copy the linklink copied! Chapter 4. Digital pathways to growth and competitiveness

The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law.

High commodity prices on international markets, followed by a surge in capital investments into the mining sector, have determined much of the good performance of the Colombian economy in past years. However, total factor productivity has contributed negatively to economic growth (OECD, 2017a). In order to reduce its dependency on commodity markets, Colombia needs a new growth strategy. The digital transformation provides Colombia with the opportunity to diversify its activities from a commodity-based to a high value-added services economy.

The first section of this chapter examines the changing structure of the Colombian production system. It shows the increasing role of the services sector and argues that the digital transformation could drive a change in sectoral specialisation, highlighting opportunities and challenges for different sectors. It also shows recent compositional changes in the information and communication technology (ICT) sector, arguing that a comprehensive policy approach might be required to foster sustainable growth in this sector.

The second section examines different aspects of Colombia’s current trade patterns. After briefly presenting some of the broader possibilities of digitalisation for trade, it digs deeper into certain service sectors, focusing mainly on ICT technologies. The evidence suggests that services have become increasingly important and could drive further export diversification. There are also signs of emerging potential for digitally enabled services, i.e. services that can be digitally transmitted. Finally, the section highlights the importance of access to information technology (IT) services from other countries and discusses how Colombia could improve its market openness in a digital world.

copy the linklink copied! Fostering sectoral diversification through digital transformation

Colombia’s production system is highly dependent on world market conditions and government spending

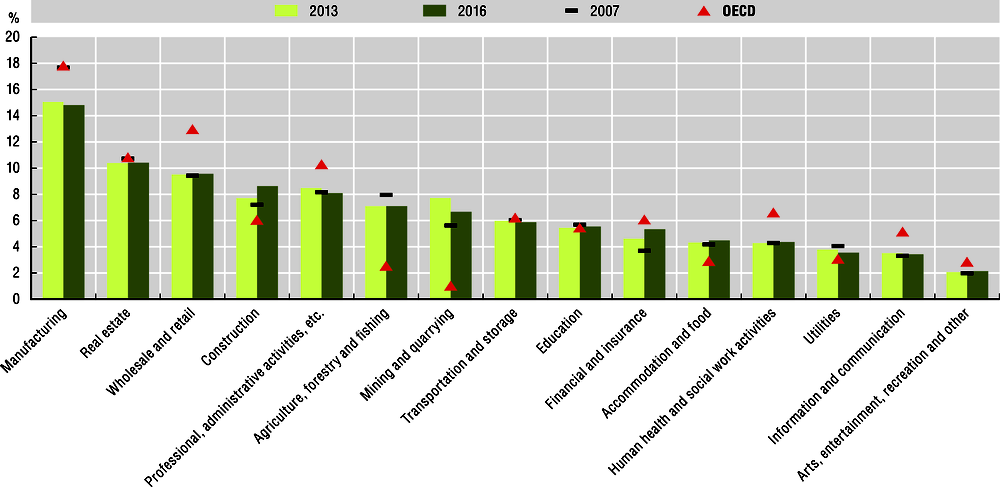

Over the last decade, the Colombian economy has seen important readjustments in the composition of its economic activities. To some extent, these dynamics reflect a systematic shift away from manufacturing towards services activities, following a global trend of “servicification” as well as increased competition from other emerging economies.

Notes: Value added from public administration and defence, compulsory social security and activities of households as employers are not included. Professional, administrative activities, etc. includes scientific, technical and support service activities. OECD is computed as a simple average over OECD countries.

Sources: Data for Colombia are drawn from DANE (2019b), “Principales agreagados macroeconómicos, base 2015”, https://www.dane.gov.co/index.php/estadisticas-por-tema/cuentas-nacionales/cuentas-nacionales-anuales; data for OECD countries are drawn from OECD (2019d), “STAN Database for Structural Analysis (ISIC Rev. 4, SNA08)”, https://stats.oecd.org/index.aspx?DataSetCode=PDB_LV (accessed on 15 April 2019).

Between 2007 and 2016, the share of manufacturing in Colombia’s total value added declined from 17.7% to 14.8% (Figure 4.1). Conversely, the share of business services increased from 45.5% to 47.1% over the same period.1 A similar dynamic has also been observed in OECD countries. However, the weight of both sectors in Colombia is lower than in OECD countries, where manufacturing and services accounted for, respectively, 17.8% and 54.5% of total value added in 2016.

The lower share of both manufacturing and service activities in Colombia reflects the growing size of the mining and the agricultural sectors, and, more recently, an increase in construction activities. Between 2007 and 2013, the contribution of the mining sector to total value added rose by about 37%, from 5.6% to about 7.7%. Since 2013, the demand from emerging economies has slowed down substantially and brought the contribution of the sector down to 6.7% by 2016. However, the sector’s significance remains over six times larger than in OECD countries (1%). Taking into account the relatively large agricultural sector (7.1% compared to 2.6% in OECD countries), it becomes apparent that the Colombian economy remains highly exposed to world market fluctuations of commodity prices (Hernández, 2013).

The value added share of the construction sector increased by over 10% between 2013 and 2016, driven by the government’s renewed efforts to close the infrastructure gap in terms of both quality and quantity, which remains large compared to OECD countries. A USD 55 billion investment plan was launched in 2011 and scaled up more recently in a fourth-generation (4G) public-private investment infrastructure programme on road concessions, the most ambitious infrastructure development initiative in Colombian history (The Economist, 2011; OECD, 2017).

Many firms in Colombia underrate the importance of ICTs for innovation

Evidence for Colombia confirms that firms operating in services invest more in ICTs than manufacturers and that innovation in services is associated with higher labour productivity growth (Gallego, Gutiérrez and Taborda, 2015).

Note: Other sectors include financial, transportation, social and ICT services as well as agriculture and construction.

Source: MinTIC (2017), “Gran Encuesta TIC: Tabla de salida empresas”, https://colombiatic.mintic.gov.co/679/w3-article-74002.html (accessed on 27 December 2018).

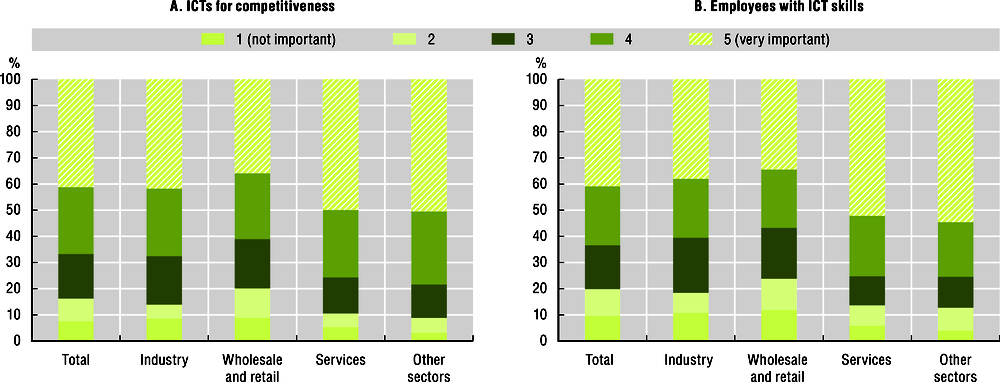

Recent results from a large ICT usage survey, the Gran Encuesta TIC (MinTIC, 2017), provide further support for the high relevance of ICT innovations for firms in services. About 50% of firms in service activities covered by the survey consider access to ICTs to be very important for their business model and competitiveness (Figure 4.2).2 Furthermore, over 50% consider it very important for their employees to possess ICT skills. These percentages are significantly higher than in the industrial sectors, where only 42% of firms consider ICTs very important for their business model and less than 40% consider ICT skills to be of high importance.

The wholesale and retail sectors stand out, with only slightly more than a third of firms regarding ICTs and ICT skills as being very important. In line with these responses, only 22% of firms in the wholesale and retail sector have used ICTs for innovation in the past two years (Figure 4.3). This contrasts starkly with other service sectors, where about 37% of firms used ICTs to innovate. At about 28%, the industrial sector was on middle ground.

Note: Other sectors include financial, transportation, social and ICT services as well as agriculture and construction.

Source: MinTIC (2017), “Gran Encuesta TIC: Tabla de salida empresas”, https://colombiatic.mintic.gov.co/679/w3-article-74002.html (accessed on 27 December 2018).

The reasons that led firms to (ICT-based) innovations thereby differ from sector to sector. While a majority of firms in industry, retail and wholesale engaged in innovations to increase sales, the most-cited reason for firms in the services sector was to raise quality (45% to 47%) and to improve their products (31% to 32%). Firms in the services sectors also used ICT innovations relatively more frequently to develop entirely new products. Overall, these numbers confirm the more fundamental role that innovations based on ICTs play for firms in the services sector.

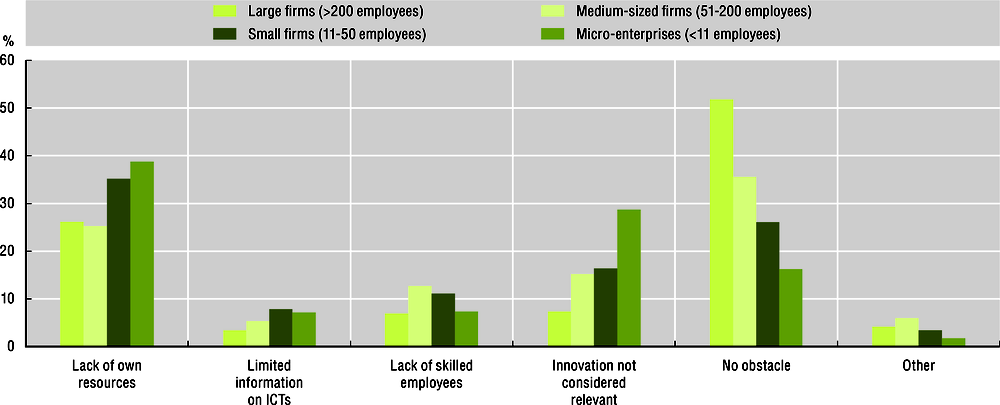

The survey also shows a striking difference between large firms (more than 200 employees) and micro-enterprises (less than 11 employees). While 71% of large firms use ICTs to innovate, the corresponding number is only 19% for micro-firms. This is at odds with the potential for digital transformation to provide even very small firms with access to global markets (OECD, 2019c).

