Chapter 3. Towards green growth1

Switzerland’s economy is performing well and recovered strongly from the 2007-09 financial crisis. The country has a Green Economy Action Plan and has made progress in greening the economy, as illustrated by its above-average performance on a number of green-growth-related indicators. There are, however, opportunities to do more. This chapter reviews Switzerland’s greening efforts and achievements in the areas of taxation and subsidies, public and private investment, innovation, international development and trade.

1. Introduction

Switzerland is a relatively small country in terms of population (around 100th in the world) and area (around 130th) but a top performer in terms of wealth measured as gross domestic product (GDP) per capita (Chapter 1). The economy is performing well and recovered strongly from the 2009 recession thanks to low interest rates, high immigration and strong exports. Recent developments, such as appreciation of the national currency, explain in part the more modest 1.5% average annual GDP growth over 2011-15, on a par with the OECD average (OECD, 2015a).

As with most advanced countries, the Swiss economy is characterised by a predominance of services, with a particularly prominent financial sector, which contributed an estimated 9.3% of GDP in 2015, compared with 7.2% in the United Kingdom and 4.1% in Germany (SIF, 2016). The industrial sector, however, remains strategic and highly competitive in certain key innovation-based sectors, particularly pharmaceuticals, chemicals and wristwatches. Though agriculture represents less than 1% of GDP, it is perceived as an important element in maintaining food security, rural development and landscape protection (Chapter 5). Switzerland has an open economy, with significant volumes of exports, imports and foreign direct investment (FDI) for its size. Trade openness (measured as exports plus imports as a share of GDP) is a noticeably high 120%, up from around 80% through the 1980s and 1990s, with a progressive increase since then.

Switzerland performs significantly better than the OECD and OECD Europe in terms of production-based resource productivity, whether in terms of energy, greenhouse gases (GHGs) or materials (OECD, 2017b). However, as the 2007 Environmental Performance Review (EPR) stressed (OECD, 2007), the country remains among OECD countries with relatively high per capita consumption-based environmental footprints. This is well illustrated by volumes of road transport and municipal solid waste (MSW), which have both risen steadily in line with GDP growth since 2000. Switzerland is the largest producer of MSW per capita in Europe and among the highest per capita consumption-based carbon dioxide (CO2) emitters in the OECD. Indeed, there is evidence that embodied CO2 emissions per capita are highly correlated with material living standards (OECD, 2017b).

As a result of the country’s relative trade openness, it is estimated that one-half to three-quarters of its environmental impact results from the import of goods and services, particularly in relation to food consumption, housing and household mobility (Frischknecht et al., 2014). Climate change, ocean acidification, nitrogen pollution and biodiversity loss have been identified as the footprint issues of main concern in relation to Swiss consumption patterns (Dao et al., 2015). While it is difficult to assess whether the impact would be any less if the same goods were produced domestically, this situation highlights the need for the green economy strategy to also address international aspects. Particular attention should be paid to addressing the increasing environmental impact of domestic consumption for developing countries. It is in this context that the indicator set identified by Switzerland to report progress against its Green Economy Action Plan (GEAP) (Section 2) includes absolute environmental footprints in addition to productivity-related metrics (FOEN, 2016a).

While Switzerland has made progress in greening its economy, as illustrated by its above-average performance on some green-growth-related indicators, it has opportunities to do more. It could, in particular, shift to a coherent green tax system (Section 3), including the removal of remaining environmentally harmful subsidies (Section 4); increase the greening of public procurement (Chapter 2) and investment practices in its prominent corporate and financial sector (Section 6); foster eco-innovation (Section 7); and align trade and environmental policies (Section 8).

2. Approach to greening the economy

Acknowledging the need for the economy to move to more sustainable resource consumption, the Federal Council in 2010 mandated the elaboration of a green economy strategy, with particular focus on clean technology innovation, resource efficiency, consumer information on products’ environmental impact and an environment-friendly tax system. In 2013, the council adopted the first GEAP; its 2016-19 version remains the centrepiece of the green economy strategy. The GEAP considers that existing policies (energy, climate, spatial planning) already help reduce the economy’s environmental impact but that resource efficiency must be improved, especially for raw materials and consumer products (FOEN, 2013; Swiss Confederation, 2016). Green jobs may result from this approach but, in a context of low unemployment, are not targeted per se (FOEN, 2013).

The 2016-19 GEAP confirms a focus on three priority areas: consumption and production, waste and raw materials, and cross-cutting instruments. It contains 27 measures aimed at conserving natural resources, reducing the environmental impact of consumption and moving to a more circular economy. It envisages a key role for voluntary initiatives from businesses, the scientific community and society, with the federal government prepared to correct market failures. This preference for voluntary initiatives and agreements in the context of greening the economy was confirmed by the rejection of more binding commitments by the parliament and the populace.

In December 2015, the Federal Assembly turned down a proposed amendment of the Environmental Protection Act that would have established a framework for promoting ecologically sound consumption patterns, strengthening the circular economy and providing information on resource efficiency. As a result, implementation of the GEAP in 2016-19 pursues the initial (2013) focus on resource efficiency and conservation through the voluntary commitment of actors concerned, e.g. the Green Economy Dialogue bringing together the private sector, non-government organisations (NGOs), science and academia.

In September 2016, the Swiss rejected a popular initiative, “For a sustainable and resource-efficient economy (Green Economy)”. It proposed amending the Constitution to include a provision requiring that, by 2050, Switzerland’s ecological footprint, when extrapolated to the world population, should not exceed one Earth. This radical initiative not only failed to achieve voter consent, but the Federal Council and parliament were also against it, arguing that the transition to a green economy was a long-term endeavour, which the economy needs time to adapt to gradually.

As a result of these votes, legislation containing extensive and binding green economy measures is very unlikely. The incremental, step-by-step approach currently favoured by the Swiss authorities, the business sector and the public alike can prevent more ambitious and transformational commitments. For instance, although the GEAP prioritises resource efficiency, Switzerland lacks a dedicated national resource efficiency strategy (EEA, 2016). Such a strategy could be integrated in the next GEAP and contribute to the design of more tangible targets, building on the Recommendation of the OECD Council on Resource Productivity.

The links between the GEAP and other strategic policy processes, such as Energy Strategy 2050 (initiated in 2013, approved in 2017) and four-year Agriculture Policy packages (Chapter 4), should be clarified, similar to the clear links identified with the Sustainable Development Strategy (SDS, launched in 2002, updated in 2016). Energy Strategy 2050 was triggered by the gradual nuclear phase-out proposed in the aftermath of the Fukushima accident and approved by referendum on 21 May 2017. It envisages reduced fossil fuel use, enhanced energy efficiency in buildings and improved fuel efficiency in the passenger car fleet. It included a plan to more closely align energy policy with climate policy by introducing a Climate and Energy Incentive System (known by the German acronym KELS), especially for transport and electricity (SFOE, 2016). Although KELS is unlikely to be pursued as initially expected, this should not prevent Switzerland from implementing green tax reform (Section 3). The SDS 2016-19 covers measures overlapping with the GEAP, Energy Strategy 2050 and the Agriculture Policy packages, including on consumption and production, energy and climate, and natural resources (Federal Council, 2016a). To address these overlaps and clarify responsibilities, it will be crucial to improve co-ordination both within the Department of the Environment, Transport, Energy and Communications (DETEC) and between it and other departments, beyond the standard consultation for proposed new legislation (Chapter 2).

As Switzerland is located in the heart of the European Union (EU), close co-operation with the EU is particularly important for the Swiss economy-environment interface. In 2016, trade with the EU accounted for 54% of exports and 72% of imports. Economic and trade relations with the EU are governed by bilateral agreements. Some have clear environmental policy implications, for instance regarding transport and carbon pricing.

3. Greening the system of taxes and charges

3.1. Overview of environmentally related taxes

Switzerland is characterised by a strong fiscal position (Chapter 1). However, social and infrastructure-related spending needs are expected to rise, placing a significant focus on spending efficiency (OECD, 2015a). The ratio of accrued total tax revenue to GDP has been stable: it was about 27% in 2014, significantly lower than in neighbouring France (45%), Italy (44%), Austria (43%) and Germany (36%), but similar to the ratios of, for example, Australia and Ireland. The difference is related in particular to below-average rates for value-added tax (VAT, 8%) and corporate tax (21%).

