5. Review of supplementary pension savings arrangements

This chapter reviews the regulation, design and outcomes of the Slovenian supplementary pension system. It assesses these elements against international standards and practices to identify possible areas where improvements may be needed to strengthen the sustainability and role of this segment of the pension system in the provision of retirement income.

The Slovenian pension system comprises a public pay-as-you-go component, as well as a supplementary component, where assets accumulate to back individuals’ future retirement income. The size of the supplementary pension component in Slovenia is relatively modest in international comparison, and this chapter aims to uncover possible areas where improvements may be required to strengthen the sustainability and role of this segment of the pension system to ensure Slovenian people receive an adequate income in retirement.

This chapter first describes the structure of the Slovenian supplementary pension system, and then analyses its coverage and contributions. The third section covers the tax treatment of retirement savings. The fourth section looks into the assets and investments of the supplementary pension system, while the fifth section analyses the risk management and funding requirements applicable to supplementary pension funds. The sixth section describes the pay-out options available to Slovenians saving for retirement and the different rules which apply to these options. The seventh section discusses aspects related to the relationship between providers and members of the supplementary pension system, including applicable fees and communication with members. The eighth section concludes by highlighting some of the challenges identified in the Slovenian supplementary pension system.

This review is complemented by a proposal for reform in Chapter 6, which offers policy options to improve and reinforce the supplementary pension system in Slovenia based on the challenges identified.

The Slovenian supplementary pension system is organised according to different types of pension plans, and comprises both mandatory and voluntary occupational and personal retirement savings arrangements. Occupational and personal retirement savings arrangements may be set up as mutual pension funds, umbrella pension funds (consisting of sub-funds) or long-term business funds; and they can be managed either by pension companies, insurance companies or banks (Table 5.1).

Different legislations and regulations apply to retirement savings arrangements, depending on their structure. Pension companies are defined and governed by the Second Pension and Disability Insurance Act (ZPIZ-2), while insurance companies may be authorised to conduct life insurance activities, including retirement savings activities under the insurance law, and banks may be licenced to operate pension funds under the bank law. Three institutions supervise the private pension system in Slovenia: the Securities Market Agency (SMA) and the Bank of Slovenia supervise retirement arrangements set up as mutual and umbrella pension funds. The Insurance Supervision Agency of Slovenia (ISA) supervises insurance and pension companies and is responsible for supervising the implementation of the provisions of ZPIZ-2 for long-term business funds.

5.2.1. Occupational schemes

The Slovenian funded pension system comprises both mandatory and voluntary occupational retirement savings components.

Mandatory occupational retirement savings plans

Occupational retirement savings plans are mandatory for two groups of workers in Slovenia: people working in arduous and hazardous occupations, and civil servants.

Mandatory scheme for workers in arduous and hazardous occupations

The mandatory scheme for workers in arduous and hazardous occupations is a hybrid defined contribution-defined benefit retirement savings plan, designed for workers who are deemed not to be able to work until the statutory retirement age, because of difficult working conditions or of an adverse effect of their occupation on workers’ health and working capacity.

Occupations covered by this scheme are considered as particularly difficult and unhealthy, or cannot be successfully performed professionally after a certain age, i.e. until the conditions to receive a public pension are fulfilled.

Occupations which are subject to the mandatory scheme for workers in hazardous jobs are meant to be determined by a commission, based on criteria set by law, although the system is not yet in force.1 Currently, the list of occupations which was set about 50 years ago still determines which workers are subject to this mandatory scheme. The list of occupations is published on the Ministry of Labour, Family, Social Affairs and Equal Opportunities’ website and includes for example miners, firefighters and lorry drivers.2 However, a new law requires that the criteria are set by a commission consisting of seven members: three appointed by employers’ associations, three appointed by national trade unions or confederations, and one appointed by the Ministry of Labour, Family, Social Affairs and Equal Opportunities.3 A special law may also define additional occupations for which enrolment into the scheme for workers in arduous and hazardous occupations is compulsory. The regulation governing this has not yet been adopted and the commission is yet to be appointed.

For workers in hazardous and arduous occupations retiring early, the occupational retirement scheme acts as a bridge between employment and the statutory retirement age, when the public pension starts covering them, and is therefore a hybrid scheme with benefits linked to assets accumulated from contributions, and subject to a minimum and maximum income based on the minimum and maximum old-age pension. Workers covered by the scheme who decide not to retire early may use assets accumulated in the scheme to receive additional retirement income upon reaching the statutory retirement age.

A single provider, Kapitalska Družba, manages this mandatory scheme, which is established as a mutual pension fund. Kapitalska Družba is fully owned by the Republic of Slovenia.

Mandatory scheme for civil servants

The mandatory scheme for civil servants is a defined contribution retirement savings plan, which all civil servants join upon starting employment.

The insurance company Modra zavarovalnica (Modra) has managed the occupational scheme for civil servants since 2004, taking over from Kapitalska Družba. Kapitalska Družba managed the civil servants fund from 2004 until 2011. In October 2011, after structural and legislative reforms, Kapitalska Družba was restructured and Modra was created as a spin-off entity for pension fund asset management and activities. Modra took over the management of the closed mutual pension fund for civil servants, among other functions.4 The scheme for civil servants is set up as an umbrella pension fund. It is closed and as such cannot be joined by workers outside the public sector. Despite the restructure, Kapitalska družba continued to manage the fund of compulsory supplementary pension insurance for people in hazardous and arduous occupations.

Voluntary occupational retirement savings plans

For all other workers in Slovenia, occupational retirement savings schemes are voluntary. If a company has a representative trade union, that trade union decides on whether a pension plan would be included in employees’ contracts. If there is no representative trade union in the company, this decision falls on a workers’ council. If there is neither a representative trade union nor workers’ council at the workplace, employees can decide directly on the formation of a pension plan at the assembly of workers or with a special written statement. In this case, the decision requires a simple majority vote (50%) by all employees. Once an occupational retirement savings plan has been set up, all employees can join the plan.

Voluntary occupational schemes can be managed by pension companies, insurance companies or banks, and may be set up as closed or open funds. Occupational plans can be managed by pension companies regulated under the Second Pension and Disability Insurance Act (ZPIZ-2), insurance companies licenced to operate life-insurance business and regulated under insurance law or banks licensed to operate pension fund management operations and regulated by the banking law. Funds may either be closed to employees of the founding employer(s) or open to employees from different employers. At present, the public sector fund is the only closed fund in Slovenia. Mutual funds and umbrella pension funds can be set up as closed funds if they have at least 1 000 members, while this membership floor does not apply to closed long-term business funds.

5.2.2. Personal schemes

Personal retirement savings schemes are voluntary, and are similar in structure to voluntary occupational schemes. They can be set up as mutual pension funds, umbrella pension funds, and long-term business funds by pension funds, pension companies and banks. Any individual can join a personal retirement savings plan, as long as they are covered by the compulsory pension and disability insurance.

5.2.3. Market structure

Kapitalska Druzba is a public company founded and owned by the Republic of Slovenia. It is in charge of providing additional funds for pension and disability insurance by managing both the mandatory scheme for workers in arduous and hazardous occupations, and the equity holdings of the Republic of Slovenia.

Modra has managed the closed scheme for civil servants since 2004. This provider was chosen through a public tender open to all financial institutions (public and private), and selected by a committee comprising four members of the government, four trade union representatives, each holding one vote, and advised by four independent members with no voting power. As a spin-off from Kapitaska Druzba, Modra was created in 2011 as a private insurance company, although fully owned by Kapitalska Druzba. The collective agreement establishing the scheme for civil servants lays out a procedure for replacing the fund manager, at the request of the fund management board. No such procedure has yet been initiated.

There are currently three pension companies. four insurance companies, and one bank offering voluntary supplementary pension funds in Slovenia (Table 5.2).

Excluding assets saved by civil servants and workers in arduous and hazardous occupations under their respective closed schemes, one pension company (Triglav pokojninska družba) and one insurance company (Prva) hold the highest market shares in terms of assets managed (with 20% and 18% of assets at end of 2020 respectively). Three additional companies – one pension company (Pokojninska druzba A) and two insurance companies (Modra zavarovalnica and Zavarovalnica Triglav) – represent 10% of assets managed or more (17%, 17% and 13% respectively). Overall, these five companies combined manage 84% of assets saved for retirement in voluntary collective and personal pension plans, while the remaining four companies combined manage 16% of assets. Table 5.2 recaps the assets managed at the end of 2020 by the different providers of voluntary supplementary pension, by company type, together with their respective market share.

A new pension plan manager may enter the market if it complies with the rules set forth by ZPIZ-2 and is granted a permit to operate a pension fund by the Insurance Supervisory Agency of Slovenia (ISA), or the Securities Market Agency (SMA), depending on the type of managing entity and chosen pension plan structure. The supervisory authority issues a permit or license to perform the activities of pension provision to the entity, and must also authorise each fund or sub-fund to operate.5 The Ministry of Labour, Family, Social Affairs and Equal Opportunities establishes and updates a register of authorised pension plan managers and their pension funds. In order for its members to benefit from the income and corporate tax relief for contributions to retirement savings plan, a pension plan manager must also be registered with the tax authority.