Figure 4.4 suggests that limited access to financial resources is the most likely explanation for this gap. The new ICT strategic sectoral plan 2019-22 launched by the Ministry of Information and Communication Technologies (Ministerio de Tecnologías de la Información y Comunicaciones [MinTIC]) (MinTIC, 2019) points out the need to improve businesses’ access to credit for projects related to the digital transformation and proposes collaboration with the financial sector as a possible means to achieve this objective.

Note: ICT = information and communication technology.

Source: MinTIC (2017), “Gran Encuesta TIC: Tabla de salida empresas”, https://colombiatic.mintic.gov.co/679/w3-article-74002.html (accessed on 27 December 2018).

The digital transformation is fostering growth in services

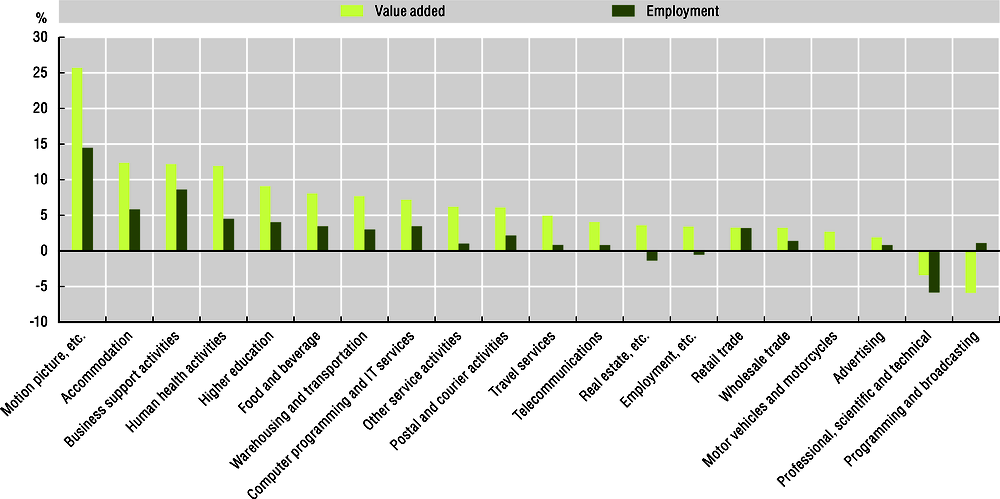

Many services sectors are profoundly affected by digital transformation and there is large heterogeneity with regard to growth dynamics between different services sub-sectors (Figure 4.5).

Notes: Industry classification following ISIC Rev. 4 (CIIU Rev. 4 A.C.). Growth rates are computed as a simple average of yearly changes. Real estate, etc. includes rental and leasing activities. Motion picture, etc. includes video, television, sound and music. Employment, etc. includes security, buildings and administrative support.

Sources: DANE (2017b, 2016b, 2015b), “Variaciones Porcentuales Corrientes – CIIU Revisión 4”, https://www.dane.gov.co/index.php/estadisticas-por-tema/servicios/encuesta-anual-de-servicios-eas (accessed on 15 November 2018); DANE (2017a, 2016a, 2015a), “Anexos evolución CIIU Rev 4 A.C.”, https://www.dane.gov.co/index.php/estadisticas-por-tema/comercio-interno/encuesta-anual-de-comercio-eac (accessed on 15 November 2018).

The following sub-section reconsiders how various services sectors in Colombia have been affected by digital transformation and discusses how government policies can help foster the digital potential in services industries. The service sectors considered are: the so-called “Orange Economy”; accommodation; business support activities; e-health; wholesale and retail; logistics; professional, scientific and technical services; financial services; and ICT services.

The Orange Economy offers large potential for productive jobs in remote areas

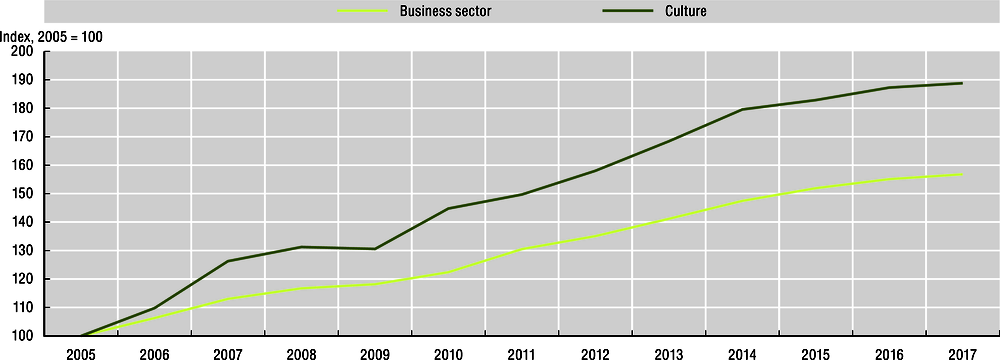

Colombia’s rich cultural assets and creative industries – the so-called “Economía Naranja” (Orange Economy) – has grown significantly faster than the business sector (Figure 4.6). The sector, which encompasses audiovisuals, design activities, cultural education, games and toys, music, books and other publications, accounted for about 1.1% of Colombia’s total value added in 2017. Audiovisuals represent by far the largest share in the creative industries, accounting for over 40% of the total value added (DANE, 2018c).

Notes: Business sector includes all sectors except Public administration and defence compulsory social security (ISIC Rev. 4, Section O) and Activities of households as employers, undifferentiated goods- and services-producing activities of households for own use (Section T). Chained volume indices (base year 2015). Data for 2017 are provisional. See DANE, Satellite Account of Culture for a definition of the cultural sector.

Sources: DANE (2019b), “Principales agregados macroeconómicos, base 2015”, https://www.dane.gov.co/index.php/estadisticas-por-tema/cuentas-nacionales/cuentas-nacionales-anuales (accessed on 15 April 2019); DANE (2019c), Cuenta Satélite de Cultura (CSC) (database), https://www.dane.gov.co/index.php/estadisticas-por-tema/cuentas-nacionales/cuentas-satelite/cuenta-satelite-de-cultura-en-colombia (accessed on 15 April 2019).

Several legislative changes have helped push the sector forward. The Film Act of 2003 (Law 814) stimulated cultural productions by creating tax incentives for individuals and companies investing in film projects as well as for film exhibitors that are screening Colombian short movies. The Colombia Filming Act of 2012 (Law 1556) fostered activities promoting Colombia as a film location and provided a cash rebate on production costs for companies filming in Colombia. Resources allocated to these measures included over USD 83 million to be spent over the years 2004-16 (Law 814) and USD 18 million for the Colombia Film Fund as well as over half a billion USD delivered in cash rebates between 2013 and 2016 (Law 1556). The measures involved yearly evaluations through the National Council of the Arts and Culture in Cinematography (UNESCO, 2017). As a result, the number of feature films produced in Colombia increased from 5 in 2013 to 41 in 2016 and the number of admissions for national films more than doubled, from 2.3 million in 2007 to 4.7 million in 2016 (UNESCO, 2018).

An initiative brought to congress by former senator and current President Iván Duque in 2017 (Law 1834) has now broadened the focus to a wider set of creative activities. Buitrago Restrepo and Duque Márquez (2013) identified the Orange Economy as a sector likely to benefit substantially from the digital transformation, turning it into a potential motor of growth for high-skilled services. In particular, the emergence of content created and distributed on line can significantly leverage human capital as productive input, reduce barriers to entry and allow new business models to prosper.

A newly formed National Council for the Orange Economy, headed by the Ministry of Culture, came together for the first time in October 2018 and unites seven ministries and five other entities in an attempt to provide a whole-of-government response to the challenges facing the sector. The strategy is also an important component of the new National Development Plan (Plan Nacional de Desarrollo [PND]) 2018-2022 (DNP, 2019) where it is included as a transversal pact focused on the protection and promotion of Colombian culture and the promotion of the Orange Economy for productivity and job creation. The plan highlights the complementarities between the Orange Economy and the tourism sector and their potential to transform the Colombian economy.

In particular, the PND aims to promote an environment that fosters the creation and distribution of cultural content as well as access to it, including through a strengthening of the property rights system. It also recognises the role that sectors like the Orange Economy can play in bringing employment opportunities to rural areas, in particular for young people. The Orange Economy is at present highly concentrated in Bogotá (El Espectador, 2018a).

While the plan highlights the complementarities between the Orange Economy and the tourism sector, the promotion of the Orange Economy in rural areas should extend beyond low-skilled activities in the tourism sector, incorporating high-tech and skill-intensive activities in the creative industries more broadly. With the creation of orange development areas (áreas de desarrollo naranja) the PND contains a conceptual framework for such policies which could be linked to other government objectives, such as MinTIC’s recently proposed initiative to close the regional ICT skill gap (MinTIC, 2019).

Several other initiatives currently in planning or underway are likely to help foster the expansion of the Orange Economy. This includes, for example, MinTIC’s Crea Digital 2019, aimed at small and medium-sized enterprises (SMEs) in the cultural industries and other innovative sectors, and New Media, fostering the creation of cultural products to be disseminated via online platforms, with a new call being foreseen in mid-2019.

The digital economy and regulatory changes are boosting accommodation services

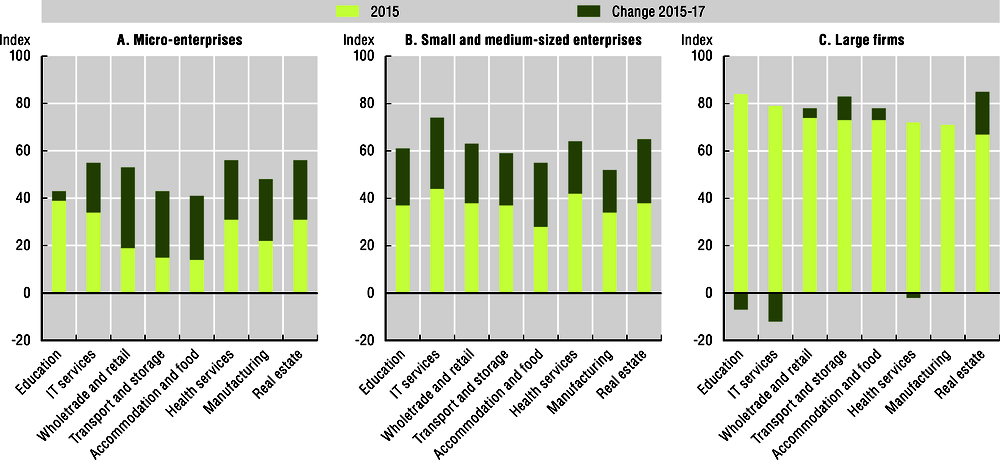

Employment in the accommodation sector grew by about 5.8% on average in each year between 2014 and 2017 (Figure 4.5). Data from the Observatory of the Digital Economy (MinTIC) suggests that digital transformation is likely to have driven part of this dynamic. The sector aggregate encompassing accommodation and food services, while overall still not a very intensive user of mature digital technologies relative to other sectors,3 has seen relatively large increases in terms of digital intensity between 2015 and 2017, in particular among micro-enterprises and SMEs (Figure 4.7). This is not surprising given the ease with which in particular small hotel or restaurant owners today can set up their website or make an appearance on specialised online platforms.

