1. Synthesising good practices in fiscal federalism

The design of intergovernmental fiscal relations can help to ensure that tax and spending powers are assigned in a way to promote sustainable and inclusive economic growth. Decentralisation can enable subnational governments to provide better public services for households and firms, while it can also make intergovernmental frameworks more complex, harming equity. The challenges of fiscal federalism are multi-faceted and involve difficult trade-offs. This synthesis chapter consolidates much of the OECD’s work on fiscal federalism over the past 15 years, with a particular focus on OECD economic surveys. The chapter identifies a range of good practices in the design of country policies and institutions related to strengthening fiscal capacity, delineating responsibilities across levels of government and improving intergovernmental co-ordination.

Fiscal federalism refers to the distribution of taxation and spending powers across levels of government. Through decentralisation, governments can bring public services closer to households and firms, allowing for better adaptation to local preferences. However, unless properly designed, decentralisation can also make intergovernmental fiscal frameworks more complex and risk reinforcing interregional inequality. Accordingly, several important trade-offs emerge from the devolution of tax and spending powers which require consideration by policy makers. In addition, globalisation and changes to the geographic concentration of economic activity reinforce the importance of inter-governmental fiscal relations and subnational governance (Boadway and Dougherty, 2019[1]).

Policies for fiscal decentralisation: A meta-analysis of OECD country surveys

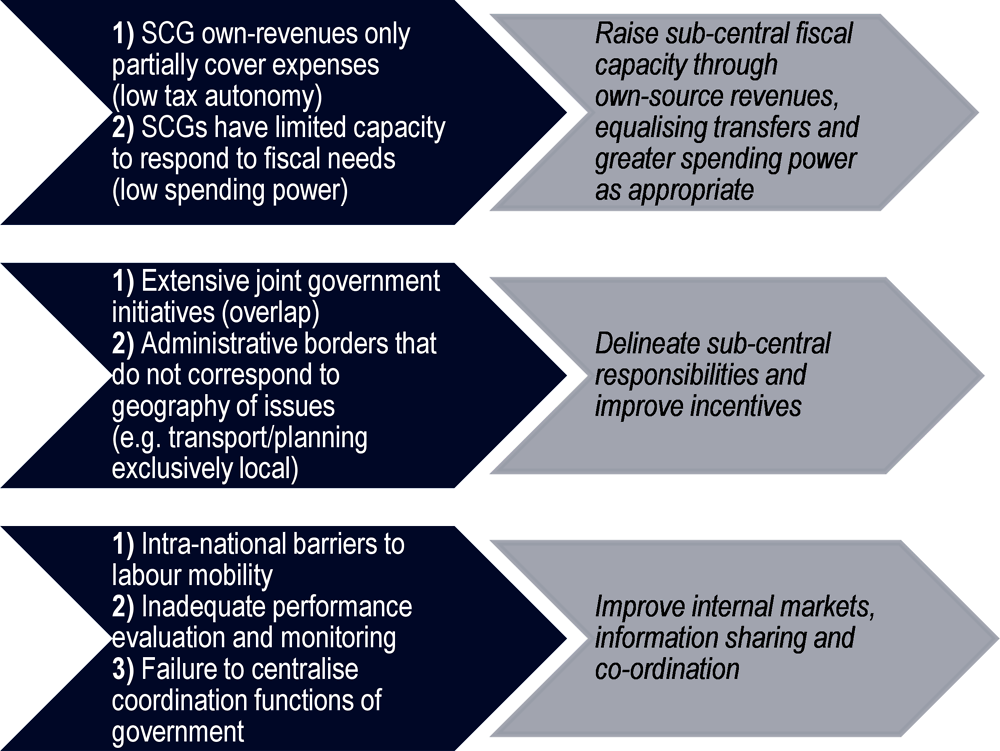

This synthesis chapter reviews both cross-country research on fiscal federalism and individual country experiences with the aim of consolidating OECD recommendations for improving fiscal relations across levels of government. To this end, it compiles the findings and recommendations presented in country-level Economic Surveys over the past fifteen years, since the inception of the Network on Fiscal Relations across Levels of Government. The chapter proposes a framework for fiscal decentralisation based on three high-level recommendations supported by several sub-recommendations (Box 1.1). The framework provides guidance to policy makers about policy options to consider along with the associated trade-offs. Figure 1.1 presents a selection of key diagnostic observations that tend to precede the three primary recommendations.

Type I. “Fiscal capacity” recommendations: strengthen subnational taxation and spending powers to allow governments to respond better to local needs and regional variations.

1. Better align own-source revenues with sub-central spending

2. Raise sub-central tax autonomy to ensure sufficient capacity

Type II. “Delineation” recommendations: clearly delineate responsibilities both horizontally and vertically to improve efficiency and equity.

Type III. “Co-ordination” recommendations: minimise barriers to internal trade and enhance inter-governmental co-ordination.

What is fiscal decentralisation?

Fiscal decentralisation refers to the assignment of tax and spending powers to sub-central governments (SCGs). The degree of fiscal decentralisation can be measured in terms of two components: tax autonomy and spending power. Tax autonomy describes the leeway that SCGs have over tax policy, such as the right to introduce or to abolish a tax, to set tax rates, to define the tax base, or to grant tax allowances/reliefs to households and firms (Dougherty, Harding and Reschovsky, 2019[2]). Spending power describes the level of control or authority of subnational decision makers over public spending, including deciding how services are organised, how funds are allocated, the preferred level and quality of inputs and outputs and how service delivery is measured and monitored (Dougherty and Phillips, 2019[3]). By bringing together tax autonomy and spending power, fiscal decentralisation captures the notion of aligning sub-central control over both taxation and budgets (OECD/KIPF, 2016[4]).

Traditionally, tax autonomy and spending power have been quantified using SCG tax and spending shares, respectively, which are readily available on a consolidated basis in the OECD’s Fiscal Decentralisation database annually.1 However, there are clear limitations to this approach. While SCG tax and spending shares give a rough indication of the extent of fiscal decentralisation, they fail to capture arrangements that lead SCGs to collect taxes or dispense funds without possessing control over, e.g., the rate of the tax or the allocation of the funds. In response, the OECD’s Network on Fiscal Relations has developed a set of tax autonomy and spending power indicators which seek to reflect more accurately the extent of subnational control over taxation and spending.

The OECD tax autonomy indicator employs a system of eleven codes to classify tax instruments according to the degree of control possessed by subnational government over the instrument in question. Codes range from a1, which indicates that the recipient SCG sets the tax rate and any tax reliefs without needing to consult a higher-level government, to e.g. d4, indicating a tax-sharing arrangement in which the revenue split is determined annually by a higher-level of government. In this way, the tax autonomy indicator captures the full spectrum of SCG control over taxation. From the inception of the Network on Fiscal Relations, the OECD has completed the tax autonomy study every three years, with the latest analysis completed in 2020, based on available data for 2018, as described in Chapter 3. This work has shown that SGCs in the OECD have significantly less tax autonomy than is suggested by simple share-based measures of decentralisation (OECD, 2013[5]; Dougherty, Harding and Reschovsky, 2019[2]).

Similar to the tax autonomy indicator, the OECD spending power indicator was developed to capture aspects of subnational control over spending that are not revealed by the spending share alone. The spending power indicator employs survey data to score subnational autonomy in various sectors on a scale from 0 (less subnational power) to 10 (more subnational power). Within each sector, survey questions assess subnational power along the several dimensions: policy autonomy (e.g. determination of policy objectives), budget autonomy (e.g. power to allocate funding), input autonomy (e.g. management of civil servants who design or provide public services), output autonomy (e.g. service standards), and evaluation/monitoring autonomy. The raw data are then used to compute scores for each sector, by country. These new indicators are described in Chapter 4 which presents spending power indicators for primary and secondary education, health care, housing, long-term care and transport sectors (OECD/KIPF, 2016[4]; Dougherty and Phillips, 2019[3]).

