro-businesses. Non-regular workers in these firms have EI coverage rates below 40%, despite a 15 percentage-points increase in the past four years. In such micro-businesses, even one in seven regular workers miss out on EI coverage, with no further improvement for this group in the past six years.

Non-regular work in a micro-business has the lowest odds of providing EI coverage. This is worrisome for at least two reasons: First, non-regular work is often involuntary and taken up because people need immediate income. Only about one-quarter of all regular workers (i.e. half of those who are in such a job voluntarily) claim to be satisfied with their working conditions (Table 2.2). Second, the chances to transition from non-regular to regular work are poor in Korea: previous OECD analysis using self-assessment data has demonstrated that one year after, 70% of those workers are still in non-regular employment and only 12% have become regular workers, and that the probability to make a successful transition falls further over time; in other words, non-regular work in Korea is quite persistent (OECD, 2013[2]).

Recent efforts to expand EI coverage had some effect but at a high cost

In 2012, the Korean government introduced a premium subsidy scheme, generally known as the Duru-Nuri Social Insurance Premium Subsidy Programme, to overcome some of the shortcomings of the EI system. The main purpose of the scheme is to raise the number of undocumented low-wage workers legally guaranteed EI but not actually enrolled – the effective blind spot. Duru-Nuri provides financial assistance to low-wage salaried workers at workplaces of up to ten employees and their employers. Initially, a pilot programme was launched in selected counties of 16 provinces. Since July 2012, the programme has been in effect nationwide. Eligibility criteria and the size of the subsidy were changed several times. Until 2016, the wage level up to which workers can qualify was gradually raised to KRW 1.4 million per month – corresponding to roughly 125% of the minimum wage. The share of the premium subsidised through the programme was increased to 60% for all newly enrolled contributors, for as long as one year, and lowered to 40% of the premium for all other currently enrolled workers (previously the rate was 50% for both groups). Employers receive the same subsidy for their part of the contribution. In 2016, the number of workers who received an EI premium subsidy was just over 700 000 and the number of employers benefitting from a subsidy was just below 340 000.7

Recent analysis by the Korea Development Institute, using about 900 000 observations on the number of registered workers in small establishments over three years – 1.5 years before and 1.5 years after the introduction of Duru-Nuri –, suggests that the subsidy programme increased the number of EI registered workers by 1.36%. Approximately 98.5% of the programme cost was a deadweight loss: the large majority of subsidised people would have been insured also without the subsidy (Kim, 2016[11]). Put differently, for every 1 000 subsidised employees Duru-Nuri created 15 new covered employees, implying a cost per new EI enrolment of around KRW 50 million – roughly three times the person’s annual wage. Premium subsidies alone do not seem to solve the problem of low EI coverage in Korea in very small businesses, which emerge and disappear with high frequency, in an effective manner. Many employees apparently do not consider the incentive provided by the subsidy strong enough.8

Two factors explain the ineffectiveness of the programme: The permanence of the subsidy and the fact that, for reasons of fairness, it is also paid to low-wage workers already insured. Other OECD countries do not have insurance premium subsidies of a nature comparable to Duru-Nuri. More common are reductions in insurance contributions for employers as an incentive to hire workers who are disadvantaged (e.g. young people, older workers, people with a disability) or in economically difficult times. But also such more targeted schemes struggle with high deadweight losses, even though contribution reductions tend to be given on a temporary basis.

The premium subsidy scheme could also be seen as a complement to another regulation in Korea, already in place since the inception of EI in 1995 that enables undocumented workers to claim EI benefits they should have been due. Such workers for whom EI contributions have not been made but who otherwise fulfil the eligibility and entitlement criteria and have been dismissed involuntarily can request a “confirmation of insured status” from their local Employment Centre and become eligible for EI payments in retrospect. The worker has to demonstrate the existence of the employment relationship and pay, ex post, the EI and national pension contributions that would have to be paid during the undocumented period of employment, for up to a maximum of three years. The employers who neglected to document such workers are mandated to pay their part of the contributions plus a one-off fine of KRW 300 000 per worker. The arbitration procedure nicely complements the Duru-Nuri scheme: employers have an obligation to document their workers and can receive a subsidy as an incentive to register low-paid workers but if they fail to do so, they may have to pay all EI premiums plus a fine.

In practice retrospect payment of EI premiums in order to secure EI entitlement is rare. In 2016, only 1 802 workers applied for an arbitration procedure of which 950 cases were approved (the remaining cases were rejected because entitlement criteria had not been fulfilled). The number of cases has remained relatively stable over the years. There is no research available on the reasons for the low number of cases but it is likely that these workers, typically non-regular workers in small firms, and presumably also their employers, are largely unaware of the possibility to request insured status in retrospect. It is also probably difficult for such workers to prove their employment relationship.

Enforcement of EI legislation and premium collection

With every reform step, EI coverage has improved but often only by a small margin. The slow expansion of coverage despite a series of comprehensive changes indicates that the structure of the Korean labour market has not responded sufficiently or perhaps remained unaffected. In particular, informal work – however defined – is still widespread in Korea and the life span of small businesses is still very short. This raises the question how much additional legal change would be able to achieve and, conversely, how the quite inclusive legislative framework could be better enforced.

In a recent paper, Lee (2012[12]) finds that on the basis of 2011 data around 40% of all wage workers in Korea engage in some form of informal work, defined as work that is not fully covered by minimum wage regulation, labour standards and social insurance. Notably he concludes that only 20% of this informality is due to a lack of regulation applicable in those workplaces while in all other cases non-coverage of this work is the result of non-compliance with existing legislation. Echoing the findings described above, non-compliance is more widespread in non-regular than in regular employment and far more frequent in small and micro-businesses than in larger companies.