5.3.1. Overall coverage and contributions

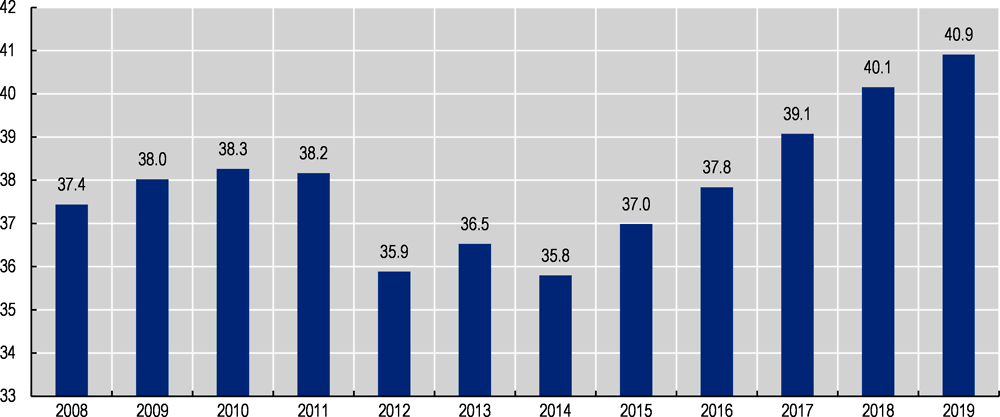

Overall, 40.9% of the Slovenian working-age population were covered by a supplementary retirement savings plan in 2019. The coverage rate has increased slightly over the past decade, from 37.4% of the working-age population in 2008 (Figure 5.1).

It is estimated that over 95% of those with a supplementary retirement savings plan hold a collective plan, i.e. a plan set up and managed through their employer. Coverage rates encompass both types of plans, occupational and personal, as disaggregated data could not be obtained.

Slovenia ranks among the middle to lower end of OECD countries with voluntary pension systems in terms of coverage. Figure 5.2 illustrates the coverage of retirement savings arrangements of Slovenia in comparison to other OECD countries where retirement savings arrangements are also voluntary. Coverage in this group of countries ranges from over 70% in countries with automatic enrolment schemes such as New Zealand and Lithuania, and over 60% for voluntary personal schemes in Poland and the Czech Republic, down to close to 12% in Italy and Turkey’s voluntary personal schemes and 5.2% in Luxembourg’s voluntary occupational scheme.

Note: Coverage rates are provided with respect to the total working-age population (i.e. individuals aged 15 to 64 years old), except for Germany (employees aged 25 to 64 subject to social insurance contributions) and Ireland (workers aged between 20 and 69). Data refer to 2019 or to the latest year available. Data refer to 2018 for Belgium and France, to 2017 for Portugal and Spain, to 2016 for Turkey, to 2015 for Germany and to 2014 for New Zealand. For Italy, the coverage rate that is shown under voluntary occupational plans also covers individuals automatically enrolled in a plan.

Source: OECD Pension Markets in Focus 2020.

The supplementary retirement system in Slovenia cannot be considered as fully voluntary as a high proportion of members are included through the mandatory schemes for civil servants and workers in arduous and hazardous occupations. When removing all members covered by these mandatory schemes, the coverage of purely voluntary supplementary retirement savings arrangements in Slovenia falls to 19.9% of the working-age population (Figure 5.2).6

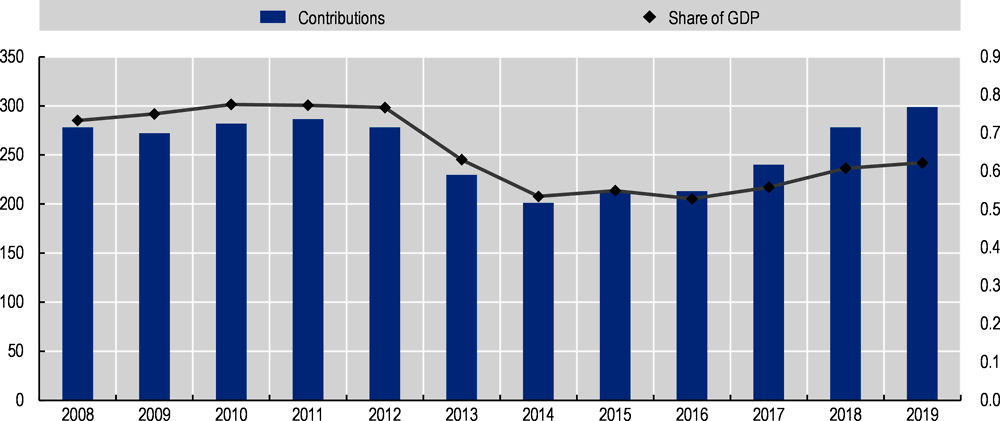

Total contributions to the supplementary pension system represented EUR 299 million in 2019, up 7% from 2018 (EUR 278 million). Over the past decade, total contributions have remained relatively stable around EUR 280 million between 2008 and 2012, declined sharply to EUR 230 million in 2013 and EUR 201 million in 2014, before increasing back starting in 2017 (Figure 5.3). The significant decline in total contributions coincides with austerity measures which came into force starting in June 2013 and affected mandatory employer contributions to the mandatory scheme for civil servants.

Contributions to the supplementary pension system are low in international comparison. In 2019, total contributions represented 0.6% of GDP in Slovenia. This is below the levels in voluntary systems in Canada, the United Kingdom, Portugal, and New Zealand (between 2% and 3% of GDP), but above those in Hungary, Germany, Luxembourg and Austria (0.2% to 0.3% of GDP) (Figure 5.4).

Source: OECD Pensions Markets in Focus 2020.

Note: Data for Austria refer to Pensionskassen only. Data for Belgium cover pension funds and individual pension savings. Data for Canada refer to trusteed pension funds only. Data for the Czech Republic includes employer, employee and state contributions. Data for Hungary refer to contributions paid into pension funds only. Data for New Zealand refer to employer, employee and state contributions into KiwiSaver plans for each financial year. Data for Portugal cover closed and open pension funds, personal retirement saving funds (established as pension funds or as collective investment schemes managed by investment companies), and personal plans offered by life insurance companies. Data for Slovenia covers contributions to both voluntary and mandatory supplementary pension plans. Data for Spain refer to contributions paid into pension funds and book reserves. Data for Turkey refer to personal plans only.

Source: OECD Pensions Markets in Focus 2020.

5.3.2. Mandatory occupational funded schemes

Mandatory scheme for workers in arduous and hazardous occupations

The mandatory scheme for workers in arduous occupations covered approximately 48 300 people in 2019, of which slightly more than half were receiving contributions from their employer. Only 252 self-employed workers were covered by this scheme in 2019, of which 91 were making contributions.

Employer contributions are currently set at 9.25% of gross wages for all workers in arduous and hazardous occupations. When this compulsory supplementary pension scheme was introduced in 2001, the contribution rate was initially set at different levels according to the different groups of employment defined in the mandatory pay-as-you-go system, with rates varying from 4.20% to 12.60% of wages from the first to the fifth group respectively. The rate was uniformed over time, first at 10.55% of wages (except for the fifth group of employment, which remained with a contribution rate of 12.60%) between 2010 and 2014, and then at 9.25% of wages from 2014. A transitional rate of 8% applies between 2017 and December 2021 to workers already enrolled in the scheme. During maternity and parental leave, occupational insurance is dormant and the employer is not required to pay contributions.

Mandatory scheme for civil servants

The mandatory scheme for civil servants was introduced in 2003 and currently covers approximately 235 000 workers, of which around 72% are women, and over 80% were receiving contributions from their employer.7 Civil servants covered by the scheme include employees of the central government, local authorities and other institutions and agencies governed by public law.8

All civil servants are covered by the scheme, from the date of their employment. There is no vesting period before joining the occupational scheme for civil servants in Slovenia, which is not the case for the scheme for civil servants in many OECD countries (OECD, 2016[1]). Even in countries where the occupational scheme for civil servants acts as a mandatory top-up on the public pension scheme, such as in Slovenia, civil servants must often have worked for a certain number of years before being fully eligible to the benefits of their specific occupational scheme. In Norway for instance, the vesting period for the civil service scheme is three years, while in Ireland it is two years. The absence of a vesting period guarantees that all civil servants in Slovenia are covered from the date they start employment in the public sector.

Contribution rates are not linked to wages, but rather depend on the date at which employees join the scheme. When the scheme was introduced on 1st August 2003, civil servants were allocated to a contribution class based on their total employment history at the time, with employment periods in both the public and private sector counting towards the total. Contribution classes were not updated after 2003, and members joining the public sector on or after 1st August 2003, are allocated to the lowest contribution class, including those who leave and later re-join the public sector. At end 2017, 57% of female civil servants and 55.6% of male civil servants therefore received the lowest employer contribution level. Employer contributions must be continued during maternity and parental leave.

