Chapter 11. Financial accounts uses

This chapter takes the perspective of users of the macro framework of financial accounts and balance sheets. Different frequencies, quarterly versus annually, may be more or less appropriate depending on the questions raised by these users. Thus, portfolio shifts may be better captured through quarterly financial accounts and balance sheets, whereas annual data may provide more accurate information for structural types of analysis. The interest in financial accounts and balance sheets is also a function of specific events and times. Undoubtedly, the 2007-09 economic and financial crisis has increased the demand for financial accounts and balance sheets, both from a general macroeconomic point of view, and from the perspective of financial stability analysis and monetary policy. This chapter highlights the latter use of financial accounts and balance sheets for policy purposes, and also discusses the use of financial statistics by famous economists, from the early 1950s to today.

1. Annual versus quarterly financial accounts and balance sheets

Financial accounts and balance sheets have traditionally been published on an annual basis, reflecting to a large extent the complexity of their compilation process. In order to get a comprehensive and fully integrated set of information on financial flows and positions across economic sectors, various statistical sources, often designed for different purposes and not necessarily sharing common methodological standards, have to be used and combined. Under these circumstances, the compilation of the accounts is a time consuming exercise of data confrontation and reconciliation, which requires expertise in both national accounts and in financial reporting. Moreover, the absence of high frequency data for some of the sectors and the poor timeliness of some of the data sources can make the compilation of quarterly financial accounts a very challenging endeavour.

However, the financial accounts and balance sheets describe financial phenomena where frequency and timeliness in the provision of statistics are particularly crucial. There is a need for timely and frequent data in financial accounts for many reasons, including the instability of financing conditions, the rapid changes of portfolio compositions and asset prices. As annual financial accounts and balance sheets lack the required periodicity and timeliness, quarterly accounts have been developed to better meet user demands. They provide the framework for detailed, timely analysis of financing developments, enabling users to pinpoint changes in the sources of finance and in financial wealth of the various sectors in the economy. Quarterly accounts also provide insight into changes in liquidity, solvency, and exposures to certain types of risks. For example, quarterly accounts facilitate the monitoring of shifts between intermediated financing and market financing, and between different types of intermediaries within the former. This provides valuable information on the effects monetary policy decisions have, such as how the so-called “unconventional measures” of central banks influence the financial conditions of borrowers.

Furthermore, quarterly financial accounts and balance sheets can show whether movements in money holding are related to portfolio shifts, or they may offer insights into the impact of such shifts on price developments. Similarly, the accounts allow for monitoring the cross-institutional sector dimension of monetary developments and their implication on balance sheets. Through the quarterly accounts, one can also relate financing developments to investment trends, both within sectors and across sectors, in particular if the quarterly accounts can be combined with high frequency data on developments in saving and investments in non-financial assets. Overall changes in wealth can then be analysed at quarterly frequency, both in terms of their determinants and components, which can also serve as platforms for modelling, forecasting and simulation tools that link the financial and non-financial spheres, borrowers, lenders and intermediaries.

Annual accounts as an intermediate step towards quarterly accounts

Timely quarterly financial accounts and balance sheets have been relied upon increasingly frequently by users in policy and research work, examples of which are presented in Boxes 11.1and 11.2. Nonetheless, although they are not well suited for analysing business cycles, annual accounts still provide very valuable information on balance sheet positions, financial investments and financing, e.g. for structural analysis.

As already discussed in Chapter 4, financial accounts and balance sheets serve as a platform for integrating financial information that otherwise would only be accessible via various statistical products which may follow different classifications, valuation techniques and recording conventions. In this box, two examples are provided of uses of financial accounts and balance sheets for the analysis of the households’ economic behaviour. They are based on the Euro Area Accounts (EAA), compiled and published on a quarterly basis by the ECB and Eurostat.

Figure 11.1 shows the dynamics of the financial portfolio of households in the Euro Area. To achieve this comprehensive representation, the compilers have put together monetary statistics, securities holdings statistics, insurance statistics, investment funds statistics, balance of payments data, and statistics on corporate balance sheets, all integrated in the institutional sector accounts framework.

The encompassing picture allows analysts, for example, to disentangle shifts in the portfolio of households. Over the period 2002-16, deposits and insurance technical reserves have been driving the dynamics of financial investment, but their roles in the different parts of the cycle have varied considerably. The large increases in financial investment during the boom prior to 2007, mirroring mainly the buoyant household disposable income, materialised in increases of deposits and insurance technical reserves, in line with the traditional household portfolio composition that favours these two asset categories. However, the downturn in household income as of 2007 and the associated decreases in financial investment initially mainly affected insurance technical reserves, while deposits continued to accelerate up to 2009, due to a portfolio shift away from investment funds. The latter trend reversed in 2013, as the recovery in financial investments again favoured investment funds, thus meeting an economy that has progressively moved towards a less banking intensive and more market based financing stance. By contrast, direct exposure to securities, as opposed to indirect exposure via investment funds, has declined, as households moved away from government securities in the aftermath of the government debt crisis.

Source: ECB and Eurostat (2017).

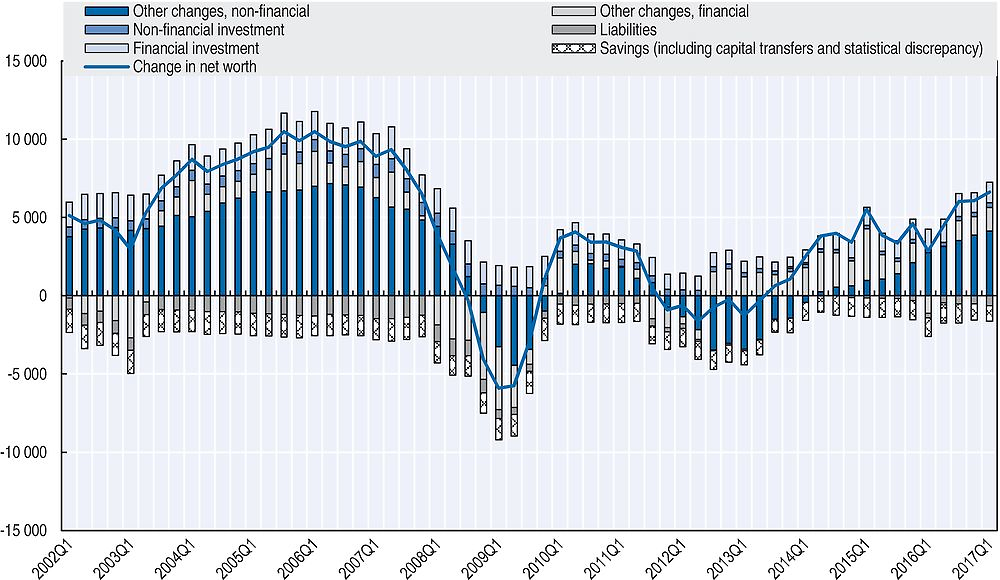

Figure 11.2 shows the accumulation of households’ net assets (including both financial and non-financial assets), or net worth. The changes in net worth are broken down into the following categories: net purchases of assets (in the figure referred to as financial investment); (minus) net incurrence of liabilities other changes in financial assets and liabilities, among which revaluations (other changes, financial); net purchases of non-financial assets (non-financial investment); and other changes in non-financial assets (other changes, non-financial). Finally, the figure also shows the total change in net worth which is due to transactions in financial as well as non-financial assets and liabilities. The latter item corresponds to saving (together with net capital transfers and the statistical discrepancy between financial and non-financial accounts), and is shown with a negative sign as it constitutes, together with the incurrence in liabilities, the source of financing for the accumulation of assets.

Figure 11.2 illustrates the possibility of combining financial and non-financial accounts in a single analytical space, in this case aimed at understanding the accumulation of net assets, or net worth, by households. The dynamics of net worth is clearly dominated by changes in asset prices (and other non-transaction related changes in assets), in particular of non-financial assets. Moreover, both financial and non-financial asset price changes tended to move in tandem, except for the period 2002-03, which is dominated by equity price falls in the wake of the bursting of the dot-com bubble, concerns about corporate governance and the geopolitical uncertainty in the aftermath of 11 September 2001; and the period 2012-14, when financial wealth recovered faster from the downturn after the 2007-09 economic and financial crisis, partially as a result of the implementation of unconventional monetary policy measures by the ECB, while non-financial assets only started to increase after 2014, thus showing a longer reaction time lag.

Source: ECB and Eurostat (2017).