Fiscal decentralisation: 1990s to today

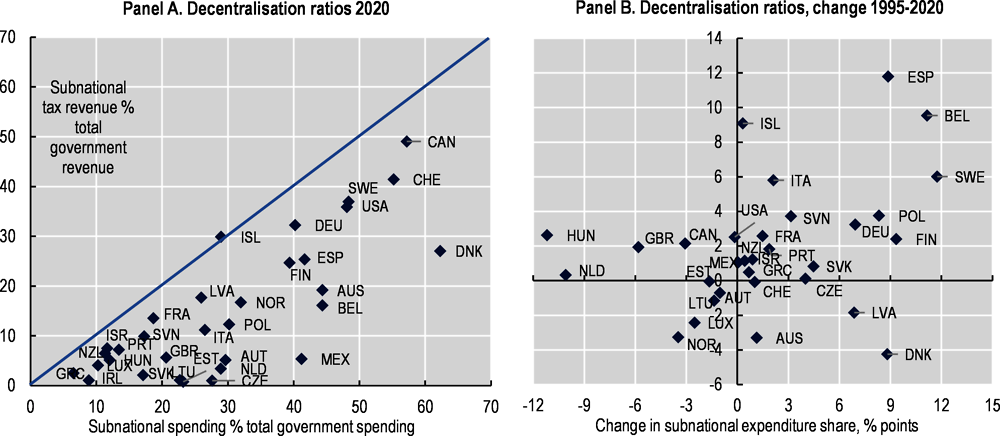

In the 1990s and the early 2000s, many countries decentralised spending further, especially in education, infrastructure, environment and neighbourhood services. The resulting rise in the vertical fiscal imbalance – the difference between spending and own revenue – was met with the growth of grants or transfers. After the economic and financial crisis of 2008-09, the share of sub-central spending started to decline again. In contrast, the sub-central revenue share has changed little over the past two decades.

Today, intergovernmental fiscal frameworks vary widely across countries, but with some key similarities. For example, in all OECD countries spending is more decentralised than revenue (Figure 1.2, Panel A). Across the OECD, SCGs averaged one-third of total government spending and one-fifth of total revenue in 2015. In 2014, the SCG share of total revenue ranged from almost 50% in the case of Canada to less than 10% for Ireland and Greece. In terms of tax autonomy, State/regional governments on average have full discretion over 70% of their tax revenue (classified as a1 by the tax autonomy indicator). Another 15% of their revenues come from shared taxes, where state governments’ consent to the sharing ratio is required. In contrast, local governments, on average, have full or close to full autonomy over only 13% of their revenue. Nevertheless, local governments retain discretion, subject to some limitations, over an additional 62% of tax revenues on average (Dougherty, Harding and Reschovsky, 2019[2]).

Meanwhile, spending power indicators for OECD countries suggest that subnational spending shares may exaggerate true SCG authority over spending. In many cases, substantial decision-making power over a given sector rests with a higher order of government even where some portion of the funding comes from the subnational level. SCG spending power is higher in federal than unitary countries, and higher in the housing, transport and education sectors as compared to the health care and long-term care sectors (Dougherty and Phillips, 2019[3]).

Note: The 45 degrees line in Panel A shows a situation where revenue decentralisation equals spending decentralisation. The farther away a country is from that line, the larger its vertical fiscal imbalance. In Panel B, Iceland’s position represents the change between 1998 and 2019.

Source: OECD Fiscal Decentralisation database.

The trade-offs of fiscal decentralisation

The modern theoretical underpinnings of decentralisation originate with Oates (1972[6]). The decentralisation theorem posits that, assuming no cost savings from centralisation, aggregate welfare across a set of jurisdictions will be superior when each jurisdiction is allowed to select its own public consumption bundle as opposed to when uniform consumption is provided across all jurisdictions. Obviously, this simple statement of the theorem does not account for the loss of economies of scale or a myriad of other factors that may intervene as fiscal decentralisation increases.

In practice, the policy maker faces a set of multi-dimensional trade-offs when designing intergovernmental frameworks for fiscal decentralisation. Previous work by the Network has discussed how decentralised fiscal frameworks allow for catering to local preferences and needs, while more centralised frameworks help reap the benefits of scale (OECD, 2013[5]). Another key trade-off derives from the effect of decentralisation on the cost of information to different levels of government. While greater decentralisation implies that subnational governments can access more information about the needs of a constituency at lower cost, it simultaneously increases the informational distance between central and subnational government. In turn, this may make information more costly from the perspective of the central government, impeding its co-ordination and monitoring functions (de Mello, 2019[7]; de Mello, 2000[8]).

Decentralisation could also engender a costly misalignment of incentives. For example, a “common pool” problem may arise when decentralisation narrows the subnational revenue base and raises the vertical fiscal gap (de Mello, 2000[8]). In this case, the necessary reliance on revenue sharing with central government to ensure SCG fiscal capacity may also distort the cost/benefit analysis of subnational governments—particularly in situations where an SCG realises a payoff without bearing the entirety of the associated cost. Rigid arrangements that entrench fiscal dependence on the central government may drive SCGs to manipulate tax-sharing agreements in order to increase their share while undermining their motivation to cultivate the local tax base. Therefore, the possible efficiency and equity gains from decentralisation are closely linked to mitigating the pitfalls of poorly designed revenue sharing (Kim, 2018[9]).

In light of these trade-offs, recent empirical work has begun examining the non-linear effects of fiscal decentralisation. This includes evidence of an inflection point for decentralisation within the health sector (Dougherty et al., 2019[10]) and data, which suggest that decentralisation may have diminishing marginal effects on economic outcomes, as discussed further below.

Empirical observations on fiscal decentralisation

Decentralisation and growth

An extensive literature reports mixed effects of decentralisation on growth. Martinez-Vazques et al. (2017[11]) provides a survey outlining much of the work to date and underscoring the ambiguous results. Within-country studies are especially inconclusive (OECD, 2019[12]). For example, studies of decentralisation among US States have found both positive e.g. Akai and Sakata (2002[13]) and negative effects e.g. Xie et al. (1999[14]) on growth. Similarly, studies of decentralisation and growth in China have reported both positive e.g. Qiao et al. (2008[15]) and negative effects e.g. Zhang and Zou (1998[16]).

This ambiguity can be contextualised by economic theory. Blöchliger and Akgun (2018[17]) outline several channels that link decentralisation to growth, both positively and negatively. First, following Tiebout (1956[18]), decentralisation may allow the mobile resident (or, more generally, mobile factor of production) to trigger inter-regional competition by “voting with her feet”. This pressure stimulates public sector productivity and, by extension, economic growth. Second, decentralisation may limit the power of special interests while enabling innovation and thereby fostering productivity. At the same time, other aspects of economic theory suggest a negative relationship between decentralisation and growth. For example, decentralisation may undermine economies of scale. Likewise, decentralisation may lead SCGs to be affected by externalities created by the policy choices of adjacent jurisdictions. In these cases, there is a risk of undersupply of public goods or inadequate taxation.

OECD research has found a broadly positive relationship between revenue decentralisation and growth, with spending decentralisation demonstrating a weaker effect, e.g. Blöchliger, Égert and Fredriksen (2013[19]); Blöchliger and Akgun (2018[17]) find that “tax decentralisation is more conducive to growth than spending decentralisation”, with a 10 percentage point increase in tax decentralisation associated with 0.1 percentage points more economic growth. This is consistent with other recent studies, including Gemmell et al. (2013[20]) and Filippetti and Sacchi (2016[21]).

Nevertheless, the role of country-specific circumstances is an important caveat to cross-national findings, as outcomes may feed back into the decentralisation process. An empirical study by the OECD that takes account of potential endogeneity issues, Dougherty and Akgun (2018[22]), found that the marginal effect of further decentralisation varies across countries to a large degree, reflecting the degree of de facto centralisation or decentralisation of existing revenue and spending responsibilities.

Decentralisation and inequality

OECD research on decentralisation and household income inequality suggests both that country specifications matter and that the effects may differ depending on the part of the income spectrum considered. For instance, Stossberg and Blöchliger (2017[23]) find that increasing decentralisation by 1% reduces the gap between the second richest and the median household income decile by 0.8%. As such, decentralisation appears to reduce the gap between high and middle-income households but may leave low incomes behind, especially where jurisdictions have large tax autonomy (Figure 1.3). More broadly, Dougherty and Akgun (2018[22]) observe that further decentralisation would increase the 90/10 income decile ratio on average, although the marginal effects vary considerably by country.

Note: Coefficients reflect percentage point changes, i.e. 0.42 means that a one percentage point increase in decentralisation (e.g. the spending share increases from 12% to 13%) is associated with an increase by 0.42 per cent points of the ratio between the median and the respective household income decile. A negative coefficient means that increasing spending decentralisation reduces the gap between that income decile and the median income. A positive coefficient means the gap to the median income is widening. “10/50” describes the lowest-income decile, “50/90” the second-highest. Asterisks (***, ** and *) indicate the level of significance at the 1%, 5%, and 10% levels, respectively.

Source: Stossberg and Blöchliger (2017[23]).

