6. Setting sail for sustainability: Opportunities and tools for fostering a blue recovery

The global COVID-19 pandemic has severely affected Fiji, hitting at the heart of its backbone economic sectors, such as international tourism and export fisheries. However, the COVID-19 crisis has also brought to the fore the need to embark on a more sustainable model of development and is offering an opportunity to shift to a new, more sustainable development trajectory. This chapter provides an initial mapping of promising initiatives and actions that could be further explored, developed and scaled up, as part of a sustainable blue recovery. These initiatives focus on four key areas that show the potential to generate benefits across the broader economy and to drive a sustainable recovery: sustainable fisheries, sustainable tourism, green shipping and marine conservation. It also highlights examples of innovative financing mechanisms that could advance these ambitions.

The global COVID-19 pandemic has severely affected Fiji, hitting at the heart of its backbone economic sectors, such as international tourism and export fisheries. The government was able to put in place response measures, including thanks to international support and relief. Combined with increased spending to counter the pandemic, the international funding alleviated the pressure produced by unprecedented revenue losses. The population showed great resilience, and was able to stay afloat thanks to government measures, as well as access to traditional resources, such as subsistence fisheries and subsistence farming, and mutual solidarity. However, the COVID-19 pandemic brought to the fore the need to embark on a more sustainable model of development. Such a model needs to rest on a more diversified economy, more diffused socio-economic benefits across the population, and a sustainable use of natural capital that considers the growing impacts from climate change and other anthropogenic pressures. As in many other countries, the COVID-19 pandemic is providing Fiji with a wake-up call and an opportunity to shift to a new, more sustainable development trajectory.

This shift, however, will not happen by itself. It will need to be steered by a coherent, unified vision and direction for a recovery that is truly sustainable. Fiji’s National Ocean Policy provides critical guidance in this respect, and its ambition and vision now need to consider opportunities and challenges stemming from the COVID-19 crisis. Ocean economy sectors, which are the foundation of Fiji’s economy, can be the centre of the recovery. They can lead a transformation that will generate positive change across economic and social areas of the whole economy. This will require policy measures and actions that take into account the complexity of inter-sectoral interactions and integrate environmental, social and economic values (OECD, 2021[1]). This will also require mobilising adequate resources across sectors, from both public and private sources, through a financing strategy that incorporates a coherent range of financial instruments and approaches.

This chapter provides an initial mapping of promising initiatives and actions that could be further explored, developed and scaled up, as part of a sustainable blue recovery. These initiatives focus on four key areas that show the potential to generate benefits across the broader economy and to drive a sustainable recovery. These areas also show strong linkages across them, reaffirming the need for integrated, cross-sectoral policy making and actions. For instance, efforts to green the shipping sector in Fiji will not only demonstrate leadership towards net zero emissions (although Fiji’s emissions are negligible at the global level). They will also reduce the costs of shipping services that depend on expensive imported fuels. In addition, they will create opportunities for enhanced inter-island connectivity that could increase the contribution of local supply to the tourism sector, provide opportunities for greater domestic tourism and generate other market development opportunities. The chapter also provides an initial overview and discussion of promising financing instruments and approaches that could mobilise an array of funding sources to help achieve the ambitions of a blue recovery.

The Fijian fisheries sector is largely focused on tuna, specifically catch fisheries within the Exclusive Economic Zone (EEZ). The country has the largest fishing capacity of any nation in the region, with most other Pacific Island Countries and Territories (PICTs) selling fishing rights to distant water fishing nations (SPC, 2021[2]).

The Pacific Community has conducted several stock assessments with the latest finding that the Fijian tuna stock is sustainably managed (Hare et al., 2021[3]) This assessment holds that the current level of effort, regulated primarily by licensing, can ensure that yield does not affect the capacity of the fish population to recover between fishing seasons. However, this finding is rooted in the present, based on past fishing activity (SPC, 2021[2]). Studies suggest that as the climate continues to change, with the ocean surface warming and the distribution of oxygen changing, the tuna population is likely to migrate. This migration has not been factored into long-term fisheries management and it represents a risk for an undiversified fishing sector (Dey et al., 2016[4]).

Fiji’s main interest in tuna is the export of fresh tuna via commercial air carriers, and the trans-shipment of frozen fish. The most lucrative of these products are the fresh fish, with the product consumed primarily in the United States and Japan, with a smaller market in Europe. The pandemic affected both export routes. Commercial air carriers almost ceased international activities completely and shipment schedules became unreliable.

In a post-COVID 19 market, flights are resuming as of February 2022 and shipments are becoming more regular, thereby restoring export channels to cater to the demand that has not declined globally. The secondary interest in tuna is in the cannery industry, with tuna processed in Fiji being canned and shipped around the world. However, this is a lower value product and makes up a small part of the sector.

The climate risks and reliance on export channels show the fisheries sector represents an ideal opportunity for diversification, both for economic growth and enhancing social and economic resilience to global and/or regional catastrophes analogous to COVID-19 (Dey et al., 2016[4]). The Ministry of Fisheries has highlighted an interest in developing its aquaculture capacity. To date, aquaculture has largely been small-scale and focused on the production of pearls for the luxury goods and jewellery industry. The ministry perceives aquaculture (including mariculture) as a means to grow the fisheries sector and provide a source of economic and food security to the local population in times of crisis (Republic of Fiji, 2020[5]).