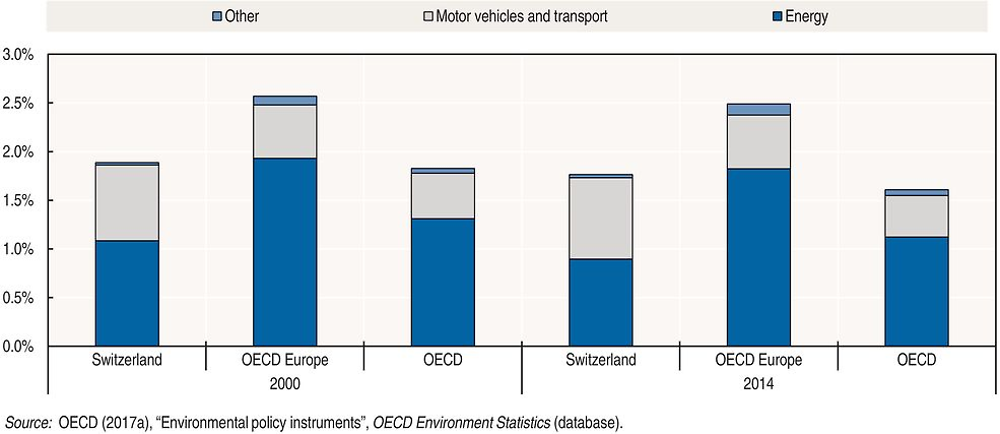

Internationally comparable environmentally related taxes (ERT) in 2014 were equivalent to 1.8% of GDP. This percentage, which was stable over the review period, is below the 2.5% OECD Europe average (Figure 3.1). ERT represented 6.8% of total tax revenue in 2014, on a par with the OECD Europe average and above the OECD average. Unlike in most OECD countries, where energy typically dominates ERT revenue, the share related to road transport has risen steadily over the past 20 years to over 45%. Two trends help explain this: since 2000 the road vehicle fleet has increased by 21% while total final energy consumption has decreased by almost 4% (Chapter 1).

The oil tax, however, still represents close to half of ERT revenue, followed by the cantonal motor vehicle tax (20%), the distance- and weight-based tax on heavy vehicles (15%) and the CO2 tax on heating and process fuels (5%) (Federal Council, 2013). The incentive tax on volatile organic compounds (VOCs) represents a negligible share. In addition to ERT revenue, Switzerland has environment-related fees, including on aircraft landing and a range of waste streams.

Switzerland could boost ERT by expanding the coverage of the distance-based transport tax and introducing new instruments, such as congestion charges. This would help the government face expected fiscal challenges. Although the budget is nearly balanced and the government debt/GDP ratio of 46% is low for the OECD, the government expects a rise in infrastructure and social expenditure in the medium to long term. Switzerland needs to ensure there are no delays in infrastructure investment (Section 5) and in efforts to improve the well-being of the most vulnerable groups.

3.2. Advancing green tax reform

After the 2007 EPR recommended implementing the green tax reform envisioned by the first SDS in 2002, some steps were taken but full implementation appears to face political difficulties despite the country’s GDP per capita being significantly above average.

Initial steps included the parliament’s 2010 adoption of Motion 06.3190 (known as the Studer Heiner motion after the deputy who introduced it). It called for the greening of the tax system, the inclusion of an environment-friendly tax system as one of six focus areas for a green economy identified in the 2010 strategy proposal that informed the GEAP, and the commissioning of a study providing an overview of the issues at stake (Baur, 2012). In 2013, however, an in-depth assessment by the Federal Council resulted in dismissal of the initial Studer Heiner motion on the grounds that it duplicated existing or planned measures and that the potential for further optimisation was modest and better addressed via individual laws and regulations (Federal Council, 2013). In March 2015, Swiss voters rejected (by 92%, with a 42% turnout rate) a popular initiative by the centrist Green Liberal Party to replace VAT with a tax on non-renewable energy sources (oil, natural gas, coal, uranium). The aim was to support the GHG reduction target and nuclear energy phase-out by promoting renewables and energy efficiency while preserving revenue and economic competitiveness. This initiative, like the Green Economy initiative rejected in September 2016, was likely perceived as too ambitious in the short term.

In 2011, after the Fukushima accident, the parliament undertook to reform Swiss energy policy and asked the Federal Council to prepare an energy strategy to foster a shift from nuclear power to renewables by 2050. In 2013 the government submitted a first package of Energy Strategy 2050 measures. On 30 September 2016, the parliament prepared the necessary amendments to the Energy Act, which were approved by referendum on 21 May 2017. The first package, covering 2018-20, provides financial support, via levies on electricity bills, to cover part of the cost of investment in renewables. Electricity consumers also subsidise renewables development via market premium and market price support (feed-in tariffs). This means electricity consumers will assume the cost of the energy transition. The act underwent a referendum because the policy involves a differentiated financial effort between households, small and medium-sized enterprises (SMEs) and large firms to support the energy transition. The case of a CHF 00.023/kWh supplement on electricity bills paid exclusively by households and SMEs (and reimbursed to large firms) illustrates this. Looking ahead to 2021 and the second stage of Energy Strategy 2050, the government has begun to explore options for shifting the basis of the energy transition policy from support by electricity consumers to tax incentives related to energy and climate. On 28 October 2015, the Federal Council sent the parliament a draft of the required constitutional amendment for consideration. However, the National Council (lower house) decided on 8 March 2017 not to examine the proposal, and the Council of States (upper house) rejected it in June 2017.

Nevertheless, there are further avenues towards a more coherent pricing and incentive system across climate-, energy- and transport-related activities. Modelling-based analysis indicates that, compared to the status quo, such a system would achieve significant additional CO2 emission reduction by 2030 with limited negative impact on GDP growth (Ecoplan, 2015). Here, Switzerland could benefit from the experience of countries that have recently implemented fiscally neutral green tax reforms, such as Portugal.

In the process, to avoid a repeat of rejection by the Federal Council and voters, particular attention should be paid to political economy issues. The distributional impact of such measures is, on average, less of an issue in Switzerland than in other countries. Thanks to its relatively high GDP per capita, the country currently has the lowest energy affordability risk in the OECD, as less than 3% of households spend more than 10% of disposable income on domestic energy (Flues and van Dender, 2017).

Switzerland should also consider reducing the frequency and duration of tax revenue earmarking, limiting it to defined objectives and periods. Earmarking enhances transparency of tax revenue use, thereby increasing public support for new or higher taxes. However, in the long run, earmarking reduces flexibility in allocating revenue and thus can lead to resource misallocation, with too much for earmarked activities and too little for other priorities. Once in place, earmarking may also make reform more difficult, as changes need to be agreed on both the tax and expenditure sides. The planned end of public financial support for energy efficiency in buildings in 2019 will eliminate part of the earmarking of the CO2 tax. The first Energy Strategy 2050 package does the same for renewables by introducing a sunset clause for new feed-in tariff commitments, six years after the package enters into force (Section 5). But other cases will continue, e.g. earmarking of the oil tax and of aircraft landing charges (Section 3.4).

3.3. Energy-related taxes

The most noticeable energy taxes are those on oil sales (close to 50% of ERT revenue in 2010) (Federal Council, 2013) and on heating and process fuel use (CO2 tax). The oil tax, in its current form, dates back nearly two decades. A generic revenue-generating tax, it mostly applies to road fuels and thus is further discussed in the transport subsection below. All energy sales are subject to VAT at the regular rate of 8%. Final electricity consumption is subject to a further tax to finance grid development (Section 5).

The CO2 tax is levied on fossil fuels (heating oil, natural gas, coal, petroleum coke, etc.) used to obtain heat or light, to produce electricity in thermal installations or to operate heat‐force coupling installations. It was introduced in 2008 as an incentive tax to internalise the external costs associated with CO2 emissions and encourage both more efficient fossil fuel use and a shift to low-carbon energy sources. Wood and biomass are exempt because they are considered CO2 neutral. The tax rate is defined per tonne-equivalent and hence depends on the carbon content of each energy source. It has been increased twice since its introduction: from CHF 36/tonne in 2008 to CHF 60/tonne in 2014 and CHF 84/tonne (about EUR 77) as of January 2016. The second increase was deemed necessary because CO2 emissions from thermal power plants in 2014 did not meet the target of a 22% reduction from the 1990 level.

The tax is collected by the Federal Customs Administration at import or wholesale (for fuels stored in registered tax-exempt warehouses). It is based on the CO2 emissions produced by combustion at standard temperature and pressure (e.g. for large combustion plants) rather than actual emissions, which would provide better emission reduction incentives. In 2016 it brought in about CHF 1 billion. Two-thirds of the revenue is redistributed uniformly to households, regardless of fossil fuel consumption, through a rebate on health insurance premiums, and to businesses in proportion to the number of employees. Most of the remainder (up to CHF 300 million) goes to a programme by which the Confederation and cantons support energy-efficient building renovations (Section 5). A further CHF 25 million is transferred to the technology fund (Section 6).