Korea can do more to improve the enforcement of its EI and other labour legislation. Enforcement is difficult in a situation in which 1 300 labour inspectors have to inspect 1.86 million workplaces. Data from the late 2000s, when the number of labour inspectors fluctuated around 1 200, suggest that in any given year only about 1-2% of all workplaces were inspected but also that in 75% of these cases a violation was detected (Lee, 2012[12]). The planned gradual increase in the number of labour inspectors by 1 000 people until 2018 is welcome; however, even the larger number of inspectors will not be enough to inspect workplaces regularly and forcefully.

Employers have an obligation to report their workers acquisition of EI insurance status to the authorities9: Failure to do so can result in a penalty of KRW 30 000 per employee not reported (up to a KRW 1 million maximum) or KRW 50 000-100 000 (and a maximum of KRW 3 million) in case of false reporting of, for example, the wage level or date of employment. If a breach of obligation is discovered, the authority can enrol the employee into EI or correct false facts with no further action from the employer. However, not only are per-person fines low but data from the Ministry of Employment also suggest that fines are seldom used: In 2016, penalties were given for a total of just over 250 000 employees not reported and just over 60 000 employees falsely reported. The low fine and the low likelihood of its application are unlikely to pose a real threat to employers.

Another way to improve EI coverage is by better identifying workplaces that should be formalised and covered. Social insurance premium collection is an important aspect in this regard. While in the past the four social insurances (pensions, health, employment, industrial accidents) operated independently, since 2011 the government has allowed the insurances to integrate the collection of their premiums at the National Health Insurance Corporation. This has led to a minimal integration of the premium collection system: today, a company receives only one envelope rather than four, but the four insurances continue to perform their main tasks (such as application, enrolment and benefit payment) independently. Better integration of tasks would be a step in the right direction because insurance cover varies by type of insurance. Health and pension insurance coverage is even lower than EI coverage for most types of non-regular work but IACI coverage is high for all workers and in most cases has been high for many years (Table 2.3). The high IACI coverage rate has yet to be achieved for the other branches of social insurance.

A recent change through which, as of 2017, the Korea Workers’ Compensation and Welfare Service (KOMWEL) became responsible for EI applications of both workers and employers (in addition to IACI applications), could be an important step. This could contribute to a further increase in EI coverage among salaried employees and improve the link with the tax authority. The latter is important because in Korea work not covered by social insurance (be it non-regular work or own-account work) is generally registered for tax purposes; it only remains informal or undocumented for insurance purposes.

