Chapter 2. Construction

The Construction sector is important, both as the creator of infrastructure for other sectors and as a great source of employment (over 1.1 million people in 2014). It is also a major contributor of GVA (EUR 9.4 billion in 2014). Among its major constraints are unclear procurement practices with unguided discretion by public authorities, caps on prices for major components such as gravel and sand and constraints on specific types of business such as market stalls and tourist constructions. Potential conflict of interest with public authorities, obsolete legislation and laws that have not kept up with recent EU legislation, such as those governing the environment have also led to wide discretion granted to authorities.

2.1. Economic overview of the Romanian construction sector

General Overview

Definition of the relevant sectors and areas of investigation

The construction sector can be defined and segmented into submarkets using various criteria:

Statistical and financial definitions are largely related and rely on the European standard classification system (NACE) which groups all core construction activities under group F (consisting of F41 Construction of buildings, F42 Civil engineering and F43 Specialized construction). A number of construction-related activities which could be considered as part of the wider construction sector1 fall outside the scope of NACE Group F but rather are dispersed into other NACE Groups such as B Mining and Quarrying, C Manufacturing, G Wholesale and Retail Trade or M Professional, Scientific and Technical Activities.

For the purpose of this study, depending on the availability of information, report objectives and relevant market, the analysis focusses on a list of NACE groups and codes which have been identified as relevant for each subsector analysed. An adapted business approach to defining the construction sector was used to define the relevant sectors/market according to the NACE classification.2 This study will attempt to focus on the areas of interest consisting of NACE group F42 Civil Engineering3 and its subsectors as well as identified subsectors relating to construction materials from groups B Mining and Quarrying and C Manufacturing.4

International Comparisons

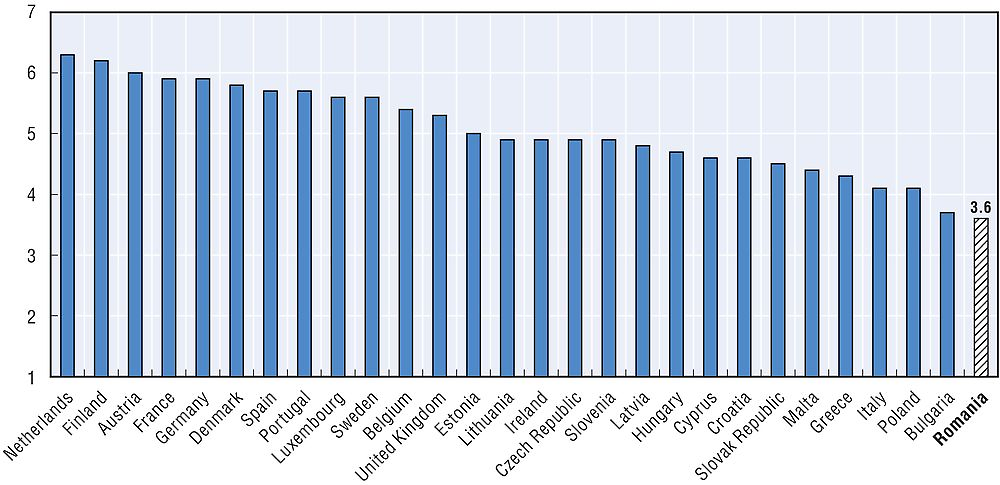

According to the World Economic Forum, the Global Competitiveness Report 2015-2016, Romania is ranked 91st on the competitive index on quality of overall infrastructure, with a score of 3.6 on a scale from 1 to 7 (Table 2.1). Looking at the second pillar that is focussed specifically on infrastructure, on the quality of roads, Romania is in 120th place, and on the quality of railroad infrastructure in 62nd place.

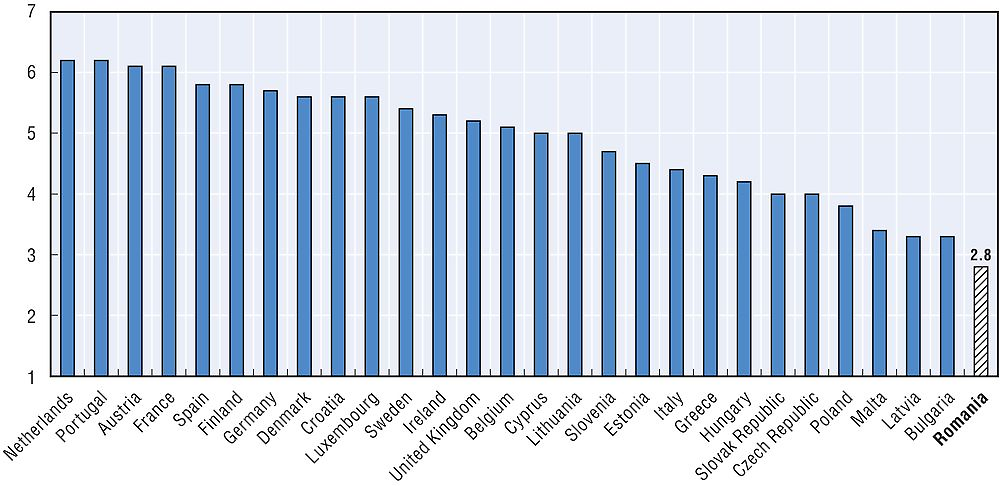

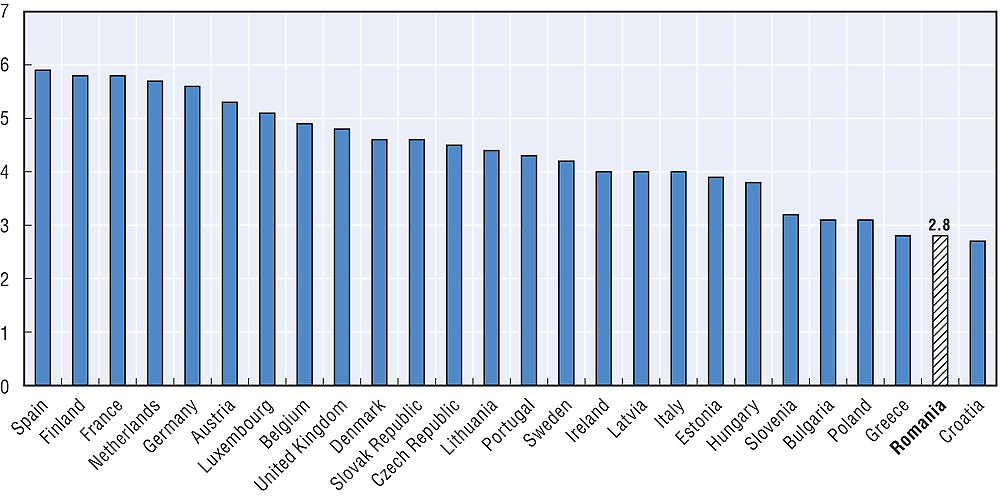

In comparison with the other 27 EU countries (Figure 2.1, Figure 2.2 and Figure 2.3), Romania is placed last on the quality of overall infrastructure and the quality of railroad infrastructure, whereas the European leader is the Netherlands. On the quality of railroad infrastructure Romania is ranked as second-last in Europe, the country scoring the lowest in this area being Croatia; the European leader in this category is Spain.

Source: World Economic Forum, Global Competitiveness Report (2015-16), http://reports.weforum.org/global-competitiveness-report-2015-2016/.

Source: World Economic Forum, Global Competitiveness Report (2015-16), http://reports.weforum.org/global-competitiveness-report-2015-2016/.

Source: World Economic Forum, Global Competitiveness Report (2015-16), http://reports.weforum.org/global-competitiveness-report-2015-2016/.

Development of the constructions sector

The overall construction sector’s importance for the Romanian economy is highlighted by the gross value added (GVA) of the sector (as a percentage of total gross domestic product [GDP]). From 2005 until 2007 construction intensified and the construction sector’s contribution to GDP reached over 9%. However, the situation changed in 2008 as a consequence of the economic and financial crisis as a slowdown of the overall real estate business, adjustment in value of real estate and budget balance issues emerged. In 2009, however, the sector reached a peak in its contribution to national GDP (10.23%), but followed a decreasing trend the years after (until 2015).

Source: National Institute of Statistics and Deloitte calculations.

The reduction of the GVA as a percentage of GDP was accompanied by a drop of revenues in the roads and railways sector, a decrease of fixed assets and a reduction in public spending in this sector (Coface, 2015). Even though the sector is still recovering and certain subsectors are still struggling to return to pre-crisis levels, others have seen slow growth resuming in the last few years.

The construction of roads and railways has seen a steady increase in the number of companies active on the market since 2010 but subsector turnover and number of employees only increased between 2010 and 2012 and contracted in 2013 (Figure 2.5).

Source: ANAF.

The Construction of utility projects subsector was relatively stable from 2008 to 2013 but has seen slight improvements in turnover throughout the period. The Construction of other civil engineering projects subsector has seen the most dramatic continued decrease in numbers of companies, employees and turnover.

Relevant government authorities and associations

In Romania the main government authorities involved in regulating, managing and supervising construction activity (including the area of construction materials) are the following:

-

The Ministry of Regional Development and Public Administration (MDRAP) carries out, as appropriate, together with the line ministries, government policy in the following areas of activity: regional development, cohesion and spatial development, cross-border, transnational and interregional co-operation, discipline in construction, spatial planning, urban planning and architecture, habitation, housing, residential buildings, thermal rehabilitation of buildings, real estate and urban planning management and development, public works, construction, central and local public administration, decentralisation, reform and administrative-territorial reorganisation, taxation and regional and local public finance, dialogue with the associative structures of local public administration authorities, development of public community services, state aid provided to local public administration authorities, industrial parks, public service management, planning, co-ordination, monitoring and control of the use of non-reimbursable financial assistance provided to Romania by European Union programmes in its areas of activity5.