While the CO2 tax rate positions Switzerland among leaders in terms of carbon pricing for emissions covered, the tax does not apply to transport fuels (see below) or to CO2 emissions covered by the Swiss emission trading system (ETS) (see the “Carbon trading and pricing” subsection). Further, GHG-intensive companies may be exempted from the CO2 tax upon request if they commit to reducing their GHG emissions continuously to 2020. Eligibility criteria are lax, however: the applicant firm proposes its own reduction target based on an “economically viable reduction potential”.

While the Swiss combination of policy instruments may be suitable for targeting various emitter categories, it complicates assessment of the CO2 tax’s effectiveness. For 2008-13, the estimated total reduction was 2.5 million to 5.4 million tonnes of CO2, which represents only 1% to 2% of reported Swiss GHG emissions for the period (FOEN, 2016b). Households achieved up to three-quarters of the reduction, which may imply that industry did not do its share. The primary driver was the replacement of heating oil with less CO2-intensive energy sources, a shift that tends to be more rapid for households than companies.

A preliminary survey indicates companies that committed to reducing their emissions in exchange for tax exemption implemented more effective emission reduction measures than companies subject to the tax (FOEN, 2016c). This may partly be explained by the limited incentive provided by the tax’s lower rates in its early years, and partly by a tendency for larger companies to seek the exemption and smaller ones to remain subject to the tax. Companies in the voluntary reduction programme may also have lower GHG abatement costs. Thus it will be difficult to assess the additional reduction effort by companies exempted from the tax until compliance with targets is fully monitored in 2021, after the commitment period ends.

3.4. Transport-related taxes

Transport of persons and goods has been increasing faster than population and GDP growth (Chapter 1). Transport remains the primary source of local air pollution by nitrogen oxide (NOX) emissions, which are growing, as well as of noise pollution. The impact of transit through the Alps has been an area of particular concern, where Switzerland continues to aim for a modal shift from road to rail. Over time the country has introduced a range of transport-related taxes, as illustrated by the high and increasing share of transport in ERT relative to other OECD countries (Figure 3.1).

Motor vehicles

Vehicle owners pay an annual tax to their canton of residence for every registered vehicle: the cantonal motor vehicle tax, which is the country’s oldest existing tax and accounts for 20% of ERT revenue (Federal Council, 2013). The rate depends on the car’s weight, power, or both. The rate disparity among cantons can be significant, partly due to variation in cantonal tax burdens and in how cantons finance road construction and maintenance. For example, Bern canton calculates the tax based on vehicle weight: CHF 240 for the first 1 000 kg, with every additional tonne taxed 14% less than the previous one. In other cantons, such as Zurich and Aargau, vehicle type and cubic capacity determine the rate.

Energy-efficient and electric vehicles benefit from exemptions or reductions in some cantons. Hybrid cars are exempt in Basel-Landschaft canton and, for the first three years, in Geneva canton (CEPE, 2015). Basing the motor vehicle tax rate on weight or power, however, continues to create perverse incentives. In particular, for the country as a whole the tax on electric vehicles remains relatively high despite the environmental criterion being taken into account. Overall, although some reductions are driven by green criteria, the motor vehicle tax remains a standard revenue-generating tax for the cantons.

A separate tax is paid at the time a vehicle is registered. Some cantons (e.g. Geneva, Obwalden) reward buyers of less polluting cars via a bonus-malus programme; there is no national standard yet. Bonus-malus systems can be effective. Results from one study (Alberini et al., 2016) point out that the retroactive nature of the malus in Obwalden led to inefficient vehicles being taken off the road faster, which did not happen in Geneva where there was no retroactivity. If not offset by revenue from the malus, the bonus generates a net deficit for cantonal budgets. Overall, registration taxation can help change fleet composition, as for example in Israel (OECD, 2016a), but it is less environmentally effective than taxing fuel or emissions because it is not linked to vehicle use.

The Constitution (Article 82) does not authorise tolls for the use of public roads, saying they must be free of charge (exempt from tax), though the Federal Assembly may authorise exceptions. Highways and freeways are subject to a low annual motorway toll: CHF 40 for unlimited use. As in many OECD countries, the revenue is earmarked for motorway construction and maintenance. Cantons may also charge road tolls under certain conditions, such as for infrastructure developed as part of a public-private partnership. Road tolls can be a very cost-effective way to tackle urban air pollution from traffic congestion. Switzerland should consider expanding the scope of exceptions to Article 82 and authorise tolls for urban road use. This would allow for congestion pricing, similarly to that in London, Milan and Stockholm. It would also make it possible to consider expanding the scope of distance-based incentives for freight vehicles of less than 3.5 tonnes and for passenger vehicles, which could be critical in limiting road transport overall (Chapter 1).

DETEC has been pilot testing a mobility pricing initiative mandated by the Federal Council in its 2011-15 term. The initiative is exploring the possibility of pricing mobility towards more effective demand-side management across transport modes and services. It could include incentives for off-peak travel load spreading, as well as differentiating charge rates based on vehicles’ pollution emissions. This instrument (which would be new in Switzerland) would not come on top of existing transport-related taxes and fees but rather progressively replace them. Consultations conducted in 2015 revealed that the majority of cantons and civil society are favourable to the principle of mobility pricing.

Switzerland is an essential link in freight transit between northern (e.g. port of Rotterdam) and southern Europe. In this context, a Swiss tax on heavy goods vehicles was introduced in 2001 to replace the so-called royalty fee on heavy vehicle traffic. Switzerland thus became one of four OECD countries (with Austria, the Czech Republic and Germany) to have a nationwide road pricing system for heavy goods vehicles. The Swiss system is the only one covering all roads rather than being limited to highways as in the other three countries. The tax is based on distance covered and vehicle weight. It is further differentiated on the basis of pollutants emitted (using the EURO standards) to encourage fleet renewal with less polluting vehicles. Thanks to this and the distance element, the tax partly complies with the polluter-pays principle.2 It is levied on all freight vehicles and trailers above 3.5 tonnes, whether licensed in Switzerland or abroad. Revenue is earmarked for construction of transalpine rail tunnels (Section 5) and coverage of road-related noise externalities.

The heavy goods vehicle tax appears to have helped encourage modal shifting of freight from road to rail, as the Alpine Initiative requires.3 By end 2014, more than two-thirds of freight travelled by train in Switzerland (FOT, 2016). With the December 2016 opening of the Gotthard Base Tunnel, at 57 km the world’s longest rail tunnel, the share is expected to rise further, as the tunnel aims to increase rail traffic between northern and southern Europe. For now, however, Switzerland is far from reaching its 2018 goal of no more than 650 000 trucks crossing the Swiss Alps per year. Despite a 30% reduction between 2000 and 2014, 1 million heavy goods vehicles travelled through the Alpine region in 2015 (FOT, 2016).

In terms of renewal or upgrade of the heavy goods vehicle fleet, the differentiation of the heavy goods vehicle tax appears to have had considerable impact (OECD, 2005). The 2007 EPR recommended continuing to price transport-related environmental externalities by strengthening and expanding the scope of distance-based incentives. Updated differentiated fees were introduced in 2012 to promote the more stringent EURO VI standards as well as diesel particle filter retrofits for EURO II and III. They continue to be an effective driver for fleet upgrades towards less polluting vehicles. Further updated classifications entered into force on 1 January 2017: low-emission vehicles in the EURO VI category no longer benefit from the 10% rebate introduced in 2012 and are subject to a tax rate of CHF 0.028 per tonne‐kilometre.

The heavy goods vehicle tax provides better incentives to reduce air pollutant emissions than the Eurovignette, its counterpart in Denmark, Luxemburg, the Netherlands and Sweden. Introduced in 1995, the Eurovignette is not distance based (it is calculated on weight and the EURO standards) and applies only to vehicles above 12 tonnes using motorways and toll highways. To speed reduction of heavy goods vehicle journeys, the heavy goods vehicle tax rates should be gradually increased, taking into account road toll developments in neighbouring countries to avoid traffic leakage. Beyond national policy in this area, further reductions relating to long-distance journeys greatly depend on efforts in other countries. For instance, France and Austria have a much lower share of rail in transalpine freight transport.

As regards road fuel taxation, Switzerland is one of only three OECD countries (with Mexico and the United States) that tax diesel at a higher rate than petrol, which makes environmental sense given the higher carbon and air pollutant emissions of diesel fuel. The current rates are CHF 0.73/litre for unleaded petrol and CHF 0.76/litre for diesel, including the oil tax (FCA, 2017). In terms of EUR per GJ, however, the Swiss tax rate for petrol is higher than that for diesel, although the gap between the two is much smaller than in most other countries (Figure 3.2).