The accommodation sector likely will further profit from recent regulatory adjustments that the Ministry of Commerce, Industry and Tourism (Ministerio de Comercio, Industria y Turismo [MinCIT]) introduced to simplify the formal registration of private accommodation service providers. While private persons previously were obliged to fulfil the same requirements as hotels in order to be registered in the National Tourism Registry, the new legislation has established an additional category for non-commercial service providers that simplifies registration in the National Tourism Registry (Decree 2063) and does not require registration in the Registry of Merchants (Decree 2119). Through this measure, MinCIT aims to reduce the high share of tourism service providers estimated to be operating in informality (41%) and to better account for the offer of rooms via peer-sharing platforms. While providers of accommodation services are, in principle, still obliged to pay a tax on their generated income, a threshold of 50 times the legal minimum wage reduces the burden for small-scale providers (El Espectador, 2018b).

Business support activities with large potential

In 2014-17, growth in value added (12.2%) and employment (8.6%) was also sustained in business support activities (Figure 4.5). The sector comprises many activities associated with business process outsourcing (BPO), such as financial planning, billing and record keeping, as well as call centres, and is likely to benefit significantly from digital transformation. The A.T. Kearney 2017 Global Services Location Index ranked Colombia 10th out of 55 countries analysed for offshoring potential, behind Brazil (5) and Chile (9) but ahead of Mexico (13), Peru (20) and Costa Rica (31). According to the report, Colombia won 12% of new BPO and shared services centres in Latin America and the Caribbean between 2011 and 2015 (A.T. Kearney, 2017).

Notes: IT = information technology. Micro-enterprises have up to 10 employees. SMEs are small (11-50 employees) and medium (51-200 employees) enterprises. Large firms have more than 200 employees.

Source: Katz, R.L. (2017), “El Observatorio de la Economía Digital de Colombia”, https://www.mintic.gov.co/portal/604/articles-61929_recurso_4.pdf.

This positive outlook seems confirmed by Amazon’s recent decision to open its first South American customer service centre in Bogotá, likely to generate as many as 600 jobs. Only a few months earlier, in April 2018, Coca Cola announced that it would shift its business unit for central Latin America from Costa Rica to the Colombian capital (Miranda, 2018).

The Productive Transformation Programme (Programa de Transformación Productiva [PTP]), established by MinCIT in 2008 to provide business development and technical assistance to companies, has singled out BPO, together with other outsourcing activities, software and IT as well as tourism, as a core pillar in its services strategy. However, for this policy to be sustainable, it is important to focus on outsourcing activities that rely on human interaction and are thus less likely to be automated in the near future (Brynjolfsson and McAfee, 2015). The current surge of customer service centres can therefore be seen as a positive development, even if activities are currently highly concentrated in Bogotá.

E-health services have large potential, but challenges remain with regard to connectivity, interoperability and data security

Between 2014 and 2017, valued added in the Colombian health sector grew by close to 12% a year (Figure 4.5). While still relatively small in comparison to the market in Brazil or Mexico, activities related to digital health have been supporting growth in the sector (Maia, Pasteiner and Martinez, 2018). In particular, micro-enterprises and SMEs in the health sector are already among the most intensive users of mature digital technologies across all sectors in Colombia (Figure 4.7).

In a country like Colombia, where a substantial share of the population lives in remote areas with difficult access to medical services, the potential for e-health solutions is large. With Law 1419 of 2010, the government provided the first regulatory ground for the development of e-health in Colombia. However, remaining limitations in last-mile connectivity (see Chapter 2), likely affecting remote areas in particular, and limited technical interoperability between health service providers might currently be keeping sector-level growth below potential. Today e-health services are therefore still concentrated in a small number of relatively densely populated areas like Antioquia, Cundinamarca and Valle del Cauca (Suárez, 2018). Besides access, the limited implementation of data security measures in healthcare facilities has also been cited as a problem that calls for government action (Cuellar, 28 September 2017).

With the new PND (Law 1955 of 2019) and the current revision of ICT policies, the Colombian government foresees action both with regard to access in remote areas and regulation on health data governance. For guidance in regard to regulation on health data governance, Colombia should refer to the OECD Recommendation of the Council on Health Data Governance. International best practices should, in particular, be followed when designing the technical, legal and administrative details for the legal framework on information flows within the Integrated Social Security System, which is foreseen in the PND.

Wholesale and retail services suffer from a lack of innovation, infrastructure and trust

Despite their increasing digital intensity (Figure 4.7), the wholesale and retail sectors have been largely underperforming in Colombia as motors of growth (Figure 4.5). Some studies suggest that a lack of competition could be responsible for the disappointing performance, in particular in the retail sector (OECD, 2015).

Nevertheless, new business models, enabled by digital technologies, are beginning to increase competitive pressure in the sector. These new businesses include large international online marketplaces, which are constantly increasing the variety of products on offer in Colombia (Vega Barbosa, 2018), as well as a rising number of domestic start-ups looking for innovative ways to overcome obstacles to e-commerce, e.g. low trust in online business transactions, high cost of digital payment methods, low quality of postal services and infrastructure (see Chapter 3, as well as CRC, 2017b). Some of these firms, including the unicorn Rappi, which is valued at more than USD 1 billion, are currently enlarging the range of their services to payment and postal services and are likely to increase the competitive pressure in those markets (CRC, 2017a).

For e-commerce to fully develop its potential, it is important that the Colombian government supports the digital transformation of the retail sector. With the programme Colombia at 1 Click, PROCOLOMBIA has recently begun fostering the use of online sales channels in Colombia, aiming at higher participation rates in online marketplaces, organising training events, or providing consultancy on logistics or customs procedures (PROCOLOMBIA, 2019). However, integrating consumers in remote areas, as well as fostering trust through consumer protection and digital security, will also be crucial for the e-commerce market to flourish. A revision of the digital security strategy, including a reference to the role for trust, is currently under way in Colombia. The draft OECD Recommendation on Digital Security of Critical Activities and the revised Recommendation of the Council on Consumer Protection in E-commerce can provide useful guidance in this regard.

It will also be important to further reduce the high transaction costs associated with digital payments. The 24 digital payment intermediaries currently operating in Colombia could help reduce these costs. For the moment, these intermediaries are neither regulated nor supervised (El Tiempo, 2018a). The unit responsible for financial regulation in the Ministry of Finance and Public Credit has recently begun to address this issue (Prieto et al. 2018) and has set up a working group with the Central Bank and the Superintendence of Finance (SFC) to consider potential approaches. To support competition in the payment market, it will be crucial that any new legislation will keep regulatory hurdles low for new entrants. Article 166 of Law 1995 of 2019 now more generally foresees measures to facilitate the operation of innovative and tech-driven business models.

Use of robotics could pave Colombia’s way to becoming a regional logistics hub

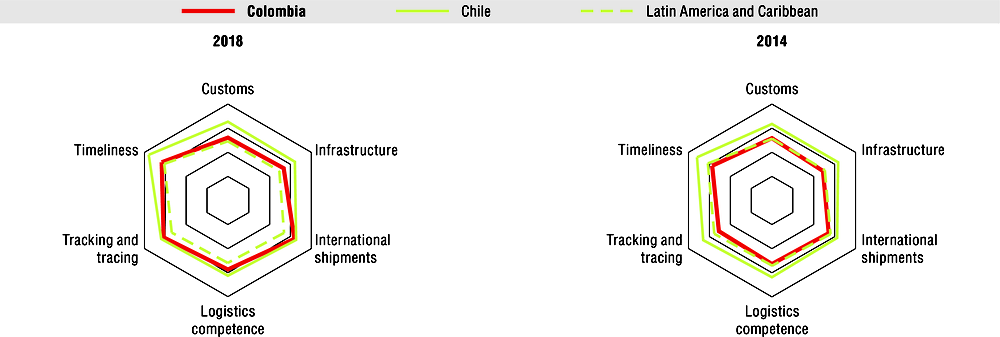

Recent results from the “Encuestra Nacional Logistica 2018” (“National Survey of Logistics”) suggest a relatively high share of innovating firms in the warehousing and transportation support sector. Almost half of all firms in the sector (47.7%) had engaged in innovation over the past two years, with the number one reason for innovation being an increase in logistics efficiency (DNP, 2018a). Looking at the World Bank Logistics Performance Index confirms that Colombia has made substantial progress in recent years over a broad set of indicators. In terms of overall performance, Colombia moved its way up the world ranking from number 97 to 58, leaping ahead of Uruguay, Costa Rica, Ecuador, Paraguay, Guatemala, the Bolivarian Republic of Venezuela, Peru and Argentina, settling right behind countries like Brazil (56) and Mexico (51) and closing in on the regional leaders Chile (34) and Panama (38). The largest improvements were made in tracking and tracing and international shipments (Figure 4.8).

Source: World Bank (2018), “International LPI”, https://lpi.worldbank.org/international (accessed in February 2019).

As the “National Survey of Logistics” suggests, the major cost component of logistics is related to warehousing and storage (46.5%), and the government should therefore foster the use of advanced technologies like robotics in warehousing to support the development of Colombia into a transport and warehousing hub for Latin America. In particular, the steady modernisation efforts in the port of Cartagena seem already to offer a basis for realistically aiming to become such a hub. While in terms of digital intensiveness the sector is relatively advanced for large firms (Figure 4.7), substantial potential for improvements exists in particular for SMEs. Improving access to finance for these firms could thereby play a crucial role.