-

Romanian National Company of Motorways and National Roads (CNADNR) is working under the authority of the Ministry of Transport with responsibility for the administration, exploitation, maintenance and development of the national roads and motorways on Romanian territory;6

-

Construction State Inspectorate (ISC) has as its main scope to verify and ensure the observance of applicable urban planning regulations and the legal requirements to assure the quality of construction work and materials.7

-

The Ministry for Environment, Waters and Forests promotes a unitary, coherent environmental policy, setting itself some major targets to comply with the acquis communautaire for the environment, increasing energy efficiency, promoting the renewable sources of energy and the ecological rehabilitation of the historically polluted areas or coastal erosion.8

-

Standing Technical Council for Construction (CTPC) is composed of qualified specialists who are part of organisations involved in introducing construction materials onto the market; its main responsibilities are: applying Romanian legislation in regard to acquis communautaire to construction materials, managing and supervising conformity certification of construction materials, managing and supervising technical agreement activity for construction and construction materials.9

-

National Agency for Mineral Resources (ANRM) has as its main responsibilities the administration of hydrocarbon resources (petroleum and natural gas resources) and mineral resources (public property), concluding agreements for mining concessions, for petroleum extraction and exploitation permits and monitoring compliance with petroleum agreements and with permits and licences.10

-

National Commission on Seismic Engineering is composed of technical experts and specialists in the construction domain. The main activities of the Commission are: it technically approves the recondition interventions on constructions considered vital for the society of which the functionality during and after an earthquake has to be fully assured, it approves the interventions for buildings considered as high seismic risk.11

The Social Dialogue Commission is part of the Ministry of Regional Development and Public Administration and has a consulting role. Its main responsibilities are to inform and consult its social partners about the legislative initiatives and to ensure social partnerships between the administration, employers’ associations and trade unions (in order to ensure permanent communication of issues derived from the main activity of the Ministry of Regional Development and Public Administration).12

The industry players are organised in various associations, especially:

-

Federation of Building Materials Industry (PATROMAT)

-

Professional Association of Mineral Aggregates Producers (APPA)

-

Romanian Construction Entrepreneurs Association (ARACO)

-

Patronal Association of Constructors (PATROCONS)

In Europe, technical assessment bodies (TABs) are designated for technical assessment of construction materials and for issuing the European Technical Assessment (ETA). In Romania, the following institutions make up the TAB:

-

The National Institute for Research and Development in Construction, Urban Planning and Sustainable Spatial Development “URBAN-INCERC”

-

The Research Institute for Construction Equipment and Technology (ICECON)

-

The Research Institute for Transport (INCERTRANS)

Moreover, the Body responsible for standardisation of construction in Romania is the Romanian Standards Association (ASRO) which is a non-governmental private legal entity of public interest. The main responsibilities of ASRO consist of developing, approving and managing documentation and editing, publishing and disseminating information related to national and international standards.13

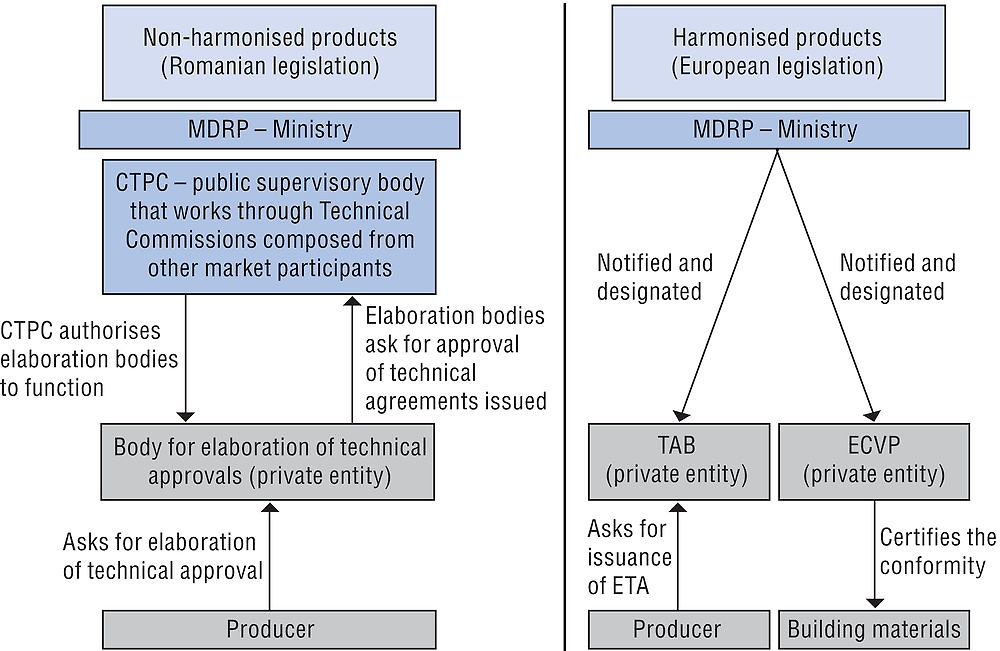

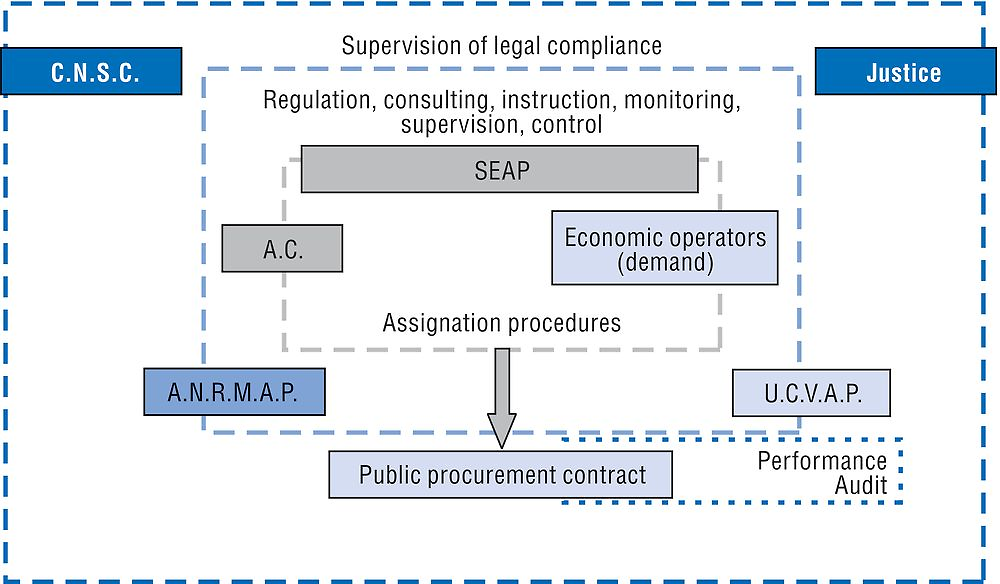

The chart below describes the process and parties involved in issuing technical approvals and ETAs for construction materials:

Source: Deloitte calculations.

Civil Engineering

Overview

The construction of roads and railways accounts for approximately 66.7% of the turnover of the overall civil engineering sector. In second place is the construction of utility projects with approximately 17% of turnover in the sector and the last contribution to the cumulated turnover is in construction of other civil engineering projects.

In the Civil engineering sector the supply generally consists of a diversified group of private companies, both Romanian owned and international, which often partner together and engage in subcontracting to execute complex projects. The following table presents the top ten companies in the civil engineering construction industry, in terms of 2014 turnover:

Table 2.3 demonstrates that the top ten companies in the industry account for approximately 20% of the total turnover generated in the entire civil engineering construction subsector, of which 13.18% comes from the Construction of roads and railways sector (more specifically, from the Construction of roads and motorways subsector), 3.63% from the utility construction sector (construction of utility projects for electricity and telecommunications subsector) and 3.03% from other civil engineering projects (however, this turnover comes from only one company).

Construction of roads and railways

Description of the subsector

The construction of roads and railways capitalises on sizable amounts allocated from the state budget and other financing sources (Competition Council, 2013), such as government loans, European funds and funds provided by international development organisations such as the European Bank for Reconstruction and Development (EBRD), the European Investment Bank (EIB), the European Investment Fund (EIF), the World Bank, etc. It is an auction market where companies have to participate in auctions organised by state authorities; the state accounts for most of the demand for these projects, and previous experience, recommendations and scale requirements for participating in auctions are requested by typical tender books. Complex projects spanning long periods of time expose the sector to delays and cancellations and lead to frequent subcontracting and/or partnering. The high cost of transportation of building materials favours local suppliers.

For the Construction of roads and railways subsector demand is generally represented either by the National Company of Motorways and National Roads of Romania (CNADNR), CFR SA (for railway infrastructure), local government or state owned public transportation companies (tram networks). Private sector demand for roads and railways is limited though there are infrequent small scale projects for private beneficiaries.

The main driver of demand for construction of roads and railways is government policy in the infrastructure/transportation sector – the pipeline of projects.

The total road network of Romania (Figure 2.7) increased by 4 469 km between 2007 and 2014 or 5.5% while the motorway network (Figure 2.8) increased by 402 km in the same interval – representing a growth of a 143%.

Source: National Institute of Statistics.

Source: National Institute of Statistics.

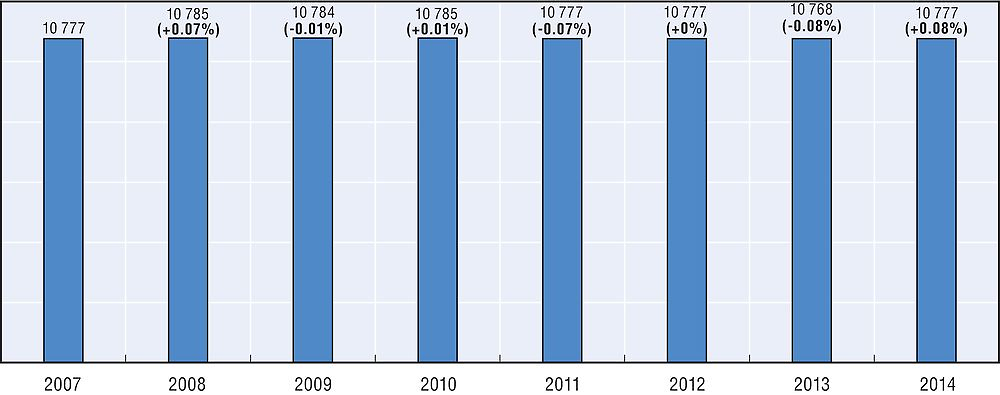

On the other hand, the length of railways in use (Figure 2.9) did not experience any changes from 2007 until 2014. Even if in some years there has been some variation in this indicator, in 2014 it returned to the same level as in 2007, namely 10 777 km of railways in use.