All in all, saving shows a relatively modest contribution to the accumulation of net worth, as compared to the other changes in assets. The first years after the 2007-09 economic and financial crisis, saving showed an increase as a precautionary reaction, then it decreased following subdued income growth, and finally, since 2014, it started to increase modestly, as both income recovery and precautionary behaviour converged, thus contributing to a stronger net asset accumulation.

At the same time, there is no fundamental methodological dichotomy between annual and quarterly accounts. They simply represent two stages in the development of the same statistical product determined by available data sources and statistical capacity. In this respect, the compilation of annual accounts provides valuable insights for developing quarterly statistics. On the basis of their experience with the annual data, compilers gain understanding of the sources available and the integration challenges. Thus, the experience with annual accounts helps statisticians to familiarise themselves with the adjustments required to align each of the sources with the national accounts standards, or the needs for the estimation of items not sufficiently covered by available sources.

Importantly, differences in methodological standards which led to resource intensive adjustments of source statistics are becoming less relevant, facilitating the compilation of quartrely accounts. A major milestone in this respect has been the efforts undertaken by the international statistical community to align the latest international standards for compiling national accounts, the 2008 System of National Accounts (2008 SNA), with the latest standards for balance of payments, the Balance of Payments and International Investment Position Manual (BPM6). This has removed what has traditionally been a major source of discrepancy, as the balance of payments is one of the most important sources used to compile financial accounts and balance sheets.1 Moreover, high frequency financial statistics in certain jurisdictions are increasingly being aligned with the standards for the institutional sector accounts. This is, for example, the case in the European Union, where recent updates of the regulatory framework for the compilation of statistics on balance sheets for Monetary Financial Institutions, Financial Vehicle Corporations, Investment Funds and Insurance Corporations are aligned, to the extent possible, with the European System of Accounts (ESA) 2010, the adaptation of the 2008 SNA in the European context.

At the same time, new high frequency financial data are becoming available, extending good periodicity to other areas that in the past required the use of “quarterisation techniques”. In particular, the availability of micro-databases in the areas of securities and loans have increased the ability to produce highly reliable and frequent data covering the non-financial sectors.

Moreover, the development of sophisticated analytical technologies supporting multi-dimensional data has also enabled the complex geometry of financial accounts, in particular in from-whom-to-whom data, to be compiled more easily with a higher periodicity. Similarly, methodological and technological developments now enable much faster and efficient algorithms for balancing the data, which also contributes to the feasibility of timely quarterly financial accounts.

It should be reiterated that the financial accounts are a single entity, for which the quarterly and annual accounts are just two representations of the same system, only different in terms of periodicity. In this they do not depart from non-financial, current and capital, sector accounts, for which quarterly and annual accounts also co-exist. However, in some countries there may be a difference between the two cases. In non-financial sector accounts, the availability and/or the quality of quarterly source statistics can be quite problematic, as a consequence of which the quarterly accounts are often constructed using indicators to extract quarterly patterns out of the annual accounts; this is due to the fact that the statistical basis for high quality non-financial accounts is usually of annual frequency. In financial accounts and balance sheets, however, the compilation objective is to develop a high quality quarterly statistical basis and appropriate methods on which the compilation of the accounts can be based. This is unavoidable if the intention is capturing financial developments, which are by nature of higher frequency. The annual financial accounts and balance sheets then just become a “by-product” of the quarterly accounts (rather than the latter being an extension of the former), by using temporal aggregation of quarters.

A clear example of published quarterly financial accounts and balance sheets that has followed the above two-stage development pattern can be found in the quarterly Euro Area Accounts (EAA), jointly published by the ECB and Eurostat. The project started back in 20052 by combining Euro Area financial statistics (or building blocks) and nationally available financial accounts and balance sheets. The project required the development of quarterly national accounts in a number of countries to be successful at the Euro Area level, which was achieved in 2007. Meanwhile, the institutions developed and published annual accounts, which served to help them gain experience in data completion and adjustment, confrontation and reconciliation. The interim experience with annual accounts was particularly useful for better understanding the implications of integrating financial and non-financial accounts, which is pursued in EAA for most institutional sectors.

The 2007-09 economic and financial crisis and the increased need for quarterly accounts

In the years following the onset of the global economic and financial crisis in 2007, the financial markets have shown declines in the value of assets, large financial transactions, disorderly balance sheet restructuring, shifts in portfolios, and adjustments to saving, financing and intermediation patterns. The crisis has taken various forms, and has impacted many areas, from the housing markets to the sustainability of government finances. Sharp financial movements initiated by non-bank intermediaries resulted in large banking crises intertwined with government debt crises. Imbalances moved swiftly across sectors and countries. Balance sheet configurations were suddenly at the centre of political concerns, including the relationship between them and the non-financial economy.

Understanding the intricate relationships between these events required, in principle, undertaking the challenging task of pooling and analysing economic and financial data with different methodological backgrounds. Moreover, traditional analysis often lacked comprehensive and methodologically consistent tools to help make sense of the various messages embedded in this multiplicity of data. Financial accounts and balance sheets, in particular if integrated with non-financial sector accounts, may fill this gap and provide useful insights for the analysis.

For example, the financing patterns of non-financial corporations are a major topic that financial accounts and balance sheets can shed light on. The run-up to the 2007-09 economic and financial crisis saw an increase in financing channels other than traditional banking loans. The phenomenon took different shapes, but in the Euro Area securitised loans were the most prominent; see Chapter 3 and the discussion on the “originate-to-distribute” model. More generally, one can also monitor from the financial accounts and balance sheets developments in the “shadow banking” sector. i.e. high-leverage institutions providing finance and performing bank-like intermediation without formally being banks (without being subjected to bank regulations). Financial accounts and balance sheets thus allow a user to see the developments of shadow banking in conjunction with banking and in relation to the overall sources of corporations' financing; see Box 11.2.

Chapter 5 discusses non-financial corporations in detail. Figure 11.3 presents the total financing of non-financial corporations in the Euro Area, broken down by financial instrument, to show changes in financing patterns over the last 15 years. The Euro Area non-financial corporations have been very dependent on bank financing (MFI loans) up to the start of the 2007-09 economic and financial crisis, especially from 2005 onwards, when the last financing boom period started. As a consequence, the crisis manifested itself in the Euro Area with a sharp decline in bank financing, also accompanied in the first two years by a fall in trade credits, both reflections of the sudden decline in economic activity.

The continued downturn in financing in the subsequent years was also characterised by very low bank financing, reflecting the severe banking crisis in many countries, but, as opposed to the previous period, this was partially offset by more buoyant financing via the issuance of debt securities and inter-company financing (trade credits and intercompany loans). This seems to indicate a gradual structural change in the sources of financing in the Euro Area towards more market-based funding, as opposed to bank financing, also considering that loans granted by Other Financial Institutions (OFIs) and non-residents may cover funding from securitisation companies and the issuance of securities via captive institutions.

The figure also illustrates the possibility of presenting financial accounts and balance sheets together with other information that may shed light on, or supplement, the analysis of financing trends. In this case, the cost of borrowing is shown to pinpoint periods where, for various reasons related to the monetary policy stance, it was not fully following the same pattern as financing. This happened, for example, from 2003 to mid-2005, from 2010 to 2012, and notably since 2014 with the clear decoupling of the two series.

Source: ECB and Eurostat (2017), EAA; ECB (2017), MFI Interest Rates.

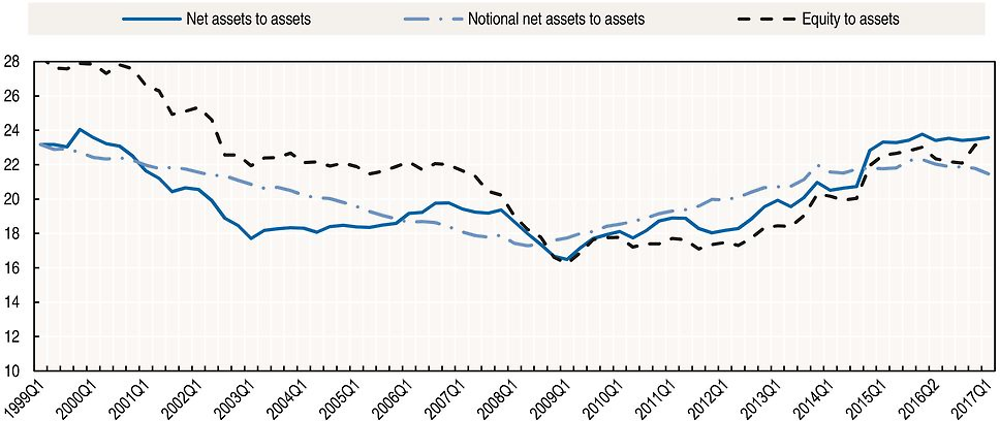

Figure 11.4 presents the capital position of the financial corporations’ sector in the Euro Area, providing a macroeconomic perspective of the sector exposure to excess leverage. Three measures are provided. The headline indicator “net assets to assets ratio” (or capital ratio) shows the net assets (difference between total assets and total liabilities, the latter excluding equity) as a percentage of total assets, and provides a measure of (the inverse of) leverage in terms of national accounts concepts. The dynamics of this ratio, however, do not only reflect the active efforts by the financial system to build up capital buffers, as – following 2008 SNA valuation criteria – the ratio is also affected by asset price changes. As an alternative, the “notional net assets to assets ratio” (or notional capital ratio) is presented, which is calculated like the headline ratio, but with stocks/positions valued at historical acquisition costs (notional stocks), so that asset price changes do not affect the ratio.