Fiscal autonomy may also be linked to income convergence at the regional level. In a study of regions within OECD countries, Blöchliger et al. (2016[24]) find that increasing sub-central own revenue share “by 10 percentage points is associated with a reduction of the regional GDP coefficient of variation between 3.6 and 4.3 percentage points” and that “increasing the [SCG] tax share by 10 percentage points reduces disparities by 2.4 to 2.8 percentage points” (Blöchliger, Bartolini and Stossberg, 2016[24]). The underlying mechanism may be related to the pressures of inter-jurisdictional competition which drives improved public sector performance across all regions. While fiscal autonomy could raise concerns about predatory tax competition, OECD research suggests that increasing tax autonomy does not induce a “race to the bottom” with respect to subnational tax rates. In fact, over the past couple of decades SCG tax rates have “trended up rather than down and generally converged over time” (OECD, 2013[5]).

Decentralisation, public services and social capital

Better adapting to the preferences of the community remains one of the key rationales for decentralisation. It is therefore unsurprising that decentralisation has been empirically connected to improved efficiency of public services, under the right institutional conditions (Sow and Razafimahefa, 2018[25]). Moreover, by bolstering allocative efficiency, transparency, community participation and the perceived responsiveness of the public sector, fiscal decentralisation can engender greater social capital in the form of increased trust and co-operation (de Mello, 2004[26]).

Consistent with the growth literature, recent work on sectoral decentralisation suggests both benefits and limitations to decentralisation as a policy to enhance the performance of the education and health care sectors. In healthcare, research suggests costs fall and life expectancy rises with moderate decentralisation, but the opposite effects hold once decentralisation becomes excessive (Dougherty et al., 2019[10]). With respect to educational attainment, Lastra-Anadón and Mukherjee (2019[27]) find that a 10 percentage point increase in the subnational revenue share improves PISA scores by 6 percentage points, corresponding to an average improvement by around six positions in the PISA country ranking. The positive correlation between subnational tax revenue share and overall PISA scores in math, science and reading can be seen in Figure 1.4. A similar yet weaker relationship is found with other measures of education decentralisation, such as school autonomy or subnational education spending.

Source: Education at a Glance, OECD Fiscal Decentralisation database.

Fiscal autonomy is a rich concept, encompassing a diversity of measures that reinforce efficiency, equity and cohesion within and among SCGs. Important in enabling fiscal decentralisation, fiscal autonomy requires that SCGs receive adequate tax autonomy, spending power and/or fiscal equalisation (or similar transfers). In essence, fiscal autonomy should support the objective of ensuring that SCGs have sufficient fiscal capacity to fulfil their mandates. Depending on the structural context, fiscal autonomy may reduce the need for vertical transfers while allowing for better adaptation to local preferences. This implies that SCGs adjust their own-source revenues to match their spending responsibilities. Where possible, the role of transfers should be to correct for structural income differences among SCGs and their respective tax revenue potentials, rather than to compensate for the failure to fully exploit the local tax base (Box 1.2).

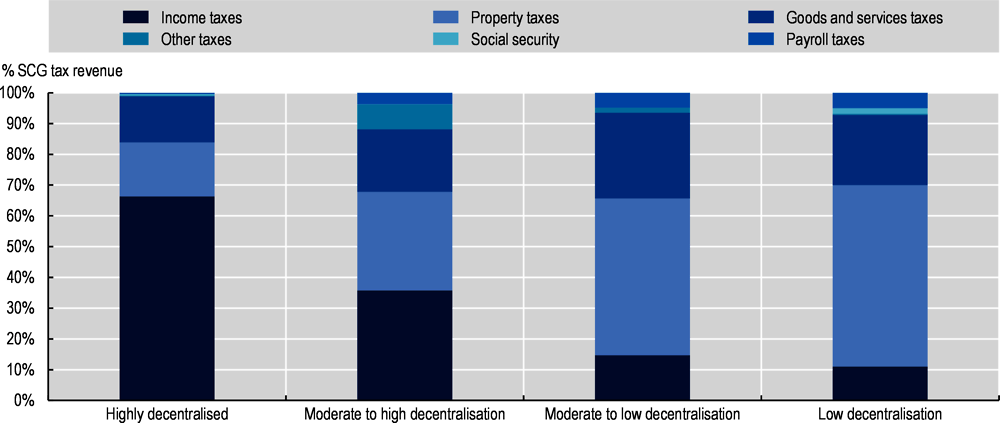

At present, SCGs draw their own-source revenues from a range of streams with income, property and consumption taxes being the primary instruments. Other taxes play a comparatively minor role. The tax mix itself appears strongly related to the extent of decentralisation, as shown in Figure 1.5. In more centralised countries, SCGs rely largely on (immovable) property taxes. Among the bottom 50% of OECD countries in terms of SCG revenue as a percentage of total government revenue, property taxes constitute 48% of the SCG tax mix on average. As decentralisation increases, income taxes start to play a greater role. SCGs in the top quartile in terms of SCG revenue as a percentage of total government revenue see income taxes constituting on average 62% of their tax mix. The subnational tax mix has changed relatively little over the last 20 years, with a decline in the share of property taxes and a rise in the share of consumption and income taxes – especially personal income tax. Since around 2010, the property tax share has again been on the rise. Overall, the subnational share of total taxation has hardly increased (see Figure 1.2, Panel B).

Note: Each column represents a quartile of OECD countries in order of decreasing sub-central revenues as a share of total government revenue. Revenues from tax-sharing agreements where the SCG does not control the rate are not included. Where data for 2019 was not available at the time of publication, data for 2018 was used.

Source: OECD Global Revenue Statistics database.

Like the SCG tax mix, sub-central tax autonomy varies substantially by country. In particular, a clear difference is apparent between the level of SCG tax autonomy in federal and unitary countries (see Chapter 3). Of the ten OECD countries with a federal or quasi-federal structure (i.e. with state or regional governments), seven have a very high degree of tax autonomy. In three – Australia, Switzerland, and the United States – state-level governments have full autonomy over 100% of their tax revenue. In another three federal/quasi-federal countries – Canada, Belgium and Spain – over 90% of state-level revenue is classified as fully autonomous, and in one additional federation, Mexico, the share is over 80%. In contrast, full SCG tax autonomy is infrequently observed within unitary countries. However, Dougherty et al. (2019[2]) note that within 16 of 35 OECD countries examined, local governments have a substantial amount of tax autonomy, with full or restricted discretion on tax rates for at least 85% of their tax revenue.

SCG fiscal autonomy: Adapting to local preferences while spurring competition, convergence and investment

Consistent with the theoretical foundations established by Oates (1972[6]), enhancing SCG fiscal autonomy allows the bundle of public goods consumed to be selected locally, thus better matching local preferences. Additionally, sub-central fiscal autonomy enables interregional competition—not only in terms of tax rates, but just as importantly in terms of public services. Naturally, this may give rise to fears of predatory tax competition or worsening inequality. However, OECD research suggests that fiscal decentralisation is generally conducive to convergence, both in terms of tax rates and per capita income (Blöchliger, Bartolini and Stossberg, 2016[24]) .

Decentralisation has also been linked to greater public investment, with a 10% point increase in decentralisation (as measured by both SCG spending and revenue share of government total) “lifting the share of public investment in total government spending from around 3% to more than 4% on average” (Blöchliger, Égert and Fredriksen, 2013[19]). The investment driven by decentralisation appears to accrue principally to soft infrastructure, that is human capital as measured by education. As with tax rates and income, the link may be explained by the pressures of interregional competition, which drives productive investment as regions aim to attract workers and firms.

The role of grants and transfers

Various circumstances may lead SCGs to be unable to fully fund their spending responsibilities using own-source revenues. The gap may be driven by a combination of both structural inequalities related to geography and income as well as inadequate fiscal autonomy. Filling the gap may require vertical transfers or grants from central government (and sometimes horizontal transfers from other SCGs). However, it is important to differentiate between grants that rectify structural inequalities (e.g. equalisation) and grants that are necessitated by inadequate fiscal autonomy and therefore displace own-source revenues. This is because excessive reliance on grants in place of own-source revenues can pose certain problems, particularly in the absence of proper transfer design. In addition to their pro-cyclical tendencies, grants are susceptible to the tumultuous character of political economy: complex formulas are vulnerable to rent seeking, which can cause an inefficient or regressive allocation of government spending. Lastly, grant-related dependence on other levels of government can reinforce deficit bias where the transfer system rewards larger sub-central fiscal gaps (OECD/KIPF, 2016[4]).