Source: National Institute of Statistics.

Subsector characteristics

The top ten companies in terms of turnover in the Construction of roads and railways sector14 are presented in the following table:

The top ten15 companies in the Construction of roads and railways sector (Table 2.4) account for 24.1% of the sector’s turnover. The highest share in this sector is held by “DELTA ANTREPRIZA DE CONSTRUCTII SI MONTAJ 93 SRL”, which contributed to the turnover of the Construction of roads and railways sector by 4%.

Table 2.5 shows that the most important activity in the construction of roads and railways is represented by the construction of roads and motorways, with over 95% of the turnover of the sector coming from this activity (ratio quite stable in the last 3 years), representing EUR 1 732 m in 2014.

In terms of gross profit (Table 2.6), in 2014 the construction of roads and motorways registered EUR 24.6 m, representing 94% of the gross profit of the sector. In the last three years, gross profit in the sector has experienced a downward trend from 2012 until 2014, with the only exception being in the construction of railways where in 2014 the subsector registered a cumulated positive gross profit after two years of losses.

In roads and railways construction, in 2014, 10.7% of the enterprises accounted for 80% of the turnover from the sector.16

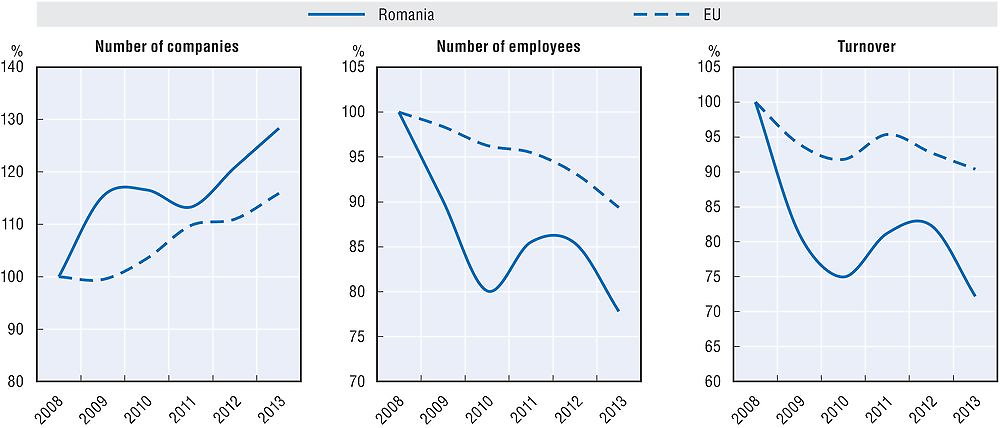

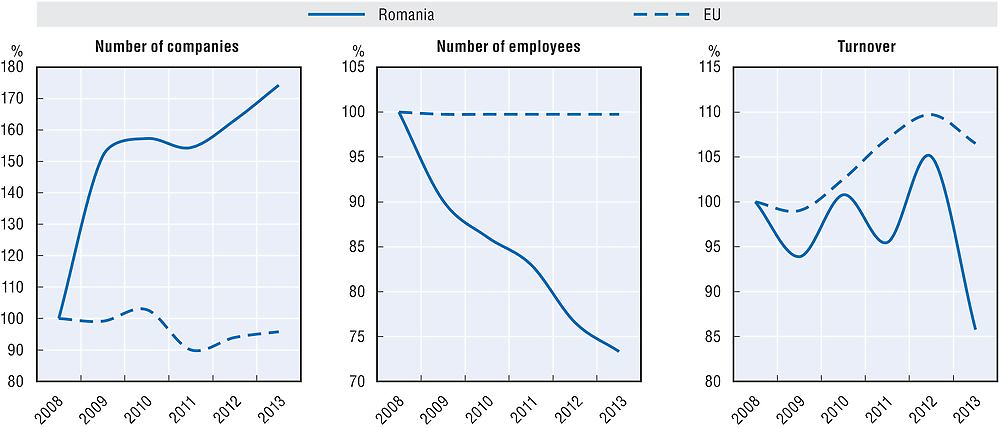

The development of the sector points to an increasing trend from 2008 until 2013 regarding the number of companies in Europe. Romania follows the same trend with the exception of 2011 when there was a brief drop in this indicator. However, the general trend between 2008 and 2013 was a reduction in the number of employees in this sector in both Europe and Romania (with the exception in Romania in 2011 where the number of employees increased by 6.8% compared to 2010, despite the reduction in the number of companies in the same year).

Source: Eurostat and Deloitte calculations.

Construction of utility projects

Description of the subsector

Construction of utilities often relies on financing from local budgets and external financing from the European Union (which runs programmes and national programmes in the area of transportation, environment, regional and rural development, large projects programme etc.), international development organisations (e.g. EBRD, EIB, EIF, World Bank) or the banking system. Local policies to extend network coverage to address availability gaps as well as government policy in the energy and utilities sector are key for these projects. It is also an auction market where companies have to participate in auctions organised by state authorities by following the general procurement procedure. This is frequently the case because the state is often the ultimate beneficiary, including where distribution networks are leased to private companies (due to the practice of granting concessions of networks to private operators rather than selling/transferring these, even for new projects).

In the Construction of utility projects subsector both supply and demand can be represented by the same companies. For example, in some cases Transgaz acts as a beneficiary of construction of utilities projects, in other cases it can act as a supplier. In general, subsector demand consists of both private and state companies mainly in the production, transportation and distribution chains for natural gas, electricity, petroleum products, water and sewage, telephones, TV and data.

Major state-owned companies include Transgaz (gas transportation), Transelectrica (electricity transportation), Conpet (transportation of petroleum products), water companies owned by public administrations and even public data projects such as the Netcity project in Bucharest. Private beneficiaries include natural gas distributors (GDF Suez and EON), electricity distributors (Electrica regional companies, Enel regional companies, CEZ, EON), private water companies (e.g. Apanova), etc.

The main drivers of demand for the construction of utility projects include the following: government, local authority and state company policies to cover any utilities availability gaps and to develop new capabilities in the energy and utilities sectors; available external funding including available EU funds; and foreign direct investment.

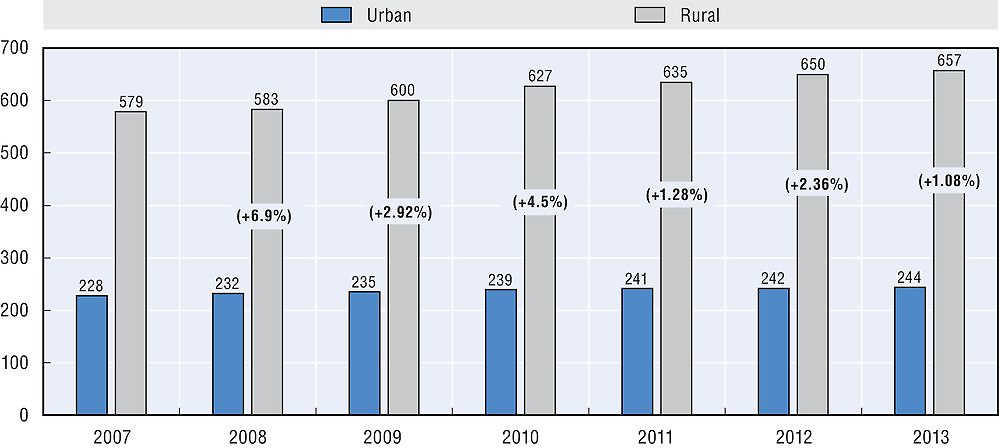

Note: Urban settlements are defined according to Romanian statistical standards which identify all municipalities and cities as urban settlements and all villages and communes as rural settlements.

Source: National Institute of Statistics.