Over time, EI has turned into a flat-rate payment

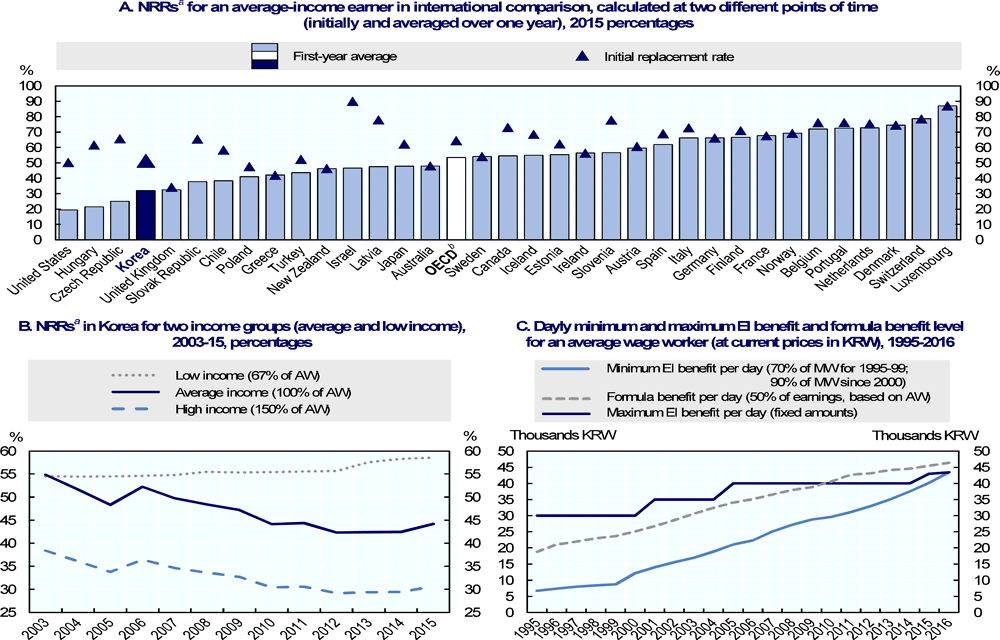

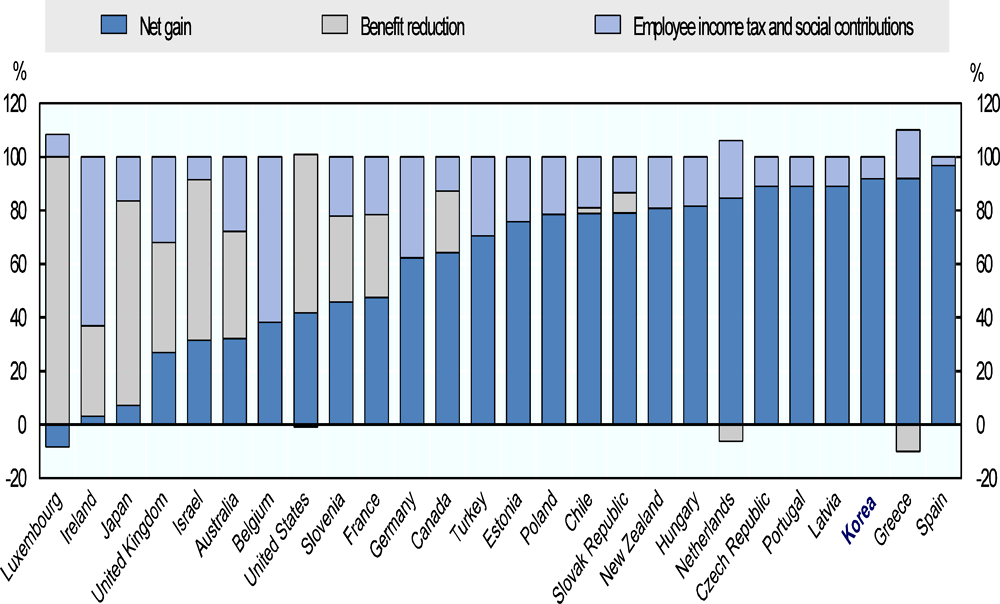

A second problem of the EI scheme is the gradual erosion of the level of payments. Unemployment benefits in Korea have never been particularly generous in an international comparison but for many workers their value has fallen over time. For an average wage worker, EI initially replaces around 50% of the worker’s wage – compared to an OECD average of around 65% (Figure 2.7, Panel A). The situation deteriorates if looking at the situation of workers unemployed for a longer period, even though long-term unemployment is low in Korea:10 averaged over one year of unemployment, the income replacement rate is only 32% (because EI is only paid for a relatively short period), unless the person becomes eligible for BLSP. These benefit levels are among the lowest in the OECD; the OECD average for one year of unemployment is over 50%.

has fallen over time

and development of minimum and maximum thresholds of daily EI entitlements since 1995 (Panel C)

Note: AW: Average worker. EI: Employment insurance. KRW: Korean won.

a. Net replacement rate (NRR) is the ratio of net income out of work to net income while in work. Calculations consider cash income as well as income taxes and mandatory social security contributions paid by employees. Social assistance and housing-related benefits potentially available as income top-ups for low-income families are not included. Family benefits are included, while entitlements to severance payments are excluded. NRRs are calculated for a 40-year-old worker with an uninterrupted employment record since age 22. They are averages over four different stylised family types (single parents and one-earner couples, with and without children) and two earnings levels on the lost job (67% and 100% of average full-time wages). The one-year average is a somewhat artificial number insofar as the unemployment benefit payment duration is shorter than one year in around half of the OECD countries. Due to benefit ceilings, NRRs are in most countries lower for individuals with above-average earnings (see also Chapter 3).

b. Unweighted averages of the 34 OECD countries shown in Panel A above (excluding Mexico).

Source: OECD Tax and Benefit Models, www.oecd.org/els/social/workincentives for Panels A and B; and author’s own compilation for Panel C.

Figure 2.7 (Panel B) also shows that, today, EI initially replaces close to 60% of the net wage for a low-income earner, around 45% for an average earner and around 30% for a high-income earner – suggesting considerable progressive redistribution within the EI scheme. Replacement rates have fallen sharply in the past decade for most workers except those earning a low income. For workers earning the average wage or more, the initial net replacement rate has fallen by around 10 percentage points in only ten years.

How is this fall in replacement rates explained? Korea has seen an unusual development in the past two decades by way of which the EI system has gradually moved away from its original structure. The maximum EI payment has remained largely unchanged ever since the introduction of the system whereas the minimum EI payment, fixed at 90% of the minimum wage, has gradually increased in line with the minimum-wage increase. As a consequence, today the minimum EI payment is almost equal to the maximum. This is very different from the situation in 1995, the year when EI was introduced: back then the minimum EI payment corresponded to one-fifth of the maximum (Figure 2.7, Panel C).

Panel C also shows the “intended” daily benefit for an average earner. In 1995, this intended payment was right between the minimum and the maximum. In the mid-2000s, however, an average earner hit the EI maximum and ever since then the actual payment was lower than the intended one. If the rapid increase in the minimum wage planned by the new government materialises – a 15% increase for three consecutive years – both the minimum and the maximum EI entitlement and the actual payment for all EI recipients would increase accordingly. In this case, the current somewhat unusual situation of a minimum that equals the maximum would continue.

Some EI features and developments could be reconsidered

It is surprising that this shift in payment structure could happen with so little resistance. It appears that EI premium increases which would be needed to re-establish the original payment features of the system and to raise benefit payments back to their level initially agreed more than 20 years ago are highly unpopular – more unpopular than the ongoing erosion of the system. Partly this development can be explained by the fact that the Korean EI scheme was introduced at a time of very low unemployment. The crisis in the late 1990s resulted in some increase in EI premiums to cover the fast increasing number of unemployed at the time but the appetite for a sufficiently large premium increase to fund a true insurance for all workers was lacking.

Whether the current situation is sustainable in the long run remains to be seen. For many jobseekers and their families EI entitlements are no longer providing a sufficient income to maintain the level of living. This has been accepted so far because of the low average duration of unemployment in Korea and maybe it has also contributed to that low duration because workers have strong incentives to find a new job quickly.

