Chapter 4. Waste, materials management and circular economy

Korea is a good performer in waste management and is now seeking to move further towards a circular economy approach. This chapter examines trends in materials use and waste generation, as well as related policies, objectives, and legal and institutional frameworks. It looks at the instruments Korea uses to encourage waste prevention and reduction and to promote recycling and related markets. It studies the environmental effectiveness of Korea’s waste disposal and management before focusing on food waste, waste electrical and electronic equipment, and construction waste. The chapter also discusses engagement in international co-operation and outreach.

1. Introduction

Korea is among the fastest growing countries in the OECD. Resource- and energy-intensive industries are predominant, and small and medium-sized enterprises (SMEs) play an important role, especially in the environmental industry and technology development sectors, where they represent 90% of firms. Economic growth relies heavily on imports of energy and mineral resources and on exports by Korean industries, driven by the information and communication technology (ICT) and electronics sectors. This is accompanied by growing domestic consumption of natural resources and materials, and growing amounts of waste generated. Korea is the most densely populated country in the OECD, and GDP per capita and average disposable income of households remain below the OECD averages1 (Basic Statistics, Chapters 1 and 5).

These characteristics create particular economic and environmental challenges for the management of waste and materials, and have shaped Korean waste polices over the past 25 years. Efforts have focused first on reducing the amount of waste going to final disposal to cope with rapidly growing volumes, little space for landfilling and local opposition to waste disposal facilities; and second on increasing the amount of valuable waste materials that are recovered for recycling and reuse so as to become less dependent on imports for the supply of strategic raw materials. Public authorities have also been keen on keeping prices of public services, including waste management, at an affordable level for all.

Korea has a well-developed and fully fledged policy framework in place, using a variety of instruments and associated with quantitative targets and efficient monitoring of compliance and enforcement. It can build on a very good record in integrated waste management and has in the past achieved top results among OECD countries. This laid the groundwork for a good overall performance in waste and materials management over the review period, with important progress since the 2006 OECD Environmental Performance Review (EPR).

The current aim is to move further towards a life cycle-based “circular economy” approach that keeps valuable materials in the economy. This will require even greater economic efficiency and improved policy alignment, additional efforts to apply the 3Rs (reduce, reuse, recycle) and more systematic consideration of all stages in the life cycle of materials and the value chain of products. It will need to be accompanied with strengthened international co-operation in these areas, particularly in Asia, along with expanded outreach activities and further development of external markets, areas in which Korea is well placed for action.

Korea’s overall good performance in waste management does not leave much room for manoeuvre. In the years ahead, it will be important to focus efforts on the transition to a truly circular economy and on those areas where efficiency gains can be obtained.

2. Trends in waste management and material consumption

2.1. The information basis

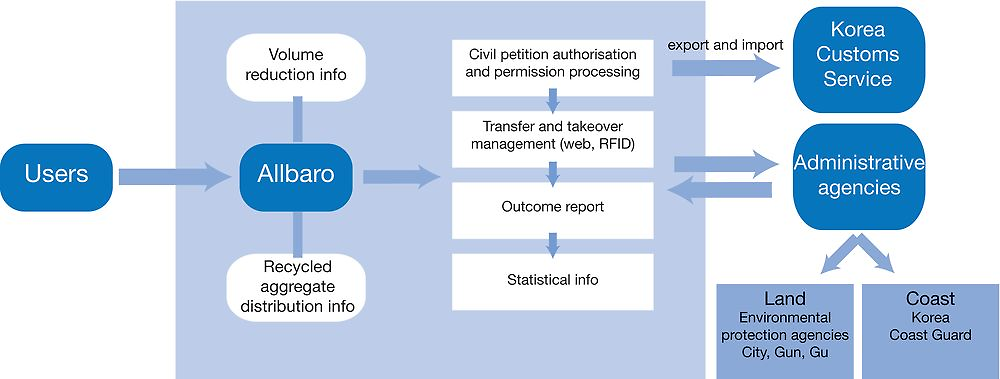

Korea has a well-developed monitoring system for waste generation and treatment, with mandatory reporting by businesses and local authorities and a web-based online information system through which waste transfers, treatment processes and process results are reported and managed in real time (Box 4.1).

Allbaro is a comprehensive online waste information and management system (www.allbaro.or.kr). It was initially developed to track the transport of hazardous waste. Following a trial in 2001, the system was implemented in September 2002 to serve businesses that discharge large amounts of designated waste (more than 200 tonnes per year) and their subcontractors associated with waste collection, transport and treatment. The system has been gradually expanded to cover other waste streams.

The Allbaro system enables online preparation and tracking of official transfer documents. It digitises and processes the waste transfer certificates that circulate between waste producers, transport agents, processing agents and administrations, and allows users to compare and analyse license information and actual waste transfer data. Government administrators oversee the entire process of waste management in real time, and can check whether waste is transferred in a legal and transparent manner to prevent illegal disposal.

The system is used by over 340 000 businesses, representing about 128 million tonnes of waste, i.e. most of the waste generated by business operations in Korea. Waste flows are monitored in real time through radio-frequency identification (RFID). A user can thus trace waste transfers and the various waste processing stages, and see the processing results at any time. The data from Allbaro are used for the generation of annual statistical reports on waste management and for statistical analysis. The system is also used to monitor developments in waste reduction, the reduction methods used and model cases in the business sector, and to encourage co-operation and sharing of best practices among enterprises. Businesses with outstanding performance get a reward or benefit from a presentation programme for model businesses. The information on processing results – secondary raw materials and recycled products – is used in combination with an online platform for the exchange of reusable and recyclable products to stimulate recycling markets.

The Allbaro system involves the participation of the Ministry of Environment (MOE), KECO, local governments and local environmental agencies, and users. A partnership has been established with the Korea Coast Guard that controls waste at sea. The system is managed by KECO, which maintains and further develops the system, takes care of the data processing and provides education and training.

Source: KEI (2013), “Recyclable Resources Market in Korea”, Korea Environmental Policy Bulletin, Vol. 11, No. 1, Korea Environment Institute, Sejong.

Data and statistics on waste generation and management have been produced since 1996 and are updated regularly. Definitions, however, differ from those used in international work. A breakdown of waste generation by industry as requested in the OECD questionnaire has been available since 2010. Data on municipal waste are collected from regional governments through surveys carried out by the Korea Environment Corporation (KECO), which also manages the Allbaro online waste management system. Other waste‐related data come from surveys, such as an agricultural waste survey and a recycling market survey.

Most data produced are freely available on public websites (in Korean only). Korea is an OECD leader in Open Government Data, with high overall levels of availability and accessibility of government data on the national web portal and of government support for their use (OECD, 2015).

Monitoring and analysis of material flows are less developed. Efforts focus on analysis of flows of particular metals, including strategic metals; these data are regularly updated (annually for some metals, every three years for others). Macro-level material flow accounts (MFAs) in line with OECD guidance were set up on a pilot basis for 1991-2009 and updated recently. But they are not maintained as part of the official statistical system,2 and the results are not linked to waste statistics. It is thus not easy to get a full picture of the material flows through and within the economy, how they relate to waste streams and recycling efforts, and where further opportunities for efficiency gains exist. Hence little use is made of these data in national waste and materials management policies.

Regular production of MFAs at macro and industry level, and further integration with waste data as part of the Korean Resource Cycle Information System, would be all the more important since Korea is moving towards greater resource circulation and life-cycle-based management. Synergies could also be explored with the Korean Chemical Information Platform (https://kreachportal.me.go.kr), which since 2014 has enabled electronic processing of the reporting, registration and evaluation of chemical materials.

More generally, the wealth of data produced by Korea could be better used to inform decision making, set targets, monitor the effectiveness of policy measures and support public information. Information from Allbaro could be combined with material flow data to monitor the circulation of materials and waste in the economy and assess the performance of resource circulation policies. Industries could be encouraged to produce material flow and waste information to monitor their resource productivity, and to use this information in combination with accounting data to implement material flow cost accounts. This would be a powerful tool to help analyse the environmental and financial consequences of material and energy use practices and identify opportunities for efficiency gains. Industries could also be encouraged to more systematically include such information in corporate reporting, integrated performance assessments and financial statements. Guidance on reporting criteria could be provided by the government to ensure harmonised data and reports.

