Chapter 3. Green growth1

Estonia is pursuing an ambitious green tax reform, operates several support schemes to stimulate green investment and has a growing environmental goods and services sector. However, vehicle taxation is limited, and pollution taxes are too low to have an impact on environmental performance of firms. This chapter presents Estonia’s progress in using economic and tax policies to reach environmental objectives. It analyses public and private investment in environment-related infrastructure and reviews the promotion of environmental technologies, goods and services as a source of economic growth and jobs.

1. Introduction

Estonia is a small and open economy. It experienced strong growth after its accession to the European Union (EU) in 2004, followed by a sharp contraction due to the global financial crisis (OECD, 2012a, 2011). The economy rebounded quickly, with an export-led recovery. Gross domestic product (GDP) rose in real terms above pre-crisis levels in 2015. Unemployment has fallen to 6%, below the OECD average of around 8%, but skill mismatches keep structural unemployment high (OECD, 2015a).

Estonia’s fiscal position is strong, and the government is initiating further substantial reforms. The country has a large potential for improving productivity, but the productivity gap compared to high-income countries has been slow to narrow (Kappeler, 2015) for several reasons. Low foreign direct investment inflows in high value-added activities, a focus on low value-added manufacturing and limited knowledge transfer from domestic research institutions and foreign firms to Estonian firms have all contributed to the productivity gap. Transport infrastructure has been upgraded, but bottlenecks remain. The government is reforming a number of areas (e.g. labour market, research and development), which can help strengthen growth (Chapter 1).

Estonia faces challenges in moving to a more environmentally sustainable economic model (OECD, 2015a). Within the OECD, Estonia’s economy is the most greenhouse gas intensive and carbon intensive, and among the most energy intensive (Annex 1.A1; Annex 1.B1; Annex 1.B2). This is largely a result of the dominance of oil shale as an energy source (70% of supply). Under existing policies, income growth will continue to increase greenhouse gas (GHG) emissions. Given that over two-thirds of its emissions fall under the EU Emissions Trading System (ETS), potential increases in the ETS carbon price could have a larger economic impact in Estonia than in other European countries.

2. Framework for sustainable development and green growth

Estonia’s National Strategy on Sustainable Development, “Sustainable Estonia 21”, adopted in 2005, sets out the government’s framework for pursuing social, economic and environmental objectives, as well as preserving the viability of the Estonian cultural space. The strategy is implemented through various sectoral strategies and action plans, with progress monitored via a set of sustainable development indicators. The latest monitoring report shows progress towards several targets for improving economic welfare and environmental quality (Statistics Estonia, 2015). Estonia’s Sustainable Development Commission is reviewing the Sustainable Estonia 21 strategy to analyse to what extent it complies with the UN Agenda 2030 goals. Based on this review, the government will decide whether to renew the strategy.

The 2007 Estonian Environmental Strategy to 2030 defines long-term development objectives and identifies the most problematic areas in the field of environment. The Environmental Strategy was complemented by an Environmental Action Plan for 2007-13 in line with the EU programming period (as it relied extensively on European structural funds for implementation). However, the plan was not renewed after 2013. Therefore, it is unclear how the Environmental Strategy objectives will be achieved by 2030.

There is no dedicated green growth strategy, but green growth initiatives are included in various governmental strategies and plans. The Entrepreneurial Growth Strategy 2020 includes “more efficient use of resources” as one of its priorities, but is not specific about attaining it. The Estonian government has an ambitious agenda for a green tax reform for the coming years. It aims to shift part of the tax burden from income to consumption, use of natural resources and pollution of the environment. At the same time, it aims to keep the tax system simple and transparent with as few exceptions and differences as possible (Ministry of Finance, 2015). Authorities have launched a multi-year process involving relevant ministries, stakeholders and academia to inform the effort of revising the structure of environmentally related taxes. The project will assess external costs of all main forms of pollution with the intent to adjust environmental taxes so that they better reflect assessed values. The project is expected to finish in 2017, with changes to the tax system made by 2020.

Reducing the high carbon intensity of the energy sector is a priority for Estonia, but progress has been limited. In 2017, the Ministry of the Environment is expected to adopt the General Principles of the Climate Policy until 2050. This is in line with the Paris Agreement and the EU long-term climate and energy objectives for 2050. After 2020, Estonia intends to reduce GHG emissions by 70% by 2030 compared to the 1990 level. This target is significantly more ambitious than that of the EU’s Nationally Determined Contribution under the United Nations Framework Convention on Climate Change (UNFCCC).

The Ministry of Economic Affairs and Communications has recently developed a new National Development Plan of the Energy Sector until 2030. It aims to ensure an energy supply at a reasonable price for consumers with an acceptable environmental impact, in accordance with the long-term energy and climate policies of the EU.2 The plan includes benchmarks for renewable energy and energy efficiency operational programmes and general goals for thermal insulation of buildings. However, it does not incorporate a vision of minimal reliance on fossil fuels in the context of achieving GHG emission reduction by 2050 and beyond.

3. Towards greener taxation

3.1. Overview

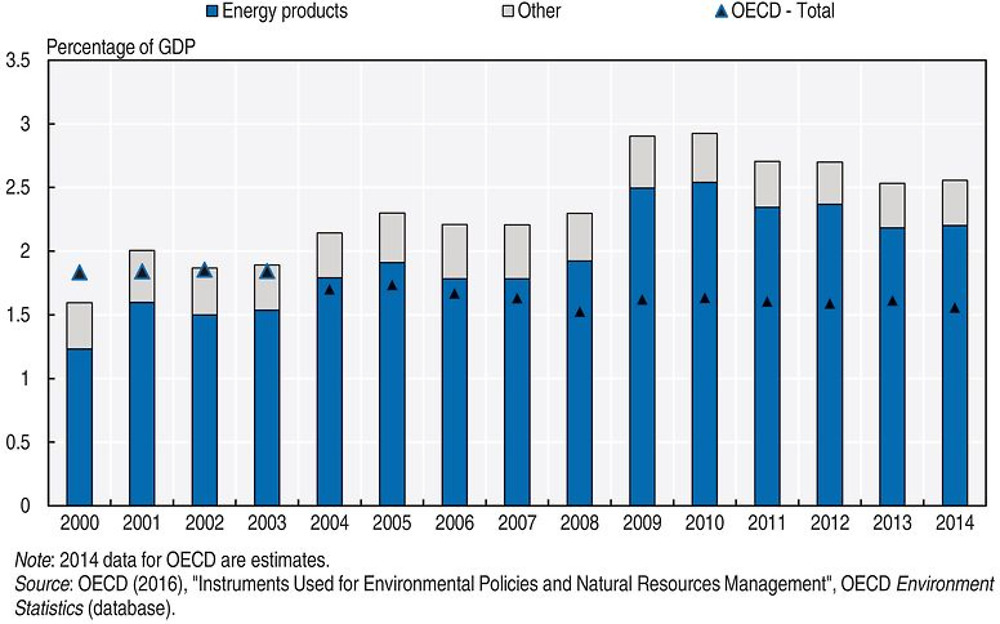

Revenues from environmentally related taxes increased from 1.6% to 2.6% of GDP between 2000 and 2014, mostly due to increased excise taxes on petrol and diesel; this puts Estonia in the upper third of OECD member countries on this indicator (Annex 3.A). Environmentally related taxes raised a significant amount of tax revenue, accounting for 8% of total tax revenues in 2015, up from 5.2% in 2000 (OECD, 2016a) and above the OECD average (Basic Statistics).

In 2014, taxation of energy products made up 86% of revenues from environmentally related taxes, well above the OECD average of about 70%. The overall increase in environmentally related tax revenue was due mainly to a significant increase in energy tax rates between the mid-1990s and 2010. A new excise tax on electricity was also introduced during this period. The increases were driven by both the requirement to increase some tax rates to at least the minimum levels prescribed by the 2003 EU Energy Taxation Directive, as well as the government’s green tax reform agenda. New energy tax rates were adopted by Parliament for 2010-15, partly in response to the 2009 fiscal crisis (Hogg et al., 2014). Since 2010, revenue from energy taxes as a share of GDP has declined (Figure 3.1).

In OECD member countries, taxes on motor vehicles and transport are, on average, the second most important category in terms of revenue as a share of GDP. For Estonia, however, these taxes are modest, raising an amount equal to just 0.06% of GDP in 2014. Estonia is one of the few EU Member States that does not tax passenger cars, despite road transport being a significant source of air pollution and CO2 emissions (Chapter 1).

Since 2005, Estonia has been implementing a green tax reform, whose goal is to increase taxation of pollution and other negative environmental effects while decreasing labour taxes. Raising environmentally related taxes could indeed give the government leeway to lower labour taxes that may be putting a brake on growth and employment, as the tax burden as a percentage of labour cost (the so-called tax wedge) in Estonia is higher than the OECD average (OECD, 2015a). The rates of environmental taxes3 have been increased, while the rate of personal income tax was reduced from 26% to 21% between 2005 and 2012 (Oras and Salu, 2013). Total tax revenues compared to GDP have varied considerably over this period, increasing from almost 30% to about 35% between 2005 and 2009, and declining again to less than 33% in 2014. The green fiscal reform should be pursued further.

The design of the environmental tax system has recently been the subject of active study and debate. In 2013, in the context of the government’s review of environmental taxes, the government commissioned the Stockholm Environment Institute (SEI) in Tallinn and the Tartu University Social Science Research Centre to assess the impact of environmental taxes in Estonia. The study, which examined the use of these instruments over 2000-10, recommended increasing environmental tax rates by up to 5% per year over 2016-30 (Lahtvee et al., 2013). The additional revenue could compensate for inflation and motivate resource-use efficiency, as well as eliminate existing exemptions (discussed below). For the oil shale extraction tax, the study proposed a 16% nominal rate increase annually over 2016-30, starting from the 2015 level. It also proposed to significantly increase tax rates for oil shale-related waste (Chapter 4).

3.2. Taxes on energy products

Tax rates on energy in Estonia are rather low and vary considerably across energy sources and uses. There is broad scope to increase and adjust energy tax rates, which do not reflect well the negative impact of energy use on the environment and fail to provide a consistent carbon price signal.