The reluctance to increase EI premium rates is understandable insofar as higher non-wage labour costs potentially reduce international competitiveness; this is especially relevant for the export-oriented industrial production which is still at the heart of Korea’s economy. But the current situation arose from political decisions, not out of necessity. Over 20 years, benefit entitlements have fallen so drastically that resurrecting the initial situation would indeed require an increase in premium rates. It will require a political discussion on what the future EI benefit level should be to keep the system economically viable and socially sustainable. In the past, EI surpluses have been used to introduce new tasks, such as maternity leave and parental leave benefit which were introduced without a corresponding increase in premiums or additional dedicated tax funding.

The EI scheme in Korea also includes elements the existence of which might have to be reconsidered. Employment promotion allowances were introduced as an incentive for EI benefit recipients to find new employment quicker. There are three forms of such allowances but only the Early Re-employment Allowance (ERA) is relevant in practice. ERA is offered to benefit recipients who find stable work before the end of their EI entitlement period. After a series of reforms, the allowance now equals 50% of the remaining benefit entitlement (or two-thirds if the EI recipient is over the age of 55 or has a disability). To be entitled, a recipient must: a) find a new job in the first half of his entitlement period; and b) have been employed (or engaged in his/her own business) for a period of at least 12 consecutive months. Until the late 2000s, ERA entitlement criteria have been much laxer and total ERA spending corresponded to about 15% of total spending for job-seeking benefits. After the recent reforms, the ERA spending level dropped to less than 5% of this. The various changes and corresponding cuts in both ERA recipients and ERA spending were justified because of analysis which showed that ERA came with considerable deadweight effects (Hwang, 2013[13]). It remains to be seen whether this is not the case any longer with the revised ERA criteria.

Preventing poverty and exclusion: Basic Livelihood Support Payment

The second most important social benefit programme in Korea is BLSP, a means-tested social assistance programme providing cash and in-kind benefits to eligible persons living in absolute poverty. BLSP was put in place in 2000 in response to the rapid increase in the number of poor and unemployed people in the aftermath of the Asian financial crisis of the late 1990s.11 BLSP was long criticised for its strict eligibility criteria that exclude many deserving families and for a payment structure which creates dependence on rather low financial support. Both issues have been addressed recently but certain problems continue. In addition, there are issues around the group of conditional BLSP recipients – a small group that could grow bigger and would benefit from more attention.

An increasing number of recipients but eligibility remains strict

Local governments are in charge of determining BLSP entitlement and providing corresponding benefits and services.12 In order to receive BLSP, an applicant has to meet both income and family requirements. Household income (income and assets converted into income) must be below a given threshold level, which is determined in relation to standardised median income – objectively derived from a household survey – and varies by household size and type of benefit (Table 2.4). Before mid-2015, thresholds had been defined by the government every year in relation to the minimum cost of living. The current thresholds imply that a family or household of four people would only be entitled to living benefit (the main component of BLSP) if having a total income similar to Korea’s minimum wage although such household could possibly still be entitled to other BLSP components. The steep increase in thresholds with household size implies that BLSP is designed as a payment to support larger families.

The family requirement implies that applicants cannot receive benefits if they have a close family member (a parent, child or spouse) capable of supporting them – the so-called family support obligation rule. Eligibility does not depend on whether such family support is actually provided. The capacity of family support is measured by the family members’ income and assets. The crux is that relatives with a relatively low income are supposed to support their income-poor family member even though, in 2015, the government raised the threshold income to be accepted as an incapable legal supporter from 130% of the minimum cost of living to 100% of median income.

Income requirements and the family support obligation both keep the BLSP caseload under control. Today, about 1.7 million Koreans receive one or several BLSP benefits, corresponding to around 3.2% of the population. This level is similar to the OECD average but low in comparison with OECD countries with an otherwise stringent and immature social protection system – despite a significant increase recently (up from 1.33 million in 2014) because of changes in the income thresholds for applicants as well as potential supporting relatives.

Unpublished estimates suggest that without the family support obligation rule the number of BLSP recipients in Korea could be roughly twice as high as it is today.13 This is relevant for two reasons:

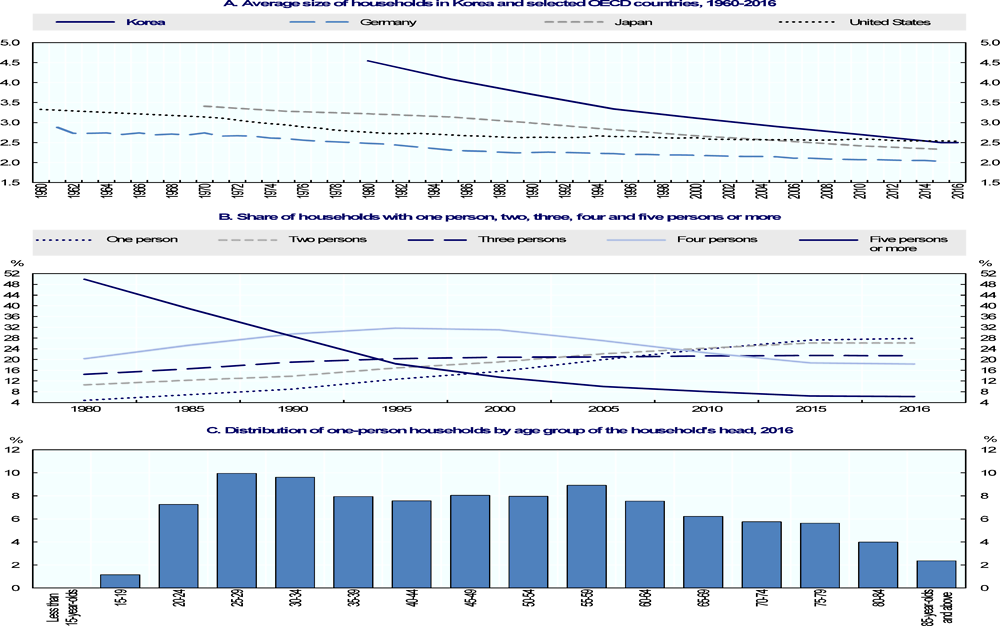

-

First, family relations and household composition have changed drastically in Korea in the past few decades. The average household size, for example, declined from 4.7 people per household in 1980 to 2.7 in 2016 and the share of one-person households increased from only 5% to almost 25% in the same period (Figure 2.8); both trends will continue into the future. Accordingly, family ties are also changing. Not the least because of such changes in household and family structures, rules similar to Korea’s family support obligations have been abolished or reduced in other OECD countries which had or still have comparable rules on paper, such as Austria, Belgium, France, Germany, Japan or Switzerland.14

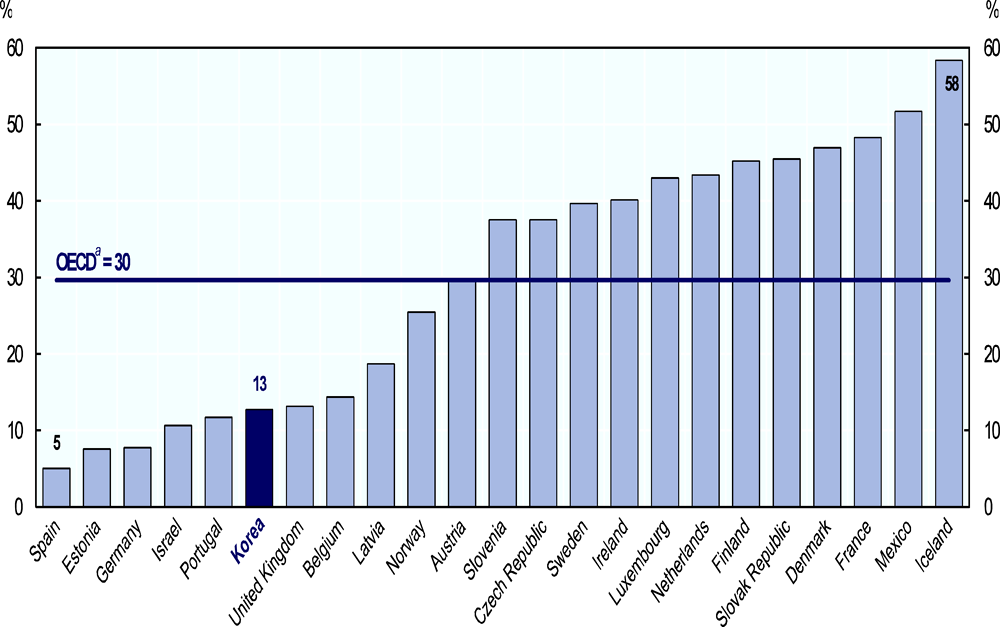

-

Second, relative to the total number of poor working-age individuals, social assistance take-up is relatively low in Korea: BLSP covers around 13% of that population compared with an (unweighted) OECD average of around 30% (Figure 2.9). Abolishing the family obligation rule would bring Korea closer to this OECD average on this measure.

and distribution of one-person households by age (Panel C), 1980-2016

Source: Korean Statistical Information Service (KOSIS), http://kosis.kr/statHtml/statHtml.do?orgId=101&tblId=DT_1JC1611&conn_path=I3 (accessed on 6 October 2017). For Germany, see Table 6 for Western Germany from www.bib-demografie.de/SiteGlobals/Forms/Suche/EN/Servicesuche_Formular.html?nn=3214948&resourceId=3075566&input_=3214948&pageLocale=en&templateQueryString=household+size&sortOrder=score+desc&searchArchive=false&searchIssued=false&submit.x=0&submit.y=0 (accessed on 24 October 2017); and for the United States, US Census Bureau; Bureau of Labor Statistics, “America’s Families and Living Arrangements: 2016”, www.statista.com/statistics/183648/average-size-of-households-in-the-us/ (accessed on 24 October 2017).

selected OECD countries, 2013

Source: Calculation based on OECD Social Benefit Recipients Database, www.oecd.org/fr/social/recipients.htm.

A more customised benefit with flexible entitlements

A second main issue for Korea’s BLSP concerns its benefit level and structure. BLSP provides seven different benefits15 and, until recently, one of the biggest problems was that the income thresholds for all types of benefit were identical. This meant that recipients received all or nothing, and that those receiving benefit had a strong motivation to remain on benefits. This is confirmed by evidence showing that about one quarter of all recipients have been on BLSP for more than ten years and roughly half of them for more than five. The 2015 reform of BLSP eligibility criteria addressed the benefit accumulation issue by de-linking the various benefits and transforming BLSP from a single payment to a more customised payment. The four main types of benefits are now phased out gradually: living benefit is phased out first and education benefit last (see Table 2.4).