2.2. The material basis of the Korean economy

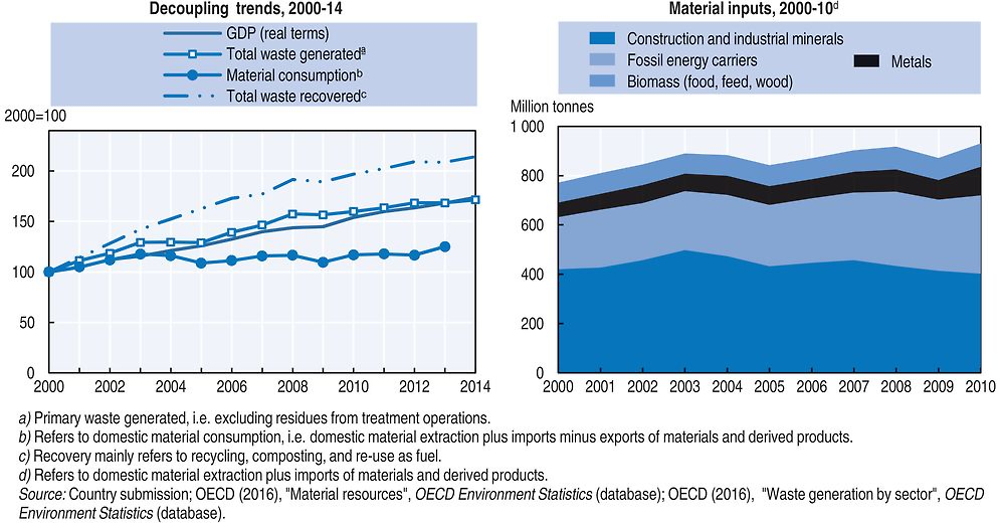

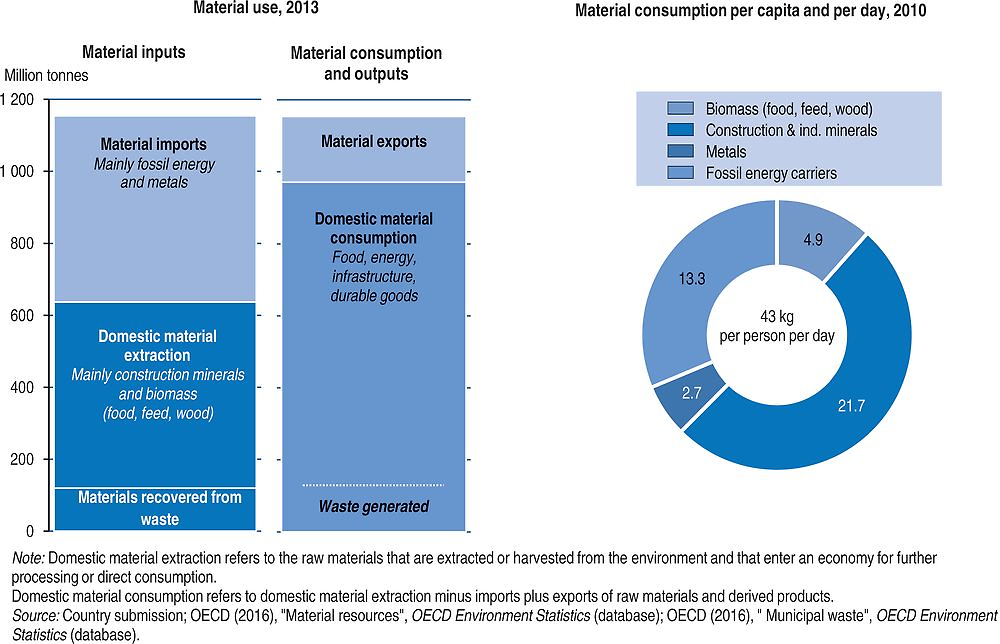

Korea is among the OECD’s most resource-intense economies, due to its resource-intensive industries and a dynamic construction sector. The amounts of material resources used as inputs for domestic production and consumption increased by more than 30% between 2000 and 2013, reaching about 1 billion tonnes in 2013. The amounts of waste generated over the same period increased by 68%, reaching 144 million tonnes in 2013 (Figure 4.1).

More than half (53%) of the material resources used as inputs for domestic production and consumption are imported. The country’s import dependence is particularly high for fossil fuels and metals (close to 100%) and wood (more than 75%), while most construction minerals are available in the country. An estimated 20% of the material inputs are used for products that are exported, and about 80% are consumed in the country (in the form of energy and food consumption, durable goods, infrastructure).

Domestic material consumption (DMC)3 grew by 25% over 2000-13. From 2004, it grew at a lower rate than GDP, resulting in an overall 34% improvement in material productivity (defined as the amount of economic value generated per unit of materials used, expressed in terms of GDP per unit of DMC). In 2013, Korea generated almost USD 2 000 of economic value per tonne of materials used in the country. This is slightly more than the OECD average. Though reliable data on the raw material equivalents embodied in international trade are not yet available, estimates suggest that, had these raw materials been accounted for, productivity gains would have been lower. About 17% of Korea’s material consumption ends up as waste that is subsequently recovered to a great extent (Figures 4.1, 4.2).

About half the materials consumed are construction minerals, a share higher than in most OECD countries. This is mainly due to the replacement or renovation of apartment buildings built in the 1960s and 1970s and to big infrastructure projects such as the construction of a high speed railway. It is followed by fossil energy carriers (31%), which registered the largest increase over the period due to the expansion of industrial activity and increasing living standards. Per capita DMC remains below the OECD average (as does GDP per capita), but is higher than the world average. The level is comparable to those in Belgium and the Czech Republic.

2.3. Trends in waste generation and management

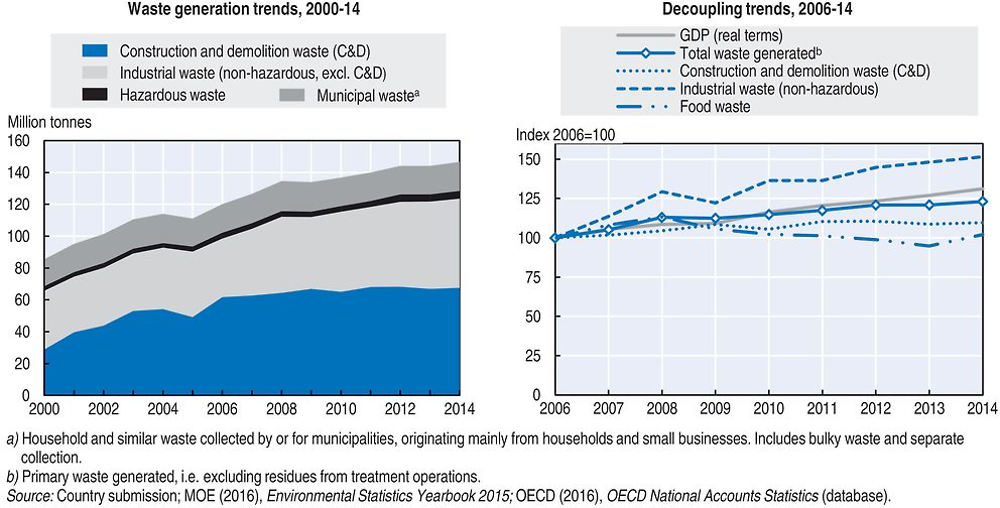

Korea generated 146.6 million tonnes of waste in 2014. This represents 2.9 tonnes per capita and 8.6 tonnes per USD 1 000 of GDP, which is lower than in many other OECD countries. Waste generation remains closely linked to economic growth; it increased by 71% since 2000, at a rate close to economic activity (74%). While in the first half of the 2000s, the amounts of waste grew at a faster rate than GDP, recent data indicate a flattening of the growth rate and first signs of a weak decoupling from economic growth. Whether this indicates a new trend remains to be seen in the years to come (Figure 4.3, Table 4.1).