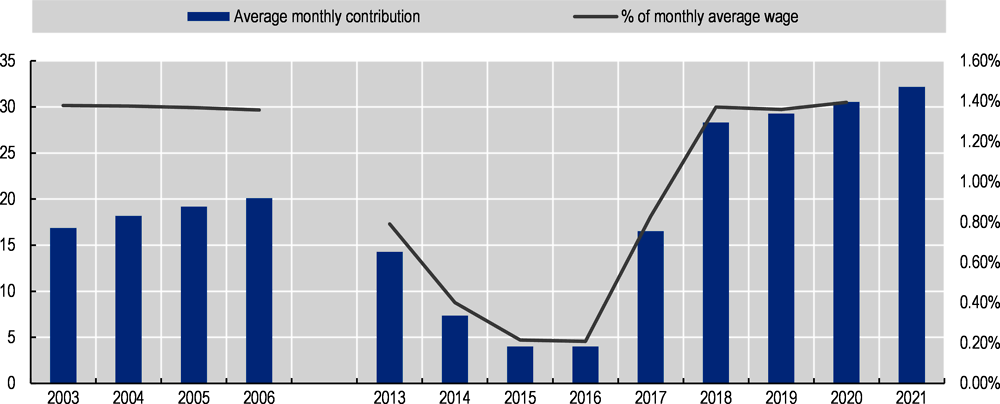

The annual increase in the average salary of employees of legal entities in Slovenia over the period from January to October of the previous year determines the monthly contribution for the lowest contribution class.9 In 2003, this monthly contribution was set at EUR 16.86, while from 1 January 2021, it is set at EUR 32.18. Between June 2013 and December 2017, this calculation rule was not applied due to austerity measures being implemented, and monthly contributions were not increased but rather significantly cut by a factor of up to almost ten, before being set back to levels close to those of May 2013 in January 2018. Table 5.3 details the range of monthly contributions received by civil servants in 2003, 2015 and 2021: from EUR 16.86 in 2003, EUR 2.68 in 2015 and EUR 32.18 in 2021 for the lowest contribution class, i.e. for civil servants joining the scheme with no prior employment history in 2003 or after 2003, to EUR 42.22 in 2003, EUR 5.62 in 2015 and EUR 61.62 in 2021 for those with 35 years of service or more prior to 1st August 2003.

The monthly contribution received by most civil servants represented approximately 1.4% of the average monthly wage in Slovenia in 2020. Figure 5.5 shows the evolution of the lowest contribution received by civil servants, i.e. the contribution received by most civil servants, between 2003 and 2021, in EUR and as a percentage of the average monthly wage. This fraction of the average wage has remained constant over time, except between 2013 and 2017 when austerity measures were in place, and when the contribution received by the majority of civil servants represented between 0.2% and 0.8% of the average monthly wage.

Note: Data on contributions unavailable between 2007 and 2012. The monthly contribution shown is the weighted average of contributions received during a given year. The average wage is expressed in EUR at current prices for the years considered.

Source: IER report on the umbrella pension fund for civil servants, https://www.modra.si/wp-content/uploads/2021/01/Premije-JU-2021.pdf and OECD estimates.

5.3.3. Voluntary occupational and personal funded schemes

Coverage of voluntary retirement savings schemes

Voluntary pension schemes, either occupational or personal, represent approximately 310 000 pension contracts at the end of 2017. The coverage of supplementary retirement savings arrangements in Slovenia may include some minor double counting of members holding more than one pension contract with different pension providers. Based on data received from supplementary pension providers, the Institute of Economic Research (IER) estimates that 5% of individuals hold more than one voluntary retirement savings policy with one pension provider. No data could be obtained as to how many individuals hold pension contracts with more than one provider.

A majority of voluntary supplementary retirement savings contracts in Slovenia receive contributions from either members and/or their employers. According to IER data for 2017, 62% of voluntary policies received contributions at some point during the year 2017. The vast majority of voluntary plans with accruing contributions (around 70% in 2017) receive contributions only from employers. Around 18% accrue contributions from both employer and employee. Only about 10% of supplementary retirement savings plans accruing contributions, or 6% of all policies, receive contributions only from individuals. This category includes voluntary occupational schemes where employers no longer contribute (about 2% of policies in 2017), for instance plans to which workers continue to contribute after having left the employer which set up the plan.

Men are more likely to have a voluntary supplementary pension savings account than women. Overall, 56.7% of voluntary supplementary retirement savings contracts which had a positive balance at the end of 2017 were held by men, and 43.3% by women, with only two pension management companies out of the eight surveyed having (slightly) over 50% female members. Similar results were found when analysing contracts which received contributions in 2017, indicating that men and women were as likely to contribute to their supplementary retirement plan during a given year.

Employer contributions to voluntary occupational schemes during maternity and parental leave are voluntary. Collective agreements and rules of pension contracts may include the continuation of employer contribution to voluntary occupational retirement schemes during maternity and parental leave. However there is no obligation for employers to pay contributions to the retirement accounts of employees during maternity and parental leave.

Stopped contributions to retirement savings plans during periods of maternity and parental leave are one of the sources of the gender gap in private pensions in many OECD countries (OECD, 2021[2]). This is especially true in countries where occupational arrangements are voluntary or based on automatic enrolment, such as Austria, Lithuania, New Zealand, and the United States. Belgium and Denmark have a similar setting to that of Slovenia, and plan rules dictate whether contributions continue or are halted during maternity and parental leave. Other countries with voluntary or quasi-mandatory occupational schemes such as Canada, Ireland, Japan, Korea, Luxembourg, the Netherlands, Poland, the Slovak Republic, Sweden, Switzerland and the United Kingdom mandate employer contributions to continue during periods of maternity and parental leave.

Coverage and contribution rules specific to voluntary occupational schemes

Once a voluntary occupational pension plan has been set up, all employees are included in the plan under the same conditions, with the ability to opt-out. A minimum tenure of employment of up to one year may be required by employers to enrol employees into the company pension plan.

Employer contributions to voluntary occupational plans are not determined by law, but are subject to collective bargaining between employers and employees. However, the Ministry of Labour, Family, Social Affairs and Equal Opportunities sets a minimum annual employer contribution amount, which is revised annually. This minimum contribution amount is set by law (currently at EUR 316.20) and is indexed by average salary growth.

Contributions to voluntary retirement savings schemes

Accounts to which both employer and employee contribute regularly have the highest average balance. The average balance of assets on voluntary retirement savings accounts was EUR 4 758 in 2017 and was higher for accounts which received a contribution during the year 2017. Dormant accounts in 2017 had an average balance of approximately EUR 2 900 for both occupational and personal plans. Accounts which received contributions from employers only in 2017 had an average balance of EUR 5 255 (10% higher than average), those receiving contributions from members only had an average balance of EUR 7 115 (50% higher), and those receiving contributions both from members and employers had an average balance of EUR 8 438 (77% higher) (Table 5.4).

Women who received contributions in 2017 had lower contributions and lower balances than men, particularly when receiving contributions from their employer only (Table 5.4). Account balances at the end of 2017 were 17% lower for women (EUR 4 731) than men (EUR 5 668), when contributions were made by employers only. The gender difference in account balances was 9% and 5% respectively when contributions were made by members only, and by members and their employers in 2017.

The gender pay gap has consequences on employer contributions received by women in voluntary pension arrangements. Outside of the public sector, employer contributions are generally set at a percentage of wages and may therefore be affected by salary differences between men and women. The amount of employer contributions was 14% lower for women than for men, both when contributions were paid only by employers (EUR 666 for women and EUR 776 for men) and when contributions were paid by employers and employees (EUR 803 for women and EUR 933 for men). This gender gap in employer contributions is higher than the gender wage gap, which according to data from Eurostat, was 8.4% in 2017.10

Gender differences also appear in the distribution of employer contributions by age cohorts. While both genders appear to receive comparable employer contributions as a percentage of their annual salary in middle ages, women younger than 26 and older than 58 receive lower contributions as a percentage of their annual salary than men of the same age groups, according to IER data. This suggests that women of younger and older age groups may be more represented than men in occupations or industries where employers pay lower contributions to voluntary pension plans.

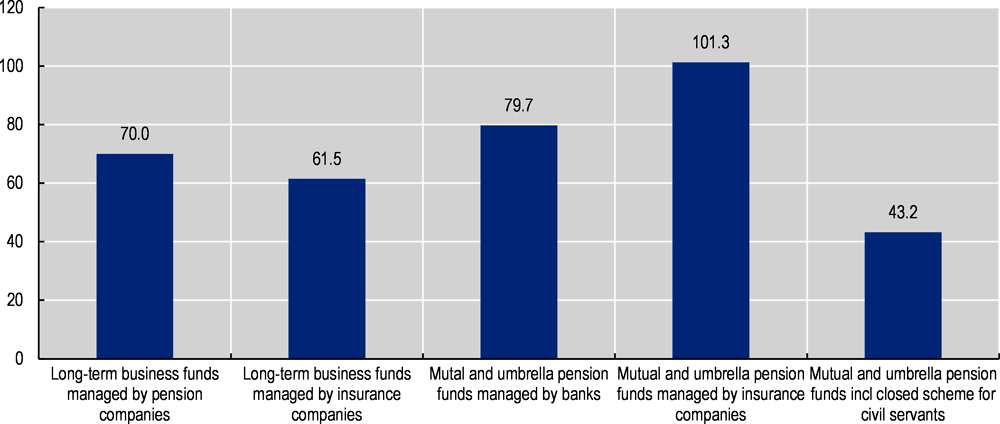

Data from pension fund managers managing voluntary occupational and personal retirement savings plans indicate that for accounts with contributions paid in 2020, the average monthly contribution received was higher for mutual and umbrella pension funds than for long-term business funds. Mutual and umbrella funds managed by insurance companies had the highest average monthly contribution (EUR 101.3, or 4.7% of the monthly average wage in Slovenia), followed by those managed by a bank (EUR 79.7, or 3.7% of the monthly average wage). Long-term business funds received slightly lower average monthly contributions: EUR 70 (or 3.25% of the monthly average wage) for those managed by pension companies, and EUR 61.5 (i.e. 2.8% of the monthly average wage) for those managed by insurance companies (Figure 5.6). Given the weight of the scheme for civil servants, the average monthly contribution to mutual and umbrella pension funds managed by insurance companies falls to EUR 43.2 (i.e. 2% of the monthly average wage) in 2020 if contributions to this scheme are taken into account.