The period from 2003 to 2007 reflects the different dynamics of the two ratios, as the headline ratio was increasing on the back of strong asset price increases, while the notional ratio was decreasing, leading to a concomitant decrease of capital reserves relative to assets. More generally, the notional ratio shows the different dynamics of leverage before and after the 2007-09 economic and financial crisis. The ratio decreases very rapidly during the boom period up to the end of 2008, as a consequence of a large increase in lending that was not matched by a similar increase in precautionary capital buffers. This changed sharply after 2008, when the trend reversed and capital was built up more rapidly than lending as a result of a combination of precautionary reactions, more stringent regulatory requirements and government interventions.

Figure 11.4 is completed with the “equity to assets ratio”, calculated as the quotient of equity liabilities at market value to assets at market value. Compared to the headline indicator, it shows whether the market perception of the capital stance is larger or smaller than what can be derived from the net assets of the sector. As such, the difference between the two ratios is nothing but a measure of “Tobin’s q”. Figure 11.4 shows a clear change in the relation between the ratios (i.e. in the market perception of the capital position relative to the value of net assets) before and after the start of the 2007-09 economic and financial crisis, with the equity ratio being larger than the net assets to assets ratio before 2008 (Tobin’s q being larger than 1), and being smaller after 2008 (q lower than 1).

Note: Equity comprises listed and unlisted shares and other equity. Net assets is the difference between assets and liabilities, the latter excluding equity. All assets and liabilities are valued at market value. The “notional net assets to assets” ratio is calculated on the basis of net assets and assets excluding changes in prices of assets and liabilities. Interbank deposits and Eurosystem financing are netted out from assets and liabilities.

Source: ECB and Eurostat (2017).

After the start of the crisis, the extraordinary balance sheet constraints faced by Monetary Financial Institutions (MFIs) also fostered alternative sources of financing. Apart from shadow banking, market financing via bonds became relevant in areas where it was not prevalent before, such as in the Euro Area; see also Box 11.2. This shift in composition and relevance, visible through the analysis of financial accounts and balance sheets, impacted monetary policy decisions aimed at restoring the credit financing channels through the so-called “unconventional measures”. Again, financial accounts facilitated the identification of the type of instruments and institutions that, if targeted, could have a stronger impact on the access to financing by non-financial corporations.

“From-whom-to-whom” breakdowns and network analysis tools

“From-whom-to-whom” (FWTW) breakdowns (see Chapter 2), whose importance had already been highlighted as far back as 1968 by Brainard and Tobin, are attracting increasing interest among analysts. Counterpart sector information is key to understanding financing and investment flows, by supporting analysis on which sectors are financing which other sectors. Using tools of network analysis, these inter-sector relationships can be identified as direct or as indirect (those that go from ultimate lenders to ultimate borrowers via intermediaries), thus also facilitating the monitoring of the role of the various sectors in the intermediation function. The FWTW presentations constitute the ultimate tool for a true “flow-of-funds” analysis.

Similarly, a FWTW presentation of balance sheets provides information on inter-sector exposures. This tool can better answer questions such as which sectors would be more affected by a decline in asset prices of equity and debt instruments issued by a given sector. Network theory can be applied to disentangle how shocks in asset prices impact across sectors, how leverage rebalancing effects would travel in the network, or which sectors are the most vulnerable and interconnected. Financial stability analysis, from a macro perspective, benefits enormously from the availability of counterpart sector information.

The more granular the sector breakdown, the more useful the analytical possibilities brought by FWTW information become. In particular, having rich subsector details for financial institutions is a prerequisite for a high quality financial stability analysis of vulnerabilities, contagion and propagation chains. Similarly, further breakdowns of the non-financial sectors (for instance, disaggregating households by income or wealth quintiles, or non-financial corporations by size or balance sheet structure) would enhance the information content for the analysis of exposures. In other words, the richer, the more complex and the more representative the networks in the FWTW matrices are, the more can be obtained from network analysis applied to them.

Further exploitation of micro-data and distributional household accounts

The availability of source data for compiling granular breakdowns might be rather limited for some sectors, in particular for the non-financial sectors. However, by combining information from core financial accounts and balance sheets with micro-data (including survey data and administrative registers), one could still infer FWTW matrices with high granularity. Generally, further work in the area of combining macro- and micro-data to enhance the macro analysis is very high on the agenda of financial accounts compilers. For example, in the aftermath of the 2007-09 economic and financial crisis, a significant amount of work has been done, and is still ongoing, to compile very detailed data on the issuances and holdings of securities. Another line of work in integrating macro and micro information relates to information on the distribution of income, consumption, saving and wealth across households. The increasing inequality in income and wealth in modern economies has not only become a matter of social and political importance, but also of high relevance for monetary and financial stability policy. Financial and non-financial sector accounts, by providing key indicators for the households sector, offer the possibility of linking national accounts with micro-data on income and wealth of households. While sector accounts offer detailed and complete information on the “average” household in an economy, households surveys and administrative data (e.g., from tax authorities) have the potential to provide key distributional information that could be mapped with the aggregate information in the traditional system of national accounts. For more information on the complexities of this micro-macro linking, refer to Zwijnenburg et al. (2016).

2. The use of financial accounts to assess financial stability

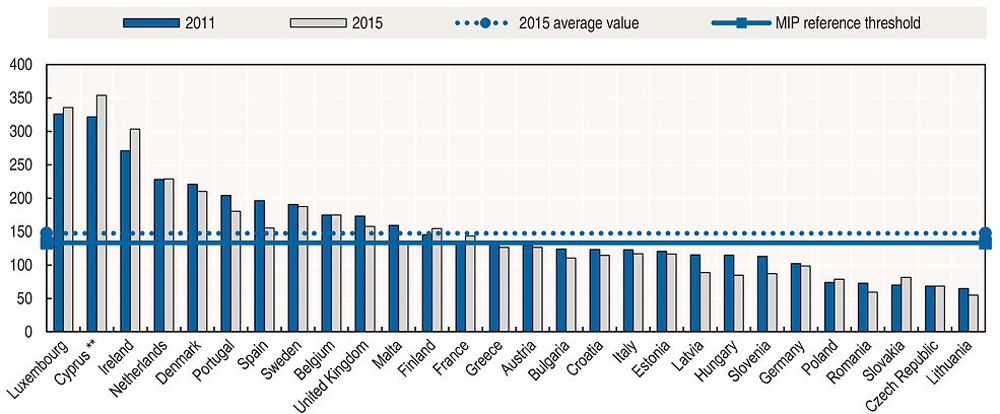

As discussed extensively in Chapter 10, financial accounts and balance sheets play a key role in financial stability analysis. This analysis focuses on the assessment of risks that represent a potential threat for the financial system. The evaluation encompasses either risks originated within the financial system, such as liquidity and market risks which spread through financial intermediaries, or risks from outside the financial system, mainly from macroeconomic conditions such as business cycle conditions, developments in non-financial sectors’ debt levels, and international imbalances (Bardsen et al., 2006). Financial accounts and balance sheets are instrumental in detecting imbalances and thus offering important insights into mismatches that may lead to significant rebalancing by corporations and households. Sectoral indicators built on financial accounts are relevant for policy purposes, such as the so-called “Macroeconomic Imbalances Procedure” (MIP) in Europe, and the so-called “IMF Balance Sheet Approach”.