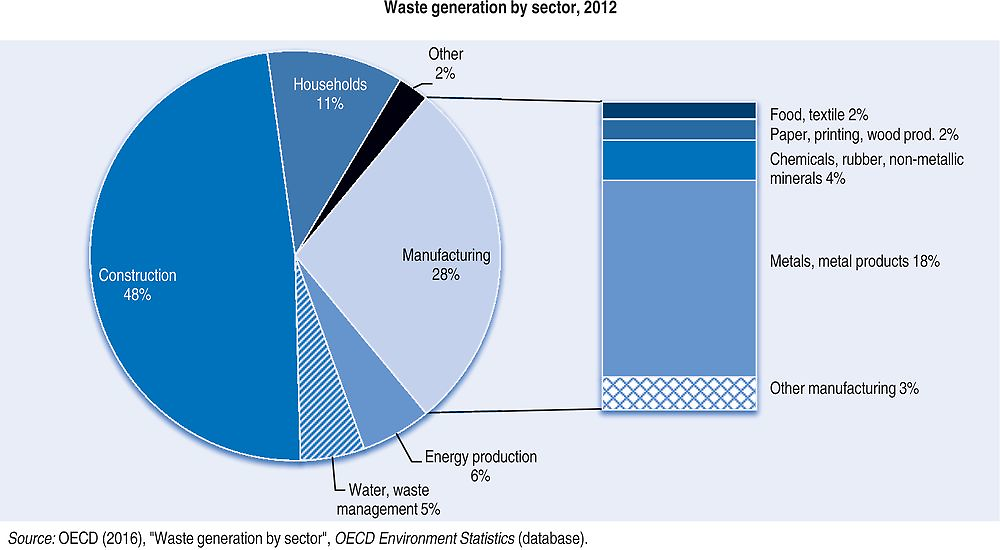

As in many countries, construction and demolition activities are responsible for the largest share of the waste generated (48%), followed by manufacturing (28%) with manufacturing of basic metals and metal products representing 18% (2012 data). Waste from households account for 11% (Figure 4.4).

Between 2000 and 2014 general business waste (industrial waste) grew by 51% and hazardous waste by 73%, while construction and demolition waste more than doubled (+135%). In 2014, 57% of designated waste was recycled, compared with 50% in 2000 and 61% in 2005, while 19% was landfilled, compared with 3% in 2000 and 18% in 2005.

Over the review period, there was a marked shift from landfilling to recycling and incineration with energy recovery. Most of the waste generated is recovered for reuse in the economy. Only 9% is landfilled, 6% incinerated and 1% kept in permanent storage or dumped into the sea. Sea dumping of sewage sludge, food waste leachates, and livestock wastewater was banned in 2012-13 when the 1996 Protocol to the London Convention took effect; such waste is now incinerated or recycled (Table 4.1).

The amounts of waste recovered and recycled have more than doubled since 2000. Since 2006, they have grown on par with waste generation, leaving the overall recycling rate almost unchanged at 84%. Recycling rates are higher than in many other OECD countries. They are highest for construction and demolition waste (97%), food waste (96%) and tyres, followed by packaging materials, large and medium-sized waste electrical and electronic equipment (WEEE), vehicles and municipal waste. This is accompanied with an increase in the amounts of recycled products and secondary raw materials available on the market. The high recycling rate is mainly driven by construction waste that weighs a lot and is almost entirely recycled, mainly through backfilling and mounding (Section 8.3). But recycling rates for other industrial waste and for designated hazardous waste are also growing.

Generation of municipal waste has increased by 7% since 2000, showing considerable decoupling from final private consumption, which increased by 52%. The amounts generated per capita remained stable (361 kg per person) and below the OECD average (525 kg per person). This can be attributed to the volume-based waste fee (VBWF) system that has been in place since 1995 and to the free collection of recyclable waste.

The upward trend in food waste generation has been curbed in recent years, with a decrease of 9.6% between 2008 and 2014. In 2014, food waste accounted for 27% of municipal waste; about 96% of it is recycled into feed and compost, and fuel for electricity production. This is attributable to Korea’s active food reduction policy (Section 8.1).

The management of municipal waste has continued to shift from landfill dominated treatment towards more recovery. The performance of separate collection of municipal waste has improved over time for major waste streams. Some 77% of municipal waste (recyclable and non-recyclable) is collected from door-to-door, 23% from dedicated collection points. As a result, landfilling has decreased from 47% to 16%; and the overall recovery4 rate has grown steadily since 2000 (from 48% to 82%). Material recycling increased from 41% to 59%. The highest growth rates can be observed for waste incinerated with energy recovery, which has almost tripled since 2000 (+275%). This can be attributed to the government’s active waste-to-energy policy, implemented since 2008. As a result, some waste that was previously recycled is now being converted into energy (Figure 4.5).

3. Objectives and policies for waste and materials management

3.1. Policy framework and objectives

Korea has a well-developed policy framework using a mix of instruments associated with quantitative targets for waste reduction and recycling. It promotes an integrated approach to waste and material management, building on the principle of the 3Rs. The aim is to minimise landfilling of untreated waste, maximise cyclical use of materials in the economy and encourage recycling of waste materials into high value products. The stated goal is to move away from a waste and materials-oriented approach towards a life-cycle-based “circular economy” approach, and to establish an efficient resource circulation society. This move is driven by concerns about climate change and the supply security of raw materials and solid fuels. Priority is given to the economic value of waste as a resource.

In recent years, the policy focus has been shifting from material recycling to energy recovery through the production of solid refuse fuels and incineration as part of a broader effort to increase the country’s energy autonomy via a waste-to-energy policy.

The main policy documents are the Comprehensive National Waste Management Plans (NWMP) and the Fundamental Plan for Resource Circulation (FPRC), complemented with more specific plans and legislation to deal with selected waste streams: construction waste, food waste, hazardous waste, WEEE and waste vehicles. The plans are supported by measures to promote extended producer responsibility and green public procurement (GPP), to foster recycling markets and to support technology development, clean production and innovation.

The second NWMP (2002-11), covering part of the review period, promoted an integrated approach to waste management along with quantitative targets for waste reduction and recovery. It was revised in 2008 to further strengthen the management system for hazardous waste, among other elements. A third NWMP is in preparation, having been delayed by discussions about the elaboration of a new law on resource circulation (see below). The plan will include targets for resource circulation, and will regulate the performance of resource circulation in industries and in the provinces.

The first FPRC (2011-15) was established with the stated goal of establishing a zero-waste society that goes beyond purely quantity-based resource circulation and shifts towards qualitative resource circulation by encouraging upcycling (i.e. recycling that upgrades the value of the materials recycled).

3.2. Legal framework

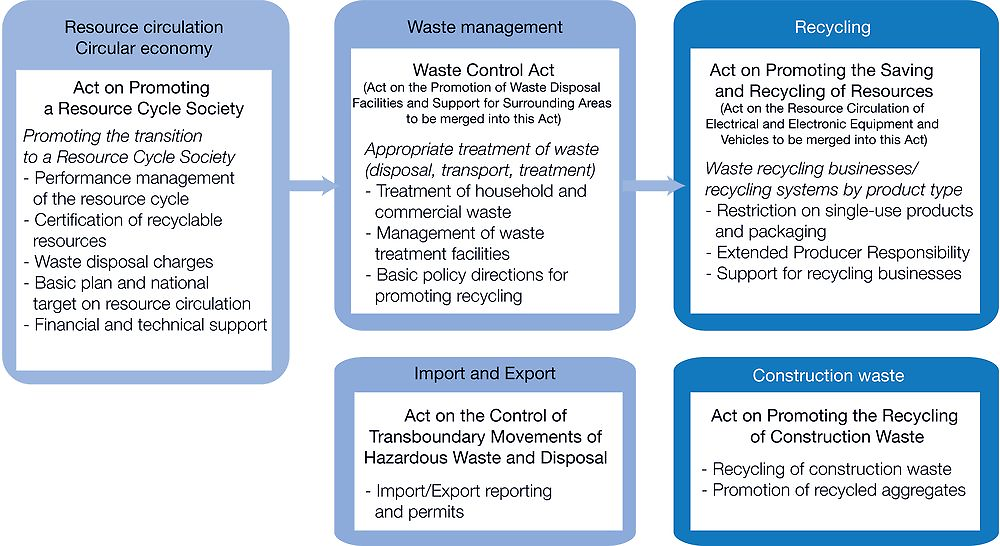

The legal framework for waste and material management is comprehensive. Reflecting the country’s policy objectives, it shifted progressively from a pure waste management approach in the mid-1980s to a 3Rs approach in the 1990s and more recently to a circular economy approach that considers waste to be a domestic resource.

The main laws are the Waste Control Act (1986), which regulates the recycling of commercial waste (industrial, hazardous, construction), and the Act on Promoting the Saving and Recycling of Resources (1992), which restricts the use of disposable goods in the service sector (restaurants, food stores, hotels), among other provisions. They are supplemented by laws that address specific types of waste and specific management challenges, such as the recovery and recycling of construction and demolition waste, WEEE and waste vehicles. Transboundary movements of hazardous waste and their disposal are regulated under a 1992 act that transposes the provisions of the Basel Convention into national law. Other relevant laws include the Environmental Technology Promotion Act (1994) and the Act on Promoting a Transition towards Environment-Friendly Industry (1995).