The 2007 EPR recommended increasing the tax levels for both fuels to further improve the pricing of environmental externalities. This was not done; in fact, inflation eroded the tax rates in real terms. Furthermore, depending on the exchange rate between the euro and the Swiss franc, fuel prices in Switzerland have sometimes led to sales of significant volumes to drivers from neighbouring countries (OECD, 2013a). After the appreciation of the Swiss franc against the Euro in early 2015, however, fuel tourism to Switzerland decreased significantly, causing a significant dip in road fuel tax revenue (-5.1% in 2015). Increasing the tax levels for diesel and petrol can help compensate for this in the short term and encourage reduced domestic fuel consumption.

The possibility of expanding the CO2 tax base to road fuels was considered, but a parliamentary consultation led to abandoning the idea due to the unlikelihood of public support. Hence, while motor fuels are within the scope of the CO2 Act, they are exempt from the CO2 tax, as are road fuel imports4 (unlike fuel imports for processes and heating). However, over 2006-12, a separate tax of CHF 0.015/litre on petrol and diesel imports was used to finance the Climate Cent Foundation, a voluntary programme set up by the Swiss business sector to undertake GHG reduction projects in Switzerland and abroad.5 Since 2012, Switzerland has imposed penalties on car imports so as to green its fleet. Like the EU, it has introduced CO2 emission regulations for new cars, which took effect on 1 July 2012. Swiss importers had to reduce the level of CO2 emissions from cars registered for the first time in Switzerland to an average of 130 grams/km by 2015. If the CO2 emissions per kilometre exceeded the target level, a penalty applied as of the above date. The CO2 standard for passenger cars will be lowered to 95 grams/km as of 2020, and extended to light duty vehicles.

Tax treatment of company cars and commuting expenses

As in many other OECD countries, a special tax regime applies to personal use of company cars and to commuting expenses. A recent OECD study (Harding, 2014) estimated that the Swiss tax system captured barely 20% of a benchmark for neutral tax treatment of company car benefits relative to cash wage income; the country ranked 22nd out of the 26 countries examined. Only 10% of a company car’s acquisition value is added to the employee’s annual taxable income, and fuel costs paid by the employer do not count as taxable income. Employees have a perverse incentive to be paid part of their salary in the form of company cars, and no incentive to limit their use or to choose efficient vehicles.

Deductions related to commuting expenses are available. As an incentive to favour public transport over personal cars, the full cost of an annual subscription is deductible. Switzerland is the only country besides Germany to provide an annual fixed sum deduction for employees cycling to work. Expenses related to commuting by car are deductible only if deemed necessary due to distance or unavailability of public transport; such deductions are calculated at a rate of about EUR 0.7/km, significantly higher than in other countries with similar deductions: Germany comes second at EUR 0.3/km (Harding, 2014).

As Chapter 1 noted, volumes of personal transport (train and road) have been increasing in Switzerland faster than population and GDP. The tax treatment of company cars and commuting expenses has likely contributed to this trend. The mobility pricing project provides opportunities to make environmentally beneficial adjustments, such as increasing the taxable share of a company car acquisition value and creating explicit incentives to buy more efficient vehicles.

Aviation

Switzerland has had landing charges since 1981 at its major airports in relation to noise caused by aircraft. The revenue is earmarked for noise remediation measures and compensation payments to residents. An additional landing charge related to aircraft NOX emissions was introduced in Zurich (1997), Geneva (1998), Bern (2000) and Basel (2003). Upon introduction of the NOX emission charge, the noise-related charge was lowered on a similar order of magnitude to ensure revenue neutrality for airports.

Together with Sweden, Switzerland was the first country to introduce an emission-based landing charge. The Swiss instrument was aligned in 2010 with a tax model now harmonised throughout Europe. Until then, the level of the NOX charge was differentiated by engine classification in order to favour aircraft using the best available low-emission engine technology. Since 2010, the differentiation has been refined to bring the rate closer to actual NOX emissions, thus reinforcing application of the polluter-pays principle.

Since 2009, the revenue from landing charges has been earmarked for security and anti-pollution measures at airports. In 2014, CHF 35 million was allocated to projects spanning 2014-21. So far, available funds have exceeded the demand for anti-pollution projects, despite an increasing number of applications. Examples of such projects involve installation of solar photovoltaic panels and heat pumps, replacement of diesel-fuelled vehicles with electric ones, studies to evaluate the impact of aircraft emissions and ecological compensation measures at airports pursuant to the Act on the Protection of Nature and Cultural Heritage (Article 18b).

Kerosene and aviation gasoline for domestic flights are subject to the oil tax and VAT but not to the CO2 tax. Two-thirds of the revenue from taxes on kerosene is earmarked for a special air transport fund to finance security, safety and (since 2014) environmental measures. Kerosene used in international flights is not subject to any taxation, pursuant to the 1944 Chicago Convention on International Civil Aviation.

3.5. Carbon trading and pricing

Switzerland fulfilled its international GHG reduction commitment under the Kyoto Protocol through a combination of domestic measures, purchase of emission reduction certificates abroad and the effect of Swiss forests as sinks. Emissions, however, have remained almost constant since 1990 (FOEN, 2016b; OECD, 2015c) (Chapter 1). In light of this trend, the 20% reduction domestic target for 2020 stipulated in the CO2 Act (30% conditional) and the 50% reduction target for 2030 of Switzerland’s Intended Nationally Determined Contribution require increased effectiveness of the combination of carbon pricing instruments currently in use.

In parallel to the introduction of the CO2 tax, Switzerland introduced an ETS for GHGs in 2008, three years after the EU and before any country of North America or Asia (OECD, 2016b). Under the CO2 ordinance, the ETS covers CO2, NO2, CH4, HFCs, NF3, SF6 and PFCs, though in practice monitoring and reporting are compulsory and effective only for CO2, NO2 and PFCs. Over 2008-12 the system was voluntary, as an alternative to paying the CO2 tax. Since 2013 it has been mandatory for large, energy-intensive installations and companies, chiefly in cement, chemicals, pharmaceuticals, refining, steel, paper and district heating. Medium-sized companies may join voluntarily. In all, 55 companies were included as of 2016. The ETS accounts for 11% of national emissions, compared with 45% for the EU ETS, 66% for the Korean ETS and 85% for the Californian and Quebecois cap-and-trade systems (ICAP, 2016).

For 2008-12, emission allowances were allocated for free according to targets taking into account the expected activity level of each company. For 2013-20, further free allowances have been allocated to energy- and trade-intensive sectors at risk of relocating abroad and are based on benchmarked emission factors. Other emitters’ share of free allowances decrease over time (80% in 2013, declining to 30% in 2020), except fossil fuel thermal power plants. Allowances not allocated for free are auctioned by the Emissions Trading Registry. In 2015, the ETS cap was 5.44 million tonnes of CO2 equivalent (Mt CO2 eq). It will decrease by 1.74% a year to 4.9 Mt CO2 eq by 2020.6

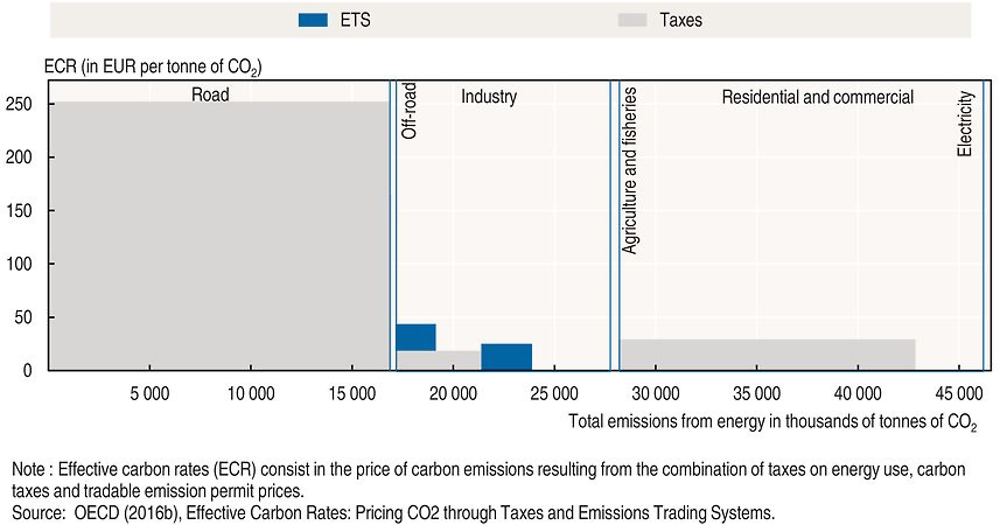

The price signal the ETS provides fell from CHF 40.25 in May 2014 to CHF 6.50 in March 2016. This reflects generous initial allowances and limited trading opportunities given the low number of actors covered, but more fundamentally is a result of a hardship regulation to avoid an unreasonable burden for companies covered. In 2012 in the industrial sector, an estimated 24% of emissions were covered by the ETS only, 21% by taxes only (on oil and/or CO2) and 19% by both a tax (on oil) and the ETS (OECD, 2016b). Smaller GHG-intensive companies not participating in the ETS are exempt from the CO2 tax if they commit to reducing their emissions through binding agreements. As a result of the limited coverage and modest trading price of the ETS, most non-road Swiss GHG emissions remain unpriced or low priced on an effective carbon rate basis (Figure 3.3). Higher pricing on emissions outside transport is, therefore, needed.