The role of aquaculture as a secure source of nutrition in times of stress has been a driver of industry development in many Southeast Asian (SEA) countries (Béné et al., 2016[6]). Of potential environmental co-benefit is the relationship between aquaculture as a source of food and the maintenance of protected area regulations during times of crisis. During the height of the COVID-19 pandemic, many Fijian mainlanders moved back to island communities and began to place greater fishing pressure upon natural resources. In some cases, this meant breaking protected area rules and, often unintentionally, breaking licensing regulations. Through equitable planning processes and training, aquaculture could provide a source of relief to natural resources under similar circumstances in the future.

In the Asia-Pacific region, the aquaculture industry – with goals focused on enhancing food security – has typically been grown in a public-private partnership format, with government agencies providing subsidies and forms subsidies and forms of supply chain support for operators (Weirowksi and Liese, 2010[7]). The governments of many major aquaculture exporters typically play a role in training stakeholders; provide brood stock; and provide or support access of aquaculturists to feed stocks. . Though their support in acquiring and retaining land tenure rights and accessing subsidies has contributed to the degradation of coastal ecosystems throughout the region, which highlights the need to carefully design any subsidy to ensure that it has robust environmental controls and contingent upon sustainable operations. Such a role for the Ministry of Fisheries has been highlighted in the draft National Fisheries Policy (Republic of Fiji, 2020[5]). However, extensive public developments, or private industry stakeholder investments, will need to scale alongside small-scale stakeholder participation. Many public stakeholders also contribute significantly to research, including in new species, disease control and prevention; pollution control measures; and sustainable low-cost feed stocks, and/or hatchery technologies.

The Ministries of Fisheries and Economy have highlighted a number of products that could be targeted for aquaculture growth in the 5-year and 20-year National Development Plan (Ministry of Economy, 2017[8]) and the National Fisheries Policy Draft (Republic of Fiji, 2020[5]). These commodities include:

tilapia (Ministry of Economy, 2017[8]; Republic of Fiji, 2020[5]),

prawn and shrimp (Ministry of Economy, 2017[8]; Republic of Fiji, 2020[9]),

seaweed (Ministry of Economy, 2017[8]; Republic of Fiji, 2020[5]),

niche markets: seagrapes, bêche-de-mer, marine fish (Ministry of Economy, 2017[8]),

Tilapia and prawns/shrimp are commodities produced intensively by Asian producers, which make up 70% of the market (FMI, 2021[10]). Both groups or organisms require a fresh/brackish water pond or closed systems. Intensive growth in production could result in widespread land conversion or tank development demands. These have driven environmental challenges throughout the Southeast Asia (SEA) region, particularly as a major driver of mangrove degradation and deforestation (Hishamunda et al., 2009[11]). Sustainable production of both groups of organisms requires site selection practices that mitigate or completely avoid the degradation of coastal ecosystems. The environmental impact of specific species of tilapia has been observed to lessen through the application of technologies that use less water/production unit and allow more efficient nutrient use (de Godoy et al., 2022[12]). With regard to habitat loss, the environmental impact assessment (EIA) and licensing process outlined in the Aquaculture Decree 2016 and the forthcoming National Fisheries Policy (Republic of Fiji, 2020[5]) may provide the necessary protections to avoid the widespread ecosystem degradation seen in many SEA countries. However, these mechanisms have not yet been tested extensively.

The sustainability of shrimp and prawn aquaculture is challenged by a series of factors that include land conversion, disease outbreaks, invasive species and wastewater management (Phillips, 1995[13]). Recent industry improvements have addressed major concerns in the sustainability and environmental footprint of production. These improvements include pond management techniques to reduce crowding and nutrient and toxin build-up; the recognition of the value of mangroves to shrimps; and incentives to maintain the ecosystem (Macusi et al., 2022[14]). Even among advanced aquaculture industries, not all issues have been resolved. This highlights the challenge in entering a market with a significant stigma generated by environmental impacts. A number of emerging technologies and new developments can be applied to improve economic and environmental sustainability. These include investment in closed systems with careful disease controls (Hishamunda et al., 2009[11]), and exploring the use of biofloc approach to rearing shrimp larvae (Emerenciano, Gaxiola and Cuzo, 2013[15]). However, sustainability in aquaculture requires extensive training, sustainable land-use planning and the necessary investment to ensure availability of appropriate technologies. In addition, research must keep up with challenges, such as tank/pond management, feed sources and disease outbreaks.

Mariculture opportunities include seaweed farming and a potential exploration of expanding pearl production, and an evaluation of the farming of sea cucumbers.

Seaweed farming is a growing form of mariculture in the region (Subasinghe, 2017[16]) with markets for the product across Asia. However, there are significant variances in species preferences according to the culinary application and the country. Throughout SEA, seaweed is grown by large-scale and small-scale stakeholders. Growing the local Fijian industry could focus on adding value through intercommunity collaboration, identifying ideal locations for production and linking these areas with ideal locations for drying and processing. However, support will be needed for production and to enhance market access for small-scale stakeholders. The primary consumers of the product are in Asia. Consequently, significant work will be required to access the market due to the distance between the supplier and the consumer. In addition, local producers will need to be trained to culture the appropriate species and process them to meet consumer demands. Pursuing growth will provide co-benefits, including climate change mitigation through the capacity of seaweed to sequester carbon dioxide from the atmosphere and regulate local dissolved CO2 in the coastal zone. However, shipping will likely cancel out some of the removals.