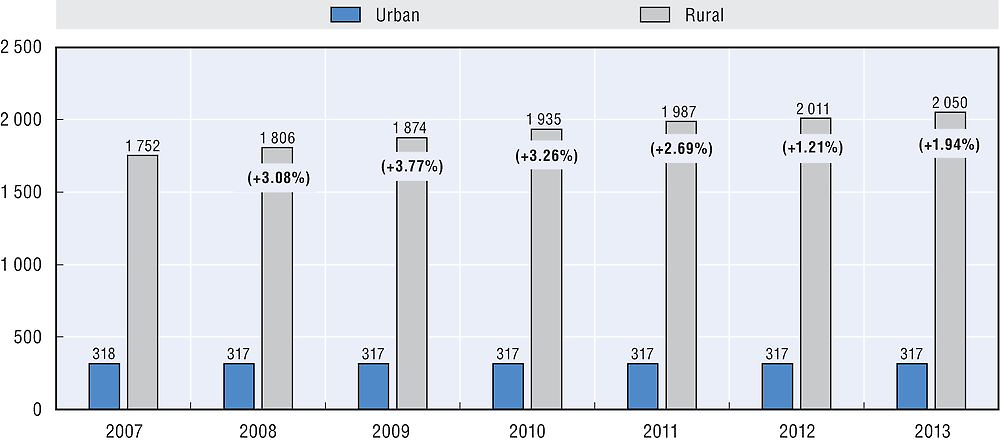

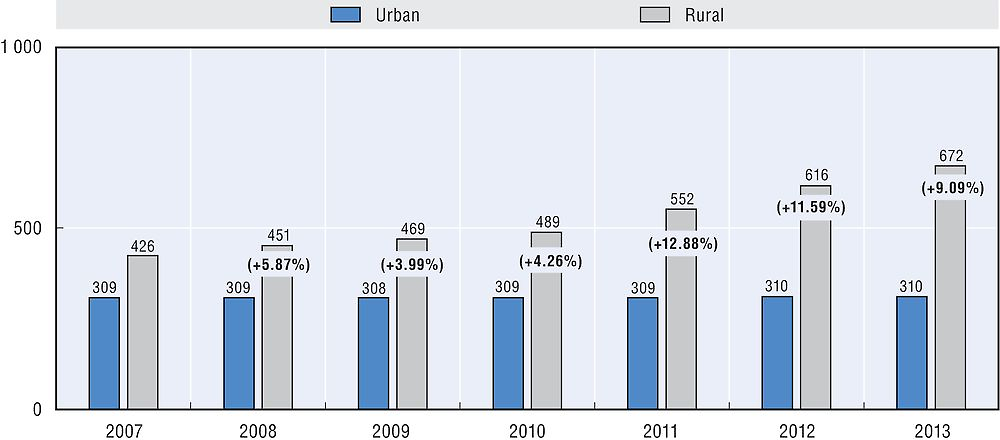

Access to public utilities has been slowly improving as 298 towns and villages in the rural area gained public water distribution networks between 2007 and 2013 (Figure 2.11). As well, 246 rural towns and villages and one urban town gained public sewage networks in the same time period (Figure 2.12), 94 towns and cities had natural gas distribution networks built (Figure 2.13) and the overall number of households with an internet connection improved from 31% to 56%. Further extensions of utilities networks were completed in the period.

Source: National Institute of Statistics.

Source: National Institute of Statistics.

Subsector characteristics

The top ten companies in terms of turnover in the Construction of utility projects sector17 are presented in the following table:

In the construction of utility projects sector, the main players (presented in Table 2.7) account for 44.92% of the total turnover from construction of utilities projects. The top company, “SOCIETATEA FILIALA DE INTRETINERE SI SERVICII ENERGETICE ’ELECTRICA SERV’ S.A.”, contributed 13.11% to the turnover of sector followed by “ELECTROMONTAJ SA” with 8.23%.

Table 2.8 presents the structure of the financial results from the companies active in the construction of utility projects sector. There are two main activities in this sector, namely construction of utility projects for fluids (53% of the sector’s turnover) and construction of utility projects for electricity and telecommunications (47% of the total turnover of the sector).

The gross profit of the companies involved in construction utility projects registered a cumulated loss in 2014 for construction of utility projects for electricity and telecommunications of EUR 1.19 m (Table 2.9). However, the loss was compared to the one previous year. In the construction of utility projects for fluids, gross profit amounted to EUR 7.65 m, and this indicator followed an increasing trend over the last three years.

From 2008 until 2013, the number of companies active in the construction of utility projects has followed an increasing trend, with the only exception in 2011 when the number of active companies was lower than in 2010. In Europe, the situation was not the same, as the evolution of the number of companies in this sector did not follow a clear trend. However, the evolution of the number of employees shows a general personnel reduction in Romania, while in Europe the number of employees working in the construction of utility projects remained relatively stable.

Source: Eurostat and Deloitte calculations.

Construction of other civil engineering projects

Description of the subsector

In the Construction of other civil engineering projects subsector demand consists of state companies and administrations relating to waterways, port management, flood prevention (for port infrastructure, dredging, dykes), both state and private companies and private or state companies for industrial construction work excluding chemical plants and refineries.

The main drivers of demand for Construction of other civil engineering projects include general economic and industrial sector growth, government policy in the infrastructure/water transportation sector and available external funding including available EU funds.

Subsector characteristics

The top ten companies in terms of turnover in the Construction of utility projects sector18 are presented in the following table:

Table 2.10 shows that the top ten companies in the construction of other civil engineering projects sector account for 39.42% of the sector’s turnover. Out this percentage, 21.64% of the market share comes from the construction of water projects, while the rest – 17.78% – comes from construction of other civil engineering projects. “HIDROCONSTRUCTIA SA” alone contributed to the total turnover of the sector by 18.63%, as the main player in the sector.

Based on data on the top ten constructors, Table 2.11 shows that the main subactivity in 2014 was the construction of water projects, representing almost 60% of the total turnover of this activity. Also, 66% of the employees are working in this area.

With regards to gross profit (Table 2.12), the construction of water projects suffered a loss of EUR 34.14 m in 2014. The construction of other civil engineering projects reached a low total profit of EUR 83 606. For each subsector the trend of the previous three years was a decrease in gross profit, the most significant reduction being in 2014.

Between 2008 and 2013 the number of companies involved in the construction of other civil engineering projects (in Romania) decreased (on average) – Figure 2.15, the only increase being in 2010 compared to 20.8% in 2009, followed by a drop of 22% in 2011. In Europe the evolution of the number of companies show a decreasing trend from 2009 until 2013. The number of employees in Romania also fell over the same period, by more than the number of companies. The only year when there were more people employed in this subsector than the previous year was 2011 (but it was followed by a higher drop in 2012). The turnover of the companies also suffered a reduction from year to year between the period 2008 to 2013, for both Romania and the European average.

Source: Eurostat and Deloitte calculations.

Construction materials

Overview

Construction materials generally represent inputs for the construction industry and as such there is a significant overlap between demand for construction materials and supply of construction works. Demand for building materials is mainly driven by the construction sector and ultimately by the overall state of the economy. The nature of both production and consumption of most building materials contributes to this close link between local building materials and the construction sector as a whole (including construction of residential and commercial buildings and specialised construction).

Demand for building materials also originates from sources such as international demand, especially in the case of high value added construction materials, construction materials which can easily be transported over long distances and certain products such as those derived from wood, glass and plastics, and from “do it yourself” construction, renovation and repair activities. Imports of construction materials also play a role in satisfying demand for the products mentioned above.

Sector characteristics

The sector is highly dependent on the development of the construction industry which provides demand for construction materials. It is a largely local market due to high transportation costs – building materials are generally supplied to construction companies in relative vicinity of the manufacturing facilities. However, some construction materials are more easily transported and have a higher value, and are therefore suited to transportation over long distances e.g. wood, glass or high value added products. Construction materials represent a diversified subsector consisting of a wide range of products resulting from processing of outputs from various materials/resources industries (e.g. metals, glass, chemical, forestry).

The top ten companies in the construction materials industry19 (in term of the turnover from 2014) are the following:

Data for the last complete available year from Eurostat are presented in Table 2.14 (2012). Incomplete data for 2014 is referred to in the analysis below depending on availability.