A digital strategy is needed for professional, scientific and technical services

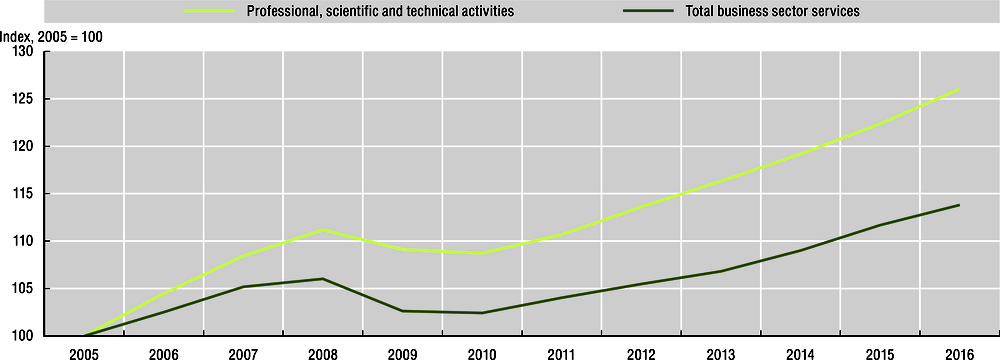

Professional, scientific and technical activities have been a growth industry and major source of employment in many countries (Figure 4.9). The sector, encompassing activities such as legal, architectural or engineering services, is considered knowledge intensive (see, for example, National Science Board [2018]) and thus can generate high-income jobs that are critical in evolving services markets like the one in Colombia.

Notes: 2005 = 100. In Canada and Israel, employment is measured as the number of jobs rather than persons.

Source: OECD (2019d), “STAN Database for Structural Analysis (ISIC Rev. 4, SNA08)”, https://doi.org/10.1787/stan-data-en (accessed on 15 April 2019).

However, in contrast to other countries, the sector shrank considerably in Colombia between 2014 and 2017 (Figure 4.5). This decline mostly occurred over the first two years of the period (2014-16), which is likely explained, at least to some extent, by the decline in mining activities. Between 2016 and 2017, value added began rising again while employment continued to decline (-2.5%), though significantly less than in the previous years (-7.5% on average). Because over the whole period the decline in value added was smaller than the decline in employment, labour productivity has likely been growing over time.

For the years 2018-22, the recently presented PND projects production in the sector to grow by close to 5% on average per year, topped only by financial and insurance activities (5.1%) and significantly above projected gross domestic product (GDP) growth (3.8%) (DNP, 2019). However, while the National Planning Department (Departamento Nacional de Planeación [DNP]) document recognises the role of digital transformation as a factor fostering growth in financial services, growth in scientific, professional and technical services are expected to be driven mostly by public construction work, mining as well as public administration.

Not least in the light of a growing potential for ICT-enabled services, for Colombia the digital transformation could open a route to diversification in knowledge-intensive services. However, to foster digital transformation in the sector and remain competitive, creating the right ecosystem for professional services will be of utmost importance (WEF, 2017). The government should therefore reassess whether the current regulatory framework is fit for the digital transformation.4 The need to adapt to changing skill requirements for these jobs has been acknowledged, for example in CONPES document 3920 of 2018.

Digitalisation brings new growth opportunities for financial services

The Colombian financial services sector, in particular Fintech, has been very dynamic in recent years. The Inter-American Development Bank (IADB) (IADB, IDB Invest and Finnovista, 2018) shows that, out of 1 166 identified Fintech start-ups in 18 Latin American countries, 148 were Colombian. This places Colombia behind the regional leaders Brazil (380) and Mexico (273) but ahead of Argentina (116) and Chile (84). With an increase of 76% in the number of start-ups between 2017 and 2018, Colombia was the fastest growing Fintech ecosystem among these five countries.

According to the IADB study, about 45% of Colombian start-ups are currently still in relatively early stages of entrepreneurship, encompassing activities from product conceptualisation to product launch. The remaining 55% are in advanced stages of entrepreneurship, and thus ready to scale-up and expand. This compares to 64% of start-ups in advanced stages for the whole region and 78% for Brazil, implying that Colombian start-ups will profit relatively more from support in early stages of the start-up lifecycle. As the other four leading countries, Colombia has an active Fintech association (Colombia Fintech), established in 2016.

The largest segments of the Colombian Fintech market are payments and remittances. Data from a previous survey (Pombo et al., 2017) further reveal that outward orientation of Colombian entrepreneurs is more pronounced than in other countries: while 31% of respondents among Colombian entrepreneurs indicated activity in other Latin American countries, this share was only 11% for Brazil and 8.6% for Mexico, suggesting large internationalisation potential.

Compared to the fast growth of the sector, Fintech regulation in Colombia still appears to be overly burdensome: 26% of Colombian Fintech entrepreneurs considered current regulation to be excessive (Pombo et al., 2017), against 13% in Brazil, 4% in Chile, 14% in Mexico and 13% in Peru. External financing of Fintech entrepreneurship in Colombia also seems more problematic than in other countries. In 2018, only 53% of Colombian entrepreneurs obtained third-party funding, significantly less than in the other Latin American countries: 88% in Chile, 78% in Brazil, 67% in Venezuela and 65% in Mexico. This suggests scope to increase access to finance for the sector.

The government has taken some important steps to create a more favourable regulatory environment for the sector. With companies specialised in electronic deposits and payments (sociedad especializada en depositos y pagos electronicos [SEDPE]), the Ministry of Finance and Public Credit has created a new type of financial institution, mostly restricted to payment and transfer transactions, but subject to significantly lighter regulation than traditional banks. In addition, financial transactions below a certain threshold (roughly USD 580) are exempt from the usual financial transaction tax (Gravámen a los Movimientos Financieros), colloquially referred to as “4 por mil” (“4 x 1 000”) (Ministry of Finance and Public Credit, 2018). The first SEDPE has now begun to operate in Colombia and several more are registered. This regulatory change will likely help increase competition in the payment sector, reduce costs of financial transactions and thus enhance financial inclusion, potentially opening up the e-commerce market to more users in the country.

With Decree 1357 from July 2018, the government has also issued a first crowdfunding legislation, allowing crowdfunding platforms to collect funds for productive investment projects. The decree is limited to equity crowdfunding and does not apply to peer-to-peer lending. Crowdfunding platforms can only be established by authorised sole purpose stock corporations, stock exchanges or trading systems. The total amount that can be raised is limited, with the ceiling depending on the type of investors (Fradique-Méndez and Ordoñez, 2018).

Additionally, since December 2018, credit and banking institutions are allowed to invest in financial innovation and tech companies. The new regulation (Decree 2443) aims at fostering financial inclusion and entrepreneurship and an acceleration of the digital transformation in the banking sector.

With innovaSFC, the SFC has launched a broader strategy for the promotion of sustainable and responsible innovation in the financial sector. As part of this strategy, the SFC has established additional channels to exchange with the sector on innovation (elHub) as well as a sandbox environment (laArenera) that allows firms to test new technologies and business models under observation. The first company initiated its activities under the scheme in February 2019 and four others have been approved since. Several more companies are currently being considered for approval or have indicated their interest in participation.

ICT services are gaining importance but would benefit from better government co-ordination

The ICT sector is the backbone of the digital economy. Compared to many advanced economies, the size of the sector in Colombia is relatively small, accounting for only 2.3% of value added, against 5.1% for OECD countries (Figure 4.10). The size of the sector is also small compared to regional peers, including Costa Rica (4.7%), Mexico (3.3%) and Brazil (3.3%), but also Chile (2.8%) and Argentina (2.6%).

The sector is dominated by telecommunications services, which account for 78.5% of total ICT value added. This share is significantly higher than in OECD countries (29.5%), but also compared to regional peers, including Brazil (40.7%), Mexico (43.3%), Costa Rica (44.5%), Chile (49.7) and Argentina (61.4%).

Note: The ICT sector includes computer, electronic and optical products (ISIC Rev. 4, D26), telecommunication services (D61), and IT and other information services (D62, D63).

Source: OECD (2019f), “Trade in value added”, https://doi.org/10.1787/data-00648-en (accessed on 22 April 2019).

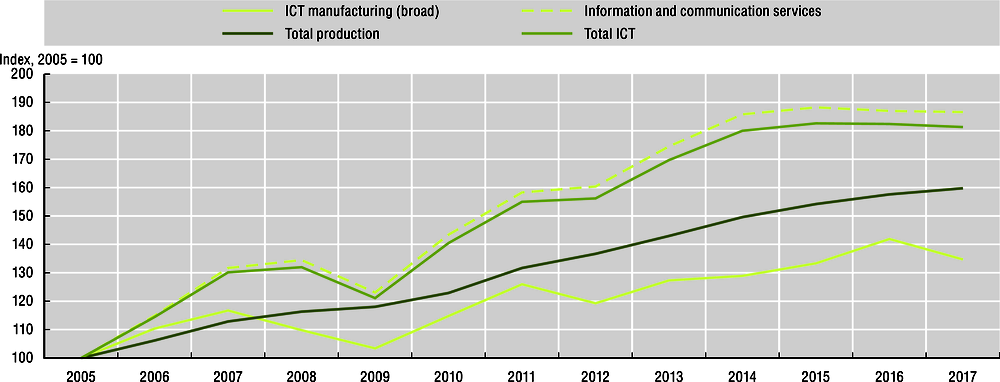

Despite its small size, the ICT sector as a whole has contributed positively to growth in Colombia over the past 12 years, increasing in size relative to other sectors (Figure 4.11). Growth was driven by ICT services, whereas the ICT manufacturing sector has been less dynamic. However, since 2014, growth in the ICT sector has been lagging behind growth in other sectors.

Notes: ICT = information and communication technology. Classification: CIIU Rev. 4 A.C. (60 groups). ICT manufacturing includes manufacturing of computer, electronic and optical products as well as electrical equipment (C52). ICT services include telecommunication services, IT services and consulting, broadcasting and media (J81-J84). Data for 2017 are preliminary.

Source: DANE (2019b), “Principales agregados macroeconómicos, base 2015”, https://www.dane.gov.co/index.php/estadisticas-por-tema/cuentas-nacionales/cuentas-nacionales-anuales (accessed on 15 April 2019).

According to data from a newly established satellite account for the sector, full-time equivalent employment in the telecommunications sector significantly diminished between 2015 and 2017, falling from 277 510 to 200 407. A decrease in employment was also observed in ICT wholesale (-17 093), infrastructure (-1 826) and manufacturing (-187). On the contrary, a significant number of jobs were created in IT services over the same period (22 289) and, to a lesser extent, in content and media services (1 190) (DANE, 2018b).5

In the light of overall slowing dynamics in some parts of the sector, the government should assess whether the relatively large number of government programmes aimed at the sector are being effective. In particular, many programmes tend to be relatively small and are operated in parallel by distinct government agencies, applying different approaches and following different objectives (PTP, 2017b). This can make the available programmes difficult to assess and access for firms in the sector.