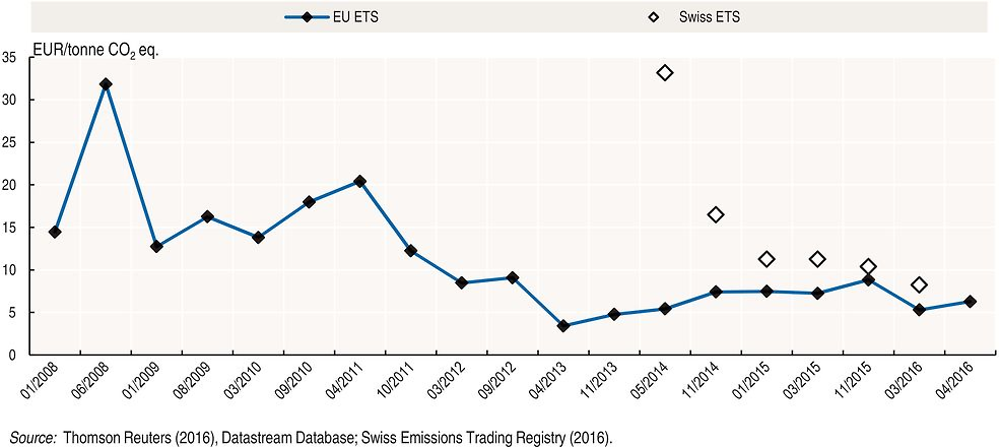

Negotiations to link the Swiss and EU ETS via mutual recognition of emission allowances were initiated in 2008 and concluded in 2016. Ratification of the link is a core element of consultation on future Swiss climate policy, which ended in November 2016. Many elements of the Swiss ETS already match EU ETS provisions (e.g. benchmarks for attributing emission allowances). Further adjustments will be needed, however, particularly to define terms for inclusion of aviation emissions, which are covered by the EU but not the Swiss ETS. As long as the systems are not linked, conditions for participating companies remain different. The significantly higher Swiss price in the first rounds of auctions in 2014 led the Federal Council to adopt the hardship regulation to avoid potential competitive disadvantages for Swiss companies. As a direct consequence, prices then drew closer to the EU ETS level (Figure 3.4).

From the Swiss side, potential benefits mainly lie in addressing issues related to the small size of the Swiss ETS. The link is expected to enable more cost-effective emission reductions, enhanced liquidity, clearer price formation and price stability (ICAP, 2016; IETA, 2015; OECD 2015c). From the other side there are potential areas of concern. One relates to the limited impact of the EU ETS on investment behaviour to date due to the availability of too many emission allowances and resulting low allowance prices. This will lead to decreased incentives for Swiss companies unless the EU ETS is reformed by reducing emission caps and introducing allowance reserves (OECD, 2016c). Furthermore, future interaction between the coverage of the linked systems, on the one hand, and the Swiss domestic CO2 tax and voluntary emission reduction programme, on the other, will need to be rationalised. A deep decarbonisation pathway simulation indicates that a long-term target of 1 tonne of CO2 per capita in the energy sector can be achieved in Switzerland if a uniform CO2 price of about CHF 500 per tonne of CO2 is in effect by 2025 (Ecole Polytechnique Fédérale de Lausanne, 2017).

Finally, Switzerland’s 2030 climate mitigation target relies heavily on international offsets (Section 1), but it is unclear how that would be compatible with the EU’s intention to focus solely on domestic emission reduction targets from 2020 onwards. The impact in this context would be minor given the low level of Swiss ETS emissions (the 55 companies account for less than 6 million tonnes) relative to the EU ETS (with 12 000 installations representing 2 billion tonnes). However, this again underlines the dilemma faced by Switzerland in terms of addressing the international impact of its national environmental footprint (production and consumption) without neglecting further domestic actions.

3.6. Tax on volatile organic compounds

VOCs are used as solvents in many industries and are contained in products such as paints, varnishes and certain detergents. Released to the atmosphere, they may interact with NOX to form ground-level ozone. An ordinance introduced a VOC incentive tax in 2000. The tax applies to VOCs of environmental relevance in terms of emission volumes. The ordinance specifies the taxed VOCs in two lists: one of affected organic substances, the other of products containing VOCs. The tax is levied either at point of import or on entry into production. The rate was initially set at CHF 2/kg of VOCs produced or imported. It was raised to CHF 3 in 2003 and has remained at that level. The revenue (CHF 125 million in 2015) is redistributed in full to households through a rebate on health insurance premiums.

Tax exemption is granted where a stationary installation’s VOC emissions are consistently below 50% of the limit value prescribed in the Air Pollution Control Ordinance (further technical and operational eligibility criteria also apply). The tax is refunded if VOCs embedded in industrial use are not released into the environment, or if products containing VOCs are exported. The latter does not help reduce Switzerland’s overall ecological footprint.

A 2009 assessment concluded that the incentive tax has had a positive effect on cutting VOC emissions, although expectation of the tax ahead of its introduction appeared more effective than the tax itself. Further, the tax appears less effective than direct regulations applying to substances and products not subject to the tax, under the 1985 Air Pollution Control Ordinance and EU legislation (VOC Solvents Emissions Directive, 1999/13/EC) for imports. However, the tax has raised awareness of the environmental and health problems linked to VOCs and encouraged innovation in three key industries: printing, paint making and metal cutting (OECD, 2010).

Switzerland has set a 30% VOC emission reduction target by 2020 from 2005 levels. In recent years, however, emissions have been more or less unvaried in all activities, whether or not subject to the VOC tax. Meeting the target under a business as usual scenario will be challenging given the increasing marginal costs for industry to find substitutes for VOCs and VOC-containing products and the difficulty of assessing consumption patterns. Combining the tax with direct regulations (i.e. taxing VOCs and VOC-containing products that do not meet the requirements of the Air Pollution Control Ordinance) can enhance effectiveness, particularly with higher tax rates and/or more stringent legal requirements.

3.7. Waste-related fees

The Environmental Protection Act stipulates that MSW management must be financed according to the polluter-pays principle. A bin-liner fee was introduced as early as 1975 and is now in place in 90% of municipalities. But MSW is an area that illustrates Switzerland’s difficulty in reducing its consumption-related environmental impact. As Chapter 1 noted, landfilling has been eliminated (following a prohibition on disposing of combustible waste in landfills) and recycling rates have increased with the introduction of fees. However, the combined fee system has not proved effective in reducing MSW generation per capita, which has continued to rise since 1975 and remains significantly above the OECD average. There is a need to increase waste minimisation incentives (e.g. by raising the bin-liner fee) while managing the risk of illegal dumping.

Difficulties in reducing MSW generation may be due in part to the large and stable share of incineration, a disposal technology that not only is less environmentally desirable than reuse and (in most instances) recycling, but also requires constant incoming volumes to avoid underutilisation and remain profitable. Incineration has been at the heart of Switzerland’s waste disposal strategy since landfilling of combustible waste was prohibited in 2000. The construction of 30 MSW incinerators benefited from public financial support. However, these facilities’ operation and maintenance costs have to be self-financed from i) municipal bin liner fees; ii) gate fees on industrial and commercial waste, where incinerators compete with each other; or iii) sales of district heat or electricity from waste‐to-energy facilities.

In 2014, incinerator operators signed a voluntary agreement with the federal government to reduce CO2 emissions by 18% by 2020. In return, however, the waste sector was entirely exempted from the ETS (OECD, 2015c), so the relative effectiveness of the voluntary agreement needs to be assessed. Switzerland should also tackle NOX emissions from incineration and consider taxation, e.g. as in Sweden.

To encourage recycling, fees are in place for specific waste streams. Prepaid disposal fees are charged on glass beverage containers and batteries. The fee for glass is collected directly from domestic manufacturers and importers. When it took effect in 2002, about 90% of glass was already being recycled, based on a separate collection stream since the 1970s. The focus, therefore, is on promoting the best possible ecological reuse of waste glass. For batteries, the fee is included in the sale price of each battery and accumulator. FOEN’s current target is to raise the collection rate from around 72% of used batteries to 80%, but the target does not consider options for reducing demand for batteries. Other prepaid recycling fees exist for PET beverage containers, aluminium and food cans. Over the past 25 years, recycling rates have risen (e.g. to over 80% for PET), but in a context of increasing volumes of MSW generated. Switzerland should set waste management priorities according to the waste hierarchy, favouring reduction over reuse and recycling.