Table 5.5 presents a summary of coverage and contributions for the mandatory scheme for workers in arduous and hazardous occupations, for the mandatory scheme for civil servants, and for voluntary occupational and personal plans.

Note: Average computed using data for accounts which received a contribution during the year 2020.

Source: Ministry of Labour, Family, Social Affairs and Equal Opportunities https://www.gov.si/teme/prostovoljno-dodatno-pokojninsko-zavarovanje/.

Savings in supplementary retirement plans in Slovenia are taxed according to the exempt, exempt, taxed (EET) principle, where contributions and returns on investment are tax exempt under certain conditions, and benefits are taxed. This tax treatment of retirement savings is the most common across OECD countries, and is applied in 18 of the 37 member jurisdictions (OECD, 2018[3]).

5.4.1. Contributions

Employers and employees have a joint tax relief up to a ceiling. This relief is valid if the pension plan is approved by the Ministry of Labour, Family, Social Affairs and Equal Opportunities and entered into a special register kept by the competent tax authority.

Employer contributions are a deductible expense which is not subject to corporate income tax, and are not included in an employee’s taxable income up to 5.844% of the employee’s gross wage.11 Since 2013, this cap cannot exceed EUR 2 819.09 per year.12 Before the pension reform of 2013, employer contributions could only be tax deductible if at least 50% of employees participated in the occupational pension plan of a given employer.

Individual contributions to occupational and personal pension plans attracting a tax deduction are capped at the unused portion of employer contributions attracting tax relief. If both the employer and the employee pay contributions, and the total amount of contributions exceeds the maximum contribution entitled to tax relief, the employee may only receive tax relief on the difference between the contribution paid by the employer and the ceiling. Contributions above the set ceiling cannot be deducted from taxable income. However, there is an exemption that applies to civil servants, for whom contributions to supplementary pension insurance are uncapped.

Employer contributions above 5.844% of the employee’s gross wage or above EUR 2 819.09 are subject to social contributions. Contributions within the ceiling are not subject to social contributions.

Employee contributions are made from income that has already been subject to social contributions.

There are no mechanisms such as subsidies or matching contributions to encourage participation and increase the contribution of individuals who pay low or no income tax. The OECD Roadmap for the Good Design of Defined Contribution Pension Plans (OECD, 2012[4]) recommends including financial subsidies or matching contributions for those individuals, in particular when participation to retirement savings arrangements is voluntary (OECD, 2018[3]).

According to 2018 data from the Ministry of Finance, 57 445 individual taxpayers claimed tax relief for contribution to their voluntary supplementary pension plan, of which 269 (i.e. less than 1%) claimed relief up to the ceiling of EUR 2 819.09.

5.4.2. Investment returns

Returns on investment in supplementary retirement savings plans are tax exempt.

5.4.3. Benefits

Supplementary pensions in payment are subject to taxation, but not to social contributions.

Pension savings withdrawn as annuities are subject to ordinary income tax rules, although only 50% of annuity payments are included in the income for tax calculation purposes.

Pension savings withdrawn as lump sums are subject to the Personal Income Tax Act. A 25% withholding tax, or advance payment of personal income tax is charged upon withdrawal. Withdrawn amounts are then included in the annual taxable base for the assessment of personal income tax, which is paid according to progressive tax rates. The only exception to this rule is for redemption due to death where a beneficiary was stipulated in the policy, in which case the person inheriting the amount is subject to the Inheritance and Gifts Tax Act, and may therefore be exempt from tax on the inherited amount.

A double taxation would occur if income tax were to be paid both at the time that contributions are made and withdrawn. To avoid a double taxation of amounts saved in excess of the annual tax deductible contribution cap of EUR 2 819.09, from 1st January 2020 taxpayers demanding a lump sum withdrawal of their retirement savings may request that the portion corresponding to contributions in excess of the annual cap is excluded from the annual taxable base upon withdrawal.13

In addition, voluntary pension assets withdrawn during the first ten years of a pension contract attract an 8.5% Insurance Premium Tax, charged on the basis of the contributed amount, even if they are drawn down as an annuity.14 This provision ensures that voluntary supplementary pension assets withdrawn early are treated similarly to other insurance savings instruments. The insurance premium tax does not apply to withdrawals from voluntary retirement savings plans caused by the death of the contributing member in the first ten years of the plan. After ten years, amounts saved in voluntary personal pension plans can be withdrawn without a penalty.

The Insurance Premium Tax does not apply to withdrawals of assets stemming from mandatory contributions, i.e. to employer contributions made to the plan for workers in hazardous and arduous occupations or to the supplementary scheme for civil servants. Assets from these plans may be withdrawn in cash during the first ten years of a contract if the plan was joined less than ten years before the retirement date of the member, and assets accumulated in the plan are eligible for a lump sum withdrawal (i.e. below a threshold of EUR 5 120 in total).

5.4.4. Tax advantage

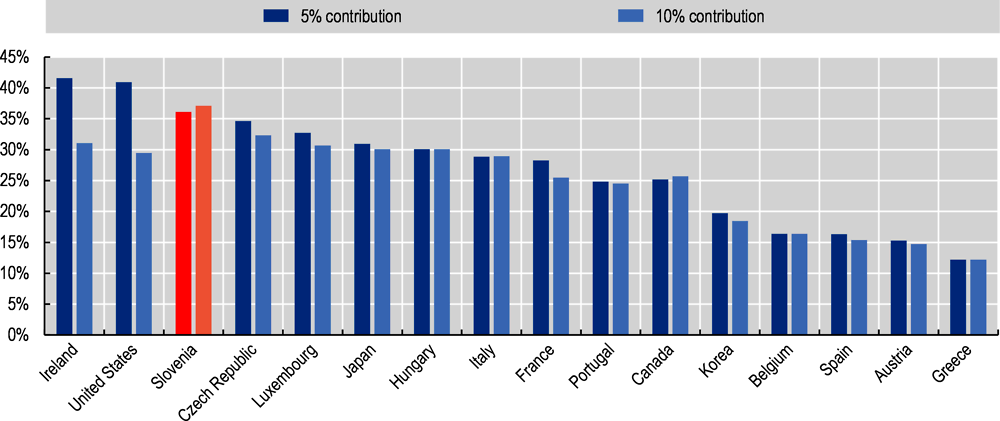

The tax advantage in Slovenia ranks among the highest of OECD countries with voluntary retirement savings arrangements only, at 36% and 37% for contribution levels of 5% and 10% respectively. The tax advantage can be calculated as the amount of taxes saved over their lifetime by a hypothetical average earner by contributing to a retirement savings plan rather than to a traditional savings account (OECD, 2018[3]). Assuming members contribute 5% or 10% of their wages to either a retirement savings plan, or to a traditional savings account, Figure 5.7 illustrates the tax advantage, i.e. the present value of taxes saved as a percentage of the present value of contributions, in OECD countries with voluntary retirement savings arrangements only, in 2018. Values computed range from 12% in Greece for both contribution levels to 42% in Ireland for a 5% contribution.

In 15 of the 16 OECD countries considered with voluntary retirement savings plans only (i.e. all except for Hungary), the value of the overall tax advantage varies with the income level of the individual contributing (Figure 5.8). This is due to a combination of different tax regimes, plan specific limits on the amount of contributions attracting tax relief and the characteristics of the personal income tax system in different countries.

Note: Calculations based on the 2018 tax treatment of contributions in countries with voluntary private pension systems only, assuming a contribution rate of 5% or 10%.

Source: OECD (2018[3]), Financial Incentives and Retirement Savings, https://dx.doi.org/10.1787/9789264306929-en.

Note: Calculations based on the 2018 tax treatment of contributions in countries with voluntary private pension systems only, assuming a 5% contribution rate.

Source: OECD (2018[3]), Financial Incentives and Retirement Savings, https://dx.doi.org/10.1787/9789264306929-en.

Average earners receive the highest tax advantage in Slovenia. High-income earners (earning four times average earnings) benefit from a higher overall tax advantage than average earners and low-income earners (earning 60% of average earnings) in seven of the 16 countries analysed, including Japan, Italy, Korea and Canada. In the United States and Luxembourg, high-income and average earners receive a similar tax advantage, which is higher than that received by low-income earners. On the other side of the spectrum, low-income earners receive a higher tax advantage in Portugal and Belgium. Slovenia is part of the group of four countries, also including Ireland, the Czech Republic and France, where average earners receive the highest tax advantage.

Low-income earners in Slovenia receive a lower tax advantage than average earners due to the progressive nature of the tax advantage, which is calculated as a percentage of contributions, i.e. of wages in the analysis. High-income earners do not benefit from the tax relief on contributions above the ceiling of EUR 2 819.09 and pay higher taxes upon withdrawal, hence they receive an overall lower tax advantage than average earners.

5.5.1. Assets under management

Total assets managed in supplementary pension arrangements in 2019 amount to EUR 3.51 billion, or 7.3% of Slovenian GDP. Figure 5.9 shows the evolution of assets since the introduction of the supplementary pension system in 2003, when assets managed totalled EUR 272 million (1.1% of GDP).

Source: OECD Global Pension Statistics.