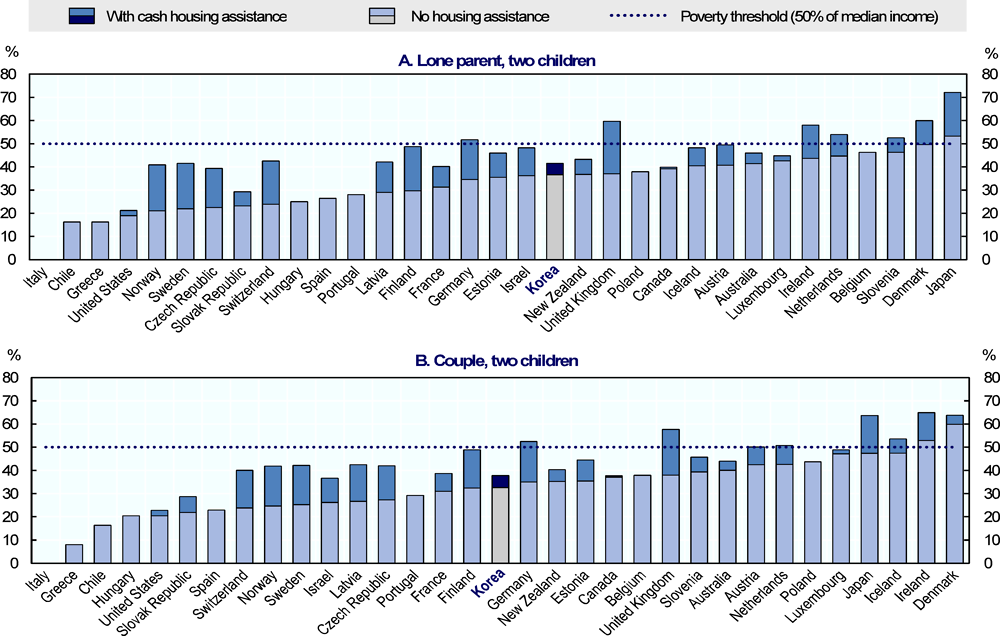

It is too early to assess the full impact of the 2015 BLSP reform. In the first instance, the more customised payments improve the income situation of a number of recipients and their families. This is reflected in the overall increase in BLSP recipiency after the reform and a particularly fast increase in the number of education benefit recipients, as well as somewhat higher average payments. Improved entitlements for certain groups of BLSP recipients were well justified. Comparing pre-reform net income levels of families relying on social assistance suggested Korea found itself in the lower third of OECD countries for most family types (OECD, 2013[2]). Updated post-reform estimates of net income levels of these groups suggest that lone parent and two-couple families with two children who rely on BLSP still find their income considerably below a relative poverty threshold, with the maximum disposable income provided to these families being at or somewhat below 40% of equivalised medium income, taking cash housing benefit entitlements into account. However, the 2015 estimates put Korea closer to the middle of OECD countries for most types of families (Figure 2.10).

but are comparable with other countries’ cash minimum income benefits

for two family types, selected OECD countries, 2015

Note: Details of assumptions made in the calculations are available in the table “Income Adequacy” which is available under the statistics heading on the Benefits and Wages website referenced below. Countries are ranked in ascending order of the category “No housing assistance”.

Source: OECD Tax and Benefit Models, www.oecd.org/els/social/workincentives.

The longer-term impact of the reform on, for example, the duration of benefit payments or benefit dependence and the number of people moving off benefit remains to be seen (Wan, 2016[14]). Earlier analysis by the OECD has suggested that BLSP, mainly because of the low tax burden imposed on Korean workers, generally creates less of a poverty trap than minimum-income systems in many other OECD countries – although effective tax rates when taking up work can potentially be high for some income and family situations (OECD, 2013[2]). This situation should have improved further with the more customised phase-out of the various payment components of BLSP.

Very few BLSP recipients with work capacity

A discussion about improved work incentives and reduced benefit dependency may, however, be relatively fruitless in relation to BLSP. A closer look at BLSP beneficiaries reveals that among all recipients of the living benefit only some 75 000 (or 6% of the total) are so-called conditional recipients. Various medical evaluations can be performed by the pension insurance authority, on request of the local welfare office, to assess whether or not living benefit recipients have the ability to work. If so, they receive a conditional benefit and must get in touch with the local Job Centre where they are entitled to services to help them find and access employment. Virtually all other OECD countries employ similar activation measures as part of their social assistance measures, although the extent of enforcement varies considerably across countries and localities.

The low share of conditional recipients suggests that BLSP in Korea is largely a payment for people unable to work.16 This partly explains the large gaps in Korea’s social safety net: for those who are no longer (or never were) entitled to EI, there is effectively no other support available for a person able to work in principle but not able to find a job or to access the labour market. This can be a particular problem for people with health issues. The situation is very different in most other OECD countries in which one or more of the following situations may arise (see Chapter 3): a) social assistance schemes may cater for a larger number of people who are able to work but have exhausted their unemployment benefit entitlements; b) special unemployment assistance schemes may provide benefits for jobseekers in long-term unemployment or those not entitled to unemployment benefits in the first place; and c) additional other systems might be available to help people temporarily unable to work because of sickness, disability or care obligations. Neither of these options is available in Korea.17 Instead, a large share of BLSP recipients of working age are classified as unable to work and, thus, as non-conditional recipients because of disability or lone parenthood.

What is happening with the small group of conditional BLSP recipients in Korea? Conditionality implies they have to participate in the Self-Reliance Programme (SRP)18 organised by the Ministry of Health and Welfare or the Employment Success Package Programme (ESPP) provided by the Ministry of Employment and Labor. Of the roughly 49 000 individuals annually who have participated in SRP, one-third became self-reliant – meaning that they either found employment or started a business or stopped receiving BLSP payments. A more rigorous evaluation of the cost-effectiveness of SRP, however, is not available. Of the roughly 26 000 BLSP recipients who participate in ESPP (see more on this group further below), one in eight succeeded in finding work or starting a business immediately. In the future, efforts could be made to improve these success rates, especially in the event of a further easing of BLSP eligibility criteria whereby the number of conditional recipients with work capacity would increase and the issue of work activation and labour market reintegration would become more pressing.