Sea cucumber farming is growing in popularity to meet the demand of the Chinese market primarily, although sea cucumbers are also consumed throughout the region, including in Fiji. There is a significant variance in value of sea cucumbers. Certain species generate hundreds of dollars per kilo, while others generate much less. For the vast majority of sea cucumber farming practices, the juveniles are collected from the immediate environment and then reared in pens in the tidal zone. As such, it is possible to overexploit the local population. Developing the local industry, particularly as an export commodity, will face legal challenges. Export of sea cumbers has been banned since 2017 in response to local populations dropping to densities below which natural populations can be sustained. The Ministry of Economy’s 5-year and 20-year National Development Plan (Ministry of Economy, 2017[8]) and the Ministry of Fisheries’ draft National Fisheries Policy (Republic of Fiji, 2020[5]) both identify bêche-de-mer for development. They are perhaps focused on growing the domestic market for the commodity. Blue Ventures has had success in developing local capacity and market access in Madagascar and provides a potential model for replication and scale (Arnull et al., 2020[17]).

To create a strong aquaculture export and domestic market that can compete with others in the region the Ministry of Fisheries must likely play a strong supporting role in the industry, particularly for small-scale stakeholders. The price point for products may not be competitive or profitable if only private stakeholders support the supply chain for the pond/tank rearing of fish. In Fiji there are private fisheries producer that represents an ideal partner for scaling-up of the industry. It could be both a supplier in the export market and a potential provider of basic aquaculture supplies, including brood stock and feed. Investments in these private partners will be critical for industry growth. However, the government will need to fill in gaps to provide a full range of support, while minimising public-private competition and inefficiencies. At the basic level, the ministry will likely play a leading role in providing or subsidising access to feed stock and brood stock for scaling up businesses and incentivising the entry of small-scale producers. The provision of these resources would incur consistent operating costs, including up-front costs in training, personnel, technology and tank infrastructure.

The University of Fiji is conducting a series of aquaculture pilot projects with the support of the Japan International Cooperation Agency, including many on species of interest to the Ministry of Economy (Ministry of Economy, 2017[8]) and the Ministry of Fisheries (Republic of Fiji, 2020[5]). The projects are exploring a broad range of aquaculture technologies and applications to identify pilots worthy of further investment and scaling. For its part, the University of the South Pacific through its aquaculture programme is offering a range of courses in aquaculture. It is also supporting development of foundational knowledge and skills to grow the base of practitioners in the country.

Before the COVID-19 pandemic, the tourism sector had been marked by sustained growth and came to represent the bulk of Fiji’s economy, but its prospects are now uncertain, both in Fiji and globally. Different futures are possible. One scenario is the return to pre-pandemic trends. Another possible scenario is a transform towards a more sustainable sector that puts local well-being and revitalisation of natural capital at the centre. Yet another scenario is that the tourism sector could decay, undermined by climate change and the significant reduction of long-haul intercontinental travel due to COVID-19. Some of these scenarios are explored in Yeoman et al. (2022[18]).

For a country like Fiji, each possible future will be affected by a number of external factors. These include developments in the COVID-19 pandemic, health measures and emission targets in other countries. Other factors include the impacts of protracted uncertainty and/or changed environments on international tourists’ preferences. Nonetheless, the government of Fiji still retains control over rules, regulations and policies that can shape the future of the tourism sector. One track leads to regeneration of communities, cultures, heritage and natural capital, while the other leads to greater social and environmental unsustainability.

Fiji needs clear targets and requirements, as well as adequate incentives and support, to ensure more sustainable development of the tourism sector in support of a sustainable recovery. This should target a number of critical areas, including energy efficiency, use of renewable energy, waste management systems, use of local supply, zoning and protected areas, labour rules and health requirements. These targets and requirements will aim to foster backward and forward linkages with the rest of the economy, ensure strong local returns and directly contribute to advance the conservation and restoration of natural habitats and wildlife. Currently, the National Development Plan mandates sustainable energy use, enforcement of building codes related to energy efficiency and enhanced waste management in the tourism sector. However, a lack of targets, roadmap and support measures to achieve them seems to have stalled progress.

The tourism sector is composed of a diffused ecosystem of private players. Consequently, the government will need to work closely with tourism associations and private sector representatives to ensure stakeholder ownership and co-operation towards a more sustainable tourism sector. Interviews for this report highlighted that closer consultation and collaboration between the government and the tourism private sector were established during the COVID-19 pandemic. This helped prepare for the opening of borders and to define enhanced safety standards, protocols and COVID-19 mitigation practices needed to improve traveller safety. Fiji can build on this growing relationship by creating a stable mechanism for government and the tourism private sector to collaborate on the definition and monitoring of shared objectives. This will be particularly important in light of the government’s emerging strategy for the tourism sector.

The paragraphs below highlight opportunities and examples that can be built upon to develop Fiji’s tourism more sustainably for a sustainable blue recovery.

Growing energy efficiency and sustainability: Linking fiscal incentives for hotel renovations under COVID-19 to enhanced sustainability standards

Standards and incentives in the tourism sector can help Fiji move towards a low-carbon, climate-resilient development pathway. Fiji has made several commitments domestically in the national development policy (NDP) and internationally in its Nationally Determined Contribution (NDC), to increase electricity generation from renewable energy sources to 100% by 2036. Additionally, Fiji seeks a 30% reduction in greenhouse gas (GHG) emissions by 2030 from the 2013 baseline (NDP and NDC). Third, it wants to ensure access to affordable, reliable, modern, sustainable energy, increasing the share of renewable energy and expanding infrastructure and upgrading technology for equitably supplying modern and sustainable energy services. Since 2013, however, a number of off-grid resorts have introduced solar and battery systems to cover all or part of their electricity demand. Wind energy, instead, continues to play a small role in electricity generation (UNFCCC, n.d.[19]). To move away from diesel consumption and meet energy generation demand of off-grid hotels, further expansion of solar PV and wind energy have been identified as key priorities.