The weight of assets in supplementary pension arrangements in Slovenia is still low in international comparison, both when looking at all OECD jurisdictions and when focusing only on those with voluntary retirement savings arrangements. On average across all OECD countries, assets in retirement savings arrangements represented 91.5% of GDP in 2019, with wide disparities across countries, from around 200% in countries with mandatory schemes such as Denmark or the Netherlands, down to under 3% in Turkey, Luxembourg and Greece (Figure 5.10, Panel A). When comparing Slovenia (7.3%) only to countries with voluntary systems, the amount of assets in the retirement system is still relatively low, as only Austria, Hungary, Turkey and Luxembourg have assets representing less than 7% of national GDP for 2019, and some countries with mature supplementary pension markets such as Canada and the United States have over 150% of GDP in retirement savings assets (Figure 5.10, Panel B).

Note: The charts show the evolution of assets in retirement savings plans between 2009 and 2019, except for Finland (2011-19), Lithuania (2010-19) and Switzerland (2013-19).

Source: OECD Global Pension Statistics.

Assets in mandatory schemes increased by 86% between 2011 and 2019, from EUR 900 million to just under EUR 1.7 billion. The relative weight of assets in the scheme for civil servants as a proportion of assets in mandatory schemes decreased from 58% (EUR 520 million) in 2011 to 53% (EUR 883 million) in 2019, in favour of the scheme for workers in arduous and hazardous occupations which increased from 42% (EUR 381 million) in 2011 to 47% (EUR 788 million) in 2019 (Figure 5.11).

Source: Modra and Kapitalska Druzba annual reports from 2011 to 2019.

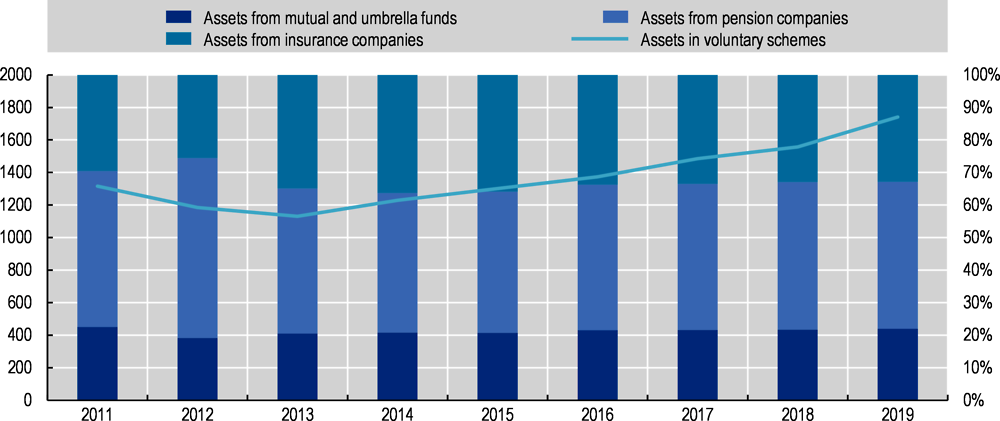

Assets in voluntary retirement savings arrangements increased by about 40% between 2010 and 2020, from EUR 1.3 billion to EUR 1.9 billion, after having dipped in 2012 and 2013 (Figure 5.12). The proportion of assets in voluntary schemes managed by each type of plan has remained relatively stable over time. Over the past few years, about half of assets have been managed by insurance companies, about 45% by pension companies, less than 5% by banks. In 2020, these percentages corresponded to around EUR 1 billion with insurance companies, around EUR 850 million with pension companies, and around EUR 5 million with banks.

Source: Ministry of Labour, Family, Social Affairs and Equal Opportunities and OECD calculations.

5.5.2. Investment strategies

Article 271 of the Second Pension and Disability Insurance Act stipulates that the investment strategy of pension funds must be done according to the prudent person principle, for the long-term benefit of members, and taking into account liquidity and security criteria. This is in line with the OECD Core Principles of Private Pension Regulation (OECD, 2016[5]) on investment and risk management. Diversification across instruments and issuers is required, and the law specifies that sustainability aspects and environmental, social and governance (ESG) factors may be taken into account as part of the analysis when selecting investments.

Supplementary pension providers in Slovenia must offer a life-cycle strategy or a guaranteed return on net contributions to members. The mandatory fund for workers in arduous and hazardous occupations only offers a minimum guaranteed return, while all other pension arrangements, including the scheme for civil servants, offer the life-cycle option to their members, with three sub-funds with different risk profiles designed for different age groups.

Mandatory plan for workers in arduous and hazardous occupations

Assets managed by Kapitalska Druzba in the plan for workers in arduous and hazardous occupations are subject to an annual minimum return. That return is conceptually similar to the minimum return in the guaranteed fund or sub-fund of other pension providers offering a life-cycle strategy, but that guaranteed return can be less than the minimum guarantee return set by the law. The objective of the fund is therefore to ensure at least the guaranteed minimum return, with minimal risk and taking into account liquidity criteria.

The minimum return on net contributions is calculated annually by the Ministry of Finance and corresponds to 40% of the average return on Slovenian Government bonds of a duration greater than one year.15

Kapitalska Druzba is responsible for delivering at least the guaranteed investment return on assets saved in the scheme. The difference between the actual net asset value and the guaranteed value of the fund’s assets is computed monthly, and the pension fund manager is required to establish provisions or liabilities corresponding to the unattained guaranteed value. While the guaranteed return ensures that assets saved for retirement do not fall below a set floor, it comes at a high cost (OECD, 2012[6]). Guarantees reduce the expected value of benefits from defined contribution plans relative to a situation where there are no guarantees, as assets are not invested in higher risk assets, which are expected to provide higher returns over the long run.

The plan for workers in arduous and hazardous occupations is also subject to solidarity reserves, which are meant to be allocated to a specific contract upon withdrawal to ensure the monthly stream of income reaches the minimum pension amount.

Solidarity reserves are computed based on the guaranteed rate of return. For the minimum return to assets, Kapitalska Druzba applies a 60% factor instead of the mandatory 40% of the return on Slovenian Government bonds of a duration greater than one year, with the amount earned from the part between 40% and 60% being allocated to solidarity reserves. Any amount in excess of the return from the 60% factor is credited to members’ personal accounts.

Members retiring from the plan in compliance with early retirement rules receive a monthly stream of income which is computed based on their accumulated assets, but also subject to the minimum public pension to which a member would be entitled if they worked for 40 years. Solidarity reserves ensure that all members who qualify for early retirement receive this minimum pension, including those whose assets accumulated are insufficient at the time of early retirement.

The matching of the duration of assets with that of liabilities is encouraged. Upon early retirement, Kapitalska Druzba is also in charge of making monthly payments to members until they reach the statutory retirement age. Its investment policy continues to require the prudent management of its liabilities towards annuitants while monthly payments are being made.

Voluntary plans and closed scheme for civil servants

The life-cycle option was introduced by the 2012 Pension and Disability Insurance Act (ZPIZ-2) and requires offering three funds with different investment strategies and risk profiles, including one guaranteed fund. This is consistent with the recommendations from the OECD Roadmap for the Good Design of Defined Contribution Pension Plans (OECD, 2012[4]) on default investment strategies to protect people close to retirement against extreme negative outcomes. The first transfers from guaranteed to non-guaranteed funds occurred in 2016. Hence, before 2016, all pension funds could only offer a guaranteed return on contributions.

All voluntary plans, as well as the closed scheme for civil servants, offer a life-cycle investment strategy to their members, with different risk profiles and corresponding asset allocations. The three risk profiles are dynamic or high shares for younger savers, prudent, balanced or mixed for savers approaching retirement, and guaranteed for those close to retirement.

Different supplementary pension providers have designed different target age groups and consequently different rules for their risk profiles based on asset allocation, as shown in Table 5.6. Providers must disclose the authorised proportion of high-risk assets in each risk profile, together with a corresponding target age group. High-risk assets include equities, real estate, derivatives, private equity and other alternatives, and non-investment grade debt securities.

The latest available data corresponding to 2017 from the Institute for Economic Research shows that 85% of assets were managed in guaranteed funds or sub-funds. The guaranteed minimum return on net contributions is calculated annually by the Ministry of Finance and corresponds to 40% of the return on Slovenian Government bonds of a duration greater than 1 year.

Members may request to switch investment strategies once a year, but are forbidden from saving into a strategy meant for a younger age group. This may not be optimal for all savers, depending on their overall pension arrangements and savings. The OECD Roadmap for the Good Design of Defined Contribution Pension Plans (OECD, 2012[4]) emphasises the importance of the coherence between the different components of people’s retirement income, and recommends allowing people to select the investment strategy best suited for them according to their risk profile and investment horizon. For example, individuals whose contributions to the public pension scheme already ensure them a relatively high retirement income may not need as much security from their supplementary pension arrangement, and could therefore enjoy a higher expected retirement income by allocating their retirement assets to a higher risk and higher return investment strategy than the one meant for their age group.

The process to choose an investment strategy for retirement savings depends on the provider. Providers should assign new members to the risk profile corresponding to their age group by default.16 Members who started contributing to their retirement savings plan before the life-cycle option was introduced saved in the guaranteed investment strategy. Upon the introduction of the life-cycle option, some providers, such as Prva, chose to assign new contributions to the investment strategy corresponding to the member’s age group by default.17 Other providers chose to maintain existing members in their previous default investment strategy (i.e. the guaranteed fund). Members with previously accumulated assets could also request to have these assets transferred to the risk profile corresponding to their age group, or could choose to keep them in the guaranteed option.

Regulation requires that changes between investment strategies corresponding to a change of the member’s age group are done at once rather than gradually. When members reach an age threshold to transition from one risk profile to another, their accumulated assets, and new contributions must be transferred to the investment strategy corresponding to their new (older) age group within three years. This one-off transfer puts a significant weight on the market conditions prevailing at the time of the transfer, and therefore on the timing of the fund manager’s transfer decision. If the transfer occurs at a time when market conditions deteriorate, selling higher-risk/growth assets may incur a loss for the member.