Supporting jobseekers actively: Employment Success Package Programme

Well aware of the gaps in the social protection system, the Korean government introduced the ESPP scheme in 2009 as a way of helping jobseekers neither entitled to EI nor receiving BLSP but facing considerable disadvantages, especially in the form of low income. ESPP combines targeted employment support with some income support. Over the years, ESPP was expanded rapidly in many different ways and the programme still has considerable potential for further expansion. The challenge for the government is to expand programme capacity as well as quality at a fast enough pace and, at the same time, to raise participation and make it attractive for those eligible to participate.

Assessing the effectiveness of ESPP

ESPP provides targeted, case-managed job-search support as well as training to improve employability, but also various flat-rate allowances as an incentive to participate in the programme and in training and as a reward for having found a job (see Box 2.2).

ESPP is a comprehensive employment service operated by the Job Centre or contracted out to private employment agencies. The programme can last for up to 12 months (it ends as soon as the participant finds a job), with the possibility of re-referral after a suspension period of varying length. ESPP was first introduced for low-income jobseekers only but later on expanded to also include other risk groups, some of them (notably eligible youth) irrespective of their income situation. The programme consists of three stages:

First stage

The main purpose of the first stage, which is obligatory and lasts at least three weeks, is to clarify people’s ability and enhance their motivation to work. It includes individual counselling, group counselling, vocational psychological testing, an evaluation of the employability, and the preparation of an Individual Action Plan (IAP).

The counsellor profiles the participants into one of four levels of employability (very low, low, normal, and high), depending on individual barriers and labour market experience. Services are provided in line with the level of employability. Participants must prepare an IAP at the end of the first stage, after a minimum of three face-to-face sessions with their counsellor, which should include relevant personal and career information and a plan for vocational training. Those who complete an IAP are paid a basic participation allowance of KRW 150 000 (about EUR 115). If a participant attends special programmes, an additional allowance of up to KRW 100 000 is paid (varying by type of participant).

Second stage

The purpose of the second stage is to provide the vocational training and job experience needed to strengthen the participant’s employment competence. This stage can last for 6-8 months but is not obligatory if no training needs have been identified in the first stage.

Participants choose services based on their IAP, in consultation with their counsellor. The tuition fee of KRW 3 million is provided as a training subsidy (some participants have to cover a co-payment of 5-50%). During the training, participants receive a training participation allowance of KRW 284 000 per month and a monthly support allowance of KRW 116 000 to cover expenses occurring during the period of vocational training. There is also special training for those who want to run their own business.

Third stage

The purpose of the third stage, which is obligatory and can last for up to three months, is to help participants find employment through intensive job-placement services provided by either the Job Centre or a private employment agency.

Services include searching for the best job match for each participant based on vocational preferences, aptitudes and participation history in the second stage of the programme. Participants can also receive coaching on job-interview skills and be accompanied during their job interviews. In 2016, the average number of direct referrals at the third stage was 1.63 referrals per participant. During this stage, participants receive KRW 20 000 per month to cover their costs. Type I participants (low-income jobseekers) who obtain a job of more than 30 hours a week which also has EI coverage can receive an employment success allowance worth up to KRW 1.5 million in total and paid in three instalments, as follows: KRW 300 000 after three months in the job, another KRW 400 000 after six months, and another KRW 800 000 after 12 months. As of 2018, youth participants will also be entitled to payments worth KRW 900 000 (three times 300 000).

The programme was introduced at a time when a lot was known from other OECD countries on how to set-up and structure an effective activation programme and Korea did not shy away from taking other countries’ experiences into account. The programme has many features that were shown to be essential, such as frequent face-to-face counselling, well-customised intervention, strong user involvement, and a strong degree of flexibility in the type and timing of interventions. ESPP also has a good balance of incentives and requirements in place for those who (could) participate.

ESPP reaches out to a number of target groups, classified into type I and type II. Type I participants include jobseekers with less than 60% of median income (the biggest group), various groups of disadvantaged jobseekers e.g. disabled people, lone mothers or youth at risk (with no income threshold), and conditional BLSP recipients. Type II participants include jobseekers aged 35-64 (with up to 100% of median income) and young jobseekers under age 35 (without any income threshold). The classification matters mostly for how services are provided (see below).

The result of the strong programme features is that the majority of participants complete the programme and that ESPP has promising employment outcomes. Of all participants in 2015, over 80% started a job in the course of the programme including just a little less than 80% of the low-income group. However, the quality of the jobs that these jobseekers find is debatable. First, less than half of all ESPP participants find a job that pays more than KRW 1.5 million or 60% of median income. This is not surprising given that ESPP is predominantly targeted to low-income jobseekers who struggle in finding employment. Secondly, and more importantly, only four in five ESPP participants keep their job for more than three months and six in ten of them for more than six months, even though four in five jobs come with EI coverage (Table 2.5). It is not known if and how fast these people find another, maybe better job. Fast job turnover is not uncommon in the Korean economy that is dominated by short-term and other forms of atypical employment. In view of the labour market disadvantage of most ESPP participants, however, more can be done to connect people with more sustainable jobs.