The EU Macroeconomic Imbalances Procedure

To improve governance, the European Union adopted a surveillance procedure in 2011 to detect and correct macroeconomic imbalances. This Macroeconomic Imbalance Procedure (MIP) has an alert mechanism, in which a scoreboard of indicators monitors country risks in a more systematic way. The scoreboard contains indicators that are able to capture both internal and external imbalances of countries, including countries’ competitiveness. The indicators are used as an initial screening tool for the alert mechanism report (AMR). For each of the indicators, a threshold is defined which is to be considered as indicative, and countries reporting values beyond this threshold are not considered automatically vulnerable. The assessment of countries is based on an “economic reading” of the scoreboard, which also takes into account other relevant economic information.

With respect to financial accounts and balance sheets the MIP scoreboard covers, for example, private sector debt, private sector credit flow, and total liabilities of the financial sector. The presence of stock and flow indicators makes it possible to capture short-term deteriorations as well as longer term accumulations of imbalances (European Union, 2012). Figure 11.5 summarises the MIP private sector debt indicator, based on financial accounts and balance sheets, for European countries. At the end of 2015, the average debt was about 150 per cent of GDP, slightly larger than the MIP reference threshold. The heterogeneity of the debt indicator plotted in the figure may reflect country-specific factors; for example, in Ireland and Luxembourg, the high presence of multinational enterprises contributes to the high ranking.

1. The private sector refers to non-financial corporation and household sectors. Countries are decreasingly ordered according to 2011 debt ratio.

2. Note by Turkey: The information in this document with reference to “Cyprus” relates to the southern part of the Island. There is no single authority representing both Turkish and Greek Cypriot people on the Island. Turkey recognises the Turkish Republic of Northern Cyprus (TRNC). Until a lasting and equitable solution is found within the context of the United Nations, Turkey shall preserve its position concerning the “Cyprus issue”.

Note by all the European Union Member States of the OECD and the European Union: The Republic of Cyprus is recognised by all members of the United Nations with the exception of Turkey. The information in this document relates to the area under the effective control of the Government of the Republic of Cyprus.

Source: Eurostat (2017b), Macroeconomic Imbalance Procedure Indicators (database), http://ec.europa.eu/eurostat/web/macroeconomic-imbalances-procedure.

Figure 11.5 shows that 16, out of 28, European countries recorded a debt ratio below the reference threshold in 2015, while ten countries showed a debt ratio increase, as compared to the level at the end of 2011. The contribution of new transactions to the debt developments since 2011 can be assessed in Figure 11.6. Between 2012 and 2015, repayments were larger than the incurrence of new debt in fewer than half of countries (in the figure presented as negative flows). Only three countries exceeded the reference threshold in 2012, and only one country exceeded the threshold in 2014 and 2015.

1. The private sector refers to non-financial corporations, households, and non-profit institutions serving households.

Source: Eurostat (2017b), Macroeconomic Imbalance Procedure Indicators (database), http://ec.europa.eu/eurostat/web/macroeconomic-imbalances-procedure.

The analysis of financial stability in the IMF Balance Sheet Approach

Analyses of determinants of financial and currency crises, which have hit many economies since the 1970s, focus on different variables. The first models, typically referred to as first generation models and developed by Krugman (1979) and Flood and Garber (1984), emphasise the role of fundamentals in generating crises: fiscal budget, foreign trade deficits, inflation, interest rates, etc. The deterioration of these variables can give rise to imbalances with the pegged exchange rate to which the central bank is committed. These imbalances may be overlooked if central banks have large stocks of foreign reserves, but when reserves are low, or are perceived as low by the market, a speculative attack on the currency could be triggered. In line with the prediction of these models, the 1992-93 speculative attacks to the exchange rate mechanism (ERM) of the European Monetary System have been attributed to inadequate monetary and fiscal policies (BIS, 1993). The Mexican crisis in 1994-95 shared some similarities to the ERM dysfunction. In the midst of severe political instability, the government adopted a relaxed monetary and fiscal discipline in the run-up to the presidential election. As a consequence, foreign capital inflows reduced along with foreign exchange reserves, and the government was finally unable to roll over the dollar-denominated short-term debt (Krugman, 2010). This situation led the Mexican authorities to depreciate the peso.

Not all economists agreed with these interpretations. Empirical evidence by Eichengreen et al. (1995) shows that, while some speculative attacks are preceded by rapid growth of money and inflation, other attacks cannot be explained very well by imbalances, but seem more in line with a story of self-fulfilling crises, where sudden change in market participants’ sentiment plays a crucial role. The second-generation models developed by Obstfeld (1994) hold this view.

The debate about the role of fundamentals led in 1989 to the proposal of the so-called “Washington consensus” among US economic officials, the International Monetary Fund and the World Bank (Williamson, 2004). Based on the experience of Latin America economies during the 1980s, the Washington consensus document discussed economic policy instruments that are perceived as important for sustaining growth in developing countries. The list of ten policy prescriptions addressed topics related to fiscal discipline, public expenditure priorities, tax reform, interest rates, exchange rates, trade liberalisation, foreign direct investment, privatisation, deregulation, and property rights. In line with this policy agenda, strong privatisation, deregulation and trade liberalisation were prescribed and followed in Latin America and Eastern Europe. However, growth was below expectations. Similarly, the take-off in Sub-Saharan Africa revealed disappointing results, despite significant policy reform (Rodrik, 2006).

While the first two generations of models seem to fit many crisis stories up to the mid-1990s, they fail to explain the disruption in the major Asian economies in the late 1990s. The Asian crisis of 1997-98 (a “new-style” crisis as labelled by Dornbusch [2002]) shifted attention to other directions. The third generation of models highlighted the presence of currency mismatches in corporations’ and banks’ balance sheets, in particular where banks borrowed in foreign currency and lent in local currency. As a consequence, financial shocks were amplified and spread to other sectors and economies, even in the presence of a sound fiscal situation and a sustainable external deficit. The key lessons learned were that the economy should be seen as a network of sectors where interactions could lead to a potential contagion of shocks. Due to the removal of capital restrictions and increased globalisation, economies had become more interconnected, with shocks not being restricted to a single sector or country, but having possible spill-over effects, which leads to more systemic risk.

After the Asian crisis, the IMF fostered the foundation of a new approach to country surveillance beyond monitoring inflation, public sector and balance of payments imbalances. This new strategy, implying a critique of the Washington consensus strategy,3 was called the Balance Sheet Approach (BSA). It was proposed by Allen et al. (2002), as a complement to the flow analysis. The BSA focuses on stock variables and the analysis of a wider range of sectors (central bank, other depository corporations, other financial corporations, general government, non-financial corporations, other resident sectors, and non-residents). It is evident that such an analysis can only be based on the availability of balance sheets for each of the sectors, including FWTW information. The agreed scheme, as presented in Table 11.1, looks like the traditional financial accounts and balance sheets, but adapted to take into account inter-sectoral assets and liabilities, in the same vein as the FWTW version of the financial accounts and balance sheets. The information that can be derived from this table only relates to the overall position of the sectors, i.e. total assets and total liabilities, with a breakdown by currency. In addition, one can derive information on the counterpart sector, in particular whether there are large exposures toward the Rest of the World, which generally plays an important role during the build-up of a crisis. The matrix was and is considered as a starting point to investigate the presence of risks and to evaluate the potential transmission channels of shocks.

|

Table 11.1. Balance sheet matrix1

|

|---|

|

|

|

← 1. A: Assets; L: Liabilities. |

|

Source: IMF (2015), Balance Sheet Analysis in Fund Surveillance, www.imf.org/external/np/pp/eng/2015/061215.pdf. |

Within the BSA framework, the analysis focuses on four different risks (Allen et al., 2002):

-

“maturity mismatch”, typically related to balance sheets where long-term assets coexist with short-term liabilities;

-

“currency mismatch”, in the presence of liabilities denominated in foreign currencies;

-

capital structure, looking at the debt exposures compared to equity; and

-

solvency, analysing whether assets are able to cover all liabilities.

Key indicators to unveil potential vulnerabilities are the “net financial position” (or net financial worth) of sectors, along with the “net foreign currency position” (defined as the difference between assets and liabilities denominated in foreign currencies) and “net short-term position” (defined as the difference between short-term assets and short-term liabilities). Large negative foreign currency positions may signal a sectoral vulnerability to exchange rate variations, in particular in the case of high short-term debt which may be difficult to roll over. Large negative net financial positions may be correlated to solvency problems, and a high leverage can exacerbate the vulnerability of a sector. Finally, short-term liabilities highlight, for example, a sector’s (in)ability to withstand rises in the interest rate.