Fiscal equalisation as the companion of fiscal autonomy

Fiscal equalisation plays an important role in rectifying structural inequalities by correcting for economic conditions beyond the control of local government with the aim of mitigating differences in service quality between regions (OECD, 2013[5]). In order to encourage optimal exploitation of the local tax base, revenue-equalising transfers should be calculated based on potential revenue (i.e. tax effort) as opposed to actual revenue. Meanwhile, cost-equalising transfers should be based on a few key indicators or standardised costs, rather than actual expenditure. In addition, institutional measures such as arms-length oversight bodies and budget rules should be employed to help to ensure the effectiveness of equalising transfers.

Guidance from country surveys

The synthesis below is based on Forman, Dougherty and Blöchlinger (2020[28]). OECD Economic Surveys are cited by name and year, and more information is available at: www.oecd.org/economy/surveys/.

Strengthening own-source revenues

The principal survey recommendation related to fiscal autonomy is to strengthen the SCG tax base including through property taxation, consumption taxes and income taxes. Sometimes this is merely a matter of encouraging SCGs to employ powers that they currently possess, but have been hesitant to use for political reasons. For example, Spain (2007) was urged to encourage regional and local governments to more fully take advantage of their own taxing powers. Korea (2008) was advised to support SCGs in changing local income tax rates to increase self-sufficiency while avoiding volatile revenue sources like corporate taxes. In certain cases, SCGs do need new powers to secure own-source revenues. Mexico (2013) was urged to allow states to charge income and consumption taxes over and above the equivalent federal taxes. Economic surveys have consistently recognised the importance of allowing SCGs to harness their own tax bases—not only to replace transfers, but also to motivate local authorities to pursue policies that encourage revenue-enhancing economic growth.

The mobility of the tax bases assigned to the sub-central level is a particularly important consideration in the context of fiscal decentralisation. Box 1.3 summarises OECD guidance for policy makers when designing the SCG tax mix.

Less mobile tax bases are more suitable as revenue sources for SCGs given the possibility of predatory tax competition between jurisdictions.

Examples of taxes suitable for subnational assignment include taxes on immobile bases, resource royalties, conservation charges, single stage sales taxes, motor vehicle registration taxes, business taxes, parking taxes, property taxes, and personal income surcharges.

Taxes less suitable for assignment to lower levels of government include customs duties, value-added tax, corporate income tax, wealth/inheritance and carbon taxes. These taxes may be better levied at the national level.

Property taxation has distinct benefits, but these are undermined when valuations are out of date. For example:

Property taxes induce fewer behavioural distortions when compared with other taxes and are harder to avoid.

Empirical work suggests a shift to property taxation may be growth enhancing.

Consumption taxes have the advantage of efficiency and when properly designed need not undermine equity. For decentralised countries, switching to a destination-based VAT is often desirable, although this can limit the scope of SCG fiscal autonomy.

Piggy-backing SCG income taxes on central government income taxes can help to allocate tax room between the two levels of government, but can also lead to administrative complexity.

Sources: OECD (2006[29]); Hagemann (2018[30]); OECD (2019[12]).

Property taxes

The recommendation to strengthen subnational own revenue by increasing property taxation has featured across numerous country surveys.2 For 22 countries, surveys urged a “boost” to property taxation (Hagemann, 2018[30]). Such a “boost” would typically take one of three forms: raising rates, broadening the base or updating valuations.

Raising rates

Raising rates, that is increasing the rate at which immoveable property is taxed, was recommended in the cases of Finland (2014), Denmark (2012, 2014), Mexico (2013), the Netherlands (2010) and Korea (2005). In Finland, the survey noted that the central government had taken action to raise the band of permissible property tax rates from which municipalities could choose. Similarly, Mexico was advised to allow municipalities to decide their own property tax rates in an effort to increase them. The survey noted the particular challenge posed by the need for congressional approval to raise rates, creating a political incentive to deny permission. In the Korean case, the survey called for increasing local government revenues through greater taxation of property holdings. This would serve as a partial replacement for transaction taxes. Transaction taxes are seen to reduce labour mobility and land use efficiency, whereas taxes on property holdings may encourage efficient land use. In particular, the government was encouraged to accelerate the rise in effective tax rates on property holdings from 0.1% to 1%.

Broadening the base

SCGs should ensure that their property tax base is sufficiently broad by e.g. reducing exemptions and tax-free thresholds, as recommended in the cases of Australia (2006) and Mexico (2013). The Australian survey noted that tax exemptions on the following types of holdings lead to an excessive narrowing of the property tax base: owner-occupied residential land, primary production land and land held by charities and religious bodies. Moreover, tax-free thresholds were set for low value commercial and industrial holdings. In fact, this created an incentive to sub-divide plots as a way of avoiding taxes. In Mexico, the property tax base was undermined by limited technical capacity to administer the tax system and failure to track property values and ownership.

Updating valuations

Out of date property values have been identified as lowering SCG property tax revenues across a range of surveys including Austria, Belgium, Estonia, Finland, France, Germany, Greece, Indonesia, Mexico, Portugal and Sweden (Hagemann, 2018[30]). In particular, the Austrian survey (2005) noted that “up-to-date valuation of real estate is a precondition for strengthening revenue-raising powers of municipalities on the basis of real estate taxes”. In some cases, out of date values have been linked to infrequent updating of property registries (Almy, 2014[31]). In Mexico, the lack of regular valuation kept taxed property values well below market value with data showing “cadastral values 60% below market values in about half of the 32 states”. In the Belgian case (2015), a similar problem of infrequent valuations was observed. One solution discussed was devolving responsibility for updating the cadastre to the regions by creating regional cadastres. This would resolve the mismatch between the federal responsibility for updating valuations and the increases in regional revenues that would arise from the updates. Such a move would be broadly consistent with the objective of aligning revenues with responsibilities.

Piggy-backing taxes

A recurrent theme across both the Network’s publications and country surveys has been the balanced apportioning of fiscal room across central and sub-central government. For example, in the case of “piggy-back” taxation, SCGs add their own income tax on top of the tax charged by central government. This can maintain administrative simplicity in cases where the piggy-backed tax is also collected centrally (and then distributed). Austria (2005) was encouraged to consider doing precisely this, incorporating a state-level tax into its income tax schedule. To prevent shrinkage of the tax base, it was also suggested that the federal government should prescribe a range of rates from which all SCGs could choose. Piggy-backing income tax was also discussed in the case of Australia (2006), where it was proposed that the states implement an income tax surcharge to replace grants that they had received from the commonwealth. Ceding tax room to SCGs need not be restricted to income taxation. For example, it was recommended that Korea (2008) replace the nationwide comprehensive property tax (CPT) with increased local property taxes.

Improving consumption taxes: Destination-based VAT

Consumption taxes are thought to be less distortionary and more conducive to growth than most other forms of taxation and policy options exist to enhance their progressivity (Cournède, Fournier and Hoeller, 2018[32]). In the case of SCGs, some surveys have posited a destination based VAT as the preferred approach to the taxation of consumption. In contrast with origin-based taxes, destination-based taxes avoid distorting the producer’s choice of location (given that the consumer is considered less mobile).3 Both the United States (2005) and Brazil (2009) were advised to consider this approach.

Raising SCG spending power

The second component of fiscal autonomy is spending power. As spending power is typically more decentralised than tax autonomy (Figure 1.2, Panel A), it is unsurprising that measures to increase SCG spending power have been featured less prominently than measures to raise tax autonomy among the surveys reviewed. However, eight of the surveys did include explicit calls to increase the spending power of SCGs, typically through devolution of responsibility (an aspect of spending autonomy).

Adequate SCG spending power both enables adaptation to local preferences and reinforces a visible connection between local taxes and service provision, which drives efficiency and service improvements. This is particularly true in cases where the benefits of a certain service are localised to the jurisdiction where they are delivered (Oates and Schwab, 1988[33]). For example, in Korea (2008) the gap between the range of services available in communities – such as education and policing – and the limited role of local government in funding them, motivated recommendations to both raise local property taxes and assign greater spending responsibility to municipalities. Similarly, it was recommended that municipalities in Belgium (2009) take on financial responsibility for social assistance. Again, this was seen as a way of incentivising local government to provide more suitable and better-adapted support to the long-term unemployed. In bearing the cost of social assistance, municipalities would realise a monetary benefit from successfully transitioning people back into the labour market. In this way, reducing the cost of the service would require improving outcomes.