The Waste Control Act specified the types of waste whose recycling was permitted and the treatment types that could be used. Its provisions were very restrictive and rigid, strictly limiting the number of authorised recycling methods and uses of recycled products. With the increased focus on recycling and resource circulation, these provisions proved to be counterproductive, as they represented barriers to the development and use of new recycling technology, and hence to the recycling of valuable materials. The act was revised in July 2015 to overcome these obstacles. The revised act, taking a more positive approach, specifies only the types of waste materials and recycling methods that are forbidden by law, and gives waste generators and recycling businesses greater flexibility concerning the recycling of all other waste and the development of related technology.

To support the new policy approach to waste and materials, the legal framework is being streamlined and restructured. All legal acts on waste disposal, recycling and transboundary movement of waste are being brought together in a coherent framework under the umbrella of a new law, the Framework Act on Resource Circulation, adopted in late May 2016 and entering into force in 2018; application decrees are pending (Figure 4.6). It will be accompanied by a new NWMP.

Implementation of the framework act is expected to further encourage the use of recycled and remanufactured products, and help businesses find a market for their recycled materials. One goal will be to achieve a 3% landfill rate and 87% recovery rate. Implementation will also further consolidate extended producer responsibility by assessing the resource circulation potential of consumer products, and issuing certificates for recyclable and recycled resources. It will strengthen the waste-to-energy policy by charging a disposal tax for waste that is landfilled or incinerated without energy recovery. And it will create a framework to ensure that businesses committed to resource recovery get the financial and technical support they need.

Source: Country submission.

3.3. Institutional arrangements and governance

The MOE is responsible for the policy and legal framework for waste management at the central level. It implements and revises waste-related legislation; develops, co‐ordinates, enforces and monitors the NWMPs; and conducts waste-related statistical surveys that inform the development and implementation of national waste policies. It manages the disposal and treatment of controlled waste carried out by the private sector (the government having devolved these functions to the private sector in the early 2000s) and issues permits and authorisations for transboundary movements of hazardous waste. The MOE works closely with other ministries, including the Ministry of Science, ICT and Future Planning (MSIP) on nuclear waste; the Ministry of Health and Welfare on medical waste; the Ministry of Trade, Industry and Energy (MOTIE) on control of transboundary movements of hazardous waste; the Ministry of Land, Infrastructure and Transport on construction waste; and the Ministries of Agriculture, Food, and Rural Affairs and of Health and Welfare on food waste.

Local authorities (16 regional autonomous governments: nine provinces and seven metropolitan areas) are responsible for establishing basic plans on waste treatment within their jurisdiction, including current and planned developments and related financing. They manage the disposal and treatment of non-hazardous municipal and business waste, and take care of the installation and operation of waste treatment facilities and the long-term closure and aftercare of landfills. To carry out these functions, they can impose a charge on landfilled waste; the revenue feeds into a fund to cover post-closure landfill costs. Since 2002, local authorities have also been responsible for the permitting and enforcement systems concerning waste management in their jurisdictions, and for compliance and enforcement inspections, which can be delegated to private sector inspectors. The MOE provides assistance and guidance on inspections and monitoring, which has led to improved consistency in inspection and enforcement, though room for further progress exists.

Municipalities (cities and counties) are responsible for the collection, transport and management of municipal waste, including the separate collection of recyclable waste and the establishment of drop-off recycling centres within easy reach. Collection frequency and treatment methods are specified in the local basic plans, which take into account local circumstances, including storage and recycling capacity. A total of 3 488 administrative districts are in charge of waste collection and separation. Waste collection is carried out directly or outsourced to a private company. Municipalities set tariffs for waste collection and collect recycling and waste disposal charges.

Most incineration plants and landfills for municipal waste are managed by local authorities. Some disposal sites are run by private operators. The Sudokwon Landfill in Incheon, near Seoul, has been run since 2000 by a public-private partnership, the Sudokwon Landfill Site Management Corporation, affiliated with the MOE, which replaced the municipal operator. Most hazardous waste landfills are owned and managed by the private sector.

Businesses are responsible for managing their non-hazardous waste, including construction waste. They can do so directly in their own facilities or outsource the treatment to certified specialised operators. All waste transfers and disposal methods have to be registered in the Allbaro system.

3.4. Policy instruments

Korea employs a range of complementary policy instruments to encourage waste reduction, reuse and recycling. These include separate collection requirements, mandatory recycling targets for packaging materials and products, voluntary agreements for waste reduction and recycling in businesses, economic instruments such as volume-based municipal charging schemes and deposit/refund systems for beverage containers, extended producer responsibility and take-back systems for waste that is easy to recycle, a landfill ban on food waste, and charging schemes for business waste and for products that are difficult to recycle or contain harmful substances.

These instruments are complemented by mandatory GPP; information instruments such as eco-labelling, awareness-raising campaigns and training; and measures that support the development, commercialisation and export of new technology (e.g. clean production, recycling technology, use of biogas). Korea exports its know-how in waste management through bilateral and multilateral co-operation, including technical agreements that open up new markets for Korean industries.

Many of the measures taken and the targets in place apply to the amount of waste generated or collected, i.e. to the end of life of materials and products. New measures increasingly apply to the design and production phases or include provisions that stimulate actions during these phases (remanufacturing, design for environment, reduction of toxic contents in products).

Targets

Objectives and quantitative targets have played an important role in Korean waste and material management policies. Targets are set for waste reduction, for waste treatment and disposal rates, and for recycling rates. They are closely monitored, and regularly reviewed and updated. Mandatory targets are imposed on product recycling, such as consumer electronics under the extended producer responsibility system; on recycling of end-of-life vehicles; and on waste reduction by businesses. Other targets are set to serve as a guide for government policies and public action, such as those set for food waste reduction and for the recovery and upcycling of construction waste.

Korea reached most of its quantitative targets during the review period and set new ones. However, it did not meet the overall objective set in the second NWMP to reduce total waste generation by 8.5% between 2002 and 2011, to 374 314 tonnes per day. Indeed, in 2011, 383 333 tonnes of waste was generated per day, and waste generation continues to grow, though at a lower rate than in the 1990s.

Economic instruments

The use of economic instruments in line with the polluter-pays principle is well established and was extended over the review period. Taxes and charges are used in combination with financial support and targets to create incentives for waste reduction and recycling. Korea is one of the few countries where manufacturers and importers have to pay a waste product charge to internalise the waste management costs of products that are hard to recycle or contain hazardous substances. The VBWF system for collection of mixed household waste has been extended to the whole country, except small settlements and remote areas; since 2010 it has also applied to food waste. Together with free separate collection services for recyclable waste, it has been instrumental in reducing waste going to final disposal.

Investment in waste treatment and recycling facilities, in recycling technology and in research and development (R&D) for clean production and eco-innovation benefits from government subsidies, tax credits and long-term low interest rate loans.

Information tools

The government uses various channels and tools to inform the public about waste management issues and raise awareness about the importance of waste reduction and recycling and environmentally sound management. Among them are advertisements, public discussions and conferences, and voluntary agreements with businesses. To reduce food waste, special TV advertisements are broadcast during national holidays such as Lunar New Year and Chuseok, the Korean Thanksgiving Day, and are included in TV entertainment programmes. The government also organises public contests on practical examples of effective waste reduction that are compiled in promotional booklets, and on ideas for food waste reduction and user-created contents.

Information campaigns are also carried out to stimulate the collection and recycling of WEEE. A campaign to collect used cell phones in elementary and middle schools, through large retailers and railway corporations, resulted in the collection of 350 000 phones. A campaign called Recycle 2008 targeted the collection of used home appliances on islands, providing free “after sale” services and promoting recycling.

3.5. International co-operation and outreach

Korea is a party to the London Convention on the Prevention of Marine Pollution by Dumping of Wastes and Other Matter, and to the Basel Convention on the Control of the Transboundary Movements of Hazardous Wastes and their Disposal. It participates actively in multilateral and regional organisations and hosts major international meetings related to waste and material management. In 2012, it launched the Korea Basel Forum, a public-private co-operation platform for implementation of the Basel Convention. Korea plays an important role in regional initiatives to promote the 3Rs (e.g. in the Asia-Pacific 3R Forum) and green growth. Outreach has a twofold objective: a) exchanging experience with other countries; and b) exporting Korea’s know-how and opening up new markets for Korean industries (in waste management and recycling, technology development, etc.). It includes MOUs and technical co-operation agreements with developing countries, as well as waste-related aid projects, transferring Korea’s waste management experience and technology. Bilateral policy dialogues on waste and material management have also been established with Germany and Japan.