Prior to the 2007-09 economic and financial crisis, the IMF only complemented the more traditional flow based indicators with balance sheet analysis for a few economies (IMF, 2015), in particular for transition countries like Estonia, Latvia, and South Africa. Advanced countries were considered to be in sound condition and less exposed to the above mentioned risks and vulnerabilities, although some sectoral vulnerabilities were highlighted. For example, the IMF (2002) strongly emphasised the high indebtedness of non-financial corporations in the United States. After the global financial crisis the IMF increased the use of the balance sheet analysis in its surveillance, and at the same time launched different initiatives to enhance the availability of data. The G-20 Data Gaps Initiative (see Chapter 10) and the IMF’s Special Data Dissemination Standard Plus addressed the issue of data shortage and made further recommendations to enhance data availability. New initiatives aim at recovering currency breakdown, remaining maturity4, off-balance sheet items (contingent assets and liabilities), and bilateral counterparty statistics to track sectoral interlinkages. In the same vein, Palumbo and Parker (2009) discussed the importance of having a more detailed classification of assets which separates out structured financial products, along with the need to have a more detailed representation of financial intermediaries, which allows users to analyse which intermediaries are more exposed to leverage.

During the first half of the 1990s, Thailand was a starring economy part of the so called “Asian miracle”, thanks to the liberalisation of financial markets and the reduction of foreign trade barriers. Driven by exports and the inflow of large amounts of foreign capital, the economy experienced an accelerated GDP growth along with a strong increase in investments. Notwithstanding this background, Thailand was one of the Asian economies hit in the late 1990s by the severe Asian crisis.

By using balance sheets, it is possible to analyse and assess whether imbalances were at work before the crisis unfolded. At the end of 1996, non-financial corporations and banks showed a high short-term debt denominated in foreign currency, which posed risks in case of exchange rate depreciation (Dawson, 2004). Non-financial corporations had raised foreign currency debt provided by domestic banks, thus increasing sectoral linkages (Allen et al. 2002). While foreign exchange reserves increased coherently with the large country imports, the foreign exchange reserves looked inadequate to the risks posed by the amounts of foreign short-term debt. Banks were also suffering a maturity mismatch in their balance sheets, with short-term assets unable to cover short-term liabilities.

The flow analysis also highlighted weakness in the current account. Due to lower competitiveness, exports decreased in 1996, in turn provoking a deficit of the current account. This fragile outlook was perceived by international lenders as a very risky and vulnerable situation, mainly because the foreign currency denominated short-term debt was not matched by the country’s foreign exchange reserves. As a consequence, lenders decided to reduce their exposures. In 1997 the Thailand currency (baht) underwent a speculative attack which led to an exhaustion of international reserves and to a devaluation of around 30 per cent. This triggered the crisis, with foreign lenders refusing to roll over the Thai debt.

Detecting imbalances through the financial accounts and balance sheets

Chapter 10 discussed how the 2007-09 economic and financial crisis drew new attention to balance sheets and to their interplay with financial flows. Important questions have been analysed through financial accounts statistics: leverage cycles, intermediation chains, interactions between the real economy and financial systems, etc. (Winkler et al. [2014]). Some research using these statistics showed how the potential signs of weakness could have been detected, at least partly, before the outbreak of the crisis.

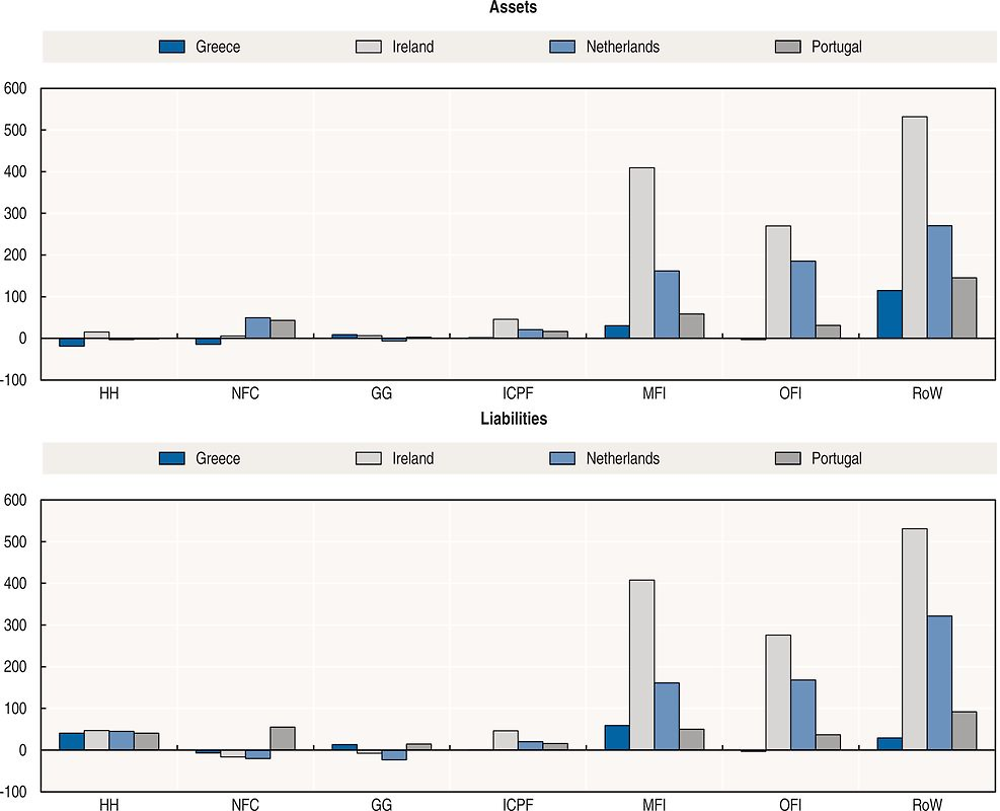

Focusing on the financial structure of the G7 plus some small European countries (Greece, Ireland, the Netherlands and Portugal), Infante et al. (2012) ran a simple exercise by comparing gross and net positions of each institutional sector between two periods: the average financial stocks between 1997 and 1999 (a period with relatively balanced financial positions) and the financial stocks at the end of 2007, before the inception of the crisis, when the imbalances may have reached their peak. The first pattern that emerged revealed intense international integration5 between the 1990s and 2007. Thanks to the removal of capital controls, low interest rates, rapid liquidity and credit expansion, showing favourable global financial conditions, all countries increased their assets and liabilities with the Rest of the World; see Figures 11.7 to 11.9.

While well-developed and open global financial systems may allow for the optimal allocation of capital and diversification of risks, higher levels of asset and liability positions have been shown to increase exposure to valuation gains or losses and increase financial stability risks. Furthermore, the foreign currency denomination of liabilities along with a large presence of debt, as explained in the previous section, may increase the fragility of the country in case of currency devaluation. Figure 11.7 to 11.9 also shows that internationalisation is usually more intense in small countries than in large countries: the average stocks of the Rest of the World’s assets as a percentage of GDP moved from 3.5 to 6 times GDP between 1997-99 and 2007 (with Ireland reaching a peak in 2007 equal to 13 times the GDP), while the liability side changed from 3.4 to 5.8 times GDP. Looking at the domestic sector, the imbalances were mainly accumulating in the balance sheets of households. In banking and other financial sectors, the net positions were rather balanced. However, the composition of assets and liabilities hid some important vulnerabilities, in particular related to the use of leverage and the characteristics of debt. Intermediaries employed short-term debt (i.e. interbank loans) to widen their balance sheets (which raised maturity mismatches) and, in many cases, relied on foreign capital.

Map legend (for Figures 11.7- 11.9): HH: households; NFC: non-financial corporations; GG: general government; ICPF: insurance corporations and pension funds; MFI: monetary financial institutions; OFI: other financial intermediaries; RoW: Rest of the World.

Source: Source (for Figures 11.7- 11.9): Infante et al. (2012). ‘Imbalances in Household, Firm, Public and Foreign Sector Balance Sheets in the 2000s : A Case of “I Told You So?”’

Source: Source and map legend: See Figure 11.7.

Source: Source and map legend: See Figure 11.7.