The large gap in skilled ICT workers is also a challenge for the sector (Observatorio TI, 2017). The MinTIC programme IT Talent (Talento TI) tries to address this skill gap by offering financial support to students who want to pursue training in IT-related professions (see Chapter 5).

Productive transformation policy in Colombia requires a cross-sectoral approach to digitalisation

In 2008, MinCIT created the PTP with the aim of promoting productivity and competitiveness in Colombian firms in line with the priorities set in the National Productivity and Competitiveness Policy (CONPES 3527, 2008) and updated in the Productivity Development Programme of 2016 (CONPES 3866) (Box 4.1). The PTP reaches out to companies with calls for proposals and specialised programmes that aim at improving the efficiency of productive processes in targeted sectors. These activities can involve technical assistance, interventions and training programmes as well as financing and consultation for firms that engage in new methods and international standards aimed at improving productivity. The programme currently works with 18 economic sectors, supporting projects in 29 out of the 32 Colombian departments and has provided technical assistance to over 1 000 firms and 10 000 productive units.

In 2016, the DNP issued CONPES 3866, a productivity development policy (PDP) that includes a ten-year roadmap towards higher productivity. The document highlights a need to improve managerial capabilities with regard to entrepreneurship and technology absorption and to improve access to finance, with a focus on innovative firms. It also contains measures to close the skill gap and to raise quality standards in order to help Colombian producers compete on international markets. Throughout, the plan emphasises the need for diversification and a shift of the economy towards more advanced goods and services.

For the PDP to achieve its goals, it is crucial to overcome some problems that have hampered productivity policies over the last two decades. These include low coherence of a multitude of short-term government programmes, with changing priorities and limited funding. There is also evidence of poor co-ordination between government agencies at the regional and national level (Reina, Oveido and Tamayo, 2015; Reina, Castro and Tamayo, 2013).

CONPES 3866 points out the need for better policy co-ordination across policy silos as well as a clear governance structure and regular evaluations. It foresees this role for the National Competitiveness, Science, Technology and Innovation System (SNCCTI), established in 2015 through the merger of the National Competitiveness and Innovation System and the National Science, Technology and Innovation System. Within the SNCCTI, MinCIT has the technical lead on issues related to productivity development.

In October 2018, the executive committee of the SNCCTI came together to discuss the principal strategies to be followed for the next four years in line with the new PND 2018-2022. At this meeting, the executive committee reiterated the importance of co-ordinating public and private actors and of ensuring the continuity of policies (DNP, 2018b).

The selection of targeted sectors by the PTP is based on several criteria, including the potential to dynamise production, employment and exports and to increase sophistication of Colombian products. Targeted sectors include seven sectors in the agro-industrial complex (e.g. cacao and processed foods), seven manufacturing industries (e.g. cosmetics and fashion) as well as four services, including BPO, software and IT as well as wellness and nature tourism. Several sectors are grouped in distinct value chains. For example, cosmetics, pharmaceutics and plastics form part of the chemicals value chain, whereas BPO and software and IT services together form the Industry 4.0 value chain (PTP, 2017a).

With the exception of the Industry 4.0 value chain, the PTP currently does not have a transversal strategy for the digital transformation in sectors, even if digital technologies have been at the core of individual programmes and form part of the overall action plan to promote knowledge and technology transfers (PTP, 2017a). There is further no particular focus on services with digital export potential, apart from outsourcing activities and IT services. In particular, the PTP currently does not specifically target high-potential sectors such as creative industries or financial services.

iNNpulsa, the Colombian management unit of business growth of the national government, with the support of MinTIC, has recently put forward a new proposal for a Smart Manufacturing Program that aims to raise awareness among business leaders, identify manufacturing companies keen on investing in and adopting new technologies, to connect them to relevant research institutions and offer them financial incentives for the adoption of advanced manufacturing technologies. For the first year, the programme aims to assess the readiness of 40 companies, initiate 15 co-funded projects fostering the absorption of advanced manufacturing technologies and provide support to 10 start-ups active in the development of advanced manufacturing technologies (iNNpulsa, 2018).

As part of the strategy, the programme further aims to create or strengthen advanced manufacturing centres in the country. In January 2019, President Iván Duque and Murat Sönmez, head of the Centre for the 4th Industrial Revolution (C4IR) at the World Economic Forum in Davos, jointly signed an agreement for Medellín to host the first C4IR in Latin America. The network aims at facilitating the exchange of research and analysis in a trusted environment and expanded in 2018 to include centres in the People’s Republic of China (hereafter “China”), India and Japan. Together with Colombia, Israel and the United Arab Emirates have also announced the opening of centres in 2019. The Colombian centre will be institutionally based within Ruta N (see Chapter 5) and promote entrepreneurship and the development of new technologies in the region, with a focus on artificial intelligence (AI) and data science.

It will be crucial for Colombia to ensure that the multitude of activities supporting the productive transformation of the country are closely co-ordinated across government actors and over time. This involves close co-ordination between regional actors and the national government to promote efficient feedback of opportunities into the planning of new projects and spreading best practices across regions and programmes. It also involves the continuous co-ordination among government agencies to reduce duplication and create clear responsibilities for transversal objectives (e.g. skills or ICT sector policies). This likely requires the creation of an appropriate institutional setting that can ensure alignment of government programmes with the goals set in the national agenda for competitiveness and that hold government agencies accountable for the co-ordination of projects at the operational level. Constant evaluation and accountability should form a crucial part of such an institutional setting.

-

Foster digital uptake by businesses as a mean to diversify production activities.

-

Complement infrastructure investments with a digital strategy for services to enhance overall productivity.

-

Encourage technical interoperability and data security among e-health providers, following the OECD Recommendation of the Council on Health Data Governance; foster the use of e-health solutions in remote areas through access policies.

-

Foster the diffusion of the Orange Economy into remote areas to capitalise on cultural diversity and create job opportunities for highly skilled workers.

-

Foster the use of advanced technologies, e.g. robotics, to reduce costs in warehousing and storage; encourage use of digital tools among SMEs in the sector.

-

Support the digital transformation in the retail and wholesale sector by improving (postal and other) infrastructure, fostering consumer trust and enhancing competition in the digital payment sector.

-

Support the current surge in outsourcing activities in areas that are unlikely to be automatised in the near future (e.g. because they rely on human interaction); diversify the supply of these services among regions.

-

Assess whether the regulatory framework for professional services is fit for digital transformation.

-

Continue supporting the growth of the Fintech economy, by improving access to finance and providing regulatory flexibility, with a special focus on smaller firms.

-

Streamline government programmes aimed at supporting the IT and information services.

-

Foster policy coherence and co-ordination of productivity policies at the national and regional level and over time.

copy the linklink copied! Digital market openness and the road to international competitiveness

Digital technologies are transforming the environment in which firms compete, trade and invest. They create new opportunities for trade by reducing trade costs, in particular for small firms, allowing for more efficient co-ordination of global value chains (GVCs), enabling the diffusion of technologies across borders, and connecting businesses and consumers globally (WTO, 2018; López González and Jouanjean, 2017).

Digitalisation is linked with more trade. Analysis shows that a 10% increase in “bilateral digital connectivity” raises goods trade by nearly 2% and trade in services by over 3%. A positive impact arises across all sectors of economic activity, from vegetables to food, mining to metals, footwear to textiles, manufacturing to services. However, it is highest for exports of more sophisticated manufactures and digitally deliverable services.

Digitalisation might also increase the benefits that can be drawn from regional trade agreements. When combined with a regional trade agreement, a 10% increase in digital connectivity increases exports by an additional 2.3%. Finally, there is a statistically significant relationship between ICT goods imports, digitalisation and services exports, suggesting that, just as services have become more important for goods exports, ICT goods increasingly enable the export of digitally deliverable services (López González and Ferencz, 2018).

Indeed, digital transformation has led to growing complementarities between goods and services, giving rise to more trade in “smart” products. Digitalisation has also led to more trade in parcels and lower value digital services (applications) and is increasing the tradability of services. As a result, today’s international trade transactions are more numerous and complex, which raises new challenges for existing trade and trade policy frameworks. In this evolving environment, ensuring that the benefits of digital trade are reaped for businesses and consumers requires new approaches to market openness (López González and Ferencz, 2018; Casalini, López González and Moïsé, 2019).

Digital transformation offers new opportunities for agriculture and food trade, including for more inclusive participation in agro-food GVCs. The wider adoption of technologies such as digital platforms, connected devices and sensors through the Internet of Things, cloud computing, AI and distributed ledger technologies (blockchain) are driving change and giving data a more central role in today’s agrifood value chain.

Digitisation is boosting productivity as a range of digital tools allow producers to access information (e.g. product prices and standards) and services (e.g. payment services) more easily and at a much lower cost. New digital platforms and applications can give smallholders access to agricultural extension and advisory services that previously required the physical presence of experts. Small firms can now be “born global” and consumers can participate directly in trade, substituting traditional wholesalers or retailers with new types of digital intermediaries. These intermediaries often provide additional services through digital applications and platforms which can help smallholders access new and more lucrative markets.

But while digital technologies reduce some costs of engaging in trade, others remain: access to (efficient) transport and trade infrastructure still matters for accessing quality inputs and export markets, particularly for perishable products. Yet digitalisation can also help reduce some of these costs, by, for example, increasing the efficiency and reliability of customs management and the trade logistic chain. Digital technologies can support implementation of the World Trade Organization’s Trade Facilitation Agreement, in particular for automation of processes and consultation and communication, as well as providing new tools for trade finance.

Digital technologies can also enable more automatic checks for compliance with standards, and a more transparent and efficient trade regulatory environment. Increased data management capacity can support improved product traceability and better monitoring of product integrity. That is, in addition to product safety, particularly for perishable products, digital technologies can make it possible to verify that a product is what it claims to be. Moreover, this increased information can create new markets in the agro-food chain for consumers willing to pay more for products they can verify as being produced in a certain way (such as sustainability, or by smallholders or female producers).

Digital technologies can transform the agriculture sector, from enabling further product differentiation and creating access to new markets to new ways to operate transactions and distribute value along the supply chain. However, many tools are at an early age of development and governments need to ensure the security and quality of new technologies and services. In addition, there is a need for greater knowledge among public and private stakeholders about the capacities and limits of new digital technologies.

Source: Jouanjean, M. (2019), “Digital opportunities for trade in the agriculture and food sectors”, https://doi.org/10.1787/91c40e07-en.