Since 1999, the environment ministers of Korea, China and Japan have met every year to tackle environmental issues in north-east Asia. This Tripartite Environment Ministers Meeting is the highest-level co-ordination mechanism on environmental co-operation among the three nations. Waste is one of ten priority areas, and a collaboration mechanism on waste trade in north-east Asia has been set up. Since 2005, a waste seminar has been held every year with the participation of experts and government officials to discuss waste policies and issues, including hazardous waste management, transboundary movement of e-wastes, the 3Rs and a sound resource-recycle society.

As part its international co-operation programme for environmental technology, Korea supports joint research with institutes in countries importing Korean technology. It also provides technology support concerning research and analyses on waste management, recycling and harmful substance management. The countries involved have been expanding to include China, Viet Nam, Russia, the United States and countries in the Middle East and Europe. Sharing some of Korea’s environmental technology and policies with developing countries in the form of pilot projects is seen as an important way to promote exports of environmental technology by Korean firms. Examples include the installation of a hazardous waste incinerator in the city of Linyi in Shandong, China (2012), projects in Indonesia and in African countries, a grant project for construction of a landfill in Cambodia (2009) and a project on managing urban waste and abandoned mines in Mongolia.

Korea also supports developing countries in establishing national waste management master plans and in building capacity on waste and material management. Over 2007-15, 11 countries benefitted from its support in this area, including Algeria, Costa Rica, Indonesia and Viet Nam.

4. Encouraging waste prevention and reduction

The target groups for waste reduction efforts are households and consumers, along with retail and manufacturing businesses. Target product categories include food, packaging materials, single-use disposable goods, and goods that contain toxic components or are hard to recycle. Many efforts aim at reducing the amounts going to final disposal. Other measures address reduction at source and prevention, through remanufacturing (e.g. machinery, medical devices) and eco-design (e.g. electric and electronic equipment) and through information and awareness raising campaigns (food waste, WEEE) and restrictions on the use of disposable goods and excessive packaging.

4.1. The volume-based waste fee system for municipal waste and food waste

The VBWF system, initiated in 1994, applies the polluter-pays principle to reduce amounts that going to final disposal and to maximise separate collection of recyclable materials. The fee is calculated based on the amount of mixed residual waste collected. It applies to municipal waste originating from households and businesses, and was expanded to food waste in 2010. Recyclable waste collected separately remains free of charge regardless the amount. This helps ensure a stable collection performance, which is important for the downstream recycling channels, and for negotiating good prices for selling the recyclable materials.

The VBWF is collected by local administrative districts; the system covers 142 out of 145 local authorities (3 478 out of 3 488 administrative districts; the districts not covered are those that are very small – fewer than 50 households – or located in remote areas that are difficult to reach, such as mountains (two-thirds of the territory is mountainous) and islands (the country has more than 3 000).

The collection methods, billing systems and fee level vary according to local circumstances. The methods in use include:

-

Radio frequency identification-based billing. The RFID system uses electronic tags to record which container is picked up and where, and to calculate the fee according to the weight of waste collected. This method is recommended by the MOE.

-

Payment chip or sticker. The waste generator buys a payment chip or a sticker that is attached to the waste container. This method is commonly used for the collection of bulky waste for which the price varies according to the type and size of the items collected.

-

Designated standard garbage bag system, in which the waste generator buys standard 20 litre plastic disposal bag. The fee is built into the bag purchase price. The bag system is the most common. It is used for mixed household waste and food waste. The government sets an affordable price for the bags. Local governments can adjust it, after consideration of their fiscal situation and consumer prices. Hence the prices vary across the country. Low income household can receive the bags for free. Each administrative district has its own bags that until recently could only be used in the district where they were bought. This has generated complaints from citizens moving from one district to another.

The VBWF system has been instrumental in limiting and reducing the amounts of municipal waste generated and going to final disposal. Landfill rates have steadily decreased, down to 15.6%, accompanied by a significant increase in recovery rates to 59.1%. It has been estimated that between 1995 and 2013 the system generated cumulated gross economic value of KRW 21 353 billion.

The VBWF has increased over time. But, as with other public services, its level remains very low and the system seems to be starting to lose its incentive role. An attempt to harmonise and raise the price of garbage bags at the national level in 2008 failed; in a context of recession and increasing consumer prices, local authorities were reluctant to impose an extra financial burden on citizens.

Remaining and new challenges include illegal dumping, which, although reduced, remains of concern; incineration without energy recovery; and inappropriate waste sorting practices by households and small businesses. The share of recyclable materials put in official bags for residual waste remains high (70%) and has been growing. This signals decreasing public motivation and challenges the effectiveness of the VBWF system. Recent years have also seen a sharp increase in the number of small households, whose consumer behaviour differs and which generate much more waste per capita than bigger households.5

Korea needs to find new and better ways to address changing behaviours and further improve the efficiency of the VBWF system. The government recently took measures to oblige businesses in several districts that dispose of large amounts of household-like waste to write their name and contact information on the garbage bags they dispose of. The waste bag system has become more flexible: in case of a move, the bags bought in one district can be used in another in combination with a special permission sticker, and smaller and cheaper 3 and 5 litre bags have been introduced to satisfy the needs of smaller households. Beyond these measures, it will also be important to take better advantage of the synergies with other measures, such as reduction at source of single-use disposable products and packaging waste.

There is a potential conflict between, on the one hand, the objective of increasing the cost-effectiveness of waste management through the use of economic instruments and the application of the polluter-pays principle to achieve full cost recovery, and, on the other, the social objective of keeping fees for public services at an affordable level for everyone. While the government favours a reduction in the management costs, this may not be sufficient; ultimately, an increase in the fees imposed on households and other generators of municipal waste may be required. This could be supported with the development of a long-term plan for cost recovery by the MOE in collaboration with local governments.

4.2. Product charges and waste reduction plans in the business sector

Businesses are subject to several complementary measures and economic instruments to encourage them to reduce the amounts of waste they generate and dispose of. These include waste product charges for products that are difficult to recycle or to manage, mandatory waste reduction plans for large companies, recycling duties under extended producer responsibility, and the planned waste disposal charges for landfilling and incineration.

To reduce waste in industry through clean production, the MOE supports R&D investment in waste reduction and reuse technology, and MOTIE supports environmental SMEs in developing and commercialising cleaner production technology (around 140 core types, including zero-pollution technology).

MOTIE has further supported reuse of goods by giving a legal basis to nurturing remanufacturing industries through an amendment of the Act on Promoting a Transition towards Environment-Friendly Industry in 2005. The revised act established a detailed implementation system, including quality certification of remanufactured products and financial support. The scope of items subject to remanufacturing, formerly limited to automobile parts and WEEE components, has been expanded progressively to include industrial machinery, electronic products, military equipment and medical devices.

Waste charging system for manufacturers and importers

Korea is one of the few countries where manufacturers and importers have to pay a waste product charge, the Advance Disposal Fee (ADF), on products that contain hazardous substances, are difficult to recycle or are likely to cause management problems. Such a fee creates incentives to design products that are easier to dismantle and recycle, and that contain less harmful substances. It also helps internalise the management costs for small waste streams for which take-back programmes would be too costly. The ADF applies to containers for pesticides and hazardous chemicals, and to anti-freeze solutions, chewing gum, disposable diapers, cigarettes, and non-packaging plastics that are not included under extended producer responsibility, such as PVC pipes, toys and kitchenware. The system is designed to prevent and control waste generation by applying the polluter-pays principle. As separate collection and recycling technology evolves, products subject to the ADF are progressively integrated into the producer responsibility system.

The ADF, collected by KECO for the MOE, feeds into the Special Account for Environmental Improvement. The revenue is used to fund studies on waste reduction and reuse, to develop related technology and facilities, to fund waste recovery and reuse operations by local governments, and to buy and store reusable materials. The rate rose from 20% of the disposal cost in 2008/09 to 60% in 2010/11 and 100% in 2012.

Businesses that sign voluntary agreements on the collection and recycling of plastic waste and that perform well can be exempted from the ADF. For economic reasons, exemptions are also given to SMEs with annual revenue below KRW 20 billion, and to small and medium-sized start-ups.

Business Waste Reduction Programme

The Business Waste Reduction Programme, introduced in 1996, imposes mandatory waste reduction targets for big enterprises. The aim is to reduce negative environmental impact by minimising the amount of harmful waste going to final disposal, controlling waste generation and expanding recycling. The programme targets businesses and operations that generate large amounts of waste (i.e. a three-year average of more than 1 000 tonnes of non‐hazardous waste per year, and more than 100 tonnes of hazardous waste). The programme covers 2 312 businesses, including 1 538 target businesses that are subject to mandatory waste reduction, and 18 types of business operations.