The domestic financial developments can be associated with the sustained international financial integration, and the size of financial systems was found to be positively correlated to the external financial positions (Lane and Milesi-Ferretti, 2008). This interplay between the financial system and international capital flows led to an increase of credit growth, thus raising the likelihood of a crisis outbreak (Mendoza and Terrones [2008]; Schularick and Taylor [2012]). In presence of open financial systems, domestic banks managed to enhance their funding opportunities thanks to the possibility of collecting financial resources from foreign depositors or from international interbank counterparties. The latter opportunities allowed banks to increase their non-monetary liabilities (i.e. wholesale funding), and to grant credit beyond collected deposits. The dynamics of loan growth showed a decoupling from money growth (Schularick and Taylor [2012]). Lane and McQuade (2013) also emphasised that the domestic credit growth was strongly correlated with international capital flows; the correlation involved only debt flows and not equity instruments.

Leverage has been an important factor in explaining the build-up of mismatches and financial instability. Adrian and Shin (2008) documented how financial intermediaries exploited the asset price booms to expand the size of their balance sheets, through actively managing leverage, while a symmetric strategy was adopted during downturns in order to shrink the balance sheets. Any increase in asset prices, with liabilities valued at their nominal values, automatically raised the value of the assets of financial intermediaries, and consequently the market value of their equity (defined as total assets minus total debt liabilities), resulting in a reduction of leverage. Contrary to the evidence for other sectors, financial intermediaries reacted to this by restoring leverage to at least its previous level by increasing liabilities (mainly using repurchase agreements), which in turn were employed in new market claims, for instance the acquisition of new securities or the supply of loans.

Through the US financial accounts and balance sheets, Adrian and Shin (2008) produced evidence of a pro-cyclical use of leverage by showing the co‐movement of assets and liabilities for both the banking sector and the security brokers and dealers. During the expansionary phase, the growth of assets was matched with an increase in liabilities, in order to restore the leverage ratio, while during the downturns the reduction in the value of assets was followed by a reduction in liabilities. The pro-cyclicality was more pronounced for security brokers and dealers than for the banking sector, due to the differences in the composition of the balance sheets of the two classes of intermediaries. Banks hold a large amount of loans that are recorded in the financial balance sheets at book value, while security brokers and dealers hold, for instance, securities reported in the balance sheets at market value, which are therefore more vulnerable to developments in market prices.

Based on the data from the institutional sector accounts, Girón and Mongelluzzo (2014) also verified the impact of the use of leverage by monetary financial institutions on credit developments. The authors focused not only on the balance sheets (outstanding positions) of monetary financial institutions, but also on the net acquisitions of assets (financial transactions), to disentangle changes in leverage due to asset price movements (defined by authors as automatic reaction of leverage) and those due to deliberate decisions to increase positions through net acquisitions of assets (active leverage). They confirmed leverage pro-cyclicality for six out of ten European countries (Belgium, France, Germany, Italy, the Netherlands, and Spain). Moreover, before 2008, the growth in the provision of credit on the assets side, with the ensuing enlargement of the balance sheets, could not be associated with a proportional increase in the banks’ own equity, but was instead boosted by inordinate growth of liabilities and therefore by an increase of leverage.

The increase of leverage in the financial sector did not only translate into an increase of loans to households and non-financial corporations, but to some extent also led to the growth in the size of lending/borrowing within the financial intermediation system itself. Using financial accounts and balance sheets from 1995 to 2007, Bartiloro and di Iasio (2012) proved that financial innovations introduced by banks, mainly in funding activities, did not result in a significant improvement of non-financial corporations' financial conditions. Changes in intermediation activity only led to an increased interconnectedness within the financial system. The authors reported a low ratio of deposits to liabilities in the United States’ financial sectors (19 per cent), compared to higher percentages in Italy and Spain (respectively 42 and 56 per cent). At the same time, data showed a larger use of short-term loans, which was at the heart of the increased interconnections within the financial system. Moreover, to complement deposits with short-term funding in the wholesale credit market, banks benefited from loan securitisation which helped them to recover liquidity from illiquid assets (i.e. mortgages). Securitisation contributed to the relaxation of banks’ reliance on the savings of non-financial sectors, and the building up of linkages within financial systems.

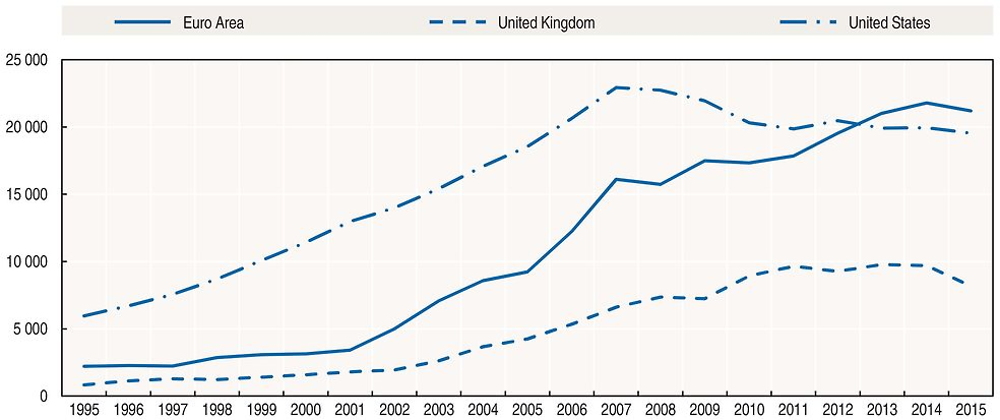

Based on US financial accounts and balance sheets, Adrian and Shin (2009) added evidence on the deep transformation in the financial system. Securitisation was intensively used by banks, increasing their interconnections with the financial markets for debt securities. Starting from the 1980s, bank loans, mainly mortgages, were transformed into securities and sold to investors, a process that mirrored the very large growth of security brokers and dealers’ assets, or more generally the assets of the other financial intermediaries. Banks originated loans and distributed them to the market with the aim to reduce lending risk by spreading it among a large number of agents, in this case the holders of the securitised loans. This mechanism explained, at least partly, the increase of subprime mortgages. Figure 11.10 shows the evolution of assets of other financial intermediaries (excluding investment funds) in the United States, the Euro Area and the United Kingdom during the last two decades; in all these economies the assets show a strong positive trend. Between 1995 and 2007 the sector in the United States grew almost 300%, while in the other countries the growth was even more pronounced (around 600% in the Euro Area6 and almost 700% in the United Kingdom).

← 1. Euro Area contains Austria, Belgium, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovak Republic, Slovenia and Spain. For some countries time series are not complete, German data are reported from 1999, for Ireland and Slovenia data starts from 2001, finally the first observation for Luxembourg is 2002.

← 2. For comparability across countries, the sector includes other financial intermediaries (excluding non-MMF investment funds and insurance corporation and pension funds), financial auxiliaries, captive financial institutions and money lenders.

Source: OECD (2017), “Financial Balance Sheets, SNA 2008 (or SNA 1993): Non-consolidated stocks, annual”, OECD National Accounts Statistics (database), https://doi.org/10.1787/data-00720-en.

Rebalancing mismatches after the 2007-09 economic and financial crisis

The 2007-09 economic and financial crisis was triggered by sectoral imbalances and evolved into a balance sheet recession. The recovery relied on re-balancing the mismatches. Within Euro Area countries, the correction of the macroeconomic imbalances started in the period between 2008 and 2010. Measures were directed to the recapitalisation of financial institutions to assure a proper functioning of the financial system, and to the consolidation of government finances along with the adoption of structural reforms. Adjustments took place in countries with foreign trade deficits (Greece, Spain, Portugal and Ireland), mainly through a compression of domestic demand (ECB, 2012). Non-financial corporations and households consequently increased their saving rates, to reduce their debt. Corporate debt was reduced in Spain, while it remained stable in Greece and Portugal. Also in the United States, households increased their saving, jointly with a moderation of consumption and a lowering of residential investments which had peaked during the years before the crisis. Uncertainty on future conditions affected the US corporate sector, which reacted by augmenting the retained earnings and reducing their debt exposure.

To offset the impact of the crisis and to support private demand, the governments adopted counter-cyclical measures which, together with the financial support to the financial system, resulted in a worsening of government debt. Although Koo (2011), for example, considered these measures as insufficient to compensate for the decline in aggregate demand, after the sovereign debt crisis, governments of the Euro Area countries started to rebalance their balance sheets.