Pension annuity providers

Upon retirement, members of the supplementary pension system may purchase a pension annuity from the pension or insurance company of their choice. Pension annuity providers must set up a long-term business fund for the payment of pension annuities, and their investments are subject to rules defined in legislation.18 Pension annuity providers must comply with insurance regulatory rules related to technical provisions and capital requirements based on their investments and liabilities.

5.5.3. Asset allocation

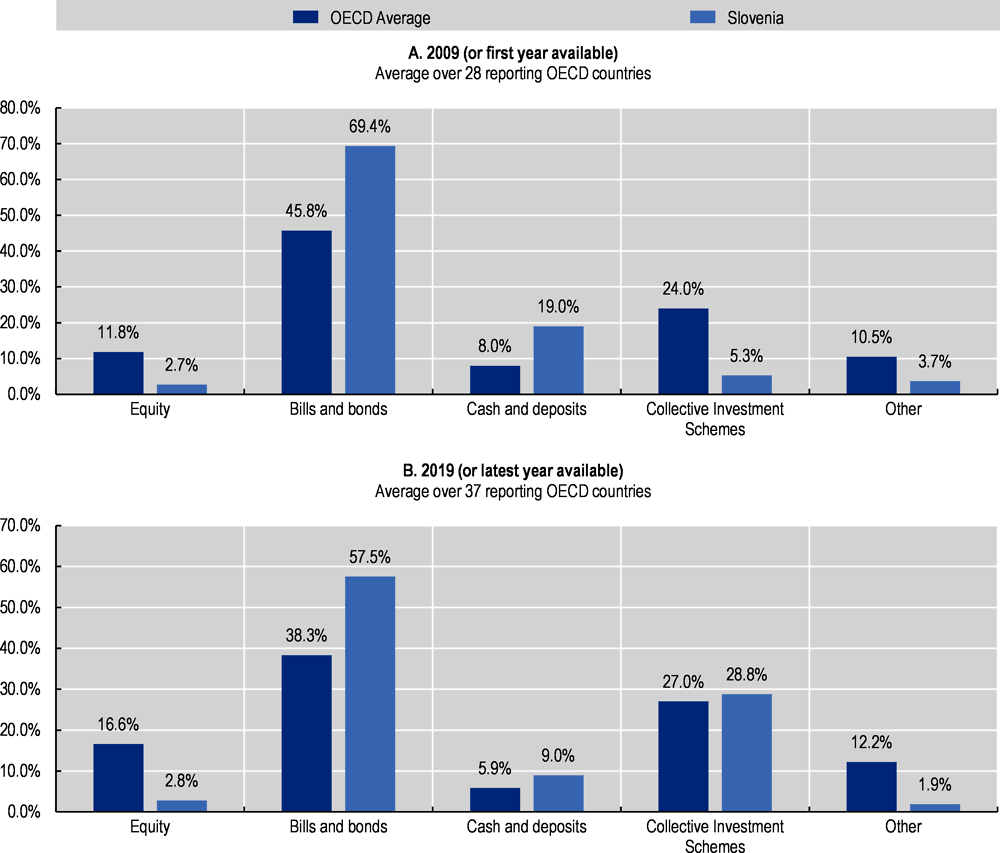

Overall in 2019, the asset allocation of retirement savings arrangements in Slovenia has a larger portion of fixed income assets (bills and bonds) and cash than the average OECD jurisdiction, a similar portion of units of collective investment schemes and a smaller allocation to equities and alternatives (Figure 5.13). Since 2009, the average allocation of Slovenian schemes to bills and bonds and to cash has decreased (from 69.4% and 19% to 57.5% and 9% respectively), while that to units of collective investment schemes has significantly increased (from 5.3% to 28.8%). No change was made to direct investments in equities (2.7% vs 2.8%) and a slight decrease was observed in alternatives (3.7% vs 1.9%) over the decade in Slovenia, contrary to a significant increase in average OECD allocations to equities (from 11.8% to 16.6%), and a slight increase in average allocations to alternatives and units of collective investment schemes (from 10.5% to 12.2% for alternatives).

The predominance of bills and bonds in the Slovenian asset allocation can be explained by the importance of guaranteed funds. Before 2016, guaranteed funds were the only investment option offered to individuals saving for retirement, and even though the life-cycle investment strategy was introduced in 2016, around 85% of assets remained invested in guaranteed funds in 2017, according to data from the Institute of Economic Research.

Investment in collective investment schemes is significant in Slovenia. In the absence of a look-through, it is impossible to say how much of this category of investment corresponds to units in equity or fixed income funds, although it is likely that these collective schemes also include a substantial portion of fixed income investments.

The share of assets in retirement savings plans invested abroad has increased over the decade in Slovenia, from 31.6% in 2009 to 65.2% in 2019 (OECD, 2020[7]).19 This corresponds mostly to assets denominated in EUR and issued in other countries of the euro area, as only 5.4% of investments in Slovenian retirement plans are issued in foreign currencies in 2019, despite the absence of quantitative restrictions on foreign-denominated assets.

Several quantitative investment limits are defined in legislation, and apply to pension providers in Slovenia, mostly regarding investments into alternative assets.20 Direct investments into real estate may not represent more than 20% of assets in any retirement plan, and private investment in venture capital funds may not represent more than 1% of assets. Pension providers may not invest in derivatives, except for hedging purposes. Concentration rules also apply to investments by retirement savings plan providers. While risk management principles call for a diversification of assets, quantitative investment limits may not always be the most appropriate solution to reduce risk according to international experience. The OECD carries out an annual survey of investment regulations of pension funds (OECD, 2019[8]). Prudential risk-based management principles and flexibility around thresholds may be more suitable to leave room for pension fund managers’ analysis and avoid forcing pension funds to sell assets as soon as they reach a set threshold.

Note: The average allocation for 2009 or first year available is an average over 28 reporting OECD countries. The average allocation for 2019 or latest year available is an average over 37 reporting OECD countries.

Source: OECD Global Pension Statistics.

Mandatory scheme for workers in arduous and hazardous occupations

The mandatory scheme for workers in arduous and hazardous occupations offers a single investment strategy, with a guaranteed minimum return on net contributions.

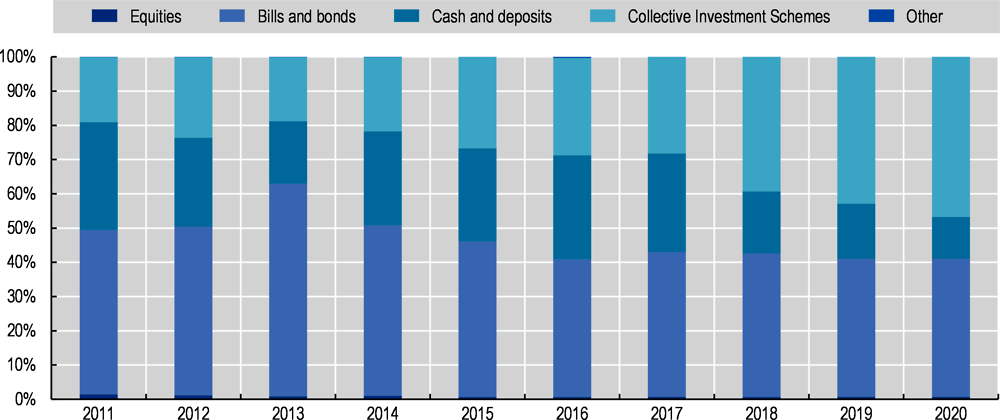

Due to the guaranteed nature of the investment return, the long-term target of the fund is to be invested mainly in low risk debt securities. The investment policy details the long-term target asset allocation as follows:

Similar to the average trend in Slovenia (Figure 5.13), the asset allocation of the fund for workers in arduous and hazardous occupations has seen a decrease in the share of cash and deposits (from 31.4% in 2011 to 12.2% in 2020), and of direct investments in bills and bonds (from 48.1% in 2011 to 40.3% in 2020) in favour of units of collective investment schemes (Figure 5.14). This decrease in assets held in cash is unsurprising given the low – and even negative – rates paid on deposits in EUR over the period. Collective investment schemes may comprise fixed income as well as equity investments, and company information specifies that debt investments account for the highest proportion of assets.21 However, more detailed information would be needed to assess whether the fund invests in line with its long-term target asset allocation.

Source: Kapitalska Druzba annual reports from 2011 to 2020.

Other pension funds in Slovenia, including the mandatory scheme for civil servants, offer different sub-funds according to the life-cycle strategy and therefore have different asset allocations for each sub-fund, depending on its target risk and return profile.

5.5.4. Investment performance

Investment returns in Slovenian retirement savings arrangements have been mostly stable between 2007 and 2019 in nominal and real terms (Figure 5.15). Despite the high proportion of assets in guaranteed funds and the falling yields in euro denominated bonds (for instance the yield on EUR AAA 10-year government bonds declined from 3.9% in January 2007 to -0.2% in December 2019), real rates of return have only been slightly negative for two years (2011 and 2018) over the period.22

Note: Yearly returns calculated as the ratio between the investment income at the end of the year, net of investment expenses, and the average.

level of assets during the year.

Source: OECD Global Pension Statistics and OECD (2020[7]), “Pension Markets in Focus”, https://www.oecd.org/pensions/private-pensions/pensionmarketsinfocus.htm.