Target businesses have to prepare a waste reduction and recycling plan every three years, and to report on the results obtained. The Allbaro system is used to monitor developments in waste reduction, the reduction methods used and model cases. This information is used to encourage co-operation and sharing of best practices among enterprises. Businesses with outstanding performance are rewarded with either priority access to government funding and technical support for waste reduction technology and facilities, or a presentation programme for model businesses (e.g. at fairs and through publications showcasing good practices). Companies that underperform are given a technical diagnosis and receive information and guidance on how to reduce waste.

The amount of waste generated by the businesses targeted by this programme tend to increase at a slower pace than production output. More than 90% of the waste generated is recovered for reuse and recycling. These positive results are insufficient, however, to curb the upward trend in industrial waste generation. SMEs, which represent an important share of Korea’s industrial base, are exempted from many waste reduction measures and obligations, but receive training and support. Further progress will require additional measures, including a greater focus on the needs of SMEs.

The government also needs to provide greater impetus to industries to fully engage them in such projects. Regulations and targets are still often perceived as a burden rather than an opportunity, and many developments in the business sector remain dependent on government support. This indicates that there is room for efficiency gains and that further progress can be made with resource productivity, waste reduction at source, design for environment and integrated performance management. Implementation of the 2016 Framework Act on Resource Circulation will be instrumental in this respect.

Circular business models

One area to be considered in particular is further development of circular business models that achieve greater resource efficiency and fully integrate waste as a resource in the production cycle via the concept of industrial symbiosis. Korea has ample opportunities for industrial symbiosis and closed-loop processes in industry. Further steps could be taken to establish eco-industry town projects that bring together firms or clusters of industries that are complementary and in which the by-products or residuals of one enterprise are used as a resource by another enterprise, with mutual economic and environmental benefits. This could build on experience with existing projects such as the eco-energy town projects managed by the MOE, MOTIE and MSIP, and the network of eco-industrial parks established under the eco-industry master plan (MOTIE) and supported by regional centres. Waste treatment firms could be integrated into such complexes to improve opportunities to match material inputs and outputs.

There are also important synergies between policies that encourage eco-innovation, clean production, R&D, eco-friendly businesses, remanufacturing and energy efficiency, and policies that encourage integrated waste and material management and a circular economy. Although co-operation exists, such synergies could be better exploited if all ministries involved worked together to establish a consolidated overview of the existing support measures, and if mechanisms were in place to co-ordinate the relevant programmes and to assess their costs and benefits.

4.3. Disposable and overpackaged products

To reduce the amount of disposable goods and use of excessive packaging, priority is given to legal instruments combined with voluntary agreements. Measures to reduce waste at source include the Packaging and Labelling Recommendation System (2003) and the Packaging Inspection System, which identifies excessive packaging. The use of disposable single-use products (e.g. cups, vinyl bags, plastic shopping bags) and overpackaged products has been regulated since 1994.

-

Businesses that use a lot of disposable products have to restrict their use and cannot give them out for free. Regulations and targets are differentiated according to the business type (Table 4.2).

-

To reduce unnecessary packaging, restrictions are imposed on product packaging methods (e.g. double or triple layers and empty space inside containers), and on packaging materials by prohibiting the use of materials that are difficult to recycle, including PVC.

To assist local authorities in monitoring and inspecting target businesses, the MOE developed guidelines on restrictions of use of disposable products. Special attention is given to limiting overpackaged products during such traditional holidays as the Lunar New Year and Chuseok, and during the school admission and graduation periods. The targets and measures are regularly updated to reflect behavioural changes and technical developments concerning recycling and packaging methods. In 2008, biodegradable resin products were thus exempted from the regulation on disposable products, the disposable cup deposit programme was abolished, and the use of disposable paper cups and free paper bags was permitted, a move that non-governmental organisations have criticised.

Voluntary agreements have been signed by the MOE with businesses that typically use disposable products, including:

-

Major coffee shops and fast-food restaurants, which agreed to reduce the use of disposable products, enhance the collection and recycling of used disposable cups and provide incentives to people using reusable cups, including instant cash discounts. The agreement, signed in 2002, was renewed in 2013. It includes the setting of quantitative reduction targets and the dissemination of inspection results via press releases.

-

Five megastores and two bakery franchises (agreements signed in 2010 and 2012, respectively), which agreed to reduce the use of disposable plastic bags and promote the use of shopping baskets, volume-based garbage bags and packing containers instead.

-

Large-scale distributors of farm products and civic groups, which agreed to reduce the use of accessory product packaging for agricultural and fishery products (e.g. paper bands and ribbons on fruit gift baskets for Chuseok), and to increase the use of reusable packaging materials (agreement signed in 2011, expanded in 2013).

-

The cosmetics industry, which signed an agreement on a pilot project to reduce the packaging of cosmetics containers and increase the use of refillable containers.

5. Promoting recycling

Recycling is promoted through various channels and instruments. The target groups are consumers, manufacturers, construction firms and importers. Target waste types and products for which recycling is mandatory include food waste, product packaging materials (paper, glass, aluminium, synthetic resin), batteries, lubricants, tyres, fluorescent light bulbs, WEEE and vehicles. Many measures that address recycling at the end of products’ life also encourage changes in their design and processing, including reduction of toxic contents.

Recycling is further supported through investment in recycling and clean production technology, and through government support for the construction of recycling facilities. The development of markets for recyclable products and materials is encouraged by the GPP system, which has been extended to all government institutions (Chapter 3), and by green purchasing by consumers and an online trading system for recycled and recyclable materials and products open to businesses, waste operators and households.

5.1. Separate collection and recycling of municipal waste

Waste recycling and separate collection by households and small businesses is encouraged by volume-based fees on the collection of non-recyclable waste and food waste, associated with free separate collection services; and by the extended producer responsibility system. Recyclable waste is collected separately through door-to-door collection, local recycling centres and take-back systems. Free pickup services are provided for large waste home appliances covered by the producer responsibility system.

Real estate developers have to install proper on-site waste collection equipment or pay the local government for such equipment and its operation. Since 2010, local governments have been obliged to install and operate recycling centres to promote trading in second-hand goods and recycling of large reusable waste items; 136 such centres are currently in operation. Private collectors often establish separate waste collection contracts directly with multistorey buildings or apartment blocks, which enables them to sell the recyclable material collected to recycling businesses at reduced operating costs.

The performance of the separate collection of municipal waste has improved over time for major waste streams. Recovery rates are close to 60% and have grown steadily over the past decade. This led to the provision of more and higher quality material to recycling businesses, and an increase in the amount of recycled products and secondary raw materials available on the market.

5.2. Extended producer responsibility

Korea was among the early adopters of extended producer responsibility. Its system is well established and legally based, and is supported by solid monitoring and enforcement. The legal obligations for waste recycling lie with producers, but the system requires shared duties between all stakeholders (e.g. consumers, local governments and the central government) (Figure 4.7).

Source: Based on Yong-Chul Jang, Chungnam National University, presentation on 10 March 2016 at 3R Conference, Hanoi.

The extended producer responsibility system was introduced in 2003 and its scope broadened progressively. Initially, it was limited to selected products (batteries, tires, lubricants), packaging containers (e.g. paper packs, glass bottles, metal cans, synthetic resin packaging) and selected electric and electronic equipment. Since 2004, products such as fluorescent lamps, styrofoam floats and additional types of packaging materials have been added. In 2014, the range of electric and electronic products covered was further expanded and associated with a special target management system. In 2016, the system covered 43 different types of packaging container and product categories. Products subject to the ADF are integrated into the producer responsibility system as their recyclability and associated recycling processes evolve.

Recycling methods and standards are specified in the enforcement regulation of the recycling act and in the Eco-Assurance Act, which applies to WEEE and to vehicles. The Eco-Assurance Act also controls the use of hazardous substances and encourages design for environment (DfE); it is the Korean equivalent of the European Union directives on Restriction of Hazardous Substances and WEEE.

End-of-life vehicles are managed under a partial extended producer responsibility system that encourages carmakers to use environment-friendly materials in vehicles’ production and facilitate their recycling at the end of their life. A specific Vehicle Eco-Assurance System (EcoAS), using the principle of producer responsibility, was introduced in 2008 for cars, vans and small trucks. It imposes recycling obligations, covering the vehicles’ life cycle, on vehicle manufacturers, importers, dismantlers and scrap recyclers, and provides standards and guidelines on how to meet the obligations. The recycling target was set at 85% in 2008-14, and increased to 95% in 2015. The system produces good results; more than 85% of targeted vehicles are recycled. However, the obligation only concerns cars, vans and small trucks; it could be usefully expanded to other vehicles, such as buses and larger trucks (above 3.5 tonnes), now exempted.