He et al. (2010) analysed balance sheet adjustments by quantifying how sectors in the United States dealt with securitised assets (i.e. mortgage backed securities and other asset-backed securities) when the crisis started. Between the second quarter of 2007 and the second quarter of 2009, the problems in the repo markets, in particular the rise in (agreed) write-offs on debt and the worsening of credit conditions started to affect non-bank financial intermediaries which in turn started to deleverage. Mortgage backed securities had to be transferred to the government sector, which played a pivotal role in the adjustment of the whole financial sector. In addition to buying securities, the government indirectly helped the banking sector by offering guarantees. Banks were mainly financed through government-backed debt, while the Treasury also purchased preferred shares and various hybrid debt instruments. Contrary to other financial intermediaries’ balance sheets, banks increased the acquisition of securitised assets, resulting in a further increase in leverage7. Leverage was almost doubled as compared to normal periods, showing that not all sectors deleveraged in the same way. According to this view, leverage was re-distributed across the financial intermediaries. A possible explanation for this banking behaviour is that commercial banks still had access to stable funding, while other financial intermediaries were mainly funded through repos.

The policy use of sectoral indicators

The increased understanding of the causes of the 2007-09 economic and financial crisis pushed policy makers to increase the monitoring of financial flows and positions, with the aim of detecting potential misalignments and designing measures to intervene. For years, economists focused on price variables as sufficient indicators of market equilibrium, neglecting the potential information contained in the financial transactions and positions of sectors (Visco [2012]). In 2009, the IMF and the Financial Stability Board (FSB) recommended a number of improvements in statistics to strengthen economic analysis and policy. The recommendations of the G20 Data Gaps Initiative (DGI) (see Chapter 10) stressed the relevance of monitoring the risks in the financial sectors, the (inter)national financial linkages, and the potential vulnerabilities of domestic sectors through financial accounts and balance sheets data and other comparable financial statistics. The communication of official statistics was also considered as an important area of improvement.

Several countries produce a financial stability review through which the developments of risks in financial systems and the sectoral exposure are assessed, along with their ability to withstand shocks.8 Heath (2013) mentions the key role that institutional sector accounts play in the analysis of macroeconomic conditions and the development of macro policies. The recent compilation of FWTW statistics was also considered relevant to demonstrate the linkages with other domestic sectors and their exposures towards the Rest of the World. The analysis of links within the financial system is at the heart of the shadow banking statistics, whose implementation represents one of the goals of the second phase of the G20 DGI launched in September 2015. The DGI fosters the regular collection and dissemination of reliable statistics for policy use and addresses the need for more granular data to enhance the analysis of vulnerabilities and possible spill-over effects.

The dissemination and improved communication of statistical information is considered as a priority for closing the statistical data gaps and therefore improving the functioning of markets (Heath, 2013). This was supported, amongst others, by the IMF Special Data Dissemination Standard Plus. With respect to pre-existing categories of statistics, starting from 2012 the IMF Executive Board also approved a further enhancement of data that includes references to the measurement of government debt and financial balance sheets more generally.

The crisis fallout in Europe showed different degrees of resilience across countries, in particular within the Euro Area, due to differences in the level of internal macroeconomic imbalances. A thorough analysis of the origins of the imbalances (different trends in competitiveness, heterogeneity in fiscal positions, the flow of capital from northern to southern countries, and so on) pointed to weaknesses in economic governance. As discussed previously, the EU Macroeconomic Imbalances Procedure provides a surveillance programme to detect and correct macroeconomic imbalances by relying on a scoreboard of indicators that monitor country risks in a systematic way, which are based on information in national accounts. The use of financial accounts and balance sheets, and more generally indicators based on national accounts, thereby assures consistency across indicators along with comparability across countries, thanks to the common methodology applied.

3. Uses of financial accounts and balance sheets in economic research

Financial accounts were first modelled by Morris A. Copeland who published in 1952 “A Study of Moneyflows in the United States” (see De Bonis and Gigliobianco [2012] for a full narration). Copeland collaborated with economists and statisticians at the Federal Reserve and the National Bureau of Economic Research. In 1955 the Federal Reserve produced the first version of what they referred to as the annual “flow of funds”. Quarterly flow of funds were published for the first time in 1959 in the Federal Reserve Bulletin. With the regular publication by the Federal Reserve, financial accounts and balance sheets became an established tool of economic analysis. In the 1960s other countries started to set up the collection of financial accounts on a regular basis. As such financial accounts became part of a triad that also included (non-financial) national accounts and input-output tables (Klein [2003]).

Money demand, asset portfolios, and econometric models: Tobin’s contribution

In his Nobel Memorial Lecture held in 1981, James Tobin spoke on “Money and finance in the macroeconomic process”. Tobin’s goal was to summarise a system of simultaneous equations, or a model of general equilibrium interdependence, where the relationships between variables describe the national economy. In his lecture Tobin presented two tables. The first referred to the “flow of funds” matrix in the United States for eleven assets and nine sectors in 1979. In the second table the data were further aggregated into four sectors and four assets. Then Tobin presented a model of the determination of output and prices in the short-run. Among the main features of the model were typical characteristics of financial accounts and balance sheets, such as the presence of different assets, the consideration of both flows and stocks, the modelling of both monetary policy operations and other financial operations, the sources of new supplies of private wealth, and household demand for asset accumulation.

Of course, the interest of Tobin for flow of funds was not new. While Keynes had put emphasis on income and interest rates as the main determinants of money demand, Tobin progressed to explain the demand for financial assets, where the latter are chosen according to their risk-return profile, in the general framework of portfolio choice theory. As wealth does not only consist of money but also includes other financial assets and non-financial assets, Tobin looked at the way economic agents distribute wealth across financial and non-financial assets.

Brainard and Tobin (1968) proposed an econometric model based on interrelated financial markets for assets and liabilities. Prices, interest rates and quantities in the financial system both influence and are influenced by the real economy. A large amount of research followed, by, amongst others, scholars belonging to the so-called Yale School. Econometric models were also developed by national central banks. For instance, the 1986 version of the Bank of Italy Quarterly Econometric Model contained a complete description of the links between saving, non-financial investments and financial flows9.

The fall of financial accounts and balance sheets and the work of Godley

In the 1960s and the 1970s financial accounts were at the centre of economic analysis. From the mid-1980s until the 2007-09 economic and financial crisis, interest in financial accounts and balance sheets more or less vanished, for a number of reasons: a growing focus on the micro-economic foundations of macroeconomics; the increasing role of monetary and credit aggregates for the conduct of monetary policy that implied a lower focus on the entire financial system; trust in the self-correcting market mechanism through price adjustments, while considering quantities – both flows and stocks – less important; the rational expectation critique of Keynesian models; a growing inclination among economists to separate monetary and real phenomena; and the problems of achieving full international harmonisation of statistics until the introduction of the 1993 System of National Accounts (SNA93).

In contrast, Wynne Godley never abandoned the idea that economic models should be founded on flows and stocks, and developed consistent models of the US economy and other countries. In his approach, modern economies have an institutional structure comprising (non-financial) enterprises, banks, governments and households. The evolution of economies through time is dependent on the way these agents take decisions and interact with one another (Godley and Lavoie [2007]). At the beginning of each period stock variables in an economy – i.e. all physical stocks together with financial assets and liabilities – offer a summary of the past evolution. Transactions between the different institutional sectors then take place: final consumption, non-financial investments, government expenditures, the payment of taxes and the generation of profits, and the purchases and sales of financial assets and liabilities. These transactions move the stock variables from their state at the beginning of each period to their state at the end, to which holding gains and losses will have to be added. In their book Godley and Lavoie start from a simple model with one asset, money, and one country. They then make the model more complex by adding portfolio choices, bonds, holding gains, and the open economy.

Godley and Lavoie recognised that their model – sometimes labelled as the New Cambridge School – shared some features with the tradition of Tobin and the Yale School: the tracking of stocks; the existence of several assets and rates of return; the modelling of financial and monetary policy constraints; and the importance of agents’ budget constraints. The Yale school and the New Cambridge school are in agreement on the importance of consistent accounting, consistent stock-flow analysis and consistent constraints on behavioural relationships. Godley and Lavoie also emphasised how their models are distinct from those of Tobin. For example, they provide a clearer description of the dynamics of the economy, while Tobin put more emphasis on one-period models; market clearing through prices only occurs in some specific financial markets, and changes in quantities rather than in prices keep the economy in equilibrium; and institutions are not intermediaries acting on behalf of individuals.

Comparing financial systems and building balance sheets: Goldsmith’s contribution

Goldsmith dedicated his research programme to the building of national and sector balance sheets, following the scientific advice of Hicks (1935) – who suggested that “We shall have to draw up a sort of generalized balance sheet, suitable for all individuals and institutions” – and presenting in Goldsmith (1985) a reconstruction of the national balance sheets of twenty countries from 1688 to 1978. When Modigliani and Brumberg first “invented” the life-cycle model, they cross-checked their intuition with Goldsmith’s figures (see Modigliani [1999] and Fano [2011]).