A digital trade transaction rests on a series of trade-related factors that enable or support the transaction. For example, ordering a “smart” speaker from a digital retailer requires access to the Internet, the cost of which is conditioned by the regulatory environment in the telecommunications sector. Access to the retailer’s website depends on the regulatory environment which determines the conditions under which the retailer can establish the webpage. The purchase of the speaker also depends on factors such as the ability to pay electronically, the costs of delivering the product across borders, and the tariff and non-tariff barriers faced by the physical device.

A barrier on one of these linked transactions will affect the need or the ability to undertake the other transactions. This means that market openness needs to be approached more holistically, taking into consideration the full range of measures that affect the ability to undertake any particular transaction. From a trade policy perspective, the benefits of the digital transformation are therefore contingent on the combined and smooth functioning of issues which span goods, services and digital connectivity.

However, the nature of the measures that affect how modern firms engage in digital trade is changing; in the digital era old trade issues have new consequences. For instance, de minimis thresholds may have a higher impact today than they had in the past due to growing cross-border trade in parcels arising from new e-commerce business models. But there are also new measures that raise new issues, as might be the case of electronic payments or cross-border data flows. At the same time, access to digital networks and supporting digital services, including logistics and computer services, are increasingly important for digital trade in goods and services to flourish (López González and Ferencz, 2018; Casalini, López González and Moïsé, 2019).

With services increasingly embedded in goods and growing trade in digitally enabled services, restrictions to services trade are growing (Ferencz, 2019). Some of the most common measures relate to policies that impede access to communication infrastructure and movement of information across networks. Less common are barriers affecting electronic transactions and payments. However, other impediments such as the obligation to establish a local presence before engaging in digital trade are also common. A key emerging challenge is that the regulatory environment for digital trade is increasingly tightening, particularly for measures affecting infrastructure and connectivity, among which are measures affecting the movement of data (Ferencz, 2019).

The new era of digital trade provides a range of new opportunities for Colombia. While the impact of digitalisation is pervasive across all sectors, and digitalisation is transforming all forms of trade, including in more traditional sectors of Colombian comparative advantage such as agriculture (Box 4.3), in what follows, some of the focus is on the role of ICT technologies (Jouanjean, 2019).

Colombia should embrace the digital transformation to increase trade and diversify exports

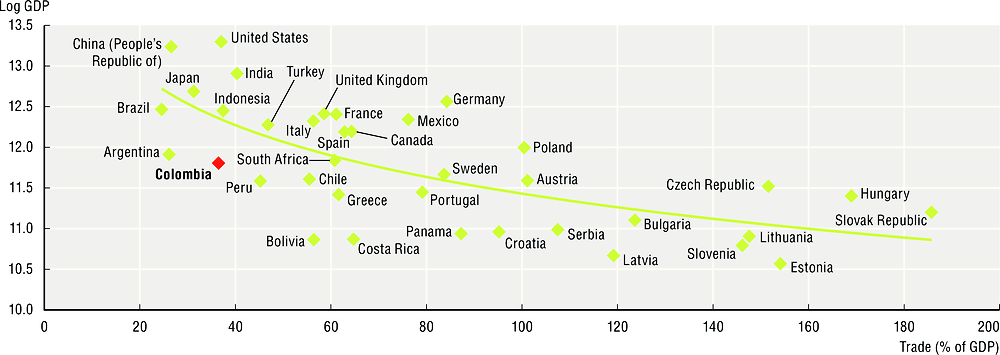

Colombia has a relatively low trade-to-GDP ratio (36.5%) compared to other countries of similar size (Figure 4.12). While trade relative to GDP tends to be lower for large countries, economies that are comparable to Colombia in terms of economic size (GDP), such as South Africa or Sweden, trade relatively more.

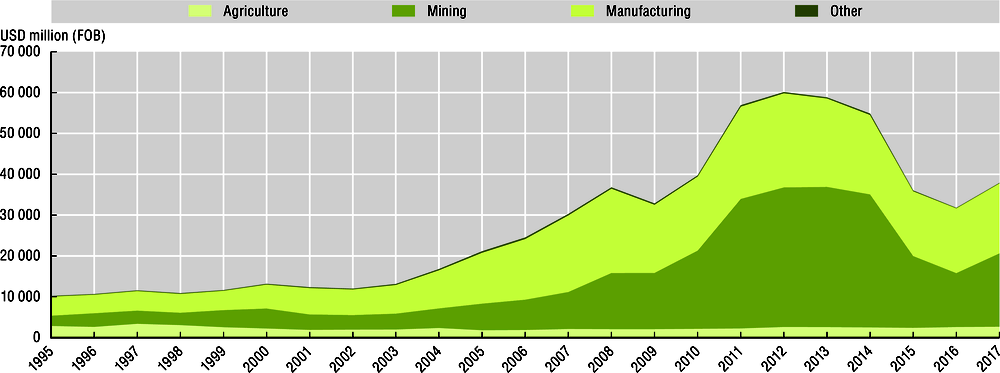

Colombia’s exports have been, in part, driven by changes in world commodity markets over the last decade. Exports of the mining sector expanded substantially during the height of the commodity price boom, accounting for up to 57% of total goods export in 2012 (Figure 4.13). Manufacturing exports also grew substantially in that period, largely determined by the performance of refinement of petroleum, chemical products and basic metal products that jointly accounted for more than 56% of manufacturing exports.

Exports of the mining sector contracted significantly from 2013 onwards, when demand from emerging economies began to slow down. Exports of the manufacturing and agricultural sector profited from the subsequent currency depreciation, but at the same time were more affected than other sectors by the rising cost of raw materials (OECD, 2018a). Nevertheless, in 2016 mining activities still accounted for almost half of all Colombian goods exports (47%).

The digital transformation provides an opportunity for Colombia to increase and diversify its trade. Indeed, higher Internet penetration is associated with more open economies and exporting more products to more destinations. Digitalisation can also enable more trade across all sectors of the economy, including primary, manufacturing and services (López González and Ferencz, 2018).

Notes: Log GDP measured in purchasing power parity at constant (2011, international dollars) prices.

Source: World Bank (2019b), World Development Indicators (database), https://databank.worldbank.org/data/reports.aspx?source=world-development-indicators (accessed on 30 July 2019).

Notes: FOB = free on board. Industry classification ISIC/CIIU Rev. 4. Other includes electricity, gas, steam and air conditioning supply (D35); other activities (D36-D99); total waste (DWASTE) and unallocated or confidential activities.

Source: DANE (2018a), “Colombia, exportaciones totales”, https://www.dane.gov.co/index.php/estadisticas-por-tema/comercio-internacional/exportaciones.

Although from a low base, gross services exports are growing faster than in many other countries

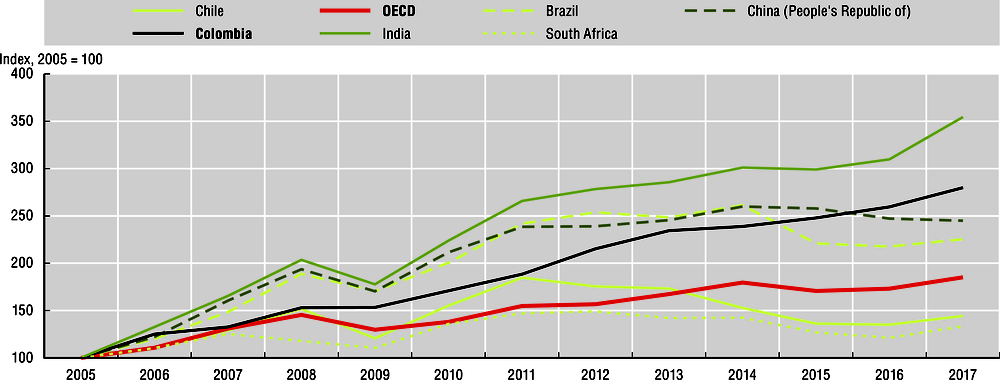

Between 2005 and 2017, Colombian exports of services increased by a factor of 2.8, compared to a factor of 2.45 in China, 2.25 in Brazil and 1.85 in OECD countries on average (Figure 4.14). Only India (3.54), Poland (3.21), Ireland (3.18), Lithuania (3.1) and Iceland (2.84) had higher growth rates for services exports.

As a result, the share of services in Colombia’s total exports almost doubled between 2011 and 2017, from 8.8% to 17.4%, surpassing South Africa (15.2%), Brazil (13.7%) and Chile (12.7%). However, the services share in exports remained far behind other countries, including Costa Rica (44.6%), India (37.8%), the United States (33.9%) and the EU28 (31.3%) (OECD, 2019a).

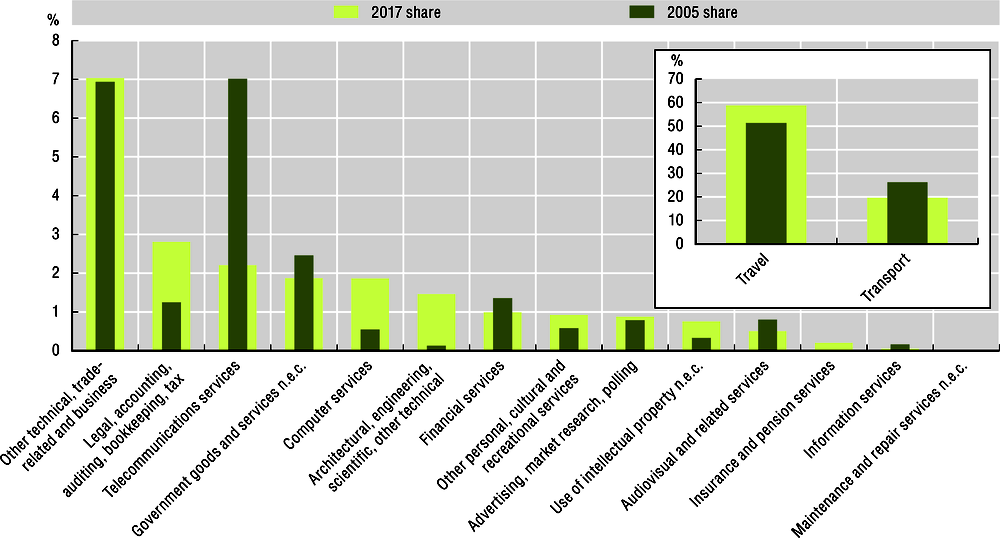

The composition of Colombia’s gross exports in services has been changing since 2005. The most important service trade category, by far, is travel services, encompassing services consumed by non-residents, i.e. in the case of Colombia, mostly tourism services in the form of accommodation, food, beverages and domestic transport services purchased by foreign visitors. The share of travel services in total services exports significantly increased between 2005 (51.4%) and 2017 (58.9%), a trend that is partly driven by improvements in the overall security situation. However, the digital transformation likely supported this process, for example by increasing real-time updates on the security situation and enhancing access to digital tourism services (e.g. online booking), price comparison websites and travel recommendations.