For electrical and electronic equipment there is an extended producer responsibility programme in which producers and importers are required to pay an advance recycling fee for equipment they place in circulation. The funds are used to finance the collection and recycling of equipment by three private sector systems. Here again, the fees have had a positive effect in that Switzerland has one of the world’s best collection and recycling results, but they appear not to have reduced waste volumes generated. Furthermore, although Switzerland pays special attention to recovery of imported rare metals with a view to more economical resource management, current fees and policy instruments do not address the broader issue of the global impact of electronic waste, significant volumes of which are exported and treated abroad, particularly in non-OECD countries.

4. Removing environmentally harmful subsidies and tax exemptions

A 2013 report by the Federal Council provides an overview of environmentally harmful subsidies and tax exemptions. The report was prepared in response to, and as a means of dismissing, the Studer Heiner motion calling for green tax reform. It found that tax exemptions accounted for the majority of the value concerned, particularly in agriculture (VAT exemption) and aviation (absence of excise tax on kerosene, in line with the Chicago Convention). The assessment indicated such measures cost the government over CHF 5 billion a year (Table 3.1). This sum is equivalent to almost 40% of the 2010 revenue of Swiss environmentally related taxes, which totalled CHF 11 billion for internationally comparable ERT plus CHF 2.7 billion for other ERT (Federal Council, 2013). The design of a more coherent pricing and incentive system across climate-, energy- and transport-related activities would provide a good opportunity to reassess such subsidies and exemptions.

4.1. Transport- and energy-related support to fossil fuel consumption

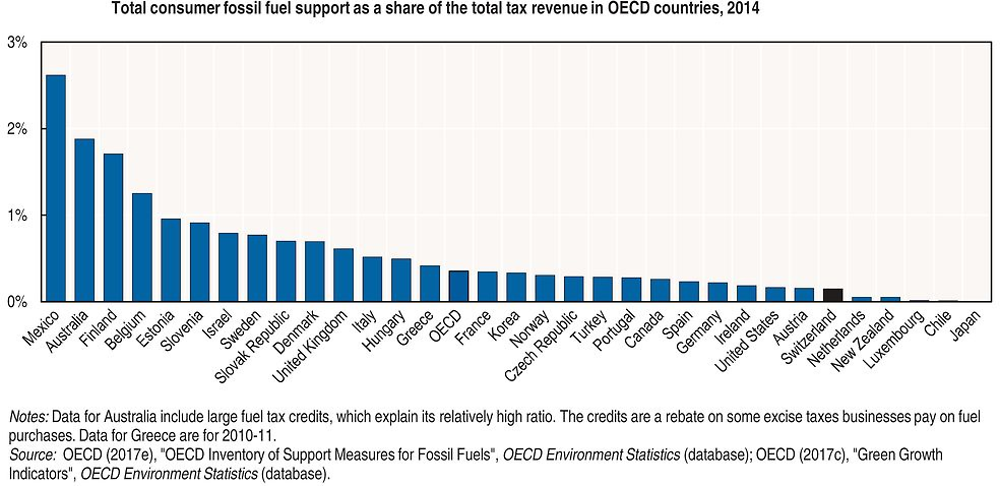

Final consumption of energy in Switzerland is dominated by imported fossil fuel products, with oil (37%) and natural gas (11%) representing close to 50% in 2014 (IEA, 2016). As Switzerland does not produce crude fossil fuels, its support to fossil fuel consumption only concerns industrial and final consumers (OECD, 2015d; OECD, 2013b). The annual support has been estimated at CHF 260 million since 2012 (Figure 3.5), exclusively in the form of tax expenditure (excise and CO2 tax refunds and exemptions). This places Switzerland among countries with a relatively low ratio of tax exemptions for fossil fuel consumption to total tax revenue (0.1%, compared to the 0.4% OECD average) (Figure 3.5).

Swiss tax exemptions or reductions have historically benefited particular sectors (agriculture, forestry, public transport) (OECD, 2013b). Switzerland does not intend to remove these environmentally harmful subsidies and is even considering extending tax reductions to include snow grooming vehicles.

A noticeable trend is the growing share represented by CO2 tax exemptions in total environmentally harmful subsidies. This is a consequence of the tax rate increase from CHF 12 in 2008 to CHF 84 as of early 2017. Exemptions to the tax thus implicitly provide a rising subsidy for GHG emissions. The tax’s impact and effectiveness are particularly diminished by the exemption of transport fuels and GHG-intensive companies (on international competitiveness grounds). To be exempted, SMEs must commit to CO2 emission reduction targets (Section 3). Recent assessments commissioned by the government reveal that tax-exempt SMEs have taken steps to reduce emissions, but there is no evidence as to whether they would have achieved more or less if subject to the tax. GHG-intensive large enterprises are also exempt from the tax due to their inclusion in the ETS. Although in theory the ETS imposes a cap on the sector’s emissions, the price of emission credits under the ETS is much lower than the CO2 tax level.

Given that Switzerland already performs particularly well in terms of production-based GHG intensity (Chapter 1), further reducing CO2 emissions in Swiss manufacturing industry would likely entail high marginal costs and hence require a much higher carbon price incentive, which is probably unfeasible in the short term. In this context, CO2 tax exemptions provide a negative price signal and constitute a policy misalignment. Moreover, the implicit CO2 tax under the Swiss (or future Swiss-EU) ETS does not provide a price signal anywhere close to the current CO2 tax. Should Switzerland maintain its policy focus on short-term competitiveness for GHG-intensive SMEs, the risk of lagging behind in low-carbon innovation and performance in the longer term will increase.

In addition to hydropower, Switzerland relies heavily on nuclear power to meet its electricity needs while maintaining a low-carbon electricity mix. The planned phase-out of nuclear power raises the question of a substitute energy source. Phasing out support to fossil fuel consumption would free up resources and create further incentives on the supply side to develop renewables, including hydropower (Section 5), and improve energy efficiency on the demand side. In 2014, for instance, estimated annual fossil fuel subsidies (CHF 260 million) were nearly equivalent to subsidies for use of renewables (CHF 270 million, though the sum rose to CHF 338 million in 2015) (Fondation RPC, 2016). For a country that lacks fossil fuel resources and imports about 70% of its total primary energy supply, fossil fuel subsidies are also an obstacle to energy security.

4.2. Agricultural policy support and land use-related tax privileges

The level of agricultural policy support remains one of the highest in the OECD at over 60% of gross farm receipts in 2013-15. This is three times the OECD average and makes the country one of the largest OECD providers of support relative to GDP, and the largest relative to agricultural value added.

Prior to the 1990s, output-based support created production and trade distortions, including in relation to developing countries, and barely considered environmental safeguards. Since the agricultural reforms initiated in the 1990s, Switzerland has increasingly responded to a number of agri-environmental challenges (Chapter 1). Importantly, an increasing share of direct payments to farmers is now explicitly based on environment-friendly practices rather than number of hectares farmed or livestock headcount. Moreover, payments are conditional on satisfying environmental criteria, such as frequent crop rotation and low nutrient use (OECD, 2016d; OECD 2015e). Further reforms should seek to achieve absolute decoupling of environmental performance from agricultural production. However, market price support and some output-based direct payments remain (e.g. a lump sum per hectare to ensure food supply). While their aim is to support farm incomes, they have no positive effect on environmental goals, and may even impede achievement of environmental policy objectives.

Switzerland plans to make further positive adjustments (e.g. strengthening ecological requirements in dairy production) in Agriculture Policy 2018-21. It should pursue its efforts to explicitly put agricultural policy support at the service of achieving agri-environmental objectives, including by removing remaining fossil fuel-related tax exemptions and reductions in the sector, e.g. on oil use and on methane emissions. In April 2016, the National Council (lower house) proposed to stop taxing farmers’ earnings from selling their land after it is rezoned for non-agricultural purposes. This proposal, now pending approval by the Council of States court, would further encourage urban sprawl and its undesired externalities. It would come in addition to cantonal property taxes7 and communal taxes8 that already provide strong fiscal incentives to local authorities to make large plots of land available on the outskirts of municipalities in an attempt to attract high-income taxpayers (Blöchliger et al., 2017).

5. Environmental protection expenditure and infrastructure investment in support of green growth

5.1. Environmental protection expenditure

The share in GDP of public environmental protection expenditure (EPE) decreased between 2000 and 2008, then after the financial crisis stabilised at around 0.7% (CHF 4.3 billion), in line with the EU average (Eurostat, 2016). As in other OECD countries, most EPE goes to sewage treatment, although its share has been decreasing since 2000, reflecting progressive application of the polluter-pays principle.