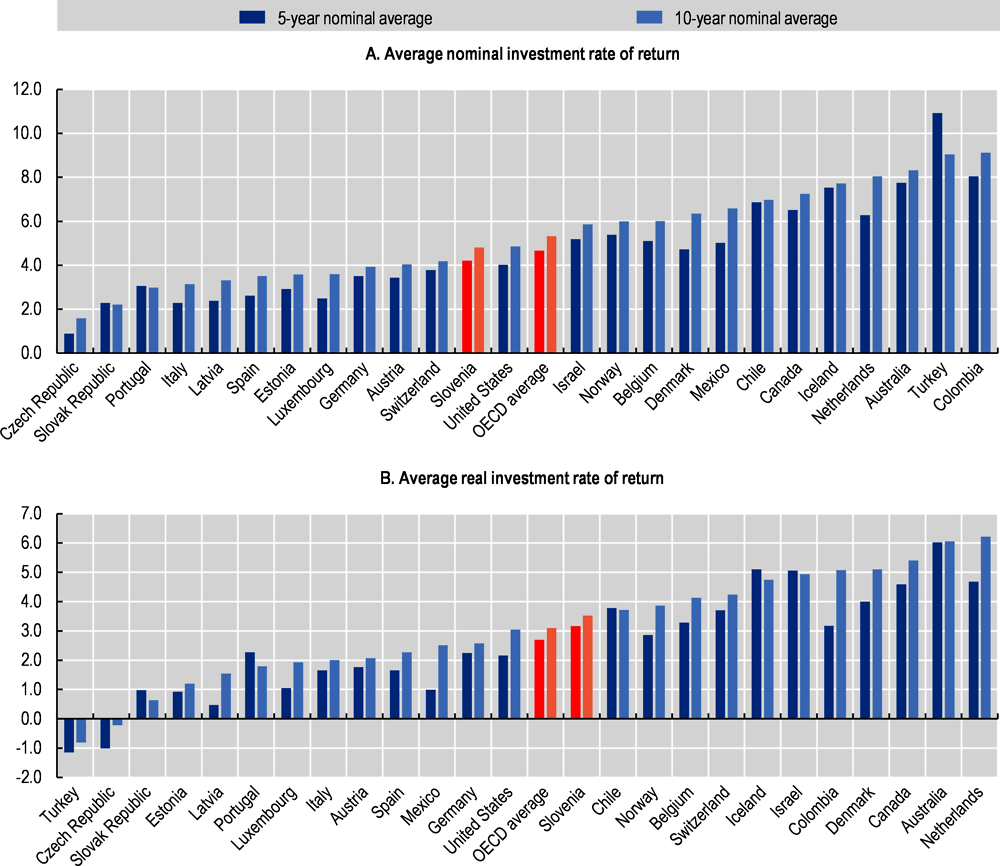

In international comparison, the investment performance of retirement savings arrangements in Slovenia has been close to the OECD average both in nominal and real terms over the past five and ten years (Figure 5.16). The 5-year and 10-year nominal rates of return of Slovenian pension plans were respectively 4.2% and 4.8% (Figure 5.16, Panel A), compared to 4.7% and 5.3% for the OECD average. The real rate of return over five and ten years was 3.2% and 3.5% respectively (Figure 5.16, Panel B), compared to 2.7% and 3.1% for the OECD average. Compared to other euro area countries, Slovenian plans have performed rather well as only Belgium and the Netherlands have registered higher average performances (both nominal and real) on average over the two periods considered. This is especially noticeable given the low allocation to high risk and high return assets in Slovenian retirement savings arrangements overall, compared to other countries (for instance, allocation to equities in 2019 was 47.8% in Belgium and 30.7% in the Netherlands on average, compared to 2.8% in Slovenia).

Note: 5-year averages refers to the returns from December 2014 to December 2019, and 10-year averages refer to returns from December 2009 to December 2019.

Source: OECD Global Pension Statistics.

5.6.1. Risk management

Custody of pension assets must be delegated to an external custodian. In 2004, a requirement for all pension funds to use a custodian was introduced in order to increase supervision and public trust in the private pension sector. The custodian must be authorised to perform custody services under Directive 2011/61 / EU of the European Parliament and of the Council of 8 June 2011, or be a stockbroking company with a registered office in Slovenia, and licenced by the Securities and Market Agency to provide custody services. The custodian is in charge of:

Legislation requires all pension fund managers to prepare a comprehensive risk management policy, which is subject to review by the pension entity’s supervisor.23 All pension fund managers must report to their supervisor on the limits, methods and measures of risk at least once a year.

These provisions are in line with the OECD Core Principles of Private Pension Regulation (OECD, 2016[5]) relating to risk-based controls, custody and risk management.

5.6.2. Funding requirements at the management entity level

Solvency and capital requirements depend on the structure of the pension fund and its corresponding regulations, all of which comply with rules and directives set out by the European Union, and are consistent with the OECD Core Principles of Private Pension Regulation (OECD, 2016[5]) on the conditions for effective regulation and establishment of pension plans, pension funds and pension entities.

Pension companies are subject to the Second Pension and Disability Insurance Act and Directive (EU) 2016/2341 of the European Parliament and of the Council of 14 December 2016 on the activities and supervision of institutions for occupational retirement provision (IORPs);

Insurance companies are subject to the Insurance Act and Directive 2009/138/EC of the European Parliament and of the Council of 25 November 2009 on the taking-up and pursuit of the business of Insurance and Reinsurance (Solvency II);

Banks are subject to the Banking Act and Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012.

Each pension fund manager is obliged to report quarterly to its supervisor (i.e. the Securities Market Agency or the Insurance Supervision Agency) on the amount of the management company’s capital.

In accordance with the provisions ZPIZ-2, the assets of a pension fund in the event of bankruptcy proceedings against a pension fund manager are considered to be members’ assets and are not available to repay other creditors.

In addition, the pension fund manager and custodian shall ensure the separation of the pension fund’s assets from:

In the event that a bankruptcy or liquidation proceeding has been instituted against the manager, the management of the mutual pension fund or the umbrella pension fund may be transferred to another manager. For the scheme for workers in arduous and hazardous occupations, the Republic of Slovenia is the ultimate guarantor to ensure that the guaranteed return continues to be paid should there be a transfer to another management company from Kapitalska Druzba.24

5.6.3. Funding requirements at the fund level

Pension funds or sub-funds which offer a guaranteed return on net contributions are subject to rules to ensure this guaranteed return is reached on an annual basis. This is in line with the OECD Core Principles of Private Pension Regulation (OECD, 2016[5]), which recommend that pension funds should be subject to minimum funding rules to ensure adequate funding of pension liabilities. In particular, the financial risk of offering a guaranteed rate of return should be borne by the pension entity, which should set aside capital to meet the promise.

For all pension funds, Article 313 of ZPIZ-2 stipulates that provisions must be set aside to cover any shortfall in investment return compared to the guaranteed return. Provisions may not exceed 20% of the capital of the pension fund manager, and a cash transfer for the value exceeding 20% of capital must be made within 15 working days of the breach between the provision account and the fund asset account. In case provisions are insufficient to compensate for the deficit, the pension fund manager’s capital must be used to ensure the guaranteed asset value can be paid. The structure of the capital and that of provisions must be reported monthly by pension fund managers to their supervisor.

The mutual fund managed by Kapitalska Druzba for workers in arduous and hazardous occupations also has solidarity reserves, which were introduced in 2016 by ZPIZ-2, to ensure that workers eligible to retire early could receive the minimum pension amount even if assets in their account were insufficient.25 At the end of 2019, the fund had EUR 4.82 million of solidarity reserves, of which EUR 4.81 million were unallocated.26

Members reaching the age of 58 in a given year, and members requesting this information, must be provided with information on their pay-out options and future rights arising from supplementary pension saving.27

Across retirement savings arrangements, annuitisation is either compulsory or encouraged through tax incentives. The OECD Roadmap for the Good Design of Defined Contribution Pension Plans (OECD, 2012[4]) recommends protecting individuals’ overall retirement income against longevity risk. Annuitisation of assets in defined contribution retirement savings plans may be adequate for people whose income from the public pay-as-you-go system does not protect them sufficiently from longevity risk. However, it may not be optimal for individuals whose other sources of retirement income already protect them from longevity risk.

5.7.1. Occupational schemes

Annuities from the occupational supplementary pension system represent a small portion of retirement income. Based on the latest available data corresponding to 2017, the Institute for Economic Research estimates that annuities from occupational retirement savings schemes will represent between 9% and 16% of future retirees’ public pension income. For members of occupational schemes currently aged between 25 and 35, and assuming their contribution pattern remains unchanged until retirement, annuities are expected to represent 9% and 10% of public pension income for women and men respectively when only employers contribute to the plan, and 14% and 16% for women and men respectively when both employer and employee contribute to the plan.

Scheme for workers in arduous and hazardous occupations

Specific rules apply to the scheme for workers in arduous and hazardous occupations.28 Periods of contribution to the scheme are augmented by 25% for the purpose of assessing the eligibility to early retirement. Members are deemed entitled to an occupational pension from the scheme for workers in arduous and hazardous occupations if they have sufficient assets in their account, and either 42.5 years of contribution, or 40 years of contribution and have reached a minimum age set between 52 and 60, depending on the categorisation of their occupation. Members fulfilling the criteria but with insufficient assets may be eligible to an occupational pension from the scheme if they have been contributing to it for at least 17 years, in which case solidarity reserves will be used to complement members’ assets. An occupational pension can be received from the scheme for workers in arduous and hazardous occupations during a period which cannot exceed the 25% added contribution period nor extend beyond statutory retirement age.