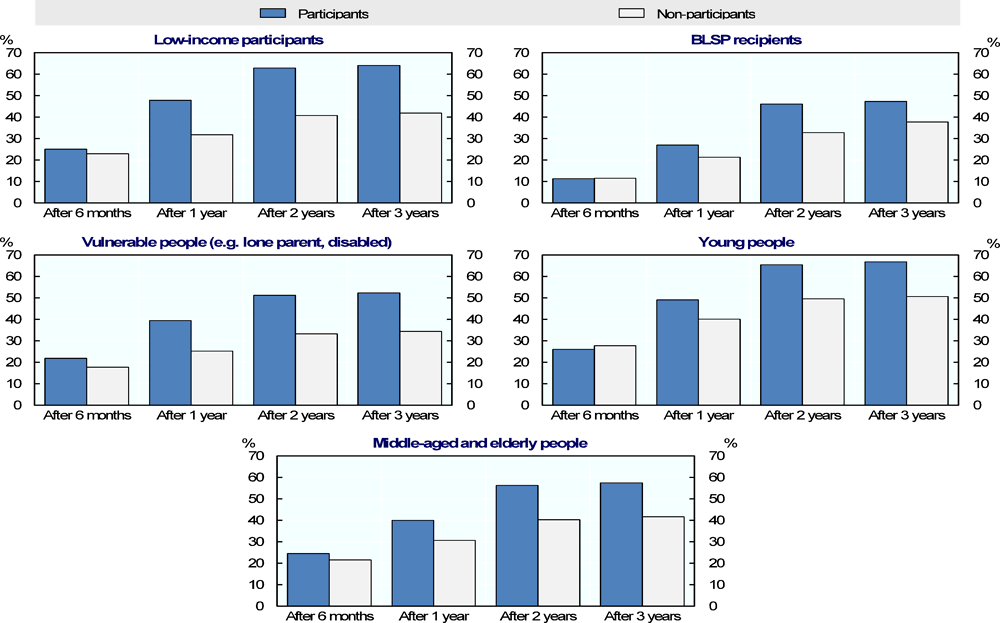

More in-depth performance evaluation by Lee (2016[15]) suggests ESPP is quite effective in bringing programme participants into employment. Comparing the experience of ESPP participants with that of non-participants, i.e. comparable groups of people who had applied for ESPP but were not selected into the programme, shows that ESPP has a positive employment effect for all people and especially so for some of the most disadvantaged groups; only initially employment effects are masked by a lock-in effect. For low-income clients of ESPP, for example, employment rates are 16 percentage points higher one year on compared with those people not admitted to the programme, and 22 percentage points higher three years on (Figure 2.11). The effect is just a fraction smaller for vulnerable groups (lone parents or disabled people), young people and middle-aged and elderly people. For conditional BLSP recipients who are referred to ESPP the effects are smaller in the first year but also reach 15 percentage points after three years. Over time, the effects were relatively stable for all groups but with a clear tendency towards improved ESPP effectiveness between 2009-2011 and 2014. This suggests that the competence of caseworkers and the quality of services is improving, although it could also reflect the improved economic and business conditions.

Note: BLSP: Basic Livelihood Security Programme; ESPP: Employment Success Package Programme. Non-participants are people who have applied for ESPP but were not selected into the programme.

Source: Lee (2016[15]), An evaluation of the employment impact of the Employemnt Success Package Program, KLI, Seoul..

Expanding the capacity of a promising programme

Creating an effective programme of such size and type more or less from scratch is a very ambitious task in terms of building the sheer capacity of the service. The number of ESPP participants increased from 10 000 in 2009 to 300 000 by 2015. Initially, the programme was developed for low-income jobseekers only – people living below 60% of the median income level (previously measured as 150% of the minimum cost of living) – but, over the years, in recognition of the power of the programme, ESPP was expanded to other target groups.19 In 2015, 47% of all participants belonged to the low-income group.

Korea has done well in developing and expanding ESPP services. The ESPP budget has increased 32-fold between 2009 and 2015 to reach KRW 217 billion in 2015. Funding comes from general taxation, with a drawback being that it is a “budget programme”, with the budget set every year. ESPP was gradually rolled out in all 94 Job Centres under the responsibility of the Ministry of Employment and Labor and the number of staff assigned to ESPP has been increased accordingly. However, the staff increase could not fully keep pace with the increase in the number of participants: since 2009, the caseload has increased from 80 clients per ESSP counsellor to 100 clients and must be expected to rise even higher in the coming years (the caseload of the Job Centres increased particularly fast in 2012 and 2013).

The fast increase in service capacity could not have been stemmed by the PES alone. In parallel, a private employment service market was created and a share of the task entrusted to private service providers. As of 2017, this market includes 333 private employment agencies (plus 399 branch offices) which in total employ slightly more ESPP counsellors than the Job Centres. Building this market was not straightforward and the role of private providers has changed over time. Initially they had responsibility for a certain share of the target group – at that time, jobseekers with very low income. The latest change in 2015 meant that Job Centres gained full responsibility for all low-income clients, while all other clients are now serviced by private providers.

Whether this is the right way of splitting the task is unclear and there is no evidence available which would prove that more vulnerable clients had not been served well before the latest change.20 For the future, therefore, other ways of sharing of tasks between public and private providers could still be envisaged. Private employment service providers in Korea not only provide services but are also responsible for all client contact. This is unusual among OECD countries which usually tend to keep much of the job-search monitoring and activation process of clients under public supervision and outsource employment service delivery only. This is the case, for example, in Australia and the United Kingdom – the two OECD countries that have gone the furthest in terms of privatising employment services (see Box 2.3).

Assuring high-quality employment services