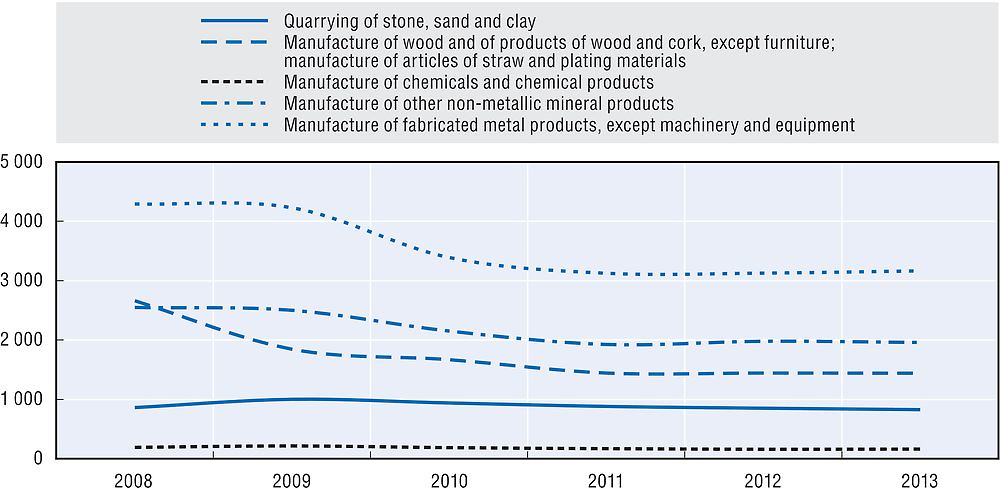

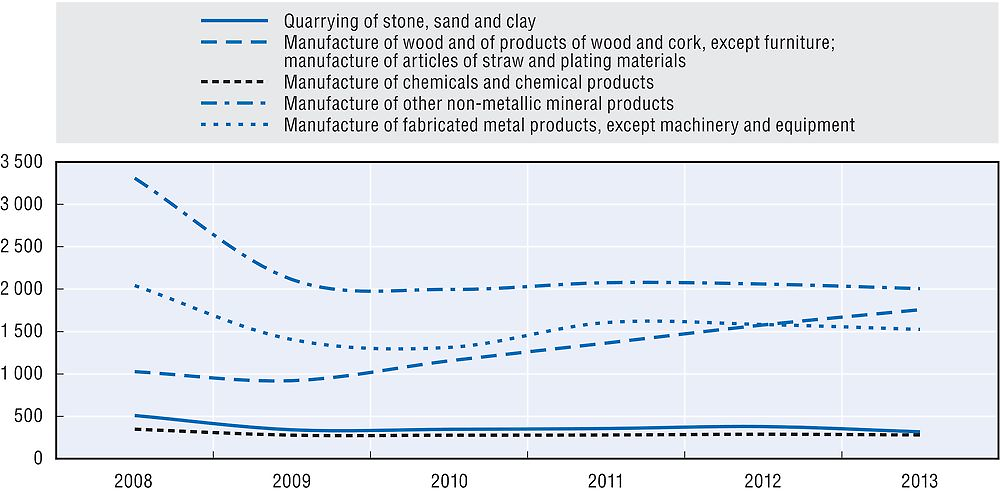

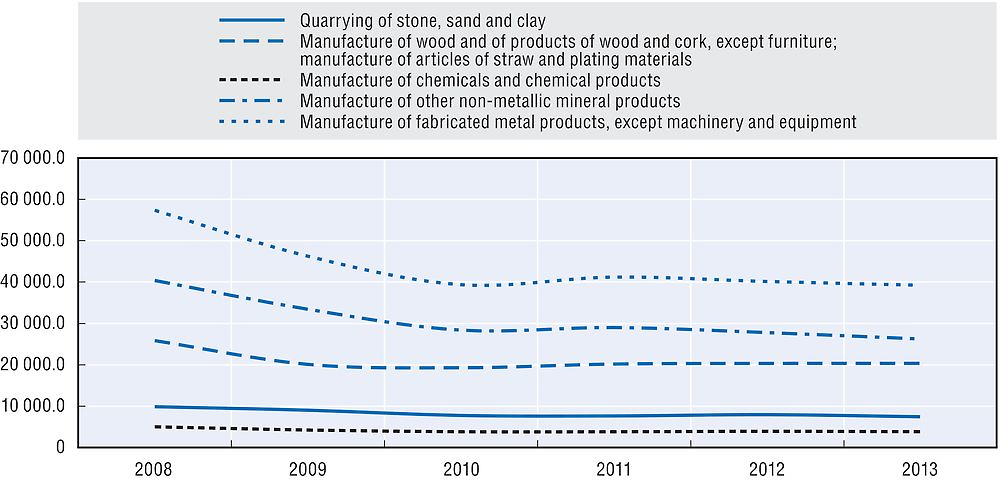

In 2014, there were 846 companies in the quarrying of stone, sand and clay activity, representing a 2.17% increase compared to 2013.20 The total number of active companies for this activity followed a decreasing trend from 2009 until 2013. In 2013 there were 7 431 people employed in this area, a relatively stable value between 2010 and 2013 (in 2010, however, there was a 14% drop). The turnover generated by these companies followed a general increasing trend after a sharp contraction in 2009, reaching EUR 355 m in 2014.

In the manufacture of wood and products of wood and cork, except furniture, manufacture of articles of straw and plating materials subsector the total number of companies in 2013 was 1 444.21 The number of companies has decreased every year since 2008, resulting in a total reduction of 45.8% over the period 2008 to 2013. On the other hand, the number of employees has decreased only in the first two years after 2008, but more people were employed in 2011, 2012 and 2013 compared to the previous period, reaching 20 337 employees in 2013. The companies in the three activities considered relevant in this study generated a total turnover of EUR 1 757 m in 2013, following an increasing trend from 2009 on.

In the manufacture of chemicals and chemical products subsector, the number of active companies was 162 in 2014, showing a 1.2% decrease compared to 2012.22 The number of employees was 3 818 people in 2013, decreasing by almost 1.5% from the previous year. The turnover generated by the companies operating in this area was relatively stable over the period 2010-2014, reaching EUR 311 m in 2014.

For the relevant activities operating in the manufacture of other non-metallic mineral products subsector, there were 1 959 active companies in 2013, employing 26 241 people and generating a turnover of EUR 2 006 m. The evolution of the number of companies shows in 2012 the first year of superior value compared to the previous year, after three consecutive years of reduction. The number of employees registered a cumulated reduction of 35% over the period 2008-2013, and the turnover decreased by 40% from 2009 until 2012.

In 2014, there were 3 279 companies operating in the manufacture of structural metal products subsector, representing a 3.63% increase compared to 2013.23 The total number of active companies for this activity followed a decreasing trend from 2009 until 2013. In 2013 there were 39 223 people employed in this area. The 3 279 companies generated a cumulated turnover of EUR 1 513 m, a value lower than in 2013.

Source: Eurostat and Deloitte calculations.

Source: Eurostat and Deloitte calculations.

Source: Eurostat and Deloitte calculations.

Public Procurement

Relevant legislation

The field of public procurement in Romania is currently regulated in primary legislation by a single act: Government Emergency Ordinance (GEO) No. 34/2006 on the award of public procurement contracts, public works concession contracts and concession of services,24 which implements EU Directives 2004/17/EC and 2004/18/EC in public procurement and concessions.

Secondary legislation details the implementation in specific areas, including procurement and operational aspects of the general sector, utilities sector, concessions and electronic procurement.

The public tender procedures are regulated in the former EU Directives on procurement, respectively open tender, restricted tender, competitive dialogue, negotiated procedures, frameworks agreements and dynamic purchasing system. The deadlines set within the procedures, including those regarding the submission of offers or contestations, the timeframe for requesting clarifications and the obligation of contracting authorities to respond to requests, comply with the provisions of the directives.

Also, the thresholds for publication of the different announcements regarding the public procurement procedures, such as the tender announcement, tender documentation or awarding announcement, in the national and European publication systems, implement the provisions of the EU Directives.

Relevant government authorities

Central functions of the public procurement system are fulfilled by the following institutions:

-

ANRMAP (National Regulatory and Monitoring Authority for Public Procurement) is the institution managing the public procurement system in Romania, with the fundamental role of defining, promoting and implementing the public procurement policy. The institution has a legislative function, offers advisory and operational support and performs ex ante evaluation of the tender documentation and ex post control.

-

UCVAP (Unit for the Coordination and Verification of Public Procurement) is an institution under the Ministry of Finance responsible for the ex ante verification of the procedures for awarding public procurement contracts, public works concession and service concessions by the contracting authorities;

-

CNSC (National Council for Solving Complaints) is an independent body with administrative-jurisdictional activity, which has jurisdiction to hear appeals made in the award of public procurement procedures before the contract is concluded. In exercising its powers, the Council takes decisions.

-

AADR (Agency for Romanian Digital Agenda) is a specialised public institution under the Ministry for Information Society which aims to operate nationwide systems for eGovernment. It is the administrator of the Electronic System of Public Procurement (Sistemul Electronic de Achizitii Publice – S.E.A.P.).

-

Court of Auditors is an operationally independent body within the Court of Accounts. The Court of Auditors is the only competent national authority to conduct external public audits in accordance with EU and national legislation, performing system audits and audits of operations.

-

Competition Council is an autonomous body, which administers and implements Competition Law and which aims to protect, maintain and stimulate competition and a normal competitive environment, in order to promote the interests of consumers.

-

Courts of appeal are courts in the constituency within which several tribunals and specialised courts operate. They represent the second instance for settlement of disputes in the matter of public procurement.

In addition, the management authorities and the implementation bodies which are charged with managing EU funds can also issue opinions on the conformity of a procurement procedure.

The steps of a public procurement procedure are as follows:

-

The contracting authority asks for approval of the tender documentation from ANRMAP.

-

After obtaining ANRMAP`s approval, the contracting authority publishes tenders above the legal threshold in the Electronic System of Public Procurement (SEAP).

The procurement directives define a variety of procurement procedures. The basic characteristics of the most common ones are:

-

In an open procedure any business may submit a tender.

-

In a restricted procedure any business may ask to participate, but only those who are pre-selected will be invited to submit a tender. This saves time and money for both businesses and buyers.

-

In a negotiated procedure the public authority invites at least three businesses with whom it will negotiate the terms of the contract. This procedure can take place with or without prior publication. Most contracting authorities can use this procedure only in a limited number of cases.

-

The competitive dialogue is often used for complex contracts where the public authority cannot define the technical specifications at the outset.

-

-

Bidders submit their offers online or offline.

-

UCVAP performs ex ante verification of the procedures for awarding public procurement contracts.

-

The contracting authority designates a winner of the procedure.

-

Any interested third party can appeal the result of the procedure in the first instance with CNSC and in the second instance with the Court of Appeal.

-

A contract is signed between the contracting authority and the economic operator(s).

-

ANRMAP, the Competition Council and the Court of Auditors can verify various aspects of the procurement procedure after the contract is signed/finalised.

Source: ANRMAP (2012), “Sistemul de achizitii publice din Romania” (Romanian Public Procurement System), http://romaniacurata.ro/wp-content/uploads/2012/04/Sistemul-de-achizitii-publice.pptx.

Following the issuance of three new EU Directives in 2014 on public procurement, respectively Directives 2014/23/EU, 2014/24/EU and 2014/25/EU, the national legislation in force is due to change. The transposition of the new EU Directives into Romanian legislation is planned to be made through four pieces of primary legislation that are, at the moment of writing this report, subject of public debate (one piece of legislation dealing with classical procurement, one dealing with utilities, one dealing with concessions and public private partnership and one piece of legislation dealing with appeals). Also, the national strategy on public procurement is subject to public debate.

Following the enactment of Government Emergency Ordinance No. 13/2015 on the set-up, organisation and functioning of the National Agency for Public Procurement (“ANAP”) in May 2015, ANRMAP and UCVAP shall be dissolved and their attributions will be undertaken by ANAP, which is an institution subordinated to the Ministry of Public Finance. However, until the issuance of the methodological norms for the functioning of ANAP, ANRMAP and UCVAP shall continue to perform their attributions.

General problems of public procurement in Romania

According to the European Commission’s Single Market Scoreboard,25 the overall performance of the Romanian public procurement system is below average, with a poor score for two out of the three dimensions26 (bidders’ participation, accessibility and effectiveness of the procedure).

In Romania, public procurement is currently carried out by thousands of decentralised contracting authorities (in accordance with the National Strategy on Public Procurement27 in the period 2007-14, an annual average of 7 300 public contracting authorities conducted online and offline procurement procedures using SEAP or direct commitment with values below or above the thresholds set by EU law).

According to the National Strategy on Public Procurement, some of the main deficiencies of the national procurement system are:

-

lack of integrated functionality and co-operation among responsible authorities;

-

emphasis on regulation and control functions within the system, leading to a lack of involvement of the contracting authorities; and

-

insufficient orientation of involved institutions towards an efficient use of public funds, but rather towards compliance with procedures.

The National Strategy on Public Procurement (2015) states that there is a generalised perception that deficiencies of the system are imposed primarily on the persons involved in the procedure who are punished as individuals, instead of identifying and solving the shortcomings of the system. This perception determines risk avoidance behaviours through which implementing best practice is replaced by an emphasis on the literal application of the rules and using just judgment is replaced by a mechanical approach. Some of the consequences are:

-

the widespread use of the criterion ”the lowest price”, even if significant intellectual services or complex works are required;

-

a focus on detailed technical specifications instead of performance specifications; or

-

a focus on qualification criteria in the evaluation of technical proposals.