More broadly, recommendations that would increase the spending power of SCGs were also included in the Surveys of Australia (give states full management of education funding), Canada (enhance municipal fiscal capacity), the Czech Republic (encourage municipalities to offer childcare), France (ensure regions have adequate fiscal capacity to support vocational training), Japan (provide local governments with greater financial resources), and the United States (assign responsibility for highway funding to states).

Reducing transfer dependence

While well-designed transfers can be an important source of SCG financing, under certain circumstances they can be replaced by stronger own-source revenues that require less dependence on higher levels of government. The recommendation to reduce SCG dependence on transfers through raising own-source revenues has featured prominently in several country surveys. For example, it was observed for Japan (2005) that the former grant system undermined SCGs’ incentives to develop own-source revenues. Subsequent economic surveys acknowledged the positive effect of the so-called “trinity reforms” in furthering fiscal decentralisation through the transfer of tax revenue from the centre to SCGs. In fact, a recent survey of Japan (2017) provided evidence that these reforms have succeeded in reducing excessive allocation to public works (in lieu of other priorities). Similarly, transfer dependence among German Lander has been given extensive treatment in Economic Surveys. Recommendations for Germany (2006) include redesigning the equalisation system to enable the Lander to retain more own-source revenue, and increasing the scope of the Lander to generate such revenue.

Transfer reform and own-source revenues: Two sides of the same coin

Belgium’s country survey (2009) highlighted the complementarity of intergovernmental transfer reform and measures to strengthen own-source revenues. While the survey suggested reducing transfers to the regions (which would improve the revenue base of the federal government), SCGs were encouraged to utilise their own taxing powers to generate revenues. This advice was broadly reflected by the Sixth State Reform of 2012-14, which strengthened regional fiscal autonomy. Similarly, the economic surveys of Italy (2007) and Switzerland (2015) contained similar recommendations to constrain transfers as a way of encouraging SCGs to cultivate their own tax bases. In the Italian case, the use of a system of standardised costs and less than 100% equalisation was seen as the way to achieve this. In the Swiss case, there was a comparable recommendation to reduce transfers to cantons whose tax effort was below par.

It is always desirable to delineate responsibilities logically and to assign policy functions clearly. Where functions are not properly delineated between levels of government, fragmentation and overlap may arise. Box 1.4 presents key guidelines for successfully assigning responsibilities in the context of multi-level governance.

Ten guiding principles, which apply to all types of countries, have been identified. They are set out below:

1. Clarify the policy areas assigned to different government levels to avoid duplication, waste and loss of accountability.

2. Clarify the functions assigned to different government levels such as financing, regulating, strategic planning, implementing, or monitoring.

3. Ensure balance in the way different policy areas and functions are decentralised. This allows for complementarity and integrated policy packages for territorial development.

4. Align responsibilities and revenues while enhancing the capacity of subnational governments to manage their own resources.

5. Actively support subnational capacity building. More responsibilities at the subnational level need to be complemented with the human resources to manage them.

6. Build adequate co-ordination mechanisms across levels of government to manage shared responsibilities

7. Support cross-jurisdictional co-operation through specific organisational arrangements or financial incentives to increase efficiency through economies of scale.

8. Allow for asymmetric arrangements and pilot experiences to ensure flexibility in implementation.

9. Effective decentralisation requires complementary reforms in land-use governance, citizen participation and public service delivery.

10. Enhance data collection and strengthen performance monitoring to provide useful data for decision making and peer learning.

Source: OECD (2019[12]).

As seen in Box 1.4, clear delineation of responsibilities often relies on the basic principle that sub-central spending should be covered as much as possible by sub-central own taxes, with equalisation compensating for structural inequalities. A similar idea is that a given public service should be assigned to the level of government whose geographical extent covers both residents who benefit from that public service and the residents who pay for it. For example, if commuters from outside city limits use the public transit system of the city in which they work, a regional public transit system should be created to cover the entire area. This minimises externalities and helps to define an optimal size for an administrative region.

Signs of delineation problems

Examining the mismatch between spending shares and spending power can provide insight into the extent of delineation problems. Typically, actual spending power is more limited than spending shares would suggest because central governments may choose to delegate certain spending to SCGs while still exerting substantial control over service delivery. For example, a high spending share in the presence of low spending power may indicate that the SCG functions merely as an agency charged with implementing the central government’s policies. This may lead to excessive constraints on the SCG’s ability to meet the needs of its constituents, undermining the core objective of decentralisation. A notable attempt to address this can be found among the “free municipality” initiatives of the Nordic countries. For example, in Denmark municipalities were given more leeway in structuring the services that they pay for in order to better meet the needs of their residents (Allain-Dupré, 2018[34]).

The OECD’s spending power indicator has the potential to illuminate the extent of the gap between spending share and spending power (OECD/KIPF, 2016[4]; Dougherty and Phillips, 2019[3]), but where quantitative data is unavailable, qualitative evidence of fragmentation can also suggest a delineation problem. One indicator of delineation problems is a lack of correspondence between administrative boundaries and the natural geographical expanse of a particular service, such as transportation or water governance. Reassigning public functions and co-ordinating between regions can lead to better alignment. For example, municipal mergers can go together with greater responsibilities for the merged administrations. In several countries, a new intermediate (regional) level was created to take over responsibility for higher education, specialised health care, transport infrastructure and economic affairs (OECD, 2019[12]).

Guidance from country surveys

Fragmentation can occur across two dimensions: vertical and horizontal. In the former case, a single policy functions is spread incoherently across different levels of government. In the latter case, numerous small SCGs at the same level are assigned responsibility for a given public service without adequate co-ordination. In both cases, co-ordination failures and foregone economies of scale can arise due to fractured service provision and incongruous policies. Both horizontal and vertical fragmentation can seriously undermine the quality of public services and cause needless inefficiency. In response to vertical fragmentation, economic surveys have often recommended consolidating responsibility for an entire public service within a single level of government. In the case of horizontal fragmentation, they have tended to recommend enhanced co-operation or mergers of local government service providers.

Complex systems like health care, education and social services are particularly susceptible to vertical fragmentation

Among the surveys reviewed, nearly 40% of the delineation-related (Type II) recommendations pertained explicitly to health care, education or social services. This suggests that large, complex sectors face particular challenges with respect to overlap and fragmentation. For example, in terms of health care, the economic survey of Australia (2014) noted that primary care was allocated to the Commonwealth while states retained responsibility for public hospitals. This created opportunities for cost shifting, such as public hospitals passing the burden of post-operative care onto general practitioners. The same survey noted that Australia’s education system was affected by “complex and opaque funding arrangements” involving multiple levels of government. In a similar vein, the French vocational training system was seen to suffer from delineation problems. A 2014 reform introduced roles for a diverse range of actors such as national government, regions, and chambers of commerce. In addition, co-ordinating bodies were put in place at both the national and regional levels. This lead to a lack of clarity with respect to overall responsibility for the new system (Brandt, 2015[35]). In Mexico, the education system was found to be highly fragmented between the federal and state governments. An opaque, multi-part grant system was used to channel funds from the centre to the states, leading to asymmetries in the delivery of education services across the territory. In the area of social services, the economic survey of Spain (2008) identified a disconnect between the financing of unemployment benefits at the national level and the management and design of labour market reintegration support at the regional level. As regions received more funding when they faced a larger unemployed population, there was little incentive for them to design policies that reduce long-term unemployment.

Assignment to a single level can be a remedy for fragmentation

The typical remedy for fragmentation is to ensure that complete responsibility for a given public service is assigned to a single level of government. SCGs are often heavily involved in providing public services and assigning responsibility to them may allow for adaptation to local preferences. In the Australian case, the survey recommended clarifying roles and improving co-ordination between levels of government, while noting that in some cases reallocation of responsibility for an entire sector to a specific level of government may be necessary. This was consistent with the findings of Australia’s National Committee of Audit (NCA), which argued for complete state-level control over funding allocations to schools. Similarly, the economic survey of France (2014) recommended that the respective roles of national and regional vocational training councils be clarified to ensure that they did not interfere with one another. In particular, it was recommended that spending responsibility be assigned to one actor (e.g. regions). In the case of the Spanish unemployment system, the survey suggested it would be ideal to assign both financial responsibility for unemployment benefits and implementation of active labour market policy (ALMP) to the same level of government. However, acknowledging the political complexity of the task, the survey called for better monitoring and evaluation of ALMP implementation.