Mandatory recycling rates, fees and take-back systems

The MOE sets a mandatory recycling rate for each product category annually; it is associated with sanctions in case of non-compliance. The rates are designed to increase over time and are defined through consultation with stakeholders and experts. For each category the rate is calculated on the basis of quantity produced, quantity previously recycled and national recycling capacity. It is adjusted to take into account developments in recycling technology, product life cycle, etc. To give manufacturers a longer-term perspective and help them plan their recycling activities, since 2008 the annual targets have been accompanied by longer-term (five year) recycling targets (Table 4.3).

Under extended producer responsibility, producers and importers with recycling obligations pay a recycling fee to a Producer Responsibility Organisation (PRO)6 that collects and recycles the used products or packaging materials and manages the fees. Allotments are distributed among the members of the PRO according to the mandatory recycling quantity assigned to each producer. Until 2013, seven PROs were operating; then the MOE merged the six packaging PROs into one, the Korea Packaging Recycling Association, to reduce administrative costs.

The fees paid by producers fully cover the PROs’ costs for collection, treatment and administration. A large share of the fees comes from food manufacturers, retailers and producers of cosmetics, and the plastic packaging industry. The revenue generated and the way funds are used differ among the PROs. Each PRO decides how and to whom to distribute the funds. A majority (70-90%) of the fees are used to remunerate recyclers, and about 1-5% are used for information and awareness-raising campaigns.

Compliance and enforcement

KECO, a public entity under the MOE, monitors producer compliance. Producers, importers and recycling firms are obliged to record the recycling process online in Allbaro, including amount of waste collected, amount recycled and recycling methods used. KECO checks the records through on-site inspection. Waste that is treated and recycled in an unauthorised facility does not count towards fulfilment of the producer’s responsibility.

When a producer with a recycling obligation fails to comply or when a PRO fails to fulfil members’ obligation, the MOE imposes payment of the recycling cost of the unmet portion, plus a surcharge of up to 30%. When a producer exceeds its targets, the amounts that surpassed the targets can be used for the following two years.

Producers of items covered by extended producer responsibility, other than electrical and electronic equipment, with yearly output of less than KRW 1 billion, along with importers with imports of less than KRW 300 million, are exempt from the fees.

Results

Overall, the system performs well. The number of producers with recycling obligations and recycling businesses has been growing. The ratio of producers per recyclers rose from 6.6 in 2003 to 7.3 in 2012. Recycling rates for products such as packaging and tyres increased significantly (to 74% and 62%, respectively, in 2012). The total amount of recycled waste products and packaging materials grew by more than 60% (from 938 000 tonnes in 2002 to 1.52 million tonnes in 2012), and the total amount of products recycled under the producer responsibility system increased by 70% (from 928 000 tonnes to 1.16 million tonnes). This represents cumulative savings in landfill costs of KRW 2.89 trillion, and cumulated revenue of KRW 3.05 billion from selling the recycled materials, as well as the estimated creation of up to 9 769 jobs over ten years. Positive effects are also seen with respect to DfE improvements for consumer electronics (Table 4.4).

Progress is slower for products such as household fluorescent light bulbs and batteries, cardboard, packaging materials – particularly styropore and plastics used in farming and fishing – and small consumer electronics, whose recycling rates, though increasing, remain low compared to the sales and the stocks in use. This leaves room for further progress. The capacity of Korea’s recycling facilities is large enough to process 100% of all extended producer responsibility target products plus other products that could be integrated in the system.

At the same time, Korea has a large informal recycling sector composed of very small family-type firms that have traditionally been involved in scrap collecting and recycling. Given the importance of this sector, Korea would benefit from gaining better knowledge of the sector and integrating it into the formal recycling system – and possibly into the producer responsibility system. This could be done, for example, by creating a network or association in which informal recyclers would register as entrepreneurs who benefit from training and support, and who apply minimum recycling and safety standards to their activities. A useful first step would be to study the sector to better understand its functioning in terms of number of establishments and people involved, types of waste collected and pathways used.

5.3. Waste-to-energy policy

With a net import dependence of 87% for the primary energy supply (Chapter 1), further development and use of new and renewable energy sources is crucial for Korea’s economic development. The government plans to increase the share of renewables in total primary energy supply from 3.2% in 2012 to 20% by 2050. An important part of the planned increase is expected to come from the use of waste as fuel (residual heat from waste incineration, landfill gas, biogas, solid refuse, etc.).

A set of Measures for Energy from Waste Resources and Biomass was released in October 2008, followed by an implementation plan in July 2009. Their objective is to increase by 2020 the shares of combustible and organic waste that are recycled as an energy source to 90% and 36% respectively (compared to 1.5% and 2% in 2012). The government particularly encourages the production of solid refuse fuel (SRF) from combustible waste, the establishment of SRF power plants and the upgrading of power plants to generate electricity using biogas from organic waste. This is supported by an SRF Product Information Management System that was set up in late 2010 to promote exchange of information between manufacturers and users (www.SRF-info.or.kr, in Korean).

To facilitate implementation of waste-to-energy measures, legal provisions were or are being amended. One example concerns sewage sludge, whose dumping at sea was banned in 2012. An amendment now enables its use as fuel in coal-fired power plants and combined heat and power plants. Other examples concern the supply of biogas through city gas lines and the development of production standards for biogas used as a vehicle fuel. Other amendments concern the raw materials, manufacturing processes and quality standards for producing SRF, which allow the use of combustible waste to produce SRF (originally forbidden under the Waste Control Act). Since 2014, SRF imports have been legal.

Government financial support for waste-to-energy facilities has been gradually increasing since 2007 (in 2014, about KRW 105.3 billion of financial aid was allocated to such facilities). Twelve SRF manufacturing facilities and boilers are in operation (including in Wonju and Busan), and eight are under construction. Ten plants converting organic waste, including food waste, to biogas are in operation (among them one at the Sudokwon Landfill site in Incheon and one in Seoul), and eight such plants are under construction (in Busan and Daejon).

The policies and support measures put in place by the government are showing initial results. The ban on direct landfilling of food waste (2005) and the development of new measures and technology for the use of biogas have contributed to these results. In the first half of 2015, domestic production of SRF totalled about 770 000 tonnes, imports 130 000 tonnes and consumption 880 tonnes. This represents increases of 36-63% from the previous year.

The further success of the waste-to-energy policy will depend on factors including the evolution of oil prices (currently very low), the level of economic activity (now slowing), the solidity of the SRF market and public acceptance of SRF facilities. Despite the government’s awareness-raising efforts and compensation, local opposition to construction of such facilities remains high in some areas. Further success will also depend on developments concerning waste-to-energy technology and improvement in the quality of recovered combustible waste. So far, the production costs of converting waste to energy have been much lower than that of solar power (by 10%) and wind power (by 66%), but the waste-to-energy processes currently in use have been criticised for low energy efficiency because combustible waste is less efficient than other energy sources.

There are also potential conflicts between the objective of maximising use of waste as a resource for energy production (waste-to-energy policy) and that of maximising material recovery through improved recycling and reduction of waste. Many waste materials can be used for both purposes. Little information is available to assess and compare the life cycle-wide costs and benefits of the two approaches and identify optimal uses for the various waste streams.

6. Promoting recycling markets

Markets for recycled products are encouraged by a recycling market support programme targeted at SMEs, the GPP system, which has been extended to all government institutions, and an online trading system for recycled and recyclable materials and products that is open to businesses, waste operators and households. They are further supported by measures that encourage green purchasing by consumers.

6.1. Recycling market support for SMEs

A recycling market support programme provides long term low interest loans to recycling businesses to support facility installation, management stability and technology development. The programme targets SMEs whose annual average sales in the two previous years did not exceed KRW 30 billion. Between 1994 and 2015, 2 996 companies benefitted from the programme and a total of KRW 1 241 billion was lent (Table 4.5).

The programme has increased the recycling efficiency of the targeted SMEs. Efforts are also being made to prevent potential environmental harm from recycling. Progress in the past few years has slowed, however; further improvement in recycling performance was hampered by the number of legal restrictions concerning the materials whose recycling is allowed. The recent revision of related provisions in the Waste Control Act and implementation of the Framework Act on Resource Circulation are expected to give new impetus to the programme.