Investing in energy efficiency in the tourism sector can also underpin economic recovery, as well as create healthy spaces, increase energy security, boost employment and productivity, and move closer to the achievement of climate goals. On 24 March 2022, the Fijian Ministry of Economy announced the 2021-22 revised budget measures. These included a 12-month further extension of the five-year income tax holiday regime for investments in hotel renovations and refurbishments until 31 December 2023. This measure is a valuable contribution to help restart the tourism sector. However, without links to energy efficiency standards and requirements, this measure misses the opportunity to help shift the trajectory of Fiji’s tourism sector and its contribution to a blue recovery.

Besides energy efficiency, the tax holiday regime for investments in hotel renovations and refurbishments could be connected to materials and circular economy. In particular, it could develop closed-loop systems, reduce the use of virgin materials, and increase the potential of bio-based materials (UNEP, 2020[20]). This could further lower energy and cooling demand and provide sustainable cooling solutions for resilience and adaptation.

In September 2020, the Global Alliance for Buildings and Constructions (GlobalABC) issued a call to include building renovation and modernisation in COVID-19 recovery plans. It recommended a massive renovation wave – spurred by tailored support mechanisms and designed with national and local stakeholders – to make the building stock more energy-efficient. The Platform for REDESIGN 2020 highlights examples of such actions. REDESIGN 2020 is an Online Platform on Sustainable and Resilient Recovery from COVID-19 supported by the Japanese Ministry of the Environment, the United Nations Framework Convention on Climate Change and the Institute for Global Environmental Strategies. Examples within REDESIGN 2020 include commitments by the European Union in the Renovation Wave, the United Kingdom in its Public Sector and Social Housing Decarbonisation schemes, and France in its support of public housing and public buildings.

Reducing food import vulnerabilities: The experience of hotels’ food gardens and the example of the Contemporary Island Cuisine Training

There is great potential in strengthening the links between the three large sectors of tourism, agriculture and fisheries/aquaculture to maximise economic benefits to the local economy. Fiji’s tourism sector relies largely on imported produce because it provides a steady supply, high quality and prices that are sometimes lower than local produce. Overall, however, the food import bill is a significant cost driver for Fiji’s tourism sector, estimated at FDJ 794.9 million in 2017 (IFC, 2018[21]). The strong reliance on imported foods also limits opportunities to use touristic experiences for bringing to fruition and strengthening linkages with the culture and heritage of the country. Fiji’s arable land stands at 9% of its territory (World Bank, 2022[22]). However, channelling resources to grow or produce certain fresh produce items locally could potentially cut down Fiji’s food import bill by FDJ 24.1 million (USD 11.8 million) (IFC, 2018[21]).

The COVID-19 crisis may be giving impetus and accelerating progress in this direction. In the wake of COVID-19, food imports had become both more expensive and more difficult to access. This disruption of value chains has pushed several hotel chains to turn to local production. Several chains have established food gardens and even set targets to achieve larger shares of locally produced food (Table 6.1).

Promoting consumption of local foods will require a change of mindset, a focus on locally grown and produced food, and innovative ways to substitute locally available produce in local and international menus. Moreover, increasing consumption of local production is also an important ally in reducing transportation-related emissions. Raising awareness of tourists, chefs, kitchen staff and purchasing managers will be an important part of fostering greater use of local produce.

The Fijian Ministry of Agriculture and the Ministry of Industry, Trade and Tourism have been working with the Fiji Hotel and Tourism Association to raise awareness through the Contemporary Island Cuisine Training. This annual event showcases innovative Fijian menus to interested budding and experienced local chefs. This initiative promotes use of locally grown produce on resort menus and beverage lists. It also connects farmers and communities with chefs, while introducing Fiji’s young chefs to new ways to treat local produce. As they understand the resorts’ demand, farmers are then encouraged to plant and supply local produce accordingly. In doing so, they generate more local income for their own livelihoods and their communities.

Development co-operation providers could support sustainable sourcing, drawing on positive examples in other countries. In the Seychelles, for instance, the International Fund for Agricultural Development (IFAD) is partnering with hotels and resorts on sustainable agricultural projects. They aim to keep imports to a minimum and ensure these accommodation facilities only source local produce from inclusive and environmentally conscious practices. Through the organic vegetable garden on the resort and the IFAD partnership, for instance, the Hilton Seychelles Labriz Resort & Spa now sources over 80% of its vegetables locally.