Co-funding in federations: An indication of fragmented assignment

Multi-level co-funding, that is joint funding provided by multiple levels of government, may be a sign of fragmentation. While multi-level co-funding can be justified when there are clear inter-regional spill-overs, such spill-overs are not always present. The economic surveys of both Germany (2006) and Switzerland (2006) highlighted inefficiencies arising from federal-state co-funding arrangements. First, states face an incentive to spend on projects even when the associated benefits are small, which can undermine a clear connection between cost and service provision in the eyes of the public. Second, complex mediation processes between governments can slow things down. Third, the administration of the funding can be costly and impede programme evaluation. Finally, the rigidity of earmarked funding from the federal government can undermine optimal allocation by SCGs.

To resolve these challenges, the surveys recommend moving away from systems of earmarked co-funding based on expenditure. Instead spending responsibility should be clearly assigned to the SCGs, with fiscal inequality corrected by revenue equalisation. Consistent with these recommendations, the Swiss reform of 2003 reduced the grant system by around 30% by assigning funding and regulatory power either fully to the federal or state level. At the same time, the portion of total transfers to cantons available to help them shoulder their new responsibilities increased from 25 to 40%.

It is important to note that where SCGs are unable to finance expenditure on critical social infrastructure such as primary education, well designed co-funding can play an important role. For example, the economic surveys of Germany (2016, 2018) recognised the removal of constitutional barriers to federal co-funding of education as a positive step towards helping financially weak municipalities make important investments in local education infrastructure.

Horizontal fragmentation and geographical divisions

Whereas the gap between spending share and spending power suggests vertical fragmentation between levels of government, excessive geographic division of local services indicates horizontal fragmentation. Horizontal fragmentation may lead to an obvious inefficiency arising from the inability to exploit scale economies, however an additional inefficiency arises from the co-ordination problems associated with unnatural divisions of cross-jurisdictional issues. In these cases, cross-border externalities may lead to a mismatch between the paying and benefitting jurisdictions. Synergies from amalgamating services across borders may improve outcomes, including in the areas of transport, urban waste management, water supply, fire-fighting and hospital administration (de Mello, 2019[7]).

The Valle de México metropolitan area provides an example of failure to integrate policy across a region. Land use planning is largely divided along the boundary lines of the 51 municipalities in the area. Similarly, public transport provision is fragmented between Mexico City and the State of Mexico. One remedy discussed in the Mexico surrvey (2019) would be to create metropolitan structures for cross-boundary public service delivery and integrated urban planning. A legal mechanism that fosters co-operation across different policy areas would help to overcome fragmentation.

Where small municipalities are struggling to provide cost-effective public services, amalgamation of jurisdictions is an obvious solution but not always optimal. Inter-municipal co-operation arrangements are more flexible and can be designed to take into account the differing functional areas (geographical zones) that make most sense for a given service. Though sometimes outright mergers of small municipalities have been recommended, such as in France (2015), Norway (2010) and Austria (2005), for Japan it was recommended that greater focus be placed on inter-municipal co-operation arrangements built around collaborations to provide an individual service or set of services. Underscoring the broad applicability of inter-municipal co-operation to avoid horizontal fragmentation, de Mello (2019[7]) provides further examples of this approach in Finland, France, Italy and Turkey.

A particularly interesting response to geographical fragmentation is found in the Belgian case. Co-ordination problems related to water policy were observed to derive from the fact that authority in this area was assigned to regions, whereas river basins do not follow regional borders. It was therefore suggested that water policies be better integrated by establishing water authorities at either the river basin or the national level (OECD, 2011[36]). Subsequent to this recommendation, Belgium’s Sixth State Reform led to broad changes in the institutional context as more competences were devolved to the regions. Nonetheless, overcoming geographical fragmentation remains important. This is facilitated by cross-regional bodies, such as the Groupe Directeur Eau which co-ordinates interested parties in the area of water governance (Bruxelles environnement, 2019[37]).

In certain cases, geographical fragmentation has motivated the creation of new regional levels of government. In Denmark, a wide-ranging municipal government reform was partially motivated by the view that health care provision was too fragmented across small administrative units. In response, health care responsibilities were re-assigned to one of five newly created regions (OECD, 2012[38]).

Intergovernmental fiscal relations are by no means restricted to questions of fiscal policy. Co-ordination and information flows also play a central role in effective fiscal federalism. For example, co-ordination failures may lead to different levels of government working at cross-purposes. Lack of monitoring and benchmarking may allow service standards to slip, particularly when data are absent or inaccessible. Regulatory barriers to intra-national trade may hamper the free flow of goods, capital and labour within a country. Needless variation in SCG procedures may undercut the benefits of scale, particularly in the area of procurement. Finally, inadequate human and physical capital within the subnational public service can impede policy implementation.

Avoiding these issues in decentralised settings requires adequate inter-governmental fiscal co-operation (IFC). IFC can reinforce regulatory coherence between levels of government, while reducing policy contradictions or tensions and eliminating internal market barriers. Similarly, co-operation can facilitate the sharing of skills and technologies between SCGs. It can also create “peer pressure” to support adhering to agreed-upon rules or adopting common standards. Finally, IFC can help SCGs harness economies of scale in both important areas of public spending (e.g. infrastructure) and administration (e.g. taxation or procurement) (Ter-Minassian and de Mello, 2016[39]; de Mello, 2019[7]).

Illustrative examples of IFC in practice are provided by both Canada (federal) and Denmark (unitary). In Canada, the Council of the Federation, a body composed of provincial and territorial Premiers, acts as a forum for IFC. It has promoted co-operation in the areas of internal trade, health care, water resources, energy and transportation (Ter-Minassian and de Mello, 2016[39]). In Denmark, a 2007 reform of local government aimed to implement complementary vertical fiscal co-operation (additional grants and funds from central government to compensate SCGs for new costs) and horizontal fiscal co-operation (mergers of municipalities). In this case, IFC served to link “a territorial reform, a reallocation of tasks across levels of government, and a financing and equalisation system reform. This allowed compensating costs and benefits to carry over from one reform element to the other” (OECD, 2012[38]).

Based on a synthesis of OECD economic surveys, seven broad types of recommendations to support IFC in decentralised settings were identified: improve policy alignment and co-ordination between levels of government, eliminate internal market barriers and reduce regulatory fragmentation, enhance monitoring including through oversight at the national level, benchmark performance nationally and internationally, improve the quality and accessibility of performance measurement data, implement joint procedures and centralise procurement across SCGs, and build SCG professional capacity. Table 1.3 shows, which countries have been subject to these recommendations.

Guidance from country surveys

Improve policy alignment and co-ordination across levels of government

Any form of multi-level governance introduces the possibility that different levels of government may be working at cross-purposes. In the context of fiscal decentralisation, the prospect of contradictory, poorly co-ordinated or misaligned policy takes on new dimensions as questions of efficiency and incentives come into play. Indeed, co-ordination across levels of government, and in particular vertical co-ordination, has been identified as a key challenge in governance and fiscal policy by the OECD, IMF and European Committee of the Regions (Allain-Dupré, 2018[34]). This is reflected within the recommendations of the economic surveys, which have explicitly identified policy alignment and co-ordination as areas for improvement in several cases (Box 1.5).

Among EU countries, trouble absorbing EU funds can be a sign of poorly co-ordinated fiscal policy as well as inadequate SCG capacity (Figure 1.6). Recent OECD work has identified both capacity constraints and co-ordination deficiencies as encumbering the use of diverse financing mechanisms by SCGs (OECD, 2018[40]). In particular, 68% of respondents to a 2016 Committee of the Regions survey on obstacles to local and regional investment identified “capacity to design and manage public investment and PPPs funded by the EU Structural Funds and other EU programmes ” as either a challenge or major challenge for local/regional authorities (OECD-CoR, 2016[41]). The 2018 OECD economic survey of the European Union highlighted the importance of streamlined administration and enhanced administrative capacity to ensure the uptake of EU funds, particularly when it comes to co-ordinating with SCGs. Country surveys have echoed a similar message. For example, in Italy the central government’s failure to work effectively with local administrative agencies was cited as an impediment to the disbursement of EU Structural and Cohesion Funds. The surveys (2017, 2019) called for the central government to strengthen its role in setting minimum standards for project preparation and execution, while ensuring that a central co-ordinating agency had sufficient power to support regional efforts in implementing the projects. Likewise, the Czech Republic’s struggle to effectively absorb EU funds was linked to co-ordination issues arising from a heavily decentralised administration of the associated programmes in its 2008 survey. In response, a general simplification of the administrative process was recommended. Beyond EU funds, similar problems can arise when countries are faced with managing their own fiscal space. In Switzerland, the 2017 survey called on federal and cantonal governments to improve co-ordination to ensure that the significant fiscal space available was adequately utilised and to avoid persistent underspending.