Several other sectors that contributed significantly to services exports either reduced their contribution in relative terms (e.g. transport services) or more or less sustained their contribution relative to other sectors (e.g. other technical and trade-related business services).

Source: OECD (2019a), Balance of Payments BPM6 (database), https://stats.oecd.org/Index.aspx?DataSetCode=MEI_BOP6.

Notes: n.e.c. = not classified elsewhere. Other technical, trade-related and business includes other business services n.e.c., trade-related services, operating leasing services, waste, agricultural and mining services (43-46).

Source: OECD (2019e), “Trade in services – EBOPS 2010”, https://doi.org/10.1787/data-00583-en (accessed on 31 July 2019).

While relatively small in absolute terms, the contribution of several services that, at least to some extent, can be digitally delivered (potentially ICT-enabled services) increased. Thus, professional and management consulting services, and in particular legal, accounting, auditing, bookkeeping and tax consultation services, more than doubled between 2005 and 2017, from 1.25% to 2.8%. Even larger growth rates were observed for exports in technical services, such as architectural, engineering, scientific and other technical services, whose contribution, while small in absolute terms, significantly increased from close to 0 (0.13%) to 1.46%.

Other potentially ICT-enabled sectors, such as financial and audiovisual, grew significantly between 2005 and 2017 in absolute terms (103% and 75% respectively), but lost ground to other service sectors with higher growth rates. Exports of telecommunication services diminished significantly even in absolute terms (from USD 210 million to USD 183 million), in line with the reduction in employment and revenues discussed above and in Chapter 2.

Some of these dynamics were likely supported by the relatively open regulatory framework for most services sectors, including for computer, construction, professional services, telecommunications, distribution, transport, financial, audiovisual and logistics services, where Colombia compares favourably with OECD countries (OECD, 2018a).

ICT embodiment in Colombian exports and production is low

Compared to OECD countries, Colombia has a low share of ICT value added in exports. With the limitation that the embodiment of ICT value added in exports only captures ICT content embodied in purchased inputs and excludes in-plant or firm production, the embodiment in exports can more broadly serve as a proxy for the ICT intensity of production.6 Depending on the sector, ICT value added, e.g. arising from the use of computers, cloud computing and other ICT products, contributed between 0.15% (real estate activities) and 58.6% (IT and other information services) to sector-level gross exports. This compares to shares ranging from 0.96% for real estate activities to 62.7% for telecommunications and 61.3% for IT and other information services in OECD countries (Figure 4.16).

Notes: n.e.c. = not classified elsewhere. ICT goods include computer, electronic and optical products (D26); ICT services include telecommunications (D61) and IT and other information services (D62, D63). The figure gives the share of (purchased) ICT value added in gross exports by exporting industry.

Source: OECD (2019f), “Trade in value added”, https://doi.org/10.1787/data-00648-en (accessed on 22 April 2019).

ICT value added content was particularly low for some key export products of Colombia, including agriculture, forestry and fishing (0.3% compared to 1.2% in OECD countries); mining and quarrying (0.4% to 1.3%); but also accommodation and food services (0.3% to 1.4%).

ICT services imports are growing fast

Because the domestic ICT services sector is relatively small in Colombia (Figure 4.10), the digital transformation of sectors crucially depends on the availability of ICT goods and services from world markets and the knowledge embedded within them.

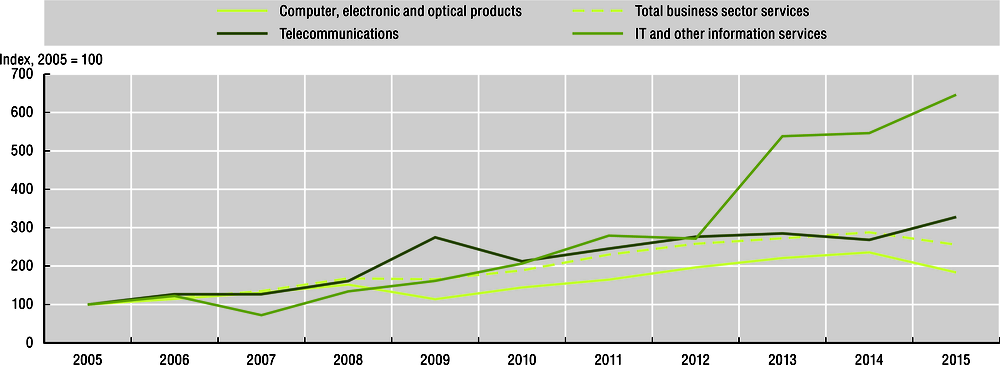

In particular, with the rise of cloud services and ever-cheaper access to virtual computing power, an increasing share of these ICT inputs is now being delivered in the form of ICT services. This has fuelled fast growth in imports of ICT services, in particular IT and information services. Imports of IT and information services grew by a factor of 6.5 between 2005 and 2015, significantly faster than other business services (Figure 4.17).

Note: Imports refer to gross imports worldwide.

Source: OECD (2019f), “Trade in value added”, https://doi.org/10.1787/data-00648-en (accessed on 22 April 2019).

Note: World gross imports and exports. Foreign value added measures the value added produced abroad and embedded in gross exports; domestic value added measures the value added produced domestically and embedded in gross exports.

Source: OECD (2019f), “Trade in value added”, https://doi.org/10.1787/data-00648-en (accessed on 22 April 2019).

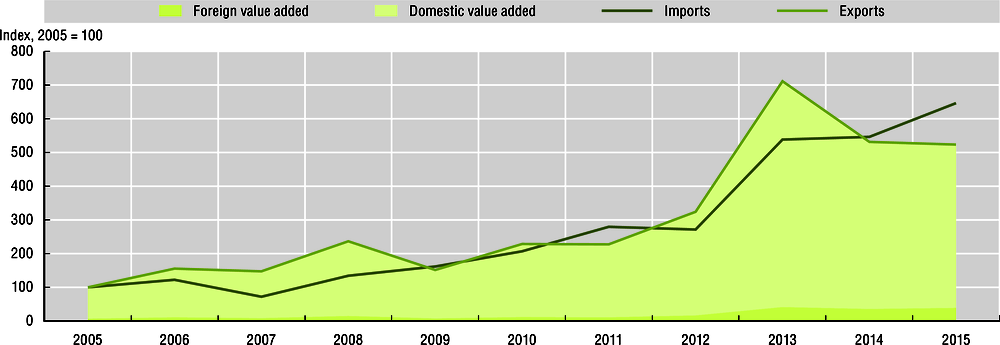

Importantly, imported IT and information services are not only crucial inputs into digital transformation across sectors, but in particular for the domestic ICT sector. The increasing access to information services from world markets has accordingly likely helped to make the domestic IT services sector more competitive: while gross exports of the sector are still small compared to imports (12%), implying a negative trade balance, exports of Colombian IT and other information services have grown just as fast as imports over the past years (Figure 4.18).7

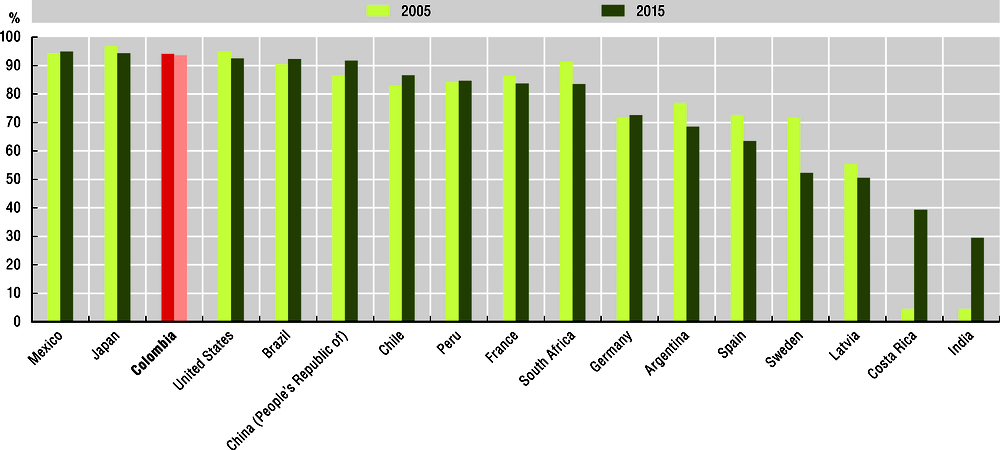

Despite the significant increase in exports, about 93.7% of value added created by the sector was absorbed domestically in 2015 (Figure 4.19). While this points to a relatively low export orientation of the domestic ICT sector, it could also reflect the activity of multinational enterprises that supply ICT services to the Colombian market via foreign direct investments and local affiliates rather than exports from abroad.

Notes: Share of domestic value added by IT and other information services (D62, D63) that is absorbed by total domestic final demand.

Source: OECD (2019f), “Trade in value added”, https://doi.org/10.1787/data-00648-en (accessed on 22 April 2019).

Export promotion programmes would benefit from better co-ordination

The Colombian government is actively engaged in promoting exports by local firms and fostering their integration in GVCs, with some programmes focusing specifically on services and ICTs. The key agency in export promotion is PROCOLOMBIA, associated with MinCIT. PROCOLOMBIA is based on 3 pillars – namely exports, foreign direct investment and tourism – and currently has over 30 offices in Colombia and abroad, with a reach in 33 countries and 19 departments. Since 2012, all three pillars are supported by the country brand strategy Marca País Colombia (CO), aiming at promoting Colombia’s value proposition to the world.

PROCOLOMBIA has several lines of action particularly linked to services sectors. In line with the sector strategy prioritised through the Productivity Transformation Programme, the agency specifically promotes foreign investments in the software and IT sector, outsourcing activities as well as wellness and nature tourism (see above), but also for data centres and connected goods and services. In 2015, MinCIT introduced the strategy Colombia Exporta Servicios, with the goal of increasing services exports to USD 9 billion by 2018 (MinCIT, 2015). The strategy has been realised with participation of PROCOLOMBIA. With services exports currently standing at USD 8.9 billion (2018), up from USD 7.6 billion in 2015, the programme will come close to reaching the original goal.8

The initiative is based on three strategic pillars, namely strengthening entrepreneurial capacity, trade promotion and improving the business climate. It provides guidance on the provision of several services to other countries, including digital animation and video games, mobile applications, audiovisuals, BPO, software, communications, engineering, and health. However, in spite of the potential for many of these services to be digitally delivered, this potential is not specifically addressed by the programme. Additionally, some dynamic and potentially competitive sectors with a relatively high outward orientation such as Fintech, are currently not explicitly included in the export strategy.