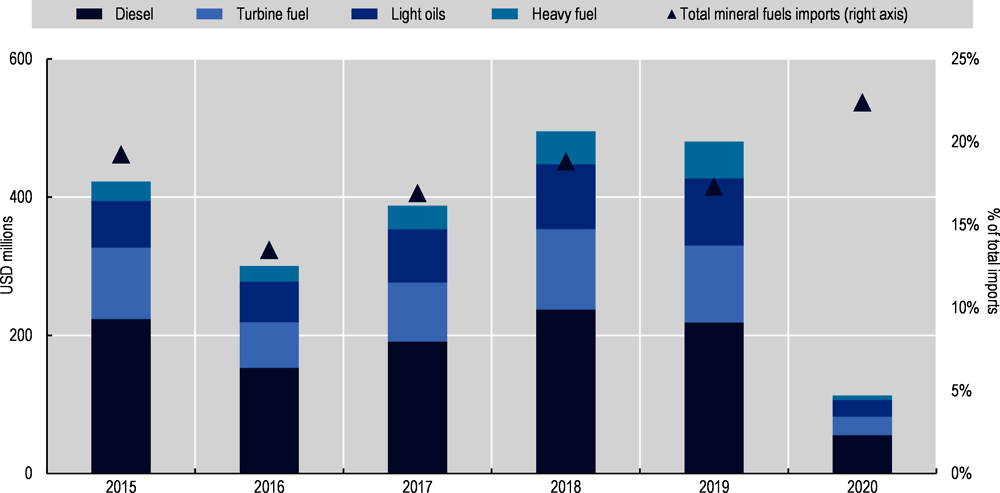

Fiji’s fuel imports represent a growing cost on Fiji’s import bill and have adverse environmental impacts. In monetary terms, fuel imports represented USD 420 million in 2005 and USD 650 million in 2008 (Holland et al., 2014[24]). In 2020, despite the drop following the COVID-19 pandemic, fuels imports in Fiji accounted for 25% of total imports (Figure 6.1). Maritime transport accounts for over 20% of domestic fossil fuel imports (Holland et al., 2014[24]). Total emissions from maritime transport in 2016 are estimated at 214 Gg of CO2e and could reach 342 Gg of CO2e in 2040 under a business-as-usual scenario (Prasad and Raturi, 2019[25]). The same estimate suggests that fuel consumption could rise from 79 million to 127 million between 2016-40, assuming a 2% annual growth rate in maritime passenger and freight activity. Additionally, Fiji’s Low Emission Development Strategy estimates total emissions for the Fiji maritime sector at 174 kt of CO2 in 2016. Passengers and cargo shipping accounted for more than one-third of total emissions in 2016 (Table 6.2). The contribution of fishing to domestic emissions relates to the use of two-stroke outboard motors, which are cheaper than other options but fuel-intensive, making them the least efficient type of small motor (Newell, 2020[26]).

Investing in alternative fuels, fuel efficiency measures and clean technologies can reduce dependency on fossil fuels and make Fiji less vulnerable to external shocks.

Substituting fossil fuel in uneconomical routes can reduce dependency on fossil fuels and have positive effects to other segments of Fiji’s maritime sector. Fiji has ten uneconomical routes that are unattractive to private operators within the Lau Group islands. These routes are under the Fijian Government Shipping Franchise Scheme (GSFS), which funds 42% of the cost of the fuel originally implemented to attract private operators. Introducing technologies such as the four Flettner rotor can reduce carbon emissions by in 7 327 tons (Table 6.2). Although they account for a small share of Fiji’s emissions, they can serve as a first step to diffusing innovative low-carbon and fuel-saving options. For instance, the Flettner rotor and the Greenheart Project vessel have an estimated installation cost of between USD 1-2 million. In 2018/19 alone, the Fijian government spent USD 1.06 million in subsidies for uneconomical routes.1 Searcy (2017[28]) estimates the gradual reduction of GSFS subsidies more than compensate government's efforts to promote fuel efficiency and can actually result in savings over 20 years. Scaling up such technologies that are at the demonstration and prototype stages as soon as possible is urgent to ensure achievement of zero emissions by 2050.

In addition, according to Prasad and Raturi (2019[25]), implementing fuel-efficient measures such as reducing speed of certain vessels alleviates diesel consumption by 5.2%.2 Cleaner fuels such as biodiesel blend (B5) can decrease diesel consumption by almost 4%, from 97 to 93 million litres. Fuel products derived from coconut oil can be easily blended with diesel (e.g. coconut-derived biodiesel) and help reduce Fiji’s reliance on imported fossil fuel.

Two pilot projects are exploring maritime solar energy across Pacific SIDS. This is part of the Global Maritime Technologies Cooperation Centres (MTCC), funded by the European Union and implemented by the International Maritime Organization (IMO). Vanuatu and Samoa hosted the MTCC-Pacific Pilot projects with cost savings estimated between USD 45 050-48 053 and GHG emissions reductions between 101-135 tonnes annually (Bola, n.d.[29]). Solar systems for vessels can be installed in all vessels in Pacific SIDS, independent of age. Moreover, the technology is already available and could be immediately adopted by Fiji’s ageing fleet.

The Sustainable Sea Transport Initiative (SSTI) is another example of efforts in Fiji and in the Pacific to develop an efficient sustainable sea transport. SSTI has developed a pilot project and a first prototype sailing ship in partnership with the University of Queensland.