Estonia taxes most energy products, although there are a number of exemptions and reduced rates for various users. An excise duty is levied on all energy products, except for peat and wood, which are important sources of local air pollution. Energy taxes on petrol and diesel are well above the minimum tax rates prescribed by the 2003 EU Energy Taxation Directive,4 and future rate rises are planned. However, there are several exemptions and reduced rates for specific uses of fuel, such as agriculture and fisheries5 (OECD, 2013a). These exemptions weaken incentives to use energy efficiently and result in tax revenue losses.

Estonia implemented a CO2 pollution tax in 2000. Initially, it was applied to large energy producers with a total thermal capacity greater than 50 MW. With the entry into force of the Environmental Charges Act on 1 January 2006, the tax was applied to all power plants, regardless of size, duplicating the coverage of the ETS. The tax rate gradually increased from EUR 0.32 to EUR 2 per tonne of CO2 from 2009 onwards. The effect of this measure on inducing carbon abatement was likely negligible given the low level of the tax rate; the tax is primarily intended to raise revenue (OECD, 2012b). However, companies can opt to invest the payable amount in low-carbon technologies instead of paying the tax, which most energy producers do (Kearns, 2015).

A tax on electricity generation was abolished in 2008 and replaced by an electricity excise duty (EUR 4.47 per MWh, as of 1 January 2014). Companies that control the power networks pay this tax, but the excise duty is unrelated to the emission intensity of the fuel used in the production of electricity. Thus, fuels with lower carbon content are subject to a relatively higher tax per tonne of CO2, which provides no incentive for switching to less carbon-intensive fuels. The CO2 pollution tax still remains in place for heat generation (OECD, 2012b).

Estonia also has a “renewable energy tax” levied on electricity consumers to finance the feed-in premium subsidy for renewable energy (Section 4.2). It is paid by all consumers in Estonia in proportion to their consumption. The renewable energy tax is listed separately on electricity bills so that consumers can see exactly how much is paid. The rate of the tax is set under the Electricity Market Act (2007). The tax for 2015 was 1.07 EUR cents/kWh, including VAT (Elering, 2015).

As in most OECD member countries, petrol is taxed at a higher effective rate than diesel. This is regrettable from an environmental perspective as diesel emits more CO2 and local air pollutants, including NOx and PM, than an equivalent volume of petrol. Moreover, Estonia’s petrol and diesel prices are among the lowest in OECD Europe, although Estonia’s taxes on diesel have been rising faster than those on petrol. Taxes represent just over half of the end-use price of petrol, among the lowest rates in OECD Europe. Despite numerous increases in fuel taxes up to 2010, emissions from cars have not lowered noticeably; newly registered cars in Estonia still have high average CO2 emissions (EEA, 2014).

As a result of exemptions for biomass and for natural gas not used for heating, just over half (56%) of the energy use for heating and process purposes and 55% of CO2 emissions from such uses are untaxed (OECD, 2013b). Despite increases in taxes on natural gas and fuel oil, tax rates on fossil fuel use in heat and electricity generation (based mostly on oil shale) remain much lower than those on transport fuels. This difference is more pronounced than in many other OECD member countries. Natural gas is taxed only when used for heating. The use of biomass, biofuels, coal or liquefied petroleum gas is exempt from taxes if used for heating (OECD, 2013b).

There is a low effective tax rate (in terms of energy content and CO2 emissions) on oil shale – the dominant energy source for electricity generation and the largest source of CO2 emissions. The coverage of electricity generation by the EU ETS may partly explain the low effective rate for it. However, the use of oil shale is responsible for a number of other negative environmental impacts, including those on air quality (Chapter 1), which calls for a higher tax on it. In its recent audit (NAO, 2014a), the National Audit Office concluded that environmental taxes on oil shale use failed to motivate companies to prevent or reduce potential environmental damage (Chapter 5).

To provide a consistent carbon price signal, tax rates for CO2 emission sources not already covered by the EU ETS should be raised in accordance with their carbon content, to the extent that taxes already levied on these sources do not already reflect the social costs of carbon. This can be done gradually, taking into account the need to compensate the potential impact on low-income households.

3.3. Carbon pricing via the EU Emissions Trading System

In addition to the implicit and explicit carbon taxes described above, Estonia is pricing some of its GHG emissions via the EU ETS, which covers 71% of the country’s GHG emissions – the highest share of any EU country. These emissions are generated by 46 stationary installations and three entities in aviation (EEA, 2015). Power and heat generation in Estonia is responsible for more than 80% of all ETS-regulated emissions (IEA, 2013).

In its early stages, the EU ETS allocated nearly all emission allowances for free. In the first two trading periods (2005-12), Estonia was granted emissions allowances of around 19 million tonnes (Mt) of CO2 per year – more than the actual emissions from sectors covered by the ETS. In the third period (2013-20), it was granted 13.3 Mt per year, 30% less than in the previous period (IEA, 2013), but still representing about 98% of Estonia’s verified emissions (EEA, 2015). From 2013, an increasing share of emission allowances is being auctioned (Box 3.1). However, Estonia, like some other economies in transition, was eligible for temporary exemptions from auctioning by developing a national plan of investments in modernising power generation. As a result, the ETS has so far had no effect on the dominance of oil shale in the country’s energy mix.

The EU ETS is in its third phase (2013-20), having undergone significant changes from the second phase. It now covers CO2 emissions from petrochemicals, ammonia and aluminium; N2O emissions from the production of nitric, adipic and glyocalic acid; and fluorocarbons emissions from the production of aluminium. There has been a transition from a system of national caps to a single, EU-wide cap that will decrease by 1.74% per year until 2020 (due to the decreasing cap, emissions in the sectors covered will be 21% lower in 2020 than in 2005).

The share of auctioned allowances has increased from less than 4% in Phase II to more than 40% in Phase III. In the coming years, the amount of freely allocated allowances will decrease gradually each year until 2020; at that time, only the trade-exposed, energy-intensive manufacturing industry will receive free allowances. In the interim, allocation rules have been harmonised based on performance benchmarks for the remaining free allocation of allowances.

Source: OECD (2015f).

The NAO found that the government had not sufficiently used the ETS to encourage GHG emission reductions: companies that received allowances exceeding their actual emissions during the first commitment period did not use money gained from the sale of allowances for environmental investments (NAO, 2009). It has been estimated that companies earned substantially from sales of allowances in the first commitment period. For example, Eesti Energia (the state-owned energy company) received EUR 179 million from such sales, which was transferred to the state budget (NAO, 2009). During 2005-10, the use of gas in electricity production, in fact, was cut in half, indicating the EU ETS did not encourage a fuel switch from oil shale to gas (OECD, 2012b).

Since the ETS covers a large portion of the country’s GHG emissions, the Estonian economy is vulnerable to increases in the allowance prices of the ETS, which would make high GHG emissions very costly in the future. A study by Ernst and Young (2014) of the macroeconomic impacts of Estonian oil shale mining and production identified CO2 price (along with oil prices and changes in environmental tax rates) among the main risks to the sector (Chapter 5).

In total, Estonia priced 80% of its CO2 emissions from energy use in 2012, and 17% were priced above EUR 30 per tonne of CO2 (OECD, 2016e). This can be clearly seen on Figure 3.2, where the tax rates and prices of emission allowances for various energy sources have been converted into effective carbon rates, taking into account the average carbon content of each fuel.6 For example, about 58% of industrial sector emissions are subject to a tax of EUR 5 per tonne of CO2, two subsectors are covered by the ETS at EUR 7 per tonne and about 28% of the sector’s carbon emissions are not priced at all.

3.4. Distributional issues of energy taxation

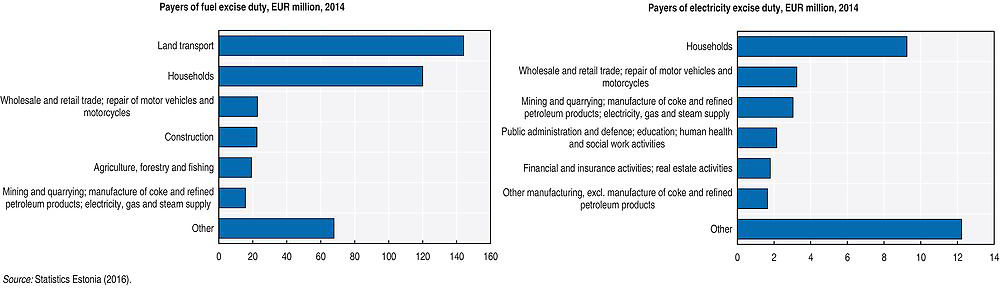

Households bear a significant share of the tax burden on fuel and electricity. As shown in Figure 3.3, households, together with land transportation businesses, paid two-thirds of the total amount of fuel taxes in 2013. Households also paid a significant share of the electricity excise duty in 2013. A recent study looking at the distributional effects of energy taxes in Estonia suggests that, overall, such taxes are progressive (Poltimäe, 2014). In the mix of energy taxes, the progressive effect of the motor fuels excise outweighs the regressive impact of electricity excise duty.

Compared to other EU countries, Estonia has one of the highest energy consumption levels per capita (INSIGHT_E, 2015), driven in part by low energy prices. While households benefit from these low prices, the large energy use increases their vulnerability to price increases. As energy costs rise, energy poverty may become a concern (Kappeler, 2015).

A study for the European Commission has estimated the number of households in energy poverty. It assessed how many households in each country spend double the national average energy share of household expenditure.7 The results show that Estonia has a relatively high incidence of energy poverty compared to most Western European countries, with almost 20% of the population affected. For comparison, several EU Member States, such as Estonia’s Baltic neighbours Latvia and Lithuania, as well as Ireland, Greece and Hungary, have energy poverty rates between 30% and 40%, while Romania is at almost 50% (INSIGHT_E, 2015). Only 3% of Estonian households are unable to afford to keep their homes adequately warm (EC, 2015).

Tackling the challenge of energy poverty requires a mix of instruments. These range from financial support to households for energy-savings investments (e.g. purchase of low‐consumption appliances) to regular adjustment of subsistence payments to account for changes in energy prices (e.g. due to increased energy taxes) (OECD, 2015a). There are no specific measures for integrating poverty and distributional concerns into environmental policy decisions in Estonia.