1. Unweighted average across 25 EU countries.

Source: Caldera Sánchez (2018[42]), data from European Commission (2018), “Open Data Portal for the European Structural and Investment Funds (https://cohesiondata.ec.europa.eu/)”; European Commission (2014), "Analysis of the Budgetary Implementation of the Structural and Cohesion Funds".

The economic surveys have recommended increased multi-level co-ordination and policy alignment across a diverse range of government functions. Concerning environmental policy, Spain (2014) was urged to improve the horizontal alignment of regional pollution taxes by implementing a uniform tax among jurisdictions to increase efficiency. Austria (2005) was urged to focus on the vertical alignment of state and federal environmental objectives. A particular example is a major infrastructure project, which was supported by the federal government because it would aid the sustainability of transport, but simultaneously opposed by local government owing to concerns about local nature protection.

Other areas where increased co-ordination has been called for include health care, R&D, labour market and migration policy. In Australia (2014), improved state-federal co-ordination in health care was seen as a way of reducing the incentive to cost-shift between levels of government. Likewise, it was observed that lack of co-ordination was the leading cause of inefficiency in Switzerland’s (2015) highly fragmented health care system. In Austria (2005), vertical misalignment between federal and state R&D support programmes suggested a need for better co-ordination. State administered programmes were designed based solely on the needs of the state, without considering the federal government’s broader objective of fostering innovation. Similarly, Spain (2014) was called upon to improve the effectiveness of public investment in R&D and to reduce duplication through improved co-ordination across levels of government, perhaps via the creation of a national public investment agency. The same survey noted a vertical misalignment between regions and central government with respect to labour market policy: while central government paid unemployment benefits, it was left to the regions to support job seekers in finding work. In Belgium, migration policy was subject to a complex division of responsibility between the federal government and regions. The federal government oversaw residence permits, while the regions were responsible for certain work permits. A third category of permit, work permits issued to those with limited right of residence (e.g. asylum seekers), was issued by federal authorities. The 2015 economic survey of Beligum therefore called for careful co-ordination between levels of government, in particular to avoid harmful interregional competition such that variation in work permit rules did not become a distortionary factor in, for example, company location decisions.

An important area in which co-ordination was also advocated for is public investment – and infrastructure more broadly. In 2014, the OECD adopted the Council Recommendation on Effective Public Investment across Levels of Government which promotes vertical and horizontal co-ordination mechanisms, to enhance the effectiveness of public investment spending (OECD, 2014[43]). Specific modes of co-ordination cited include contracts, platforms for dialogue and co-operation, specific public investment partnerships, joint authorities, or regional or municipal mergers.

Eliminate internal market barriers and regulatory fragmentation

Internal market barriers include any impediment to the free-flow of goods and factors of production within a country that does not serve a useful social purpose. In some cases, such impediments come in the form of inconsistent or fragmented regulatory regimes. Examples include differing professional certification schemes across SCGs, different business licensing procedures, or needless inconsistencies in land-use regulations and building codes.

Economic surveys have identified internal market barriers and regulatory fragmentation as challenges in both federal and unitary contexts. However, given the often greater autonomy of SCGs within federations (Phillips, 2018[44]), it is unsurprising that the majority of references to internal market barriers pertain to federal countries. In Germany (2016) and Canada (2014), harmonising the recognition of immigrants’ qualifications across SCGs was recommended to facilitate integration. In Switzerland, a similar call was made for labour market uniformity by reducing restrictions on labour market access between cantons. Additionally, the 2015 and 2017 surveys of Switzerland noted that cantons should harmonise building laws and codes. In Spain (2014), implementing the market unity law was endorsed as a way of reducing the regional barriers to entry posed by fragmentation in the business licensing system. Finally, market barriers also present themselves in emerging areas like renewable energy. In Belgium (2009), it was suggested that green and combined heat and power (CHP) certificates be made transferable between all regions.

Benchmark performance nationally and internationally

Monitoring, evaluation and oversight are inseparable from benchmarking. Benchmarking, the comparing of performance measurements to a reference point, has a special significance in the context of fiscal decentralisation. This is because decentralisation implies that benchmarking should take place at both the cross-jurisdictional and cross-country levels. Phillips (2018[44]) provides a survey of benchmarking systems, with a focus on the special relevance of benchmarking in decentralised settings as well as approaches to competitive benchmarking.

While benchmarking may be applied across all areas of sub-central jurisdiction, economic surveys provide some illustrative examples of contexts where it was explicitly recommended:

Australia: Benchmarking the management of environmentally sensitive areas (2004 survey).

India: Participating in an international survey as a way of benchmarking state-level educational outcomes (2011 survey). Continuing to benchmark states with respect to one another and to share best practises in “labour regulations and land laws” (2016 survey).

Italy: Using cost benchmarking in public procurement (2015 survey).

Spain: Benchmarking regional public services with respect to cost and quality (2010 survey).

Improve quality and accessibility of performance data

Benchmarking and performance measurement are dependent on the availability of relevant data at the sub-central level. Yet making quality data accessible is easier said than done. This lead to explicit calls for improving available data on SCG performance in the surveys of Australia (public service quality), France (public service quality and cost), Germany (performance of public-private partnerships), Italy (procurement costs), Mexico (budget disclosure and fiscal transfers) and Switzerland (public salaries).

Implementing joint procedures and centralising procurement across SCGs

Co-ordination can aid SCGs in overcoming the loss of scale that may be associated with some aspects of decentralisation. For example, a central purchasing body can help achieve larger procurement volumes and/or increased administrative efficiency (OECD, 2015[45]). These factors have helped to motivate inter-municipal shared service models for procurement in e.g. England (Murray, Rentell and Geere, 2008[46]) and Queensland, Australia. In Queensland, the implementation of the Local Buy shared procurement programme was estimated to be saving local authorities between USD 4 million and USD 7 million per year (Dollery, Hallam and Wallis, 2008[47]).

Centralising procurement at the subnational level is a theme observed across several economic surveys. In France, the exceptionally large number of municipalities (communes) was linked to sub-optimal purchasing practises. Centralised, electronic procurement was recommended in the 2015 survey to standardise processes. Similar recommendations were made for Germany (2016), with a particular focus on the need for up-skilling the local civil service. In Italy, the 2015 survey noted that a massive reduction in the number of subnational purchasing centres (from 32 000 to less than 40) had already been proposed as a way of centralising procurement. Finally, Switzerland was encouraged in the 2007 economic survey to harmonise procurement rules across cantons to increase process accountability and competition among suppliers.

Build SCG professional capacity

The existence of capacity limitations particular to SCGs is supported by ample evidence. Such capacity limitations can extend to human resources and physical capital within the public sector, including low technical skills of tax officials and limited use of modern IT systems (Ter-Minassian, 2021[48]). This is echoed by survey recommendations calling for professionalisation or up-skilling of the sub-central public service. In both France (2015) and Germany (2016), surveys called for improving the skills of employees involved in subnational procurement. In the German case, this was explicitly linked to the advent of e-procurement, which would require stronger skills in the areas of data analysis and re-use.

Some middle-income countries have received more general encouragement to increase the technical competency of SCGs. Mexico (2019) was urged to build capacity and professionalise the civil service at the state and municipal levels. Similarly, Indonesia (2016) was advised to expand assistance to help regions to improve budget planning and implementation capacity.

Enhance monitoring, including through oversight at the national level

Dougherty, Renda and von Trapp (2021[49]) note the emergence of subnational independent oversight bodies as a recent extension of the global trend towards using such institutions to support policy development and decision making. Independent oversight bodies can be divided into three types: Independent Fiscal Commissions (IFIs), Independent Productivity Commissions (IPCs) and Regulatory Oversight Bodies (ROBs).

The first and third type, IFIs and ROBs, are of particular interest in the context of fiscal decentralisation because of their respective roles in fiscal scrutiny and policy co-ordination. Several of the surveys called for the use of oversight bodies or enhanced monitoring to support fiscal decentralisation, typically in a form resembling IFIs or ROBs. Importantly, many of these bodies were proposed at the national level in order to facilitate co-ordination among SCGs. For example, for Belgium it was recommended in 2011 that the National Account Institute or Federal Planning Bureau expand their scope to examine the fiscal consequences of the then current assignment of responsibilities across levels of government. Indeed, following the 2013 co-operation agreement on fiscal policy, the High Council on Finance had its scope broadened to monitor compliance with the agreement. The Council explicitly takes into account burden sharing among levels of government to ensure fairness when setting multi-annual budget targets. Similarly, Denmark’s central government was encouraged in the 2014 survey to carefully monitor its division of fiscal responsibilities with local government. In Mexico, INEE, the national education oversight body, and the Ministry of Education were encouraged in 2019 to work together to enhance the monitoring and evaluation capacity of SCGs. In Switzerland (2009), education was also urged to be subject to greater cross-cantonal scrutiny, owing to differences in policy, spending and resources across cantons. In this context, the Swiss Conference of Cantonal Ministers of Education was referenced as an important forum for agreeing on minimum standards.