Reviving traditional knowledge is an opportunity to build resilience and reduce dependency on fossil fuels. The use of small canoes and traditional watercraft such as the camakau is associated with reduced reliance on fossil fuel and is part of Fiji’s national Maritime and Land Transport Policy (Ministry of Infrastructure and Transport, 2015[30]). In the Pacific, several countries have turned to these options. In 2018, the government of the Marshall Islands added its first sailing cargo vessel to service national waters (GIZ, 2021[31]). The acquisition is part of the Transitioning to Low Carbon Sea Transport project formed between the Marshall Islands and GIZ that has been extended to Fiji as announced at COP 26. One objective is to develop and pilot-test low-carbon propulsion technologies in co-operation with partners. The initiative poses a great opportunity to scale prototypes such as the Flettner rotor and the Cerulean project vessel. The Drua is an example of Fijian traditional knowledge that can be used as an alternative to fuel-dependent engines. These vessels are made out of native wood and coconut fibre, and are completely metal free (UNFCCC, 2017[32]). They require two crew members and can carry up to ten passengers.

Regulation and market-based measures are key to increase the appeal of low-carbon alternatives.

Across the Pacific, taxes and levies have been adopted to increase the competitiveness of reducing emissions. For instance, the Marshall Islands and the Solomon Islands proposed a levy of USD 100/tCO2-eq emitted by vessels starting in 2025. If implemented, the levy would increase either annually or every five years by 30% or 100% (IEA, 2021[33]). Additionally, to ensure that new technologies are effective in reducing Fiji’s reliance on fossil fuels, regulation must ensure that imported vessels can incorporate these innovations. Most 20-year-old vessels, which are the majority of Fiji’s fleet, have lower fuel economy, especially if not maintained properly (Prasad and Raturi, 2019[25]). Further, encouraging the purchase of vessels with engines certified to operate on biodiesel or biodiesel blend can help promote decarbonisation of Fiji’s maritime fleet.

Bilateral and multilateral partners have been supporting domestic and regional shipping decarbonisation (Table 6.3). Led by the governments of Fiji and the Marshall Islands, the Pacific Blue Shipping Partnership seeks to mobilise USD 500m to foster renewal of domestic fleets across the Pacific until 2030. The governments of Fiji, the Marshall Islands, Solomon Islands, Tuvalu and Vanuatu announced the partnership at the UN Secretary-General’s Climate Action Summit in 2019. Scaling up technologies at demonstration and prototype stage is key to modernise fleets across the Pacific, ensuring a 40% reduction in emissions by 2030. The Cerulean project is a joint research and development collaboration between Swire Shipping and the University of the South Pacific’s Micronesian Centre for Sustainable Transport. With trials expected by the end of 2022 and 2024, the vessel is expected to deliver GHG emission savings of more than 25% (Maritime UK, 2021[34]).

Marine protection in the country is distributed between three primary mechanisms: the locally managed marine areas (LMMAs), formal marine protected areas (MPAs) and marine conservation agreements (MCAs) between communities and the tourism sector. Most area-based management tools in the country are LMMAs (Techera et al., 2009[35]).With LMMAs, responsibility for management rests with community leaders, who are supported by government ministries and a number of non-governmental organisations (NGOs) and consultants. These areas are managed sustainably by regulating permitted activities to minimise ecological degradation that could otherwise be caused by land-based pollution sources and unsustainable fishing practices. The types of management differ according to the area being managed. Local communities make key decisions with partners engaged for advice. In some cases, the areas are completely closed off to fisheries activities, but the large majority employ regulations that limit damaging practices (Jupiter et al., 2014[36]).

There are four inshore protected areas in Fiji, although the Ministry of Fisheries holds a mandate to designate 30% of the Exclusive Economic Zone (EEZ) as protected areas by 2030. The Protected Area Committee (PAC) has led identification of a network of areas that, if protected, would act to safeguard major hotspots of biodiversity throughout the country. The draft selection of areas is undergoing review and stakeholder consultation.

The emerging blue bond is geared towards funding marine protection as one area. Protecting marine resources generates value indirectly for fisheries. It potentially enhances and replenishes the long-range fisheries stock and enhances stability of the fishery – under effective and science-based management processes (Garcia, Ye Yimin and Charles, 2018[37]). From a return-on-investment perspective, tourism is the most direct source of economic value that MPAs generally provide. The preservation and maintenance of biodiversity can be used to encourage tourism and direct and indirect revenue. However, the offshore strategy makes it challenging to generate revenue from tourism because it is difficult to access most areas. This, in turn, creates the perception that protection directly generates a return on investment among prospective investors in the bond.

Tourism may be a potential, though small, source of finance for the management of protected areas set up through MCAs between local communities and locally based tourism operators. A draft policy brief by the PAC recommended establishment of a trust fund to pay for Fiji’s network of marine and terrestrial protected areas. It suggested potential ideas for generating revenue (e.g. environmental levies, debt-for-nature swaps, etc.) should be further explored. In contrast, employing a tourism-based approach to generate the funding necessary to manage 30% of the EEZ effectively as a no-take zone is difficult given the need to generate tourism interest in and support access to these areas. The management of the broader offshore MPA strategy will require an influx of revenue and technological innovations to reduce the resource demands of effective management.

Centralised funding models from other parts of the world could be modified to fit the demands of the country and meet some of the needs for near-shore, small-scale protected areas management. In the Philippines, the National Implemented Protected Area System (NIPAS) Act established a system where tourism revenue to each of the designated areas is centralised into the Integrated Protected Area Fund. The fund is managed by the Department of Environment and Natural Resources (Republic of the Philippines, 1992[38]). That fund is then used to provide management funding to each of the NIPAS areas to ensure they receive a baseline source of finance with the capacity to cover primary management costs (La Viña, Kho and Caleda, 2010[39]). Each area fundraises on top of this baseline. However, the system ensures that difficult-to-access areas for tourists still receive a level of funding for management that they would otherwise have had to generate through other means. In Fiji, an analogous approach could be applied at a more local level, grouping nearby LMMA managing communities. This could focus on funding management needs and supporting diversification of their marine economic assets. Any fund created in this scenario would likely be better managed through a community-based organisation or partner to ensure flexibility and greater impact.