3.5. Transport taxes

There are few taxes on motor vehicles in Estonia. In 2014, revenue from these taxes amounted to 2.5% of environmentally related tax revenues, well below the OECD average. There is a heavy goods vehicle tax on vehicles weighing 12 tonnes or more, which was introduced in 2004. Tax rates correspond to EU minimum levels and vary according to the type of vehicle. There is also a car registration fee, which applies to personal vehicles and is based on either the type or origin of the vehicle.

Estonia should consider policy measures to better address the environmental impacts of road transport. These could include a road pricing system, a congestion charging system for Tallinn, or taxes on motor vehicles (either a purchase or annual tax, or both) adjusted to reflect the environmental characteristics of the vehicle. Well-designed measures would help reduce the high vehicle emissions of NOx and PM; they would also help meet the GHG emission target for non-ETS sectors, which Estonia is at risk of missing if no additional measures are taken.

The government is analysing options for vehicle taxation, including taxation of vehicle use based on environmental characteristics. It commissioned a study to identify road transport taxation options to help better implement the user pays and polluter pays principles. The study examined several taxation approaches, including time-based or distance-based road charging for trucks and an annual tax on passenger cars. It analysed the economic and technical practicality of various options and their potential socio-economic impact, but not the external costs of vehicle use (Ernst and Young, 2015). Based on this study, the government is planning to introduce road charges for heavy duty vehicles, but not taxes on passenger cars.

A road pricing system that varies with the time and location of driving and with vehicle category, combined with fuel taxes that reflect CO2 emissions caused by use of different fuels, is probably the optimal way of addressing negative social and environmental impacts from road transport. If that is considered difficult to implement, one-off and/or annual taxes on passenger vehicles can play a useful role if they vary according to emissions of local air pollutant of the vehicles, as is done, for example, in Israel (OECD, 2016f).

3.6. Other environmental taxes and fees

Estonia has had numerous environmental taxes in place since 1991, including resource extraction, pollution and water abstraction taxes currently regulated by the Environmental Charges Act (2006). Their revenues grew modestly in real terms (2010 prices) between 2005 and 2014. Most revenue comes from extraction and waste disposal taxes, both of which are related to oil shale mining and processing (Figure 3.4). As the largest source of pollution, the oil shale industry paid 72% of environmental taxes in 2013 (MoE, 2015a). Municipal wastewater treatment plants contribute about two-thirds of total water pollution tax revenues (MoE, 2015b).

Polluters can avoid paying all or part of pollution taxes if they invest the corresponding funds in a new project that will reduce pollution by at least 15% per product unit. However, according to the government, substitution (offsetting) of pollution taxes accounts for a small share (less than 1%) of the total revenue collected from these taxes.

Revenues from environmental taxes are shared between the state and local authorities within whose jurisdiction the given activity is located. Allocating a portion of the revenues to local authorities helps compensate for the environmental impacts imposed in that area. A part of these revenues channelled to the state budget is allocated to the Estonian Environmental Investment Centre (EIC) to finance projects to protect the environment (discussed below). In 2014, EUR 90 million in revenue was collected from environmental taxes and allocated to the EIC (EUR 36 million), the state budget (EUR 39 million) and local authorities (EUR 15 million) (MoE, 2015a).

Resource extraction

Mining companies pay a tax for extraction and use of mineral resources belonging to the Estonian state with the aim of capturing a share of their profits. Taxed minerals include oil shale, peat and a range of construction materials, such as dolomite, limestone, gravel and sand. These taxes should be based on the estimated value of the resource in the given mine or quarry, essentially amounting to a rent. However, no methodology for assessing the financial value of mines and quarries has yet been developed (MoE, 2014). By the end of 2017, the ongoing codification of environmental law is expected to have changed the procedure for calculating mineral extraction taxes (Chapter 2). In 2016, the extraction taxes for oil shale mining were significantly reduced to alleviate the burden on industry in the context of a dramatic drop in the market price of oil that made the transformation of oil shale into shale oil much less profitable. This tax break is inconsistent with the green tax reform pursued by the Estonian government (Chapter 5).

Air and water pollution

Pollution taxes, especially for air and water pollution, are imposed on a wide range of parameters, including numerous heavy metals and other hazardous substances. Emissions and discharges of most of these hazardous pollutants are not monitored. Rather, they are estimated based on technological characteristics of the production process, thereby removing the potential incentive impact of the taxes for these pollutants. Rates vary depending on the location of polluters (with polluters located in bigger towns and recreational areas paying more). A non-compliance fee, with rates of up to 100 times the basic rate, applies to emissions of air and water pollutants that either exceed permitted levels or are emitted without a permit (Chapter 2). All water users also benefit from a 50% discount on water pollution tax rates if their discharges stay below permitted effluent limit values, and if they submit self-monitoring reports on time. This, together with non-compliance rate multipliers, constitutes a double compliance incentive, which is hardly justified.

Since 2000, basic air and water pollution tax rates have increased significantly (Figure 3.5). However, they remain well below marginal abatement costs, making it preferable for polluters to pay the tax rather than to take abatement actions. Indeed, the impact of Estonian pollution taxes on the environmental performance of firms appears limited to date (NAO, 2014a). Yet the government is reluctant to raise rates further due to a concern about burdening industry and hindering investment. For greater effectiveness, air and water pollution taxes should focus on a limited number of priority pollutants whose emissions or discharges are monitored, and tax rates for these pollutants should be increased to provide a real incentive for their abatement (Box 3.2).

Pollution taxes levied on the quantity of pollution released into the environment can have two primary functions: changing environmentally damaging behaviour and raising revenues for the treasury. To achieve an incentive impact, polluters should be sensitive to production-cost changes represented by the pollution tax; the tax rate should be high enough to make pollution reduction cost-effective; and emission monitoring and payment enforcement should be strong. A fairly stable tax base with low administrative costs could provide a predictable revenue stream, which is why OECD member countries generally rely on product taxes rather than pollution taxes as a source of revenues.

Regardless of the primary purpose of a pollution tax, it must be levied only on pollutants that are routinely monitored. Pollution taxes that exist in Western European countries (e.g. Sweden, Denmark, Norway, Italy) are limited to a few pollutants. Those are usually SO2 and/or NOx for air emissions, and nitrogen, phosphorus and organic substances for wastewater discharges.

An analysis of the country’s main environmental problems and respective government priorities should guide the choice of pollutants to be taxed. Pollution taxes are most effective when targeting a limited number of big stationary sources. If major contributors to the problems are numerous small sources, mobile sources or diffuse pollution (e.g. from agriculture), pollution taxes may not be the best policy tool.

Source: OECD (2012d).

Waste disposal

A waste disposal tax applies to municipal, construction, mining waste and hazardous waste, including oil shale ash and semi-coke (Chapter 4). Basic rates vary according to the type of waste and its hazard level. The disposal tax is also often referred to as landfill tax, even though the disposal tax is levied not just on landfilling, but also, according to the Environmental Charges Act, on “other activities that result in the discharge of waste into the environment”, which includes on-site storage. As part of the same system, non-compliance fees of up to 500 times the basic rate (for hazardous waste) apply in case of disposal of waste in quantities higher than those specified in a facility’s permit, reaching 1 000 times the basic rate for promiscuous hazardous waste dumping. The revenues go to the state and municipal budgets and the EIC, as discussed above.

In addition, landfill operators impose a “gate fee” on waste brought to landfills in order to recover their costs. This service fee (usually EUR 20-25 per tonne) is paid on top of the waste disposal tax (about EUR 30 per tonne of non-hazardous waste as of 2015), with the revenue channelled to the operator.

A packaging excise tax was introduced in 1997 with rates depending on the packaging material. Plastic packaging and metal are taxed at the highest rate of EUR 2.5 per kg. There are a number of exemptions, notably for exported products. This tax is only payable by those organisations that fail to meet obligations to recover and recycle their waste as part of an extended producer responsibility (EPR) scheme; the rates are high to encourage compliance and most producers do comply (Hogg et al., 2014). Waste policies are further discussed in Chapter 4, while policies related to mining waste are discussed in Chapter 5.

Water abstraction

Estonia has a water abstraction tax covering abstraction of groundwater and surface water. Water abstraction is metered by users and reported quarterly. Rates vary considerably, depending on the type of water use, with preferential rates for some uses, notably mining. Agricultural irrigation (whose rates are low) is exempt from the tax, as is fish farming and hydropower generation.

The abstraction tax revenue is divided between the state and local government budgets. About 32% of the total revenue of EUR 13 million (2014) comes from the oil shale mining sector, related mostly to the pumping of groundwater from mines. Cooling water accounts for about 20% of the total water abstraction tax revenue, almost solely paid by oil shale-fired power plants in north-eastern Estonia (MoE, 2015b).

3.7. Fees for municipal water supply and sewerage services

A fee (water tariff) is paid for centralised water supply and sewerage services to recover their costs, in accordance with the Public Water Supply and Sewerage Act (1999). The tariff accounts for both water supply and sewerage services, is set per cubic metre of supplied water and based on actual consumption measured by water meters. This tariff for households rose by 77% over 2007-14 – from EUR 1.59 to EUR 2.80 per cubic metre. Households enjoy a slightly lower tariff than business users, but Estonia intends to harmonise these rates by 2021 (MoE, 2015b).

Water tariffs do not allow full cost recovery of municipal water supply and sewerage services. The cost recovery rate has been estimated at 86% nationally in 2014 (it is higher in Tallinn and Tartu). Local water and wastewater utilities receive significant subsidies from the EU Cohesion Fund (EUR 474 million in 2007-13), the EIC (EUR 98 million in 2007-13) and municipal budgets (MoE, 2015b).

3.8. Financial incentives for biodiversity protection

There are provisions for compensating private owners of protected forests, which cover 80 000 ha – one-third of the total protected area. Private owners have a right to compensation only with respect to Natura 2000 areas: EUR 110 per ha per year in conservation zones, EUR 60 per ha per year in limited management zones. In reality, only owners of 50 000 ha of protected forests have asked for such compensation. The compensation is financed by EU funds. In fact, Estonia has the biggest budget for support for Natura 2000 private forest land among EU Member States: EUR 28 million for 2014-20 (Ministry of Rural Affairs, 2014). The few owners of non-Natura 2000 protected forests demand equal compensation for forest management restrictions on their land.