Finally, Dougherty et al. (2021[49]) also identify important instances of oversight bodies at the sub-central level (e.g. Ontario’s Financial Accountability Office), noting as well that they may be co-ordinated at the national level (e.g. COAG in Australia). Surveys have sometimes made similar recommendations for oversight at the sub-central level. In Spain, monitoring and evaluation of employment services at the regional level was seen as a second-best alternative to fully assigning the provision of such services to central government (OECD, 2010[50]).

References

[13] Akai, N. and M. Sakata (2002), “Fiscal decentralization contributes to economic growth: evidence from state-level cross-section data for the United States”, Journal of Urban Economics, Vol. 52/1, pp. 93-108.

[34] Allain-Dupré, D. (2018), “Assigning Responsibilities across Levels of Government”, OECD Working Papers on Fiscal Federalism, No. 24.

[31] Almy, R. (2014), “Valuation and Assessment of Immoveable Property”, OECD Working Papers on Fiscal Federalism, No. 19.

[17] Blöchliger, H. and O. Akgun (2018), “Fiscal decentralisation and economic growth”, in Fiscal Decentralisation and Inclusive Growth, OECD Publishing, Paris.

[24] Blöchliger, H., D. Bartolini and S. Stossberg (2016), “Does Fiscal Decentralisation Foster Regional Convergence?”, OECD Economic Policy Papers, No. 17.

[19] Blöchliger, H., B. Égert and K. Fredriksen (2013), “Fiscal Federalism and its Impact on Economic Activity, Public Investment and the Performance of Educational Systems”, OECD Economics Department Working Papers, No. 1051.

[1] Boadway, R. and S. Dougherty (2019), “Decentralisation in a globalised world: Consequences and opportunities”, in Fiscal Decentralisation and Inclusive Growth in Asia, OECD Publishing, Paris, https://dx.doi.org/10.1787/a47d130f-en.

[35] Brandt, N. (2015), “Vocational training and adult learning for better skills in France”, OECD Economics Department Working Papers, No. 1260, OECD Publishing, Paris, https://dx.doi.org/10.1787/5jrw21kjthln-en.

[37] Bruxelles environnement (2019), Coordination de la mise en œuvre de la politique de l’eau au niveau belge.

[42] Caldera Sánchez, A. (2018), “Building a stronger and more integrated Europe”, OECD Economics Department Working Papers, No. 1491, OECD Publishing, Paris, https://dx.doi.org/10.1787/4ce667b4-en.

[32] Cournède, B., J. Fournier and P. Hoeller (2018), Public finance structure and inclusive growth, OECD Publishing.

[7] de Mello, L. (2019), Intergovernmental Cooperation: Challenges, Trends and International Experience, Paper prepared for the “Jornada sobre Experiencias de Cooperación y Asistencia entre Municipios”, University of Barcelona, Barcelona.

[26] de Mello, L. (2004), “Can Fiscal Decentralisation Strengthen Social Capital?”, Public Finance Review, Vol. 32/1, pp. 4-35.

[8] de Mello, L. (2000), “Fiscal Decentralization and Intergovernmental Fiscal Relations”, World Development, Vol. 28, pp. 365-380.

[47] Dollery, B., G. Hallam and J. Wallis (2008), “Shared services in Australian local government: A case study of the Queensland local government association model”, Economic Papers: A journal of applied economics and policy, Vol. 27/4, pp. 343-354.

[22] Dougherty, S. and O. Akgun (2018), “Globalisation, decentralisation and inclusive growth”, in Fiscal Decentralisation and Inclusive Growth, OECD Publishing, Paris.

[2] Dougherty, S., M. Harding and A. Reschovsky (2019), “Twenty years of tax autonomy across levels of government: Measurement and applications”, OECD Working Papers on Fiscal Federalism, No. 29, OECD Publishing, Paris, https://dx.doi.org/10.1787/ca7ebc02-en.

[10] Dougherty, S. et al. (2019), “The impact of decentralisation on the performance of health care systems: A non-linear relationship”, OECD Fiscal Federalism Working Papers, No. 27.

[3] Dougherty, S. and L. Phillips (2019), “The spending power of sub-national decision makers across five policy sectors”, OECD Working Papers on Fiscal Federalism, No. 25, OECD Publishing, Paris, https://dx.doi.org/10.1787/8955021f-en.

[49] Dougherty, S., A. Renda and L. Trapp (2021), “Independent oversight bodies: lessons from fiscal, productivity and regulatory institutions”, in Making Institutions Work, HSRC Press.

[21] Filippetti, A. and A. Sacchi (2016), “Decentralization and economic growth reconsidered: The role of regional authority”, Environment and Planning C: Government and Policy, Vol. 34/8.

[28] Forman, K., S. Dougherty and H. Blöchliger (2020), “Synthesising good practices in fiscal federalism: Key recommendations from 15 years of country surveys”, OECD Economic Policy Papers, No. 28, OECD Publishing, Paris, https://dx.doi.org/10.1787/89cd0319-en.

[20] Gemmell, N., R. Kneller and I. Sanz (2013), “Fiscal decentralization and economic growth: spending versus revenue decentralization”, Economic Inquiry, Vol. 51/4, pp. 1915–1931.

[30] Hagemann, R. (2018), “Tax Policies for Inclusive Growth: Prescription versus Practice”, OECD Economic Policy Papers, No. 24.

[9] Kim, J. (2018), “Fiscal decentralisation and inclusive growth: An overview”, in Fiscal Decentralisation and Inclusive Growth, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264302488-3-en.

[27] Lastra-Anadón, C. and S. Mukherjee (2019), “Cross-country evidence on the impact of decentralisation and school autonomy on educational performance”, OECD Working Papers on Fiscal Federalism, No. 26.

[11] Martinez-Vazquez, J., S. Lago‐Peñas and A. Sacchi (2017), “The Impact of Fiscal Decentralization: A Survey”, Journal of Economic Surveys, Vol. 31/4, pp. 1095-1129.

[46] Murray, J., P. Rentell and D. Geere (2008), “Procurement as a shared service in English local government”, International Journal of Public Sector Management, Vol. 21/5, pp. 540-555.

[6] Oates, W. (1972), Fiscal Federalism, Edward Elgar Publishing.

[33] Oates, W. and R. Schwab (1988), “Economic competition among jurisdictions: efficiency enhancing or distortion inducing?”, Journal of Public Economics, Vol. 35/3, pp. 333-354.

[51] OECD (2021), Making Property Tax Reform Happen in China: A Review of Property Tax Design and Reform Experiences in OECD Countries, OECD Fiscal Federalism Studies, OECD Publishing, Paris, https://dx.doi.org/10.1787/bd0fbae3-en.

[12] OECD (2019), Making Decentralisation Work: A Handbook for Policy-Makers, OECD Multi-level Governance Studies, OECD Publishing, https://dx.doi.org/10.1787/g2g9faa7-en.

[40] OECD (2018), Monitoring Report: Implementation of the Recommendation of the Council on Effective Public Investment across Levels of Government, OECD Publishing.

[45] OECD (2015), Government at a Glance 2015, OECD Publishing, Paris, https://doi.org/10.1787/gov_glance-2015-en.

[43] OECD (2014), Recommendation of the Council on Effective Public Investment Across Levels of Government, OECD/LEGAL/0402, OECD, Paris.

[5] OECD (2013), Fiscal Federalism 2014: Making Decentralisation Work, OECD Publishing, Paris, https://dx.doi.org/10.1787/9789264204577-en.

[38] OECD (2012), “Denmark: The Local Government Reform”, in Reforming Fiscal Federalism and Local Government: Beyond the Zero-Sum Game, OECD Publishing, Paris.

[36] OECD (2011), OECD Economic Surveys: Belgium 2011, OECD Publishing.

[50] OECD (2010), OECD Economic Surveys: Spain 2010, OECD Publishing.

[29] OECD (2006), OECD Economic Surveys: Australia 2006, OECD Publishing.