Ultimately, the consequences are detrimental to obtaining a good price-quality ratio and the effective use of public procurement in promoting public policies.

Therefore, despite validation by ex ante control of procurement procedures applied by contracting authorities, some issues can be challenged and held to be illegal at a later stage (ex post control, auditing), obliging the contracting authority to bear penalties/related financial corrections. In the absence of a common approach, ex post control is carried out by various institutions (ANRMAP, Court of Auditors) analysing the same items (documents/procedures), determining the contracting authority to adopt the option with minimal risk when awarding contracts.

Moreover, due to the requirement to justify in detail the award criterion ”the most advantageous offer economically”, contracting authorities are discouraged from using this criterion and prefer to rely on the criterion of ”the lowest price”, even when it is not appropriate to use it, because it is perceived as the most secure in the event of subsequent checks. Such an approach substantially restricts the development of strategic procurement policies and leads to losses of efficiency in the use of public funds.

According to the same strategy mentioned above, due to the widespread use of the criterion “the lowest price”, reflected in substantial differences between the estimated price and the contract price, current market conditions in Romania determine economic operators to compete strongly on the price criteria which has an adverse effect on ensuring sustainable and efficient use of public funds (“value for money”).

According to the CNSC Activity Report28 of 2014, out of over 18 000 procedures published in SEAP, 20% were appealed in first instance, out of which 40% referred to construction contracts. Thus, according to the National Strategy on Public Procurement the large number of appeals was perceived by the administration more as an abuse of the economic operators rather than as an indicator of the lack of capacity in the public procurement system. Legislative solutions envisaged, respectively the guarantee of good conduct, were repealed by the Constitutional Court29 and are also subject to an infringement procedure before the European Court of Justice.

According to a recent report of the Romanian Academic Society,30 because of an unclear, unstable, and overregulated legislative framework worsened by sometimes contradictory implementation of the rules and a lack of administrative capacity, contracting authorities and economic operators end up being sanctioned both by national monitoring and control bodies and corresponding EU institutions via financial corrections. Furthermore, public projects are placed on hold until contestations and legal disputes are settled in courts, thus leading to a waste of public resources. Nevertheless, putting on hold public procurement projects is not mandatory according to national legislation, but is left for the decision of the CNSC and the courts.

In 2013, the Romanian Competition Council issued a report following a sector inquiry on the construction market of roads and highways. The competition authority scrutinised the said market and identified certain factual situations which could trigger competition issues, as we describe below:

-

partnerships between companies active on the market with the view of participation in tenders;

-

sub-contracting of part of works awarded to a contractor following completion of tender procedure;

-

increase of initial cost of works after the tender procedure through addenda to the contract until in the end the final cost overtakes the initial one.

Relevance of public procurement for the Romanian construction sector

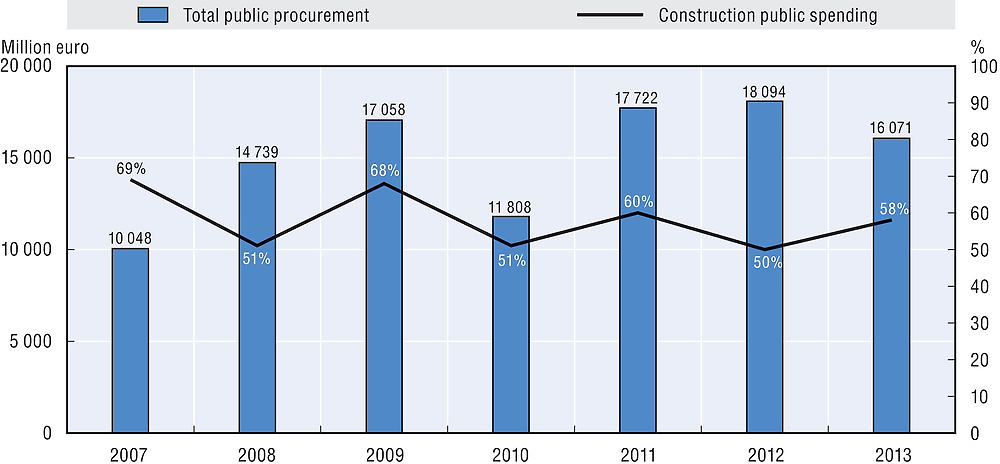

According to a report of the Romanian Academic Society,31 public spending in the construction sector accounts for 58% of total public procurement. More precisely, public spending in construction reached nearly EUR 7 billion in 2007, peaked at EUR 11.6 billion in 2009 and one year later dropped to EUR 6 billion. Afterwards it surged again to EUR 10.6 billion (2011) and in the following two years it settled to around EUR 9.1 billion. Public procurement in the construction sector follows the same trend as total public procurement. The year 2009 represents the peak, both in absolute value and in percentage share of GDP and the share of total government expenditure.

Source: Romanian Academic Society (SAR) (2015) Romanian public procurement in the construction sector. Corruption risks and particularistic links (30 March 2015): http://anticorrp.eu/publications/report-on-romania/. Construction procurement constitutes a significant share of total procurement, as shown in the figure below.

Source: Romanian Academic Society (SAR) (2015) Romanian public procurement in the construction sector. Corruption risks and particularistic links (30 March 2015): http://anticorrp.eu/publications/report-on-romania/.

The corruption report prepared by SAR (2015) reveals that the award criterion for construction procedures over EUR 1 m was in 46.3% of the cases “the lowest price”. Instead, contracts receiving European funding were awarded at “the lowest price” in 37.4% of the cases, the rest being awarded based on “the most economically advantageous” criterion.

Among the most frequent public authorities awarding works public procurement contracts over EUR 1 m (SAR, 2015), there were five entities that signed over 100 contracts from 2007 to 2014: the Romanian National Company of Motorways and National Roads (CNADNR: 444 contracts), the Bucharest City Hall (118 contracts), the National Housing Agency (110 contracts) and two gas national companies (over 100 contracts). Bucharest road and public domain administrations followed closely (under 100 contracts).

The National Strategy on Public Procurement mentions some of the main deficiencies identified during implementation of works contracts, such as: the transfer of responsibility for authorisation of works from the contracting authority to the supplier, thus leading to significant delays in execution of contracts; lack of flexibility of technical indicators used in the procurement procedure; barriers in subcontracting after the award of the contract, low quality of works performed due to tight financing; addenda to contracts in order to satisfy the real needs of the contracting authority.

2.2. Restrictions to competitiveness in construction

According to the OECD paper “Competition in the construction Industry” (2008), the construction industry plays a fundamental role in the economy and development of every country. Its significance stems from the creation of structures and infrastructures on which every other industry depends, as well as making a major contribution in generating employment. The report describes the construction sector in general as a fragmented industry that is prone to cartel activity. This fragmented structure also exists in Romania, as described in the Economic overview above. According to the report, the following features encourage cartel formation: i) a lack of differentiation in product delivery among construction firms, ii) a lack of transparent bidding procedures, iii) the large number of clients, and iv) the need for subcontracting of works (OECD, 2008).

Unclear provisions

In the revised construction legislation we identified several unclear provisions that give public authorities far-reaching discretional powers unguided by any requirements or guidelines. This discretion might lead to possible abuses among market participants if interpreted by public authorities on a case-by-case basis. Also, the provisions granting discretionary powers to public authorities result in regulatory uncertainty for market participants.

The restrictions that have been identified come from two types of legal provisions: i) a lack of definition of the important notions used in the legislation, or a lack of clear criteria that can be objectively applied by the authorities when taking a decision, and/or ii) far-reaching powers/discretion granted to local authorities. Based on these provisions, authorities can make administrative decisions on a case-by-case basis and may come to different conclusions or interpretations in similar situations, thus favouring one competitor and discriminating against another. This may lead to additional costs for market participants and to an unpredictable business environment for private investors.

Although administrative decisions may sometimes require discretion and the flexible exercise of judgement and decision, legislation should be clear enough not to allow any practical discrimination between undertakings that are active in the same market. Although we do not recommend excessive regulation of all possible situations that might arise in practice, we suggest eliminating the lack of clarity in legislation, either by clarifying the provisions or by giving examples and/or guidelines with clear and objective criteria on how the legislation should be interpreted. Additionally, previous decisions of the authorities on the same subject should be published on its website. Thus, while administrative discretion remains for public administrations, such measures would ensure a higher degree of transparency and reduce unpredictability for the business environment.

Granting parking places on public land

Description of the obstacle

According to Article 33 of Annex 1 of Government Decision No. 525/1996 for approving general urbanism regulation, when requesting a building permit for execution of construction works for a building that, by its purpose requires parking places, the building permit can only be obtained if a minimum number of parking places are placed outside the public grounds (i.e., on private land). Exceptionally, local public authorities can allow the building of parking places on public land.

Two issues arise as regards this legal provision:

-

It is not clear whether the requirement refers solely to new buildings. The legal provision may also be interpreted in the sense that the existence of a sufficient number of parking places is required by the authorities each time a building permit is required for construction works to an existing building (or when the owner changes the existing purpose of the building to a new one);

-

It is not clear whether the local authorities may use public land to grant parking places at their sole discretion.

In order to establish the conditions under which such provisions apply, several cities have concretised the general norm through decisions of their local councils. For example, the Local Council of Bucharest, through Decision 66/2006,32 established that the obligation to have parking spaces for new buildings is not applicable for the city centre and buildings not having access to roads. Moreover, developers building outside the central area of the city have the option to build only 80% of the parking places necessary, provided that they pay the public authority a fee of EUR 10 000 for each parking place not built. The fees collected are deposited by the public authority in a fund for building parking spaces on public land.

Other local authorities, such as Brasov,33 Cluj-Napoca34 and Pitesti,35 have issued similar local council decisions establishing how the parking places available (residential or not) will be assigned to natural persons or legal entities.