Expenditure on air and climate, and to a lesser extent on biodiversity and landscape, has increased significantly (Figure 3.6). The rise reflects increased efforts to curb CO2 emissions since the introduction of the CO2 tax in 2008. The steady decrease of EPE on sewage treatment since 2000 reflects the decline in investment needs at sewage treatment plants, which are already equipped with tertiary treatment, though upgrades to better treat micro-pollutants have been under way 2016 (Chapter 4). EPE on MSW management has slightly decreased despite the rising volumes generated, possibly as a result of increased recycling and stable use of installed incinerator capacity (Chapter 1). EPE on biodiversity and landscape (Chapter 5) is closely linked to related public financial support, which has continued to increase under Agriculture Policy 2014-17.

EPE is shared between the federal, cantonal and municipal levels (Chapter 2). Since the 2008 fiscal equalisation reform, federal transfers to cantons have had to follow joint programme agreements which include EPE. Plans call for federal transfers supporting cantonal biodiversity activities to double in 2016-19, reaching up to CHF 60 million a year (Chapter 5). The reform also requires rich cantons to support poor (often mountain) cantons.

Looking ahead, Switzerland expects environmental expenditure to increase as ageing infrastructure (e.g. urban wastewater pipelines) is replaced or rehabilitated. In addition, if population, the economy and urbanisation grow as forecast, existing infrastructure will need to be expanded. In this context, demand-side management and incentives for less resource-intensive production and consumption patterns (e.g. new incentives to reduce water and energy use, minimise MSW and foster air and water pollution prevention) could reduce reliance on EPE.

5.2. Greening infrastructure investment

Renewable energy resources

The decision to phase out nuclear power following the Fukushima accident in Japan (2011) prompted authorities to try to speed up deployment of renewables other than hydropower, which already represents over half of electricity generation and around 13% of total primary energy supply (Chapter 1).

In 2009, Switzerland introduced feed-in tariffs (FITs) for electricity generated from renewables (solar photovoltaic, wind turbines, hydropower plants up to 10 MW and geothermal- and biomass-powered plants). The FITs take the form of guaranteed prices per kWh for operators, which cover the difference between production costs and electricity market prices. They are granted for 20 years (10 years for some biomass plants) and are funded by earmarking revenue from the charge on grid use, which is capped by law (Section 3). While the policy reached its initial goal of triggering development of new renewables-based capacity (Fondation RPC, 2016), in 2014 only 3% of the electricity produced benefited from FITs (OECD, 2015c). Switzerland appears to have voluntarily aimed at relatively slow development to avoid windfall profits, to keep running costs manageable in the FIT programme and, when it comes to wind power, to protect landscapes.

In 2014, FIT adjustments were made for solar photovoltaic installations on dwellings. A one-off investment grant, instead of a recurring FIT, may now cover up to 30% of the installation costs of photovoltaic panels, thereby encouraging self-consumption of the electricity produced. Furthermore, the FIT was cut by between 12% and 23%. Such measures were driven by falling electricity prices and technology costs as well as high demand for household photovoltaic installation, which resulted in a long waiting list. Early assessment indicates that the adjustments have been effective in addressing FIT-related issues such as windfall profits in some instances and the cost burden of the long-term payment commitment (Fondation RPC, 2016). However, budgetary and market price support to renewables should be further optimised to sustain the financial viability of such a policy in a scenario of increased development of renewables-based installations.

As of 2018, the first package of Energy Strategy 2050 measures will replace FITs with private contracts (contracts for difference) and introduce additional investment grants, thereby moving to solutions for supporting renewables development that are more responsive to changing market conditions. Such moves will be critical to creating the conditions for renewables to contribute their share to a time- and cost-efficient nuclear phase-out while avoiding increased reliance on imported fossil fuels. Further steps can be taken to this end. While an auction system is not applicable due to the small size of the Swiss market, tenders can be considered for allocating FITs (OECD, 2015a). This could build upon the energy-efficiency competitive tenders introduced in 2010 for industry. Tenders would require FIT applicants to demonstrate that their investments would not be made in the absence of support. Such an “additionality” prerequisite to avoid windfall profits already applies for energy-efficiency competitive tenders. It can meaningfully be replicated for investment in renewables. In the longer run, carbon pricing remains the most cost-efficient way to create incentives for favouring renewables over fossil fuels. Switzerland should consider replacing support with further differentiation of taxation between fossil fuels and renewables in effective carbon rate terms.

Energy-efficient buildings

Switzerland set a target of reducing emissions from buildings by at least 40% by 2020 compared to 1990 levels, with an interim target of 22% by 2015, which was reached. A joint federal-cantonal buildings programme was established in 2010 and is expected to run until 2019. Since 2010, a third of the revenue of the CO2 tax on heating and process fuels (introduced in 2008) has been earmarked to fund this programme (up to the current CHF 300 million ceiling, to be raised to CHF 450 million in 2018). Two-thirds of this goes to the federal level to subsidise refurbishments and the rest to the cantons (which are to match it with their own funds) to subsidise the use of renewables and waste heat. As Section 3 noted, earmarking has significant shortcomings. But in the case of the buildings programme, redistributing a tax paid by occupiers to owners of the flat to enable them to improve energy efficiency makes economic sense. The occupier ultimately benefits from the improvement through reduced energy bills, while the owner would otherwise probably not have undertaken the improvements unless required to by the building code.

The rises in the CO2 tax rate in 2013 and 2016 increased funding availability for the buildings programme in comparison with the first redistribution of the tax revenue in 2010. Between 2010 and 2014, CHF 1 billion was allocated to the programme, making it possible to refurbish some 17 million square metres of building area and install nearly 5 000 wood heating systems, 30 000 solar thermal collectors and 8 500 heat pumps. It is estimated that by 2020 the average annual CO2 reduction effect, compared with business as usual, will be 1.2 million tonnes, which falls short of the CO2 Act objective of 1.5 million to 2.2 million tonnes. While the federal level of the programme is on track, the cantonal level has underachieved. This can be explained by the fact that available cantonal funds are lower than predicted due to budgetary cuts and difficulties in mobilising matching funds. Even so, the programme’s cost-effectiveness (estimated at CHF 65 per tonne of CO2 avoided after four years of implementation) exceeded expectations (Federal Council, 2016b).

In the context of Energy Strategy 2050, the Federal Assembly prolonged the buildings programme beyond 2019 and increased the maximum amount earmarked for it to an annual CHF 450 million, which lowers the cantonal share and will thus partly address the corresponding funding shortfall. Known limitations of existing tax breaks for energy efficiency building renovations (modest incentive effect, significant windfall profit, limited redistribution impact, loss of tax revenue) will have to be addressed (SFOE, 2015; INFRAS, 2015). Policy coherence should also be sought between tenants (the majority of households) and owners.

Sustainable transport

The 2007 EPR recommended targeted public investment supporting a continued transport modal shift from road to rail, in addition to fiscal and incentive measures (Sections 3 and 4). In line with trends observed prior to that, the volume of public spending on rail-related infrastructure investment and maintenance has continued increasing since 2007. Following a rise in road infrastructure investment since 2009, the transport infrastructure in 2012 was split almost equally between road (51%) and rail (46%). By comparison, neighbouring Austria increased the share of rail to over 80% over the same period (ITF, 2016).

New investment is intended to contribute directly to the modal shift policy (Section 3). Earmarking of the heavy goods vehicle tax helped finance construction of the Gotthard Base Tunnel, which opened in December 2016. A rail infrastructure financing programme approved in 2014, following a popular initiative, introduced a permanent infrastructure investment and maintenance fund. Together with traffic demand management measures, cost-efficient ways to finance investment in transport infrastructure will need to be rapidly sought given the projected 50% passenger and 77% freight increases between 2010 and 2030 (Union des Transports Publics, 2016).

Public-private partnerships should be further explored. They have been little used to finance transport infrastructure at the federal level, perhaps in part because of the advantageous financial conditions Switzerland enjoys when raising funds on capital markets. In addition, Swiss pension funds cannot invest more than 15% of their resources in infrastructure. By contrast, several public-private partnership projects have emerged in the cantons. For example, Geneva canton plans to finance a road crossing of Lake Geneva (bridge or tunnel) and the Geneva bypass (estimated at CHF 3 billion) using a 50-year public-private partnership and a toll system. In the first phase (10 years) the private partner would design and construct the projects, at its cost; in the second (40 years) it would operate and maintain them, with the canton paying “rent” financed by a toll it would levy. At the end of the partnership, when the infrastructure is returned to the canton, the toll could be maintained if the infrastructure were declared to be of national scope and included in the national road network. For rail infrastructure, innovative public-private partnerships for cost and benefit sharing would have to be designed.