Estonia is not considering other payments for ecosystem services. While the private nature tourism industry generates an annual turnover of EUR 10-15 million (Ehrlich, 2013), access to all protected areas, even on private property, is free in accordance to the commonly accepted Nordic principle of free access to nature.

4. Eliminating environmentally harmful subsidies

The OECD defines environmentally harmful subsidies as “a result of a government action that confers an advantage on consumers or producers, in order to supplement their income or lower their costs, but in doing so, discriminates against sound environmental policies” (OECD, 2003). As in other OECD member countries, environmentally harmful subsidies in Estonia exist in multiple forms. There are exemptions from excise taxes and reduced rates for certain users, including households, agriculture and fisheries, as well as tax breaks for company cars. The excise duty reduction for diesel fuel and light heating oil used for specific purposes amounted to EUR 74 million in 2011, decreasing to EUR 47.6 million in 2014, which corresponds to 9.3% of environmental tax revenues (OECD, 2015b). Peat and wood products used for heating are also exempted from the value added tax (VAT) and excise duty. In addition, according to the Ministry of Finance (2015), the free allocation of EU ETS emission allowances amounted to a subsidy for the energy sector of nearly EUR 74.5 million in 2014 (Section 3.3).

No comprehensive data exist on the extent or magnitude of environmentally harmful subsidies in Estonia. Developing such an assessment would provide robust evidence upon which to develop a clear approach to phasing them out.

Fossil fuels

Despite the removal of some exemptions8 for oil shale and shale-derived products in recent years, the oil shale industry still benefits from government support. It is estimated that in 2014 support to producers of shale-derived oil amounted to more than EUR 4.8 million (OECD, 2015b). In 2011, support for oil shale-based electricity and heat production amounted to EUR 3.5 million (OECD, 2013a), which dropped to around EUR 170 000 in 2013 (OECD, 2015b).

The recent decline in oil prices represents an opportunity for Estonia to reduce fossil fuel subsidies with a relatively low impact on consumers (Section 3.4). It provides momentum to help alleviate some of the political obstacles in reforming subsidies, which are generally linked to public approval and vested interests (Benes et al., 2015). In addition, subsidy savings can be redirected towards investments in renewable sources and energy efficiency initiatives.

Company cars

Income tax breaks granted to employees for the use of a company car influence the composition of the vehicle fleet and the intensity of vehicle usage. Employees get two types of benefit from a company car: the benefit of not paying or paying lower fixed costs (purchase, insurance, registration, etc.) and the benefit of not having to cover variable costs (fuel, repairs, maintenance) (Harding, 2014). Lower fixed costs may encourage employees to choose a larger car, while lower variable costs may encourage them to drive more at zero marginal cost. These benefits may increase car ownership by households and hence the size of the vehicle fleet. All these factors have substantial negative impacts on the environment and on society (Harding, 2014; Roy, 2014).

A study of 27 OECD member countries showed that no tax system captures all the benefits enjoyed by employees with a company car; on average, countries tax only half these benefits in kind. Estonia is among the ten OECD member countries that capture the fewest taxable benefits of company cars. The non-business use of company cars is subject to a 50% VAT deduction (Estonia has received a derogation until the end of 2017 from an EU directive requiring such use to be subject to VAT).

Forestry

In addition to support for fossil fuels, Estonia has subsidies for agriculture, fisheries and forestry. Whereas VAT exemptions for forestry were abolished at the end of 2011, the sector continues to receive significant subsidies from domestic and EU sources. In 2012, the total domestic forestry support amounted to EUR 3.4 million, while the respective EU funding was EUR 8.7 million (MoE, 2015a). A substantial share of the funding is targeted at promoting sustainable forestry practices and forest protection, which cannot be regarded as an environmentally harmful subsidy.

5. Investing in the environment to promote green growth

5.1. Environment protection expenditure

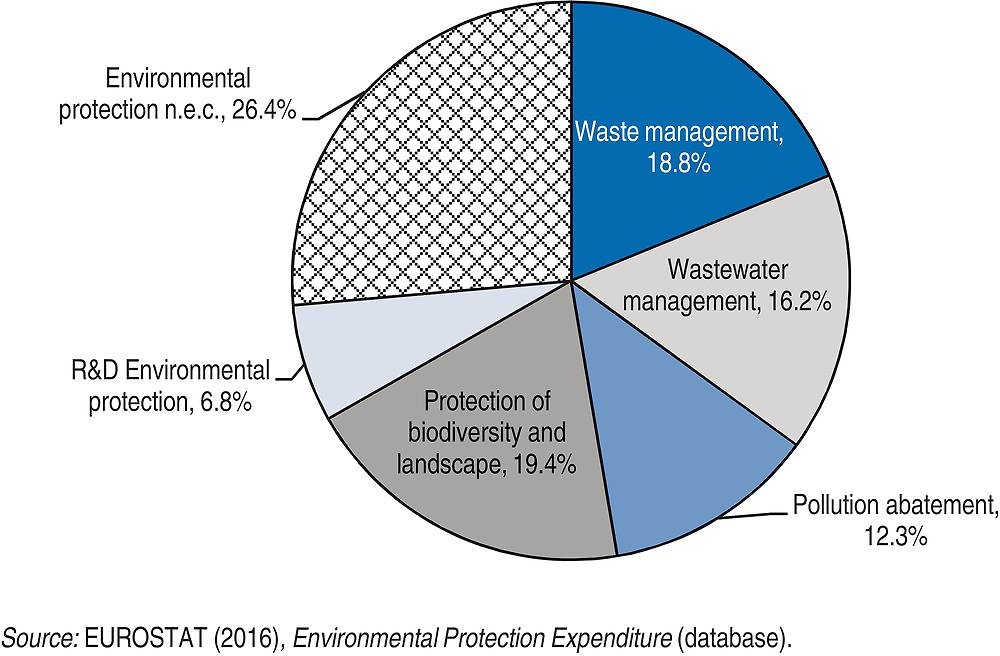

Government expenditure on environmental protection rose from 0.7% to 0.9% of GDP between 2000 and 2012, just above the EU28 average of 0.8% (Eurostat, 2016b). As mentioned in Section 3.7, major public funds are provided for upgrading the municipal water supply and wastewater treatment infrastructure: 35% of the public expenditure accounts for waste and wastewater management (Figure 3.6). However, the share of environment in governmental expenditure increased from 1.5% in 2000 to 2.5% in the mid-2000s, then fell back to about 1.5% in 2014 (OECD, 2016d), mostly due to the decline in the revenue from the sale of surplus CO2 credits (discussed below). The government-run green investment initiatives are described in Section 5.2.

Between 2010 and 2013, pollution abatement expenditure by production enterprises more than doubled from EUR 135.4 million to EUR 298.6 million (with a 71% share of investments) (MoE, 2015a). Production enterprises tend to invest more in end-of-pipe installations (for the reduction of pollution already generated) and less in integrated technologies (for the prevention or reduction of the amount of pollution created at the source). Expenditures of environmental service providers (“specialised producers”) also rose significantly: from EUR 547.1 million in 2008 (with a 17% share of investments) to EUR 620.4 million (with a 15% share of investments) in 2014 (Statistics Estonia, 2016).9 Waste management accounts for the largest share of business sector expenditure (Figure 3.7).

5.2. Green investment

Estonia has a dedicated investment agency hosted by the Ministry of Economic Affairs and Communications that provides investment support for environmental projects: the EIC. Established in 2000, the EIC funds a range of environmental projects, including large-scale ones such as reconstructing or constructing combined heat and power plants, district heating systems, and onshore and offshore wind parks. In its 15 years of operation, the EIC has disbursed more than EUR 1.3 billion to support over 18 000 projects. In 2014, the EIC funded 956 projects under its Environmental Programme with EUR 44.1 million (EIC, 2015a). EIC grants and loans are financed from environmental pollution and natural resource taxes, EU structural funds and the sale of excess carbon credits.

Since 2010, the EIC has been the implementing agency for the Green Investment Scheme (Box 3.3), which channels revenue from the sale of surplus CO2 credits available under the Kyoto Protocol (“assigned amount units”, or AAUs) to environmental projects (EIC, 2015a). It is expected that projects financed through this scheme will reduce CO2 emissions by 1.5 million tonnes over the next 20 years (IEA, 2013).

The Green Investment Scheme is a financing mechanism that channels funds from the sale of surplus carbon credits (known as assigned amount units, or AAUs) available under the Kyoto Protocol. Between 2009 and the end of 2011, Estonia sold around 60 million AAUs. By October 2012, the value of total sales was nearing EUR 400 million – almost 1% of GDP for each of the three years the scheme had been in full swing.

The rules for AAU sales stipulate that all revenue raised from credit sales must be used to fund projects that lower greenhouse gas emissions. Revenues have funded projects to build wind farms, as well as combined heat and power installations. Projects have also aimed to improve district heating networks and energy efficiency in buildings, industry and transport.

Source: IEA (2013); EIC (2015b).

The financial management of EIC projects is regularly evaluated. However, environmental benefits of individual projects are assessed only with respect to certain EU funds, if required by the conditions of individual support schemes.

Investment in renewable energy

Estonia is actively promoting renewable energy, with subsidies for renewables increasing substantially from EUR 1.5 million to nearly EUR 65 million between 2004 and 2014 (MoE, 2015a). A feed-in-tariff scheme, introduced by the Electricity Market Act in 2007, applies to electricity produced from renewable energy or efficient combined heat and power (CHP). In 2015, 48% of total subsidies for electricity produced from renewable sources were expected to go to wind generators; 37% to electricity produced from biomass by power stations with capacity of more than 20 MW; and 14% to hydropower, electricity produced by small power stations and combustion of waste (Elering, 2015).