For the software and IT sector, PROCOLOMBIA has further been running the Colombia Bring IT On campaign since 2014, which is funded by MinTIC and aims at better positioning the Colombian IT and digital content industry in international markets (Apps.co, 2016). According to MinTIC, 2 645 firms have benefited from the programme as of 2019. The programme is further supported by the IT Mark, an acknowledgement by MinTIC for firms that help to better position the sector in the domestic economy and on world markets (see Chapter 5).

While Colombia Bring IT On and Colombia Exporta Services both fit into the MinCIT strategy, the initiatives are currently presented on different websites, with limited interlinkages between them. This can make it difficult for firms to find and access the available support for the sector. More generally, the alignment of existing government programmes relating to the software and IT sector has also been recommended by the PTP (2017b) as part of its recent assessment of the cluster.

For sectors beyond services, MinCIT is currently also fostering closer co-ordination with the IADB on the use of the IADB’s digital e-commerce platform ConnectAmercias in order to better connect SMEs from Colombia with other SMEs across Latin American countries and the Caribbean.

International market openness in a digital age

As highlighted above in the context of Colombia’s rising exports of IT and information services, the performance of the digital industry hinges crucially on access to technology and knowledge imports as well as competition from other countries. This links closely to the current policy debate on market openness principles for a digital world. New business models, deeply integrated GVCs and increasing cross-border data flows are changing the determinants of market openness and complicate policy making in this area (López González and Ferencz, 2018; López González and Jouanjean, 2017).

In terms of classical market openness for trade, Colombia has made great progress in developing a regulatory framework supportive of trade and investments. This involved improving the legal framework for intellectual property rights protection and signing numerous bilateral investment treaties and free trade agreements, including with its largest trade partner (the United States, Decree 993, 2012) as well as with the European Union and Peru (OECD, 2014; MinCIT, 2018). Significant progress has also been made in the area of digital trade policy and non-tariff trade barriers.

Since 2011, Colombia, together with Chile, Mexico and Peru, forms part of the Pacific Alliance, which aims at deeper integration of the region via the free movement of goods, services, resources and people. Importantly, along with several chapters that seem relevant in the context of digital transformation, including telecommunication or financial services, the Additional Protocol to the Framework Agreement to the Pacific Alliance further offers a relatively large number of e-commerce provisions that could determine digital trade among the participating countries over the coming years (Monteiro and Teh, 2017). This includes, for example, measures to facilitate commercial transactions realised by electronic means (e-commerce) and to avoid unnecessary barriers (Art. 13.3 and 4). The additional protocol furthermore recognises the importance of accounting for the interest of all stakeholders when defining e-commerce policy, including business, consumers, non-government organisations and relevant public institutions (Art. 13.3). Overall, the protocol incorporates more provisions on consumer protection than other trade agreements and stipulates that the parties shall standardise information provided to consumers in e-commerce, considering at least the conditions of use, prices, additional charges if applicable, and forms of payment (Monteiro and Teh, 2017). Countries have also explicitly stated an interest (non-binding) to negotiate commitments regarding cross-border flows of information in the future (Art. 13.11).

As most of these provisions are currently non-binding or best endeavours only, it is unclear to what extent they will translate into positive trade effects. Nevertheless, it is important for Colombia to enable trade in the digital era and to increase consumer trust into cross-border transactions. This will be crucial, as a lack of trust has been identified as one of the main factors that prevent Colombians from engaging in e-commerce and other forms of digitally enabled trade (CRC, 2017b).

In 2012, Colombia joined the World Trade Organization’s Information Technology Agreement (ITA), which aims at liberalising trade in ICT products. This was a crucial step, in consideration of the low productivity of the domestic ICT manufacturing sector. More recently, Colombia also signed the ITA extension, which added 201 new product categories to the original agreement. Eliminating remaining tariffs on technology imports according to the agreed-upon schedule should now be a priority for Colombia.

Non-tariff measures and trade facilitation

Cadestin, Gourdon and Kowalski (2016) find that about 40% of Colombian imports involve products affected by so-called non-tariff measures (NTMs). These measures often relate to regulations and procedures put in place to assess the compliance of products with domestic quality or product safety standards. In some cases, NTMs can have an adverse trade effect, but in others they can have a positive impact, in particular when they help firms signal quality in their products (see Cadot, Gourdon and van Tongeren [2018]).

Consumer goods are often affected by these measures, meaning that the application of NTMs might be of particular relevance for cross-border business to consumer e-commerce transactions. These challenges have been confirmed in OECD interviews with businesses active in cross-border e-commerce in Colombia. To increase competition and broaden access to a larger variety of goods and services at lower prices, Colombia could aim at reducing unnecessary trade costs related to NTMs.

Trade facilitation refers to transparent, predictable and straightforward border procedures that expedite the movement of goods across borders. In terms of administrative procedures at the border, progress has been particularly noticeable in areas such as administrative simplification, customs reforms, or with respect to the streamlining the processes of preparing technical regulations and the management of import licencing via the single window for international trade transactions, the Ventanilla Única de Comercio Exterior, introduced in 2004 (OECD, 2018a). In the context of the single window, the government has recently launched a pilot that could help facilitate the submission of documents for air cargo shipments. In particular, as part of its anti-narcotics management, the national police requires all exporters to submit a “letter of responsibility” for each shipment. In 2014, this document was systematised for all maritime operations registered in the single window, benefiting 719 871 containerised cargo operations between 2017 and 2018 according to information provided by MinCIT. At airports, it is generally still required for the legal representative of the exporting company to sign this document and present it physically to the anti-narcotics officers. However, in October 2018, the government started a pilot to systematise the operations for air cargo (Circular No. 036), dropping the requirement of physical documentation for Avianca Airlines and 19 air cargo exporting companies selected by the anti-narcotics management. According to MinCIT, the new approach has the potential to eliminate about 2.2 million documents per year and significantly reduce response times in the context of anti-narcotics management.

In international comparison, Colombia now outperforms other Latin America and Caribbean (LAC) countries in terms of the cost of documentary requirements for both imports and exports, but is still significantly behind OECD countries (World Bank, 2019a). However, obtaining, preparing and submitting documents for Colombian exporters still requires about 7.5 hours more than in regional peer countries (60 vs. 52.5 hours). Border processing itself, including customs clearance or inspections, still requires around 50 hours more (112 hours) than in other LAC countries (62-63 hours) for both imports and exports, indicating significant room for improvement. The World Bank’s trading across borders indicator, summarising Colombia’s performance in terms of time and costs for trade documentation and border compliance, shows that overall Colombia still ranks far behind OECD countries but also below the Latin American average, including countries such as Argentina, Brazil, Ecuador and Peru (World Bank, 2019a). The effective use of digital tools to streamline border processes should therefore be high on Colombia’s trade policy agenda, an aspect that has been explicitly acknowledged in the PND 2018-2022, within the pact for entrepreneurship, formalisation and productivity (DNP, 2019). Full implementation of the Trade Facilitation Agreement could help cut Colombia’s trade costs by up to about 14.5%, fostering the country’s integration into GVCs (OECD, 2018b).

The latest OECD Trade Facilitation Indicators (TFI) show that in 2017 Colombia equalled or exceeded the average performance of upper middle-income countries in all TFI areas, in particular for areas such as automation, governance and impartiality, documents or trade community involvement.9 Colombia achieved best or close to best practice performance with regard to information availability, trade community involvement, advance rulings, fees and charges, simplification and harmonisation of documents, automation, internal border agency co-operation, and governance and impartiality.10 However, between 2015 and 2017 Colombia lost some ground with regard to information availability, involvement of the trade community and appeal procedures, highlighting a need to keep track with other countries.

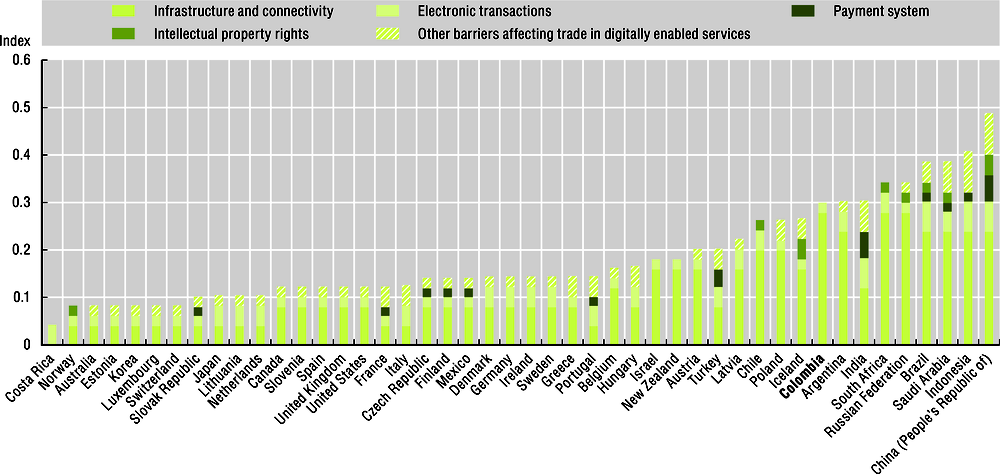

Digital Services Trade Restrictiveness

With an index value of 0.299 in the new OECD Digital Services Trade Restrictiveness Index (DSTRI), Colombia ranked 38th out of 46 countries for which the DSTRI was available in 2018 (Figure 4.20). The DSTRI collects information on and measures cross-cutting barriers that affect trade in digitally enabled services. It is comparable across 46 countries and can help to identify regulatory bottlenecks to digital trade. Data are collected from publicly available laws and regulations. The framework of measures is comprised of five policy areas: 1) infrastructure and connectivity; 2) electronic transactions; 3) measures affecting payment systems; 4) intellectual property rights; and 5) a cluster of other cross-cutting barriers. The index is based on a binary scoring system of 0s and 1s, where 1 indicates the presence of a restriction. The final index is derived by aggregating the weighted contribution of individual measures resulting in indices ranging between 0 (no barriers) to 1 (high barriers) (Ferencz, 2019).

Notes: Based on qualitative information, composite indices provide a weighted average over identified (binary) restrictions in five standard policy categories, with values between 0 and 1. Complete openness to trade and investment gives a score of 0, while being completely closed to foreign services providers yields a score of 1.