An analogous system applied in Fiji would likely have to be split into two parts. One part would be managed by the Ministry of Fisheries (for offshore), including all MPAs. The second would cover all the LMMAs. It would be jointly managed by the Ministry of Fisheries and iTaukei Affairs Board (who have appointed conservation officers based in the provincial offices), with a steering group of representative community leaders.

References

[17] Arnull, J. et al. (2020), “Biophysical site-suitability summary for community based sea-cucumber aquaculture, Southwest Madagascar”, commissioned by the Prince Albert II of Monaco Foundation, Project No. 2505, Blue Ventures, April.

[6] Béné, C. et al. (2016), “Contribution of fisheries and aquaculture to food security and poverty reduction: Assessing the current evidence”, World Development, Vol. 79, pp. 177-196, https://doi.org/10.1016/J.WORLDDEV.2015.11.007.

[29] Bola, A. (n.d.), “Low carbon, safe, accessible, and affordable maritime transport”, Maritime Technology Cooperation Centre – Pacific, http:////www.pacificmet.net/sites/default/files/inline-files/documents/3.5%20MTCC-Pacific%20Pilot%20Project%20Update%202021_PICOF_3.5.pdf.

[12] de Godoy, E. et al. (2022), “Environmental sustainability of Nile tilapia production on rural family farms in the tropical Atlantic Forest region”, Aquaculture, Vol. 547, p. 737481, https://doi.org/10.1016/J.AQUACULTURE.2021.737481.

[4] Dey, M. et al. (2016), “Economic impact of climate change and climate change adaptation strategies for fisheries sector in Solomon Islands: Implication for food security”, Marine Policy, Vol. 67, pp. 171-178, https://doi.org/10.1016/J.MARPOL.2016.01.004.

[15] Emerenciano, M., G. Gaxiola and G. Cuzo (2013), “Biofloc Technology (BFT): A review for aquaculture application and animal food industry”, in Biomass Now – Cultivation and Utilization, InTech, https://doi.org/10.5772/53902.

[27] Fiji Bureau of Statistics (n.d.), Latest Key Statistics Release, https://www.statsfiji.gov.fj/index.php/latest-releases/key-stats (accessed on 19 May 2022).

[10] FMI (2021), “Tilapia market by source, form & application for 2021–2031”, Tilapia Market – Analysis, Outlook, Growth, Trends, Forecasts, Future Market Insights, https://www.futuremarketinsights.com/reports/tilapia-market.

[37] Garcia, S., J. Ye Yimin and A. Charles (2018), “Rebuilding of marine fisheries”, Fisheries and Aquaculture Technical Paper, No. 630/1, Food and Agriculture Organization of the United Nations, Rome, https://agris.fao.org/agris-search/search.do?recordID=XF2018002004.

[31] GIZ (2021), Transitioning to Low Carbon Sea Transport, GIZ, Bonn, http://www.giz.de/en/worldwide/59626.html.

[3] Hare, S. et al. (2021), The western and central Pacific tuna fishery: 2020 overview and status of stocks..

[11] Hishamunda, N. et al. (2009), “Commercial aquaculture in Southeast Asia: Some policy lessons”, Food Policy, Vol. 34/1, pp. 102-107, https://doi.org/10.1016/J.FOODPOL.2008.06.006.

[24] Holland, E. et al. (2014), “Connecting the dots: Policy connections between Pacific Island shipping and global CO2 and pollutant emission reduction”, Carbon Management, Vol. 5/1, pp. 93-105, https://doi.org/10.4155/cmt.13.78.

[33] IEA (2021), International Shipping, Tracking Report November 2021, webpage, https://www.iea.org/reports/international-shipping (accessed on 23 March 2022).

[21] IFC (2018), From the Farm to the Tourist’s Table: A Study of Fresh Produce Demand from Fiji’s Hotels and Resorts, International Finance Corporation, Washington, DC, https://www.ifc.org/.

[36] Jupiter, S. et al. (2014), “Locally-managed marine areas: Multiple objectives and diverse strategies”, Pacific Conservation Biology, Vol. 20/2, pp. 165-179, https://doi.org/10.1071/PC140165.

[39] La Viña, A., J. Kho and M. Caleda (2010), Legal Framework for Protected Areas: Philippines, International Union for Conservation of Nature, Gland, Switzerland, https://scholar.google.com/scholar?hl=en&as_sdt=0%2C5&q=Legal+Fraemwork+for+Protected+Areas%3A+Philippines.&btnG=.

[14] Macusi, E. et al. (2022), “Environmental and socioeconomic Impacts of shrimp farming in the Philippines: A critical analysis using PRISMA”, Sustainability, Vol. 14/5, p. 2977, https://doi.org/10.3390/SU14052977.

[34] Maritime UK (2021), “The Cerulean project”, 20 September, http://www.maritimeuk.org/priorities/environment/netzeromaritime-showcase/cerulean-project/.

[8] Ministry of Economy (2017), 5-Year & 20-Year National Development Plan, Ministry of Economy, Republic of Fiji, Suva, https://www.fiji.gov.fj/getattachment/15b0ba03-825e-47f7-bf69-094ad33004dd/5-Year-20-Year-NATIONAL-DEVELOPMENT-PLAN.aspx (accessed on 14 April 2022).