Initially, large projects (with installed capacity of over 100 MW) to produce renewable electricity were not eligible for the scheme, but this restriction ended in July 2009. This enabled the use of biomass in the Narva Power Plants to become eligible for support, which significantly increased the amount of subsidies under the support scheme (OECD, 2012b). Boosted by these subsidies, heat production from biomass in CHP plants has risen rapidly beginning in 2008 and reaching 1 400 GWh in 2013 (Kearns, 2015). Over 95% of electricity generated from biomass comes from subsidy-eligible CHP plants.

Subsidies for wind generation are limited to the first 600 GWh of electricity produced in a given year, an amount that Estonian wind farms already produce during a typical year. Although additional proposals for wind farms have been submitted, the economic viability of these projects is uncertain in the absence of additional subsidies (Kearns, 2015).

Overall, an estimated EUR 706 million was invested in renewable energy production in 2013, of which 78% came from private investors and around 22% came from Eesti Energia. Large shares went to wind (EUR 372 million) and biomass (EUR 293 million), with small amounts going to biogas, solar and hydro. In 2014, an additional EUR 55 million was invested in renewables (MoE, 2015a). Low oil prices can also discourage new investments in shale oil production (Chapter 5) and contribute to the uptake of renewable sources in the electricity system, presently dominated by oil shale.

Subsidies for renewable energy are financed, in part, by a renewable energy charge applied to electricity consumers. The transmission system operator Elering manages the subsidy system, tracking production of renewable-based electricity, billing consumers, delivering subsidies to producers and reporting to Statistics Estonia.

Draft amendments to the Electricity Market Act introduced in 2016 aim at aligning the scheme with the European Commission’s new state aid guidelines in force since June 2014. A new bidding scheme would get new renewable electricity production capacities to the market starting in 2017. The support level would then be differentiated between existing and new producers: existing producers will keep receiving the current feed-in premium of EUR 53.7 per MWh (a payment on top of the market price), while newcomers will receive a feed-in premium with a capped total revenue of EUR 93 per MWh.

Investment in energy efficiency

According to the National Development Plan of the Energy Sector until 2030, the total 2016-19 funding needs for energy efficiency improvements are EUR 336 million in the housing sector, EUR 87 million in industry and street lighting, EUR 68 million in public sector buildings and EUR 45 million in district heating. Over 2014-20, the EU through its Cohesion Policy will invest some EUR 238 million in energy efficiency improvements in public and residential infrastructure, as well as in high-efficiency cogeneration and district heating in Estonia. This investment is expected to lower energy consumption in about 40 000 households (EC, 2015).

Estonia also had a small, but successful, loan programme to improve energy efficiency by renovating apartment buildings (IEA, 2013). It was funded through the sale of surplus carbon credits and implemented by Estonia’s Credit and Export Guarantee Fund (KredEx) and Germany’s KfW. In 2011, loans and grants under this initiative were estimated to have reduced energy use by an average of 40% (MoE, 2013). In 2014, 25 apartment associations used long-term loans from KredEx to finance renovations, totalling EUR 4.3 million; EUR 9.1 million was allocated to reconstruction grants for 97 apartment buildings (KredEx, 2015).

Overall, incentives for energy efficiency could be strengthened, in both heating networks and in buildings (OECD, 2015a). There is either no metering or inadequate metering in many district heating systems. The government’s plan to introduce regulations to improve incentives for efficiency in heating networks by reducing losses to 15% by 2017 is a step in the right direction. The government has also proposed draft regulation that encourages the use of renewable biomass in district heating.

The Estonian real estate market is characterised by a high level of home ownership, with only a small rental market. Still, the government may need to provide tax incentives for landlords to invest in improving the energy efficiency of their residential properties (OECD, 2015a). In another issue of concern, some local governments have established district heat supply areas, in which customers cannot change the type of heat supplied unless they switch to renewable energy. This prevents customers from investing in economically justified high-efficiency alternatives (IEA, 2013).

Investment in sustainable transport modes

Investment in transport infrastructure represented 1.3% of GDP in 2013, more than the OECD average of 0.8%, but with more than half of it allocated to road infrastructure. Estonia has also invested significantly in modernising public transportation. Over 2005-12, close to EUR 430 million was invested in public transport services, including railways, buses and streetcars. The EU plans to invest EUR 232 million over 2014-20 in energy-efficient rail transport (including the Rail Baltica project) under its Cohesion Policy (EC, 2015).

Estonia’s Electromobility programme supported the purchase of electric cars through KredEx, as well as the building of charging stations (167 of which have been installed as of early 2016, at 40-60 km from each other). The programme, deemed excessively costly, ended in 2015. KredEx disbursed around EUR 1 million for electric car subsidies in 2011 and around EUR 6.8 million in 2014 (KredEx 2015), amounting to over EUR 15 000 per car. However, clean vehicles accounted for less than 1% of new passenger cars purchased in 2013 (Eurostat, 2016c).

Biofuels were exempt from excise duties until July 2011; the value of the exemption reached a peak in 2010 at nearly EUR 85 million (Ministry of Finance, 2015). Since 2013, biofuel use in road transport has been subsidised under the Ambient Air Protection Act, which allocates EUR 43 million from the sale of AAUs to promote biomethane for road use (OECD, 2015c). The National Transport Development Plan aims to increase the share of alternative fuel vehicles to make biomethane or compressed gas generated from biomass the main alternative fuel in Estonia (OECD, 2015c). Estonian cities have also tried to promote alternative fuel use in transport. In 2011, the city of Tartu took part in the EU-supported Baltic Biogas Bus projects to promote biogas buses in urban public transport. However, to achieve the 2020 EU target of the 10% share of renewable energy sources in the transport sector, Estonia would need to step up efforts to promote blending of biofuels into regular motor fuel and the use of biogas.

Support for environmentally friendly practices in agriculture

There are a number of environment-related payments under the 2014-20 Rural Development Programme, developed under the EU Common Agricultural Policy (Government of Estonia, 2014). It includes EUR 170 million for environmentally friendly agricultural practices (e.g. planning and management practices, awareness of environmental impact of different methods) and EUR 78 million for organic farming.

5.3. Promoting green markets and jobs

Producing environmental goods and services (EGS) generates growth and employment, while contributing to greener growth. According to a pilot study, the value added of the EGS sector accounted for almost 6% of GDP (EUR 732 million), compared to the EU average of 2.2% of GDP (Eurostat, 2016a; Statistics Estonia, 2016).10 The study suggests that energy saving and management and renewable energy generation are the main contributors to the EGS sector, in terms of both value added and employment (Figure 3.8). In 2013, the share of direct and indirect renewable energy-related employment in Estonia’s total employment was 0.71%, above the EU average of 0.53% (EC, 2015).

The Estonian Commission on Sustainable Development reviewed the potential for green jobs in a report commissioned by the State Chancellery (Värnik et al., 2012). The report examined the types of jobs that would be considered “green” in four sectors (agriculture, forestry, construction and transportation) and concluded that better environmental education would contribute to the “greening” of jobs.

Public procurement can be a tool to boost a market for green products and services, as well as to promote environmentally friendly business behaviour. Governments can create demand by making it a condition of tendering for government contracts that the applicant commit to maintaining specified environmental standards up and down the supply chain. Among OECD member countries, the United States, Germany and Japan have been at the forefront in promoting green public procurement (GPP) by setting targets via the legal framework and issuing guidelines (OECD, 2013c).

The number of environmental friendly procurements in Estonia should rise from 6% to 15% between 2014 and 2018, according to the MoE Development Plan for 2015-18. This is significantly lower than the EU average of 26% of all public contracts satisfying the EU core GPP criteria (EC, 2012), which itself is way below the indicative 50% target the EU had set for 2010. To promote GPP in Estonia, training sessions for local government and specialists from state authorities explain the concept and procedures of environmentally sound procurement. An electronic platform is under development to increase the role of environmental criteria in the procurement process.

6. Promoting eco-innovation as a new source of growth

6.1. Overall innovation performance

Estonia’s eco-innovation performance is below the EU average, ranking 19th among EU Member States in 2015. Estonia ranked higher than its Baltic neighbours Latvia and Lithuania, but lower than Western European and Nordic countries (Eco-Innovation Observatory, 2016). Since 2000, Estonia has been catching up with EU innovation leaders, building on strong economic growth and a well-developed information and communication technology (ICT) sector and strengthening its research and development (R&D) through market-oriented reforms (Eco-Innovation Observatory, 2016).

Over 2005-10, Estonia had one of the highest growth rates in gross domestic expenditure on R&D (GERD) in the OECD at 11.8% per year. At 1.74% of GDP in 2013, this is lower than the OECD average of 2.4%, but higher than the European average of 1.9% (OECD, 2015d). Business innovation remains below the OECD median in terms of R&D expenditure, the number of top firms, patents and trademarks (OECD, 2012c). R&D expenditures by businesses (BERD) almost doubled over the same period, increasing from 0.42% to 0.82% of GDP. R&D spending by business is highly concentrated in a limited number of high-technology sectors and firms: just 58 companies account for three-quarters of BERD (OECD, 2012c).

Framework for innovation

Estonia has no specific eco-innovation policy, but it incorporates eco-innovation measures into the strategic development plans of various ministries. For example, the National Development Plan of the Energy Sector until 2030 includes targets for the share of renewables in final energy consumption of 50% by 2030. At the same time, the Estonian Research and Development and Innovation Strategy 2014-20 “Knowledge-based Estonia” does not mention eco-innovation.

The economic impact of the Estonian R&D system appears to have been limited to date (EC, 2013; NAO, 2014b, 2013), spurring the government to reform innovation policies (Kapeller, 2015). Access to finance appears to be a limiting factor and many firms remain either unaware of R&D grants (Deloitte, 2015) or complain that the application is long and bureaucratic (Eco-Innovation Observatory, 2016). In addition, poor co-ordination between different ministries responsible for innovation in their respective areas has been cited as another problematic area (OECD, 2015e).

“Knowledge-based Estonia” puts “smart specialisation” at the heart of the R&D approach. ICT, healthcare and resource efficiency, among others, have been identified as having the greatest potential for adding value. By 2020, the strategy aims to increase total investment in R&D to 3% of GDP (and private R&D spending to 2% of GDP), and enhance labour productivity to 80% of the EU average (Ministry of Education and Research, 2014). Given current R&D levels, these targets may be difficult to achieve.