Goldsmith’s work has been a precursor of comparative economics: countries differ because their financial systems differ. In his interest for the quantitative comparison of financial structures, Goldsmith introduced the financial interrelations ratio (FIR), the ratio of gross financial assets to non-financial (real) wealth. FIR measures the weight of the financial system with respect to the real economy. The ratio depends directly on the amount of liabilities issued in the period and the change in the value of the stock of outstanding liabilities. The FIR is also dependent on the inverse of the ratio of non-financial wealth to GDP (see Bartiloro et al. [2005] for a breakdown of FIR into its components).

FIR generally increases with time because the growth of financial assets tends to be faster than that of real wealth. According to Goldsmith, the process stops when FIR reaches the value of 1 or 1.5; thereafter the ratio stabilises. Goldsmith reached this conclusion looking at long time series, but did not provide a theoretical explanation of this tendency. When FIR increases, the financial structure becomes more complex. For instance the stock exchange becomes more important and non-bank intermediaries start to develop. In arriving at this conclusion, Goldsmith already intuited the importance of what we today call the shadow banking system and its role in increasing FIR. There is a positive correlation between per capita GDP and the size of financial systems but the causality nexus is difficult to ascertain.

Goldsmith also introduced the financial intermediation ratio (FIN), with the goal to analyse the degree of “institutionalisation” of a country’s financial structure and the role played by intermediaries. There are different definitions of FIN (see Goldsmith [1969], Chapter 6). One can look for instance at the ratio between the liabilities of financial corporations – the central bank, commercial banks, other financial intermediaries and insurance companies and pension funds – and the total financial liabilities in a country. FIN is high in countries like the United Kingdom, Canada, Japan, the United States and Germany; see Table 11.2. Countries like Italy and Spain are characterised by lower levels of FIN, where financial intermediation is less developed with respect to the assets of the other institutional sectors. The financial intermediation ratio can also be calculated for banks alone, so as to better understand the role they play in different economies.

The literature on finance and growth, still at the centre of the debate, often starts with Goldsmith’s research on the correlation between economic development and the size of the financial system. Many scholars supported the view that the causality nexus goes from developments in the financial markets to economic growth (see, for instance, Demirguc-Kunt and Levine [2001]). Other economists, however, were of the opinion that “finance follows”, or that the impact of financial developments on economic growth has been overemphasised. Following the 2007-09 economic and financial crisis, sceptical views became more common, arguing that finance has a non-linear effect on growth. Despite the differences in interpretations and results, all scholars paid tribute to Goldsmith’s measurement of financial system dimensions.

How Thomas Piketty studied the wealth/income ratios

Piketty underlined the importance of household wealth to income ratios in developed countries with his publicly acclaimed Capital in the Twenty-First Century (2014). Building time series exploiting the availability of financial accounts and balance sheets, including statistics on non-financial assets, he showed that the ratio of total household net wealth to GDP has risen from 2-3 times in 1950 to 4-6 times today. Piketty started his analysis with the dynamics of the wealth to income ratio in France and the United Kingdom, the two countries for which the longest time series are available. He shows that in both countries the ratio has followed a U-curve since 1700, and that it is nowadays at the same level as three centuries ago. Over the same period, wealth has also undergone a metamorphosis, with a sharp relative decline in wealth of land, replaced by the value of dwellings (even if the increase in the value of dwellings can often be associated with the value of the underlying land). Net foreign assets, i.e. the difference between assets and liabilities with non-residents, have always been minor, in spite of the two countries’ colonial empires. Since the 1980s, privatisations have reduced government owned assets and increased private wealth in both countries.

In Germany and the United States the dynamics of the wealth to income ratio were quite different. Since the late nineteenth century, the so-called Gilded Age, Germany has always had less private wealth than France and Britain, despite relatively high household savings rates since World War II, for two reasons. First, house prices in Germany are lower than in France and Britain, in part due to the relatively low demand for owner-occupied dwellings (as compared to other countries), and market flooding of low-value houses following the national reunification in 1989. Second, the value of corporate equity in Germany is relatively low, due to the impact of the so-called “Rhenish capitalism”, where the involvement of banks is crucial and the stock exchange is underdeveloped. Wealth has also been consistently lower in the United States as compared to France or the United Kingdom; in the United States, houses have historically been cheap by international standards due to abundant availability of land. The United States’ net foreign assets too have always been negligible, as the country was never a colonial power.

Since 1870 the wealth to income ratio in Europe has always been higher than in the United States, except between 1920 and 1980. Between 1915 and 1950, wealth in Germany, France and the United Kingdom was destroyed by war, by the reduction in net foreign assets, and by low saving. After 1950, private wealth did not expand significantly, reflecting the slow rise in asset prices until 1980, as a consequence of strong public intervention. Private wealth in these rich countries amounted to between 2 and 3.5 times GDP in 1970. On the contrary, since 1980, the ratio rose quickly in all countries. In 2013, it was higher in Spain, Italy, France and the United Kingdom than in the United States, Canada, and Germany; see Table 11.3. The rise in the ratios, disregarding short-term fluctuations, is also related to the jump in the prices of dwellings and shares, which had moved relatively slowly in the decades following 1945, because of rent control and financial regulation.

According to Piketty, the increase in the wealth to income ratios is not only explained by the increase of the numerator, but also by the low GDP growth rate, first and foremost due to low population growth in advanced countries. Piketty expects a further decrease in GDP growth, thus remaining rather pessimistic about the potential of population growth and technical progress to replicate the “golden age of growth” from 1950 to 1980. This forecast is akin to the secular stagnation hypothesis put forward by Summers (2014). A further finding, developed by Piketty and Zucman (2014), is that the increase in wealth to income ratios is more related to the accumulation of past saving than to increases in the prices of non-financial and financial assets owned by households. This finding is not that straightforward in view of the real estate and stock market bubbles in the 1980s/1990s as well as in the twenty-first century. Moreover capitalist economies differ from one another, because households choose to invest in different types of financial assets (De Bonis and Pozzolo, 2012). In some countries the composition of financial assets is tilted towards listed shares and insurance/pension instruments (such as in the United States and the United Kingdom), while in other countries bank deposits and debt securities are more popular (such as in Italy and Japan). Since the 1970s, households have generally increased the share of investments in the stock market, either directly or indirectly via investment funds, and – with the exception of Japan – decreased their investments in bank deposits (De Bonis, Fano and Sbano, 2013).

Piketty (2013) builds upon the work of Goldsmith (1985), by reconstructing balance sheets for a number of countries. As an annex to his successful book, Piketty also made available another 900 pages of statistical time series and methodological discussion on income, wealth and other macroeconomic variables for eight countries: the United States, Japan, Germany, the United Kingdom, France, Italy, Canada and Australia (see http://piketty.pse.ens.fr/files/PikettyZucman2013Appendix.pdf). Some scholars have argued that a good part of the increase in the wealth to income ratio depends on trends in real estate investments and house prices. The problem is the difficulty of establishing a common methodology that allows for the measurement and international comparison of countries’ shares of increases in wealth that are due to saving, to higher prices of financial assets, and to higher house prices. There is no doubt whatsoever that wealth has increased significantly, particularly in developed countries, but we still do not have a consensus on the determinants. Econometric analysis is often hampered by problems with clearly distinguishing the causal nexus of wealth and other macroeconomic and institutional variables, such as saving, unemployment, interest rates, social expenditures, taxation, and the age composition of population.

The reassessment of interactions between the real economy and the financial sector

More generally, the interactions between the financial sector and the real economy were already studied before the 2007-09 economic and financial crisis. There are different strands of literature, such as the study of the correlation between money, credit and nominal national income; the analysis of the non-monetary effects of the banking crises in the propagation of the Great Depression; the research into the bank lending channel and the subsequent declinations of the bank capital channel and the liquidity channel, which stress that capital and liquidity matter for credit supply; and the “financial accelerator” approach (Bernanke et al., 1996).

Most of the previous contributions told a partial story, and their results have not been well incorporated in macro-econometric models. These models sometimes emphasised only the demand for credit without taking into account the supply side of credit. The amount of IMF research on macro-financial linkages was quite limited; even by the end of 2008 the research efforts in this area were insufficient. However, after the 2007-09 economic and financial crisis, the importance of such interactions is now well-acknowledged and at the centre of economic research.