Differentiated mobility pricing and taxation (Section 3) would also help raise funds for investment in sustainable transport and limit demand for road transport, e.g. through further distance-based taxation. This is especially relevant since increases in public rail transport tariffs, combined with the exclusion of road fuels from the CO2 tax, have made passenger car use a cheaper option on many routes. However, in this area, perhaps more than others, Swiss direct democracy makes it difficult to adopt policy reforms that restrict personal freedom.

6. Greening investment practices in the corporate and financial sectors

The Swiss economy features many large companies and a sizeable financial industry. Further steps to promote mainstreaming of environmental considerations into business and investment decisions, as well as to mobilise private participation in green investment, would yield significant environmental benefits domestically and internationally. Switzerland has the potential to lead by example. Close institutional co-ordination is required between FOEN and federal entities in charge of private sector regulation, particularly the State Secretariat for Economic Affairs (SECO) and the State Secretariat for International Financial Matters.

6.1. Corporate social responsibility and private investment

Switzerland is a large provider of direct investment in foreign economies, both relative to the size of its economy and in absolute terms. Its outward FDI stock has more than doubled over the last decade.9 At the end of 2014, it stood at over CHF 1 trillion or 151% of GDP (SNB, 2016), the third largest share in the OECD (after Ireland and Luxembourg). In 2015, Switzerland had the fifth largest outward FDI flows in the OECD, exceeded only by the United States, Ireland, the Netherlands and Japan.

In this context, the environmental sustainability of outward Swiss FDI can significantly contribute to the transition to a greener economy globally. The UN Global Compact Network and OECD Guidelines for Multinational Enterprises (MNE) provide useful frameworks, especially if combined with trade-related provisions (Section 8). Switzerland proactively participates in most activities under the “proactive Agenda of the MNE guidelines” (OECD, 2016f), and has adopted its own Corporate Social Responsibility Action Plan for 2015-19. However, the parliament rejected a legislative proposal to follow MNE guidance for global supply chain effects of Swiss outward FDI. This demonstrates the strong Swiss preference for co-ordinated voluntary approaches over regulatory requirements, as discussed in other sections of this chapter and in Chapter 2.

6.2. Greening the financial sector

Switzerland hosts a significant financial centre (asset managers, commercial banks, equity investors and funds, institutional investors). Financial transactions are estimated to represent 9.3% of GDP, the second largest share in the OECD, after Luxemburg (28.4% of a much less diversified economy). By comparison, the respective UK and US shares are 7.2% and 7.0% (SIF, 2016). Accordingly, the Swiss financial sector can be an important provider of green finance and a primary driver for greening investment practices domestically and internationally.

However, a FOEN-commissioned independent assessment of the environmental performance of the Swiss financial sector suggests a lot remains to be done. From a climate perspective, holdings of the Swiss equity fund market are estimated to contribute to a global scenario of temperatures rising by between 4°C and 6°C (South Pole Group, 2015) rather than being aligned with the international objective of well below 2°C under the Paris Agreement (UNFCCC, 2015). A number of large Swiss banks are among the many international commercial banks that continue to significantly contribute to financing fossil fuel-related investment (Rainforest Action Network, 2016; Fair Finance, 2015). More generally, the share of assets managed according to environmental, social and governance (ESG) criteria remains negligible despite growth in recent years (Swiss Sustainable Finance, 2016).

A significant step in mainstreaming environmental principles entails excluding financing of certain types of projects. In 2015, nuclear energy and so-called ecological destruction were among the ten types of projects that some Swiss investors stopped financing or investing in (Swiss Sustainable Finance, 2016). In 2016, Publica, Switzerland’s largest public pension fund, decided to divest from coal companies because of their vulnerability to climate mitigation policies. This type of exclusion, if replicated, would have a significant impact in terms of reducing the financial sector’s climate footprint.

Other steps Switzerland has taken to green its financial sector include setting up Swiss Sustainable Finance, a collaborative platform established by SECO to deepen dialogue with the financial sector and promote integration of ESG criteria into investment policies and processes by asset managers, institutional investors and capital market actors. A team of Swiss government, private sector and civil society experts drafted an indicative roadmap in this area (FOEN, 2016d). Such a collaborative approach has the potential to lead to a significant step forward in greening the financial sector. In 2016, the Federal Council established principles for a consistent policy on environmental sustainability in financial markets (Swiss Confederation, 2016; Federal Council, 2016c).

Switzerland is also engaged internationally, having hosted an international workshop in 2016 on environmental risk analysis in the financial sector, and feeding into the G20 Green Finance Study Group work. It supports multilateral voluntary initiatives such as the Financial Stability Board Task Force on climate-related financial disclosure, the 2° Investing Initiative and the Inquiry into the Design of a Sustainable Financial System project of the UN Environment Programme (FOEN, 2015).

Swiss authorities are, however, reluctant to translate such work into more binding action plans, let alone legislation. Voluntary initiatives and international co-operation are prioritised, with the aim of avoiding excessive burdens on the financial industry and ensuring a level playing field with foreign counterparts. The two do not necessarily have to be mutually exclusive, however, and voluntary initiatives alone are unlikely to deliver at the scale and speed needed to address pressing environmental issues such as climate change. For example, 2015 French legislation introduced a reporting obligation for institutional investors on i) their integration of environment in investment policies, ii) GHGs embodied in their investments, iii) their contribution to meeting domestic and international objectives and iv) the financial risk they face because of climate change. While further methodological development is needed to measure carbon-related financial risk, Switzerland could consider making it mandatory to disclose such readily available factual information as the number and volume of investments in and financing of environmentally harmful (e.g. fossil fuel-related) activities. This could initially be tested with publicly owned entities. If later rolled out to other actors, it could significantly speed up the sensitisation of the financial sector to decisions’ environmental impact (including in relation to climate change) and would serve as powerful leverage to encourage behaviour change at scale.

Such information disclosure, however, would not necessarily lead the sector to invest in green infrastructure such as renewables projects. Data on private investment in such projects, along with analysis of public interventions that triggered the investment, would provide clear evidence of the extent to which the financial sector contributes to greening the economy. In this context, obstacles to public-private partnerships at the federal level and to pension funds’ participation in infrastructure investment (energy, transport, buildings) should be removed (Section 5).

7. Promoting environmental technology and eco-innovation

7.1. Innovation profile and strategy

Switzerland has a competitive advantage in science, technology and innovation (OECD, 2014a). As a quality-adjusted measure of research output, it has the OECD’s largest share of documents with a high citation impact. It also has by far the largest share (over 25 per thousand) of doctorate holders in the working age population, including a significant proportion of graduates from abroad (OECD, 2015f). The latter underlines the country’s attractiveness to foreign scientists. Switzerland has an above-average rate of international scientific co-authorships, reflecting a proactive policy of fostering collaboration to promote networking and joint research and development (R&D) projects (OECD, 2016g; OECD, 2014a). While many countries tend to focus their public research strategy on specialised public institutes, Switzerland gives a more central role to universities. Co-operation with the private sector is also fostered through voluntary economic-environmental collaboration.

Every four years, the federal government releases an overarching research strategy. Over 2013-16 it established three main policy guidelines: reinforce the high level of public R&D (typically through National Centres of Competence in Research), increase provision of well‐qualified human capital and create framework conditions conducive to innovation (OECD, 2015f). In addition, four-year master plans for environmental and energy-related research and innovation are prepared, respectively, by FOEN and the Federal Energy Research Commission. Approved by the Federal Council, they serve as planning instruments for all federal bodies and as orientation for cantons and municipalities. In this context, the clear continuity of themes and priorities in the 2013-16 and 2017-20 plans provide a coherent and stable framework.

The environmental research master plans include sustainable resource use as a priority theme (FOEN, 2016e; FOEN, 2012), while the energy research master plans systematically cover four priority themes: energy efficiency in buildings, fuel-efficient and low-carbon mobility, environmentally sustainable energy supply and resource-efficient production processes and products (CORE, 2016; CORE, 2012). Both sets of master plans are closely linked with national strategies for energy (2013), the green economy (2016-19) and sustainable development (2016-19). Research activities relating to the concept of circular economy have received increasing focus across both series of master plans, not only regarding product development and design, but also more holistically in terms of steering economic development. New research plans addressing public transport are being prepared for 2017-20 to support implementation of Energy Strategy 2050.

As part of initial federal steps towards a green economy in 2010, a “cleantech” master plan was released for 2011-14. It focused on climate change and growing natural resource scarcity. It aimed to provide a framework for joint clean technology policy across federal offices, cantons, the business sector, science and research, as well as NGOs. Despite having raised the policy profile of the Swiss clean technology sector, the Federal Council decided in 2016 to discontinue this master plan. The effectiveness of the now looser co-ordination of clean technology activities is to be assessed by 2019.

7.2. Public R&D expenditure and support of eco-innovation