Harm to competition

The wording of the legal provision may lead to an arbitrary application of the law on a case-by-case basis, thus leading to heterogeneous practices across various cities or even inside the same city.

First, it is not clear if the obligation to ensure parking places outside public land applies only to newly-built constructions. It seems to be at the sole discretion of local authorities in each city to decide when and where such a requirement is applicable. If interpreted in the sense that parking places are also necessary in each case where a building permit is required for construction work to an existing building or when the owner changes its current purpose to a new one, the owners of existing buildings might be prevented from performing such works (of course, only if the existing building does not have the minimum number of parking places).

Second, due to lack of any clear objective criteria for granting parking places, one undertaking might receive parking places on public land (in exchange for an amount to be paid below the real costs of building a parking space) while another would need to invest significant funds in building its own parking places.

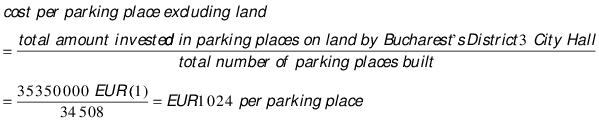

The analysis presented in Annex 2.A2 leads to the conclusion that the cost of each parking space differs from area to area and from city to city. The main influential factor that causes these differences to occur is the cost of land. The range of costs for each parking place (also including the cost of land) is between EUR 2 644 and EUR 49 024 (in central Bucharest). However, on average, the cost per parking place is EUR 11 574 for a ground floor option, EUR 15 121 for the two floors of underground parking and EUR 13 777 for three floors of underground parking. The cost per parking place calculated on each scenario is equivalent to the cost advantage/benefit of a private investor for each parking place granted by the local public authority through the exception identified.36

Policy maker’s objective

The objective of the provision is to provide a solution for the lack of sufficient parking places by allowing public land to be used for the necessary parking places.

Recommendation

We recommend amending the legislation in the sense that the requirement to ensure parking places in order to obtain the building permit is applicable only when erecting new buildings. Furthermore, in order to avoid discretionary application of the legislation by public authorities, the possibility of granting parking places on public land should be limited solely to areas such as city centres, protected areas or areas in which the buildings have no direct access to roads. Each city hall would then establish which areas fall under the exception.

Lack of clear/objective criteria to be used in the control activity of the State Construction Inspectorate

Description of the obstacle

In Romania, the State Construction Inspectorate (SCI) is responsible for controlling and inspecting construction activities, thus ensuring compliance of constructions with the legislation in force, the quality of the construction works and the uniform application of legal provisions in the field. SCI decides on the type of control applicable to each construction process (including the type of control in case of verification of a quality management system), taking into account the complexity of the works. The control applied may be either a regular one (planned control of all important documents and operations which is carried out on the basis of a prior established agenda) or a random one (unplanned control of selective documents and operations).

The legislation in force does not prescribe any criteria for SCI when deciding to pursue random control.

Harm to competition

Due to a lack of clear criteria when assessing the type of control applicable, SCI might discriminate between competing undertakings on the market. There is only limited predictability for the subjects of the random control activities. Those operators subject to random control need to allocate supplementary time resources for controls by SCI.

Policy maker’s objective

The lawmaker has allowed SCI to decide on the type of control applicable to each construction process during the execution phase in order to use its resources efficiently and to prioritise. According to SCI, a “system procedure” could be implemented containing criteria on the type of control (a “system procedure” provides general rules in comparison to an “operational procedure” which provides detailed criteria).

Recommendation

Implement a “system procedure” to be used by the SCI when assessing the complexity of the works and deciding when to apply random controls.

Annexes subject to a demolition permit

Description of the obstacle

Article 8 of Law No. 50/1991 regarding authorisation for the execution of construction works establishes the obligation to obtain a demolition permit prior to any demolition, removal or dismantling, partial or total, of a construction. The constructions that are subject to a demolition permit are not clearly defined in this piece of legislation, as the lawmaker also included the installation annexes in the notion of constructions, a notion which is not explained in the law.

Harm to competition

Lack of definition for installation annexes to constructions, might trigger arbitrary application of the provision by public authorities, on a case-by-case basis. In practice, this would result in discrimination among market participants as the authorities might come to different interpretations when issuing the building permit.

Policy maker’s objective

The demolition permit should guarantee that demolitions of constructions are performed in a safe manner, both for the construction and for the population. The object of the provision is to discourage any potentially dangerous demolition works without obtaining a demolition permit, by including in the buildings subject to demolition permit a broad category of assets of the building.

Recommendation

We recommend to define the installation annexes to construction that are subject to a demolition permit, taking into account what affects the structural stability of buildings.

Different treatment of undertakings in comparable situations

Under the revised legislation, we identified several provisions that limit services/sales of goods without an objective justification. Especially, by limiting the categories of products that can be sold in specific places, by interfering with the business activity of the undertakings depending on their location or by establishing a different treatment towards undertakings active on the market depending on their size, there might be discrimination between undertakings in comparable situations.

Street sales from stalls

Description of the obstacle

According to Article 1 of Law No. 50/1991 regarding authorisation for the execution of construction work, the execution of construction work is possible only after obtaining a building permit. Among the exceptions to this rule, according to Article 11 of the same law, construction work for placing stalls for the distribution and trading of newspapers, books and flowers is exempt from the obligation to obtain a building permit. This exception is applied in cases where the stalls are affixed directly to the ground, do not have foundations or platforms, and are not supplied with any public utilities except electricity.

Harm to competition

Restricting the products that vendors are allowed to sell in stalls may potentially limit the development of businesses of market participants and may also limit consumer choice. These restrictions affect three groups: i) the vendors who already have the respective stalls are restricted to trading only newspapers, books and flowers; ii) the undertakings that are interested in street trading of products other than newspapers, books and flowers do not benefit from the exception, resulting in potentially higher costs for them compared to the “preferred traders” and iii) consumers have access to a more limited variety of products.

Our research in other EU Member States (for example Austria) showed that the differentiation of construction regulations is based on the size of the project but not on the categories of products sold.

Policy maker’s objective

The objective of this provision is to reduce the administrative burden for simple constructions with low complexity. We have not identified the reasons why only stalls selling books, flowers and newspapers are covered by the exception.

We identified street trading regulations in municipalities in Austria, Germany and in the United Kingdom. Street trading provisions in London, for example, foresee an application in writing, including information on the time, date and location of the envisaged street sale, to a local district council. An application may be rejected, among other reasons, if the stall would cause interference or inconvenience to street users or if there are convictions for previous behaviour (e.g. the failure to pay fees or misusing the licence) making a seller unsuitable to hold a licence.

Recommendation

We recommend extending the exemption from the obligation to obtain a building permit to also include all stalls which are directly affixed to the ground, without foundations or platforms and that only need to be supplied with electricity.

However, keeping in mind environmental and public safety considerations together with the public’s right to use the street, we recommend that each city hall issues a public policy with respect to street trading and the conditions under which such businesses may be permitted to operate without a building permit.

The availability of spaces to be used for street trading should be a decision for each city hall and each city hall should implement limits in order to ensure that the undertakings carrying out commercial activities on public land are not abusing this right. It should ensure that vendors are not transforming such stalls into actual stores and that environmental and public safety considerations together with the public’s right to use the street are observed.

Thus, the legislation should provide, for example, the following types of limitations for a stall erected on public land:

-

It shall not lead to, or cause, congestion or block pedestrian traffic on the sidewalk (establishing thus maximum sizes of the stall).

-

Commercial activities would involve a short transaction period necessary for completing the sale or rendering the service.

-

It shall not cause undue noise or offensive odours.

Construction work in coastal areas

Description of the obstacle

According to Law No. 597/2001 regarding certain protection and authorisation measures of construction in the coastal areas of the Black Sea, in seaside resorts and tourist beach areas, it is prohibited to carry out construction or maintenance works between 15 May and 15 September. Starting in 2014, works within a project financed with non-reimbursable external funds, on-going works, seasonal works, urgent works and works that do not affect touristic activities are exempt from the abovementioned prohibition, and are therefore allowed.

Harm to competition

This provision interferes with the business activity of undertakings due to the fact that the interdiction to carry out construction or maintenance works in coastal areas is applicable automatically, without prior assessment of the execution period, location to risk the health and safety of persons made by the local public authority.

In addition, the legal provision discriminates between undertakings carrying out economic activity inside the interdiction zone and those located outside the interdiction zone (i.e. resorts in the mountains or at historical sites) for which there is no such prohibition.

Finally, the large number of exceptions may allow circumvention of the application of the interdiction, considering that the interdiction is not applicable for a project financed with non-reimbursable external funds, on-going works, seasonal works, urgent works or works that do not affect tourist activities.

Policy maker’s objective

The objective of the provision is to keep construction works from interfering with tourist activity during the full occupancy season in coastal areas.

International comparison did not reveal regulations similar to the Romanian legislation on works in tourist areas. In the EU Member States investigated, for example in Croatia, hotels and similar tourist buildings may only be constructed within special spatial areas and have to be built in accordance with regional and municipal zoning plans (thus, rules are established at a local level). In addition, further spatial zoning rules apply to construction in most parts of the coastal area and islands.

In Romania, when issuing a building permit, the local authorities have the power to analyse each case and to regulate the periods when construction can be carried out or prohibited in cases where such construction works may damage the health of the population.37

Recommendation

We recommend to abolish Article 6 of Law No. 597/2001. Any restriction to build should only be established when necessary at the local community level rather than at the national level. Each public authority has the capacity to establish when a construction could affect tourist activities and thus to regulate the time periods when construction can be carried out or prohibited.

Fire protection authorisation

Description of the obstacle

Government Decision No. 1739/2006 for approving the types of constructions for which fire protection authorisation should be obtained establishes that buildings under a specific size (determined in consideration of the number of square metres [m2] of a building and type and the purpose of a building) do not need a fire protection permit.

A fire protection permit certifies the implementation of fire safety measures provided by the law. This permit is mandatory, as a functioning condition, for undertakings owning buildings who carry out their activity in these buildings.

Harm to competition

This provision might create advantages for those enterprises owning small-size buildings.