6.2. The recyclable resources marketplace

To further encourage recycling, curb waste generation and divert valuable resources from landfill and incineration, in 2013 Korea introduced an online market for recyclable resources, a customised and web-based trading system (or marketplace) for users and suppliers of recyclable materials and reusable products. The system is open to businesses, public waste operators and households (private persons). It focused first on waste material (e.g. waste synthetic resins7), used furniture, home electronics and baby products. Since 2015 it has covered used machines and equipment, semi-processed goods and any other recyclable or reusable material or good. The system is being connected to information from the Allbaro system to avoid duplicating registration of items, but more could be done to fully exploit the synergies between the two systems.

Suppliers register information about the type of waste material or used product available, its composition and its properties (quality, quantity); users use this information to find and purchase optimal products. Four types of trading operations are in service: i) matching system, ii) auction, iii) group purchase and iv) ordinary trading, in which a consumer can personally search for and buy products. In 2014, a help desk providing liaison between waste collectors and waste treatment firms, a GIS-based search function and an electronic bidding tool were added to the system. In 2015, regional distribution centres were established to reduce the costs of logistics.

Users include the 800 000 business operators that generate, transport and treat waste, as well as local government recycling centres and citizens (mainly for used home electronics and furniture). In 2013, the market had 53 635 registered users, 44% being individuals and 56% businesses. By the end of 2014, the system had registered around 690 000 trades. The most traded resources were waste synthetic polymer compounds, recyclable raw materials, recycled aggregates and abandoned metal; the resources with the highest transaction values were oil, synthetic polymer compounds, metal and board.

The government plans to make greater use of this system to stimulate demand and create new markets for reused goods and recycled materials, in line with the introduction of landfill and incineration charges in the framework of the new law on resource circulation. It also plans to initiate trading of purchased but unused goods owned by the government, including the Public Procurement Service (PPS).

Despite these very positive measures, recycling markets remain weak. They suffer from a general mistrust in the quality of recycled materials and reused products. And in recent years, low oil and raw material prices have undermined their effectiveness, making it difficult for recycled products to compete with new products. Strengthening the recycling markets to make them more resilient against the volatility of commodity prices and stimulating demand for recycled goods beyond the public sector are essential. To achieve this, the government needs to strengthen action at the following levels.

-

Restore trust in recycled goods, for example through well-targeted information campaigns and expanded use of quality labels for recycled goods.

-

Guarantee high quality in recycled goods by informing recyclers about the material content of recovered products, developing minimum quality standards and creating incentives for upcycling waste into high-value products. A first step has been taken with the creation of a quality certification system for materials recovered after intermediate treatment or from recycling processes (e.g. used organic solvent, used moulding sand, animal residues, sludge, waste acid).

-

Continue developing external markets and strengthening bilateral and multilateral co‐operation on resource circulation and the 3Rs.

6.3. Green purchasing by the public sector

Measures to improve recycling markets and move towards a circular economy are further supported by the government’s green public procurement system. The Act to Promote the Purchase of Environment-friendly Products (2004) makes it mandatory for public institutions to buy such products. It is complemented with a basic plan on promoting the purchase of green products (2005). Since 2006, the scope of the GPP system has expanded considerably and today it covers all government institutions.

Environment-friendly or green products are those that have received environmental certification, such as the Eco-Label in existence since 1992, or the Good Recycling (GR) mark launched in 1997. These products are given preferential treatment. For example, they are exempt from the eligibility evaluation when the PPS issues calls for tender for Multiple Award Schedule (MAS) contracts,8 they are selected as procurement excellence products, and they receive bonus points in other eligibility assessments. By the end of 2015, 15 060 products had been granted Eco-Label certification and 229 products GR-mark certification.

In addition to products certified as “green”, PPS has identified 100 products that meet a “minimum green standard” and whose purchase is mandatory. They were selected based on life-cycle costing, taking into account factors linked to energy efficiency, standby power or recycling.

As a result, the volume of GPP rose from KRW 255 billion in 2004 to KRW 862 billion in 2006 and KRW 2 402 billion in 2015, representing 8% of total public procurement.

6.4. Green purchasing by consumers

The government also encourages and supports efforts in the private sector to expand the availability of green products to consumers, mainly through voluntary agreements between the MOE and private firms. Examples include the establishment of green product corners at large retailers (373 retailers, or 97%, participated in the project, launched in late 2007). Other examples include guidelines for green purchasing and training for green purchasing target management. Green purchasing is further supported by civic groups, such as the Green Purchasing Network.

To encourage environment-friendly behaviour, a Green Credit Card programme was created by the Korean Environmental Industry & Technology Institute and the MOE with private sector backing in July 2011 (Chapter 3). It rewards environment-friendly behaviour by consumers and users of public services such as water and energy, the use of public transport and the purchase of environment-friendly goods. The rewards come in the form of points that can be used to buy products or services, be exchanged for cash or be given as donations to environmental funds. Uptake of the card exceeded expectations; there are more than 10 million users where 3 million were originally expected – equivalent to about a fifth of the population. At the same time, eco-related sales increased significantly, by 160% from 2013-14.

7. Improving the environmental effectiveness of waste disposal and management

Waste disposal

Waste disposal by municipalities and industry has improved considerably since 2006. All substandard landfills have been upgraded thanks to a programme comprising application of leak prevention materials, construction of advanced leachate treatment facilities and thorough soil covering. Soil quality in and around landfills is controlled through regular monitoring and inspection, along with through impact assessments in neighbouring areas. Additional regular inspections are carried out to detect and prevent soil contamination in controlled landfills of capacity of over 10 000 m3 and commercial landfills of capacity of over 150 000 m3. After closure, monitoring of leachate, gas emissions, and ground and surface water quality continues for 30 years, during which use of the site is restricted.

Korea has been particularly successful in managing its large landfill sites and converting them gradually into eco-industrial leisure complexes. A prominent example and model case is the Sudokwon Landfill in Incheon, whose management model and know-how have been exported to other countries. Today, the Sudokwon site features, beside its remaining landfills, a range of activities, including an eco-energy town, natural areas, sports fields, a golf course and flower gardens, and is a venue for cultural and sporting events (Box 4.2).

The Sudokwon Landfill Site is the world’s largest landfill, covering 20 square kilometres. Established in 1990 on land reclaimed from the sea, the site uses advanced, high-tech waste management technologies to treat every day about 20 000 tonnes of waste from households, construction sites and businesses from the Seoul Metropolitan Area where about 40% of the national population lives.

The “Dreampark” is a project initiated in 2000 by Sudokwon Landfill Site Management Corporation (SLC) to convert its used landfill sites into an ecological leisure and education space that can be enjoyed by local residents and international tourists alike. A sports park for local residents encompassing a soccer field, basketball court, tennis court, athletics track and more is already available, as are a flower garden, a botanical garden and a greenhouse for tree seedlings. In partnership with local residents, 5.3 million trees have been planted at the site; the goal is to reach 10 million. The Dreampark cultural classes programme, established in 2012, offers classes in fashion, traditional music, yoga, etc. A horse riding centre, swimming pool and golf course, constructed for the 2014 Asian Games, are now open to residents. A trekking course, campsite, nature observation zones, theme park and more are under construction or planned for the near future. The Dreampark is a place where visitors can learn both about nature and about waste management and recycling, for example during the annual Dreampark Festival. Beyond providing leisure and educational amenities, the Dreampark is expected to stimulate the local economy by creating jobs, increasing land prices and attracting investment. About 400 000 local jobs have been created to date.

SLC actively pursues waste-to-energy projects. The complex houses a “Waste-to-Energy Town” bringing together facilities to treat and recycle household food waste, construction waste, sewage sludge and more while simultaneously using some of the energy by-products and selling others. To date, 2.96 billion kWh of electricity has been generated by the landfill gas power plant, equivalent to about USD 33 million in electricity revenues per year. SLC also recycles sludge to create solid fuel, which is then sold to thermal power generation plants. Projects to produce biogas from food waste and SRF from construction waste are in the pipeline.

Source: SLC (2015), “Waste to Energy, Landfill to DreamPark”.

Small- and medium-sized incinerators are controlled twice a year through joint visits by local authorities and inspectors, during which the existence and performance of pollution prevention equipment is checked. Small incinerators with improper pollution prevention systems are being progressively shut down. Very small incinerators, however, are inspected less frequently (every three years) and continue to raise concerns about their environmental impact. And the use of best available technology is not mandatory for waste incinerators that are subject to the new integrated permitting system for polluting facilities.

Direct landfilling of untreated waste and incineration without energy recovery still exist. It is estimated that half the waste going to final disposal (about 8% of the amount generated) contains materials that could be recovered.

Illegal dumping