[30] Ministry of Infrastructure and Transport (2015), Maritime Transport Policy, Ministry of Infrastructure and Transport, Republic of Fiji, Suva.

[26] Newell, A. (2020), “Emissions from smaller boats need to be addressed”, 8 July, Fiji Sun, https://fijisun.com.fj/2020/07/08/emissions-from-smaller-boats-need-to-be-addressed/.

[1] OECD (2021), COVID-19 pandemic: Towards a blue recovery in small island developing states, https://www.oecd.org/coronavirus/policy-responses/covid-19-pandemic-towards-a-blue-recovery-in-small-island-developing-states-241271b7/ (accessed on 26 April 2022).

[40] OECD (2020), Sustainable Ocean for All : Harnessing the Benefits of Sustainable Ocean Economies for Developing Countries, OECD Publishing, Paris, https://www.oecd-ilibrary.org/sites/bede6513-en/index.html?itemId=/content/publication/bede6513-en (accessed on 26 April 2022).

[13] Phillips, M. (1995), “Shrimp culture and the environment”, in Towards Sustainable Aquaculture in Southeast Asia and Japan, SEAFDEC Aquaculture Department, lloilo, The Philippines, https://repository.seafdec.org.ph/bitstream/handle/10862/124/adsea94p037-062.pdf?sequence=1.

[25] Prasad, R. and A. Raturi (2019), “Fuel demand and emissions for maritime sector in Fiji: Current status and low-carbon strategies”, Marine Policy, Vol. 102, pp. 40-50, https://doi.org/10.1016/J.MARPOL.2019.01.008.

[5] Republic of Fiji (2020), Draft National Fisheries Policy, Republic of Fiji, Suva.

[9] Republic of Fiji (2020), National Fisheries Policy, Republic of Fiji, Suva, https://www.fisheries.gov.fj/images/National_Fisheries_Policy_draft_June_2020.pdf (accessed on 14 April 2022).

[38] Republic of the Philippines (1992), Republic Act No. 7586, Republic of the Philippines, Manila.

[28] Searcy, T. (2017), “Harnessing the wind: A case study of applying Flettner rotor technology to achieve fuel and cost savings for Fiji’s domestic shipping industry”, Marine Policy, Vol. 86, pp. 164-172, https://doi.org/10.1016/J.MARPOL.2017.09.020.

[2] SPC (2021), The Western and Central Pacific Tuna Fishery : 2020 Overview and Status of Stocks: Oceanic Fisheries Programme, Secretariat of the Pacific Community.

[16] Subasinghe, R. (2017), “Regional review on status and trends in aquaculture development in Asia-Pacific 2015”, FAO Fisheries and Aquaculture Circular, No. 1135/5, Food and Agriculture Organization of the United Nations, Rome.

[35] Techera, E. et al. (2009), “Status and potential of locally-managed marine areas in the South Pacific: meeting nature conservation and sustainable livelihood targets through wide-spread implementation of LMMAs”, SPREP/WWF/WorldFish-Reefbase/CRISP, pp. 343-354, https://www.researchgate.net/publication/46446261_Status_and_potential_of_locally-managed_marine_areas_in_the_Pacific_Island_Region_meeting_nature_conservation_and_sustainable_livelihood_targets_through_wide-spread_implementation_of_LMMAs.

[23] Toepfer, N. (unpublished), Tourism stakeholder perceptions of climate risk and sustainable tourism transitions in Fiji.

[20] UNEP (2020), 2020 Global Status Report for Buildings and Construction: Towards a Zero-emission, Efficient and Resilient Buildings and Construction Sector, United Nations Environment Programme, Nairobi, https://wedocs.unep.org/bitstream/handle/20.500.11822/34572/GSR_ES.pdf.

[32] UNFCCC (2017), “Fijian canoe as symbol of resilience and unity displayed at COP23”, 26 October, UNFCCC News, https://unfccc.int/news/fijian-canoe-as-symbol-of-resilience-and-unity-displayed-at-cop23.

[19] UNFCCC (n.d.), , United Nations Framework Convention on Climate Change, Geneva.

[7] Weirowksi, F. and A. Liese (2010), “Public private partnerships in small-scale aquaculture and fisheries”, The WorldFish Center, Penang, http://pubs.iclarm.net/resource_centre/WF_2731.pdf.

[22] World Bank (2022), Arable land (% of land area), Fiji, (database), https://data.worldbank.org/indicator/AG.LND.ARBL.ZS?locations=FJ (accessed on 26 April 2022).

[18] Yeoman, I. et al. (2022), Does Tourism Have a Future in the Pacific Islands?, Asian Development Bank, Mandaluyong, The Philippines.

Notes

← 1. The value is provided in Fijian dollars and converted using FJD 1=USD 0.462 exchange rate. Fijian Parliament, 2020. Review Report on the Petition for Government to Provide Reliable, Safe and Affordable Shipping Services for the Lau Group, Parliamentary Paper No. 132/19, www.parliament.gov.fj/wp-content/uploads/2020/09/Review-Report-on-the-Petition-for-Government-to-Provide-Reliable-Safe-and-Affordable-Shipping-Services-for-the-Lau-Group.pdf.

← 2. The reduction is relative to a business as usual scenario which assumes a 2% rate of increase of vessels’ activity level (tkm).