Policy maker’s objective

Most probably, the lawmaker has considered that small buildings are easier to evacuate.

Recommendation

We recommend abolishing this exception and making fire protection authorisation compulsory for all buildings, irrespective of their size.

Conflict of interest

Description of the obstacle

We have identified several provisions in the revised legislation which might lead to potential conflict of interest between competing undertakings (or potential competitors), mainly due to the involvement of professional associations in the decision-making process of the competent public authorities. Members of professional associations, usually experts in their field, participate and collaborate with public authorities, providing technical expertise, and thus contributing to the decisions taken by the authorities and even control the activity of other competitors, and are subsequently involved in the control carried out by the SCI. Thus, competitors are in a position to (potentially) directly affect competing undertakings. This risk is increased even more by the fact that the national competent authority for controls in the construction sector, the SCI, works together with professional associations on multiple levels.

Romanian law does not provide mechanisms and rules to determine, manage or avoid possible conflict of interest for these specific scenarios.

Examples of the involvement of professional associations in the construction field.

All construction works must be verified by quality experts in all phases of construction. In accordance with Article 23 of Decision No. 925/1995 approving the regulation of verification and technical expertise of quality of projects, execution work and construction, the certificate of the quality experts can be suspended/cancelled by the Ministry of Regional Development and Public Administration (MDRAP), based on a report prepared by a group of three experts. One member of the group must be an expert recommended by a professional association active in the field.

A similar situation was identified in the legislation regarding the measures undertaken to mitigate the seismic risk of existing buildings. According to Government Ordinance No. 20/1994 on measures to mitigate the seismic risk of existing buildings, intervention works to buildings containing a seismic risk are carried out by state authorities (MDRAP) based on a technical solution issued by a designer. Technical solutions are also reviewed by the National Commission for Seismic Risk, a technical body set up by the authority with a consultative role. This commission analyses the technical solution and advises MDRAP, the authority that approves the technical solution. Members of the commission also include experts appointed by professional associations and representatives of employers’ unions in the field. Even though formally MDRAP is not obliged to consider the input received from the National Commission for Seismic Risk when deciding whether to approve or not the technical solution, it is likely that MDRAP follows the advice of the National Commission for Seismic Risk (as its members are the ones providing technical input and expertise).

Additionally, the SCI also works with professional associations in order to develop expertise, prepare research reports and issue technical solutions.

Finally, professional associations also collaborate with public authorities in the field of energy performance of constructions. According to Emergency Ordinance No. 18/2009 for increasing the energy performance of housing blocks, representatives of professional associations in the field of energy performance (such as energy auditors) collaborate with technical committees when approving local programmes for increasing the energy performance of housing blocks. A possible conflict of interest might arise as the energy auditors would be subsequently involved in the control procedure of the SCI. Two provisions are provided in the current legislation:

-

According to Article 31 of Law No. 372/2005 regarding energy performance of buildings, specialists appointed by professional associations in the construction field participate in the checks carried out by the SCI.

-

According to Article 16 of Order No. 3152/2012 approving Control procedures regarding the unitary application of the legal provisions regarding energy performance of buildings and the control of heating/air conditioning systems, the professional associations of construction designers, plumbing engineers, energy auditors, architects and technical experts in air conditioning/heating systems participate in the checks carried out by the SCI.

Thus, energy auditors contribute in the first instance to the technical committees in creating the rules which they then also control by participating in checks together with the SCI.

Harm to competition

In all the cases above, market participants decide on the matters of their competitors. There is a danger of foreclosure of competition, a dictation of the interests of the professional associations, especially against newcomers or so-called mavericks, which aggressively compete in a market, and the possible exchange of sensitive information between competitors. Another negative consequence could be the implementation of unnecessary administrative barriers due to a tendency to standardise interests and actions in cases where the members of private associations may influence the attitude of the public authorities and the legislation in their favour.

Policy maker’s objective

The involvement of professional associations in the decision-making process of the authorities could prove to be beneficial as they come with high expertise. The lawmaker established such a procedure due to a lack of their own experts working in public administration.

Recommendation

We recommend amending the national legislation in order to establish a complete, clear and accessible set of conflict rules to be followed by professional associations. The implementation of an ethical code of conduct should be mandatory for each professional association involved in public decisions. The code of conduct should cover at least rules regarding identification of what constitutes a conflict of interest (i.e., an expert who is part of a technical commission or committee controlling or analysing the issuance of a permit for a competitor), the disclosure procedure and the obligation to abstain from actively participating in the decision-making process of the authority in case of conflict. As a result of this recommendation, each representative of a professional association taking part in a government decision would have the necessary knowledge and tools to disclose the potential conflict of interest and, if this is the case, refrain from actively participating in the activity of the technical commission or committee in question. Such codes of conduct are also implemented in other fields in other Romanian sectors (see, for example, Law No. 7/2004 regarding the code of conduct applicable to public servants or Regulation No. 5/1995 on the code of ethics and conduct of the members and staff of the National Securities Commission).

It might also be helpful (although not a legal measure) to hire more independent experts for the internal structures of public authorities, which would mitigate the risk of conflict of interest. Also, compliance training within the associations and ministries might be helpful. However, this as well as the hiring of experts may be difficult to implement in practice, from the perspective of both the number of experts available and the increased costs for public authorities.

Opportunity notice

Description of the obstacle

In Romania, the functions of an area (such as housing, services, production, circulation, green spaces and public institutions) and the coefficient of utilisation of a terrain (the part of the land that can be used for buildings) are mentioned in planning regulations.

When a private investor wishes to build but the project is not compatible with existing planning regulations, he/she may request a derogation from the existing planning regulations already approved for the respective area. For that purpose, the investor prepares and submits to the public authority (i.e., the local council) a technical document generally called an “opportunity study”. After analysing the opportunity study, the planning and the Territory Arrangement Department within the city hall can issue the opportunity notice. Often, this department is advised by a consultative technical commission (such consultative commissions do not exist in every municipality). The opportunity notice also needs to be approved by the mayor of the municipality. Based on the opportunity notice, the local council can then issue a new zonal urbanistic plan.38

We identified the following issues in relation to this process:

-

As described, the decision of the planning and territory arrangement department within the city hall that issues the opportunity notice is often based on the input given by a consultative technical commission. Each city hall can decide through a local council decision if it wants to set up such a consultative technical commission or not. The technical commission i) has no clear criteria when it advises on the opportunity study prepared by the investor and ii) it is not organised in the same manner in all localities.

-

Upon amendment and based on the opportunity notice, the initial coefficient of terrain usage39 may be exceeded by a maximum of 20%. This limitation applies to all lands except those located in an area with an economic purpose, such as industrial parks, technological parks, supermarkets, hypermarkets, commercial parks, service areas and other similar areas. There are two issues related to this matter: i) for those excepted areas there is no limitation of percentage by which the initial coefficient of land usage may be exceeded, and ii) the notion of “similar areas” is not defined.

Harm to competition

Considering that the consultative technical commissions are not organised in the same manner in all counties and that there are no clear criteria when giving input for changing existing urbanistic plans, this might lead to arbitrary advice in granting the opportunity notices.

As regards the coefficient of land usage:

-

The lack of a definition for the notion of “similar areas” may lead to an uneven application of the law by the local authorities and discrimination may take place between market participants.

-

The possibility for the land located in areas designated to be of economic interest should have different coefficients of land usage.

Lawmaker’s objective

We have not identified any objective concerning the organisation of the consultative technical commission. As regards land usage, according to the official recital, the objective is to allow economic and industrial development in certain areas in accordance with local economic interests.

Recommendation

The legislation should be amended in order to ensure that the technical commissions have the same organisational structure in all localities. Also, MDRAP should prepare a checklist and clear elements should be taken into consideration by the consultative technical commission when advising the planning and territory arrangement department within city hall with respect to the opportunity study.

In order to limit possible differing interpretations of “similar areas”, we recommend either defining the notion of “similar areas” or eliminating it from the exception. In all cases, the lawmaker should set a threshold for the changes that can be made to the usage coefficient for land located in areas destined for economic activity.

Technical approvals

General description of legal framework

Technical approval, also called a technical agreement, is a favourable technical assessment regarding the use of new products, procedures or equipment for which there are no national standards or other official technical regulations in force, or the existing standards or rules are not completely suitable for the products, procedures or equipment. Technical approvals are required for a wide range of products including building materials.

The applicable legislation and issuance mechanism is different for harmonised or non-harmonised products:

-

For non-harmonised products, the technical approvals are elaborated by specialised entities which must be Romanian legal persons or associations of Romanian legal persons. The elaboration entities are private companies. According to data from the Standing Technical Council for Construction (CTPC) website,40 there are currently 12 such entities active on the market. The elaboration entities must be authorised by the CTPC, a public supervisory body under MDRAP. The CTPC also approves the technical approvals issued by elaboration entities.

-

For harmonised products, EU legislation (mainly EU Regulation No. 305/2011 setting forth harmonised conditions for the marketing of construction products and repealing Council Directive 89/106/EEC) is directly applicable in Romania. In this case, the technical approval that is to be obtained by each manufacturer and applicable at the European level is called a European Technical Assessment (ETA). It is elaborated by technical assessment bodies (TABs). TABs are private Romanian entities notified to MDRAP, as providing this type o work. According to data from the CTPC website,41 there are currently three such entities active on the market.

For further reference, please see Figure 2.6Relationship between several institutions for issuance of ETAs in Section 2.1 of this chapter.

Issues identified in the relevant legislation with respect to technical approvals for building materials

We identified several restrictions to competition. One of them consists of the composition of the CTPC and the participation of competitors in the authorisation process of the elaboration entities. The CTPC is formed, among others, of representatives appointed specifically by such existing elaboration entities. This means that the entities elaborating technical approvals are in a position to influence the decision of the CTPC according to their own interests. This is an issue of conflict of interest, similar to that described in Section 2.2.3 above. For such cases, we also recommend that national legislation be amended in order to establish a complete, clear and accessible set of conflict rules to be followed by the CTPC.