6.2. Eco-innovation performance

Although clean energy and environmental issues are increasingly important government priorities, Estonia still lags behind many EU countries in terms of eco-innovation. Estonia has managed to reach EU-28 average levels of eco-innovation inputs and activities, but is considerably behind on eco-innovation outputs, socio-economic outcomes and resource efficiency outcomes – key components determining overall performance (Eco-Innovation Observatory, 2016).

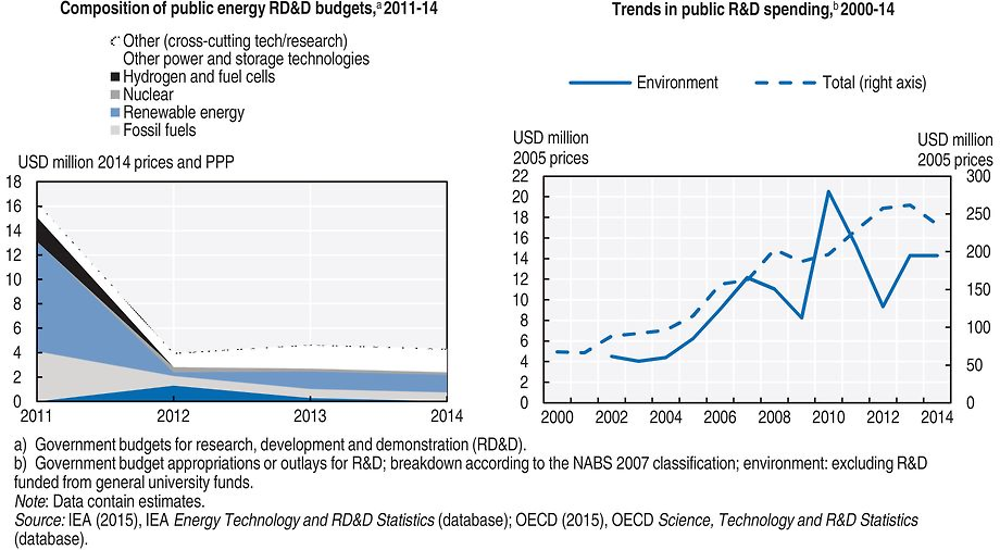

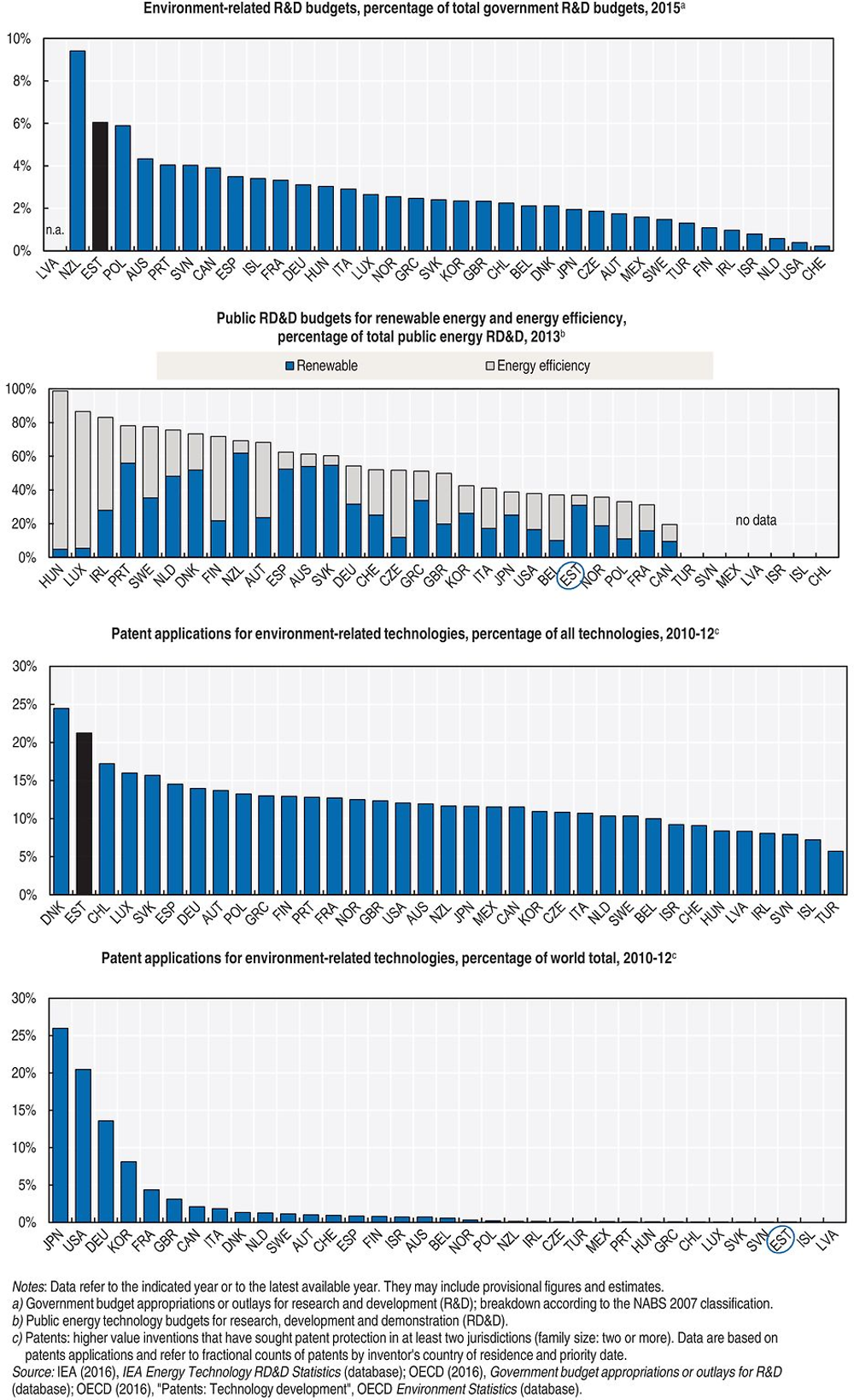

Public R&D spending allocated for the environment has followed the upward trend of public R&D spending since 2000; it peaked in 2010 due to considerable one-off investments in the oil shale industry (Figure 3.9). In 2014, Estonia ranked second among OECD member countries in terms of environment-related R&D as a share of total public R&D budgets (about 6%) (Annex 3.A2).

Among OECD member countries, Estonia has the lowest share of energy efficiency in total energy-related public R&D budget (Annex 3.A2) and ranks 23rd in terms of patents per capita for environment-related technologies (Figure 3.10). The share of environment-related technology in patent applications went from 0.7% in 2000-02 to 21.2% in 2010-12, exceeding the OECD average of 12% (OECD, 2016g).

The Estonian government stimulates business R&D and innovation with direct funding, as well as non-financial measures, such as awareness raising and award competitions. In addition to investments in environmental projects and promotion of entrepreneurship (discussed above), the Green Industry Innovation programme (co-financed by Norway) aims at increasing the competitiveness of green businesses and “greening” existing industries by optimising their process management, especially through the use of ICT. The most prominent examples of eco-innovation in Estonia are the use of novel ICT to optimise energy production, encourage energy efficiency and reduce waste (Eco-Innovation Observatory, 2016).

A good example of efforts in the energy sector is the Estonian Energy Technology Programme. It involves multiple stakeholders to develop more efficient oil shale technologies and new energy resources, mainly renewables (OECD, 2012c). In 2011, the oil shale sector accounted for one-quarter of public R&D expenditures before declining to 17% in 2014 (IEA, 2016). Innovation policy is also a main driver of the Electromobility programme (Section 4.2).

The EU supports investments to increase the competitiveness of small and medium-sized enterprises (SMEs) in Estonia, focusing on resource efficiency. It has allocated over EUR 145 million under its Cohesion Policy for R&D and adoption of low-carbon technologies across the SME community (EC, 2015).

Eco-innovation in Estonia could be enhanced on a number of fronts. For instance, there is significant potential to strengthen the focus on energy efficiency: in 2014, only a tiny share of public R&D for energy went to energy efficiency (Annex 3.A2). In addition, access to finance could be improved by raising firms’ awareness about existing instruments and reducing their administrative complexity. Green public procurement could be strengthened to provide demand-side stimulus. Better co-ordination among ministries on eco-innovation could reduce duplication and reinforce the impact of current efforts.

7. Environment, trade and development

7.1. Development co-operation

Estonian’s net official development assistance (ODA) has increased steadily since 2000 (Figure 3.11). In 2014, ODA reached USD 38 million with the ratio of ODA as a share of gross national income (GNI) rising to 0.15% in 2015, up from 0.14% of GNI the previous year. Estonia intends to continue this steady increase of development co-operation and to advance its status and role among other international donors.

The Ministry of Foreign Affairs manages Estonia’s development co-operation. The Strategy for Estonian Development Co-operation and Humanitarian Aid for 2011-15 sets out detailed objectives, as well as sectoral and geographic priorities (OECD, 2015e). Fostering environmentally friendly and sustainable development is one of the five strategic goals of Estonian development co-operation, while other areas cover civil society, good governance, health and education. Bilateral assistance has been mostly provided to Afghanistan, Georgia, Moldova and Ukraine, often in the form of small-scale technical co-operation projects (OECD, 2015e). Estonia is an observer to the OECD Development Assistance Committee (DAC).