Members choosing to retire early and complying with eligibility criteria must generally use their accumulated assets to purchase a monthly stream of income unless they fulfil certain conditions for a lump sum withdrawal. Lump sums may be requested by members eligible to retire early and who have accumulated less than EUR 5 120 in assets from their occupational scheme. Members of the Slovenian armed forces may also request a lump sum withdrawal if they have served for at least 10 years and their contract is not extended, or if their contract is terminated due to age restrictions. Members of the border police who have not concluded a new contract in an occupation covered by the scheme for workers in arduous and hazardous occupations in the six months after their contract is terminated may also request a lump sum. A lump sum payment may also be requested by the heirs of a member who dies before having retired from their occupation.

All other members choosing to retire early under the scheme must convert their assets into a monthly stream of income, which is managed and paid by Kapitalska Druzba. Members retiring under the scheme for workers in arduous and hazardous occupations receive a monthly stream of income based on their accumulated assets, and subject to their minimum and maximum old-age public pension for 40 years of contribution. Members with sufficient accumulated assets may choose the amount of the monthly income they receive between the minimum and maximum and therefore manage the timing of their pension payments if they wish so by deferring the payment of a portion of their assets to a later date. Solidarity reserves are used to ensure the minimum monthly income payment is paid during the period up to statutory retirement age for members with insufficient balances.

The calculation method to assess eligibility to the occupational scheme differs from that of the public pension scheme. Periods of contribution to the scheme for workers in arduous and hazardous occupations are increased by a factor of 1.25 when assessing the conditions to acquire the right to early retirement under the occupational scheme. However, the added period of pensionable service (corresponding to the increase by 1.25 times) is not taken into account when assessing the conditions for retirement under the public pension system. Members retiring early under the occupational scheme may therefore find that they do not have sufficient contribution periods under the public pension scheme to receive their full public pension after having received the early retirement payment under the occupational pension scheme. These members can however, voluntarily contribute to the public pension scheme, in order to ensure they can receive a full pension under the public scheme at the statutory retirement age. The cost for such additional purchase is calculated on 20% of the average annual salary in Slovenia. Alternatively, while individuals are receiving income from the occupational scheme, they can also pay voluntary contributions to the public pension once they retire early, in order to meet the 40-year minimum requirement. In this situation, they are subject to a more favourable basis for the payment of contributions, which is 20% of the last known average annual salary of employees in Slovenia. Currently this contribution for recipients of occupational pensions amounts to EUR 90.40 per month.

Those members who do not retire early and choose to continue working until statutory retirement age may keep their assets in the fund and transfer them upon retirement to purchase an annuity from an annuity provider. Similarly, members who have not used all of their assets for the purchase of an occupational pension during their early retirement may transfer them at a later stage to purchase an annuity and increase their retirement income. In 2019 for example, 740 members requested to withdraw their savings as a lump sum or to have them transferred to an annuity provider, for a total combined amount of EUR 16.6 million.

Very few members of the scheme for workers in arduous and hazardous occupations actually use this scheme to retire before statutory retirement age. In 2019 for instance, 213 members of the scheme retired, and a total of 286 retirees received an occupational pension on 31st December 2019 (for an annual amount of EUR 3.8 million in total), compared to the 48 356 members of the scheme at that date. Several factors may explain this situation. One reason is that the list of eligible jobs includes some that can be easily performed until workers attain the retirement age for the public pension. Those workers tend to view occupational insurance as a good source of additional income to complement the public pension, and many do not see it as a transitionary payment to enable retirement before the statutory retirement age. Another reason could be linked to the discrepancy between the calculation periods for the occupational and public pension schemes. Members of the occupational scheme who do not have sufficient contribution periods in the public pension system if retiring early, may not always be aware of the option to purchase or may not be able to afford the purchase of additional years necessary to ensure they will receive a full old-age pension at statutory retirement age, and consequently do not use their occupational scheme as a bridge to retirement, but rather to complement their retirement income once they receive their public pension.

Other occupational schemes

For savings accumulated in occupational schemes, either voluntary or mandatory, an annuity should be purchased from a life insurance or pension company of the member’s choice, at retirement age. Withdrawal as a lump sum is authorised only if funds do not exceed a threshold defined by law, and which is set at EUR 5 120 for 2020, i.e. about 20% of the annual average wage. Before 2013, payments as lump sums could be requested regardless of the account balance, as long as the member was in the plan for at least 120 months.

The threshold of EUR 5 120 to request a lump sum applies to each contract separately, therefore individuals having saved in different occupational schemes, for instance those who have changed employers during their career, may request to withdraw their assets as lump sums even if the overall sum of their total assets from different contracts exceeds the threshold. This feature may prove ineffective especially for workers in non-standard forms of work such as temporary contractors or part-time workers, who may change jobs more frequently. It may also discourage members from consolidating their accounts when changing occupations, and therefore lead them to keep several accounts with low balances.

The Slovenian annuity market comprises several types of annuities, including standard, guaranteed and accelerated annuities, as detailed in Table 5.7. Guaranteed annuities respond to bequest demand from members given that they are inheritable during the guarantee period. In addition to being inheritable during the guarantee period, accelerated and partially accelerated annuities pay a significantly higher stream of income (from twice more for partially accelerated annuities up to 12 times more for accelerated annuities) during the guarantee period, and only pay a lower portion of lifetime income thereafter.

Annuity calculation

Regulations 110/13, 94/14, 21/16 and 68/19 define rules and minimum requirements for how annuity providers should compute annuities purchased with retirement savings.29 Annuities should be computed based on the age of the member and their account balance. Any other personal circumstances, such as gender or health status, should not be taken into account when calculating the pension annuity. All annuity providers must therefore use unisex tables for pricing annuities.

Different rules apply to pension companies and insurance companies with respect to the mortality tables they use for reserving. Pension companies must use gendered mortality tables defined by regulation for reserving. Ahead of 2016, there were no official mortality tables based on the Slovenian population, hence for contracts written before 1st October 2016, pension companies must use German mortality tables DAV 1994R for reserving. For contracts written after that date, Slovenian mortality tables SIA65 from 2010 must be used by pension companies to this aim. Insurance companies may choose the mortality tables to use for reserving – which can be, but do not have to be, unisex – as long as they produce technical provisions at least as high as those produced using the German DAV 1994R and Slovenian SIA65 2010 tables.30

The Slovenian SIA65 mortality tables take into account expected mortality improvements as well as the selection effect leading pensioners and annuitants to have lower mortality than the general population. The mortality improvements derived for the tables are, appropriately, based on the historical experience of the Slovenian population. However, the selection effect to adjust the level of the general population mortality to the level of pensioner mortality is based on earlier experience of annuitants in the United Kingdom (when annuitisation was mandatory), making some adjustments to reflect the experience of annuitants in Germany, where the annuitisation for personal pension products such as Riester is also mandatory. Both countries demonstrate similar selection factors, and it is likely to be a reasonable estimate of the selection experienced in Slovenia. In Slovenia, around 40% of the population have occupational plans requiring that they annuitise, compared to around 50% of the United Kingdom working population having an occupational pension plan, prior to the introduction of automatic enrolment. Nevertheless, the appropriateness of this assumption for the Slovenian population could be further investigated.

While the SIA65 tables do account for mortality improvements, the fully generational tables are not used in practice. Rather, the tables are reduced to a one dimensional table using the age-shift method, which could result in an inaccurate estimate of technical reserves needed to cover pension and annuity liabilities. Given current technological capabilities and advancement over the years, it no longer seems impractical to apply the full two-dimensional generational tables rather than the one-dimensional approximation.

Profit sharing is required at a rate of 90%. Any profit stemming from investment returns or mortality experience must be distributed to annuitants. Profit is computed annually, and 50% of shared profits must be used to increase annuity amounts, while the remaining 50% of shared profits is set as reserves.

Annuity payments should be made monthly, except if lower than EUR 30, in which case they can be made quarterly, semi-annually or even annually.

The discount rate used for annuity calculations must be no less than 0.5% per annum, and no more than 4.00% per annum. Regardless of actual interest rates levels, annuity calculations must be done with a rate included in the 0.5% to 4.00% range. This may not be optimal as it may lack flexibility, and having rules to define the annuity rate may prove more effective than setting numerical boundaries.

The cost of providing an annuity may not exceed 12% of the purchase amount of the annuity that will be paid to the insured. Legislation also mandates that the long-term business fund for the payment of pension annuities may, in addition to the costs taken into account in the calculation of the pension annuity, be charged only by the operating costs of this fund specified in the pension plan for the payment of pension annuities.

5.7.2. Personal schemes

For voluntary personal plans, there are no conditions to request the payment of funds accumulated, and a lump sum may be requested at any time, before or after the statutory retirement age.31 Table 5.8 details the number of withdrawals as well as the amounts withdrawn from personal retirement savings plans between 2011 and 2018. There is generally a downward trend in both the number of withdrawals and the total amounts of assets withdrawn, with 2 549 withdrawals for a total of EUR 8.8 million worth of assets in 2011, compared to 491 and EUR 2.2 million in 2018. This is likely linked to the different tax treatments of personal savings depending on their duration and withdrawal method. Savings maintained in a pension account for at least ten years do not attract the Insurance Premium Tax of 8.5%. Withdrawals as annuities enjoy a preferred tax treatment compared to lump sums, and therefore encourage individuals to withdraw only once to annuitise, rather than several times during the life of the pension contract.