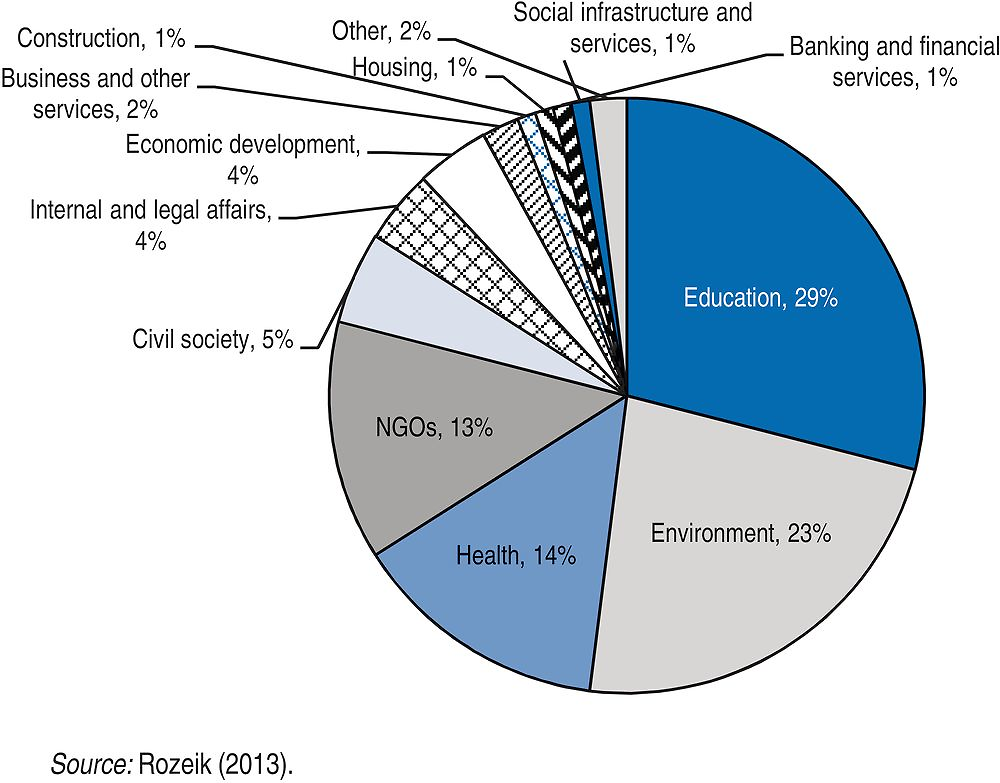

Environment-related bilateral ODA accounts for only a small share of Estonian ODA – USD 0.8 million in 2014 and USD 1.2 million in 2013 (in constant 2014 prices) based on data reported to the OECD DAC International Development Statistics database. However, a study of Estonia’s development co-operation commissioned by the EU noted that infrastructure projects related to the environment accounted for around a quarter of Estonia’s bilateral development over 1998-2012 (Figure 3.12). In addition, the Ministry of the Environment donated over EUR 1.6 million in 2012 to the United Nations Environment Programme for Strengthening Climate Change Adaptation in Rural Communities for Agriculture and Environmental Management in Afghanistan (Rozeik, 2013).

7.2. Export credits

KredEx, the Estonian export credit guarantee agency, helps Estonian firms to develop more quickly and expand into foreign markets by providing loans, venture capital, credit insurance and guarantees. It is financed largely by EU structural funds. To support investments in energy efficiency and renewable energy, KredEx provides loan guarantees, mainly for rebuilding houses and improving their energy efficiency, as well as grants for installing renewable energy generation in private households (solar panels, wind generators). A recent evaluation shows that KredEx funding has a positive impact on the performance of receiving companies, in terms of company size, exports, profitability and labour productivity (Vicente, 2014). Estonia backs the 2012 OECD Recommendation on Common Approaches for Officially Supported Export Credits and Environmental and Social Due Diligence. However, by 2016, KredEx had not developed a webpage for environmental and social due diligence and had yet to screen any transactions falling under the Common Approaches (OECD, 2016c).

Enterprise Estonia (EAS) provides grants to support the development of export-capable enterprises that create additional value, including those in the environmental sector. Over 2008-12, EAS awarded close to EUR 60 million in grants to 179 projects under the technology investment programme for industrial firms (MoE, 2015a). An evaluation of the impact of the EAS grant scheme shows that grants are more likely to be given to relatively large, successful and young exporting firms (Vicente and Kitsing, 2015). The study also finds evidence that receiving one or more EAS grants has a strong effect on a firm’s performance, as measured by the number of employees, sales revenue, labour costs and gross profits.

7.3. WTO Environmental Goods Agreement

Estonia, as an EU Member State, is taking part in negotiations for a multilateral Environmental Goods Agreement (EGA) within the framework of the World Trade Organization. The EGA would seek to gradually eliminate import duties on a list of goods that help monitor or improve the environment. Several goods considered for inclusion in the list are used to generate renewable energy or to improve energy efficiency.

-

Continue green tax reform by further shifting the tax burden from labour towards environmentally harmful activities without increasing the overall tax burden on the economy; regularly evaluate its economic impact; focus air and water pollution taxes on a limited number of priority pollutants whose emissions or discharges are monitored; increase the tax rates for these pollutants to provide a real incentive for their abatement; develop a methodology for setting resource extraction tax rates based on the value of extracted resource; expand the use of economic instruments for biodiversity protection, including payments for ecosystem services.

-

Raise and adjust tax rates on negative environmental externalities of energy production and use, including the tax on CO2 emissions for sectors not already covered by the EU ETS; set tax rates for diesel at least at the same level as for petrol; strengthen incentives for energy efficiency in both heating networks and buildings by broadening the use of metering and introducing penalties for heating network operators when they fail to meet heat loss targets.

-

Consider introducing policy measures to address the environmental damage from road transport via a road pricing system or taxes on motor vehicles adjusted to reflect the environmental characteristics of the vehicle; continue investments in the use of biofuels in motor vehicles; eliminate fiscal incentives for the use of company cars.

-

Develop a comprehensive assessment of the extent and magnitude of environmentally harmful subsidies and set priorities for phasing them out; continue to phase out exemptions and preferential rates (of energy excise taxes, water abstraction taxes, resource extraction taxes, etc.) for certain economic sectors, such as agriculture.

-

Monitor the effectiveness of the Environmental Investment Centre and other investment support schemes to ensure they support government priorities, add value in addressing environmental problems and reflect the principles of sound public finance.

-

Strengthen eco-innovation by improving access to finance by raising firms’ (in particular SMEs’) awareness about existing support mechanisms and reducing their administrative complexity; improve co-ordination between government institutions, enterprises and academia on research and development; enhance green public procurement by expanding the range of procurement categories with green purchasing criteria and designating and training procurement officials in public institutions on effective use of such criteria.

References

Benes, K. et al. (2015), Low Oil Prices: An Opportunity for Fuel Subsidy Reform, Columbia University, New York, http://energypolicy.columbia.edu/sites/default/files/energy/Fuel%20Subsidy%20Reform_October%202015.pdf.

Deloitte (2015), Estonia Corporate R&D Report 2015, Deloitte Central Europe, Prague, www2.deloitte.com/content/dam/Deloitte/ee/Documents/tax/ee_central_europe_rdsurvey_estonia_2015_noexp.pdf.

EC (2015), Country Factsheet Estonia, Commission Staff Working Document accompanying the document “State of the Energy Union”, Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee, the Committee of the Regions and the European Investment Bank, SWD(2015) 222 Final, Brussels, 18 November 2015.

EC (2013), “Erawatch Country Reports 2012: Estonia”, IRC Scientific and Policy Reports, European Commission, Brussels, http://ftp.jrc.es/EURdoc/JRC83974.pdf.

EC (2012), “The uptake of green public procurement in the EU27”, submitted to the European Commission, DG Environment, prepared by the Centre for European Policy Studies, Brussels, 29 February 2012, http://ec.europa.eu/environment/gpp/pdf/CEPS-CoE-GPP%20MAIN%20REPORT.pdf.

Eco-Innovation Observatory (2016), Eco-innovation in Estonia, EIO Country Profile 2014-15, Brussels, https://ec.europa.eu/environment/ecoap/sites/ecoap_stayconnected/files/estonia_eco-innovation_2015.pdf.

EEA (2015), EU ETS Data Viewer (database), www.eea.europa.eu/data-and-maps/data/data-viewers/emissions-trading-viewer (accessed 12 August 2015).

EEA (2014), Climate and Energy Country Profiles 2014: Estonia, A Joint Report of EEA and Ecologic Institute, European Environment Agency, Copenhagen, www.eea.europa.eu/themes/climate/ghg-country-profiles/country-profiles-1.

Ehrlich, Ü. (2013), Eesti loodusturism kui majandusharu [Estonian Nature Tourism as an Economic Activity], http://ec.europa.eu/environment/nature/legislation/fitness_check/evidence_gathering/docs/Member%20State%20Stakeholders/Nature%20Protection%20Authorities/EE/MS%20-%20EE%20-%20NPA %20-%20Loodusturism_Ehrlich.pdf.

EIC (2015a), Yearbook 2014, Environmental Investment Centre, Tallinn, http://kik.ee/sites/default/files/kik_ar_2014_eng.pdf (accessed 4 November 2015).

EIC (2015b), “Green Investment Scheme”, webpage, Environmental Investment Centre, Tallinn, http://kik.ee/en/green-investment-scheme (accessed 3 November 2015).

Elering (2015), “Renewable Energy Subsidy”, webpage, http://elering.ee/renewable-energy-subsidy-2/ (accessed 14 August 2015).

Ernst and Young (2015), Study of Transport Taxation Possibilities for Estonia: Summary, 1 October 2015, Ernst and Young Baltic, Tallinn.

Ernst and Young (2014), Estonian Oil Shale Mining and Oil Production: Macroeconomic Impacts Study, 23 May 2014, Ernst and Young Baltic, Tallinn, www.energiatalgud.ee/img_auth.php/6/64/EY._Estonian_oil_ shale_mining_and_oil_production_macroeconomic_impacts_study.pdf.

Eurostat (2016a), Environmental Goods and Services Sector (database) and Annual National Accounts (database) (accessed 19 May 2016).

Eurostat (2016b), Environmental Protection Expenditure (database) http://ec.europa.eu/eurostat/web/environment/environmental-protection-expenditure/database (accessed 1 June 2016).

Eurostat (2016c), Passenger cars in the EU, webpage, http://ec.europa.eu/eurostat/statistics-explained/index.php/Passenger_cars_in_the_EU (accessed 6 October 2016).

Government of Estonia (2014), Information on LULUCF Actions in Estonia, Report under LULUCF Decision 529/2013/EU Art 10, Submission to the European Commission, www.envir.ee/sites/default/files/information_on_ lulucf_actions_in_estonia_2.pdf.

Harding, M. (2014), “Personal tax treatment of company cars and commuting expenses: Estimating the fiscal and environmental costs”, OECD Taxation Working Papers, No. 20, OECD Publishing, Paris, https://doi.org/10.1787/5jz14cg1s7vl-en.

Hogg, D. et al. (2014), Study on Environmental Fiscal Reform Potential in 12 EU Member States: Final Report to DG Environment of the European Commission, Eunomia Research & Consulting Ltd, Bristol, http://ec.europa.eu/environment/integration/green_semester/pdf/EFR-Final%20Report.pdf.

IEA (2016), Energy Technology Research and Development (database), http://stats.oecd.org/Index.aspx? DataSetCode=BUDGET_RDD (accessed 15 December 2015).

IEA (2013), Energy Policies Beyond IEA Countries: Estonia 2013, IEA/OECD Publishing, Paris, https://doi.org/10.1787/9789264190801-en.

INSIGHT_E (2015), “Energy poverty and vulnerable consumers in the energy sector across the EU: Analysis of policies and measures”, Policy Report for the European Commission, May 2015, https://ec.europa.eu/energy/sites/ener/files/documents/INSIGHT_E_Energy%20Poverty%20-%20Main%20Report_FINAL.pdf.

Kappeler, A. (2015), “Estonia: Raising productivity and benefitting more from openness”, OECD Economics Department Working Papers, No. 1215, OECD Publishing, Paris, www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=ECO/WKP(2015)33&docLanguage=En.

Kearns, J. (2015), Trends in Estonian Oil Shale Utilization, International Centre for Defence and Security, Tallinn, October 2015, www.icds.ee/fileadmin/media/icds.ee/failid/Jordan_Kearns_-_Trends_in_Estonian_ Oil_Shale_Utilization_Oct_2015.pdf.

KredEx (2015), “KredEx earned a profit of EUR 1.2 million”, News webpage, 22 April 2015, www.kredex.ee/en/kredex/news/kredex-earned-a-profit-of-eur-12-million (accessed 17 November 2015).

Lahtvee, V. et al. (2013), “Keskkonnatasude mõjuanalüüs” [Environmental Analysis of the Impact of Charges], SEI Tallinn and Tartu University Social Science Research Centre, www.seit.ee/publications/4447.pdf (accessed 3 October 2015).

Ministry of Education and Research (2014), “Knowledge-based Estonia”, Estonian Research and Development and Innovation Strategy 2014-12, Ministry of Education and Research of Estonia, Tartu, www.hm.ee/sites/default/files/estonian_rdi_strategy_2014-2020.pdf (accessed 25 November 2015).

Ministry of Finance (2015), “Tax and Customs Policy”, webpage, www.fin.ee/tax-policy (accessed 4 November 2015).

Ministry of Rural Affairs (2014), “Eesti maaelu arengukava 2014-20” [Estonian Rural Development Plan 2014-20], Ministry of Rural Affairs of Estonia, Tallinn, www.agri.ee/et/eesmargid-tegevused/eesti-maaelu-arengukava-mak-2014-2020.

MoE (2015a), Response to the Questionnaire for the OECD Environmental Performance Review of Estonia, Ministry of the Environment, Tallinn.

MoE (2015b), “Assessment of the cost recovery and pricing policy for the WFD River basin management planning”, Background Document for River Basin Management Plans, Ministry of the Environment, Tallinn.

MoE (2014), Eesti keskkonnategevuskava aastateks 2007–2013, lõpparuanne [Environmental Action Plan of Estonia for 2007-13, Final Implementation Report], Ministry of the Environment, Tallinn, www.envir.ee/sites/default/files/ktk_2007-2013_lopparuanne.pdf.

MoE (2013), Sixth National Communication of Estonia under the United Nations Framework Convention on Climate Change, Ministry of the Environment, Tallinn, https://unfccc.int/files/national_reports/non-annex_i_natcom/application/pdf/est_nc6.pdf (accessed 17 November 2015).

NAO (2014a), Actions of the State in Directing the Use of Oil Shale: Does the State Guarantee that Oil Share Reserves are used Sustainably?, National Audit Office of Estonia, Tallinn, 19 November 2014, www.riigikontroll.ee/tabid/206/Audit/2314/Area/15/language/en-US/Default.aspx.

NAO (2014b), Impact of Innovation Support Measures on Competitiveness of Companies, National Audit Office of Estonia, Tallinn, 1 December 2014, www.riigikontroll.ee/tabid/206/Audit/2340/Area/4/language/en-US/Default.aspx.

NAO (2013), Overview of the Use and Preservation of State Assets in 2012-13 – Summary of Problems in the Development and Economy of Estonia by the National Audit Office, National Audit Office of Estonia, Tallinn, www.digar.ee/arhiiv/nlib-digar:245551.

NAO (2009), State’s Efforts of Reducing Greenhouse Gas Emissions, National Audit Office of Estonia, Tallinn, 26 November 2009, www.riigikontroll.ee/tabid/206/Audit/2125/Area/15/language/et-EE/Default.aspx.

OECD (2016a), OECD Database on Instruments used for Environmental Policy and Natural Resources Management, www.oecd.org/env/policies/database (accessed 27 May 2016).

OECD (2016b), OECD Science, Technology and R&D Statistics (database) http://stats.oecd.org/Index.aspx? DataSetCode=GBAORD_NABS2007 (accessed 30 May 2016).

OECD (2016c), Review of Members’ Responses to the Environmental and Social Survey, Working Party on Export Credits and Credit Guarantees, TAD/ECG(2015)17/FINAL, 24 February 2016, https://one.oecd.org/document/TAD/ECG(2015)17/FINAL/en/pdf.

OECD (2016d), OECD National Accounts (database), http://stats.oecd.org/Index.aspx?DataSetCode= SNA_TABLE1 (accessed 5 April 2016).

OECD (2016e), Effective Carbon Rates: Pricing CO2 through Taxes and Emissions Trading Systems, OECD Publishing, Paris, https://doi.org/10.1787/9789264260115-en.

OECD (2016f), “Israel’s green tax on cars: Lessons in environmental policy reform”, OECD Environment Policy Papers, No. 5, OECD Publishing, Paris.

OECD (2016g), Patents: Technology development, in OECD Environment Statistics (database), http://stats.oecd.org/Index.aspx?DataSetCode=PAT_DEV (accessed 5 Octobre 2016).

OECD (2015a), OECD Economic Surveys: Estonia 2015, OECD Publishing, Paris, https://doi.org/10.1787/eco_surveys-est-2015-en.

OECD (2015b), OECD Database on Support for Fossil Fuels, www.oecd.org/site/tadffss/data/ (accessed 6 December 2015).

OECD (2015c), “Climate Change Mitigation Policies: Estonia”, webpage, www.compareyourcountry.org/cop21 (accessed 20 December 2015).

OECD (2015d), Science, Technology and Industry Outlook Policy Database, http://qdd.oecd.org/Table.aspx? Query=0343775C-EB53-4591-8287-F4B0A36A1D35 (accessed 25 November 2015).

OECD (2015e), Development Co-operation Report 2015: Making Partnerships Effective Coalitions for Action, OECD Publishing, Paris, https://doi.org/10.1787/dcr-2015-en.

OECD (2015f), Climate Change Mitigation: Policies and Progress, OECD Publishing, Paris, https://doi.org/10.1787/9789264238787-en.

OECD (2013a), “Estonia”, in Inventory of Estimated Budgetary Support and Tax Expenditures for Fossil Fuels 2013, OECD Publishing, Paris, https://doi.org/10.1787/9789264187610-12-en.

OECD (2013b), Taxing Energy Use: A Graphical Analysis, OECD Publishing, Paris, https://doi.org/10.1787/9789264183933-12-en.

OECD (2013c), Mapping out Good Practices for Promoting Green Public Procurement, GOV/PGC/ETH(2013)3, OECD meeting of Leading Practitioners on Public Procurement, 11-12 February 2013.

OECD (2012a), OECD Economic Surveys: Estonia 2012, OECD Publishing, Paris, https://doi.org/10.1787/eco_surveys-est-2012-en.

OECD (2012b), Estimating Effective Carbon Prices: Case Study of Estonia, Working Party on Integrating Environmental and Economic Policies, ENV/EPOC/WPIEEP(2012)6/REV1, OECD Publishing, Paris.

OECD (2012c), “Estonia”, in OECD Science, Technology and Industry Outlook 2012, OECD Publishing, Paris, https://doi.org/10.1787/sti_outlook-2012-46-en.

OECD (2012d), Refocusing Economic and Other Monetary Instruments for Greater Environmental Impact: How to Unblock Reform in Eastern Europe, Caucasus and Central Asia, EAP Task Force, www.oecd.org/env/outreach/2012_EM_Refocusing%20Economic%20Instruments_ENG.pdf.

OECD (2011), OECD Economic Surveys: Estonia 2011, OECD Publishing, Paris, https://doi.org/10.1787/eco_ surveys-est-2011-en.

OECD (2003), Environmentally Harmful Subsidies: Policy Issues and Challenges, OECD Publishing, Paris, https://doi.org/10.1787/9789264104495-en.

Oras, K. and K. Salu (2013), “Environmental taxes account enables analysing the taxes macroeconomically”, Quarterly Bulletin of Statistics Estonia, No. 4/2013, Statistics Estonia, Tallinn, www.stat.ee/65376.

Poltimäe, H. (2014), “The distributional and behavioural effects of environmental taxes in Estonia”, PhD thesis, unpublished.

Rozeik, A. (2013), Developing Open, Rule-based, Predictable, Non-discriminatory Trade Relations with Priority ODA Recipients in accordance with the implementation of MDG8a International and National Targets, Praxis Centre for Policy Studies, Tallinn, http://praxis.ee/fileadmin/tarmo/Projektid/Praxise_Akadeemia/OdaBulg/Praxis_ODABULG_trade_analysis.pdf (accessed 25 November 2015).

Roy, R. (2014), “Environmental and related social costs of the tax treatment of company cars and commuting expenses”, OECD Environment Working Papers, No. 70, OECD Publishing, Paris, https://doi.org/10.1787/5jxwrr5163zp-en.

Statistics Estonia (2016), www.stat.ee/en (accessed 12 May 2016).